Embed Size (px)

Citation preview

What is Long Term Care?

Kathleen King

VP for Health PolicyFebruary 20, 2004

Definition of Long Term Care

• Care provided on a regular basis for three months or more that includes:

• Help with daily activities such as shopping, cooking, taking medications;

• Help with personal care tasks such as bathing or dressing; or

• Help with nursing care such as monitoring blood pressure or side effects of medications.

Long Term Care Care can be Provided

• At home by family members or paid staff;

• In an assisted living facility; or

• In a nursing home

Long Term Care as a Percentage of Personal Health Spending, 2002

Total Personal Health Care Expenditures, billions ($1,304.2)

LTC: Nursing Home and Home Health

($139.3)10%

Physican and Clinical Services (339.5)

25%

Other Retail Outlet Sales of Medical

Products ($50.5)

4%

Other Professional Services ($162.0)

12%

Hospital Care ($486.5)37%

Prescription Drugs ($162.4)

12%

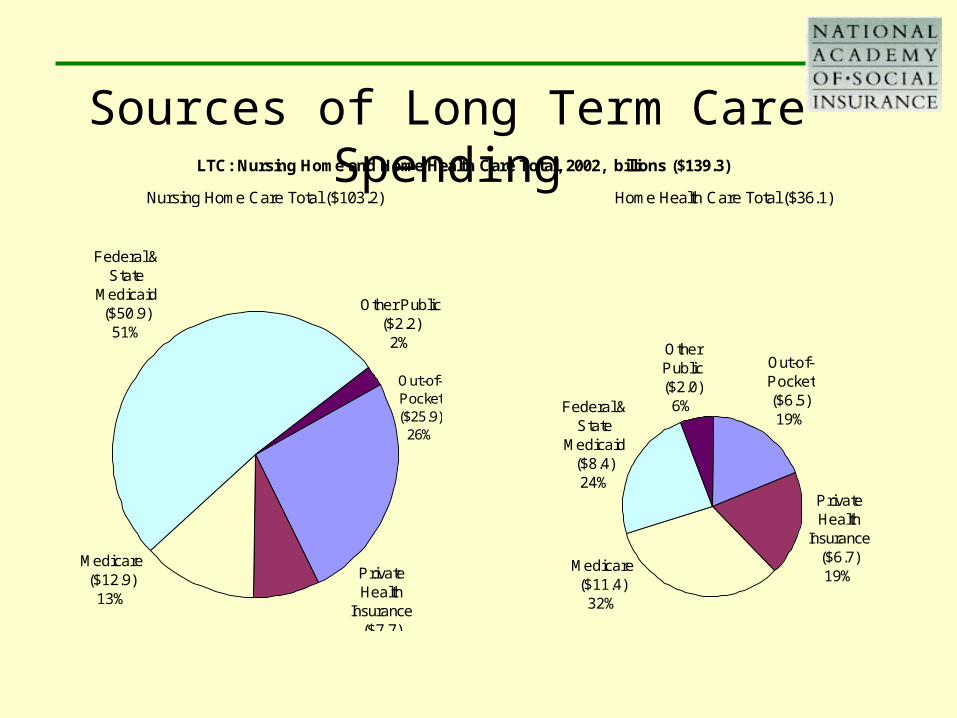

Medicare ($12.9)

13%

Out-of-Pocket ($25.9)

26%

Federal & State

Medicaid ($50.9)

51%

Other Public ($2.2)

2%

Private Health

Insurance($7.7)

8%

Out-of-Pocket ($6.5)19%

Private Health

Insurance ($6.7)19%

Other Public ($2.0)

6%

Medicare ($11.4)

32%

Federal & State

Medicaid ($8.4)24%

LTC: Nursing Home and Home Health Care Total, 2002, billions ($139.3)

Home Health Care Total ($36.1)Nursing Home Care Total ($103.2)

