Embed Size (px)

Citation preview

1

Welcome and Introduction

Bernd HesseNGPON2 Council Chairman, BASE Chairman, Broadband Forum

Sen. Director Technology Development, [email protected]

2

Introduction

Welcome to

BASEBroadband Access Summit Event

Broadband Access Summit Events BASE is an educational event to update the market on the latest technology and use cases for innovative access technologies. These workshops are quarterly events and will ensure to cover all regions. BASE will focus on providing technology advantages, updates and readiness for deployment of next generation access networks. Base is an industry event, to provide the audience an opportunity to hear from leading component and system vendors, as well as network operators, as they share their insights on the latest technologies, applications, use cases, and deployments. The focus areas are:

• Optical Access Technologies• Copper Access Technologies• Virtual Access Technologies• Optical Connectivity • 5G Fixed Technologies

3

BASE overview• Broadband Forum organized 5 workshops in 2017

• Workshops are educational event to update the market on the latest technology and use cases for innovative access technologies.

• Workshops are industry events, to provide the audience an opportunity to hear from • leading component • system vendors• network operators

• Focus is on providing technology advantages, updates and readiness for deployment of next generation access networks with the Focus Areas

• Optical Access Technologies• Copper Access Technologies• Virtual Access Technologies• Optical Connectivity • 5G Fixed Technologies

• Workshops are quarterly events and will ensure to cover all regions.

4

BASE Agenda structure

Segment Track 1Optical

Track 2Copper

Track 3Virtual Access

Track 4Optical Connectivity

Track 55G Fixed

Worldwide Access Market overview

Component Market update

Ecosystem Overviews

Integration and Applications

Best Practices

Presenter

Lead analysts from market research companies will provide market updates

Component vendors will provide status, challenges and innovations

System Vendors will present individual solution offerings and capabilities

Leading operators will provide their view for choosing the specific technologies as their access network architectures

Consultants will provide their view on access planning scenarios

BASE workshop

5

BASE Next steps• Establish new BBF Councils

– Virtual Access Council

– Optical Connectivity Council

– 5G Fixed Council

• Establish BASE cross Council function

• Plan BASE for 2018– Multiple tracks with target areas

• Optical Access Technologies √

• Copper Access Technologies √

• Virtual Access Technologies

• Optical Connectivity

• 5G Fixed Technologies

– Define on locations• Q1 Athens prior to BBF Q meeting √

• Q2 Asia Location TBD

• Q3 Europe Location TBD

• Q4 North America Location TBD

√

6

Agenda BBWF BASE Berlin Oct 2017 (1)8:00 - 8:40

8:40 - 8:45

8:45 - 10:45

Track 1 - Virtualization track room Track2 - Keynote room

Track 1: NG-PON2 Track2: GFASTModerator Moderator

Time Robert Conger AVP of Cloud and Portfolio Strategy / Adtran Michael Weissman Marketing / Sckipio

NG-PON2 Standards and Components Update Gfast Certification, Testing, and Standardization

Hal Roberts System Engineer and Architect / Calix Lincoln Lavoie Senior Engineer for broadband Technologies / UNH-IOL

Enabling new architectures with converged technologies GFast is ready for the Gigabit era

Kevin Bourg Director, Optical Network Architect / Corning Rami Verbin CTO / Sckipio

Time for Fiber Management Pivot Dynamic Timing Assignment in GFast

Farshid Mohammadi Head Worldwide Sales / GoFoton Werner Heinrich Director Portfolio Management Broadband Solutions / Adtran

Empowering NGPON2 by tunable simple optics The evolution of power requirements in converged access networks

Antonio Teixeira CTO & Founder / PicAdvanced Rudy Musschebroeck Director, Business development / Commscope

Low-Cost Coherent Detection for NG-PON2 Standardization of xDSL and MGfast in ITU-T

Jesper Bevensee Jensen CTO & Founder / BiFrost Communications Hiroshi OTA Study Group Advisor, ITU/TSB

NGPON2 Optical Design Considerations The DSL roadmap from G.fast to Terabit-fast

RYAN MCCOWAN Director Portfolio Management / Adtran John M. Cioffi CEO & Chairman, Board of Directors ASSIA Inc.

10:45 - 10:55

Market update

8:45 - 9:05

9:05- 9:25

9:25 - 9:45

Break

Roland Montagne Principal Analyst, Director DigiWorld Institute / Idate

9:45 - 10:05

10:05 -10:25

Component market update

Keynote room

8:00 - 8:10

8:10 - 8:40

Welcome and Intro

Bernd Hesse BBF BASE Chairman, Sen.Director Technology Development / CALIX

Access Market update "FTTH Global Perspective – Lessons to be learned"

10:25 -10:45

Break

7

Agenda BBWF BASE Berlin Oct 2017 (2)10:55 - 12:15

Track 1 - Virtualization track room Track2 - Keynote room

Track 1: NG-PON2 Track2: GFASTModerator Moderator

Time Robert Balsamo VP Advanced Architecture Standards, Advanced Architecture / Calix Mark Fishburn Director Marketing /BBF

NG-PON2 a catalyst for SDA Fiber to the Distribution Point Minus the Fiber

Thomas Martin Principal Sales Engineer / Calix Kurt Raaflaub Head of Strategic Solutions Marketing / Adtran

Building Scalable SDN-Controlled NGPON2 Access Systems The rise of copper to multi-gigabit

Robert Conger AVP of Cloud and Portfolio Strategy / Adtran Keith Russell Product Marketing Director / Nokia

Getting more from the fiber networks with NGPON2 Deploying Gfast: lessons learnt today and moving forward

Ana Pesovic Marketing Director Fixed Networks / Nokia Craig Thomas Senior Director International Marketing / Calix

NG-PON2 and underlining technologies The New Software Defined Access Networks (SD Access)

Paulo Mao-Cheia System and Network Development Manager / Altice Labs Michael Howard Senior Research Director, Carrier Networks / IHS Markit

12:15 - 12:35

12:35 - 14:00

Track 1 - Virtualization track room Track2 - Keynote room

Track 1: NG-PON2 Track2: GFASTModerator Moderator

Time Michael Howard Senior Research Director, Carrier Networks / IHS Ray Le Maistre Editor in Chief/ Lightreading UBB2020

