Embed Size (px)

Citation preview

Water Monitoring Report2017–18

May 2019

ISBN 978 1 920702 05 2

Australian Competition and Consumer Commission 23 Marcus Clarke Street, Canberra, Australian Capital Territory, 2601

© Commonwealth of Australia 2019

This work is copyright. In addition to any use permitted under the Copyright Act 1968, all material contained within this work is provided under a Creative Commons Attribution 3.0 Australia licence, with the exception of:

� the Commonwealth Coat of Arms

� the ACCC and AER logos

� any illustration, diagram, photograph or graphic over which the Australian Competition and Consumer Commission does not hold copyright, but which may be part of or contained within this publication.

The details of the relevant licence conditions are available on the Creative Commons website, as is the full legal code for the CC BY 3.0 AU licence.

Requests and inquiries concerning reproduction and rights should be addressed to the Director, Content and Digital Services, ACCC, GPO Box 3131, Canberra ACT 2601.

Important notice

The information in this publication is for general guidance only. It does not constitute legal or other professional advice, and should not be relied on as a statement of the law in any jurisdiction. Because it is intended only as a general guide, it may contain generalisations. You should obtain professional advice if you have any specific concern.

The ACCC has made every reasonable effort to provide current and accurate information, but it does not make any guarantees regarding the accuracy, currency or completeness of that information.

Parties who wish to re-publish or otherwise use the information in this publication must check this information for currency and accuracy prior to publication. This should be done prior to each publication edition, as ACCC guidance and relevant transitional legislation frequently change. Any queries parties have should be addressed to the Director, Content and Digital Services, ACCC, GPO Box 3131, Canberra ACT 2601.

ACCC 05/19_1522

www.accc.gov.au

Cover photo: Darling River, NSW March 2018

Source: iStockphoto

iiiWater monitoring report 2017–18

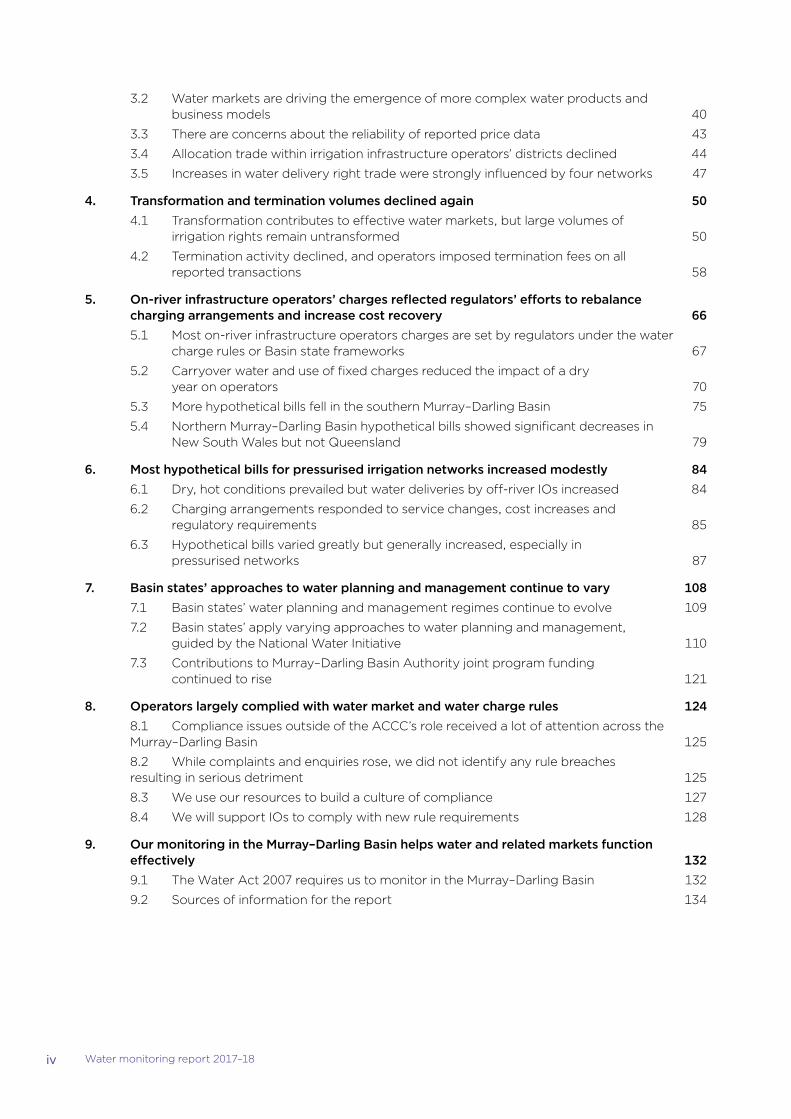

ContentsAbbreviations viii

Glossary xi

Key findings xvii

Summary xixDrought conditions began to emerge xix

Some areas experienced record prices for traded water entitlements xx

There was widespread debate and many reviews of water policy and governance arrangements in the Murray–Darling Basin xx

Water charge rules changes move forward xxi

Allocation trade declined xxi

Trade in water delivery rights remained low relative to total rights on issue xxii

A lower volume of irrigation rights was transformed xxii

And termination activity declined xxiii

Some on-river hypothetical bills increased while others decreased xxiv

Off-river hypothetical bills continued to increase for most networks xxv

There are significant differences between each Basin State’s water planning and management arrangements xxviii

Complaints increased slightly during 2017–18 but compliance with the water market and water charge rules is generally good xxix

1. Drought and water deliverability challenges loomed 21.1 Seasonal conditions were drier than in previous years 2

1.2 Water availability declined 3

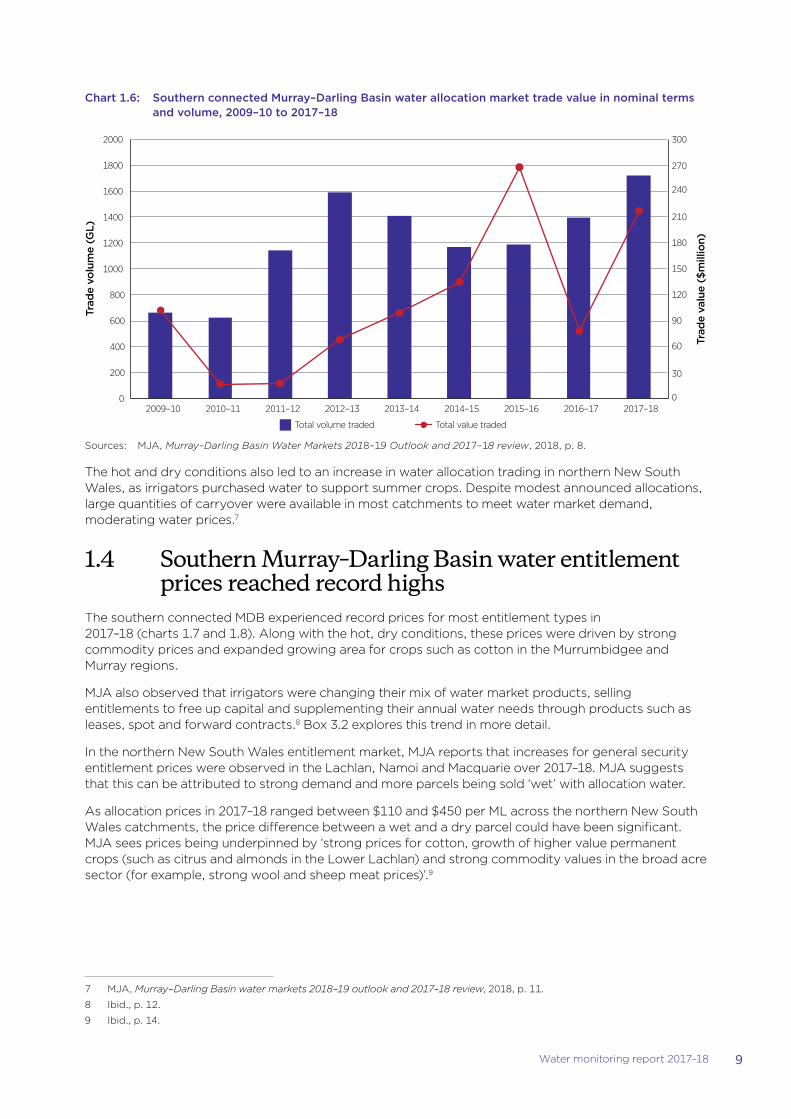

1.3 Most trading zones saw record water allocation trade volumes and higher prices 8

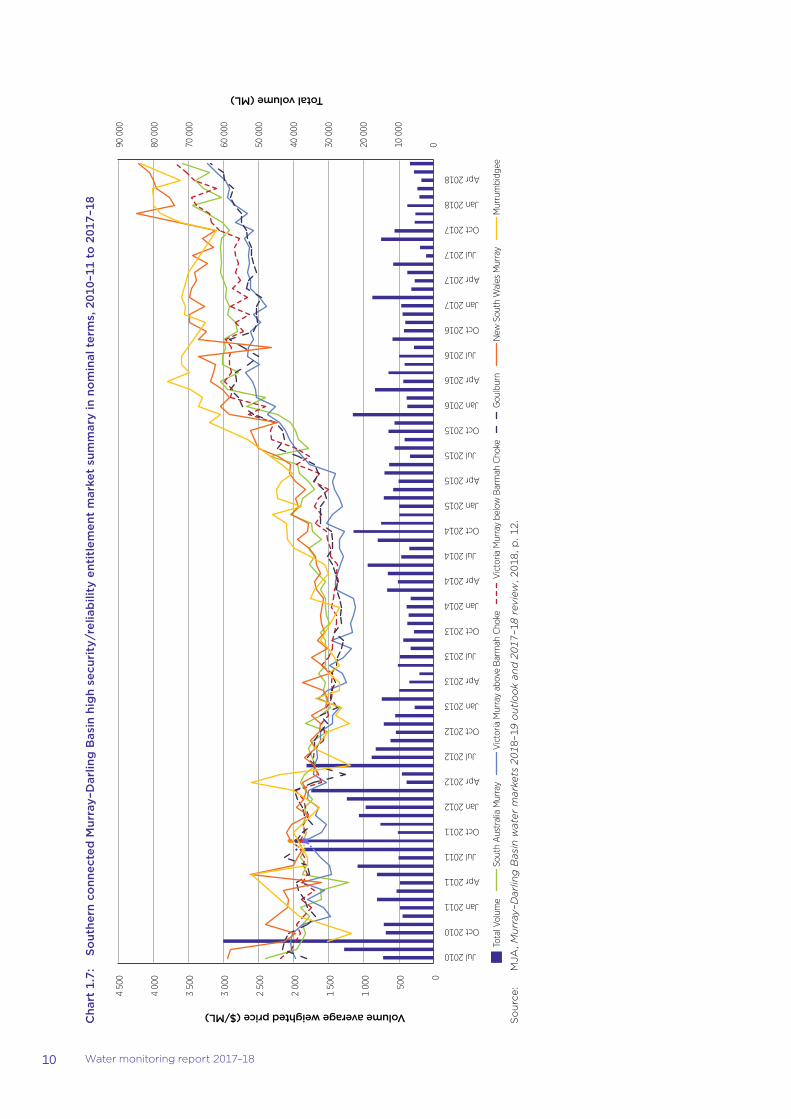

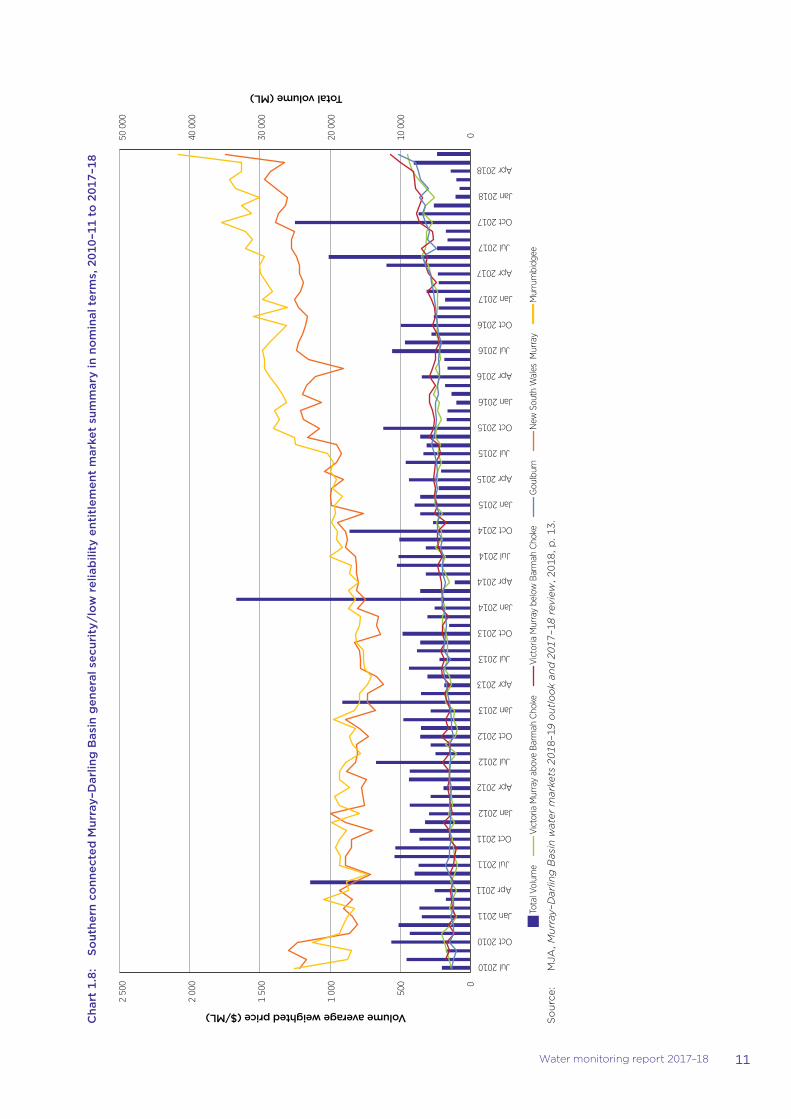

1.4 Southern Murray–Darling Basin water entitlement prices reached record highs 9

1.5 New South Wales introduced subsidies for fixed charges due to drought conditions 12

1.6 Energy prices remained a concern for irrigators and water infrastructure operators, particularly in pressurised systems 12

1.7 Changing cropping choices are placing a premium on high reliability water 13

1.8 Mass fish deaths in the Lower Darling in late 2018 and early 2019 increased pressure on governments and water managers 15

2. Murray–Darling Basin policy, legal and governance arrangements were widely reviewed and evaluated 202.1 Compliance concerns in New South Wales led to commitments to improve monitoring and enforcement across the Murray–Darling Basin 20

2.2 The Murray–Darling Basin Authority and Productivity Commission found issues with the Basin Plan’s impact and implementation 26

2.3 Other inquiries examined water governance, management and service delivery and recommended changes 30

2.4 The Australian Minister for Agriculture and Water Resources revised the water charge rules 34

3. Murray–Darling Basin water markets are growing, with potential for improvement 383.1 Murray–Darling Basin water market effectiveness has improved since 2007 but market functioning has room for improvement 39

iv Water monitoring report 2017–18

3.2 Water markets are driving the emergence of more complex water products and business models 40

3.3 There are concerns about the reliability of reported price data 43

3.4 Allocation trade within irrigation infrastructure operators’ districts declined 44

3.5 Increases in water delivery right trade were strongly influenced by four networks 47

4. Transformation and termination volumes declined again 504.1 Transformation contributes to effective water markets, but large volumes of irrigation rights remain untransformed 50

4.2 Termination activity declined, and operators imposed termination fees on all reported transactions 58

5. On-river infrastructure operators’ charges reflected regulators’ efforts to rebalance charging arrangements and increase cost recovery 665.1 Most on-river infrastructure operators charges are set by regulators under the water charge rules or Basin state frameworks 67

5.2 Carryover water and use of fixed charges reduced the impact of a dry year on operators 70

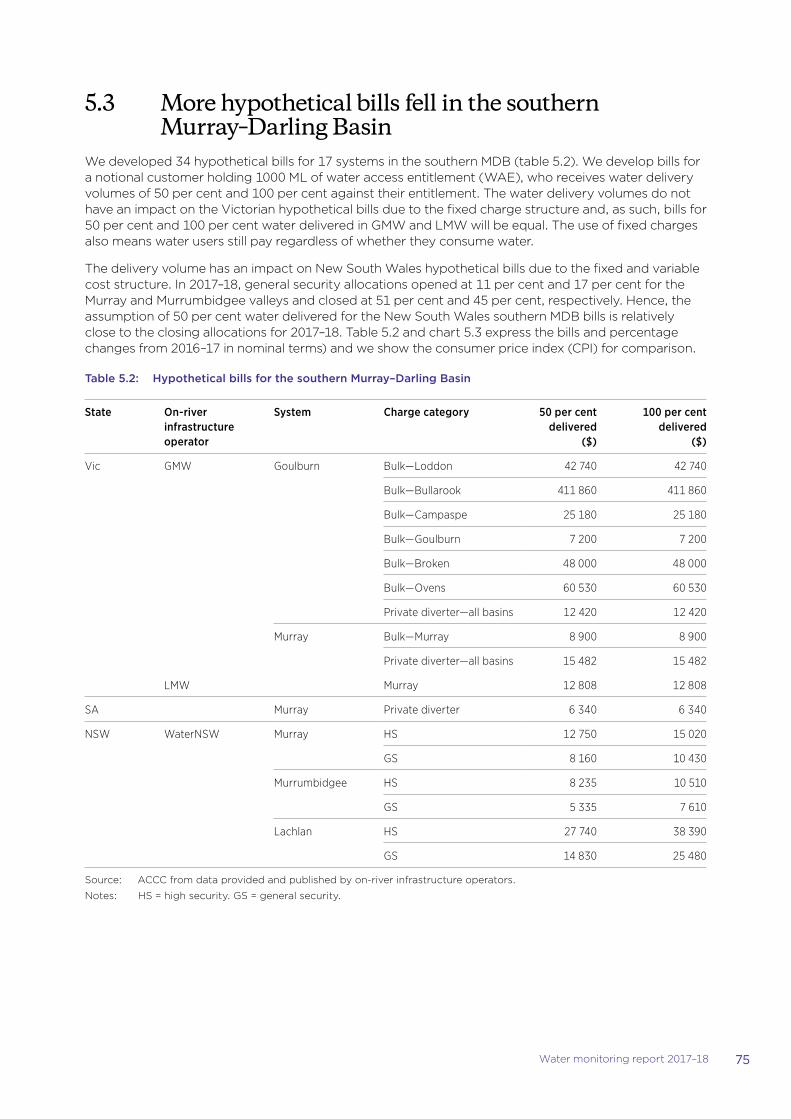

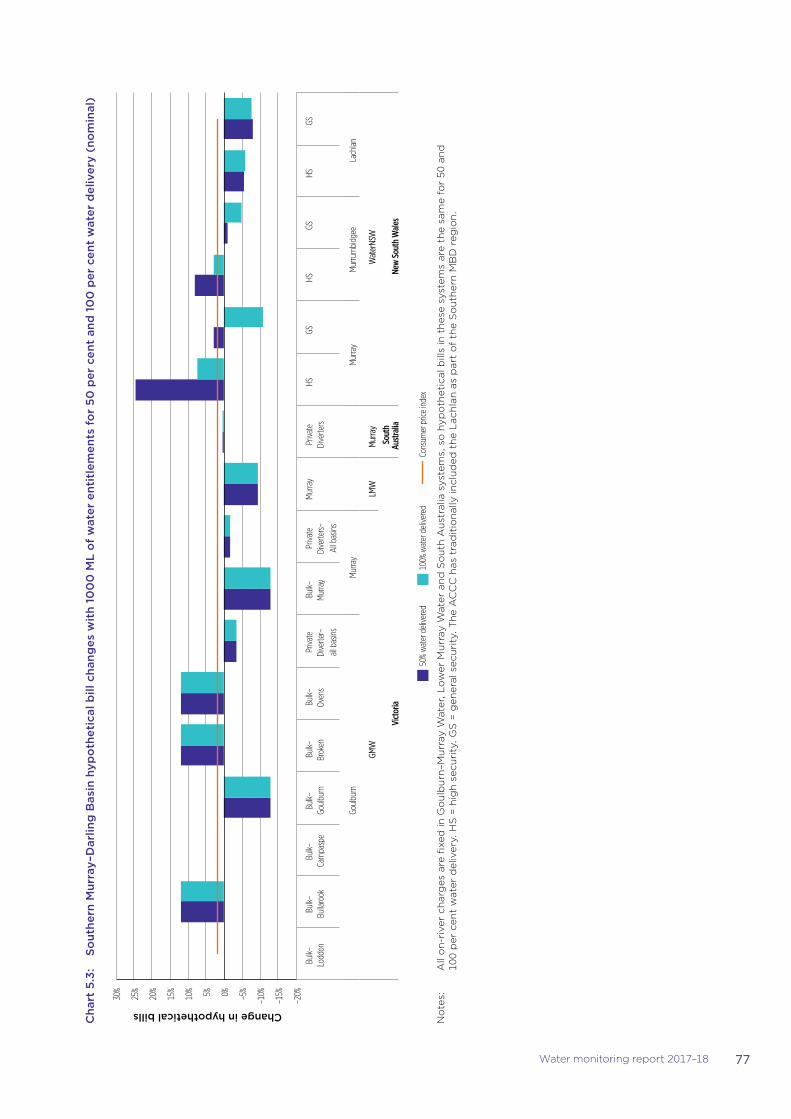

5.3 More hypothetical bills fell in the southern Murray–Darling Basin 75

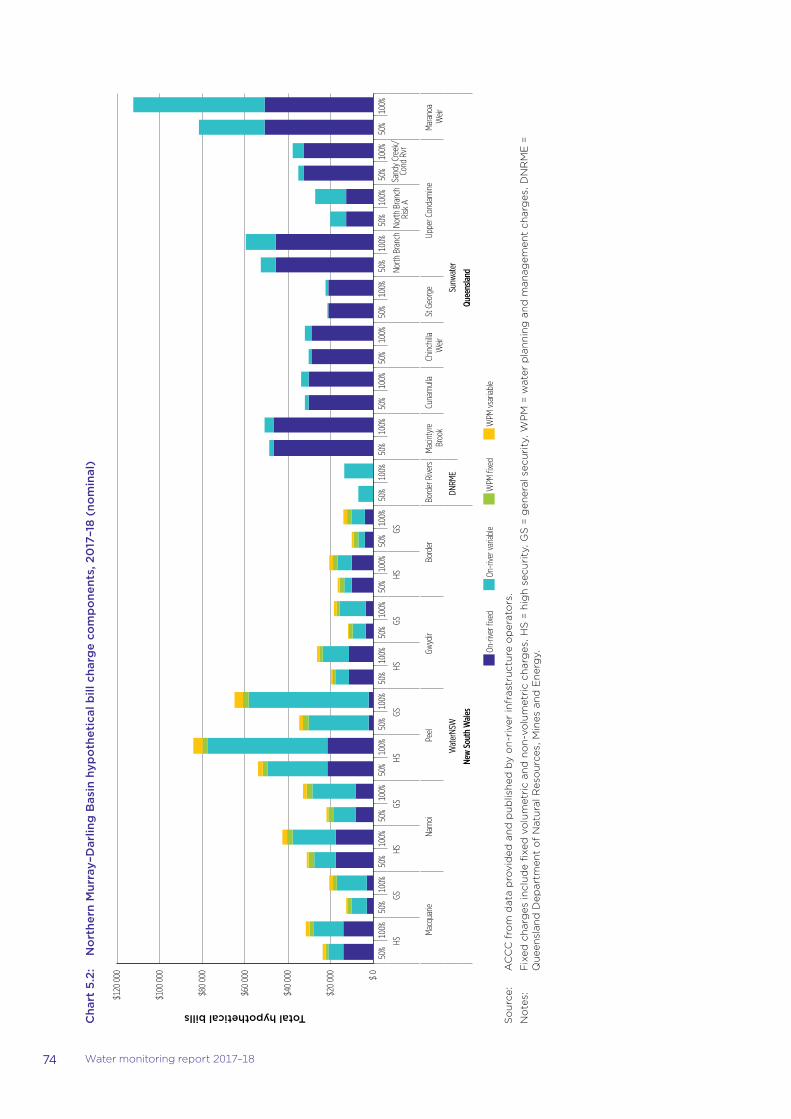

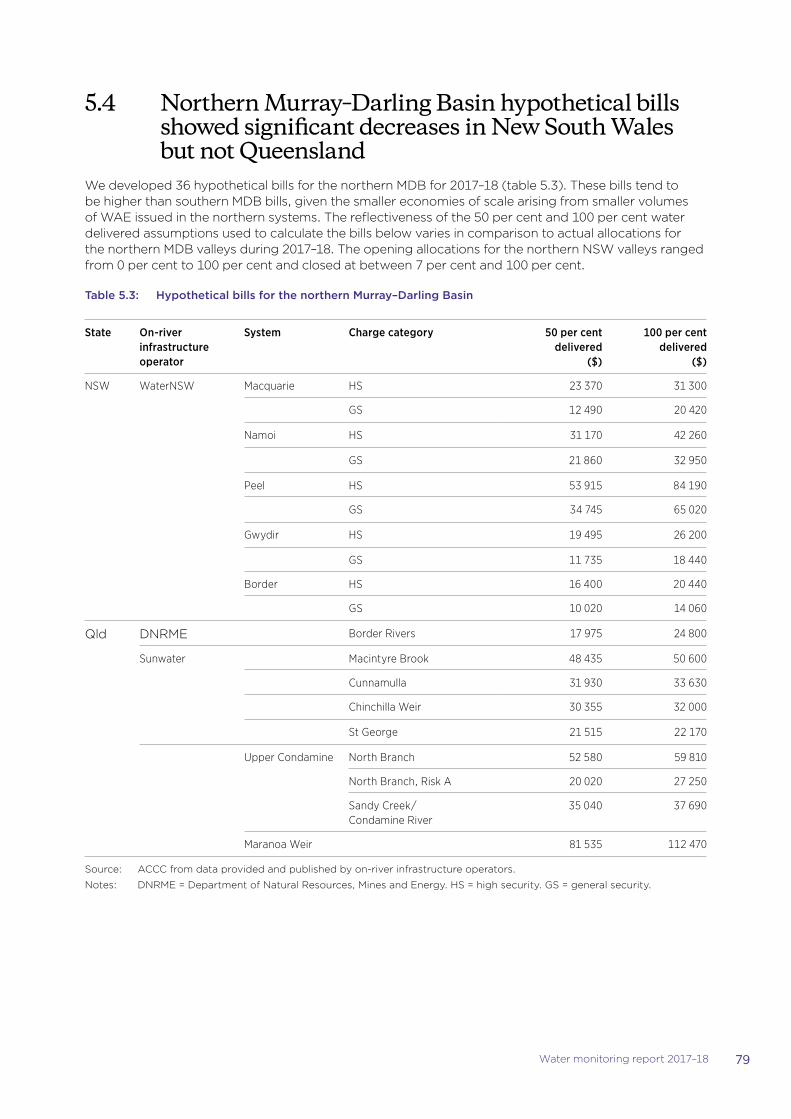

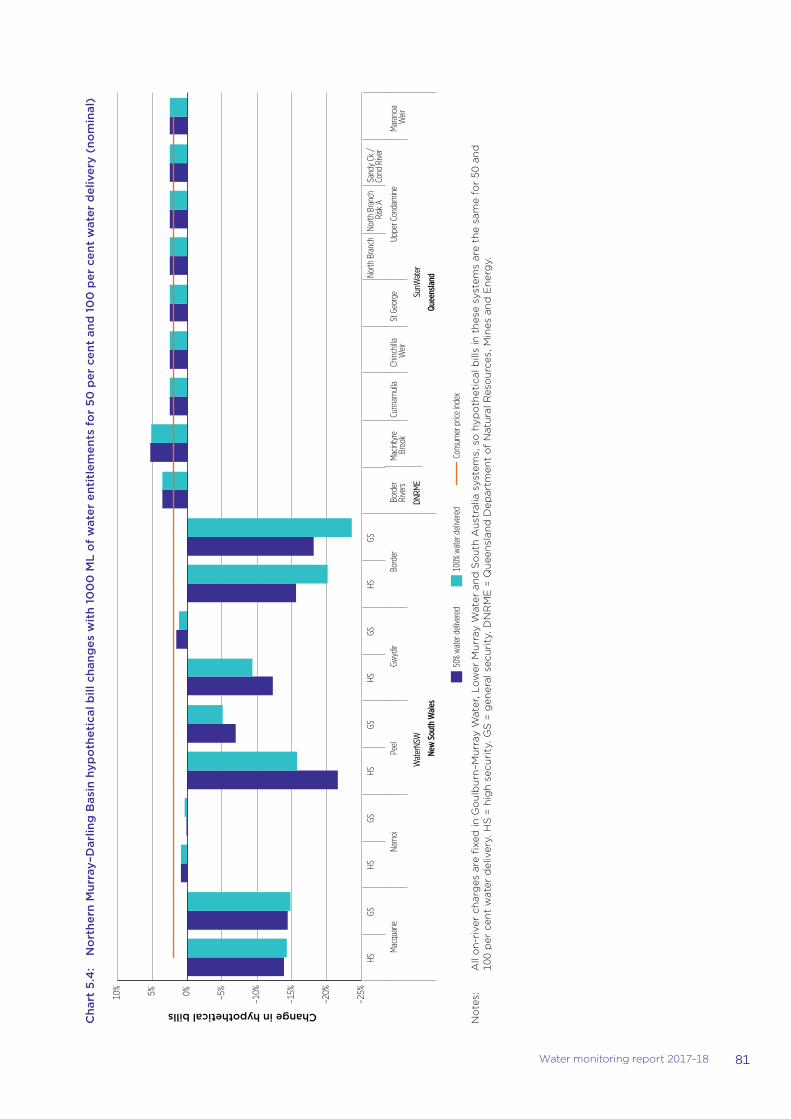

5.4 Northern Murray–Darling Basin hypothetical bills showed significant decreases in New South Wales but not Queensland 79

