Embed Size (px)

DESCRIPTION

Walt Disney - Content Is King analyses Walt Disney's successful business strategy that led to an annualized growth rate of 20% and makes specific recommendations as to how Disney could maintain its industry-beating growth rate.

Citation preview

© 2001 Peter Louis. All Rights Reserved

1

The Walt Disney Company

“Content is King”

By Peter Louis

Instituto de Empresa

December 2001

© 2001 Peter Louis. All Rights Reserved

2

Agenda

Disney’s strategy

Is there a competitive advantage?

Current strategic challenges

Recommendations

Conclusions

© 2001 Peter Louis. All Rights Reserved

3

Disney’s strategy

1. Strong corporate culture

2. Innovative brands

3. Employee “buy-in”

4. Diversification

© 2001 Peter Louis. All Rights Reserved

4

Strong corporate culture

This was based on TCC:

– Teamwork

– Communication

– Co-operation

© 2001 Peter Louis. All Rights Reserved

5

Innovative brands

Develop brands that were:

– Highly differentiated

– Were wholesome and expressed American values

– Fun and fallible

© 2001 Peter Louis. All Rights Reserved

6

Employee “buy-in”

Employee identification made them:

– Customer focused

– Customer friendly

© 2001 Peter Louis. All Rights Reserved

7

Diversification

Brand extension

– 2 versions of Winnie-the-Pooh

Channel occupation

– Beauty & the Beast, the movie

– Beauty & the Beast, the Broadway musical

© 2001 Peter Louis. All Rights Reserved

8

Is there a competitive

advantage?

© 2001 Peter Louis. All Rights Reserved

9

19992000

2001

Sony

Disney

Coca Cola

0

10

20

30

40

50

60

70

80

90

$ billions

Years

World's Most Favorite Brands

Source: Interbrand,

Citigroup

Company 1999 2000 2001

Coca Cola 1 1 1

Disney 6 8 7

Sony 18 18 20

Rank

Source: Interbrand, Citigroup

Brand Value

Company 1999 2000 2001

Coca Cola 83.8 72.5 68.9

Disney 32.3 33.6 32.6

Sony 14.2 16.4 15

Source: Interbrand, Citigroup

Disney’s brand equity

© 2001 Peter Louis. All Rights Reserved

10

Yes!

© 2001 Peter Louis. All Rights Reserved

11

Is it sustainable?

© 2001 Peter Louis. All Rights Reserved

12

Yes…

© 2001 Peter Louis. All Rights Reserved

13

but only if

Disney continues to both:

1. Innovate

2. Update the competitive advantage

© 2001 Peter Louis. All Rights Reserved

14

Current Strategic

Challenges

© 2001 Peter Louis. All Rights Reserved

15

Current strategic challenges

1. Recession & September 11

2. ABC

3. Talent drain

4. Where’s Mickey’s magic touch?

5. Video Games

6. Context is Queen

© 2001 Peter Louis. All Rights Reserved

16

Recession & September 11

Slow down: Trans Atlantic / Pacific flights

US to grow by:

– 0.7 per cent in 2002 (IMF)

– 3 per cent in 2003 (OECD)

EU to grow by

– 3 per cent in 2003 (OECD)

Japan, perhaps recovering in in 2004 (OECD)

© 2001 Peter Louis. All Rights Reserved

17

ABC

A strategic fit but:

1. How do we produce Disney hits?

2. How do we realize synergies in costs /

revenues?

3. How do we reconcile different business

cultures?

© 2001 Peter Louis. All Rights Reserved

18

Talent drain

1994 – 2000, 75 high-level executive departures.

This can affect:

– Employee morale

– Productivity

– Company direction

– Bottom line

© 2001 Peter Louis. All Rights Reserved

19

Disney’s Revenue, 1983 - 2000

-

5,000

10,000

15,000

20,000

25,000

30,000

($m

illi

on

s)

1983 1985 1987 1989 1991 1993 1995 1997 1999

Years

Revenue, 1983-2000

Source: Annual reports

1995 ABC

merger

© 2001 Peter Louis. All Rights Reserved

20

Disney’s Net Income Growth,

1984 - 2000

Net Income Growth, 1984 - 2000

-100%

-50%

0%

50%

100%

150%

200%

250%

300%

1984

1986

1988

1990

1992

1994

1996

1998

2000

Years

Perc

en

t

% change NI Linear (% change NI)

Source: Annual reports

1995 ABC

merger

© 2001 Peter Louis. All Rights Reserved

21

Where’s Mickey’s magic touch?

