Embed Size (px)

Citation preview

WELCOME TO

NAMIBIAN TRUSTS – TO TRUST OR

NOT TO TRUST PRESENTED ON 5 APRIL 2016

BY

PROFESSOR WILLIE M VAN DER WESTHUIZEN

MILLERS INC

GEORGE

Member of the PhatshoaneHenney Group

INTRODUCTION

• From a South African perspective the Namibian

trust law is a bit like Michael J Fox’s movie

“Back to the future”

• To understand the future of the Namibian Trust

Law one has to move a bit back in history

• The previous trust legislation of South Africa

namely, The Trust Moneys Protection Act, 34 of

1934 is still applicable in Namibia which was

administered by South Africa until its

independence in 1990.

Millers Attorneys George © member of PhatshoaneHenney Group 2

INTRODUCTION

• This does not mean that the Namibian

legislation is outdated. The question is more a

matter of whether the newer RSA legislation is

an improvement – The answer falls outside the

scope of this presentation

• The differences, although sometimes subtle, is

important to note.

• We will thus in this presentation concentrate on

the differences / similarities, some pitfalls &

common errors, application possibilities & the

tax implications and then decide whether to

trust or not to trust the Namibian Trust.

Millers Attorneys George © member of PhatshoaneHenney Group 3

Millers Attorneys George © Member of the PhatshoaneHenney Group 4

FORMAT Focus will be on practical discussion and points

substantiated by principles, case and relevant

law and divided in:

1. PART 1 : THE DIFFERENCES / SIMILARITIES,

SOME PITFALLS & COMMON ERRORS,

APPLICATION POSSIBILITIES & THE TAX

IMPLICATIONS

2. PART 2 : ADDITIONAL REFERENCE SLIDES

AS FURTHER READING MATERIAL -- NOT

DISCUSSED (AS SUPPLEMENTED BY THE

BIBLIOGRAPHY – SLIDE 54)

PART 1A

DIFFERENCES

&

SIMILARITIES

Millers Attorneys George © Member of the PhatshoaneHenney Group 5

UNIQUE OR HYBRID TRUST

LAW SYSTEM IN NAMIBIA &

THE RSA

Millers Attorneys George © member of the PhatshoaneHenney Group 6

NAMIBIA IS A CIVIL LAW

COUNTRY • But the Common Law (as opposed to statutory law) of

Namibia applicable to trusts is the same as for South

Africa

• Thus the trust creation and administration as well as the

powers and fiduciary duties of trustees are the same,

save for some adaptations in respect of local Namibian

legislation.

• The Namibian trust law is, as said, regulated by the Trust

Monies Protection Act of 1934, which Act was repealed

in South Africa in 1989 and this causes some important

differences (but also some unsuspected similarities)

Millers Attorneys George © Member of the PhatshoaneHenney Group 7

Millers Attorneys George © member of the PhatshoaneHenney Group 8

UNIQUE LOCAL TRUST LAW (B2)

ROMAN DUTCH LAW

CIVIL LAW COUNTRY ENGLISH LAW

COMMON LAW COUNTRIES

TRUST IN WIDE SENSE TRUST IN STRICT SENSE

NAMIBIAN / RSA TRUST LAW

REAL TRUST “BEWIND” TRUST

TRUSTEE “LEGAL” OWNER CURATOR / EXECUTOR

ADMINISTRATOR/CONTROL

BENEFICIARY :

ONLY PERSONAL RIGHT

BENEFICIARY :

OWNER WITH VESTED RIGHT

NAMIBIA IS A CIVIL LAW

COUNTRY • As in the RSA the typical discretionary trust can also be

created in Namibia by making a small donation of say

N$100 to the trustees (the Namibian dollar is coupled to

the SA Rand) whereby the beneficiaries then possess

merely a spes (hope) to receive benefits from the trust

via the exercising of their discretion by the trustees

• In this way the trust is the ideal protective vehicle for the

beneficiary who may find him- or herself in financial

difficulties or who is experiencing risks because of

relationship problems.

Millers Attorneys George © Member of the PhatshoaneHenney Group 9

NB FORMALITIES IN RE CREATION (B9.2.2*)

• In Namibia however, where the donation exceeds a N$1000

the deed of donation, and thus the trust deed will require

specific important formalities

• Until 1956 a donation, whether executed or not, was

revocable in regard to the amount thereof in excess of

£500 (R1000) unless it was registered in the deeds office or

embodied in a notarial deed.(See LAWSA vol 8 part 1 par

276)

Millers Attorneys George © member of the PhatshoaneHenney Group 10

NB FORMALITIES IN RE CREATION (B6.1 & B9.2.2*)

• Thus prior to the enactment in the RSA of section 5 of the General Law Amendment Act 50 of 1956 it was required of donations of more than £500 (R1000) to be notarially executed. Section 5 states that “no donation concluded after the commencement of this Act shall be invalid merely by reason of the fact that it is not registered or notarially executed”.

• This section 5 was however not made applicable to Namibia where currently donations of more than N$1000 is still required to be notarially executed

• B6.1 & B9.2.2 = Wills & Trusts see Bibliography at end

Millers Attorneys George © member of the PhatshoaneHenney Group 11

PART 1B

SOME PITFALLS /

COMMON ERRORS,

Millers Attorneys George © Member of the PhatshoaneHenney Group 12

MOST COMMON REASONS

FOR INVALIDITY THAT ARE

STILL GREY AREAS IN NAMIBIA

1. Formation of a trust with only oneself (See slide

65)

2. Object too vague; changing object (Slides 66-69)

3. Exceeding the specific power of appointment

(Slides 70-73)

4. Variation where beneficiaries have accepted

benefits– certain areas still uncertain despite

Potgieter-case (See slides 74-81)

Millers Attorneys George © member of the PhatshoaneHenney Group 13

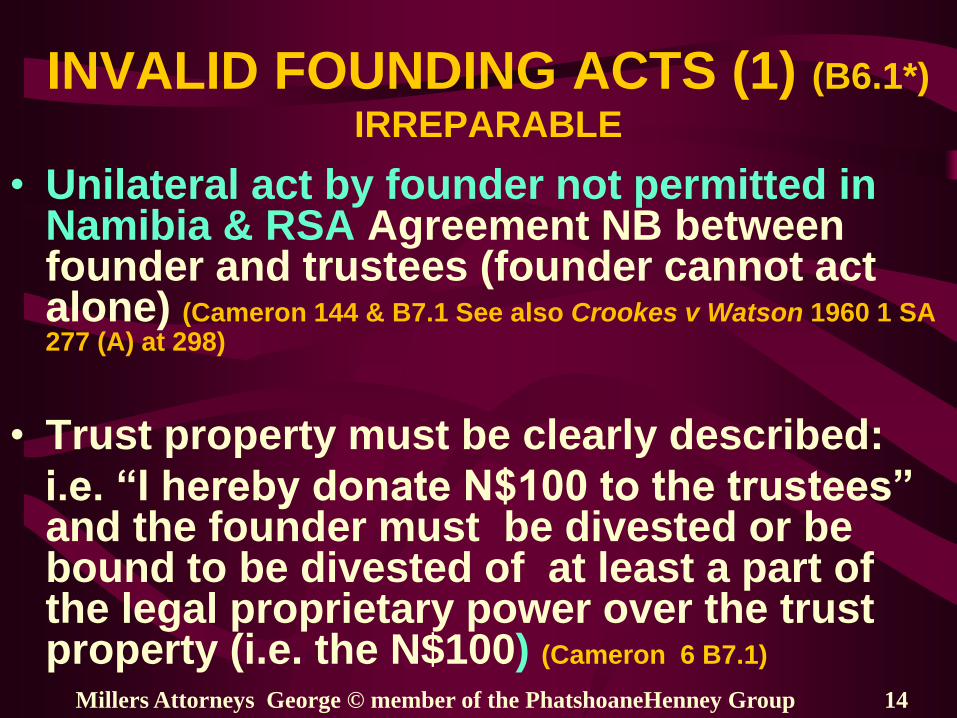

INVALID FOUNDING ACTS (1) (B6.1*)

IRREPARABLE

• Unilateral act by founder not permitted in Namibia & RSA Agreement NB between founder and trustees (founder cannot act alone) (Cameron 144 & B7.1 See also Crookes v Watson 1960 1 SA 277 (A) at 298)

• Trust property must be clearly described:

i.e. “I hereby donate N$100 to the trustees” and the founder must be divested or be bound to be divested of at least a part of the legal proprietary power over the trust property (i.e. the N$100) (Cameron 6 B7.1)

• B6.1= Wills & Trusts see Bibliography at end

Millers Attorneys George © member of the PhatshoaneHenney Group 14

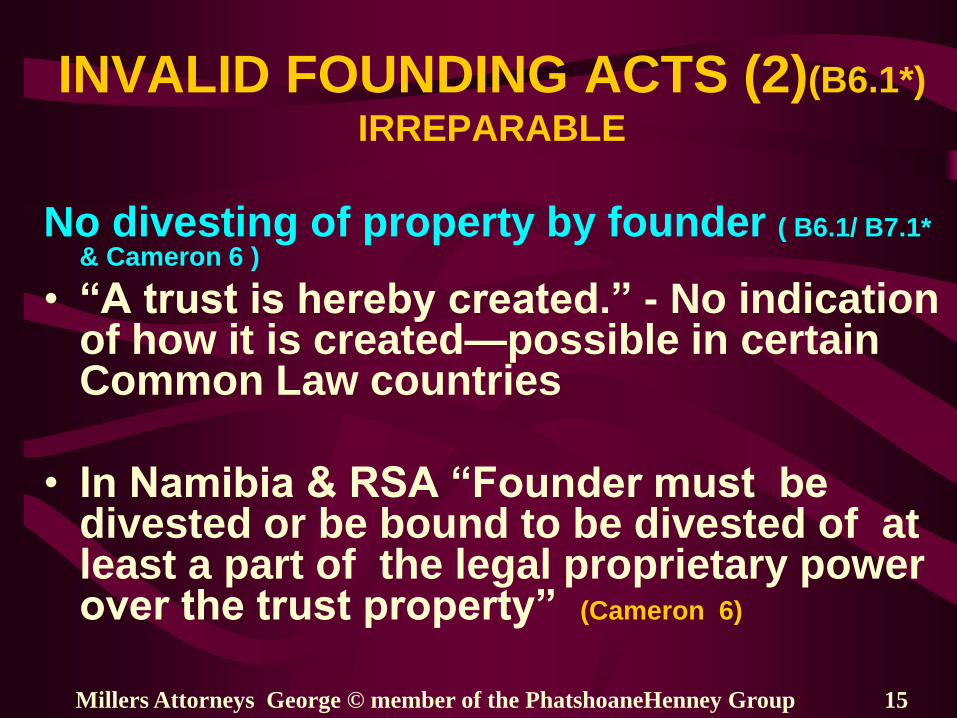

INVALID FOUNDING ACTS (2)(B6.1*)

IRREPARABLE

No divesting of property by founder ( B6.1/ B7.1* & Cameron 6 )

• “A trust is hereby created.” - No indication of how it is created—possible in certain Common Law countries

• In Namibia & RSA “Founder must be divested or be bound to be divested of at least a part of the legal proprietary power over the trust property” (Cameron 6)

Millers Attorneys George © member of the PhatshoaneHenney Group 15

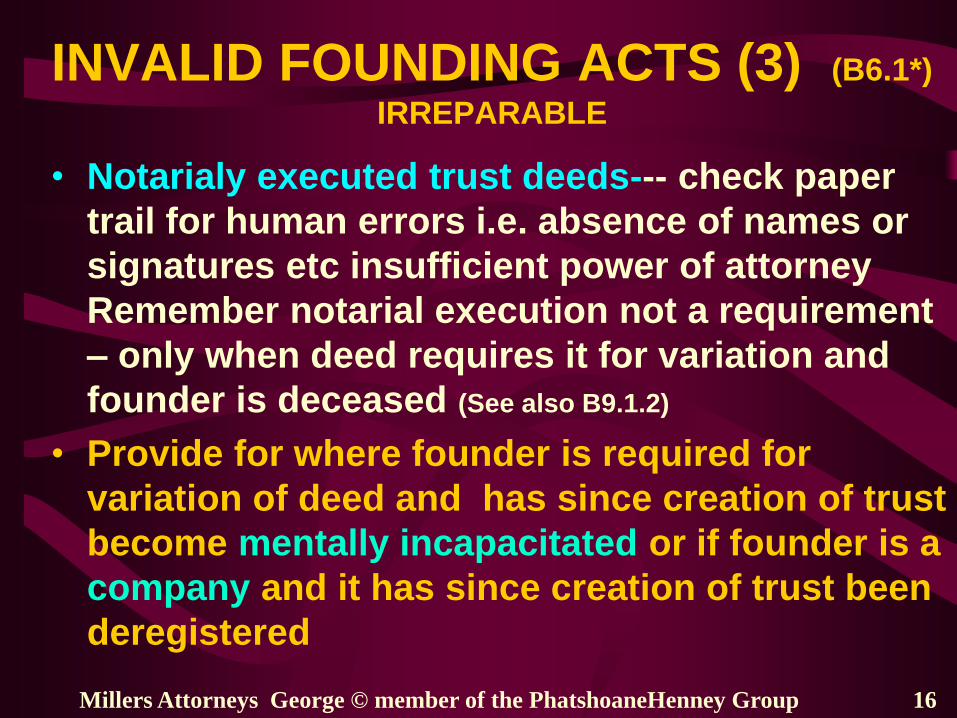

INVALID FOUNDING ACTS (3) (B6.1*)

IRREPARABLE

• Notarialy executed trust deeds--- check paper

trail for human errors i.e. absence of names or

signatures etc insufficient power of attorney

Remember notarial execution not a requirement

– only when deed requires it for variation and

founder is deceased (See also B9.1.2)