Enabling the UK’s next generation network

Trevor Linney Head of Access Technology Research / BT

NGPON2 as a new way of looking at the access AT&T Gfast Overview

Vincent O'Byrne Director- Technology Group / VZ Tom Starr Lead Member of technical staff / AT&T

NG NETWORKS & SERVICES ENABLING STRATEGY DT’s Access 4.0 – first findings

Luis Alveirinho Director of Engineering & Network Operations / Portugal Telecom Robert Soukup Senior program manager / DT

Towards the Gigabit society Modernising Cyta' s copper access network for complementing FTTH

deployments

Marco Boselli Fixed Access Engineer / Vodafone Charis Themistou Head of Planning and Design Section / CYTA

Panel discussion Panel discussion

All All13:45 - 14:00

13:30 - 13:45

Integration and applications update

13:15 - 13:30

12:35 - 13:00

13:00 - 13:15

Break

Ecosystem market update

10:55 - 11:15

11:15 - 11:35

11:55 - 12:15

11:35 - 11:55

8

Segment 1

Market update

9

Last figures and players strategies Superfast Broadband will be detailed.What are the position of the different regions of the World regarding FTTH rollouts?What are the key players in that field?Finally we will list different drivers for Fiber and identify why we need NGPON2 now.

Access Market update "FTTH Global Perspective – Lessons to be learned"

Market update

Roland Montagne Principle Analyst IDATE

FTTH Global Perspectives

Lessons to be learned

Broadband Forum Access Summit – Berlin, October 24th 2017

Contact

Roland MONTAGNE

Principle Analyst

Director DigiWorld Institute UK

www.idate.org © IDATE DigiWorld 2017 – p. 11

1. FTTx Worldwide Key Trends 3

2. Major Players Worldwide 7

3. FTTH…

3.1. ... in Europe 11

3.2. ... in LATAM 21

3.3. ... in APAC 28

3.4. …and now in Sub Saharan Africa 36

4. Drivers for Fibre: The Gigabit Race, Short Latency and 4K / 8K ! 43

5. Conclusion: Why NG PON 2 now? G.Fast Drivers 49

Agenda

www.idate.org

1. FTTx Worldwide Key Trends

FTTH Global Perspective: Lessons to be learned

www.idate.org © IDATE DigiWorld 2017 – p. 13

FTTx Worldwide key trends

> Superfast technologies(1) represented nearly 48% of

broadband access subscriptions at end 2016, 9 points more

than one year before.

> FTTH/B is still the leading superfast broadband solution, far

ahead of FTTx/D3.0, followed by VDSL

FTTH/B represented 68% of FTTx subscriptions at end 2016. Growth of

FTTH/B subscriptions will continue until 2021.

FTTx/D3.0 represented at end 2016, 20% of FTTx subscriptions. After two

years of significant growth, proportion of FTTx/D3.0 on Superfast

Broadband is levelling off.

VDSL, for its part, lagged behind, representing 12% of subscriptions at

June 2016 . This proportion is quite stable.

> The regional breakdown is very heterogeneous

No huge changes in the geographical predominance of APAC on the

FTTH/B market.

FTTH/B is also the main deployed technology in MENA. It was the case

also in LATAM, but now it is meeting stronger competition from VDSL

technologies in the region (especially in Brazil).

FTTx/D3.0 is still dominant in North America and is by and large growing

more rapidly than other technologies.

There is considerable space for VDSL and other copper based

technologies such as G.Fast in Europe, where incumbents still wish to

optimise their copper networks.

(1) For the definition of superfast platforms we have considered here three main architectures: FTTH/B,

FTTN and FTTx/D3.0 deployed by cable operators

Breakdown of superfast broadband technologies, as of December 2016

Source: IDATE DigiWorld, World FTTx market, August 2017

www.idate.org © IDATE DigiWorld 2017 – p. 14

Breakdown of Superfast broadband technologies

Geographical breakdown of the three main superfast broadband architectures, at December 2016

Source: IDATE DigiWorld, World FTTx market, August 2017

VDSL: 62 million subscribers (1) FTTH/B: 342 million subscribers FTTx/D3.0: 101 million subscribers

505 million FTTx

subscribers Worldwide

at end 2016

MEA = Middle East and Africa; LATAM = Latin America; APAC = Asia-Pacific; NA = North America; EUR = Western + Eastern Europe

(1) 11.8 M FTTx°+LAN subscribers in China are not taken into account.

