Embed Size (px)

Citation preview

1 2 3 4 5

HILLNCO.COM

What Employment Benefits are Taxable and How Do I Calculate

Them?

1 2 3 4 5

HILLNCO.COM

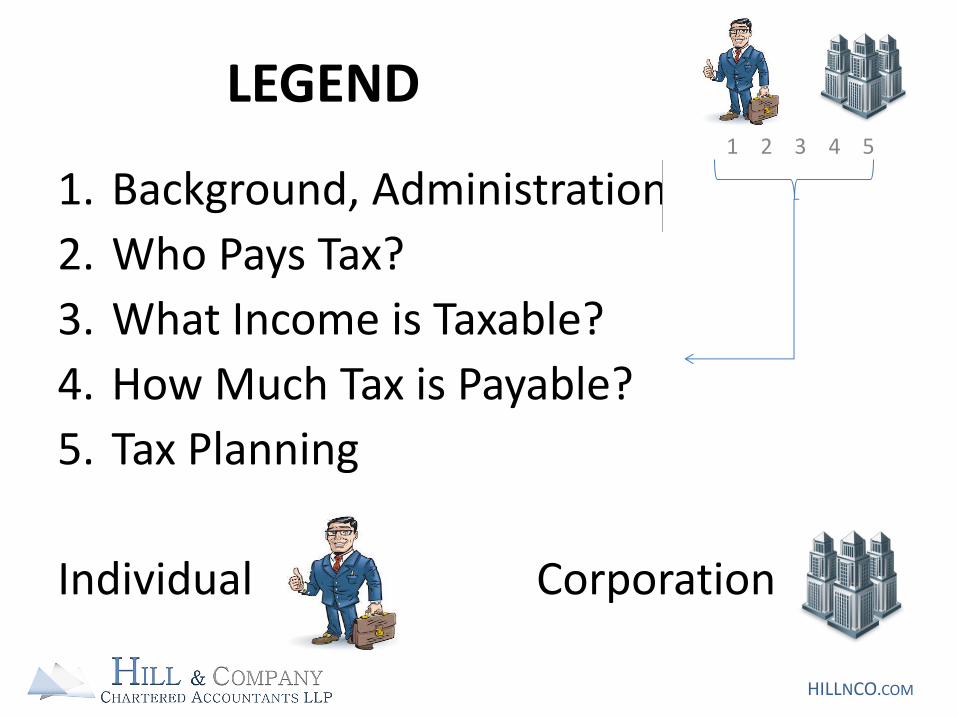

1. Background, Administration

2. Who Pays Tax?

3. What Income is Taxable?

4. How Much Tax is Payable?

5. Tax Planning

Individual Corporation

LEGEND

1 2 3 4 5

HILLNCO.COM

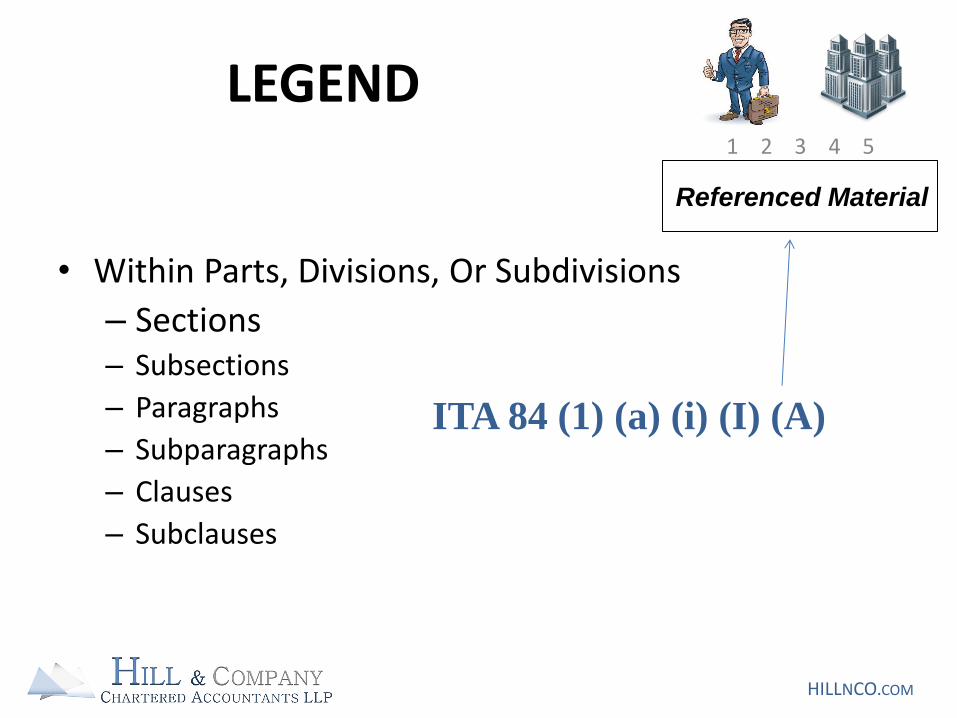

• Within Parts, Divisions, Or Subdivisions

– Sections – Subsections

– Paragraphs

– Subparagraphs

– Clauses

– Subclauses

ITA 84 (1) (a) (i) (I) (A)

Referenced Material

LEGEND

1 2 3 4 5

HILLNCO.COM

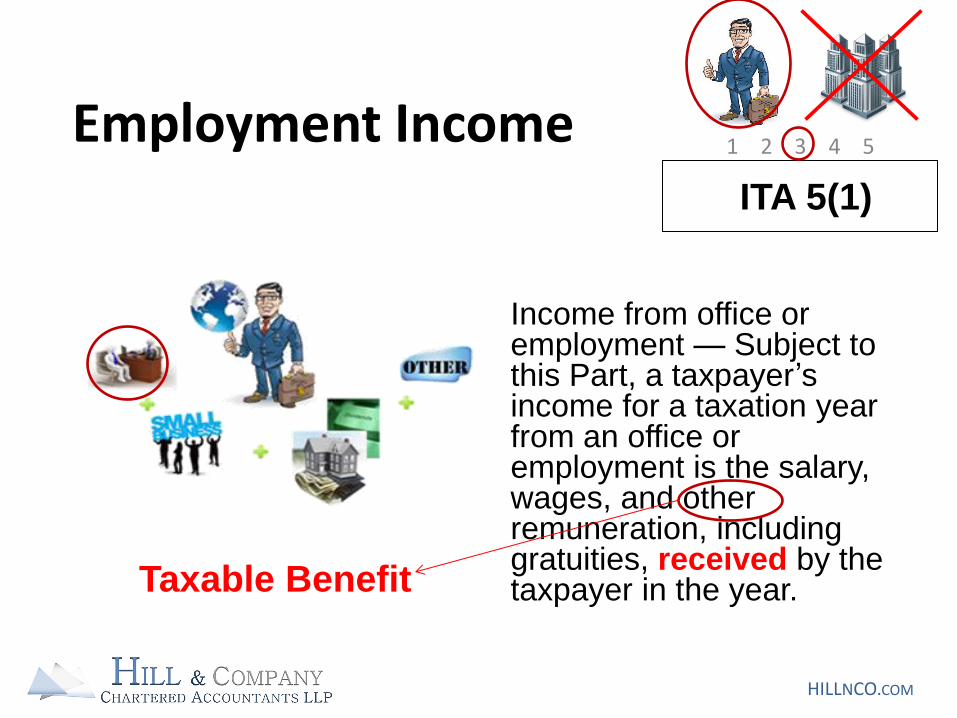

Employment Income

Income from office or employment — Subject to this Part, a taxpayer’s income for a taxation year from an office or employment is the salary, wages, and other remuneration, including gratuities, received by the taxpayer in the year.

