Embed Size (px)

Citation preview

February 5, 2018

The Packaging Conference

What Is America Drinking?U.S. Market Trends

-2- Copyright © 2018 Beverage Marketing Corp.

Unique Beverage Industry Expertise for Providing “Added-Value” to Selected Clients

Beverage Marketing Capabilities

Cutting Edge Insights: New Age Emergence, Multiple Beverage Competition, Specialty Beer Opportunity, Bottled Water Dominance, Hyper-Category Competition, Micro-

Marketing Age

Beverage Marketing Corporation utilizes an integrated model for providing information, analysis and advice to beverage industry clients

-3- Copyright © 2018 Beverage Marketing Corp.

Beverage Marketing Capabilities

All data in this presentation is supplied by:

With a special packaging module is by:

-4- Copyright © 2018 Beverage Marketing Corp.

The Shifting Beverage Landscape

Market Overview

Key Trends

Category Updates

Projections

Agenda

-5- Copyright © 2018 Beverage Marketing Corp.

Beverage Headlines

Liquid refreshment beverage market grew for fourth consecutive year in 2017 after flat performance in 2013; however, growth was slower in 2017 than in 2016

Carbonated soft drinks (CSDs) continued modest sales declines in 2017, and have now decreased annually for more than a decade

Bottled water widened its gap over CSDs as the largest beverage category in the U.S., driven primarily by the single-serve PET segment

Niche categories continue to outperform traditional mass-market categories with exception of bottled water

Wine and spirits led alcohol growth in 2017, and beer experienced essentially flat performance once again

State of the Industry – The Good and the Bad

1

2

3

4

5

The Shifting Beverage Landscape

-6- Copyright © 2018 Beverage Marketing Corp.

Unemployment Rate2000 – 2017

2012 2017

2.7%

1.9%

0.5%0.1%

2.8%

0.8%

3.1%

4.0%

-1.2%

4.0%

5.0%

2.3%2.0%

2.6%

2.0%

0.9%0.8%

1.4%

3.5%

1.9%

1.2%

3.1%3.2%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2013 2014 2015 2016

4.0%4.7%

5.8%6.0%

5.5%5.1%

4.6% 4.6%

5.8%

9.3%9.6%

9.0%

8.1%7.4%

6.2%

5.3%4.9%

4.4%

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

Quarterly GDP Change2011 – Q3 2017

The Shifting Beverage Landscape

The economy continues to move in a positive direction with improved GDP growth and lower unemployment, a key to successful beverage market performance

Source: Beverage Marketing Corporation; Bureau of Economic Analysis, Department of Commerce, Department of Labor

-7- Copyright © 2018 Beverage Marketing Corp.

Annual U.S. Consumer Sentiment Index1995 – 2017

Source: Thompson Reuters/University of Michigan

The Shifting Beverage Landscape

Consumer sentiment surpassed pre-recession levels in 2015 for the first time, but and increased modestly in 2017 after dipping in 2016

92 94103 105 106 108

89 90 8895 89 87 86

64 66 73 6876 79 84

93 9297

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

-8- Copyright © 2018 Beverage Marketing Corp.