www.idate.org © IDATE DigiWorld 2017 – p. 15

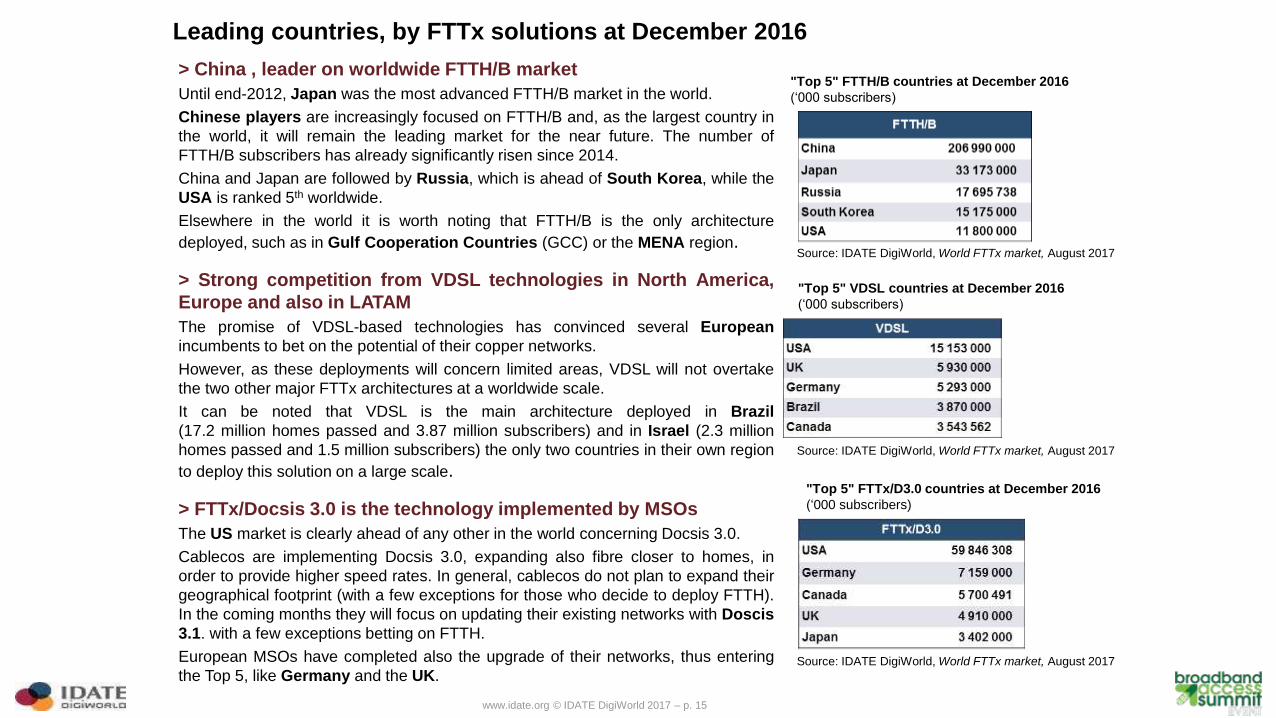

Leading countries, by FTTx solutions at December 2016

> China , leader on worldwide FTTH/B market

Until end-2012, Japan was the most advanced FTTH/B market in the world.

Chinese players are increasingly focused on FTTH/B and, as the largest country in

the world, it will remain the leading market for the near future. The number of

FTTH/B subscribers has already significantly risen since 2014.

China and Japan are followed by Russia, which is ahead of South Korea, while the

USA is ranked 5th worldwide.

Elsewhere in the world it is worth noting that FTTH/B is the only architecture

deployed, such as in Gulf Cooperation Countries (GCC) or the MENA region.

> Strong competition from VDSL technologies in North America,

Europe and also in LATAM

The promise of VDSL-based technologies has convinced several European

incumbents to bet on the potential of their copper networks.

However, as these deployments will concern limited areas, VDSL will not overtake

the two other major FTTx architectures at a worldwide scale.

It can be noted that VDSL is the main architecture deployed in Brazil

(17.2 million homes passed and 3.87 million subscribers) and in Israel (2.3 million

homes passed and 1.5 million subscribers) the only two countries in their own region

to deploy this solution on a large scale.

> FTTx/Docsis 3.0 is the technology implemented by MSOs

The US market is clearly ahead of any other in the world concerning Docsis 3.0.

Cablecos are implementing Docsis 3.0, expanding also fibre closer to homes, in

order to provide higher speed rates. In general, cablecos do not plan to expand their

geographical footprint (with a few exceptions for those who decide to deploy FTTH).

In the coming months they will focus on updating their existing networks with Doscis

3.1. with a few exceptions betting on FTTH.

European MSOs have completed also the upgrade of their networks, thus entering

the Top 5, like Germany and the UK.

"Top 5" FTTH/B countries at December 2016

(‘000 subscribers)

"Top 5" VDSL countries at December 2016

(‘000 subscribers)

"Top 5" FTTx/D3.0 countries at December 2016

(‘000 subscribers)

Source: IDATE DigiWorld, World FTTx market, August 2017

Source: IDATE DigiWorld, World FTTx market, August 2017

Source: IDATE DigiWorld, World FTTx market, August 2017

www.idate.org

2. Major players Worldwide

FTTH Global Perspective: Lessons to be learned

www.idate.org © IDATE DigiWorld 2017 – p. 17

World leading providers, all FTTx architectures

> There are 5 Asian and 3 US players in the global Top 10. Then one player from Russia and one from Western Europe

> Indeed, only one player from Western Europe enters the ranking thanks to its large-scale FTTN+VDSL rollouts (BT)

> Two US cablecos have now completed their infrastructures migration to FTTx/D3.0: Comcast and Charter (Spectrum)

> The Mega merger in USA has taken European cableco Virgin Media out of the TOP 10 chart

> China’s three telcos (China Telecom, China Unicom and China Mobile) top this FTTxranking

106 M subscribers

FTTH/B

4.7 M subscribers

FTTN+VDSL#95.7 M subscribers

FTTH

#10

70 M subscribers

FTTH/B

#2

#1

7.4 M subscribers

FTTB

#819.9 M subscribers

FTTH/B

#424.7 M subscribers

FTTx/D3.0

#3

#77.8 M subscribers

FTTH/B

31 M subscribers

FTTH/B

#6

#521.4 M subscribers

FTTx/D3.0

Source: IDATE DigiWorld, World FTTx market, August 2017

www.idate.org © IDATE DigiWorld 2017 – p. 18

Snapshot of the world’s leading FTTH/B providers

19.9

106

70

7.85.7

3.8

3.5

4.6

7.4

31

Worldwide FTTH/B leaders (million), December 2016

Source: IDATE DigiWorld, World FTTx market, August 2017

3

<1

www.idate.org © IDATE DigiWorld 2016 – p. 19

Telcos vs. cablecos> Cable operators have played a major role in fostering the superfast

broadband market in the US and Europe

• Competition from cablecos that have upgraded their infrastructure has pushed

telcos to launch their own projects, either based on FTTH/B or FTTN+VDSL

• Deploying a superfast broadband network based on fibre was the only way to

compete with cablecos by providing faster connections and TV services (HD &

multiscreen)

> Cable operators in the US have now upgraded all their networks to FTTx+

Docsis 3.0

• Now American cablecos can provide speeds up to 2 Gbps in selected areas

(Comcast) but most of the time maximum speed available is 100 Mbps or below

(Charter Spectrum),

• Docsis 3.1 can extend the bandwidth provided on HFC plants, which is why

some operators are considering implementing this technology or even switching

from Fiber+Coax directly to FTTH/B at mid term (Altice USA).

> In Europe, FTTx + Docsis 3.0 has been largely deployed particularly in the

UK, Germany and Benelux

• In the UK, Virgin Media has already upgraded its entire network, representing

13.2 M households. It provides value-added services, including TV services, not

supported by the ADSL network.

• In Spain, Ono, now part of Vodafone group, is the leading cableco with nearly 2

M FTTx/D3.0 subscribers.

• In Germany, Kabel Deutschland – which is also part of the Vodafone group – was

reporting 3.7 million subscribers and 15.5 million homes passed as of end 2016.