ITA 5(1)

Taxable Benefit

1 2 3 4 5

HILLNCO.COM

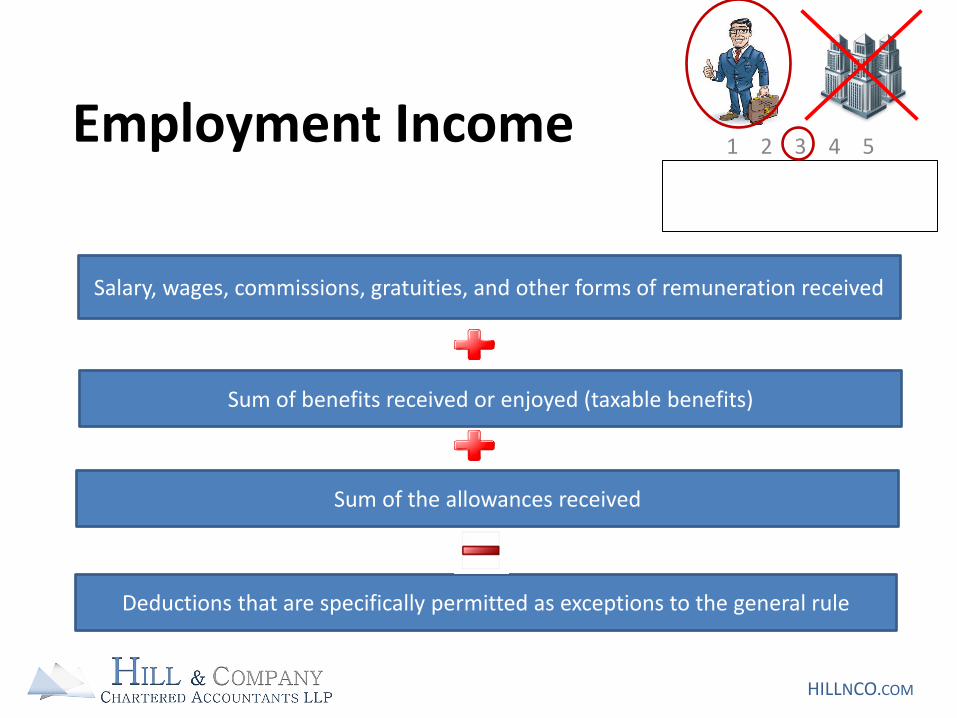

Employment Income

Salary, wages, commissions, gratuities, and other forms of remuneration received

Sum of benefits received or enjoyed (taxable benefits)

Sum of the allowances received

Deductions that are specifically permitted as exceptions to the general rule

1 2 3 4 5

HILLNCO.COM

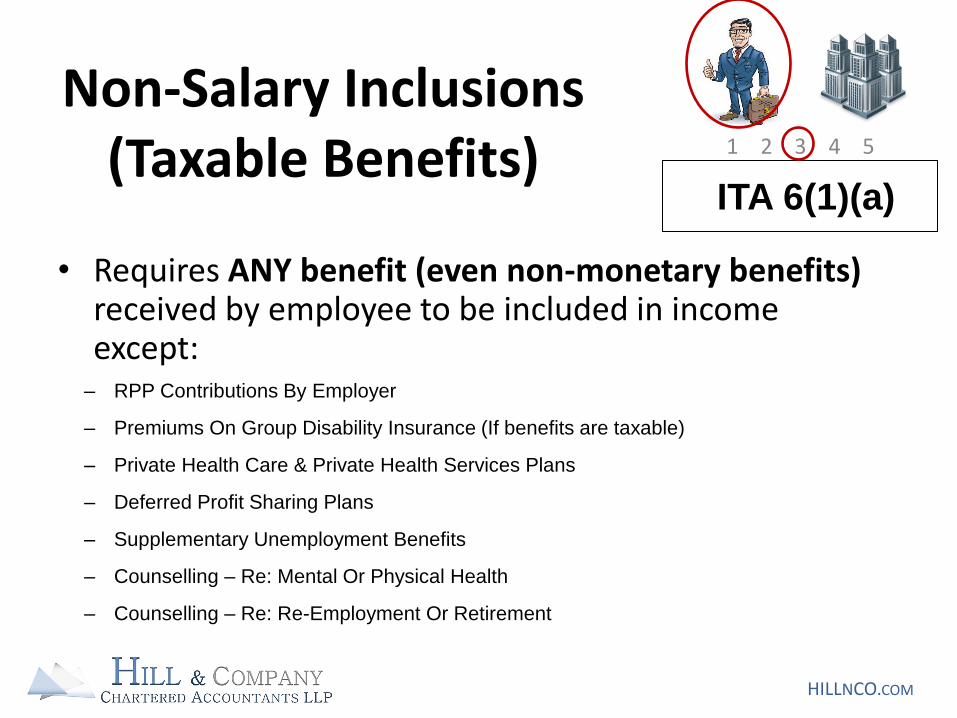

Non-Salary Inclusions (Taxable Benefits)

• Requires ANY benefit (even non-monetary benefits) received by employee to be included in income except:

– RPP Contributions By Employer

– Premiums On Group Disability Insurance (If benefits are taxable)

– Private Health Care & Private Health Services Plans

– Deferred Profit Sharing Plans

– Supplementary Unemployment Benefits

– Counselling – Re: Mental Or Physical Health

– Counselling – Re: Re-Employment Or Retirement

ITA 6(1)(a)

1 2 3 4 5

HILLNCO.COM

Non-Salary Inclusions (Taxable Benefits)

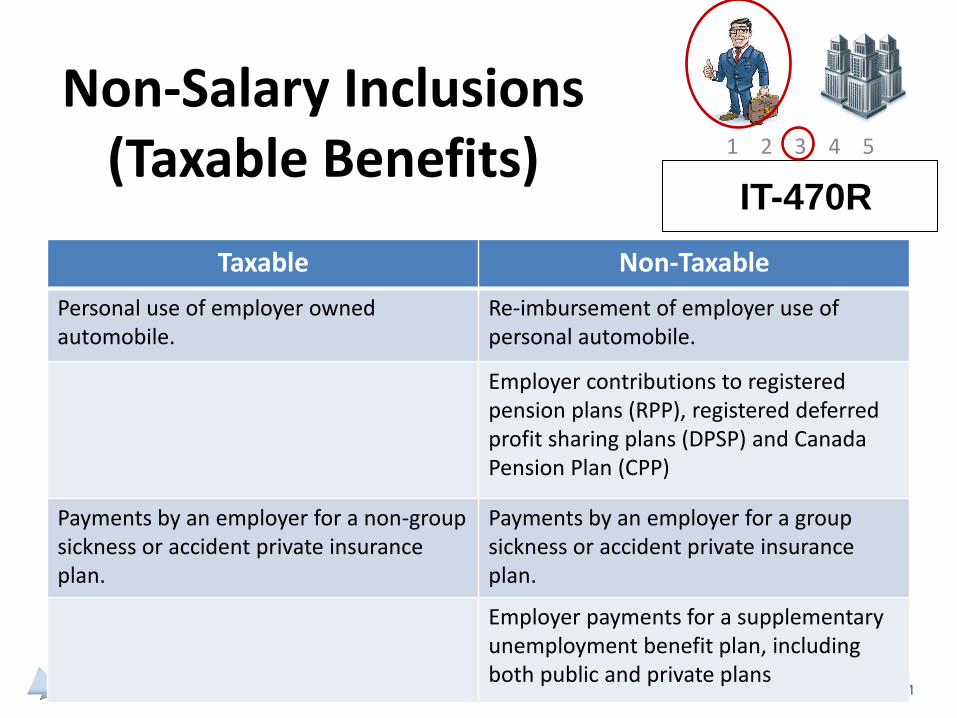

Taxable Non-Taxable

Personal use of employer owned automobile.

Re-imbursement of employer use of personal automobile.

Employer contributions to registered pension plans (RPP), registered deferred profit sharing plans (DPSP) and Canada Pension Plan (CPP)

Payments by an employer for a non-group sickness or accident private insurance plan.