7th most valuable brand, yet:

– Generates 82 per cent of revenue domestically

(2000 annual report)

– Increasing European per capita expenditures

could raise $2 billion (1999 annual report)

– Lack of new innovative content (themes, movies,

etc.)

© 2001 Peter Louis. All Rights Reserved

22

Is there life still in myths,

history and fairy tales?

© 2001 Peter Louis. All Rights Reserved

23

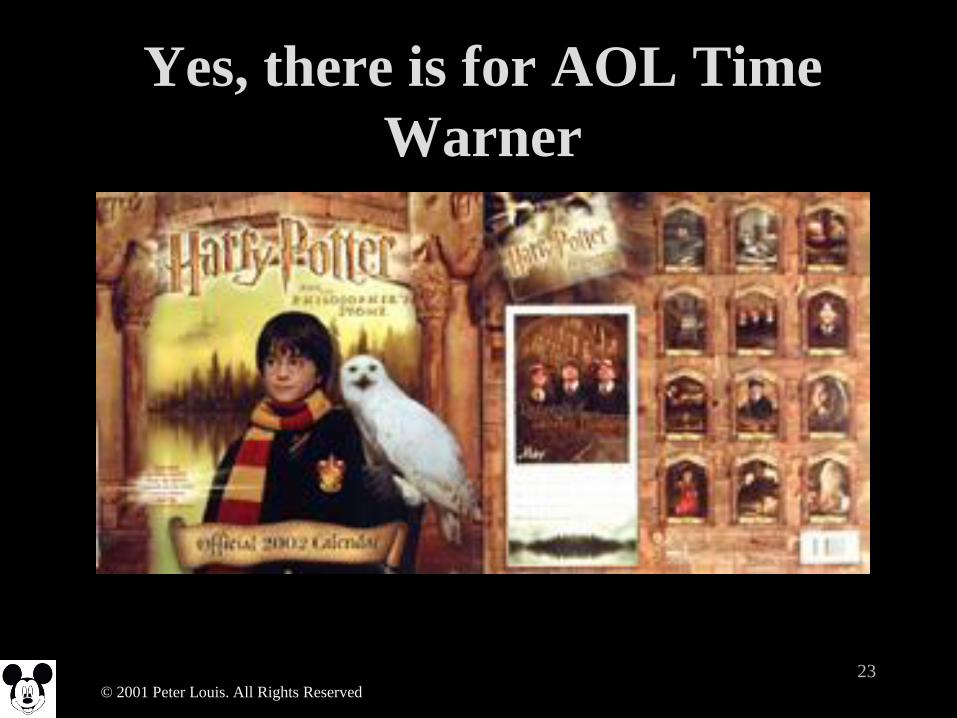

Yes, there is for AOL Time

Warner

© 2001 Peter Louis. All Rights Reserved

24

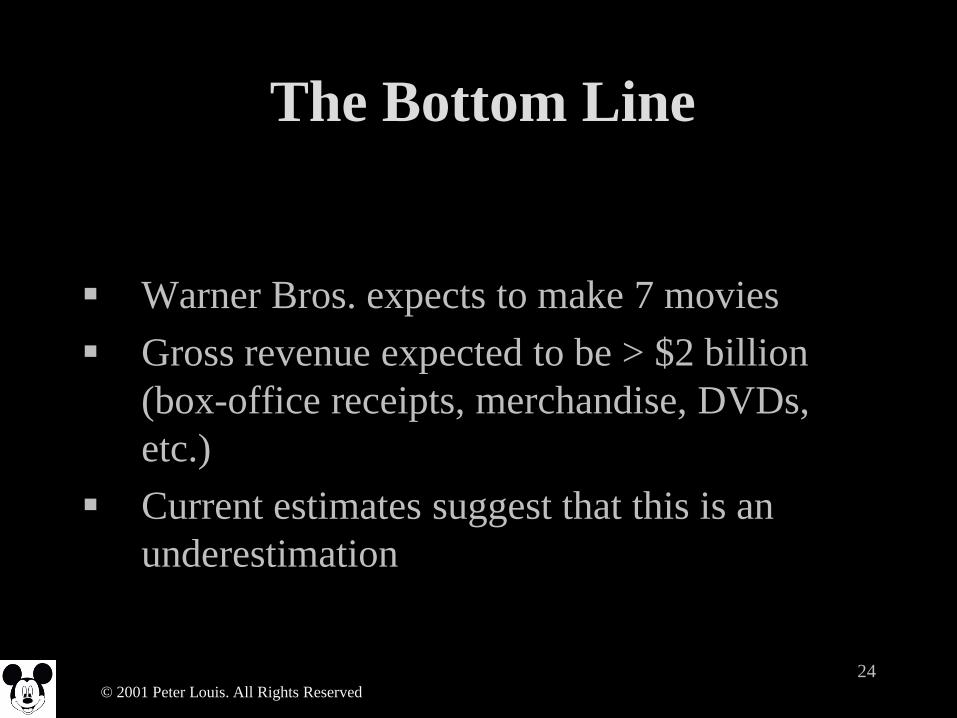

The Bottom Line

Warner Bros. expects to make 7 movies

Gross revenue expected to be > $2 billion

