Embed Size (px)

Citation preview

We stand by you

ANNUAL CONFERENCE FOR IN-HOUSE LAWYERS

Information and advise duties: How to tackle “misselling”?

By Antoine MAFFEI and Ferheen MAHOMED

Information and advise duties: How to tackle « misselling » ? 2

Summary

INFORMATION AND ADVISE DUTIES: HOW TO TACKLE MISSELLING ?

Information and advise requirements under the Markets in Financial Instruments Directive (MiFID) and an Asian perspective 3 categories of investors under the MiFID The scope of the information and advise duties of investment services providers under the

MiFID depends on the category to which the investors belong to An Asian perspective

Structured loans entered into between local authorities and credit institutions The Charter of conduct of business between local authorities (collectivités locales) and credit

institutions (the GISSLER Charter) Are structured loans entered into between local authorities and credit institutions financial

instruments in the sense of the MiFID?

The Packaged Retail Investment Products (PRIPs) Main features of PRIPs Are PRIPs financial instruments in the sense of the MiFID?

A French approach under consideration: the Deletré Report 2 Scope of the Deletré Report 2: all financial, banking and insurance products Main recommendations under the Deletré Report 2

Conclusion

Information and advise duties: How to tackle « misselling » ? 3

The classification of investors under the MiFID

INFORMATION AND ADVISE REQUIREMENTS UNDER THE MiFID AND

AN ASIAN PERSPECTIVE

Introduction of 3 categories of investors: Non professional clients (clients non professionnels or clients de détail) Professional clients (clients professionnels) Eligible counterparties (contreparties éligibles)

(Annex II of the MiFID / Articles D. 533-11 to D. 533-14 of the CMF)

Purpose: drawing up of different levels of requirements in terms of information and advise (applicable to investment services providers) which will depend on the category to which the investors belong to

Information and advise duties: How to tackle « misselling » ? 4

Scope of the information and advise requirements applicable to investment services providers under the MiFID

INFORMATION AND ADVISE REQUIREMENTS UNDER THE MiFID AND

AN ASIAN PERSPECTIVE

Any Information addressed by investment services providers to investors must be: fair clear not misleading

(Article 19.2 of the MiFID / Article L. 533-12 CMF)

Information requirements applicable prior to and after the provision of investment services

(Article 19 of the MiFID)

Information and advise duties: How to tackle « misselling » ? 5

Scope of the information and advise requirements applicable to investment services providers under the MiFID

INFORMATION AND ADVISE REQUIREMENTS UNDER THE MiFID AND

AN ASIAN PERSPECTIVE

1. Non professional clients Definition: clients which are not professional (Article 4 of the MiFID) Reinforced information and advise requirements applicable to the investment services

providers

2. Professional clients List of professional clients: in Annex II of the MiFID implemented under French law by Article

D. 533-11 of the CMF Attenuated information and advise requirements applicable to investment services providers

3. Eligible counterparties List of eligible counterparties: in Article D. 533-13 of the CMF Information and advise requirements do not apply to investment services providers in respect

