Embed Size (px)

Citation preview

West MerciaPolice Authority

Statement of Accounts2010/11

Statement of Accounts 2010/11

Page 1

West Mercia Police Authority

CONTENTS TREASURER’S FOREWORD TO THE ACCOUNTS...........................................................2 About the Accounts A Review of the Year Personal Assurance Statement of the Treasurer INDEPENDENT AUDITOR’S REPORT TO MEMBERS OF WEST MERCIA POLICE AUTHORITY FOR YEAR ENDED 31 MARCH 2011..........................................................10 STATEMENT OF RESPONSIBILITIES FOR THE STATEMENT OF ACCOUNTS ...........14 POLICE AUTHORITY APPROVAL....................................................................................15 ANNUAL GOVERNANCE STATEMENT ...........................................................................16 MOVEMENT IN RESERVES STATEMENT .......................................................................24 COMPREHENSIVE INCOME AND EXPENDITURE STATEMENT ...................................26 BALANCE SHEET .............................................................................................................27 CASH FLOW STATEMENT ...............................................................................................29 NOTES TO THE ACCOUNTS ............................................................................................30 FIRST TIME ADOPTION OF INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRS) ............................................................................................................................90 PENSIONS FUND ..............................................................................................................92 GLOSSARY OF TERMS ....................................................................................................94

Page

Page 2

West Mercia Police Authority

TREASURER’S FOREWORD TO THE ACCOUNTS ABOUT THE ACCOUNTS This Statement of Accounts sets out the overall financial position of West Mercia Police Authority for the year ending 31 March 2011. The accounts are prepared in a format stipulated by the Chartered Institute of Public Finance and Accountancy (CIPFA) in accordance with best accounting practice. The format of the accounts has changed for 2010/11 to comply with the Code of Practice on Local Authority Accounting in the United Kingdom 2010/11 based on International Financial Reporting Standards. The Statement of Accounts consists of: 1. Personal Assurance Statement of the Treasurer to the West Mercia Police

Authority The Treasurer’s assurance statement to the Police Authority’s external auditors. 2. Auditor’s Report This is the External Auditor’s report and opinion on the accounts and conclusion on

arrangements for securing economy, efficiency and effectiveness in the use of resources.

3. Statement of Responsibilities for the Statement of Accounts This section details the financial responsibilities of the Police Authority and the

Treasurer in respect of the Statement of Accounts. 4. Police Authority Approval

The date and signature of the Chair of the Audit Committee for the approval of the Statement of Accounts.

5. Annual Governance Statement This section describes how the Police Authority conducts its business in accordance

with proper standards. The Annual Governance Statement does not form part of the Statement of Accounts but is included here for reporting purposes.

6. The Accounting Statements consist of the following:-

- Movement in Reserve Statement This statement shows the movement in the year on the different reserves held

by the authority, analysed into ‘usable reserves’ which can be applied to fund expenditure or reduce local taxation and ‘unusable reserves’ which record accounting transactions.

Statement of Accounts 2010/11

Page 3

West Mercia Police Authority

- Comprehensive Income and Expenditure Statement

The statement shows the accounting cost in the year of providing services in

accordance with generally accepted accounting practices. This is different from the cost in the year of providing services which are funded from taxation. The Police Authority raises taxation to cover expenditure in accordance with regulations, this is different from the accounting cost. The taxation position is shown in the Movement in Reserves Statement.

- Balance Sheet

The Balance Sheet shows the value as at the Balance Sheet date of the assets and liabilities recognised by the Authority.

- Cash Flow Statement The Cash Flow Statement shows the changes in cash and cash equivalents of

the Authority during the reporting period.

- Notes to the Accounts The Notes to the Accounts provide further disclosures to the Accounting

Statements and detail the Accounting Policies applied in preparing the Accounting Statements.

7. Police Pension Fund, Net Assets Statement and Notes to the Police Pension

Scheme

The Police Pensions Fund Account contains the contributions from the Authority at a rate of 24.2% of police officers’ pay which are used to pay police pensions during the year. Any surplus or deficit on this account at the end of the year is paid to or claimed from the Police Fund.

Page 4

West Mercia Police Authority

A REVIEW OF THE YEAR West Mercia Police Authority provides a police service to the 1.2 million people within the local authority areas covering Herefordshire, Shropshire, Telford and Wrekin and Worcestershire. It is the fourth largest police area in the country and the largest landlocked force in England and Wales. West Mercia has been one of the most economical forces in the country in terms of cost per 1,000 population for a long time and has enjoyed a national reputation for achieving value for money. The police service in West Mercia has a strong value for money ethos. Assets are valued at £84.9m but external long-term borrowing is limited to £10.0m. A policy of employing members of police staff where appropriate has led to West Mercia being one of the most civilianised forces in the country with a ratio of one police staff to 1.15 police officers, thus freeing police officers for operational duties. In 2010 Her Majesty’s Inspector of Constabulary (HMIC) introduced a ‘Police Report Card’. The overall view stated “Most types of crime have reduced steadily in the West Mercia Police area in recent years, giving it generally below average crime rates and making it a comparatively safe place to live. The Force spends slightly more money and is a low to medium cost force in comparison to its peers. It employs more police officers with fewer community support officers”. By reference to all 31 English Shire Forces it spends 98% of the average. The Authority’s income for each year is generally fixed at the start of the year by the level of government grant and council tax. Its expenditure is dominated by the cost of its employees which comprises the largest part of the budget. The major influences on expenditure are the number of employees recruited, the annual national pay awards and the level of major incidents which require additional resources. The Authority’s cash flow is positive as grant income tends to be received in advance of payroll dates. The Authority’s financial position is that it is holding reserves of £32.0m to meet future obligations and potential risks. One of these reserves is the Sustaining Service Delivery Reserve, standing at £18.2m. This sum will be re-invested in maintaining services during 2011/12 and 2012/13. For 2010/11 planned resources were £203.6m and this was to be funded from grants (£124.9m) and council tax (£78.7m). Actual spending was £196.2m. Spending is being curtailed in response to the reduction in government funding. The Authority has made capital investments on buildings, I.T. and vehicles during the year and these will continue into 2011/12. In previous years the Authority has had a very low level of debt, however in 2007/08 £10.0m was borrowed from the Public Works Loans Board to fund part of these investments. In 2010/11, there was £6.0m of capital expenditure on assets, which will require borrowing of £3.8m. However, use of working capital enables this borrowing to be delayed; thereby exploiting the best advantage in the lending and borrowing markets. Capital investment of £18.3m is planned for 2011/12 with £16.0m of this funded by borrowing and the balance by grants and internal funds.

Statement of Accounts 2010/11

Page 5

West Mercia Police Authority

The Authority has created a pensions reserve to show the estimated liability in relation to retirement benefits. This is explained in more detail in note 22 to the accounts. The Audit Commission published a review of financial management in local government (“Summing Up”). This included attention to certain balance sheet ratios: 31 March

2009 31 March

2010 31 March

2011 � Working capital ratio 1.79 1.75 2.03 � Reserves as a proportion of

expenditure 0.11 0.11 0.14

� Borrowing as a proportion of revenue funding 0.05 0.05 0.05

� Borrowing as a proportion of assets 0.12 0.12 0.12

These ratios have been assessed for the past three years for West Mercia and they provide a favourable picture of:

� Cash available to meet short term liabilities � Cash being used advantageously to avoid borrowing � Reserves to meet accrued commitments and risk based contingencies � Low cost of borrowing � Asset values well in excess of borrowing.

Accounting Policies From 2010/11 all local authorities, including police authorities, are required to prepare their accounts under International Financial Reporting Standards (IFRS). The main reason for adopting IFRS is to bring benefits in consistency and comparability between financial reports in the global economy. It will also have benefits in aligning local authority accounting with the private sector accounting. For 2010/11 the 2009/10 accounts have been restated in line with IFRS. The change to IFRS reporting has resulted in a change to some of the Accounting Policies adopted by the Authority. These changes are detailed in Note 1 to the Accounting Statements. The significant changes as a result of adopting IFRS include the following changes to the opening balance sheet: Police Pensions £39.950m Government Grants £ 8.692m Accumulated Absences £ 3.476m The section on First Time Adoption of IFRS explains these variations in greater detail. The government announced that the Consumer Price Index (CPI) rather than the Retail Price Index (RPI) is to be used for the indexation of public service pensions from April 2011. This change in policy has resulted in a ‘gain’ on Past Service Costs of £11.7m for police staff and £175.3m for police officers.