Payments by an employer for a group sickness or accident private insurance plan.

Employer payments for a supplementary unemployment benefit plan, including both public and private plans

IT-470R

1 2 3 4 5

HILLNCO.COM

Non-Salary Inclusions (Taxable Benefits)

Taxable Non-Taxable

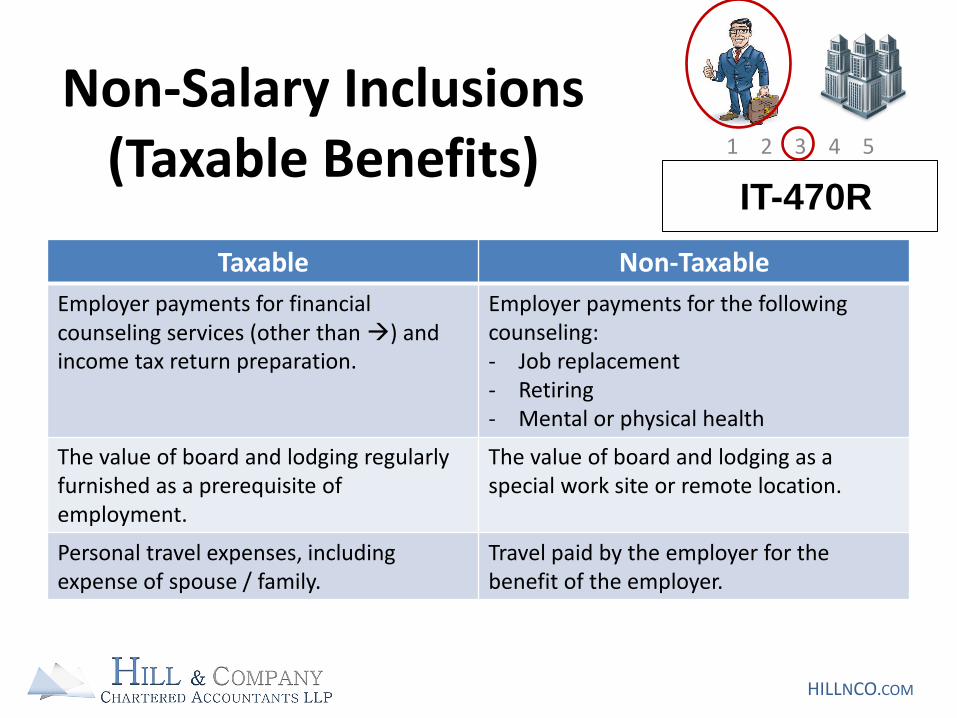

Employer payments for financial counseling services (other than ) and income tax return preparation.

Employer payments for the following counseling: - Job replacement - Retiring - Mental or physical health

The value of board and lodging regularly furnished as a prerequisite of employment.

The value of board and lodging as a special work site or remote location.

Personal travel expenses, including expense of spouse / family.

Travel paid by the employer for the benefit of the employer.

IT-470R

1 2 3 4 5

HILLNCO.COM

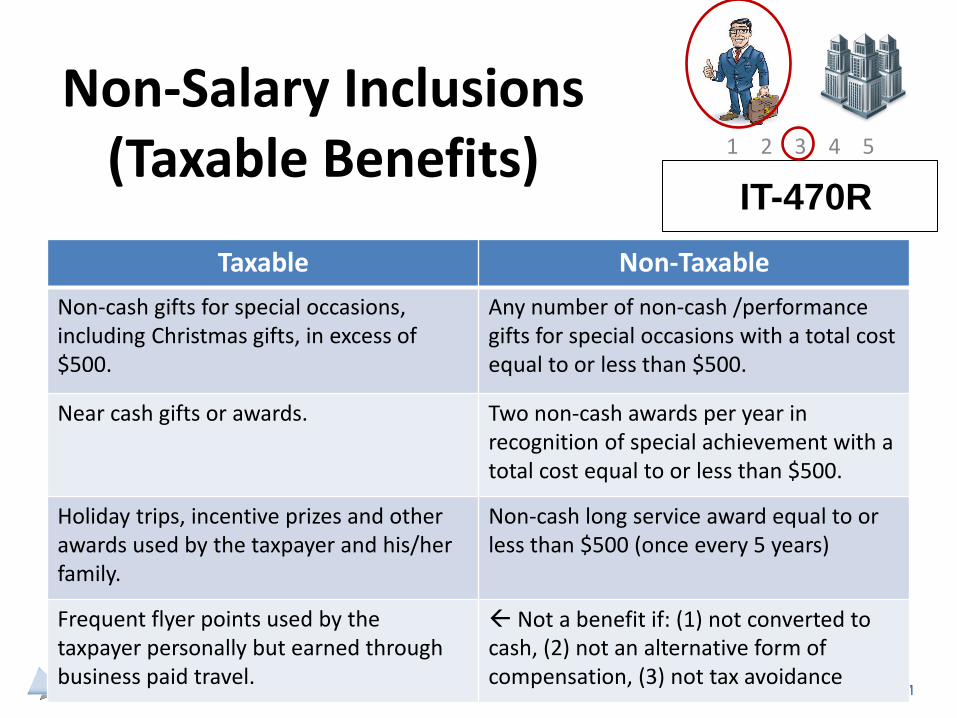

Non-Salary Inclusions (Taxable Benefits)

Taxable Non-Taxable

Non-cash gifts for special occasions, including Christmas gifts, in excess of $500.

Any number of non-cash /performance gifts for special occasions with a total cost equal to or less than $500.

Near cash gifts or awards. Two non-cash awards per year in recognition of special achievement with a total cost equal to or less than $500.

Holiday trips, incentive prizes and other awards used by the taxpayer and his/her family.

Non-cash long service award equal to or less than $500 (once every 5 years)

Frequent flyer points used by the taxpayer personally but earned through business paid travel.

Not a benefit if: (1) not converted to cash, (2) not an alternative form of compensation, (3) not tax avoidance

IT-470R

1 2 3 4 5

HILLNCO.COM

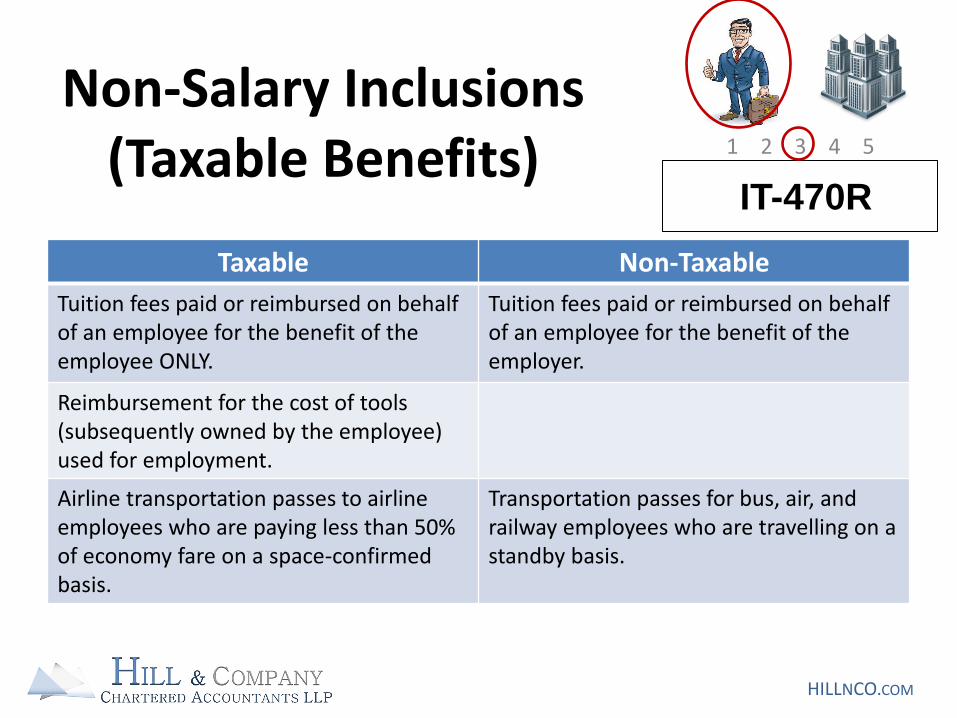

Non-Salary Inclusions (Taxable Benefits)

Taxable Non-Taxable

Tuition fees paid or reimbursed on behalf of an employee for the benefit of the employee ONLY.

