Embed Size (px)

Citation preview

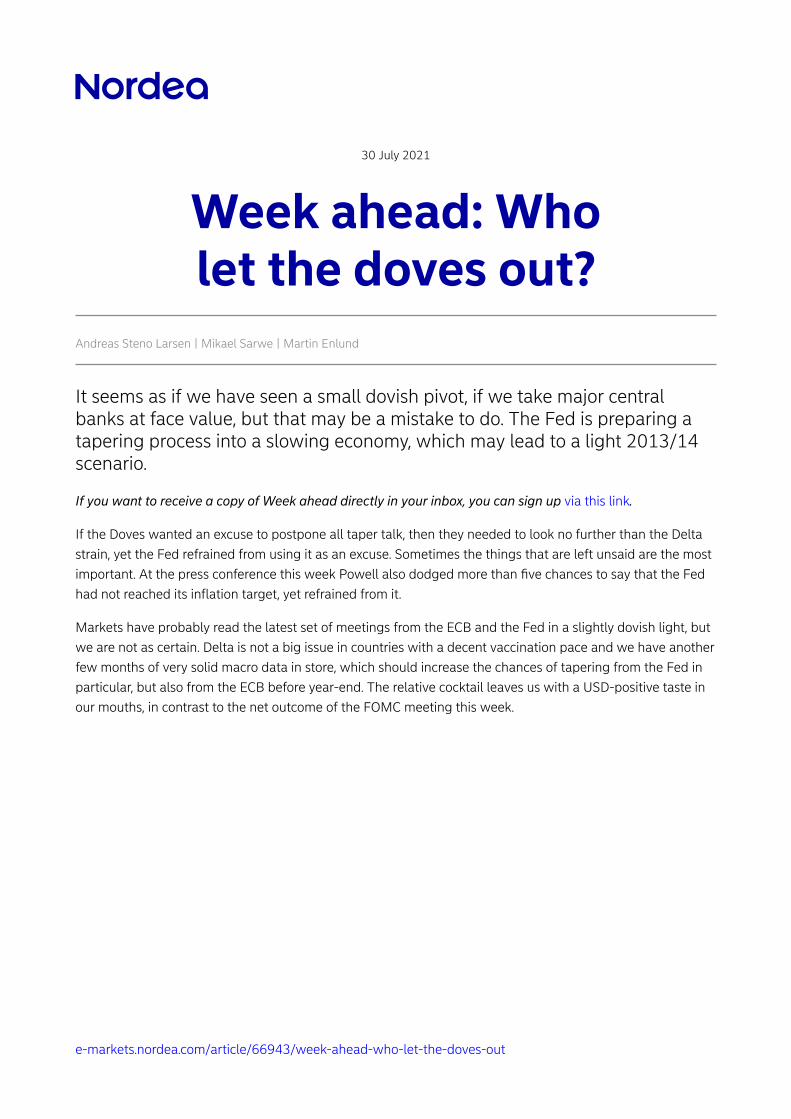

30 July 2021

Week ahead: Wholet the doves out?

Andreas Steno Larsen | Mikael Sarwe | Martin Enlund

It seems as if we have seen a small dovish pivot, if we take major centralbanks at face value, but that may be a mistake to do. The Fed is preparing atapering process into a slowing economy, which may lead to a light 2013/14scenario.

If you want to receive a copy of Week ahead directly in your inbox, you can sign up via this link.

If the Doves wanted an excuse to postpone all taper talk, then they needed to look no further than the Deltastrain, yet the Fed refrained from using it as an excuse. Sometimes the things that are left unsaid are the mostimportant. At the press conference this week Powell also dodged more than five chances to say that the Fedhad not reached its inflation target, yet refrained from it.

Markets have probably read the latest set of meetings from the ECB and the Fed in a slightly dovish light, butwe are not as certain. Delta is not a big issue in countries with a decent vaccination pace and we have anotherfew months of very solid macro data in store, which should increase the chances of tapering from the Fed inparticular, but also from the ECB before year-end. The relative cocktail leaves us with a USD-positive taste inour mouths, in contrast to the net outcome of the FOMC meeting this week.

e-markets.nordea.com/article/66943/week-ahead-who-let-the-doves-out

Chart 1. The relationship between case counts and hospitalisations has CLEARLYweakened despite the Delta strain

When the Fed opened the door for taper talk at the June meeting, the immediate response was to flatten5s30s in the USD curve markedly, which is in line with the pattern we have seen in earlier balance sheettightening cycles. When the foot is taken o the QE pedal, it leads to a weakening impulse and lowerexpectations, which is why long-term bond yields tend to fade, while for instance 5-year bond yields tend togain.

