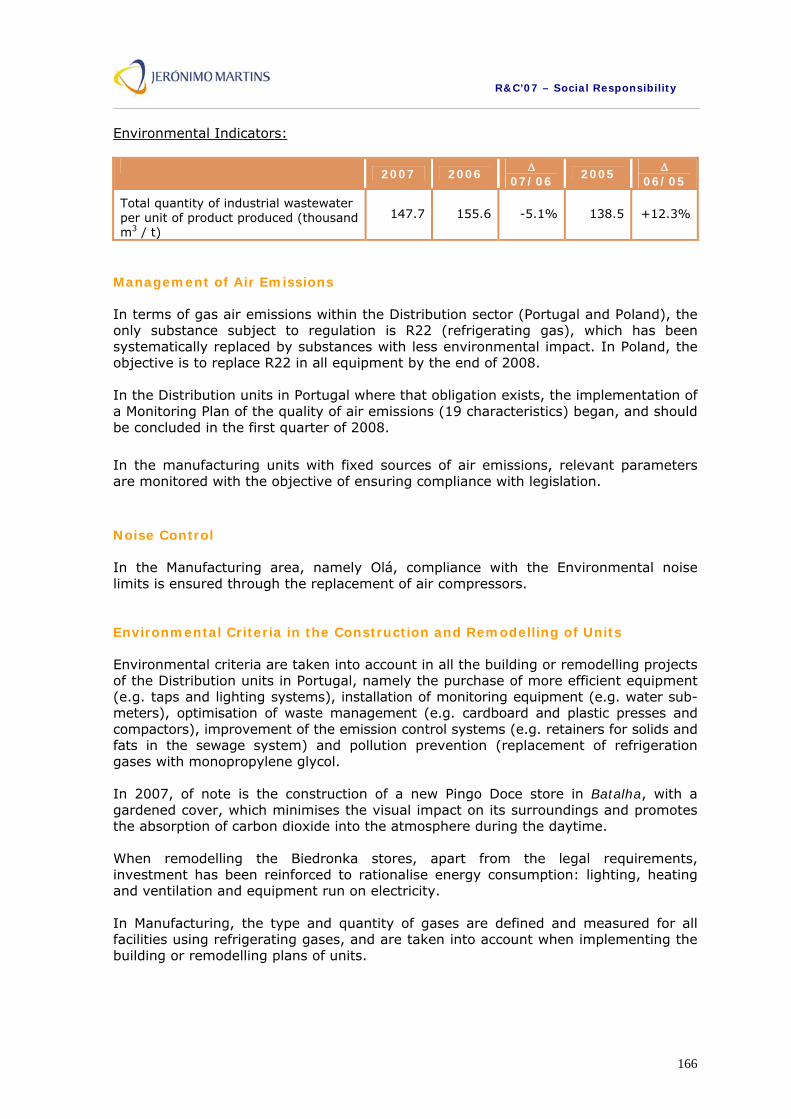

Embed Size (px)