Tuition fees paid or reimbursed on behalf of an employee for the benefit of the employer.

Reimbursement for the cost of tools (subsequently owned by the employee) used for employment.

Airline transportation passes to airline employees who are paying less than 50% of economy fare on a space-confirmed basis.

Transportation passes for bus, air, and railway employees who are travelling on a standby basis.

IT-470R

1 2 3 4 5

HILLNCO.COM

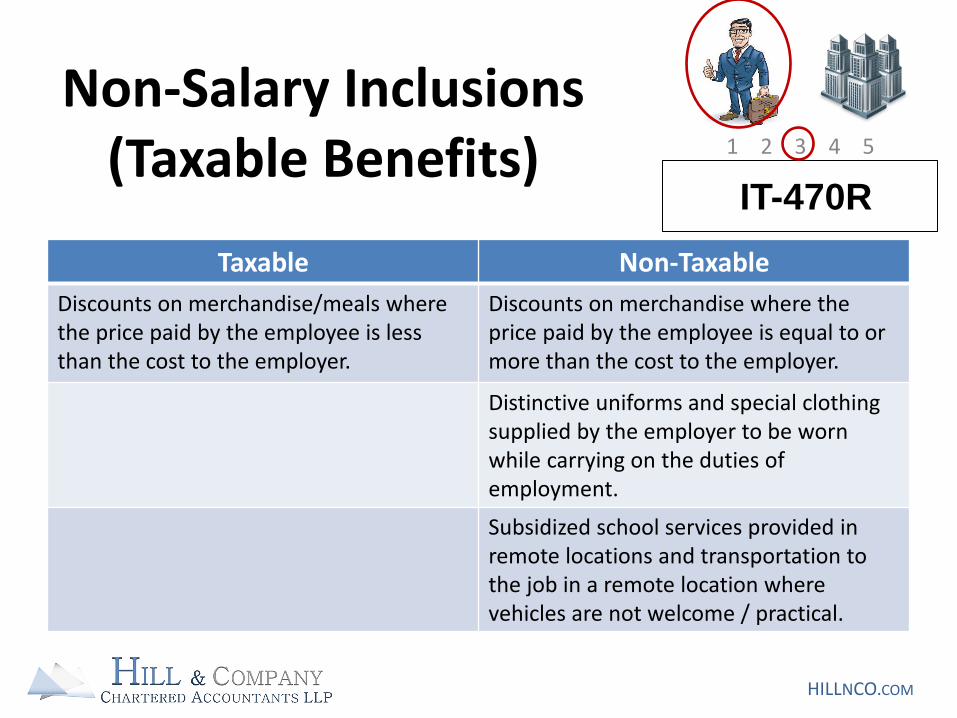

Non-Salary Inclusions (Taxable Benefits)

Taxable Non-Taxable

Discounts on merchandise/meals where the price paid by the employee is less than the cost to the employer.

Discounts on merchandise where the price paid by the employee is equal to or more than the cost to the employer.

Distinctive uniforms and special clothing supplied by the employer to be worn while carrying on the duties of employment.

Subsidized school services provided in remote locations and transportation to the job in a remote location where vehicles are not welcome / practical.

IT-470R

1 2 3 4 5

HILLNCO.COM

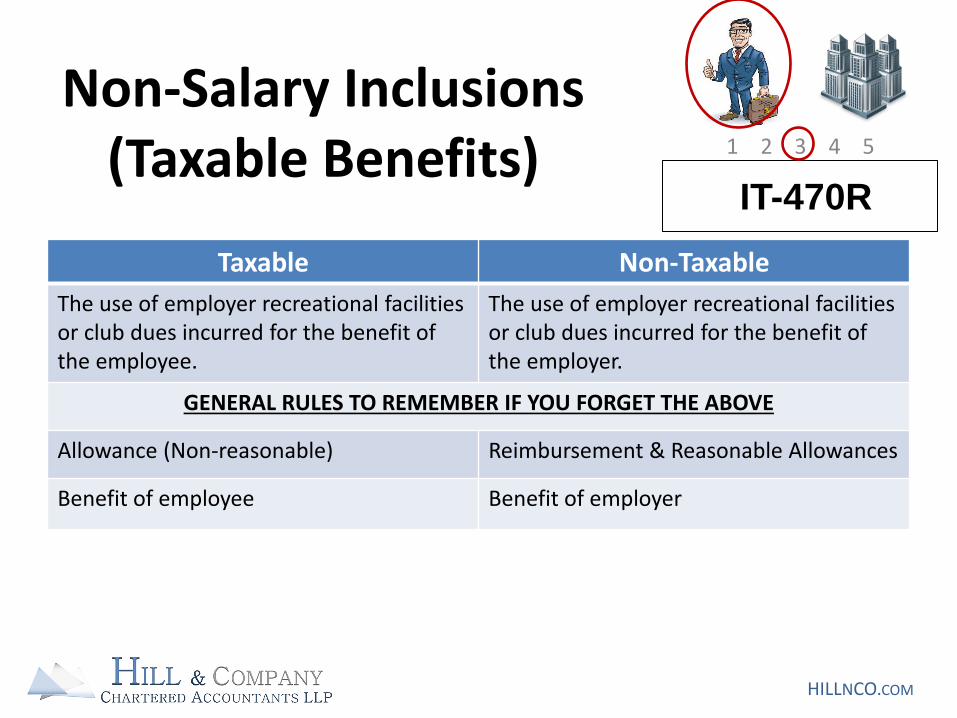

Non-Salary Inclusions (Taxable Benefits)

Taxable Non-Taxable

The use of employer recreational facilities or club dues incurred for the benefit of the employee.

The use of employer recreational facilities or club dues incurred for the benefit of the employer.

GENERAL RULES TO REMEMBER IF YOU FORGET THE ABOVE

Allowance (Non-reasonable) Reimbursement & Reasonable Allowances

Benefit of employee Benefit of employer

IT-470R

1 2 3 4 5

HILLNCO.COM

Non-Salary Inclusions (Taxable Benefits)

• GST/HST/PST that would be required to be paid by the employee (out of after tax dollars) for the benefit, this is included in the taxable benefit

ITA 6(7)

