Embed Size (px)

Citation preview

FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Insurance products are issued by: John Hancock Life Insurance Company (U.S.A.), Boston, MA 02116 (not licensed in New York) and John Hancock Life Insurance Company of New York, Valhalla, NY 10595.

1 of 64

What is Estate Planning?

MLINY05051114864AG DOLU 5/5/11

2 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

What is Estate Planning?

• Estate planning is a process.

• It’s a lifetime process.

• The estate planning process has financial dimensions.

• The estate planning process has equally important non-financial dimensions.

3 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Non-Financial Estate Planning Considerations

• Disability protection.

• Providing for a spouse.

• Providing for children, grandchildren, and in some cases, elderly parents.

• Family business succession.

• Selecting a trustee, guardian, conservator and personal representative.

• Avoiding family conflicts.

• Basic funeral arrangements.

• Organ donation decisions.

4 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Financial Estate Planning Considerations

• Organizing financial records.

• Ensuring adequate resources are available in the event of disability or death.

• Deciding who takes what, when, and how much.

• Ensuring adequate liquidity is available to pass a family business (and in many cases, ensure that all family members are treated equally).

• Minimizing exposure to transfer costs (taxes, court fees, advisor fees, etc.).

• Minimizing exposure to liability.

5 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Highest rates have been gradually reduced:

• 2005 - 47%

• 2006 - 46%

• 2007-2009 - 45%

• 2010 - 0% (Gift Tax Rate will be 35%)

• 2011-2012 - 35%

Reduction in Gift, Generation-Skipping Transfer and Estate Tax Rates

• 2004-2005 - $1,500,000

• 2006-2008 - $2,000,000

• 2009 - $3,500,000

• 2010 - No estate or GST tax

• 2011-2012 - $5,000,000

Increase in GST and Estate Tax Exemptions

(return to pre-EGTRRA in 2013)

$0

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,000

'02-'03 '04-'05 '06-'08 '09 '10 '11

Increase in GST and Estate Tax Exemptions

7 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

How Assets Are Transferred at Death

• Will.

• Joint tenancy (w/survivorship rights).

• Beneficiary designation.

• Intestate succession.

• Revocable trust.

• Irrevocable trust.

8 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Will

• Set of instructions.

• Who takes what, how much, when, and under what circumstances.

• No effect until death.

• Trusts can be established in wills.

• Can designate guardians & conservators for minors in wills.

• Wills require probate.

Deceased’sEstate

Net Estate

Beneficiaries

9 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Joint Tenancy With Right of Survivorship

• Property owned jointly during life and passes to survivor at death of one joint tenant.

• Simple.

• Supersedes provisions made in wills and/or trusts.

• Can result in unintended dispositions and tax consequences.

• Should be coordinated with overall estate plan.

Mom Dad

Asset

10 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Beneficiary Designations

• Typical examples include designating beneficiaries under life insurance contracts or IRAs.

• Unplanned designations can result in unintended dispositions and tax consequences.

• Should be carefully coordinated with overall estate plan.

Designated Beneficiary

Mom

Dad

Asset

Owner

11 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Intestate Succession

• When individuals fail to plan, estate disposition is left to state intestate succession statute.

• Varies from state to state.

• Very often results in unintended dispositions and tax consequences.

ProbateCourt

Net Estate

State-DeterminedBeneficiaries

12 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Irrevocable Trust

• Usually a separate taxpaying entity.

• Assets are irrevocably transferred to trust.

• If established and funded properly, trust assets are not included in your estate at death.

Mom &

Dad Asset Ownership

Trust Distributions

IrrevocableTrust Beneficiaries

Trusts should be drafted by an attorney familiar with such matters in order to take into account income and estate tax laws (including the generation-skipping tax). Failure to do so could result in adverse tax treatment of trust proceeds.

13 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Costs Involved in Transferring Your Estate

• Federal estate and gift taxes.

• Generation-skipping transfer tax.

• State inheritance taxes.

• Court fees.

• Legal and accounting fees.

• Appraiser fees.

• Asset selling costs.

14 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Reducing Transfer Costs Through Proper Estate Planning

Proper planning enables you to increase what your beneficiaries

receive.