Citation preview

Index

3 Message from the Chairman

I. Introduction

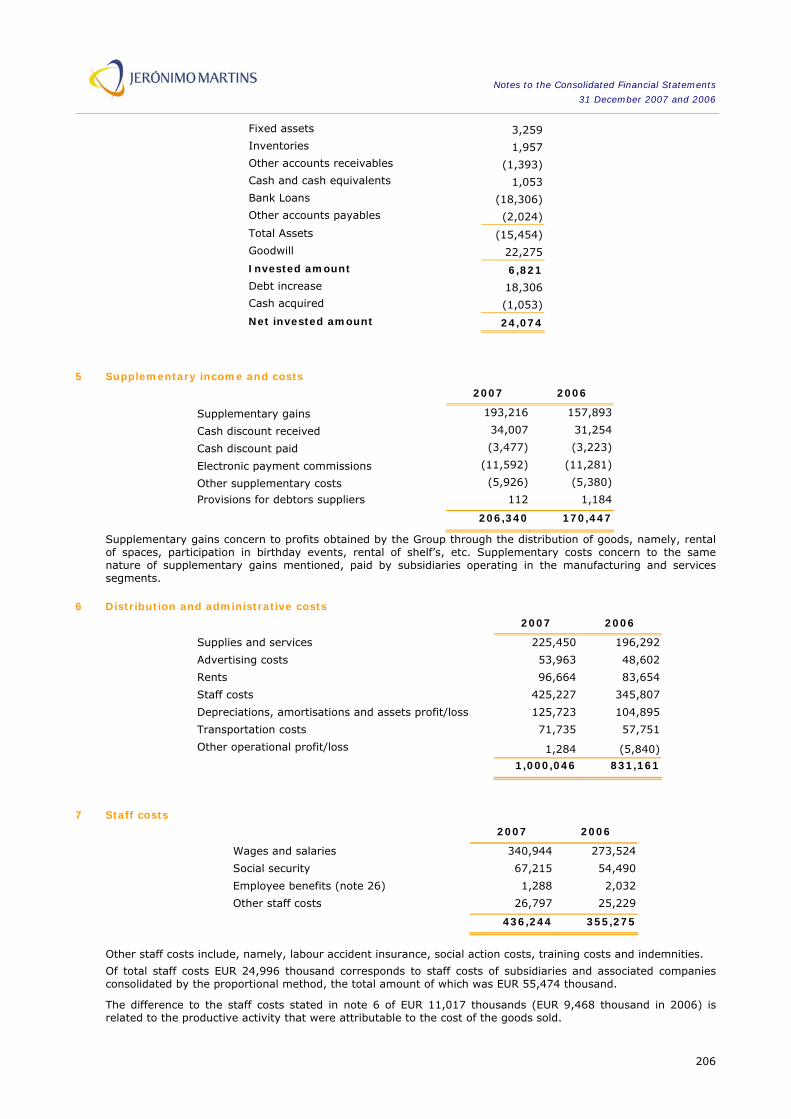

6 1. The Group’s Strategic Profile

13 2. Operating and Financial Highlights

17 3. Corporate Bodies

19 4. Business and Ownership Structure

21 5. Management Structure

23 6. Financial Glossary

25 7. Contacts

II. Corporate Governance

27 Introduction

28 1. Statement of Compliance

29 2. Disclosure of Information

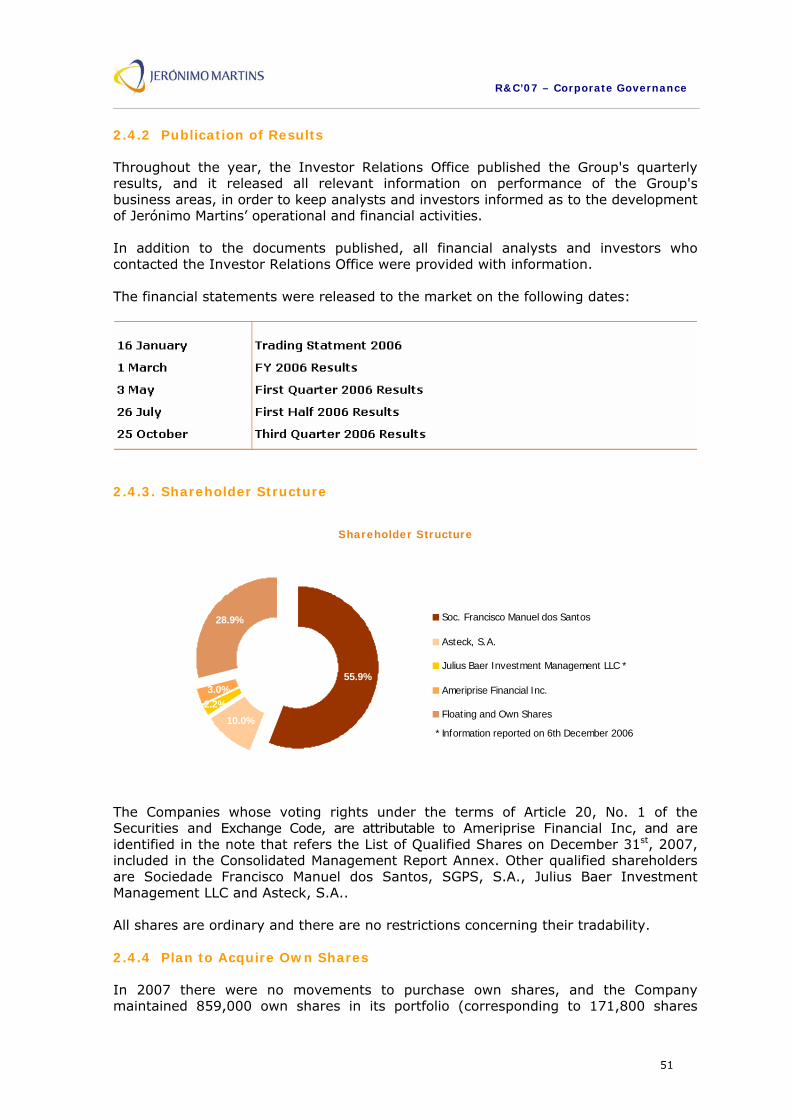

57 3. Exercise of Shareholder Voting and Representation Rights

59 4. Company Rules

60 5. Board of Directors

III. Consolidated Management Report

69 1. Relevant facts of the Year

71 2. International Macroeconomic Environment

73 3. International Sector Environment

76 4. Portugal

78 5. Poland

80 6. Overview of the Group’s Consolidated Activity

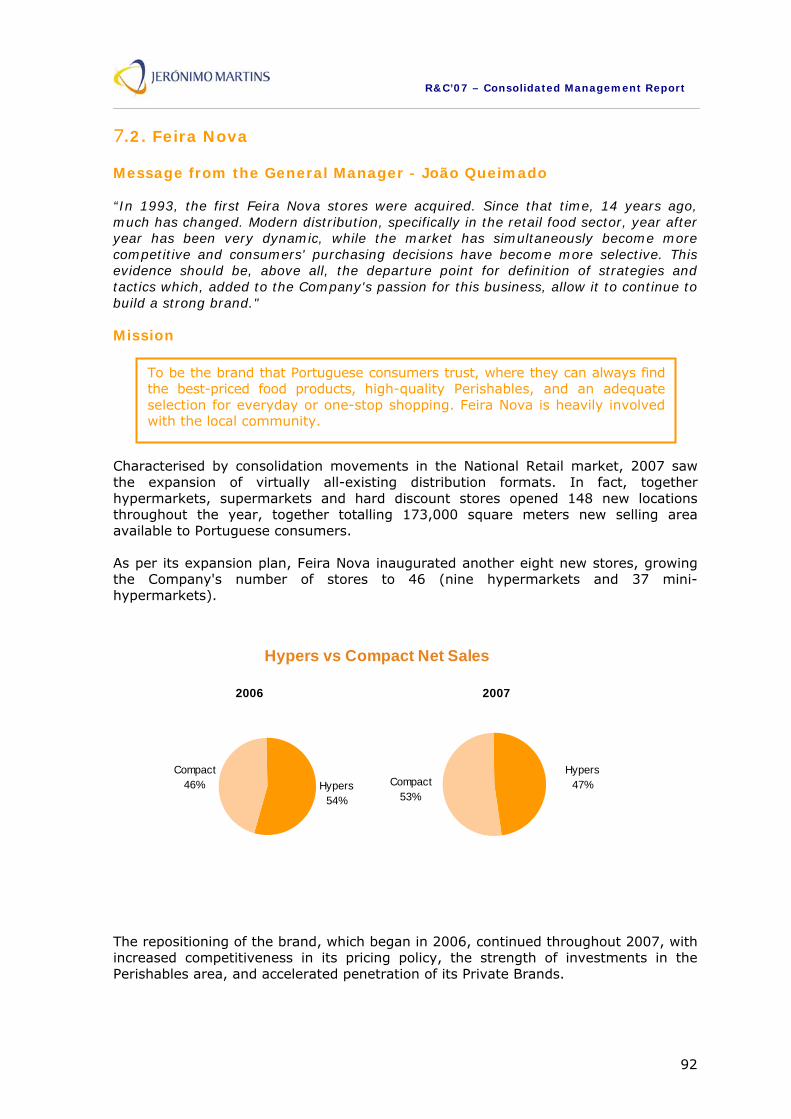

90 7. Food Distribution - Portugal

105 8. Food Distribution - Poland

108 9. Manufacturing

112 10. Jerónimo Martins Distribution

115 11. Simplification of Internal Management Processes

117 12. Group Investment Programme

119 13. Outlook for 2008

131 14. Events after Balance Sheet Date 131 15. Results Appropriation Proposal

132 16. Consolidated Management Report

IV. Social Responsibility

135 1. Relevant Facts of the Year

138 2. Jerónimo Martins and Sustainable Development

140 3. Corporate Ethics

142 4. Human Resources

151 5. Quality and Food Safety

159 6. Environmental Management

172 7. Patronage

179 8. Frequently Asked Questions

V. Consolidated Financial Statements

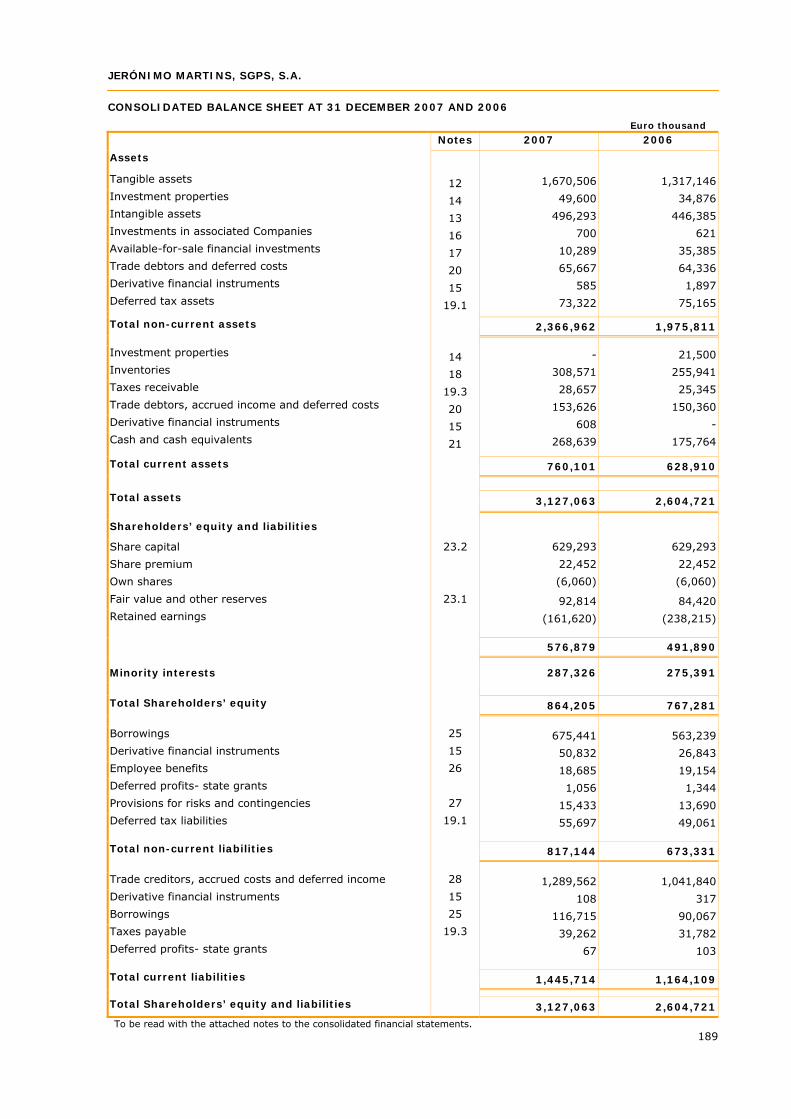

188 1. Consolidated Financial Statements

232 2. Statement of Conformity

233 3. Auditor’s Report 235 4. Report and Opinion of the Audit Committee VI. Individual Financial Statements

238 1. Management Report

246 2. Financial Statements

281 3. Auditor’s Report

283 4. Report and Opinion of the Audit Committee

285 Excerpt of the Annual General Meeting Draft Minutes

R&C’07 – Chairman’s Message

3

MESSAGE FROM THE CHAIRMAN Dear Shareholders, For Jerónimo Martins, the year 2007 was marked by a notable growth in its operations, particularly in the Distribution area, which was achieved thanks to adjusting the defined strategies, the way they were strictly implemented and the balanced management of the available resources. Consolidated sales reached 5,350 million euros, which corresponds to a year on-year growth of 21.4%, and the net profit for Jerónimo Martins amounted to 131 million euros, 13.0% more than in 2006. Largely responsible for this growth were the Pingo Doce chain, which registered a 17.5% increase in sales, passing the 1,000 million euros mark and 8.7% like-for-like growth against the previous year, and the Biedronka chain, with an excellent performance of 35.0% increase in sales and 21.1% in the like-for-like basis. With these levels of growth, both Companies strengthened their market shares. Within this consolidating leadership strategy, I am enthusiastic to write about the opening of the 1,000th Biedronka store in Warsaw, Poland, in September 2007, which is a symbol of the Group's strong investment in the Polish market. I should also like to highlight Jerónimo Martins’ continued investment in its offer of a high quality Private Brand, which is an extremely important support to its Company differentiation strategy and which grew 41.0% in retail operations in Portugal and 31.8% in Biedronka. As proof of our compliance with the highest and strictest Private Brand quality requirements, I have the pleasure to report that the Pingo Doce and Recheio Companies were the first, worldwide, to certify their private brand products development as well as the follow-up process of both products and suppliers after the launching of the products, in accordance with the NP EN ISO 9001:2000 referential system. I also would like to highlight the retail market concentrations in Portugal and Poland, in which the Group played an active part by acquiring, at the end of the year, to the Tengelmann Group the Plus chain operations in Portugal and Poland, involving 75 and 210 stores respectively and an overall turnover of around 500 million euros. Although the performance in 2007 is an important milestone in the Group’s history, it is the responsibility emerging, also from the 2,700 and the 3,700 new employees in Portugal and Poland, respectively (+19% comparing with the same period last year in the retail area) this which motivates our ambition for the new cycle that is going to commence. It is a cycle of strong, balanced and sustainable growth in all business areas and of the permanent creation of value. For Jerónimo Martins, the dawn of 2008 is already marked by new challenges. In the short-term and as soon as the acquisition of the Plus operations has been approved, a refurbishing process will take place in the respective stores and the new employees will be integrated into the Group’s culture. The basic principle of this integration will always be not only the transferral of Jerónimo Martins’ knowledge but also to receive the value and integration of best practice and knowledge from the experience of the integrated chain’s employees. Once the necessary integrations have been consolidated, the Group will return to organic growth, not forgetting to study new opportunities for growth, either by expansion into new geographic areas or new business areas. What is certain is that

R&C’07 – Chairman’s Message

4

the Group will be paying attention to any new opportunities that might arise in the food-manufacturing sector in Portugal and in Poland, while always taking into consideration the solidity of its balance sheet. I usually say that we are a “People’s Business, made by People” and it is from this perspective that I value a policy based on training. Because I believe that we are currently living in the Talent Age, the personal and professional development of the Jerónimo Martins Employees is more and more evident as a competitive advantage in this global market. In the light of this, both Portugal and Poland provide their Middle and Senior Managers with specific training at renowned national and international Academic institutions with which the Group has established protocols and long-term relationships, such as Universidade Católica Portuguesa, Universidade Nova, INSEAD, Harvard University, Kellog’s University, among others. Without ever neglecting the business and taking into consideration the importance the Perishables area holds for the Group’s strategy, I would like also to highlight the creation of the Jerónimo Martins Perishables School, which is dedicated to rigorous and professional training to develop the Employees’ technical skills in the specialised areas of butcher’s, fishery, bakery and pastry, fruit and vegetables. I am also very pleased to confirm that in 2007 the Jerónimo Martins Training School joined the “New Opportunities” Programme, in partnership with the “Employment and Professional Training Institute” and the “Institute for Quality in Training”, with a project called “Learn and Develop”. This project, which aims to give all the employees with less than third cycle or high school graduation the opportunity of receiving, in working hours, the respective qualification, already had more than 3,000 people enrolled at the end of December 2007. On the other hand, being aware of the responsibility we have towards the community of which we are a part, and the importance of integrating people with special needs - but who are able to actively participate in society and in the companies - the partnership with ACAPO (Portuguese Association of the Blind and Poorly-sighted) was reinforced, with a view to another 39 employees being integrated into Jerónimo Martins. Also with people with reduced sight in mind, a new functionality was introduced on the Group’s institutional website - www.jeronimomartins.com -, which allows people to hear the written content, in Portuguese and English, a real first in terms of the top 20 listed companies in Portugal. On closing 2007, with our eyes set on the challenges and opportunities that we come across, I would like to leave a very well-earned word of thanks to all the Employees, for their invaluable professionalism and dedication. Once again we wanted to pay homage to our Employees, making them the leading faces in this Report, as we are sure of their decisive contribution towards the Group’s outstanding performance. Finally, I also would like to express my gratitude to each of our Shareholders and I am sure that they will continue to support our project, enabling us to take Jerónimo Martins ever further.

