Embed Size (px)

Citation preview

Welcome to

LifeAdvance 24 Critical Illnesses plus Illness Assist

November 2004 Policy Series

CI Market in Canada

Challenges still present in Canada: Lack of claims experience Product was developed on statistics Desire to preserve premium rate guarantees Aggressive product features How will advances in medical science affect

CI?

Munich Re March 2004

Bright Future

Long-term sustainable productGreater awareness, availability of the product

with innovative enhancementsInitial claims are within expected limitsLearning from other countries’ ‘growing pains’

and avoiding some major pitfalls

Munich Re March 2004

Canadian CI Claims

Munich Re March 2004.

51%

43%

1%

1%4%

CancerCardio V.MSComaOther

Male Female

Policy Series 2004 Heart Attack

Heart Attack means the acute presentation of heart symptoms accompanied by the death of a portion of heart muscle as a result of inadequate blood supply and as evidenced by:

a) new electrocardiographic (ECG) changes indicative of a myocardial infarction; and

b) the elevation of cardiac markers to levels considered diagnostic for acute myocardial infarction in accordance with standardized laboratory values for the accredited hospital in Canada or the U.S. performing the test and with criteria published by one of the following:

the Canadian Cardiovascular Society the American Heart Association; or the American College of Cardiology,

or a successor organization to any of the above.

Heart Attack does not include: Elevated cardiac markers after coronary angioplasty unless

there are diagnostic changes of new Q wave infarction on the ECG.

Policy Series 2004 Stroke

Stroke means a cerebrovascular event producing neurological sequelae lasting more than 30 days and caused by intracranial thrombosis or haemorrhage, or embolism from an extra-cranial source.

There must be evidence of measurable, objective neurological deficit.

For greater certainty, findings on imaging studies, such as lacunar infarcts, which are not compatible with clinical neurological signs due to a cerebrovascular event do not satisfy the definition of Stroke.

Stroke does not include transient ischemic attacks.For the purposes of this definition, transient ischemic attack means a neurological event caused by focal brain or retinal ischemia with measurable objective evidence of neurological sequelae lasting less than 24 hours with or without imaging study changes.

Policy Series 2004 Parkinson’s DiseaseParkinson’s Disease means permanent primary idiopathic Parkinson’s disease, resulting in significant neurological impairment or in loss of cognitive function.

The degree of neurological impairment or loss of cognitive function must be sufficient to cause an inability to perform, 2 or more of the following 6 activities of daily living while participating in a generally accepted drug treatment program:

• dressing – the ability to put on, remove, fasten and unfasten all necessary clothing, braces, artificial limbs or surgical appliances.• toileting — the ability to get to and from the toilet and complete related personal hygiene;• transferring — the ability to move yourself into or out of a bed, chair, or wheelchair;• feeding — the ability to get food from a plate into the mouth; • driving — the ability to legally operate a motorized vehicle; and• mobility — the ability to walk 10 metres without aid.

The Diagnosis must include a current physical assessment from an occupational therapist who is not related by blood or marriage to the Insured or the Owner, and is not in a business relationship with the Insured or the Owner.

Policy Series 2004 Loss of Speech

Loss of Speech means the total and irreversible loss of the ability to speak due directly to damage to the speech organs (commonly known as the “voice box”) vocal cords as the result of injury or disease.

New Covered Conditions

Aplastic Anemia– means the complete and irreversible bone marrow failure resulting

in anemia, neutropenia and thrombocytopenia.

