Embed Size (px)

Citation preview

Welcome !

Presenter:

Who We Are:

• A leadership and advocacy organization for those who provide, support and benefit from financial planning.

Standard of Care

• All financial planning services will be delivered in accordance with the following standard of care:

• Put the client's best interests first; • Act with due care and in utmost good faith; • Do not mislead clients; • Provide full and fair disclosure of all material

facts; and • Disclose and fairly manage all material

conflicts of interest.

Code of Ethics

• Integrity • Objectivity • Competence • Fairness • Confidentiality • Professionalism • Diligence

From its earliest designs, the Financial Planning

Association (FPA)

included a mandate that members adhere to a

Code of Ethics that reflects their commitment to

help clients

achieve their life goals.

All FPA members are asked to commit to this

Code, CFP® certificants and non-CFP

certificants alike.

FPA's Ethics Committee is charged by

the Board of Directors with reviewing alleged

violations to the Code of Ethics and advising

staff on ways to enhance awareness by FPA

members of their

obligations under the Code.

National Website• www.fpanet.org

o General Public Tabo Planner Searcho Request Speakerso Educational Seminarso Tools & Resources

FPA’s Website Tabs

• Life Goals• Life Crisis• Find a Planner• Ask A Planner• What’s Financial Planning• Glossary

FPA Resources

o Tip of the Weeko Articleso Checklistso Brochureso Audio & Videoo Hot Topics

Contact us – Locally

• 770-516-8322

• www.fpaga.org

Contact us – Nationally

• 800.282.PLAN (7526)

• www.fpanet.org

Money Matters

Ka-ching!

Your generation has incredible spending power.

$100 Billion spent a year of your own money, plus you influence how your parents spend billions more.

What do YOU do with money?

Spending Money

• Where do you buy? What’s the connection between earning and spending?

• What is your spending personality?• Do you know where your money goes?

That money talks, I'll not deny, I heard it once: It said, "Goodbye." ~Richard Armour

TRUE OR FALSE?

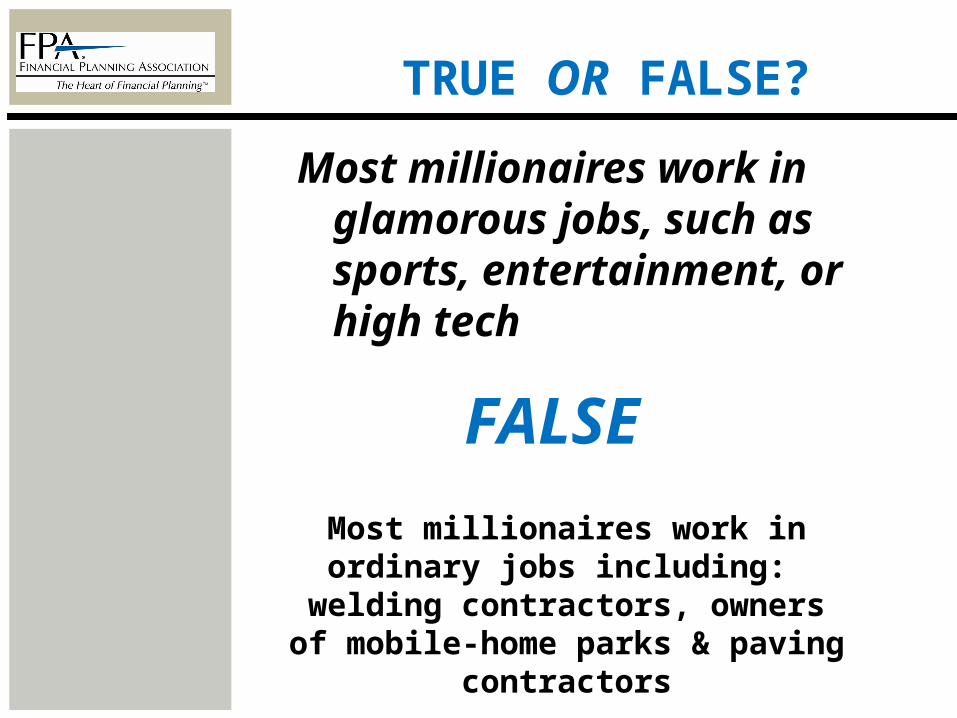

Most millionaires work in glamorous jobs, such as sports, entertainment, or high tech