1 2 3 4 5

HILLNCO.COM

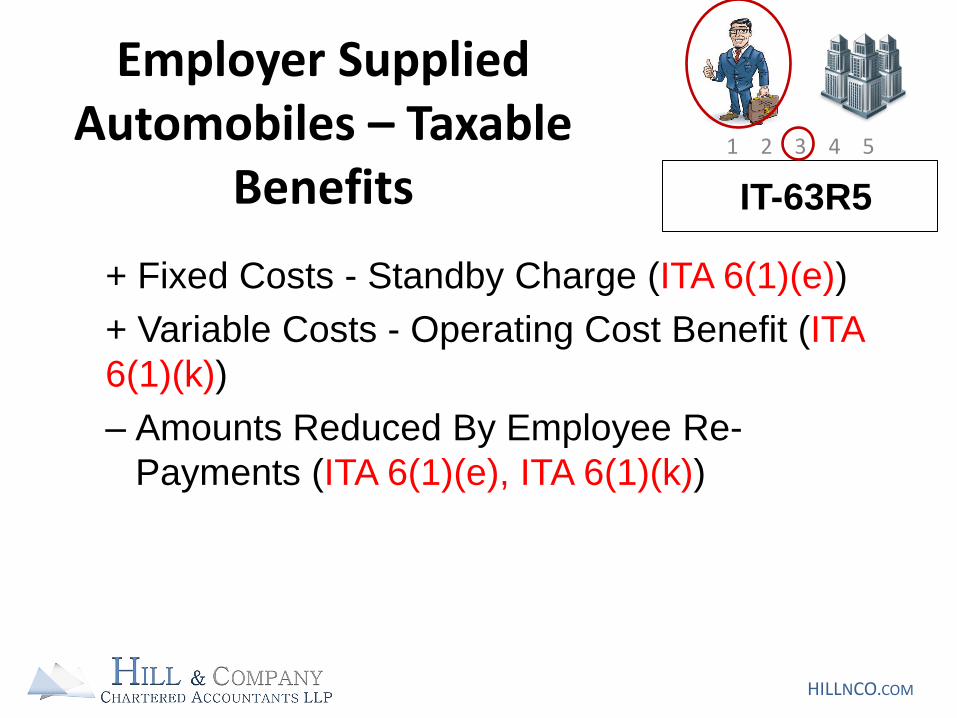

Employer Supplied Automobiles – Taxable

Benefits

+ Fixed Costs - Standby Charge (ITA 6(1)(e))

+ Variable Costs - Operating Cost Benefit (ITA

6(1)(k))

– Amounts Reduced By Employee Re-

Payments (ITA 6(1)(e), ITA 6(1)(k))

IT-63R5

1 2 3 4 5

HILLNCO.COM

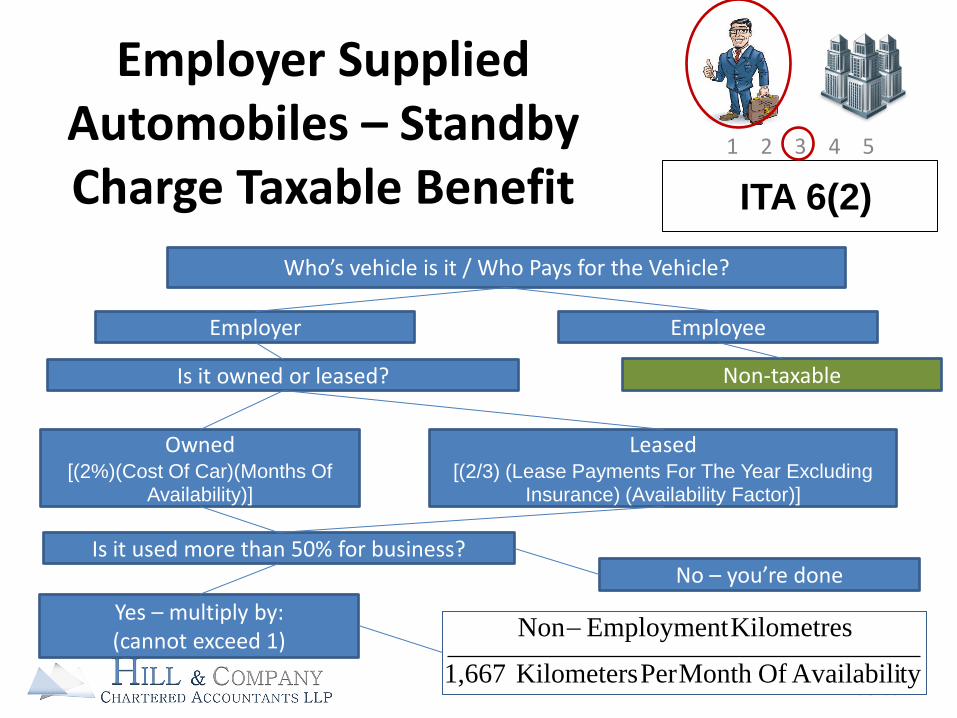

Employer Supplied Automobiles – Standby Charge Taxable Benefit ITA 6(2)

Who’s vehicle is it / Who Pays for the Vehicle?

Employer Employee

Non-taxable Is it owned or leased?

Owned [(2%)(Cost Of Car)(Months Of

Availability)]

Leased [(2/3) (Lease Payments For The Year Excluding

Insurance) (Availability Factor)]

Is it used more than 50% for business?

Yes – multiply by: (cannot exceed 1)

No – you’re done

tyAvailabiliOfMonthPerKilometers 1,667

KilometresEmploymentNon

1 2 3 4 5

HILLNCO.COM

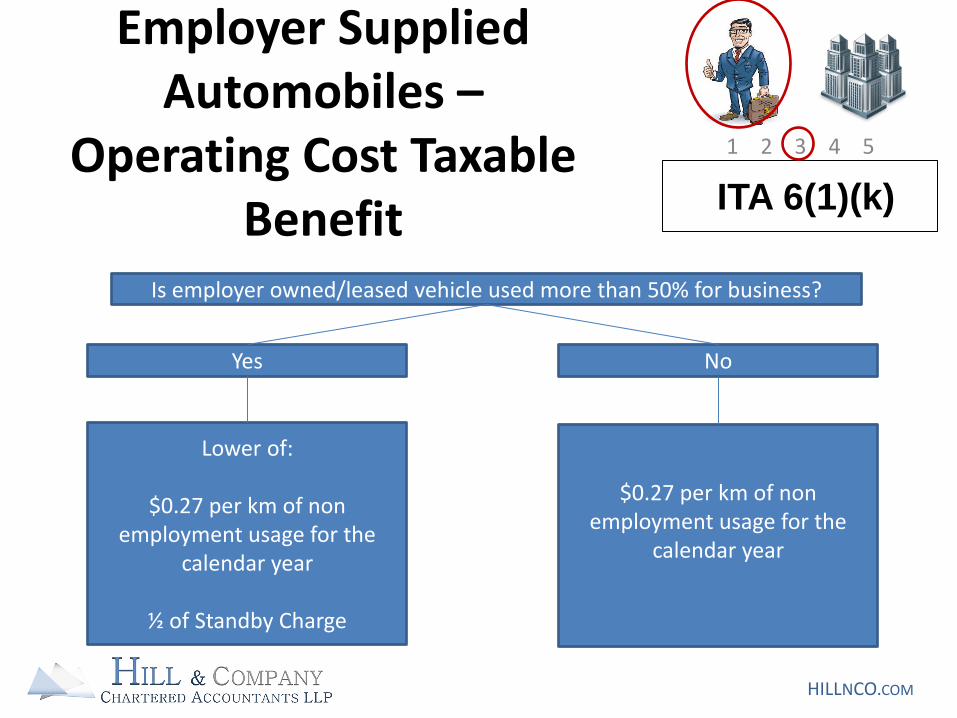

Employer Supplied Automobiles –

Operating Cost Taxable Benefit ITA 6(1)(k)

Is employer owned/leased vehicle used more than 50% for business?