(box-office receipts, merchandise, DVDs,

etc.)

Current estimates suggest that this is an

underestimation

© 2001 Peter Louis. All Rights Reserved

25

Video Games

© 2001 Peter Louis. All Rights Reserved

26

Video Games

7

21.3

0

5

10

15

20

25

Revenue

($billions)

2000 2003

Year

Actual and projected Value of Video Game Industry

CAGR=45 per cent

Source: IDC's 2001 Videogame Survey

© 2001 Peter Louis. All Rights Reserved

27

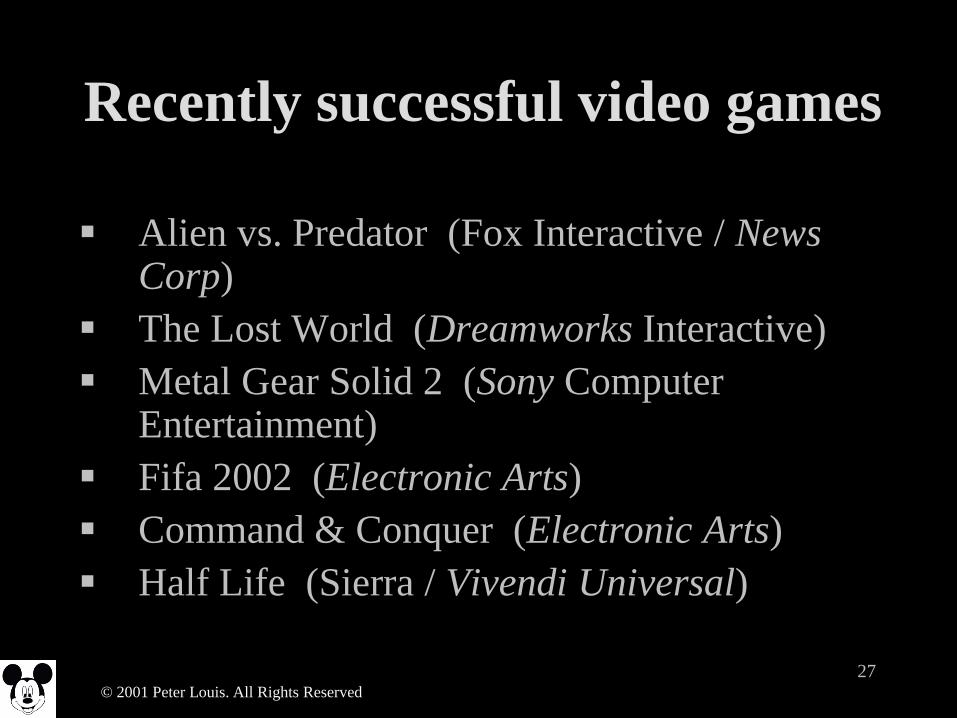

Recently successful video games

Alien vs. Predator (Fox Interactive / News Corp)

The Lost World (Dreamworks Interactive)

Metal Gear Solid 2 (Sony Computer Entertainment)

Fifa 2002 (Electronic Arts)

