Embed Size (px)

Citation preview

Dr. Bernd Fischer

Five years after Lehman

What are we doing different from a risk perspective?

10. June 2014

© IDS GmbH – Analysis and Reporting Services

2

2

Agenda

2 Consequences of the crisis and impact of regulatory changes 2

3 Impact on the treatment of risks and performance analysis

1 Looking back – what happened?

4 Conclusions

© IDS GmbH – Analysis and Reporting Services

3

3

2 Consequences of the crisis and impact of regulatory changes 2

3 Impact on the treatment of risks and performance analysis

1 Looking back – what happened?

4 Conclusions

© IDS GmbH – Analysis and Reporting Services

4

4

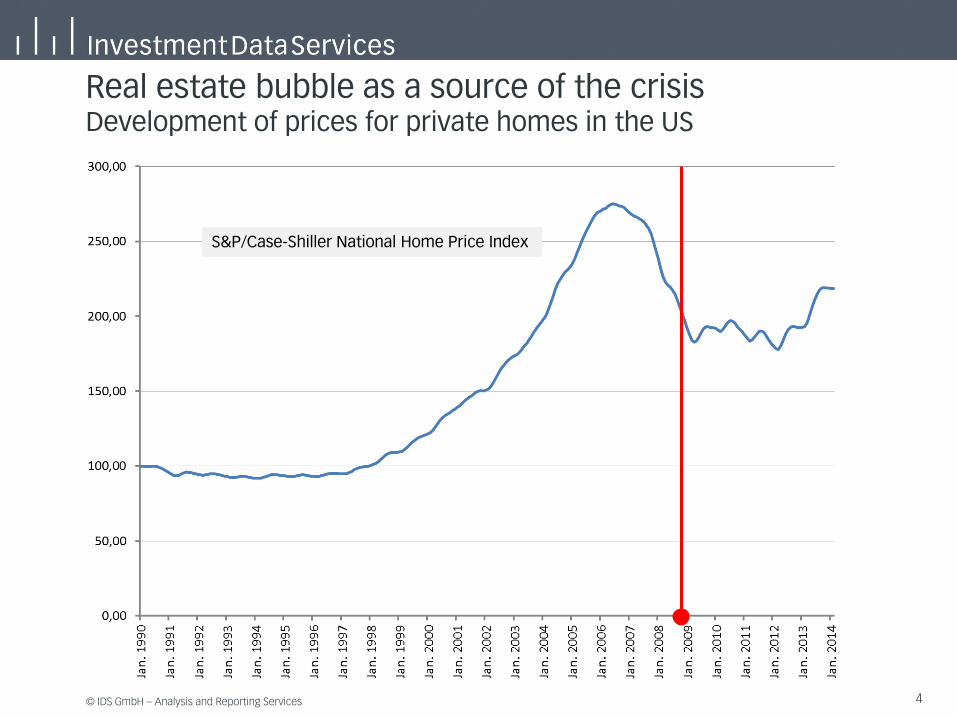

Real estate bubble as a source of the crisis Development of prices for private homes in the US

S&P/Case-Shiller National Home Price Index

© IDS GmbH – Analysis and Reporting Services

5

5

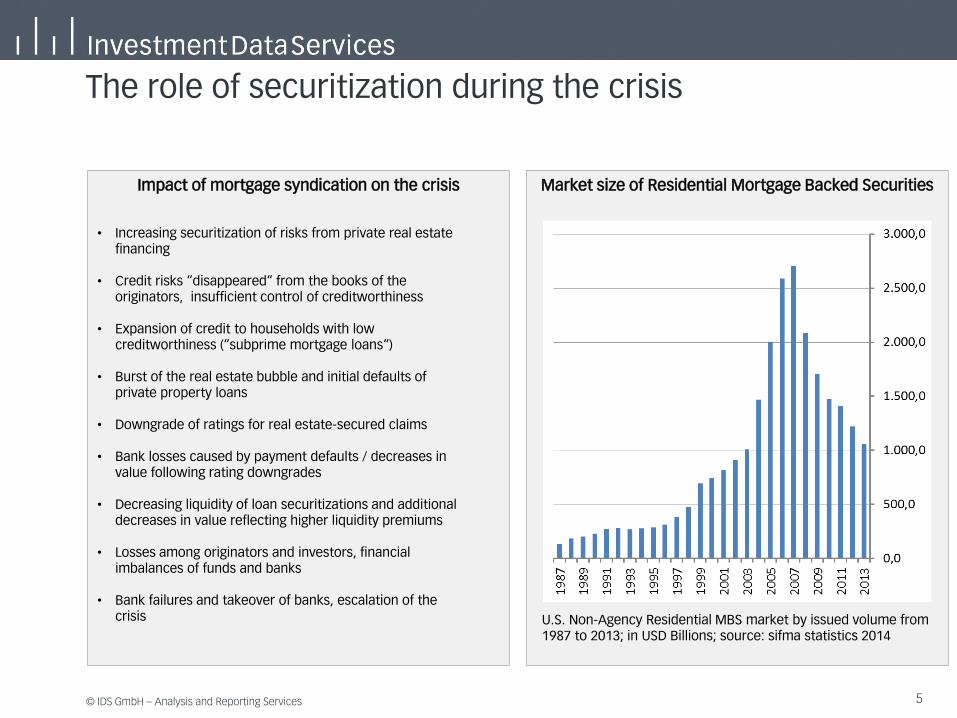

The role of securitization during the crisis

Market size of Residential Mortgage Backed Securities Impact of mortgage syndication on the crisis

U.S. Non-Agency Residential MBS market by issued volume from 1987 to 2013; in USD Billions; source: sifma statistics 2014

• Increasing securitization of risks from private real estate financing

• Credit risks “disappeared“ from the books of the originators, insufficient control of creditworthiness

• Expansion of credit to households with low creditworthiness (“subprime mortgage loans“)

• Burst of the real estate bubble and initial defaults of private property loans

• Downgrade of ratings for real estate-secured claims

• Bank losses caused by payment defaults / decreases in value following rating downgrades

• Decreasing liquidity of loan securitizations and additional decreases in value reflecting higher liquidity premiums

• Losses among originators and investors, financial imbalances of funds and banks

• Bank failures and takeover of banks, escalation of the crisis

© IDS GmbH – Analysis and Reporting Services

6

6

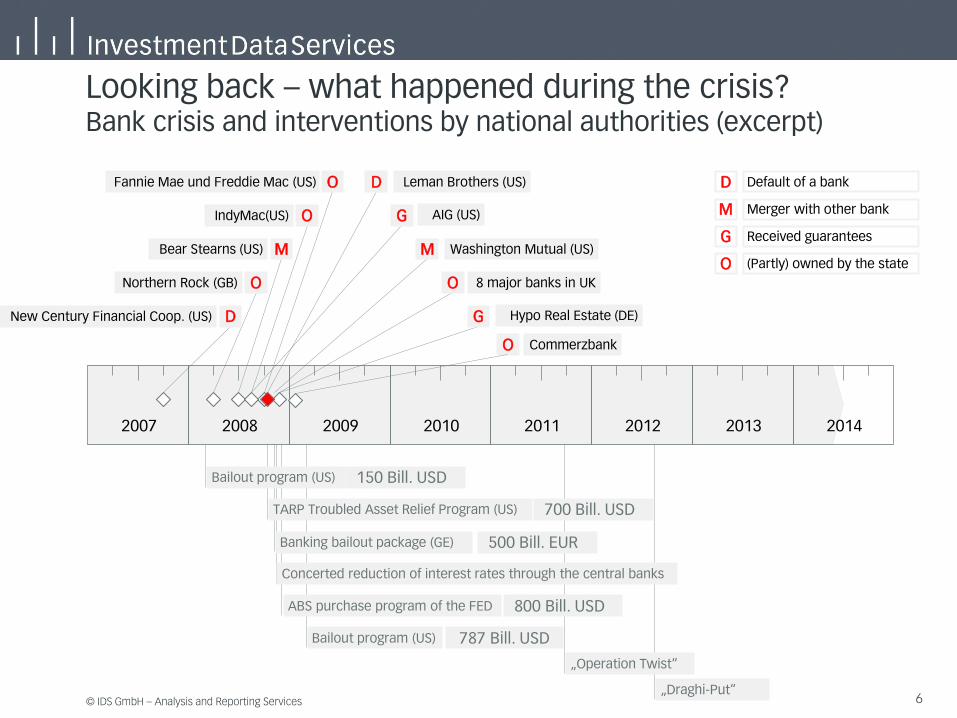

Looking back – what happened during the crisis? Bank crisis and interventions by national authorities (excerpt)