Sources of Long Term Care Spending

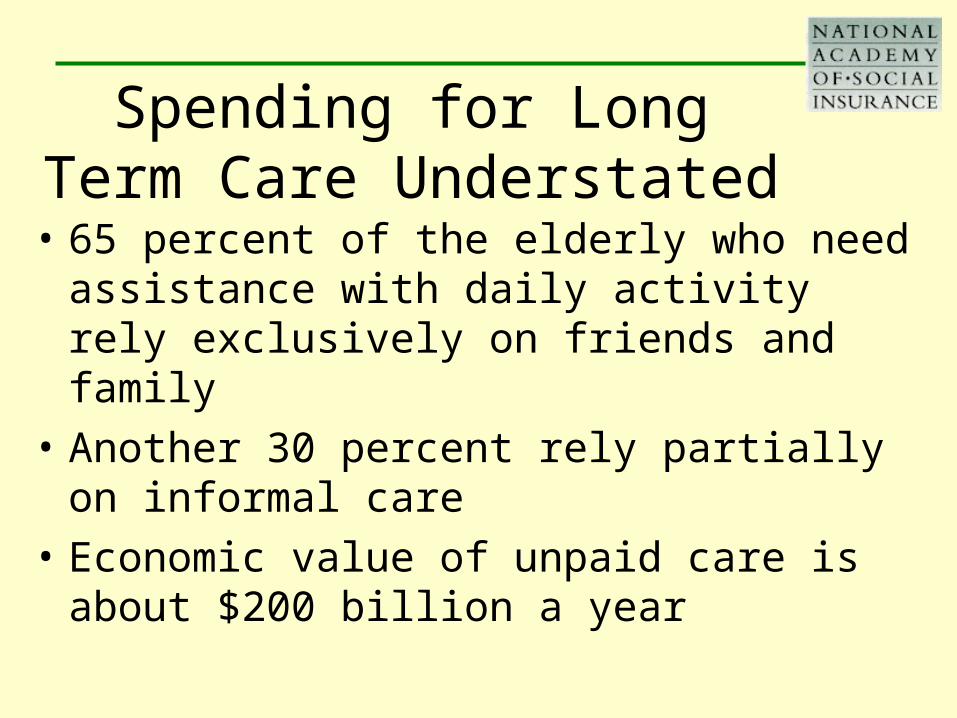

Spending for Long Term Care Understated

• 65 percent of the elderly who need assistance with daily activity rely exclusively on friends and family

• Another 30 percent rely partially on informal care

• Economic value of unpaid care is about $200 billion a year

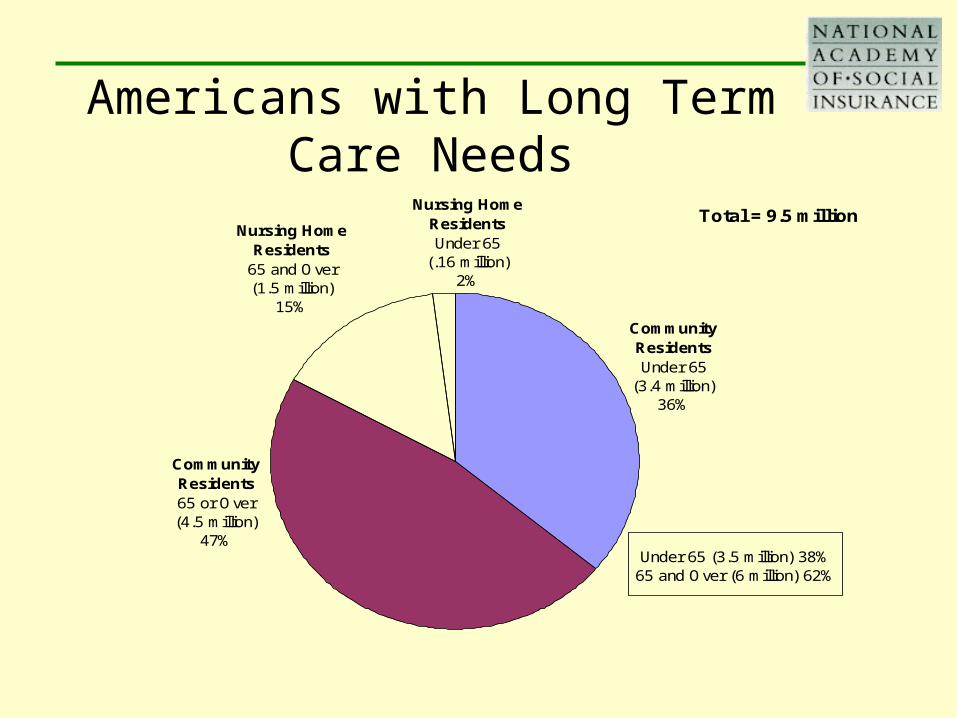

Americans with Long Term Care Needs

Total = 9.5 million

Community Residents Under 65

(3.4 million) 36%

Community Residents 65 or Over (4.5 million)