The flattener trend has recently lost a bit of momentum as the taper story has faded a bit, but we remainfirm that a taper scenario is in play as early as at the September meeting since it is evident that a larger andlarger part of the FOMC is growing concerned over the (supply-side) inflation outlook. Powell admitted that itwasn’t the “kind of inflation the Fed was looking for” but that they had to consider the rising inflation from arisk management perspective. This is a pretty material change of wording from Powell, even if he sticks to histransitory narrative (Fed review: One out of two targets met? Tapering moving closer).

It is furthermore noteworthy that the Fed seems to be preparing for a tapering scenario via increasing theweighted average maturity of the bond purchases and via incentivizing leveraged funds to buy Treasurieswith the new standing repo facility that was announced this week. Tapering is coming.

e-markets.nordea.com/article/66943/week-ahead-who-let-the-doves-out

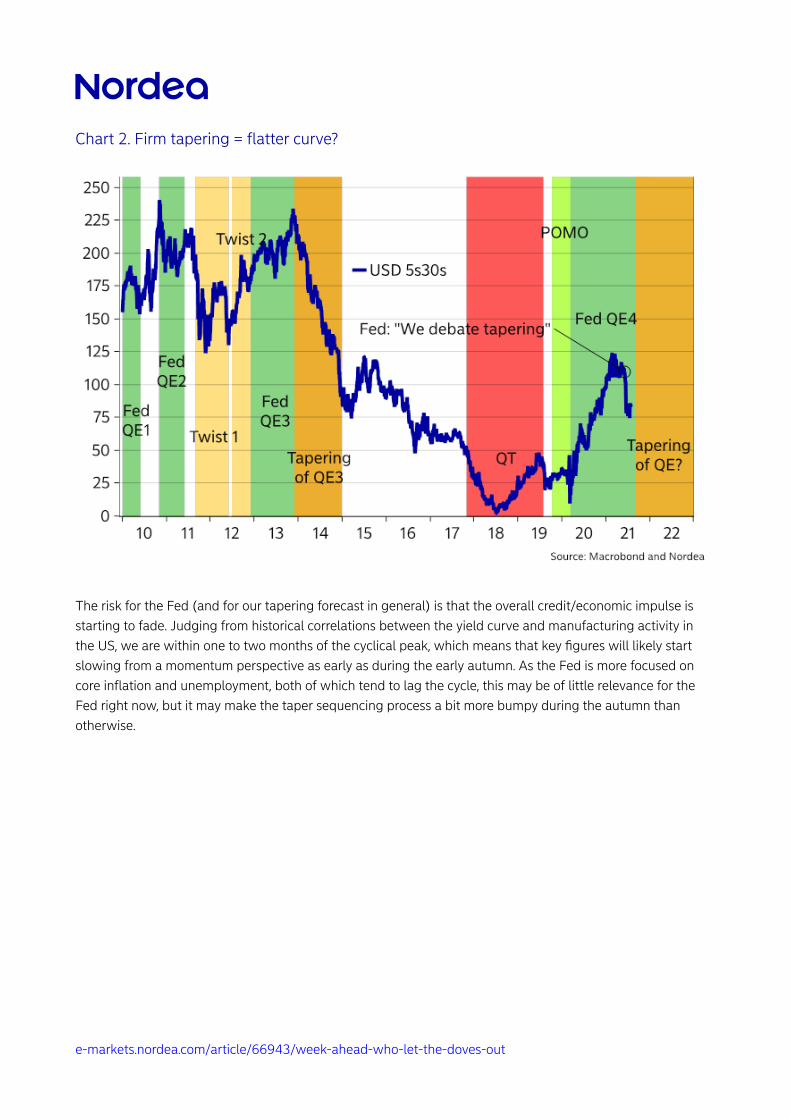

Chart 2. Firm tapering = flatter curve?