> Docsis 3.1 is now selected by several MSOs

• This is the case in Europe: TDC in Denmark plans to complete the Docsis 3.1

transformation of the entire network by the end of 2017, Virgin Media as part of

its Lightning Project is also considering Docsis 3.1

• Outside Europe: Vodafone New Zealand is also involved in Docsis 3.1 as the

solution to bring speeds of up to 1Gbps.

US A

UK

Netherlands

Germany

South Korea

Spain59.9

0.9

4.9

3.2

7.2

2.6

Japan3.4

Canada

5.7 Poland1.1

Belgium2.3

FTTx/D3.0 subscribers by region, December 2016

Geographical breakdown of FTTx/D3.0 subscribers, end 2016

(million)

1Hungary

29%

65%

1%4% 1%

Europe

North america

Latin America

Asia Pacific

Middle East & Africa

Source: IDATE DigiWorld, World FTTx market, August 2017

Source: IDATE DigiWorld, World FTTx market, August 2017

www.idate.org

3.1. FTTH in Europe

FTTH Global Perspective: Lessons to be learned

www.idate.org © IDATE DigiWorld 2017 – p. 21

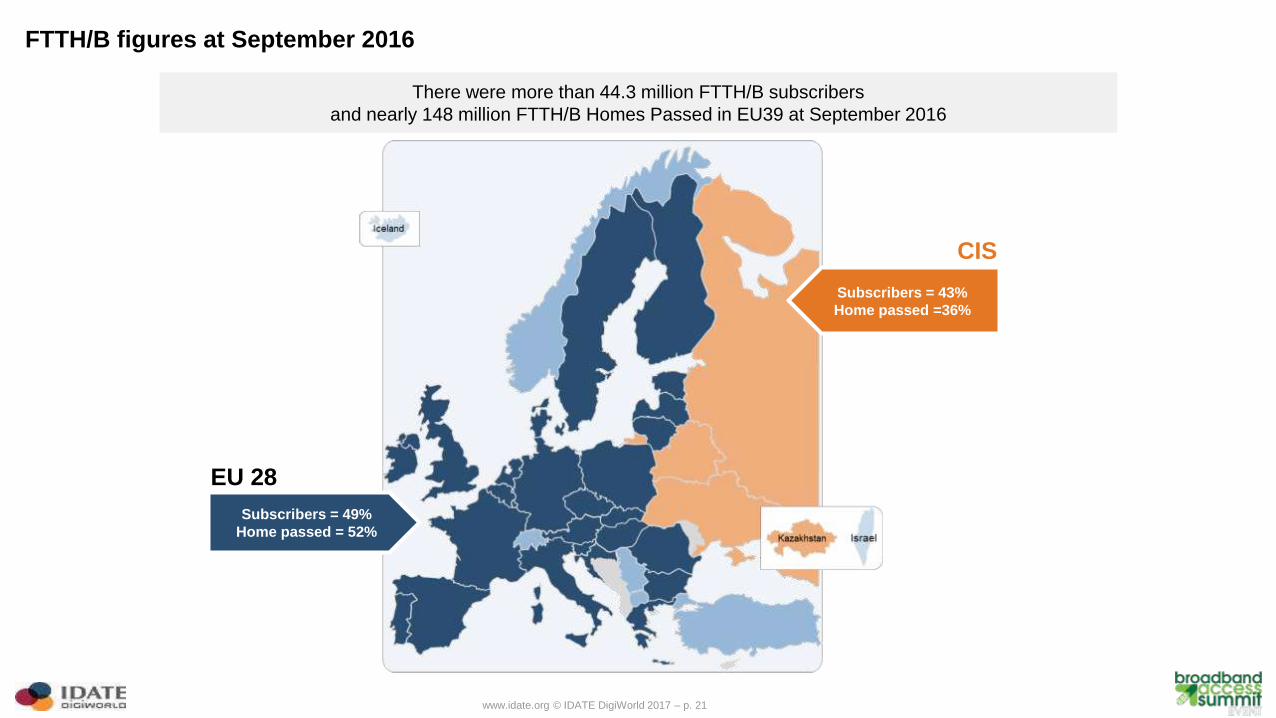

FTTH/B figures at September 2016

There were more than 44.3 million FTTH/B subscribers

and nearly 148 million FTTH/B Homes Passed in EU39 at September 2016

Subscribers = 49%

Home passed = 52%

EU 28

Subscribers = 43%

Home passed =36%

CIS

www.idate.org © IDATE DigiWorld 2017 – p. 22

Historical data and growing trends

•Interesting dynamism of the European Union since 2013

•CIS countries : higher growth rates for subs than for HP between January and September 2016

•Globally: an increase of the growth rate during the first 9 months of 2016! Especially for EU28

Source: IDATE DigiWorld for FTTH Council Europe

Growth of FTTH/B subscribers

(million)

Growth of FTTH/B Homes Passed

(million)