FALSE

Most millionaires work in ordinary jobs including: welding

contractors, owners of mobile-home parks & paving contractors

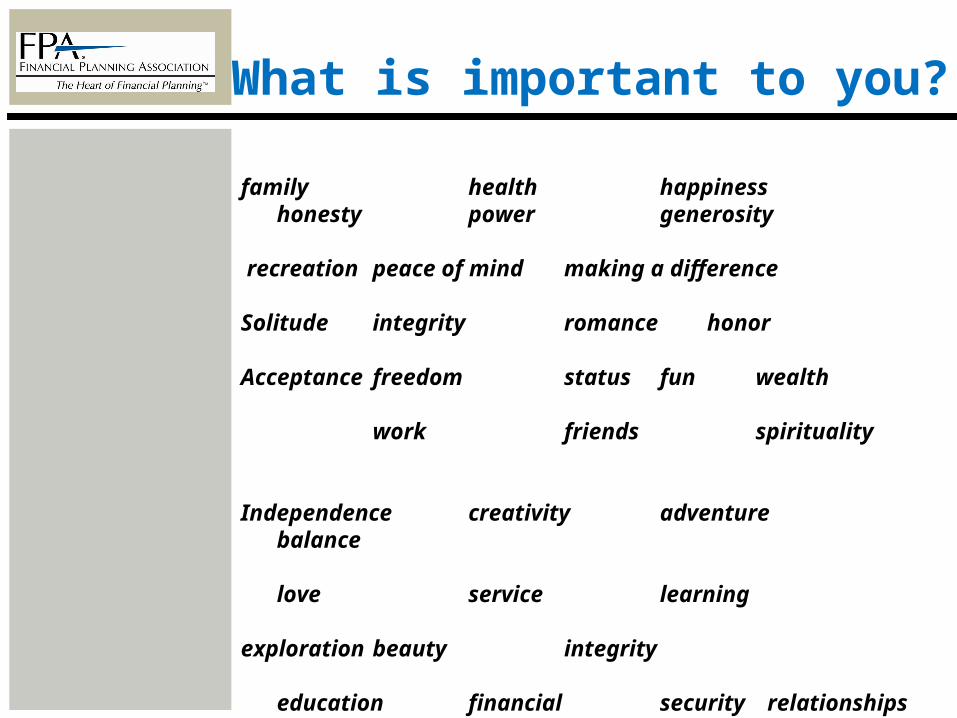

What is important to you?