The risk for the Fed (and for our tapering forecast in general) is that the overall credit/economic impulse isstarting to fade. Judging from historical correlations between the yield curve and manufacturing activity inthe US, we are within one to two months of the cyclical peak, which means that key figures will likely startslowing from a momentum perspective as early as during the early autumn. As the Fed is more focused oncore inflation and unemployment, both of which tend to lag the cycle, this may be of little relevance for theFed right now, but it may make the taper sequencing process a bit more bumpy during the autumn thanotherwise.

e-markets.nordea.com/article/66943/week-ahead-who-let-the-doves-out

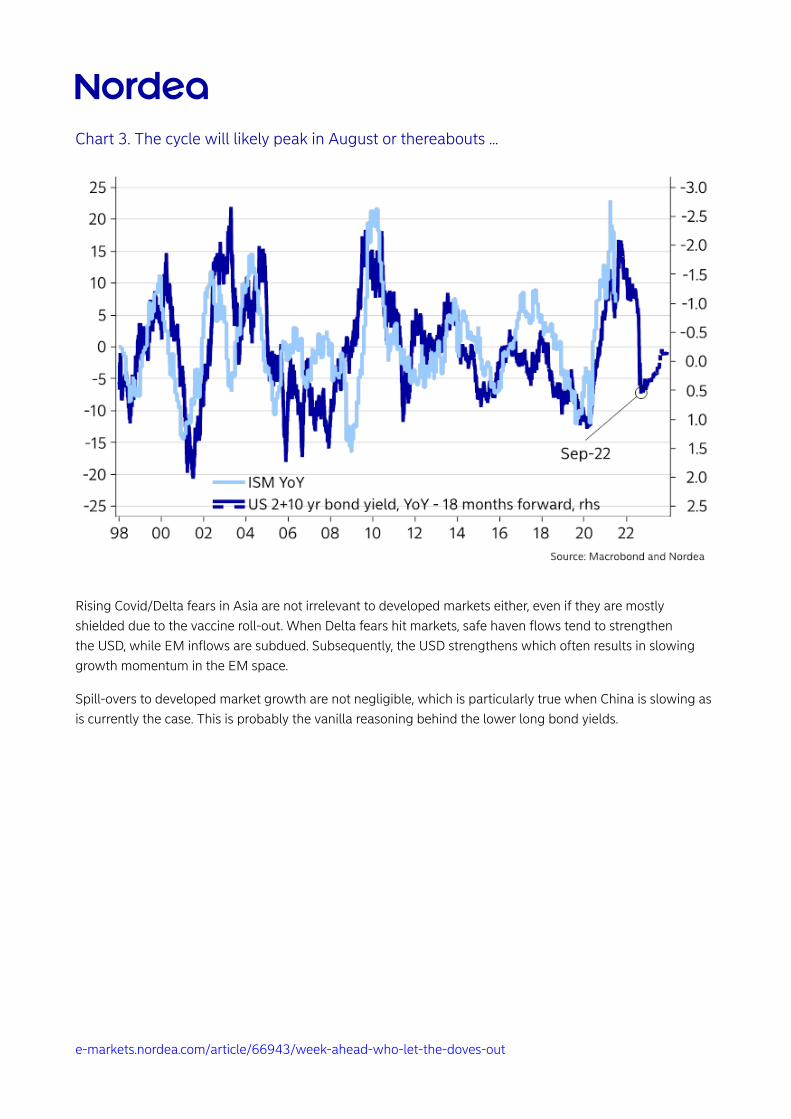

Chart 3. The cycle will likely peak in August or thereabouts …

Rising Covid/Delta fears in Asia are not irrelevant to developed markets either, even if they are mostlyshielded due to the vaccine roll-out. When Delta fears hit markets, safe haven flows tend to strengthenthe USD, while EM inflows are subdued. Subsequently, the USD strengthens which often results in slowinggrowth momentum in the EM space.

