Embed Size (px)

Citation preview

Business and Consumer Banking

Discussion Pack

Mike Pratt Group Executive, Business & Consumer Banking

August/September 2003

BCB Discussion Pack – Aug/Sept 200322

Disclaimer

The material contained in this presentation is intended to be general background information on Westpac Banking Corporation and its activities.

The information is supplied in summary form and is therefore not necessarily complete. Also, it is not intended that it be relied upon as advice to investors or potential investors, who should consider seeking independent professional advice depending upon their specific investment objectives, financial situation or particular needs.

BCB Discussion Pack – Aug/Sept 200333

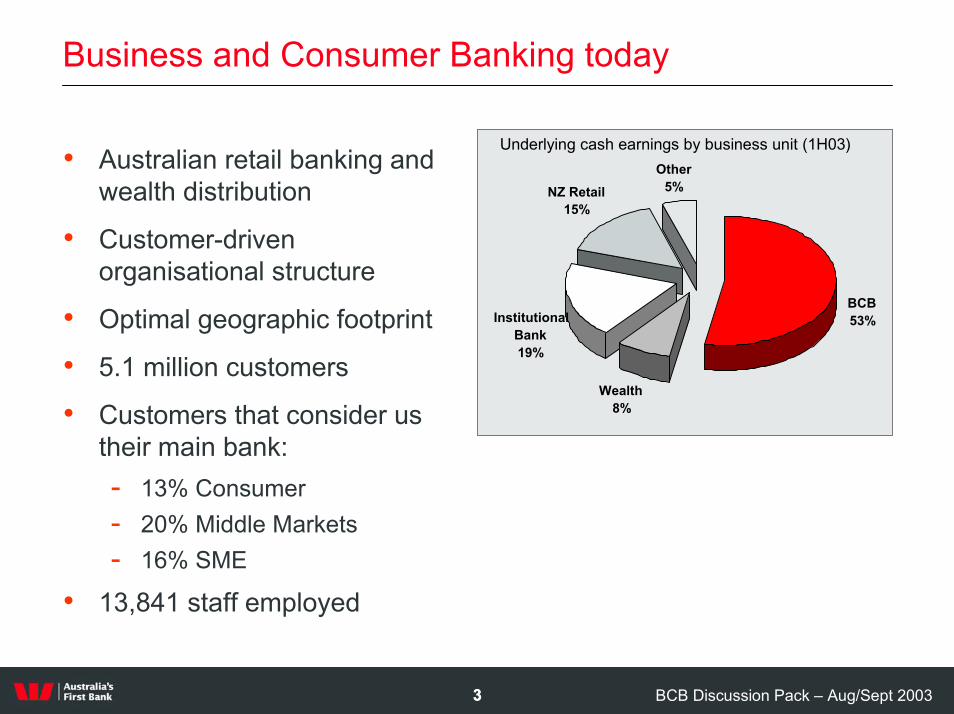

Business and Consumer Banking today

Underlying cash earnings by business unit (1H03)

BCB53%

Wealth8%

Institutional Bank19%

NZ Retail15%

Other5%

• Australian retail banking and wealth distribution

• Customer-driven organisational structure

• Optimal geographic footprint

• 5.1 million customers

• Customers that consider us their main bank:- 13% Consumer- 20% Middle Markets- 16% SME

• 13,841 staff employed

BCB Discussion Pack – Aug/Sept 200344

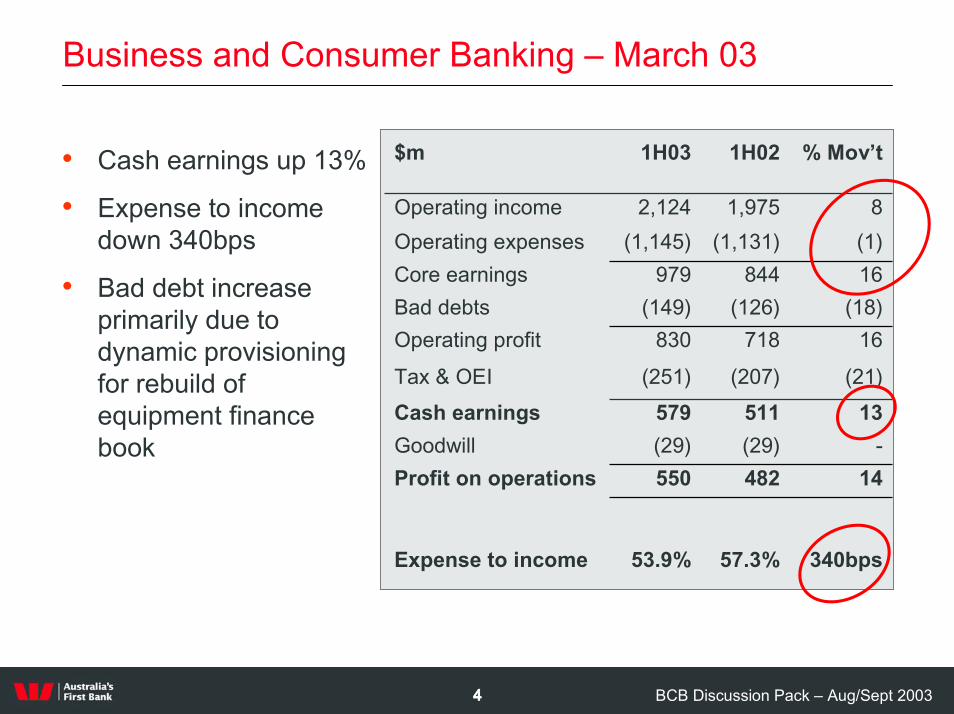

Business and Consumer Banking – March 03

14482550Profit on operations

(18)(126)(149)Bad debts

340bps57.3%53.9%Expense to income

(29)579

(251)

830

979(1,145)

2,124

1H03

-(29)Goodwill13511Cash earnings

(21)(207)Tax & OEI

16718Operating profit

16844Core earnings(1)(1,131)Operating expenses

81,975Operating income

% Mov’t1H02$m• Cash earnings up 13%

• Expense to income down 340bps

• Bad debt increase primarily due to dynamic provisioning for rebuild of equipment finance book

BCB Discussion Pack – Aug/Sept 200355

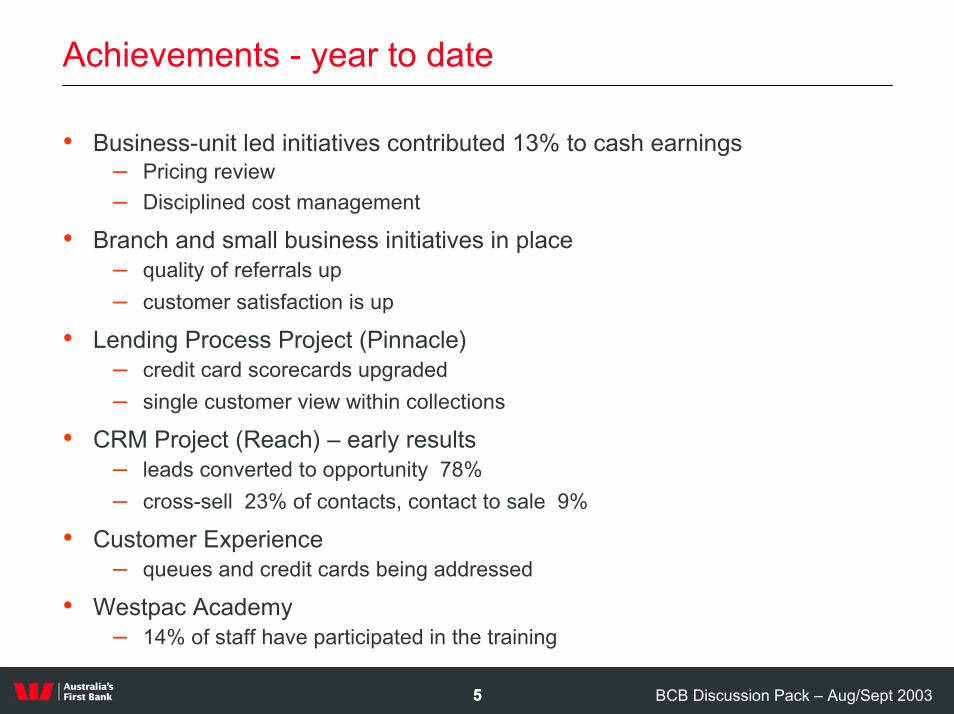

Achievements - year to date

• Business-unit led initiatives contributed 13% to cash earnings – Pricing review– Disciplined cost management

• Branch and small business initiatives in place – quality of referrals up – customer satisfaction is up

• Lending Process Project (Pinnacle)– credit card scorecards upgraded– single customer view within collections

• CRM Project (Reach) – early results– leads converted to opportunity 78%– cross-sell 23% of contacts, contact to sale 9%

• Customer Experience– queues and credit cards being addressed

• Westpac Academy– 14% of staff have participated in the training

BCB Discussion Pack – Aug/Sept 200366

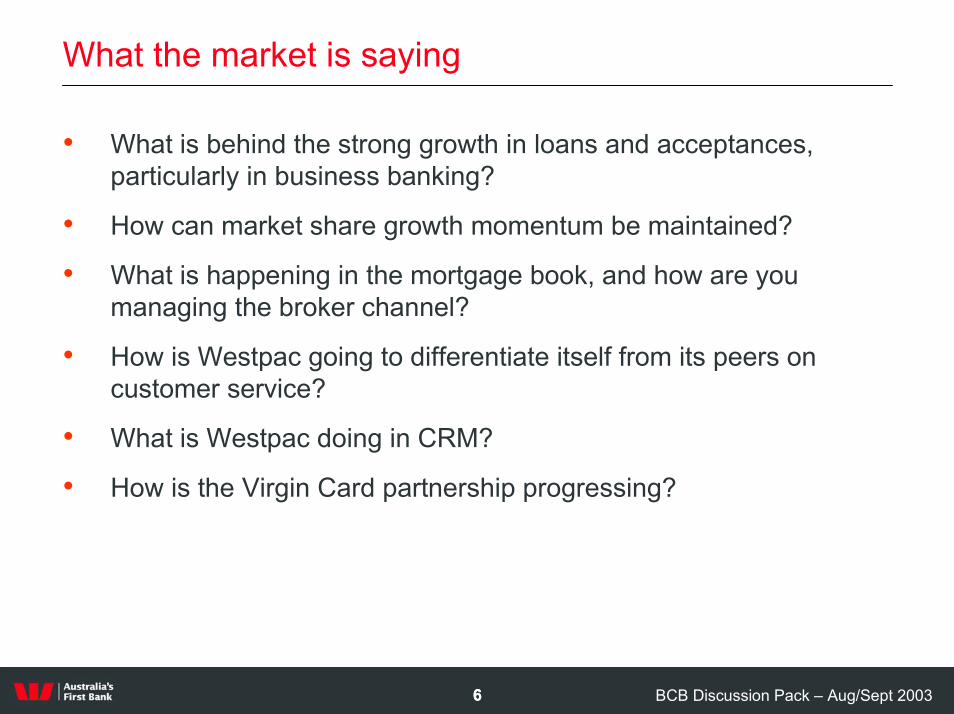

What the market is saying

• What is behind the strong growth in loans and acceptances, particularly in business banking?

• How can market share growth momentum be maintained?

• What is happening in the mortgage book, and how are you managing the broker channel?

• How is Westpac going to differentiate itself from its peers on customer service?

• What is Westpac doing in CRM?

• How is the Virgin Card partnership progressing?

BCB Discussion Pack – Aug/Sept 200377

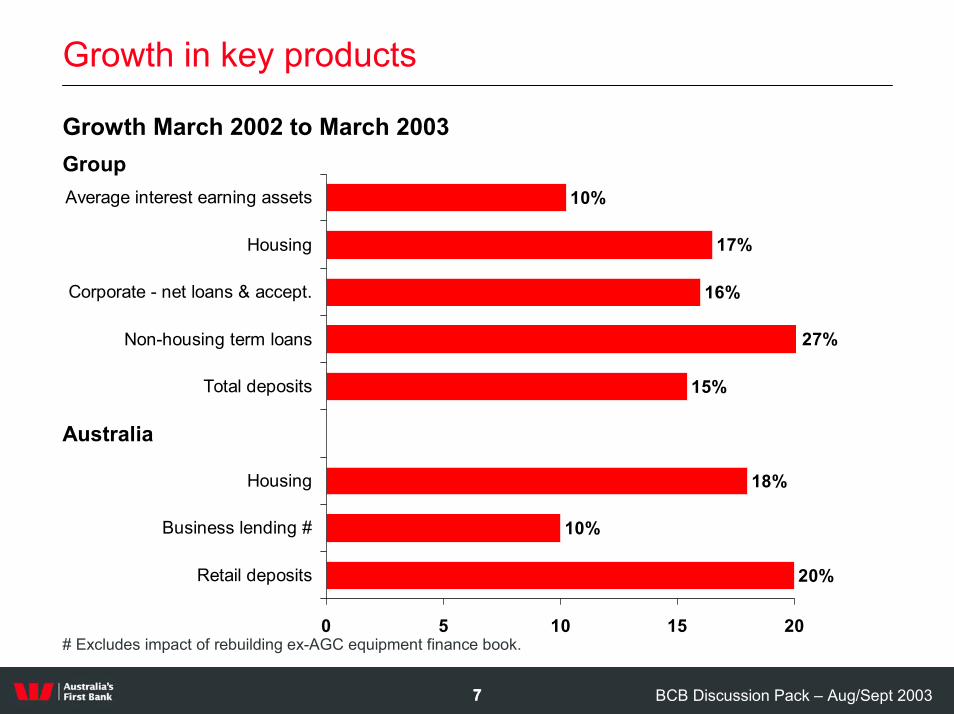

Growth in key products

Growth March 2002 to March 2003

27%

16%

17%

10%

18%

10%

20%

15%

0 5 10 15 20

Retail deposits

Business lending #

Housing

Total deposits

Non-housing term loans

Corporate - net loans & accept.