I. Introduction

6 1. The Group’s Strategic Profile

13 2. Operating and Financial Highlights 17 3. Corporate Bodies

19 4. Businesses and Ownership Structure

19 4.1. Business Structure

20 4.2. Ownership Structure

21 5. Management Structure

23 6. Financial Glossary

25 7. Contacts

R&C’07 – Introduction

6

1. THE GROUP’S STRATEGIC PROFILE Asset Portfolio Jerónimo Martins is a Portuguese Group of relevant size, whose turnover in 2007 was 5,350 thousand million euros, with 41,300 employees, and whose international business represents around 44.7% of sales and 46.8% of its employees. The Group holds a balanced business portfolio which combines the strength of the market position of its retail and wholesale operations’ in Portugal, with the growth potential of the Biedronka operation in the Polish market, and the maturity and capability for generating cash flow of its Manufacturing partnership with Unilever in Portugal. In the Food Distribution Area in Portugal, at the end of 2007, in joint terms, the Group held the leading market position, with the brands Pingo Doce (210 supermarkets in Mainland Portugal and 13 supermarkets in Madeira), Feira Nova (9 hypermarkets and 37 mini-hypermarkets), and Recheio (31 Cash & Carry stores and 2 Food Service platforms in Mainland Portugal and 1 store together with 1 Food Service platform in Madeira), and it was the market leader in the supermarket and in the Cash & Carry segments. In Poland, Biedronka, a chain of stores with a variety of food products, which combines the quality with an everyday-low-price policy, is a strong market leader in its format and has a substantial lead over competitors in terms of number of stores and brand awareness. At the end of 2007 the chain had 1,045 stores in Poland, with more than 494 million client tickets and 2,392 thousand million euros turnover for the year under review. Also in Poland, 4 pilot stores were opened in 2007 under the “Apteka Na Zdrowie” banner, joining the first store that opened at the end of 2006 after the partnership agreement signed in February 2006 with the National Association of Pharmacies in Portugal, in order to study the viability of developing a line of pharmacy retail businesses. Jerónimo Martins is also the biggest Portuguese manufacturing Group in fast moving consumer goods, through its partnership with Unilever in the areas of Food, Personal Care and Home Care, and Out of Home, which was reinforced in 2007 with the merger of FimaVG, Bestfoods, LeverElida and IgloOlá into a single organisation – Unilever Jerónimo Martins. The new Company maintains its position as market leader for Olive Oil, Margarines, Iced Tea, Ice creams and Washing Detergents, among others. The Group’s portfolio also includes a business area providing Marketing Services, Representations and Restaurants, including:

Jerónimo Martins Distribuição de Produtos de Consumo, which is the Portuguese representative for several international brands, some of which are market leaders in the fast-moving consumer food and food service markets, in this case through Caterplus, in the selective cosmetics and in the fast-moving cosmetics, through its joint venture with the Puig Group;

Hussel, a Specialised Retail chain with 21 stores, selling chocolates and

confectionary;

Jerónimo Martins Restauração e Serviços, dedicated to the development of projects in the restaurant sector, which includes the Jeronymo chain of coffee shops and the Ben & Jerry’s and Olá ice-cream stores and the Subway stores.

R&C’07 – Introduction

7

Main Historic Milestones 1792 Jerónimo Martins opens a premium grocery store in Lisbon in the Chiado area. 1944 Opening of the Fima plant (producing mainly margarine). 1949 – 1970 A joint venture was established with Unilever in Portugal to develop manufacturing and market know-how in the fast moving consumer goods markets, starting with Fima and later growing to include Lever (Soap and Detergents), Olá (Ice-Creams) and Iglo (Frozen Food). 1980 – 1995 Development of the food distribution business area through the Pingo Doce supermarkets, Feira Nova hypermarkets, the expansion of Pingo Doce to Madeira with Lidosol, the Recheio Cash & Carry, the Marketing and Representation Services, with JMD and Specialised Retail, with Hussel. Expansion through organic growth and acquisitions. Development of strategic partnerships, first with Delhaize at Pingo Doce, and then with Ahold at Pingo Doce and Feira Nova, with Booker at Recheio and with Douglas at Hussel. 1989 Jerónimo Martins is listed on the Stock Market, beginning a decade of consistent and significant increase in market capitalisation. 1995 – 2000 International expansion to Poland (Eurocash Cash & Carry, Biedronka stores and Jumbo hypermarkets), Brazil (Sé supermarkets) and England (Lillywhites chain of sports goods). Diversification of the business portfolio: In-store banking, in joint venture with BCP (Expresso Atlantico) and participation in the Telecommunications sector (Oniway). The Group moves into the Water and Tourism business with the acquisition of VMPS. 2001 – 2005 Portfolio of assets’ restructuring, with the sale of non-core businesses, improved balance sheet and minimization of exposure to financial risk. Operational restructuring, with a view to focusing the operational units on the commercial dynamics of their respective segments, maximising the scale, exploring the synergies, simplifying processes and reducing costs; creation of multi-disciplinary teams, higher organizational flexibility and launch of the Jerónimo Martins Training School. 2006–2007 New Stage of the growth strategic plan, by returning to expansion in Portugal and maintaining expansion levels in Poland; strong investment in technological update, store refurbishing for the various chains and training programmes for Management and Non-Management staff; study of new business opportunities.

R&C’07 – Introduction

8

Continuing a Pioneering Culture The Jerónimo Martins Group, pioneer in Portuguese business life in several fields, is renowned, among other reasons, for being the foremost Food Distribution company in Portugal for implementing new management practices such as:

Adopting the International Accounting Standards/International Financial Reporting Standards (IAS/IFRS) in 2000;

Starting up a Food Service platform in Oporto, in 2002;

Implementing a business-to-business (B2B) platform in its relations with

suppliers in 2004;

Obtaining from APCER (Portuguese Certifying Association) at the end of 2005 the HACCP - Hazard Analysis Critical Control Point Certification (DS 3027E: 2002) and the Environmental Management System Certification (NP EN ISO 14001: 2004), placing the Retail warehouses as the first in Portugal in the Food Distribution sector to achieve this double recognition;

Having 19 Recheio stores and two Food Service Platforms recognised with Food

Safety Certification at the end of 2006 – certification of the HACCP system, in accordance with the Codex Alimentarius CAC/RCP-1-1969, Rev.4 (2003) – becoming the first wholesale Distribution chain in Portugal to obtain a multi-site certificate in HACCP;

Obtaining, in 2007, the certification of private label activity in Pingo Doce and

Recheio according to NP EN ISO 9001:2000 guidelines – certification of internal and supplier’s processes in the development of private label products and in the control after launch - becoming the first operators worldwide to obtain this type of certification.

Jerónimo Martins also registers several innovative market initiatives. The private label range of its food retail chains in Portugal has been consolidating the image of quality and innovation through initiatives such as:

• Developing brands by major area of product and for ranges of product common to both retail banners, providing the opportunity to enlarge the assortment, to optimise the scale and to reinforce the image of specialist;

• Launching a wide range of fresh products under private label, with specific quality control requirements from the source to ensure food safety and quality standards;

• Launching, in 2006, a range of products under Pingo Doce label, alternative to the standard dairy milk products, for clients that have intolerance to milk protein – becoming the first retail company in Portugal to do so;

• Launching, in 2007, a certified organic fresh range of products under Pingo Doce, becoming the first retail company in Portugal to do so.

In 2005, the Group took another truly innovative step in the Portuguese Distribution sector by establishing the Jerónimo Martins Customer Ombudsman; In 2006 Biedronka established an unprecedented partnership with Danone, Lubella and the Polish Institute of the Mother and Child, to fight the problem of poor nutrition amongst children and young people and so Milk Start, a product which was developed

R&C’07 – Introduction

9

based on a strict nutritional profile and under the supervision of an independent institute, was launched. Finally, in July 2007, Jerónimo Martins launched the “Learn and Develop” project, as part of the national “New Opportunities” programme developed by the Ministry of Education and it was the first Company in its sector to celebrate a co-operation protocol aiming to train and certify employees, which in this case totalled 11,500. Also in 2007, a new functionality was introduced to the Group’s institutional website, enabling access to the blind, which is an unprecedented initiative among the Companies present in PSI-20. Mission Jerónimo Martins is a Group with international projection operating in food distribution and manufacturing, which aims to satisfy the legitimate interests of its Shareholders, while contributing to the economic growth and to the sustainable development of the regions where it operates. In the fulfilment of its mission, the Group aims to:

Promote maximum operational efficiency across all business areas, so as to optimise the results generated through its financial, material and human resources;

Ensure maximum customer satisfaction, by improving their quality of life

through a firm commitment in terms of innovation and in terms of offering the best possible value for money for the products and services it provides;

Direct the entire Organization to work to the highest possible standards of

conduct and of Social Responsibility, building relationships of trust with all stakeholders;

Conduct business through dynamic and flexible Organisations, staffed with

people who can bring together the benefits of their experience and know-how with an acceptance of the permanent need for change, through continual investment in training and in the most up-to-date management practice, thereby guaranteeing that the whole Organization is focused on the strategic challenges and on the activities which are real value drivers.

A Benchmark Identity Being a longstanding benchmark in its business sector and in the market in general, Jerónimo Martins has a history of 215 years, made up of hugely diverse events, experiences and learning, which have conferred to the Group its solidity and capacity for renewal, mirrored in the strength and vitality for which it is renowned. The new Jerónimo Martins' corporate identity, implemented in 2004, demonstrates and symbolizes the profound changes that have taken place within the Group. This new visual identity embodies the new reality of Jerónimo Martins and the three values that are core to its corporate culture and attitude in the market: Rigour in Management, which ensures...