Spill-overs to developed market growth are not negligible, which is particularly true when China is slowing asis currently the case. This is probably the vanilla reasoning behind the lower long bond yields.

e-markets.nordea.com/article/66943/week-ahead-who-let-the-doves-out

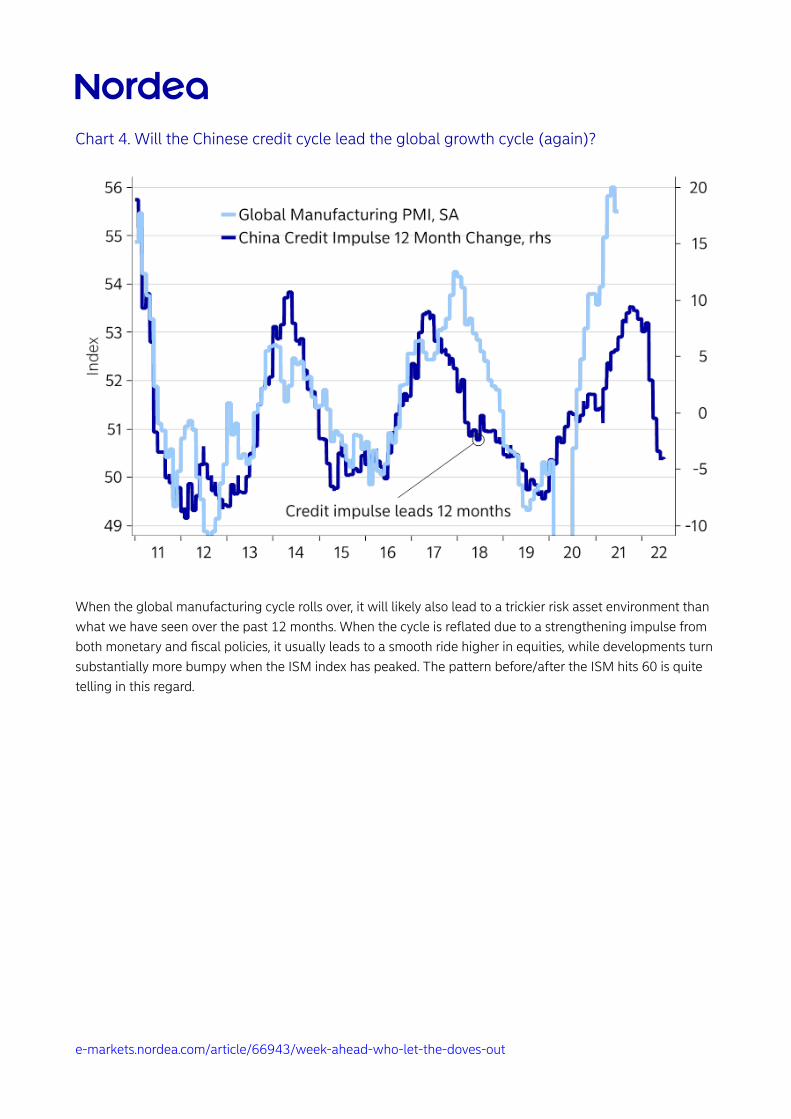

Chart 4. Will the Chinese credit cycle lead the global growth cycle (again)?

When the global manufacturing cycle rolls over, it will likely also lead to a trickier risk asset environment thanwhat we have seen over the past 12 months. When the cycle is reflated due to a strengthening impulse fromboth monetary and fiscal policies, it usually leads to a smooth ride higher in equities, while developments turnsubstantially more bumpy when the ISM index has peaked. The pattern before/after the ISM hits 60 is quitetelling in this regard.

e-markets.nordea.com/article/66943/week-ahead-who-let-the-doves-out

Chart 5. A bumpier ride for risk assets ahead if usual ISM patterns hold true

On the contrary, we have recently seen a complete landslide in 5y5y real rates, which usually sugar-coatsequity valuations. We hence still lack a smoking gun before the risk asset environment turns sour. An actualtapering decision, and not just taper talk, could prove to be such a trigger, but in any case we find that therisk/reward in paying real rates has improved markedly now that the ECB strategy review is “out of the way”.

e-markets.nordea.com/article/66943/week-ahead-who-let-the-doves-out

Chart 6. 5y5y real rates have seen a new low in EUR, and also a landslide in USD, sugar-coating equity valuations

It seems as if the flattening USD curve over the summer has been generally good news for Scandi bonds aswell, not least the suering Danish callables, which have posted a comeback over the past weeks. The mostinteresting macro story remains Norway, with a rate hike likely ahead in September, even if the market hasstarted to doubt it a little bit. After the recent dovish pivot from the ECB, we have also seen a slight dovishrepricing of the Norges Bank outlook, which is unjustified in our view.