Housing

Average interest earning assets

Group

Australia

# Excludes impact of rebuilding ex-AGC equipment finance book.

BCB Discussion Pack – Aug/Sept 200388

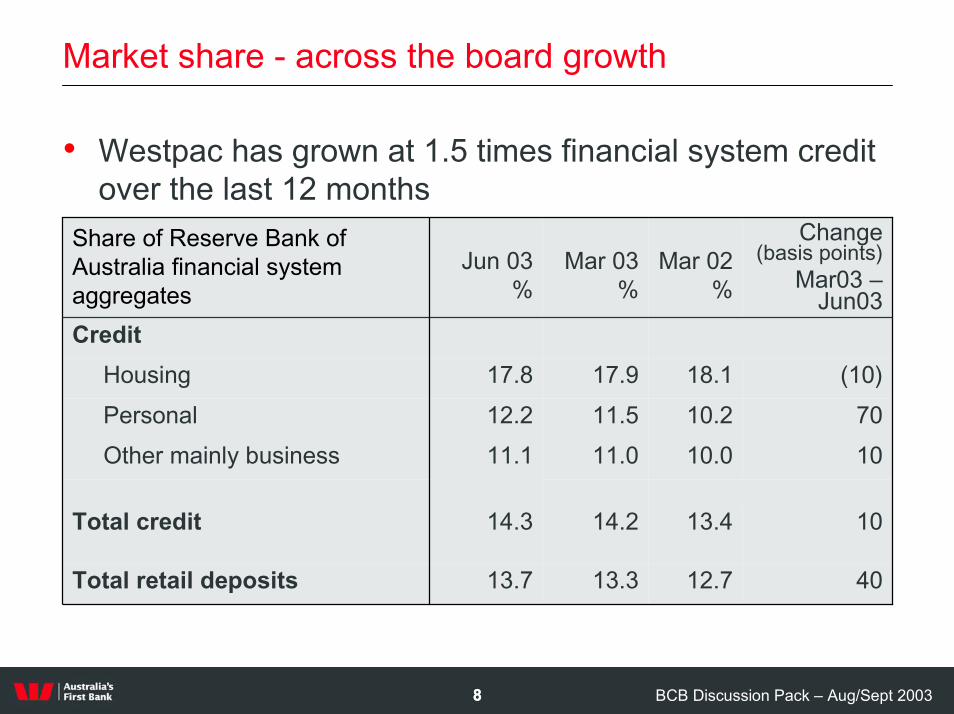

Market share - across the board growth

• Westpac has grown at 1.5 times financial system credit over the last 12 months

13.7

14.3

11.112.217.8

Jun 03%

Credit(10)18.117.9Housing

13.3

14.2

11.011.5

Mar 03%

4012.7Total retail deposits

1013.4Total credit

1010.0Other mainly business7010.2Personal

Change (basis points)

Mar03 –Jun03

Mar 02%

Share of Reserve Bank of Australia financial system aggregates

BCB Discussion Pack – Aug/Sept 200399

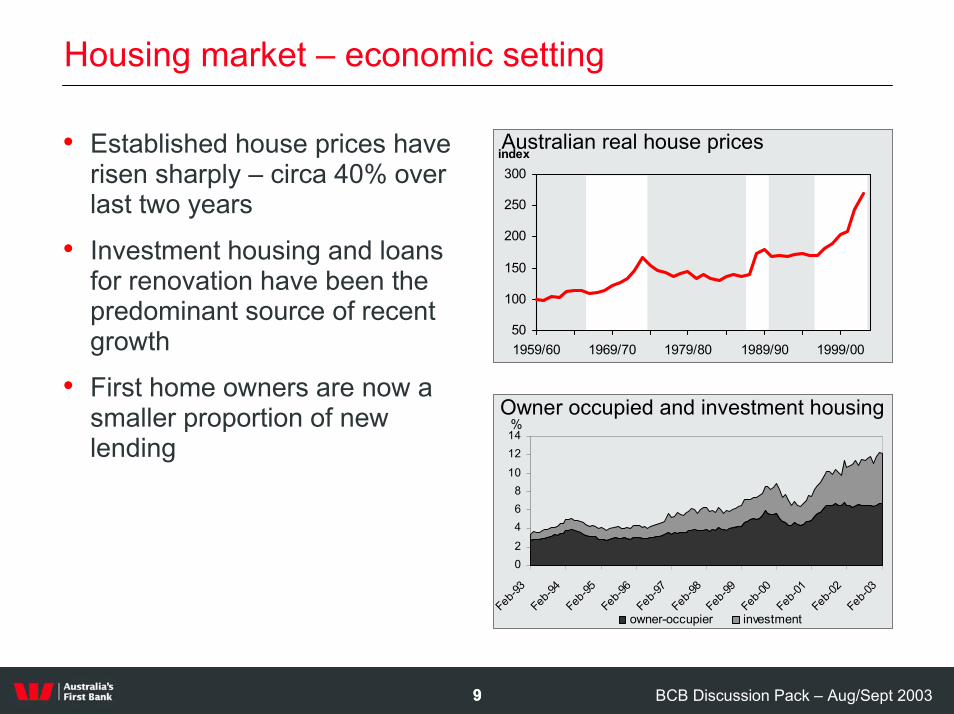

Housing market – economic setting

• Established house prices have risen sharply – circa 40% over last two years

• Investment housing and loans for renovation have been the predominant source of recent growth

• First home owners are now a smaller proportion of new lending

Australian real house prices

50

100

150

200

250

300

1959/60 1969/70 1979/80 1989/90 1999/00

index

Owner occupied and investment housing

02468

101214

Feb-93

Feb-94

Feb-95

Feb-96

Feb-9

7Feb-9

8Feb

-99Feb

-00Feb

-01Fe

b-02

Feb-0

3

owner-occupier investment

%

BCB Discussion Pack – Aug/Sept 20031010

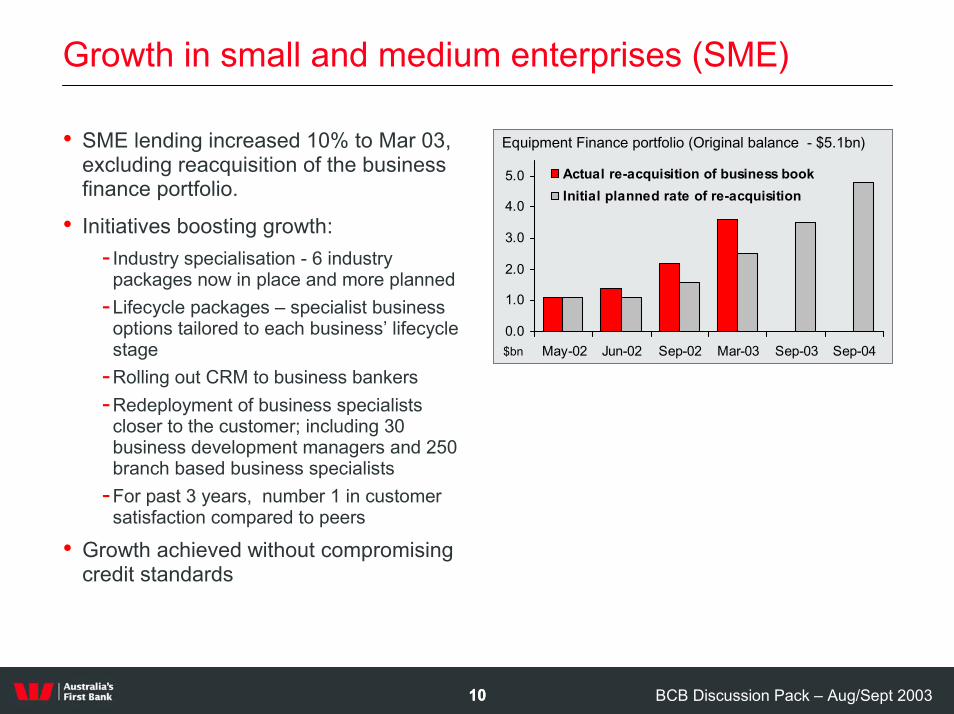

Growth in small and medium enterprises (SME)

• SME lending increased 10% to Mar 03, excluding reacquisition of the business finance portfolio.

• Initiatives boosting growth:- Industry specialisation - 6 industry

packages now in place and more planned-Lifecycle packages – specialist business

options tailored to each business’ lifecycle stage

-Rolling out CRM to business bankers-Redeployment of business specialists

closer to the customer; including 30 business development managers and 250 branch based business specialists

-For past 3 years, number 1 in customer satisfaction compared to peers

• Growth achieved without compromising credit standards

0.0

1.0

2.0

3.0

4.0

5.0

May-02 Jun-02 Sep-02 Mar-03 Sep-03 Sep-04

Actual re-acquisition of business bookInitial planned rate of re-acquisition

Equipment Finance portfolio (Original balance - $5.1bn)

$bn

BCB Discussion Pack – Aug/Sept 20031111

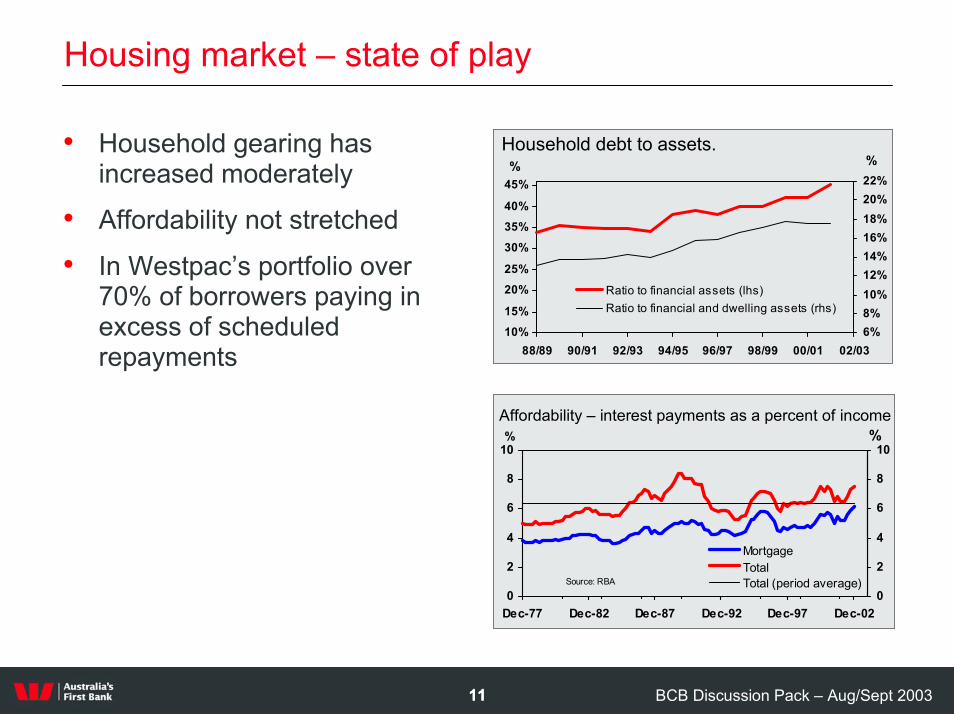

Housing market – state of play

• Household gearing has increased moderately

• Affordability not stretched

• In Westpac’s portfolio over 70% of borrowers paying in excess of scheduled repayments

Household debt to assets.