Adequate analysis of macro-economic, sector and market trends; Definition of strategic priorities;

R&C’07 – Introduction

10

Establishment and conveyance of clear, demanding objectives; Adequate control and correct critical evaluation of results.

Permanent Innovation, which stimulates...

A pioneering spirit in management processes and practices; Dynamism and market leadership.

Transparency in its Policies, which promotes...

The safeguard of the Shareholders’ interests as a priority; Ethical conduct of the Organisation in relation to all its stakeholders; Objective assessment of employees with regard to their performance and

professional development; Social Responsibility as a strategic option; Investment in strategic partnerships in those markets and regions in which it

operates. Today, Jerónimo Martins is a solid, cohesive Group, with a clear vision. It is an Organization geared towards professional excellence, which is prepared to add another chapter to its already long history, contributing to a stable and lasting future. A Strategy of Sustainable Development The Jerónimo Martins Group is a player in a sector, which is highly sensitive to the macro-economic environment globally, and in the countries in particular, and which is very diversified and dynamic, with regard to both supply and demand. It is known that macro-economic environments generate risks and opportunities and are ever more cross-connected due to globalisation. The macro-economic scenarios outlined by the experts offer significant levels of uncertainty and volatility. Financial markets demand generally higher risk premiums, as well as greater transparency and selectivity and Companies must learn how to deal with this new reality. The food world is made of progressively quicker market development cycles and has ever more demanding consumers who prefer trustworthy brands and competitive prices. The consumers have proven to be very rational in their food spending, as they have access to a great deal of information and they can choose between various alternatives. Price sensitivity, concern for quality, food safety and health as well as the need for convenient solutions are global trends, although each market still demonstrates its own degree of consumer development. Consumers are also characterized by major social and demographic trends such as ageing, racial and cultural diversity, concentration of population in “mega” urban towns, lack of time, smaller households, among other. With regard to supply, the players in the food sector, for the most part, have recently gone through profound restructuring. The ones that envision the consolidation of their market positions in highly aggressive and competitive environments stay focused on continuous incremental competitiveness and continuous differentiation of their value propositions. Depending on the local, regional or even global position that each player seeks to attain, Mergers and Acquisitions and international expansion continue to be central topics in a growth strategy.

R&C’07 – Introduction

11

It should be also added that citizens are more and more aware of environmental and social problems. Media, experts, NGO’s and governments in general, have been focusing the public debate on issues related with sustainability. On the other side, the food retail players are showing signs of being aware of the relevant role they can carry out concerning the issues related with sustainability. As the last link in the interface with the final customer, they know that the goodwill of their environmental and social initiatives can leverage the value of their brands and banners and reinforce clients’ trust. Looking from another angle, they will also influence positively a long value chain of multiple players just with the options they take.

Being aware of all this, when developing its strategy, the Jerónimo Martins Group has an economic commitment based on healthy and profitable growth. Focusing its management activity on value creation in the short, medium and long-term, the Group assumes two main priorities. First of all, the Group envisions the continuous reinforcement of its market leadership positions with regard to current assets and investment priorities will be determined that way. Simultaneously, the Group envisions the preparation for the future growth through carefully studying and testing new business opportunities for expanding the current portfolio of assets within the scope of its mission. Therefore, Jerónimo Martins intends to continue to:

• hold solid financial resources, paying particular attention to its capital

structure, to the solidity of its balance-sheet and to risk provision, while ensuring a balanced portfolio and a careful evaluation of new investments.

• promote programmes that generate strong growth in cash flow and profit for

its asset base, including expansion and consolidation operations. • guarantee continued reinforcement of the different formats, promoting focused,

flexible, creative and dynamic organisations, capitalising on scale, synergies and shared knowledge and rewarding the value creation. Continuous investment in training Management and Non-Management employees is a key factor to ensure an organizational performance of excellence.

• implement appropriate risk analysis and management mechanisms, at all

critical levels of the value chain, to firmly sustain its current business and its plans for growth in the future.

• differentiate from others by being innovative and pioneering in responding

proactively to customers’ demands and to emerging consumer trends. The investment in strategic partnerships continues to play a determining role in the desired innovative and pioneering culture.

• continually and proactively adjust the strategic plan in articulation with annual

objectives that must be very demanding but also feasible, being this the key to ensure continuous value creation for the Jerónimo Martins’ Shareholders and stakeholders in general.

R&C’07 – Introduction

12

Jerónimo Martins’ economic commitment with its shareholders has always been, and will continue to be, marked by strict compliance with economic, environmental and social rules. However, it is also relevant to say that the Group has already proven during its long history of 215 years, the will to contribute beyond what is requested. Within the scope of its corporate values, Jerónimo Martins has been implementing, for many years, a series of policies, practices and initiatives that illustrate that will. This Annual Report has a specific chapter to provide very complete information organised by major areas of interest, namely, Corporate Ethics, Human Resources, Quality and Food Safety, Environmental Management and Patronage. The Group is also convinced that the policies and practices which direct its market conduct have to evolve proactively, following the evolution of the society in general and reflecting the degree of internal maturity on each of the matters. It is this consistent attitude over time that sustains and reinforces Jerónimo Martins’ identity for its shareholders, staff and stakeholders in general. On a different level, Jerónimo Martins will continue to integrate sustainability values into the market strategy of each of the Group’s businesses, believing that clients will value and trust, more and more, on brands and banners that better integrate the relevant economic, environmental and social values and that perform in accordance over time. All in all, the strategy of sustainable development of Jerónimo Martins aims to satisfy continuously the legitimate interests of its shareholders while contributing to the economic growth and to the sustainable development of the regions in which it operates, continuing being a corporate benchmark identity, holding trustful brands and banners.

R&C’07 – Introduction

13

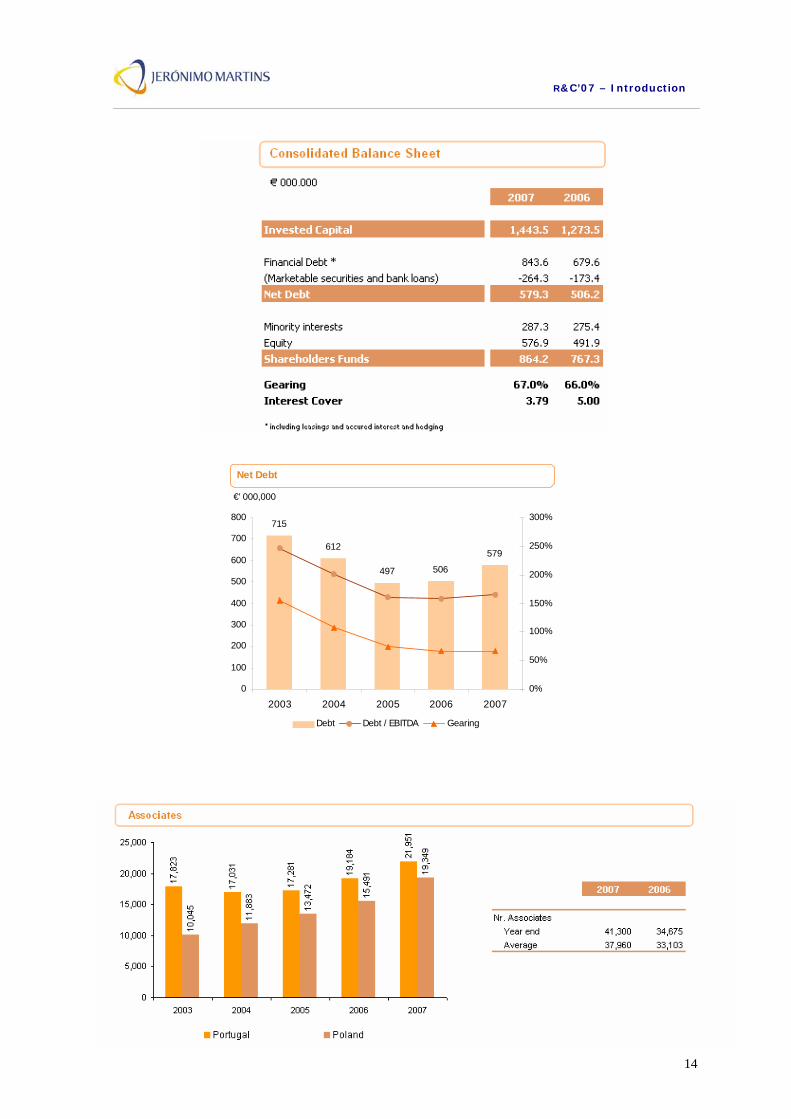

2. OPERATING AND FINANCIAL HIGHLIGHTS

R&C’07 – Introduction

14

Net Debt

612

497 506

579

715

0

100

200

300

400

500

600

700

800

2003 2004 2005 2006 20070%

50%

100%

150%

200%

250%

300%

Debt Debt / EBITDA Gearing

€' 000,000

R&C’07 – Introduction

15

10.1

%

7.5% 7.8%

4.4%

10.4

%

7.5%

8.5%

4.9%

9.7%

6.7%

8.0%

5.1%

8.2%

6.0%

5.5%

5.3%

7.0%

6.0%

4.6%

5.9%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Retail Cash & Carry Madeira Biedronka

2003 2004 2005 2006 2007

EBITDA Margin

% of Sales

R&C’07 – Introduction

16

Owne

rshi

p

Conso

lidat

ion

07 06 ℵ% 07 06

Supermarkets (Leader) 51% I 1.136,8 967,6 17,5% 210 183.770 6,7 8,7%

7,0% 8,2%Hypermarkets (3rd Player) 51% I 800,9 739,7 8,3% 46 172.039 5,0 -2,0%

Cash & Carry (Leader) 100% I 626,1 602,2 4,0% 6,0% 6,0% 33 109.634 5,7 3,6%

(Lidosol) Supermarkets 9,0 12,7%75,5% I 123,3 111,1 10,9% 4,6% 5,5% 15 14.626

(J.G.Camacho) Cas h & Carry 8,5 -0,9%

Margarine, Olive Oil, Seed OilReady to Drink Tea & Sav oury

Home Care & Personal Care 45% P

Ice Cream

R epresentat io n & M arket ing Serv ic es 100% I

C ho c o lats 51% I

5.349,7 4 .407,2 21,4% 6,6% 7,2%* in lo c al c urrenc y ('000) I - Integral

P - Proportional

18,6 21,1%39,5% 5,9% 1.045 536.7295,3%

CONSOLIDATED

11,3% 14,2%

I

322,257 327,7 -1,7%

1.715,52.392,3

Por tugal M ain land

Por tugal M ade ira

Poland

Portugal

Sale s (M illion e uro) EBITDAM arg in

Nr .Store s

07

Sale s Are a (s qm )

07

Sale s / s qm *

07

LFL %

07/06

Retail Stores (Leader)

FOOD DISTRIBUTI

ON

MANUFACTURI

NG

100%

R&C’07 – Introduction

17

3. CORPORATE BODIES Election Date: 30th March 2007 Composition of the Board of Directors elected for the term 2007-2009

President of the Board of Directors Elísio Alexandre Soares dos Santos

73 years old; President of the Group since February 1996.