15 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

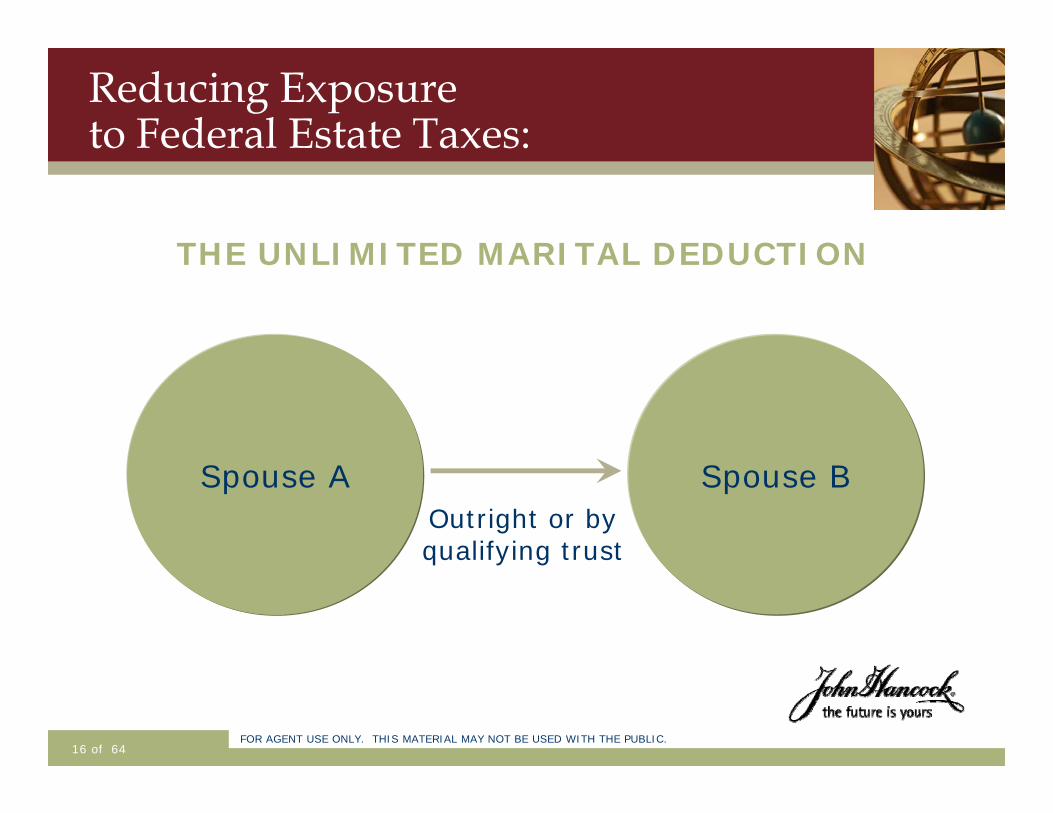

Reducing Exposure to Federal Estate Taxes:

KEY GOVERNMENT – PROVIDED TOOLS:

• Unlimited marital deduction.

• Applicable exclusion amount (formerly the unified credit exemption equivalent).

• Charitable deduction.

• Annual exclusions.

16 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Spouse AOutright or by qualifying trust

Spouse B

Reducing Exposure to Federal Estate Taxes:

THE UNLIMITED MARITAL DEDUCTION

17 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

• $13,000 Annual Exclusion removes assets and appreciation from the taxable estate.

• Lifetime Gift Exemption Amount (2011-2012) removes up to $5,000,000 of property and any future appreciation from the taxable estate.

Gift Tax Principles

18 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Gift Tax Exemption

• Gift tax exemption is $5,000,000 per person in 2011-2012.

• Gift tax has not been repealed.

• Gift tax rates are generally the same as estate tax rates.

19 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

• Current enjoyment

• Creditor protection

• Probate avoidance

• Appreciation shifting

• Income shifting

• Discounted gifts

Other Advantages of Gifting

20 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

A Flexible Sales Idea:

Spousal Access Trust

21 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

What is a Spousal Access Trust?

• An irrevocable life insurance trust (ILIT) drafted to provide the trustee access to the cash values while the insured is still alive.

• Two typesSingle Life Spousal Access TrustSurvivorship Spousal Access Trust

Trusts should be drafted by an attorney familiar with such matters in order to take into account income and estate tax laws (including the generation-skipping tax). Failure to do so could result in adverse tax treatment of trust proceeds

22 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

What does a Spousal Access Trust do?

• Achieves three objectives– Income Replacement– Estate Tax Planning– Supplemental Retirement Income

23 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Spousal Access Life Insurance Trust

• Offers flexibility in uncertain times.

• Also known as a Spousal ILIT.

• Great alternative for people who view ILITs as being inflexible.

24 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Single Life Spousal Access Trust

• Trust owns a single life insurance policy.

• Insured spouse creates the trust.

• Non-insured spouse and children may be possible beneficiaries.

• Non-insured spouse may be the trustee with ascertainable standard (health, education, maintenance and support (HEMS)).

25 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Survivorship Spousal Access Trust

• Uses second-to-die coverage.

• Neither spouse can be the trustee.

• Usually the spouse with the longest life expectancy is the beneficiary.

• One spouse retains access to cash value.

