Embed Size (px)

Citation preview

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

1

Western Australian Resources Industry

Construction to Operations Phase

Workforce Study

An investigation into the workforce dynamics and implications for skills,

training and education as major projects transition from a construction

phase to an operational phase

June 2014

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

2

CONTENTS

Executive Summary ................................................................................................................................... 5

Background and Purpose ...................................................................................................................... 10

Background ........................................................................................................................................... 10

Study Limitations ................................................................................................................................... 12

Current Resource Project Construction Pipeline and Workforce Estimates ................................. 14

Transition from Construction to Operations......................................................................................... 16

Project Development Cycle .............................................................................................................. 16

Impact on Resources Company Workforce ................................................................................... 19

Impact on the Construction Workforce ........................................................................................... 21

Resources Project Construction Workforce Dynamics ..................................................................... 24

Demand and Supply ........................................................................................................................... 24

Nature of the Resources Construction Workforce ......................................................................... 25

Relationship between the Mining and Construction Industry Workforces .................................... 35

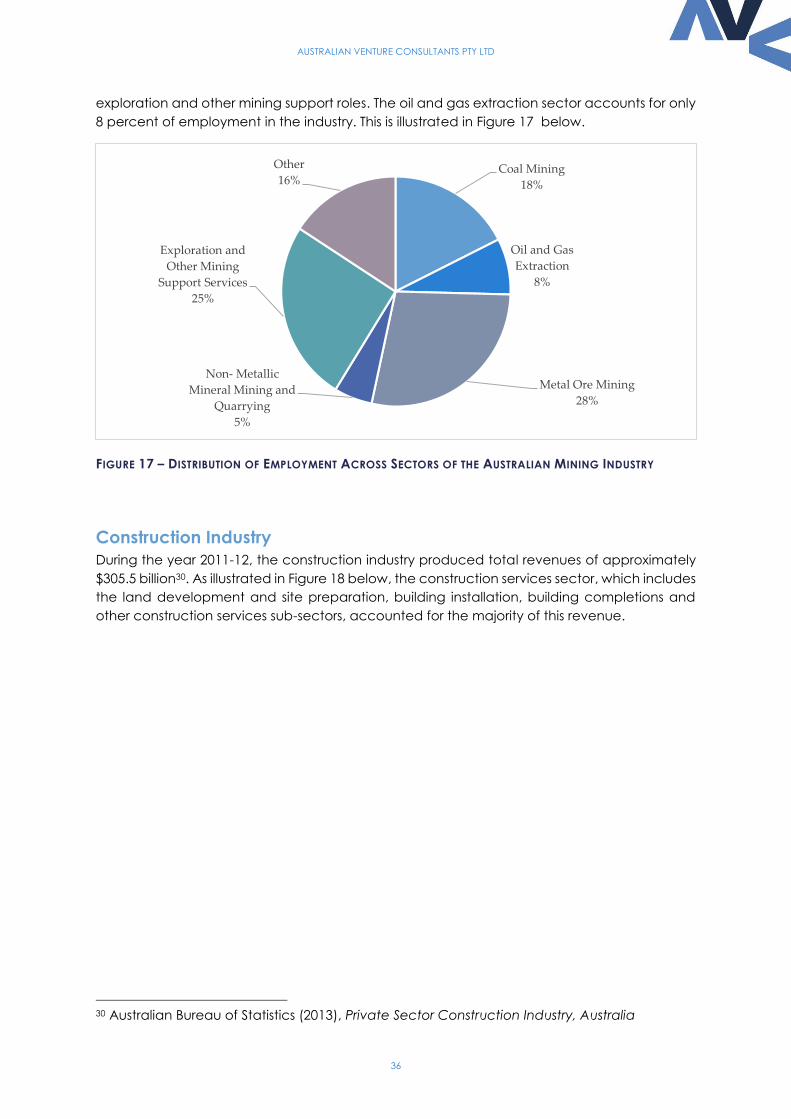

Revenue and Employment ................................................................................................................ 35

Demographic Comparison ................................................................................................................ 43

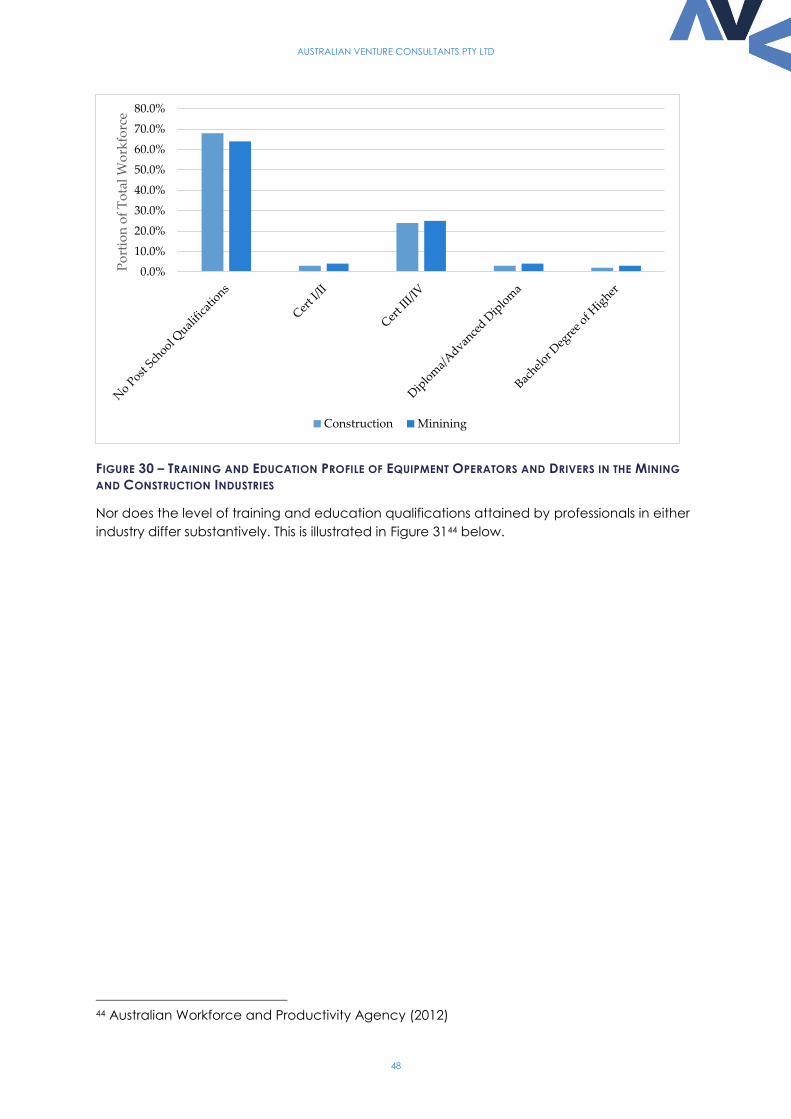

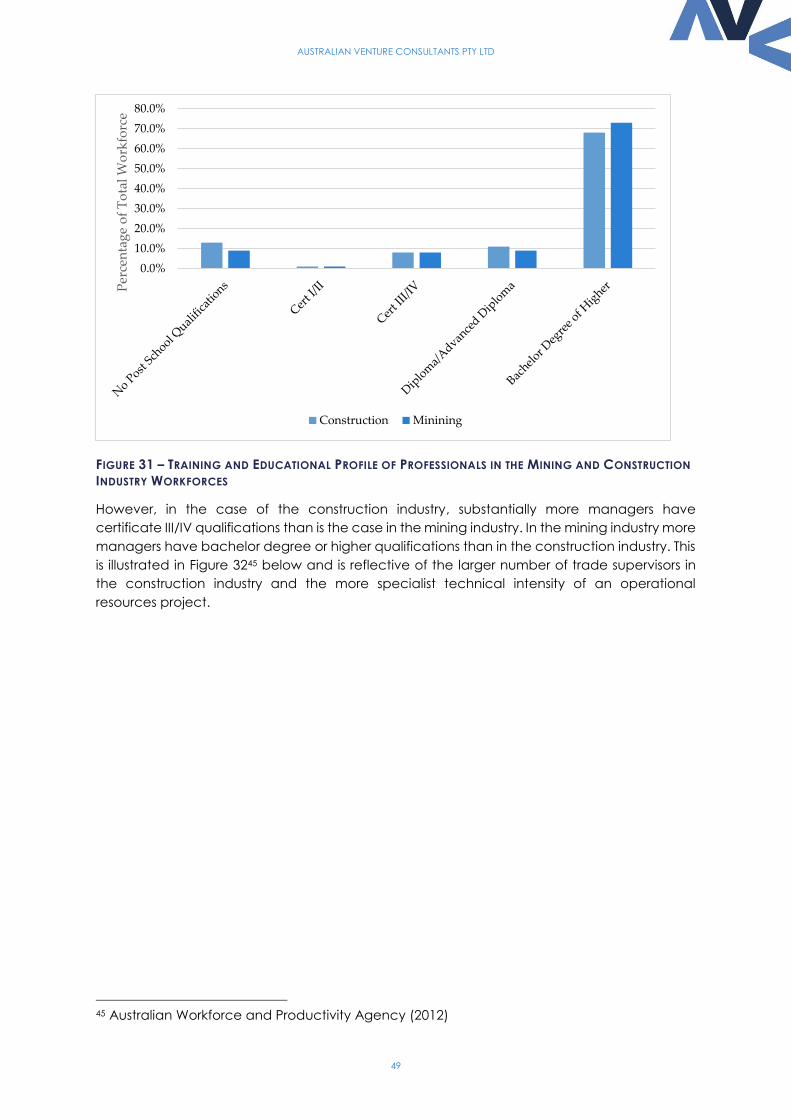

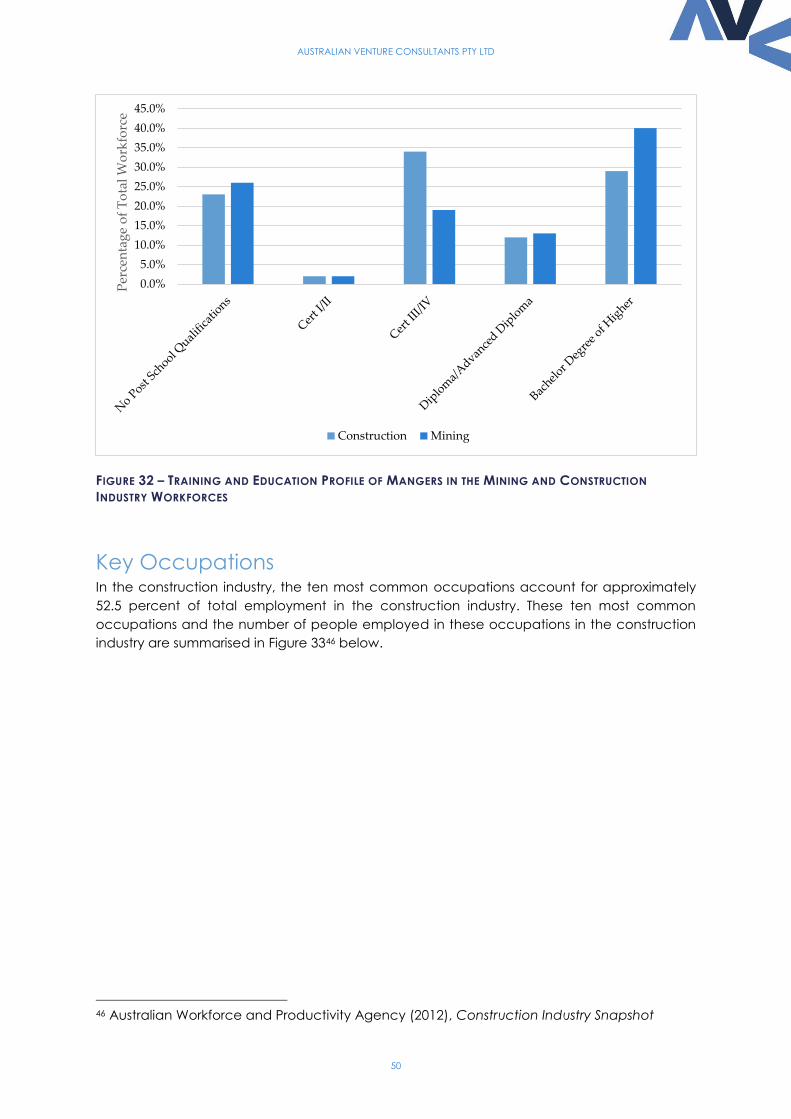

Education and Training Comparison ................................................................................................ 45

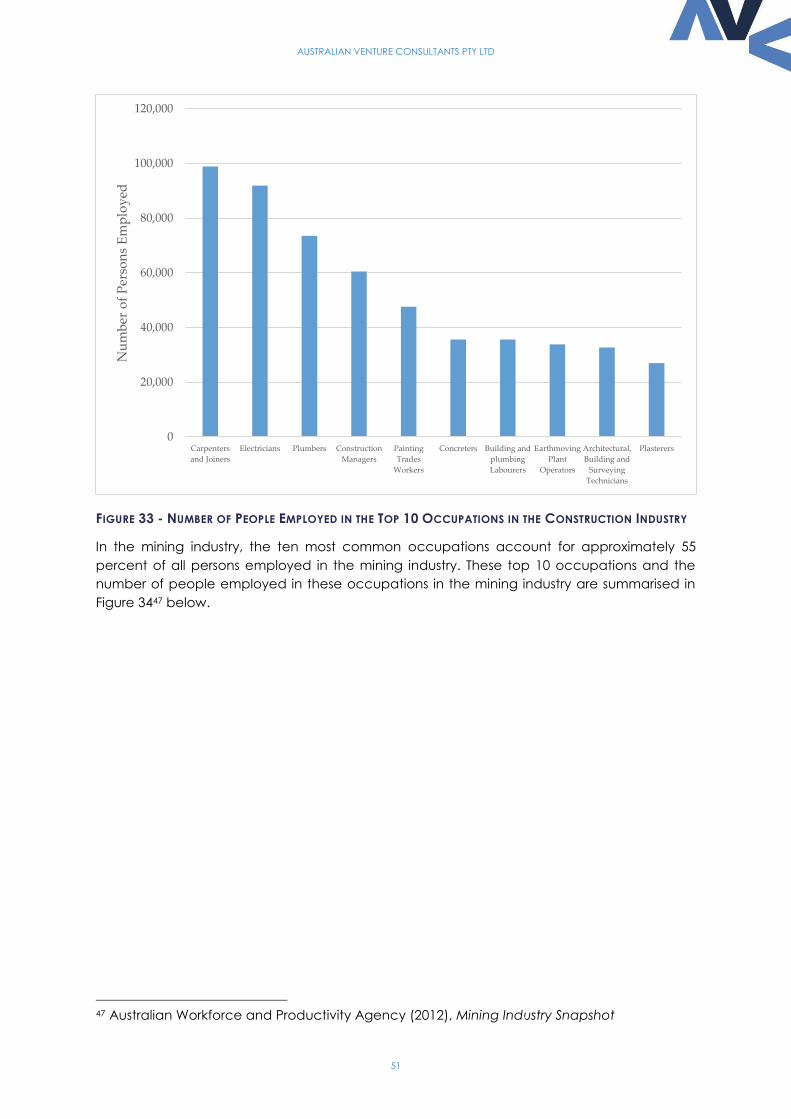

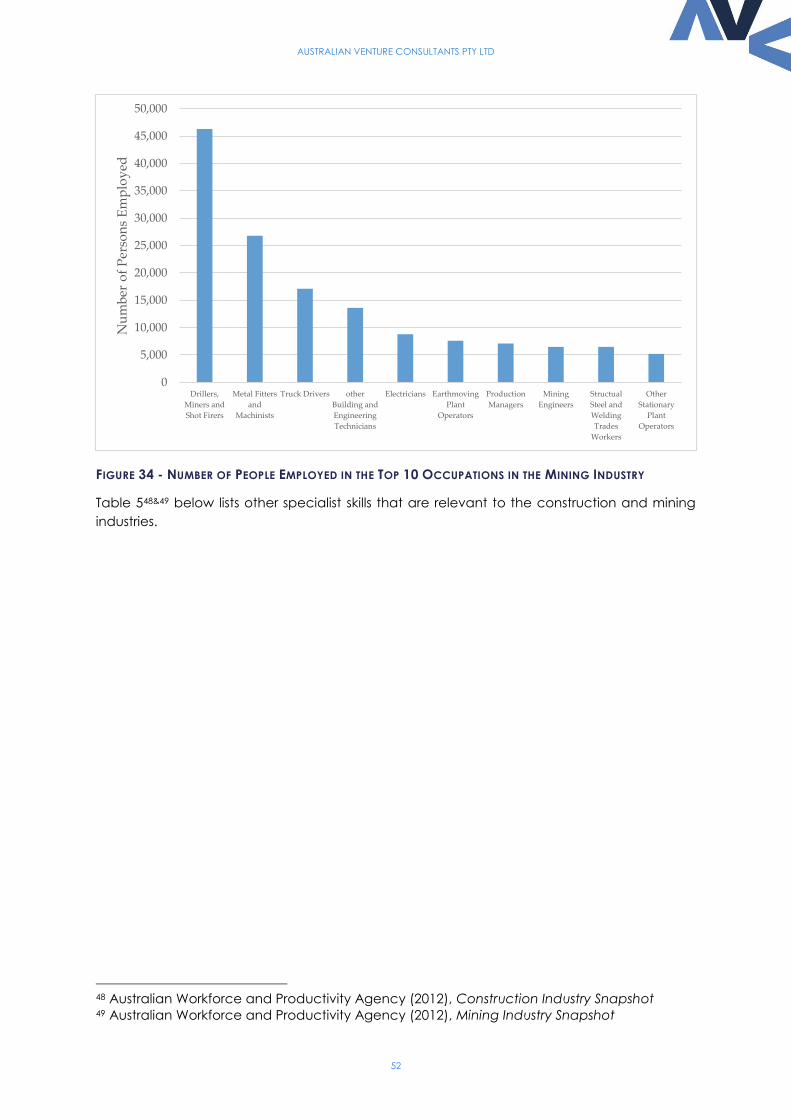

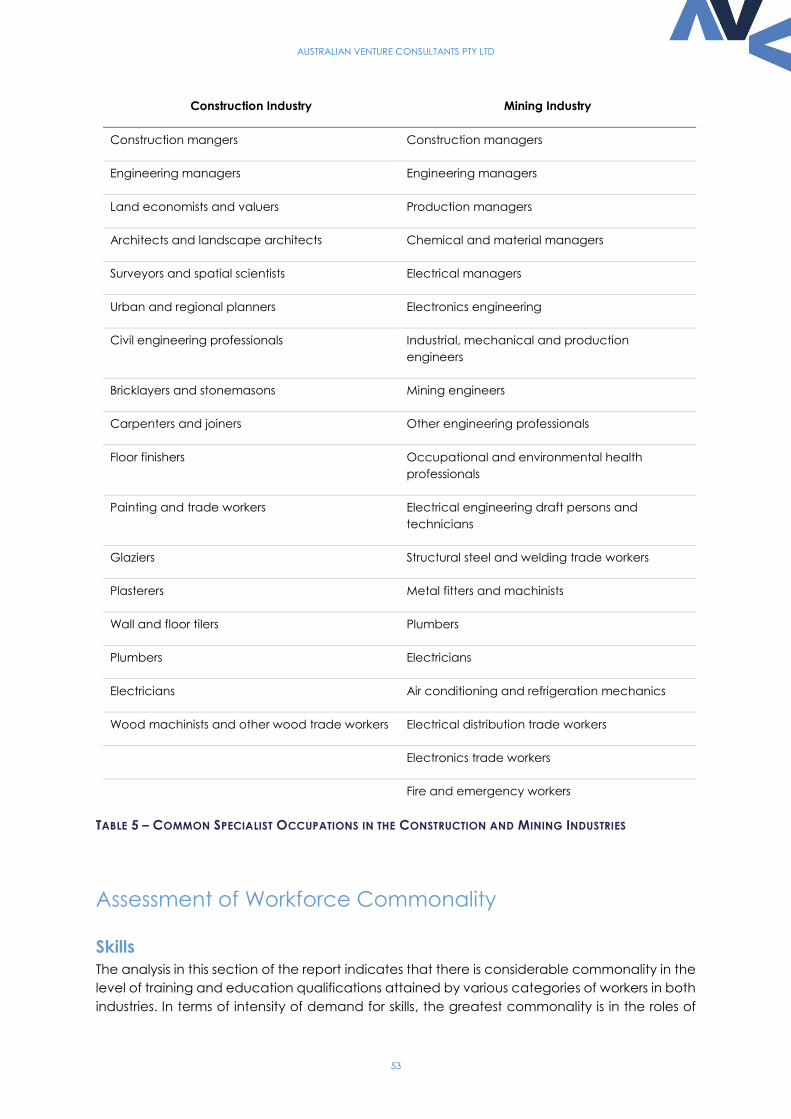

Key Occupations .................................................................................................................................. 50

Assessment of Workforce Commonality .......................................................................................... 53

Lessons from the Recent Construction Phase..................................................................................... 55

Implications for Skills, Training and Education .................................................................................... 57

Conclusions ............................................................................................................................................... 58

Appendix 1 – Overview of Western Australian Resources Industry Construction Projects ......... 59

Oil and Gas Projects ............................................................................................................................ 59

Iron Ore Projects ................................................................................................................................... 61

Ammonium Nitrate, Nitrate and Urea Projects ............................................................................... 64

Gold Projects ......................................................................................................................................... 64

Resources Infrastructure Projects ....................................................................................................... 65

Appendix 2: Construction and Operational Workforce Estimate .................................................. 67

Appendix 3: 2012-13 Submissions to Infrastructure Australia ............................................................ 69

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

3

Disclosure and Disclaimer

This document has been prepared by Australian Venture Consultants Pty Ltd (ACN: 101 195 699) (‘AVC’). AVC

has been commissioned to prepare this publication by the Resources Industry Training Council (RITC) and has

received a fee from the RITC for its preparation.