Executive Board Members:

CEO and Responsible for the Financial Area (CFO) Luís Maria Viana Palha da Silva

52 years old; President of the Executive Committee since 2004; Executive Member of Jerónimo Martins, SGPS, S.A. Board since

2001. Responsible for Food Distribution Operations Pedro Manuel de Castro Soares dos Santos

48 years old; Member of the Executive Committee; Executive Member of Jerónimo Martins, SGPS, S.A. Board since

1995. Responsible for Manufacturing Operations and Representation and Marketing Services José Manuel da Silveira e Castro Soares dos Santos

45 years old; Member of the Executive Committee; Executive Member of Jerónimo Martins, SGPS, S.A. Board since

2004. Non-Executive Members of the Board:

António Mendo Castel-Branco Borges 59 years old; Non-Executive Member of the Jerónimo Martins, SGPS, S.A.

Board since 2001. Hans Eggerstedt

69 years old; Non-Executive Member of the Jerónimo Martins, SGPS, S.A.

Board since 2001. Rui de Medeiros d’Espiney Patrício

75 years old; Non-Executive Member of the Jerónimo Martins, SGPS, S.A.

Board since 2001.

R&C’07 – Introduction

18

Artur Eduardo Brochado dos Santos Silva 66 years old; Non-Executive Member of the Jerónimo Martins, SGPS, S.A.

Board since 2004. Nicolaas Pronk

45 years old; Non-Executive Member of the Jerónimo Martins, SGPS, S.A.

Board since 2007.

Single Auditor and External Auditor:

PricewaterhouseCoopers & Associados – Sociedade de Revisores Oficiais de Contas, Lda. Palácio Sottomayor, Rua Sousa Martins, 1 – 3º, 1050-217 Lisboa Represented by: Jorge Manuel Santos Costa, R.O.C. Substitute: José Manuel Henriques Bernardo

Corporate Secretary:

Henrique Manuel da Silveira e Castro Soares dos Santos Substitute Secretary: António Neto Alves

President of the Shareholder’s General Meeting:

João Vieira de Castro Secretary of the Shareholder’s General Meeting:

Tiago Ferreira de Lemos

R&C’07 – Introduction

19

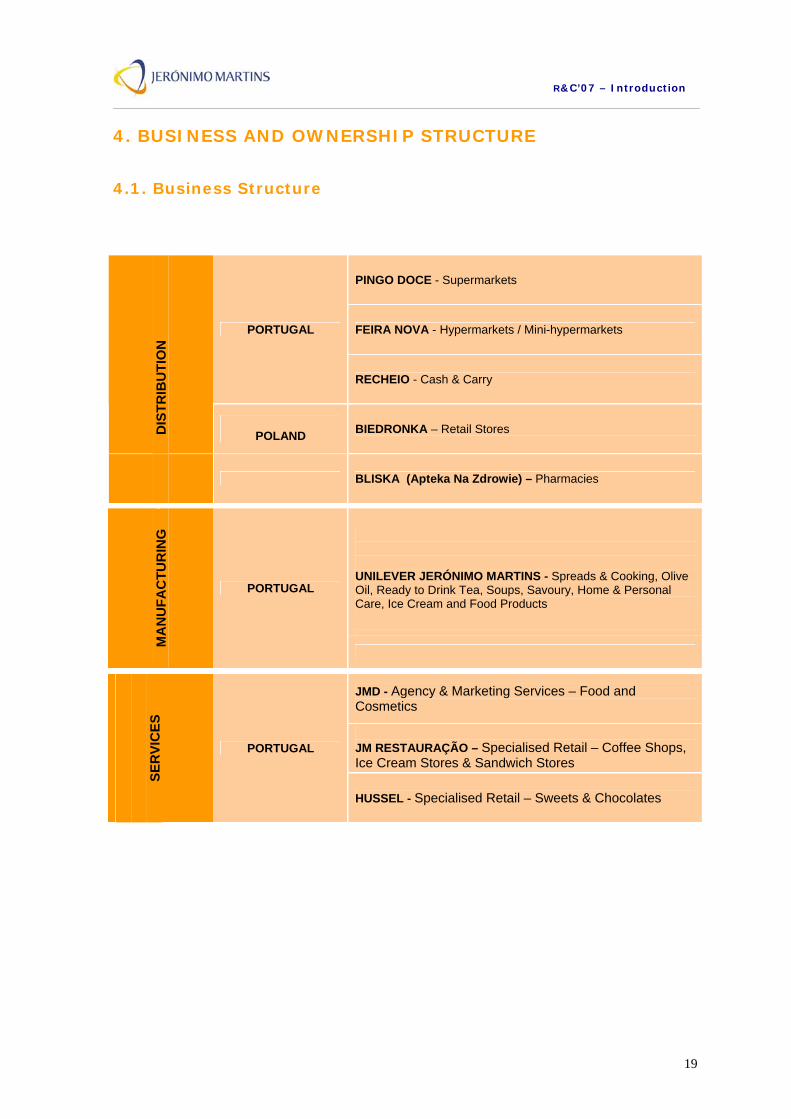

4. BUSINESS AND OWNERSHIP STRUCTURE

4.1. Business Structure

PINGO DOCE - Supermarkets

FEIRA NOVA - Hypermarkets / Mini-hypermarkets PORTUGAL

RECHEIO - Cash & Carry

D

ISTR

IBU

TIO

N

POLAND BIEDRONKA – Retail Stores

BLISKA (Apteka Na Zdrowie) – Pharmacies

UNILEVER JERÓNIMO MARTINS - Spreads & Cooking, Olive Oil, Ready to Drink Tea, Soups, Savoury, Home & Personal Care, Ice Cream and Food Products

MA

NU

FAC

TUR

ING

PORTUGAL

JMD - Agency & Marketing Services – Food and Cosmetics

JM RESTAURAÇÃO – Specialised Retail – Coffee Shops, Ice Cream Stores & Sandwich Stores

SE

RVI

CES

PORTUGAL

HUSSEL - Specialised Retail – Sweets & Chocolates

R&C’07 – Introduction

20

4.2. Ownership Structure

R&C’07 – Introduction

21

5. MANAGEMENT STRUCTURE Jerónimo Martins, SGPS, S.A. is the Group's Holding Company, which encompasses three distinct Business Areas: (1) Food Distribution, (2) Manufacturing and (3) Marketing, Representations and Restaurant Services. Food Distribution is divided into geographical areas of operation, in Portugal and Poland. In Portugal, the Operating Companies – Pingo Doce and Feira Nova – have the following Divisions in their organisation structure: Operations, Category Management, Marketing, Technical and Controller. With regard to Recheio, apart from the aforementioned Divisions, there are also the following: Food Service, Information Systems, and Human Resources. For the operation in Madeira, its structure also requires the following areas, although on a more reduced scale: Logistics, Quality Control and Human Resources. In each case, the abovementioned areas have a direct report to the Managing Director of the Company. It should also be noted that there are Functional Divisions in Retail Operations in Portugal organisation structure, providing services across the Operating Companies in each of the respective areas, namely Human Resources, Sourcing, Logistics, Perishables, Quality Control, Financial, Information Systems, Customer Ombudsman, Market Surveys, Expansion and Legal Services. In this way, there is an effort to maximize the Group's synergies in terms of scale, resources and know-how, as well as to guarantee the necessary focus on business formats and on the consumer. The Operating Companies and the Distribution Functional Divisions are represented on the Distribution Portugal Executive Board, a body that chairs the coordination and deliberation of strategic decisions regarding the business. On the other hand, Poland follows a management structure in which the head of the Business Division is responsible for the areas of Category Management, Marketing, Operations, Technical, Human Resources, Logistics, Financial, Quality Control and Information Systems. Following the merger of the former Companies FimaVG, Bestfoods, LeverElida and IgloOlá into Unilever Jerónimo Martins, the management structure of the Manufacturing area is based on a Management Board, made up of members nominated by the partners Jerónimo Martins SGPS, S.A. and Unilever. An Executive Division reports to this Body, which is made up of the Business Units’ Food, Personal and Home Care and Out of Home Divisions, as well as the Functional Divisions of Sales, Human Resources, Supply Chain (which encompasses Purchasing, Planning, Logistics, Customer Service, Quality Control and Productive Units), Financial, Legal, Communications and Information Systems. Jerónimo Martins Distribuição is in charge of Jerónimo Martins Distribuição de Produtos de Consumo, Jerónimo Martins Restauração e Serviços and the PGJM, Caterplus and Hussel joint ventures. All Companies are responsible for their operations and business managements, although Jerónimo Martins Distribuição provides its sister companies with Financial Information Systems and Logistics services.

R&C’07 – Introduction

22

Jerónimo Martins, SGPS, S.A. also includes a number of Functional Divisions whose responsibility is to support and advise the Executive Committee, the Board of Directors and the Companies of the Group, about the specific situation of each area: Human Resources, Development and Strategy, Planning and Control, Consolidation and Accountancy, Internal Auditing, Financial Operations and Risk Management, Special Projects, Investor Relations, Tax, Legal Affairs, Communications and Safety. Each of these Functional Management Divisions of the Group's Holding Company is responsible for ensuring consistency of approach for each of the objectives defined. Their activities are described in the Corporate Governance Report.