0

5

10

15

20

25

30

35

40

45

50

Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Sep-15 Sep-16

EU39

EU28

CIS

0

20

40

60

80

100

120

140

160

Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Sep-15 Sep-16

EU39

EU28

CIS

www.idate.org © IDATE DigiWorld 2017 – p. 23

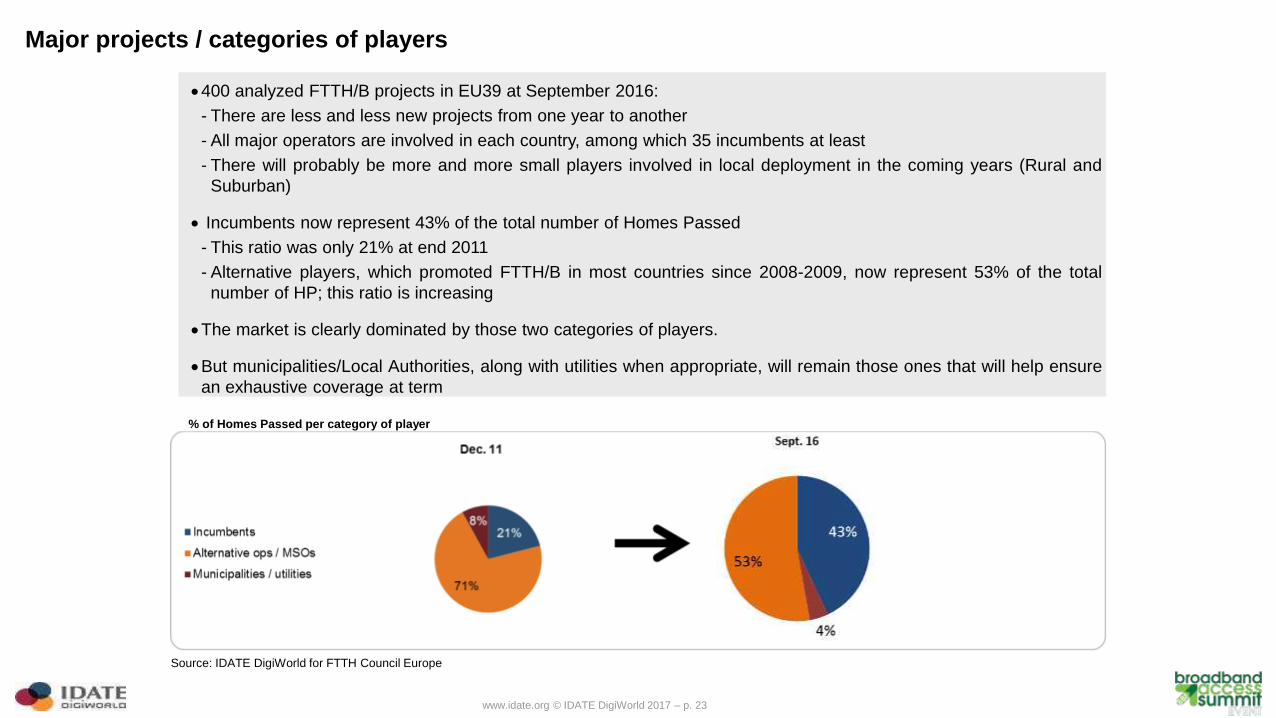

Major projects / categories of players

•400 analyzed FTTH/B projects in EU39 at September 2016:

- There are less and less new projects from one year to another

- All major operators are involved in each country, among which 35 incumbents at least

- There will probably be more and more small players involved in local deployment in the coming years (Rural and

Suburban)

• Incumbents now represent 43% of the total number of Homes Passed

- This ratio was only 21% at end 2011

- Alternative players, which promoted FTTH/B in most countries since 2008-2009, now represent 53% of the total

number of HP; this ratio is increasing

•The market is clearly dominated by those two categories of players.

•But municipalities/Local Authorities, along with utilities when appropriate, will remain those ones that will help ensure

an exhaustive coverage at term

Source: IDATE DigiWorld for FTTH Council Europe

% of Homes Passed per category of player

www.idate.org © IDATE DigiWorld 2017 – p. 24

General ranking: FTTH/B Homes Passed

•17 countries with 2 M HP or more in EU39 (10 countries in EU28, in blue on the map)

•Most significant growth rates do not necessarily concern the largest market but this confirms that, even in

countries where FTTH/B is not the leading NGA solution, the interest is growing (e.g. Bulgaria: +40%)

Countries with 2 M HP or more at Sept 2016 [Top 5 Growth rates for 9 first months 2016]

(million)

Source: IDATE DigiWorld for FTTH Council Europe

www.idate.org © IDATE DigiWorld 2017 – p. 25

General ranking : FTTH/B coverage

Average FTTH/B coverage*: EU39 45%

EU28 33%

(*) Number of HP/total number of Households

Top 10 countries in coverage at September 2016

Source: IDATE DigiWorld for FTTH Council Europe

www.idate.org © IDATE DigiWorld 2017 – p. 26

General ranking: FTTH/B Subscribers

•9 countries with 1 M subscribers or more in EU39 (5 countries in EU28, in red on the map))

•Strong growth in Spain, Belarus, Finland and Portugal

•Dynamism to highlight in France and Italy

Countries with 2 M HP or more at Sept 2016 [Top 5 Growth rates for 9 first months 2016]

(million)

Source: IDATE DigiWorld for FTTH Council Europe

www.idate.org © IDATE DigiWorld 2017 – p. 27

General ranking : FTTH/B take-up rate

Average FTTH/B take up rate (*): EU39 30%

EU28 28%

(*) Take up rate = number of subscribers / number of Homes Passed

Top 10 countries of more than 200 K subs in take-up rate at

September 2016

Source: IDATE DigiWorld for FTTH Council Europe

www.idate.org © IDATE DigiWorld 2017 – p. 28

European ranking

•The European Ranking includes countries of more than 200 K HH where the part of FTTH/B subs in the total number of HH is at least 1%

•Only 12/31 European countries with a penetration rate > 20%

Source: IDATE DigiWorld for FTTH Council Europe

www.idate.org © IDATE DigiWorld 2017 – p. 29

Key points for Europe

> There already 31 European countries that are part of the Global ranking … a positive sign even if the

bottom line is only 1%.

> Even the “reluctant” countries are moving towards FTTH/B technologies. The historic trend shows this

evolution and there are more countries reaching the 100% of coverage!

> End users are migrating to FTTH networks. But the switch to FTTH/B connection is not systematic yet

and therefore there is still a large room for communication by operators.

> Governments and local authorities are entering the game and the Digital Agenda is one of the main

important objectives to achieve.

•DAE’s main requirements are respected in all EU28 countries

•Local authorities are more dynamic in Scandinavian countries and in France: they should impulse a new

dynamic to reach more rural areas and in countries where FTTH/B is lagging far behind other architectures

•“French Model” as an example for Europe?

> Highest take up rates in Northern and Eastern countries: still strong competition from other

architectures elsewhere.