47%

Nursing Home Residents

65 and Over (1.5 million)

15%

Nursing Home Residents Under 65

(.16 million)2%

Under 65 (3.5 million) 38%65 and Over (6 million) 62%

Demographics of the Baby Boom Generation

• In 2000, 13 percent of the population was over age 65

• By 2030, 20 percent of the population will be over age 65

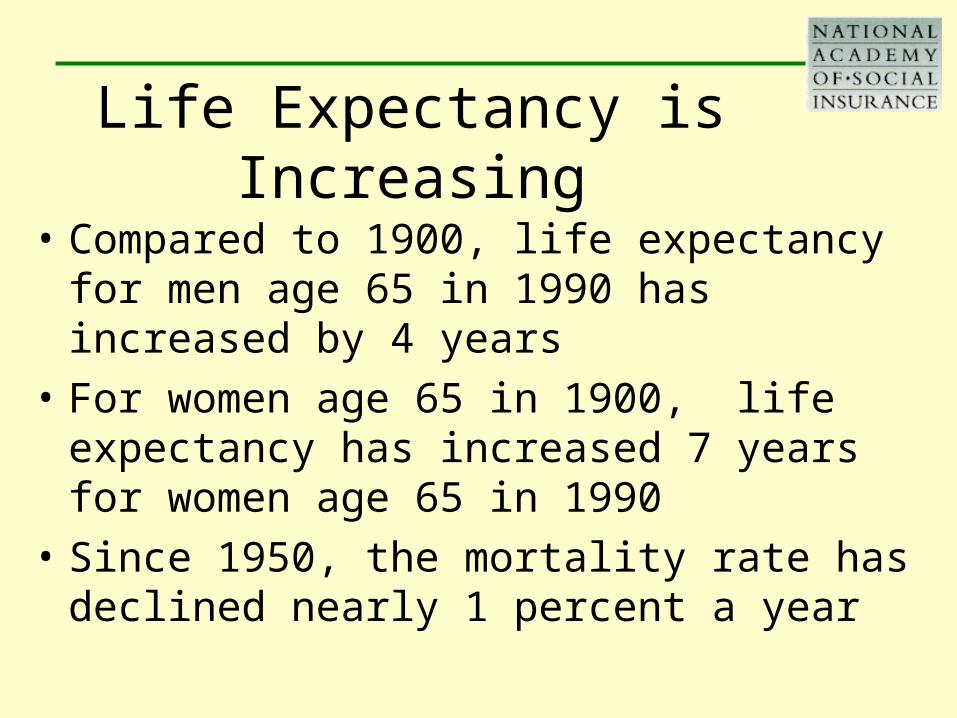

Life Expectancy is Increasing

• Compared to 1900, life expectancy for men age 65 in 1990 has increased by 4 years

• For women age 65 in 1900, life expectancy has increased 7 years for women age 65 in 1990