Page 6

West Mercia Police Authority

Operational Results The total recorded crime for the year increased slightly compared with the previous year, but over the medium term the trend of recorded crime is showing a significant reduction. • 1.3% increase in total crimes recorded • 2.6% reduction in domestic burglary and a 0.2 percentage point improvement in

sanction detection rate • 9.4% increase in robbery (and an 8.4% reduction on 2 years ago) and a 3.6 percentage

point deterioration in sanction detection rate (and a 4.2 percentage point improvement on 2 years ago)

• 8.0% increase in the level of serious violence against the person crimes (and an 8.1%

reduction on 2 years ago) and a 3.6 percentage point deterioration in sanction detection rate (and a 3.4 percentage point improvement on 2 years ago)

• 10.9% increase in the level of serious sexual offences and a 2.0 percentage point

deterioration in the sanction detection rate • 5.7% increase in the level of all violent crimes (and a 0.6% reduction on 2 years ago) • 1.9% increase in the level of assault with less serious injury • 0.3% reduction in the level of vehicle crimes • User satisfaction indicators show that 87.8% of people are fully, very or fairly satisfied

with the policing service provided. This is a 2.1 percentage point improvement on the previous year’s figures.

Environmental Issues The Authority has endorsed the principles of the Local Government Association’s Climate Change Commission. This includes the long-term challenge to achieve a 26-32% reduction in carbon emissions by 2020. West Mercia has nominated the Head of Estate Services as the lead officer on sustainability issues and he will lead a project team charged with reducing carbon emissions. For a number of years West Mercia has been making progress in these areas primarily from an economic imperative: • In 2010/11 the Force achieved a 5% reduction in units of energy consumed. • Preparation for the start of the government’s ‘Carbon Reduction Commitment’. • A cycle-to-work scheme has been introduced and over 300 cycles have been purchased

by employees via payroll deductions.

Statement of Accounts 2010/11

Page 7

West Mercia Police Authority

• Reduced water consumption force wide and implemented ‘rainwater harvesting’ at HQ. • Better and cheaper system for disposal of waste electrical equipment. • The force has achieved the ISO 14001 standard awarded by the British Standards

Institute for the quality of its energy management processes. • Three capital projects are planned or completed which will incorporate design features

to achieve the BREEAM standard of “good”. These are Market Drayton Police Station, Central Storage Building and Hindlip Gatehouse.

• For the past decade all of West Mercia’s buildings have been designed to standards

10% better than Building Regulation requirements without a cost penalty. • West Mercia’s 3,000 computer workstations are based on thin client technology. This

uses a small fraction of the energy which would be consumed by the equivalent number of personal computers. Also, West Mercia has completed the change of its computer screens from Cathode Ray Tube (CRT) to Liquid Crystal Display (LCD) computer monitors which use less energy and produce less heat, reducing cooling requirements.

• In the early 1990’s the vehicle fleet started to move to diesel from petrol and currently

78% of the fleet is diesel. This is an increase on last year’s figure of 77%. The carbon footprint of the consumption of fuel by the vehicle fleet is measured annually. In 2009/10 it was 4,375 tonnes of CO�, which equated to 361 grams per mile. In 2010/11 the carbon footprint increased to 4,449 tonnes of CO�. The increase is mainly due to a higher number of miles travelled. This equated to 359 grams per mile. National Economic Climate and Medium Term Outlook It is appropriate to consider the Police Authority’s position in the light of changes to the national economic climate over the past year. During the year the Police Authority maintained its prudent policy of making cash investments only with the Bank of England. The Authority has suffered no losses during the exceptional conditions in investment markets of the last three years. Only a small part of the Authority’s income comes from trade debtors. There have been no significant losses resulting from the bankruptcy of customer. The risk of such future losses is assessed as small. The most important influences on West Mercia’s financial position for the future are the levels of government grant and council tax. During the summer of 2010, the government confirmed that there would be significant reductions in its grants to all police authorities for 2011/12 and 2012/13. It also gave indicative figures for further reductions in 2013/14 and 2014/15. Over the four year period the reduction is of the order of £24m in cash terms.

Page 8

West Mercia Police Authority

Since 2009 a programme of reviews of operational structures, termed ‘Making the Difference’, has been underway. This has already delivered budget savings in response to the financial challenge of lower funding. The Authority has incorporated these savings into a new Medium Term Financial Plan. It has also built up and committed some financial reserves to sustain the budget in 2011/12 and 2012/13. The ‘Making the Difference’ programme is continuing and will address the financial challenges of 2013/14 and 2014/15. This will include the evaluation of a strategic alliance with Warwickshire Police.

Statement of Accounts 2010/11

Page 9

West Mercia Police Authority

PERSONAL ASSURANCE STATEMENT OF THE TREASURER TO THE WEST MERCIA POLICE AUTHORITY This statement has been given to the Police Authority's external auditors The Audit Commission. I confirm, to the best of my knowledge and belief and having made appropriate enquiries of the Chief Constable, the representation set out below and given to you in connection with your audit of West Mercia Police Authority’s financial statements for the period ending 31 March 2011. Accounting Records All the accounting records have been made available to you in accordance with Section 6 of the Audit Commission Act 1998 for the purpose of your audit and all the transactions undertaken have been properly reflected and recorded in the accounting records. To the best of my knowledge and belief, reasonable efforts have been made to ensure that records and related information which might materially affect the truth and fairness of, or necessary disclosure in, the financial statements have been made available to you and no such information has been withheld. Related Party Transactions Other than stated in the accounts, there are no related party transactions in the period which require adjustment of or disclosure to the financial statements or in the notes thereto. Law and Regulations I am not aware of any instances of actual or potential breaches of, or non-compliance with, laws and regulations governing the transactions of the West Mercia Police Authority that could have a material effect on the financial statements. I am not aware of any irregularities, or allegations of irregularities including fraud, involving management or employees who have a significant role in the accounting and internal control systems, which could have a material effect on the financial statements. Subsequent Events Other than stated in the accounts, there have been no circumstances or events subsequent to the period end which require adjustment to or disclosure in the financial statements or in the notes thereto.

Patrick Birch Treasurer to the West Mercia Police Authority 28 June 2011

Page 10

West Mercia Police Authority

INDEPENDENT AUDITOR’S REPORT TO MEMBERS OF WEST MERCIA POLICE AUTHORITY FOR THE YEAR ENDED 31 MARCH 2011 Opinion on the Authority and Pension Fund accounting statements I have audited the accounting statements and the police pension fund accounting statements of West Mercia Police Authority for the year ended 31 March 2011 under the Audit Commission Act 1998. The accounting statements comprise the Movement in Reserves Statement, the Comprehensive Income and Expenditure Statement, the Balance Sheet, the Cash Flow Statement and the related notes. The police pension fund accounting statements comprise the Fund Account, the Net Assets Statement and the related notes. These accounting statements have been prepared under the accounting policies set out in the Statement of Accounting Policies. This report is made solely to the members of West Mercia Police Authority in accordance with Part II of the Audit Commission Act 1998 and for no other purpose, as set out in paragraph 48 of the Statement of Responsibilities of Auditors and Audited Bodies published by the Audit Commission in March 2010. Respective responsibilities of the Treasurer and auditor As explained more fully in the Statement of the Treasurer’s Responsibilities, the Treasurer is responsible for the preparation of the Authority’s Statement of Accounts, including the police pension fund accounting statements, in accordance with proper practices as set out in the CIPFA/LASAAC Code of Practice on Local Authority Accounting in the United Kingdom. My responsibility is to audit the accounting statements in accordance with applicable law and International Standards on Auditing (UK and Ireland). Those standards require me to comply with the Auditing Practice’s Board’s Ethical Standards for Auditors. Scope of the audit of the financial statements An audit involves obtaining evidence about the amounts and disclosures in the accounting statements sufficient to give reasonable assurance that the accounting statements are free from material misstatement, whether caused by fraud or error. This includes an assessment of: whether the accounting policies are appropriate to the Authority and Pension Fund’s circumstances and have been consistently applied and adequately disclosed; the reasonableness of significant accounting estimates made by the Authority and the Pension Fund; and the overall presentation of the accounting statements. I read all the information in the explanatory foreword to identify material inconsistencies with the audited accounting statements. If I become aware of any apparent material misstatements or inconsistencies I consider the implications for my report. Opinion on accounting statements In my opinion the accounting statements: � give a true and fair view of the state of West Mercia Police Authority’s affairs as at 31

March 2011 and of its income and expenditure for the year then ended;

Statement of Accounts 2010/11

Page 11

West Mercia Police Authority

� give a true and fair view of the financial transactions of the police pension fund during the year ended 31 March 2011 and the amount and disposition of the fund’s assets and liabilities as at 31 March 2011, other than liabilities to pay pensions and other benefits after the end of the scheme year; and

� have been properly prepared in accordance with the CIPFA/LASAAC Code of Practice

on Local Authority Accounting in the United Kingdom. Opinion on other matters In my opinion, the information given in the explanatory foreword for the financial year for which the accounting statements are prepared is consistent with the accounting statements. Matters on which I report by exception I have nothing to report in respect of the Authority’s governance statement. I only report to you if, in my opinion the governance statement does not reflect compliance with ‘Delivering Good Governance in Local Government: a Framework’ published by CIPFA/SOLACE in June 2007.