• Provide for where founder is required for

variation of deed and has since creation of trust

become mentally incapacitated or if founder is a

company and it has since creation of trust been

deregistered

Millers Attorneys George © member of the PhatshoaneHenney Group 16

Millers Attorneys George © member of the PhatshoaneHenney Group 17

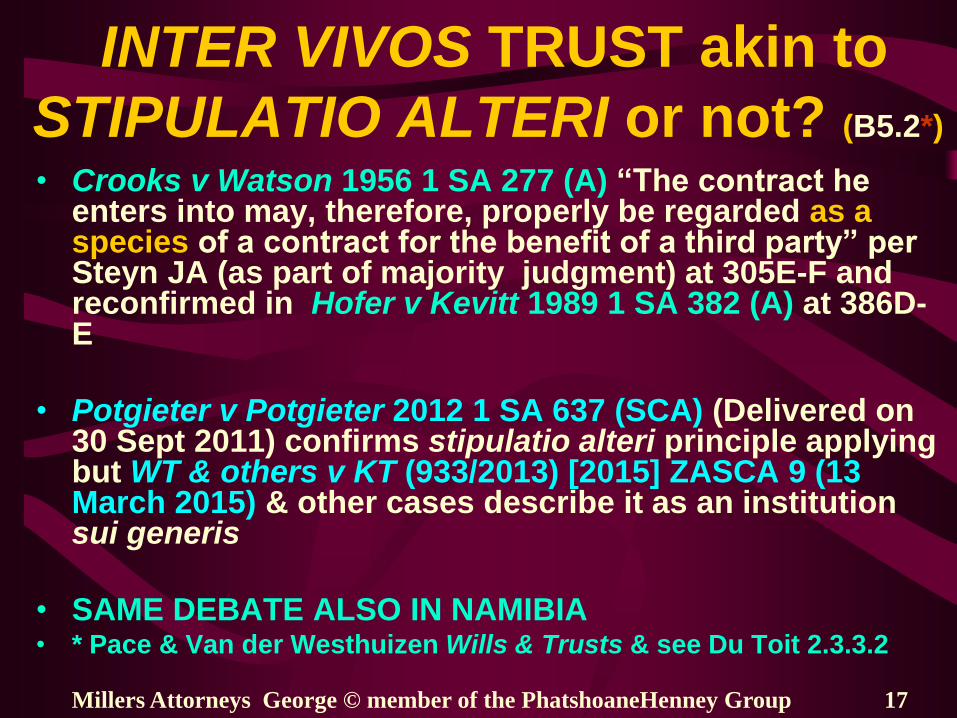

INTER VIVOS TRUST akin to

STIPULATIO ALTERI or not? (B5.2*)

• Crooks v Watson 1956 1 SA 277 (A) “The contract he enters into may, therefore, properly be regarded as a species of a contract for the benefit of a third party” per Steyn JA (as part of majority judgment) at 305E-F and reconfirmed in Hofer v Kevitt 1989 1 SA 382 (A) at 386D-E

• Potgieter v Potgieter 2012 1 SA 637 (SCA) (Delivered on 30 Sept 2011) confirms stipulatio alteri principle applying but WT & others v KT (933/2013) [2015] ZASCA 9 (13 March 2015) & other cases describe it as an institution sui generis

• SAME DEBATE ALSO IN NAMIBIA • * Pace & Van der Westhuizen Wills & Trusts & see Du Toit 2.3.3.2

Millers Attorneys George © member of PhatshoaneHenney Group 18

INTER VIVOS TRUST akin to

STIPULATIO ALTERI or not? (B5.2*)

• Various theories in re application to trust figure

• Olivier P A in his doctoral thesis entitled “Aspekte van die

reg insake Trust en Trustee met besondere verwysing na

die Amerikaanse Reg” (sic) (University of Pretoria) at 308

and 319-325 summarises the different views and states that

it varies from Murray’s (1958 Acta Juridica 64) total rejection of

equalling the trust figure with the stipulatio alteri on the one side to

total acceptance by Swanepoel (Oor Stigting..84 ev) on the other side,

with in between the views of Pollak (1956 Annual Survey 179-181),

Joubert (1956 THRHR, 150), Bayer (1956 SALJ 255) and Hahlo (1961

SALJ 195 at 204) as well as Kerr (1958 SALJ 84) but also Honore (at

23-24) and Vd Merwe and Rowland (at 355 ev All as quoted by Olivier)

See also Olivier et al par 2.11.2 and Vd Merwe & Rowland at 342, 360,

399-409 Also Du Toit 2.3.3.2 LAST WORD? NO

Millers Attorneys George © member of the PhatshoaneHenney Group 19

PROBLEM OF CONTROL /

ABUSE / ‘SHAM’ TRUSTS

ALSO IN NAMIBIA

• Tendency by founder / trustee to abuse powers /

still control trust and cause it to become an alter

ego (See also slides 82-85)

• Also failing trustee’ s duty to separate trust

property from own

• Sham trusts where trust is invalid

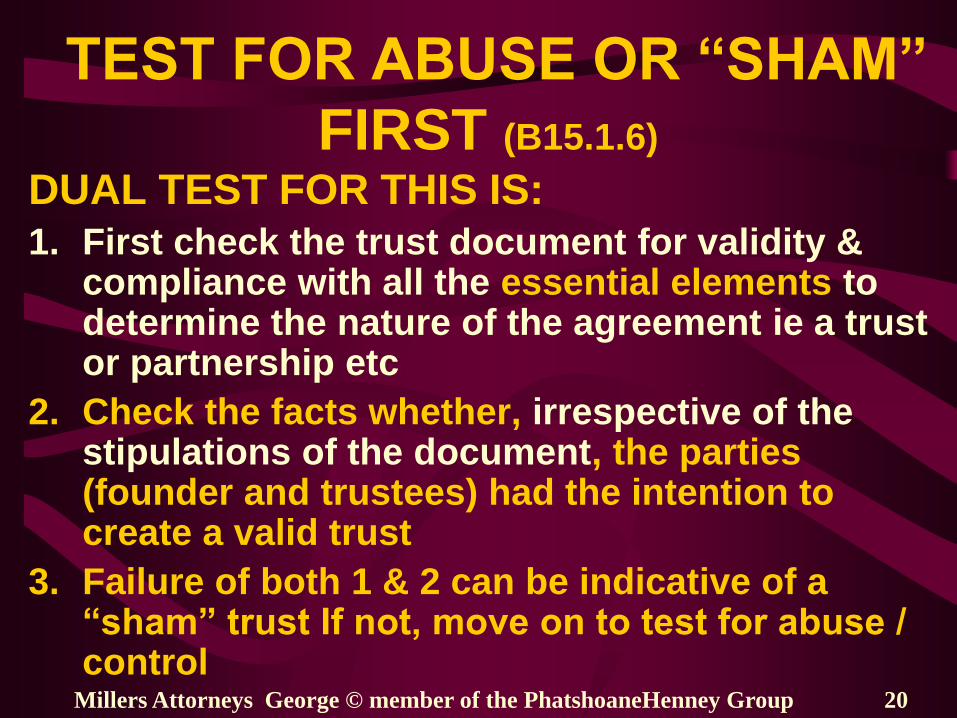

TEST FOR ABUSE OR “SHAM”

FIRST (B15.1.6)

DUAL TEST FOR THIS IS:

1. First check the trust document for validity & compliance with all the essential elements to determine the nature of the agreement ie a trust or partnership etc

2. Check the facts whether, irrespective of the stipulations of the document, the parties (founder and trustees) had the intention to create a valid trust

3. Failure of both 1 & 2 can be indicative of a “sham” trust If not, move on to test for abuse / control

Millers Attorneys George © member of the PhatshoaneHenney Group 20

Millers Attorneys Cape Town / George © member of PhatshoaneHenney Group 21

ABUSE OR “SHAM” ESSENTIALS FOR A VALID TRUST (Cameron 67)

• Founder must intend to create a trust

• Intention must be in a form to create a legal

obligation

• Trust property must be defined with

reasonable certainty

• Trust object must be defined with

reasonable certainty

• Trust object must be lawful

TRUST AS ALTER EGO (1)

“ALTER EGO” = CONTROL / ABUSE

DUAL TEST FOR CONTROL:

1. Check for control given to a specific person in the trust deed Stipulations in the deed can establish de jure control

2. Check the facts whether, irrespective of the stipulations of the trust deed, trustee has exercised/abused his/her powers on his / her own and ignored the rest of the trustees and the trust deed These surrounding facts will determine de facto control

Millers Attorneys George © member of the PhatshoaneHenney Group 22

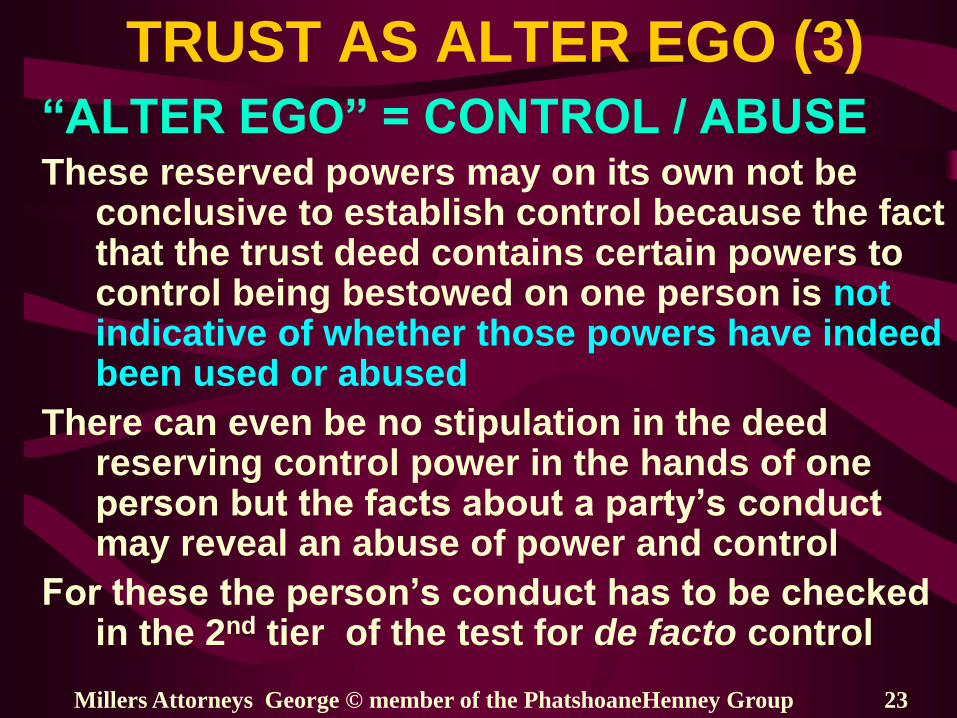

TRUST AS ALTER EGO (3)

“ALTER EGO” = CONTROL / ABUSE These reserved powers may on its own not be

conclusive to establish control because the fact that the trust deed contains certain powers to control being bestowed on one person is not indicative of whether those powers have indeed been used or abused

There can even be no stipulation in the deed reserving control power in the hands of one person but the facts about a party’s conduct may reveal an abuse of power and control

For these the person’s conduct has to be checked in the 2nd tier of the test for de facto control

Millers Attorneys George © member of the PhatshoaneHenney Group 23

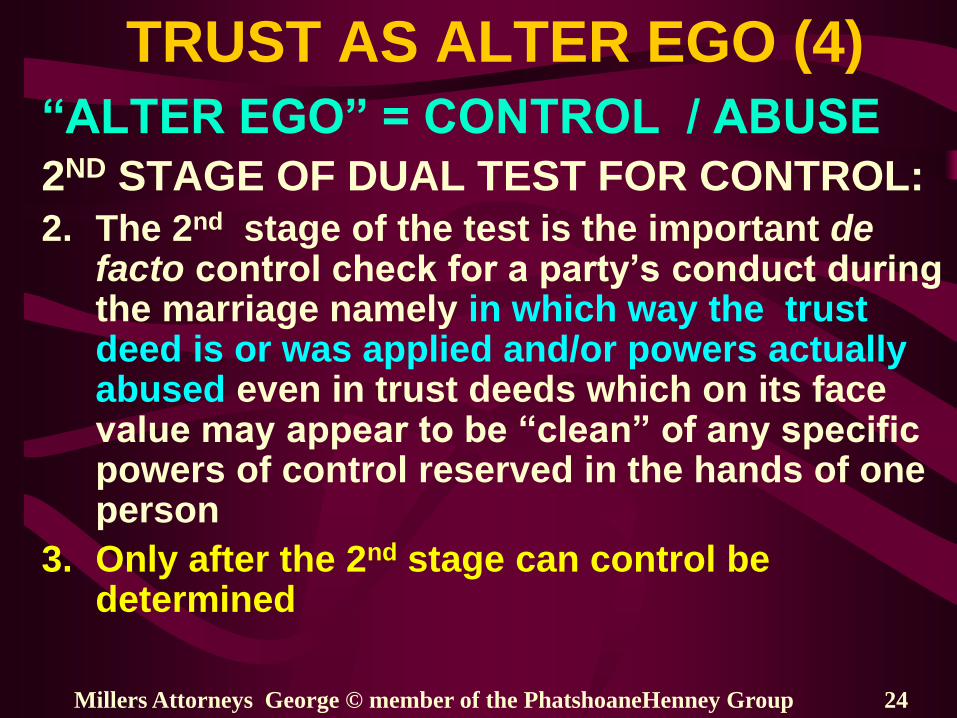

TRUST AS ALTER EGO (4)

“ALTER EGO” = CONTROL / ABUSE

2ND STAGE OF DUAL TEST FOR CONTROL:

2. The 2nd stage of the test is the important de facto control check for a party’s conduct during the marriage namely in which way the trust deed is or was applied and/or powers actually abused even in trust deeds which on its face value may appear to be “clean” of any specific powers of control reserved in the hands of one person

3. Only after the 2nd stage can control be determined

Millers Attorneys George © member of the PhatshoaneHenney Group 24

Millers Attorneys George © member of the PhatshoaneHenney Group 25

REGISTER TRUSTS IN NAMIBIA ! This is a requirement in terms of the 1934

Act

• Failure to lodge trust deed with Master a criminal offence in Namibia

• FAILURE TO GET EXEMPTION FROM SECURITY FROM MASTER CAUSED TRUS-TEES NOT TO BE ABLE TO ACT AS SUCH KRUGER v BOTHA 1949 3 SA 1147 (O); DIE MEESTER v PRESIDENT VERSEKERINGSMPY 1983 3 SA 410 (KPA) (CAMERON 218, 257-8)

• SUCH TRUSTS TO BE REGISTERED WITH MASTER ASAP

Millers Attorneys Cape Town / George © member of PhatshoaneHenney Group 26

TRUSTEE APPOINTMENT (1)

SUMMARY 1 (B6.2.3)

• Comply with specific formalities and

procedures in trust deed when trustees are

appointed and vacancies are filled e.g.

exceeding time limits and specific duty in

such a case & e.g. required minimum

number of trustees

Millers Attorneys Cape Town / George © member of PhatshoaneHenney Group 27

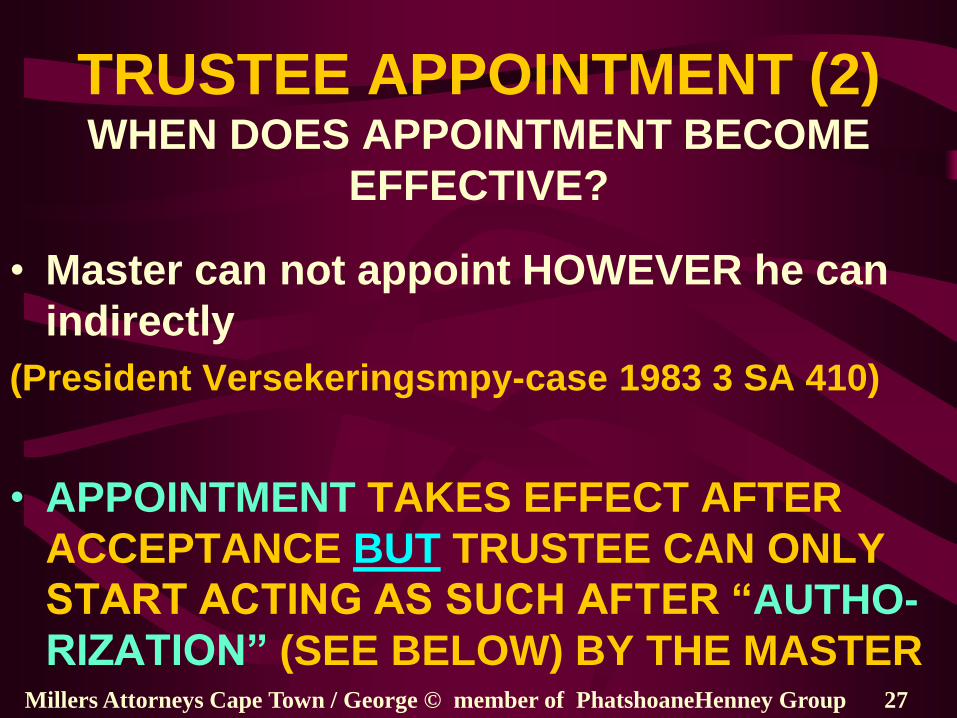

TRUSTEE APPOINTMENT (2) WHEN DOES APPOINTMENT BECOME

EFFECTIVE?