• Since 1950, the mortality rate has declined nearly 1 percent a year

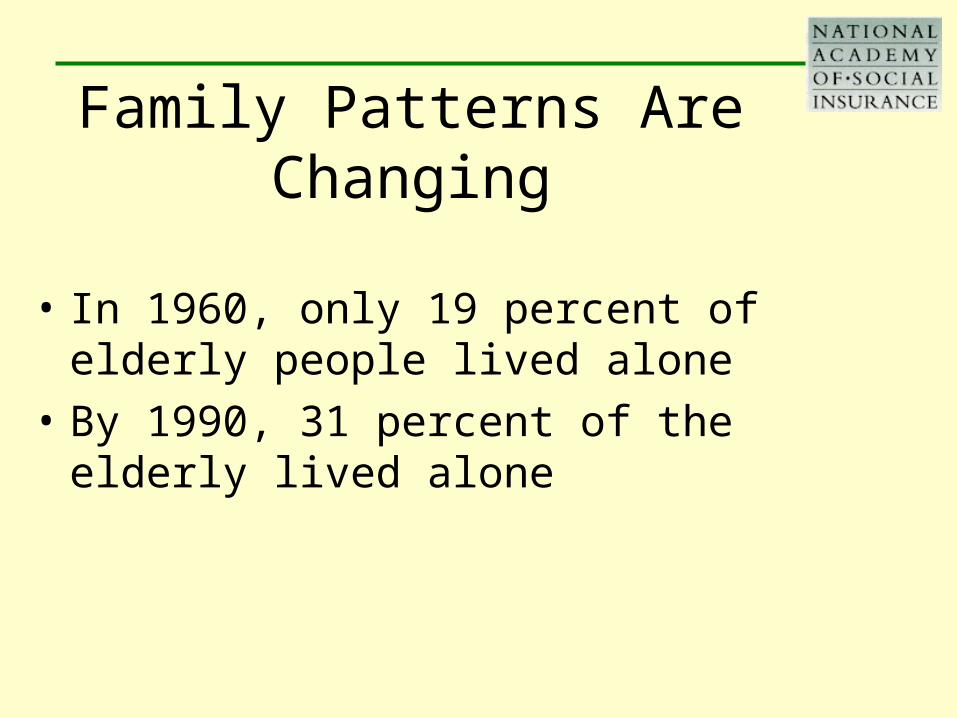

Family Patterns Are Changing

• In 1960, only 19 percent of elderly people lived alone

• By 1990, 31 percent of the elderly lived alone

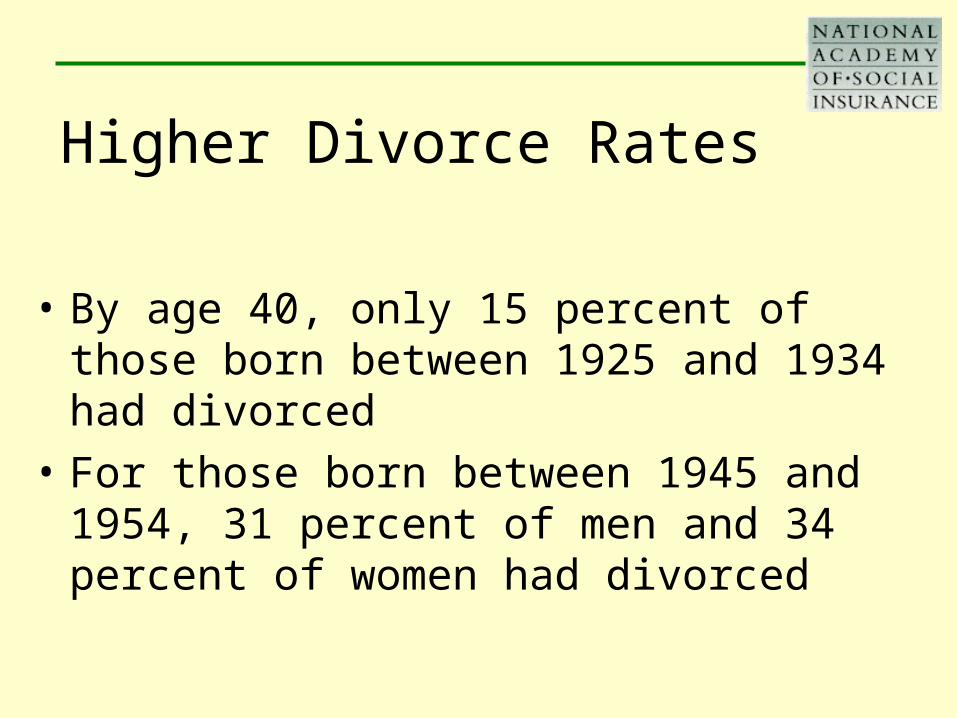

Higher Divorce Rates

• By age 40, only 15 percent of those born between 1925 and 1934 had divorced

• For those born between 1945 and 1954, 31 percent of men and 34 percent of women had divorced