While the information contained in this publication has been prepared by AVC with all reasonable care from sources

that AVC believes to be reliable, no responsibility or liability is accepted from AVC for any errors, omissions or

misstatements however caused. Any opinions or recommendations reflect the judgment and assumptions of AVC

as at the date of the document and may change without notice. AVC, its officers, agents and employees exclude

all liability whatsoever, in negligence or otherwise, for any loss or damage relating to this document to the full extent

permitted by law. Any opinion contained in this publication is unsolicited general information only. AVC is not aware

that any recipient intends to rely on this document or of the manner in which a recipient intends to use it. In preparing

this information it is not possible to take into consideration the information or opinion needs of any individual

recipient. Recipients should conduct their own research into the issues discussed in this document before acting

on any recommendation.

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

4

Interviewees

While this study was based primarily on the review of published data and literature, the

following experts provided key input and guidance to the study.

Andrew Blitz, Business Development Manager, Western Australian Local Government

Association

John Galvin, Executive General Manager, Georgiou Group

Bindi Gove, Government and External Affairs Manager, BHP Billiton Petroleum

Kiersten Gregg, General Manager Human Resources, Rio Tinto Iron Ore

Kapila Karunaratna, GM Technical, Mitsubishi Development

John Phillips, Executive Manager Workplace Business Solutions, Western Australian

Local Government Association

Jeanette Roberts, Australian Chair, Kvaerner

Justin Willis, Practice Leader Rail and Crawler Mounted Mobile Machines, SKM

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

5

Executive Summary

Background

The recent resources industry investment phase has involved a total investment of A$457 billion

(at current prices) in new resources industry capital in Australia since 2004, an average of

approximately A$40 billion per annum over that period. Approximately 55.5 percent of this

investment has been associated with Western Australian resources projects, particularly in the

iron ore and oil and gas sectors. Presently, there remains a pipeline of 48 new resources

projects with an associated capital investment of A$229 billion that are currently under

construction or have been committed to by their proponents.

This has had a dramatic impact on demand for a range of skills from the project proponents,

EPCMs managing the construction of those projects and their contractors, which have been

sourced from construction labour markets across Australia and overseas.

The resources industry is now passing through peak investment phase, with many large

resources industry construction projects transitioning into an operational phase. As such, the

size of the total workforce associated with these projects as well as the occupational structure

of that workforce will change, focusing on the operational human resource requirements.

Transition from Construction to Operations

When a new resources project transitions from the construction phase to the operational

phase the size of the total workforce associated with the project decreases dramatically. The

degree to which the size of the workforce decreases is unique to the nature of the construction

project and the operational specifics of the project. Anecdotally, the operational workforce

can be:

As low as 4 percent of the size of the construction workforce in the case of oil and gas

projects;

Around 35 percent of the size of the construction workforce in the case of iron ore

projects;

Approximately 10 percent of the size of the construction workforce in the case of

ammonium, ammonium nitrate and urea projects;

Around 7 percent of the size of the construction workforce in the case of gold projects;

and

15 precent of the size of the construction workforce for port oriented resources

infrastructure projects.

In most cases, the skills profiles have limited commonality, particularly in the case of the oil and

gas industry. In the mining industry, occupational skills are skewed heavily toward specialist

skills such as drillers and shot-firers, metal fitters and machinists and truck drivers). In

occupational skills where there is commonality such as electricians, the operational resources

industry needs in terms of workforce numbers are very small compared to those of the

construction industry.

It is key to note that the operational workforce is not a subset of the construction workforce.

The construction workforce is comprised primarily of employees and contractors of the

construction industry companies that have been successful tenderers for aspects of the

resources construction project. When the construction project is complete, those construction

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

6

industry employees and contractors remain in the construction industry, moving onto new

projects within the resources industry or more widely. Very few, if any, construction workers

transition to an operational role in a resources project.

This is primarily because, for the following reasons, the construction industry workforces are

culturally and structurally quite different:

Skills in most construction industry occupations are developed to be applicable to a

wide range of construction projects. Whereas, skills in resources industry operational

roles tend to be relatively specialised for the specific task; and

The construction workforce is largely a mobile workforce that selects the projects and

locations in which it works based on personal utility. Workers comprising that work force

are comfortable with geographic and project diversity and often thrive on that

diversity. Whereas, workers that comprise the operational resources industry workforce,

typically seek a higher degree of permanency and stability.

Most of the reduction in project workforce as projects transition to operations is the result of

construction contractors and subcontractors completing their specific tasks and exiting the

project. However, some positions that were created in the resources companies to oversee

and support the construction process also become redundant. The position most affected by

this is the project management role within the resources companies. Individuals in project

management roles are unlikely to transition back into operational roles and will be redeployed

on sustaining capital projects within the companies, or become employed by other

companies executing construction projects or by EPCMs.

During the recent resources industry investment phase, graduate programs have expanded in

many companies as these companies sought to grow the pool of professional staff available

to them. In many cases, the transition from construction to operational phase has seen a

decrease in internal activity, rendering it difficult to find places for these graduates outside of

the graduate program. This may result in a surplus of junior mining executives in the market

place in the short term until the graduate program intakes equalise.

While many companies have expanded apprentice and trainee programs on the same basis,

there is less of a challenge in the market for trade persons, apprentices and trainees. The

relative size of the pool of demand for trade skills within the resources sector and the wider

construction industry means that there is likely to be greater opportunity in the marketplace

for apprentices and trainees that have been trained on resources construction projects.

As resources projects transition to operations, some of the construction labour that is released

from these projects will be absorbed into other resources construction projects such as Roy Hill

and resources projects sustaining capital programs. But the vast majority will likely seek

employment in the conventional residential and non-residential construction sectors and the

infrastructure construction sectors, particularly transport infrastructure. Some opportunities may

also arise from investment by the Australian Defence Force.

Resources and Construction Industry Labour Market Dynamics

Whereas the operation of most resources projects is capital intensive, the construction of those

projects is labour intensive. Unlike most labour intensive enterprise, resources project

construction does not have the luxury of locating most of the labour intensive components of

the exercise in close proximity to the required labour markets. The construction workforce is

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

7

located across most parts of the world, has very versatile skills and is by its nature, a relatively

mobile workforce.

Most Western Australian resources projects are located in remote, isolated regions. If they are

in proximity to a population centre, those population centres have limited civic capacity and

limited employment opportunities beyond the new resources projects and related

infrastructure, rendering permanent relocation of a construction workforce highly unlikely. As

such, the only way that new resources projects in Western Australia can access adequate

supply of workers during the investment phase is through overseas migration and/or domestic

and international long-distance commuting.

Subclass 457 Visas have been a significant source of professional and trade labour for

resources construction projects, and while long-distance commuters comprise only

approximately 2 percent of the total Australian labour force, they are critically important to

the resources industry and resources industry projects evidenced by the fact that:

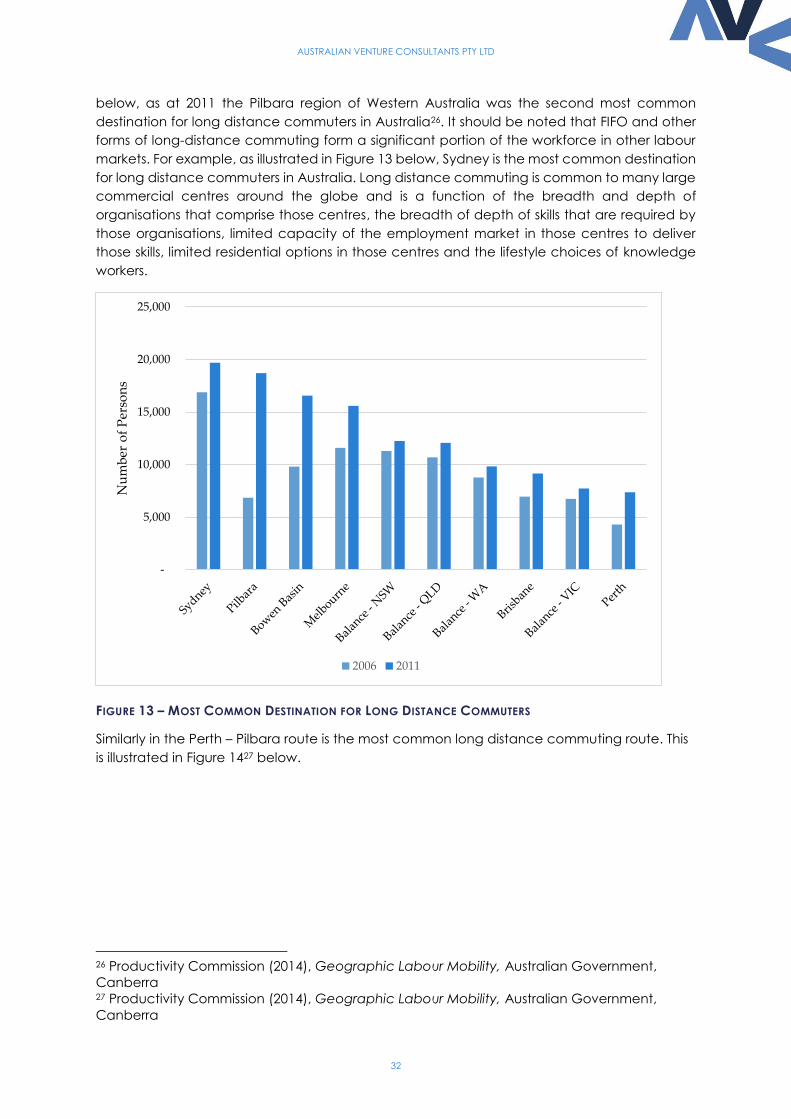

The Pilbara Region is the second most common destination for long distance

commuters;

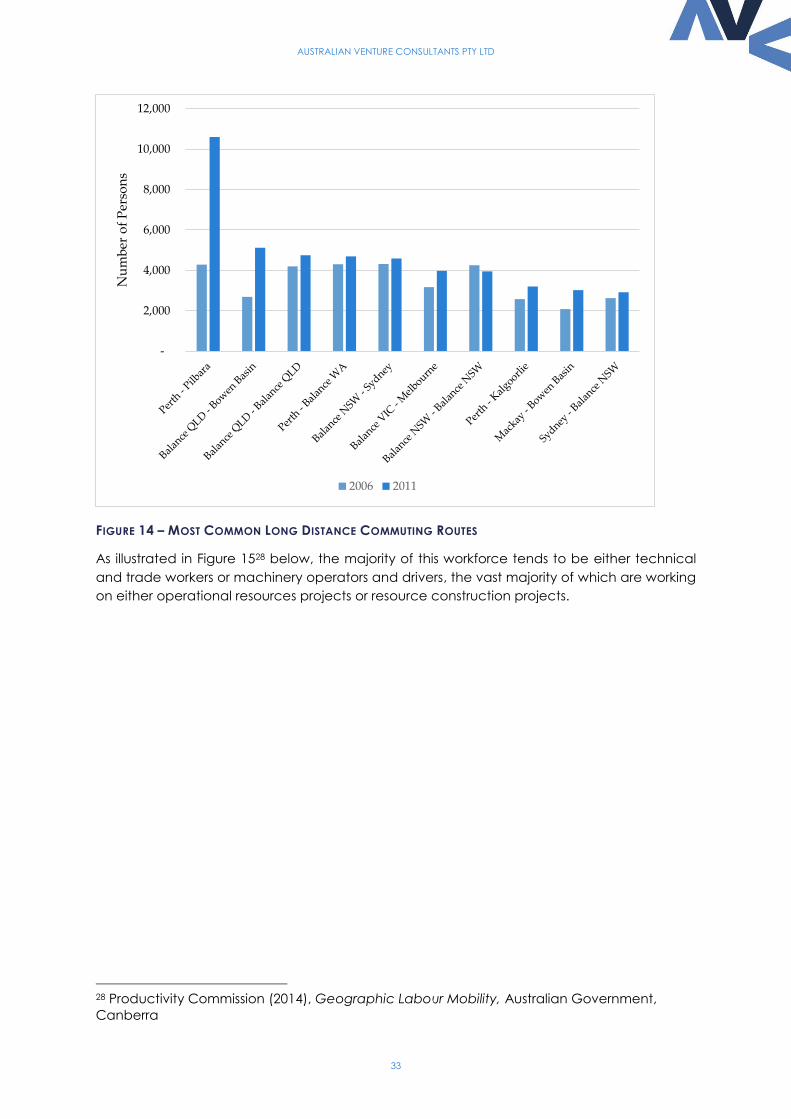

The Perth-Pilbara Region route is the most common long distance route in the Nation;

and

Approximately 70 percent of long distance commuters between Perth and the Pilbara

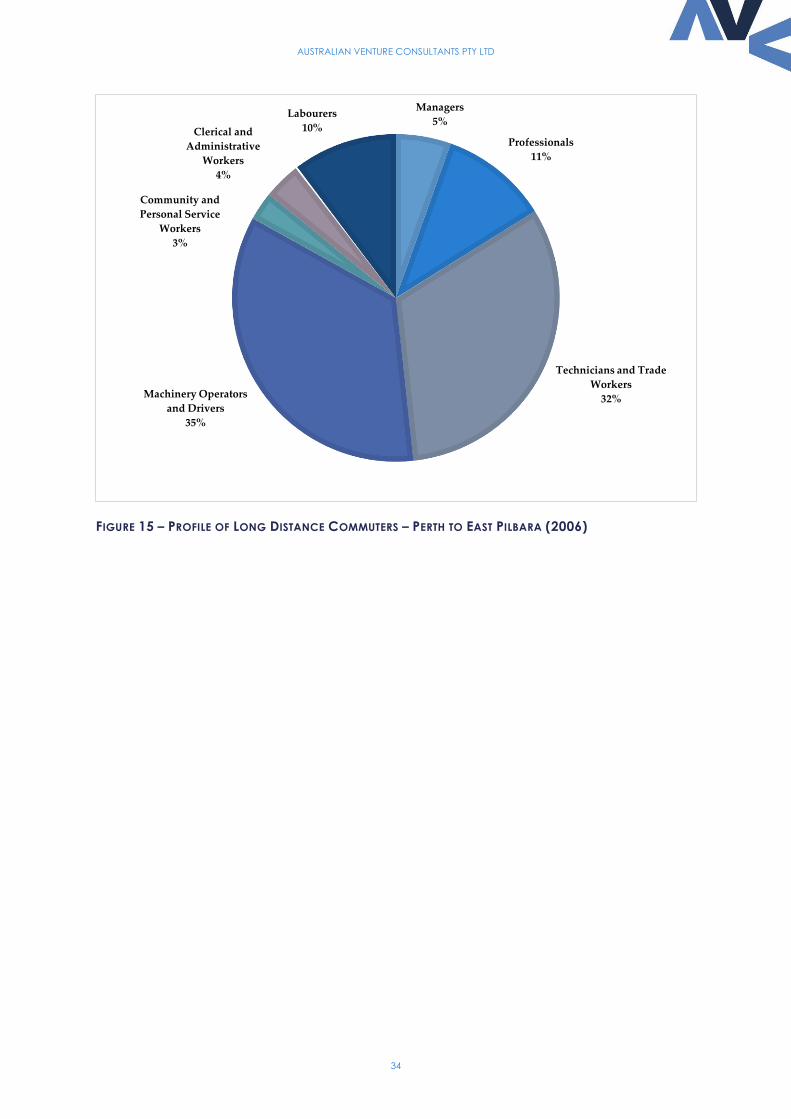

Region are machinery operators and drivers or technicians and trade workers.