• Children may be the trustees.

26 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Case Study

A Spousal Access Trust Example

The O’Connor Family

27 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

The O’Connor Family

• Kevin and Kelley, both age 45.

• Have three kids.

• Estate of $5 million.

• Problem: Concerned about estate tax uncertainty and not having enough retirement income.

28 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

The Solution:A Single Life Spousal Access Trust

• Kevin O’Connor, age 45, creates a Spousal Access Trust and funds it with a life insurance policy on his life.

• Kevin and Kelley will make gifts to the trust until age 65.

• Kelley is the trustee and a beneficiary of the trust.

29 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

How a Spousal Access Trust Works

• Kelley as trustee will be able to access the policy cash value and make distributions while Kevin is still alive.

• When Kevin dies the assets will be outside of the taxable estate and Kelley will be able to use the proceeds to pay any additional estate tax cost.

30 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Here is how a Spousal Access Trust works

Kevin gifts premium to the trust

Kelley, the trustee,purchases a John Hancock

life insurance policy on Kevin inside the trust

Death benefit passesto beneficiaries

income and estatetax free

Kelley can makedistributions for

“HEMS” from the trust

31 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

The Dynasty Trust

• Savings.

• Avoiding transfer taxes and GSTT.

• Leverage with life insurance.

32 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

The Generation-Skipping Transfer Tax (GSTT)

• Purpose.

• Flat tax at the highest estate/gift tax rate.

• Additional tax.

• Applied to “skip” gifts.

33 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

GSTT Events

• Direct skips

• Outright gift

• Gifts in trust

• Taxable distributions

• Taxable terminations

34 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

The GSTT Exemption

In 2011:

–$5,000,000 Per Estate Owner

–$10,000,000 Husband and Wife

35 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

The Dynasty Trust

• An ILIT with a multi-generational approach.

• GSTT exemption is allocated to lifetime gifts.

• Annual exclusion and applicable credit amount used to avoid gift tax.

• Potentially no transfer taxes to trust.

36 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

A Case Study: The Smiths

Client John and Allison Smith

Ages 67 & 62

Two children Ages 36 and 33

Two grandchildren Ages 4 and 1

Estate Value $10,000,000

After-tax growth rate 5%

37 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Smith children and grandchildren are named beneficiaries.

Purchase Protection Survivorship Universal Life Policy.

John&

AllisonJohn&

Allison

DynastyTrust

DynastyTrust

Smith FamilySmith Family

UL is issued by the John Hancock Life Insurance Company (U.S.A.), Boston, MA 02116

#1 Establish the Trust

38 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

John &

AllisonJohn

& Allison

DynastyTrust

DynastyTrust

Universal Life Policy

Trustee paysannual premiums

Annual gifts

$104,000 per year for 10 years

This is a supplemental illustration. Benefits and values are not guaranteed; the assumptions on which they are based are subject to change by the insurer. Actual results may be more or less favorable.

#2 Funding the Trust

39 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Wealth Maximization Approach

Minimize taxes and maximize the amount passing to heirs from an

annuity

40 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

The Problem

Deferred annuities may be subject to income taxes and

estate taxes at death

41 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

• Have enough wealth to live comfortably.

• Maximize inheritance to heirs– Minimize estate taxes– Minimize income taxes at death

Goals to Live By

42 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

• Irrevocable Life Insurance Trust (ILIT) creates liquidity.

• Deferred annuity used to pay life insurance premiums.

Strategy

43 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

An Example: Annuity Max

• Sam and Maggie Malone, 67 and 62 Preferred NS• Have $5M estate growing at 3%• Have $750k annuity growing at 5% ($400k basis)• Concerned about Transfer Taxes• Want to maximize annuity with insurance• Withdraw just over $37k annually from annuity

• Use about net $24k toward annual premium on SUL policy

Based on current estate taxes, what is their net to heirs at life expectancy?This is a supplemental illustration. Not all benefits and values are guaranteed. The assumptions on which the non-guaranteed elements are based are subject to change by the insurer. Actual results may be more or less favorable.

44 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

• Establish an Irrevocable Life Insurance Trust (ILIT).

• Trustee purchases life insurance policy.

• Deferred annuity funds gifts to the ILIT.

Annuity Maximization Strategy

45 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

The Malones name beneficiaries.

ILIT purchases survivorship universal life insurance.

Sam and

Maggie

Sam and

MaggieILITILIT BeneficiariesBeneficiaries

#1 Establish the ILIT

46 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Annuitypayments

Annual gifts

Trustee pays annual premiums

Same and

Maggie

Same and

MaggieILITILIT BeneficiariesBeneficiaries

Survivorship Universal Life Insurance

policyImmediate

Annuity

#2 Funding the ILIT

47 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Survivorship ULSurvivorship UL

Income tax free death benefit

Income and estate tax free death benefit

ILITILIT HeirsHeirsMaloneEstate

MaloneEstate

#3 In the End…

48 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

CurrentSituation

Year 26 L.E.