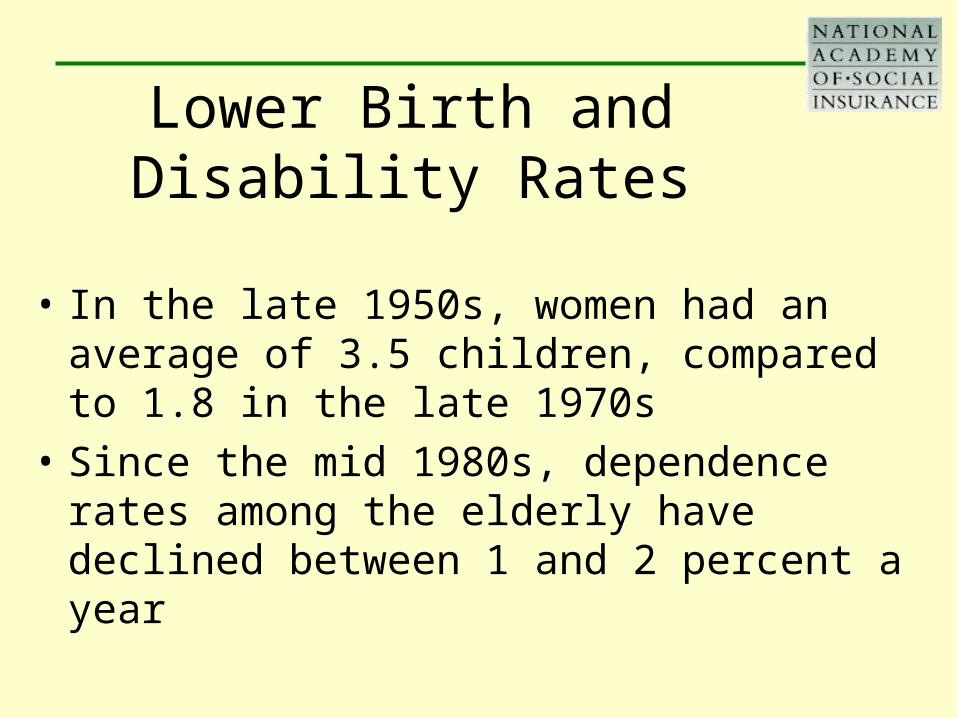

Lower Birth and Disability Rates

• In the late 1950s, women had an average of 3.5 children, compared to 1.8 in the late 1970s

• Since the mid 1980s, dependence rates among the elderly have declined between 1 and 2 percent a year

Lower Percentage of Elderly in Nursing Homes

• 5.4 percent of elderly lived in nursing homes in 1985, but only 4.6 percent in 1995 – an annual decline of .7 percent a year

Growth in Need for Long Term Care Services

• Olmstead Decision – shift in long term care settings from institutions to community settings

• Need for long term care services may increase between 2 and 4 times the current number

Lack of Understanding

• 31 percent of persons over age 45 said they had purchased ltc insurance in 2001

• 27 percent of persons ages 32-52 said they had ltc insurance in 1998

• Fact: Only 5.8 million ltc insurance policies in force in 2001

Lack of Understanding, Take 2

• 35 percent said Medicare is the primary source of payment for nursing home care

• In another survey, 30 percent said that Medicare pays the expenses of people with Alzheimer’s Disease

Lack of Understanding, Take 3

• 66 percent said the average annual cost of a nursing home is $25,000 in 2001

• Fact: Average annual national cost of nursing home care is $57,000

Dissatisfaction with Current System

• Clear preference to remain in own home and avoid nursing homes

• 45 percent of baby boomers have unfavorable views of nursing homes

• 29 percent of seriously ill people said they would rather die than enter a nursing home

CBO’s Federal Fixes

• Reduce the Overall Federal Contribution

• Reduce Mandatory Benefits or Restrict Coverage

• Increase Costs Shared by Beneficiaries

• Encourage the Use of Lower-Cost Services

Dire State Fiscal Conditions, FY 2001-2003

• Since 2001, state revenues have fallen, Medicaid spending has increased, and Medicaid has been the target of budget cuts

• States reduced provider payments, restricted eligibility and benefits and increased co-payments

Federal Estimates of Medicaid Spending Growth

• 7.5 percent in 2003 (projected)

• 11.7 percent in 2002

• 9.5 percent in 2001

• Enrollment growth slowed from 5.9 percent in 2002 to 3.9 percent in 2003

FY 2004 - Fiscal Conditions Brighten Somewhat

• Congress provided $20 billion in temporary relief, through June 2004

• Falloff in State revenues began to ease• States estimate that total Medicaid spending growth will

slow to 8.2 percent in 2004, compared to 11.9 percent from 2000-2003

• Still, 49 States and D.C. plan further cost containment this fiscal year

What About the Future of Long-Term Care?

• Not necessarily all doom and gloom

• Redefine dependency as those over age 75

• Declining disability rates

• What happens to the economy?

Designing a Long-Term Care System for the Future

• Increase public recognition of long-term care as a problem

• Baby boom generation drives a different definition of the problem

• Redesign the accidental financing system to take some pressure off Medicaid, reallocate burden

• Consider separating housing from care needs• Consider more housing options using tax incentives

Vision for the Future

• Consider other financing sources, including social insurance and private insurance

• Consider separating housing from care needs

• More housing options through tax incentives

• Focus on maintaining independence