10%15%

20%25%

30%35%40%

45%

88/89 90/91 92/93 94/95 96/97 98/99 00/01 02/03

%

6%8%10%12%14%16%18%20%22%%

Ratio to financial assets (lhs)Ratio to financial and dwelling assets (rhs)

Affordability – interest payments as a percent of income

0

2

4

6

8

10

Dec-77 Dec-82 Dec-87 Dec-92 Dec-97 Dec-02

%

0

2

4

6

8

10%

MortgageTotal Total (period average)Source: RBA

BCB Discussion Pack – Aug/Sept 20031212

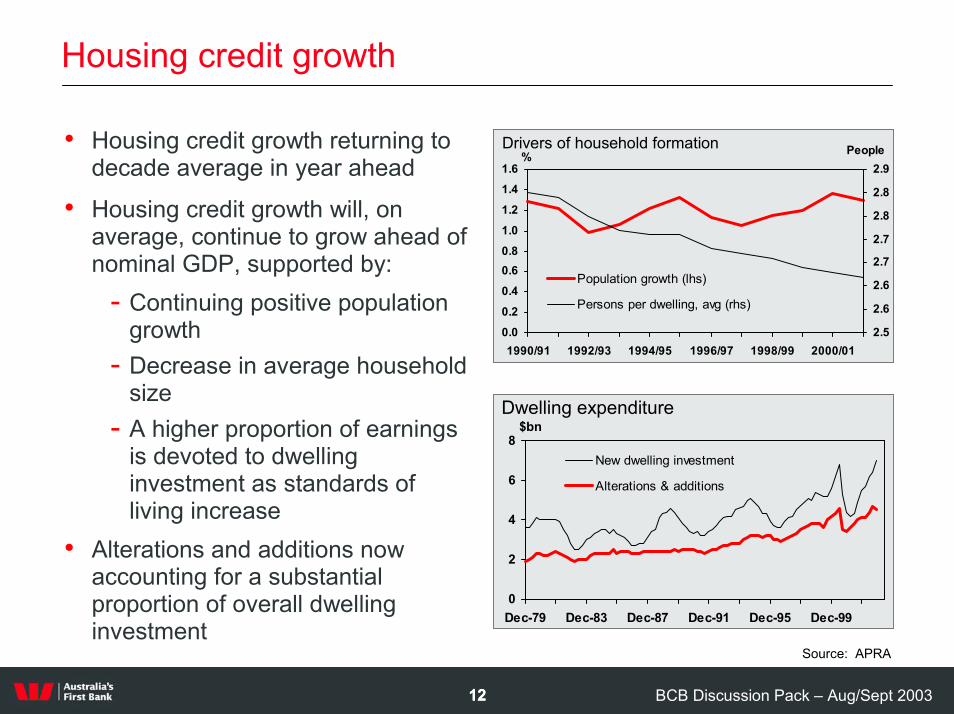

Housing credit growth

• Housing credit growth returning to decade average in year ahead

• Housing credit growth will, on average, continue to grow ahead of nominal GDP, supported by:

- Continuing positive population growth

- Decrease in average household size

- A higher proportion of earnings is devoted to dwelling investment as standards of living increase

• Alterations and additions now accounting for a substantial proportion of overall dwelling investment

0.00.20.40.60.81.01.21.41.6

1990/91 1992/93 1994/95 1996/97 1998/99 2000/01

%

2.5

2.6

2.6

2.7

2.7

2.8

2.8

2.9People

Population growth (lhs)

Persons per dwelling, avg (rhs)

Drivers of household formation

0

2

4

6

8

Dec-79 Dec-83 Dec-87 Dec-91 Dec-95 Dec-99

$bn

New dwelling investment

Alterations & additions

Dwelling expenditure

Source: APRA

BCB Discussion Pack – Aug/Sept 20031313

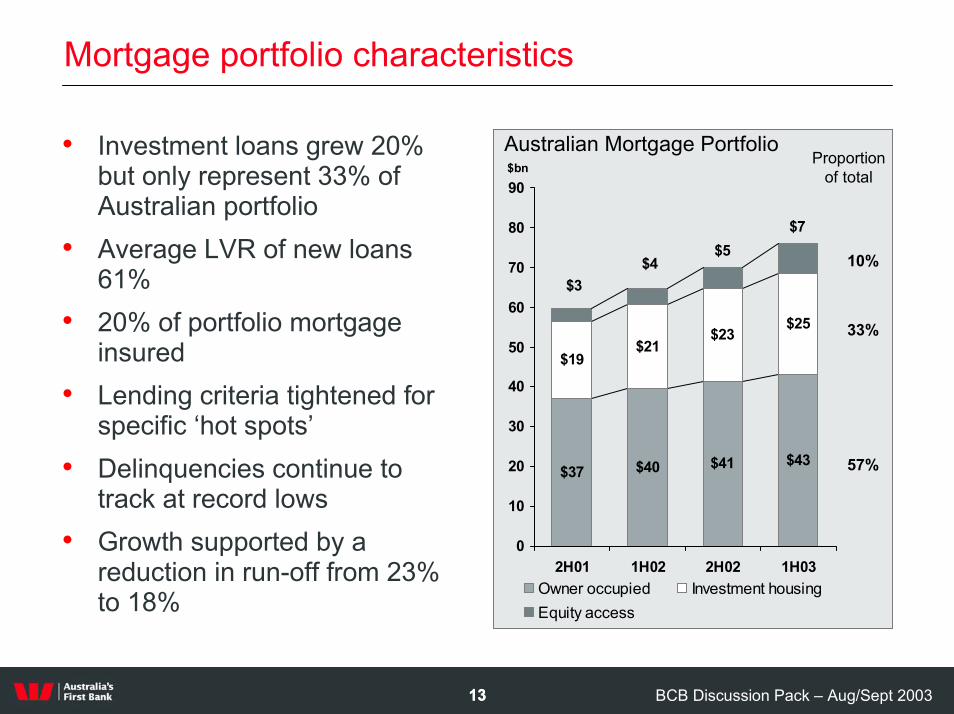

Mortgage portfolio characteristics

• Investment loans grew 20% but only represent 33% of Australian portfolio

• Average LVR of new loans 61%

• 20% of portfolio mortgage insured

• Lending criteria tightened for specific ‘hot spots’

• Delinquencies continue to track at record lows

• Growth supported by a reduction in run-off from 23% to 18%

$37 $40 $41 $43

$19$21

$23$25

$7$5

$4$3

0

10

20

30

40

50

60

70

80

90

2H01 1H02 2H02 1H03

$bn

Owner occupied Investment housingEquity access

Australian Mortgage Portfolio

10%

33%

57%

Proportion of total

BCB Discussion Pack – Aug/Sept 20031414

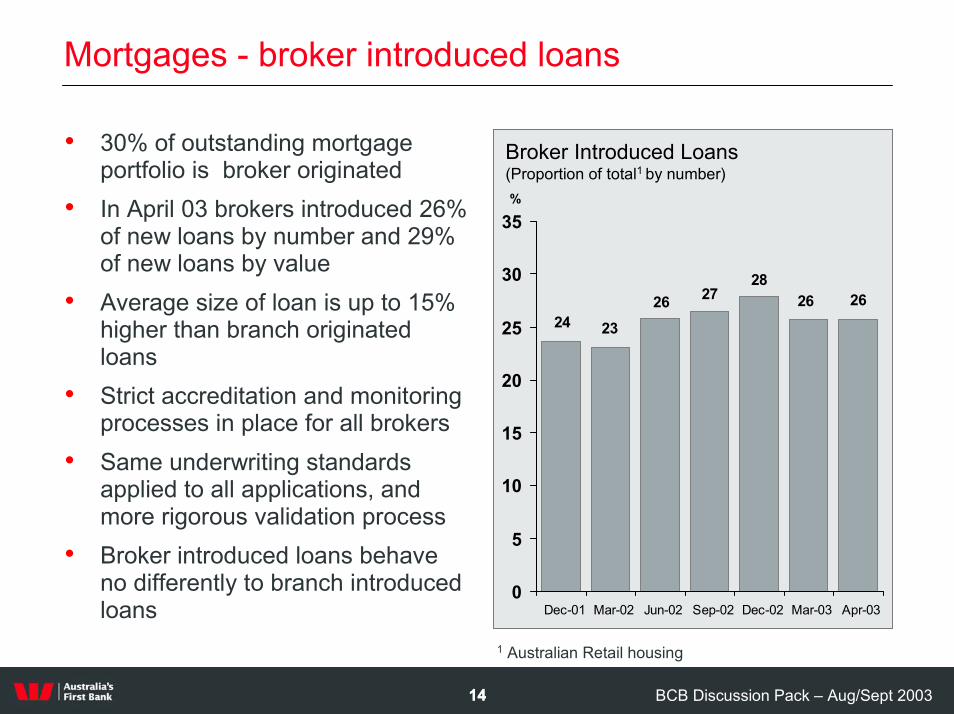

Mortgages - broker introduced loans

• 30% of outstanding mortgage portfolio is broker originated

• In April 03 brokers introduced 26% of new loans by number and 29% of new loans by value

• Average size of loan is up to 15% higher than branch originated loans

• Strict accreditation and monitoring processes in place for all brokers

• Same underwriting standards applied to all applications, and more rigorous validation process

• Broker introduced loans behave no differently to branch introduced loans

262628

27262324

0

5

10

15

20

25

30

35

Dec-01 Mar-02 Jun-02 Sep-02 Dec-02 Mar-03 Apr-03

%

Broker Introduced Loans(Proportion of total1 by number)

1 Australian Retail housing

BCB Discussion Pack – Aug/Sept 20031515

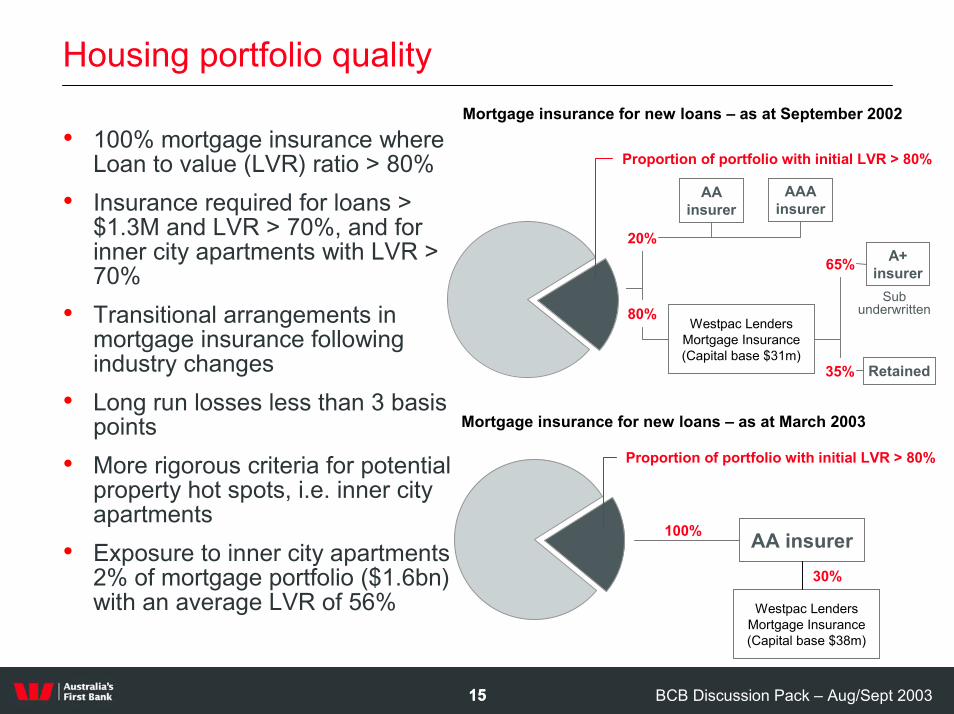

Housing portfolio quality

• 100% mortgage insurance where Loan to value (LVR) ratio > 80%

• Insurance required for loans > $1.3M and LVR > 70%, and for inner city apartments with LVR > 70%

• Transitional arrangements in mortgage insurance following industry changes

• Long run losses less than 3 basis points

• More rigorous criteria for potential property hot spots, i.e. inner city apartments

• Exposure to inner city apartments 2% of mortgage portfolio ($1.6bn) with an average LVR of 56%

20%

Mortgage insurance for new loans – as at September 2002

Proportion of portfolio with initial LVR > 80%

80%Westpac Lenders

Mortgage Insurance (Capital base $31m)

A+ insurer65%

Sub underwritten

20%

AA insurer

AAAinsurer

Retained35%

20%

Proportion of portfolio with initial LVR > 80%

AA insurer

Mortgage insurance for new loans – as at March 2003

100%

Westpac Lenders Mortgage Insurance (Capital base $38m)