6. Most hypothetical bills for pressurised irrigation networks increased modestly 846.1 Dry, hot conditions prevailed but water deliveries by off-river IOs increased 84

6.2 Charging arrangements responded to service changes, cost increases and regulatory requirements 85

6.3 Hypothetical bills varied greatly but generally increased, especially in pressurised networks 87

7. Basin states’ approaches to water planning and management continue to vary 1087.1 Basin states’ water planning and management regimes continue to evolve 109

7.2 Basin states’ apply varying approaches to water planning and management, guided by the National Water Initiative 110

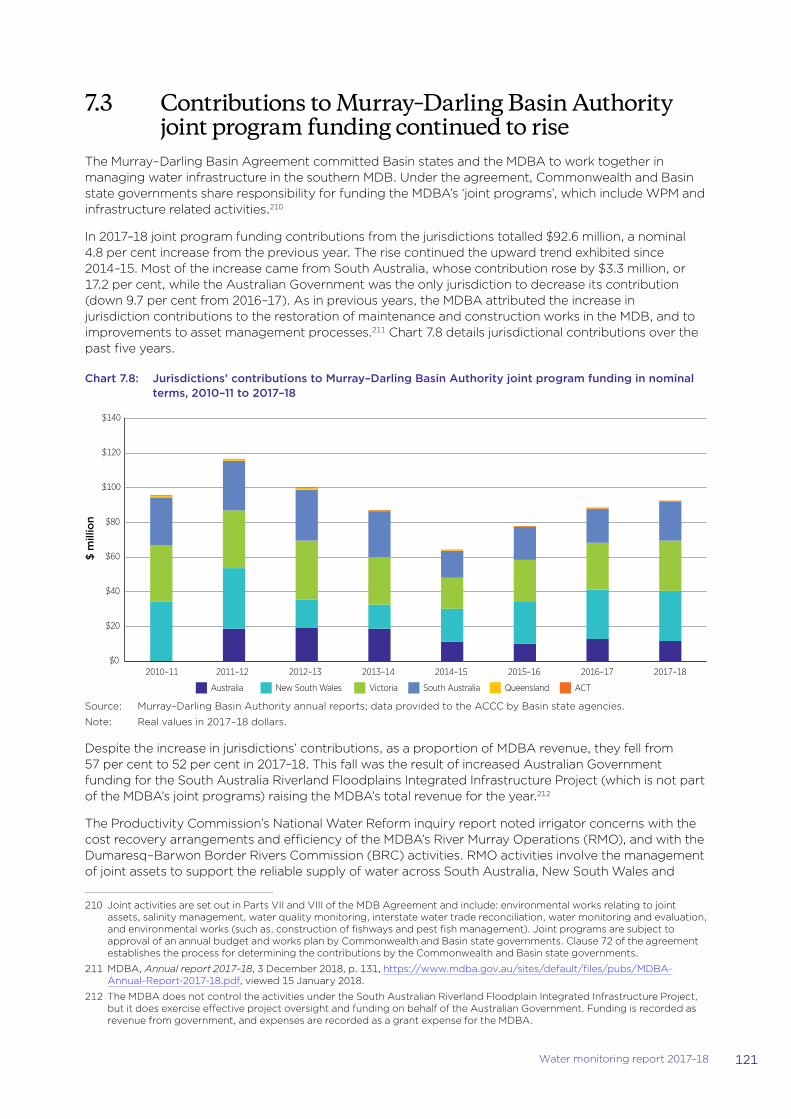

7.3 Contributions to Murray–Darling Basin Authority joint program funding continued to rise 121

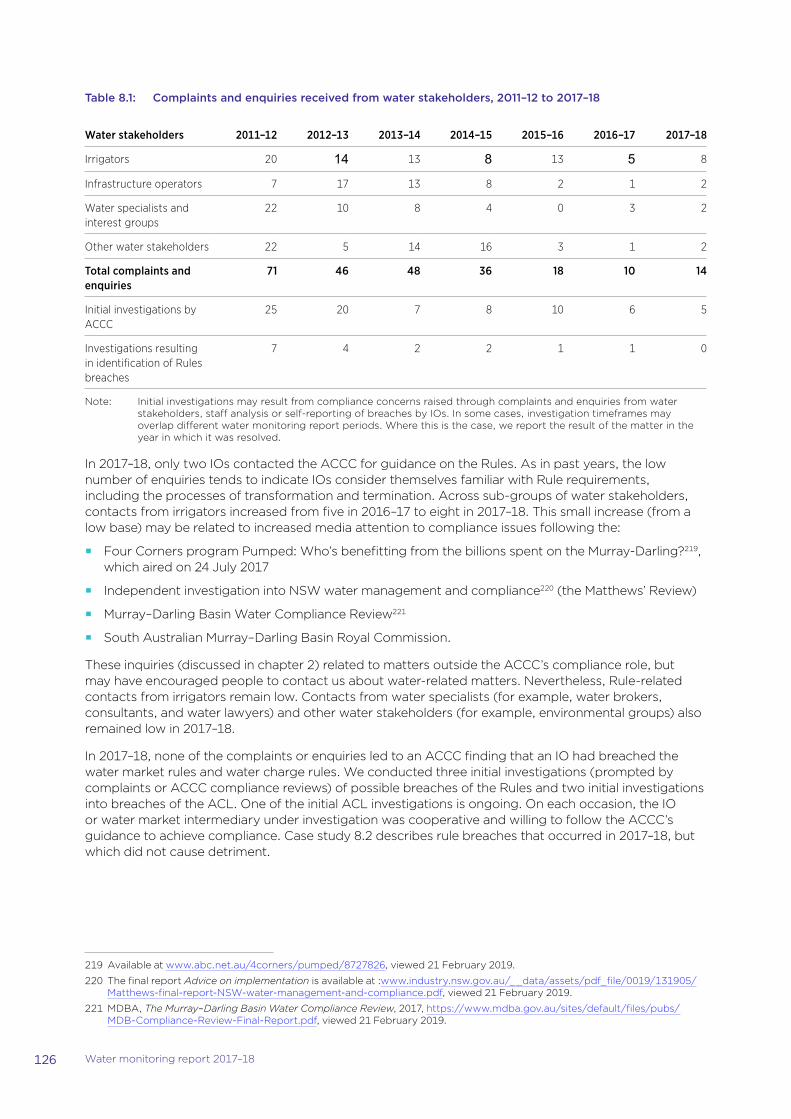

8. Operators largely complied with water market and water charge rules 1248.1 Compliance issues outside of the ACCC’s role received a lot of attention across the Murray–Darling Basin 125

8.2 While complaints and enquiries rose, we did not identify any rule breaches resulting in serious detriment 125

8.3 We use our resources to build a culture of compliance 127

8.4 We will support IOs to comply with new rule requirements 128

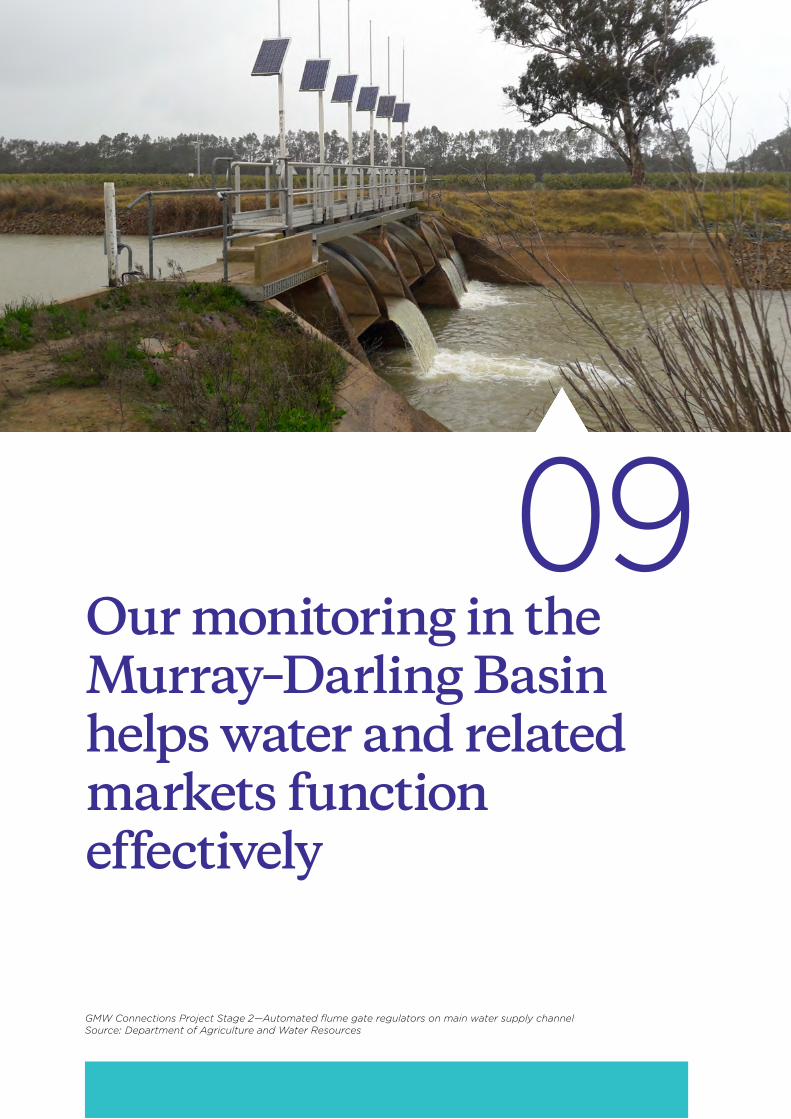

9. Our monitoring in the Murray–Darling Basin helps water and related markets function effectively 1329.1 The Water Act 2007 requires us to monitor in the Murray–Darling Basin 132

9.2 Sources of information for the report 134

vWater monitoring report 2017–18

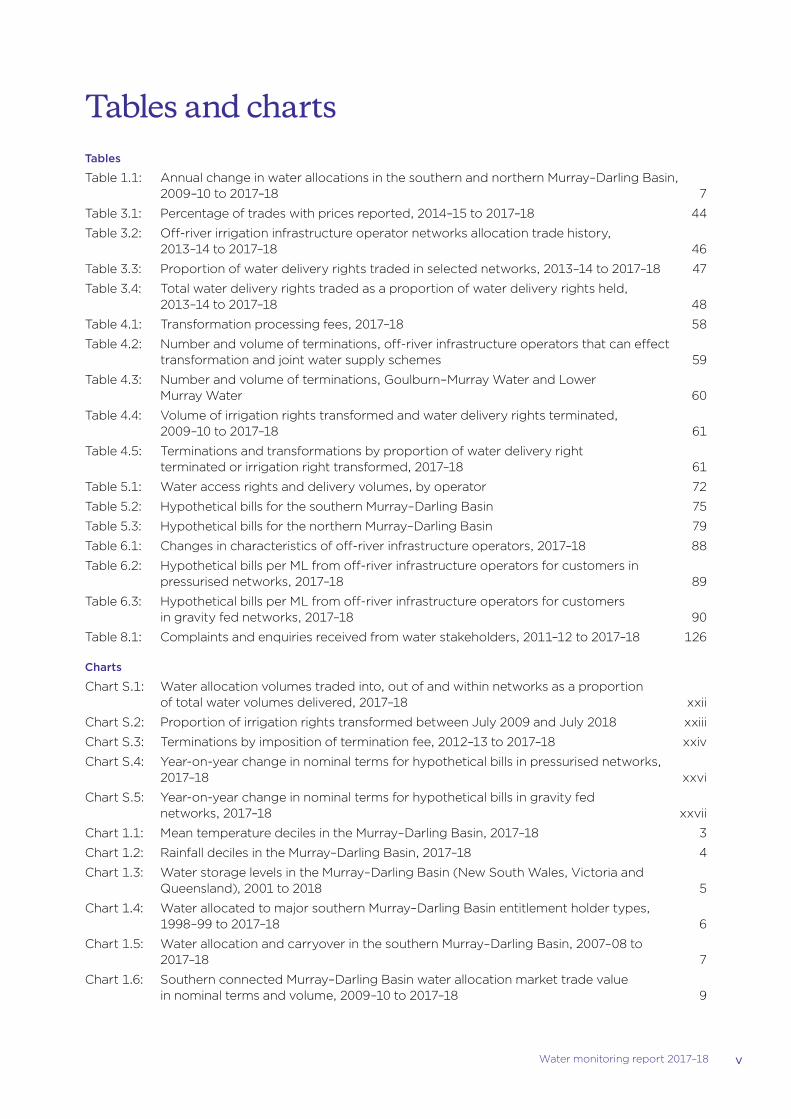

Tables and chartsTables

Table 1.1: Annual change in water allocations in the southern and northern Murray–Darling Basin, 2009–10 to 2017–18 7

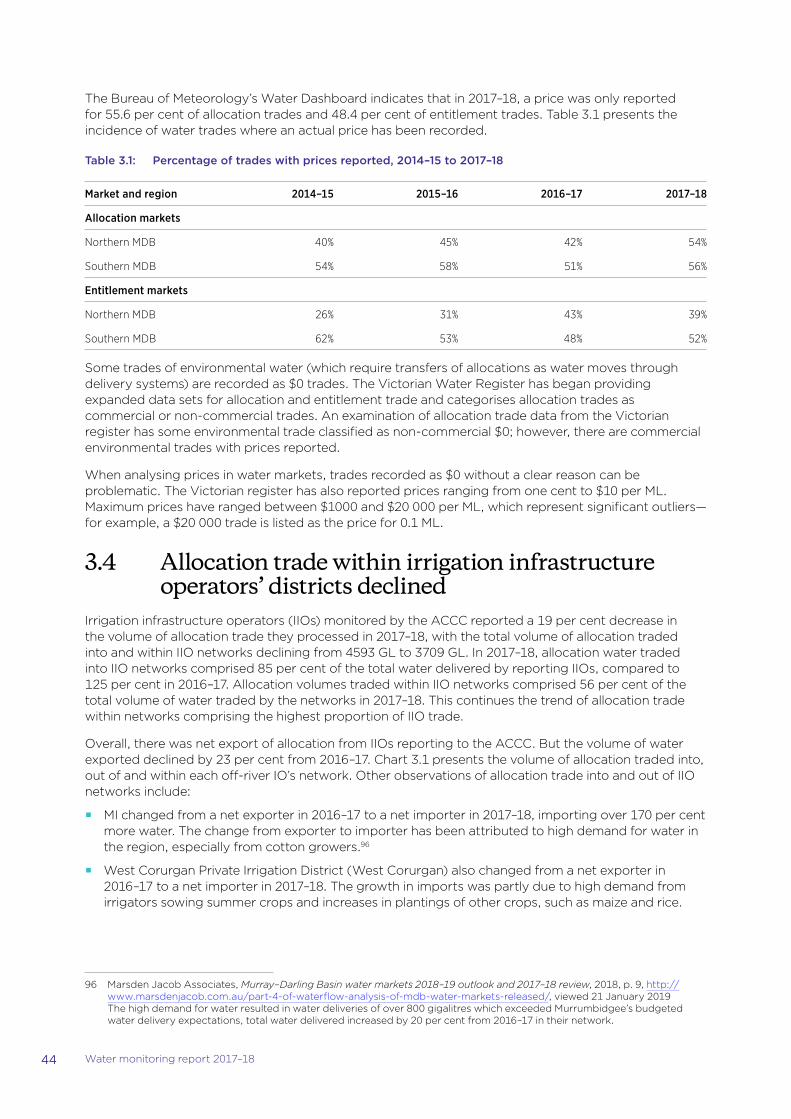

Table 3.1: Percentage of trades with prices reported, 2014–15 to 2017–18 44

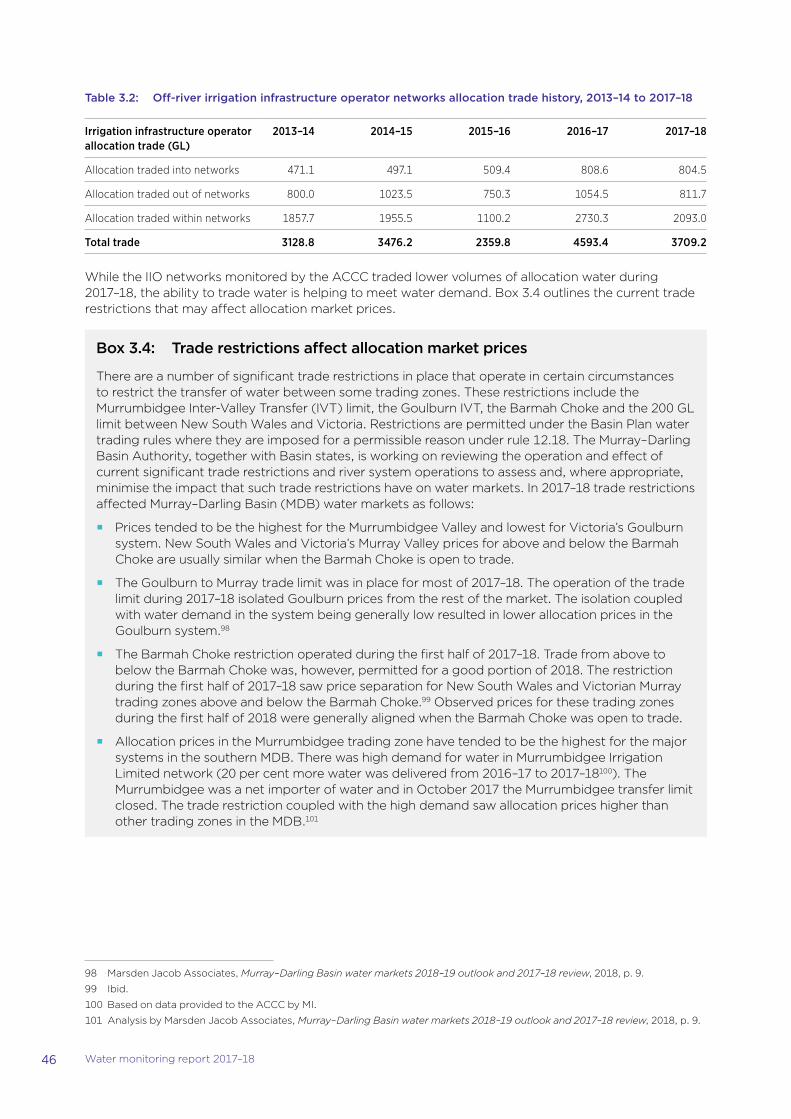

Table 3.2: Off-river irrigation infrastructure operator networks allocation trade history, 2013–14 to 2017–18 46

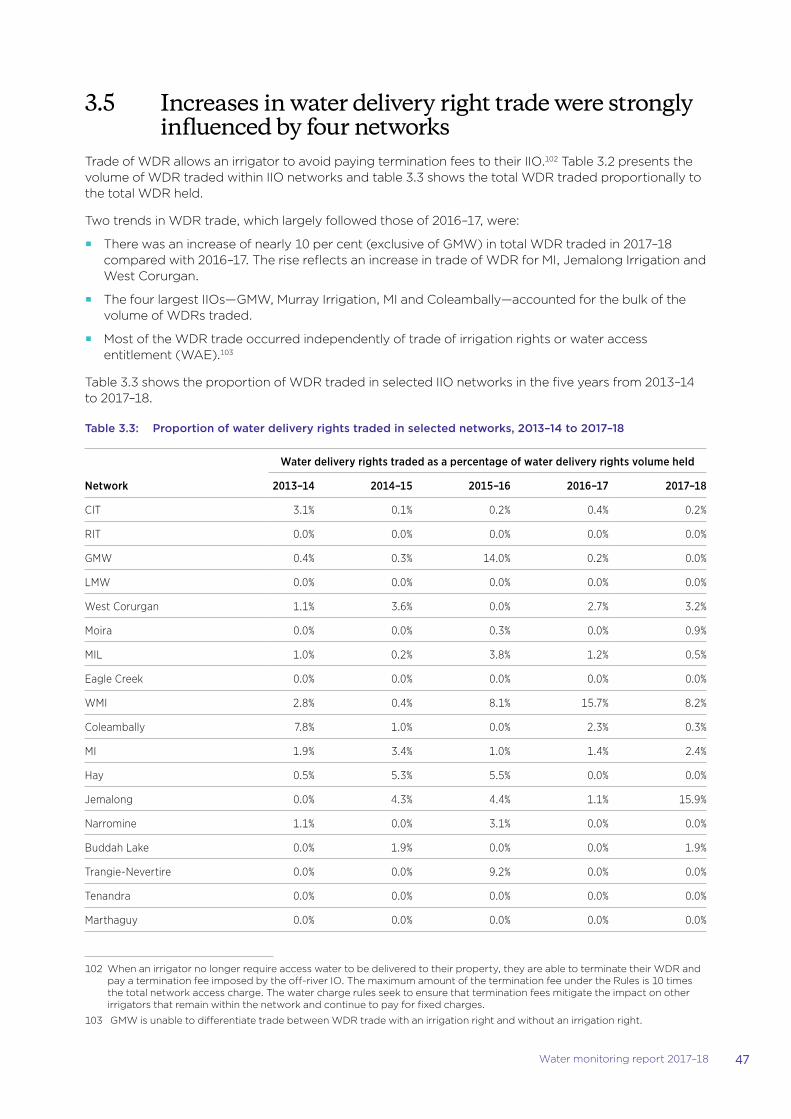

Table 3.3: Proportion of water delivery rights traded in selected networks, 2013–14 to 2017–18 47

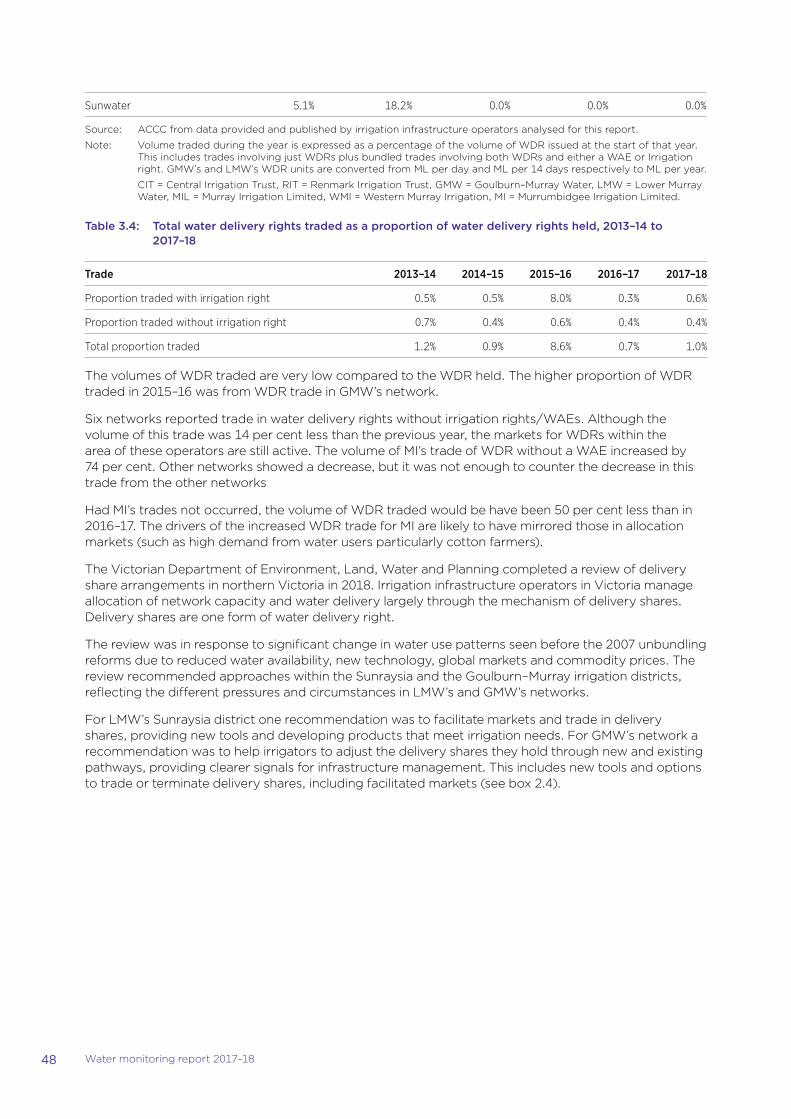

Table 3.4: Total water delivery rights traded as a proportion of water delivery rights held, 2013–14 to 2017–18 48

Table 4.1: Transformation processing fees, 2017–18 58

Table 4.2: Number and volume of terminations, off-river infrastructure operators that can effect transformation and joint water supply schemes 59

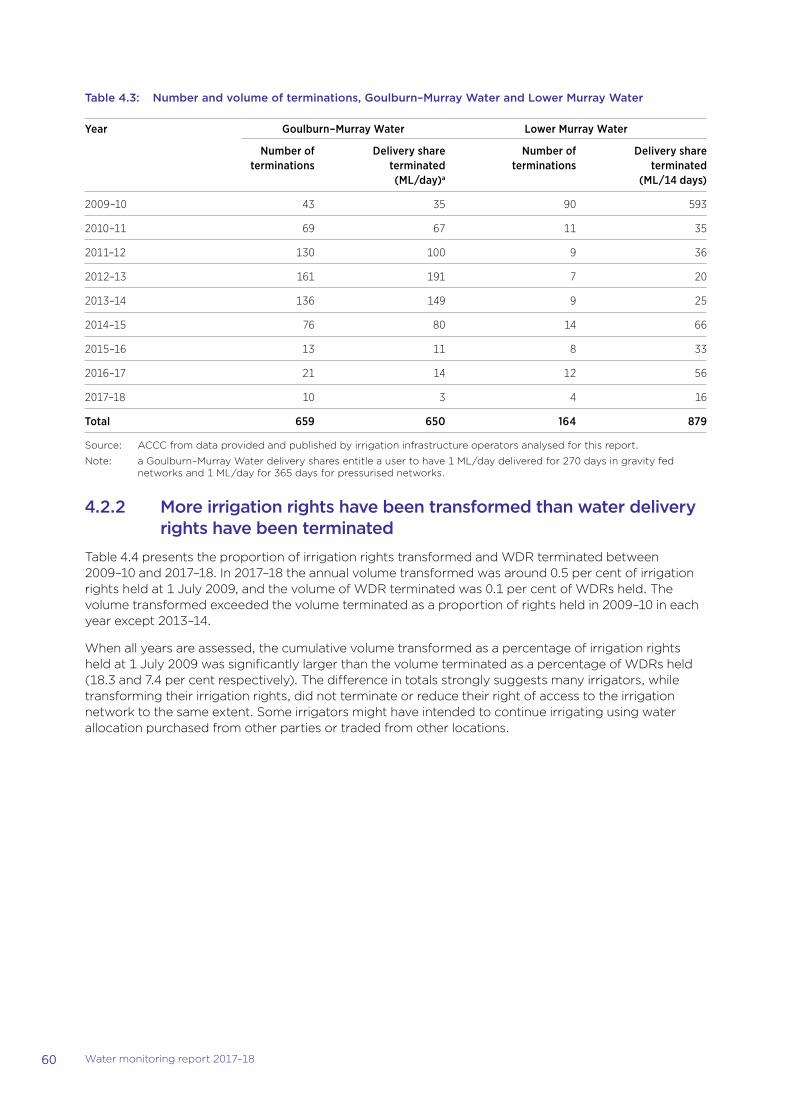

Table 4.3: Number and volume of terminations, Goulburn–Murray Water and Lower Murray Water 60