– Most common in adolescents and young adults

– Potentially life threatening - people who could not receive a bone transplant may have not been previously covered

Bacterial Meningitis– It is a bacterial infection of the fluid in a person's spinal cord and

fluid that surrounds the brain. – Particularly adding value for LifeAdvance Child rider

RMC Management Meeting 2004

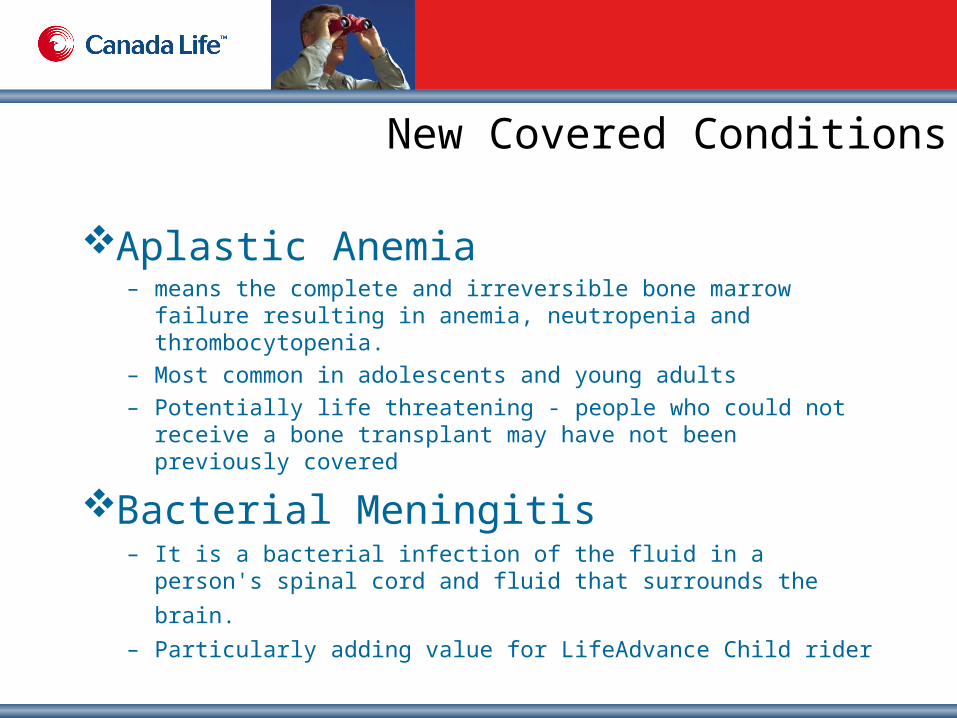

Rate Increases by Plan Type

* Approximate overall rate increase for Base Plans

** Ignores the impact of removing the built-in ROP from the Lifetime plan

0

5

10

15

20

25

T75/65 T75 T10 Lifetime **

Percentage Increase

Improved Illness Assist Benefit

$250,000 $275,000Canada LifeCompany A Company B

$250,000

10% to max $25,00025% to max $50,00010% to max $15,000

Example $250,000 lump-sum benefit

More Improvements with LifeAdvance Illness Assist –

Waiting period has been removed Does not reduce premium payback benefit

More Improvements with LifeAdvance Illness Assist –

Waiting period has been removed Does not reduce premium payback benefit

$250,000CI Lump-sum

$25,000 Illness Assist$25,000 Illness Assist

$250,000CI Lump-sum

$50,000 Illness Assist$50,000 Illness Assist

$250,000CI Lump-sum

$25,000 Illness Assist$25,000 Illness Assist

New Surgery AdvanceExample $250,000 lump-sum benefit

Canada LifeCompany A Company B

10% to max $15,00010% to max $10,000Not Applicable

CI Lump-sum

Illness AssistIllness Assist

Illness AssistIllness Assist

CI Lump-sum

Surgery AdvanceSurgery Advance

CI Lump-sum

Illness AssistIllness Assist

Advance BenefitAdvance Benefit

Canada Life continues its trendsetting pace

1 in 4.6 men and 1 in 7.8 women will develop both heart disease and cancer during their lifetime.*

*Based on Heart and Stroke, 2004 and National Cancer Institute of Canada: Canadian Cancer statistics 2004 During their lifetime, the probability of developing cancer is 1 in 2.6 for women and 1 in 2.3 for men and the probability of developing heart disease is 1 in 3 for women and 1 in 2 for men. The probability of developing both cancer and heart disease is calculated assuming the conditions are independent,

Second Event Rider

Heart Attack or Stroke Life-Threatening Cancer

Life-Threatening Cancer Heart Attack

If the insured received a critical illness benefit before his or

her 65th birthday for:

The second event coverage will be the lesser of 50% of the benefit amount selected for the basic policy and $50,000.