2007 2008 2009 2010 2011 2012 2013 2014

Default of a bank D

Merger with other bank M

Received guarantees G

(Partly) owned by the state O

New Century Financial Coop. (US) D

Northern Rock (GB) O

Bear Stearns (US) M

IndyMac(US) O

Fannie Mae und Freddie Mac (US) O Leman Brothers (US) D

AIG (US) G

Washington Mutual (US) M

8 major banks in UK O

Hypo Real Estate (DE) G

Bailout program (US) 150 Bill. USD

TARP Troubled Asset Relief Program (US) 700 Bill. USD

Banking bailout package (GE) 500 Bill. EUR

Concerted reduction of interest rates through the central banks

ABS purchase program of the FED 800 Bill. USD

Bailout program (US) 787 Bill. USD

Commerzbank O

„Operation Twist“

„Draghi-Put“

© IDS GmbH – Analysis and Reporting Services

7

7

2007 2008 2009 2010 2011 2012 2013 2014

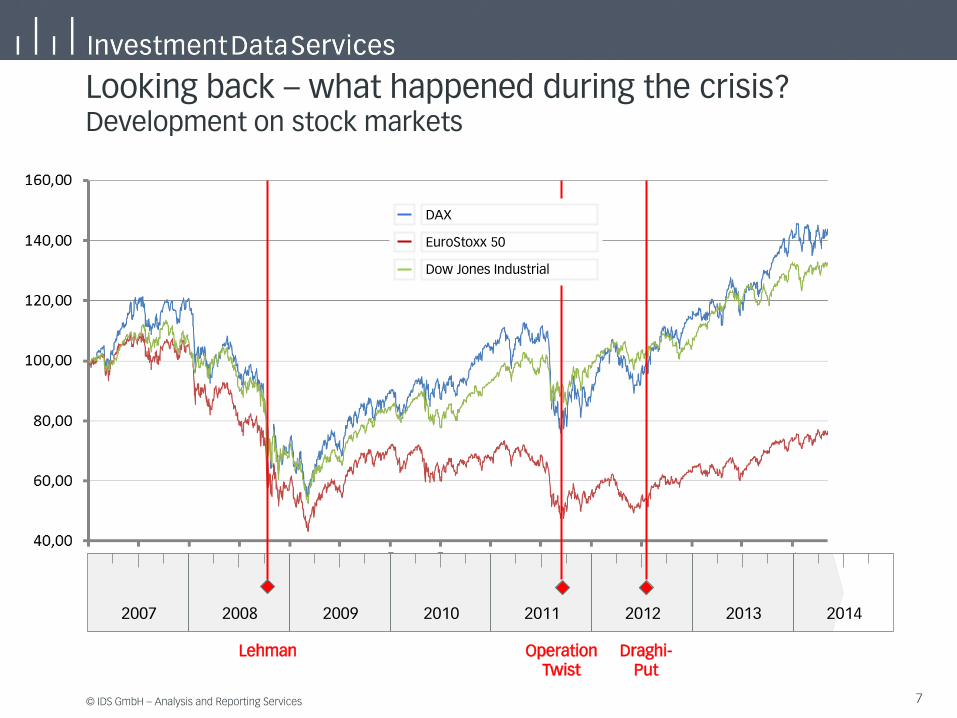

Looking back – what happened during the crisis? Development on stock markets

Lehman Draghi- Put

Operation Twist

EuroStoxx 50

Dow Jones Industrial

DAX

© IDS GmbH – Analysis and Reporting Services

8

8

2007 2008 2009 2010 2011 2012 2013 2014

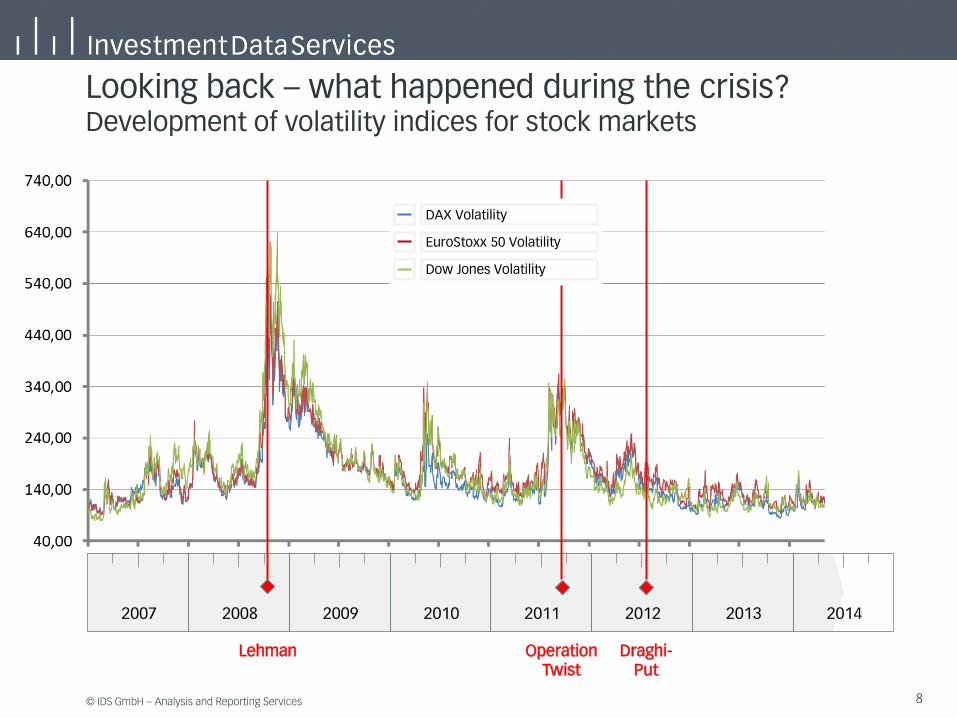

Looking back – what happened during the crisis? Development of volatility indices for stock markets

Lehman Draghi- Put

Operation Twist

DAX Volatility

EuroStoxx 50 Volatility

Dow Jones Volatility

© IDS GmbH – Analysis and Reporting Services

9

9

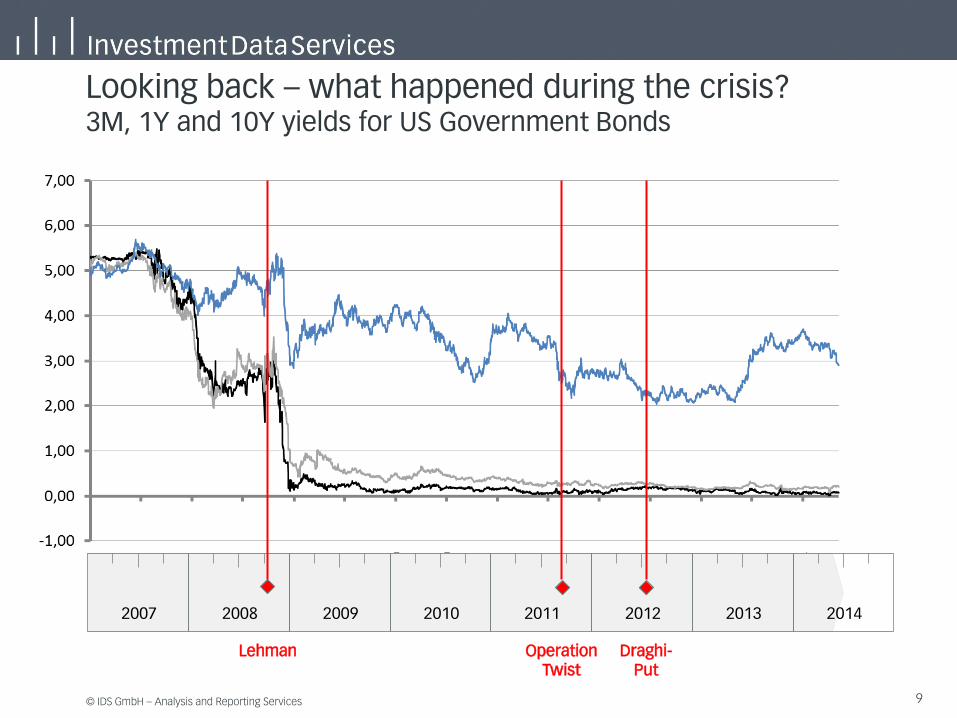

Looking back – what happened during the crisis? 3M, 1Y and 10Y yields for US Government Bonds