Resources and Construction Industries Compared

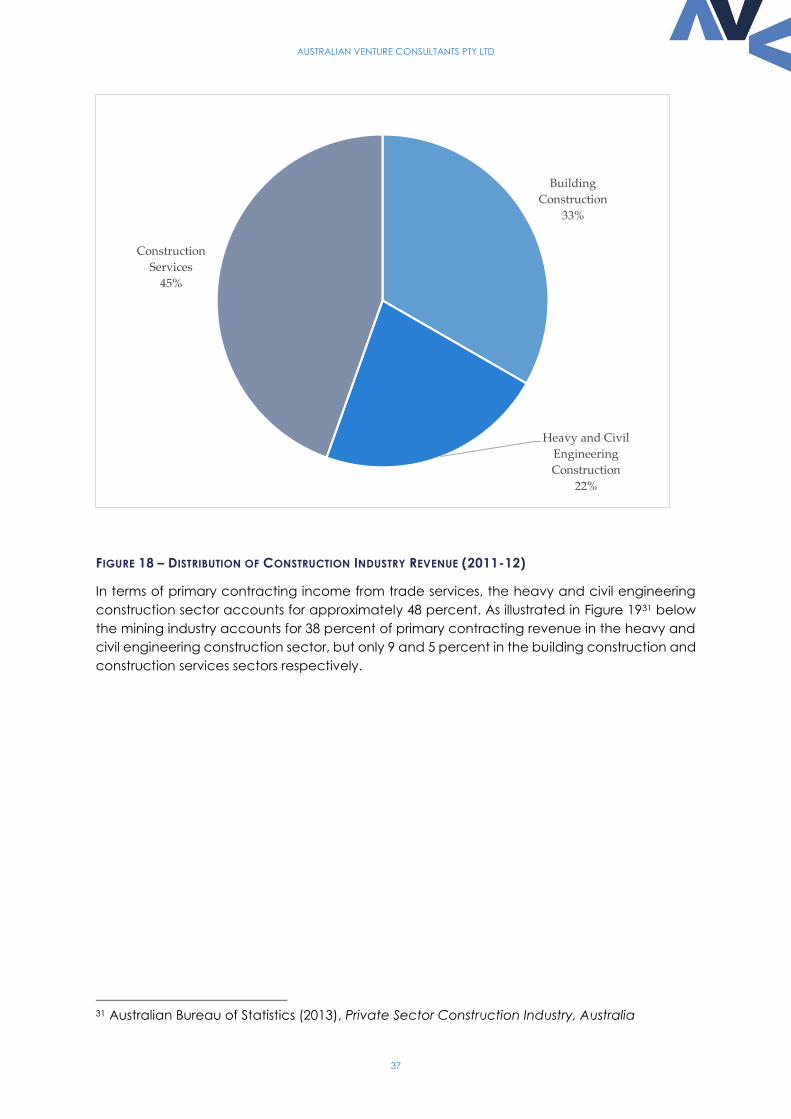

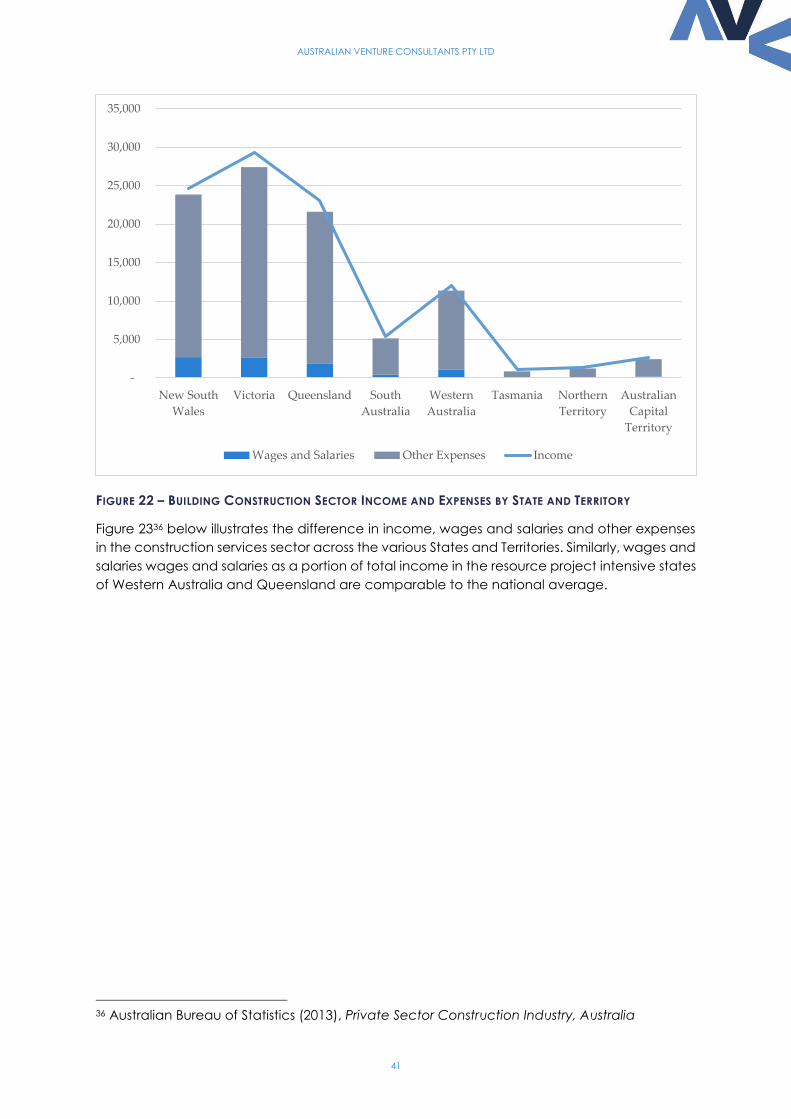

The wider construction industry is substantially larger than the resources industry. In 2011-12, the

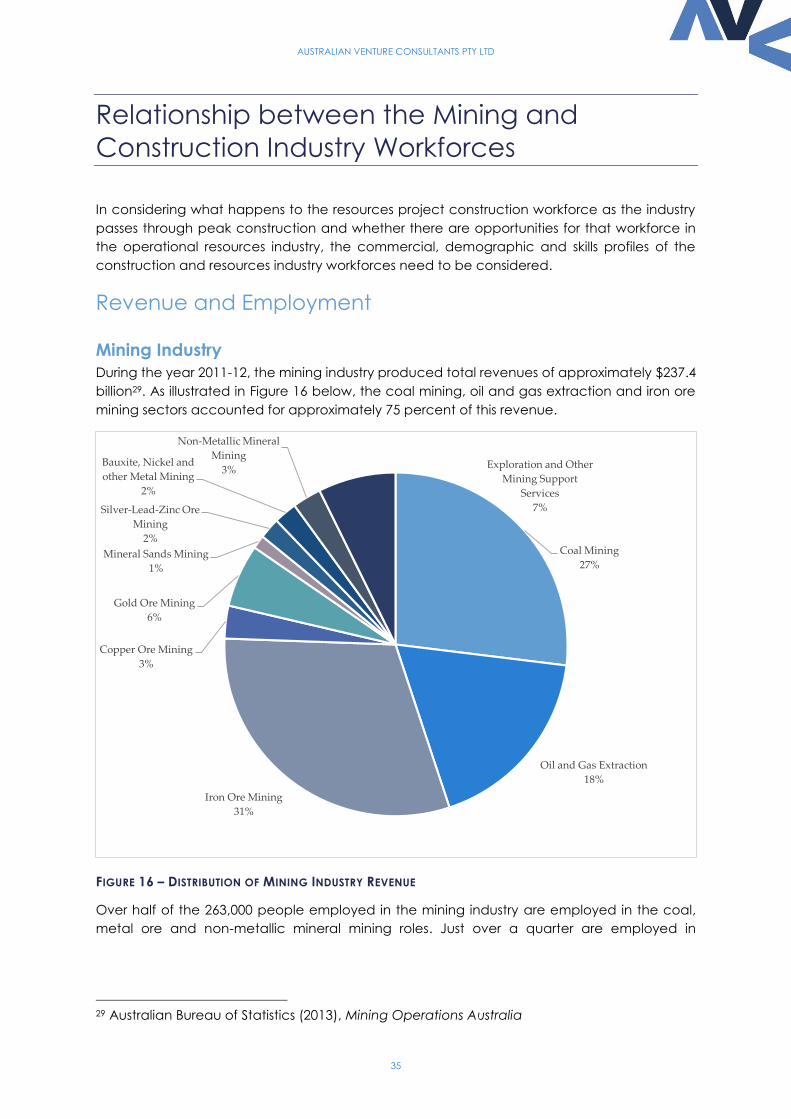

resources industry produced total revenues of approximately $240 billion, approximately 75

percent of which was produced by the coal, iron ore and oil and gas sectors. Whereas, in the

same period, the construction industry produced total revenues of approximately $305.5

billion, of which construction services accounted for approximately 45 percent and building

construction 33 percent. The heavy and civil engineering construction sector, which is the

sector of the construction industry that is most dependent on revenue from mining construction

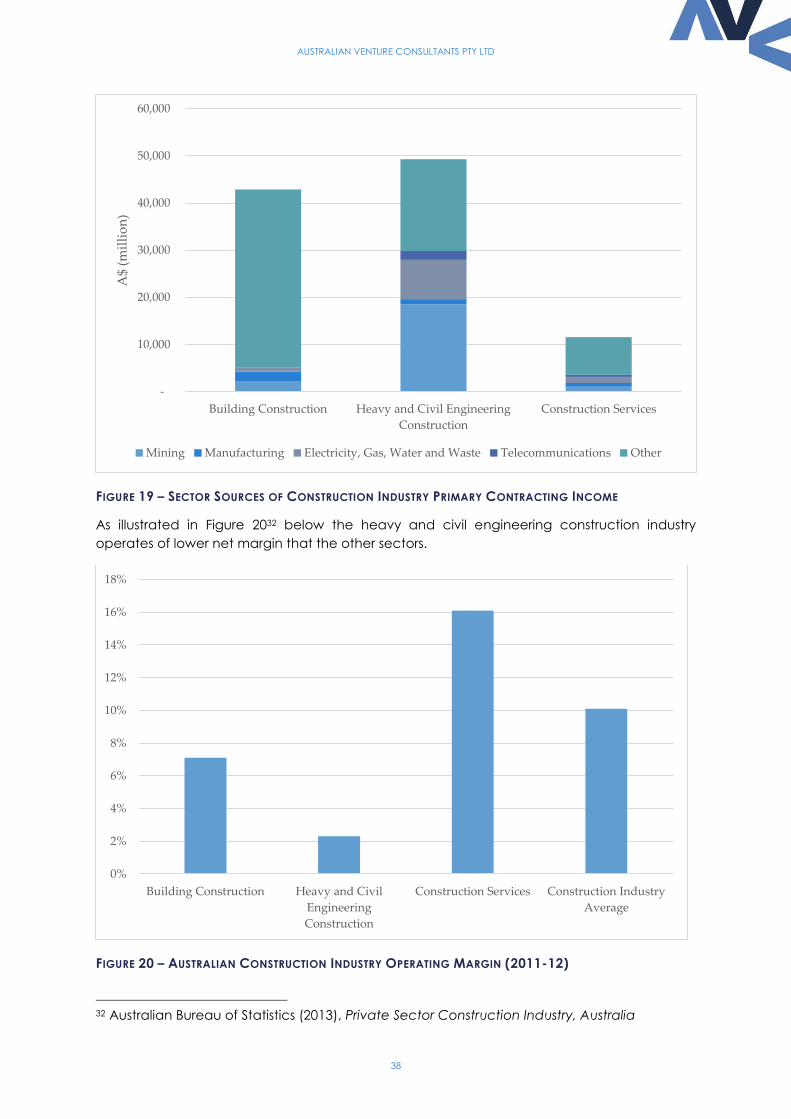

projects, accounted for only 22 percent of construction industry revenues. Revenue from

mining projects accounts for approximately 38 percent of primary contracting revenue from

trade services in the heavy and civil engineering construction sector, but only 9 and 5 percent

in the building construction and construction services sectors respectively. The heavy and civil

engineering construction sector also operates on lower margins than the other sectors of the

Australian construction industry.

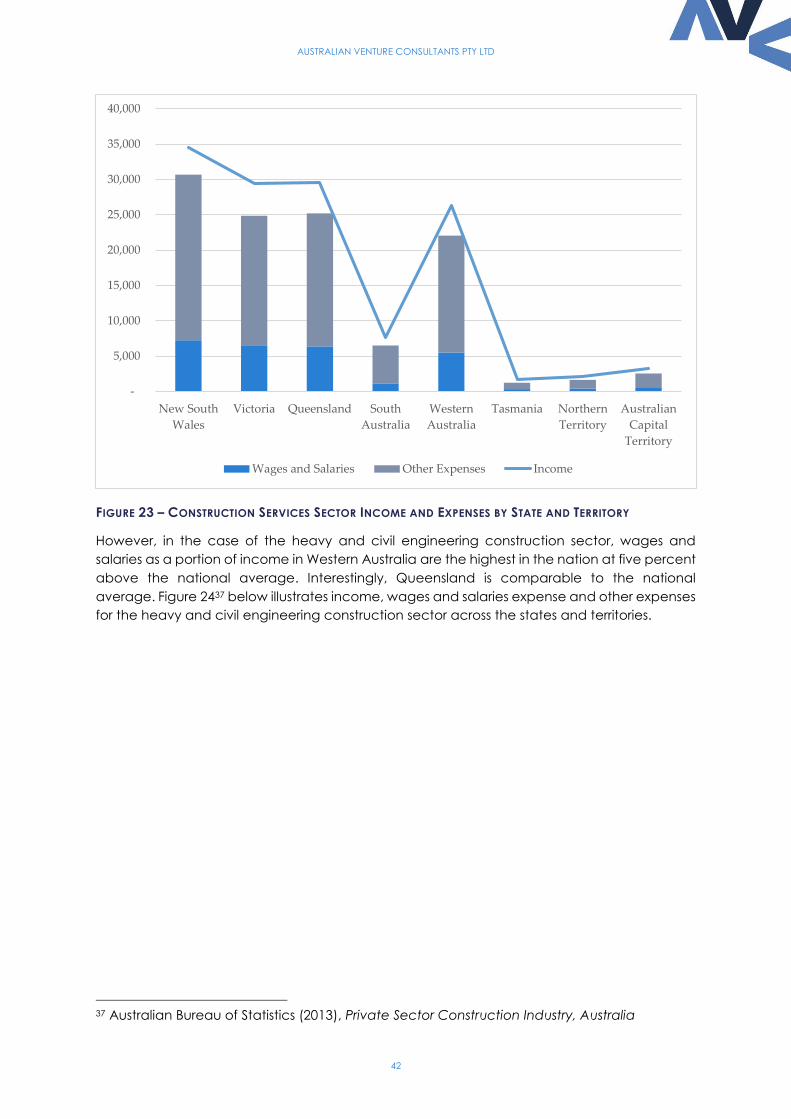

The construction industry also employs approximately 3.5 times as many people as the

resources industry. Of the 263,000 people employed in the resources industry, approximately

75 percent are employed in coal, metal ore and non-metallic mining and exploration and

other mining support roles. Of the 950,000 people employed in the Australian construction

industry, the vast majority (approximately 68 percent) are employed in the construction

services sector, with only approximately 15 percent employed in the heavy and civil

engineering construction sector. Whereas the majority of people working in the construction

services sector work for the approximate 17,500 small businesses in the sector, the majority of

workers in the heavy and civil engineering construction sector work for the approximate 70

large businesses in the sector.

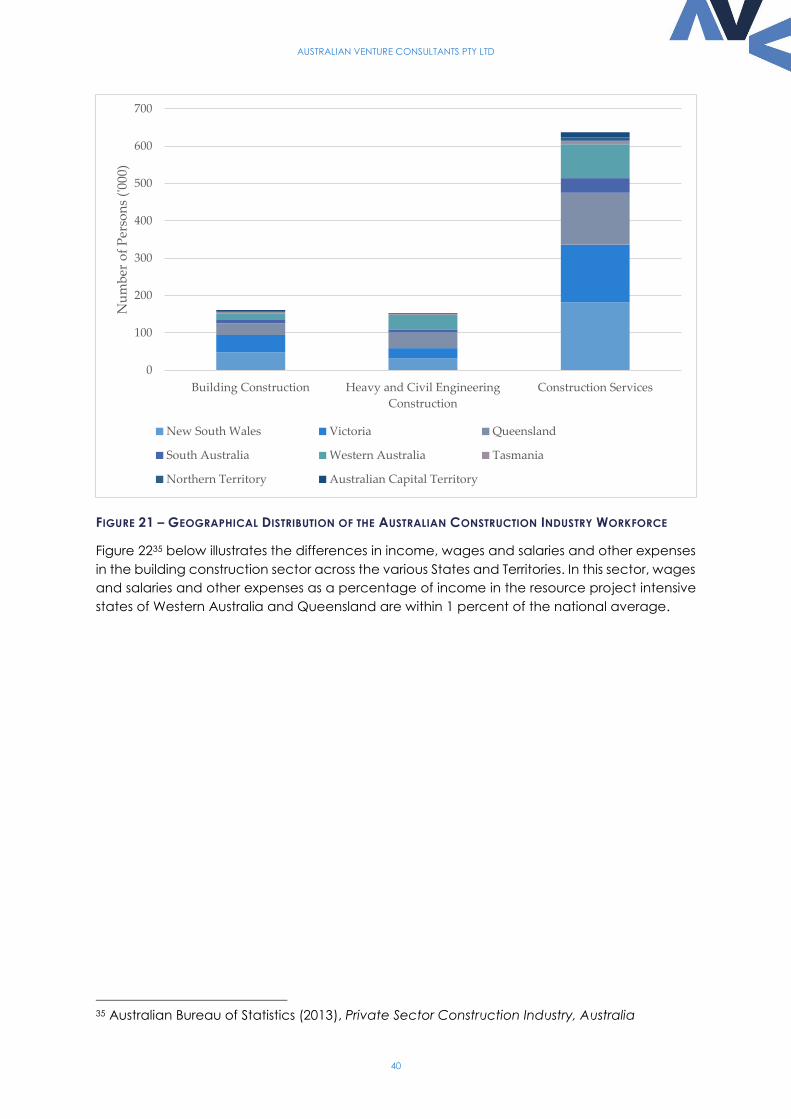

In terms of geographic location, the construction industry workforce in each of the sectors that

comprise the industry is reasonably equally distributed across the larger states of New South

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

8

Wales, Victoria, Queensland and Western Australia. The fact that there isn’t a skew in the

construction industry workforce toward Western Australia and Queensland is probably

reflective of considerable residential and non-residential construction markets in the more

populated states of New South Wales and Victoria, and the long-distance commuter intensity

of the resources project construction workforce.