> Nearly all players, even if less involved in FTTH/B than other architectures, consider that FTTH is the

end game! … and 5G will need Fibre!

www.idate.org

3.2. FTTH in LATAM

FTTH Global Perspective: Lessons to be learned

www.idate.org © IDATE DigiWorld 2017 – p. 31

Alternative operators leadership in LATAM

> A positive evolution: 82 FTTx projects in the region

> Players different from incumbents have deployed fibre in a dynamic way from 2015 to September 2016

covering with fibre more homes:

•Municipalities / Power Utilities have grown 33%

•Alternative operators growth: 19%

•Incumbents: Growth rate about 5%

Incumbents:

4 161 000 FTTH/B Homes Passed

Municipalities / Utilities:

190 800FTTH/B Homes Passed

Alternative Operators:

18 987 187FTTH/B Homes Passed

Source: IDATE DigiWorld for FTTH LATAM Chapter

www.idate.org © IDATE DigiWorld 2017 – p. 32

Global FTTH figures for LATAM

> FTTH/B is taking a bigger place in the LATAM Market due to a positive evolution in the deployment and

user’s adoption…

4 552 698 FTTH/B

subscribersby Sept. 2016

in LATAM

23 352 987 FTTH/B Homes

Passed by Sept. 2016 in

LATAM

19.5% FTTH/B Take

up rate by Sept. 2016 in

LATAM

25% growthfrom 2015

18% growthfrom 2015

+1.4 pointsfrom December 2015

Take up rate = FTTH-B subs / Total FTTH-B Home Passed

Source: IDATE DigiWorld for FTTH LATAM Chapter

www.idate.org © IDATE DigiWorld 2017 – p. 33

FTTH subscribers per countries for LATAM

> … it can be also appreciated a good evolution in lower scale markets such as Jamaica, Trinidad, Barbados and Peru…

Source: IDATE DigiWorld for FTTH LATAM Chapter

www.idate.org © IDATE DigiWorld 2017 – p. 34

FTTH Homes Passed per countries for LATAM

> While Mexico and Brazil are the leaders in homes passed, significant deployment are also performed in

other smaller LATAM Markets…

www.idate.org © IDATE DigiWorld 2017 – p. 35

FTTH Coverage for LATAM

> Coverage: Top 10 countries in terms of % of FTTH/B Homes Passed in total Households

•Number of Homes Passed not representative of effective coverage

•Here, the ratio represented is % of FTTH/B Homes Passed in total households

- 2 countries > 90% !!!

- 3 countries > 20%

- 5 countries over 10%

•Argentina: 8.5%

Source: IDATE DigiWorld for FTTH LATAM Chapter

www.idate.org © IDATE DigiWorld 2017 – p. 36

Key points for LATAM

> LATAM users want more reliable Internet services with higher bandwidth:

• Network Players are now convinced that FTTH access is the end game.

• Low quality of existing copper as a driver: Telcos are betting on FTTH/B to promise innovative services and

higher speed rates

> The competition between cablecos and telcos is a driver for FTTH/B. Some cablecos also investing in

Fiber access

> Players with presence in several countries in the region are driving FTTH rollouts (Telefonica, Telmex /

Claro, Cable & Wireless / Flow , Digicel)

> In most of cases, FTTH/B and LTE are deployed together in LATAM

> Several Governments in LATAM have promoted the creation of National Fibre Networks

• Brazil, Chile, Argentina, Costa Rica

www.idate.org

3.3. FTTH in APAC

FTTH Global Perspective: Lessons to be learned

www.idate.org

FTTH/B is taking a bigger place in the APAC Market due to a positive evolution in the deployment and specially in the user’s adoption

Source: IDATE for FTTH Council APAC

297.8 million FTTH/B

subscribers by Dec. 2016

in APAC

436.5 million FTTH/B Homes

Passed by Dec. 2016 in

APAC

68% growth from 2015

12.5% growth from 2015

68% FTTH/B Take

up rate by Dec. 2016 in

APAC

> + 20 points from December 2015

Take up rate = FTTH-B subs / Total FTTH-B Homes Passed

www.idate.org © IDATE DigiWorld 2017 – p. 39

Total FTTH/B Homes Passed by country

The Top-4: China is N0 1 by far due to the size of its market. Even though, countries like Japan, South Korea and Indonesia have reached 50 or more

than 10 million homes passed with FTTH/B networks

Also it can be observed 10 countries that have deployed FTTH/B networks passing more than 1 million homes

7.6 7.5

3.85

3.082.8

2.5 2.3 2.28

1.21 1.06

0

1

2

3

4

5

6

7

8

Thailand Taiwan India Australia Kazakhstan Philippines Hong Kong Malaysia Singapore New Zealand

FT

TH

/B H

P M

illio

ns

320

52

18 13

0

50

100

150

200

250

300

350

China Japan South Korea Indonesia

FT

TH

/B H

P M

illio

ns

Source: IDATE DigiWorld for FTTH Council APAC

The largest market worldwide. Important network overlapping. Coverage higher than gvt’s objectives

Source: IDATE DigiWorld for FTTH APAC

www.idate.org © IDATE DigiWorld 2017 – p. 40

0.00%

100.00%

200.00%

300.00%

400.00%

500.00%

600.00%

700.00%

Philippines Thailand Australia New Zealand Indonesia India China Taiwan Malaysia Kazakhstan

Source: IDATE DigiWorld for FTTH Council APAC

% variation from Dec-2015 to Dec-16 in the number of FTTH/B Homes Passed by country

An aggressive deployment plan performed by PLDT

Also, significant deployment efforts has been executed during 2016 for example in Philippines, Thailand,

Australia and New Zealand…

www.idate.org © IDATE DigiWorld 2017 – p. 41

Number of Homes Passed not representative of effective

coverage

Here, the ratio represented is % of FTTH/B Homes Passed

in total households

•5 countries > 90% !!!

•7 countries > 20%

•1 country over 10%

Source: IDATE DigiWorld for FTTH Council APAC

Japan: 100%

Singapore: 100%

Taiwan: 96.5%

South Korea: 95.7%

Hong Kong: 93%

China: 70.2%

Kazakhstan: 62.2%

New Zealand:

60.4%

Thailand: 38.7%

Australia: 34.3%

Malaysia: 33.7%

Indonesia: 20.9%

Philippines: 12.4%

India: 1.4%

Coverage: Top countries in terms of % of FTTH/B Homes Passed in total Households

www.idate.org © IDATE DigiWorld 2017 – p. 42

Total FTTH/B Subscribers by country

While China has increased its fibre subscribers and is still the leading country….