• Master can not appoint HOWEVER he can

indirectly

(President Versekeringsmpy-case 1983 3 SA 410)

• APPOINTMENT TAKES EFFECT AFTER

ACCEPTANCE BUT TRUSTEE CAN ONLY

START ACTING AS SUCH AFTER “AUTHO-

RIZATION” (SEE BELOW) BY THE MASTER

TRUSTEE APPOINTMENT (3) WHEN DOES APPOINTMENT BECOME

EFFECTIVE?

• Trust Moneys Protection Act 34 of 1934 – no

specific requirement as in RSA for trustees to

seek Master’s authority as ito s6 of RSA Trust

Property Control Act HOWEVER

• Trustees in Namibia required to furnish security

to satisfaction of Master (s 3(1))

• Failure to lodge trust deed with Master criminal

offence in Namibia ito sec 2 read with sec 6 of

1934 Act

Millers Attorneys Cape Town / George © member of the PhatshoaneHenney Group 28

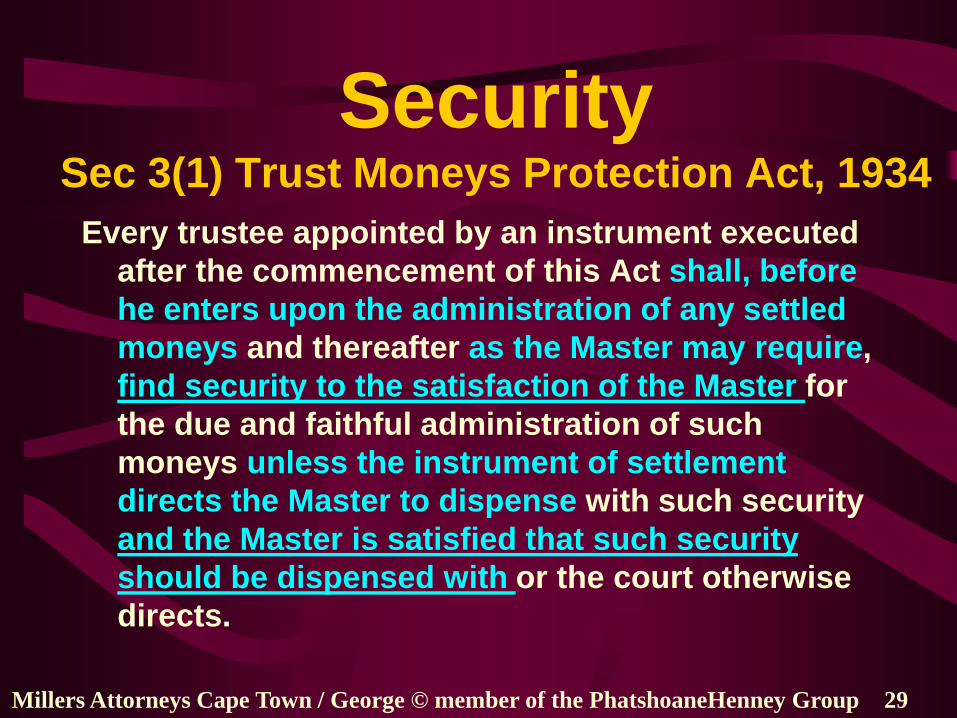

Security Sec 3(1) Trust Moneys Protection Act, 1934

Every trustee appointed by an instrument executed

after the commencement of this Act shall, before

he enters upon the administration of any settled

moneys and thereafter as the Master may require,

find security to the satisfaction of the Master for

the due and faithful administration of such

moneys unless the instrument of settlement

directs the Master to dispense with such security

and the Master is satisfied that such security

should be dispensed with or the court otherwise

directs.

Millers Attorneys Cape Town / George © member of the PhatshoaneHenney Group 29

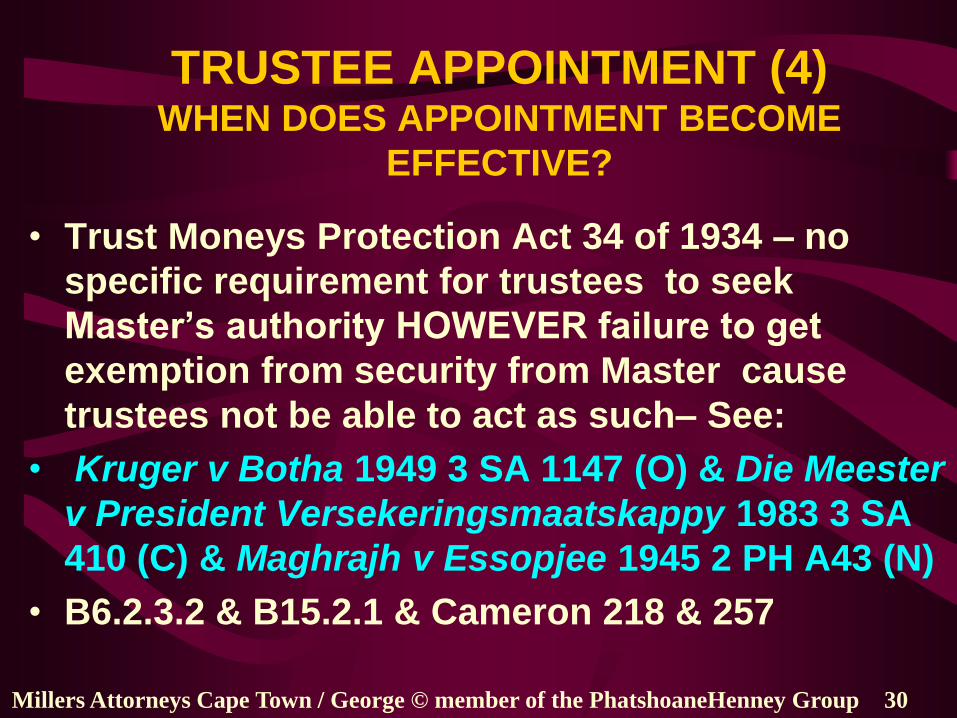

TRUSTEE APPOINTMENT (4) WHEN DOES APPOINTMENT BECOME

EFFECTIVE?

• Trust Moneys Protection Act 34 of 1934 – no

specific requirement for trustees to seek

Master’s authority HOWEVER failure to get

exemption from security from Master cause

trustees not be able to act as such– See:

• Kruger v Botha 1949 3 SA 1147 (O) & Die Meester

v President Versekeringsmaatskappy 1983 3 SA

410 (C) & Maghrajh v Essopjee 1945 2 PH A43 (N)

• B6.2.3.2 & B15.2.1 & Cameron 218 & 257

Millers Attorneys Cape Town / George © member of the PhatshoaneHenney Group 30

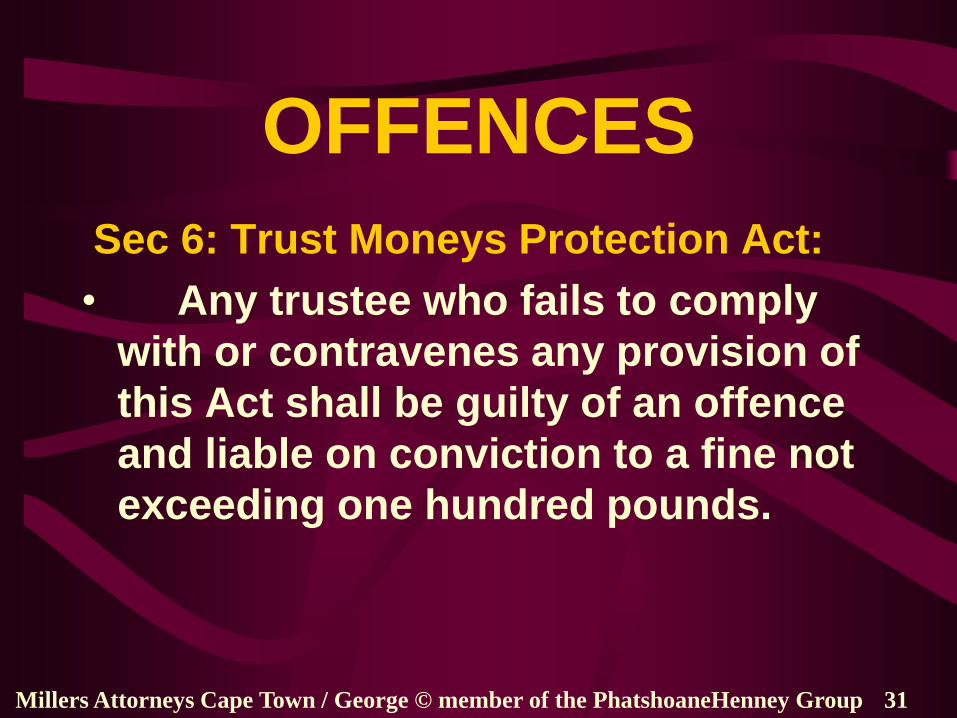

OFFENCES

Sec 6: Trust Moneys Protection Act:

• Any trustee who fails to comply

with or contravenes any provision of

this Act shall be guilty of an offence

and liable on conviction to a fine not

exceeding one hundred pounds.

Millers Attorneys Cape Town / George © member of the PhatshoaneHenney Group 31

Millers Attorneys George © Member of the PhatshoaneHenney Group 32

PART 1C

APPLICATION

POSSIBILITIES:

THE TRUST AS HOLISTIC

ESTATE PLANNING TOOL IN

NAMIBIA (SEE SLIDES 96-104)

TRUST NAMIBIAN

APPLICATION POSSIBILITIES • Risk protection

• Continuity—no limitation on perpetuity of trust

• Prevention of asset growth

• Trust as an heir Remember: AGRICULTURAL

(COMMERCIAL) LAND REFORM ACT 6 OF 1995 (to vest in

the State a preferent right to purchase agricultural land

for the purposes of the Act) not applicable to trust but

beware;

• Equitable distribution

• Family disputes

• Incapable persons eg Altzheimer’s

Millers Attorneys George © Member of the PhatshoaneHenney Group 33

APPLICATION POSSIBILITIES (CONTINUED)

• Charitable organizations

• Limited liability

• Business trust / partnerships

• Assurance opportunities

• No audit requirement

• Tax saving vehicle (income tax)

• Instead of a usufruct

• Use in times of recession

Millers Attorneys George © Member of the PhatshoaneHenney Group 34

PART 1D

THE TAX

IMPLICATIONS

Millers Attorneys George © Member of the PhatshoaneHenney Group 35

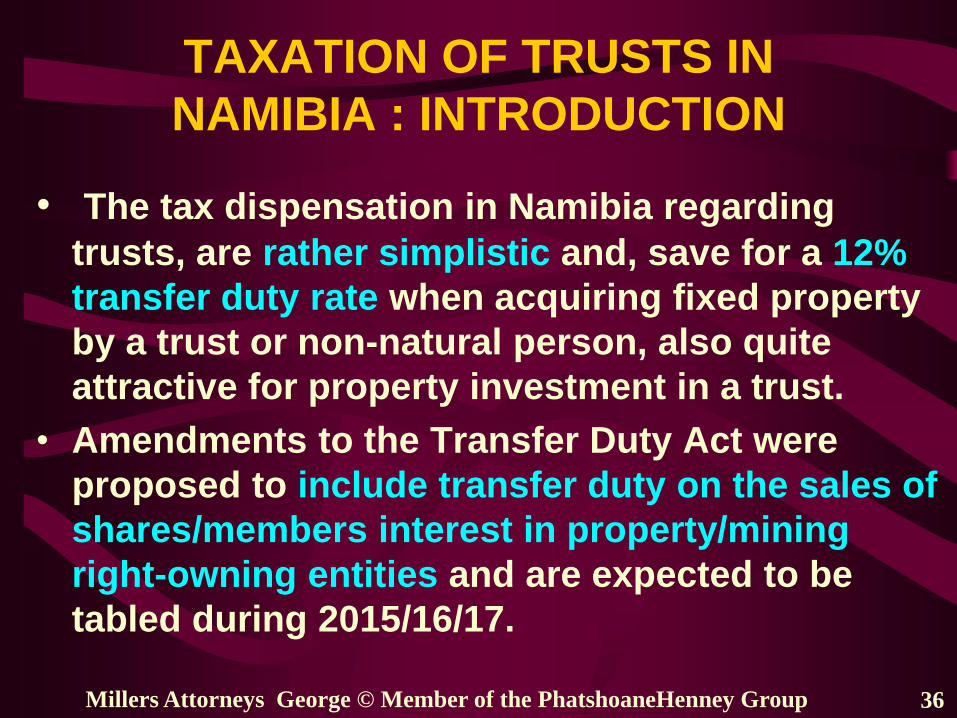

TAXATION OF TRUSTS IN

NAMIBIA : INTRODUCTION

• The tax dispensation in Namibia regarding

trusts, are rather simplistic and, save for a 12%

transfer duty rate when acquiring fixed property

by a trust or non-natural person, also quite

attractive for property investment in a trust.

• Amendments to the Transfer Duty Act were

proposed to include transfer duty on the sales of

shares/members interest in property/mining

right-owning entities and are expected to be

tabled during 2015/16/17.