family health happinesshonesty power generosity

recreation peace of mind making a difference

Solitude integrity romance honor

Acceptance freedom status fun wealth

work friends spirituality

Independence creativity adventurebalance

love service learning

exploration beauty integrity

education financial security relationships

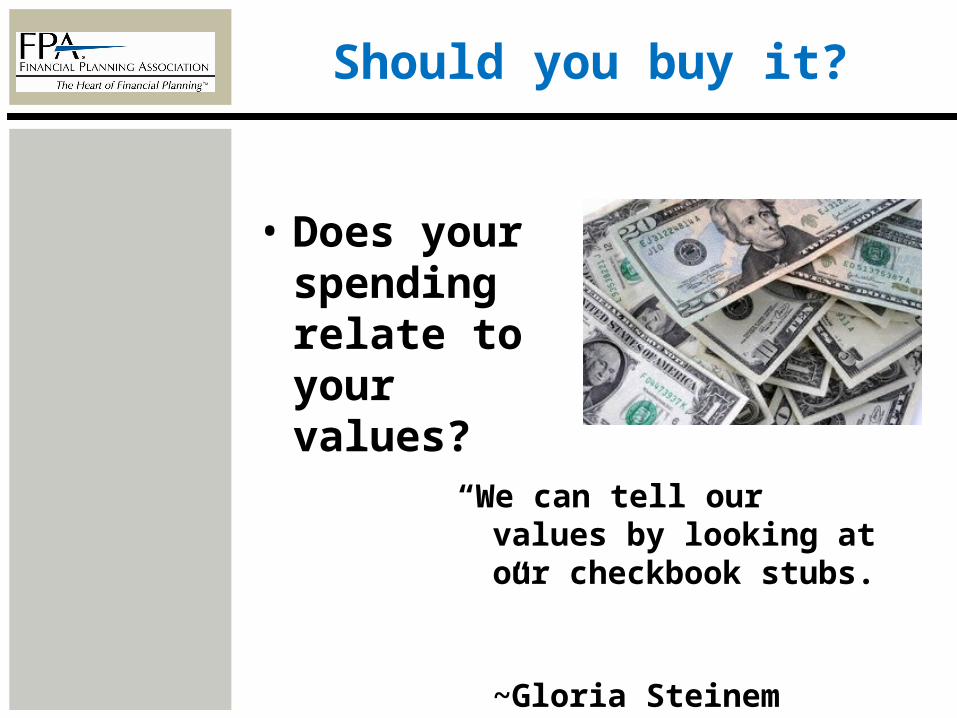

Should you buy it?

• Does your spending relate to your values?

“We can tell our values by looking at our checkbook stubs.”

~Gloria Steinem

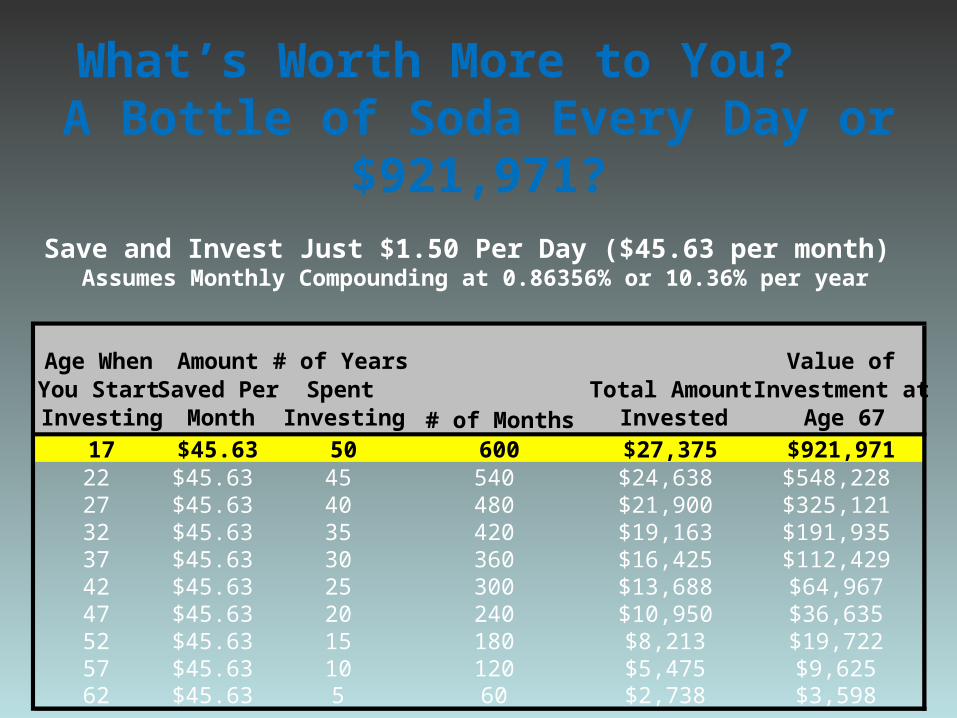

What’s Worth More to You? A Bottle of Soda Every Day or

$921,971?Save and Invest Just $1.50 Per Day ($45.63 per month) Assumes Monthly Compounding at 0.86356% or 10.36% per year