of eligible counterparties

Information and advise duties: How to tackle « misselling » ? 6

An Asian perspective

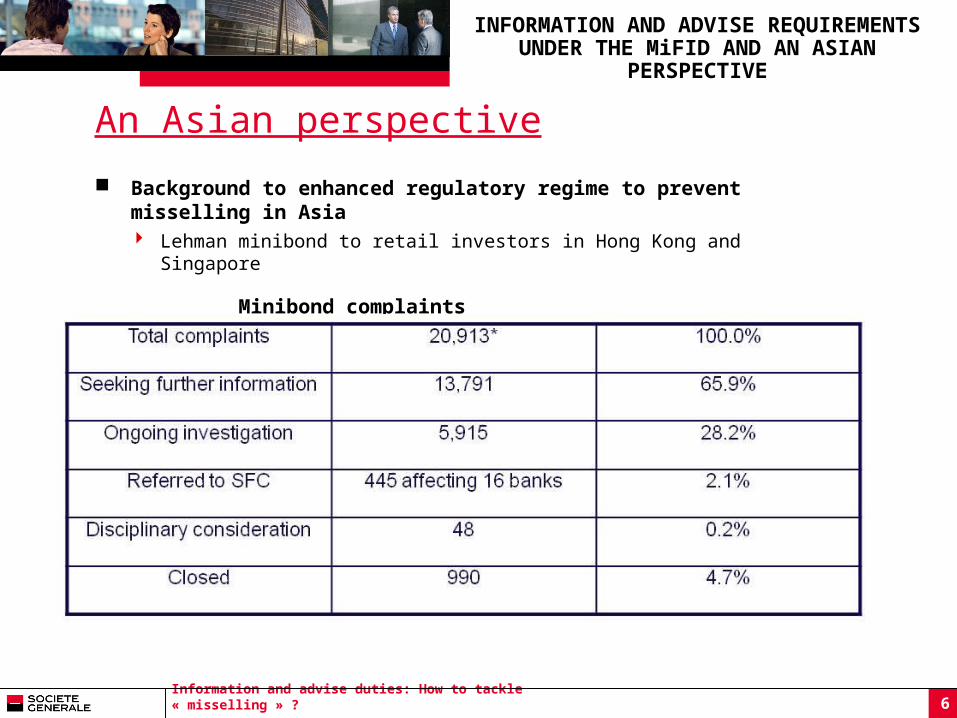

Background to enhanced regulatory regime to prevent misselling in Asia Lehman minibond to retail investors in Hong Kong and Singapore

Minibond complaints

INFORMATION AND ADVISE REQUIREMENTS UNDER THE MiFID AND

AN ASIAN PERSPECTIVE

Information and advise duties: How to tackle « misselling » ? 7

An Asian perspective

What was sold and how it was sold

• Purely on credit rating – misselling at its worst

Legislation enquiries

• Interrogation by politcians in open forum of regulators and distributing banks

Compensation by distributing banks

• 100% to senior citizens and illiterate investors, 60% to the remaining investors

INFORMATION AND ADVISE REQUIREMENTS UNDER THE MiFID AND

AN ASIAN PERSPECTIVE

Information and advise duties: How to tackle « misselling » ? 8

An Asian perspective

Resulting in enhanced regulatory regime in the region Hong Kong - Undertakings

We, __________________, the Arranger appointed by the Issuer in relation to the issue of the Product :

• confirm that we have conducted reasonable due diligence on the issuer, the guarantor and any other counterparty (where applicable), and the Product and the Offer Documents to ensure that :– the issuer will be able to comply with all laws, codes and guidelines applicable thereto; – the product is appropriate for distribution to the public taking into account the nature of the Product and the nature of

the persons likely to consider acquiring them.

Product providers are to be required to confirm that a structured product is designed fairly and is appropriate for the market(s) for which it is intended.

INFORMATION AND ADVISE REQUIREMENTS UNDER THE MiFID AND

AN ASIAN PERSPECTIVE

Information and advise duties: How to tackle « misselling » ? 9

An Asian perspectiveThe importance of assessing suitability

The key obligation that relates to the risk of misselling is the need for banks and firms to ensure that products are suitable for their clients.

This means banks and firms must know their client’s financial situation, investment experience and investment objectives (General Principle 4) and, having regard to that information, “..when making a recommendation or solicitation, ensure the suitability of the recommendation or solicitation for that client is reasonable in all the circumstances” (Para 5.2).

This is the cornerstone obligation for banks and firms engaged in the sale of financial products.

Let me be clear about the requirement of suitability. It does not mean banks and firms must make sure the client has received a copy of the prospectus, or that the client has been given a list of risks attached to the product or signed a form that says they have read the prospectus. These things might be relevant but they do not by themselves satisfy the requirement of suitability.

The onus is on the bank or the firm to ensure the product is an appropriate one for the client given the client’s financial situation, investment experience and investment objectives. The Code casts the obligation on the bank or firm to know the product is suitable. The obligation is not on the client.

It goes without saying that the person making the suitability assessment must have appropriate expertise to perform that task; have adequate training and information about the product, understand the product properly and be properly supervised. After all, the client is relying on that expertise and experience when making his investment decision.

SFC, 23 October 2008

INFORMATION AND ADVISE REQUIREMENTS UNDER THE MiFID AND

AN ASIAN PERSPECTIVE

Information and advise duties: How to tackle « misselling » ? 10

An Asian perspective

Taiwan

The issuer should ensure that a product cannot be offered to non-professional investors in Taiwan unless the same product can be offered to non-professional investors in the jurisdiction where the offshore Issuer or the product is registered. Further, the terms of the offer in Taiwan must not be less favourable than those in the “home country”.

Why? Minibonds not offered in the US / Europe

China

Banks are responsible to ensure that the products are suitable for a particular category of clients.