Page 12

West Mercia Police Authority

Conclusion on Authority’s arrangements for securing economy, efficiency and effectiveness in the use of resources Authority’s responsibilities The Authority is responsible for putting in place proper arrangements to secure economy, efficiency and effectiveness in its use of resources, to ensure proper stewardship and governance, and to review regularly the adequacy and effectiveness of these arrangements. Auditor’s responsibilities I am required under Section 5 of the Audit Commission Act 1998 to satisfy myself that the Authority has made proper arrangements for securing economy, efficiency and effectiveness in its use of resources. The Code of Audit Practice issued by the Audit Commission requires me to report to you my conclusion relating to proper arrangements, having regard to relevant criteria specified by the Audit Commission. I report if significant matters have come to my attention which prevent me from concluding that the Authority has put in place proper arrangements for securing economy, efficiency and effectiveness in its use of resources. I am not required to consider, nor have I considered, whether all aspects of the Authority’s arrangements for securing economy, efficiency and effectiveness in its use of resources are operating effectively. Basis of conclusion I have undertaken my audit in accordance with the Code of Audit Practice, having regard to the guidance on the specified criteria, published by the Audit Commission in October 2010, as to whether the Authority has proper arrangements for: � securing financial resilience; and � challenging how it secures economy, efficiency and effectiveness. The Audit Commission has determined these two criteria as those necessary for me to consider under the Code of Audit Practice in satisfying myself whether the Authority put in place proper arrangements for securing economy, efficiency and effectiveness in its use of resources for the year ended 31 March 2011. I planned my work in accordance with the Code of Audit Practice. Based on my risk assessment, I undertook such work as I considered necessary to form a view on whether, in all significant respects, the Authority had put in place proper arrangements to secure economy, efficiency and effectiveness in its use of resources.

Statement of Accounts 2010/11

Page 13

West Mercia Police Authority

Conclusion On the basis of my work, having regard to the guidance on the specified criteria published by the Audit Commission in October 2010, I am satisfied that, in all significant respects, West Mercia Police Authority put in place proper arrangements to secure economy, efficiency and effectiveness in its use of resources for the year ending 31 March 2011. Certificate I certify that I have completed the audit of the accounts, including the police pension fund accounting statements, of West Mercia Police Authority in accordance with the requirements of the Audit Commission Act 1998 and the Code of Audit Practice issued by the Audit Commission. Elizabeth Cave District Auditor Room 24, West Mercia Police HQ, Hindlip Hall, PO Box 55, Worcester, WR3 8SP

Page 14

West Mercia Police Authority

STATEMENT OF RESPONSIBILITIES FOR THE STATEMENT OF ACCOUNTS The Authority’s Responsibilities The Authority is required: • to make arrangements for the proper administration of its financial affairs and to secure

that one of its officers has the responsibility for the administration of those affairs. In this Authority, that officer is the Treasurer to the West Mercia Police Authority

• to manage its affairs to secure economic, efficient and effective use of resources and safeguard its assets

• to approve the Statement of Accounts. The Treasurer’s Responsibilities The Treasurer is responsible for the preparation of the Authority's Statement of Accounts in line with the terms of the Chartered Institute of Public Finance and Accountancy Code of Practice on Local Authority Accounting in the United Kingdom ("the Code of Practice"). In preparing this statement of accounts, the Treasurer has: • selected suitable accounting policies and then applied them consistently • made judgements and estimates that were reasonable and prudent • complied with the Code of Practice. The Treasurer has also: • kept proper accounting records which were up to date • taken reasonable steps for the prevention and detection of fraud and other irregularities • ensured that the Authority’s Statement of Accounts gives a true and fair view of the

financial position of the Police Authority at 31 March 2011 and its income and expenditure for the year ended 31 March 2011.

Patrick Birch Treasurer to the West Mercia Police Authority 28 June 2011

Statement of Accounts 2010/11

Page 15

West Mercia Police Authority

POLICE AUTHORITY APPROVAL In accordance with Regulation 8 of the Accounts and Audit Regulations 2011, I certify that the Audit Committee approved the Statement of Accounts on 28 June 2011.

Malcolm Pate Chair of the Audit Committee 28 June 2011

Page 16

West Mercia Police Authority

ANNUAL GOVERNANCE STATEMENT 1. Scope of Responsibilities 1.1 The West Mercia Police Authority (“the Police Authority”) is responsible for ensuring

an efficient and effective police force. It is responsible for ensuring its business is conducted in accordance with the law and proper standards, and that public money is safeguarded and properly accounted for, and used economically, efficiently and effectively. The Authority also has a duty under the Local Government Act 1999 to make arrangements to secure continuous improvement in the way in which its functions are exercised, having regard to a combination of economy, efficiency and effectiveness. In discharging this overall responsibility, the Authority is also responsible for putting in place proper arrangements for the governance of its affairs and facilitating the exercise of its functions, which includes ensuring a sound system of internal control is maintained through the year and that arrangements are in place for the management of risk.

1.2 This statement explains how the Police Authority has complied with these

requirements and also meets the requirements of Regulation 4 of the Accounts and Audit Regulations 2011 in relation to the publication of an Annual Governance Statement.

2. The Purpose of the Governance Framework 2.1 The governance framework comprises the systems and processes, and culture and

values by which the Police Authority is directed and controlled and its activities through which it accounts to and engages with the community. It enables the Police Authority to monitor the achievement of its strategic objectives and to consider whether those objectives have led to the delivery of appropriate, cost effective services, including achieving value for money.

2.2 The system of internal control is a significant part of that framework and is designed

to manage risk to a reasonable and foreseeable level. It cannot eliminate all risk of failure to achieve policies, aims and objectives; it can therefore only provide reasonable and not absolute assurance of effectiveness. The system of internal control is based on a continuing process designed to identify and prioritise the risks to the achievement of the Authority’s policies, aims and objectives, to evaluate the likelihood of those risks being realised and the impact should they be realised, and to manage them effectively, efficiently and economically.

2.3 The governance framework has been in place at the Authority for the year ended 31

March 2011 and up to the date of approval of the Statement of Accounts.

3. The Governance Framework 3.1 The Chief Constable is responsible for operational policing matters, the direction and

control of police personnel and for putting in place proper arrangements for the governance of the Force. The Police Authority is required to hold him to account for

Statement of Accounts 2010/11

Page 17

West Mercia Police Authority

the exercise of those functions and those of the persons under his direction and control. It therefore follows that the Police Authority must satisfy itself that the Force has appropriate mechanisms in place for the maintenance of good governance, and that these operate in practice.

3.2 In West Mercia this is achieved by the operation of a range of systems and

procedures, the most important of which is that the Police Authority and the Chief Constable publish a three-year Strategic Plan and Annual Joint Policing Plan in order to establish objectives for both the immediate year and for the medium term. This process includes liaison with a range of partners and stakeholder groups. A summary of how the Police Authority and the Force engage with the communities of West Mercia is as follows:

3.2.1 Publicised stakeholder meetings are open to the public. The meetings involve open

discussion of the Chief Constable’s policing objectives and a presentation by the Treasurer to the Police Authority on the resources available to achieve these objectives.

3.2.2 The Police Authority has increased the number of stakeholder meetings to enable a

meeting in each of the four local Authority areas of Herefordshire, Worcestershire, Shropshire and Telford & Wrekin.

3.2.3 The Force has a long established system of user satisfaction surveys for obtaining

the views of those who have had cause to contact the police in order to check that the service they received was satisfactory and inform decisions to improve the service provided. Ongoing surveys are undertaken of people who have been burgled, been the victim of vehicle crime, violent crime or racial incidents and those who have been involved in road traffic collisions. Results are produced each month and formally reported to and monitored by the Police Authority.

3.2.4 The Force conduct a local Crime and Safety Partnership Survey on a quarterly basis

for residents of West Mercia in partnership with the Police Authority and criminal justice partners. The purpose of the survey is to gain an understanding of local issues and priorities and to ascertain public perceptions of and feelings about community safety. Over the year approximately 60,000 surveys were posted to residents across West Mercia.

3.2.5 Members of the Police Authority are drawn from the local community (nine of whom

are local authority councillors drawn from across the whole Force area) with the aim of being broadly representative of the West Mercia area. In addition to their involvement with their local communities through their roles as Councillors, Magistrates and other activities, members are made aware of local concerns through their role as representatives of the Police Authority on Policing Matters Groups, Community Safety Partnerships and Community Policing Boards.