Millers Attorneys George © Member of the PhatshoaneHenney Group 36

INCOME TAX OF TRUSTS IN

NAMIBIA

Taxation of Trusts is dealt with in the

Namibian Income Tax Act 24 of 1981 (as

amended)

A trust is not defined as a person for

purposes of income tax, but the trustee is

defined to be the representative taxpayer

“in respect of income the subject of any

trust”

Millers Attorneys George © Member of the PhatshoaneHenney Group 37

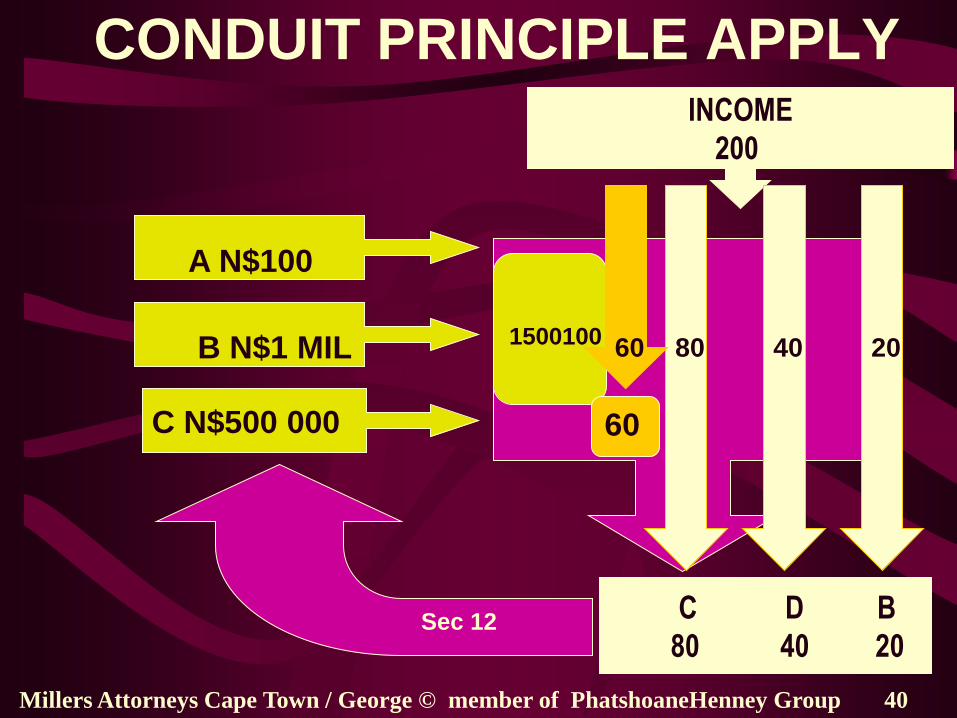

INCOME TAX OF TRUSTS IN

NAMIBIA

• A trust is taxed as similar to a natural

person (see tax rate table for individuals).

Income earned by a vesting trust and

certain distributions made by a

discretionary trust are taxed in the hands

of the beneficiary. (Sec 12 (3) & 12(5) of

Income Tax Act – the equivalent of sec 7 in

the RSA)

• Trust Tax scale vary between 18% and 37%

Millers Attorneys George © Member of the PhatshoaneHenney Group 38

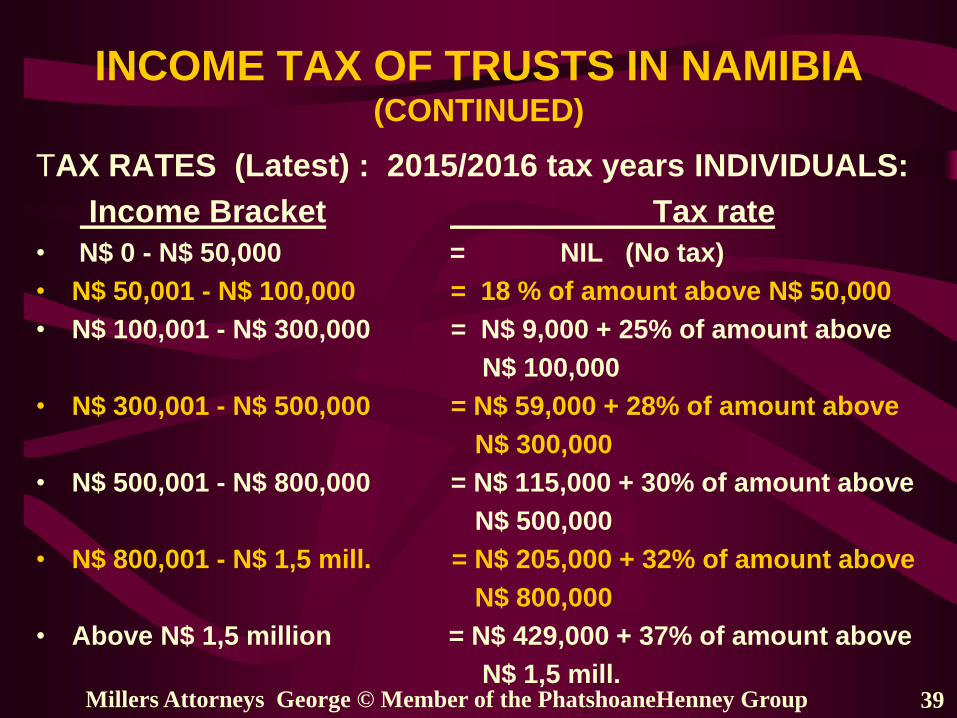

INCOME TAX OF TRUSTS IN NAMIBIA (CONTINUED)

TAX RATES (Latest) : 2015/2016 tax years INDIVIDUALS:

Income Bracket Tax rate

• N$ 0 - N$ 50,000 = NIL (No tax)

• N$ 50,001 - N$ 100,000 = 18 % of amount above N$ 50,000

• N$ 100,001 - N$ 300,000 = N$ 9,000 + 25% of amount above

N$ 100,000

• N$ 300,001 - N$ 500,000 = N$ 59,000 + 28% of amount above

N$ 300,000

• N$ 500,001 - N$ 800,000 = N$ 115,000 + 30% of amount above

N$ 500,000

• N$ 800,001 - N$ 1,5 mill. = N$ 205,000 + 32% of amount above

N$ 800,000

• Above N$ 1,5 million = N$ 429,000 + 37% of amount above

N$ 1,5 mill.

Millers Attorneys George © Member of the PhatshoaneHenney Group 39

Millers Attorneys Cape Town / George © member of PhatshoaneHenney Group 40

CONDUIT PRINCIPLE APPLY

B N$1 MIL

A

C D B

80 40 20

C N$500 000

Sec 12

INCOME

200

80

A N$100

40

20

1500100

60

60

Millers Attorneys Cape Town / George © member of PhatshoaneHenney Group 41

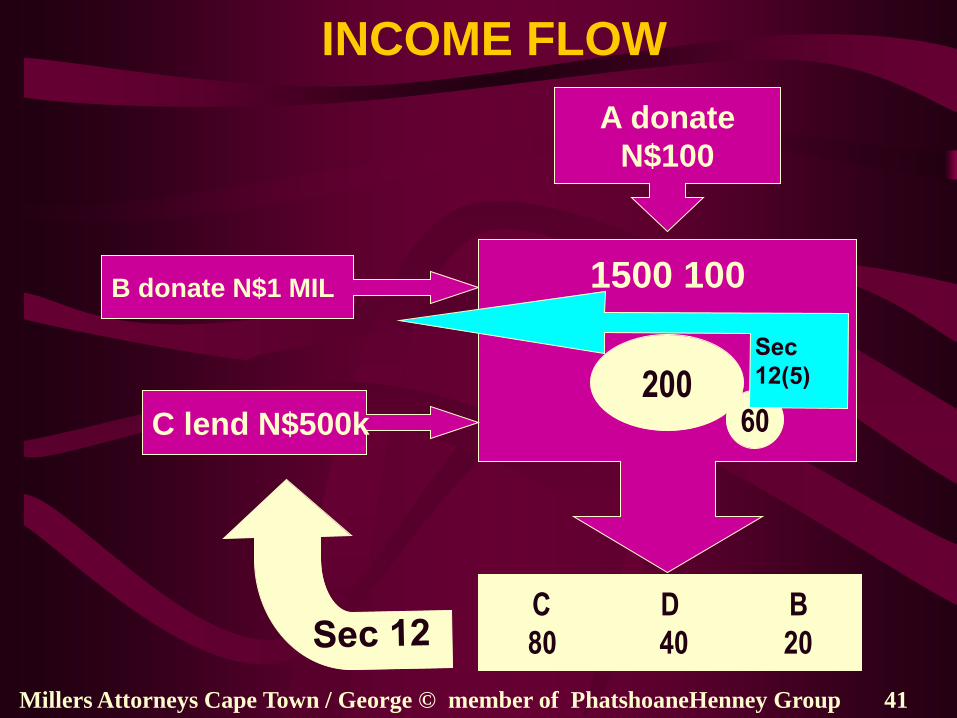

INCOME FLOW

B donate N$1 MIL

1500 100

A

C D B

80 40 20

200 60

A donate

N$100

C lend N$500k

INCOME TAX ACT Sec 12 (1)

Millers Attorneys George © Member of the PhatshoaneHenney Group 42

• "representative taxpayer" means-

• (c) in respect of income the subject of any

trust or in respect of the income of any minor or

mentally disordered or defective person or any

other person under legal disability, the trustee,

guardian, curator or other person entitled to the

receipt, management, disposal or control of

such income or remitting or paying to or

receiving moneys on behalf of such person

under disability;

INCOME TAX ACT Sec 12 (1)

Millers Attorneys George © Member of the PhatshoaneHenney Group 43

• "trustee" in addition to every person appointed

or constituted as such by act of parties, by will,

by order or declaration of court or by operation

of law, includes an executor or administrator,

tutor or curator, and any person having the

administration or control of any property subject

to a trust, usufruct, fidei-commissum or other

limited interest, or acting in any fiduciary

capacity or having, either in a private or an

official capacity, the possession, direction,

control or management of any property of any

person under legal disability

INCOME TAX ACT Sec 12

Millers Attorneys George © Member of the PhatshoaneHenney Group 44

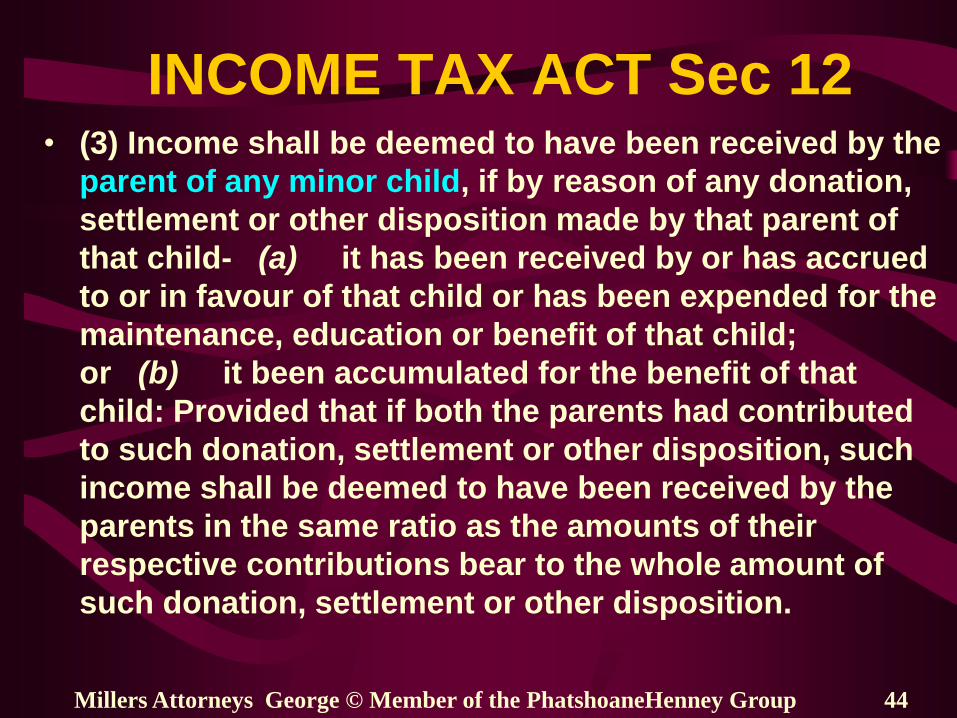

• (3) Income shall be deemed to have been received by the

parent of any minor child, if by reason of any donation,

settlement or other disposition made by that parent of

that child- (a) it has been received by or has accrued

to or in favour of that child or has been expended for the

maintenance, education or benefit of that child;

or (b) it been accumulated for the benefit of that

child: Provided that if both the parents had contributed

to such donation, settlement or other disposition, such

income shall be deemed to have been received by the

parents in the same ratio as the amounts of their

respective contributions bear to the whole amount of

such donation, settlement or other disposition.

INCOME TAX ACT Sec 12

Millers Attorneys George © Member of the PhatshoaneHenney Group 45

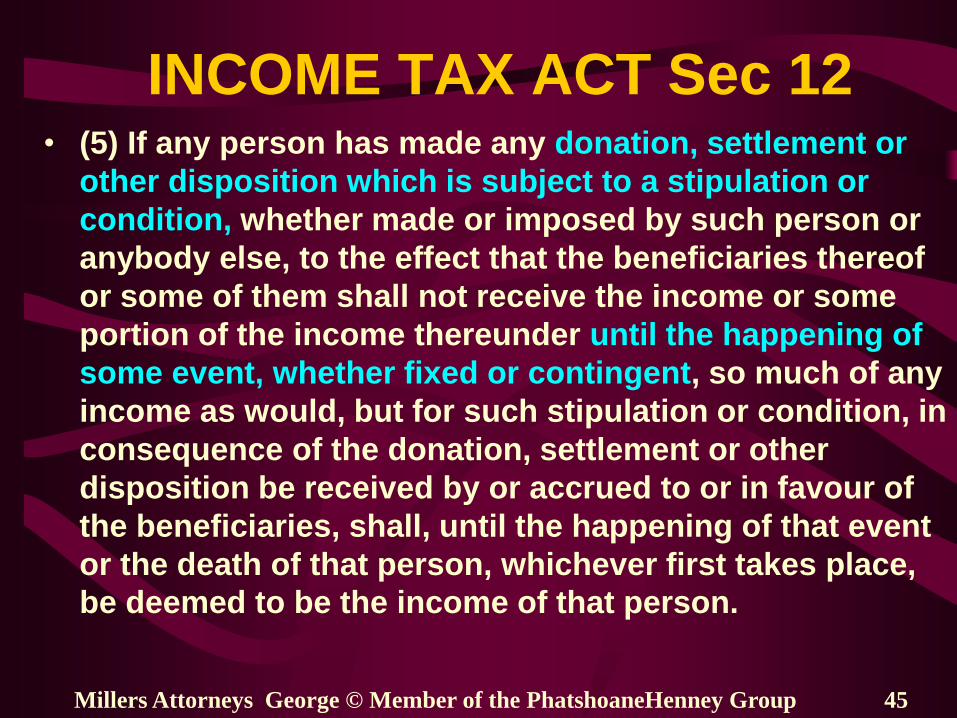

• (5) If any person has made any donation, settlement or

other disposition which is subject to a stipulation or

condition, whether made or imposed by such person or

anybody else, to the effect that the beneficiaries thereof

or some of them shall not receive the income or some

portion of the income thereunder until the happening of

some event, whether fixed or contingent, so much of any

income as would, but for such stipulation or condition, in

consequence of the donation, settlement or other

disposition be received by or accrued to or in favour of

the beneficiaries, shall, until the happening of that event

or the death of that person, whichever first takes place,

be deemed to be the income of that person.