Age When You Start Investing

Amount Saved Per

Month

# of Years Spent

Investing # of MonthsTotal Amount

Invested

Value of Investment at

Age 67

17 $45.63 50 600 $27,375 $921,97122 $45.63 45 540 $24,638 $548,22827 $45.63 40 480 $21,900 $325,12132 $45.63 35 420 $19,163 $191,93537 $45.63 30 360 $16,425 $112,42942 $45.63 25 300 $13,688 $64,96747 $45.63 20 240 $10,950 $36,63552 $45.63 15 180 $8,213 $19,72257 $45.63 10 120 $5,475 $9,62562 $45.63 5 60 $2,738 $3,598

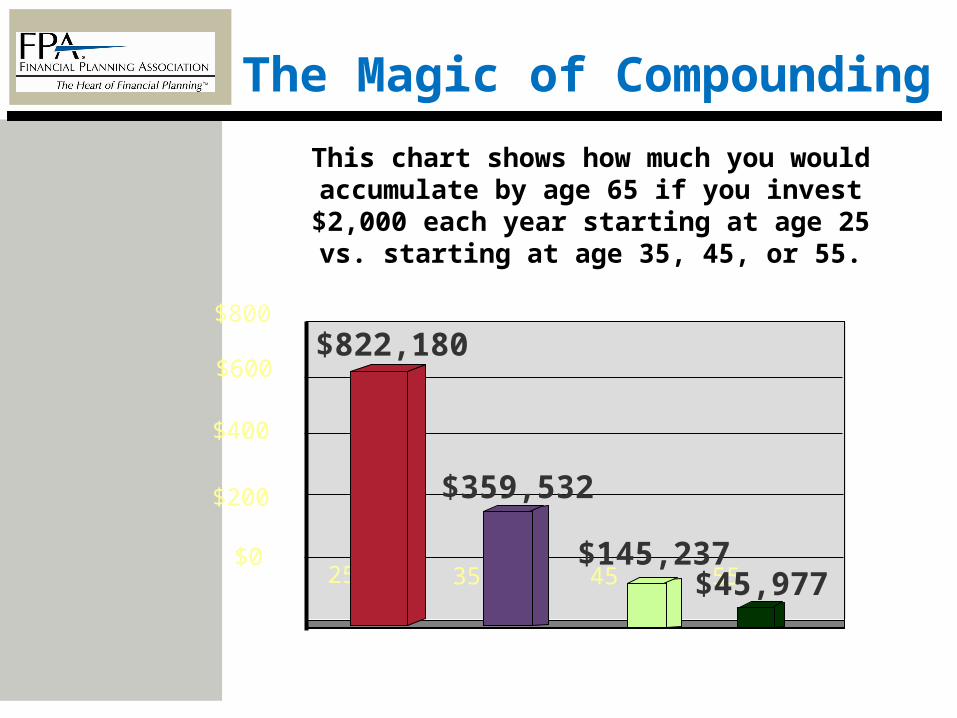

This chart shows how much you would accumulate by age 65 if you invest $2,000 each year starting at age 25 vs. starting at

age 35, 45, or 55.