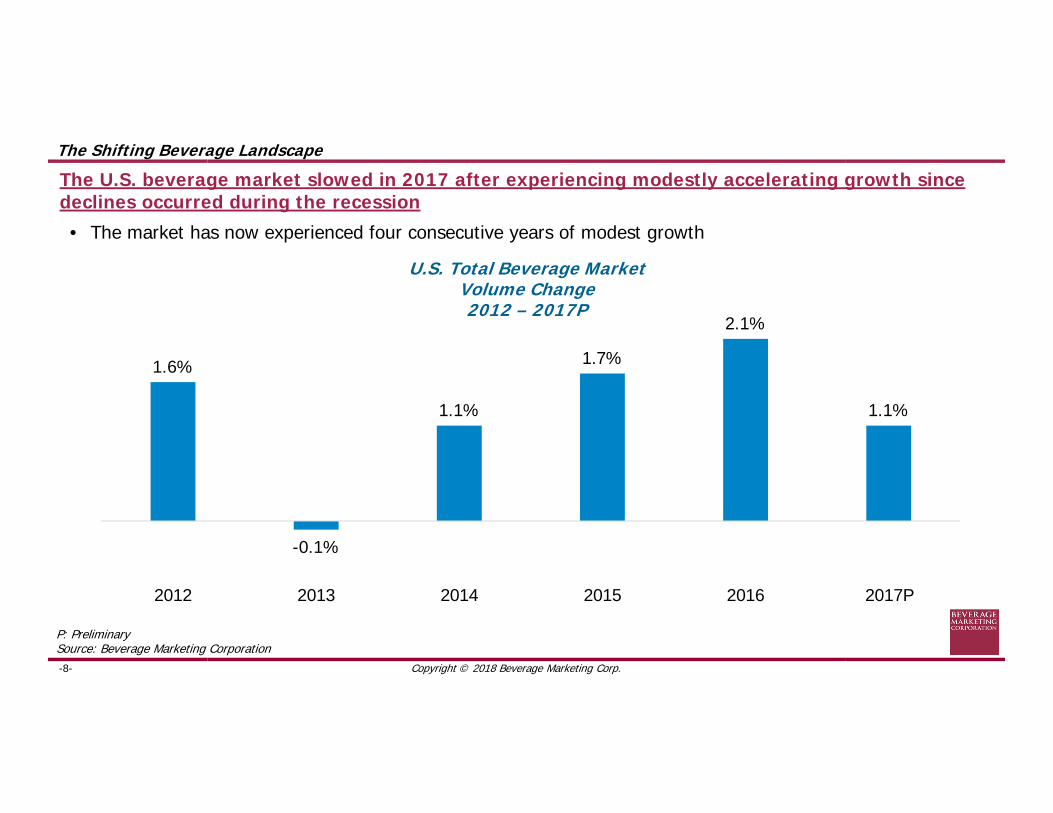

U.S. Total Beverage MarketVolume Change2012 – 2017P

P: PreliminarySource: Beverage Marketing Corporation

1.6%

-0.1%

1.1%

1.7%

2.1%

1.1%

2012 2013 2014 2015 2016 2017P

The U.S. beverage market slowed in 2017 after experiencing modestly accelerating growth since declines occurred during the recession

• The market has now experienced four consecutive years of modest growth

The Shifting Beverage Landscape

-9- Copyright © 2018 Beverage Marketing Corp.

U.S. Total Beverage MarketChange in Volume and Wholesale Dollars

2012 – 2017P

Revenues have grown consistently, and outpace volume performance due primarily to price increases, trend toward premiumization, and packaging mix shifts

1.3%

-0.1%

1.1%

1.7%

2.1%

1.1% 1.2%

3.4%

1.6%

2.7%2.3% 2.1% 2.1%

2.4%

2012 2013 2014 2015 2016 2017P 12/17P CAGR

Volume Change Wholesale Dollar Change

The Shifting Beverage Landscape

P: PreliminarySource: Beverage Marketing Corporation

-10- Copyright © 2018 Beverage Marketing Corp.

Key Factors Impacting 2017 Beverage Performance Slowdown

The Shifting Beverage Landscape

Nearly all beverage categories experienced a slowdown, especially in Q2 and Q3 of this year

Strong comparables from 2016

Modestly higher gas prices

C-store channel slowdown, possibly caused by slightly higher gas prices

Political uncertainty

More stay-at-home eating

Increased volume through difficult-to-track outlets like taprooms and coffee cafes

1

6

2

5

3

4

-11- Copyright © 2018 Beverage Marketing Corp.