Yes No

Lower of:

$0.27 per km of non employment usage for the

calendar year

½ of Standby Charge

$0.27 per km of non employment usage for the

calendar year

1 2 3 4 5

HILLNCO.COM

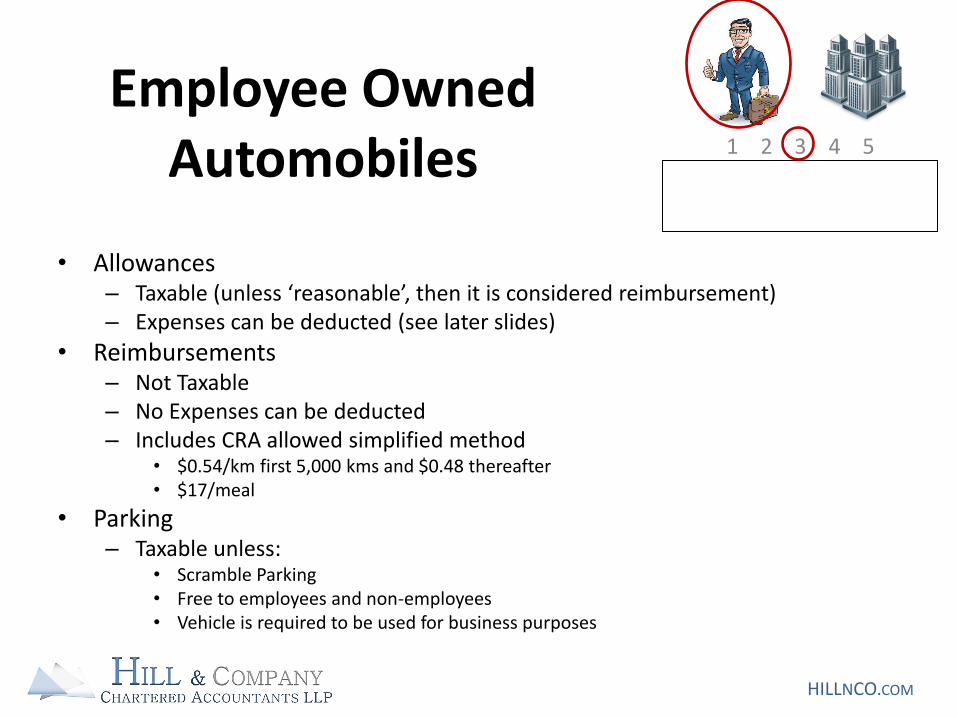

Employee Owned Automobiles

• Allowances – Taxable (unless ‘reasonable’, then it is considered reimbursement) – Expenses can be deducted (see later slides)

• Reimbursements – Not Taxable – No Expenses can be deducted – Includes CRA allowed simplified method

• $0.54/km first 5,000 kms and $0.48 thereafter • $17/meal

• Parking – Taxable unless:

• Scramble Parking • Free to employees and non-employees • Vehicle is required to be used for business purposes

1 2 3 4 5

HILLNCO.COM

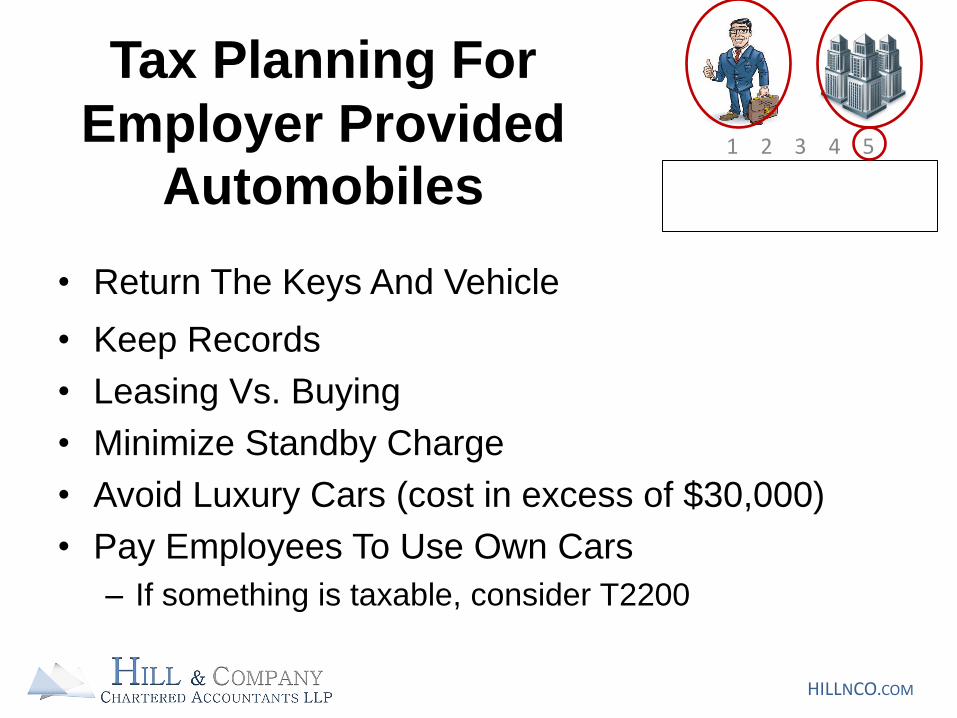

Tax Planning For

Employer Provided

Automobiles

• Return The Keys And Vehicle

• Keep Records

• Leasing Vs. Buying

• Minimize Standby Charge

• Avoid Luxury Cars (cost in excess of $30,000)

• Pay Employees To Use Own Cars

– If something is taxable, consider T2200

1 2 3 4 5

HILLNCO.COM

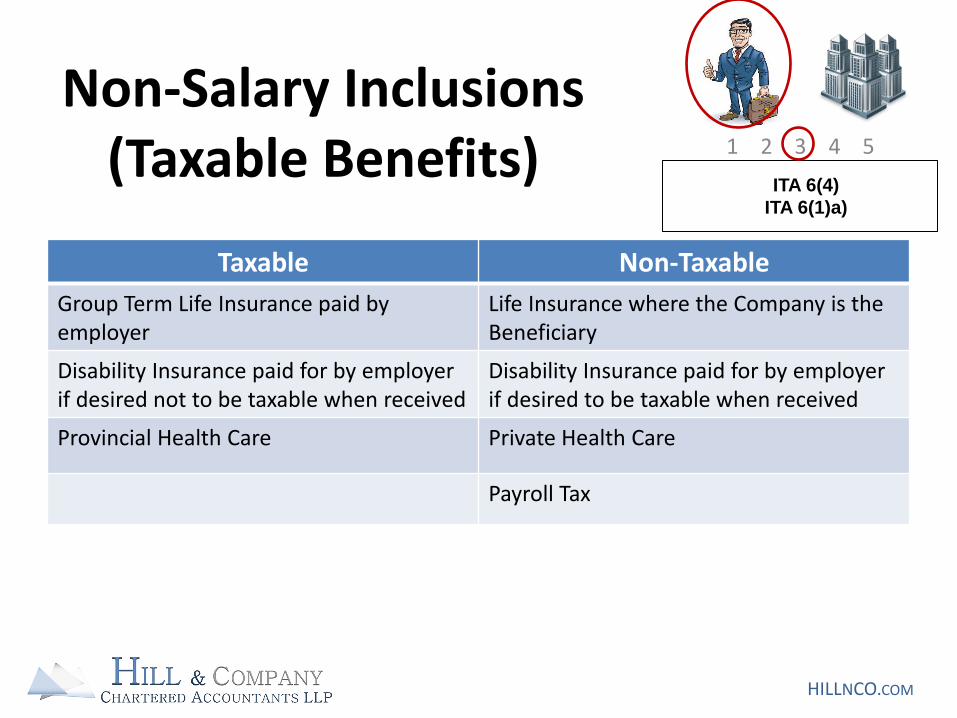

Non-Salary Inclusions (Taxable Benefits)

Taxable Non-Taxable

Group Term Life Insurance paid by employer

Life Insurance where the Company is the Beneficiary

Disability Insurance paid for by employer if desired not to be taxable when received

Disability Insurance paid for by employer if desired to be taxable when received

Provincial Health Care Private Health Care

Payroll Tax

ITA 6(4)

ITA 6(1)a)