INCOME TAX ACT Sec 12

• (6) If any deed of donation, settlement or other

disposition contains any stipulation that the right

to receive any income thereby conferred may,

under powers retained by the person by whom

that right is conferred, be revoked or conferred

upon another, so much of any income as in

consequence of the donation, settlement or other

disposition is received by or accrues to or in

favour of the person on whom that right is

conferred, shall be deemed to be the income of

the person by whom it is conferred, so long as he

retains those powers.

Millers Attorneys George © Member of the PhatshoaneHenney Group 46

TRANSFER DUTY

RELEVANT TO TRUSTS • Transfer Duty Act 14 of 1993

• (2) Subject to the provisions of section 9, there

shall be levied for the benefit of the State

Revenue Fund a transfer duty on the value of

any property acquired by any person....at a rate

of:

• (2)(1)(c) twelve per cent of the said value or the

said amount, as the case may be, if the person

by whom the property is acquired or in whose

favour or for whose benefit the said interest or

restriction is renounced is a person other than a

natural person. Millers Attorneys George © Member of the PhatshoaneHenney Group 47

TRANSFER DUTY

RELEVANT TO TRUSTS

• Transfer Duty Act 14 of 1993

• (2) For the purposes of subsection (1), any

trustee or administrator of a trust or any other

person acting in a fiduciary capacity shall, in

respect of any property acquired by him or her

or any property held by him or her of which the

value is enhanced as contemplated in that

subsection, be deemed to be a person other than

a natural person.

• [Sec 2 substituted by sec 1 of Act 20 of 2003.]

Millers Attorneys George © Member of the PhatshoaneHenney Group 48

TRANSFER DUTY EXEMPTIONS

RELEVANT TO TRUSTS Sec 9

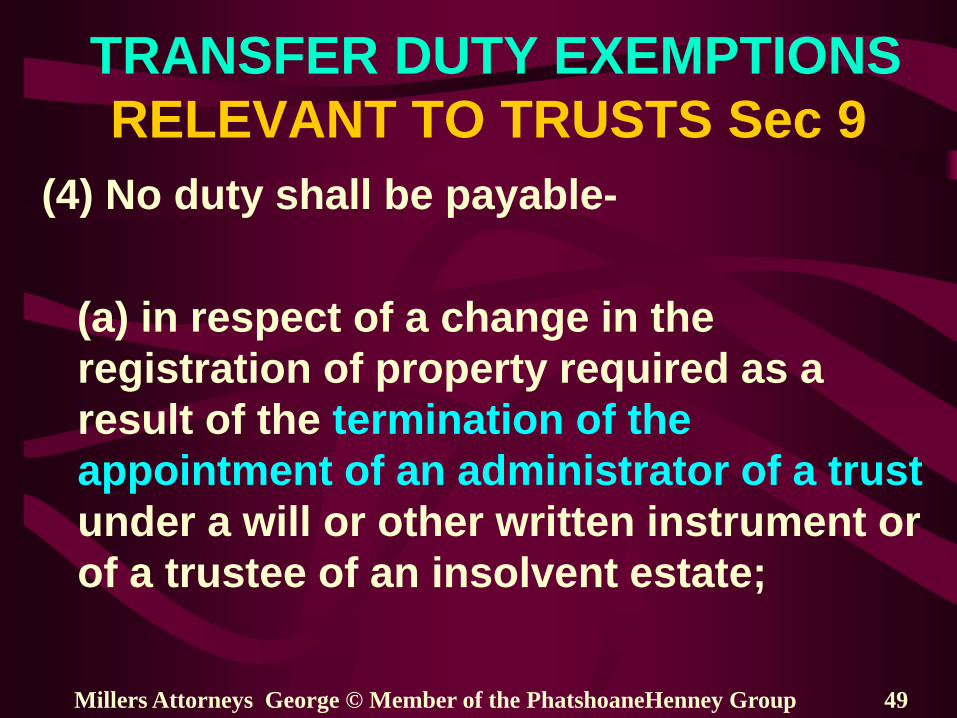

(4) No duty shall be payable-

(a) in respect of a change in the

registration of property required as a

result of the termination of the

appointment of an administrator of a trust

under a will or other written instrument or

of a trustee of an insolvent estate;

Millers Attorneys George © Member of the PhatshoaneHenney Group 49

TRANSFER DUTY EXEMPTIONS

RELEVANT TO TRUSTS Sec 9

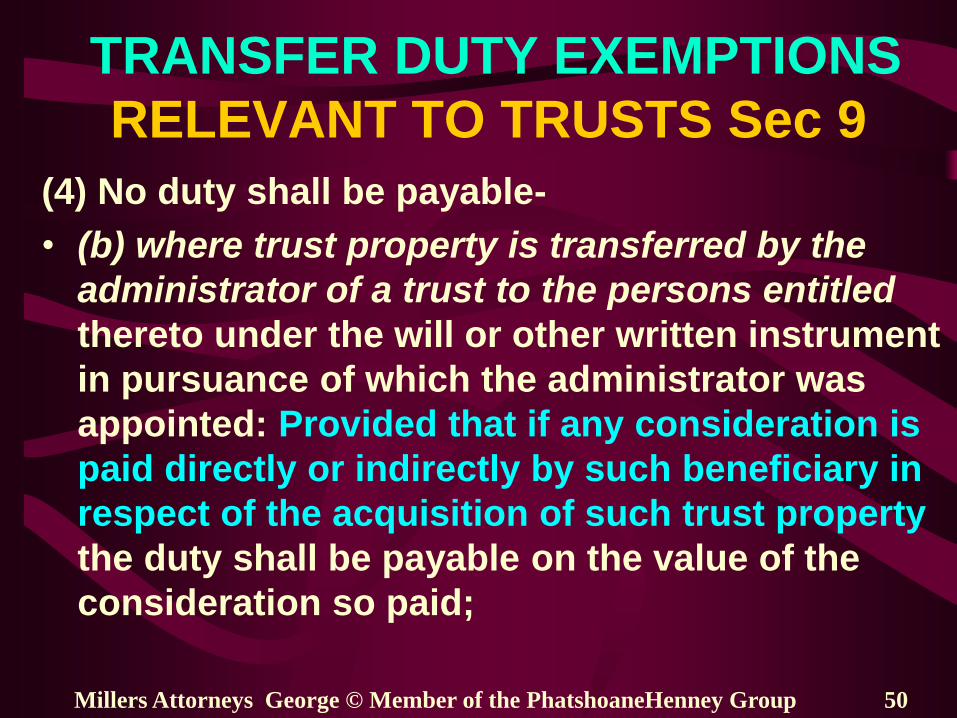

(4) No duty shall be payable-

• (b) where trust property is transferred by the

administrator of a trust to the persons entitled

thereto under the will or other written instrument

in pursuance of which the administrator was

appointed: Provided that if any consideration is

paid directly or indirectly by such beneficiary in

respect of the acquisition of such trust property

the duty shall be payable on the value of the

consideration so paid;

Millers Attorneys George © Member of the PhatshoaneHenney Group 50

TRANSFER DUTY EXEMPTIONS

RELEVANT TO TRUSTS Sec 9

• Transfer Duty Amendments: introduction of

transfer duty on the sale of shares in companies

and members’ interest in close corporations

owning property, commercial property, land and

mineral licences announced in2015/16 budget.

• This confirms the extension of transfer duties to

companies and close corporations. The effective

date has not been confirmed but is expected to

become legislation soon

Millers Attorneys George © Member of the PhatshoaneHenney Group 51

STAMP DUTY

• Stamp duty is payable at N$12 for every N$

1 000 or part therefore of the value of the

immovable property where purchased by a

juristic person or a trust.

Millers Attorneys George © Member of the PhatshoaneHenney Group 52

TO TRUST OR NOT TO TRUST “Trusts have now also pervaded all fields of social

and business institutions in Civil Law countries.

They are like those multi-vitamins preventing at

the same time stress, colds and colon

problems, sold by chemists and health shops in

Namibian (also read RSA) shopping malls; they

prevent equally well family feuds, business

risks, black economic empowerment difficulties,

public benefit and special persons’ problems.

What amazes the sceptical civilian is that they

really do prevent them” Our own adaptation for Civil Law countries of the statement by:

Pierre Lepaulle “Civil Law Substitutes for Trusts” 36 Yale LR 1126 at 1147 (1927)

Millers Attorneys Cape Town / George © member of the PhatshoaneHenney Group 53

Millers Attorneys George © member of PhatshoaneHenney Group 54

FURTHER READING MATERIAL • PACE R P & VAN DER WESTHUIZEN WM : Wills

And Trusts SERVICE ISSUE 19 (2015) LEXISNEXIS

• OOSTHUIZEN W, KING R, V VUREN L & Van Der WESTHUIZEN W M Estate Planning & Fiduciary Services Guide 2016 LexisNexis

• CAMERON E, DE WAAL M & WUNSH B : Honore’s SA Law of Trusts 5TH ED (2002) JUTA

• DAVIS, BENEKE & JOOSTE : Estate Planning SERVICE ISSUE 37 (2013) LEXISNEXIS

• MEYEROWITZ D : Meyerowitz On Income Tax THE TAXPAYER CAPE TOWN

Millers Attorneys George © Member of the PhatshoaneHenney Group 55

SERVICES

• SEMINARS / COURSES

* PROFESSIONAL AUDIENCES

* GENERAL PUBLIC / ADVISORS & THEIR CLIENTS

• HOLISTIC ESTATE PLANNING

• DRAFTING TRUST DEEDS : FAMILY, BUSINESS

& PBO TRUSTS

• LEGAL AUDITS ON TRUST DEEDS

MILLERS INC

GEORGE : TEL 044 874 1140

FAX 044 873 4848

http:/www.millers.co.za E-MAIL [email protected]

Millers Attorneys George © Member of the PhatshoaneHenney Group 56

END

THANK YOU

MILLERS INC

GEORGE : TEL 044 874 1140 FAX 044 873 4848

http:/www.millers.co.za E-MAIL [email protected]

Millers Attorneys George © Member of the PhatshoaneHenney Group 57

PART 2 ADDITIONAL

REFERENCE SLIDES AS

FURTHER READING

MATERIAL BUT

NOT DISCUSSED

Millers Attorneys George © member of the PhatshoaneHenney Group 58

TRUST HEALTH BAROMETER STRANGE / BAD CLAUSES ** : PITFALLS

Main reasons ** for pitfalls / bad / strange clauses

in trust deeds in the Namibia & RSA :

1. Ignorance of unique trust law system in the Namibia &

RSA

2. Using precedents foreign to local trust law

3. Restrictive / too creative / bad drafting

Result is that in more than 90% of trusts on

which legal audits have been done, validity can be

questioned**

** Based on empirical studies and legal audits which have been done

on trust deeds from Namibia & South Africa for more than 15

years

Millers Attorneys George © member of the PhatshoaneHenney Group 59

TRUST HEALTH BAROMETER

• ADD TO THIS THAT:

• In more than 95% of trusts where the trust deed

was amended and the beneficiaries had prior to

the amendment accepted benefits the

amendments may be invalid

• Still in more than 40%, the parties to the trust

were structured incorrectly

• THEN THE HEALTH PICTURE BECOMES

ALARMINGLY BAD THEREFORE CHECK THE

BOUNDARIES OF OUR KNOWLEDGE / SKILLS

THE BOUNDARIES OF OUR

ABILITIES ARE NB :

1. For those of us who know how much we

know.....

2. For those of us who know how little we know .....

3. For those of us who know that we do not

know.....

4. For those of us who think we know.....

5. For those of us who do not even know how little

we know......

Millers Attorneys George © member of PhatshoaneHenney Group 60

USING TRUST DEED

PRECEDENTS

FOREIGN TO

NAMIBIAN / RSA

TRUST LAW Millers Attorneys George © member of the PhatshoaneHenney Group 61

USING TRUST DEED

PRECEDENTS FOREIGN TO

NAMIBIAN / RSA TRUST LAW • Easy access to foreign (especially Common

[English] Law) precedents (inconsistent with

Namibian / RSA Trust Law)

• Practitioners ignorant of implications of using

these foreign precedents

• Examples:

- Unilateral act by founder

- General power of appointment

Millers Attorneys George © member of the PhatshoaneHenney Group 62

GREY AREA 1

FORMATION OF A TRUST

WITH ONLY ONESELF

(IRREPARABLE)

Millers Attorneys George © member of the PhatshoaneHenney Group 63

Millers Attorneys George © Member of the PhatshoaneHenney Group 64

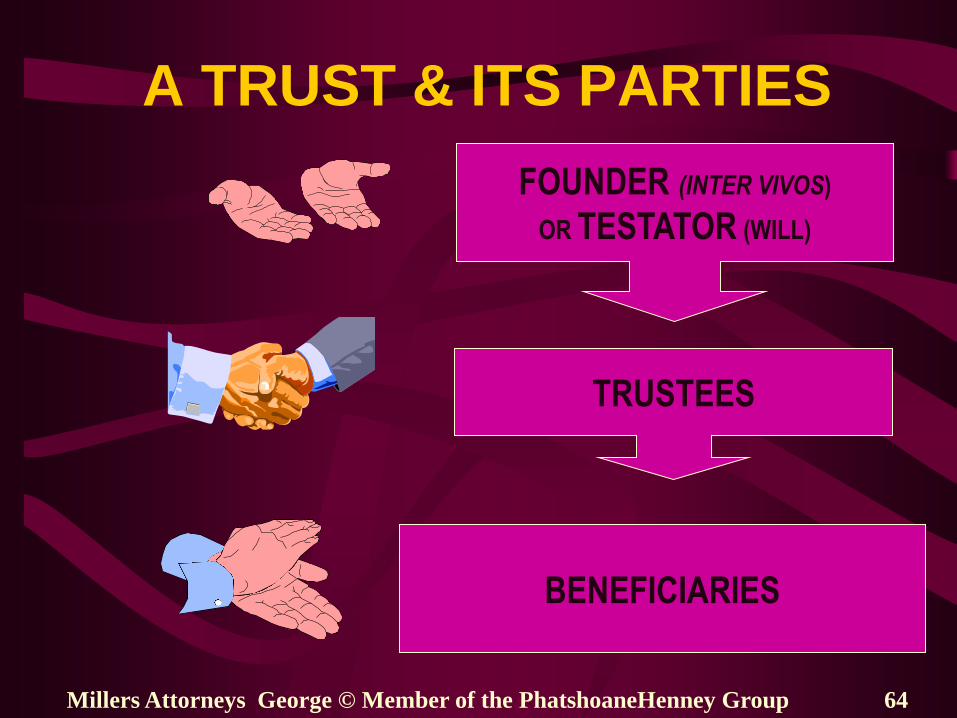

A TRUST & ITS PARTIES

FOUNDER (INTER VIVOS)

OR TESTATOR (WILL)

BENEFICIARIES

TRUSTEES

GREY AREA (1)

FORMATION OF A TRUST WITH

ONLY ONESELF (i) (B5.1 & B6.1)

• Van der Merwe v Nedcor Bank 2003 1 SA 169 (HHA) confirmed Vaal Reefs Exploration & Mining v Burger 1999 4 SA 1161 (SCA)

• “The proposition that a contract between a person as representative of another with himself is a nullity, is not correct.”