In 2017, refreshment beverages performed best while other categories experienced weak performance and tap water declined

2.2%

0.1%

-0.8%

-1.7%

Refreshment Beverages Beverage Alcohol Traditional Beverages Tap Water

U.S. Beverage MarketVolume Change

2017P

The Shifting Beverage Landscape

P: PreliminarySource: Beverage Marketing Corporation

• Bottled Water• CSD• Energy Drinks• Fruit Bevs• RTD Coffee• RTD Tea• Sports Drinks• VA Water

• Hot Coffee• Hot Tea• Milk

• Beer• Spirits• Wine

-12- Copyright © 2018 Beverage Marketing Corp.

Estimated Tap WaterVolume Growth2000 – 2017P

-0.5%

-6.6%

-4.0% -5.3%-9.4% -11.5%

-2.6%

23.5%20.0%

1.3%5.5%

-2.7%

6.2%

-0.6%-5.2%

-10.7%

-1.7%

'00/01 '01/02 '02/03 '03/04 '04/05 '05/06 '06/07 '07/08 '08/09 '09/10 '10/11 '11/12 '12/13 '13/14 '14/15 '15/16 '16/17(P)

The Shifting Beverage Landscape

One reflection of a healthy beverage industry is the decline of tap water, and tap water consumption has been trending down in recent years

• Tap water consumption declined only modestly in 2017

P: PreliminarySource: Beverage Marketing Corporation

-13- Copyright © 2018 Beverage Marketing Corp.

Decade Comparison 2007 – 2017P

Which Categories Gained, Which Lost Volume?

4.5%

3.6%

7.5%

1.3%

1.8%

11.2%

-2.2%

-1.8%

0.9%

Category Millions of Gallons 2007/17P CAGR

350

2,998-2,382

-759

94

100

183

514

4,898

Total LRB

CSD

Fruit Beverages

RTD Coffee

Value-Added Water

Sports Drinks

Energy Drinks

RTD Tea

Bottled Water

Bottled water gained the most volume over the last 10 years while CSDs lost the mostThe Shifting Beverage Landscape

P: PreliminarySource: Beverage Marketing Corporation

-14- Copyright © 2018 Beverage Marketing Corp.

Traditional Key Consumer Drivers Are Evolving

Health and wellness Balanced nutrition

Premiumization Both LRBs and alcohol

Variety Flavors, seasonals, hybrids

Packaging Convenient and proprietary

1

The Shifting Beverage Landscape

4

2

3

-15- Copyright © 2018 Beverage Marketing Corp.

Health and Wellness RTD Categories in U.S. Beverage MarketVolume Share

SEGMENT Health & Wellness* All Other** TOTAL MARKET5-YR CAGR +3.6% -1.0% +0.7%

The Shifting Beverage Landscape

Health and wellness is a key market driver. Beverage categories with health and wellness attributes are outperforming those without

• Additionally, threats of sugar taxes may accelerate this trend toward better-for-you products

* Includes bottled water, milk, 100% juice, RTD tea, dairy alternatives, meal replacement drinks, value-added water, coconut water, kombucha, sports drinks, energy drinks and protein drinks** Includes CSDs, coffee (including RTD), tea (excluding RTD), fruit drinks, beer, wine, spirits and tap water P: PreliminarySource: Beverage Marketing Corporation

Health & Wellness*36.1%

Health & Wellness*41.4%

All Other**63.9%

All Other**58.6%

2012

2017P

-16- Copyright © 2018 Beverage Marketing Corp.

U.S. Liquid Refreshment Beverage MarketCalories Per Capita Per Day

1990 – 2017P

212.5

251.6 263.0243.7 238.0 230.3 222.7 214.8 212.1 208.0 204.9 200.7 200.2 200.2 200.9 198.0

1990 1995 2000 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017(P)

The Shifting Beverage Landscape

Caloric intake from refreshment beverages has been steadily declining over the last decade

• The growth of bottled water and lower-calorie options have contributed to the caloric decline, along with a concerted push by the industry

P: PreliminarySource: Beverage Marketing Corporation

-17- Copyright © 2018 Beverage Marketing Corp.