3.2.6 Policing Matters Groups are meetings which were introduced in Shropshire,

Herefordshire, Telford & Wrekin, South Worcestershire and North Worcestershire during 2008. These meetings provide an opportunity for members of the public to meet with the local Police Commander, members of the Police Authority and representatives from partners agencies and find out what they are doing for the local

Page 18

West Mercia Police Authority

area, as well as allowing the public to raise any questions or issues of concern. They also give the Police Authority, Force and partner agencies the chance to consult with the local community on projects, processes and strategies.

3.2.7 Both the Force and Police Authority’s web sites are used to keep people informed

about current policing issues, provide information regarding services and seek feedback. The Authority’s site is also intended to provide web users with a useful way to communicate with the Authority and its members, to find out what’s going on and how to get more involved.

3.2.8 How we monitor performance We use a wide range of performance indicators to measure how well we are

performing. These indicators are assessed on an ongoing basis and are reviewed formally at a monthly meeting of Chief Officers and Senior Managers. The Police Authority is regularly informed of performance across a range of matters with Members receiving monthly monitoring reports and reviews of performance in detail at scheduled Panel meetings.

The 15 indicators below are the key measures we will use to track progress in

delivering our Strategic Aims:

Target / Measure 2011/12 Total crime: a) number recorded a) Below 72,000 b) percentage solved� b) To be monitored by Police Authority Violent crimes with injury: a) number recorded a) Below 7,100 b) percentage solved� b) 50% Serious sexual offences: a) number recorded a) To be monitored by Police Authority b) percentage solved� b) 32% House burglaries: a) number recorded a) Below 3,135 b) percentage solved� b) 21% Robbery: a) number recorded a) To be monitored by Police Authority b) percentage solved� b) To be monitored by Police Authority Monitor levels of anti-social behaviour To be monitored by Police Authority The number of fatal and serious road traffic casualties

To be monitored by Police Authority

Satisfaction with overall service provided by the police (measured by West Mercia User Satisfaction Surveys)

To be monitored by Police Authority

Monitor levels of feelings of safety To be monitored by Police Authority

Statement of Accounts 2010/11

Page 19

West Mercia Police Authority

together with crime and anti-social behaviour statistics to enable us to focus work/activity in our most vulnerable neighbourhoods Public confidence. The percentage of people who agree the police are doing an excellent or good job in their local area (measured by the Crime and Safety Partnership Survey)

To be monitored by Police Authority

� Solved = Sanction detections (detections resulting in action being taken against the offender responsible) plus community resolutions (community resolution delivers a victim focussed outcome, which is agreed as appropriate and proportionate to the act committed, by all parties, including the police).

3.3 The Police Authority and the Chief Constable assimilate the results of their

consultation, together with consideration of government policies and an assessment of the financial resources available in order to create the annual policing plan within a three year framework.

3.4 The targeted outcomes within the Joint Policing Plan are that:

• the public have confidence in the police and express satisfaction with the policing service

• the levels of crime and anti social behaviour remain low, and • communities feel safe.

3.5 The Police Authority’s strategic aims are:

• Levels of crime and anti-social behaviour remain low • The public have confidence in us and express satisfaction with our policing

service • Our communities feel safe

The priorities for the year are:

• Protect people from crime and disorder according to their needs and vulnerabilities

• Work with partners to bring offenders to account, acting in the best interest of victims and the public

• Ensure we are accessible in our communities • Provide a supportive and effective response to victims of sexual offences,

domestic abuse, child abuse and hate crime • Protect road users by working with partners to avoid casualties • Have the capability and capacity to respond to major crime investigations and

serious incidents while delivering a resilient local policing service

Page 20

West Mercia Police Authority

• Provide an efficient and effective policing service which delivers value for money through our Making the Difference Programme

• Actively pursue collaboration opportunities with other forces and partner organisations to achieve economies and efficiencies.

3.6 The Police Authority have stated the following ambitions which guide it in the

performance of its duties:

• Be accessible, be informative, be communicative and to listen to the public to ensure that their views are taken into account in the delivery of policing services

• Set a budget which balances the resource needs of the service with affordability for the local taxpayer

• Set ambitious but realistic objectives for the police service and monitor their delivery

• Ensure the high quality leadership of the Force is maintained and that the service reflects the communities its serves

• Hold the Chief Constable to account on behalf of the public • Ensure strong corporate governance by the Police Authority of the service • Oversee and pursue efficiency in the delivery of policing services, working with

partner agencies and other police forces to improve delivery and maximise value for money

• Ensure the highest standards of conduct both by members of the Police Authority and by the Police Service.

3.7 Committees 3.7.1 The Police Authority has assigned specific roles and responsibilities to a number of

subsidiary Committees and Panels in order to facilitate decision making and policy making within the context of its strategy.

3.7.2 The Committees are:

� Appointments and Remuneration Committee � Audit Committee � Standards Committee � Urgent Decisions Committee

3.7.3 Through these Committees and associated Panel structure, the Authority monitors

performance against plans and monitors quality of services for users. It also monitors standards of behaviour and adherence to regulations.

Statement of Accounts 2010/11

Page 21

West Mercia Police Authority

4. Risk 4.1 A process to address weaknesses and to ensure continuous improvement is in

place. The Deputy Chief Constable chairs the Force Risk and Opportunities Group which highlights significant risks to the Chief Officers’ Strategy Group.

4.2 West Mercia views its responsibilities within the corporate governance arrangements

seriously and has taken positive action to address identified gaps in taking informed decisions and the managing and reporting of risk.

4.3 As an integral element of its system of internal control, West Mercia has established

a corporate approach to risk management. There is a formal written Risk Management Policy and Strategic Risk Management Procedure which has undergone internal and external consultation and this is made available to all staff via the Force Intranet. Its main aim is to establish a culture whereby risk management is embedded within service delivery and Force Risk Management policy and procedures are reviewed regularly and updated as appropriate.

4.4 The Force Risk and Opportunities Group is responsible for reviewing West Mercia’s

Risk Management strategies and ensures that:

• emerging significant departmental risks are communicated to the Force Risk Management Board, to the Chief Officers’ Policy Group and to the Police Authority

• corporate risks requiring departmental or individual mitigation are communicated to the correct department or risk owner

• the Force Strategic Risk Register is regularly reviewed and updated, and key risks are prioritised in terms of probability and impact

• the risk management process is reviewed and revised as necessary • risk is championed effectively across the whole organisation.

4.5 Membership and terms of reference of the Force Risk and Opportunities Group are

set out within the Force Strategic Risk Management Procedure. West Mercia has an established post of Force Risk Co-ordinator whose main duty is to maintain the Force Strategic Risk Register and to advise on the total risk to which the Force is exposed. Risk focal points within each command have been nominated and risk awareness training and use of risk registers is cascaded, one to one, by the Risk Management Co-ordinator.

4.6 Information Risk The Force owns information collected for policing purposes, including significant

amounts of personal information. The Chief Constable manages his responsibilities, principally derived from the Data

Protection Act 1998 and the Police Act 1996 through a specific information management governance structure.

Page 22

West Mercia Police Authority

Information strategy and policy is managed in order to enhance and improve the Force’s capability in information management. Residual risk is controlled on the Chief Constable’s behalf by Data Protection, Freedom of Information, Audit, Records Management, Information Security and Vetting functions.

5. Complementary Governance Arrangements 5.1 Long-standing arrangements are in place for delegation of authority supported by

Standing Orders and Financial Regulations. There has been significant delegation of budgetary responsibility to operational managers in order to enhance the effectiveness of the use of resources.

5.2 The Authority and the Force have responded to the economic challenges posed by

the government’s spending plans by formulating a clear Medium Term Financial Plan. Significant cost reductions have been achieved as a result of a programme of management action termed ‘Making the Difference’. This has included a more centralised approach to operational decision making and to resource management. The Making the Difference programme is continuing into 2011/12 and this includes the evaluation of a strategic alliance with Warwickshire Police.

5.3 The Audit Committee has been established to undertake the core functions of the

audit process as recommended by the Chartered Institute of Public Finance and Accountancy. The Audit Committee has received training in risk management. The Chief Executive has a formal role in ensuring that all of the Authority’s activities are properly lawful. This combination of arrangements provides confidence that compliance with relevant laws and regulations is achieved.

5.4 The Force operates a whisteblowing system, an independent provided service, to

receive disclosures from police officers and police staff who may have concerns about irregular behaviour within the Force. From outside of the Force, the “Crimestoppers” facility provides a similar confidential service. The Professional Standards Department proactively promotes high standards of behaviour and investigates questionable behaviour.

5.5 The Force has developed policy on the governance of partnerships and provided

advice to officers which takes account of the wide range of partnership engagements which are in place.