2007 2008 2009 2010 2011 2012 2013 2014

Lehman Draghi- Put

Operation Twist

© IDS GmbH – Analysis and Reporting Services

10

10

2007 2008 2009 2010 2011 2012 2013 2014

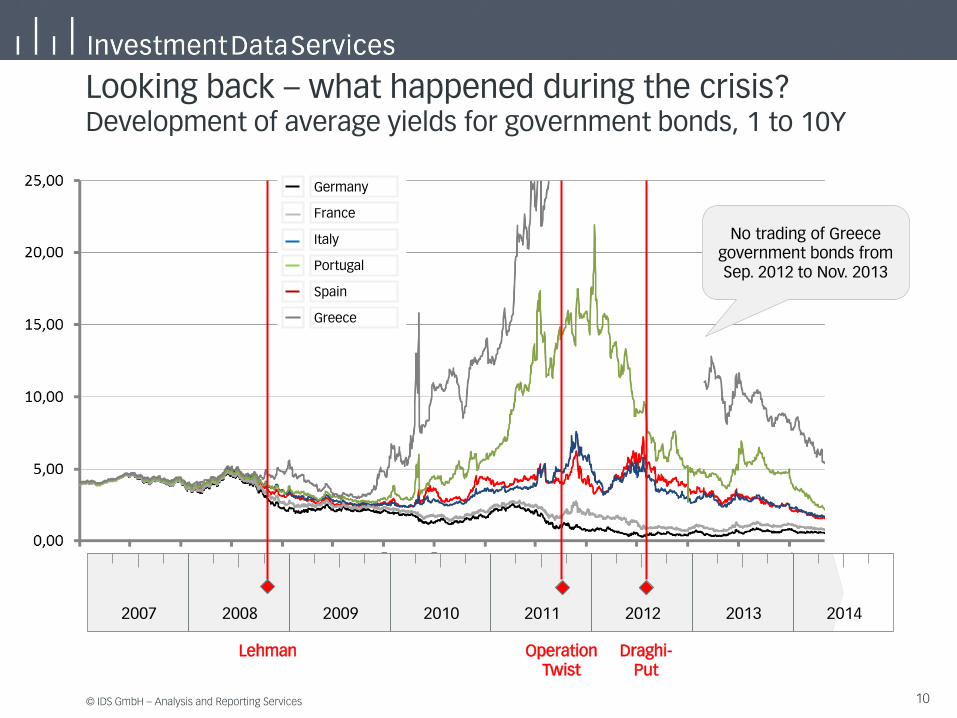

Looking back – what happened during the crisis? Development of average yields for government bonds, 1 to 10Y

No trading of Greece government bonds from Sep. 2012 to Nov. 2013

Lehman Draghi- Put

Operation Twist

Germany

France

Italy

Portugal

Spain

Greece

© IDS GmbH – Analysis and Reporting Services

11

11

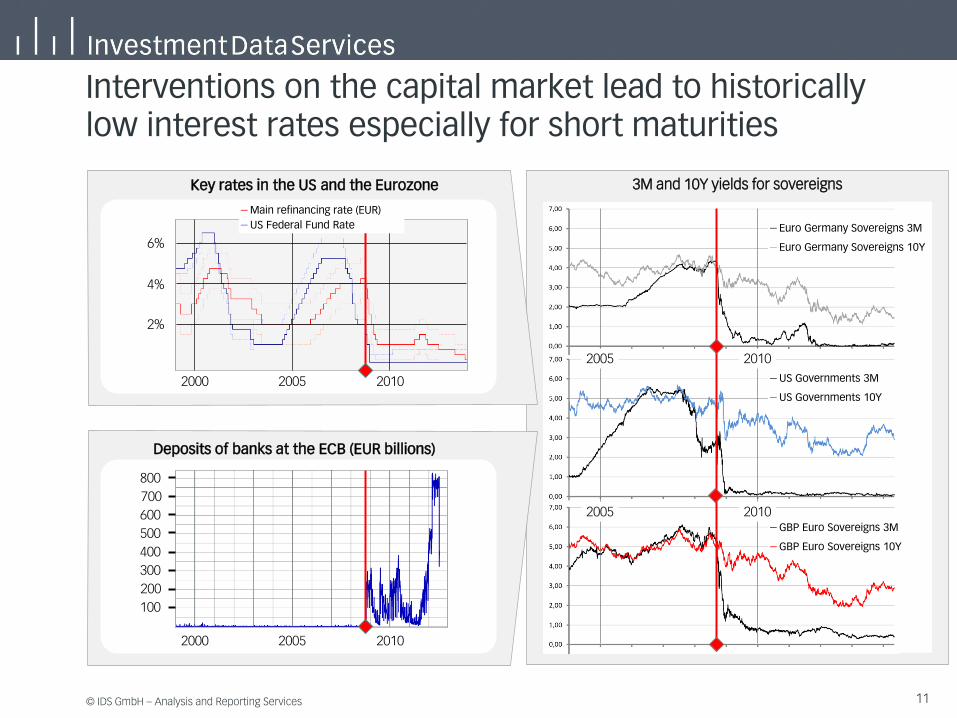

3M and 10Y yields for sovereigns

2005 2010

Euro Germany Sovereigns 3M

Euro Germany Sovereigns 10Y

US Governments 3M

US Governments 10Y

GBP Euro Sovereigns 3M

GBP Euro Sovereigns 10Y

2005 2010

500

Interventions on the capital market lead to historically low interest rates especially for short maturities

2000 2005 2010

2%

4%

2000 2005 2010

6%

US Federal Fund Rate

Main refinancing rate (EUR)

Key rates in the US and the Eurozone

Deposits of banks at the ECB (EUR billions)

100

200

300

400

600

700

800

© IDS GmbH – Analysis and Reporting Services

12

12

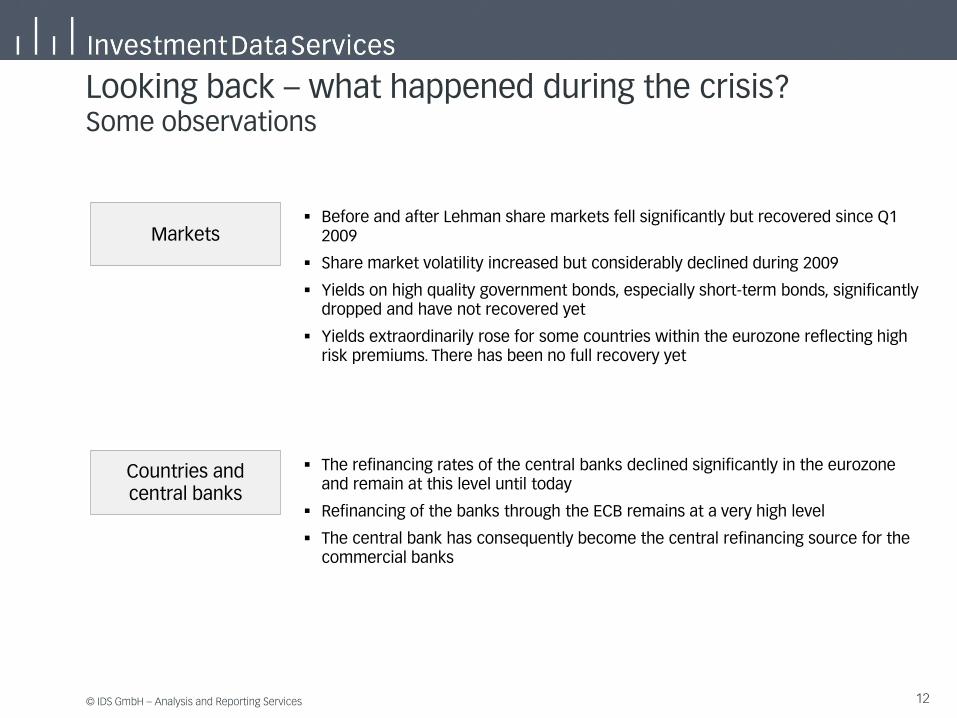

Looking back – what happened during the crisis? Some observations

Markets Before and after Lehman share markets fell significantly but recovered since Q1

2009

Share market volatility increased but considerably declined during 2009

Yields on high quality government bonds, especially short-term bonds, significantly dropped and have not recovered yet

Yields extraordinarily rose for some countries within the eurozone reflecting high risk premiums. There has been no full recovery yet

Countries and central banks

The refinancing rates of the central banks declined significantly in the eurozone and remain at this level until today