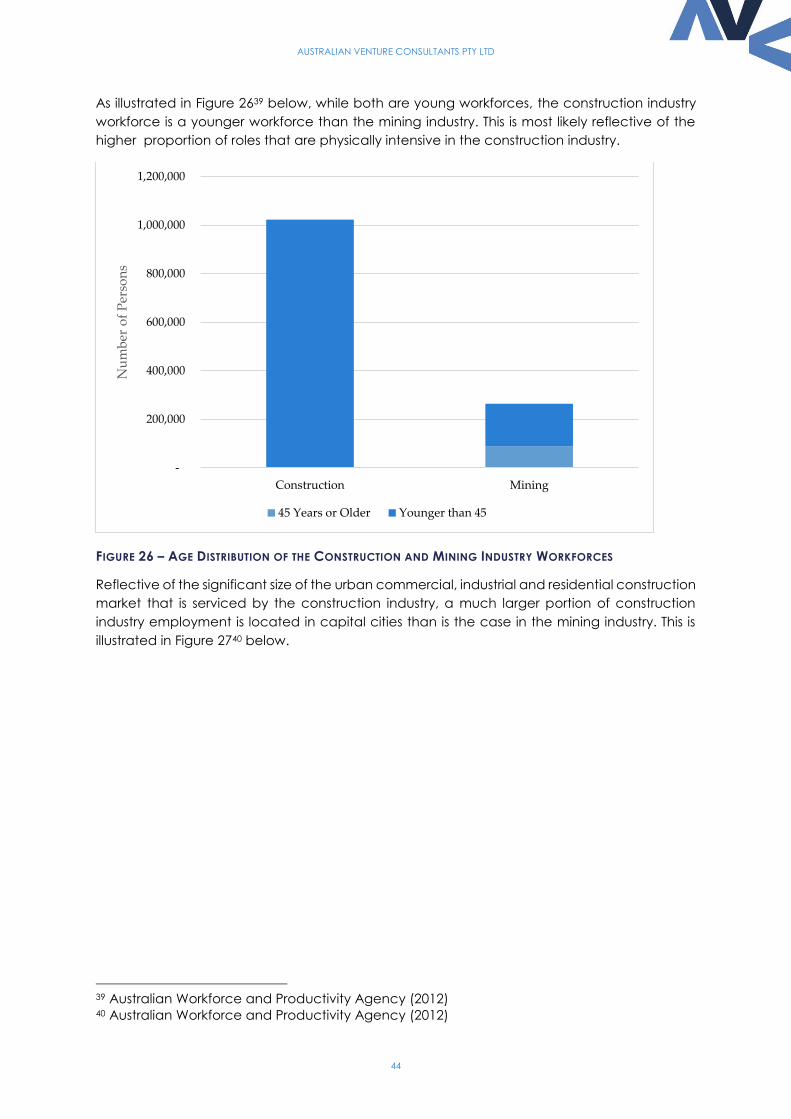

The gender and age distribution of both the mining and construction workforce is reflective of

the physical nature of work in both industries, with both workforces dominated by males under

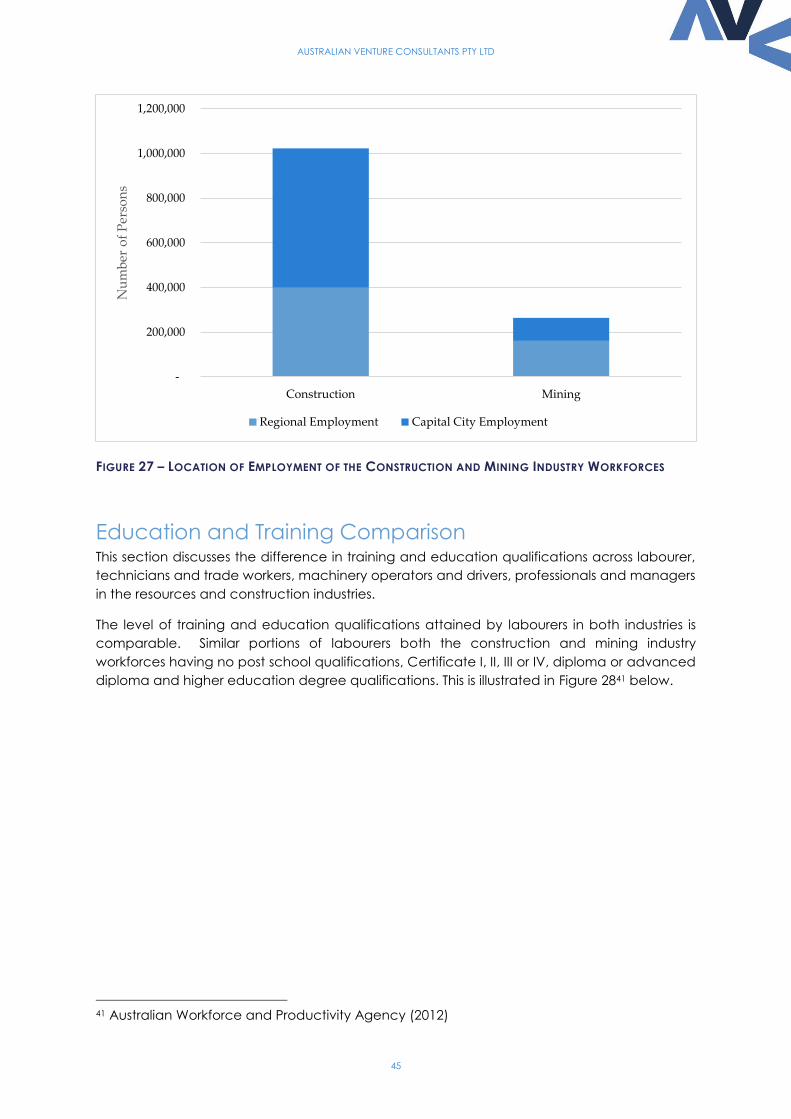

45 years of age. A much larger portion of the construction industry workforce is employed in in

capital cities as opposed to the regions.

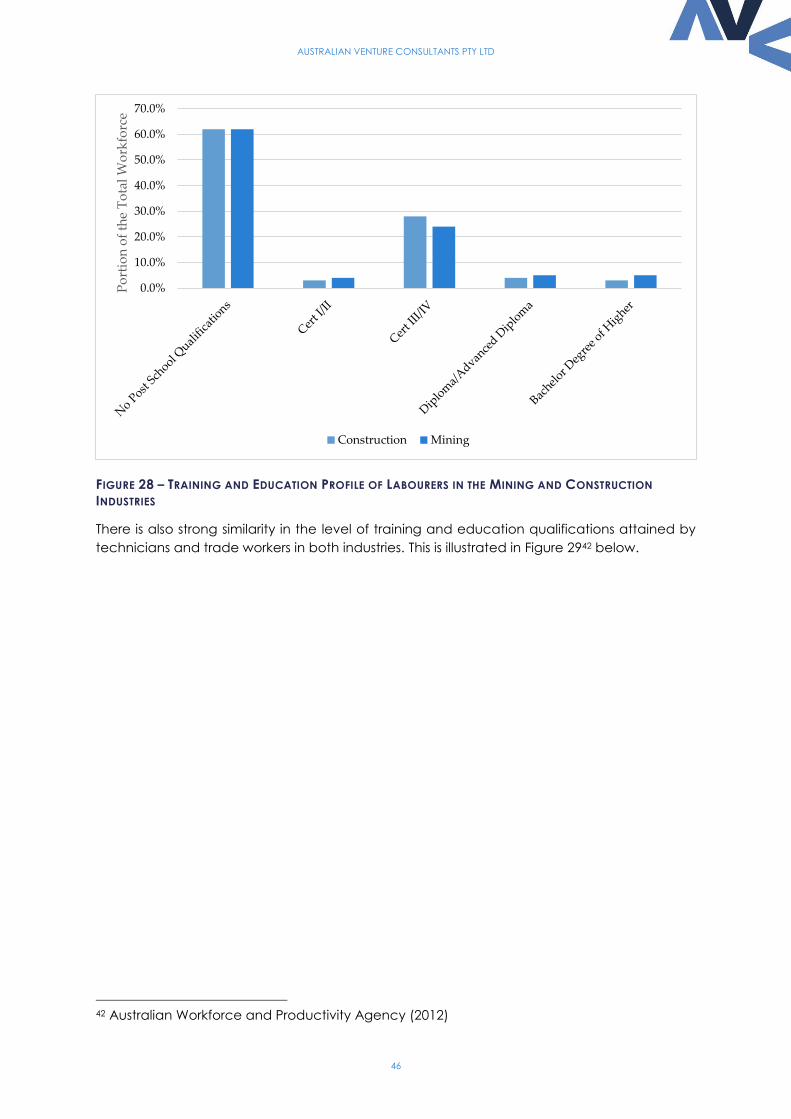

The level of training and education qualification attained by labourers, technician and trade

workers, equipment operators and drivers and professionals employed in the mining and

construction industries is comparable. However, in the case of the construction industry

substantially more managers have certificate III/IV qualifications than is the case in the mining

industry. In the mining industry more managers have bachelor degrees or higher qualifications

than in the construction industry. This is reflective of the larger number of trade supervisors in

the construction industry and the more specialist technical intensity of an operational

resources project.

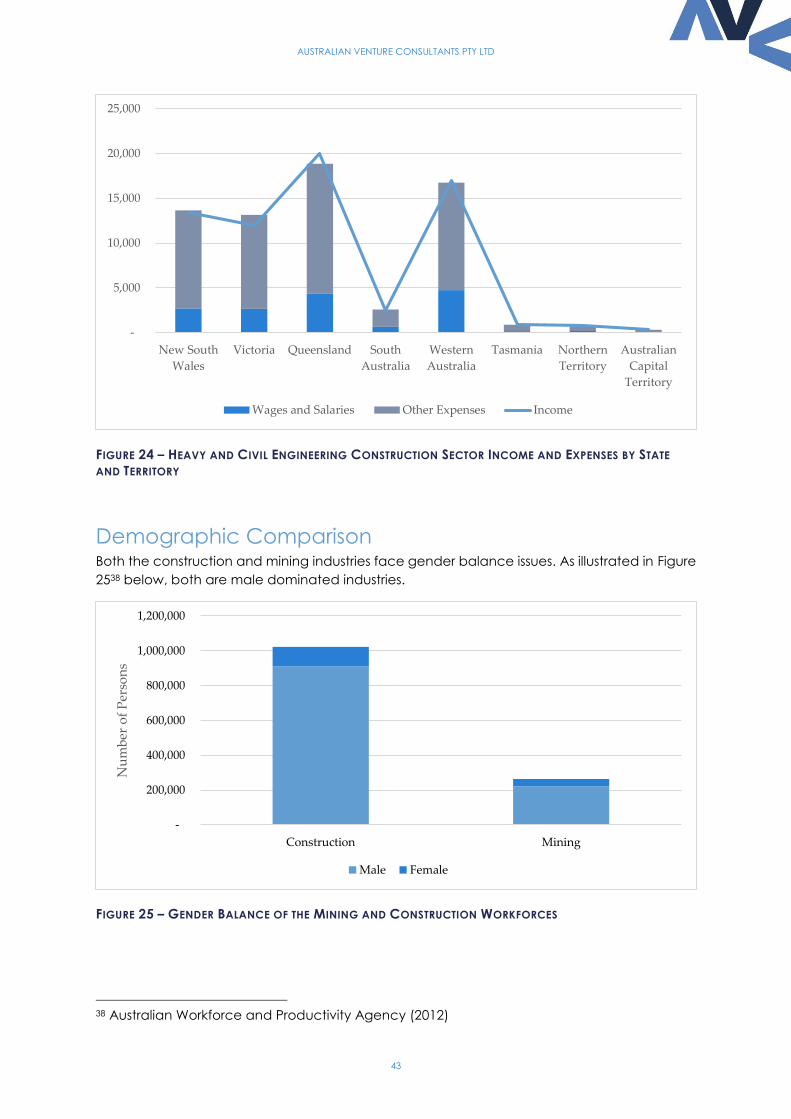

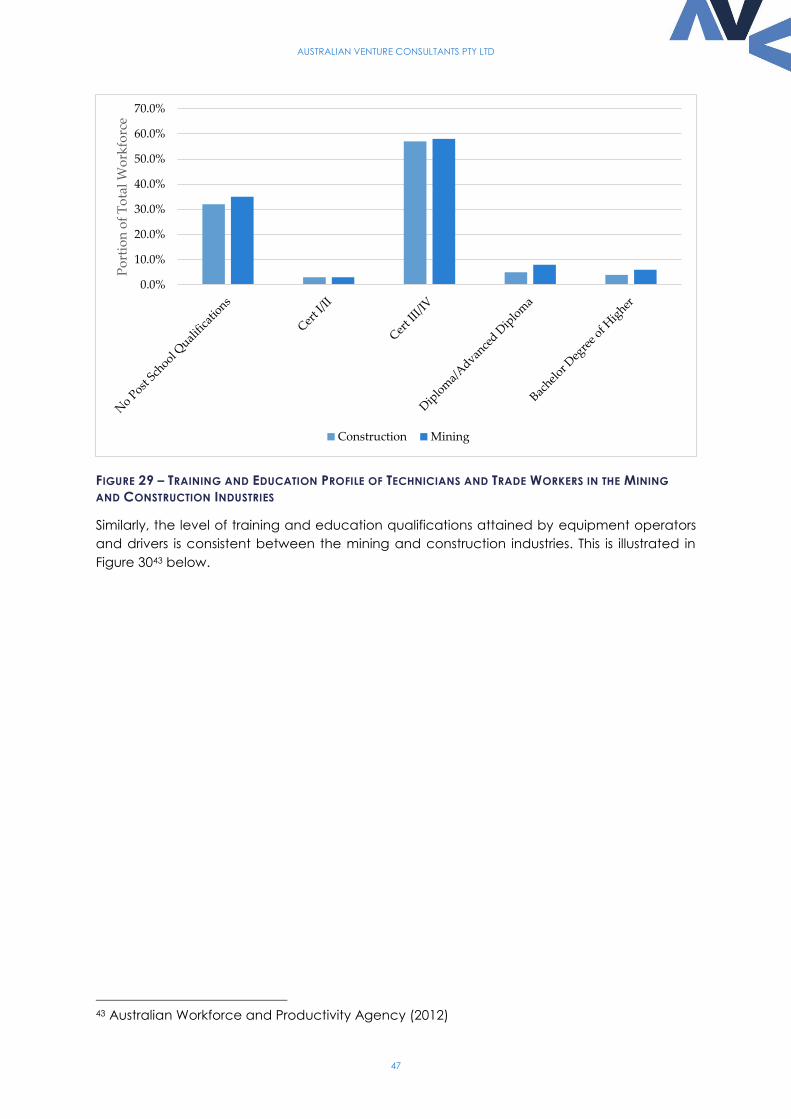

In terms of intensity of demand for skills the greatest commonality is in the roles of electricians

and earth moving plant operators, as well as speciality areas of construction and engineering

managers. However, the demand for these skills during the operational phase of the projects

is very limited compared to the opportunities in the wider construction industry for these

occupations.

There is likely to be common demand for other occupations such as structural steel and

welding trades, truck drivers and plumbers. However, the operational resources projects tend

to employ fewer numbers of persons in these roles and many functions such as drillers and shot

firers who comprise a large component of the mining industry workforce are specialist skills.

Furthermore, many of the general trades deployed at operational resources projects have a

specialist focus.

Lessons from the Recent Construction Phase

Over the past decade resources project development costs in Australia, and particularly in

Western Australia, do not compare well with other jurisdictions. A range of factors have

contributed to the unfavourable cost environment in Australia, including the evolution of the

mechanism that resources companies use to manage project construction. Necessary

increased focus on OHS and environment along with a need to integrate effectively with larger

EPCM teams on large projects, means that the internal project management teams within

resources companies have grown considerably in size and cost.

Similarly at the construction site, enhanced supervision and OHS requirements have seen

construction teams grow in size. Fragmentation of OHS training providers across sites often

results in a lack of accreditation of existing OHS training for site induction, resulting in delays of

several hours or more to get new contractors onto site.

Implications for Skills, Training and Education

As a result of the structural and cultural differences between the construction workforce and

the operational workforce there is unlikely to be a substantive market for supplementary

training designed to transition resources project construction workers to operational roles in

projects. The main opportunities for training and education are acquiring a deeper

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

9

understanding of the root cause of the productivity penalties associated with the investment

phase over the past decade and integrating those learnings in training and education

programs targeted at the resources and construction industries. Key areas in which learnings

could be gained include investment cycle management, project management, complex

remote project construction and OHS induction.

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

10

Background and Purpose

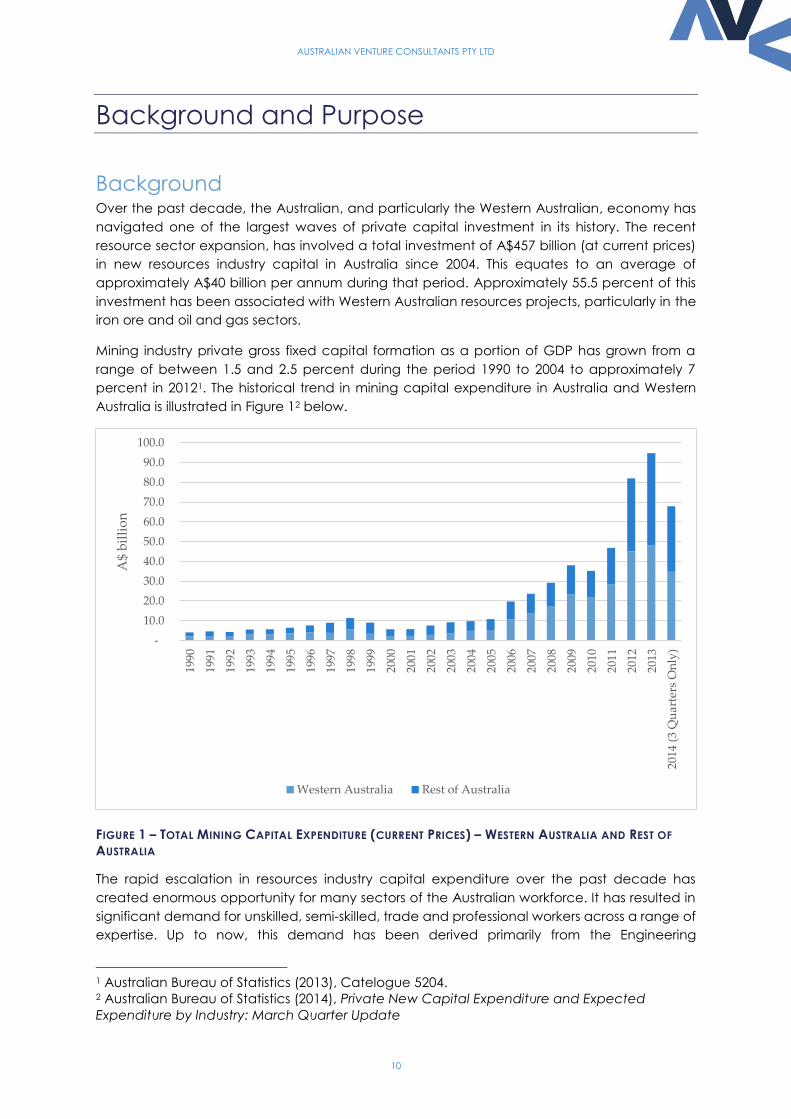

Background Over the past decade, the Australian, and particularly the Western Australian, economy has

navigated one of the largest waves of private capital investment in its history. The recent

resource sector expansion, has involved a total investment of A$457 billion (at current prices)

in new resources industry capital in Australia since 2004. This equates to an average of

approximately A$40 billion per annum during that period. Approximately 55.5 percent of this

investment has been associated with Western Australian resources projects, particularly in the

iron ore and oil and gas sectors.

Mining industry private gross fixed capital formation as a portion of GDP has grown from a

range of between 1.5 and 2.5 percent during the period 1990 to 2004 to approximately 7

percent in 20121. The historical trend in mining capital expenditure in Australia and Western

Australia is illustrated in Figure 12 below.

FIGURE 1 – TOTAL MINING CAPITAL EXPENDITURE (CURRENT PRICES) – WESTERN AUSTRALIA AND REST OF

AUSTRALIA

The rapid escalation in resources industry capital expenditure over the past decade has

created enormous opportunity for many sectors of the Australian workforce. It has resulted in

significant demand for unskilled, semi-skilled, trade and professional workers across a range of

expertise. Up to now, this demand has been derived primarily from the Engineering

1 Australian Bureau of Statistics (2013), Catelogue 5204. 2 Australian Bureau of Statistics (2014), Private New Capital Expenditure and Expected

Expenditure by Industry: March Quarter Update

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

(3

Qu

arte

rs O

nly

)

A$

bil

lio

n

Western Australia Rest of Australia

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

11

Procurement and Construction Managers (EPCMs) and their construction industry contractors

and subcontractors that give effect to the substantial construction projects that have

constituted the recent expansion of the Australian resources industry. As the new and

expanded resources industry project transition to an operational phase, opportunities will be

created for skillsets that are aligned with the operational requirements of these projects.

The recent investment phase has resulted in considerable short-to-medium term labour

migration to locations where the investment in new resources projects is occurring, particularly

Western Australia and Queensland, as well as rapid growth in the domestic Fly-In-Fly-Out (FIFO)

workforce and temporary migrant workers via 457 subclass visas.