… countries like Japan and South Korea also have more than 30 or 10 million FTTH/B subscribers…

… and it can be observed 8 countries that already passed 1 million of FTTH/B subscribers

230

0

50

100

150

200

250

China

Mil

lio

ns

33

15

0

5

10

15

20

25

30

35

Japan South Korea

Mil

lio

ns

0

1

2

3

4

5

6

Mil

lio

ns

Source: IDATE DigiWorld for FTTH Council APAC

www.idate.org © IDATE DigiWorld 2017 – p. 43

Key points for APAC

> Demography: a huge market potential

•India and China are the most populated countries in the world

•MDUs are dominating in large cities especially in China

•A huge potential of 550 M population: Bangladesh, Philippines, Vietnam and Pakistan

> Low competition from other xDSL or Cable networks

•The “quality gap” between copper and fibre networks is important: end users need fibre for higher bandwidth

•Cablecos are less dominating the broadband market than in Europe or in the US … and it’s not going to

change for now (SARFT in China)….a few exceptions like in India

> A key driver for mass market migration in APAC: NBN programs… the NZ success, now followed by the

Australian one

> Incumbents leading rollouts in APAC but also some free room for new entrants

•Some incumbents are deeply involved in national FTTH/B deployments (Philippines: PLDT accelerating now,

Indonesia, Malaysia)

•New entrants in large countries (India), mature markets (HK) or emerging markets (Vietnam)

> APAC Fibre dynamic is also being pushed by Mobile demands…

•Fibre for mobile Backhaul : LTE and metro / small cells … and 5G coming soon in APAC !!

www.idate.org © IDATE DigiWorld 2017 – p. 44

India

China

Indonesia

Vietnam

Malaysia

Thailand

Pakistan

Bangladesh

Advanced

deploymentsShort run Long run

Maturity

Horizon

Market size

Small

Large

AustraliaTaiwan

Singapore

New Zealand

PhilippinesFrontrunners

Heavy weights

?Laos

Cambodia

Myanmar

South Korea

Japan

Champions

FTTH/B APAC Markets evolution

HKRising stars

Nepal

Source: IDATE DigiWorld for FTTH APAC

www.idate.org

3.4. FTTH in Sub Saharan Africa

FTTH Global Perspective: Lessons to be learned

www.idate.org © IDATE DigiWorld 2017 – p. 46

Context

• A lack of investment in fixed copper networks,

still mainly owned by governments; the

penetration of fixed lines is declining.

• Therefore a rather low adoption of fixed BB:

4% of households in 2016 in SSA.

• Generally speaking, a lack of regulation

towards fair competition and network

openness (LLU), so leading private players to

bypass incumbent’s fixed network (FTTH).

• Leapfrog to wireless network: At the end of

2016, more than 100 active LTE networks in

43 countries deployed

• The deployment of submarine cables has

lowered international bandwidth prices

(formerly via satellite). But the access is

limited to countries with a sea frontage.

Landlocked countries need to be connected

via transnational backbones.

Networks penetration in Sub Saharan Africa (SSA)

Source : IDATE

Numer of fixed lines, fixed BB subscribers, SIM cards, Mobile BB users

4G deployments in Africa in 2016

Source : IDATE

8%1%

12%

5% 4%

118%

0%

20%

40%

60%

80%

100%

120%

140%

Fixed lines Fixed BB Mobile BB

2011 2012 2013 2014 2015 2016

www.idate.org © IDATE DigiWorld 2017 – p. 47

FTTH/B in Africa: Overview

• A native FTTH/B market

• But a good dynamic with a steady

growth in some countries, and

commercial launch in about 17 countries

in SSA.

After Submarine cables …Terrestrial backbones

Source : AfTerFibre (African Terrestrial Fiber)

FTTH/B deployments in Africa (June 2017)

Source : IDATE

Commercial

Planned

South Africa

Kenya

Namibia

Angola

Nigeria

Zambia

Zimbabwe

Mozambique

Madagascar

Lesotho

Rwanda

Réunion

Mauritius

Cameroun

Eq. Guinea

Gabon

Tanzania

Ghana

www.idate.org © IDATE DigiWorld 2017 – p. 48

FTTH leading countries in Africa

• South Africa is the leader, with 650 K FTTH subscribers.

• Other countries in the Top 5: Mauritius, Angola, Kenya and Tanzania

• Then 4 other territory and countries follow between 50 K and 15 K FTTH subscribers: La Réunion, Zimbabwe,

Mozambique, and Nigeria.

• Others countries follow such as Gabon, Cameroon, Madagascar, Rwanda, Eq. Guinea, Lesotho and Namibia.

FTTH/B subscribers by country – Top 5 (June 2017)

Source : IDATE

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

Around 3 K Less than 500

FTTH/B subscribers by country – Second league (June 2017)

Source : IDATE

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

SouthAfrica

Mauritius Angola Kenya Tanzania

www.idate.org © IDATE DigiWorld 2017 – p. 49

South Africa: the FTTH leader in Africa

The main SSA telecom market

• 20% of the SSA telecom market

A mature telecom market

• 170,3% mobile density

• 12,1% fixed BB density

Specificities

• High CAPEX needed to deploy nationally, due to population

distribution and topology – low population density

• Specificity of communities and HOA (Home Owner

Associations), launching FTTH tenders and educating the

communities

A BB market dominated by Telkom

49

FTTH subscribers in South AfricaBackground

South Africa: the land of Open Access for Fibre

Main players

• Dark Fibre & Wholesale: Vumatel, Open Serve (Telkom),

Dark Fibre Africa, Link Africa, Frogfoot Networks, Metrofibre

network, MTN, Neotel, Tesuco, Vodacom,…

• Retailers & Service Providers: Telkom, Vodacom, MTN,

Vox telecom, MWEB, WebAfrica, Cell-c, 1GB, Cape Connect,

ISP Afrika, Nexus, easi telecom, snowball, cool ieas, iconnect,

Greencom, Adept, Sonic Telecom, Comtel, Flynet …

FTTH players Source : IDATE

15 23 33

97

234

452

570

650

0

100

200

300

400

500

600

700

2010 2011 2012 2013 2014 2015 June2016

June2017

Tho

usa

nd

s

At June 2017:

- A YoY growth of 14% in terms of subscribers

www.idate.org © IDATE DigiWorld 2017 – p. 50

Africa in the global ranking50

FTTH/B subscribers in Africa (SSA)

Source : IDATE

953 000 FTTH/B subscribers at June 2016

• Close to 1,3 million FTTH/B subscribers at June 2017

• A good growth of 33% in one year

• Two countries are now well installed in global ranking

(Number of residential subscribers / number of

households) at June 2017:

- Mauritius : 53,8% in the

Top league close to Japan

- South Africa : 4,2%

• New Entry: ANGOLA with 2,3% !!