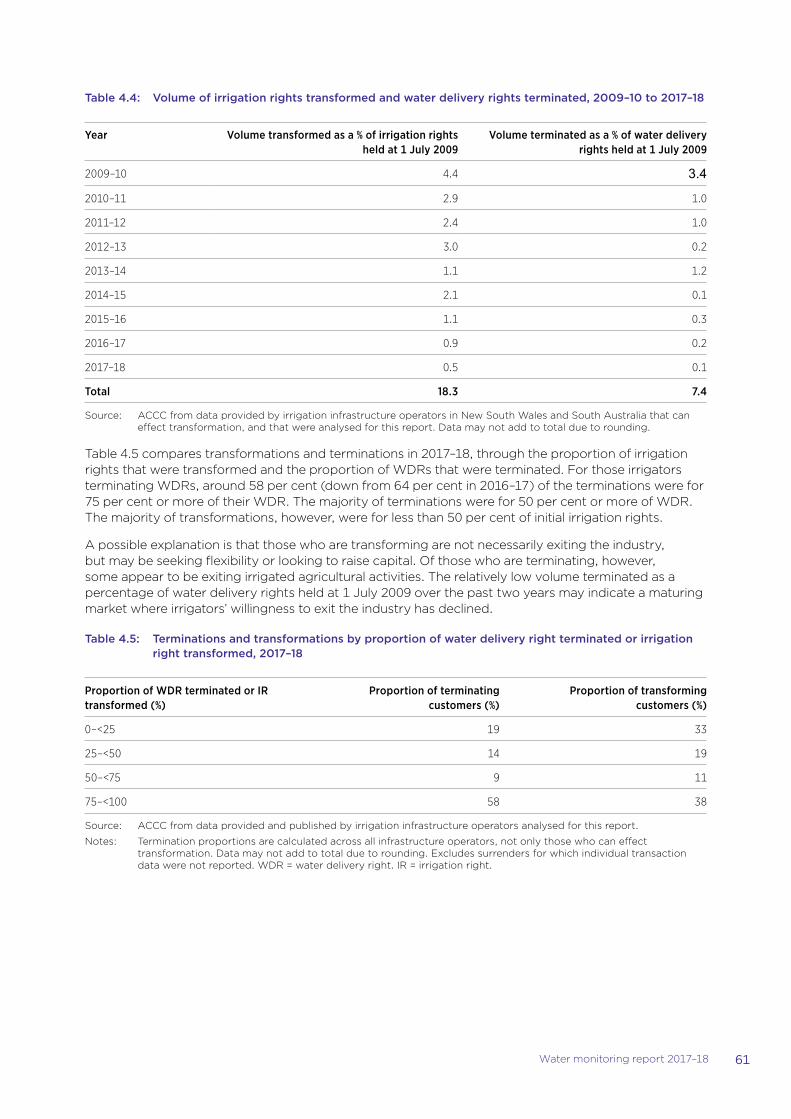

Table 4.4: Volume of irrigation rights transformed and water delivery rights terminated, 2009–10 to 2017–18 61

Table 4.5: Terminations and transformations by proportion of water delivery right terminated or irrigation right transformed, 2017–18 61

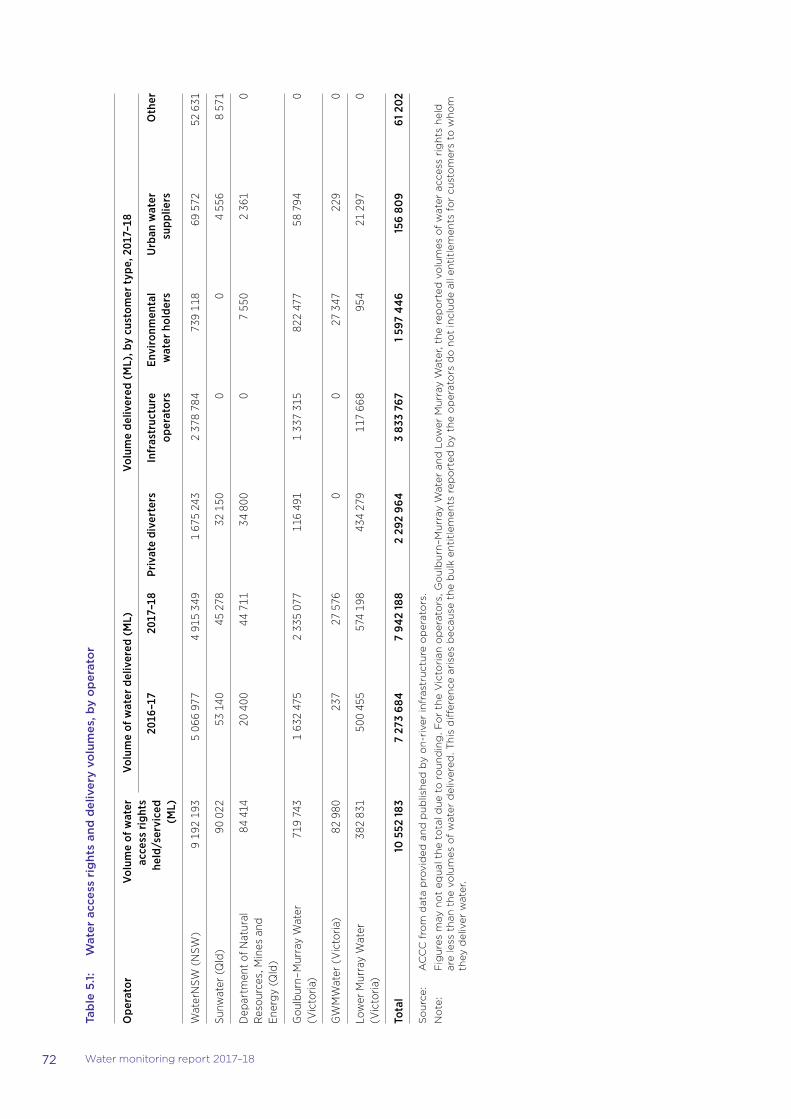

Table 5.1: Water access rights and delivery volumes, by operator 72

Table 5.2: Hypothetical bills for the southern Murray–Darling Basin 75

Table 5.3: Hypothetical bills for the northern Murray–Darling Basin 79

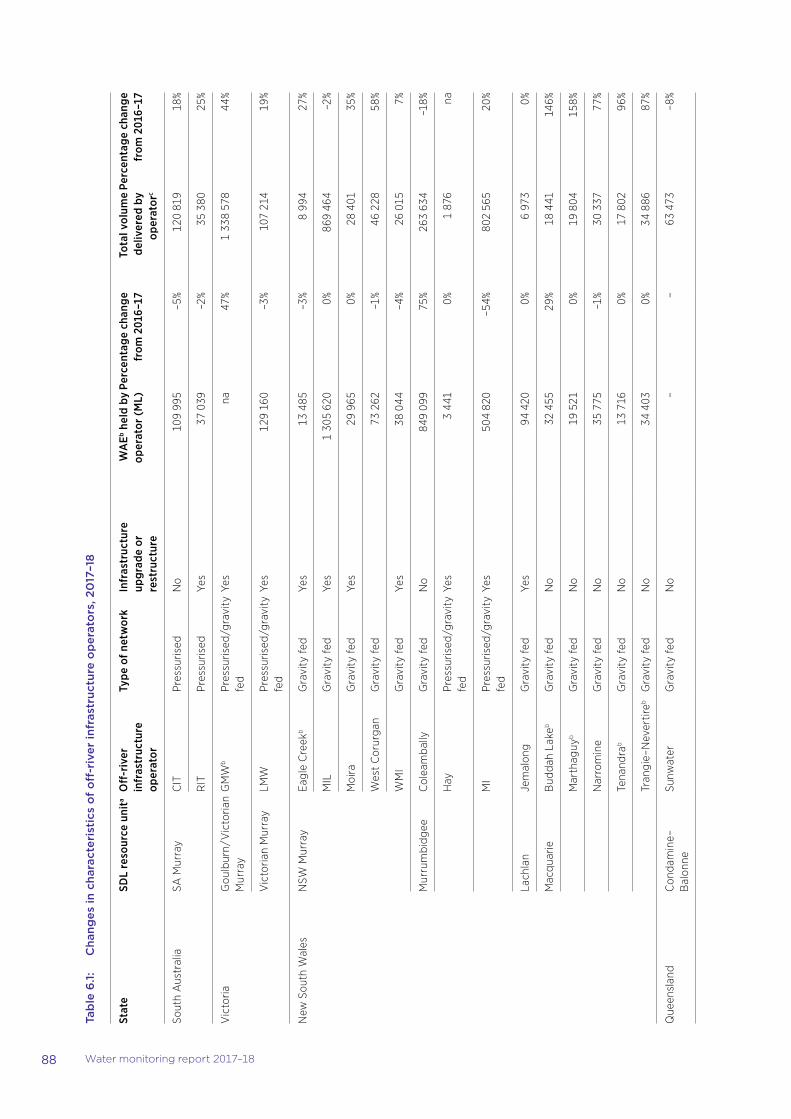

Table 6.1: Changes in characteristics of off-river infrastructure operators, 2017–18 88

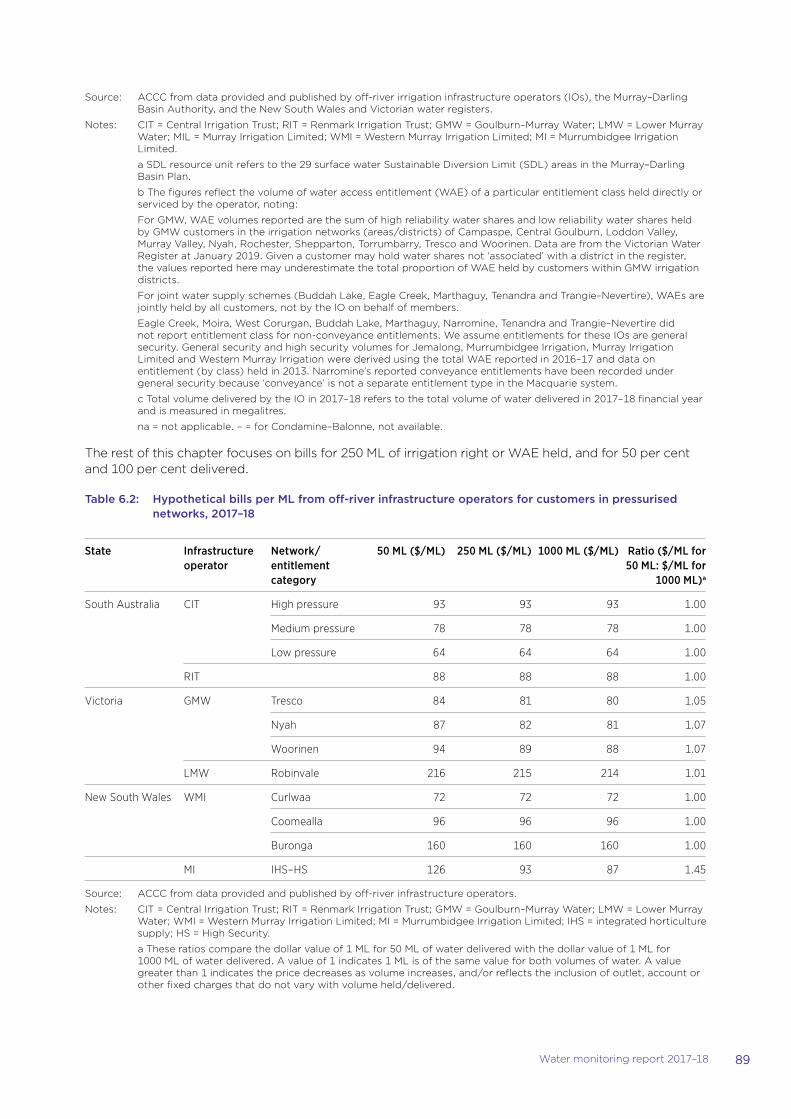

Table 6.2: Hypothetical bills per ML from off-river infrastructure operators for customers in pressurised networks, 2017–18 89

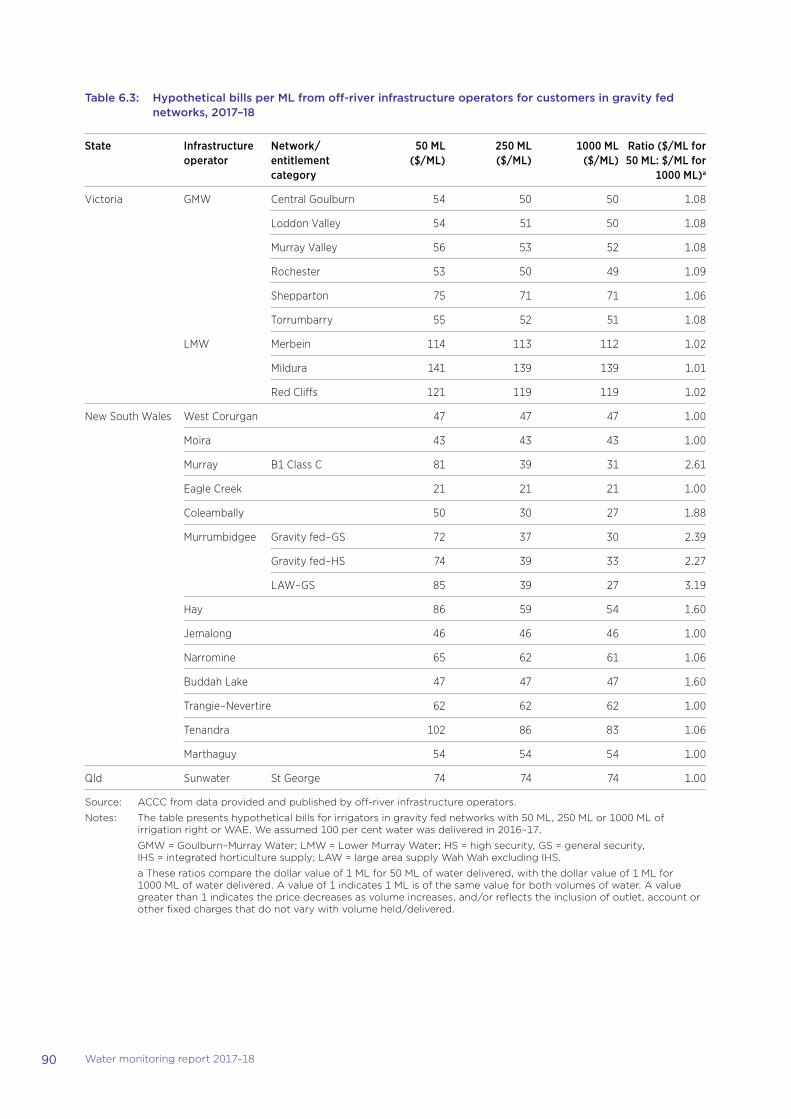

Table 6.3: Hypothetical bills per ML from off-river infrastructure operators for customers in gravity fed networks, 2017–18 90

Table 8.1: Complaints and enquiries received from water stakeholders, 2011–12 to 2017–18 126

Charts

Chart S.1: Water allocation volumes traded into, out of and within networks as a proportion of total water volumes delivered, 2017–18 xxii

Chart S.2: Proportion of irrigation rights transformed between July 2009 and July 2018 xxiii

Chart S.3: Terminations by imposition of termination fee, 2012–13 to 2017–18 xxiv

Chart S.4: Year-on-year change in nominal terms for hypothetical bills in pressurised networks, 2017–18 xxvi

Chart S.5: Year-on-year change in nominal terms for hypothetical bills in gravity fed networks, 2017–18 xxvii

Chart 1.1: Mean temperature deciles in the Murray–Darling Basin, 2017–18 3

Chart 1.2: Rainfall deciles in the Murray–Darling Basin, 2017–18 4

Chart 1.3: Water storage levels in the Murray–Darling Basin (New South Wales, Victoria and Queensland), 2001 to 2018 5

Chart 1.4: Water allocated to major southern Murray–Darling Basin entitlement holder types, 1998–99 to 2017–18 6

Chart 1.5: Water allocation and carryover in the southern Murray–Darling Basin, 2007–08 to 2017–18 7

Chart 1.6: Southern connected Murray–Darling Basin water allocation market trade value in nominal terms and volume, 2009–10 to 2017–18 9

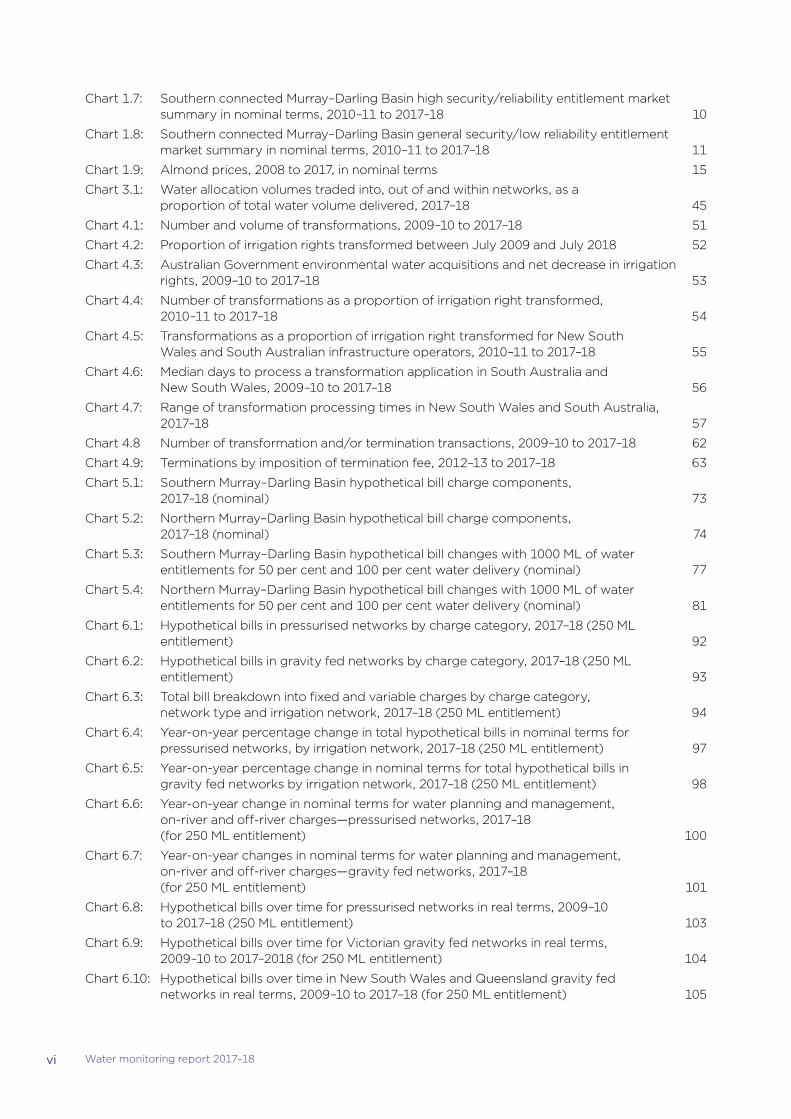

vi Water monitoring report 2017–18

Chart 1.7: Southern connected Murray–Darling Basin high security/reliability entitlement market summary in nominal terms, 2010–11 to 2017–18 10

Chart 1.8: Southern connected Murray–Darling Basin general security/low reliability entitlement market summary in nominal terms, 2010–11 to 2017–18 11

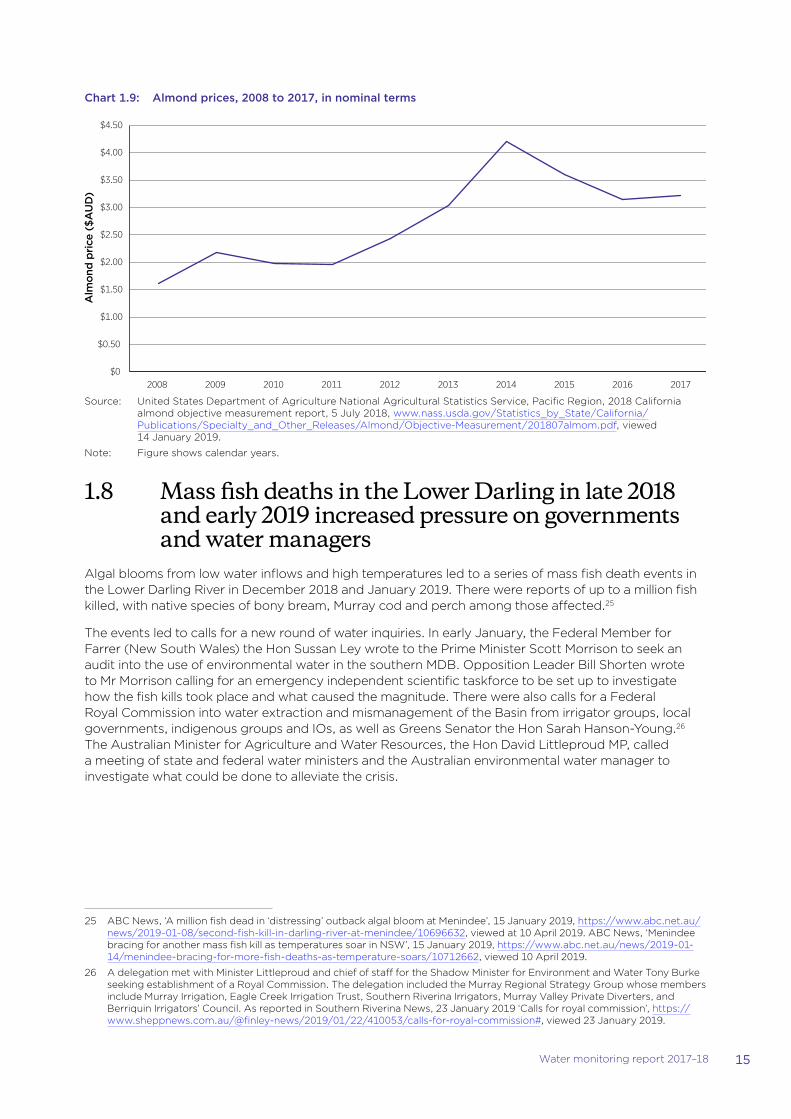

Chart 1.9: Almond prices, 2008 to 2017, in nominal terms 15

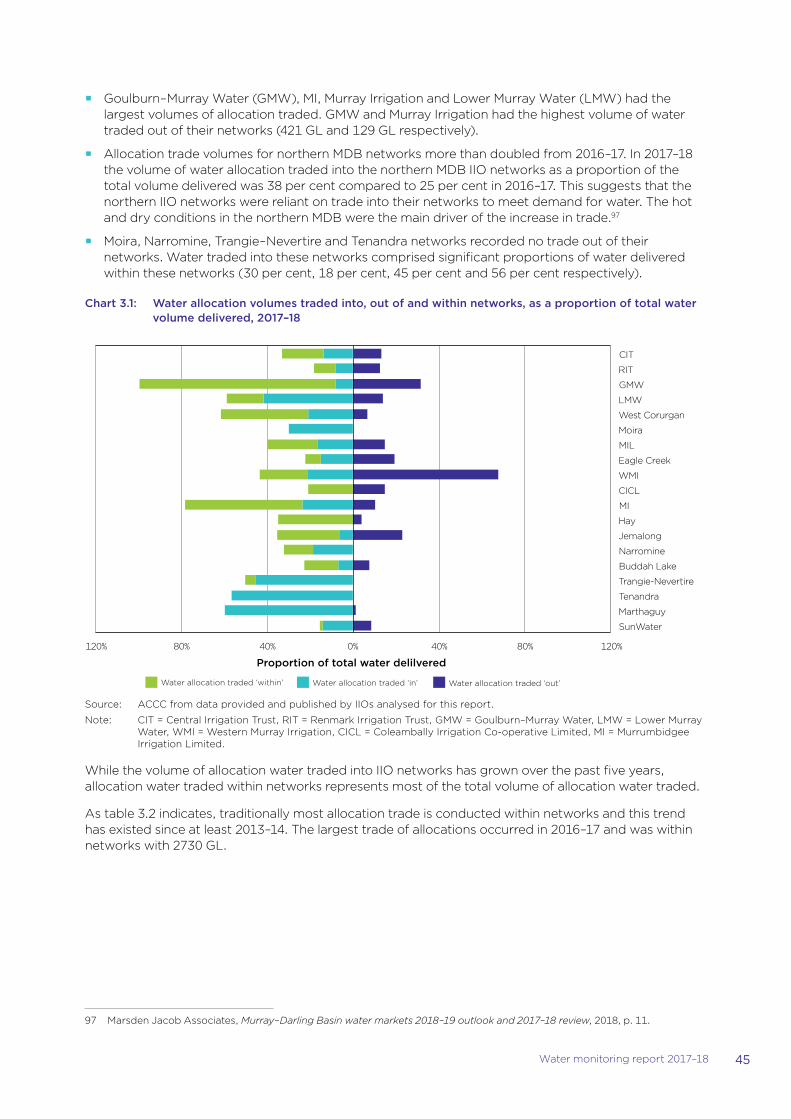

Chart 3.1: Water allocation volumes traded into, out of and within networks, as a proportion of total water volume delivered, 2017–18 45

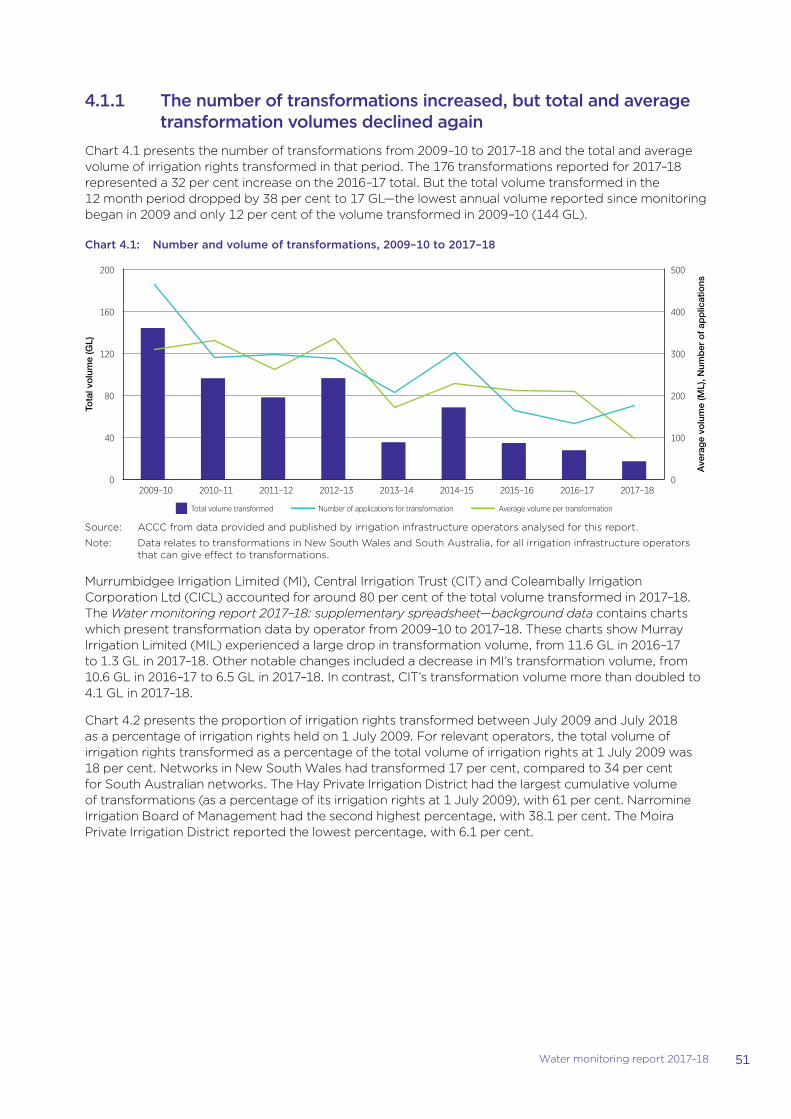

Chart 4.1: Number and volume of transformations, 2009–10 to 2017–18 51

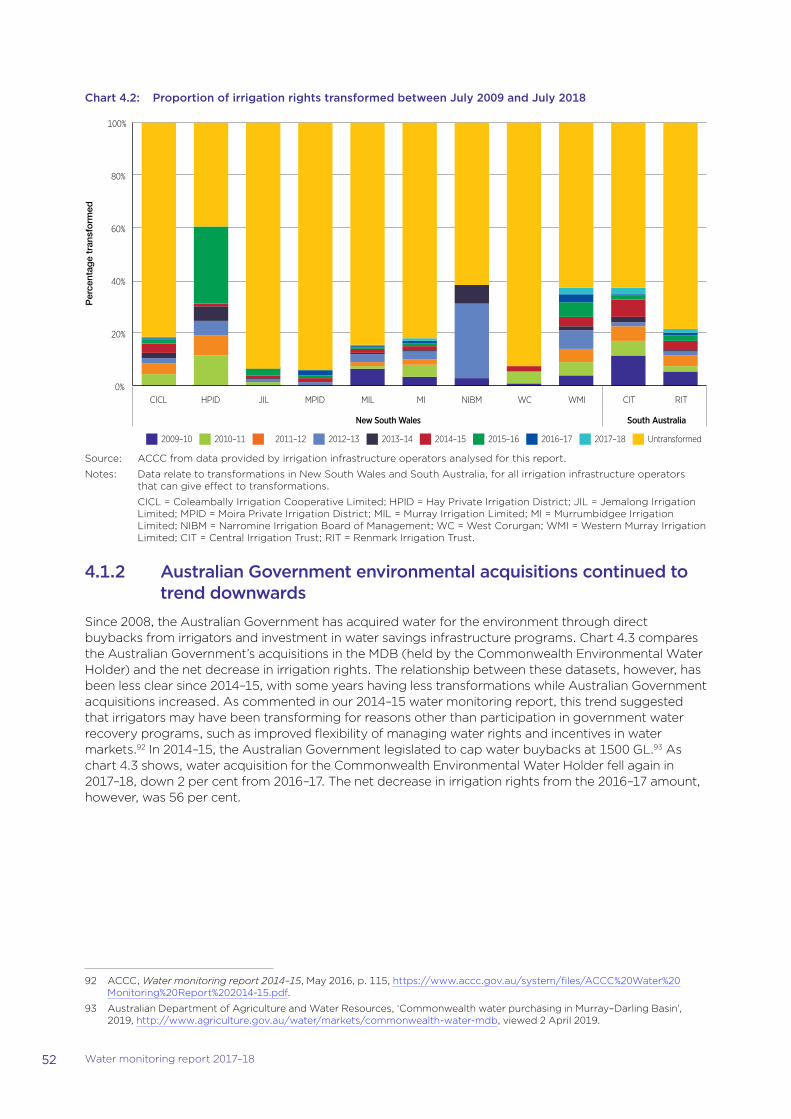

Chart 4.2: Proportion of irrigation rights transformed between July 2009 and July 2018 52