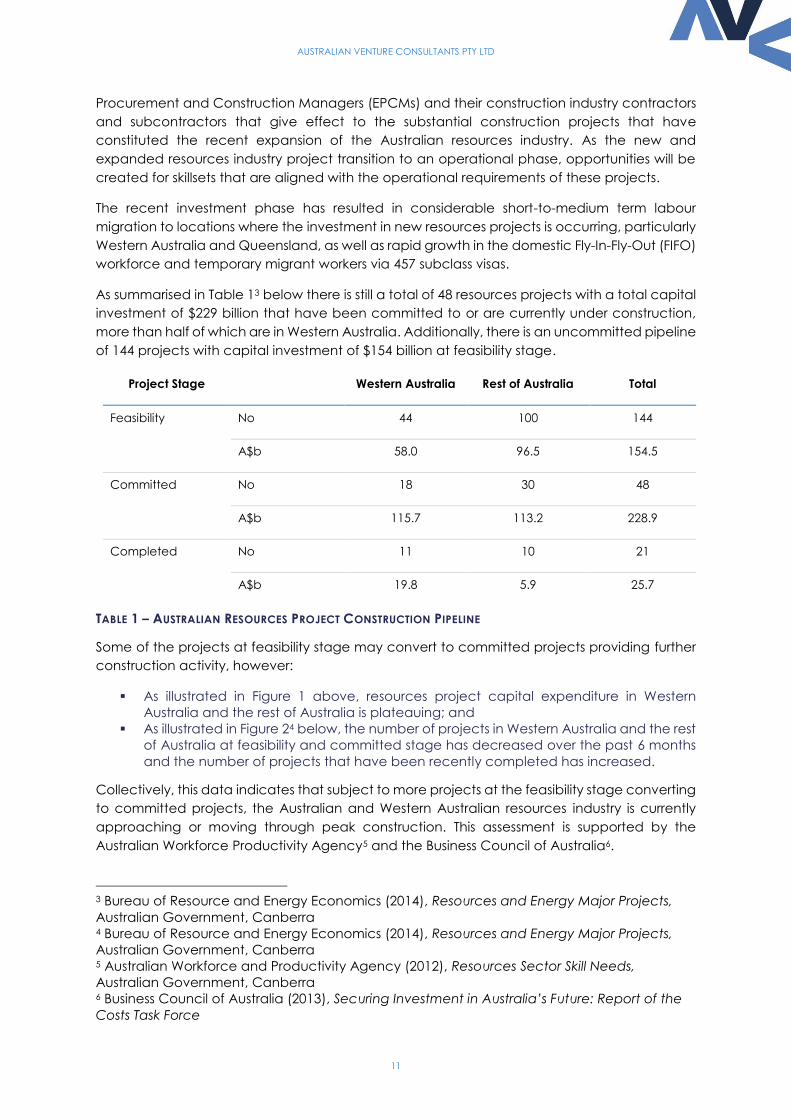

As summarised in Table 13 below there is still a total of 48 resources projects with a total capital

investment of $229 billion that have been committed to or are currently under construction,

more than half of which are in Western Australia. Additionally, there is an uncommitted pipeline

of 144 projects with capital investment of $154 billion at feasibility stage.

Project Stage Western Australia Rest of Australia Total

Feasibility No 44 100 144

A$b 58.0 96.5 154.5

Committed No 18 30 48

A$b 115.7 113.2 228.9

Completed No 11 10 21

A$b 19.8 5.9 25.7

TABLE 1 – AUSTRALIAN RESOURCES PROJECT CONSTRUCTION PIPELINE

Some of the projects at feasibility stage may convert to committed projects providing further

construction activity, however:

As illustrated in Figure 1 above, resources project capital expenditure in Western

Australia and the rest of Australia is plateauing; and

As illustrated in Figure 24 below, the number of projects in Western Australia and the rest

of Australia at feasibility and committed stage has decreased over the past 6 months

and the number of projects that have been recently completed has increased.

Collectively, this data indicates that subject to more projects at the feasibility stage converting

to committed projects, the Australian and Western Australian resources industry is currently

approaching or moving through peak construction. This assessment is supported by the

Australian Workforce Productivity Agency5 and the Business Council of Australia6.

3 Bureau of Resource and Energy Economics (2014), Resources and Energy Major Projects,

Australian Government, Canberra 4 Bureau of Resource and Energy Economics (2014), Resources and Energy Major Projects,

Australian Government, Canberra 5 Australian Workforce and Productivity Agency (2012), Resources Sector Skill Needs,

Australian Government, Canberra 6 Business Council of Australia (2013), Securing Investment in Australia’s Future: Report of the

Costs Task Force

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

12

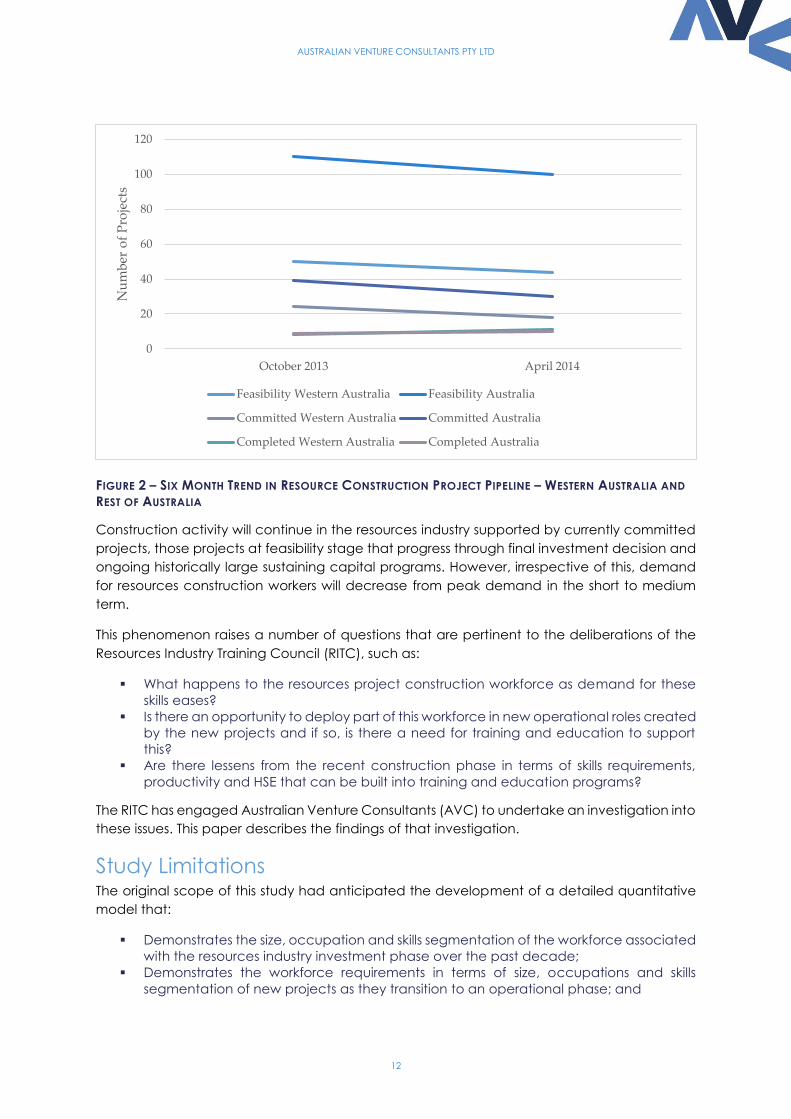

FIGURE 2 – SIX MONTH TREND IN RESOURCE CONSTRUCTION PROJECT PIPELINE – WESTERN AUSTRALIA AND

REST OF AUSTRALIA

Construction activity will continue in the resources industry supported by currently committed

projects, those projects at feasibility stage that progress through final investment decision and

ongoing historically large sustaining capital programs. However, irrespective of this, demand

for resources construction workers will decrease from peak demand in the short to medium

term.

This phenomenon raises a number of questions that are pertinent to the deliberations of the

Resources Industry Training Council (RITC), such as:

What happens to the resources project construction workforce as demand for these

skills eases?

Is there an opportunity to deploy part of this workforce in new operational roles created

by the new projects and if so, is there a need for training and education to support

this?

Are there lessens from the recent construction phase in terms of skills requirements,

productivity and HSE that can be built into training and education programs?

The RITC has engaged Australian Venture Consultants (AVC) to undertake an investigation into

these issues. This paper describes the findings of that investigation.

Study Limitations The original scope of this study had anticipated the development of a detailed quantitative

model that:

Demonstrates the size, occupation and skills segmentation of the workforce associated

with the resources industry investment phase over the past decade;

Demonstrates the workforce requirements in terms of size, occupations and skills

segmentation of new projects as they transition to an operational phase; and

0

20

40

60

80

100

120

October 2013 April 2014

Nu

mb

er o

f P

roje

cts

Feasibility Western Australia Feasibility Australia

Committed Western Australia Committed Australia

Completed Western Australia Completed Australia

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

13

Identifies any workforce transition relationship between the construction and

operational workforces of these projects.

It was also intended to identify examples in other industries where a major construction

workforce had transitioned to an operational workforce.

For two reasons, the study encountered significant difficulty in developing this model and

providing these examples. Firstly attaining detailed project employment data from companies,

EPCMs and contractors proved challenging. This was likely partly the result of political

sensitivities associated with aspects of workforce transition, but also as a result of the practical

difficulties in collecting and providing this data. Secondly, as discussed throughout this report,

the incidence of worker transition from construction roles to operational roles is very low,

primarily because the culture and lifestyle choices of construction workers is very different to

that of operational workers, as are most of the skills requirements.

The study has endeavoured to address this limitation by providing adequately supported

anecdotal evidence of the observations made in the study and by exploring other issues

associated with the recent investment phase and transition to operations that might be of

interest to the RITC, such as opportunities to focus future training and education on issues that

might improve construction project productivity.

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

14

Current Resource Project Construction

Pipeline and Workforce Estimates

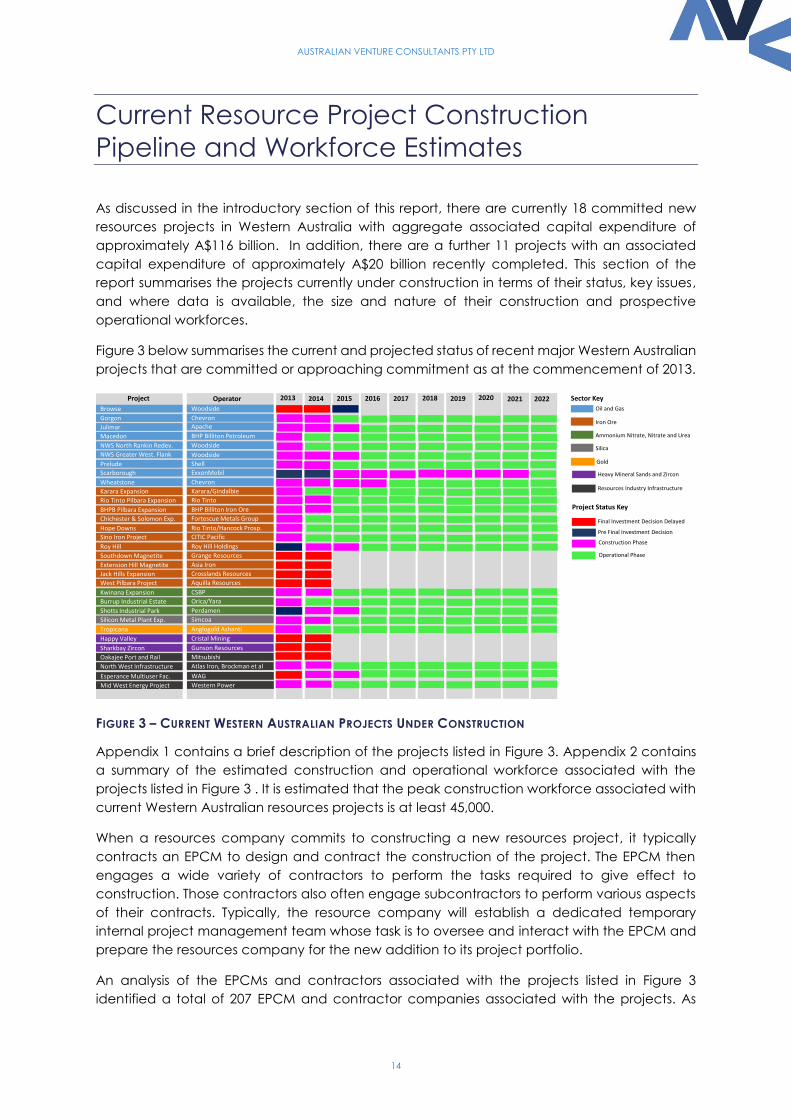

As discussed in the introductory section of this report, there are currently 18 committed new

resources projects in Western Australia with aggregate associated capital expenditure of

approximately A$116 billion. In addition, there are a further 11 projects with an associated

capital expenditure of approximately A$20 billion recently completed. This section of the

report summarises the projects currently under construction in terms of their status, key issues,

and where data is available, the size and nature of their construction and prospective

operational workforces.

Figure 3 below summarises the current and projected status of recent major Western Australian

projects that are committed or approaching commitment as at the commencement of 2013.

FIGURE 3 – CURRENT WESTERN AUSTRALIAN PROJECTS UNDER CONSTRUCTION

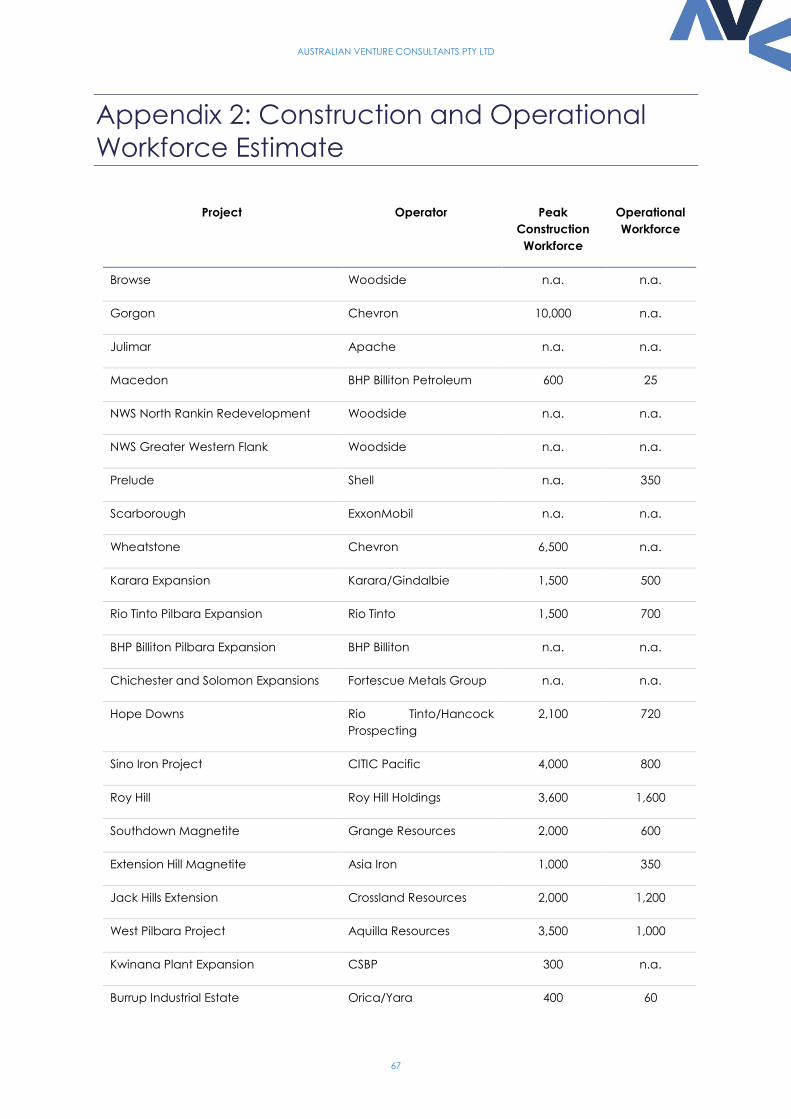

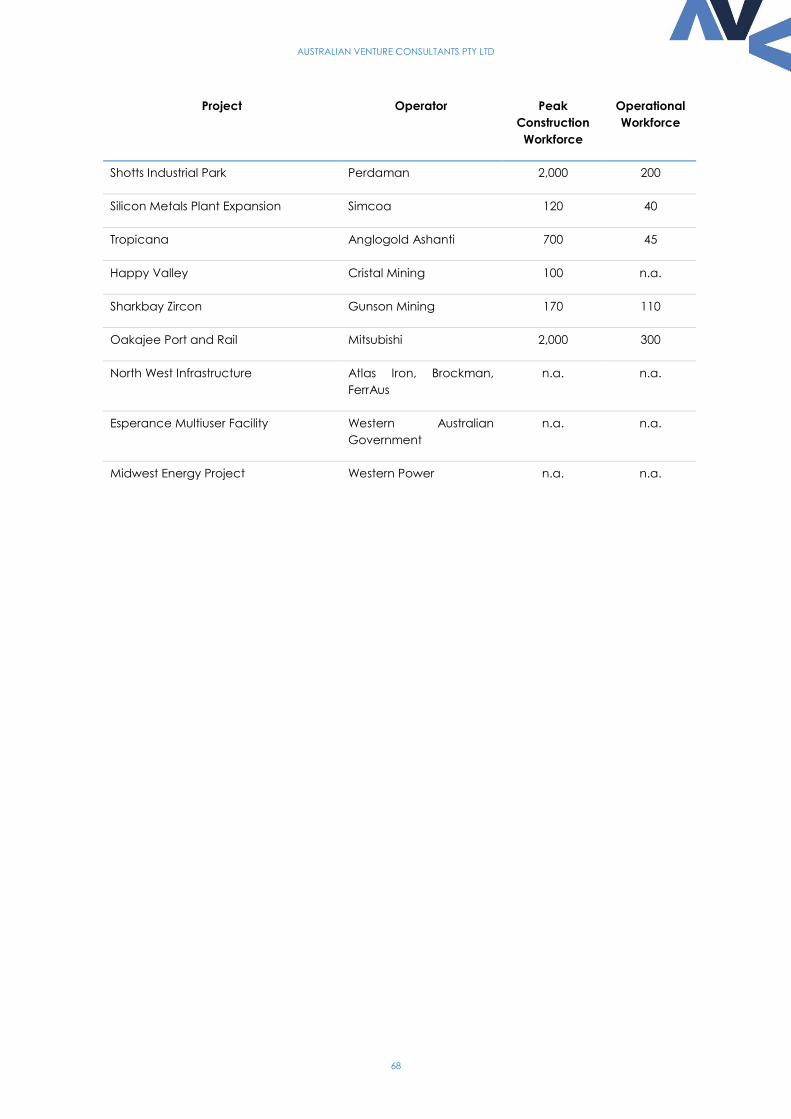

Appendix 1 contains a brief description of the projects listed in Figure 3. Appendix 2 contains

a summary of the estimated construction and operational workforce associated with the

projects listed in Figure 3 . It is estimated that the peak construction workforce associated with

current Western Australian resources projects is at least 45,000.

When a resources company commits to constructing a new resources project, it typically

contracts an EPCM to design and contract the construction of the project. The EPCM then

engages a wide variety of contractors to perform the tasks required to give effect to

construction. Those contractors also often engage subcontractors to perform various aspects

of their contracts. Typically, the resource company will establish a dedicated temporary

internal project management team whose task is to oversee and interact with the EPCM and

prepare the resources company for the new addition to its project portfolio.

An analysis of the EPCMs and contractors associated with the projects listed in Figure 3

identified a total of 207 EPCM and contractor companies associated with the projects. As

Browse

Gorgon

Julimar

Macedon

NWS North Rankin Redev.

NWS Greater West. Flank

Prelude

Scarborough

Wheatstone

Karara Expansion

Rio Tinto Pilbara Expansion

BHPB Pilbara Expansion

Chichester & Solomon Exp.

Hope Downs

Sino Iron Project

Roy Hill

Southdown Magnetite

Extension Hill Magnetite

Jack Hills Expansion

West Pilbara Project

Kwinana Expansion

Burrup Industrial Estate

Shotts Industrial Park

Silicon Metal Plant Exp.

Tropicana

Happy Valley

Sharkbay Zircon

Oakajee Port and Rail

North West Infrastructure

Project

Woodside

ChevronApache

BHP Billiton Petroleum

Woodside

Woodside

Shell

ExxonMobil

Chevron

Karara/Gindalbie

Rio Tinto

BHP Billiton Iron Ore

Fortescue Metals Group

Rio Tinto/Hancock Prosp.