Refinancing of the banks through the ECB remains at a very high level

The central bank has consequently become the central refinancing source for the commercial banks

© IDS GmbH – Analysis and Reporting Services

13

13

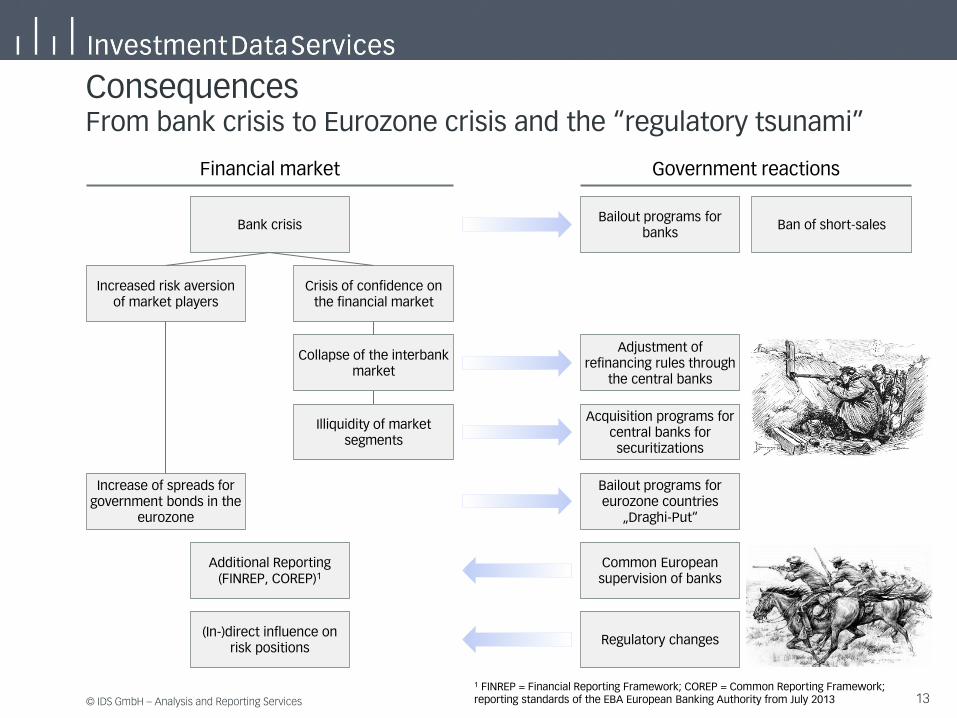

Consequences From bank crisis to Eurozone crisis and the “regulatory tsunami”

Bank crisis

Collapse of the interbank market

Illiquidity of market segments

Increase of spreads for government bonds in the

eurozone

Additional Reporting (FINREP, COREP)1

(In-)direct influence on risk positions

Adjustment of refinancing rules through

the central banks

Acquisition programs for central banks for securitizations

Bailout programs for banks

Ban of short-sales

Bailout programs for eurozone countries

„Draghi-Put“

Common European supervision of banks

Regulatory changes

Crisis of confidence on the financial market

Increased risk aversion of market players

Financial market Government reactions

1 FINREP = Financial Reporting Framework; COREP = Common Reporting Framework; reporting standards of the EBA European Banking Authority from July 2013

© IDS GmbH – Analysis and Reporting Services

14

14

2 Consequences of the crisis and impact of regulatory changes 2

3 Impact on the treatment of risks and performance analysis

1 Looking back – what happened?

4 Conclusions

© IDS GmbH – Analysis and Reporting Services

15

15

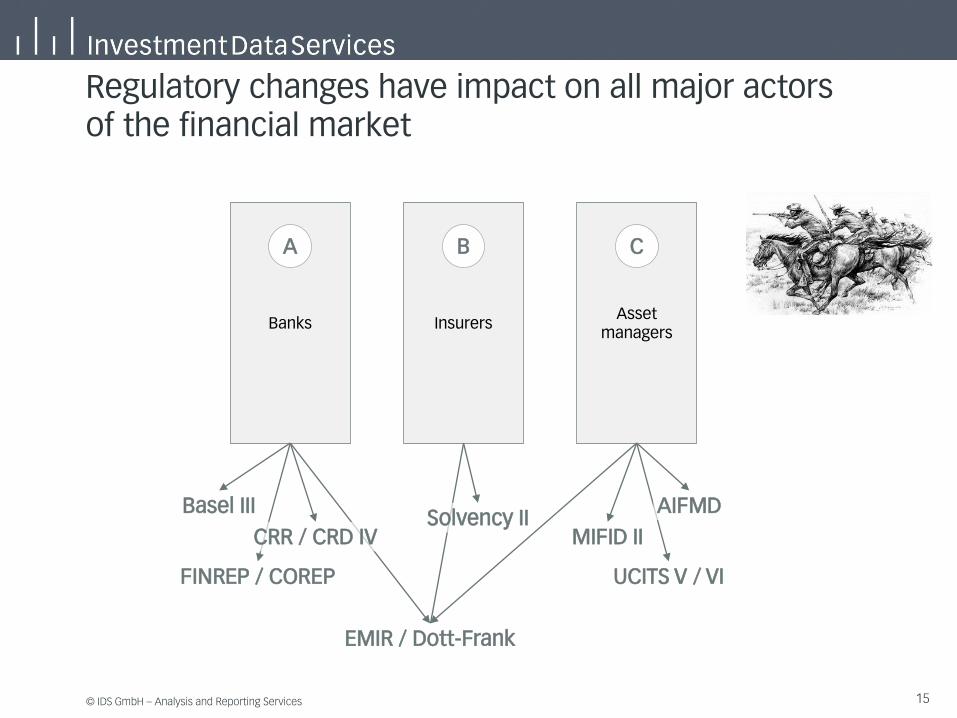

Regulatory changes have impact on all major actors of the financial market

Banks Insurers Asset

managers

A B C

Basel III

CRR / CRD IV Solvency II

FINREP / COREP

AIFMD

MIFID II

UCITS V / VI

EMIR / Dott-Frank

© IDS GmbH – Analysis and Reporting Services

16

16

Requirements for capital resources of banks will considerably rise following Basel III

From 2019 banks of the EU need to have available 62.5% of additional funds

In addition, quality requirements for the capital will rise:

The future core capital ratio will increase by 125% compared to today

Requirements for core capital instruments will be higher

The risks institutions will be able to take on with the same amount of capital will be lower1

Current ROC ratios will not be attainable

The competition of business areas for risk capital will tighten

Institutions will concentrate even more on “profitable” risks

1 ”Lower” in the sense of the regulatory risk assessment tools

62,5%

125%

Capital

A

Banks

© IDS GmbH – Analysis and Reporting Services

17

17

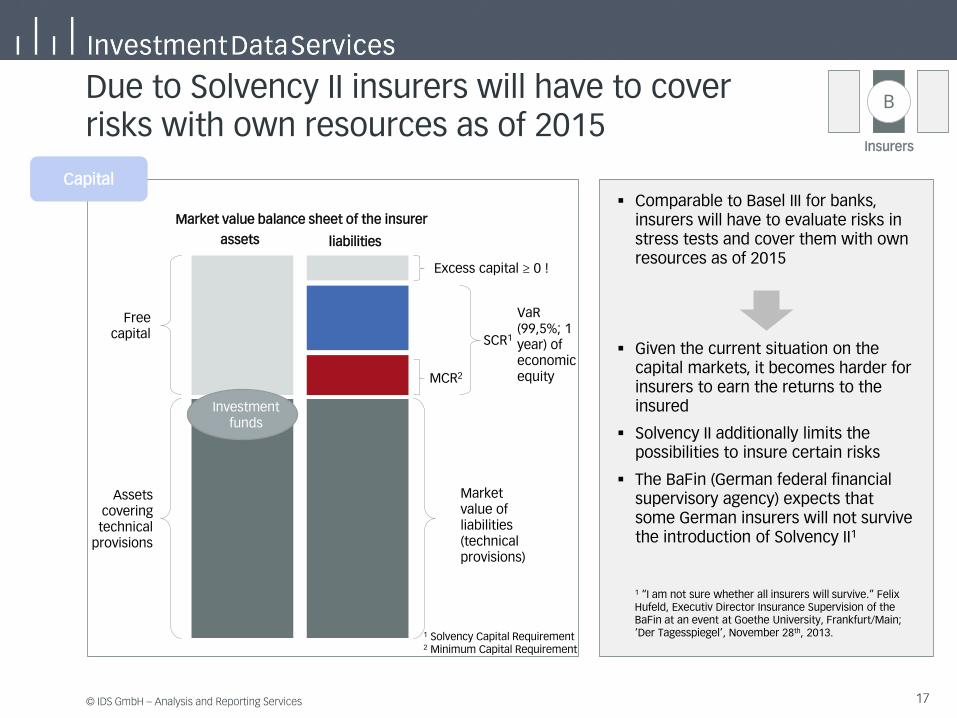

Due to Solvency II insurers will have to cover risks with own resources as of 2015

Comparable to Basel III for banks, insurers will have to evaluate risks in stress tests and cover them with own resources as of 2015

Given the current situation on the capital markets, it becomes harder for insurers to earn the returns to the insured

Solvency II additionally limits the possibilities to insure certain risks

The BaFin (German federal financial supervisory agency) expects that some German insurers will not survive the introduction of Solvency II1

1 “I am not sure whether all insurers will survive.” Felix Hufeld, Executiv Director Insurance Supervision of the BaFin at an event at Goethe University, Frankfurt/Main; ‘Der Tagesspiegel’, November 28th, 2013.