R&C’07 – Introduction

23

6. FINANCIAL GLOSSARY *

EBITDA Margin = (+ Operating Results + Depreciation + Goodwill Amortisation - Non-Recurrent Operating Results)

/ Net Sales & Services

EBITA Margin =

(+ Operating Results + Depreciation - Non-Recurrent Operating Results)

/ Net Sales & Services

OIC (Operating Invested Capital) =

+ Gross Goodwill + Net Fixed Assets + Working Capital

NOIC (Non Operating Invested Capital) =

+ Goodwill Accumulated Amortisation + Net Financial Investments + Deferred Taxes Provision + Income Tax Provision

Pre-Tax ROIC (Return, before taxes, on Invested Capital) = [Sales & Services / (OIC + NOIC – Deferred Taxes provision - Goodwill Acc. Amortisation) average] x EBITA Margin

Cash Flow =

+ Net Results + Amortisation, Depreciation and Provisions - Deferred Taxes - Non Recurrent Items (operating, disposals and financial)

Net Debt =

+ Bonds + Bank Loans + Other loans - Marketable securities and bank deposits

+ Leasing + Accrued interest

Gearing = + Net Debt / + Shareholders funds

R&C’07 – Introduction

24

Interest Cover Ratio + EBITA / [+ Financial Results (excluding non recurrent items) - Partners loans interest]

Like For Like sales: Sales made by stores that operated under the same conditions in two periods. Excludes stores opened, closed or which suffered major remodelling works in one of the periods.

* This financial glossary is based on the income statement by functions

R&C’07 – Introduction

25

7. CONTACTS Aiming to facilitate the direct access to some of Jerónimo Martins Group entities the following e-mail address are disclosed: Elísio Alexandre Soares dos Santos (Chairman of the Group) [email protected] Luís Palha (Chief Executive Officer) [email protected] Pedro Soares dos Santos (Member of the Executive Committee - Responsible for Food Distribution Operations) [email protected] José Soares dos Santos (Member of the Executive Committee - Responsible for Manufacturing and Representations and Marketing Services) [email protected] Henrique Soares dos Santos (Company Secretary) [email protected] Cláudia Falcão (Head of Investor Relations and Market Relations Representative) [email protected] Ethics Committee [email protected] Communication Department [email protected] Human Resources Department [email protected] Client’s Ombudsman [email protected]

II. Corporate Governance

Introduction

28 1. Statement of Compliance

29 2. Disclosure of Information

29 2.1. Organizational Structure and Distribution of Responsibilities

35 2.2. Specific Committees

36 2.3. Risk Control System

48 2.4. Share Price Performance

52 2.5. Dividend Distribution Policy

52 2.6. Stock Options Plan

52 2.7. Business between the Company and Members of the Board, Holders of Qualified Stakes and Companies in a Parent-Subsidiary or Group Relationship

53 2.8. Investor Relations Department

55 2.9. Remuneration Committee

56 2.10. Yearly Amount paid to External Auditor

57 3. Exercise of Shareholder Voting and Representation Rights

57 3.1. Statutory Rules on Exercising Voting Rights

57 3.2. Required Deadline for Depositing or Blocking Shares

58 3.3. Deadline for Receiving Postal Votes

58 3.4. Number of Shares Corresponding to One Vote 59 4. Company Rules

59 4.1. Code of Conduct and Internal Regulations

59 4.2. Internal Procedures for Risk Control in Company Activity

59 4.3. Measures Likely to Interfere with Public Tender Offers

60 5. Board of Directors

60 5.1. Description of the Board of Directors

64 5.2. Executive Committee

64 5.3. Structure and Role of the Board of Directors

65 5.4. Remuneration Policy of Board of Directors

65 5.5. Remuneration of the Members of the Board

66 5.6. Communications Policy for Alleged Irregularities Occurring within the Company (Whistleblower Procedure)

R&C’07 – Corporate Governance

27

INTRODUCTION The modification of the Commercial Companies Code, and the application of Decree-Law 76-A/2006 of 29 March, brought about a profound change in the rules with respect to Corporate Governance in Portugal, particularly in reforming supervision of companies through separation of supervisory functions and accounts review, thus reinforcing the independence and technical competence of members of supervisory bodies. Consequently, last year a revision of the By-Laws was discussed at the General Annual Shareholders Meeting, contemplating the changes imposed by that law in this important matter. Thus, the Company adopted the so-called "Anglo-Saxon" model of governance, with its corporate entities being called: the General Shareholders Meeting, the Board of Directors, the Audit Committee and the Chartered Accountant, as a coherent evolution of the previous monist model. In order to modernise the By-Laws and to adhere to the most advanced practices in the realm of corporate governance, an effort was made to adjust the related issues accordingly, such as: regulating votes by correspondence, the possibility of holding meetings of the Board of Directors using telematic means, as well as establishing the number of absences from meetings (without justification accepted by the Board) which will lead to declaration of definitive absence of the Director. With regard to remuneration, the By-Laws established the maximum percentage of profits from the year that may be delivered to the directors as variable pay. In 2008, and considering that the so-called new Corporate Governance package will enter into effect, Jerónimo Martins will continue to heed the respective recommendations, always seeking to follow the criteria that is interesting to the shareholder and to the market, adjusting its practices, if necessary, in order to provide more rigour and transparency. Therefore, to date the Company has already adopted (or projects that it will adopt this year) the measures that will allow it to comply with the recommendations contained in the new Corporate Governance Code. Since these recommended rules, as devised for 2008, will only take effect in 2009, this report complies with CMVM Regulation No. 7/2001, according to the instructions given by the Comissão do Mercado de Valores Mobiliários (CMVM) itself [Securities and Exchange Commission].

R&C’07 – Corporate Governance

28

1. Statement of Compliance The Company fully complies with the recommendations of the Portuguese Securities and Exchange Commission on the Governance of Listed Companies. The Company accepts, however, that in the light of the document in question, it might be thought that there has not been a complete response to the recommendation concerning the individual breakdown of remuneration paid to the Members of the Board of Directors. In this respect, the Company maintains the view that there are other options for verifying the internal distribution of remuneration and assessing the relationship between the performance of each Company sector and the level of remuneration of the Members of the Board of Directors who are responsible for supervising these sectors, considering that it is attained with indication of global remuneration of Executive Directors on one side, and Non-Executives on the other. In addition, the Board of Directors believes that the internal and external sensitivity that such a disclosure could cause in no way contributes towards improving the performance of its members. Therefore, the Recommendation has been adopted as far as remunerations in collective terms are concerned, and by differentiating the amounts paid to Executive Members (with reference to both the fixed and variable parts) and Non-Executive Members. On the other hand, as occurred last year, the recommendation with regard to the appreciation, by the General Shareholders Meeting, of a statement on the remuneration policy of the Board of Directors was adopted, as it is the Company's understanding that the purpose of this recommendation is fully adhered to by the fact of the Annual Report submitted for Shareholder approval contains the information relevant to remuneration paid in the previous year, as well as the main guidelines defined in relation to the matter in question, which will be tracked by the Remuneration Committee. As it is admitted that another interpretation of this recommendation is possible, and that the CMVM has not recognized the Company's position merit, in 2008 it will opt to autonomously submit that statement to the Shareholders.

R&C’07 – Corporate Governance

29

2. DISCLOSURE OF INFORMATION

Functional Directions Corporate Centre

Services Manufacturing Food Distribution

Portugal

Functional Directions

Operational Support

Poland

Executive Officer of the

Board

JMD

Biedronka Food Stores

Jerónimo Martins Food

Retail and Services

Caterplus Hussel PGJM

Unilever JM

Victor Guedes

Pingo Doce Supermarkets

Madeira Supermarkets Cash & Carry

Feira Nova Hypermarkets

Recheio Cash & Carry

Fima Lever Olá

JERÓNIMO MARTINS, SGPS, SA

Apteka Na Zdrowie Pharmacies

2.1. Organizational Structure and Distribution of Responsibilities Jerónimo Martins SGPS, S.A. is the Holding Company of the Group and as such, responsible for the main guidelines of the various businesses, as well for ensuring consistency between the established objectives and the available resources. The Holding is made up of a group of Functional Divisions which provide both support to the Corporate Centre and services to the Functional and Operating Divisions of the Group's Companies. In operational terms, Jerónimo Martins is organised into three business areas: (i) Food Distribution, (ii) Manufacturing and (iii) Marketing, Representations and Restaurant Services. The first area is organised into Geographical Areas and Operating Divisions. 2.1.1. Holding Company Functional Divisions The Holding Company is responsible for: (i) defining and implementing the development strategy of the Group's portfolio; (ii) strategic planning and control of the various businesses and its consistency with global objectives; (iii) defining and controlling financial policies and (iv) defining human resources policy, with direct responsibility for implementing the Management Development Policy. The Functional Divisions of the Holding Company are organised in the following way:

R&C’07 – Corporate Governance

30

Legal Affairs António Neto Alves

Internal Audit Nuno Sereno

Communication Ana Vidal

Consolidation and Accounts António Pereira

Development and Strategy Margarida Martins Ramalho

Financial Operations Conceição Tavares

Planning and Control Ana Luísa Virginia

Special Projects Francisco Martins

Human Resources Inês Cavalleri

Security Eduardo Dias Costa

Fiscal Affairs Rita Marques

GRUPO JERÓNIMO MARTINS Functional Divisions of Corporate Support

Investor Relations Cláudia Falcão

Internal Audit – Assesses the quality and efficiency of systems (both operational and non-operational) of internal control and risk control established by the Board of Directors, ensuring compliance with the Group's Manual of Procedures. The Division also guarantees full compliance with the procedures laid out in the Operations Manual of each business unit and ensures compliance with the legislation and regulations applicable to the respective operations. The activities carried out by this Functional Division can be found in detail later in this chapter. Communication – Proposes and implements strategies for external and internal communication. Included in its scope are the areas that provide media advice for the Holding Company and its subsidiaries, internal communications, patronage, communication in the area of Social Responsibility, as well as brand management and managing the institutional image of Jerónimo Martins. 2007 was marked by the development of innovative communication solutions, which were recognised by the market. Thus, the digital format of the 2006 Accounts Report obtained the award "Best Accounts Report for the Non-Financial Sector" for the second time (Investor Relations and Governance Awards, 2007). Jerónimo Martins' Internet site, through its audio functionality on online content (in Portuguese and English) ensures complete accessibility to the vision-impaired. In media relations, in addition to daily clarifications and numerous press releases, there were five events with Media and members of the Group’s Board of Directors. Of these events, the opening of the 1000th Biedronka store is noteworthy. This event resulted in significant representation by different media sources visiting Poland, Biedronka's stores and its distribution centre.