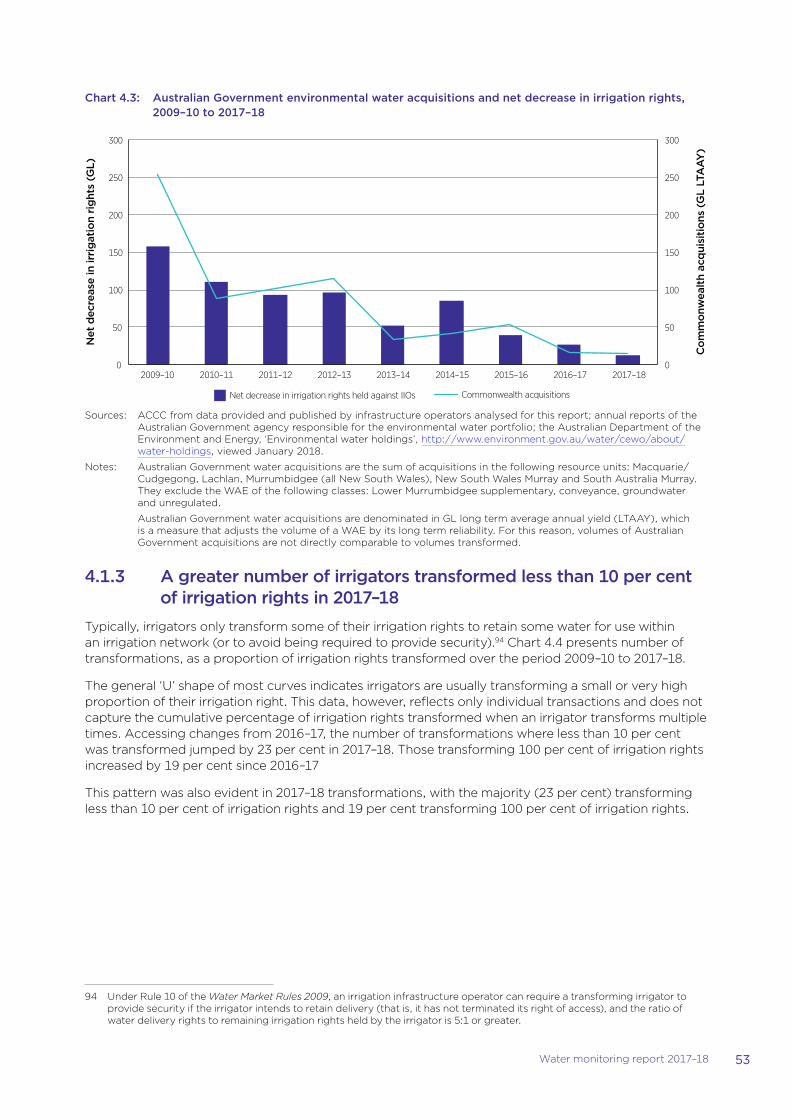

Chart 4.3: Australian Government environmental water acquisitions and net decrease in irrigation rights, 2009–10 to 2017–18 53

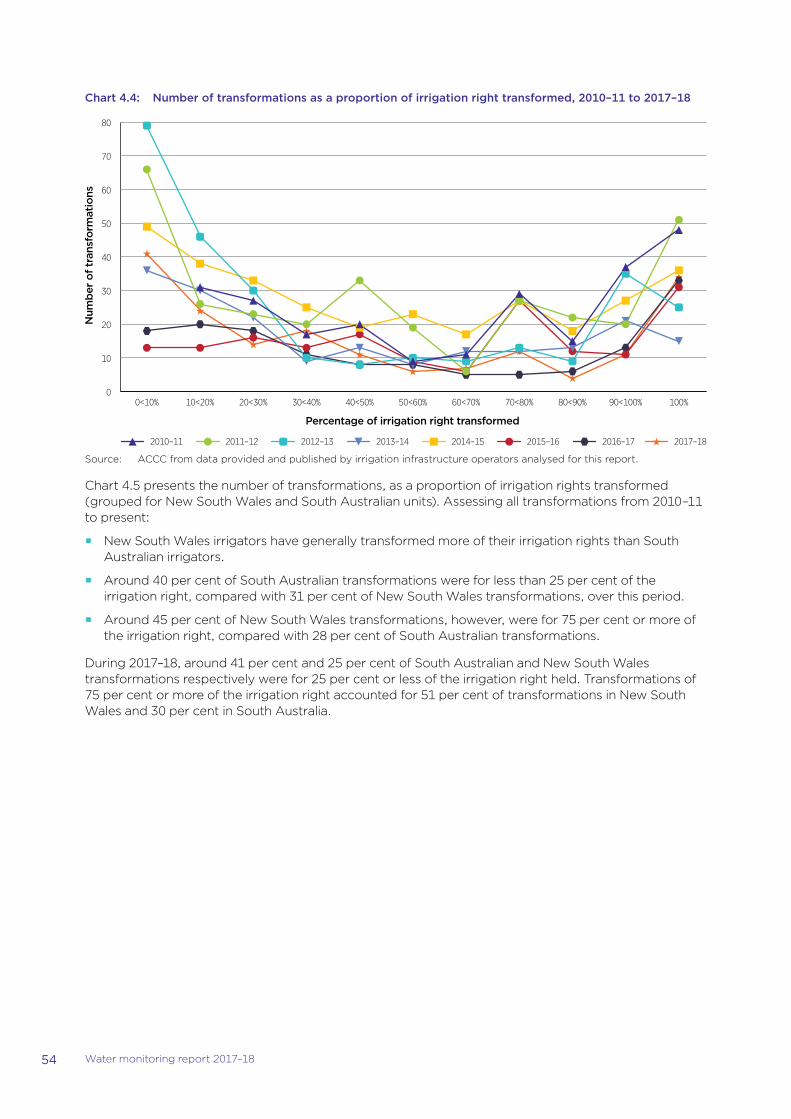

Chart 4.4: Number of transformations as a proportion of irrigation right transformed, 2010–11 to 2017–18 54

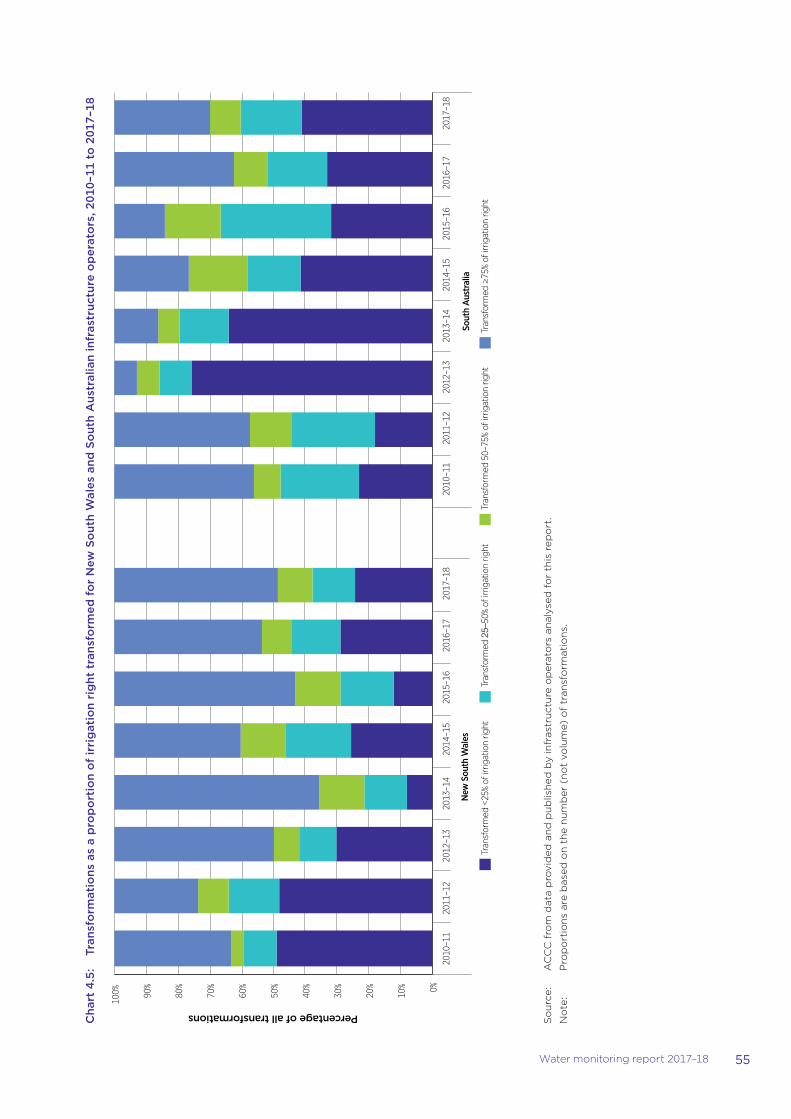

Chart 4.5: Transformations as a proportion of irrigation right transformed for New South Wales and South Australian infrastructure operators, 2010–11 to 2017–18 55

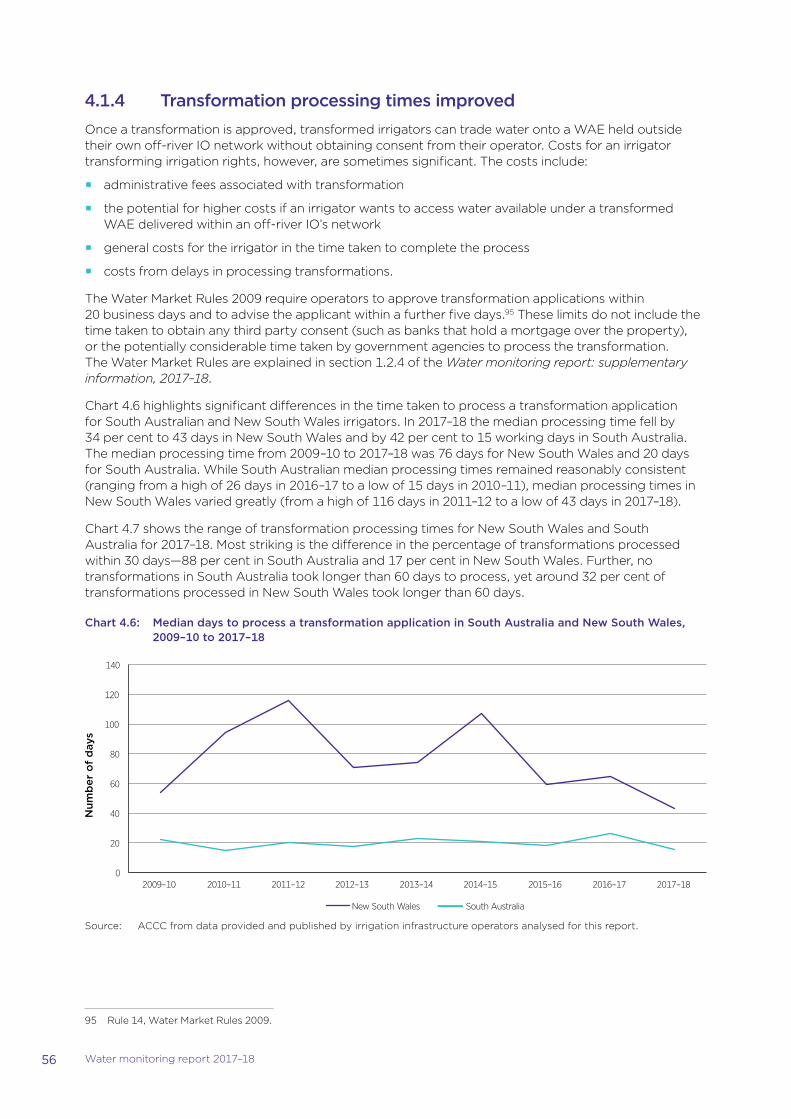

Chart 4.6: Median days to process a transformation application in South Australia and New South Wales, 2009–10 to 2017–18 56

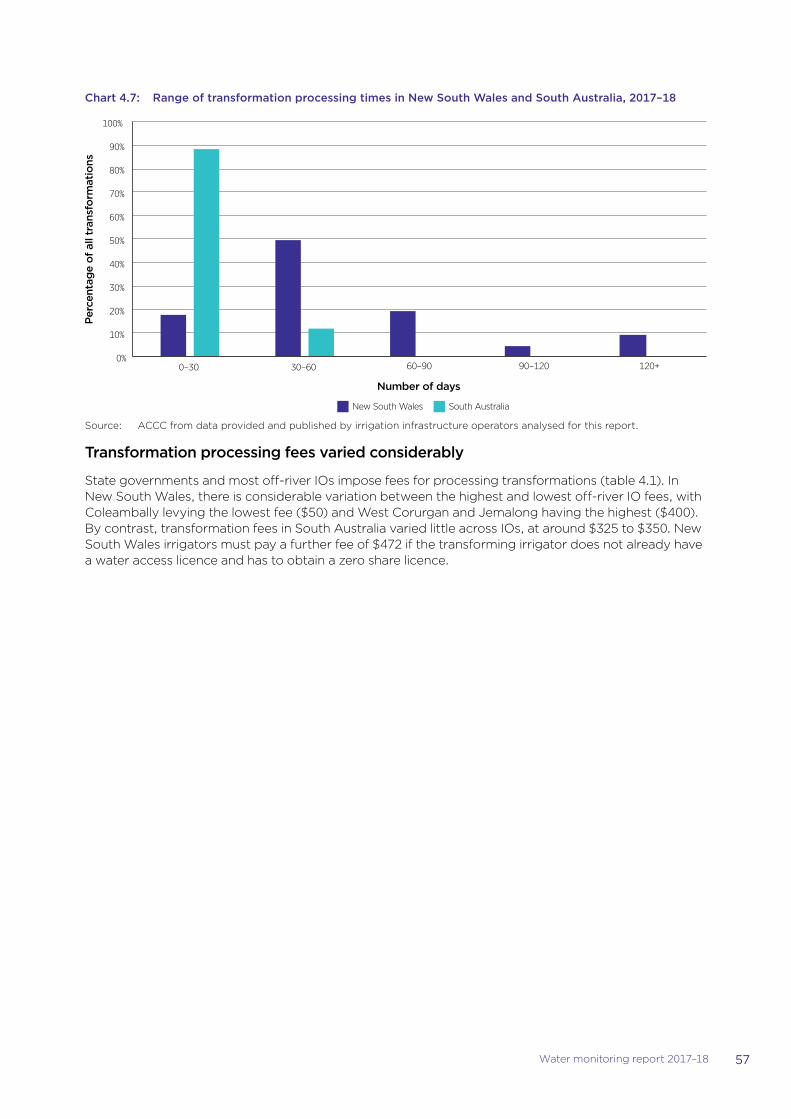

Chart 4.7: Range of transformation processing times in New South Wales and South Australia, 2017–18 57

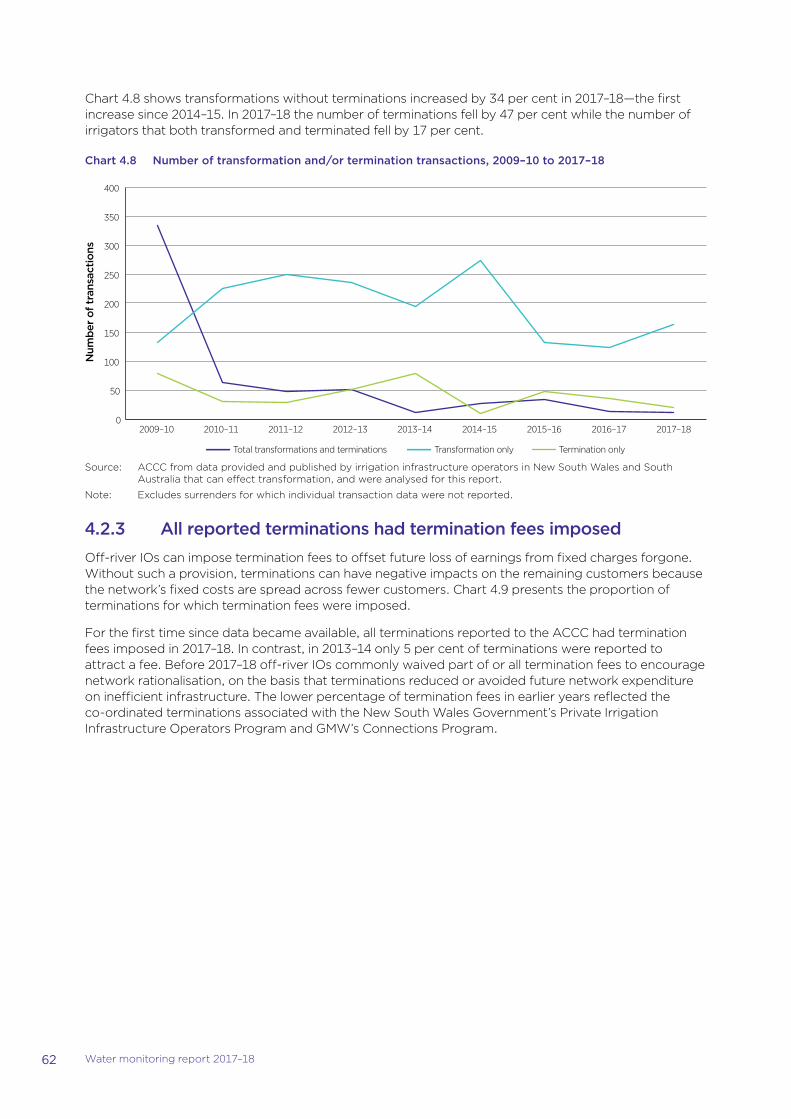

Chart 4.8 Number of transformation and/or termination transactions, 2009–10 to 2017–18 62

Chart 4.9: Terminations by imposition of termination fee, 2012–13 to 2017–18 63

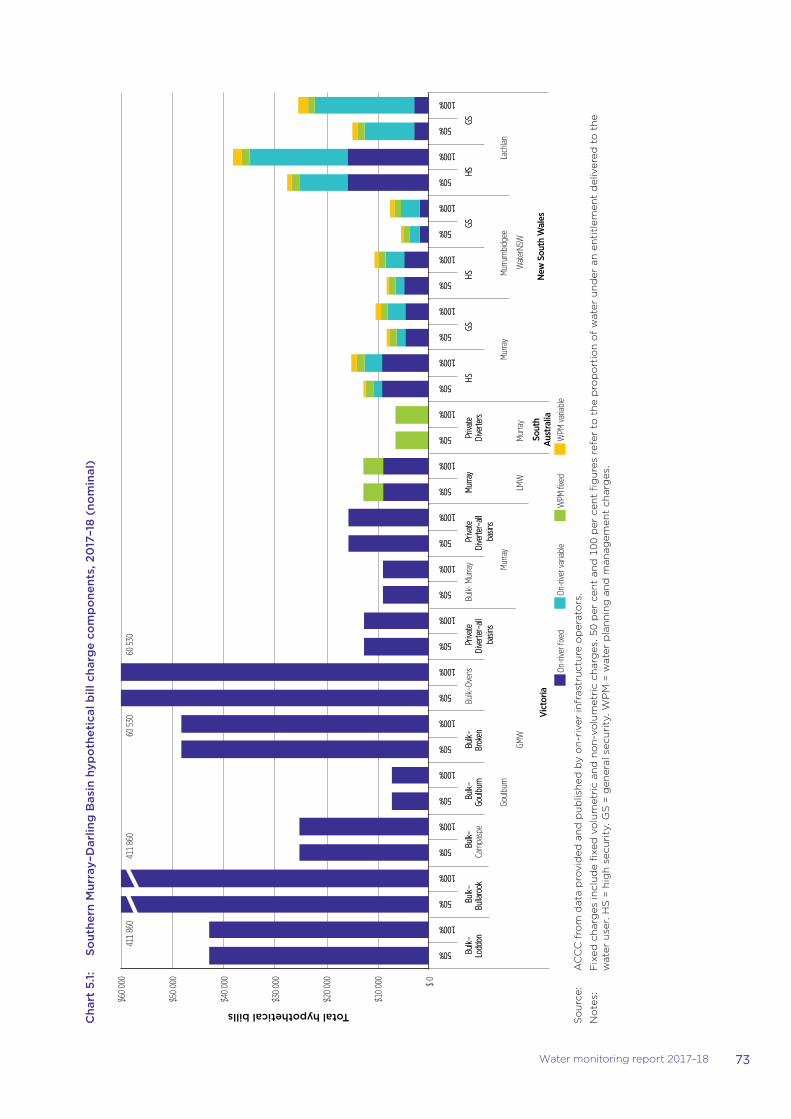

Chart 5.1: Southern Murray–Darling Basin hypothetical bill charge components, 2017–18 (nominal) 73

Chart 5.2: Northern Murray–Darling Basin hypothetical bill charge components, 2017–18 (nominal) 74

Chart 5.3: Southern Murray–Darling Basin hypothetical bill changes with 1000 ML of water entitlements for 50 per cent and 100 per cent water delivery (nominal) 77

Chart 5.4: Northern Murray–Darling Basin hypothetical bill changes with 1000 ML of water entitlements for 50 per cent and 100 per cent water delivery (nominal) 81

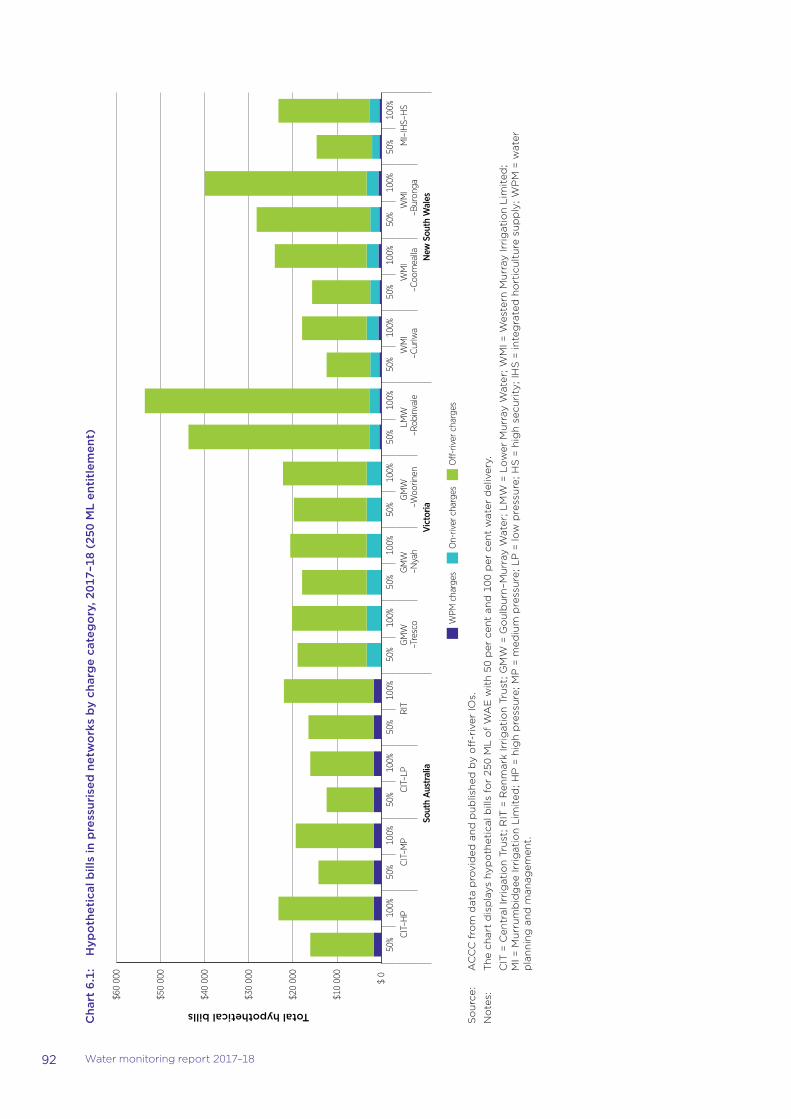

Chart 6.1: Hypothetical bills in pressurised networks by charge category, 2017–18 (250 ML entitlement) 92

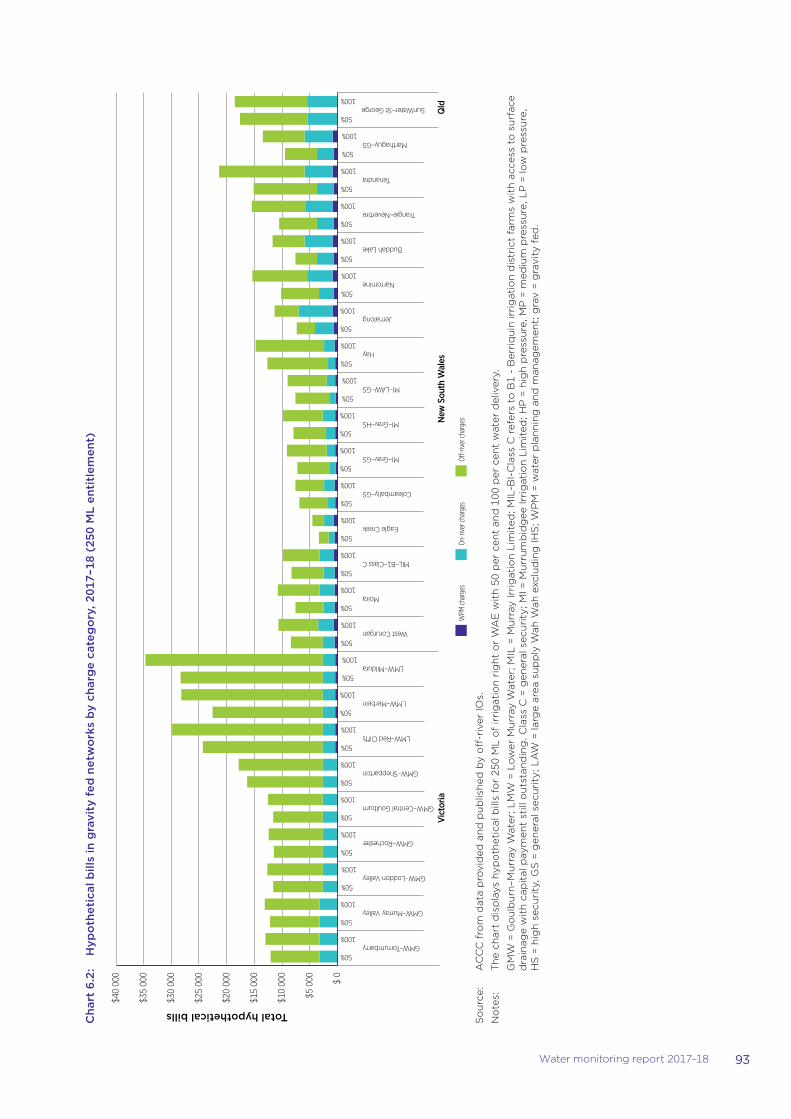

Chart 6.2: Hypothetical bills in gravity fed networks by charge category, 2017–18 (250 ML entitlement) 93