The data shown is taken from a hypothetical calculation. It assumes a hypothetical rate of return and may not be used to project or predict actual results.

L.E. = Joint Life Expectancy Year 26 based on 2008 Valuation Basic Table

Current Plan – Hold Annuity

49 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

ProposedSituation

Year 26 L.E.

This is a supplemental illustration. Not all benefits and values are guaranteed. The assumptions on which the non-guaranteed elements are based are subject to change by the insurer. Actual results may be more or less favorable. L.E. = Joint Life Expectancy Year 26 based on 2008 Valuation Basic Table

Proposed Plan – Annuitize

50 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Using Life Insurance in Charitable Planning

51 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

What is a Charitable Remainder Trust (CRT)?

• An irrevocable trust established by one or more individuals (donor(s)), for the benefit of a charity.

• CRT provides a stream of income to the non-charitable beneficiaries.

• Provides income and estate tax benefits.

• Can be established during lifetime or at death.

52 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

CRT Components

• Assets:–Low basis, highly appreciated assets such as:

• Real Estate• Stock

• Retained Interest:–After the asset is transferred to the trust, the donor retains income interest.

• Remainder Interest:–Once the CRT has terminated the remaining assets will be distributed to the charity.

53 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

The Basic CRT

Donor(s) CRT Charity

Asset

Retained Interest Remainder Interest

54 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Benefits of a CRT

• Capital Gains Avoidance

• Charitable Income Tax Deduction

• Taxable Estate is Reduced

• Increase Yield on Assets

• Benefit to Charity

55 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Wealth Replacement Trust

• An ILIT that holds a life insurance policy on the donor.

• Premium gifts are funded with CRT income payments.

• Donors can provide a benefit for family members and charity.

56 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Funding Assets

• Tangible Personal Property

• Intangibles

• Real Estate

• Marketable Securities

• Closely Held Interests– S Corporation– FLPs and LLCs

• CRT

57 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Charitable Giving and EGTRRA

• Additional tax saving due to a decrease in income tax rates can be used for CRTs.

• Income tax deductions are still attractive.

• CRTs and retirement planning – transferring IRAs and qualified plans at death to the CRT is an option.

58 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Other Planning Options

59 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Family Limited Partnerships

• Consolidate ownership and management of family assets.

• Parents allowed to make discounted gifts to children and grandchildren.

• May qualify for gift tax discounts.

60 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

GRATS and QPRTS

• Grantor Retained Annuity Trust (GRAT)– ILIT in which you transfer assets such as stocks

and retain the right to receive a fixed income for a number of years.

– Assets will pass to heirs at the end of the term.

• Qualified Personal Resident Trust (QPRT)– Assets such as a personal residence or a

vacation home can be transferred to a QPRT for a term of years.

– At the end of the trust term, property transfers to heirs.

61 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Estate Planning and the Family Business

• One out of every three family businesses makes a successful transition from one generation to the next.

• Provide for key employee.

• Plan for estate taxes.

• Plan for your successor.

62 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Role of Life Insurance

• Important source of liquidity when it is needed the most – at death.

• Death Benefits usually received income tax free.

• With proper planning it can be free of estate taxes.

Life insurance death benefit proceeds are generally excludable from the beneficiary’s gross income for income tax purposes. There are few exceptions such as when a life insurance policy has been transferred for valuable consideration. No legal, tax or accounting advice can be given by John Hancock, its agents, employees or registered representatives. Prospective purchasers should consult their professional tax advisor for details.

63 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

For more information, please contact your Regional Director or call

Advanced Markets at (888) 266-7498, option 3

64 of 64FOR AGENT USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC.

Insurance products issued by: John Hancock Life Insurance Company (U.S.A.), Boston, MA 02116, (not licensed in New York), John Hancock Life Insurance Company of New York , Valhalla, New York 10595.

This material is for informational purposes only. Although many of the topics presented may also involve tax, legal, accounting or other issues, neither John Hancock nor any of its agents, employees, or registered representatives are in the business of offering such advice. The above material was not intended or written to be used, and it cannot be used, for the purpose of avoiding any penalty that may be imposed by the Internal Revenue Service. The above material may have been written to support the promotion or marketing of the transactions or topics addressed by the written material. Individuals interested in these topics should consult with their own professional advisors to examine legal, tax, accounting or financial planning aspects of these topics.

Insurance policies and/or associated riders and features may not be available in all states.

©2011. John Hancock. All rights reserved.

Disclosures