The market is pricing 25-30bp below the June rate path from Norges Bank during 2022-23, and around 6bpbelow the path for the September meeting. As the structural liquidity outlook is tightening in Norway as well,it may be worthwhile betting on a hawkish development in NIBOR fixings over the coming months still.

e-markets.nordea.com/article/66943/week-ahead-who-let-the-doves-out

Chart 7. Markets have started to doubt the Norges Bank rate path a bit more

What is most important in the week ahead?

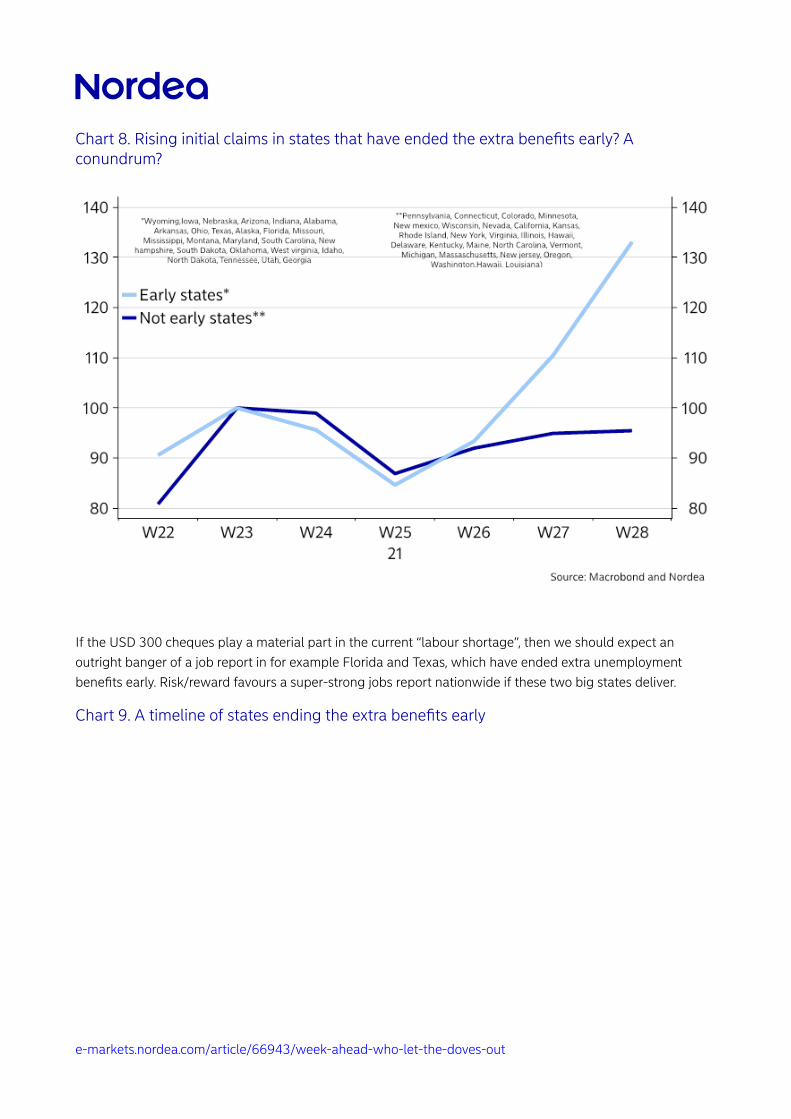

It is time for an early test of the repercussions of ending the extraordinary unemployment benefits in certainstates in the US (the famous USD 300 cheques). So far, interestingly enough, it seems as if the rise in initialclaims mainly stems from states that have ended the cheques early. Maybe those exact states have seen arelative increase in the labour force as restrictions are lifted?

e-markets.nordea.com/article/66943/week-ahead-who-let-the-doves-out

Chart 8. Rising initial claims in states that have ended the extra benefits early? Aconundrum?

If the USD 300 cheques play a material part in the current “labour shortage”, then we should expect anoutright banger of a job report in for example Florida and Texas, which have ended extra unemploymentbenefits early. Risk/reward favours a super-strong jobs report nationwide if these two big states deliver.