Chart 6.3: Total bill breakdown into fixed and variable charges by charge category, network type and irrigation network, 2017–18 (250 ML entitlement) 94

Chart 6.4: Year-on-year percentage change in total hypothetical bills in nominal terms for pressurised networks, by irrigation network, 2017–18 (250 ML entitlement) 97

Chart 6.5: Year-on-year percentage change in nominal terms for total hypothetical bills in gravity fed networks by irrigation network, 2017–18 (250 ML entitlement) 98

Chart 6.6: Year-on-year change in nominal terms for water planning and management, on-river and off-river charges—pressurised networks, 2017–18 (for 250 ML entitlement) 100

Chart 6.7: Year-on-year changes in nominal terms for water planning and management, on-river and off-river charges—gravity fed networks, 2017–18 (for 250 ML entitlement) 101

Chart 6.8: Hypothetical bills over time for pressurised networks in real terms, 2009–10 to 2017–18 (250 ML entitlement) 103

Chart 6.9: Hypothetical bills over time for Victorian gravity fed networks in real terms, 2009–10 to 2017–2018 (for 250 ML entitlement) 104

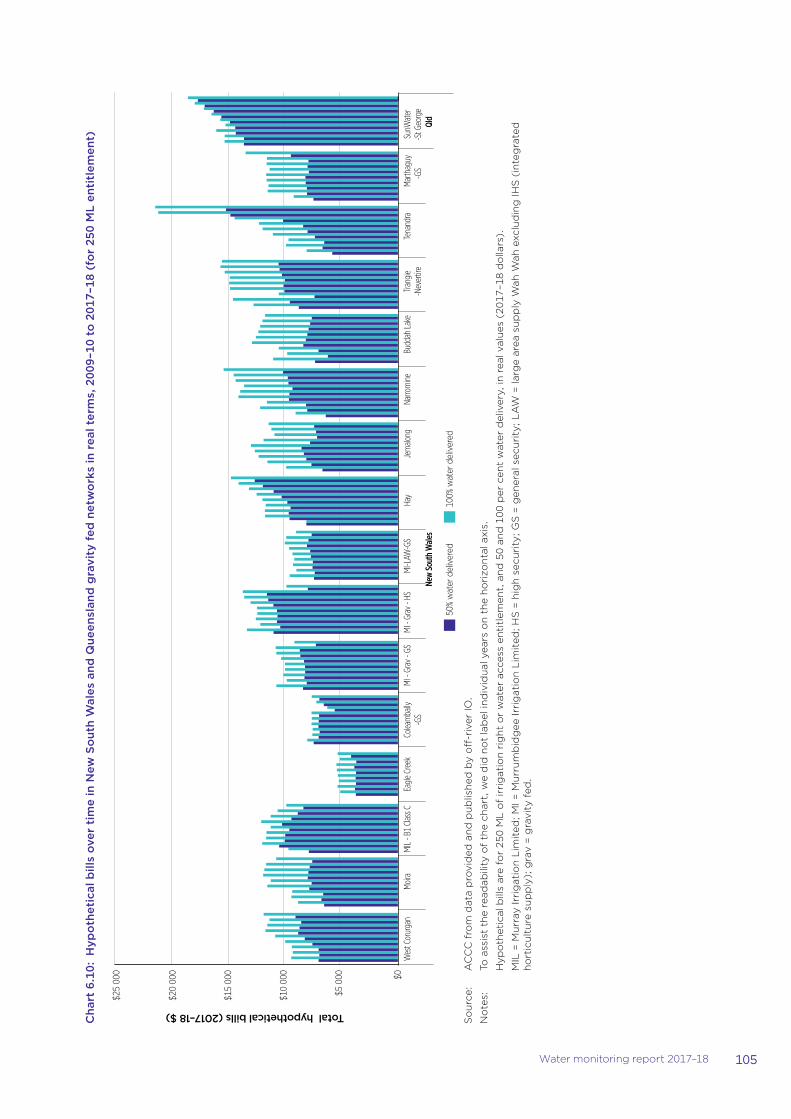

Chart 6.10: Hypothetical bills over time in New South Wales and Queensland gravity fed networks in real terms, 2009–10 to 2017–18 (for 250 ML entitlement) 105

viiWater monitoring report 2017–18

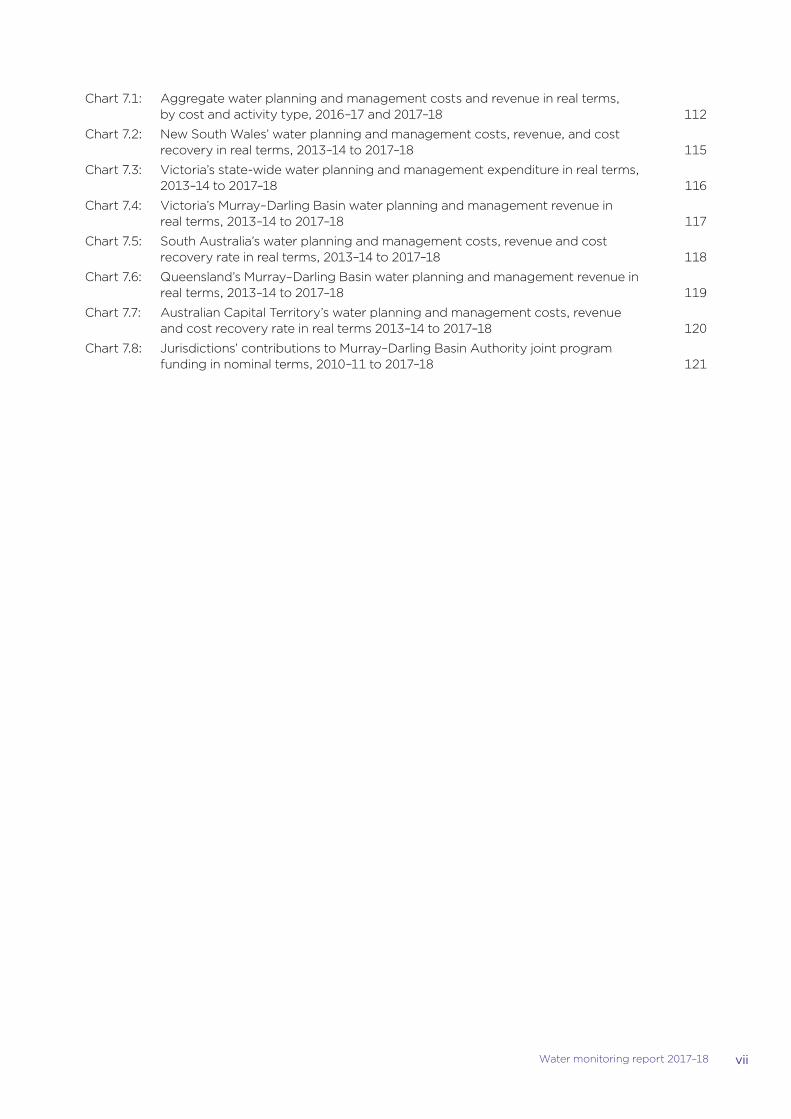

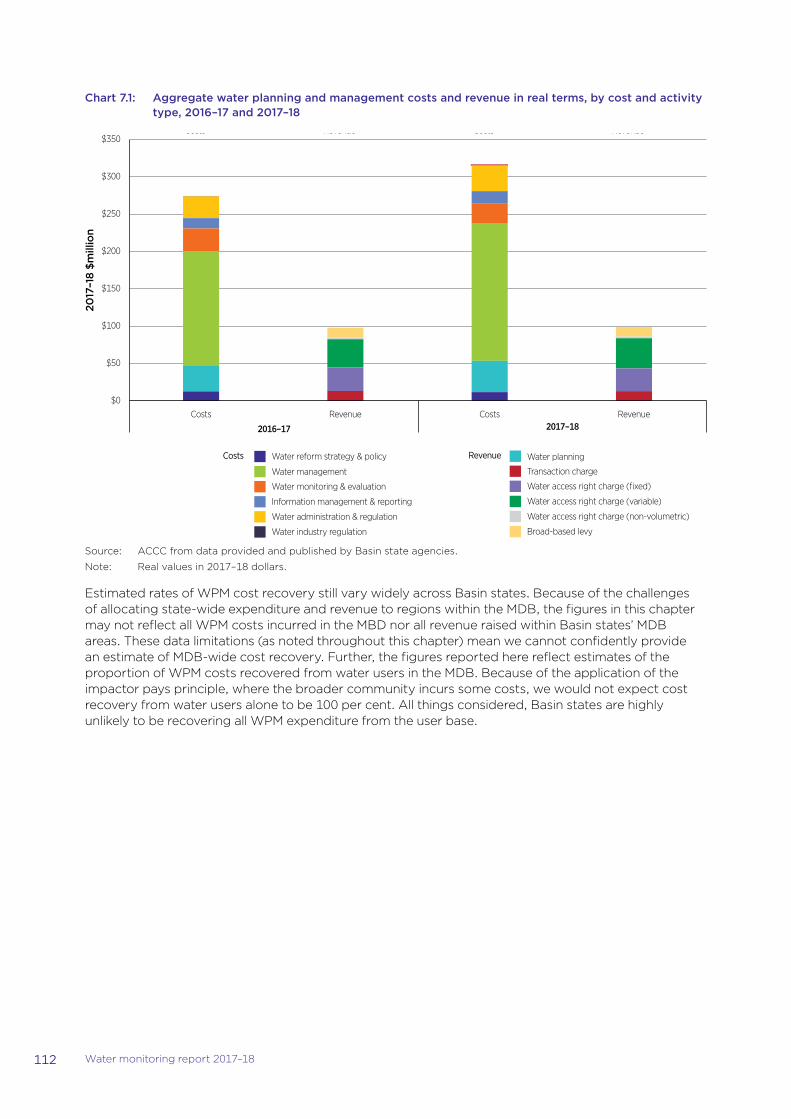

Chart 7.1: Aggregate water planning and management costs and revenue in real terms, by cost and activity type, 2016–17 and 2017–18 112

Chart 7.2: New South Wales’ water planning and management costs, revenue, and cost recovery in real terms, 2013–14 to 2017–18 115

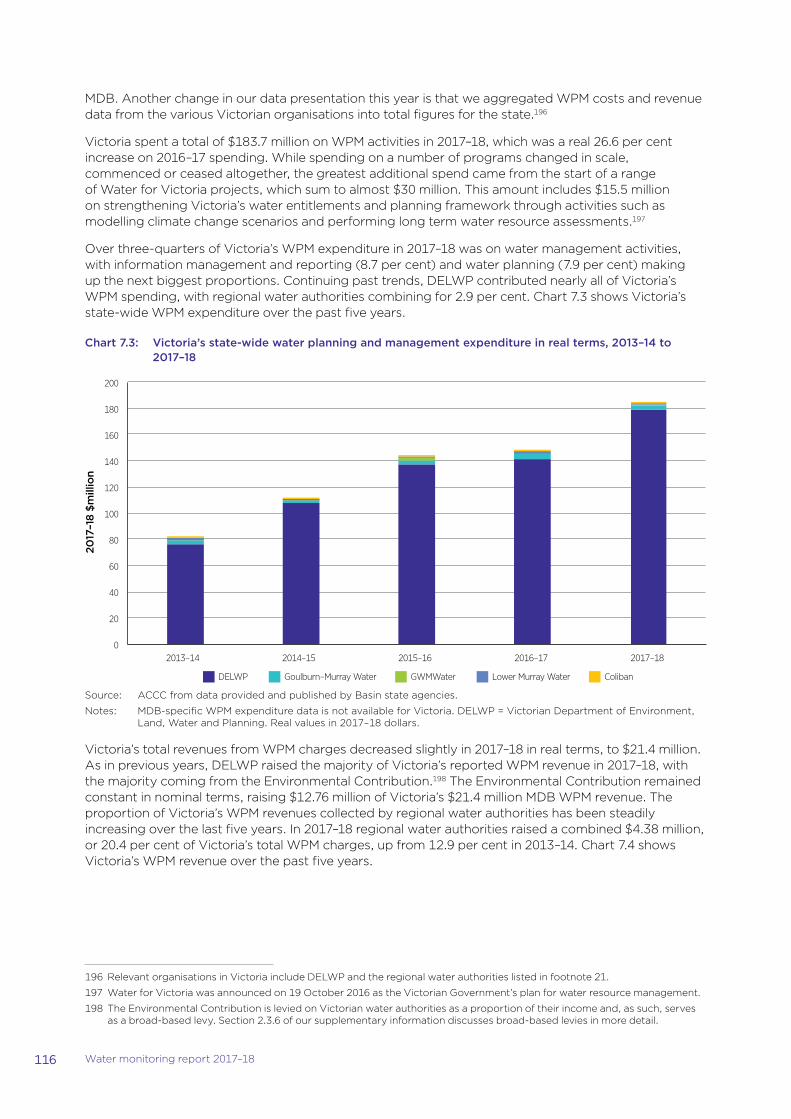

Chart 7.3: Victoria’s state-wide water planning and management expenditure in real terms, 2013–14 to 2017–18 116

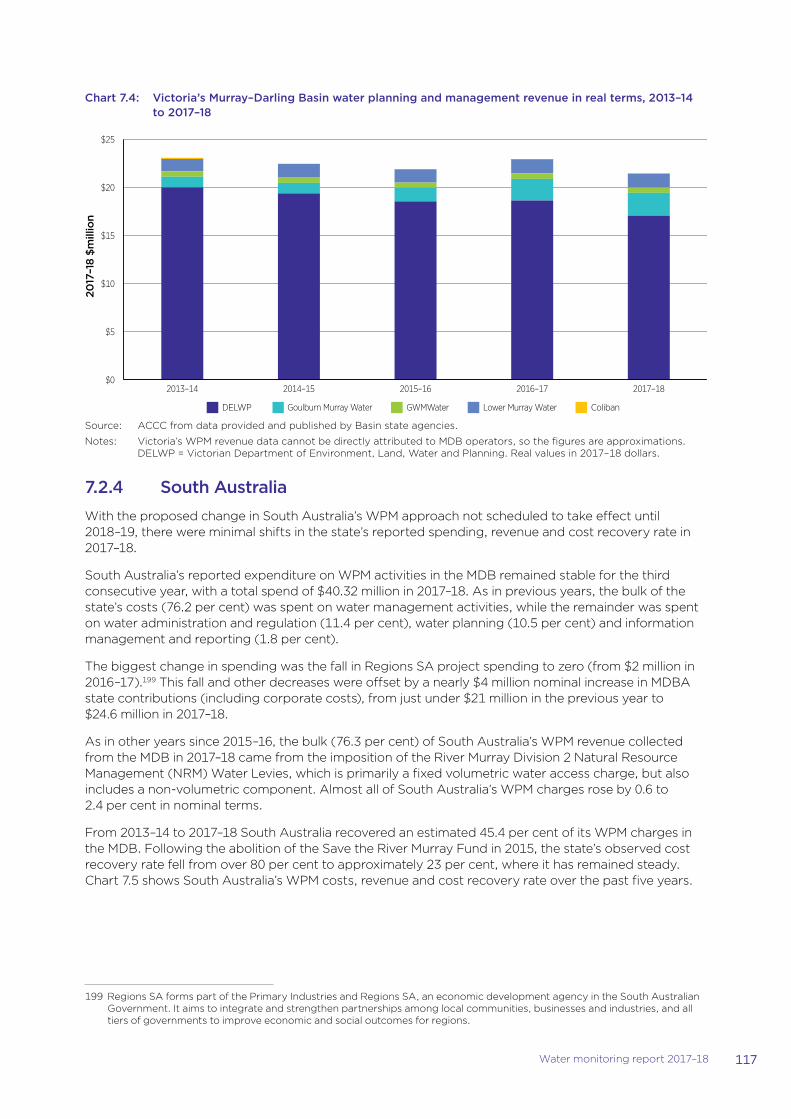

Chart 7.4: Victoria’s Murray–Darling Basin water planning and management revenue in real terms, 2013–14 to 2017–18 117

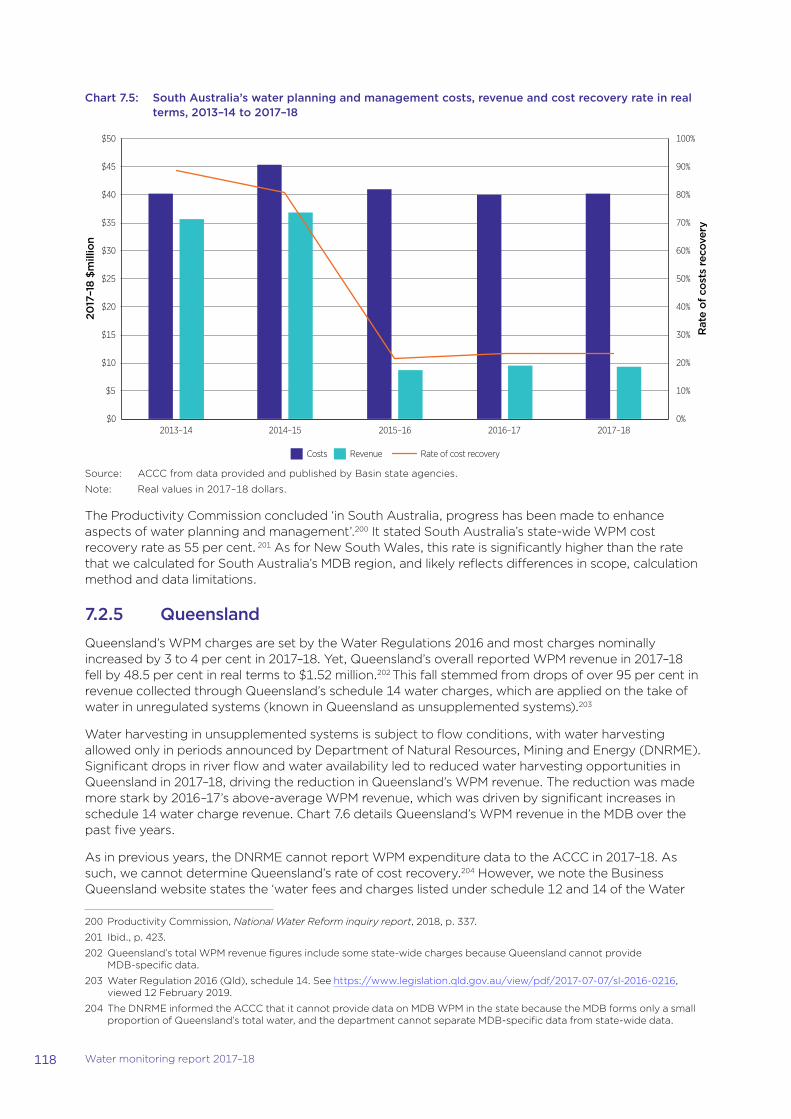

Chart 7.5: South Australia’s water planning and management costs, revenue and cost recovery rate in real terms, 2013–14 to 2017–18 118

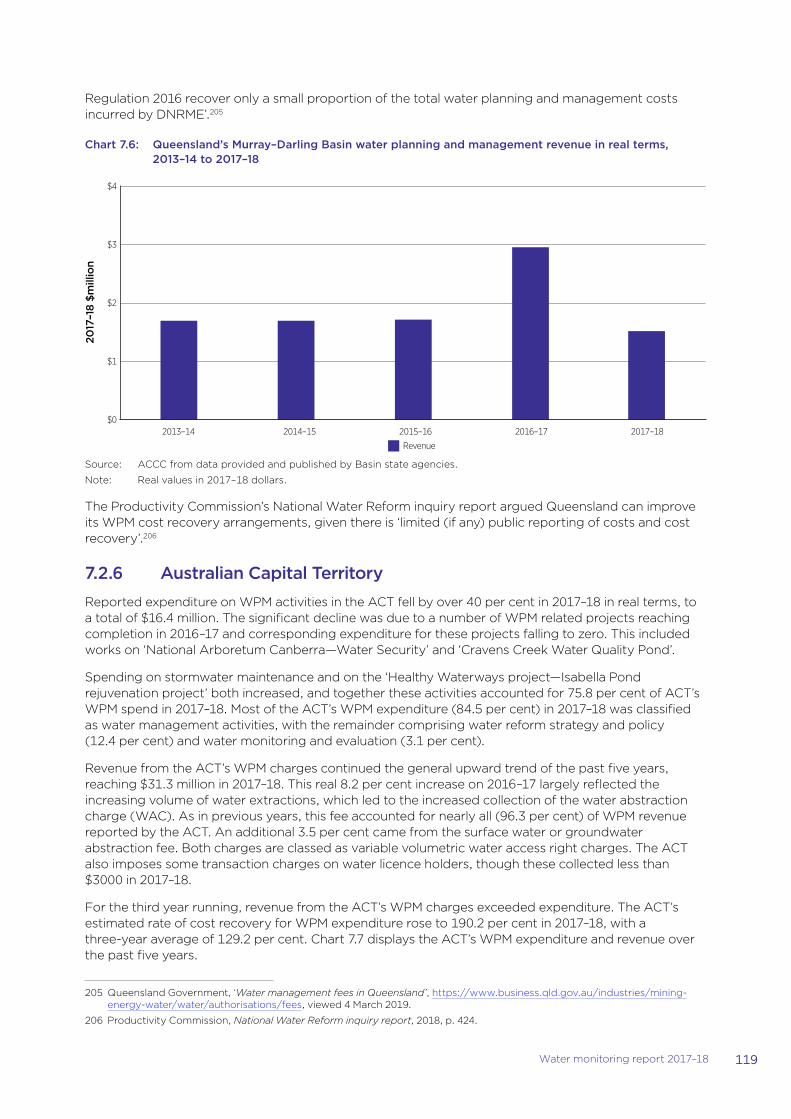

Chart 7.6: Queensland’s Murray–Darling Basin water planning and management revenue in real terms, 2013–14 to 2017–18 119

Chart 7.7: Australian Capital Territory’s water planning and management costs, revenue and cost recovery rate in real terms 2013–14 to 2017–18 120

Chart 7.8: Jurisdictions’ contributions to Murray–Darling Basin Authority joint program funding in nominal terms, 2010–11 to 2017–18 121

viii Water monitoring report 2017–18

AbbreviationsABARES Australian Bureau of Agricultural and Resource Economics and Sciences

ABC Australian Broadcasting Corporation

ABS Australian Bureau of Statistics

ACCC Australian Competition and Consumer Commission

ACL Australian Consumer Law

ALP Australian Labor Party

ATO Australian Taxation Office

AWBA Australian Water Brokers Association

BRC Dumaresq–Barwon Border Rivers Commission

CCA Competition and Consumer Act 2010 (Cth)

CICL Coleambally Irrigation Cooperative Limited

CIT Central Irrigation Trust

COAG Council of Australian Governments

CPI consumer price index

DELWP Victorian Department of Environment, Land, Water and Planning

DEWNR South Australian Department of Environment, Water and Natural Resources

DNRM Queensland Department of Natural Resources and Mines (DNRME since December 2017)

DNRME Queensland Department of Natural Resources, Mines and Energy

DOI Water Department of Industry (Water) (NSW)

DSEWPAC Department of Sustainability, Environment, Water Population and Communities

EPSDD ACT Environment, Planning and Sustainable Development Directorate

ESCOSA Essential Services Commission of South Australia

ESCV Essential Services Commission (Victoria)

EWH environmental water holder

GL gigalitre (one billion litres)

GMW Goulburn–Murray Water

GWMWater Grampians Wimmera Mallee Water

GS general security

HP high pressure

HPID Hay Private Irrigation District

HS high security

ICD irrigation corporation and district

IHS integrated horticulture supply

IIO irrigation infrastructure operator

IO infrastructure operator

IPART Independent Pricing and Regulatory Tribunal (NSW)

IR irrigation right

ixWater monitoring report 2017–18

IVT Inter-Valley Transfer

JWSS Joint Water Supply Scheme

KL kilolitres

LAW Large area supply Wah Wah excluding IHS

LAS large area supply

LTAAY The average annual yield

LMW Lower Murray Water

LP low pressure

LTAAY long term average annual yield

MDB Murray–Darling Basin

MDBA Murray–Darling Basin Authority

MI Murrumbidgee Irrigation Limited

MIL Murray Irrigation Limited

MJA Marsden Jacob Associates

ML megalitre (one million litres)

MP medium pressure

MPID Moira Private Irrigation District

NIBM Narromine Irrigation Board of Management

NRAR Natural Resources Access Regulator

NRM national resources management

NWC National Water Commission

NWI National Water Initiative

off-river IO off-river infrastructure operator

on-river IO on-river infrastructure operator

PC Productivity Commission

PIIOP Private Irrigation Infrastructure Operators Program (NSW)

QCA Queensland Competition Authority

RIT Renmark Irrigation Trust

RMO River Murray Operations

SACOME South Australian Chamber of Mines and Energy

SAMDB South Australia Murray–Darling Basin

SAS small area supplies

SDL sustainable diversion limit

TNAC total network access charge

VWAP volume weighted average prices

WAE water access entitlement

WAL water access licence

WC West Corurgan

WCIR Water Charge (Infrastructure) Rules 2010

WCTFR Water Charge (Termination Fees) Rules 2009

x Water monitoring report 2017–18

WDR water delivery right

WMI Western Murray Irrigation Limited

WPM water planning and management

WRP Water Resource Plan

xiWater monitoring report 2017–18

GlossaryBasin plan A high level framework on which the Australian Government and Basin

States agreed, and that sets standards for the management of the Murray–Darling Basin’s water resources in a coordinated and sustainable way in collaboration with the community. Officially known as the Basin Plan 2012.

Basin Plan Water Trading Rules (BPWTR)

Rules set out in Part 12 of the Basin Plan that relate to the trade or transfer of tradeable water rights. The rules commenced on 1 July 2014 and are enforced by the Murray–Darling Basin Authority.

Basin states

Basin state agencies

New South Wales, Victoria, Queensland, South Australia, the ACT

Basin State departments and water authorities.

bulk water charge A charge payable for either (or both) the storage of water for, or the delivery of water to:

(i) infrastructure operators

(ii) other operators of reticulated water systems

(iii) other persons (including private diverters and environmental water holders).

carryover Arrangements that allow water entitlement holders to hold allocated water in storages so it is available in subsequent years.

conveyance water Water required primarily to operate regulated rivers and utility supply networks to enable the delivery of water.

gravity-fed irrigation system

An irrigation system comprising channels and/or pipes that relies on the movement of water due to the force of gravity.

infrastructure charge Charges that infrastructure operators impose for access to their water service infrastructure, and for services provided in relation to that access.

infrastructure operator (IO)

Any person or entity that owns or operates infrastructure for one or more of the following purposes:

(i) the storage of water

(ii) the delivery of water

(iii) the drainage of water

for providing a service to someone who does not own or operate the infrastructure.

irrigation infrastructure operator (IIO)

An infrastructure operator that owns or operates water service infrastructure for delivering water for the primary purpose of irrigation.

irrigation network As defined in s. 7(4) of the Water Act 2007, the water service infrastructure of an irrigation infrastructure operator. In practice, an irrigation network typically constitutes a network of carriers (open channels, pipes and/or natural waterways) that convey water from a water source through customer service points to customer properties. It may be either a gravity fed network (typically using channels and/or natural waterways) or a pressurised network (using pipes).

irrigation right A person’s right against an IIO to receive water, which is not a water access right or a water delivery right. It usually can be transformed into a water access entitlement.

infrastructure service Access, or a service provided in relation to access, to water service infrastructure. It includes the storage, delivery, drainage and taking of water.

xii Water monitoring report 2017–18

joint water supply schemes

Similar to cooperatives where the members form and run an organisation to deliver water to irrigators.

non-volumetric charge A charge that does not reference a volume of a water right—for example, a charge that is levied per account, per outlet or per meter.

off-river infrastructure service/off-river infrastructure operator

The storage, delivery and/or drainage of water diverted from a natural watercourse through a network consisting of channels and/or pipes (which can be gravity fed or pressurised) to another person. An operator providing such services is an off-river infrastructure operator.

on-river infrastructure service/on-river infrastructure operator

Harvesting and storing water through infrastructure such as dams, lakes, weirs and reservoirs located primarily on a natural watercourse, and delivering water, primarily through natural watercourses. An operator providing such services is an on-river infrastructure operator.

private diverter An irrigator that extracts water directly from a natural watercourse (either a regulated or unregulated river).

pressurised irrigation system

A piped irrigation system that usually requires on water pressure for the system to work and requires pumps to pressurise the water.

regulated water charge A water charge to which any of these three sets of water charge rules applies:

�� Water Charge (Infrastructure) Rules

�� Water Charge (Planning and Management Information) Rules

�� Water Charge (Termination Fees) Rules.