30%

BCB Discussion Pack – Aug/Sept 20031616

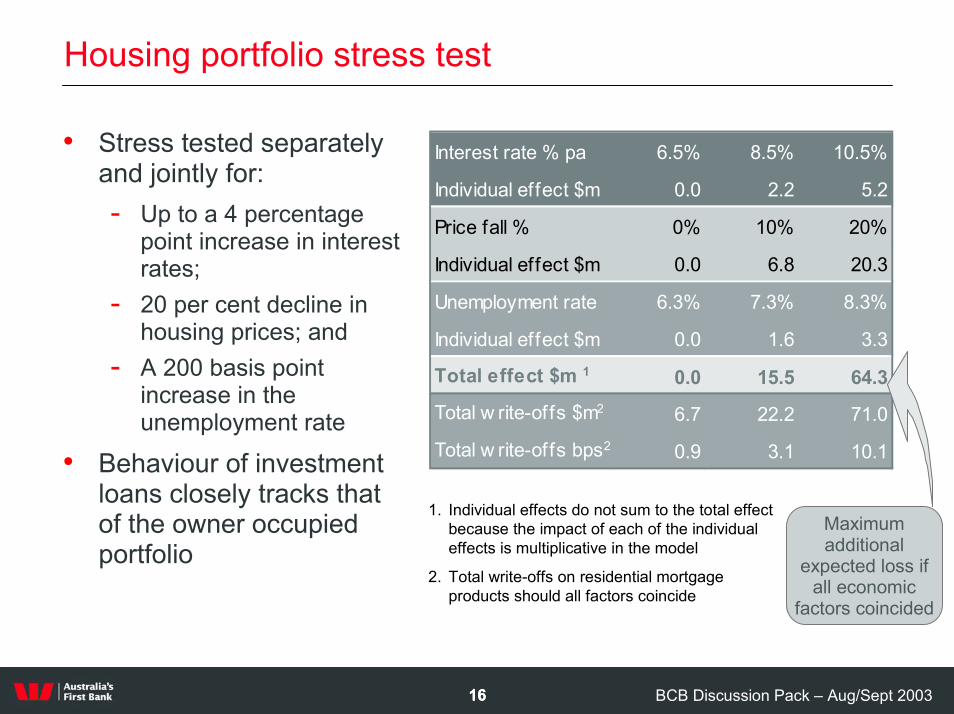

Housing portfolio stress test

Interest rate % pa 6.5% 8.5% 10.5%

Individual effect $m 0.0 2.2 5.2

Price fall % 0% 10% 20%

Individual effect $m 0.0 6.8 20.3

Unemployment rate 6.3% 7.3% 8.3%

Individual effect $m 0.0 1.6 3.3

Total effect $m 1 0.0 15.5 64.3

Total w rite-offs $m2 6.7 22.2 71.0

Total w rite-offs bps2 0.9 3.1 10.1

1. Individual effects do not sum to the total effect because the impact of each of the individual effects is multiplicative in the model

2. Total write-offs on residential mortgage products should all factors coincide

Maximum additional

expected loss if all economic

factors coincided

• Stress tested separately and jointly for:- Up to a 4 percentage

point increase in interest rates;

- 20 per cent decline in housing prices; and

- A 200 basis point increase in the unemployment rate

• Behaviour of investment loans closely tracks that of the owner occupied portfolio

BCB Discussion Pack – Aug/Sept 20031717

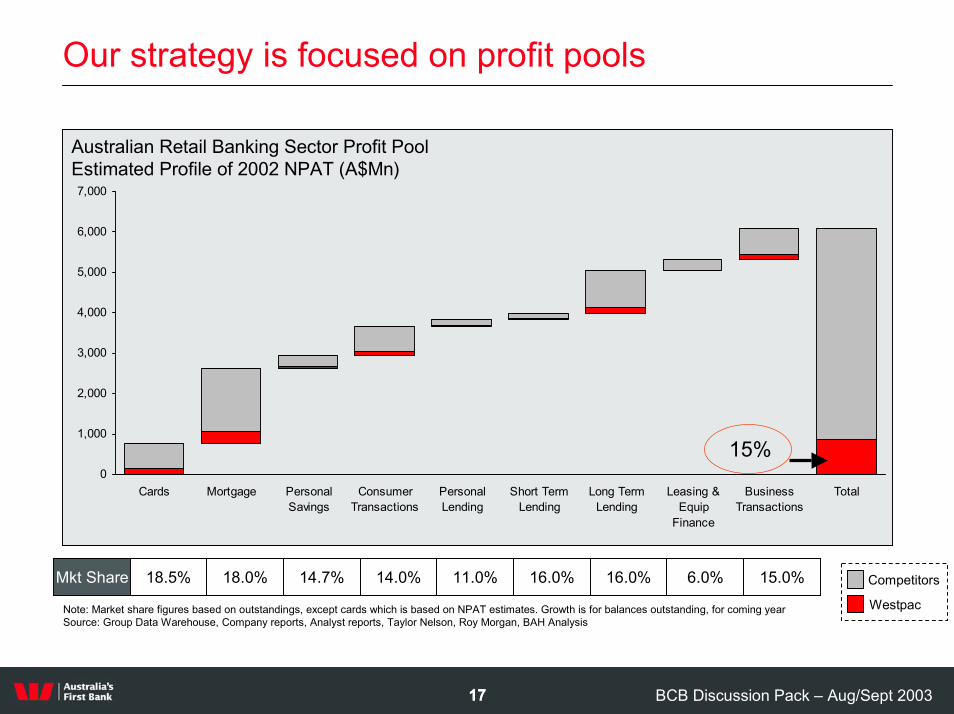

Our strategy is focused on profit pools

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Cards Mortgage PersonalSavings

ConsumerTransactions

PersonalLending

Short TermLending

Long TermLending

Leasing &Equip

Finance

BusinessTransactions

Total

Australian Retail Banking Sector Profit Pool Estimated Profile of 2002 NPAT (A$Mn)

15%

Mkt Share Competitors

Westpac

18.5% 18.0% 14.7% 14.0% 11.0% 16.0% 16.0% 6.0% 15.0%

Note: Market share figures based on outstandings, except cards which is based on NPAT estimates. Growth is for balances outstanding, for coming yearSource: Group Data Warehouse, Company reports, Analyst reports, Taylor Nelson, Roy Morgan, BAH Analysis

BCB Discussion Pack – Aug/Sept 20031818

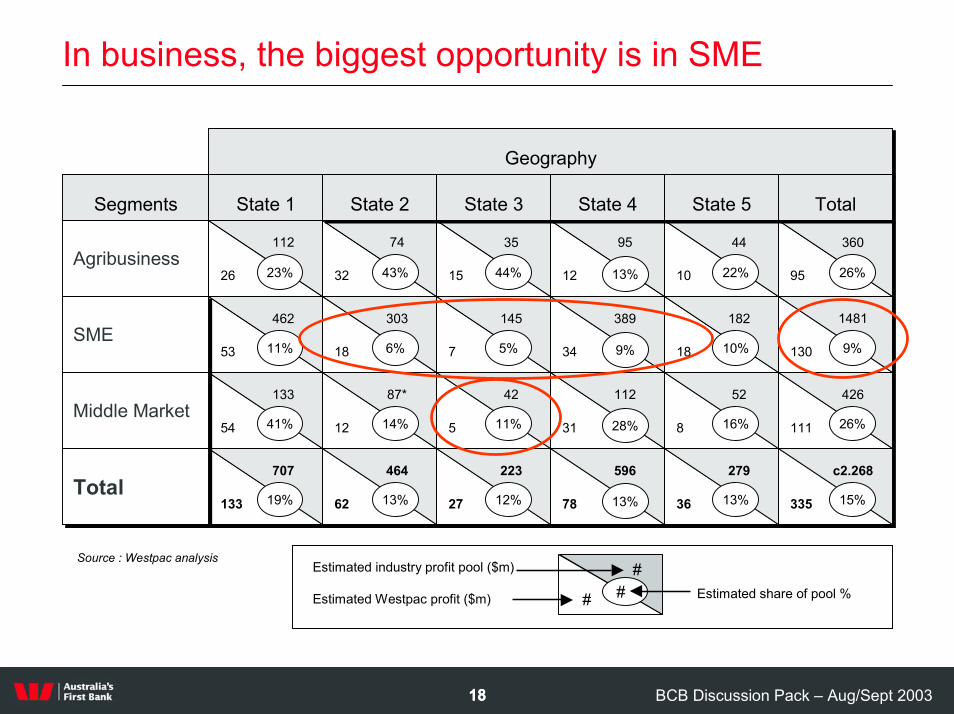

In business, the biggest opportunity is in SME

Geography

SegmentsSegments

Geography

State 1State 1

AgribusinessAgribusiness26

112

32

74

15

35

53

462

18

303

7

145

54

133

12

87*

5

42

12

95

10

44

34

389

18

182

31

112

8

52

95

360

130

1481

111

426

133

707

62

464

27

223

78

596

36

279

335

c2.268

23% 43% 44% 22% 26%

11% 6% 5% 10% 9%

41% 14% 11% 16% 26%

19% 13% 12% 13% 15%

13%

9%

28%

13%

State 2State 2 State 3State 3

SMESME

Middle MarketMiddle Market

State 4State 4 State 5State 5 TotalTotal

TotalTotal

Estimated industry profit pool ($m)

Estimated Westpac profit ($m) Estimated share of pool %##

#Source : Westpac analysis

BCB Discussion Pack – Aug/Sept 20031919

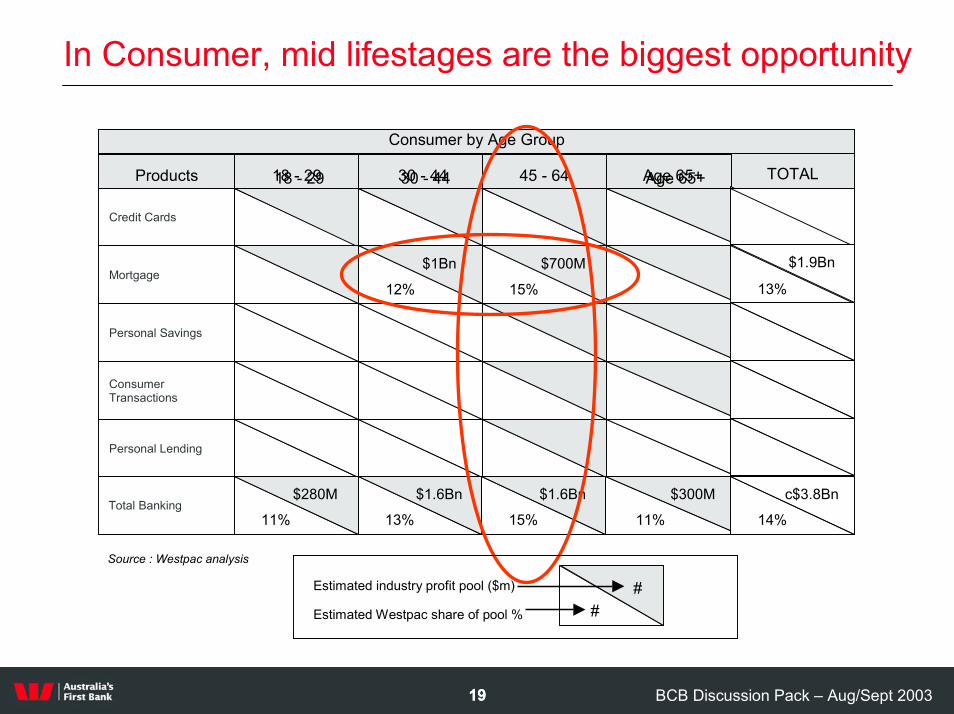

In Consumer, mid lifestages are the biggest opportunity

Products 45 - 64 45 - 64

12%

$1Bn

15%

$700M

13%

$1.6Bn

15%

$1.6Bn

Consumer by Age Group

Estimated industry profit pool ($m)

Estimated Westpac share of pool % ##

Source : Westpac analysis

TOTALProducts 18 - 29 18 - 29

Credit Cards

Mortgage

Personal Savings

Consumer Transactions

Personal Lending

30 - 44 30 - 44 Age 65+ Age 65+

$1.9Bn

13%

$280M $300M c$3.8BnTotal Banking

11% 11% 14%

BCB Discussion Pack – Aug/Sept 20032020

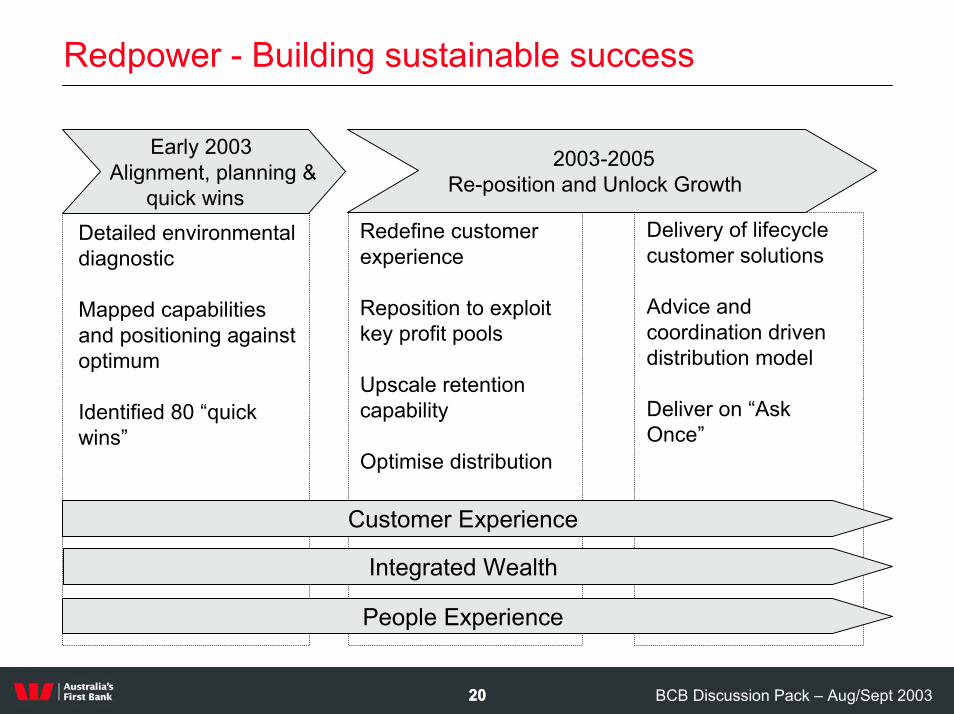

Redpower - Building sustainable success

Integrated Wealth

2003-2005Re-position and Unlock Growth

People Experience

Customer Experience

Detailed environmental diagnostic

Mapped capabilities and positioning against optimum

Identified 80 “quick wins”