Capital

Market value of liabilities (technical provisions)

MCR2

SCR1

Excess capital ≥ 0 !

Free capital

Assets covering technical

provisions

assets liabilities

VaR (99,5%; 1 year) of economic equity

Market value balance sheet of the insurer

Investment funds

1 Solvency Capital Requirement 2 Minimum Capital Requirement

Insurers

B

© IDS GmbH – Analysis and Reporting Services

18

18

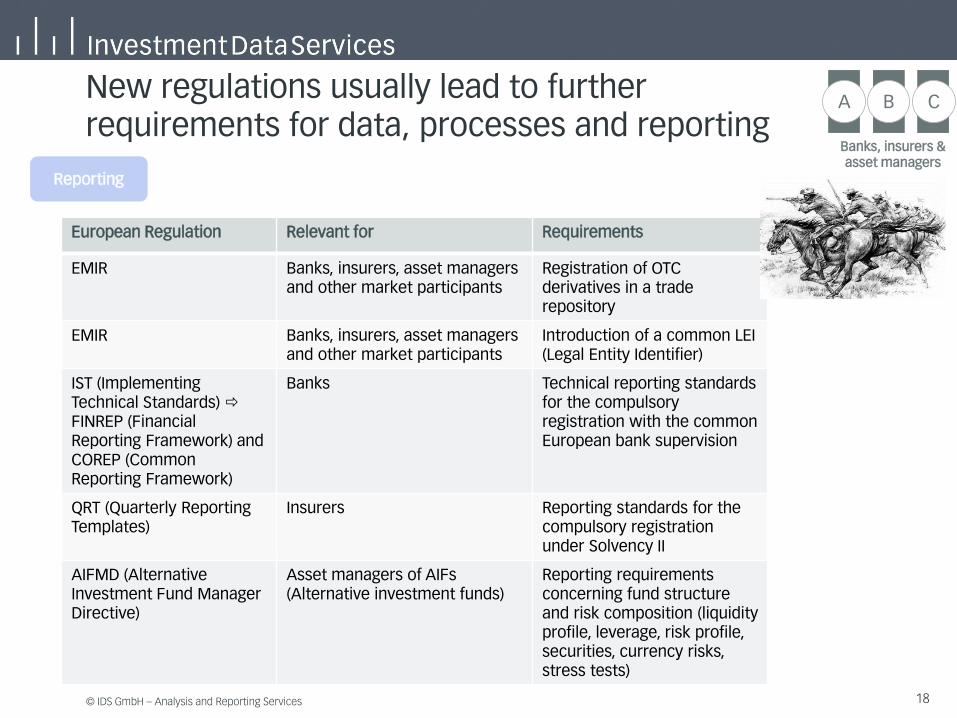

B New regulations usually lead to further requirements for data, processes and reporting

European Regulation Relevant for Requirements

EMIR Banks, insurers, asset managers and other market participants

Registration of OTC derivatives in a trade repository

EMIR Banks, insurers, asset managers and other market participants

Introduction of a common LEI (Legal Entity Identifier)

IST (Implementing Technical Standards) FINREP (Financial Reporting Framework) and COREP (Common Reporting Framework)

Banks Technical reporting standards for the compulsory registration with the common European bank supervision

QRT (Quarterly Reporting Templates)

Insurers Reporting standards for the compulsory registration under Solvency II

AIFMD (Alternative Investment Fund Manager Directive)

Asset managers of AIFs (Alternative investment funds)

Reporting requirements concerning fund structure and risk composition (liquidity profile, leverage, risk profile, securities, currency risks, stress tests)

Reporting

A C

Banks, insurers & asset managers

© IDS GmbH – Analysis and Reporting Services

19

19

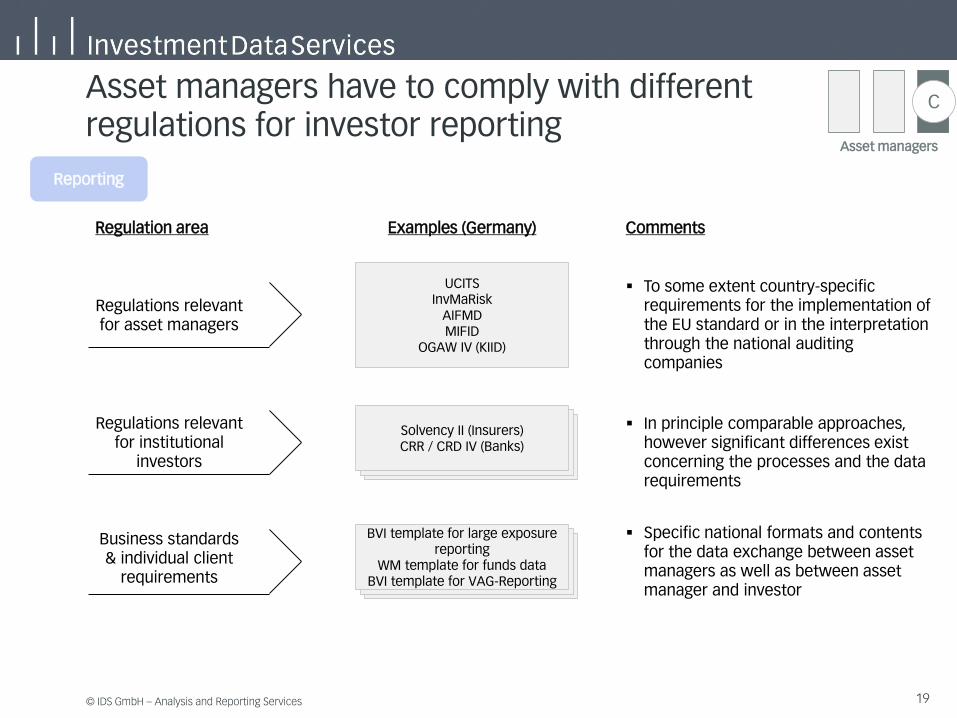

Asset managers have to comply with different regulations for investor reporting

Regulation area Examples (Germany) Comments

To some extent country-specific requirements for the implementation of the EU standard or in the interpretation through the national auditing companies

UCITS

InvMaRisk AIFMD MIFID

OGAW IV (KIID)

Regulations relevant for asset managers

Solvency II (Insurers) CRR / CRD IV (Banks)

Regulations relevant for institutional

investors

In principle comparable approaches, however significant differences exist concerning the processes and the data requirements

BVI template for large exposure reporting

WM template for funds data BVI template for VAG-Reporting

Business standards & individual client

requirements

Specific national formats and contents for the data exchange between asset managers as well as between asset manager and investor

Reporting

C

Asset managers

© IDS GmbH – Analysis and Reporting Services

20

20

Challenge 1: Classification of investments in different regulatory regimes

Exposure classes (CRR/CRD IV)

1 National governments

2 Regional governments and local authorities

3 Other authorities

4 Multilateral development banks

5 International organizations

6 Institutions

7 Covered bonds issued by banks

8 Companies

9 Retail business

10 Positions secured by real estate

11 Fund shares

12 Holdings

13 Securitizations

14 Other positions

15 Overdue positions

CIC (Solvency II)