The Shifting Beverage Landscape

Premiumization: Both alcohol and non-alcoholic categories are going more premium. Consumers are trading up to more expensive products that they believe offer better overall quality or benefits

-18- Copyright © 2018 Beverage Marketing Corp.

New Beverage Product IntroductionsThousands of SKUs

2001 – 2016

1.7 1.6 2.0

2.92.6 2.6

3.2

3.8

2.7

3.9 4.0 4.44.7 4.5 4.3 4.4

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

The Shifting Beverage Landscape

New product introductions have risen since 2001 due to the emergence of new categories and heightened consumer demand for variety

Source: Beverage Marketing Corporation; Mintel

-19- Copyright © 2018 Beverage Marketing Corp.

HPP Juice

Cold Brew Coffee

Plant-based Water

Kombucha

Select Offerings and Categories of Today’s Emerging Beverages

Coconut Water

The Shifting Beverage Landscape

Beyond traditional mainstream categories and newer niche categories, a host of emerging categories have entered the market and most boast health and wellness attributes and/or promise specific functional benefits

-20- Copyright © 2018 Beverage Marketing Corp.

Dairy Alternatives

Probiotic Matcha

Select Offerings and Categories of Today’s Emerging Beverages

Protein/Sustenance

Premium Mixers

The Shifting Beverage Landscape

Emerging beverages have provided excitement to the marketplace although not all segments will prove successful in the long run

-21- Copyright © 2018 Beverage Marketing Corp.

The Shifting Beverage Landscape

Proprietary packaging: Growth in niche categories has propelled demand for unique packaging that makes a statement on the retail shelf

-22- Copyright © 2018 Beverage Marketing Corp.

The Shifting Beverage Landscape

Smaller packaging sizes have been a source of innovation and also help contribute to reduced caloric intake

-23- Copyright © 2018 Beverage Marketing Corp.

Beverage Packaging Share by Package Type*Billions of Packaging Units

SEGMENT Plastics Cans Glass Paper Pouches Aseptic TOTAL5-YR CAGR +4.8% -0.9% +0.6% -2.2% -4.2% -0.9% +1.4%

The Shifting Beverage Landscape

Cans, plastic and glass comprise more than 90% of the beverage packaging universe

• Over the last five years, plastic has seen the most growth due mostly to the success of the bottled water category

* Includes Milk, does not include Beer kegs Source: Beverage Marketing Corporation

Plastic36.4%

Plastic42.9%

Cans40.1%

Cans35.7%

Glass15.0%

Glass14.4%

Paper6.1%

Paper5.1%

Pouches1.3%

Pouches1.0%

Aseptic1.0%

Aseptic0.9%

2012

2017P

-24- Copyright © 2018 Beverage Marketing Corp.