Redefine customer experience

Reposition to exploit key profit pools

Upscale retention capability

Optimise distribution

Delivery of lifecycle customer solutions

Advice and coordination driven distribution model

Deliver on “Ask Once”

Early 2003Alignment, planning &

quick wins

BCB Discussion Pack – Aug/Sept 20032121

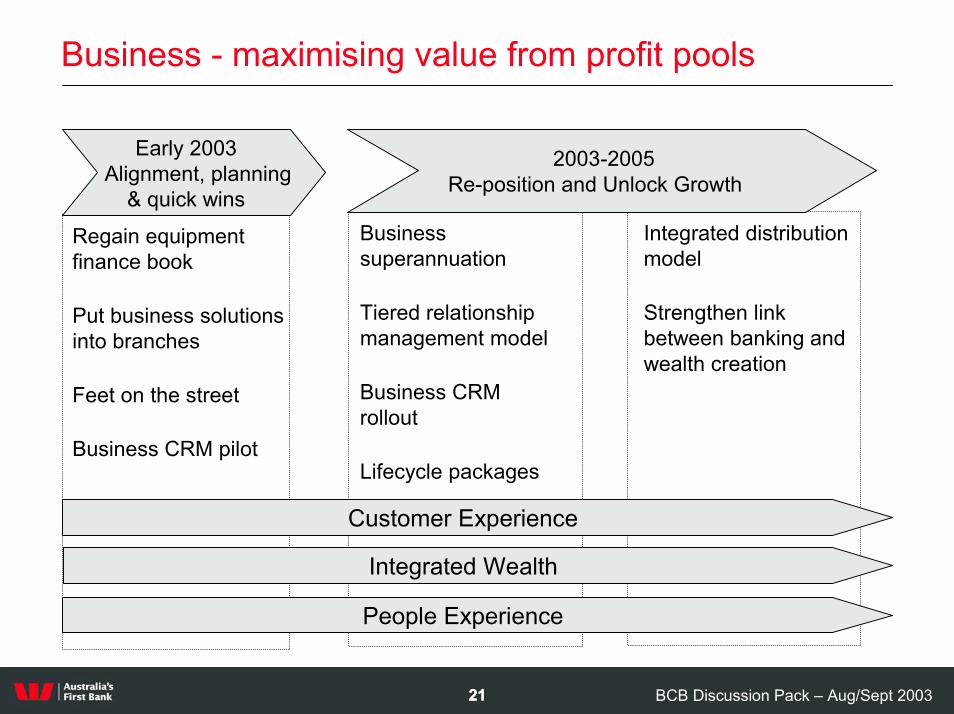

Business - maximising value from profit pools

Integrated Wealth

People Experience

Customer Experience

Regain equipment finance book

Put business solutions into branches

Feet on the street

Business CRM pilot

Business superannuation

Tiered relationship management model

Business CRM rollout

Lifecycle packages

Integrated distribution model

Strengthen link between banking and wealth creation

Early 2003Alignment, planning

& quick wins

2003-2005Re-position and Unlock Growth

BCB Discussion Pack – Aug/Sept 20032222

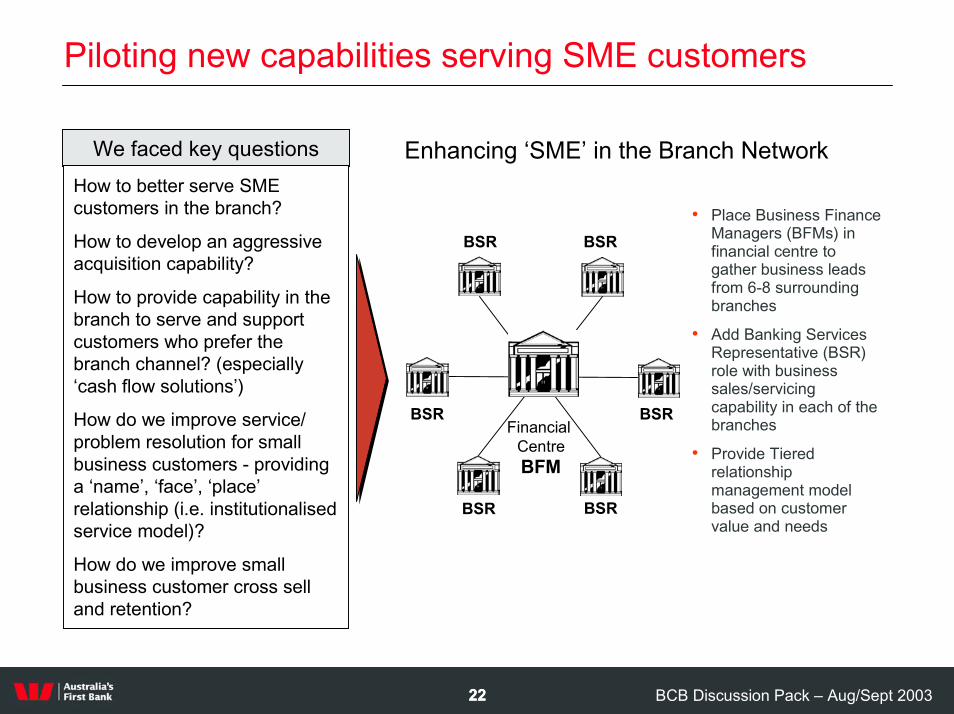

Piloting new capabilities serving SME customers

Enhancing ‘SME’ in the Branch NetworkWe faced key questionsHow to better serve SME customers in the branch?

How to develop an aggressive acquisition capability?

How to provide capability in the branch to serve and support customers who prefer the branch channel? (especially ‘cash flow solutions’)

How do we improve service/ problem resolution for small business customers - providing a ‘name’, ‘face’, ‘place’ relationship (i.e. institutionalised service model)?

How do we improve small business customer cross sell and retention?

• Place Business Finance Managers (BFMs) in financial centre to gather business leads from 6-8 surrounding branches

• Add Banking Services Representative (BSR) role with business sales/servicing capability in each of the branches

• Provide Tiered relationship management model based on customer value and needs

BSR

BSRBSR

Financial CentreBFM

BSR

BSRBSR

BCB Discussion Pack – Aug/Sept 20032323

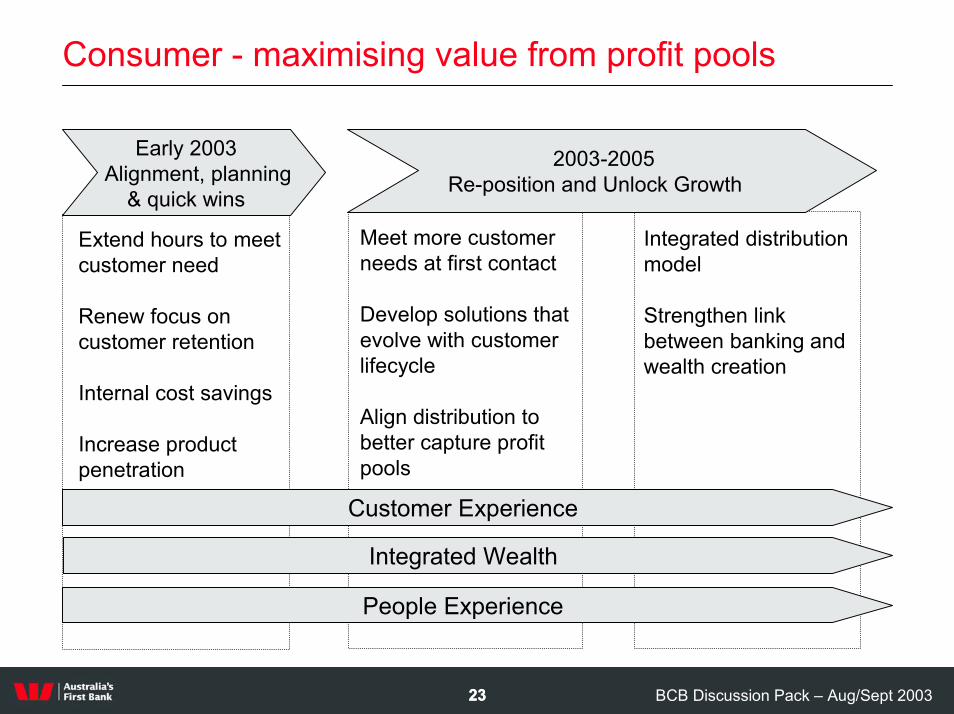

Consumer - maximising value from profit pools

Integrated Wealth

People Experience

Customer Experience

Extend hours to meet customer need

Renew focus on customer retention

Internal cost savings

Increase product penetration

Meet more customer needs at first contact

Develop solutions that evolve with customer lifecycle

Align distribution to better capture profit pools

Integrated distribution model

Strengthen link between banking and wealth creation

Early 2003Alignment, planning

& quick wins

2003-2005Re-position and Unlock Growth

BCB Discussion Pack – Aug/Sept 20032424

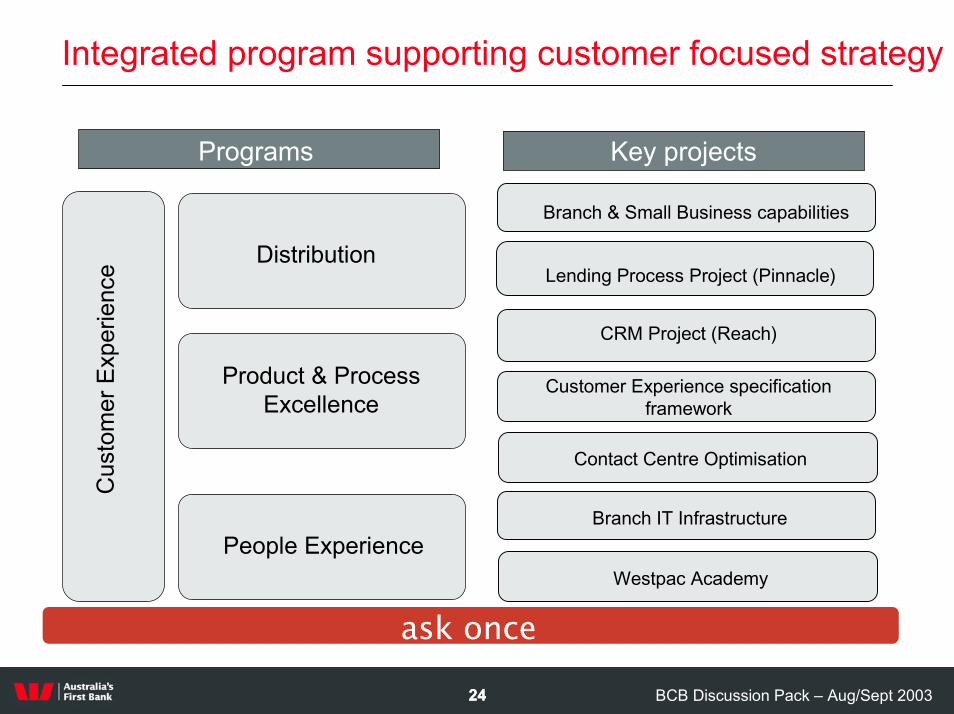

Integrated program supporting customer focused strategy

Programs Key projects

Branch & Small Business capabilities

Distribution

Product & Process Excellence

tom

er E

x pe

Lending Process Project (Pinnacle)

Cus

rienc

e

CRM Project (Reach)

Customer Experience specification framework

Contact Centre Optimisation

Branch IT InfrastructurePeople Experience

Westpac Academy

ask once

BCB Discussion Pack – Aug/Sept 20032525

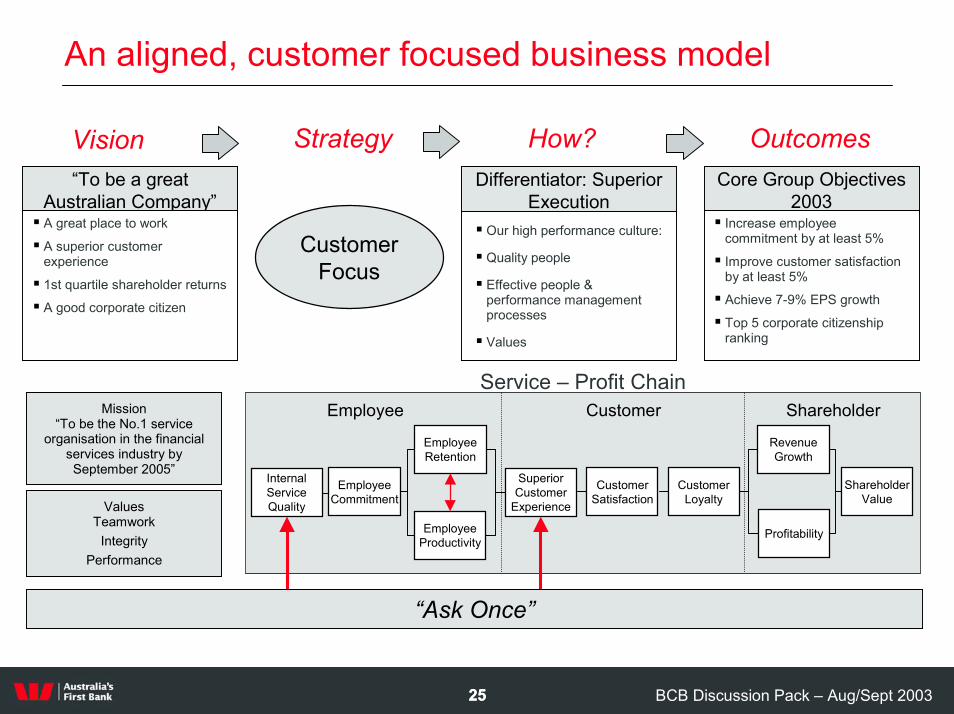

An aligned, customer focused business model

Strategy How? OutcomesVisionDifferentiator: Superior

Execution� Our high performance culture:

� Quality people

� Effective people & performance management processes

� Values

Core Group Objectives 2003

� Increase employee commitment by at least 5%

� Improve customer satisfaction by at least 5%

� Achieve 7-9% EPS growth

� Top 5 corporate citizenship ranking

“To be a great Australian Company”

� A great place to work

� A superior customer experience

� 1st quartile shareholder returns

� A good corporate citizen

Customer Focus

Service – Profit Chain

Internal Service Quality

Employee Commitment

Employee Retention

Employee Productivity

Superior Customer

Experience

Customer Satisfaction

Customer Loyalty

Revenue Growth

Profitability

Shareholder Value

Employee Customer ShareholderMission“To be the No.1 service

organisation in the financial services industry by September 2005”

ValuesTeamwork

IntegrityPerformance

“Ask Once”

BCB Discussion Pack – Aug/Sept 20032626

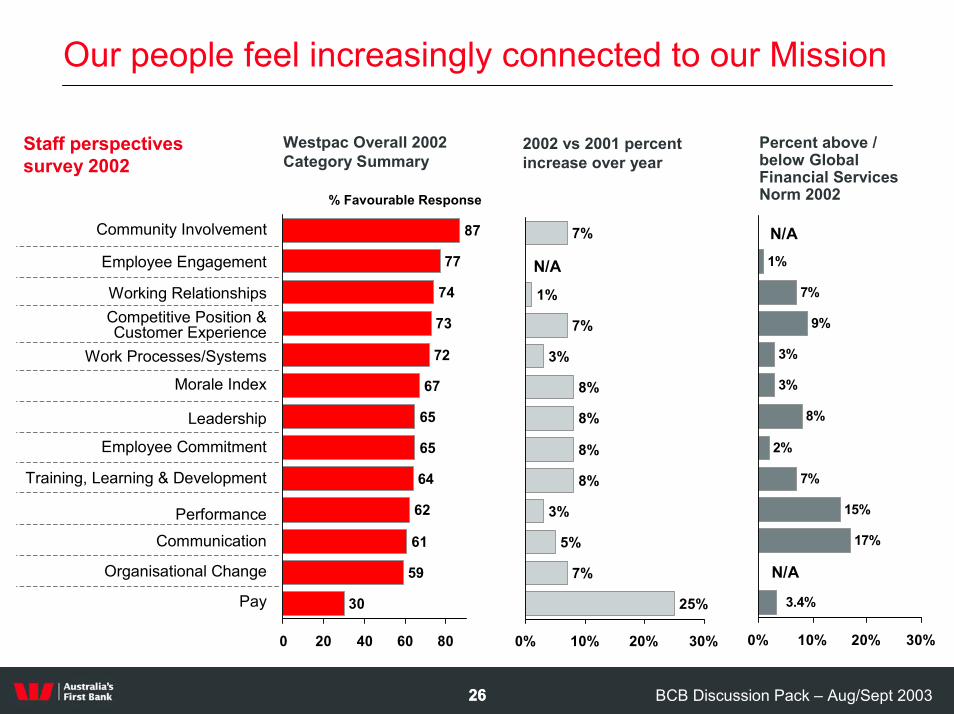

Our people feel increasingly connected to our Mission

Staff perspectives survey 2002

Westpac Overall 2002 Category Summary

2002 vs 2001 percent increase over year

Percent above / below Global Financial Services Norm 2002

1%

7%

9%

3%

3%

8%

2%

7%

15%

17%

3.4%

0% 10% 20% 30%

N/A

N/A

7%

1%

7%

3%

8%

8%

8%

8%

3%

5%

7%

25%

0% 10% 20% 30%

N/A

87

77

74

73

72

67

65

65

64

62

61

59

30

0 20 40 60 80

Employee Engagement

Working RelationshipsCompetitive Position & Customer Experience

Work Processes/Systems

Leadership

Employee Commitment

Training, Learning & Development

Communication

Organisational Change

Performance

Pay

Morale Index

Community Involvement

% Favourable Response

BCB Discussion Pack – Aug/Sept 20032727

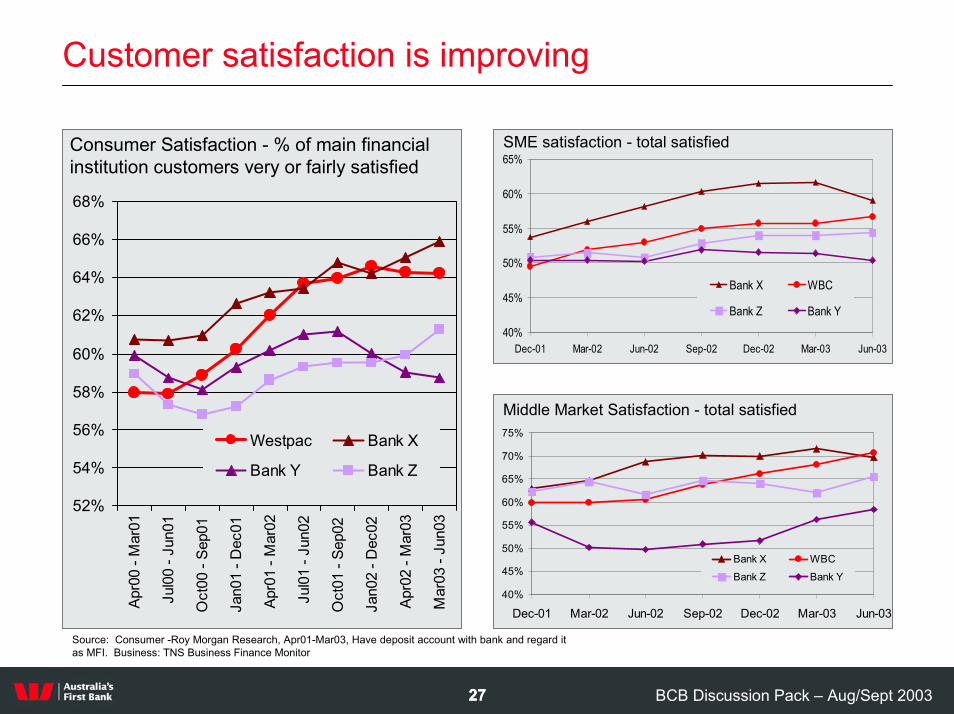

Customer satisfaction is improving

Consumer Satisfaction - % of main financial institution customers very or fairly satisfied

52%

54%

56%

58%

60%

62%

64%

66%

68%

Apr0

0 - M

ar01

Jul0

0 - J

un01

Oct

00 -

Sep0

1

Jan0

1 - D

ec01

Apr0

1 - M

ar02

Jul0

1 - J

un02

Oct

01 -

Sep0

2

Jan0

2 - D

ec02

Apr0

2 - M

ar03

Mar

03 -

Jun0

3Westpac Bank X

Bank Y Bank Z

SME satisfaction - total satisfied

40%

45%

50%

55%

60%

65%

Dec-01 Mar-02 Jun-02 Sep-02 Dec-02 Mar-03 Jun-03

Bank X WBC

Bank Z Bank Y

Middle Market Satisfaction - total satisfied

40%

45%

50%

55%

60%

65%

70%

75%

Dec-01 Mar-02 Jun-02 Sep-02 Dec-02 Mar-03 Jun-03

Bank X WBCBank Z Bank Y

Source: Consumer -Roy Morgan Research, Apr01-Mar03, Have deposit account with bank and regard it as MFI. Business: TNS Business Finance Monitor

BCB Discussion Pack – Aug/Sept 20032828

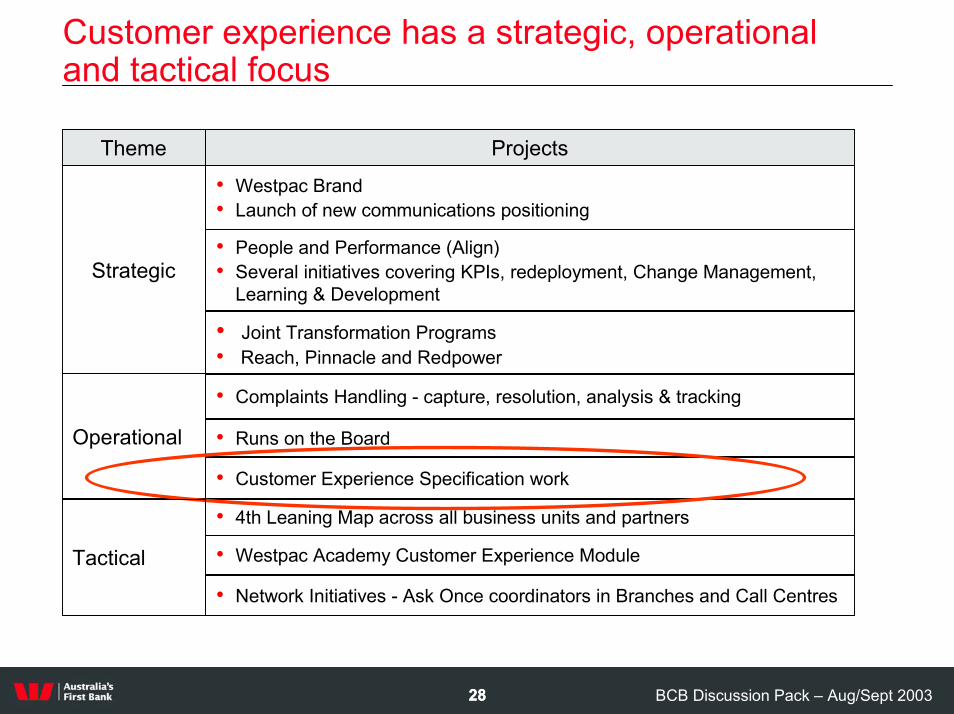

Customer experience has a strategic, operational and tactical focus

Strategic

• Westpac Brand• Launch of new communications positioning

• People and Performance (Align)• Several initiatives covering KPIs, redeployment, Change Management,

Learning & Development

• Joint Transformation Programs• Reach, Pinnacle and Redpower

• Complaints Handling - capture, resolution, analysis & tracking

• Runs on the Board

• Customer Experience Specification work

• 4th Leaning Map across all business units and partners

Theme Projects

Operational

• Westpac Academy Customer Experience Module Tactical

• Network Initiatives - Ask Once coordinators in Branches and Call Centres

BCB Discussion Pack – Aug/Sept 20032929

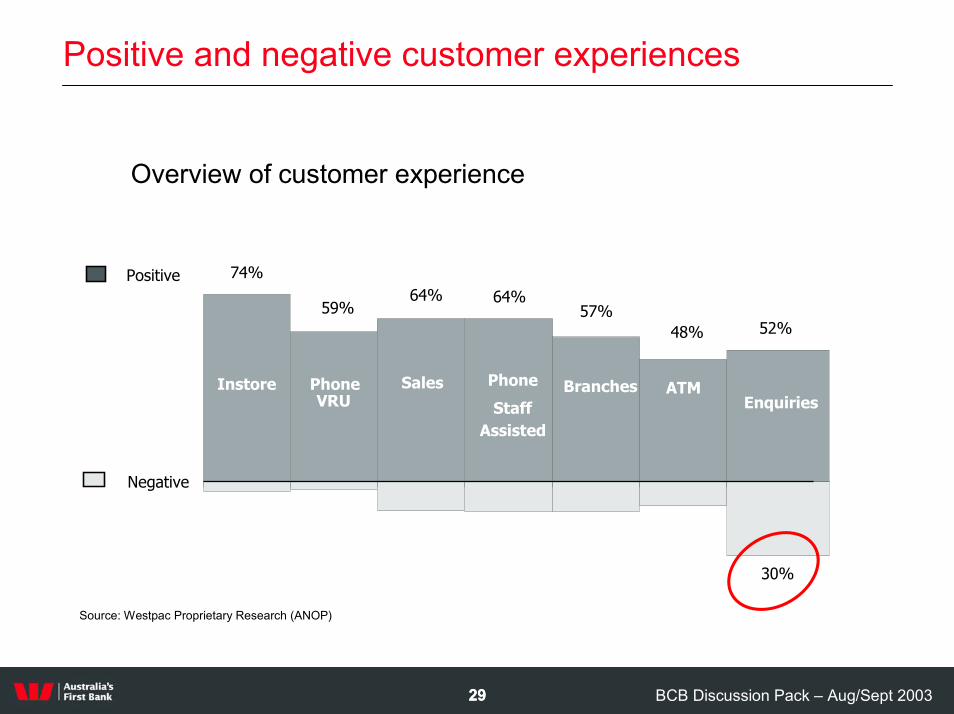

Positive and negative customer experiences

Overview of customer experience

30%

Instore PhoneVRU

Sales Phone

StaffAssisted

Branches ATMEnquiries

Positive 74%64% 64%

59% 57%52%48%

Negative

Source: Westpac Proprietary Research (ANOP)

BCB Discussion Pack – Aug/Sept 20033030

A disciplined approach identifying customer experience improvements

Complaints

count per month

1

2

3

Problem?