1 Government bonds

2 Corporate bonds

3 Equity instrument

4 Investment funds

5 Structured debt instruments

6 Asset-backed securities

7 Cash and deposits

8 Mortgages and loans

9 Real estate

A Futures

B Purchase options

C Selling options

D Swaps

E Forwards

F Credit derivatives

Asset managers need to adhere to

both classifications and comply with the

necessary regulations and

processes

Reporting

C

Asset managers

© IDS GmbH – Analysis and Reporting Services

21

21

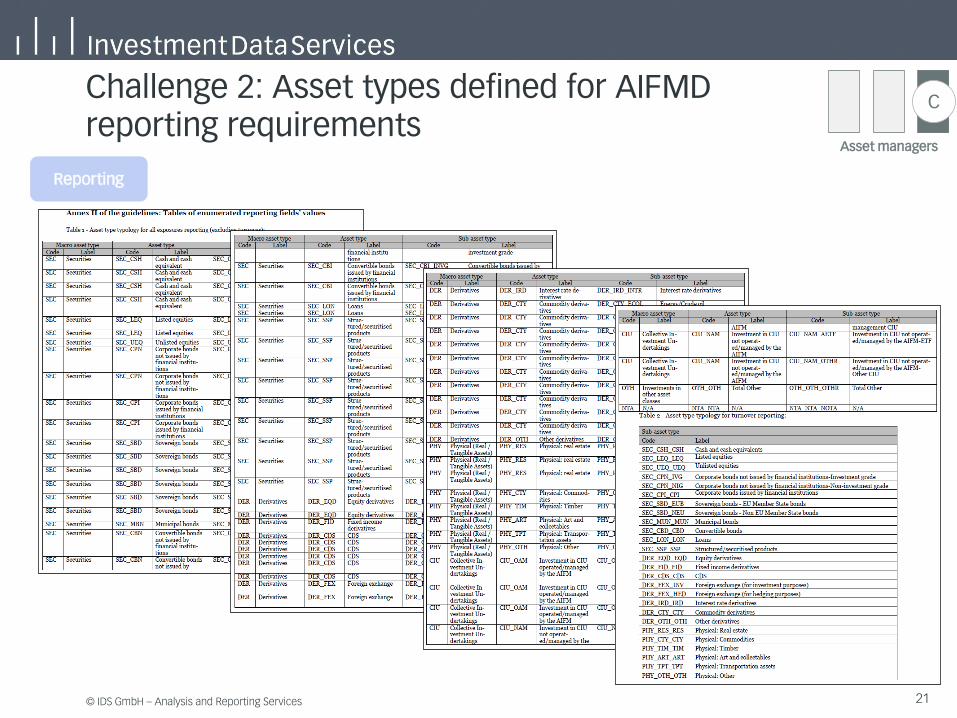

Challenge 2: Asset types defined for AIFMD reporting requirements

Reporting

C

Asset managers

© IDS GmbH – Analysis and Reporting Services

22

22

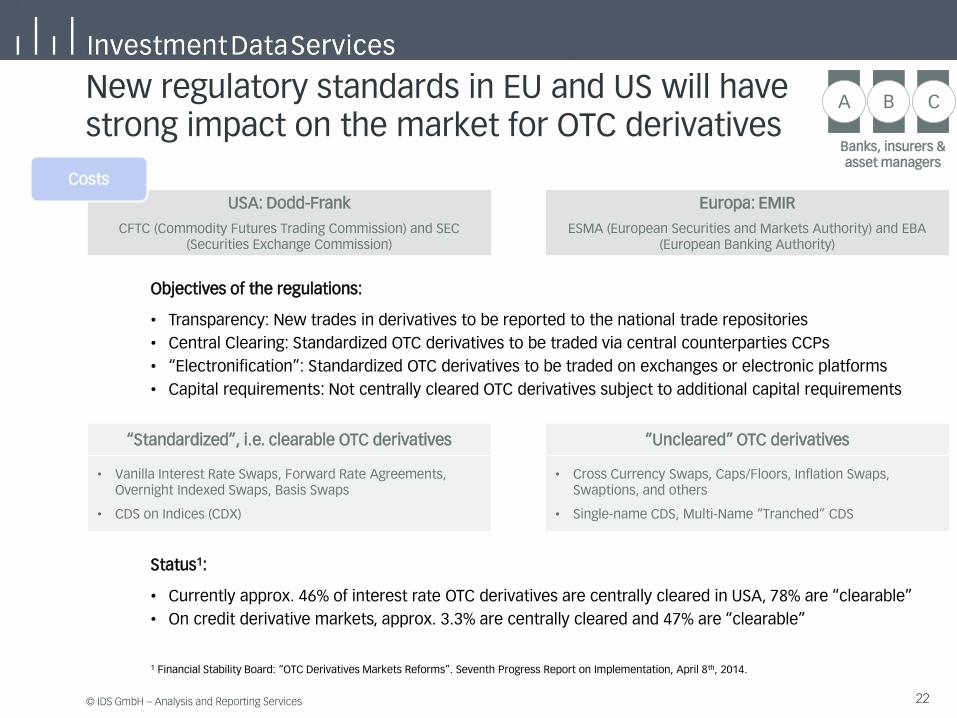

USA: Dodd-Frank

CFTC (Commodity Futures Trading Commission) and SEC (Securities Exchange Commission)

Europa: EMIR

ESMA (European Securities and Markets Authority) and EBA (European Banking Authority)

Objectives of the regulations:

• Transparency: New trades in derivatives to be reported to the national trade repositories

• Central Clearing: Standardized OTC derivatives to be traded via central counterparties CCPs

• “Electronification”: Standardized OTC derivatives to be traded on exchanges or electronic platforms

• Capital requirements: Not centrally cleared OTC derivatives subject to additional capital requirements

“Standardized”, i.e. clearable OTC derivatives

• Vanilla Interest Rate Swaps, Forward Rate Agreements, Overnight Indexed Swaps, Basis Swaps

• CDS on Indices (CDX)

“Uncleared” OTC derivatives

• Cross Currency Swaps, Caps/Floors, Inflation Swaps, Swaptions, and others

• Single-name CDS, Multi-Name “Tranched” CDS

New regulatory standards in EU and US will have strong impact on the market for OTC derivatives

Costs

Status1:

• Currently approx. 46% of interest rate OTC derivatives are centrally cleared in USA, 78% are “clearable”

• On credit derivative markets, approx. 3.3% are centrally cleared and 47% are “clearable”

1 Financial Stability Board: “OTC Derivatives Markets Reforms”. Seventh Progress Report on Implementation, April 8th, 2014.

B A C

Banks, insurers & asset managers

© IDS GmbH – Analysis and Reporting Services

23

23

Solvency capital costs for uncleared OTC derivatives Margins for centrally cleared OTC derivatives

As a result, economic costs will arise for both cleared and uncleared OTC derivatives

Costs

Initial margin

• based on value-at-risk portfolio models, with add-ons for liquidity, concentration, and counterparty risks

• Models differ between different CCPs

Variation margin +

While for initial margins sovereign bonds, MBS, corporate securities, and gold are usually accepted by the CCPs, variation margins can only be settled in cash

Additional costs for funding of collateral Additional costs for regulatory capital

A

Banks

Solvency capital requirement for credit risks in the derivative 1

• Market value + Add-on2

2 According to the mark-to-market method, Art. 274 CRR

Solvency capital requirement for possible down-grades of the counterparty according to the CVA credit valuation adjustment approach3

+

3 According to Art. 110 (4) CRR and the Regulatory Technical Standards of EBA European Banking Authority

1 Capital requirements for all derivatives

© IDS GmbH – Analysis and Reporting Services

24

24

2 Consequences of the crisis and impact of regulatory changes 2

3 Impact on the treatment of risks and performance analysis

1 Looking back – what happened?

4 Conclusions

© IDS GmbH – Analysis and Reporting Services

25

25

Crisis and regulatory changes have many impacts – in the following, we will focus on some of them