6. Review of Effectiveness 6.1 The Authority has responsibility for conducting, at least annually, a review of the

effectiveness of the governance framework, including the system of internal audit and the system of internal control. These reviews have been informed by the work of internal auditors and managers within the Authority who have the responsibility for the development and maintenance of the governance environment. In addition, comments made by the external auditors and other review agencies and inspectorates have informed this review.

6.2 The signatories have been advised on the implications of the result of the review of

the effectiveness of the governance framework by the Audit Committee, the Standards Committee and the Force Performance Monitoring Panel and a process

Statement of Accounts 2010/11

Page 23

West Mercia Police Authority

to address weaknesses and ensure continuous improvement of the system is in place.

7. Significant Governance Issues 7.1 The review of effectiveness of governance for 2010/11 has identified no significant

governance issues.

Sheila Blagg Paul West David Brierley Chair of the

Police Authority Chief Constable Chief Executive

of the Police Authority 28 June 2011 28 June 2011 28 June 2011

Page 24

West Mercia Police Authority

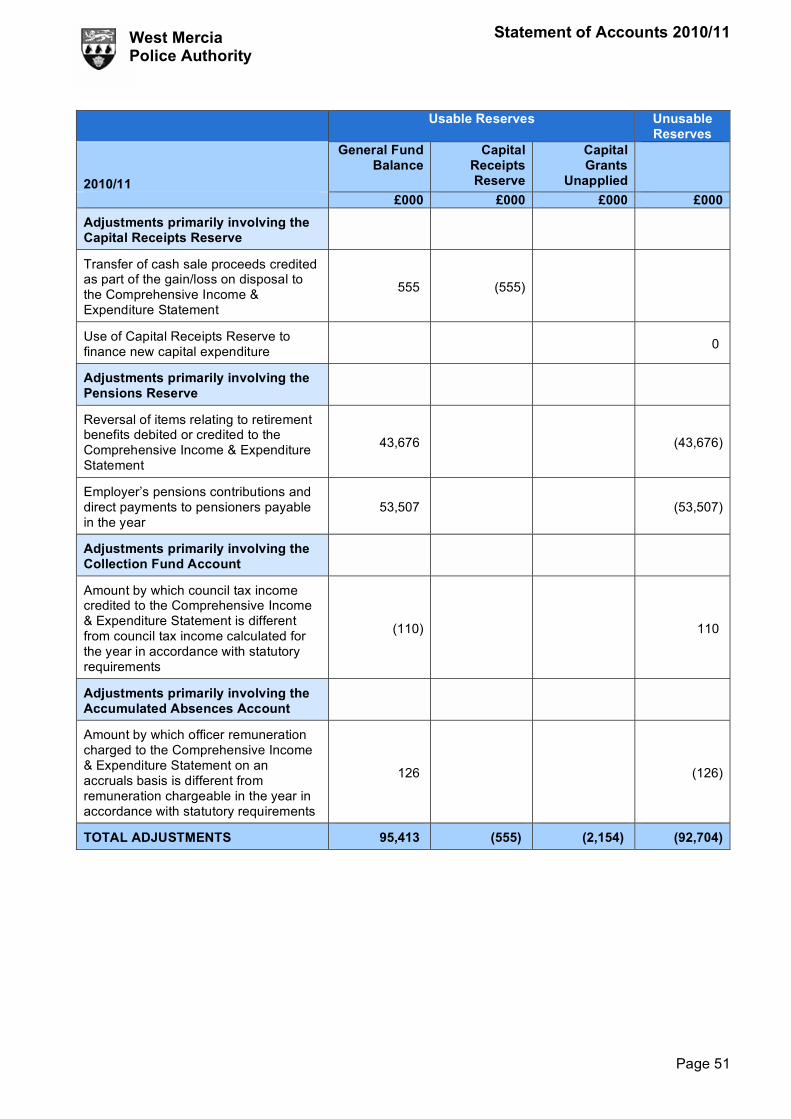

MOVEMENT IN RESERVES STATEMENT This statement shows the movement in the year on the different reserves held by the authority, analysed into ‘usable reserves’ (ie those that can be applied to fund expenditure or reduce local taxation) and other reserves. The ‘(Surplus) or Deficit on the Provision of Services’ line shows the true economic cost of providing the authority’s services, more details of which are shown in Comprehensive Income and Expenditure Statement. These are different from the statutory amounts required to be charged to the General Fund Balance for Council Tax setting purposes. The ‘Net (Increase) / Decrease before transfers to earmarked reserves’ line shows the statutory General Fund Balance before any discretionary transfers to or from earmarked reserves undertaken by the authority.

Gen

eral

Fun

d B

alan

ce

Earm

arke

d G

ener

al F

und

Res

erve

s

Cap

ital

Rec

eipt

s R

eser

ve

Cap

ital G

rant

s U

napp

lied

Tota

l Usa

ble

Res

erve

s

Unu

sabl

e R

eser

ves

Tota

l A

utho

rity

Res

erve

s

£000 £000 £000 £000 £000 £000 £000

Opening Balance at 1 April 2010

0 (24,583) 0 0 (24,583) 1,643,824 1,619,241

Movement in reserves during 2010/11

(Surplus) or deficit on provision of services (accounting basis)

(102,896) (102,896) (102,896)

Other Comprehensive Income and Expenditure

(62,837) (62,837)

Total Comprehensive Income and Expenditure

(102,896) 0 0 0 (102,896) (62,837) (165,733)

Adjustments between accounting basis and funding basis under regulations

95,413 0 (555) (2,154) 92,704 (92,704) 0

Net (Increase)/Decrease before transfers to Earmarked Reserves

(7,483) 0 (555) (2,154) (10,192) (155,541) (165,733)

Transfers to/from Earmarked Reserves 7,483 (7,483) 0 0

(Increase)/Decrease in Year 0 (7,483) (555) (2,154) (10,192) (155,541) (165,733)

Balance at 31 March 2011 0 (32,066) (555) (2,154) (34,775) 1,488,283 1,453,508

Statement of Accounts 2010/11

Page 25

West Mercia Police Authority

Gen

eral

Fun

d B

alan

ce

Earm

arke

d G

ener

al F

und

Res

erve

s

Cap

ital

Rec

eipt

s R

eser

ve

Cap

ital G

rant

s U

napp

lied

Tota

l Usa

ble

Res

erve

s

Unu

sabl

e R

eser

ves

Tota

l Aut

horit

y R

eser

ves

£000 £000 £000 £000 £000 £000 £000

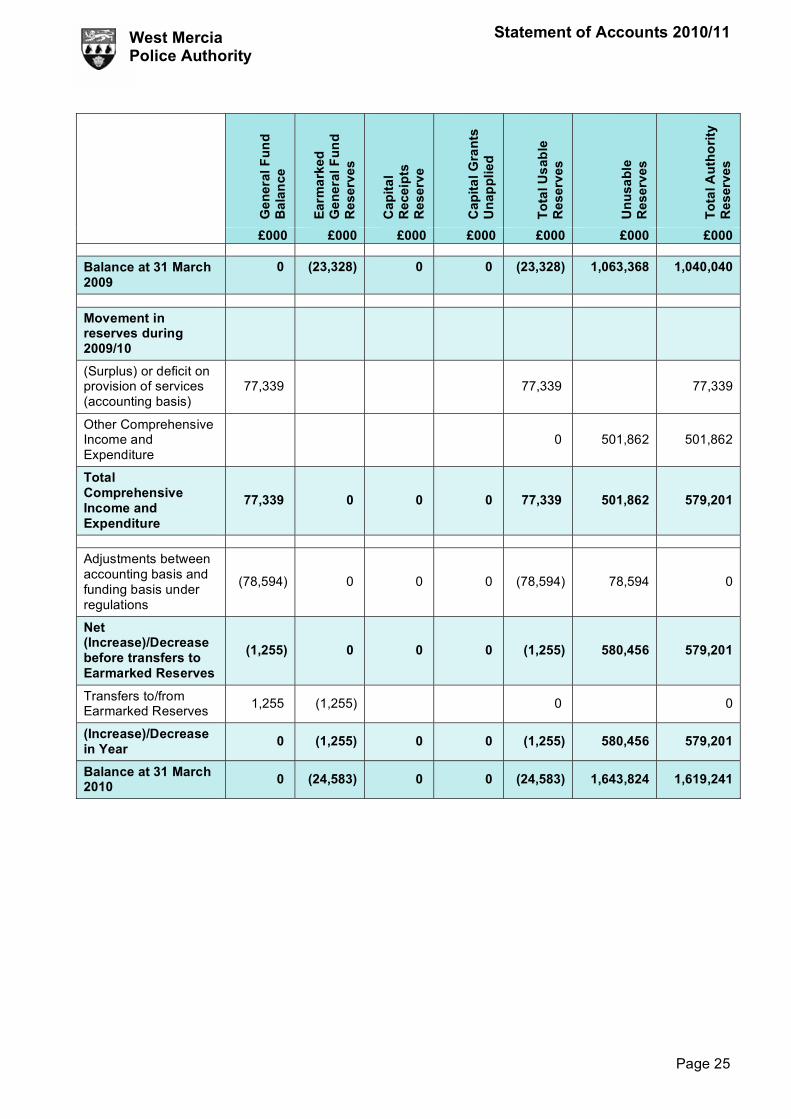

Balance at 31 March 2009

0 (23,328) 0 0 (23,328) 1,063,368 1,040,040

Movement in reserves during 2009/10

(Surplus) or deficit on provision of services (accounting basis)