See s. 91 of the Water Act 2007 for a full definition.

southern connected Murray–Darling Basin

Refers to the southern Murray–Darling Basin catchments that are hydrologically connected and water can be traded between any of these catchments (subject to trade limits).

termination When a person terminates or surrenders the whole or part of a right of access to an IIO’s network, typically by terminating a water delivery right.

termination fee A fee that an IIO may impose when an irrigator terminates.

the Act Water Act 2007 (Cth)

total network access charge

Amount on which the termination fee multiple is applied to calculate a maximum termination fee. It is the sum of all amounts that would have been payable for access to an operator’s irrigation network by an irrigator for a full financial year if termination or surrender had not occurred, excluding:

�� any amount for the amount of water actually delivered to the terminating irrigator (that is, variable irrigation network charges)

�� any amount for the storage of water

�� connection/disconnection fees

�� any amount that exceeds the cost of providing irrigators with access to an operator’s irrigation network

�� fees under ACCC approved contracts.

tradeable water right One of:

(i) water access rights

(ii) water delivery rights

(iii) irrigation rights.

xiiiWater monitoring report 2017–18

transformation Process by which an irrigator permanently transforms their entitlement to water under an irrigation right against an IIO into a water access entitlement held by the irrigator (or anybody other than the IIO), thereby reducing the volume (for example, the share component) of the operator’s water access entitlement.

volumetric charge Charge based on the volume of a water right or physical amount of water. A fixed volumetric charge is a charge based on the volume of a water right held, while a variable volumetric charge is a charge based on the volume of the right that is used in a particular manner.

water access entitlement Perpetual or ongoing entitlement, by or under a law of a state, to exclusive access to a share of the water resources of a water resource plan area.

water access entitlement trade

Change of ownership and/or location of a water access entitlement (including through the establishment of a tagging arrangement).

water access right Any right conferred by or under a law of a state to hold and/or take water from a water resource, including:

�� stock and domestic rights

�� riparian rights

�� a water access entitlement

�� a water allocation.

water allocation Specific volume of water allocated to water access entitlements in a given water accounting period.

water allocation trade Change of ownership and/or location of a particular volume of water allocation.

watercourse A river, creek or other natural watercourse (whether modified or not) in which water is contained or flows (whether permanently or intermittently). It may be a:

(i) a dam or reservoir that collects water flowing in a watercourse

(ii) a lake or wetland through which water flows

(iii) a channel into which the water of a watercourse has been diverted

(iv) part of a watercourse

(v) an estuary through which water flows.

Water Charge (Infrastructure) Rules 2010 (WCIR)

Rules for fees and charges payable to an infrastructure operator for:

�� bulk water charges

�� access to the IIO’s network, or services provided in relation to that access

�� matters specified in regulations made under s. 91(1)(d) of the Water Act 2007.

Water Charge (Planning and Management Information) Rules 2010 (WCPMIR)

Rules relating to charges for water planning and water management activities in the Murray–Darling Basin, and requiring the publication of the charge details and the process for determining the charge.

Water Charge (Termination Fees) Rules 2009 (WCTFR)

Rules for fees or charges payable to an IIO in relation to terminating access to an operator’s irrigation network (or services relating to such termination), or surrendering a right to delivery of water through the operator’s irrigation network.

water delivery right (WDR)

Right to have water delivered by an infrastructure operator. It typically represents the holder’s right of access to an irrigation network (there may also be a right to drainage), and can be terminated.

xiv Water monitoring report 2017–18

Water Market Rules/2009 (WMR)

Rules dealing with actions or omissions of an IIO that prevent or unreasonably delay transformation arrangements or trade of the resulting water access entitlement.

water service infrastructure

Infrastructure for one or more of the following purposes:

(i) the storage of water

(ii) the delivery of water

(iii) the drainage of water

for providing a service to another person.

xvWater monitoring report 2017–18

1 Document title

Photo © Victoria International Container Terminal 2017. Photo supplied by Victoria International Container Terminal Limited.

Water Monitoring Report 2017–18

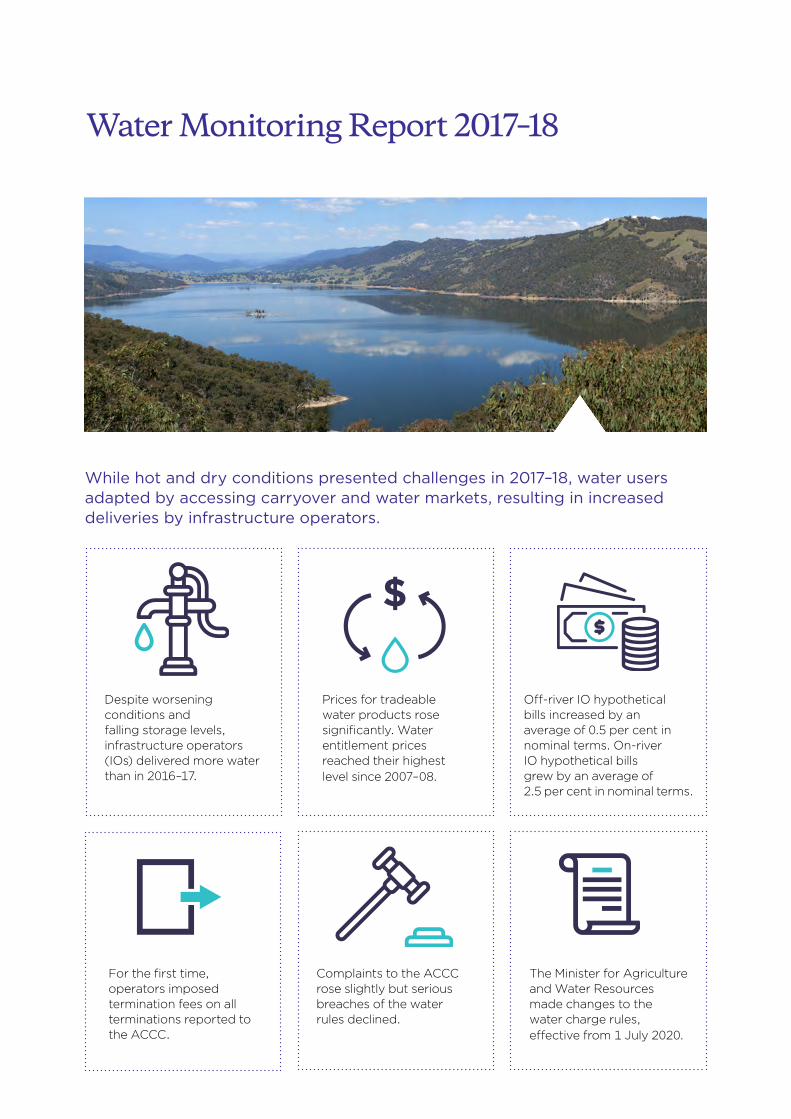

The Minister for Agriculture and Water Resources made changes to the water charge rules, effective from 1 July 2020.

For the first time, operators imposed termination fees on all terminations reported to the ACCC.

Prices for tradeable water products rose significantly. Water entitlement prices reached their highest level since 2007–08.

Off-river IO hypothetical bills increased by an average of 0.5 per cent in nominal terms. On-river IO hypothetical bills grew by an average of 2.5 per cent in nominal terms.

Complaints to the ACCC rose slightly but serious breaches of the water rules declined.

Despite worsening conditions and falling storage levels, infrastructure operators (IOs) delivered more water than in 2016–17.

$

While hot and dry conditions presented challenges in 2017–18, water users adapted by accessing carryover and water markets, resulting in increased deliveries by infrastructure operators.

xvi Water monitoring report 2017–18

Key market results 2017–18

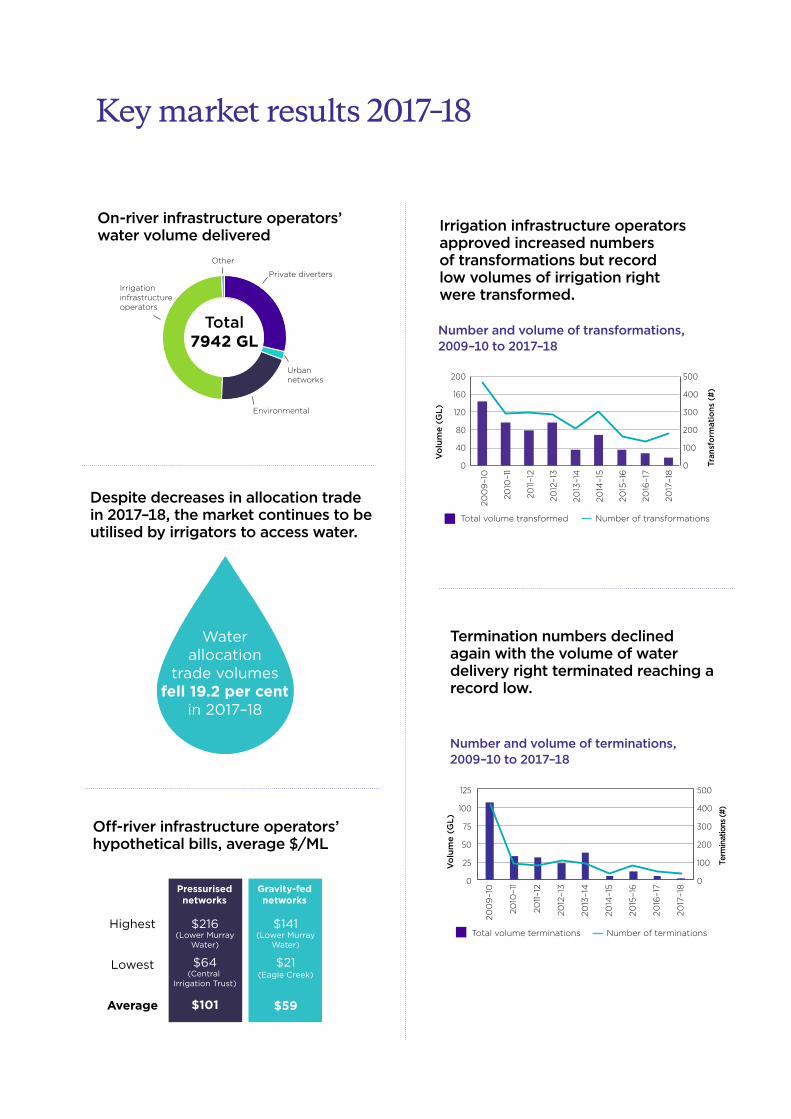

On-river infrastructure operators’ water volume delivered

Private diverters

Urbannetworks

Environmental

Irrigationinfrastructureoperators

Other

Total7942 GL

Waterallocation

trade volumesfell 19.2 per cent

in 2017–18

Despite decreases in allocation trade in 2017–18,

the market continues to be utilised by irrigators to

access water.

Despite decreases in allocation trade in 2017–18, the market continues to be utilised by irrigators to access water.

Off-river infrastructure operators’ hypothetical bills, average $/ML

Highest

Lowest

Average

$216(Lower Murray

Water)

$64(Central

Irrigation Trust)

$101

$141(Lower Murray

Water)

$21(Eagle Creek)

$59

Pressurisednetworks

Gravity-fednetworks

Irrigation infrastructure operators approved increased numbers of transformations but record low volumes of irrigation right were transformed.

200

9–1

0

2010

–11

2011–

12

2012

–13

2013

–14

2014

–15

2015

–16

2016

–17

2017

–18

Vo

lum

e (G

L)

Tran

sfor

mat

ions

(#)

Total volume transformed Number of transformations

0

40

80

120

160

200

0

100

200

300

400

500

Termination numbers declined again with the volume of water delivery right terminated reaching a record low.

Number and volume of terminations, 2009–10 to 2017–18

200

9–1

0

2010

–11

2011–

12

2012

–13

2013

–14

2014

–15

2015

–16

2016

–17

2017

–18

Vo

lum

e (G

L)

Term

inat

ions

(#)

Total volume terminations Number of terminations

0

100

200

300

400

500

0

25

50

75

100

125

Number and volume of transformations, 2009–10 to 2017–18

xviiWater monitoring report 2017–18

Key market results 2017–18

On-river infrastructure operators’ water volume delivered

Private diverters

Urbannetworks

Environmental

Irrigationinfrastructureoperators

Other

Total7942 GL

Waterallocation

trade volumesfell 19.2 per cent

in 2017–18

Despite decreases in allocation trade in 2017–18,

the market continues to be utilised by irrigators to

access water.

Despite decreases in allocation trade in 2017–18, the market continues to be utilised by irrigators to access water.

Off-river infrastructure operators’ hypothetical bills, average $/ML

Highest

Lowest

Average

$216(Lower Murray

Water)

$64(Central

Irrigation Trust)

$101

$141(Lower Murray

Water)

$21(Eagle Creek)

$59

Pressurisednetworks

Gravity-fednetworks

Irrigation infrastructure operators approved increased numbers of transformations but record low volumes of irrigation right were transformed.

200

9–1

0

2010

–11

2011–

12

2012

–13

2013

–14

2014

–15

2015

–16

2016

–17

2017

–18

Vo

lum

e (G

L)

Tran

sfor

mat

ions

(#)

Total volume transformed Number of transformations

0

40

80

120

160

200

0

100

200

300

400

500

Termination numbers declined again with the volume of water delivery right terminated reaching a record low.

Number and volume of terminations, 2009–10 to 2017–18

200

9–1

0

2010

–11

2011–

12

2012

–13

2013

–14

2014

–15

2015

–16

2016

–17

2017

–18

Vo

lum

e (G

L)

Term

inat

ions

(#)

Total volume terminations Number of terminations

0

100

200

300

400

500

0

25

50

75

100

125

Number and volume of transformations, 2009–10 to 2017–18

Key findingsDrought and water deliverability challenges emerged in 2017–18�� The majority of the Murray–Darling Basin (MDB) experienced mean temperatures very much above

the long-term average with rainfall below average for the year.

�� Most water trading zones experienced record water allocation trade volumes. Prices for water allocations rose, with record water access entitlement prices in the southern MDB.

�� In the southern MDB, water storage levels fell. Water allocated to entitlements was also lower, but water carried over from previous years helped to offset lower allocations. The use of carryover and water markets more generally, are aimed at facilitating water market participants to manage risk.

�� Energy input costs remained a concern for irrigators and infrastructure operators, particularly in pressurised systems. But new forms of energy contracting are emerging, with at least one infrastructure operator reporting success in reducing energy costs.

�� The expansion of perennial crops such as almonds continued. As these plantations expand further, water requirements in the Lower Murray River may increase.

There was widespread debate and many reviews of water policy and governance arrangements in the Murray–Darling Basin�� During 2017–18 and post 2018 MDB policy, legal and governance arrangements continued to

generate widespread debate and attract public scrutiny. Governments initiated or concluded many major inquiries and policy reviews, including a Royal Commission in South Australia.

�� The series of mass fish deaths in late 2018 and early 2019 in the Lower Darling River received considerable media attention and increased public focus on management of the Menindee Lakes and on the Murray–Darling Basin Plan and Murray–Darling Basin Agreement.

The Minister announced changes to the water charge rules�� The ACCC provided advice to the Australian Minister for Agriculture and Water Resources on

amendments to the water charge rules in 2016.

�� On 3 April 2019, the Minister amended the water charge rules based on the ACCC advice to increase transparency by requiring IOs to provide customers with more information on infrastructure charges, water planning and management charges and termination fees. Regulation of on-river infrastructure operators will return to Basin state regulatory frameworks except in specific circumstances. The changes will combine the existing three sets of water charge rules into one and commence on 1 July 2020.

�� The Minister did not accept the ACCC’s recommendations to strengthen non-discrimination requirements, reform the current regulation of distributions, or remove the right of private action. The ACCC supported expanded non-discrimination provisions as being consistent with and contributing to the achievement of the Basin Water Charging Objectives and Principles—in particular, to the achievement of ‘user pays’, full cost recovery and avoiding perverse or unintended pricing outcomes.

Transformation, termination and trade volumes were down, but MDB water markets continue to increase in sophistication, depth, volume, value and efficiency�� The number of transformation applications increased by 32 per cent from 2016–17 but the volume

of irrigation rights transformed was a record low of 17 GL. The total volume of irrigation rights transformed as a percentage of the total volume of irrigation rights as of 1 July 2009 remained around 18 per cent.

xviii Water monitoring report 2017–18

�� The number and volume of water delivery rights terminated in 2017–18 were the lowest reported since ACCC monitoring commenced in 2009, with all terminations having termination fees imposed for the first time since monitoring began.

�� The volume of water delivery right trade increased by 10 per cent in 2017–18. This reflected large trades within Murrumbidgee Irrigation Limited and Jemalong, with four off-river infrastructure operators (IOs) accounting for the bulk of water delivery right trade.

�� Trade activity for allocations within IO networks monitored by the ACCC declined in 2017–18 by 20 per cent, with a net export of water from the monitored networks.

Some on-river hypothetical bills increased while others decreased�� The six on-river IOs delivered 9 per cent more water in 2017–18 than the previous year, partly driven

by the delivery of carryover water.

�� In aggregate, hypothetical bills calculated by the ACCC for these on-river IOs increased by around 2.5 per cent in nominal terms.

�� For those hypothetical bills that showed increases, Goulburn–Murray Water’s Bullarook, Broken and Ovens systems in the southern MDB all increased by 12 per cent in nominal terms, while Murray Irrigation Limited’s high security increased by 25 per cent. In July 2018 deteriorating conditions saw the New South Wales Government announce a drought relief package that included fixed charge rebates for many water users.

Off-river hypothetical bills continue to increase for the majority of networks�� In aggregate, the average growth between 2016–17 and 2017–18 in hypothetical bills for pressurised

systems was around 5 per cent, while for gravity fed networks it was less than 1 per cent in nominal terms.

Basin states’ spending trends varied�� In 2017–18 spending in water planning and management increased in New South Wales and Victoria,

was stable in South Australia, and decreased in the ACT.

Compliance with water market and water charge rules is generally good�� Compliance with the water market rules and water charge rules (the Rules) is generally good. We

found no breaches of the Rules or Australian Consumer Law that resulted in serious detriment to irrigators or other stakeholders. We will continue to work with irrigators and IOs to educate them about their rights and responsibilities, and the need for compliance with the Rules (including amendments), to ensure transparency of regulated water charges and stakeholder confidence in the water market.

�� During the year, we received 14 complaints and inquiries regarding the Rules, IOs and water market intermediaries, up from 10 in the previous year. In 2017–18, we conducted three initial investigations into possible breaches of the water charge rules and two possible Australian Consumer Law breaches (one on-going).

xixWater monitoring report 2017–18

SummaryThe ACCC’s role in the Murray–Darling Basin

The ACCC has a number of compliance and advisory roles in the Murray–Darling Basin, including monitoring regulated water charges, transformations and terminations. It also produces an annual report for the Australian Minister for Water Resources, Drought, Rural Finance, Natural Disaster and Emergency Management. This is our ninth report.

Both on and off-river infrastructure operators (IOs) are regarded as monopolies. This is because competition is unlikely to develop between these IOs as they operate in geographically exclusive markets for water harvesting, storage and/or delivery services. Our monitoring helps highlight where IOs may be exercising their market power over irrigators and other customers and assists policy makers to determine the appropriate form of regulation for these monopolies.

We also facilitate effective water (and related) markets by monitoring and enforcing compliance with the water charge and water market rules. Due to their monopoly position, IOs are in a position, and have incentive, to prevent or unreasonably delay trade or transformation requests and increase the cost of termination.

There are a number of other Commonwealth and Basin State regulatory measures that are directly relevant to water markets in the Murray–Darling Basin and the management of Basin water resources more generally. For example, the administration of water planning and management activities, the allocation and metering of water, and the trading of water are primarily undertaken by Basin State governments.

This report utilises a range of sources to assess the state of the water market and regulated water charges. We collect data from IOs and Basin states. We also use information from reports and other sources published by a number of Australian departments and agencies, academia and industry consultants.

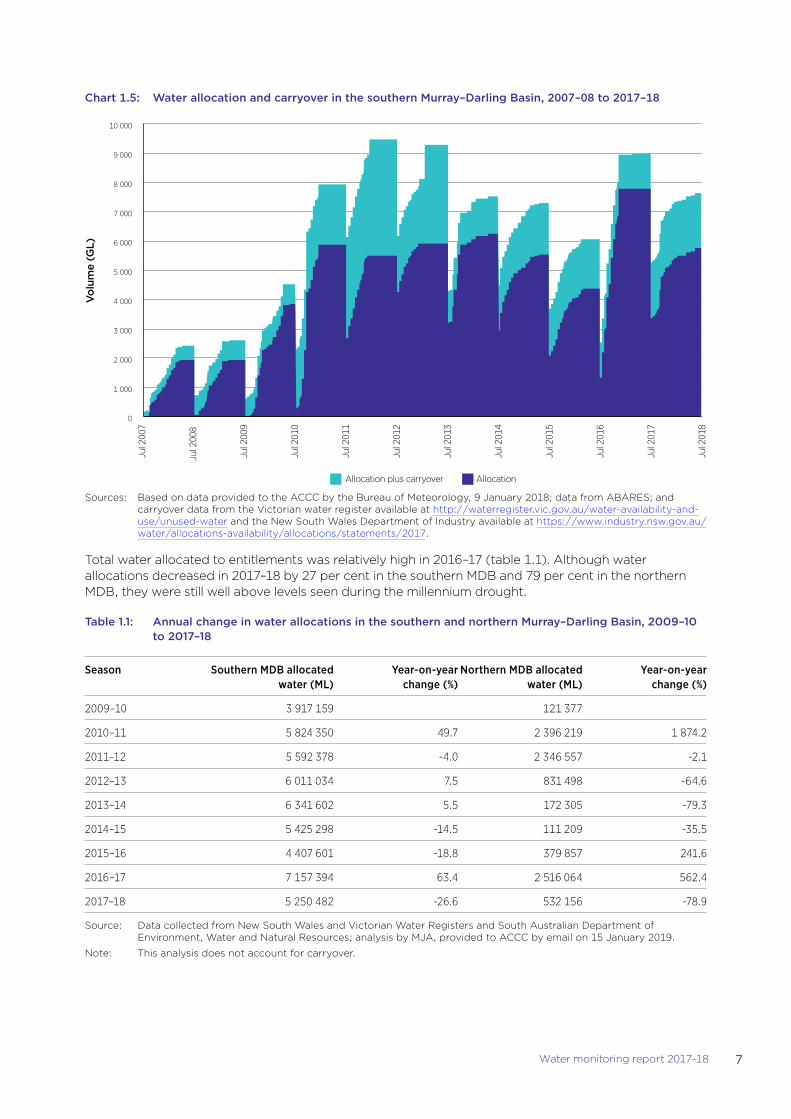

Drought conditions began to emergeThe Murray–Darling Basin (MDB) region experienced generally warmer and drier weather during 2017–18, with drought like conditions emerging in many areas. Water storage levels in the southern MDB fell by 22 per cent and water allocated to entitlements was 28 per cent lower than the previous year. However, water carried over from 2016–17 lessened the impact of the decrease in allocations. As a result water deliveries by on and off-river infrastructure operators (IOs) increased by 9 and 17 per cent respectively. Carryover is an arrangement that allows a person to retain unused water allocation for use, or trade, in the following year. A person’s ability to carryover their unused water allocation is normally dependent on them holding sufficient water access entitlements in that network, and may be subject to adjustments to account of evaporation or other losses or the risk of being lost if storages spill. Carryover arrangements, in conjunction with water markets more generally, are designed to afford water holders improved flexibility in their water use and help to manage risk.

By the end of 2017–18 reduced water availability in New South Wales, along with ongoing dry conditions and poor seasonal forecasts led to areas of New South Wales being considered to be drought affected. The New South Wales Government announced a $500 million Emergency Drought Relief Package on 30 July 2018, including rebates of up to $4000 for the fixed charges components of bills. The majority of general security licence holders (95 per cent) will receive a rebate of the entire amount of fixed charges for 2017–18 bills.

Algal blooms from low water inflows and high temperatures led to a series of mass fish death events in the Lower Darling River in December 2018 and January 2019. This led to calls for a new round of water inquiries and a refocus on the management of the Menindee Lakes, the wider MDB and the Murray–Darling Basin Plan (Basin Plan).

xx Water monitoring report 2017–18

Some areas experienced record prices for traded water entitlementsThe southern connected MDB experienced record prices for most water entitlement types in 2017–18. Underpinning these prices were strong commodity prices and expanded growing area for crops such as cotton in the Murrumbidgee and Murray regions. Expansion of perennial cropping such as almonds continued, increasing concerns about future water deliverability. Demand and competition for irrigation water is driven primarily by the relative profitability of irrigated activities. Higher value crops such as perennial tree nuts are placing a premium on high and general security/reliability water entitlement prices.

In the northern New South Wales entitlement market, increases in general security entitlement prices were observed in the Lachlan, Namoi and Macquarie valleys over 2017–18. This can be attributed to more parcels being sold ‘wet’ with allocation water, strong prices for cotton, and growth of area planted of higher value permanent crops such as citrus and almonds in the Lower Lachlan Valley.

There was widespread debate and many reviews of water policy and governance arrangements in the Murray–Darling BasinDuring 2017–18 and into 2019, planned and ad hoc reviews and evaluations of the MDB policy and governance framework led to or foreshadowed further changes to policy settings and governance arrangements.

The inquiries commissioned following the allegations of water theft and corruption in New South Wales aired on the Australian Broadcasting Corporation’s Four Corners program in July 2017 have now reported their conclusions. In response to the Matthews Review, the New South Wales Government published its Water Reform Action Package. Reforms included the restructuring of the responsible department, the adoption of a new metering framework for irrigators and establishing the Natural Resources Access Regulator (NRAR)as an independent regulator with total carriage of the compliance and enforcement of water management legislation in New South Wales.

The Australian Senate’s inquiry into the integrity of the water market in the MDB reported in November 2018. While the final report acknowledged the majority of submissions supported the Basin Plan, it noted that that the integrity of the water market had been eroded by a lack of transparency with a diminished compliance and enforcement capability. Of concern to some stakeholders, the inquiry noted the lack of provisions for the shepherding of environmental water. The inquiry also supported separating the policy and compliance functions of the Murray–Darling Basin Authority (MDBA).

The South Australian Murray–Darling Basin Royal Commission reported flaws in the implementation of the Water Act 2007 (Cth) (Water Act) and the Basin Plan. The Royal Commission report and its recommendations were substantial. The report noted key aspects of the Basin Plan had not been enacted or implemented in accordance with the objects and purposes of the Water Act, and suggested the Basin Plan is not likely to achieve its objects and purposes or those of the Water Act.

The MDBA issued a formal response to the report, rejecting the commission’s view that the Basin Plan was unlawful or had been made unlawfully. It stated the report did not present any evidence to support the commission’s assertion of maladministration, negligence and unlawful conduct by MDBA officers. The MDBA recognised, however, that the Report ‘draws attention to some important issues’, consistent with the MDBA Report Card and the recent Productivity Commission review. Then Australian Minister for Agriculture and Water Resources, the Hon David Littleproud MP, also responded to the Royal Commission report, declaring the ‘Legal advice to the Commonwealth Government under both sides of politics for the last seven years has been consistent—that the Basin Plan is lawful and was lawfully made’.

xxiWater monitoring report 2017–18

A number of inquiries assessed the policy and governance arrangements in the MDB as well as the status of water reforms. The Productivity Commission’s first five-year assessment of Basin Plan implementation found progress has been made but reform will be required to navigate the complex and challenging upcoming period. Like the Australian Senate’s inquiry to the integrity of the water market in the MDB, the Productivity Commission recommended the MDBA be separated into two institutions—the MDB Agency, which would drive intergovernmental collaboration and strategic service delivery, and the Basin Plan Regulator, which would carry out the MBDA’s compliance and evaluation functions. The Productivity Commission also found that good progress has been made in implementing the National Water Initiative, but that further work remains.

Water charge rules changes move forwardOn 3 April 2019, the Australian Minister for Agriculture and Water Resources made changes to the water charge rules. The Minister had already accepted the ACCC’s advice to remove the requirements for some IOs to prepare network service plans, with this change coming into effect on 1 July 2017. The water charge rules provide for pricing transparency and a framework for the setting of some regulated charges affecting irrigators and rural water infrastructure operators in the MDB. The Minister’s changes followed the ACCC’s advice on amendments, provided in September 2016. The ACCC’s advice was targeted at reducing the regulatory burden, promoting efficient and sustainable use of water infrastructure, facilitating effective water markets and improving pricing transparency.