R&C’07 – Corporate Governance

31

In the Internal Communications area, investments were made in profound reformation of the My JM Portal, in order to ensure an increasingly efficient and complete communication channel. Legal Affairs – Responsible for supervising the Group's corporate affairs and for ensuring strict compliance by all its Companies with legal obligations. Legal Affairs also assists the Board of Directors in preparing and negotiating contracts in which Jerónimo Martins is a party, and it heads the development and implementation of strategies for the protection of the Group's interests in the case of legal disputes, and the management of external counselling. In 2007, the Division focused its activity on overseeing compliance with company obligations, particularly in tracking the Group's reorganisation and expansion activities, particularly acquisition of Plus companies in Portugal and Poland to the Tenglemann Group, as well as other smaller-scale acquisitions. Consolidation and Accounting – Prepares consolidated financial information in order to comply with legal obligations and supports the Board of Directors, by implementing and monitoring the policies and the accounting principles adopted by the Board and common to all the Companies of the Group. The Division also verifies compliance with obligations stated in the By-Laws. In 2007, activity was centred on supervising conformance with the accounting standards adopted by the Group, supporting the Companies in the accounting assessment of all non-recurring transactions, as well as in the restructuring and expansion activities of the Group. Development and Strategy – Guarantees continuous assessment of the markets, identification of the risks, opportunities and major contingencies of the Group’s activity in the short-, medium- and long-term, and critical analysis of development plans for the different business areas. It contributes with perspectives on strategic debates that lead to growth projects, both in the current portfolio and in new business areas, and to optimisation initiatives in order to create value. It also ensures mechanisms to define priorities deriving from the strategic debate, and the common and general understanding of the main challenges that face the Organisation, leading to clear and objective communication. In 2007, the Department concentrated its efforts on performing studies, considering consolidation of the debate on the foundations of the strategic plan. In this way, it was able to evaluate the Group's competitive position, showing the businesses' competitive advantages, the areas of potential growth, and differentiation and possible contingencies. In turn, financial analysis, based on historical three-year projections, allowed showing the degree of agreement with the Group's medium- and long-term objectives. A strategic evaluation system was also presented, with trends that would allow a simple reading of the sector and the markets in connection with the projects being developed by the Group. Within this scope, the study of new business opportunities continued to be a central theme of the strategic debate, thus the Department contributed with specific studies for the vast group of initiatives that the Group has been developing in this area.

R&C’07 – Corporate Governance

32

Investor Relations - This Division is the interface with all investors - institutional and private, national and foreign - as well as the analysts who formulate opinions and recommendations regarding Jerónimo Martins’ share price. Besides guaranteeing the availability - through institutional channels, in particular the website of the CMVM (Securities Exchange Commission) - of all information that may influence the share price, the Division is responsible for providing general information and clarification regarding the different Business Areas. The activities carried out by this Functional Division can be found in detail later in this chapter. Fiscal Affairs – Provides all the Group's Companies with assistance in fiscal matters, ensuring compliance with the current legislation as well as optimising the business unit's management activities from a fiscal viewpoint. The Division also manages the Group's tax disputes and its relations with external consultants and Tax Authorities. In the course of its work in 2007, the Fiscal Affairs Department provided assistance to the Company's acquisition and restructuring operations. Furthermore, special work was carried out with regard to the different taxes in order to unify the policies adopted by the Group's different Companies. Finally, over the course of the year, the Fiscal Department collaborated in filing several procedures to better defend the interests of the Group with the Tax Authorities. Financial Operations – This Division includes two distinct areas: Risk Management and Treasury Management. The activity of the Risk Management area is dealt with in detail later in this chapter. Treasury Management is responsible for managing relations with the financial institutions that have or intend to have business dealings with Jerónimo Martins, establishing the criteria that these entities must fulfil. The Treasury is also in charge of planning the most suitable financial sources according to need for all the Companies of the Group. The type of funding, corresponding terms, cost and back-up documentation must comply with the criteria established by Management. Likewise, the Treasury is responsible for conducting business with financial institutions, optimising factors so that the best possible conditions may be obtained at all times. A large part of the treasury activities of Jerónimo Martins are centralised in the Holding Company, which is a structure that provides services to the rest of the Companies of the Group. The National Distribution Companies are completely centralised while the Polish Distribution and Representation and Restaurant areas still work independently in relation to processing payments to third parties. It is also Treasury's responsibility to elaborate and comply with the treasury budget that is based on the activity plans of the Group’s Companies. In compliance with the activities described above, namely in relation to maturity dates of the Group's debt and investments, Jerónimo Martins SGPS paid back two bond loans in advance, in the amount of 25 million euros each, and on the same date it issued two new bond loans in the amount of 70 million euros, thus increasing the

R&C’07 – Corporate Governance

33

maturity of the debt profile. The subsidiary JMR-Gestão de Empresas de Retalho SGPS, S.A. exercised the call option on the bond loan issued in June 2003, repaying the amount of 115 million euros. It then issued a new bond loan in the amount of 200 million euros, which also sought to restructure the short-term debt. In addition to increasing the maturity profile of the debt, this restructuring also resulted in reducing the average cost of the debt. Planning and Control – Responsible for defining and implementing processes, policies and procedures in the planning and control area (plans, budgets and investments), and coordinating and supporting M&A activities of companies or businesses, and company restructuring operations. In 2007, the process of reorganising the assets of Grupo Jerónimo Martins was initiated, with a view to simplifying management and maximising operating efficiency of the different business areas. Support was thus provided to various projects under way, including centralisation of the Group's brand management in one business area, and analysing different scenarios for the Group's real estate assets. It also coordinated the acquisition of Plus companies in Portugal and Poland from Grupo Tenglemann, and it will accompany the integration process until it is concluded, which is projected to be until the end of the first quarter in 2008. It also coordinated and supported other, smaller-scale acquisitions by different business areas in the Group, in Portugal and Poland, some of which have been concluded. Some adjustments were made to the Planning process in conjunction with the Departments of Strategy and Development, and Consolidation and Accounting, in order to simplify and expedite it without losing efficiency. Finally, in relation to investments and considering the Group's current phase of organic expansion, numerous proposals were analysed, which will be discussed in its own chapter in the Management Report. Special Projects– In collaboration with the various Operating Divisions of Food Distribution in Portugal, the Division's main objectives are: (i) to identify, prioritise and optimise existing processes within the Companies; (ii) to recognise new opportunities that may add value for customers; (iii) increase business profitability; (iv) increase productivity and improve competition in the markets in which they are present; and (v) to strengthen innovation processes, promote responsibility in those involved and integrate businesses and new information technologies. The activities carried out by this Functional Division are detailed in the chapter Consolidated Management Report. Human Resources – Ensures the definition and implementation of global Human Resources strategies and policies to be applied to the entire Group, in particular to its managers. It is therefore responsible for drawing up Human Resources strategies, policies, standards and procedures, particularly in the areas of recruitment, training, performance management, career management, remuneration and benefits. The

R&C’07 – Corporate Governance

34

Division is also responsible for coordinating new projects and for compliance with good Human Resources practices. The activities carried out by this Functional Division in 2007, can be found detailed in the chapter on Social Responsibility. Security – Defines and controls procedures aimed at preserving the security of personnel and assets within the Group and monitors any matters involving the police or legal authorities, when required. The Department is also responsible for supporting security system audits and risk prevention. The activities carried out by this Functional Division are detailed in this chapter in the section on the Risk Control System. 2.1.2 Operating Divisions The organizational structure of the Jerónimo Martins Group is aimed mainly at ensuring specialisation in the Group's various businesses by creating geographical areas and Operating Divisions that guarantee the required proximity to the different markets. As mentioned, the Food Distribution business is divided into Geographical Areas and currently has four Operating Divisions in Portugal - Pingo Doce (supermarkets), Feira Nova (hypermarkets), Recheio (cash & carry) and Madeira (supermarkets and cash & carries) - and an Operating Division in Poland, which includes Biedronka food stores and “Apteka Na zdrowie” pharmacies in partnership with the Portuguese National Association of Pharmacies. Manufacturing operates through a partnership between Unilever, the company Unilever Jerónimo Martins, Lda., which runs food, personal care and home care, and ice-creams businesses. Within the Group's portfolio there is also a business area dedicated to Marketing, Representations and Restaurant Services, which includes: (i) Jerónimo Martins Distribuição, which represents important, widely consumed food products and premium and mass market cosmetic brands under international brands in Portugal and that include Caterplus, a specialist in the trade and distribution of specific products for Food Service; (ii) Hussel, a retail chain specialised in chocolates and confectionary; and (iii) Jerónimo Martins Restauração e Serviços, with the chain of Jeronymo coffee shops, Ben & Jerry's and Olá ice cream stores and Subway stores. 2.1.3. Functional Operational Support Divisions The Functional Divisions at the operating level ensure that Group synergies are maximised through the sharing of resources and functions across the main markets, in order to optimise the efficiency of the Organisation and the sharing of relevant skills and know-how. The Operating Functions of Support Divisions are: Sourcing, Logistics, Quality and Environmental Control, Financial and Information Systems. These Divisions are responsible for providing services to the various distribution operating divisions in Portugal, in accordance with the guidelines given by the Group's Holding Company. They are also responsible for ensuring standard of policies and internal procedures.