INFORMATION AND ADVISE REQUIREMENTS UNDER THE MiFID AND

AN ASIAN PERSPECTIVE

Information and advise duties: How to tackle « misselling » ? 11

The GISSLER Charter: Introduction

STRUCTURED LOANS ENTERED INTO BETWEEN LOCAL AUTHORITIES AND

CREDIT INSTITUTIONS

The GISSLER Charter is a charter of conduct of business between local authorities (collectivités locales) and credit institutions

The GISSLER Charter has been signed on December 7th, 2009

The GISSLER Charter is aimed at ensuring marketing of structured loans to local authorities compliant with their needs

Strong commitments of credit institutions under the GISSLER Charter

Local authorities are committed to a high level of transparency under the GISSLER Charter

Information and advise duties: How to tackle « misselling » ? 12

Main commitments of credit institutions under the GISSLER Charter:

STRUCTURED LOANS ENTERED INTO BETWEEN LOCAL AUTHORITIES AND

CREDIT INSTITUTIONS

Credit institutions refrain from marketing to local authorities:

Financial products exposing to a risk on principal or products based on high risk indexes

Financial product with cumulative index effects (“Snowbolling Effects”)

Credit institutions undertake under their marketing approach to present products according to an agreed classification of indexes

Local authorities are recognized as non professional investors

Reinforced information duties in favor of local authorities as regards the risks attached to structured products

Reinforced advise duties in favor of local authorities

Information and advise duties: How to tackle « misselling » ? 13

Main commitments of local authorities under the GISSLER Charter:

STRUCTURED LOANS ENTERED INTO BETWEEN LOCAL AUTHORITIES AND

CREDIT INSTITUTIONS

Reinforced transparency in respect of decisions regarding borrowing and debt policies of local authorities

Main features of borrowing and debt policies provided to the deliberative body of local authorities by the executive committee of such authorities

Such provision shall enable the deliberative body to define borrowing and debt policies the executive committee will implement

Reinforced financial information in respect of structured products subscribed by local authorities

Detailed presentation of the structure and outstandings of the structured products and the type of underlying indexes by the executive committee of local authorities

Such presentation shall be provided to the deliberative body of such authorities

Information and advise duties: How to tackle « misselling » ? 14

Do MiFID requirements apply to structured products entered into between local authorities and credit institutions?

STRUCTURED LOANS ENTERED INTO BETWEEN LOCAL AUTHORITIES AND

CREDIT INSTITUTIONS

MiFID requirements apply to financial contracts (contrats financiers such as swaps, etc…) entered into (in parallel of loans) between local authorities and credit institutions (as the case may be, local authorities will be considered as non professional clients, save in the event that they have chosen to be deemed as professional clients)

MiFID requirements do not apply to structured loans entered into between local authorities and credit institutions

(In its Feedback Statement dated 3 November 2009 on MiFID complex and non complex financial instruments, CESR provides that MiFID requirements do not apply to loans as they are not MiFID financial instruments)

Information and advise duties: How to tackle « misselling » ? 15

Features of PRIPs:

THE PACKAGED RETAIL INVESTMENT PRODUCTS (PRIPs)

They provide retail investors with easy access to financial markets

They offer exposure to underlying financial assets, but in packaged forms which modify that exposure compared with direct holdings

Their primary function is capital accumulation, although some may provide capital protection

They are generally designed with the mid- to long-term retail market in mind

They are marketed directly to retail investors, although they may also be sold to sophisticated investors

Information and advise duties: How to tackle « misselling » ? 16

Examples of PRIPs

THE PACKAGED RETAIL INVESTMENT PRODUCTS (PRIPs)

Investments packaged as life insurance policies

In unit-linked life insurance policies (assurance-vie en unité de compte), a portion of the premium is used to purchase life cover (the sum insured) with the balance invested in a fund such as a UCITS

The return on the policy is linked to the performance of the funds

As opposed to traditional life insurance products, unit-linked policies usually do not guarantee the payment of a determined financial amount in particular in the case of death / survival, but instead an amount which is a multiple of the market value of one or several units. Therefore, by definition, the policy holder bears the investment risk

Information and advise duties: How to tackle « misselling » ? 17

Examples of PRIPs

THE PACKAGED RETAIL INVESTMENT PRODUCTS (PRIPs)

Structured term deposits

Structured term deposits (dépôts à terme structurés) offer a combination of a term deposit with an embedded option or an interest rate structure

They are designed to achieve a specific payoff profile (profil de rendement), which they achieve through transactions in derivatives such as interest rate and currency options

Other examples:

Investment (or mutual) funds

Retail structured securities

Information and advise duties: How to tackle « misselling » ? 18

PRIPs: MiFID financial instruments ?