1 2 3 4 5

HILLNCO.COM

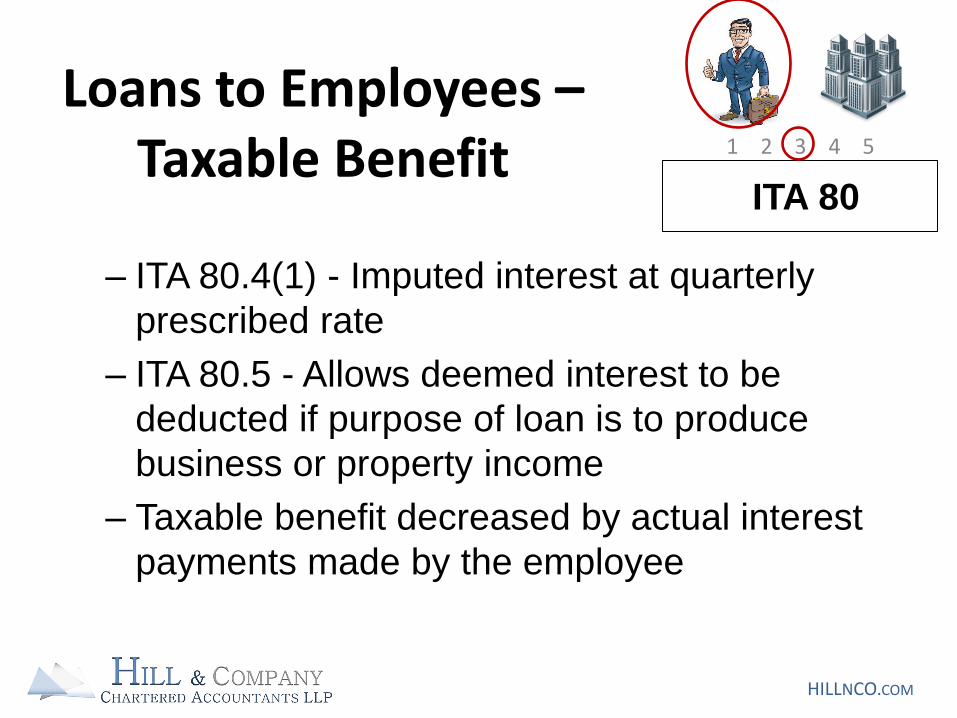

Loans to Employees – Taxable Benefit

– ITA 80.4(1) - Imputed interest at quarterly

prescribed rate

– ITA 80.5 - Allows deemed interest to be

deducted if purpose of loan is to produce

business or property income

– Taxable benefit decreased by actual interest

payments made by the employee

ITA 80

1 2 3 4 5

HILLNCO.COM

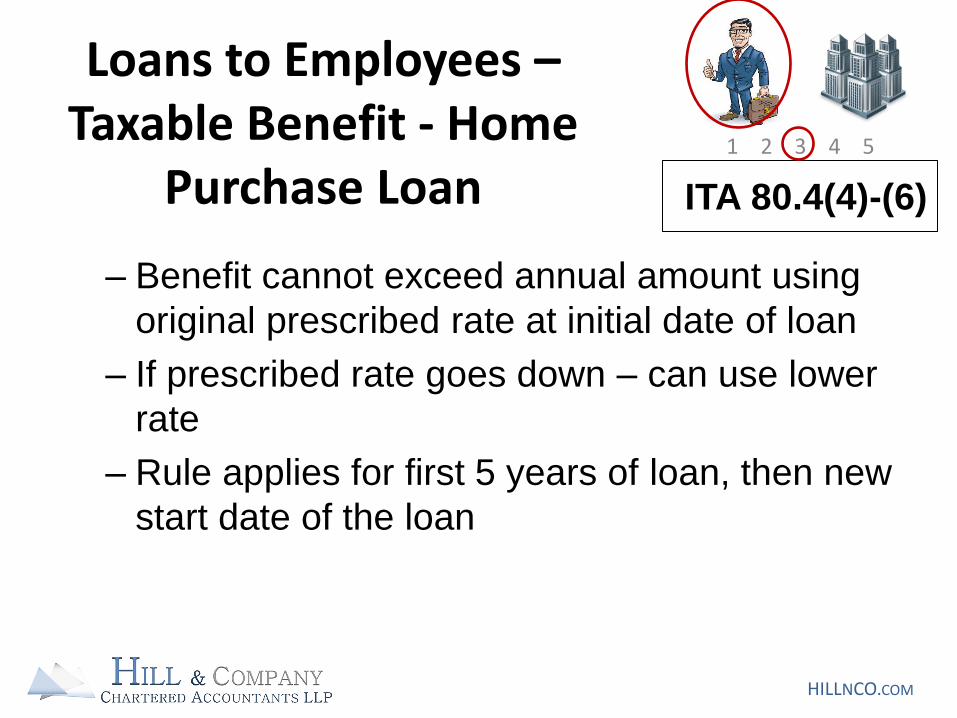

Loans to Employees – Taxable Benefit - Home

Purchase Loan

– Benefit cannot exceed annual amount using

original prescribed rate at initial date of loan

– If prescribed rate goes down – can use lower

rate

– Rule applies for first 5 years of loan, then new

start date of the loan

ITA 80.4(4)-(6)

1 2 3 4 5

HILLNCO.COM

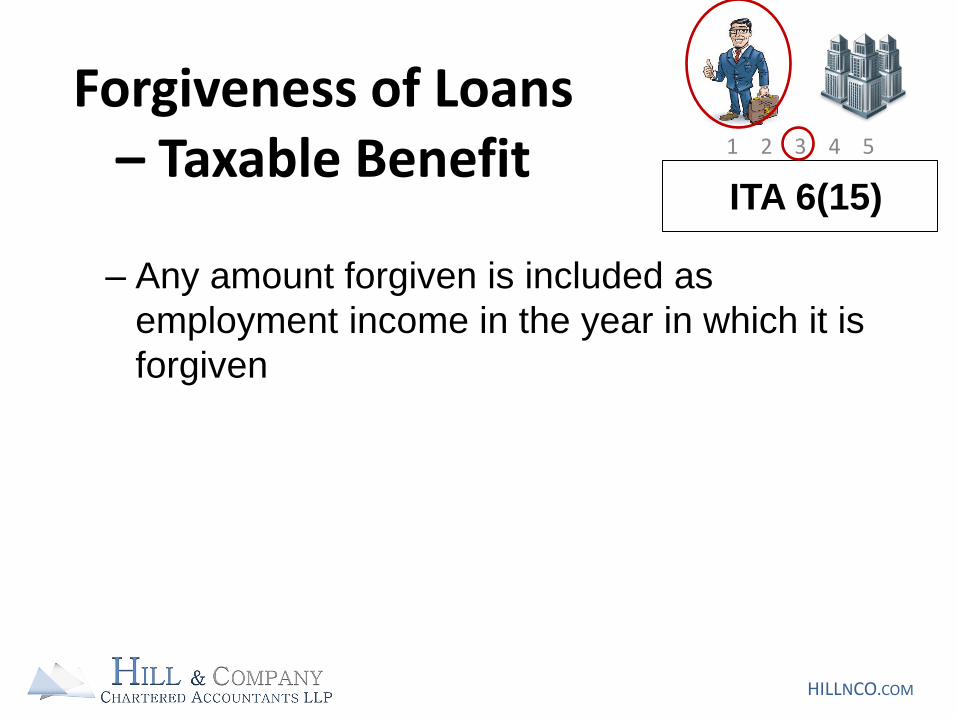

Forgiveness of Loans – Taxable Benefit

– Any amount forgiven is included as

employment income in the year in which it is

forgiven

ITA 6(15)