+

How Happy?

Size of Prize $ ?

Complaint Incidence

Rate

Current Customers Satisfaction

levels# Customer Interactions

count per month

4 5Prioritisation Framework && Profit pool

data

BCB Discussion Pack – Aug/Sept 20033131

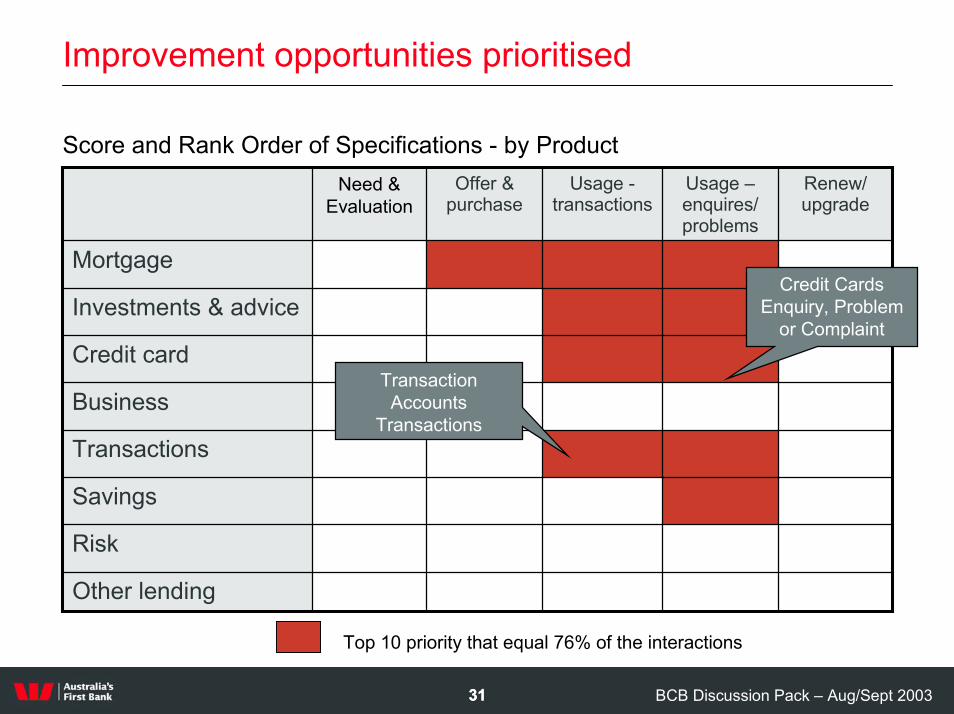

Improvement opportunities prioritised

Score and Rank Order of Specifications - by Product

Other lending

Risk

Savings

Transactions

Business

Credit card

Investments & advice

Mortgage

Renew/ upgrade

Usage –enquires/ problems

Usage -transactions

Offer & purchase

Need & Evaluation

Transaction Accounts

Transactions

Credit CardsEnquiry, Problem

or Complaint

Top 10 priority that equal 76% of the interactions

BCB Discussion Pack – Aug/Sept 20033232

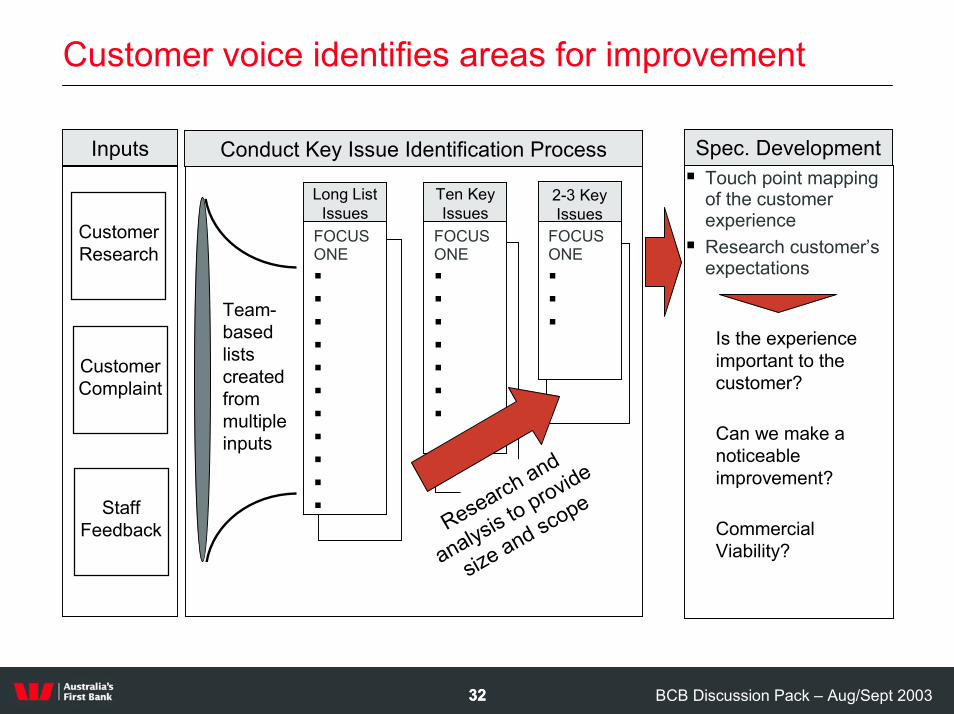

Customer voice identifies areas for improvement

Spec. DevelopmentInputs Conduct Key Issue Identification Process

Long List Issues

Team-based lists created from multiple inputs

••••••••••

Ten Key Issues

FOCUS ONE�

�

�

�

�

�

�

2-3 Key Issues

FOCUS ONE�

�

�

FOCUS ONE�

�

�

�

�

�

�

�

�

�

�

Research and

analysis to provide

size and scope

� Touch point mapping of the customer experience

� Research customer’s expectations

Can we make a noticeable improvement?

Is the experience important to the customer?

Commercial Viability?

Staff Feedback

Customer Complaint

Customer Research

BCB Discussion Pack – Aug/Sept 20033333

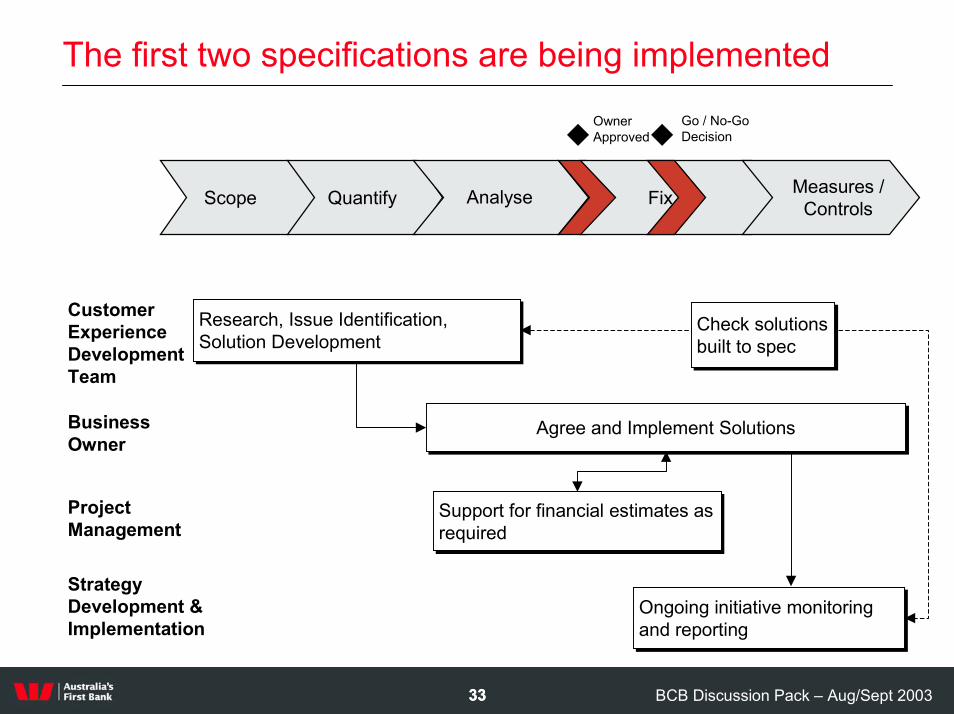

The first two specifications are being implemented

�Owner Approved

Go / No-Go Decision�

Scope Quantify Analyse Fix Measures / Controls

Customer Experience Development Team

Support for financial estimates as requiredSupport for financial estimates as required

Agree and Implement SolutionsAgree and Implement Solutions

Ongoing initiative monitoring and reporting Ongoing initiative monitoring and reporting

Check solutions built to specCheck solutions built to spec

Research, Issue Identification, Solution DevelopmentResearch, Issue Identification, Solution Development

Business Owner

Project Management

Strategy Development & Implementation

BCB Discussion Pack – Aug/Sept 20033434

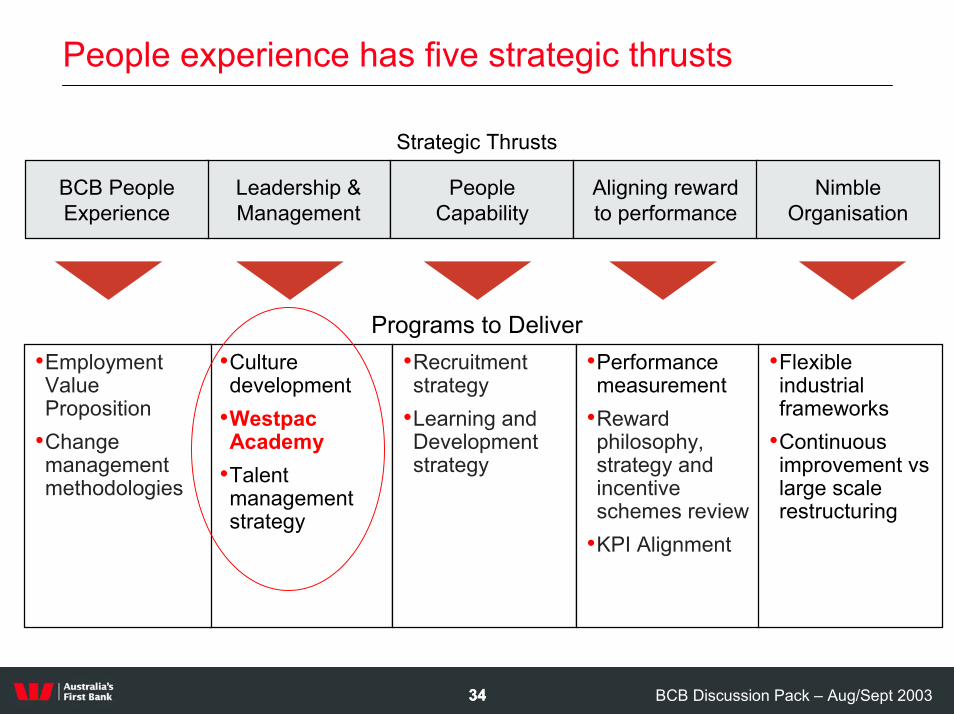

People experience has five strategic thrusts

Strategic Thrusts

BCB People Experience

Leadership & Management

People Capability

Aligning reward to performance

Nimble Organisation

•Culture development

•WestpacAcademy

•Talent management strategy

•Recruitment strategy

•Learning and Development strategy

•Performance measurement

•Reward philosophy, strategy and incentive schemes review

•KPI Alignment

•Employment Value Proposition

•Change management methodologies

•Flexible industrial frameworks

•Continuous improvement vslarge scale restructuring

Programs to Deliver

BCB Discussion Pack – Aug/Sept 20033535

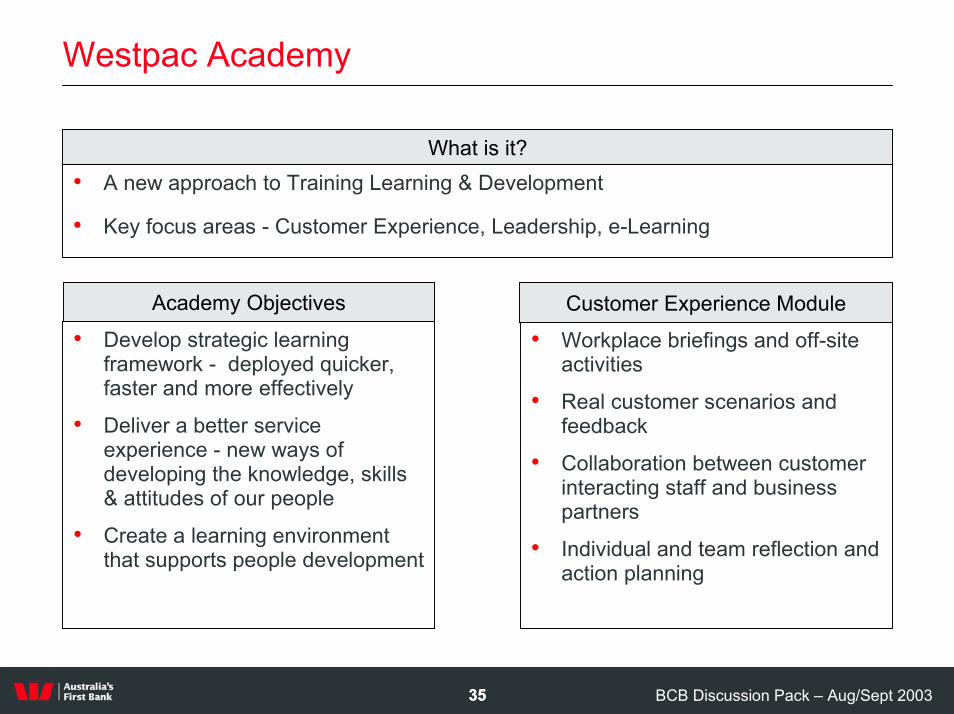

Westpac Academy

What is it?• A new approach to Training Learning & Development

• Key focus areas - Customer Experience, Leadership, e-Learning

Academy Objectives Customer Experience Module

• Develop strategic learning framework - deployed quicker, faster and more effectively