The Magic of Compounding

25$0

$200

$400

$600

25 35 45 55$0

$200

$400

$600

$800$822,180

$359,532

$145,237$45,977

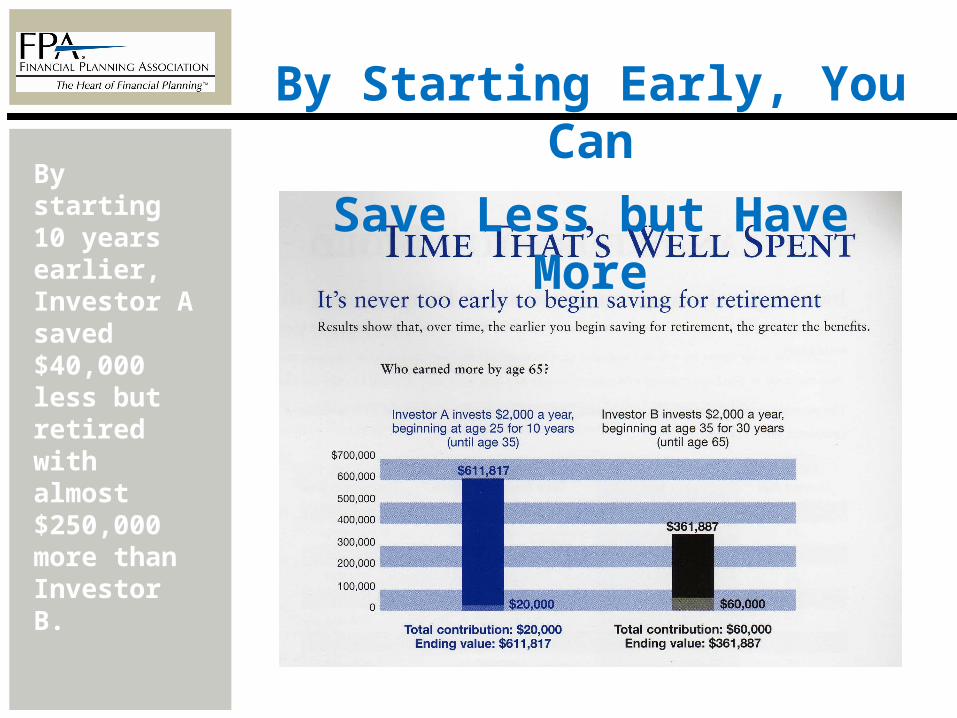

By starting 10 years earlier, Investor A saved $40,000 less but retired with almost $250,000 more than Investor B.

By Starting Early, You Can

Save Less but Have More

Time Can Work For You, or Against You…

• Inflation: the tendency for prices to rise over time.

• Inflation Erodes the Purchasing Power of Your Money!

• You can help overcome inflation by starting to save at an early age.