1 2 3 4 5

HILLNCO.COM

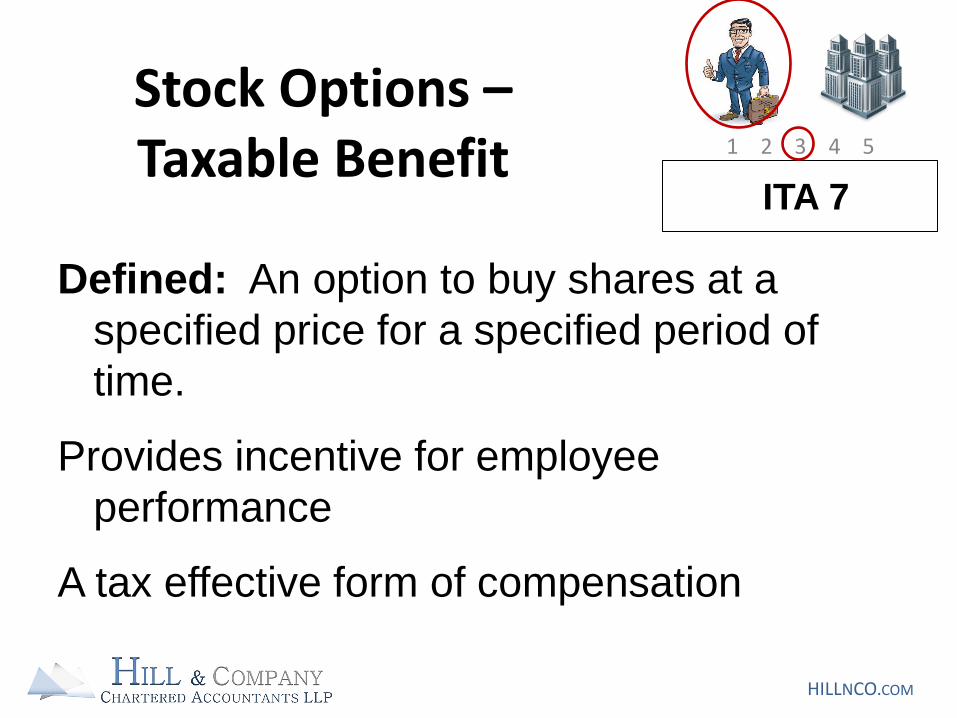

Stock Options – Taxable Benefit

Defined: An option to buy shares at a

specified price for a specified period of

time.

Provides incentive for employee

performance

A tax effective form of compensation

ITA 7

1 2 3 4 5

HILLNCO.COM

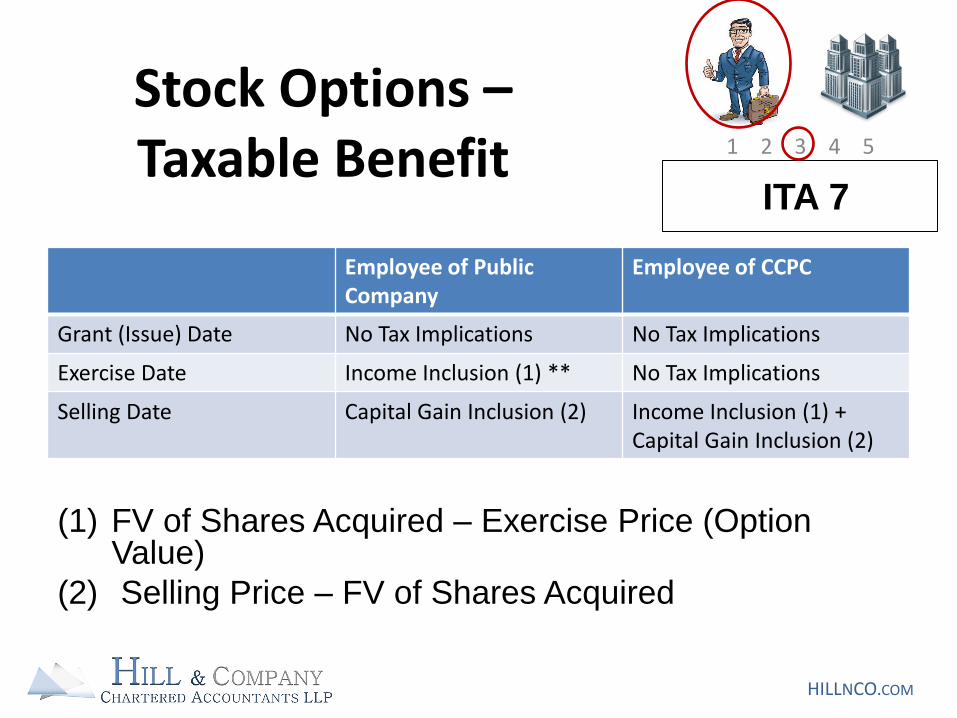

Stock Options – Taxable Benefit

Employee of Public Company

Employee of CCPC

Grant (Issue) Date No Tax Implications No Tax Implications

Exercise Date Income Inclusion (1) ** No Tax Implications

Selling Date Capital Gain Inclusion (2) Income Inclusion (1) + Capital Gain Inclusion (2)

ITA 7

(1) FV of Shares Acquired – Exercise Price (Option Value)

(2) Selling Price – FV of Shares Acquired

1 2 3 4 5

HILLNCO.COM

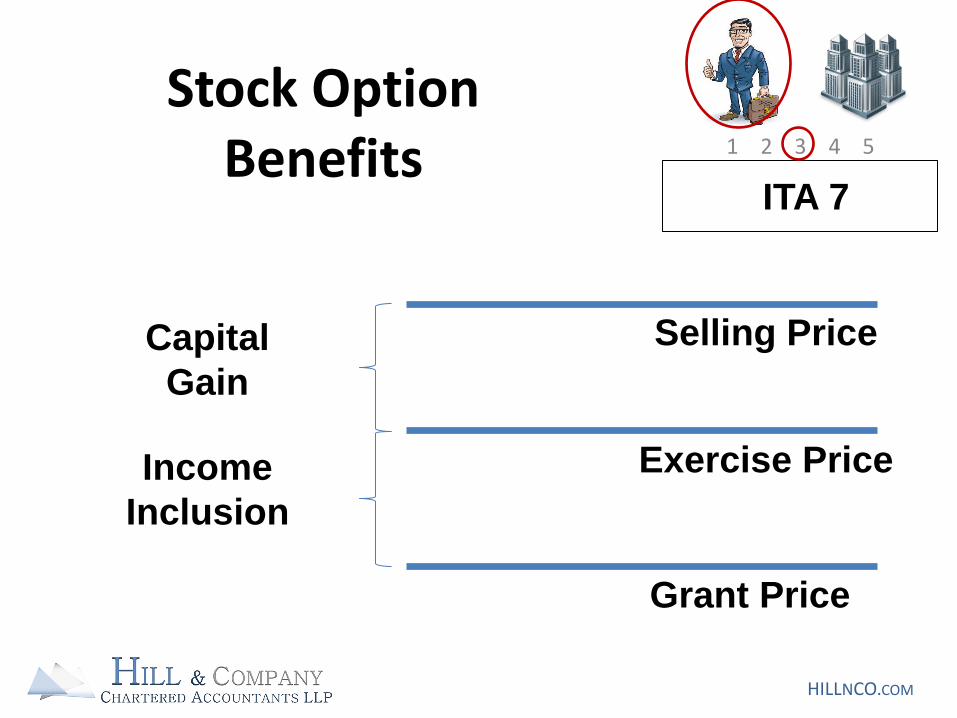

Stock Option Benefits

Grant Price

Exercise Price

Selling Price

Income

Inclusion

Capital

Gain

ITA 7

1 2 3 4 5

HILLNCO.COM

Stock Option Deduction

• One-half of employment income inclusion (taken at same time

as income inclusion)

• A deduction from Net Income to get Taxable Income

• Available if:

– At issue: option price ≥ market price; Or

– If CCPC – Available if shares held for two

years without regard to option price.

ITA 110(1)(d), (d.1)

1 2 3 4 5

HILLNCO.COM

Housing Loss Reimbursement

– Must be included in income unless: • Eligible Housing Loss

– Meet requirements for moving expense deduction

– Tax free Eligible Housing Loss • 100% of first $15,000

• 50% of any loss in excess of $15,000

ITA 6(19 – 22)

![Fringe Benefits 2015.pptx [Read-Only] - Iowa State … 1 Taxable and Non‐Taxable Fringe Benefits Center for Agricultural Law and Taxation Kristy Maitre –Tax Specialist August 10,](https://img.pdfslide.us/doc/110x75/5ace69037f8b9a56098bbf5f/fringe-benefits-2015pptx-read-only-iowa-state-1-taxable-and-nontaxable.jpg)