• Question of who does the trustee represent is still uncertain ? Millers Attorneys George © member of the PhatshoaneHenney Group 65

GREY AREA 2

TRUST OBJECT TOO

VAGUE; CHANGING

OBJECT

(REPARABLE ??)

Millers Attorneys George © member of the PhatshoaneHenney Group 66

Millers Attorneys George © member of the PhatshoaneHenney Group 67

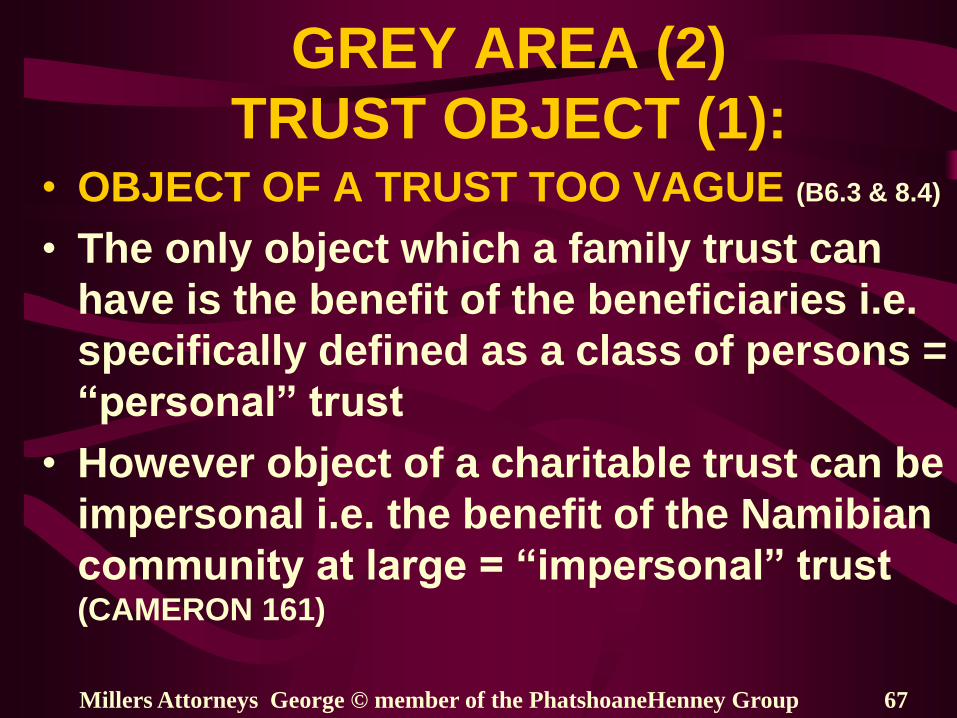

GREY AREA (2)

TRUST OBJECT (1): • OBJECT OF A TRUST TOO VAGUE (B6.3 & 8.4)

• The only object which a family trust can

have is the benefit of the beneficiaries i.e.

specifically defined as a class of persons =

“personal” trust

• However object of a charitable trust can be

impersonal i.e. the benefit of the Namibian

community at large = “impersonal” trust (CAMERON 161)

Millers Attorneys George © member of the PhatshoaneHenney Group 68

TRUST OBJECT (2):

• OBJECT OF A PERSONAL TRUST IS

UNDEFINED WHEN (B6.3 & 8.4) :

• It exceeds the specific power of

appointment e.g. where selection / scope

of beneficiaries is left to the discretion of

the trustees

OR

when trustees can create “roll over” trust

on terms as they may decide upon

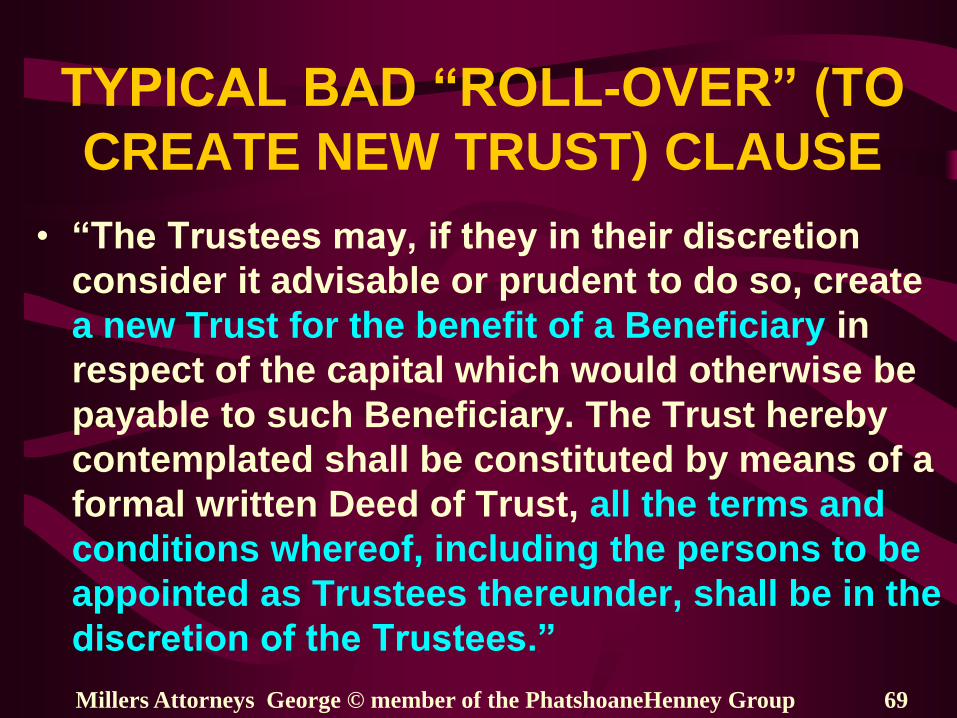

TYPICAL BAD “ROLL-OVER” (TO

CREATE NEW TRUST) CLAUSE

• “The Trustees may, if they in their discretion

consider it advisable or prudent to do so, create

a new Trust for the benefit of a Beneficiary in

respect of the capital which would otherwise be

payable to such Beneficiary. The Trust hereby

contemplated shall be constituted by means of a

formal written Deed of Trust, all the terms and

conditions whereof, including the persons to be

appointed as Trustees thereunder, shall be in the

discretion of the Trustees.”

Millers Attorneys George © member of the PhatshoaneHenney Group 69

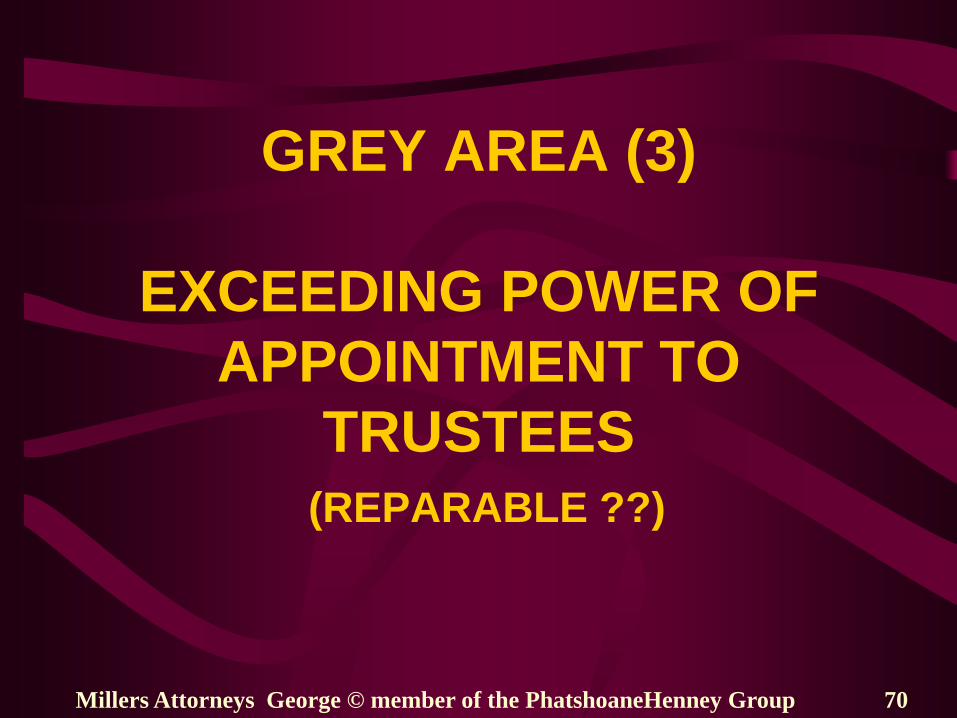

GREY AREA (3)

EXCEEDING POWER OF

APPOINTMENT TO

TRUSTEES

(REPARABLE ??)

Millers Attorneys George © member of the PhatshoaneHenney Group 70

Millers Attorneys George © member of the PhatshoaneHenney Group 71

GREY AREA (3)

EXCEEDING POWER OF

APPOINTMENT TO TRUSTEES (1)

• Our trust law distinguishes between a “general”

and “specific” (also referred to as “special”)

power of appointment (Wills & Trusts LexisNexis

B8.4.2)

• Also termed ‘a right of disposal’ or ‘power of

choosing’ (CAMERON 583)

• Only specific power of appointment accepted in

our trust law Braun v Blann & A 1984 2 SA 850 (A)

at 866H

Millers Attorneys George © member of the PhatshoaneHenney Group 72

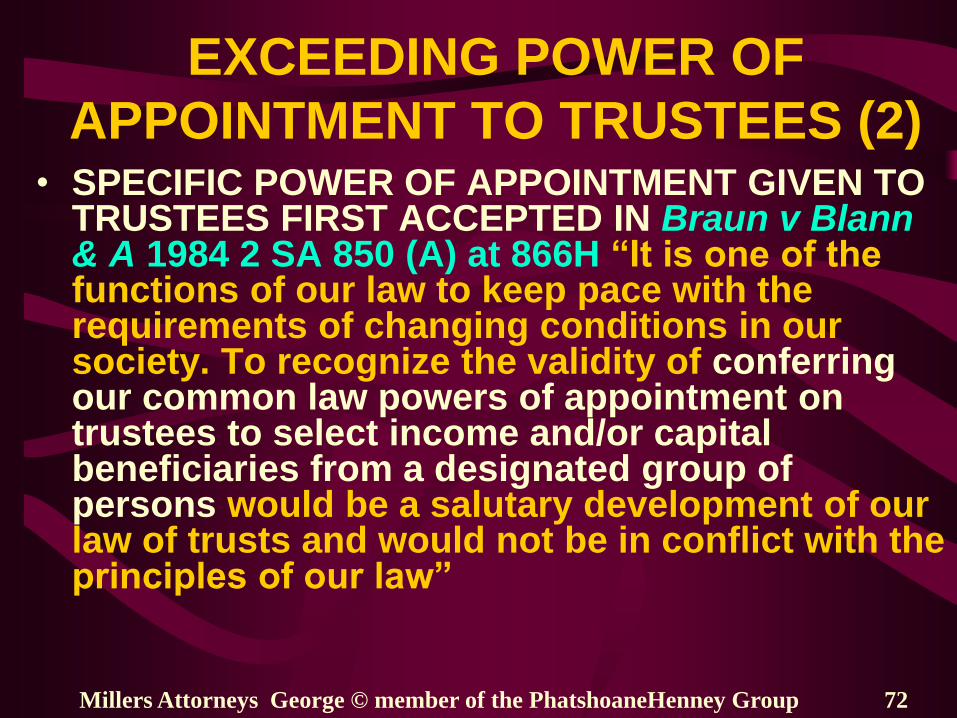

EXCEEDING POWER OF

APPOINTMENT TO TRUSTEES (2) • SPECIFIC POWER OF APPOINTMENT GIVEN TO

TRUSTEES FIRST ACCEPTED IN Braun v Blann & A 1984 2 SA 850 (A) at 866H “It is one of the functions of our law to keep pace with the requirements of changing conditions in our society. To recognize the validity of conferring our common law powers of appointment on trustees to select income and/or capital beneficiaries from a designated group of persons would be a salutary development of our law of trusts and would not be in conflict with the principles of our law”

Millers Attorneys George © member of the PhatshoaneHenney Group 73

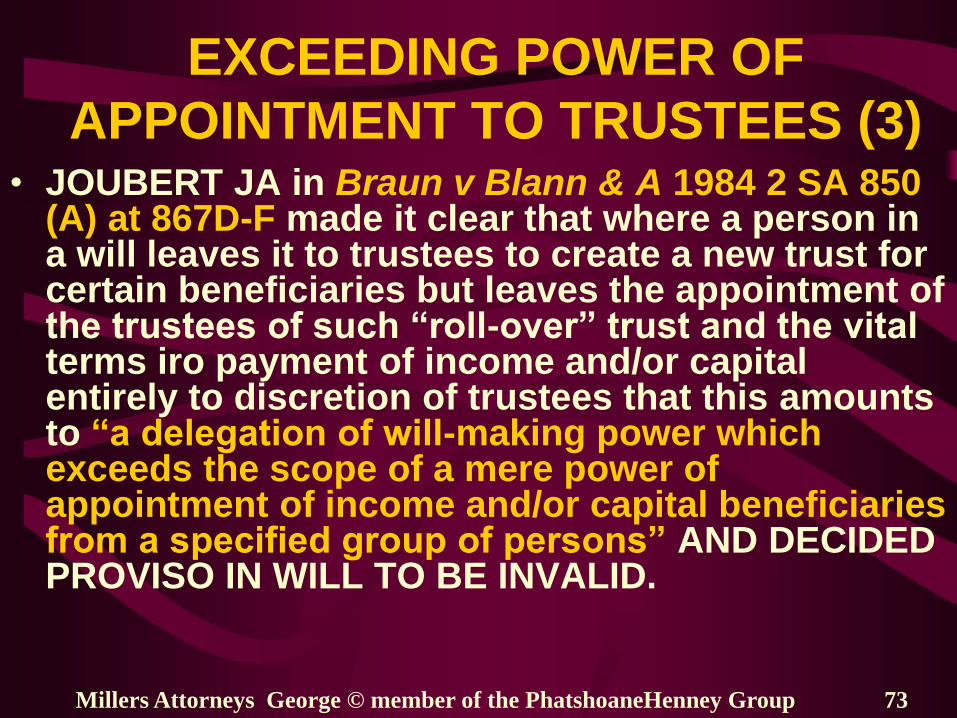

EXCEEDING POWER OF

APPOINTMENT TO TRUSTEES (3) • JOUBERT JA in Braun v Blann & A 1984 2 SA 850

(A) at 867D-F made it clear that where a person in a will leaves it to trustees to create a new trust for certain beneficiaries but leaves the appointment of the trustees of such “roll-over” trust and the vital terms iro payment of income and/or capital entirely to discretion of trustees that this amounts to “a delegation of will-making power which exceeds the scope of a mere power of appointment of income and/or capital beneficiaries from a specified group of persons” AND DECIDED PROVISO IN WILL TO BE INVALID.