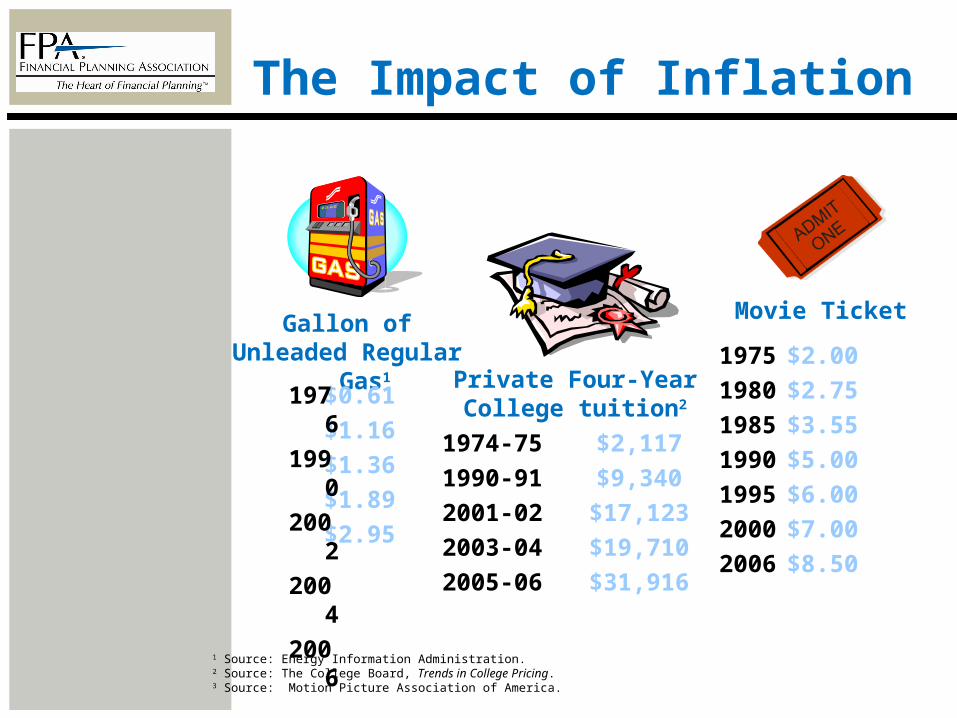

The Impact of Inflation

1 Source: Energy Information Administration. 2 Source: The College Board, Trends in College Pricing. 3 Source: Motion Picture Association of America.

Gallon ofUnleaded Regular Gas1

Private Four-YearCollege tuition2

Movie Ticket

$0.61

$1.16

$1.36

$1.89

$2.95

1976

1990

2002

2004

2006

$2,117

$9,340

$17,123

$19,710

$31,916

1974-75

1990-91

2001-02

2003-04

2005-06

$2.00

$2.75

$3.55

$5.00

$6.00

$7.00

$8.50

1975

1980

1985

1990

1995

2000

2006

TRUE OR FALSE?

4 out of 5 Millionaires

are college graduates

TRUE

We know you’ve heard it before, but…

“An investment in knowledge always pays the best interest.”

~Benjamin Franklin

It’s true! Check out the stats…

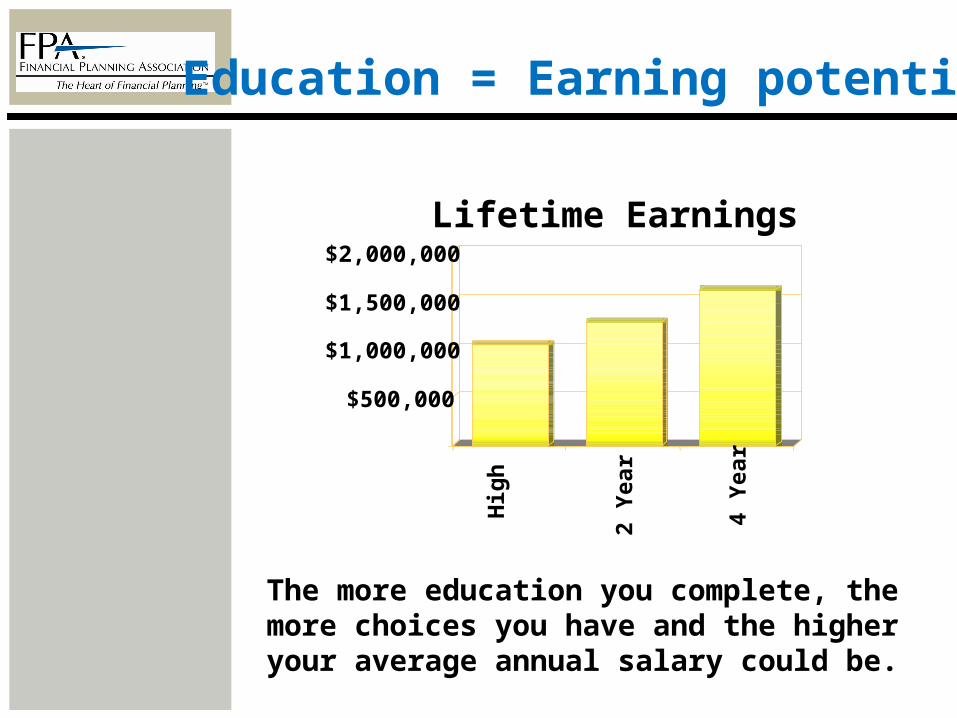

Education = Earning potential

The more education you complete, the more choices you have and the higher your average annual salary could be.