CITIC Pacific

Roy Hill Holdings

Grange Resources

Asia Iron

Crosslands Resources

Aquilla Resources

CSBP

Orica/Yara

Perdamen

Simcoa

Anglogold Ashanti

Cristal Mining

Gunson Resources

Mitsubishi

Atlas Iron, Brockman et al

Operator 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 Sector Key

Oil and Gas

Iron Ore

Ammonium Nitrate, Nitrate and Urea

Silica

Gold

Heavy Mineral Sands and Zircon

Resources Industry Infrastructure

Project Status Key

Final Investment Decision Delayed

Construction Phase

Operational Phase

Pre Final Investment Decision

Esperance Multiuser Fac.

Mid West Energy Project

WAG

Western Power

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

15

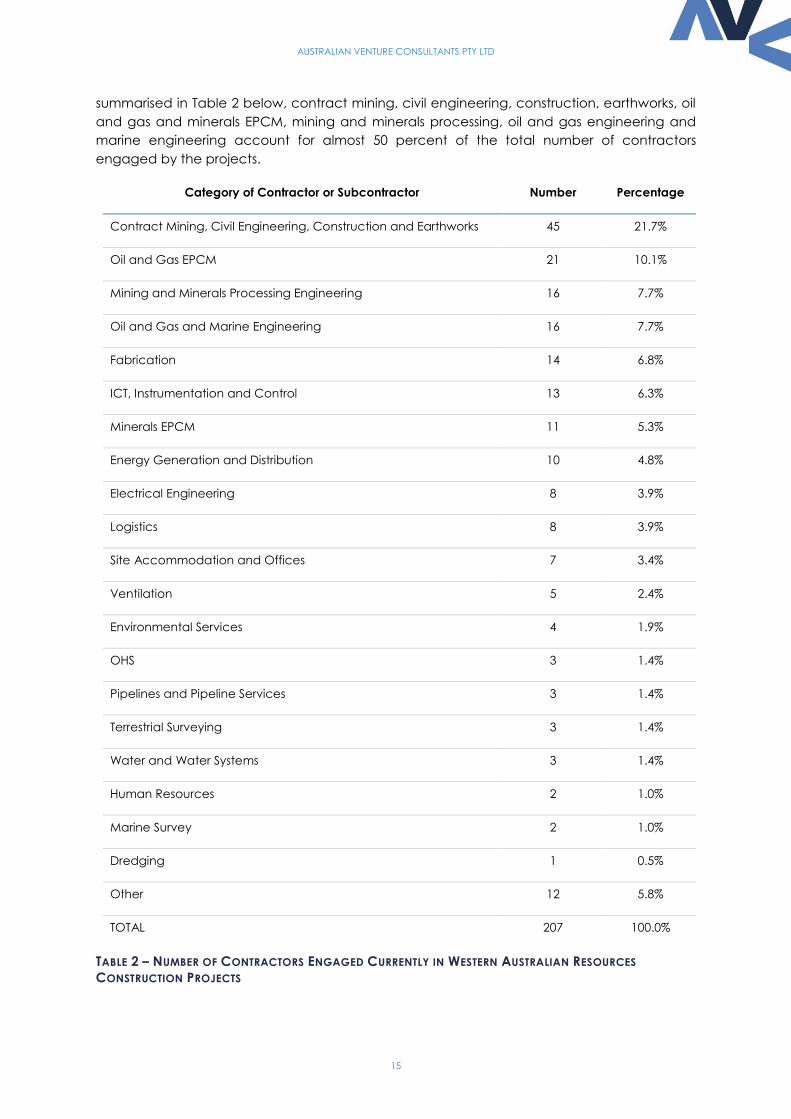

summarised in Table 2 below, contract mining, civil engineering, construction, earthworks, oil

and gas and minerals EPCM, mining and minerals processing, oil and gas engineering and

marine engineering account for almost 50 percent of the total number of contractors

engaged by the projects.

Category of Contractor or Subcontractor Number Percentage

Contract Mining, Civil Engineering, Construction and Earthworks 45 21.7%

Oil and Gas EPCM 21 10.1%

Mining and Minerals Processing Engineering 16 7.7%

Oil and Gas and Marine Engineering 16 7.7%

Fabrication 14 6.8%

ICT, Instrumentation and Control 13 6.3%

Minerals EPCM 11 5.3%

Energy Generation and Distribution 10 4.8%

Electrical Engineering 8 3.9%

Logistics 8 3.9%

Site Accommodation and Offices 7 3.4%

Ventilation 5 2.4%

Environmental Services 4 1.9%

OHS 3 1.4%

Pipelines and Pipeline Services 3 1.4%

Terrestrial Surveying 3 1.4%

Water and Water Systems 3 1.4%

Human Resources 2 1.0%

Marine Survey 2 1.0%

Dredging 1 0.5%

Other 12 5.8%

TOTAL 207 100.0%

TABLE 2 – NUMBER OF CONTRACTORS ENGAGED CURRENTLY IN WESTERN AUSTRALIAN RESOURCES

CONSTRUCTION PROJECTS

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

16

Transition from Construction to Operations

Project Development Cycle Once an in situ resource has been determined by a project proponent to exhibit size, grade,

reservoir (in the case of petroleum), geotechnical, mineralogy, access to infrastructure and

other key characteristics that adequately indicate there is a prima facie case for development

of that in situ resource, the general process for development commences with a feasibility

study (which may be preceded by a pre-feasibility study). A feasibility study will identify,

analyse and compare options for the development of the resource, based primarily on

technical and economic information that is readily available.

Should the feasibility study demonstrate a technically and economically feasible development

option that meets the project proponent’s internal hurdle rate and risk appetite, the project

will likely proceed to the Front-End-Engineering and Design (FEED) phase. If there are numerous

options for developing the project, an interim Basis-of-Design phase may be required to select

the most attractive development options upon which FEED will be based. FEED involves

evaluating technical options for different components of the preferred development

pathway, and the design of an engineering solution that has a cost contingency typically with

a maximum variance of 20 percent.

The end result of FEED is a bankable feasibility study (i.e. an investment case). This bankable

feasibility study then undergoes a rigorous internal decision process based on an exhaustive

range of operational, financial and strategic criteria, the end result of which is Final Investment

Decision (FID). At this point the resources company has committed to the project. The project

development process up to this point is usually primarily an internal process supported by

external expertise (including potentially the EPCM that may be contracted to manage the

construction phase).

The nature and quantum of skills required to construct a major resources project is very different

to the nature and quantum of skills required to operate a resources project. Very few, if any

resources companies have the resources required to construct a major new project. As such,

post-FID, a resources company will typically contract an EPCM to complete final detailed

design and procure the diverse construction goods and services required to complete the

construction project.

During this period, the resources company will establish an internal project management team

that will oversee and liaise with the EPCM throughout the construction phase. This team will be

comprised principally of project managers who are usually engineers with resources project

operational experience as well as human resources, Health Safety and Environment (HSE),

finance, legal/contract and administrative personnel.

As construction approaches completion, the project management team will often gradually

be replaced with an operational readiness team. The operational readiness team typically

includes senior operational, mining, process and HSE personnel who will form the leadership in

these areas for the project when it is operational, as well as leadership from the project

management team, internal technical expertise and corporate human resources functions

who will source the operational workforce from within the company and/or externally.

Once operational, most of the operational readiness team will convert into the operational

management team that will manage and lead the recruited operations workforce. The

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

17

project will continue to interact with the construction workforce from time to time for the

purposes of effecting sustaining capital investment, as well as ongoing maintenance.

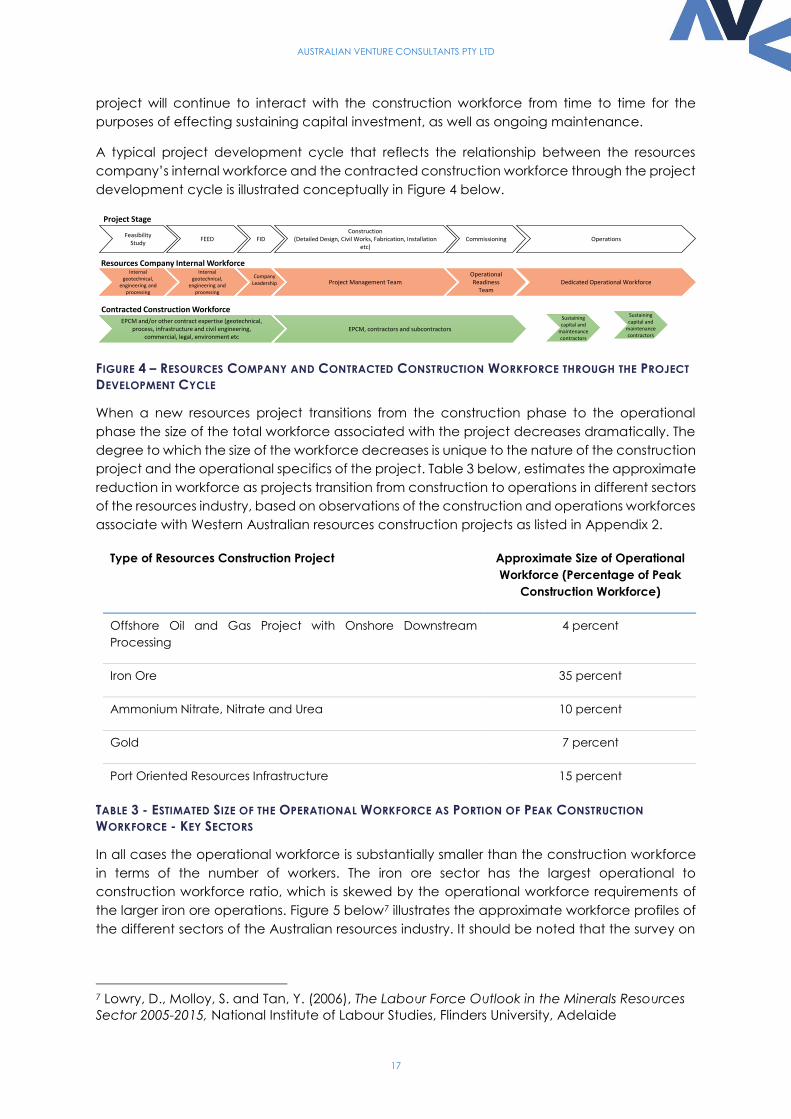

A typical project development cycle that reflects the relationship between the resources

company’s internal workforce and the contracted construction workforce through the project

development cycle is illustrated conceptually in Figure 4 below.

FIGURE 4 – RESOURCES COMPANY AND CONTRACTED CONSTRUCTION WORKFORCE THROUGH THE PROJECT

DEVELOPMENT CYCLE

When a new resources project transitions from the construction phase to the operational

phase the size of the total workforce associated with the project decreases dramatically. The

degree to which the size of the workforce decreases is unique to the nature of the construction

project and the operational specifics of the project. Table 3 below, estimates the approximate

reduction in workforce as projects transition from construction to operations in different sectors

of the resources industry, based on observations of the construction and operations workforces

associate with Western Australian resources construction projects as listed in Appendix 2.

Type of Resources Construction Project Approximate Size of Operational

Workforce (Percentage of Peak

Construction Workforce)

Offshore Oil and Gas Project with Onshore Downstream

Processing

4 percent

Iron Ore 35 percent

Ammonium Nitrate, Nitrate and Urea 10 percent

Gold 7 percent

Port Oriented Resources Infrastructure 15 percent

TABLE 3 - ESTIMATED SIZE OF THE OPERATIONAL WORKFORCE AS PORTION OF PEAK CONSTRUCTION

WORKFORCE - KEY SECTORS

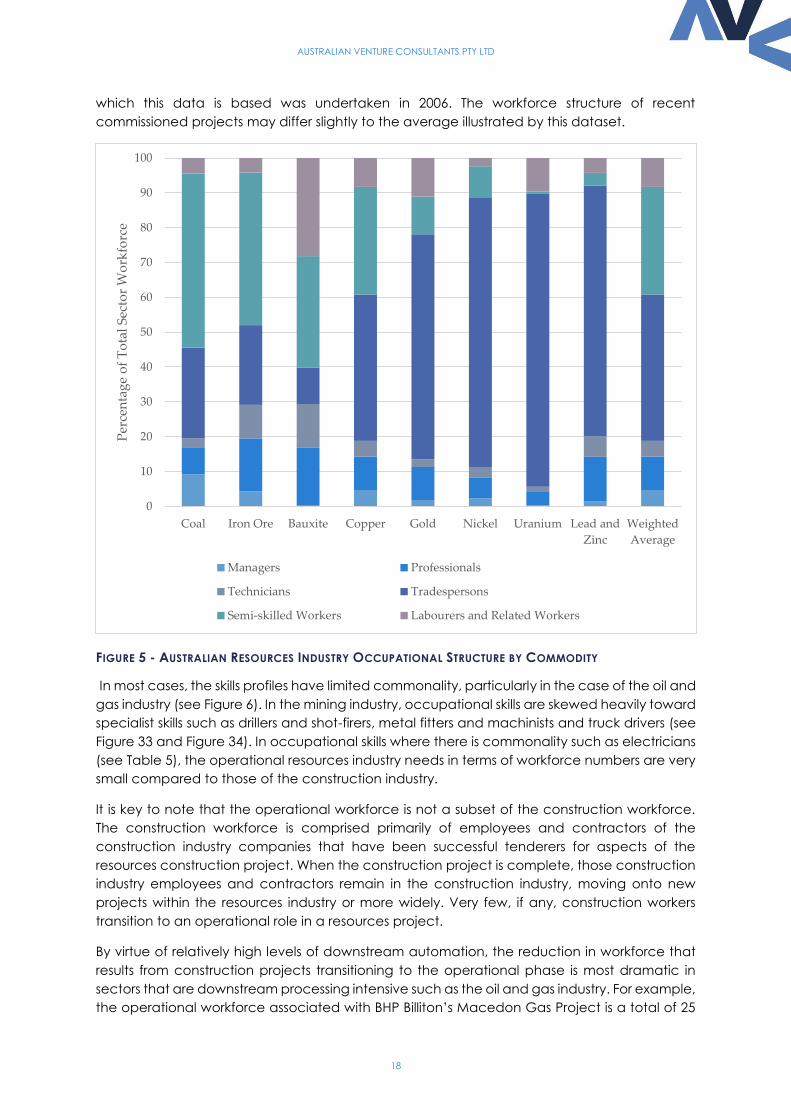

In all cases the operational workforce is substantially smaller than the construction workforce

in terms of the number of workers. The iron ore sector has the largest operational to

construction workforce ratio, which is skewed by the operational workforce requirements of

the larger iron ore operations. Figure 5 below7 illustrates the approximate workforce profiles of

the different sectors of the Australian resources industry. It should be noted that the survey on

7 Lowry, D., Molloy, S. and Tan, Y. (2006), The Labour Force Outlook in the Minerals Resources

Sector 2005-2015, National Institute of Labour Studies, Flinders University, Adelaide

Feasibility Study

FEED FIDConstruction

(Detailed Design, Civil Works, Fabrication, Installation etc)

Commissioning Operations

Internal geotechnical,

engineering and processing

Internal geotechnical,

engineering and processing

Project Management TeamOperational Readiness

TeamDedicated Operational Workforce

EPCM and/or other contract expertise (geotechnical, process, infrastructure and civil engineering,

commercial, legal, environment etc

CompanyLeadership

EPCM, contractors and subcontractors

Sustainingcapital and

maintenancecontractors

Sustainingcapital and

maintenancecontractors

Project Stage

Resources Company Internal Workforce

Contracted Construction Workforce

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

18

which this data is based was undertaken in 2006. The workforce structure of recent

commissioned projects may differ slightly to the average illustrated by this dataset.

FIGURE 5 - AUSTRALIAN RESOURCES INDUSTRY OCCUPATIONAL STRUCTURE BY COMMODITY

In most cases, the skills profiles have limited commonality, particularly in the case of the oil and

gas industry (see Figure 6). In the mining industry, occupational skills are skewed heavily toward

specialist skills such as drillers and shot-firers, metal fitters and machinists and truck drivers (see

Figure 33 and Figure 34). In occupational skills where there is commonality such as electricians

(see Table 5), the operational resources industry needs in terms of workforce numbers are very

small compared to those of the construction industry.

It is key to note that the operational workforce is not a subset of the construction workforce.

The construction workforce is comprised primarily of employees and contractors of the

construction industry companies that have been successful tenderers for aspects of the

resources construction project. When the construction project is complete, those construction

industry employees and contractors remain in the construction industry, moving onto new

projects within the resources industry or more widely. Very few, if any, construction workers

transition to an operational role in a resources project.

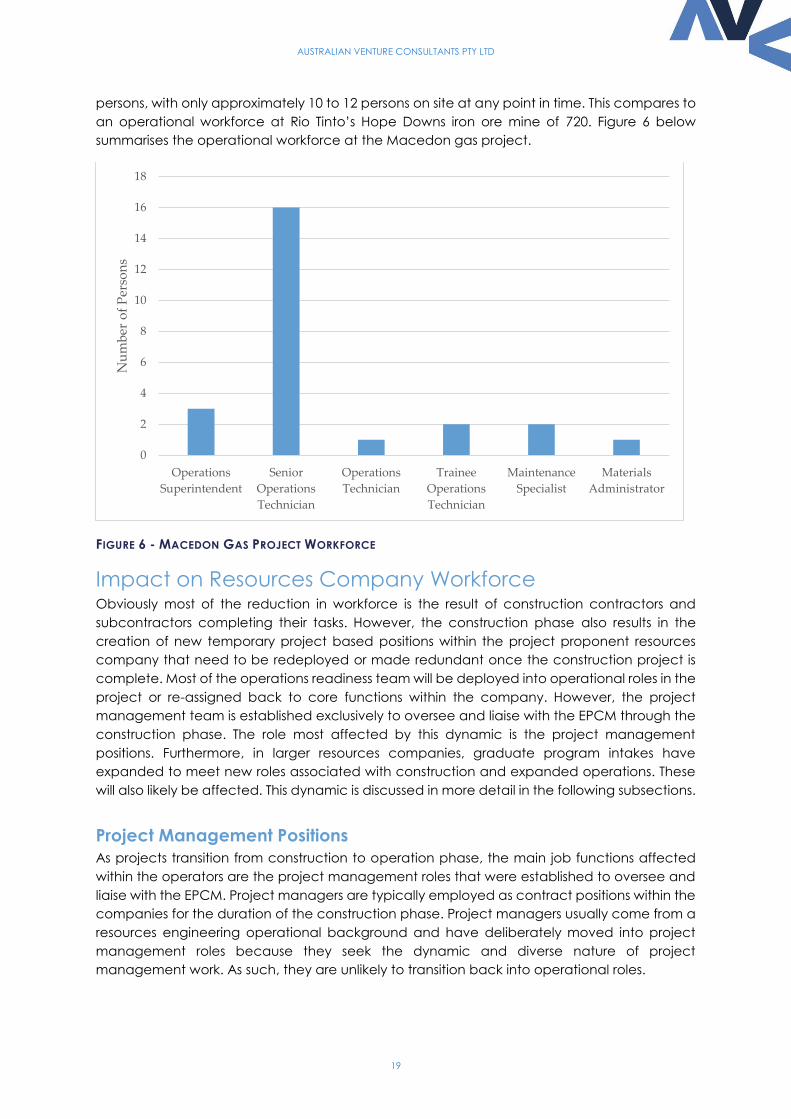

By virtue of relatively high levels of downstream automation, the reduction in workforce that

results from construction projects transitioning to the operational phase is most dramatic in

sectors that are downstream processing intensive such as the oil and gas industry. For example,

the operational workforce associated with BHP Billiton’s Macedon Gas Project is a total of 25

0

10

20

30

40

50

60

70

80

90

100

Coal Iron Ore Bauxite Copper Gold Nickel Uranium Lead and

Zinc

Weighted

Average

Per

cen

tag

e o

f T

ota

l S

ecto

r W

ork

forc

e

Managers Professionals

Technicians Tradespersons

Semi-skilled Workers Labourers and Related Workers

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

19

persons, with only approximately 10 to 12 persons on site at any point in time. This compares to

an operational workforce at Rio Tinto’s Hope Downs iron ore mine of 720. Figure 6 below

summarises the operational workforce at the Macedon gas project.