• Deliver a better service experience - new ways of developing the knowledge, skills & attitudes of our people

• Create a learning environment that supports people development

• Workplace briefings and off-site activities

• Real customer scenarios and feedback

• Collaboration between customer interacting staff and business partners

• Individual and team reflection and action planning

BCB Discussion Pack – Aug/Sept 20033636

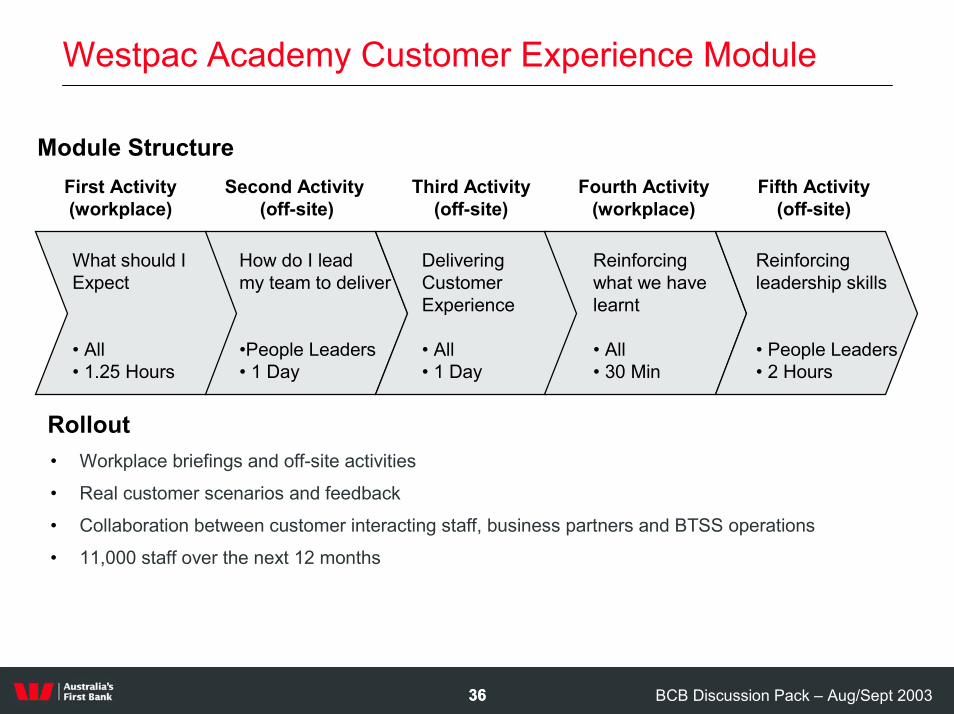

Westpac Academy Customer Experience Module

Module StructureSecond Activity

(off-site)Third Activity

(off-site)Fourth Activity

(workplace)Fifth Activity

(off-site)First Activity(workplace)

What should I Expect

• All• 1.25 Hours

How do I lead my team to deliver

•People Leaders• 1 Day

Delivering Customer Experience

• All• 1 Day

Reinforcing what we have learnt

• All• 30 Min

Reinforcing leadership skills

• People Leaders• 2 Hours

Rollout• Workplace briefings and off-site activities

• Real customer scenarios and feedback

• Collaboration between customer interacting staff, business partners and BTSS operations

• 11,000 staff over the next 12 months

BCB Discussion Pack – Aug/Sept 20033737

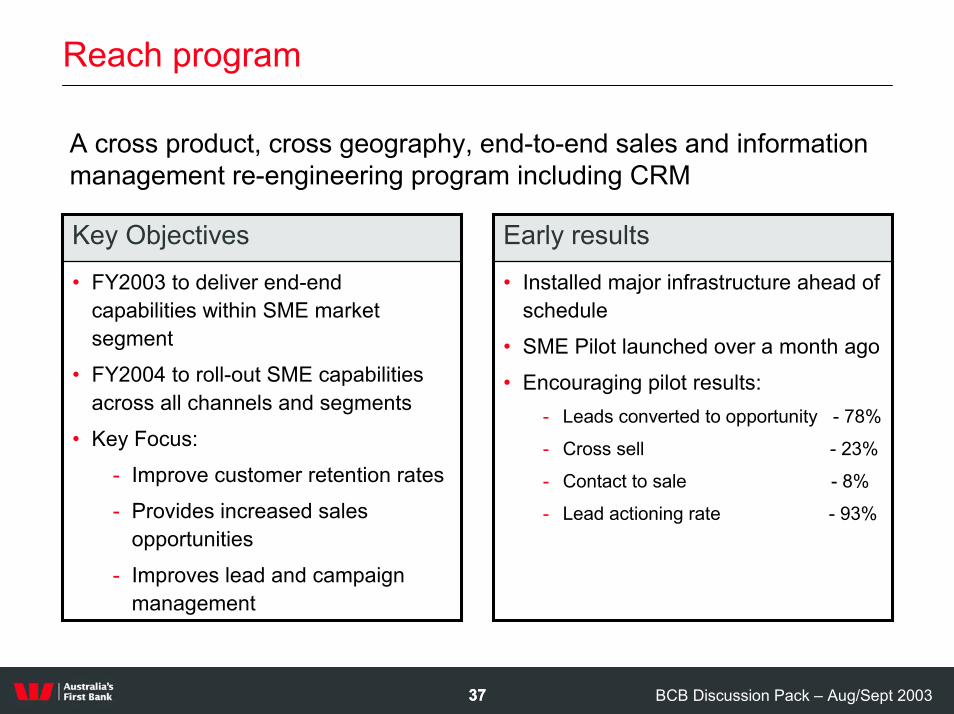

Reach program

A cross product, cross geography, end-to-end sales and information management re-engineering program including CRM

• Installed major infrastructure ahead of schedule

• SME Pilot launched over a month ago • Encouraging pilot results:

- Leads converted to opportunity - 78%

- Cross sell - 23%

- Contact to sale - 8%

- Lead actioning rate - 93%

• FY2003 to deliver end-end capabilities within SME market segment

• FY2004 to roll-out SME capabilities across all channels and segments

• Key Focus:- Improve customer retention rates- Provides increased sales

opportunities- Improves lead and campaign

management

Early resultsKey Objectives

BCB Discussion Pack – Aug/Sept 20033838

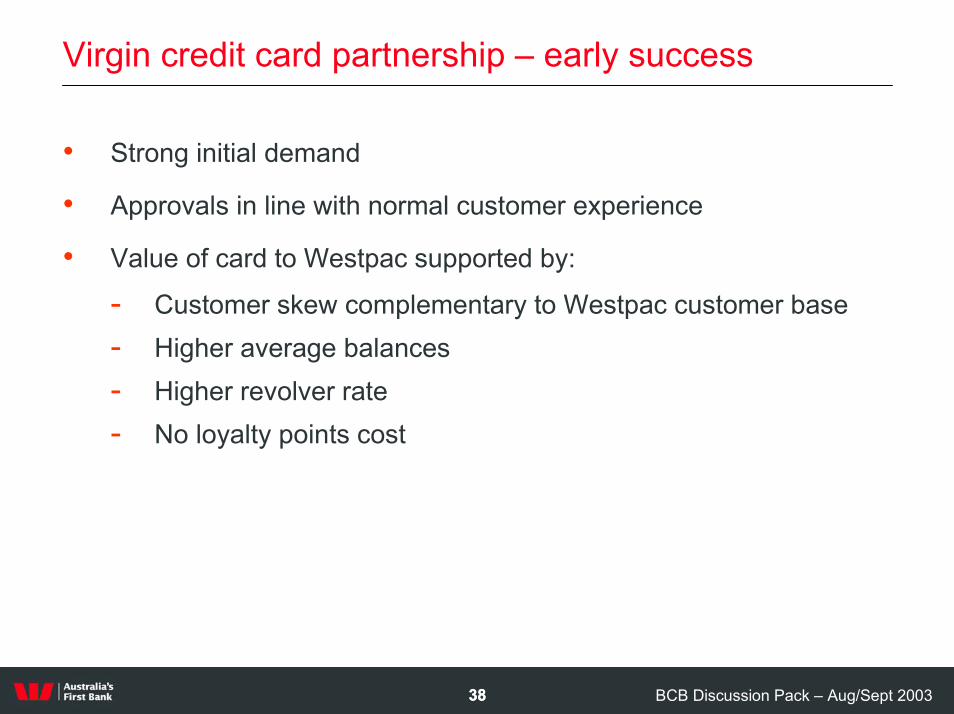

Virgin credit card partnership – early success

• Strong initial demand

• Approvals in line with normal customer experience

• Value of card to Westpac supported by:

- Customer skew complementary to Westpac customer base- Higher average balances - Higher revolver rate- No loyalty points cost

BCB Discussion Pack – Aug/Sept 20033939

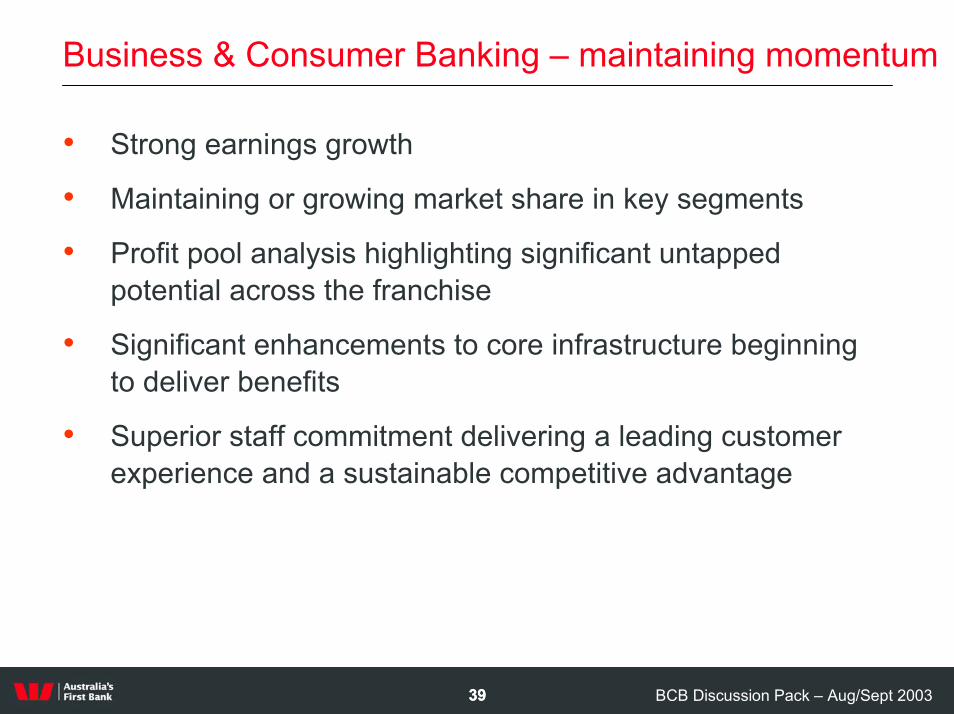

Business & Consumer Banking – maintaining momentum

• Strong earnings growth

• Maintaining or growing market share in key segments

• Profit pool analysis highlighting significant untapped potential across the franchise

• Significant enhancements to core infrastructure beginning to deliver benefits

• Superior staff commitment delivering a leading customer experience and a sustainable competitive advantage