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

Hig

hS

ch

oo

l

2 Y

ear

4 Y

ear

Lifetime Earnings

Saving vs. Investing

• SAVE for short-term goals• INVEST for long-term goals

• Saving is putting money aside and not wasting it.

• Investing is putting your time or money into something with the hope of getting something greater in return – invest to make a profit.

• Investing involves risk; the more risk, the greater the possible reward.

“The safe way to double your money is to fold it over once and put it in your pocket.”

~Frank Hubbard

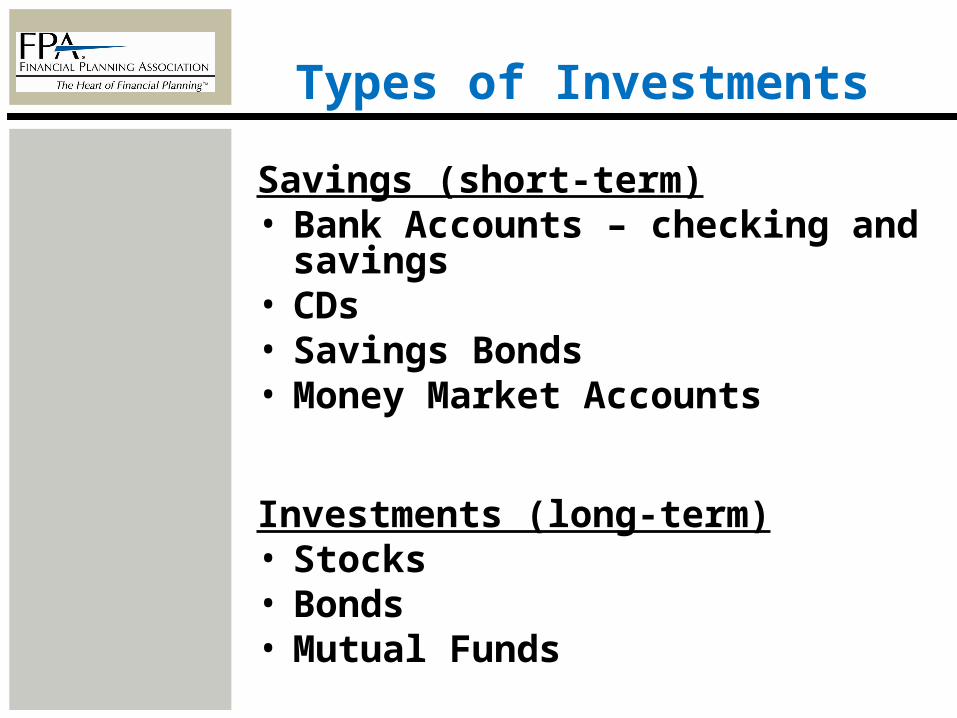

Types of Investments

Savings (short-term)• Bank Accounts – checking and

savings• CDs• Savings Bonds• Money Market Accounts

Investments (long-term)• Stocks• Bonds• Mutual Funds

“We are made wise not by the recollection of our past, but by the responsibility for our future.”