77,339 77,339 77,339

Other Comprehensive Income and Expenditure

0 501,862 501,862

Total Comprehensive Income and Expenditure

77,339 0 0 0 77,339 501,862 579,201

Adjustments between accounting basis and funding basis under regulations

(78,594) 0 0 0 (78,594) 78,594 0

Net (Increase)/Decrease before transfers to Earmarked Reserves

(1,255) 0 0 0 (1,255) 580,456 579,201

Transfers to/from Earmarked Reserves 1,255 (1,255) 0 0

(Increase)/Decrease in Year 0 (1,255) 0 0 (1,255) 580,456 579,201

Balance at 31 March 2010 0 (24,583) 0 0 (24,583) 1,643,824 1,619,241

Page 26

West Mercia Police Authority

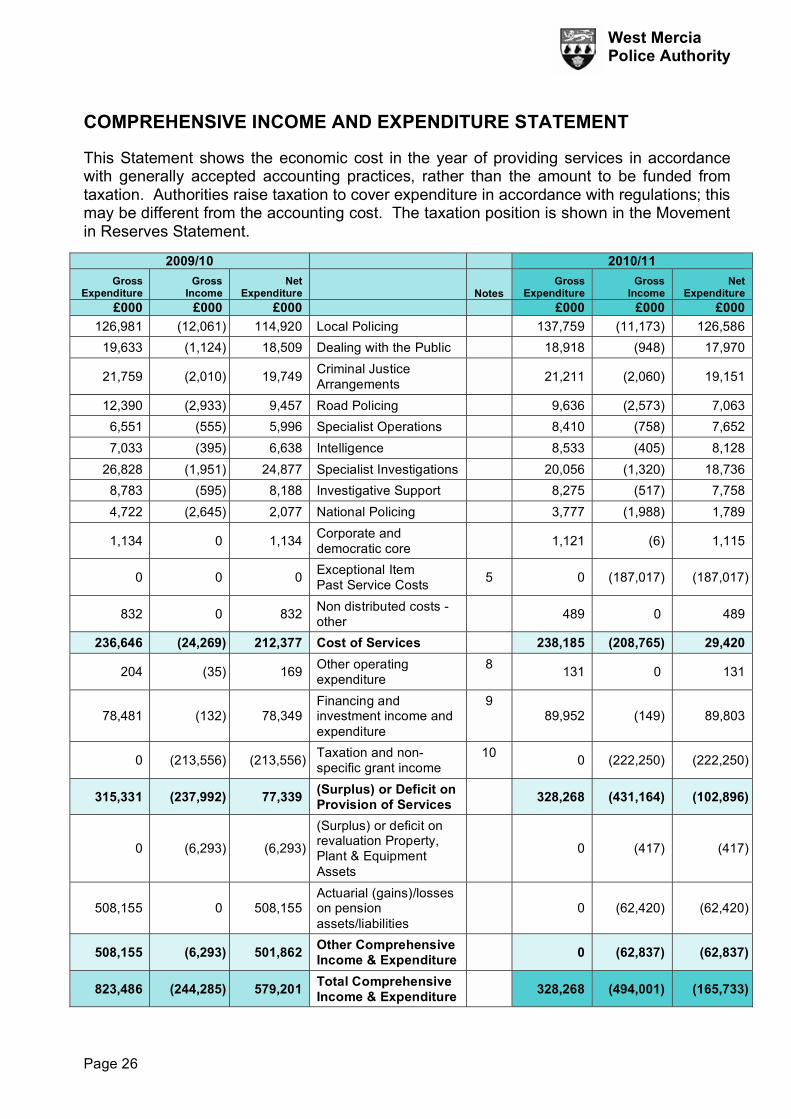

COMPREHENSIVE INCOME AND EXPENDITURE STATEMENT This Statement shows the economic cost in the year of providing services in accordance with generally accepted accounting practices, rather than the amount to be funded from taxation. Authorities raise taxation to cover expenditure in accordance with regulations; this may be different from the accounting cost. The taxation position is shown in the Movement in Reserves Statement.

2009/10 2010/11 Gross

Expenditure Gross

Income Net

Expenditure Notes Gross

Expenditure Gross

Income Net

Expenditure £000 £000 £000 £000 £000 £000

126,981 (12,061) 114,920 Local Policing 137,759 (11,173) 126,586 19,633 (1,124) 18,509 Dealing with the Public 18,918 (948) 17,970

21,759 (2,010) 19,749 Criminal Justice Arrangements

21,211 (2,060) 19,151

12,390 (2,933) 9,457 Road Policing 9,636 (2,573) 7,063 6,551 (555) 5,996 Specialist Operations 8,410 (758) 7,652 7,033 (395) 6,638 Intelligence 8,533 (405) 8,128

26,828 (1,951) 24,877 Specialist Investigations 20,056 (1,320) 18,736 8,783 (595) 8,188 Investigative Support 8,275 (517) 7,758 4,722 (2,645) 2,077 National Policing 3,777 (1,988) 1,789

1,134 0 1,134 Corporate and democratic core

1,121 (6) 1,115

0 0 0 Exceptional Item Past Service Costs 5 0 (187,017) (187,017)

832 0 832 Non distributed costs - other

489 0 489

236,646 (24,269) 212,377 Cost of Services 238,185 (208,765) 29,420

204 (35) 169 Other operating expenditure

8 131 0 131

78,481 (132) 78,349 Financing and investment income and expenditure

9 89,952 (149) 89,803

0 (213,556) (213,556) Taxation and non-specific grant income

10 0 (222,250) (222,250)

315,331 (237,992) 77,339 (Surplus) or Deficit on Provision of Services

328,268 (431,164) (102,896)

0 (6,293) (6,293)

(Surplus) or deficit on revaluation Property, Plant & Equipment Assets

0 (417) (417)

508,155 0 508,155 Actuarial (gains)/losses on pension assets/liabilities

0 (62,420) (62,420)

508,155 (6,293) 501,862 Other Comprehensive Income & Expenditure

0 (62,837) (62,837)

823,486 (244,285) 579,201 Total Comprehensive Income & Expenditure

328,268 (494,001) (165,733)

Statement of Accounts 2010/11

Page 27

West Mercia Police Authority

BALANCE SHEET The Balance Sheet shows the value as at the Balance Sheet date of the asset and liabilities recognised by the authority. The net assets of the authority (assets less liabilities) are matched by the reserves held by the authority. Reserves are reported in two categories. The first category of reserves are usable reserves, ie, those reserves that the authority may use to provide services, subject to the need to maintain a prudent level of reserves and any statutory limitations on their use (for example, the capital receipts reserve should only be used to fund capital expenditure or repay debt). The second category of reserves are those that the authority is not able to use to provide services. This category of reserves includes reserves that hold unrealised gains and losses (for example, the revaluation reserve) where amounts would only become available to provide services if the assets are sold; and reserves that hold timing differences shown in the Movement in Reserves Statement line ‘Adjustments between accounting basis and funding basis under regulations’. The opening balance sheet at 1 April 2009 is shown as a requirement of the transition to IFRS.