• La Reunion as a territory: 16,7%

1,27 M FTTH/B subscribers at June 2017

www.idate.org © IDATE DigiWorld 2017 – p. 51

Key points for Africa

> Incumbents have not invested enough in the cooper network … Driver for FTTH

> Many governments have established national BB plans … but in several SSA countries Regulation not

really favorable for FTTH competition

> Open Access as a clear driver for FTTH… but for the moment only in South Africa

> World Bank as a major investor in the region, but up to now mainly focus on backbones.

> Private pan-regional players such as Liquid Telecom, MTN, Wananchi Group, Visabeira Group,

Vodafone, Orange stir up the market

> Importance of submarine cable / backbone as a prerequisite

➢ Businesses addressed first in some countries but Residential FTTH is not reserved to an Elite …

upper middle class is developing and will be addressed with FTTH offering

> The demand for BB connection is rising with new services and content available (particularly Netflix

now widely available in Africa & 4K).

> 4G and mobile of tomorrow (5G) will fuel FTTH business plan.

www.idate.org

4. Drivers for Fibre :

The Gigabit Race, Short Latency and 4K TV !!

FTTH Global Perspective: Lessons to be learned

www.idate.org © IDATE DigiWorld 2017 – p. 53

How Gbps plans are evolving

53

Since 2013, Providing Gigabit

access has become a goal in

itself. The momentum has

been largely influenced by

Google’s initiatives, since

followed by private sector

operators and especially a

number of cities.

At the federal level, the

Government and the FCC

have announced new

measures in support of city-

led rollouts.

Europe

The Digital Agenda (DAE)

sets Europe’s connectivity

targets: 30 Mbps for all, and

100 Mbps connections or more

for at least 50% of European

households by 2020.

These appear very modest

targets when compared to

current technological

possibilities, and the

accelerated pace of the Gigabit

race, which more and more

ISPs seem willing to join.

Elsewhere around the world

In Asia, selling Gigabit-speed

access is a strategic choice for

private sector operators..

In Latin America and the Middle

East, just providing the entire

population with broadband

access is already a challenge,

so Gigabit access is not really

on the table as yet. But a few

ISPs do offer ultra-fast plans,

aimed at a very specific

clientele.

USA

www.idate.org © IDATE DigiWorld 2017 – p. 54

2025 EU New Objectives: September 14th 2016

•1 Gbps for schools, universities, research centres, transport hubs, all providers of public services such as

hospitals and administrations, and enterprises relying on digital technologies,

•All European households, rural or urban, should have access to connectivity offering a download speed of at

least 100 Mbps, which can be upgraded to 1 Gbps,

•All urban areas as well as major roads and railways should have uninterrupted 5G coverage. As an interim

target, 5G should be commercially available in at least one major city in each EU Member State by 2020

54

www.idate.org © IDATE DigiWorld 2017 – p. 55

Status of 1 Gbps plans around the world

Where are 1 Gbps plans available?

Source: IDATE DigiWorld, The Gigabit Race

www.idate.org © IDATE DigiWorld 2017 – p. 56

Monetizing Gigabit & Latency: MyRepublic in Singapore, NZ… and Indonesia now!

•1 Gbps offer for around 29 EUR / month

•+ a dedicated offer with short latency for online

Gamers: + 10 Singapore Dollar (~ 6 EUR)

•This represents 25% of their subscribers

basis

•FTTH deployment in Singapore has been done

following a 3 layers Open Access model…

•…but MyRepublic is deploying is own OLT and

ONT GPON equipment now!

•… to control QoS!!

•MR also provides specific services such as

Teleport which enables end users to stream US

series that are usually “geo-restricted”

56

Source: MyRepublic

www.idate.org © IDATE DigiWorld 2017 – p. 57

China Telecom Sichuan: FTTH first then successful 4KTV !!!

• China Telecom Sichuan (CTS) covers a Territory 90 M inhabitants

• End 2015, CTS announced having rolled out FTTH infrastructure to all of the 21 province’s cities, and its main

villages and towns

• First Province in China to be 100% FTTH covered in 3 years only!

• 10 M FTTH subscribers and more than 9 M IPTV 4K subscribers !!

• Next step is 4K HDR …. Up to 25/30 Mbps necessary

Source: IDATE DigiWorld, April 2016, Chengdu

www.idate.org

5. Conclusion : Why NG PON 2 now ? … and G.Fast Drivers

FTTH Global Perspective: Lessons to be learned

www.idate.org © IDATE DigiWorld 2017 – p. 59

Why NGPON 2 now?

• Gigabit Race is now a reality worldwide and this will accelerate in the 18 months to come….how to face this with

today GPON? How to serve large MDUs?

• Short latency applications will come and not only for Online Gaming…. VR is here

• TV and Video booming : 4K HDR already here (Netflix) and 8K will start probably in 2018 (Japan)

• FTTH not only for Residential…need to differentiate traffic

- Mobile Broadband and 5G coming: recent 1.3 billion USD agreement between Verizon and Corning / Prysmian

is a sign!

- Businesses: Cloud access and Ethernet Service with dedicated lambda

www.idate.org © IDATE DigiWorld 2017 – p. 60

Drivers for G.Fast

• FTTH main challenges find solutions with G.Fast

- To solve the cost of the last mile and especially homes installation for Fibre

- The MDU case in the USA

• BT : is not the only one to opt for G.Fast but the volume is there: 10 M Homes !

• Swisscom opened G.Fast commercial services one year ago

• NG Fast promises to deliver 10 Gbps over copper

• …. And Fibre will be close : GPON backhaul for G.Fast

• G.Fast Field trials and deployments are now well underway all across the Globe.

• Ecosystem is being build with all main active vendors proposing G.Fast but also innovative chipset suppliers

(Sckipio).

www.idate.org © IDATE DigiWorld 2017 – p. 61

IDATE Research: Stream FTTx & Gigabit

61

MERCI !!! Roland MONTAGNE

Principle Analyst

Director DigiWorld Institute UK

mob: +33 680 850 480