~George Bernard Shaw

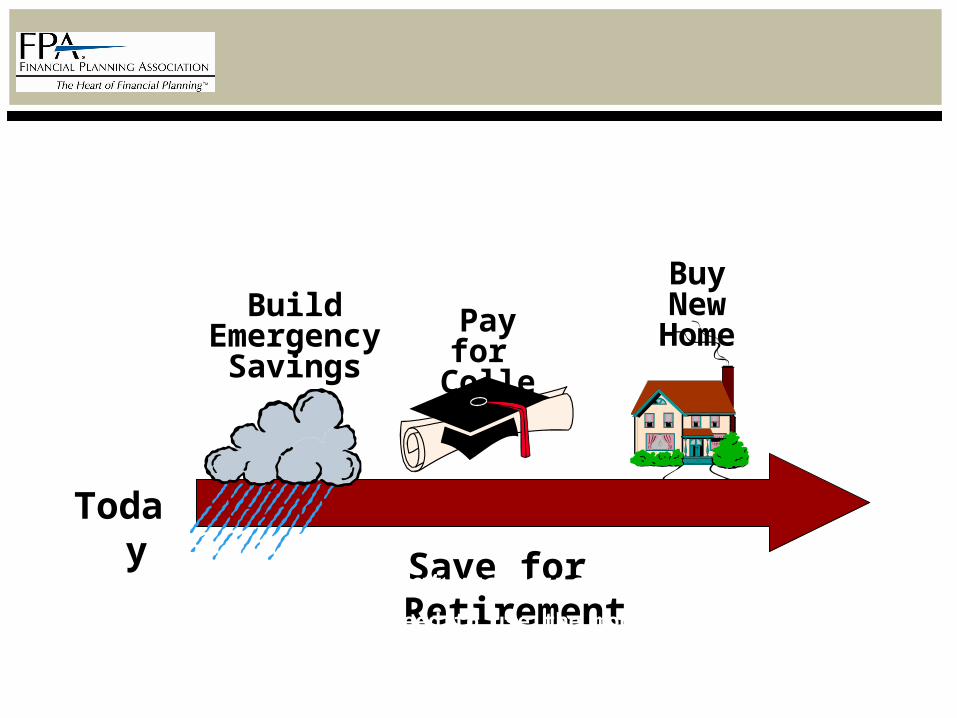

BuildEmergency

Savings

Pay for

College

Save for Retirement

Today

BuyNew

Home

Investment Objective – what are you saving for?

• Time Horizon – When do you need to use the money?

• Risk Tolerance – How comfortable are you with the market’s ups and downs?

What Can You Do NOW?

Be smarter about your spending

• Shop around for the best deals• Don’t buy on impulse• Use coupons or wait for sales• Always use cash

What Can You Do NOW?

• Start saving NOW in a bank account for money you’ll need in the short term.

• Spend money only on what you NEED (and plan for spending on things you WANT).

• LIST your financial goals – with as much detail as possible.

“Save $150 for a new skateboard.”“Avoid spending on junk food to save for a new pair of jeans.”

How Do You Open an Account?

Savings Account:• Need Social Security number or ITIN • Need state issued photo ID • No minimum age to open Savings Account• If under 18, must be secondary account w/

parent/guardian

Checking Account:• Need Social Security number or ITIN• Need State issued photo ID• Must be 16 years or older. • If under 18, must be secondary account w/

parent/guardian

“You got to be careful. . . if you don't know where you're going, you might not get there.”

~Yogi Berra

Let’s review

• Time value of money

• More education means more choices

• NOW is the time to start saving…any amount is better than nothing!

Thank You!

Curriculum Development Committee:Beth Albrecht, BestPrepCarla Barker, Northwestern MutualJohn Comer, Comer Consulting LLCMike Eckert, Cornerstone Capital ManagementAndy Fishman, Affiance FinancialShawn Jacobson, Legacy Financial AdvisorsBob Kaitz, BestPrepSteve Lear, Affiance FinancialNicole Middendorf, Strategic FinancialJanet Stanzak, Financial EmpowermentBonnie Vagasky, BestPrep

BestPrep gratefully acknowledges the Foundation for Financial Planning for providing financial support to fund this project. We also are indebted to the Financial Planning Association of Minnesota for their help in creating and piloting this presentation.

Contact us – Locally

• 770-516-8322

• www.fpaga.org

Contact us – Nationally

• 800.282.PLAN (7526)

• www.fpanet.org

![Copyright 2014, I am Norm I am Norm Youth Advocacy Workshop [Presenter name(s) here]](https://img.pdfslide.us/doc/110x75/56649cf95503460f949ca2ed/copyright-2014-i-am-norm-i-am-norm-youth-advocacy-workshop-presenter-names.jpg)