Chart 9. A timeline of states ending the extra benefits early

e-markets.nordea.com/article/66943/week-ahead-who-let-the-doves-out

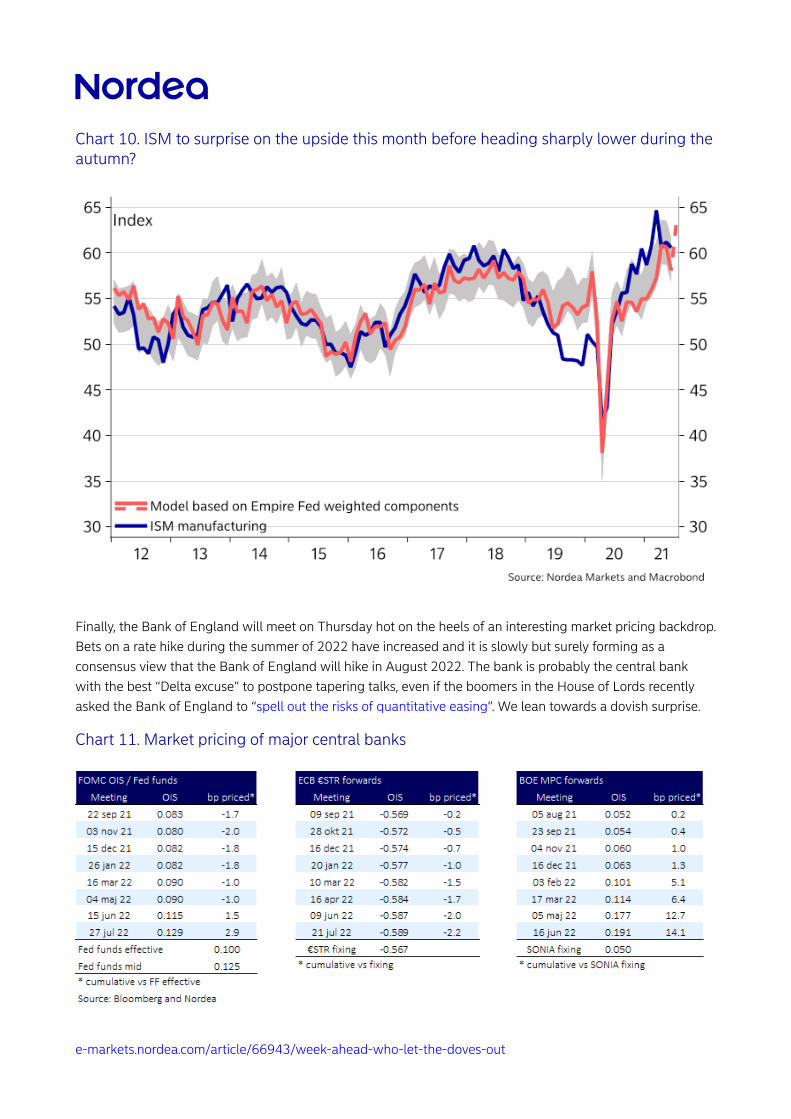

Risk/reward also favours a resurge in the ISM manufacturing index as some of the important regional surveyshave generally surprised on the upside. This also goes hand in hand with the cycle indicator that we showedearlier in this analysis, pointing to a cycle high in the ISM around August. In general, we find that macro datawill remain decently supportive of a more hawkish Fed in the month ahead.

e-markets.nordea.com/article/66943/week-ahead-who-let-the-doves-out

Chart 10. ISM to surprise on the upside this month before heading sharply lower during theautumn?

Finally, the Bank of England will meet on Thursday hot on the heels of an interesting market pricing backdrop.Bets on a rate hike during the summer of 2022 have increased and it is slowly but surely forming as aconsensus view that the Bank of England will hike in August 2022. The bank is probably the central bankwith the best “Delta excuse” to postpone tapering talks, even if the boomers in the House of Lords recentlyasked the Bank of England to “spell out the risks of quantitative easing”. We lean towards a dovish surprise.

Chart 11. Market pricing of major central banks

e-markets.nordea.com/article/66943/week-ahead-who-let-the-doves-out

Andreas Steno LarsenChief Global FX/FI [email protected]+45 55 46 72 29

Mikael SarweDirector, Head of Strategy [email protected]+46 8 614 99 09

Martin EnlundGlobal Chief FX [email protected]

e-markets.nordea.com/article/66943/week-ahead-who-let-the-doves-out