R&C’07 – Corporate Governance

35

2.1.4 Matters Committed to the Members of the Executive Committee While their functions are carried out collectively, each Member of the Executive Committee holds supervisory responsibilities in certain specific areas, as follows: Luís Palha da Silva (President): Development and Strategy, Financial Area, Reporting and Operational Control, Investor Relations, Legal Affairs, Fiscal Affairs, Human Resources and Communication. Pedro Soares dos Santos: Food Distribution Operations, including Sourcing, Logistics, Quality Control, Human Resources, Security and Information Systems. José Soares dos Santos: Manufacturing Operations, Marketing Services, Representations and Restaurants. 2.2. Specific Committees 2.2.1 Audit Committee From alteration of the By-Laws approved in the Annual General Shareholders Meeting of 2007, that the Audit Committee is in effect, which is a result of changes to the Code of Commercial Companies imposed by Decree-Law 76-A/2006 of 29 March. Thus, as voted on in the mentioned General Shareholders Meeting, and arising from the Board of Directors, the Audit Committee is responsible for supervising Company management and assessing corporate structure and governance. In addition to the responsibilities conferred by law, the Audit Committee, in performing its activities, is particularly responsible for the following: assessing the Company's governance structure, monitoring the process of preparing and releasing financial information, the efficacy of internal control systems, internal audit and risk management, as well as approving activity plans within the scope of risk management and tracking its execution, especially evaluating the recommendations resulting from audit activities and reviewing the procedures put into place. The Audit Committee, which has three Non-Executive Managers as members, including: Mr. Hans Eggerstedt (President), Mr. António Borges and Mr. Rui Patrício, all of whom are independent according to legal criteria, met four times during 2007, paying particular attention to the internal control and risk management systems. 2.2.2 Ethics Committee The Ethics Committee of the Jerónimo Martins Group is currently comprised of Ana Vidal (Director of Communications) presiding, Mr. Hugo Cunha (Director of Human Resources of Recheio), Mr. António Neto Alves (Director of the Company's Legal Department), Professor Leslaw Kanski (Director of the Legal Department of Jerónimo Martins Dystrybucja), and by Ms. Ewa Micinska (Director of Labour Relations of Jerónimo Martins Dystrybucja). Reporting to the Chairman of the Board of Directors of the Company, its mission is to provide independent supervision of the disclosure of, and compliance with, the Code of Conduct of the Group in all its Companies. In performing its duties, the Ethics Committee: (i) establishes channels of communication with the targets of the Group's Code of Conduct and gathers information sent for this purpose; (ii) administers a suitable internal control system for compliance with the Code of Conduct and assesses the recommendations arising from

R&C’07 – Corporate Governance

36

these controls; (iii) evaluates questions that, also in compliance with this Code of Conduct, may be submitted to it by the Board of Directors of Jerónimo Martins and by the Audit Committee, and impartially analyses any questions raised by employees, customers or business partners through the system to communicate alleged irregularities; and, finally (iv) submits to the Company's Board of Directors any measures it considers appropriate for adoption in this area, including the review of internal procedures, as well as proposals for changing the Code of Conduct. During 2007, the Ethics Committee met twelve times and examined various questions submitted to it by the Executive Committee, the Group's employees or by third parties. In the year in question, special attention was given to the bottom-up communication system, which ensures that all employees at all levels can communicate possible irregularities, seeking to strengthen efficiency in the two countries where the Group operates. 2.2.3 The Internal Control Committee The Internal Control Committee, appointed by the Board of Directors and reporting to the Audit Committee, is specifically responsible for assessing the quality and reliability of the internal control system and the process of preparing financial statements, as well as assessing the quality of the monitoring process in effect at the Companies of Jerónimo Martins, seeking to ensure compliance with the laws and regulations to which they are subjected. In performing its tasks of assessing the quality of the monitoring process being used in the Companies of the Group, the Internal Control Committee must obtain regular information on the legal and fiscal contingencies that affect the Group's Companies. The Internal Control Committee meets monthly and is comprised of a President (Mr. David Duarte) and three members (Mr. José Gomes Miguel, Mr. Nuno Sereno and Mr. Henrique Santos), none of whom are Company Board Members. In 2007, the Internal Control Committee met ten times to carry out its activities of supervision and assessment of risks and critical processes and to review the reports prepared by the Internal Audit Department. When a representative of the External Audit team is invited to attend these meetings, the Committee is also informed of the conclusions of the external audit work that takes place during the year. 2.3. Risk Control System 2.3.1 Risk Management The Company, and in particular its Board of Directors, dedicate a great deal of attention to the risks affecting their business. Business continuity is critically dependent on the elimination or control of risks that may materially affect its assets (people, information, equipment, facilities), thereby jeopardising the strategic objectives they have set. The Group's Risk Management Policy formalises this concern. Because of the size and geographical dispersion of Jerónimo Martins’ activities, the success of risk management depends on the participation of all employees, who should assume it as an integral part of their jobs, particularly through the identification and reporting of risks associated with their area. All activities must be carried out with an understanding of what risk is and an awareness of the potential impact of unexpected events on the Company and its reputation.

R&C’07 – Corporate Governance

37

Risk Management Objectives Within the Group, Risk Management aims to meet the following objectives:

To promote the identification, evaluation, handling and monitoring of risks, in accordance with a methodology common to the whole Group;

To regularly assess the strengths and weaknesses of key value drivers; To develop and implement programmes to cover and prevent risk; To integrate Risk Management into business planning; To promote the awareness of the workforce with regard to risks and the positive

and negative effects of all processes that influence operations and that are sources of value creation;

To improve the decision-making and priority-setting processes, through the structured understanding of the business processes of the Group, their volatility, opportunities and threats.

The Risk Management Process (RMP) In the first place, risk evaluation seeks to distinguish what is irrelevant from what is material. This requires active management and involves consideration of sources of risk, probability of occurrence, and the consequences of their manifestation within the context of the control environment. Controls may encompass both the likelihood of occurrence of an event and the extent of its consequences. The RMP is cyclical in nature, and includes (i) identification and evaluation of risks; (ii) definition of management strategies; (iii) implementation of control processes; and (iv) monitoring of the process. The RMP of the Group complies with the Federation of European Risk Management Associations (FERMA) standards, which is seen as a model of good practice. The objectives defined during the strategic and operational planning process are the departure point of the RMP. At this time internal and external factors that may compromise fulfilment of the established goals are being identified and assessed. This approach is based on the concept of Economic Value Added (EVA). It begins with the analysis of the key value drivers of both the operating profit and the cost of capital, in an attempt to identify the factors of uncertainty that may negatively influence the generation of value. In this manner, a systematised, interconnected perspective of the risks inherent to processes, functions and organisational Divisions is developed. 2.3.2. Organization of Risk Control The risk areas where management must be assumed by specific departments are as follows: Quality, Food Safety and Environment Management of this risk area, which in Distribution in Portugal is coordinated by the Quality and Environment Division, works in prevention, monitoring and training,

R&C’07 – Corporate Governance

38

minimising food risks (with an impact on the consumers’ health) and progressively reducing the associated environmental impacts of the Group's products and services. The following are important management tools in this risk area: • Performing periodic simulations that recreate a crisis scenario and allow

assessment of how adequate existing procedures are; • Audits to select, assess and track suppliers' proposals for improvements; • Regular internal audits aimed at assessing compliance with good practices

(environmental, hygiene and labour) and compliance with the requirements of systems (HACCP Food Safety System/Environmental Management System, Quality Management System), and monitoring a product throughout the entire logistics chain;

• Implementation of analytical control plans, both internal – store operations – involving work surfaces, product handling/transformation in the stores and the water used, and external – suppliers – such as the periodic control that private brand products are subject to, or research of the phytopharmaceutical residue in fruit and vegetables;

• Training for current staff and subcontractors to ensure good practices with regard to the environment, labour, production, exposure and hygiene;

• Undertaking innovative projects for the Group's activities (for example, promoting technologies that rely on renewable energy sources), seeking to prevent pollution and to reduce costs;

• Periodically review existing HACCP Food Safety Systems, adapting them to the new business areas that emerged in 2007, such as the Restaurants and Central Kitchens of Pingo Doce.

The activities developed by the Quality and Environmental Division in 2007, are detailed in the chapter on Social Responsibility. Contingency Plan for the Bird Flu Pandemic The World Health Organisation (WHO) has warned that bird flu (H5N1 virus) has a high likelihood of becoming the next pandemic. Previous pandemics had a huge impact on people’s lives and on the economy on a global scale. Currently in Phase 3 (WHO), transmission between humans has already occurred in more than one geographical region. However, the virus has still not acquired the capacity for effective transmission; therefore the WHO has not yet decreed progress to the next phase. In addition to being a public health problem, a pandemic flu constitutes a social and economic risk with a huge impact on the supply chain, caused by breakdowns in areas of the economy as important as production and distribution of fuel, energy, water and food products. In order to minimise the impact of a possible pandemic, it is considered necessary to prepare and implement contingency plans aimed at reducing the propagation of the disease, as well as finding ways to keep business activities running. Hence, the Company has an operational contingency plan that establishes which management activities and procedures must be carried out to minimise the impact of a pandemic on the Organisation and guarantee business continuity.

R&C’07 – Corporate Governance

39

In 2007, a process of divulging the contingency operating plan to employees working in the Group's companies was developed. Hygiene and Safety at Work (HSW) In this area the continuous action has focussed on the gradual implementation of a safety culture, with consequent improvement in working conditions and accident reduction. As such, safety and hygiene in the workplace audits were carried out, especially focussing on professional risk factors, and physical, chemical and biological hazards were assessed. The prevention of possible emergency situations was also made a priority in the action programme for this area, and there are several Internal Emergency Plans, including one for the head office. In the Food Distribution area in Portugal, the Director of HSW heads coordination of the risk management process. In Poland, this responsibility is decentralised among the implementation regions of the Biedronka operation. As for the Manufacturing, this risk area is managed centrally, covering all the Companies involved. Security of People and Property The Security Department is responsible for ensuring that conditions exist to guarantee the physical integrity of people and facilities, intervening in cases of theft and robbery, as well as fraud and other illegal and/or violent activities perpetrated in the facilities or against the Group's employees. Among the responsibilities of the Security Department are: (i) definition and control of procedures in terms of prevention, and safety of the Group's personnel and property, including supervision of the performance and strategies of the security/surveillance firms hired; (ii) follow up, when deemed necessary, of events involving the police or judicial authorities; and (iii) providing support to security system and risk prevention audits. The Security Department is one of the Functional Divisions that comprise Holding Company of the Group and it reports directly to a member of the Executive Committee. In the course of its operations, the Division is in close contact with the Operations, Legal Affairs, Internal Audit and Risk Management Divisions. Facilities and Equipment The Companies Technical Teams, in strict collaboration with the respective Operations Departments have responsibility for: (i) guaranteeing the definition and execution of programmes for regular maintenance of facilities, in order to meet operational needs, and (ii) managing the process that aims to ensure the lowest level of negative impacts of equipment maintenance and repair on operations. In this area of risk Technical Managers are also involved in supervising the status of electrical equipment, the management of the means of protection and detection of fires as well as the storage of flammable material.

R&C’07 – Corporate Governance

40