Millers Attorneys George © member of the PhatshoaneHenney Group 74

GREY AREA (4) (still iro certain aspects)

VARIATION WHERE

BENEFICIARIES HAVE

ACCEPTED BENEFITS

(REPARABLE)

Millers Attorneys George © member of the PhatshoaneHenney Group 75

VARIATION OF BENEFICIARIES

PERSONAL TRUST (B18.2.2)

• First establish whether beneficiaries have acquired any rights Then determine the kind of right ie if vested or real or personal right and if beneficiary a minor heed should be taken of all the protective rules pertaining to minors eg Court application may be necessary

• Where rights of beneficiaries are not vested but they have accepted benefits ito stipulatio alteri they then have to be party to amendment Crookes v Watson 1956 1 SA 277 (A) Hofer v Kevitt 1998 1 SA 382 (SCA) Now also Potgieter v Potgieter 2012 1 SA 637 (SCA) (personal right vis-à-vis trustees and statutory fiduciary duty of trustees)

Millers Attorneys George © member of the PhatshoaneHenney Group 76

TRUST OBJECT: Personal

• CHANGING OBJECT OF THE TRUST ? (B6.3

& 8.4)

• The only object which a family trust can

have is the benefit of the beneficiaries i.e.

specifically defined as a class of persons

– What if that class of beneficiaries is

substituted with a new class (sale of trust) or

– A specific beneficiary i.e. a spouse

specifically named, in deed is substituted

– Object changed? Valid amendment?

Millers Attorneys George © member of the PhatshoaneHenney Group 77

VARIATION BY AGREEMENT(1)

• Where founder is alive, the stipulations of trust deed can be varied ito rules of the law of contract instead of derived powers ito trust deed’s variation clause All subject to beneficiaries’ rights

• Can one only rely on derived powers ito trust deed to amend? No – Potgieter-case

• Can one argue that the derived powers to amend will be binding on the beneficiaries, even where they have accepted benefits? No – Potgieter-case

Millers Attorneys George © member of the PhatshoaneHenney Group 78

VARIATION OF AGREEMENT (2) Acceptance? (B18.2.2 & Cameron 498/9)

• No form is prescribed for acceptance –

acceptance even after death of founder

• Advisable for beneficiary to write to trustees

accepting the benefits under a trust

• A “mere mental attitude of approbation” does not

amount to acceptance

• Unequivocal expression of intention to accept

(benefit) needed – factually determined Where

beneficiary is not a party to the trust deed can he

accept deed’s terms if he does not even know

what it is?

Millers Attorneys George © member of the PhatshoaneHenney Group 79

VARIATION OF AGREEMENT (3) (B18.2.2)

Acceptance? (B18.2.2)

• Remember trustees are also bound by their

common law fiduciary duty to exercise an

independent view and cannot adhere to

founder/trustee’s wishes which can prejudice the

existing beneficiaries ie to amend trust deed to

include e.g. new spouse/friend etc

• See practical examples from case law in

Cameron 499-500

• Because the trust is not a true stipulatio alteri,

can all the acceptance of benefits rules apply?

Millers Attorneys George © member of the PhatshoaneHenney Group 80

VARIATION OF AGREEMENT (4)

Still unresolved after Potgieter-case:

1. Is a trust really akin to a true stipulatio alteri ? – See all

the exceptions – eg PBO trust & none of the parties drop

out - is it correct that all the rules also apply to the trust?

2. What is the nature of the right of such a beneficiary that

has accepted benefits?

3. Can one renounce your acceptance? E.g. after a divorce

4. What about beneficiaries who have accepted but cannot

be traced for an amendment ?

5. Can you do a blank acceptance? E.g. when you learn that

you are a beneficiary to a trust, can you accept the

benefits blank and so cause yourself to become a party

to the trust until your demise – also iro of all possible

variations ?

Millers Attorneys George © member of the PhatshoaneHenney Group 81

Variation? Check also for “TESTAMENTARY RESERVATION”

• It is a contractual right / power and not a

testamentary right given in the trust deed to a

founder or one or more of the trustees to

prescribe the formula for the distribution of

benefits among the beneficiaries

• Right to be exercised in a specific way and in a

specific document namely the last will of the

person for whom the right is contractually

reserved

• Erroneous application often causes

discretionary nature of trust to change or

disappear and vesting to take place

THUS

IS THE “INDEPENDENT

OUTSIDER” TRUSTEE

NECESSARY OR JUST A

GOOD IDEA (or perhaps only

‘window dressing’)?

Millers Attorneys George © member of PhatshoaneHenney Group 82

IS “INDEPENDENT” REALLY

“INDEPENDENT” ? (1) AND IS IT REALLY WORKING?

• APPEARS AS IF NOT : Two examples where

“independant outsiders” were trustees :

• Jordaan-case 2001 3 SA 288 (CPD)

• Badenhorst-case 2006 2 SA 255 (SCA)

• There may be more case-examples where

“independent outsider” did/could not prevent

abuse of power by co-trustee

Millers Attorneys George © member of PhatshoaneHenney Group 83

“INDEPENDENT” REALLY

“INDEPENDENT” ? (2)

In Badenhorst v Badenhorst 2006 2 SA 255 (SCA)

(Delivered on 29/11/05) Combrinck AJA held the

following on the two tier test for control:

• That control would have to be de facto and not

necessarily de iure, and to determine whether a

party had such control it was necessary to first

have a regard to the terms of the trust deed and

to consider how the affairs of the trust were

conducted during the marriage. (Par 9)

• SEE ALSO ADDITIONAL REFERENCE SLIDES iro

CONTROL & TAX & INSOLVENCY

Millers Attorneys George © member of the PhatshoaneHenney Group 84

“INDEPENDENT” REALLY

“INDEPENDENT” ? (3) • TRUST REGARDED AS ALTER EGO

1) Jordaan v Jordaan 2001 3 SA 288 (C) 301BC

2) Follow-up on 1) :Zazeraj NO v Jordaan

Unreported Case no 22526/11 (Judgment on 22-

3-2012) ZAWCHC Meer J decided:

• Defence of res judicata cannot succeed –not the

same issues or parties [19-21]

• Variation of trust deed invalid – [22 & 27]

• Trustees have to account to beneficiary [23 & 27]

• Trustee removed as trustee [24 & 27]

Millers Attorneys George © member of the PhatshoaneHenney Group 85

DRAFTING STRANGE,

SOMETIMES BAD OR

RESTRICTIVE

CLAUSES IN TRUST

DEEDS Millers Attorneys George © member of the PhatshoaneHenney Group 86

Millers Attorneys George © member of the PhatshoaneHenney Group 87

VALIDITY OF TRUST DEED

The fact that a trust deed was filed with the Master

of the High Court does not mean that deed is valid (B8.5*)

No duty on the Master to check for validity (B8.5*)

*Pace R & Van der Westhuizen WM Wills & Trusts LexisNexis Service

Issue 14 par B 8.5

Millers Attorneys George © member of the PhatshoaneHenney Group 88

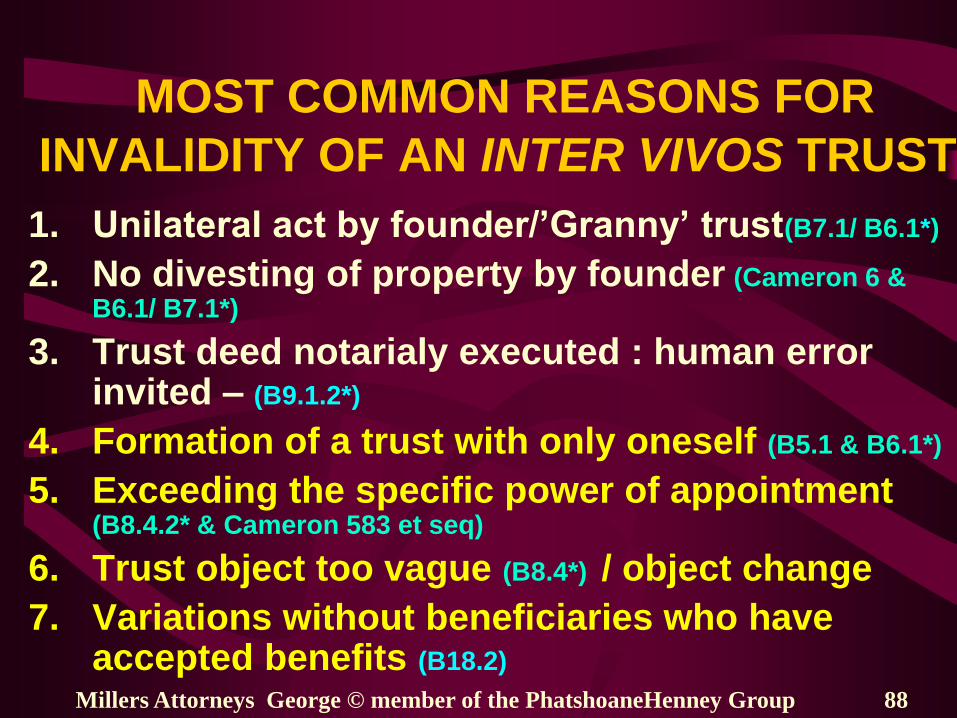

MOST COMMON REASONS FOR

INVALIDITY OF AN INTER VIVOS TRUST

1. Unilateral act by founder/’Granny’ trust(B7.1/ B6.1*)

2. No divesting of property by founder (Cameron 6 & B6.1/ B7.1*)

3. Trust deed notarialy executed : human error invited – (B9.1.2*)

4. Formation of a trust with only oneself (B5.1 & B6.1*)

5. Exceeding the specific power of appointment (B8.4.2* & Cameron 583 et seq)

6. Trust object too vague (B8.4*) / object change

7. Variations without beneficiaries who have accepted benefits (B18.2)

Millers Attorneys George © Member of the PhatshoaneHenney Group 89

MORE

ERRORS MADE WITH

TRUSTS & TRUST

DEEDS (also in RSA)

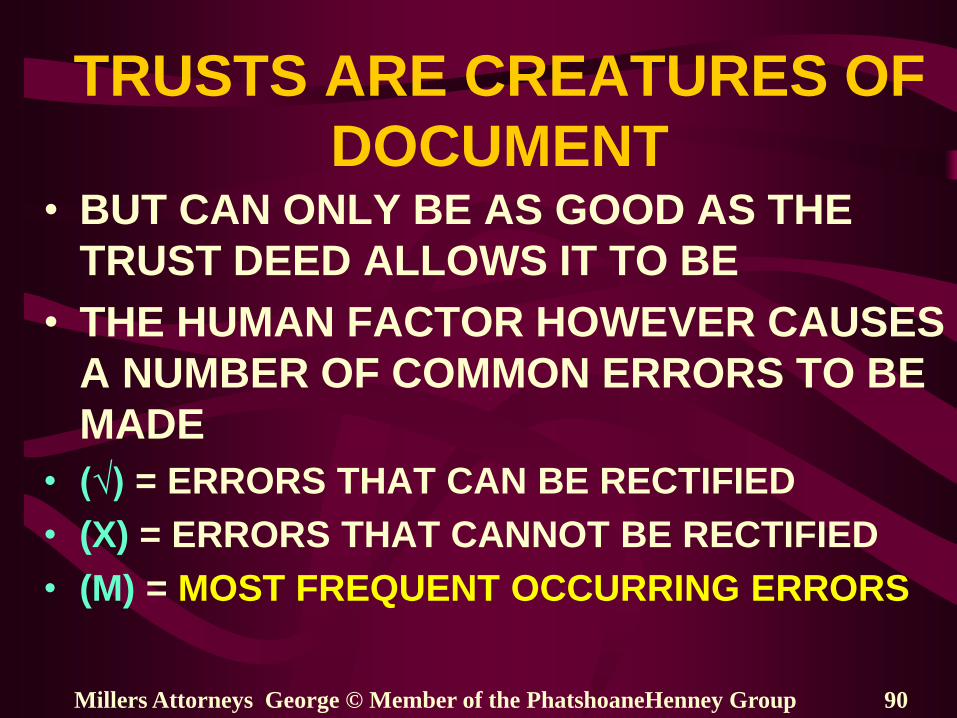

TRUSTS ARE CREATURES OF

DOCUMENT • BUT CAN ONLY BE AS GOOD AS THE

TRUST DEED ALLOWS IT TO BE

• THE HUMAN FACTOR HOWEVER CAUSES

A NUMBER OF COMMON ERRORS TO BE

MADE

• (√) = ERRORS THAT CAN BE RECTIFIED

• (X) = ERRORS THAT CANNOT BE RECTIFIED

• (M) = MOST FREQUENT OCCURRING ERRORS

Millers Attorneys George © Member of the PhatshoaneHenney Group 90

COMMON ERRORS MADE THAT

CAN BE RECTIFIED (1)

• Exceeding specific power of appointment (√) (M)

• Object too vague (√)

• Using of standardized deeds— copy & paste – one size does not fit all (√)

• Trust deeds drafted with very rigid terms (√)

• No power to substitute trustees (√)

• Excessive power/“Alter ego” for one trustee ie to nominate beneficiaries (Sec 12(6) of Income Tax Act can find application)(√)(M)