1 April 2009 31 March 2010 31 March 2011 £000 £000 Notes £000

88,026 84,836 Property, Plant & Equipment 11 83,556

410 425 Investment Property 12 470

1,140 1,060 Intangible Assets 13 880

20 10 Long Term Debtors 14 7

89,596 86,331 Long Term Assets 84,913

142 555 Assets Held for Sale 15 0

411 432 Inventories 16 457

11,216 10,897 Short Term Debtors 17 11,143

23,931 11,714 Cash and Cash Equivalents 18 17,271

35,700 23,598 Current Assets 28,871

(23,274) (16,622) Short Term Creditors 19 (14,251)

(23,274) (16,622) Current Liabilities (14,251)

(413) (420) Provisions 20 (516)

(10,881) (10,062) Long Term Borrowing 15 (10,062)

(1,130,733) (1,701,816) Liability Relating to Defined Benefit Pension Schemes 35 (1,542,213)

(35) (250) Capital Grants Receipts in Advance 31 (250)

(1,142,062) (1,712,548) Long Term Liabilities (1,553,041)

(1,040,040) (1,619,241) Net Assets (1,453,508)

Page 28

West Mercia Police Authority

1 April 2009 31 March 2010 31 March 2011

£000 £000 Notes £000 (23,328) (24,583) Usable Reserves 21 (34,775)

1,063,368 1,643,824 Unusable Reserves 22 1,488,283

1,040,040 1,619,241 Total Reserves 1,453,508

Statement of Accounts 2010/11

Page 29

West Mercia Police Authority

CASH FLOW STATEMENT The Cash Flow statement shows the changes in cash and cash equivalents of the authority during the reporting period. The statement shows how the authority generates and uses cash and cash equivalents by classifying cash flows as; operating, investing and financing activities. The amount of net cash flows arising from operating activities is a key indicator of the extent to which the operations of the authority are funded by way of taxation and grant income or from the recipients of services provided by the authority. Investing activities represent the extent to which cash outflows have been made for resources which are intended to contribute to the authority’s future service delivery. Cash flows arising from financing activities are useful in predicting claims on future cash flows by providers of capital (ie borrowing) to the authority.

2009/10 2010/11 £000 Notes £000

77,339 Net (surplus) or deficit on the provision of services (102,896)

(76,827) Adjustments to net (surplus) or deficit on the provision of services for non-cash movements 91,311

2,917 Adjustments for items included in the net (surplus) or deficit on the provision of services that are investing and financing activities

2,803

3,429 Net cash flows from Operating Activities 23 (8,782)

7,981 Investing Activities 24 3,225

807 Financing Activities 25 0

12,217 Net increase or decrease in cash and cash equivalents (5,557)

(23,931) Cash and cash equivalents at the beginning of the reporting period (11,714)

(11,714) Cash and cash equivalents at the end of the reporting period 18 (17,271)

Page 30

West Mercia Police Authority

NOTES TO THE ACCOUNTS 1. ACCOUNTING POLICIES

1.1 General Principles

The Statement of Accounts summarises the Authority’s transactions for the 2010/11 financial year and its position at the year end of 31 March 2011. The Authority is required to prepare an annual Statement of Accounts by the Accounts and Audit Regulations 2011 which must be prepared in accordance with proper accounting practices. These practices primarily comprise the Code of Practice on Local Authority Accounting in the United Kingdom 2010/11 and the Best Value Accounting Code of Practice 2010/11 supported by International Financial Reporting Standards (IFRS). The accounting convention adopted in the Statement of Accounts is principally historical cost, modified by the revaluation of certain categories of non-current assets and financial instruments.

1.2 Accruals of Income and Expenditure

Activity is accounted for in the year that it takes place, not simply when cash payments are made or received. In particular:

� Revenue from the sale of goods is recognised when the Authority transfers the

significant risks and rewards of ownership to the purchaser and it is probable that economic benefits or service potential associated with the transaction will flow to the Authority.

� Revenue from the provision of services is recognised when the Authority can measure reliably the percentage of completion of the transaction and it is probable that economic benefits or service potential associated with the transaction will flow to the Authority.

� Supplies are recorded as expenditure when they are consumed – where there is a gap between the date supplies are received and their consumption, they are carried as inventories on the Balance Sheet.

� Expenses in relation to services received (including services provided by employees) are recorded as expenditure when the services are received rather than when payments are made.

� Interest receivable on investments and payable on borrowings is accounted for respectively as income and expenditure on the basis of the effective interest rate for the relevant financial instrument rather than the cash flows fixed or determined by the contract.

� Where revenue and expenditure have been recognised but cash has not been received or paid, a debtor or creditor for the relevant amount is recorded in the

Statement of Accounts 2010/11

Page 31

West Mercia Police Authority

Balance Sheet. Where debts may not be settled, the balance of debtors is written down and a charge made to revenue for the income that might not be collected.

1.3 Cash and Cash Equivalents

Cash is represented by cash in hand and deposits with financial institutions repayable without penalty on notice of not more than 24 hours. Cash equivalents are investments that mature in no more than three months from the date of acquisition and that are readily convertible to known amounts of cash with insignificant risk of change in value. This is a change in accounting policy as a result of the introduction of IFRS. In the Cash Flow Statement, cash and cash equivalents are shown net of bank overdrafts that are repayable on demand and form an integral part of the Authority’s cash management.

1.4 Exceptional Items When items of income and expense are material, their nature and amount is disclosed separately, either on the face of the Comprehensive Income and Expenditure Statement or in the notes to the accounts, depending on how significant the items are to an understanding of the Authority’s financial performance.

1.5 Prior Period Adjustments, Changes in Accounting Policies and Estimates and Errors

Prior period adjustments may arise as a result of a change in accounting policies or to correct a material error. Changes in accounting estimates are accounted for prospectively, ie, in the current and future years affected by the change and do not give rise to a prior period adjustment. Changes in accounting policies are only made when required by proper accounting practices or the change provides more reliable or relevant information about the effect of transactions, other events and conditions on the Authority’s financial position or financial performance. Where a change is made, it is applied retrospectively (unless stated otherwise) by adjusting opening balances and comparative amounts for the prior period as if the new policy had always been applied. Material errors discovered in prior period figures are corrected retrospectively by amending opening balances and comparative amounts for the prior period. 1.6 Charges to Revenue for Non-Current Assets

Services are debited with the following amounts to record the cost of holding fixed assets during the year:

� depreciation attributable to the assets used by the relevant service

Page 32

West Mercia Police Authority

� revaluation and impairment losses on assets used by the service where there are no accumulated gains in the Revaluation Reserve against which the losses can be written off

� amortisation of intangible fixed assets attributable to the service.

The Authority is not required to raise council tax to fund depreciation, revaluation and impairment losses or amortisations. However, it is required to make an annual contribution from revenue towards the reduction in its overall borrowing requirement equal to an amount calculated on a prudent basis determined by the authority in accordance with statutory guidance. Depreciation, revaluation and impairment losses and amortisations are therefore replaced by the contribution in the General Fund Balance (Minimum Revenue Provision), by way of an adjusting transaction with the Capital Adjustment Account in the Movement in Reserves Statement for the difference between the two.

1.7 Employee Benefits

Benefits Payable During Employment Short-term employee benefits are those due to be settled within 12 months of the year-end. They include such benefits as wages and salaries, paid annual leave and paid sick leave, bonuses and non-monetary benefits (eg, cars) for current employees and are recognised as an expense for services in the year in which employees render service to the Authority. An accrual is made for the cost of holiday entitlements (or any form of leave, eg, time off in lieu) earned by employees but not taken before the year-end which employees can carry forward into the next financial year, being the period in which the employee takes the benefit. The accrual is charged to Surplus or Deficit on the Provision of Services, but then reversed out through the Movement in Reserves Statement so that holiday benefits are charged to revenue in the financial year in which the holiday absence occurs. This is a new accounting policy introduced under IFRS.

Termination Benefits This policy applies to members of police staff only. Termination benefits are amounts payable as a result of a decision by the Authority to terminate an officer’s employment before the normal retirement date or an officer’s decision to accept voluntary redundancy and are charged on an accruals basis to the Cost of Services in the Comprehensive Income and Expenditure Statement when the Authority is demonstrably committed to the termination of the employment of an officer or group of officers or making an offer to encourage voluntary redundancy. Where termination benefits involve the enhancement of pensions, statutory provisions require the General Fund Balance to be charged with the amount payable by the Authority to the pension fund or pensioner in the year, not the amount calculated according to the relevant accounting standards. In the Movement in Reserves Statement, appropriations are required to and from the Pensions Reserve to remove the notional debits and credits for pension enhancement termination benefits and

Statement of Accounts 2010/11

Page 33

West Mercia Police Authority

replace them with debits for the cash paid to the pension fund and pensioners and any such amounts payable but unpaid at the year-end. Post Employment Benefits Employees of the Authority are members of two separate pension schemes: � The Police Pension Scheme for Police Officers

� The Local Government Pensions Scheme for Police Staff administered by

Worcestershire County Council

Both schemes provide defined benefits to members (retirement lump sums and pensions), earned as employees worked for the Authority. However, the Police Pension Scheme for police officers is an unfunded defined benefit final salary scheme, meaning that there are no investment assets built up to meet the pensions liabilities, and cash has to be generated to meet the actual pensions payments as they eventually fall due. Under the Police Pension Fund Regulations 2007, if the amounts receivable by the pensions fund for the year is less than amounts payable, the Police Authority must annually transfer an amount required to meet the deficit to the pension fund. This cost is met by a central government pension top-up grant. If however, the pension fund is in surplus for the year, the surplus is required to be transferred from the pension fund to the Police Authority which then must repay the amount to central government. If police officers retire because of an injury on duty, they may be entitled to an Injury Award Pension. This cost is not met by the Home Office Top Up grant. It is part of the operating expenses of the Police Authority. Pension Schemes The Local Government Scheme and the Police Pension Scheme are accounted for as defined benefits schemes.