Second Event Rider In Action

30 days 12 months

1st Event

Second event rider coverage continues until the earlier of 11 years or age 75

2nd Event

Elimination period

$50,000

$250,000

Premium Payback Riders

Introducing

Flexibility & Affordability

Lifetime Permanent (T100 Paid up at age 100)

Ideal for wealthy client

Who want to quick pay

Option AIt’s also ideal for middle income

clients.

Option Byounger clients and

those who would like the most affordable

premium payback offer.

Option C

Premium Payback at Withdrawal Request T100

Issue Ages18-65

100%Year 15

50%Year 10

Option A

100%Year 20

75%Year 15

Option B

100%Year 25

50%Year 15

Option C

Note: Optional withdrawal dates available at each year After the first option date.

Price Comparisons With ROP – T100 Option A

Existing Plan New Plan – Option A

Age 35 $1,088

$1,980

% increase

44%

Age 40 $1,489

Age 45 $2,145

Age 50 $3,024

$1,564

$2,918

$4,281

33%

36%

41%

Note: T100 plan, $100,000 coverage with ROPD and ROP option A

Price Comparisons With ROP – T100 Option B

Existing Plan New Plan – Option B

Age 35 $1,088

$1,779

% increase

32%

Age 40 $1,489

Age 45 $2,145

Age 50 $3,024

$1,438

$2,581

$3,728

20%

21%

23%

Note: T100 plan, $100,000 coverage with ROPD and ROP option B

Price Comparisons With ROP – T100 Option C

Existing Plan New Plan – Option C

Age 35 $1,088

$1,162

% increase

25%

Age 40 $1,489

Age 45 $2,145

Age 50 $3,024

$1,360

$2,340

$3,444

11%

9%

14%

Note: T100 plan, $100,000 coverage with ROPD and ROP option C

Partial WithdrawalsReduced Paid-up Pay-up all future premiums by reducing coverage Options begins once PPB reaches 100% Each 5 year interval Rate card will be available

Receive eligible premiums when surrendering a portion of coverage Remaining coverage stays inforce with premium payback