Risk measurement

Performance analysis

Fair value calculation & pricing

Leverage

New risk models for alternative assets

1

2

3

4

5

© IDS GmbH – Analysis and Reporting Services

26

26

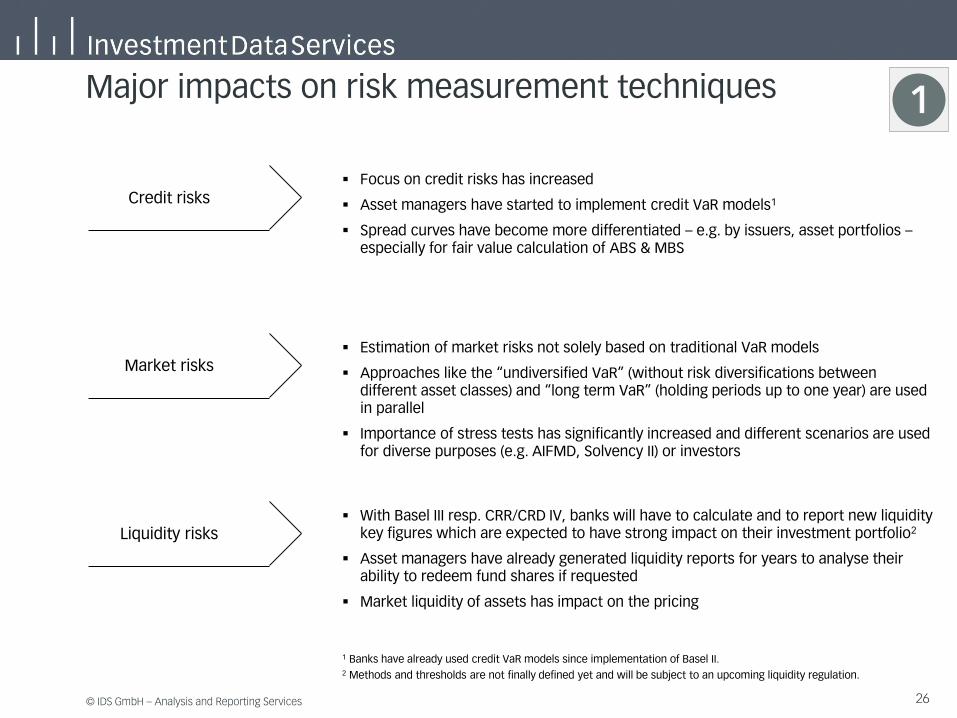

Major impacts on risk measurement techniques 1

Focus on credit risks has increased

Asset managers have started to implement credit VaR models1

Spread curves have become more differentiated – e.g. by issuers, asset portfolios – especially for fair value calculation of ABS & MBS

Credit risks

Market risks

1 Banks have already used credit VaR models since implementation of Basel II.

Estimation of market risks not solely based on traditional VaR models

Approaches like the “undiversified VaR” (without risk diversifications between different asset classes) and “long term VaR” (holding periods up to one year) are used in parallel

Importance of stress tests has significantly increased and different scenarios are used for diverse purposes (e.g. AIFMD, Solvency II) or investors

Liquidity risks With Basel III resp. CRR/CRD IV, banks will have to calculate and to report new liquidity

key figures which are expected to have strong impact on their investment portfolio2

Asset managers have already generated liquidity reports for years to analyse their ability to redeem fund shares if requested

Market liquidity of assets has impact on the pricing

2 Methods and thresholds are not finally defined yet and will be subject to an upcoming liquidity regulation.

© IDS GmbH – Analysis and Reporting Services

27

27

Regulation Relevant for Requirement

UCITS IV (DerivateV) Asset managers Daily VaR; monthly stress tests according to the requirements defined by the asset manager

CRR / CRD IV Banks Monthly stress tests according to the requirements made by specific investors or associations

CRR / CRD IV Banks Long-term VaR Undiversified VaR

Solvency II Insurers Quarterly stress tests according to the requirements defined by the regulatory authorities

AIFMD Asset managers Quarterly stress tests according to the requirements defined by the regulatory authorities

Internal risk management

Asset managers Partly internal methods for guarantee funds or the market risk analysis of the portfolio management

Example: Calculation of market risks for funds in different regulatory regimes

Funds are often sold to investors via share classes. Thus, it becomes necessary to calculate portfolios using different calculation methods !

1

© IDS GmbH – Analysis and Reporting Services

28

28

Different leverage calculation methods according to CESR and AIFMD requirements

CESR (for UCITS funds)

AIFMD (gross approach)

AIFMD (commitment approach)

Cash Not included Not included Market value

Derivatives Add-on2 Market value + Add-on Market value + Add-on

Securities with embedded derivatives

Market value + Add-on Market value + Add-on Market value + Add-on

Netting and hedging Optional Prohibited Obligatory

2 Add-on according to mark-to-market method of CRR = Base value of derivative (nominal amount for nominal underlying position) multiplied with a factor which depends on asset type and maturity of derivative.

not optional, both methods have to be used within AIFMD

Has to be compliant with complex rules of the AIFM directive – e.g. regular checks of sufficient correlations between stocks and indices or recognition of defined

time buckets for hedging

2

With CRR/CRD IV, banks will have to compare the nominal value of positions that carry risks with their capital1

Asset managers already calculate leverage ratios for funds and report them to national supervisory authorities

Different methods are used for different types of funds:

1 Methods and thresholds are not finally defined yet and will be subject to an upcoming liquidity regulation.

© IDS GmbH – Analysis and Reporting Services

29

29

Performance analysis 3

Development of new models in the FI space

Traditional yield curve models („shift-twist-butterfly“) less relevant for current market environment

Instead: focus on spread developments / factors

Credit-Beta relative to swap curves

New asset classes

© IDS GmbH – Analysis and Reporting Services

30

30

Valuation and pricing of financial products has become significantly more complex

4

The set of spread curve factors is more

refined

Market liquidity of assets is reflected by specific liquidity

spread premiums

Yield curves for fair value calculation of risk-free

transactions are questioned

Costs for funding of economic capital and /or collateral have

impact on the pricing

© IDS GmbH – Analysis and Reporting Services

31

31

Example 1: Libor & Euribor have lost their importance for the valuation of almost risk-free transactions

4

Calculation of market values based on SWAP curves, e.g. Euro SWAP curve

SWAP curves have been used for discounting cash flows and the calculation of forward rates

SWAP curves based on LIBOR/EURIBOR rates were considered as almost risk-free

Due to the crisis and the LIBOR/EURIBOR scandals, both rates are no longer seen as risk-free rates

Market participants use overnight rates to valuate risk-free transactions

Different yield curves are used to discount cash flows and to calculate forward rates

Euro Money Market Rates Pre-Crisis Euro Money Market Rates Post-Crisis

Comparison of Euribor rates vs. EONIA swap rates as of 24. March 2006 Comparison of Euribor rates vs. EONIA swap rates as of 24. March 2014

Euribor EONIA Swap Euribor EONIA Swap

Before “Lehman” After “Lehman”

© IDS GmbH – Analysis and Reporting Services

32

32

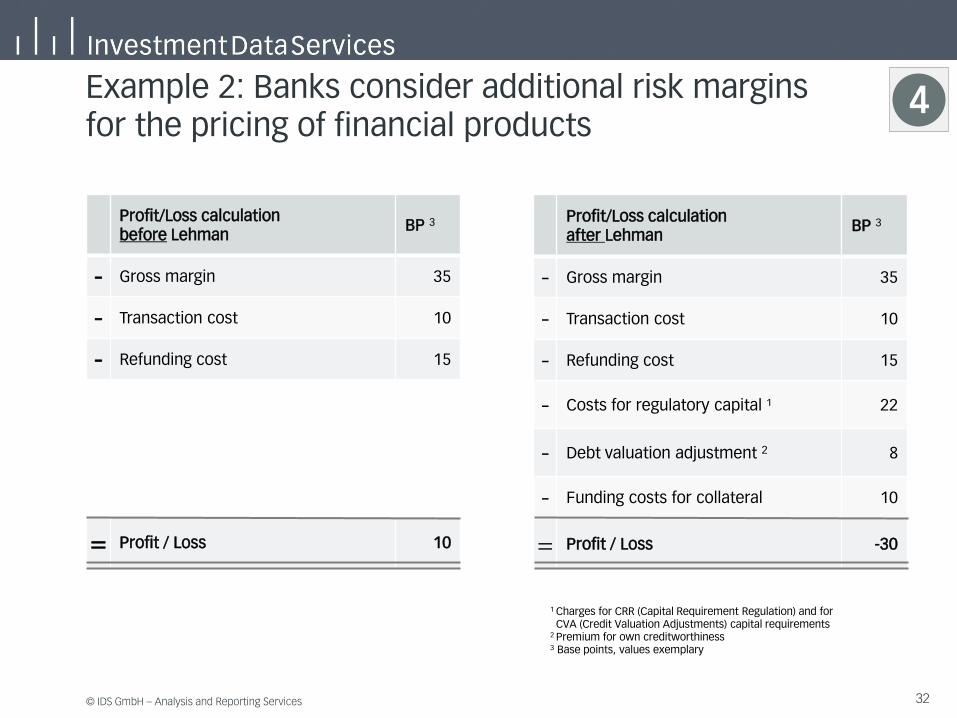

Example 2: Banks consider additional risk margins for the pricing of financial products