� The liabilities of the Worcestershire County Council pension fund attributable to the

Authority and the Police Pensions Scheme attributable to the Authority are included in the Balance Sheet on an actuarial basis using the projected unit method – ie, an assessment of the future payments that will be made in relation to retirement benefits earned to date by employees, based on assumptions about mortality rates, employee turnover rates, etc, and projections of projected earnings for current employees.

� International Accounting Standard (IAS)19 requires the nominal discount rate to be

set by reference to market yields on high quality corporate bonds or where there is no deep market in such bonds then by reference to government bonds.

For police pensions liabilities are discounted using the nominal discount rate based on government bond yield of appropriate duration plus an additional margin. Based on this methodology, the nominal discount rate at 31 March 2011 is assumed to be 5.7% a year, compared to 5.8% a year at 31 March 2010.

Page 34

West Mercia Police Authority

For police staff liabilities are discounted to their value at current prices, using a discount rate of 5.5% based on corporate bond yields.

� The pension increase assumption as at 31 March 2011 is based on the Consumer

Price Index (CPI) expectation of inflation rather than the Retail Price Index (RPI). This is as a result of the Government’s announcement that CPI is to be used for the indexation of public service pensions from April 2011.

� The assets of Worcestershire County Council’s pension fund attributable to the

Authority are included in the Balance Sheet at their fair value:

- quoted securities – current bid price - unquoted securities – professional estimate - unitised securities – current bid price - property – market value

� The change in the net pensions liability is analysed into seven components:

- current service cost – the increase in liabilities as a result of years of service

earned this year – allocated in the Comprehensive Income and Expenditure Statement to the services for which the employees worked

- past service cost – the increase in liabilities arising from current year decisions whose effect relates to years of service earned in earlier years – debited to the Surplus or Deficit on the Provision of Services in the Comprehensive Income and Expenditure Statement as part of Non Distributed Costs

- interest cost – the expected increase in the present value of liabilities during the year as they move one year closer to being paid – debited to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement

- expected return on assets – the annual investment return on the fund assets attributable to the Authority, based on an average of the expected long-term return – credited to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement

- gains or losses on settlements and curtailments – the result of actions to relieve the Authority of liabilities or events that reduce the expected future service or accrual of benefits of employees – debited or credited to the Surplus or Deficit on the Provision of Services in the Comprehensive Income and Expenditure Statement as part of Non Distributed Costs.

- actuarial gains and losses – changes in the net pensions liability that arise because events have not coincided with assumptions made at the last actuarial valuation or because the actuaries have updated their assumptions – debited to the Pensions Reserve

- contributions paid to the Worcestershire County Council’s pension fund – cash paid as employer’s contributions to the pension fund in settlement of liabilities; not accounted for as an expense.

Statement of Accounts 2010/11

Page 35

West Mercia Police Authority

In relation to retirement benefits, statutory provisions require the General Fund Balance to be charged with the amount payable by the Authority to the pension fund or directly to pensioners in the year, not the amount calculated according to the relevant accounting standards. In the Movement in Reserves Statement, this means that there are appropriations to and from the Pensions Reserve to remove the notional debits and credits for retirement benefits and replace them with debits for the cash paid to the pension fund and pensioners and any such amounts payable but unpaid at the year-end. The negative balance that arises on the Pensions Reserve thereby measure the beneficial impact to the General Fund of being required to account for retirement benefits on the basis of cash flows rather than as benefits are earned by employees. Discretionary Benefits

The Authority also has restricted powers to make discretionary awards of retirement benefits in the event of early retirements. Any liabilities estimated to arise as a result of an award to any member of staff are accrued in the years of the decision to make the award and accounted for using the same policies as are applied to the Local Government Pension Scheme.

1.8 Financial Instruments

Financial Liabilities Financial liabilities are recognised on the Balance Sheet when the Authority becomes a party to the contractual provisions of a financial instrument and are initially measured at fair value and are carried at their amortised cost. Annual charges to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement for interest payable are based on the carrying amount of the liability, multiplied by the effective rate of interest for the instrument. The effective interest rate is the rate that exactly discounts estimated future cash payments over the life of the instrument to the amount at which it was originally recognised. For the borrowings that the Authority has, this means that the amount presented in the Balance Sheet is the outstanding principal repayable (plus accrued interest); and interest charged to the Comprehensive Income and Expenditure Statement is the amount payable for the year according to the loan agreement. The following recommended policy will be adopted in respect of gains and losses on the repurchase or early settlement of borrowing. However, in 2010/11 West Mercia did not have any transactions of this nature. Gains and losses on the repurchase or early settlement of borrowing are credited and debited to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement in the year of repurchase/settlement. However, where repurchase has taken place as part of a restructuring of the loan portfolio that involves the modification or exchange of existing instruments, the premium or discount is respectively deducted from or added to the amortised cost of the new or modified loan and the write-down to the Comprehensive

Page 36

West Mercia Police Authority

Income and Expenditure Statement is spread over the life of the loan by an adjustment to the effective interest rate. Where premiums and discounts have been charged to the Comprehensive Income and Expenditure Statement, regulations allow the impact on the General Fund Balance to spread over future years. The Authority will adopt a policy of spreading the gain or loss over the term that was remaining on the loan against which the premium was payable or discount receivable when it was repaid. The reconciliation of amounts charged to the Comprehensive Income and Expenditure Statement to the net charge required against the General Fund Balance is managed by a transfer to or from the Financial Instruments Adjustment Account in the Movement in Reserves Statement. Financial Assets Financial assets are classified into two types:

� loans and receivables – assets that have fixed or determinable payments but are

not quoted in an active market � available-for-sale assets – assets that have a quoted market price and/or do not

have fixed or determinable payments.

Loans and Receivables Loans and receivables are recognised on the Balance Sheet when the Authority becomes a party to the contractual provisions of a financial instrument and are initially measured at fair value. They are subsequently measured at their amortised cost. Annual credits to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement for interest receivable are based on the carrying amount of the asset multiplied by the effective rate of interest for the instrument. For most of the loans that the Authority has made, this means that the amount presented in the Balance Sheet is the outstanding principal receivable (plus accrued interest) and interest credited to the Comprehensive Income and Expenditure Statement is the amount receivable for the year in the loan agreement. When assets are identified as impaired because of a likelihood arising from a past event that payments due under the contract will not be made, the asset is written down and a charge made to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement. The impairment loss is measured as the difference between the carrying amount and the present value of the revised future cash flows discounted at the asset’s original effective interest rate. West Mercia has no impairment losses imposed on the carrying amounts in 2010/11. Any gains and losses that arise on the derecognition of an asset are credited or debited to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement.

Statement of Accounts 2010/11

Page 37

West Mercia Police Authority

Available-for-Sale Assets The following recommended policy has been adopted. However, in 2010/11 West Mercia has no financial instruments which are relevant to this policy. Available-for-sale assets are recognised on the Balance Sheet when the Authority becomes a party to the contractual provisions of a financial instrument and are initially measured and carried at fair value. Where the asset has fixed or determinable payments, annual credits to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement for interest receivable are based on the amortised cost of the asset multiplied by the effective rate of the interest for the instrument. Where there are no fixed or determinable payments, income (eg, dividends) is credited to the Comprehensive Income and Expenditure Statement when it becomes receivable by the Authority. Assets are maintained in the Balance Sheet at fair value. Values are based on the following principles: � instruments with quoted market prices – the market price � other instruments with fixed and determinable payments – discounted cash flow

analysis � equity shares with no quoted market prices – independent appraisal of company

valuations.

Changes in fair value are balanced by an entry in the Available-for-Sale Reserve and the gain/loss is recognised in the Surplus or Deficit on Revaluation of Available-for-Sale Financial Assets. The exception is where impairment losses have been incurred – these are debited to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement, along with any net gain or loss for the asset accumulated in the Available-for-Sale Reserve. Where assets are identified as impaired because of a likelihood arising from a past event that payments due under the contract will not be made (fixed or determinable payments) or fair value falls below cost, the asset is written down and a charge made to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement. If the asset has fixed or determinable payments, the impairment loss is measured as the difference between the carrying amount and the present value of the revised future cash flows discounted at the asset’s original effective interest rate. Otherwise, the impairment loss is measured as any shortfall of fair value against the acquisition cost of the instrument (net of any principal repayment and amortisation). Any gains and losses that arise on the derecognition of the asset are credited or debited to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement, along with any accumulated gains or losses previously recognised in the Available-for-Sale Reserve.

Page 38

West Mercia Police Authority