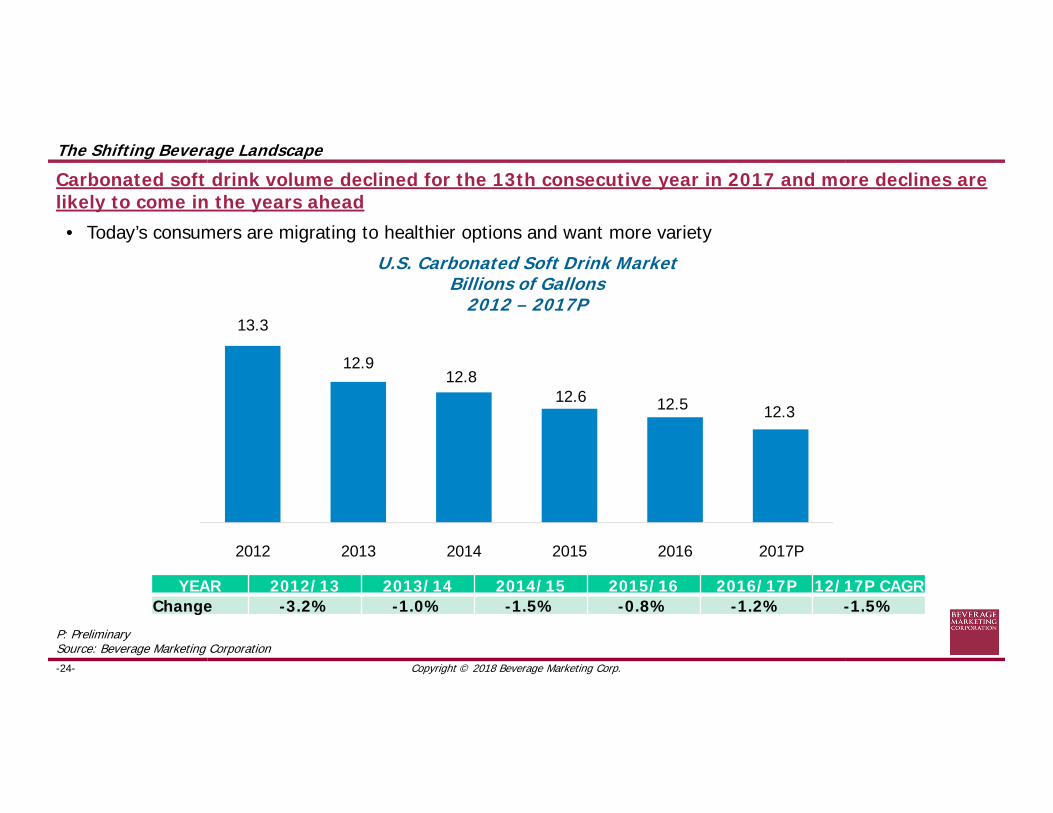

U.S. Carbonated Soft Drink MarketBillions of Gallons

2012 – 2017P13.3

12.912.8

12.6 12.5 12.3

2012 2013 2014 2015 2016 2017P

YEAR 2012/13 2013/14 2014/15 2015/16 2016/17P 12/17P CAGRChange -3.2% -1.0% -1.5% -0.8% -1.2% -1.5%

The Shifting Beverage Landscape

Carbonated soft drink volume declined for the 13th consecutive year in 2017 and more declines are likely to come in the years ahead

• Today’s consumers are migrating to healthier options and want more variety

P: PreliminarySource: Beverage Marketing Corporation

-25- Copyright © 2018 Beverage Marketing Corp.

Stevia/Erythritol Stevia/Erythritol Stevia/Erythritol

Sugar/Stevia Sugar/Stevia Stevia

The Shifting Beverage Landscape

Search for zero-calorie sweeteners continue; ideal sweetener should be natural, stable, in good supply, cost effective, and taste like sugar

-26- Copyright © 2018 Beverage Marketing Corp.

The Shifting Beverage Landscape

Besides natural zero-calorie sweeteners, marketers are seeking novel ways to engage the carbonated beverage consumer – some times with products outside the CSD category

-27- Copyright © 2018 Beverage Marketing Corp.

Broader product portfolio in a range of formats appeals to array of consumer need states

Heightened focus on high-margin, high-growth segments such as RTD coffee and tea

Enhanced nationwide distribution capabilities combining each company’s strengths

Proven and experienced beverage industry management team

$600 million in annual cost savings by 2021

12

34

5

The Shifting Beverage Landscape

The acquisition of DPSG by Keurig provides a range of synergies

Source: Beverage Marketing Corporation

But also poses some questions and challenges

Is strategic rationale sound?

Can new company manage complexity of integration seamlessly?

1

2

-28- Copyright © 2018 Beverage Marketing Corp.