Under the Minister’s changes, the three existing sets of water charge rules will be combined into the Water Charge Rules 2010. Infrastructure operators will be required to include more information on their schedule of charges about pass-through charges, and to provide more information to their customers about termination fees, which will be calculated using only fixed volumetric charges. Amendments will also largely return price regulation of on-river infrastructure operators back to Basin states’ regulatory frameworks.

The Minister did not accept the ACCC’s advice on strengthening the current non-discrimination provisions or improvements to ensure financial and water distributions are made to customers in reflection of their contribution to the ongoing fixed costs of operating the infrastructure network. In particular, the ACCC had supported expanded non-discrimination provisions as being consistent with and contributing to the achievement of Basin Water Charging Objectives and Principles. In particular, it supported the achievement of ‘user pays’, full cost recovery and avoiding perverse or unintended pricing outcomes.

Although the Minister initially intended these changes to the water charge rules to commence on 1 July 2019, after further consultation, this was postponed until 1 July 2020. The additional time before the changes take effect will allow a smooth and efficient transition to the amended rules.

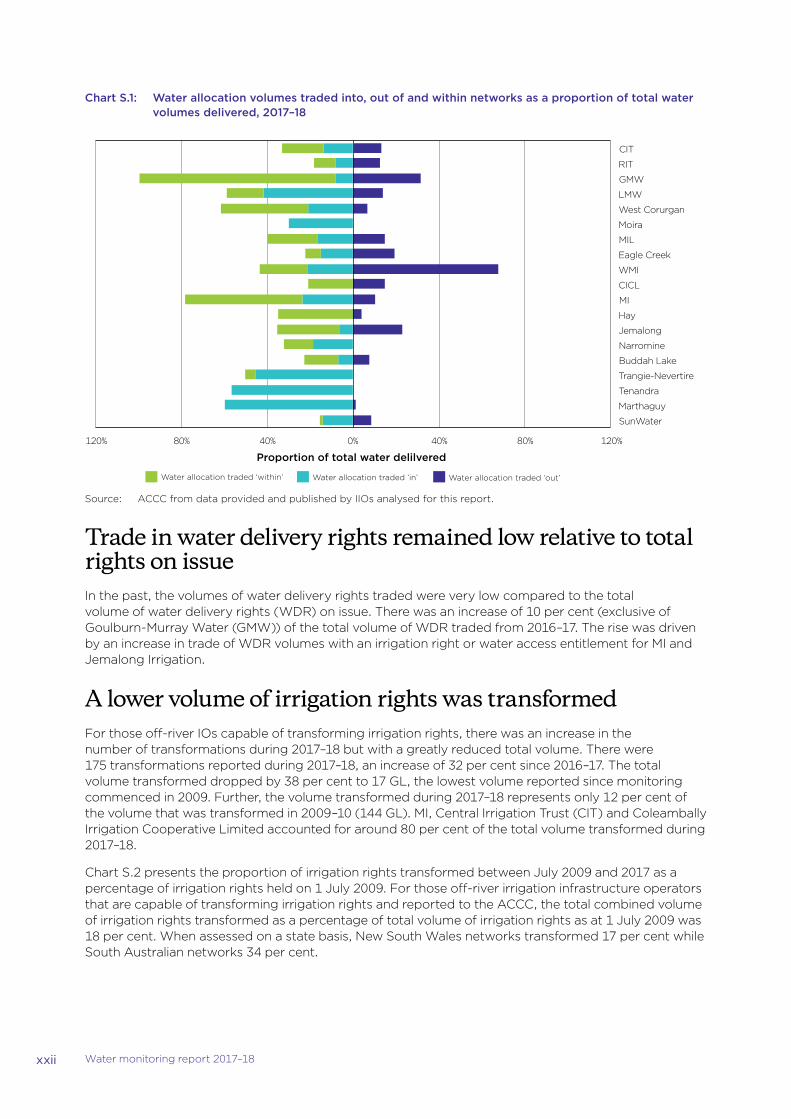

Allocation trade declinedTrade activity for allocations within IO networks monitored by the ACCC declined in 2017–18 by 19 per cent from 4600 GL to 3700 GL, with a net export out of water from the monitored networks. This volume of water was, however, 23 per cent lower than in 2016–17 (chart S.1).

Murrumbidgee Irrigation Limited (MI) and West Corurgan Private Irrigation District both changed from net exporters of water in 2016–17 to net importers in 2017–18. MI’s change was attributed to high demand for water in the region, especially from cotton growers. The West Corurgan increase was partly due to higher demand from irrigators sowing summer crops, and increases in plantings of other crops, such as maize and rice.

xxii Water monitoring report 2017–18

Chart S.1: Water allocation volumes traded into, out of and within networks as a proportion of total water volumes delivered, 2017–18

120% 80% 40% 0% 40% 80% 120%

CIT

RIT

GMW

LMW

West Corurgan

Moira

MIL

Eagle Creek

WMI

CICL

MI

Hay

Jemalong

Narromine

Buddah Lake

Trangie-Nevertire

Tenandra

Marthaguy

SunWater

Water allocation traded ‘out’Water allocation traded ‘in’ Water allocation traded ‘within’

Proportion of total water delilvered

Source: ACCC from data provided and published by IIOs analysed for this report.

Trade in water delivery rights remained low relative to total rights on issueIn the past, the volumes of water delivery rights traded were very low compared to the total volume of water delivery rights (WDR) on issue. There was an increase of 10 per cent (exclusive of Goulburn-Murray Water (GMW)) of the total volume of WDR traded from 2016–17. The rise was driven by an increase in trade of WDR volumes with an irrigation right or water access entitlement for MI and Jemalong Irrigation.

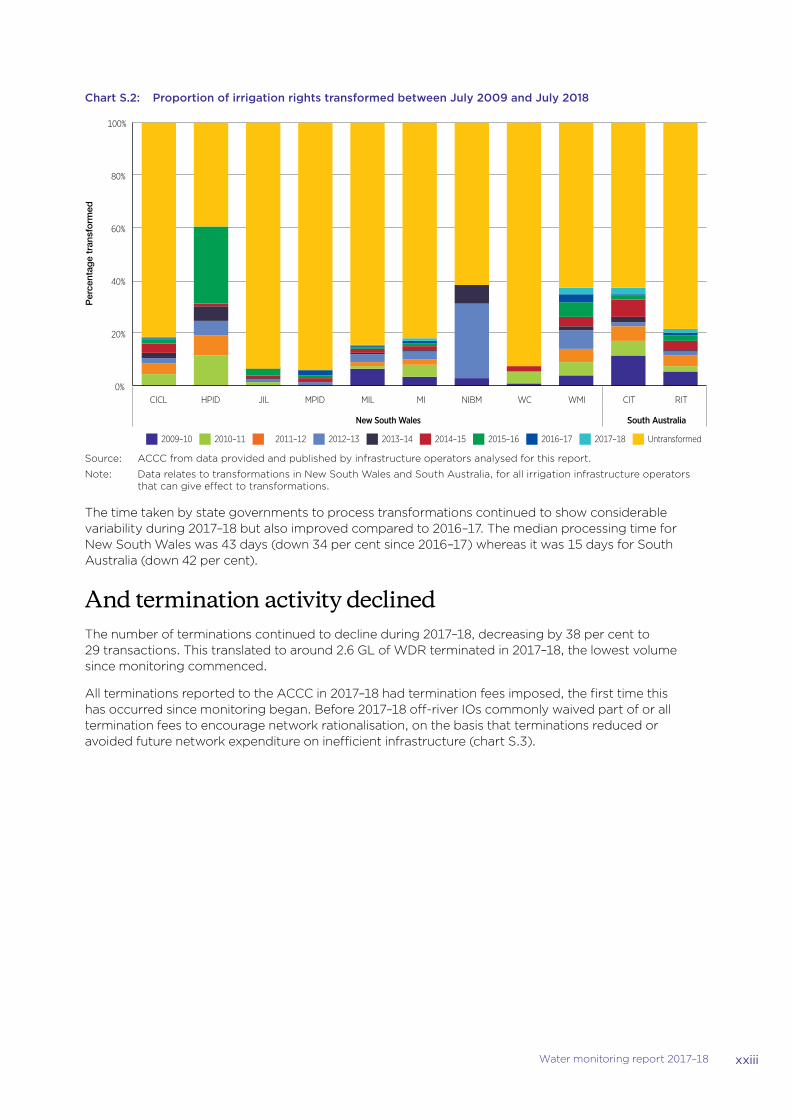

A lower volume of irrigation rights was transformedFor those off-river IOs capable of transforming irrigation rights, there was an increase in the number of transformations during 2017–18 but with a greatly reduced total volume. There were 175 transformations reported during 2017–18, an increase of 32 per cent since 2016–17. The total volume transformed dropped by 38 per cent to 17 GL, the lowest volume reported since monitoring commenced in 2009. Further, the volume transformed during 2017–18 represents only 12 per cent of the volume that was transformed in 2009–10 (144 GL). MI, Central Irrigation Trust (CIT) and Coleambally Irrigation Cooperative Limited accounted for around 80 per cent of the total volume transformed during 2017–18.

Chart S.2 presents the proportion of irrigation rights transformed between July 2009 and 2017 as a percentage of irrigation rights held on 1 July 2009. For those off-river irrigation infrastructure operators that are capable of transforming irrigation rights and reported to the ACCC, the total combined volume of irrigation rights transformed as a percentage of total volume of irrigation rights as at 1 July 2009 was 18 per cent. When assessed on a state basis, New South Wales networks transformed 17 per cent while South Australian networks 34 per cent.

xxiiiWater monitoring report 2017–18

Chart S.2: Proportion of irrigation rights transformed between July 2009 and July 2018P

erce

ntag

e tr

ansf

orm

ed

0%

20%

40%

60%

80%

100%

CICL HPID JIL MPID MIL MI NIBM WC WMI CIT RIT

New South Wales South Australia

2009–10 2010–11 2011–12 2012–13 2013–14 2014–15 2015–16 2016–17 2017–18 Untransformed

Source: ACCC from data provided and published by infrastructure operators analysed for this report.

Note: Data relates to transformations in New South Wales and South Australia, for all irrigation infrastructure operators that can give effect to transformations.

The time taken by state governments to process transformations continued to show considerable variability during 2017–18 but also improved compared to 2016–17. The median processing time for New South Wales was 43 days (down 34 per cent since 2016–17) whereas it was 15 days for South Australia (down 42 per cent).

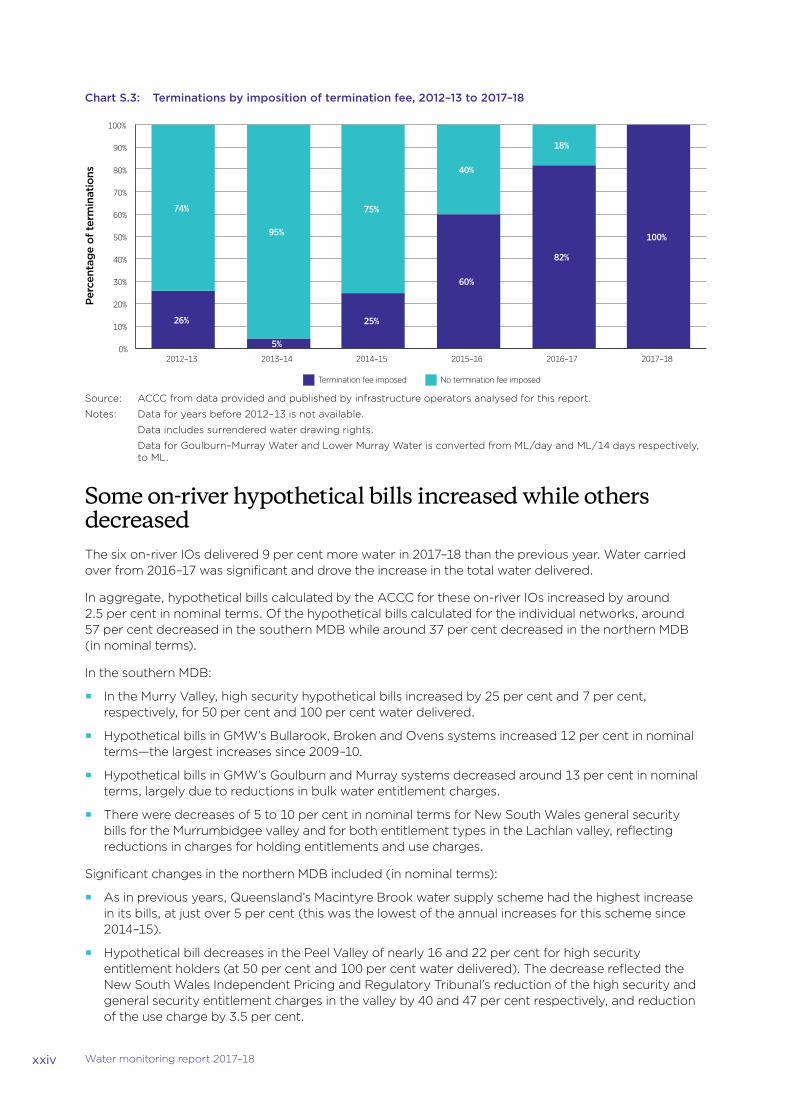

And termination activity declinedThe number of terminations continued to decline during 2017–18, decreasing by 38 per cent to 29 transactions. This translated to around 2.6 GL of WDR terminated in 2017–18, the lowest volume since monitoring commenced.

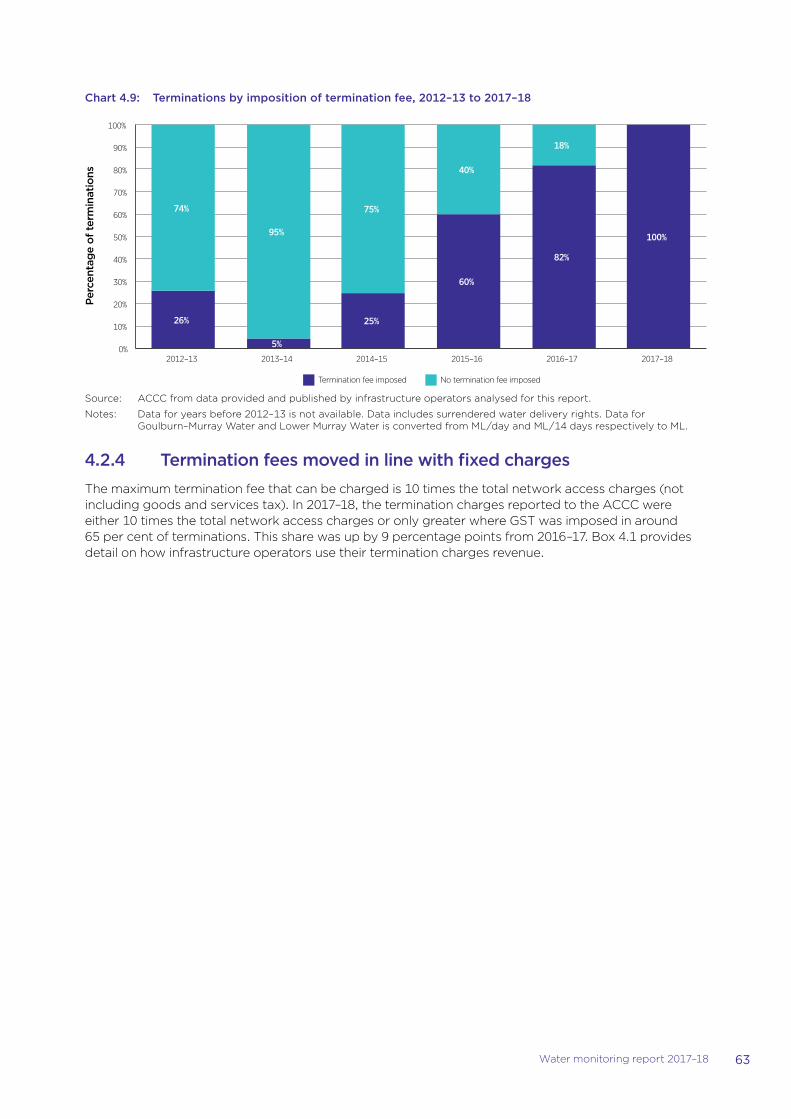

All terminations reported to the ACCC in 2017–18 had termination fees imposed, the first time this has occurred since monitoring began. Before 2017–18 off-river IOs commonly waived part of or all termination fees to encourage network rationalisation, on the basis that terminations reduced or avoided future network expenditure on inefficient infrastructure (chart S.3).

xxiv Water monitoring report 2017–18

Chart S.3: Terminations by imposition of termination fee, 2012–13 to 2017–18

26%

5%

25%

60%

82%

100%

74%

95%

75%

40%

18%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012–13 2013–14 2014–15 2015–16 2016–17 2017–18

Termination fee imposed No termination fee imposed

Perc

enta

ge

of t

erm

inat

ions

Source: ACCC from data provided and published by infrastructure operators analysed for this report.

Notes: Data for years before 2012–13 is not available.

Data includes surrendered water drawing rights.

Data for Goulburn–Murray Water and Lower Murray Water is converted from ML/day and ML/14 days respectively, to ML.

Some on-river hypothetical bills increased while others decreasedThe six on-river IOs delivered 9 per cent more water in 2017–18 than the previous year. Water carried over from 2016–17 was significant and drove the increase in the total water delivered.

In aggregate, hypothetical bills calculated by the ACCC for these on-river IOs increased by around 2.5 per cent in nominal terms. Of the hypothetical bills calculated for the individual networks, around 57 per cent decreased in the southern MDB while around 37 per cent decreased in the northern MDB (in nominal terms).

In the southern MDB:

�� In the Murry Valley, high security hypothetical bills increased by 25 per cent and 7 per cent, respectively, for 50 per cent and 100 per cent water delivered.

�� Hypothetical bills in GMW’s Bullarook, Broken and Ovens systems increased 12 per cent in nominal terms—the largest increases since 2009–10.

�� Hypothetical bills in GMW’s Goulburn and Murray systems decreased around 13 per cent in nominal terms, largely due to reductions in bulk water entitlement charges.

�� There were decreases of 5 to 10 per cent in nominal terms for New South Wales general security bills for the Murrumbidgee valley and for both entitlement types in the Lachlan valley, reflecting reductions in charges for holding entitlements and use charges.

Significant changes in the northern MDB included (in nominal terms):

�� As in previous years, Queensland’s Macintyre Brook water supply scheme had the highest increase in its bills, at just over 5 per cent (this was the lowest of the annual increases for this scheme since 2014–15).

�� Hypothetical bill decreases in the Peel Valley of nearly 16 and 22 per cent for high security entitlement holders (at 50 per cent and 100 per cent water delivered). The decrease reflected the New South Wales Independent Pricing and Regulatory Tribunal’s reduction of the high security and general security entitlement charges in the valley by 40 and 47 per cent respectively, and reduction of the use charge by 3.5 per cent.

xxvWater monitoring report 2017–18

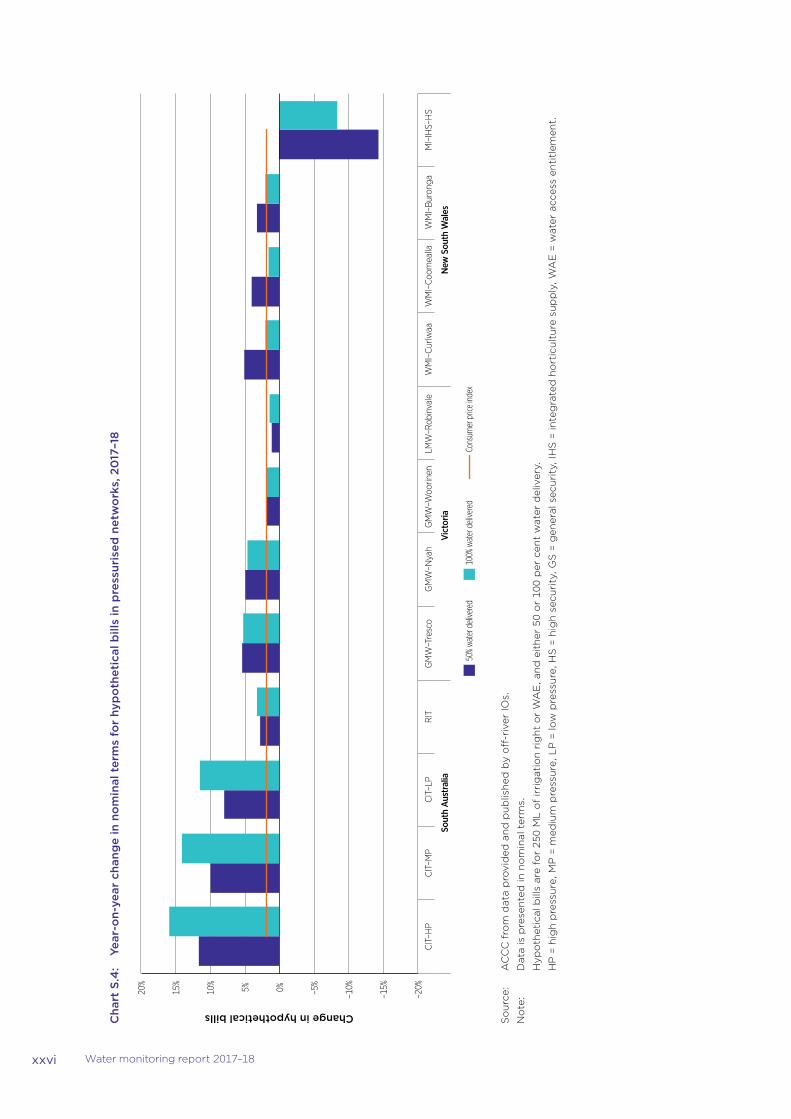

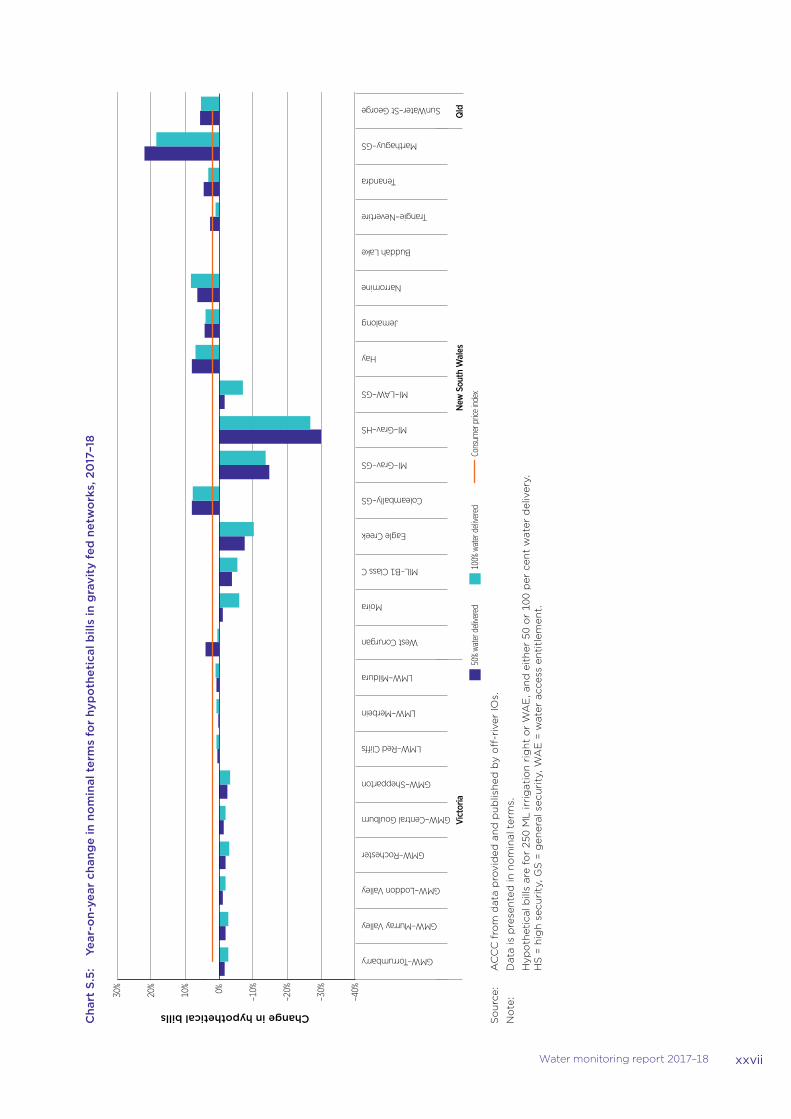

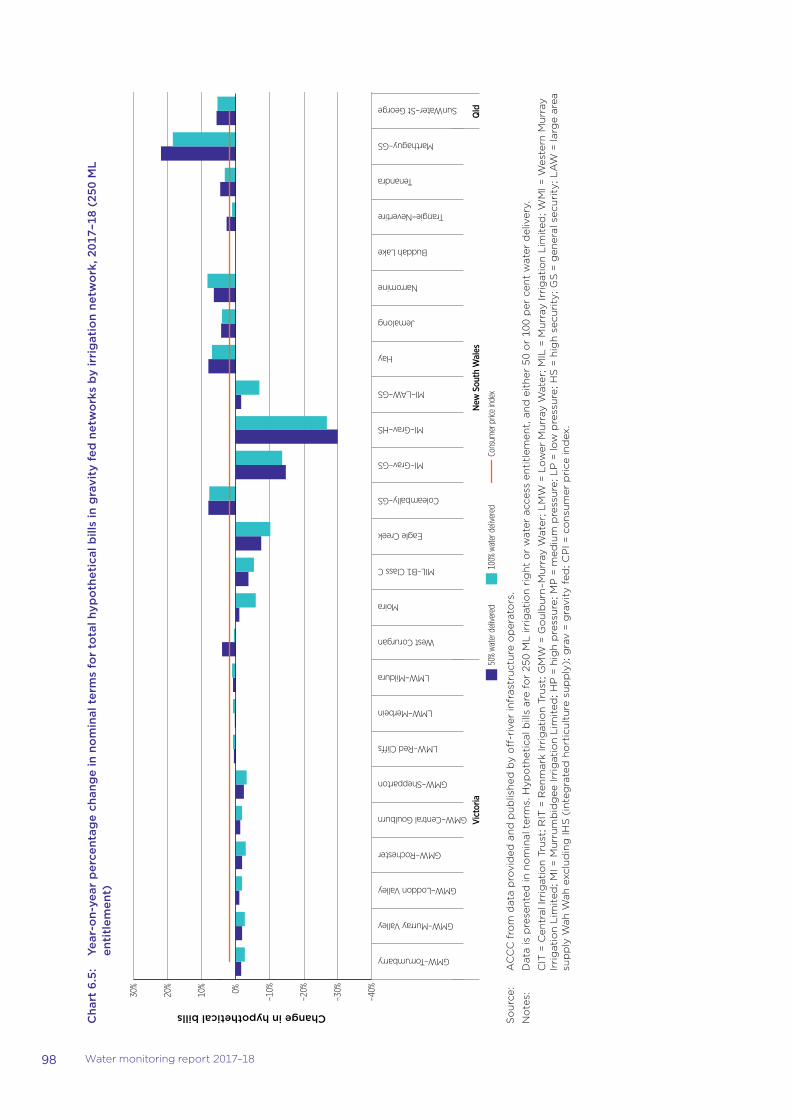

Off-river hypothetical bills continued to increase for most networksAcross both pressurised and gravity fed networks, 60 per cent of hypothetical bills had increases in nominal terms during 2017–18, two percentage points below the equivalent figure in 2016–17. Of those networks that had increases, 49 per cent were in excess of the consumer price index (CPI) (charts S.4 and S.5)

In aggregate, the average growth for all pressurised hypothetical bills was 4 per cent in nominal terms since 2017–18. Within this type network, all hypothetical bills apart from MI increased during 2017–18. Of those that increased, 75 per cent had a rise exceeding CPI. The average aggregate increase in gravity fed networks was less than 1 per cent in nominal terms since 2016–17. Around 56 per cent of these networks had increases in hypothetical bills and only 36 per cent of these exceeded CPI.

Within individual networks, we observed:

�� For pressurised networks, the largest increase in a hypothetical bill over the past 12 months was CIT, increasing by 16 percent in nominal terms for 100 per cent of water delivered. This rise reflected increases in its variable use fee which increased by 38 per cent for peak services. CIT’s medium pressure hypothetical bills had the second highest increase with a rise of 14 per cent in nominal terms, also reflecting increases in variable use fees.