Millers Attorneys George © Member of the PhatshoaneHenney Group 91

Millers Attorneys George © Member of the PhatshoaneHenney Group 92

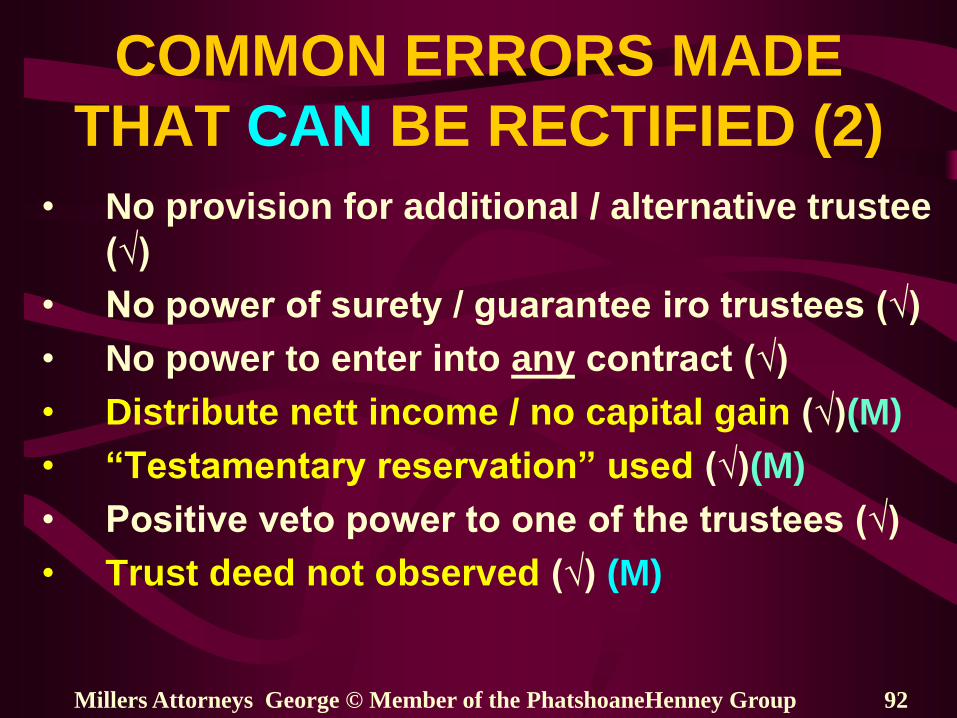

COMMON ERRORS MADE

THAT CAN BE RECTIFIED (2)

• No provision for additional / alternative trustee

(√)

• No power of surety / guarantee iro trustees (√)

• No power to enter into any contract (√)

• Distribute nett income / no capital gain (√)(M)

• “Testamentary reservation” used (√)(M)

• Positive veto power to one of the trustees (√)

• Trust deed not observed (√) (M)

Millers Attorneys George © Member of the PhatshoaneHenney Group 93

COMMON ERRORS MADE

THAT CAN BE RECTIFIED (3) • Only administrative elements may be amended

and founder deceased (√) (M)

• Allowing “in laws” without complete discretion

(√)(M)

• Beneficiaries related by blood/affinity and

other clauses in trust deed (√)(M)

• Incorrect/no roll-over clause into new trust

(√)(M)

• No power to take out short term insurance

(√)(M)

Millers Attorneys George © Member of the PhatshoaneHenney Group 94

COMMON ERRORS MADE

THAT CAN BE RECTIFIED (4) • Resignation clause silent on to whom notice be

given (√)

• Trust deed silent on specific benefits to

trustees i.e. free accommodation (√)(M)

• BBEE/other trusts structured as bewind trusts

(√)(M)

• Family trusts with obligation to keep minutes

and to audit (√)(M)

• Failure to lodge trust deed with Master also

necessary in terms of 1934 Act (√)

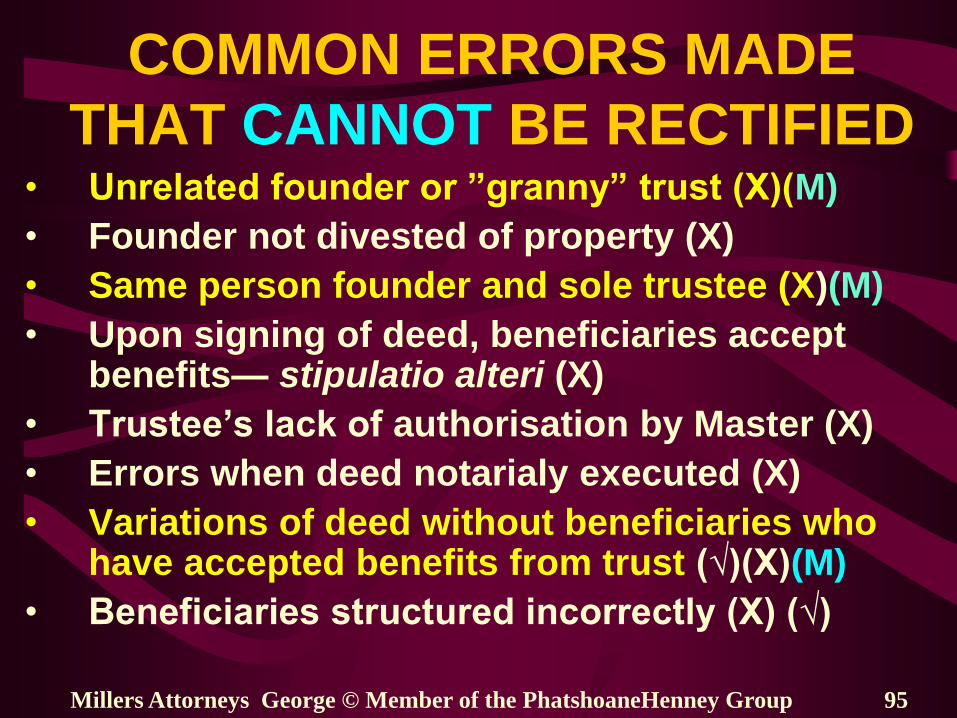

COMMON ERRORS MADE

THAT CANNOT BE RECTIFIED • Unrelated founder or ”granny” trust (X)(M)

• Founder not divested of property (X)

• Same person founder and sole trustee (X)(M)

• Upon signing of deed, beneficiaries accept benefits— stipulatio alteri (X)

• Trustee’s lack of authorisation by Master (X)

• Errors when deed notarialy executed (X)

• Variations of deed without beneficiaries who have accepted benefits from trust (√)(X)(M)

• Beneficiaries structured incorrectly (X) (√)

Millers Attorneys George © Member of the PhatshoaneHenney Group 95

THE TRUST AS RISK

PROTECTION & FAMILY

RELATIONSHIP VEHICLE

FOR RESTRUCTURED

FAMILIES

Millers Attorneys George © Member of the PhatshoaneHenney Group 96

ESTATE PLANNING DURING

DIVORCE / REMARRIAGE (1)

PLANNING BEFORE DIVORCE IS FINAL

1.Review existing estate plan and:

2.Nomination of guardian

3.Powers of attorney

4.Review estate plan of divorcee’s parents

5.Children’s support and their protection

6.Life insurance (nominations)

7.Beneficiary / trustee review

8.Will

Millers Attorneys George © Member of the PhatshoaneHenney Group 97

ESTATE PLANNING DURING

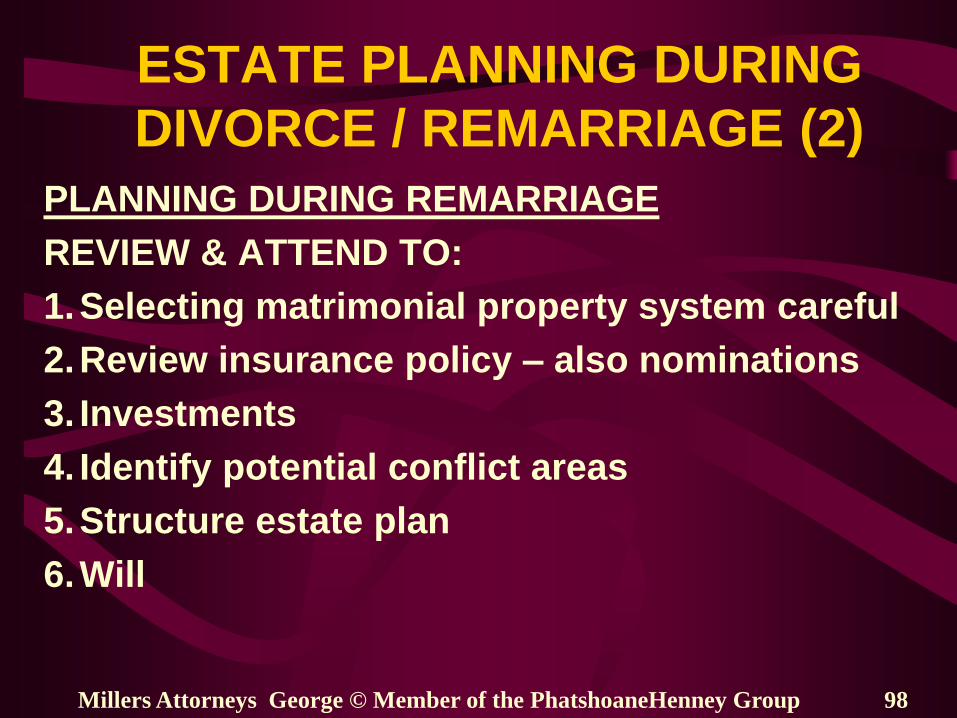

DIVORCE / REMARRIAGE (2)

PLANNING DURING REMARRIAGE

REVIEW & ATTEND TO:

1.Selecting matrimonial property system careful

2.Review insurance policy – also nominations

3. Investments

4. Identify potential conflict areas

5.Structure estate plan

6.Will

Millers Attorneys George © Member of the PhatshoaneHenney Group 98

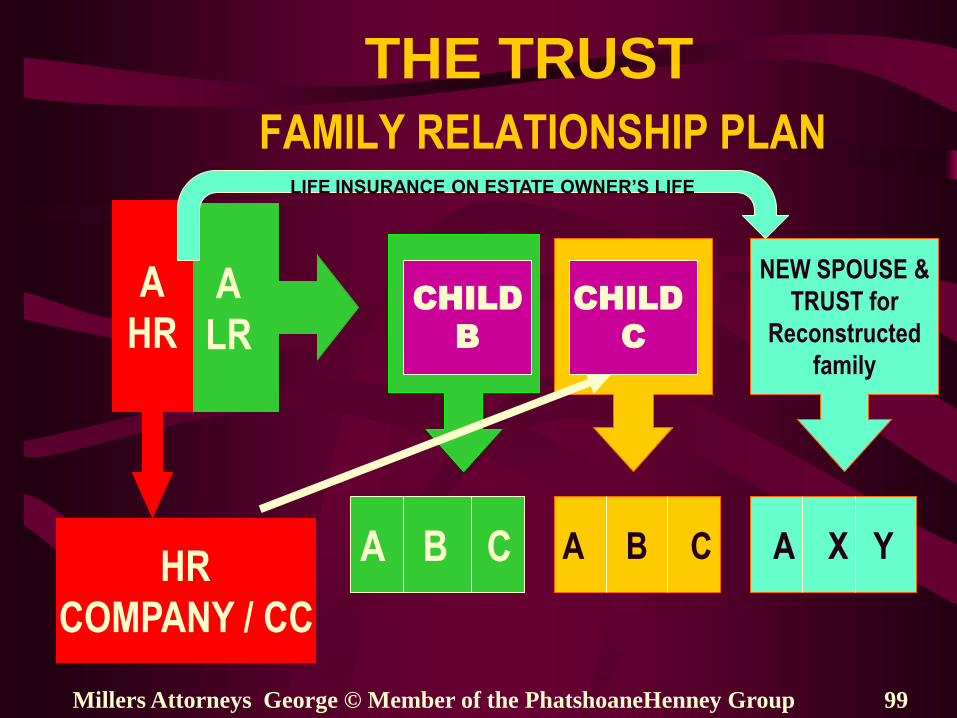

THE TRUST

FAMILY RELATIONSHIP PLAN

Millers Attorneys George © Member of the PhatshoaneHenney Group 99

A

LR LR

TRUST

A B C

MR

TRUST

A B C HR

COMPANY / CC

A

HR CHILD

B

CHILD

C

NEW SPOUSE &

TRUST for

Reconstructed

family

A X Y

LIFE INSURANCE ON ESTATE OWNER’S LIFE

THE ABSENCE OF A BUSINESS

RELATIONSHIP PLAN

INADEQUATE SEPARATION OF INTEREST

GROUPS WHERE THERE ARE :

• Separate shareholders / partners

• BEWARE of risks for trust beneficiaries

with vested rights (ownership) and

“bewind” trust in some business trusts

(which sometimes simulate partnerships)

Millers Attorneys George © Member of the PhatshoaneHenney Group 100

THE TRUST

BUSINESS RELATIONSHIP PLAN

Millers Attorneys George © Member of the PhatshoaneHenney Group 101

A LR

TRUST

A1 A2 A3

MR

TRUST

B1 B2 B3

FAMILY

TRUST

A

FAMILY

TRUST

B

HR

COMPANY / CC

B

OFF-SHORE TRUSTS (1) ESTABLISHMENT HOW ?

• Different trusts rules in different

jurisdictions especially different from

Namibia – Common Law countries

(British related) vs Civil Law countries

(Roman Dutch Law related ie Namibia)

• See explanation by Davis et al Estate

Planning §17.2 on the Jersey trust

described as the “Rolls Royce” of trust

jurisdictions

Millers Attorneys George © Member of the PhatshoaneHenney Group 102

OFF-SHORE TRUSTS (2)

BASIC CHARACTERISTICS?

• Trust deed should specify proper law of

the trust – Founder can specify

• Usually unrestricted powers to add or

exclude beneficiaries – Contra Namibia?

• Common to have “letter of wishes” to

guide trustees

• Founder to relinquish control to trustees

Protector employed to address founder’s

concerns

Millers Attorneys George © Member of the PhatshoaneHenney Group 103

OFF-SHORE TRUSTS (3)

BASIC CHARACTERISTICS? (2)

• Protector not a trustee but can usually

appoint trustees

• Protector usually possess veto rights eg

vote required to make substantial

advances or resettlement into new trust -

- Position described as “fiduciary”.

However role of protector uncertain in

Namibia – at best an agent of the founder

and not subject to Master’s authority

Millers Attorneys George © Member of the PhatshoaneHenney Group 104

TO TRUST OR NOT TO TRUST “Trusts have now pervaded all fields of social

institutions in Common Law countries. They are

like those extraordinary drugs curing at the

same time toothache, sprained ankles and

baldness, sold by peddlers on the Paris

boulevards; they solve equally well family

troubles, business difficulties, religious and

charitable problems. What amazes the sceptical

civilian is that they really do solve them”

Pierre Lepaulle “Civil Law Substitutes for Trusts” 36 The Yale Law

Journal 1126 at 1147 (1927)

Millers Attorneys George © Member of the PhatshoaneHenney Group 105

Millers Attorneys George © Member of the PhatshoaneHenney Group 106

END

THANK YOU

MILLERS INC

GEORGE : TEL 044 874 1140 FAX 044 873 4848

http:/www.millers.co.za E-MAIL [email protected]