Built-in Options

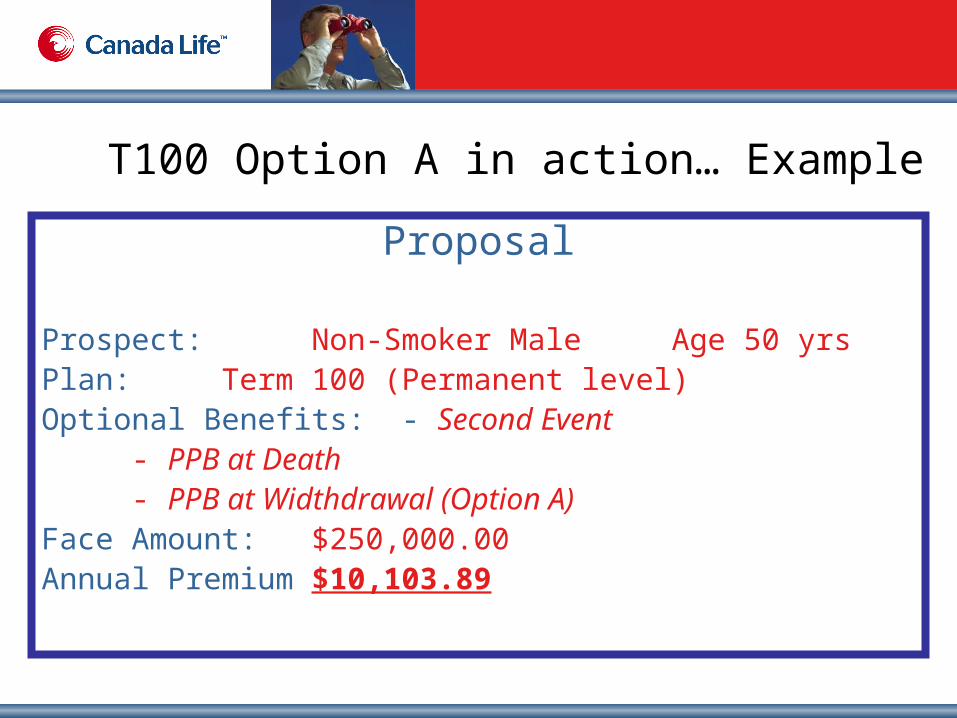

T100 Option A in action… Example

Proposal

Prospect: Non-Smoker Male Age 50 yrsPlan: Term 100 (Permanent level)Optional Benefits: - Second Event

- PPB at Death- PPB at Widthdrawal (Option A)

Face Amount: $250,000.00Annual Premium $10,103.89

75

Premium Payback

$50,519

Premium Payback

$151,558

50% Partial Withdrawal at age 65Face Amount $125,000Partial Premium Payback $ 70,398

Paid-Up FeatureAt age 75

Premium Payback $251,885Result

$250,000 Paid-Up PolicyPlus

$64,365 Premium Payback

Age 50

Option A - T100 (Permanent)

Level Term to 75 Premium Payback Options

Issue Ages18-49

100%Year 15

50%Year 10

Option 1

100%Age 65

50%Age 60

Option 2

100%Age 75

0%At Expiry

Issue Ages 18-60

Note: Optional withdrawal dates available at each year After the first option date on option 1 and option 2.

Issue Ages18-60

T75 with PPB Cost CompareT75

With PPB(Option 1)

T75With PPB(Option 2)

T75With PPBXAt Expiry

Male, Age 40, Non-SmokerBenefit Amount: $100,000

Annual Premium $1,902 $1,586<16% A

$1,443<23% A, <8% B

Total PremiumsPaid

$66,557 $55,478 $50,480

PPB at 10th

Anniversary$9,509 $0.00 $0.00

PPB at 15th

Anniversary$28,526

100% return$0.00

50% age 60100% age 65

$0.00100% Expiry

Note: The premium payback benefit amount will vary from the amount illustrated – upward or downward – if the policy is modified at the request of the owner by, example, the addition or removal of optional riders/benefits.