�� Marthaguy Irrigation Scheme had the largest increase in hypothetical bills within gravity fed networks with rises of 22 and 19 per cent in nominal terms (for 50 and 100 per cent water delivered). Until 2017–18 Marthaguy’s off-river charges had not changed since 2011–12. Marthaguy’s operating and maintenance fee rose by 39 per cent and its pumping charge rose by 15 per cent

xxvi Water monitoring report 2017–18

Cha

rt S

.4:

Year

-on-

year

cha

nge

in n

om

inal

ter

ms

for

hyp

oth

etic

al b

ills

in p

ress

uris

ed n

etw

ork

s, 2

017

–18

–20%

–15%

–10%

–5%

0%

5%

10%

15%

20%

CIT

–HP

CIT

–MP

CIT

–LP

RIT

G

MW

–Tre

sco

GM

W–N

yah

GM

W–W

oorin

en

LMW

–Rob

inva

le

WM

I–C

urlw

aa

WM

I–Co

omea

lla

WM

I–B

uron

ga

MI–

IHS–

HS

Sout

h A

ustr

alia

Vict

oria

New

Sou

th W

ales

50% water delivered

100% water delivered

Consum

er price index

Change in hypothetical bills

So

urc

e:

AC

CC

fro

m d

ata

pro

vid

ed a

nd

pu

blis

hed

by

off

-riv

er IO

s.

No

te:

Dat

a is

pre

sen

ted

in n

om

inal

ter

ms.

H

ypo

thet

ical

bill

s ar

e fo

r 25

0 M

L o

f ir

rig

atio

n r

igh

t o

r W

AE

, an

d e

ith

er 5

0 o

r 10

0 p

er c

ent

wat

er d

eliv

ery.

H

P =

hig

h p

ress

ure

, MP

= m

ediu

m p

ress

ure

, LP

= lo

w p

ress

ure

, HS

= h

igh

sec

uri

ty, G

S =

gen

eral

sec

uri

ty, I

HS

= in

teg

rate

d h

ort

icu

ltu

re s

up

ply

, WA

E =

wat

er a

cces

s en

titl

emen

t.

xxviiWater monitoring report 2017–18

Cha

rt S

.5:

Year

-on-

year

cha

nge

in n

om

inal

ter

ms

for

hyp

oth

etic

al b

ills

in g

ravi

ty f

ed n

etw

ork

s, 2

017

–18

–40%

–30%

–20%

–10%

0%

10%

20%

30%

GMW–Torrumbarry

GMW–Murray Valley

GMW–Loddon Valley

GMW–Rochester

GMW–Central Goulburn

GMW–Shepparton

LMW–Red Cli�s

LMW–Merbein

LMW–Mildura

West Corurgan

Moira

MIL–B1 Class C

Eagle Creek

Coleambally–GS

MI–Grav–GS

MI–Grav–HS

MI–LAW–GS

Hay

Jemalong

Narromine

Buddah Lake

Trangie–Nevertire

Tenandra

Marthaguy–GS

SunWater–St George

Vict

oria

N

ew S

outh

Wal

esQ

ld

Change in hypothetical bills

50% water delivered

100% water delivered

Consum

er price index

So

urc

e:

AC

CC

fro

m d

ata

pro

vid

ed a

nd

pu

blis

hed

by

off

-riv

er IO

s.

No

te:

Dat

a is

pre

sen

ted

in n

om

inal

ter

ms.

H

ypo

thet

ical

bill

s ar

e fo

r 25

0 M

L ir

rig

atio

n r

igh

t o

r W

AE

, an

d e

ith

er 5

0 o

r 10

0 p

er c

ent

wat

er d

eliv

ery.

H

S =

hig

h s

ecu

rity

, GS

= g

ener

al s

ecu

rity

, WA

E =

wat

er a

cces

s en

titl

emen

t.

xxviii Water monitoring report 2017–18

Increases in off-river charges drove the majority of rises in hypothetical billsAcross both pressurised and gravity fed networks, around 86 per cent of off-river IO hypothetical bill changes were driven by either increases or decreases in off-river charges in dollar terms, rather than changes in water planning and management (WPM) or on-river charges (75 per cent for pressurised networks and 88 per cent for gravity fed). Changes in off-river charges contributed to increases for all pressurised network hypothetical bills, but in gravity fed networks, changes in these charges drove decreases in 40 per cent of network bills.

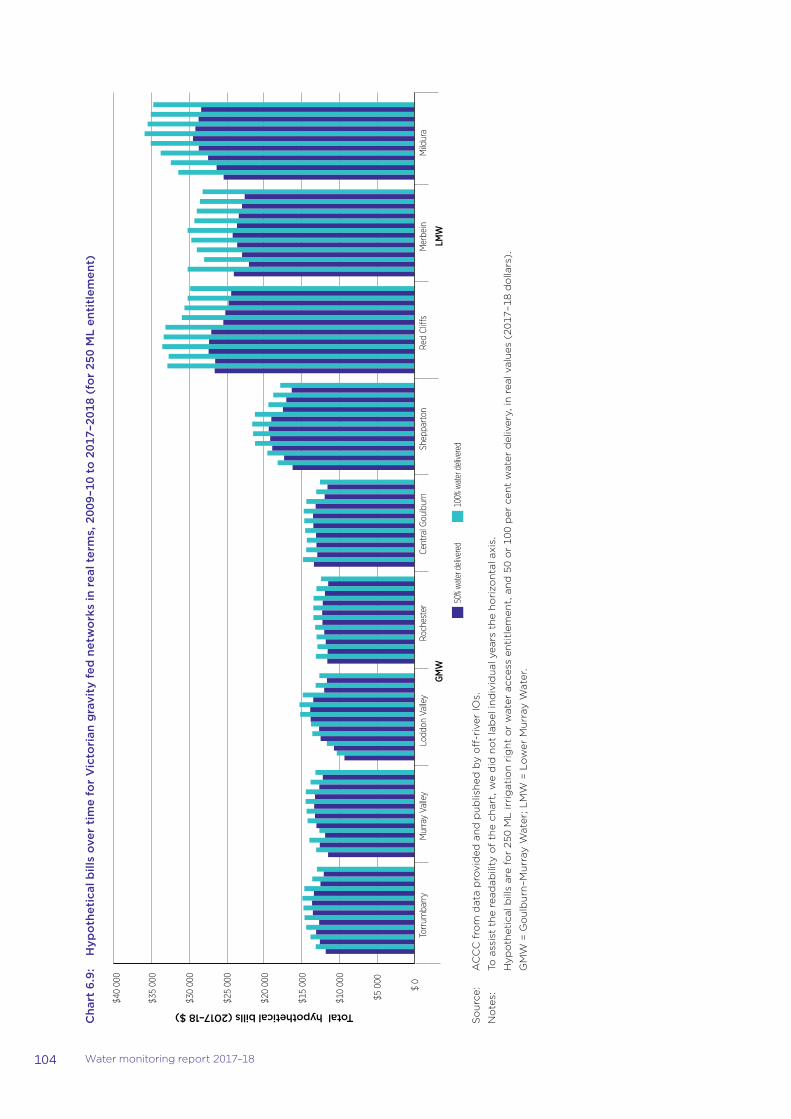

While hypothetical bills have generally increased from 2009–10, average increases have not been excessiveThe average aggregate bill change including both 50 and 100 per cent allocations from 2009–10 to 2017–18 was 12 per cent in real terms (reflecting both increases and decreases in networks). By network type, the average aggregate bill change was 12 per cent in pressurised networks and 11 per cent in real terms in gravity fed networks. Other observations include:

�� around 27 per cent of the hypothetical bills decreased over the period from 2009–10 to 2017–18 (both in real terms)

�� between network types there was considerable variation with 8 per cent of hypothetical bills in pressurised networks decreasing over this period and 36 per cent of hypothetical bills in gravity fed networks decreasing (both in real terms)

�� in pressurised networks, the largest percentage increase occurred at GMW’s Nyah network with rises of 43 and 32 per cent in real terms for 50 and 100 per cent water allocation respectively

�� Tenandra had the largest increase of the gravity fed networks with its hypothetical bills increasing by 162 per cent (50 per cent allocation) and 166 per cent (100 per cent allocation) in real terms. Other large increases include Hay Private Irrigation District with growth of 82 and 56 per cent for 100 and 50 per cent allocation respectively.

There are significant differences between each Basin State’s water planning and management arrangementsBasin state water authorities and departments undertake a range of water planning and management activities to promote sustainability of water use, maintain ecosystem health, and minimise the impact of water extraction. These authorities and departments also impose charges to recover a proportion of the expenditure associated with these activities.

Both the New South Wales Department of Industry (Water) and WaterNSW increased their spending on water planning in 2017–18, driving a 25.1 per cent increase in New South Wales’ total WPM expenditure in the MDB. WPM revenue collected by WaterNSW remained relatively stable in 2017–18. The New South Wales Government established the NRAR as an independent regulator with total carriage of the compliance and enforcement of New South Wales water management legislation.

Victoria spent an additional $30 million on Water for Victoria projects across the state in 2017–18. The majority of Victoria’s WPM revenue in the MDB continues to be collected by the Victorian Department of Environment, Land, Water and Planning through the environmental contribution levy. The proportion of Victoria’s WPM revenue collected by regional water authorities continues to grow, however, reaching 20.4 per cent in 2017–18.

South Australia announced planned reforms to the legislation establishing its WPM regime, though these did not come into effect in 2017–18. Accordingly, the state’s WPM expenditure and revenue remained relatively constant in 2017–18.

Queensland’s Department of Natural Resources, Mining and the Energy (DNRME) cannot provide the ACCC with data on their WPM spending. DNRME collected 46 per cent less revenue in 2017–18 than

xxixWater monitoring report 2017–18

in 2016–17, bringing Queensland’s WPM revenues closer to pre-2016–17 levels, following a spike in that year.

ACT’s expenditure on WPM activities fell by over 40 per cent in 2017–18. This fall, coupled with a slight increase in WPM revenue, led to ACT’s WPM revenue being nearly double its spending in 2017–18.

Complaints increased slightly during 2017–18 but compliance with the water market and water charge rules is generally goodWe received 14 complaints and inquiries about the water market or water charge rules (the Rules) in 2017–18, more than half of these from irrigators. This represents a small increase since 2016–17 (when we received 10 complaints and inquiries), but Rule-related complaints and enquiries have declined markedly since 2011–12 (71 complaints).

In 2017–18 the ACCC conducted three initial investigations (prompted by complaints or ACCC compliance reviews) of possible breaches of the water charge rules and two initial investigations into breaches of the Australian Consumer Law (ACL). One of the initial ACL investigations is ongoing. No breaches of the Rules or ACL that resulted in serious detriment to irrigators or other stakeholders were found. On each occasion, the IO or water market intermediary under investigation was cooperative and willing to follow the ACCC’s guidance to achieve compliance. As in previous years, this affirms our impression of a generally good compliance culture among IOs.

Nevertheless, we will continue to work with irrigators and IOs to educate them about their rights and responsibilities, and the need for compliance with the Rules (including amendments) to ensure transparency in regulated water charges and confidence in the water market by all stakeholders.

In 2018–19 we will undertake monitoring and compliance activities that promote informed and well-functioning markets for water (and related rights and services). To this end, we will focus on trade barriers relating to transformations, pricing transparency and stakeholder education about the water charge rule changes that take effect on 1 July 2020.

xxx Water monitoring report 2017–18

Drought and water deliverability challenges loomed

Almond crop in Murray-Darling Basin Source: iStockphoto

01

2 Water monitoring report 2017–18

1. Drought and water deliverability challenges loomed

Key points

�� Seasonal conditions were drier in 2017–18 than the previous year across much of the country.

�� In the southern Murray–Darling Basin (MDB), water storage levels fell and water allocated to entitlements was also lower, but water carried over from previous years helped to buffer the lower water allocations.

�� Prices for water allocations rose and there were record entitlements prices in the southern connected MDB.

�� Irrigators are changing their mix of water market products, selling entitlements to free up capital and supplementing their annual water needs through products such as leases, spot and forward contracts.

�� Electricity prices continue to create pressure on irrigators and operators to decrease their energy costs. Joint purchasing agreements may offer a vehicle for some infrastructure operators to constrain their energy costs.

�� Expansion of perennial cropping continued, raising some concerns about future water deliverability.

This chapter provides a snapshot of key influences on irrigation water use in 2017–18. It also describes other significant factors affecting the environment in which infrastructure operators (IOs) and irrigators operate:

�� Section 1.1 describes seasonal conditions, which influence both water availability and the water needs of crops.

�� Section 1.2 looks at water available in storages, water allocations and carryover across the Murray–Darling Basin (MDB).

�� Section 1.3 provides an overview of water allocation trading in 2017–18, while section 1.4 looks at water access entitlement (WAE) trades and prices.

�� Section 1.5 examines the introduction by New South Wales of a rebate for fixed charges.

�� Section 1.6 looks at the price of electricity (a major input cost for IOs and for many irrigators) and section 1.7 considers implications for water use of increases in cotton and almond planting.

�� Section 1.8 describes recent mass fish deaths and the response by government.

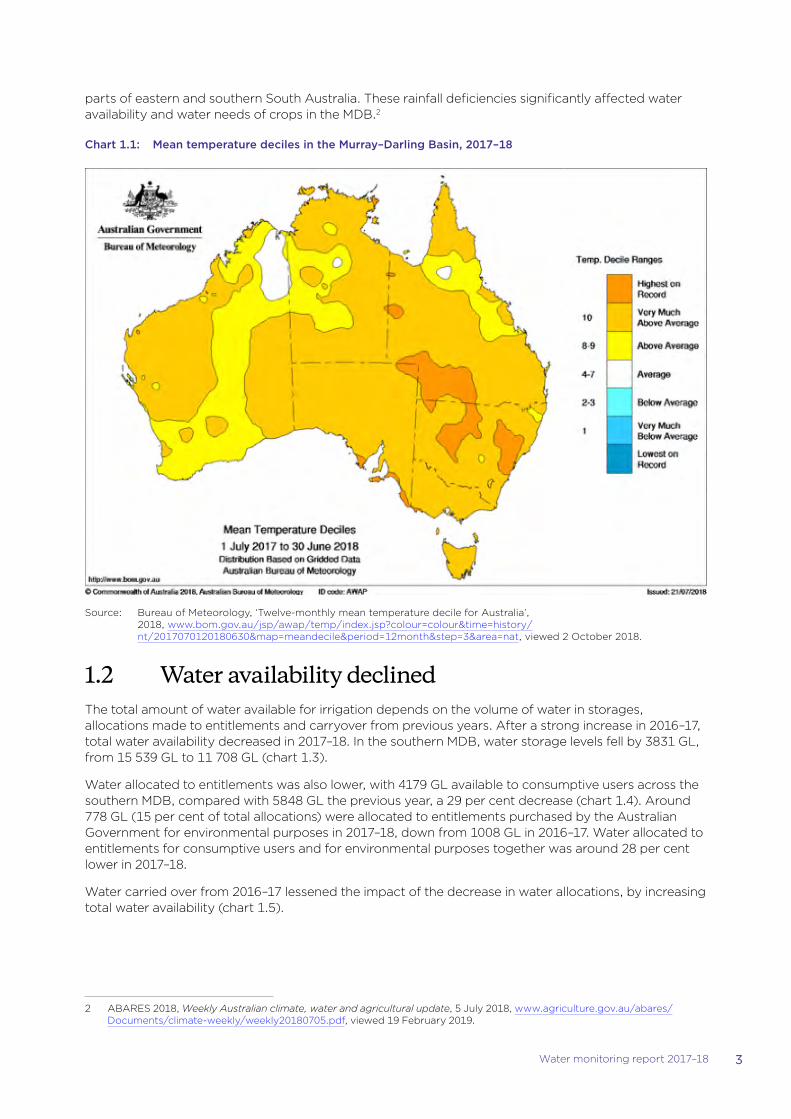

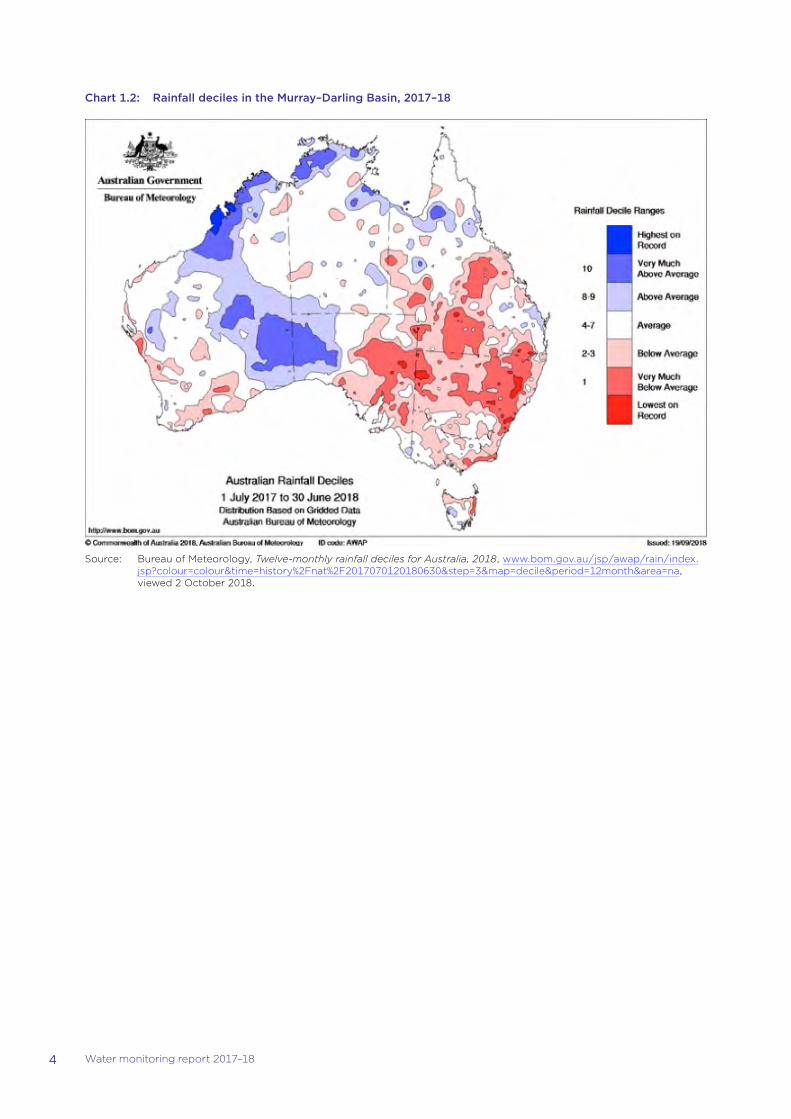

1.1 Seasonal conditions were drier than in previous years

Many regions throughout the MDB experienced mean temperatures well above average (chart 1.1) and below average rainfall (chart 1.2). After a dry winter, the southern MDB received welcome rain in November and December 2017, and some areas in southern New South Wales and Victoria experienced the wettest December day on record.1

However, by the end of June 2018 the Australian Bureau of Agricultural and Resource Economics and Sciences (ABARES) reported that rainfall deficiencies had increased across large parts of eastern Australia and southern South Australia. There were serious to severe rainfall deficiencies across large areas of New South Wales, large areas of southern to central Queensland, parts of eastern Victoria, and

1 Bureau of Meteorology, ‘Australia in December 2017’, http://www.bom.gov.au/climate/current/month/aus/archive/201712.summary.shtml, viewed 5 March 2019.

3Water monitoring report 2017–18

parts of eastern and southern South Australia. These rainfall deficiencies significantly affected water availability and water needs of crops in the MDB.2

Chart 1.1: Mean temperature deciles in the Murray–Darling Basin, 2017–18

Source: Bureau of Meteorology, ‘Twelve-monthly mean temperature decile for Australia’, 2018, www.bom.gov.au/jsp/awap/temp/index.jsp?colour=colour&time=history/nt/2017070120180630&map=meandecile&period=12month&step=3&area=nat, viewed 2 October 2018.

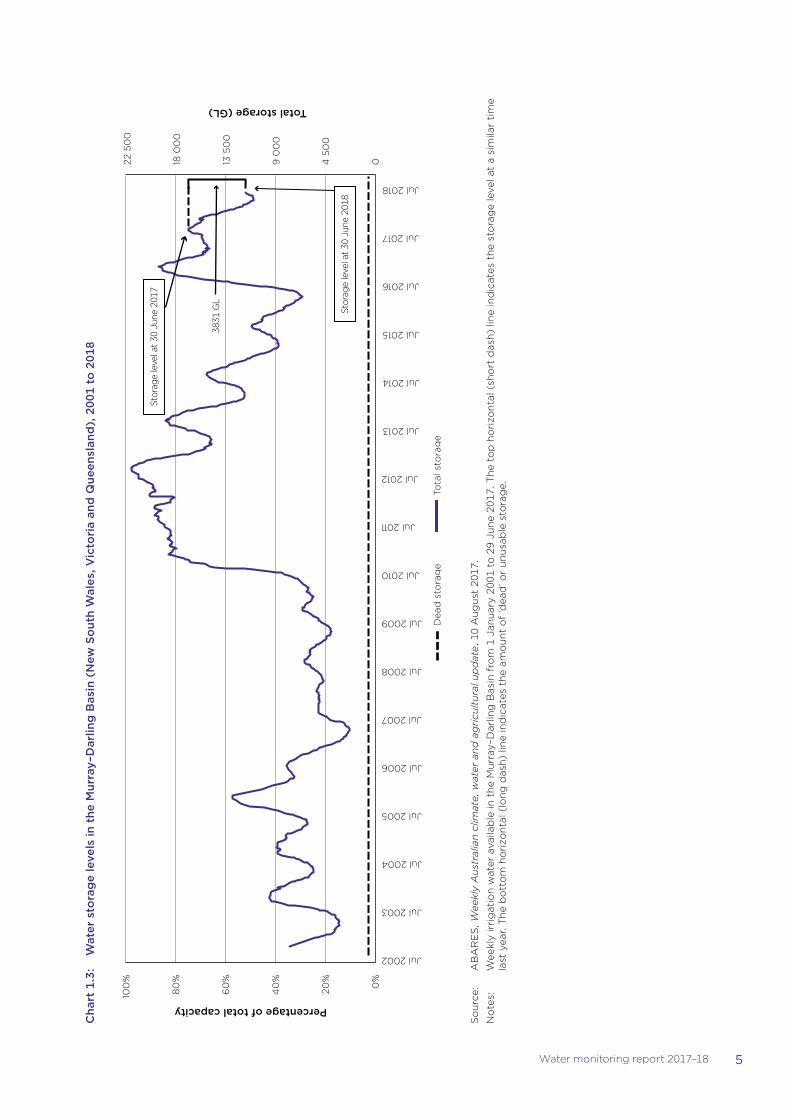

1.2 Water availability declinedThe total amount of water available for irrigation depends on the volume of water in storages, allocations made to entitlements and carryover from previous years. After a strong increase in 2016–17, total water availability decreased in 2017–18. In the southern MDB, water storage levels fell by 3831 GL, from 15 539 GL to 11 708 GL (chart 1.3).

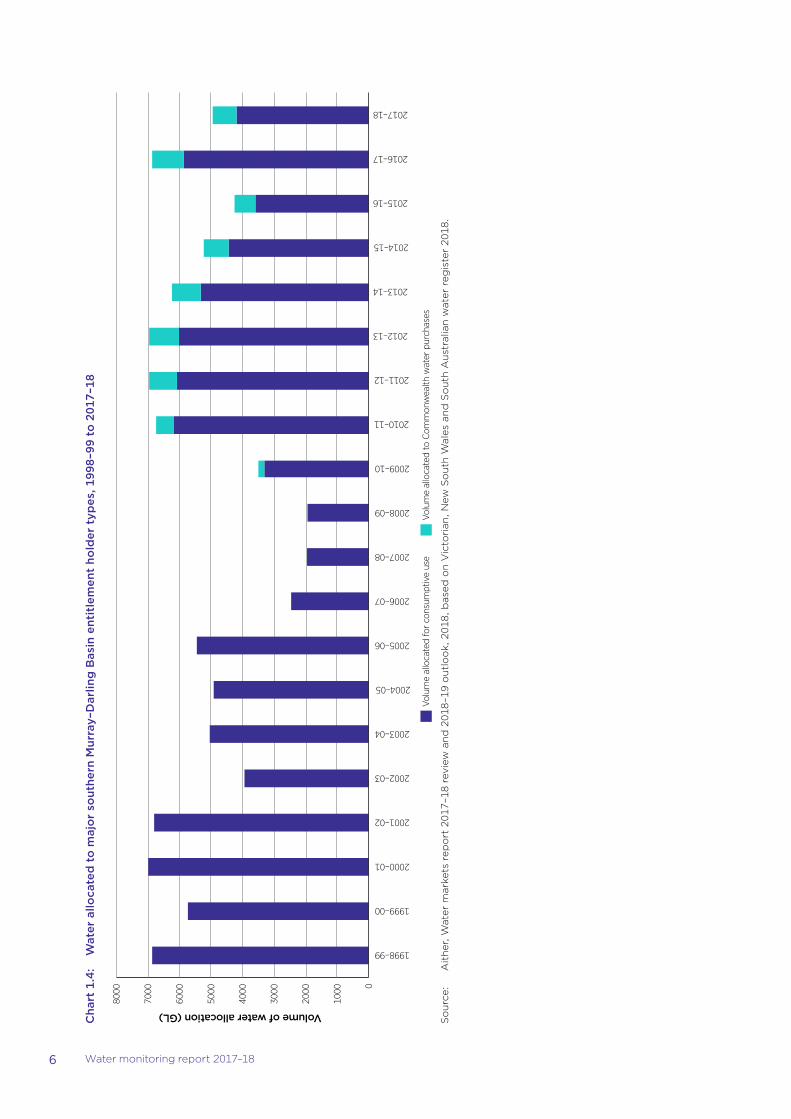

Water allocated to entitlements was also lower, with 4179 GL available to consumptive users across the southern MDB, compared with 5848 GL the previous year, a 29 per cent decrease (chart 1.4). Around 778 GL (15 per cent of total allocations) were allocated to entitlements purchased by the Australian Government for environmental purposes in 2017–18, down from 1008 GL in 2016–17. Water allocated to entitlements for consumptive users and for environmental purposes together was around 28 per cent lower in 2017–18.

Water carried over from 2016–17 lessened the impact of the decrease in water allocations, by increasing total water availability (chart 1.5).

2 ABARES 2018, Weekly Australian climate, water and agricultural update, 5 July 2018, www.agriculture.gov.au/abares/Documents/climate-weekly/weekly20180705.pdf, viewed 19 February 2019.

4 Water monitoring report 2017–18

Chart 1.2: Rainfall deciles in the Murray–Darling Basin, 2017–18

Source: Bureau of Meteorology, Twelve-monthly rainfall deciles for Australia, 2018, www.bom.gov.au/jsp/awap/rain/index.jsp?colour=colour&time=history%2Fnat%2F2017070120180630&step=3&map=decile&period=12month&area=na, viewed 2 October 2018.

5Water monitoring report 2017–18

Cha

rt 1

.3:

Wat

er s

tora

ge

leve

ls in

the

Mur

ray–

Dar

ling

Bas

in (

New

So

uth

Wal

es, V

icto

ria

and

Que

ensl

and

), 2

001

to 2

018

Stor

age

leve

l at

30 J

une

2017

Stor

age

leve

l at

30 J

une

2018

3831

GL

0

4 5

00

9 0

00

13 5

00

18 0

00

22 5

00

0%

20%

40

%

60

%

80

%

100

%

Jul 2002

Jul 2003

Jul 2004

Jul 2005

Jul 2006

Jul 2007

Jul 2008

Jul 2009

Jul 2010

Jul 2011

Jul 2012

Jul 2013

Jul 2014

Jul 2015

Jul 2016

Jul 2017

Jul 2018

Total storage (GL)

Percentage of total capacity

Dea

d s

tora

ge

Tota

l sto

rag

e

So

urc

e:

AB

AR

ES

, Wee

kly

Au

stra

lian

clim

ate,

wat

er a

nd

ag

ricu

ltu

ral u

pd

ate,

10

Au

gu

st 2

017.

No

tes:

W

eekl

y ir

rig

atio

n w

ater

ava

ilab

le in

th

e M

urr

ay–D

arlin

g B

asin

fro

m 1

Jan

uar

y 20

01 t

o 2

9 Ju

ne

2017

. Th

e to

p h

ori

zon

tal (

sho

rt d

ash

) lin

e in

dic

ates

th

e st

ora

ge

leve

l at

a si

mila

r ti

me

last

yea

r. T

he

bo

tto

m h

ori

zon

tal (

lon

g d

ash

) lin

e in

dic

ates

th

e am

ou

nt

of

‘dea

d’ o

r u

nu

sab

le s