FIGURE 6 - MACEDON GAS PROJECT WORKFORCE

Impact on Resources Company Workforce Obviously most of the reduction in workforce is the result of construction contractors and

subcontractors completing their tasks. However, the construction phase also results in the

creation of new temporary project based positions within the project proponent resources

company that need to be redeployed or made redundant once the construction project is

complete. Most of the operations readiness team will be deployed into operational roles in the

project or re-assigned back to core functions within the company. However, the project

management team is established exclusively to oversee and liaise with the EPCM through the

construction phase. The role most affected by this dynamic is the project management

positions. Furthermore, in larger resources companies, graduate program intakes have

expanded to meet new roles associated with construction and expanded operations. These

will also likely be affected. This dynamic is discussed in more detail in the following subsections.

Project Management Positions

As projects transition from construction to operation phase, the main job functions affected

within the operators are the project management roles that were established to oversee and

liaise with the EPCM. Project managers are typically employed as contract positions within the

companies for the duration of the construction phase. Project managers usually come from a

resources engineering operational background and have deliberately moved into project

management roles because they seek the dynamic and diverse nature of project

management work. As such, they are unlikely to transition back into operational roles.

0

2

4

6

8

10

12

14

16

18

Operations

Superintendent

Senior

Operations

Technician

Operations

Technician

Trainee

Operations

Technician

Maintenance

Specialist

Materials

Administrator

Nu

mb

er o

f P

erso

ns

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

20

Some project managers will likely move onto sustaining capital investment projects within the

companies, particularly those who are highly skilled and therefore a target for retention within

the companies. Others will potentially be recruited by project management teams in other

companies, or by the EPCMs seeking experienced project managers that understand project

proponent decision-making dynamics.

Operational Workforce

New projects will require a new operational workforce. Some of the new operational positions

will be filled internally if the company has existing operational projects. However, the vast

majority will likely be newly recruited to the company. Completing a construction project on

time is a key criteria for construction project performance, which in turn partly motivates

deploying the quantum of resources (within cost constraints) that is required to mitigate the

risk of scheduling slippages. However, once a project is operational, productivity becomes a

key performance measure. As a result, resources companies will seek to optimise labour

productivity when recruiting and managing the operations workforce, perhaps more so than

in the case of the construction workforce. This involves ensuring that workers employed in

longer-term operational roles have:

An optimal range and level of skills for the role;

Workplace values and attitudes that are consistent with the company’s and the

project’s culture, particularly with respect to work ethic and OHS;

Values, attitudes and capacity that motivate them to seek longer-term employment in

order to mitigate the productivity penalties associated with staff turnover;

Characteristics that are aligned with the company’s human resources KPIs such as

diversity.

Graduate, Apprentice and Trainee Positions

Many companies in the resources and construction sector have grown graduate,

apprenticeship and trainee programs in response to internal demand generated by the rapid

escalation of construction activity in the resources industry.

During the recent resources industry investment phase, graduate programs have expanded in

many companies as these companies sought to grow the pool of professional staff available

to them. In many cases, the transition from construction to operational phase has seen a

decrease in internal activity, rendering it difficult to find places for these graduates outside of

the graduate program. This may result in a surplus of junior mining executives in the market

place in the short term until the graduate program intakes equalise.

While many companies have expanded apprentice and trainee programs on the same basis,

there is less of a challenge in the market for trade persons, apprentices and trainees. The

relative size of the pool of demand for trade skills within the resources sector and the wider

construction industry means that there is likely to be greater opportunity in the marketplace

for apprentices and trainees that have been trained on resources construction projects.

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

21

Impact on the Construction Workforce

Managing Workforce Requirements

By virtue of the sheer size of the construction workforce associated with resources project

capital investment since 2004, as the projects transition to an operational phase there will

inevitably be reduction in the demand for skilled and unskilled labour that has been associated

with the construction of these project. This will likely result in a surplus of many construction skills

in the labour market in the short-term. This is most likely not being felt in Western Australia to

any great degree as yet because the more expensive FIFO workers (Eastern States and

Overseas) will naturally be the first to be impacted. However, much of this labour will move

onto other projects within the resources industry, but principally in other sectors of the

economy.

Importantly, increasingly this construction workforce will bring to new projects both within the

resources industry and the wider economy new skills, particularly in remote complex

construction and OHS, enhancing the capability of the Australian construction industry.

Other Resources Industry Projects

The construction of other resources projects such as Roy Hill will absorb some of the

construction workforce as it is released from other projects and other projects in the pipeline

may graduate to construction providing further opportunity in resources project construction.

Additionally, there are significant sustaining capital programs due to commence. For example,

BHP Billiton Iron Ore has an estimated A$2.0 billion of sustaining capital investment in its pipeline.

These programs will also absorb some of the construction workforce as it is released from

projects currently under construction.

Other Construction Market Opportunities

The construction workforce is not resources project specific. As discussed in a subsequent

section of this report, with the exception of the heavy and civil engineering sector, where

mining industry projects account for approximately 38 percent of primary contracting

revenue, mining industry construction projects only account for between 5 and 9 percent of

revenue in other sectors of the construction industry. The Australian construction industry

employs a total of 950,000 people, of which only 16 percent are employed by the sector most

dependent on mining industry projects.

Multi-sector contractors have the luxury of being able to draw employees from sectors where

conditions are softer and redeploy them in sectors where there is stronger demand. This has

been the case with the recent demand for resources project construction. As the resources

project construction market softens, these contractors will redeploy the workforce in markets

where there is growing demand. Interestingly, where this is happening, contractors are

reporting a transfer of improved OHS skills to non-resources projects. As discussed in a following

subsection, the Commonwealth Government’s National Infrastructure Program stands to be a

major beneficiary of this phenomenon.

In terms of civil construction, the main markets where skills will be redeployed are the residential

and non-residential construction markets and the infrastructure construction market. In the

case of fabrication skills, defence force contracts are likely to absorb some of the released

skills.

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

22

Residential and Non-residential Construction Markets

Based on record low interest rates, the Australian Construction Industry Forum is expecting total

residential building expenditure to grow at an average annual growth rate of 2.3 percent

between 2013-14 and 2022-23, with relatively strong growth in the short term, moderating by

around 2016-17 to 2019-20. Residential starts are expected to peak at approximately 185,000

new dwellings by 2017-188.

Non-residential building expenditure is projected to grow at an average rate of 1.3 percent

per annum from approximately $34 billion in 2012-13 to just below $40 billion by 2022-239.

Increased employment opportunities in both the residential and non-residential construction

market will assist in facilitating the movement of skilled labour.

National Infrastructure Program

The 2013 national infrastructure priority list sets outs priorities for Australia’s infrastructure

investment portfolio. A total of 79 proposals were submitted to Infrastructure Australia by state

and territory governments for inclusion on the 2013 priority list with an estimated cost of

approximately $80 billion. Of these, 34 were included on the priority list with an estimated value

of $24 to $27 billion. Appendix 3 contains a list of projects submitted to Infrastructure Australia

in 2012-1310.

The majority of these projects are major transport projects including road and port projects.

This is supported by a 2014-15 Federal Government budget commitment of A$50 billion for vital

transport infrastructure. Significant investment in, particularly road and port infrastructure by

state, territory and the Federal Government will create construction based employment

opportunities.

Australian Defence Force

Over the next decade, the Australian Government is planning a substantial increase in

Australian Defence Force (ADF) acquisitions across all services, at an estimated cost of more

than $200 billion11. The Defence Materiel Organisation (DMO) estimates that over the next 10

years, approximately 53 percent of its total acquisition and sustainment investment will be

spent in Australia. Over the same period, an estimated 37 percent of capital equipment

acquisition and sustainment will be spent on domestic activity, while approximately 70 percent

of the Australian Defence Force (ADF) sustainment expenditure will be spent in Australia12.

ADF related industries include shipbuilding and repair, boatbuilding and repair, aircraft

manufacturing and repair, fabricated metal product, explosive manufacturing and air space

transport, all of which are fabrication intensive. However, some Defence materiel supply also

comes from the construction sector, including businesses engaged in the construction of

8 Australian Construction Industry Forum (2014), ACIF Forecasts for Residential Building 9 Australian Construction Industry Forum (2014), ACIF Forecasts for Residential Building 10 Infrastructure Australia (2013), National Infrastructure Plan, Australian Government,

Canberra 11 Skills Australia (2012), Defence Industry Workforce Strategy: Background Paper, Australian

Government 12 Skills Australia (2012), Building Australia’s Defence Supply Capabilities: Main Report for the

Defence Industry Workforce Strategy, Australian Government, Canberra

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

23

buildings and other civil engineering structures, additions, alterations, reconstruction,

installation and maintenance and repairs of other buildings13.

There is significant commonality between some of Australia’s largest defence contractors and

contractors that played a prominent role in the recent Western Australian resources industry

construction phase14 and it is highly probable that workers from these contractors will be

transitioned to defence contracts related employment.

Transition to Operational Roles

Very few resources project construction workers transition to operational roles with projects.

While there is some commonality of skills and that commonality could potentially be widened

through additional supplementary training, the structure and culture of the construction

workforce is such that most construction workers do not desire operational roles. This is

discussed in more detail in a later section of this report.

13 Skills Australia (2012), Defence Industry Workforce Strategy: Background Paper, Australian

Government 14 Skills Australia (2012), Defence Industry Workforce Strategy: Background Paper, Australian

Government

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

24

Resources Project Construction Workforce

Dynamics

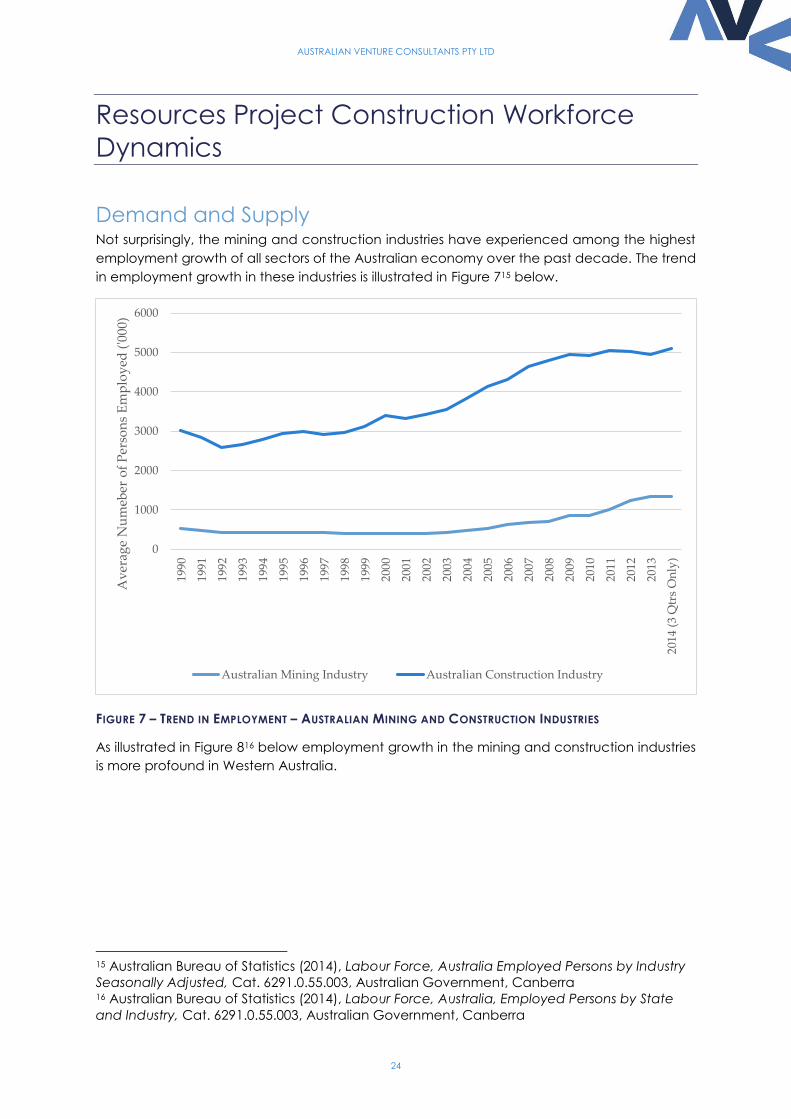

Demand and Supply Not surprisingly, the mining and construction industries have experienced among the highest

employment growth of all sectors of the Australian economy over the past decade. The trend

in employment growth in these industries is illustrated in Figure 715 below.

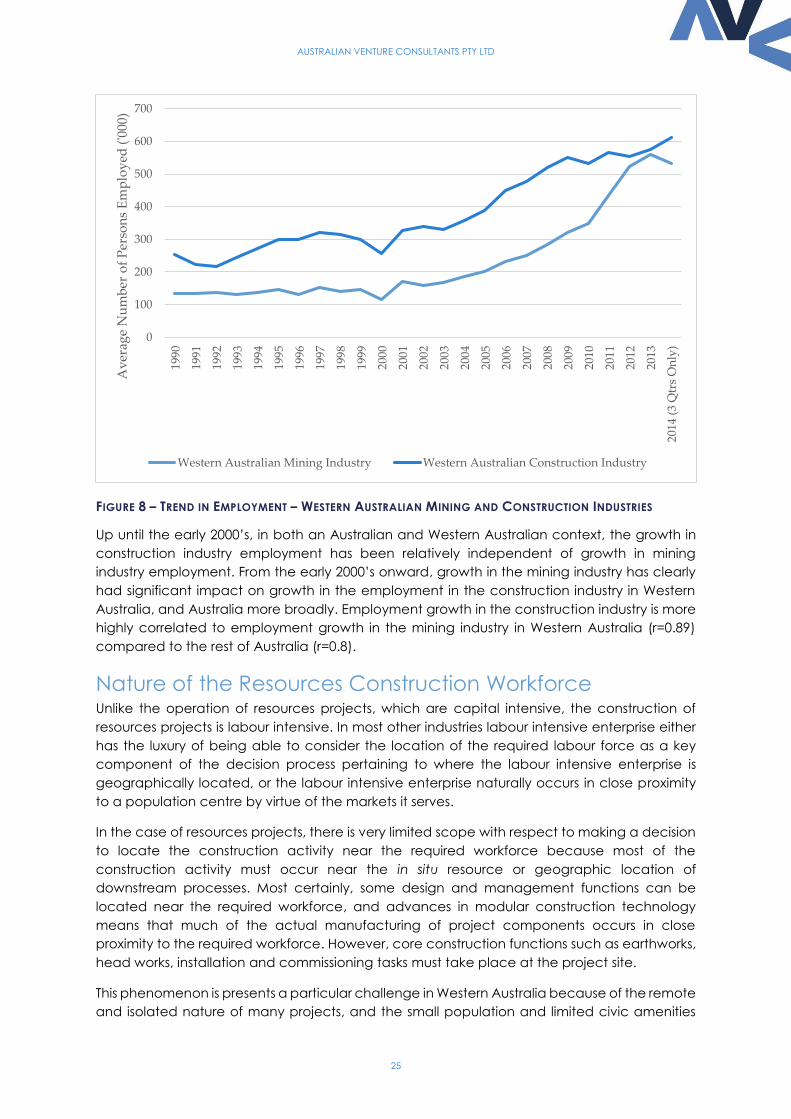

FIGURE 7 – TREND IN EMPLOYMENT – AUSTRALIAN MINING AND CONSTRUCTION INDUSTRIES

As illustrated in Figure 816 below employment growth in the mining and construction industries

is more profound in Western Australia.

15 Australian Bureau of Statistics (2014), Labour Force, Australia Employed Persons by Industry

Seasonally Adjusted, Cat. 6291.0.55.003, Australian Government, Canberra 16 Australian Bureau of Statistics (2014), Labour Force, Australia, Employed Persons by State

and Industry, Cat. 6291.0.55.003, Australian Government, Canberra

0

1000

2000

3000

4000

5000

6000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

(3

Qtr

s O

nly

)

Av

erag

e N

um

eber

of

Per

son

s E

mp

loy

ed (

'000

)

Australian Mining Industry Australian Construction Industry

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

25

FIGURE 8 – TREND IN EMPLOYMENT – WESTERN AUSTRALIAN MINING AND CONSTRUCTION INDUSTRIES

Up until the early 2000’s, in both an Australian and Western Australian context, the growth in

construction industry employment has been relatively independent of growth in mining

industry employment. From the early 2000’s onward, growth in the mining industry has clearly

had significant impact on growth in the employment in the construction industry in Western

Australia, and Australia more broadly. Employment growth in the construction industry is more

highly correlated to employment growth in the mining industry in Western Australia (r=0.89)

compared to the rest of Australia (r=0.8).

Nature of the Resources Construction Workforce Unlike the operation of resources projects, which are capital intensive, the construction of

resources projects is labour intensive. In most other industries labour intensive enterprise either

has the luxury of being able to consider the location of the required labour force as a key

component of the decision process pertaining to where the labour intensive enterprise is

geographically located, or the labour intensive enterprise naturally occurs in close proximity

to a population centre by virtue of the markets it serves.

In the case of resources projects, there is very limited scope with respect to making a decision

to locate the construction activity near the required workforce because most of the

construction activity must occur near the in situ resource or geographic location of

downstream processes. Most certainly, some design and management functions can be

located near the required workforce, and advances in modular construction technology

means that much of the actual manufacturing of project components occurs in close

proximity to the required workforce. However, core construction functions such as earthworks,

head works, installation and commissioning tasks must take place at the project site.

This phenomenon is presents a particular challenge in Western Australia because of the remote

and isolated nature of many projects, and the small population and limited civic amenities

0

100

200

300

400

500

600

700

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

(3

Qtr

s O

nly

)

Av

erag

e N

um

ber

of

Per

son

s E

mp

loy

ed (

'000

)

Western Australian Mining Industry Western Australian Construction Industry

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

26

that exist in most population centres that are in proximity to projects. The only significant

exception to this is the Darling Ranges bauxite-alumina industry, which is in close proximity to

the Perth Metropolitan, Peel and South West regional centres.

It is this relatively unique labour market dynamic that has resulted in a dramatic increase in the

mobility of the construction workforce in Australia. Whereas resources projects are limited with

respect to optimising the location of construction activity for workforce access, construction

workers reside in most parts of the world and have relatively versatile skills that can be

deployed on construction projects in a wide range of industries. As such, most construction

workers can make decisions as to where they live, the industries they work in and how they

interact with the projects they work on, on the basis of personal utility.

Resources projects have limited options with respect to sourcing construction skills from small

labour markets that are in proximity to the projects, meaning that labour working on those

projects must relocate. Opportunities for the construction workforce to permanently or semi-

permanently relocate to a location in close proximity to resources projects is in most cases

constrained by the absence of a civic centre, or adequate civic centre in proximity to the

project and/or the lack of a sustained construction market in a civic centre that might be in

proximity to the project. As such, a well-managed Fly-in-Fly-out (FIFO) construction workforce

program is the only realistic option for the construction of many Western Australian resources

projects.