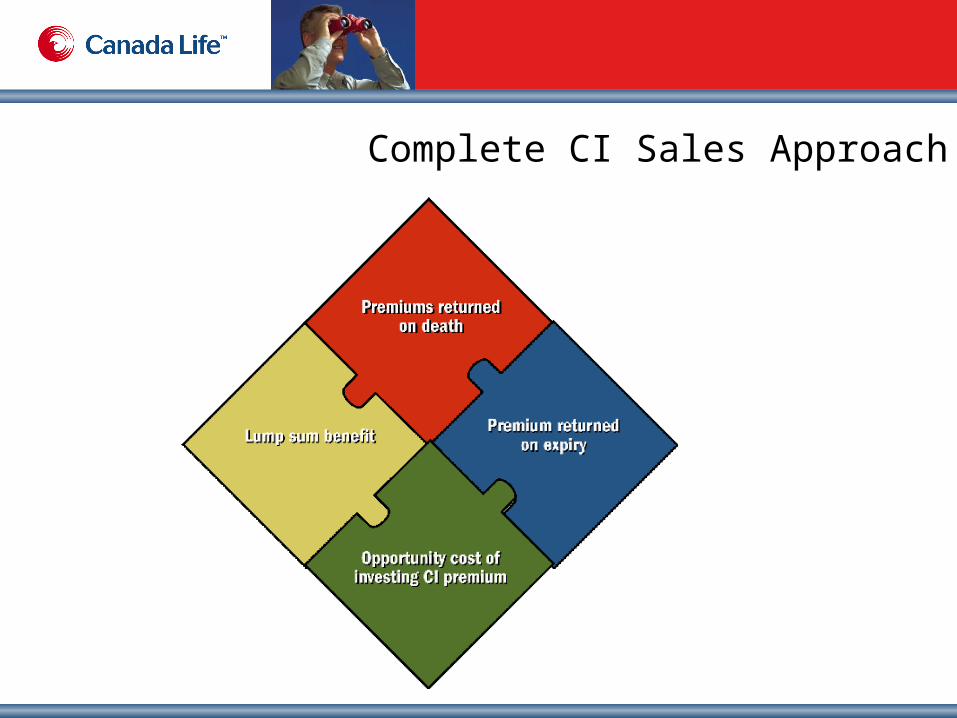

Complete CI Sales Approach

Level Term to age 75

40 yrs 45 yrs 50 yrs 55 yrs 60 yrs 65

Monthly Investment $1,000.00

Assume 6% annually

$679,581

Asset Protection Strategy

$583,733

Monthly Investment $1,000.00

*Less CI Monthly Premium $ 141.04

Net Monthly Investment $ 858.96

Issue ages 18-49 *CI Plan Level T75 – S100,000, 2nd Event, PPB/D/W/E

In 15 yrs $100,000 are required To cover expenses incurredDue to a Critical Illness

$410,953

Opportunity Cost

After 46% marginal tax rate

$ 53,536

$ 28,909

$1,156Annual opportunity cost ………………………………

Before tax opportunity cost

Annual LifeAdvance Premium $1,692.48 versus

Example Cont’d

ROP Benefit available at age 65* $ 42,312

Invest $1,000 per month at 6% over 25 years $679,581

Invest $858.96 per year at 6% over 25 years $583,733

+

10yrs R&C with Premium Payback Riders100%

Year 15

50%Year 10

Issue age 50 >PPBW

100%Age 65

50%Age 60

Issue age < 50

PPBW

Note: Optional withdrawal dates available at each year After the first option date on PPBW.