THE PACKAGED RETAIL INVESTMENT PRODUCTS (PRIPs)

In its feedback statement dated 3 November 2009 on MiFID complex and non complex financial instruments, CESR provides that the MiFID requirements do not apply to deposits or life insurance products as they are not MiFID financial instruments

The Commission of the European Communities considers that the appropriate approach is to apply the same legislative requirements across all sales of PRIPs, irrespective of the distribution channel employed

According to the Commission of the European Communities:

The MiFID provisions on conduct of business (including information and advise duties of investment services providers in favor of investors) and conflicts of interests offer a benchmark for such requirements

The extension of these measures to all PRIPs could be achieved by creating a new directive aimed at extending the scope of the relevant MiFID provisions so that they apply to all entities selling the relevant products

(Update on Commission work on PRIPs dated 16 December 2009 and Communication from the Commission to the European Parliament and the Council on PRIPs dated 30 April 2009)

Information and advise duties: How to tackle « misselling » ? 19

PRIPs: MiFID financial instruments ?

THE PACKAGED RETAIL INVESTMENT PRODUCTS (PRIPs)

Legal issues arising in France as regards life insurance products

Ordinance n° 2009-106 dated 30 January 2009 on life insurance products marketing and on mutual contingency and insurance transactions:

• Information duties applicable to life insurance providers

• Advise duties applicable to life insurance providers

European insurance community has expressed material concerns in respect of the application of MiFID to life insurance products marketing

• MiDIF requirements are not adapted to life insurance products (peculiarly, the classification of clients)

Information and advise duties: How to tackle « misselling » ? 20

Deletré Report 2: Introduction

A FRENCH APPROACH UNDER CONSIDERATION: THE DELETRÉ REPORT

2

The Deletré Report 2 dated July 2009 on the supervision of professional obligations towards customers in the financial industry deals with the whole of financial, banking and insurance products and services

Some recommendations of the Deletré Report 2 had been submitted to public consultation until 31 december 2009

Main purpose of the Deletré Report 2: implementation of a procedure aiming at improving customers’ protection and creating standardized rules in order to stop marketing practices non compliant with customers’ needs

Information and advise duties: How to tackle « misselling » ? 21

Main recommendations under the Deletré Report 2 submitted to public consultation

A FRENCH APPROACH UNDER CONSIDERATION: THE DELETRÉ REPORT

2

Introduction under French law of the loyalty principle (principe de loyauté) in the financial industry

Investment and banking services providers shall implement specific procedures so that they act loyally vis-à-vis customers

Supervision of such obligation by the French supervision authorities

Setting up of recommendations in order to implement the loyalty principle (such recommendations to be approved by the French supervisor, after consultation with customers and professionals)

Reinforced supervision of investment and banking services providers by professional associations which represent those providers (provided that such associations are authorized and supervised by the French supervision authorities in the financial industry)

Information and advise duties: How to tackle « misselling » ? 22

Main recommendations under the Deletré Report 2 submitted to public consultation

A FRENCH APPROACH UNDER CONSIDERATION: THE DELETRÉ REPORT

2

Burden of proof placed on the investment and banking services providers

Investment and banking services providers need to prove that they have acted loyally vis-à-vis customers

This implies relevant traceability system as regards due diligences conducted by such providers

The French Banking community has expressed material concerns in this respect

Information and advise duties: How to tackle « misselling » ? 23

Overview of the main requirements which may apply to products providers in the future: The approach in Asia

The approach in Asia represents a significant departure from the existing regime and imposes onerous additional obligations on the product providers. Similar to the proposals developed by the Committee of European Securities Regulators (CESR) and the “TCF” approach of the UK Financial Services Authority (FSA), it appears that product providers will, in the future, be required to:

ensure that products - covering all elements of design - are appropriate for the target market, given the risk tolerance and preference of that target market, and communicate this to distributors

provide enough information to the distributors to enable the distributors adequately to assess suitability for their customers

CONCLUSION

Information and advise duties: How to tackle « misselling » ? 24

Overview of the main requirements which may apply to products providers in the future: The approach in Asia

consider the distribution of the total gross investment returns of the product, split between the different stakeholders in the product and whether this distribution is fair, particularly from the investors’ perspective

ensure all relevant risks – market, liquidity, counterparty – are accurately identified and stress tested during the product design process

state clearly key product risks and assess these against prevailing market conditions

assess continually any risks posed to the product before and after the sale, and alert investors if contingency action needs to be taken

act with due care and diligence when passing on promotions which the product providers have created to the distributors

ensure that systems and controls offer an effective framework for risk management in a range of market conditions

CONCLUSION

Information and advise duties: How to tackle « misselling » ? 25

Some practical points from an Asian perspective

Issues to look for

Product v client suitability

Documentation of client profile

Refreshment of profile: requirements of the Code

Record of suitability assessment / recommendations made

Client sign-offs of profile

Audit trail of communications / correspondence with client

Language of account documentation

Ongoing self-assessments

CONCLUSION