Profit/Loss calculation before Lehman

BP 3

- Gross margin 35

- Transaction cost 10

- Refunding cost 15

= Profit / Loss 10

Profit/Loss calculation after Lehman

BP 3

- Gross margin 35

- Transaction cost 10

- Refunding cost 15

- Costs for regulatory capital ¹ 22

- Debt valuation adjustment 2 8

- Funding costs for collateral 10

= Profit / Loss -30

1 Charges for CRR (Capital Requirement Regulation) and for CVA (Credit Valuation Adjustments) capital requirements 2 Premium for own creditworthiness 3 Base points, values exemplary

4

© IDS GmbH – Analysis and Reporting Services

33

33

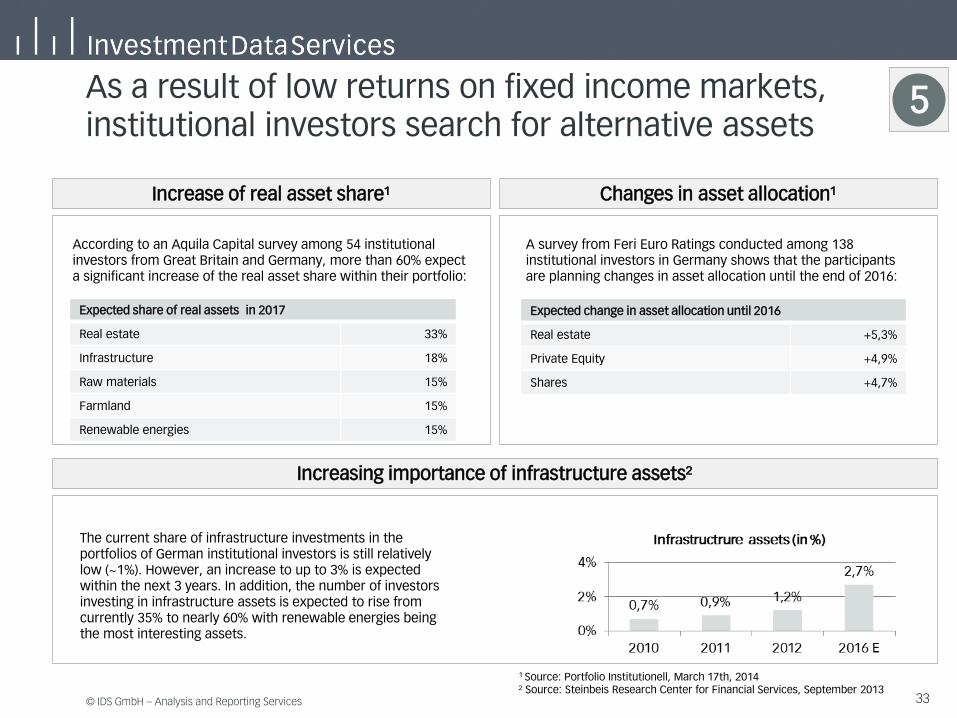

As a result of low returns on fixed income markets, institutional investors search for alternative assets

Expected share of real assets in 2017

Real estate 33%

Infrastructure 18%

Raw materials 15%

Farmland 15%

Renewable energies 15%

Expected change in asset allocation until 2016

Real estate +5,3%

Private Equity +4,9%

Shares +4,7%

Increase of real asset share¹ Changes in asset allocation¹

According to an Aquila Capital survey among 54 institutional investors from Great Britain and Germany, more than 60% expect a significant increase of the real asset share within their portfolio:

A survey from Feri Euro Ratings conducted among 138 institutional investors in Germany shows that the participants are planning changes in asset allocation until the end of 2016:

The current share of infrastructure investments in the portfolios of German institutional investors is still relatively low (~1%). However, an increase to up to 3% is expected within the next 3 years. In addition, the number of investors investing in infrastructure assets is expected to rise from currently 35% to nearly 60% with renewable energies being the most interesting assets.

Increasing importance of infrastructure assets²

1 Source: Portfolio Institutionell, March 17th, 2014 ² Source: Steinbeis Research Center for Financial Services, September 2013

5

© IDS GmbH – Analysis and Reporting Services

34

34

Redefined focus of central banks and sovereign wealth funds

5

Changes in their investment strategy

Look for innovative investments as returns of traditional assets are insufficient

Core / satellite approach

Overlay strategies

Fully transparent

© IDS GmbH – Analysis and Reporting Services

35

35

2 Consequences of the crisis and impact of regulatory changes 2

3 Impact on the treatment of risks and performance analysis

1 Looking back – what happened?

4 Conclusions

© IDS GmbH – Analysis and Reporting Services

36

36

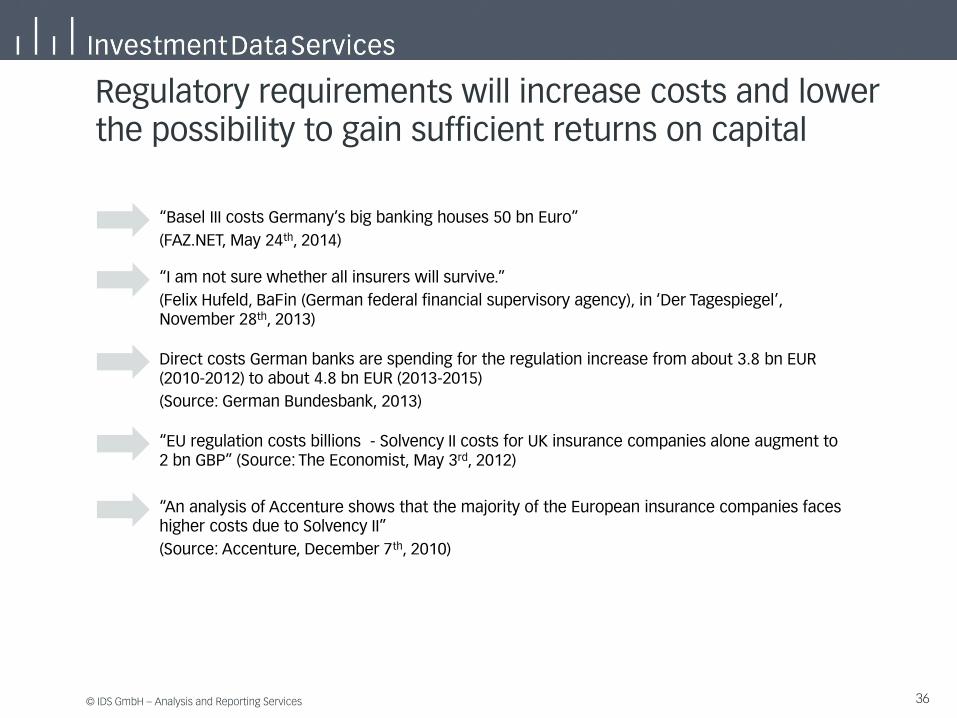

“Basel III costs Germany’s big banking houses 50 bn Euro”

(FAZ.NET, May 24th, 2014)

Regulatory requirements will increase costs and lower the possibility to gain sufficient returns on capital

“I am not sure whether all insurers will survive.”

(Felix Hufeld, BaFin (German federal financial supervisory agency), in ‘Der Tagespiegel’, November 28th, 2013)

Direct costs German banks are spending for the regulation increase from about 3.8 bn EUR (2010-2012) to about 4.8 bn EUR (2013-2015)

(Source: German Bundesbank, 2013)

“EU regulation costs billions - Solvency II costs for UK insurance companies alone augment to 2 bn GBP” (Source: The Economist, May 3rd, 2012)

“An analysis of Accenture shows that the majority of the European insurance companies faces higher costs due to Solvency II”

(Source: Accenture, December 7th, 2010)

© IDS GmbH – Analysis and Reporting Services

37

37

Conclusions Some personal remarks

To offset the rising cost of regulation and higher product complexity, financial institutions are increasingly looking for cost saving measures

Outsourcing/ offshoring

Strong trend towards outsourced managed services

This trend will continue as further regulatory requirements are to be expected

© IDS GmbH – Analysis and Reporting Services

38

38

Contact

Dr. Bernd Fischer

Managing Director

+49 69 2443 1 3118

IDS GmbH – Analysis and Reporting Services Koeniginstrasse 28 Bockenheimer Landstrasse 42–44

80802 Munich 60323 Frankfurt/Main

www.InvestmentDataServices.com