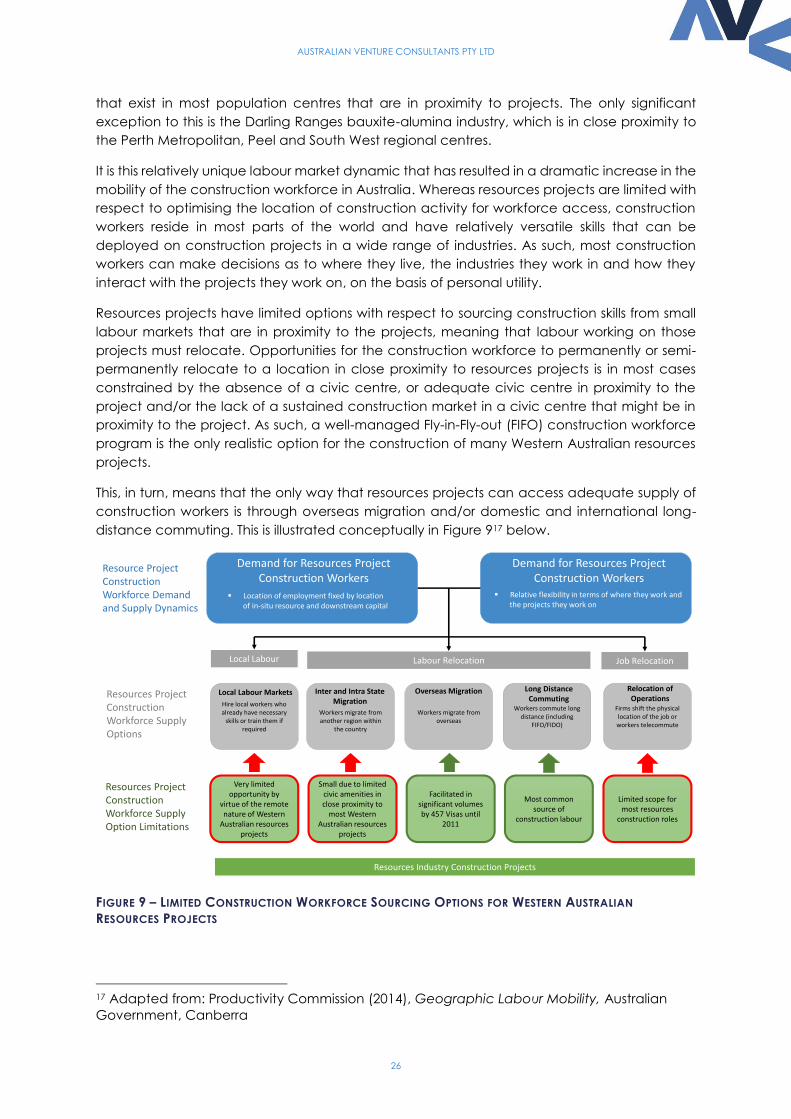

This, in turn, means that the only way that resources projects can access adequate supply of

construction workers is through overseas migration and/or domestic and international long-

distance commuting. This is illustrated conceptually in Figure 917 below.

FIGURE 9 – LIMITED CONSTRUCTION WORKFORCE SOURCING OPTIONS FOR WESTERN AUSTRALIAN

RESOURCES PROJECTS

17 Adapted from: Productivity Commission (2014), Geographic Labour Mobility, Australian

Government, Canberra

Demand for Resources ProjectConstruction Workers

Location of employment fixed by locationof in-situ resource and downstream capital

Demand for Resources ProjectConstruction Workers

Relative flexibility in terms of where they work andthe projects they work on

Resource ProjectConstructionWorkforce Demandand Supply Dynamics

Hire local workers who already have necessary

skills or train them if required

Workers migrate from another region within

the country

Workers migrate from overseas

Workers commute long distance (including

FIFO/FIDO)

Firms shift the physical location of the job or workers telecommute

Local Labour Labour Relocation Job Relocation

Resources Industry Construction Projects

Very limited opportunity by

virtue of the remote nature of Western

Australian resources projects

Small due to limited civic amenities in close proximity to

most Western Australian resources

projects

Facilitated in significant volumes by 457 Visas until

2011

Most common source of

construction labour

Limited scope for most resources

construction roles

Resources ProjectConstructionWorkforce SupplyOptions

Resources ProjectConstructionWorkforce SupplyOption Limitations

Local Labour Markets Inter and Intra StateMigration

Overseas Migration Long DistanceCommuting

Relocation ofOperations

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

27

While operational resources projects face a similar dilemma, the scale of the problem is

somewhat mitigated by the fact the operational workforce is much smaller in terms of number

of workers required and in some cases narrower in terms of breadth of skills. Furthermore, the

increased deployment of automated systems at operational resources projects means that

the oversight of those ICT enabled systems can be conducted from remote operations centres

located in regional population centres. This is particularly the case in the oil and gas industry,

and while only a few mining operations operate substantive remote operating centres, this will

likely be an increasing trend across the Australian resources industry.18

The following subsections describe the dynamics of the different sources of construction

workforce available to resources projects as summarised in Figure 9.

Local Labour Market

For resources projects that are not in practical proximity to a regional population centre, hiring

construction skills from a local market is not an option. However, many resources projects are

in close proximity to Western Australian regional centres and towns such as Kalgoorlie,

Meekatharra, Newman, Tom Price, Karratha, Port Hedland and, more recently, Onslow,

Broome, Ravensthorpe and Geraldton. Indeed many of these towns have developed and

grown as a result of resources project activity. Regardless, skilled workers are generally scarce

in regional population centres.

Where a resources construction project occurs in close proximity to a small local contractor

and/or labour market, there will likely be a propensity for that local contractor and/or labour

market to seek contracts with the resources industry construction project. Where a project

engages this labour this may create a short term labour and/or service shortage in that local

market. However, it is often the case that local labour and/or contractors that have worked

on resources construction projects receive significant economic benefits and develop a

higher level of skills and capabilities from having worked on the project, particularly with

respect to OHS, which they are then able to offer their local market. In many cases, it is likely

that the opportunity created by the resources project has been the catalyst for the expansion

of local service businesses.

In smaller local communities, local government shires are often the main employers and

contractors of a range of engineers, tradespeople and machinery operators. Where this

workforce is attracted to opportunities on resources construction projects, it will typically return

with a more developed skillset and service offering that can be deployed on civic works and

maintenance. While demand for local shire employed or contracted skills from resources

construction projects has created some tension between resources companies and some

local shires, it is probable that once the projects are operational, labour market pressures will

decrease and a higher quality of skills and capabilities will be available to the shires.

Inter and Intra State Migration

Historical commentaries have criticised the Australian population for an apparent low

propensity to relocate to employment markets. However, a recent study by the Australian

18 Australian Venture Consultants (2012), Rise of the Machines? Adoption of Automation

Technology in the Australian Resources Industries and its Implications for Vocational

Education and Training and Higher Education, Resources Industry Training Council

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

28

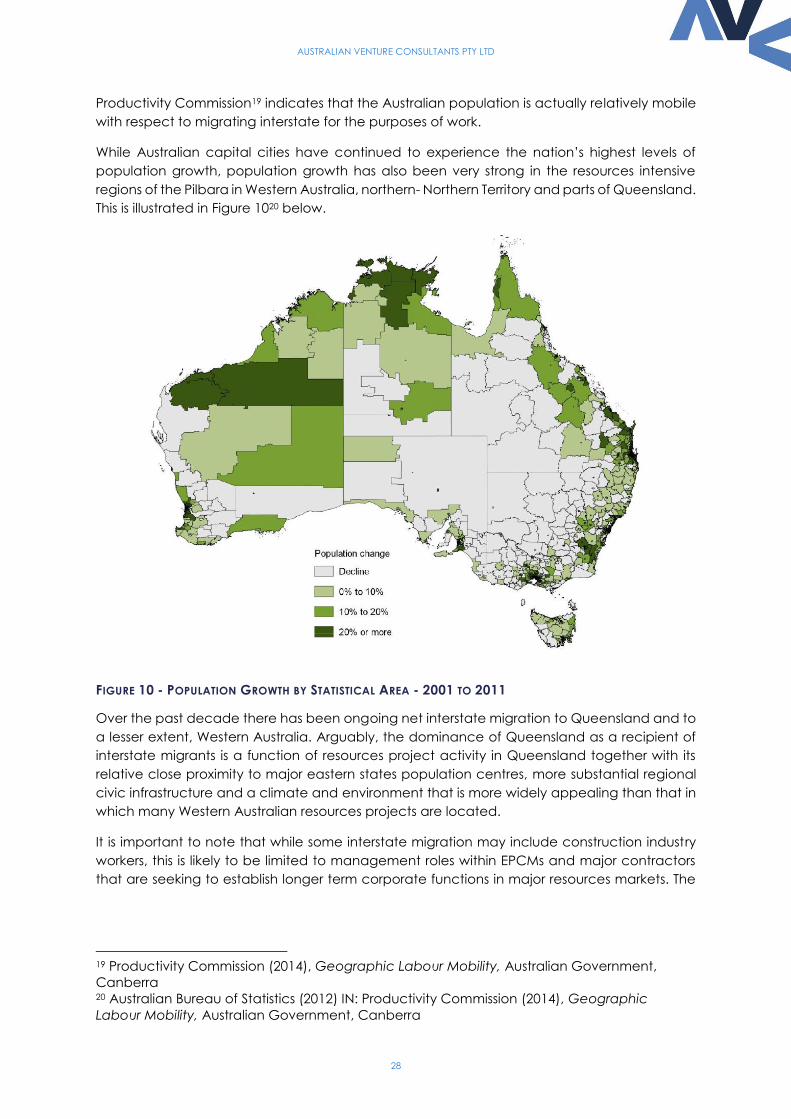

Productivity Commission19 indicates that the Australian population is actually relatively mobile

with respect to migrating interstate for the purposes of work.

While Australian capital cities have continued to experience the nation’s highest levels of

population growth, population growth has also been very strong in the resources intensive

regions of the Pilbara in Western Australia, northern- Northern Territory and parts of Queensland.

This is illustrated in Figure 1020 below.

FIGURE 10 - POPULATION GROWTH BY STATISTICAL AREA - 2001 TO 2011

Over the past decade there has been ongoing net interstate migration to Queensland and to

a lesser extent, Western Australia. Arguably, the dominance of Queensland as a recipient of

interstate migrants is a function of resources project activity in Queensland together with its

relative close proximity to major eastern states population centres, more substantial regional

civic infrastructure and a climate and environment that is more widely appealing than that in

which many Western Australian resources projects are located.

It is important to note that while some interstate migration may include construction industry

workers, this is likely to be limited to management roles within EPCMs and major contractors

that are seeking to establish longer term corporate functions in major resources markets. The

19 Productivity Commission (2014), Geographic Labour Mobility, Australian Government,

Canberra 20 Australian Bureau of Statistics (2012) IN: Productivity Commission (2014), Geographic

Labour Mobility, Australian Government, Canberra

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

29

short-term nature of most resources project construction contracts means that workers will

migrate on a short-term basis or engage through a FIFO program.

The fact that approximately 10 percent of the total Australian mining industry workforce moved

residence between labour markets prior to the last census date, whereas only 4 percent of the

construction industry workforce did the same21 suggests that permanent inter-state migration

is driven by new operational roles or longer term project management roles within mining

companies that result from the expansion of the mining industry, rather than permanent

relocation of construction workers associated with the mining industry.

Overseas Migration

Compared to Queensland, the Western Australian labour market has been more dependent

on overseas migration to meet its growing workforce needs, which is most likely the result of

workers located in the Eastern States reluctant to relocate to Western Australia, which often is

perceived as relatively remote22.

While international migration has always played an important role in Australia’s population

growth, the vast majority of migrants have traditionally settled in the Nation’s capital cities.

Over the past decade, there has been a substantial increase in overseas migrants settling in

regional areas23. This has at least in part been the result of Australian, state and territory policies

designed to attract skilled migrants to regional Australia to address the regional skills deficiency

discussed in a previous section of this report.

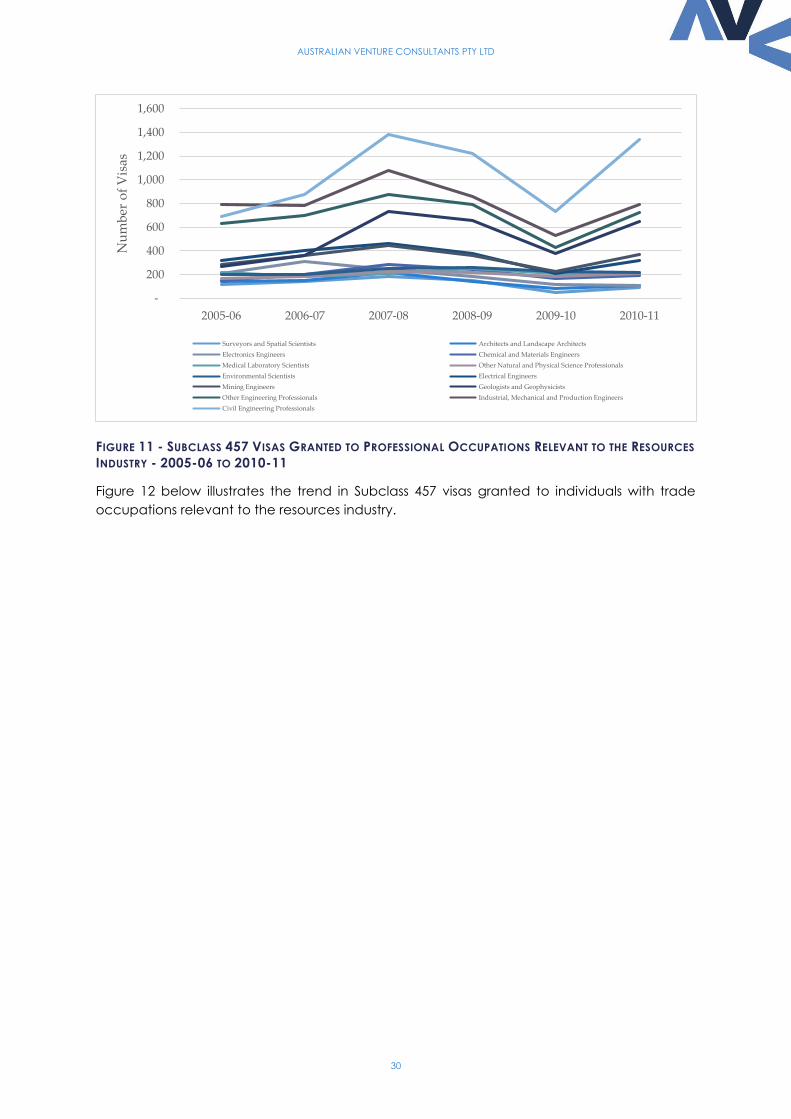

Many migrants working in the Australian resources industry have come to Australia on Subclass

457 Visas, which allow skilled persons to come to Australia to work for an approved employer,

accompanied by their immediate family for a period of between one day and four years.

Operational mining companies, EPCMs and contractors involved in resources construction

projects have used the 457 visa program to address skills shortages in both professional and

trade areas. However, they have not been the main users of the 457 visa program, with

accommodation and food services, health care and social assistance, information media and

telecommunications and other services sectors each routinely accounting for over 10 percent

of 457 visa applications24.

Figure 11 below illustrates the trend in Subclass 457 visas granted to individuals with professional

occupations relevant to the resources industry.

21 ABS IN: Productivity Commission (2014), Geographic Labour Mobility, Australian

Government, Canberra 22 Productivity Commission (2014), Geographic Labour Mobility, Australian Government,

Canberra 23 Productivity Commission (2014), Geographic Labour Mobility, Australian Government,

Canberra 24 Department of Immigration and Border Protection (2014), Subclass 457 Quarterly Reports,

Australian Government, Canberra

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

30

FIGURE 11 - SUBCLASS 457 VISAS GRANTED TO PROFESSIONAL OCCUPATIONS RELEVANT TO THE RESOURCES

INDUSTRY - 2005-06 TO 2010-11

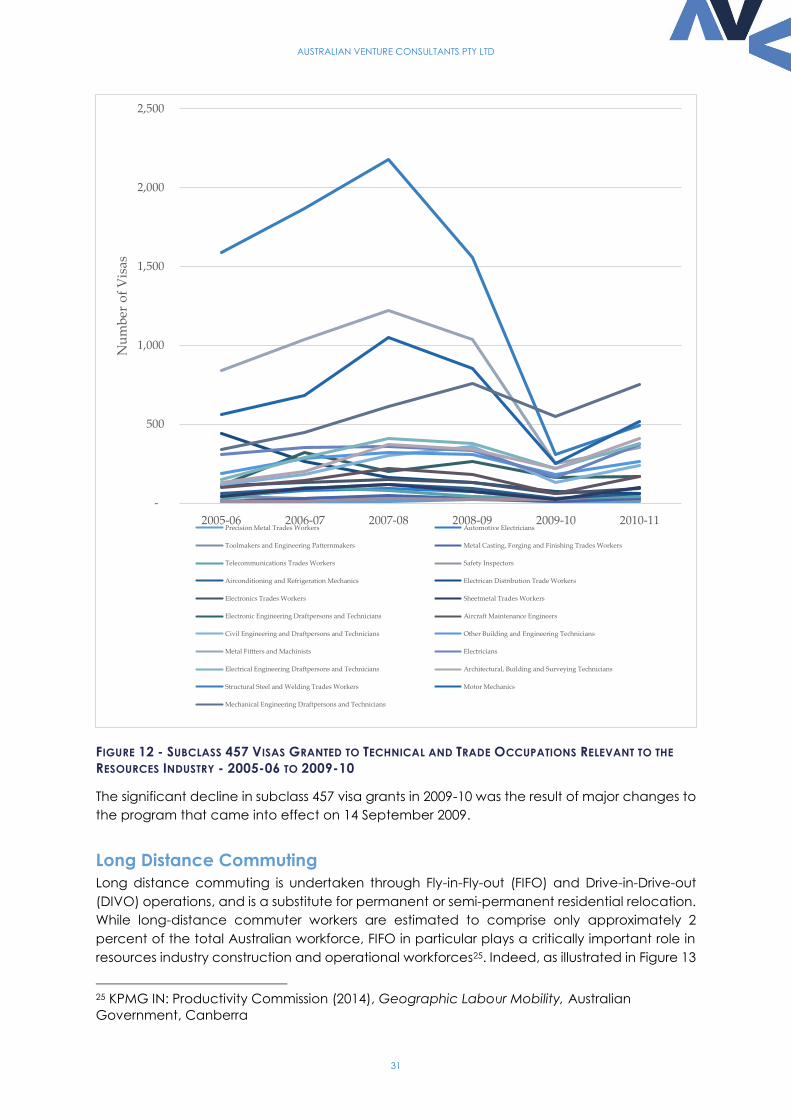

Figure 12 below illustrates the trend in Subclass 457 visas granted to individuals with trade

occupations relevant to the resources industry.

-

200

400

600

800

1,000

1,200

1,400

1,600

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11

Nu

mb

er o

f V

isas

Surveyors and Spatial Scientists Architects and Landscape Architects

Electronics Engineers Chemical and Materials Engineers

Medical Laboratory Scientists Other Natural and Physical Science Professionals

Environmental Scientists Electrical Engineers

Mining Engineers Geologists and Geophysicists

Other Engineering Professionals Industrial, Mechanical and Production Engineers

Civil Engineering Professionals

AUSTRALIAN VENTURE CONSULTANTS PTY LTD

31

FIGURE 12 - SUBCLASS 457 VISAS GRANTED TO TECHNICAL AND TRADE OCCUPATIONS RELEVANT TO THE

RESOURCES INDUSTRY - 2005-06 TO 2009-10

The significant decline in subclass 457 visa grants in 2009-10 was the result of major changes to

the program that came into effect on 14 September 2009.

Long Distance Commuting

Long distance commuting is undertaken through Fly-in-Fly-out (FIFO) and Drive-in-Drive-out

(DIVO) operations, and is a substitute for permanent or semi-permanent residential relocation.

While long-distance commuter workers are estimated to comprise only approximately 2

percent of the total Australian workforce, FIFO in particular plays a critically important role in