The Shifting Beverage Landscape

The acquisition of DPSG by Keurig helps to fill in product portfolio voids

DPSG and Keurig Product Portfolios

1McKinsey Retail Dollar Estimates for 2011 to 2016, based on Beverage Digest, Nielsen and Euromonitor; US + Canada; excludes non-packaged formats (e.g. CSD Fountain, Coffee Shop Retail locations

-29- Copyright © 2018 Beverage Marketing Corp.

Heightened consumer demand for healthier refreshment and variety

Legislation and messaging from government and regulatory agencies

Tax threats aimed at reducing consumption

Negative commentary from medical studies

Steady drumbeat of negative press

1

2

3

4

5

The Shifting Beverage Landscape

Consumer health and variety demands negatively impact CSD consumption. CSD category performance is further impacted by other external factors that contribute to consumption declines

Source: Beverage Marketing Corporation

-30- Copyright © 2018 Beverage Marketing Corp.

U.S. Bottled Water MarketBillions of Gallons

2012 – 2017P

9.7 10.210.9

11.812.8

13.7

2012 2013 2014 2015 2016 2017P

YEAR 2012/13 2013/14 2014/15 2015/16 2016/17P 12/17P CAGRChange +4.8% +7.4% +8.0% +8.5% +6.7% +7.1%

The Shifting Beverage Landscape

Bottled water has experienced healthy growth each year since the recession

• The category is aided by its positioning as the ultimate health beverage

• The category now is now the largest beverage category in the U.S.

P: PreliminarySource: Beverage Marketing Corporation

-31- Copyright © 2018 Beverage Marketing Corp.

U.S. Retail PET Water MarketBranded vs. Private Label

SEGMENT PRIVATE LABEL BRANDED TOTAL5-YR CAGR +12.5% +3.8% +7.7%

The Shifting Beverage Landscape

Private label PET water accounts for virtually half of the single-serve market today

P: PreliminarySource: Beverage Marketing Corporation

Branded59.5%

Branded50.4%

Private Label40.5%

Private Label49.6%

2012

2017P

-32- Copyright © 2018 Beverage Marketing Corp.

The Shifting Beverage Landscape

Sparkling water is on fire – fastest growing segment in the bottled water category

-33- Copyright © 2018 Beverage Marketing Corp.

Enhanced Waters

PH Balanced Water Plant WaterEssence Water Space Age Water

The Shifting Beverage Landscape

Similar to craft soda, from a small base, enhanced waters of all types are now proliferating and gaining traction in all parts of the country

• These premium value, craft type waters are adding additional benefits to consumers’ water experience beyond vitamins and minerals

-34- Copyright © 2018 Beverage Marketing Corp.

Projected Water & CSD GrowthMillions of Gallons

2011 – 2021P

0

3000

6000

9000

12000

15000

18000

2011 2012 2013 2014 2015 2016P 2017P 2018P 2019P 2020P 2021P

Bulk, HOD, Vended, Sparkling, Imported Waters

Premium Retail PET Waters

CSDs10-Yr CAGR: -1.4%

Enhanced Water

Flavored Water

The Shifting Beverage Landscape

Bottled water became the leading beverage catetgory in the U.S. on a volume basis in 2016, surpassing CSDs and widened its volume gap in 2017

• As CSDs continue to decline and bottled water continues to grow, the gap between the two categories is only likely to widen even more

• On a dollar basis, CSDs continue to be larger than bottled water however

P: ProjectedSource: Beverage Marketing Corporation

-35- Copyright © 2018 Beverage Marketing Corp.

The Shifting Beverage Landscape

Consumers

Shopping

Product

Technology

• Using digital to articulate needs

• Fulfill needs

• Aids in safety of product

Voice

• Shop faster

• Swift convenience

• Authenticity

• Some personalization

• Wellness as status symbol vs material things

• Younger consumers have voice in purchase decision

• Older consumers are articulate ambassadors

Summary

The ability of beverage companies to address global consumer trends will impact their performances in the future

• Consumer trends can be placed in four bucketsGlobal Consumer Trends

Source: Beverage Marketing Corporation; Euromonitor International

-36- Copyright © 2018 Beverage Marketing Corp.