Issue Ages18-60

100%Age 75

0%At Expiry

PPBX

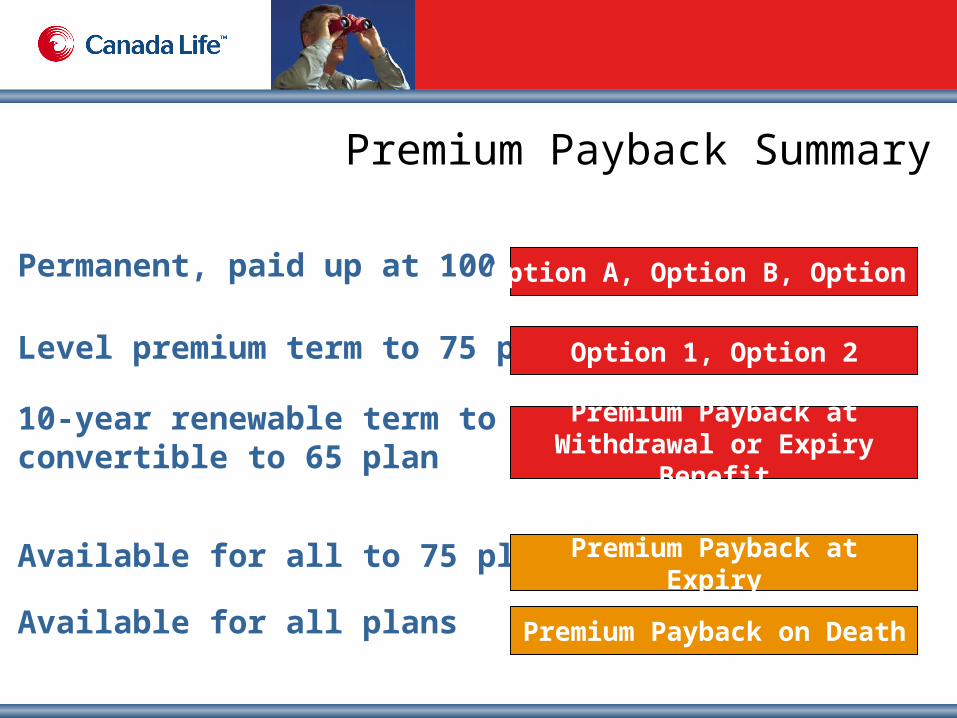

Premium Payback Summary

Permanent, paid up at 100 plan

Level premium term to 75 plan

10-year renewable term to 75, convertible to 65 plan

Available for all to 75 plans

Available for all plans

Option A, Option B, Option C

Option 1, Option 2

Premium Payback at Withdrawal or Expiry Benefit

Premium Payback at Expiry

Premium Payback on Death

Applications dated on or before December 31, 2004 and received in Head Office by January 10, 2005 - clients may apply for existing policy series (22 critical illnesses plus illness assist benefit) or new November 2004 policy series (24 critical illnesses plus illness assist benefit) by specifying on application.

.

Transition Rules

Applications dated on or after January 1, 2005 or received in Head Office after January 10, 2005 - will be issued as new November 2004 policy series only.

“It’s Not the Strongest of the Species That Survives, nor the Most Intelligent,

but Rather the One Who Is Responsive to Change.”

“It’s Not the Strongest of the Species That Survives, nor the Most Intelligent,

but Rather the One Who Is Responsive to Change.”

Charles Darwin

1934 Depression 1935 Spanish civil war 1936 Economy still struggling 1937 Recession 1938 War clouds gather 1939 War in Europe 1940 France falls 1941 Pearl Harbor 1942 Wartime price controls 1943 Industry mobilizes 1944 Consumer goods shortages 1945 Postwar recession predicted 1946 Dow tops 200 – market too high 1947 Cold war begins1948 Berlin blockade 1949 Russia explodes A-bomb 1950 Korean War 1951 Excess profits tax1952 U.S. seizes steel mills 1953 Russia explodes H-bomb 1954 Dow tops 300 – market too high 1955 Eisenhower illness1956 Suez crisis

1957 Russia launches Sputnik 1958 Recession 1959 Castro seizes power in Cuba 1960 Russia downs U-2 plane 1961 Berlin Wall erected 1962 Cuban missile crisis 1963 Kennedy assassinated 1964 Gulf of Tonkin 1965 Civil rights marches 1966 Vietnam War escalates 1967 Newark race riots 1968 USS Pueblo seized 1969 Money tightens – markets fall 1970 Cambodia invaded – Vietnam War 1971 Wage/price freeze 1972 Largest U.S. trade deficit ever 1973 Energy crisis 1974 Nixon resigns 1975 Clouded economic prospects 1976 Economic recovery slows 1977 Market slumps 1978 Interest rates rise 1979 Oil prices skyrocket

1980 Interest rates at all-time high 1981 Steep recession begins1982 Worst recession in 40 years 1983 U.S. Embassy, Marine barracks bombed 1984 Record federal deficits1985 Economic growth slows 1986 Dow nears 2000 – market too high 1987 Record-setting market decline 1988 Junk bond scandal 1989 October “Mini-Crash” 1990 Persian Gulf crisis 1991 Recession 1992 Riots sweep Los Angeles 1993 Bombing of World Trade Center 1994 Rising U.S. interest rates 1995 Oklahoma City bombing 1996 U.S. government shutdown 1997 Collapse of Thailand economy 1998 President impeachment proceedings1999 Y2K 2000 Internet stocks plummet 2001 September 11 terrorist attacks 2002 WorldCom accounting scandal 2003 SARS/Blackout/War in IRAQ2004 US Election

Reasons Not to Invest

Source : 2000 Financial Knowledge Inc

Tax atRate of Inflation

3%3% 4%4% 5%5% 6%6% 7%7% 8%8%

25% 4.0 5.3 6.6 8.0 9.3 10.7

30% 4.3 5.7 7.1 8.6 10.1 11.4

35% 4.6 6.2 7.7 9.2 10.8 12.3

40% 5.0 6.6 8.3 10.0 11.7 13.3

45% 5.4 7.2 9.1 10.9 12.7 14.5

50% 6.0 8.0 10.0 12.0 14.0 16.0

GOING BROKE SLOWLY