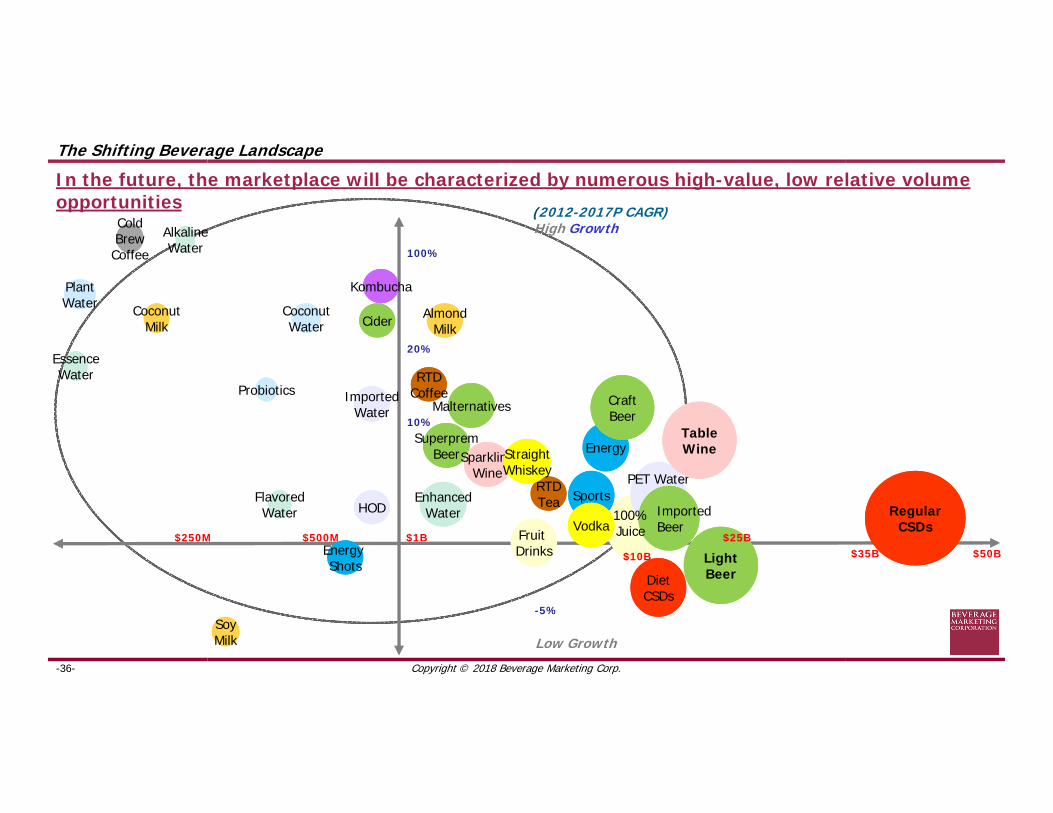

$1B

High Growth

Low Growth

$500M

20%

0%

-5%

(2012-2017P CAGR)

$250M$35B $50B

10%

The Shifting Beverage Landscape

In the future, the marketplace will be characterized by numerous high-value, low relative volume opportunities

RegularCSDs

HOD

ImportedWater

EnhancedWater

FlavoredWater

EssenceWater

AlkalineWater 100%

PET Water

Fruit Drinks $10B

DietCSDs

Sports

Energy

RTDCoffee

RTDTea

SoyMilk

AlmondMilk

CoconutMilk Cider

CraftBeer

Malternatives

ImportedBeer

100% Juice

LightBeer

$25B

SuperpremBeer

TableWineSparkling

WineStraightWhiskey

Vodka

Kombucha

CoconutWater

Probiotics

PlantWater

ColdBrewCoffee

Energy Shots

Thank You

• Strategic Associates

• Research

• Advisors

Beverage Marketing Corporation