Command & Conquer (Electronic Arts)

Half Life (Sierra / Vivendi Universal)

© 2001 Peter Louis. All Rights Reserved

28

And of course, the hit…

© 2001 Peter Louis. All Rights Reserved

29

Lara Croft: Tomb Raider,

became…

© 2001 Peter Louis. All Rights Reserved

30

Lara Croft: Tomb Raider,

grossing…

© 2001 Peter Louis. All Rights Reserved

31

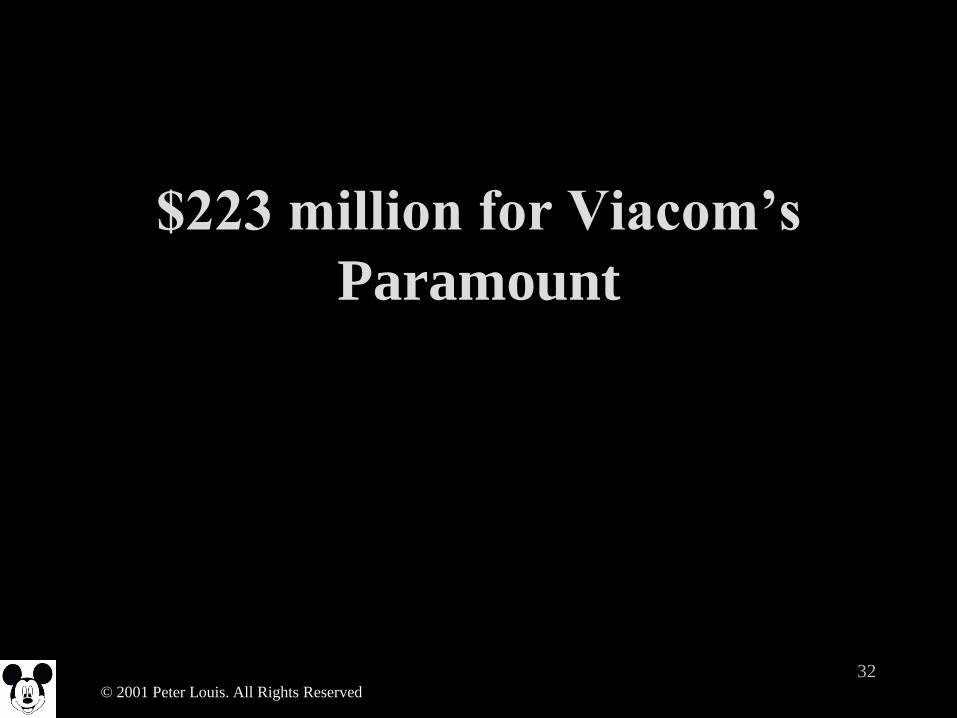

$700 million for the game

publishers EIDOS

© 2001 Peter Louis. All Rights Reserved

32

$223 million for Viacom’s

Paramount

© 2001 Peter Louis. All Rights Reserved

33

If content is king then…

© 2001 Peter Louis. All Rights Reserved

34

Context is Queen

© 2001 Peter Louis. All Rights Reserved

35

Context is Queen

Rationale behind CapCities / ABC acquisition. It gave Disney:

ESPN, ESPN2

– cable access for NHL “The Might Ducks” franchise

ABC

– mass distribution network for Disney program library

Publications

– To distribute Disney material and promote Disney

© 2001 Peter Louis. All Rights Reserved

36

However, looking at the

Internet…

© 2001 Peter Louis. All Rights Reserved

37

Disney / AOL Time Warner

Revenue Streams

Walt Disney Co Revenue Streams, 2000

Media

Networks

37%

Studio

Entertainment

24%

Consumer

Products

10%Internet Group

2%

Parks and

Resorts

27%

Source: Annual reports

AOL Time Warner Revenue Streams, 2000

AOL

21%

Cable &

Networks

34%

Publishing

12%

Filmed

Enterntainme

nt & Music

33%

Source: Annual reports

AOL Time Warner’s Internet segment earns 21 per cent

Disney’s internet segment earns 2 per cent

© 2001 Peter Louis. All Rights Reserved

38

But who wants to play Video

games over the Internet?

© 2001 Peter Louis. All Rights Reserved

39

Video Gamers!

51%

60%

62%

65%

76%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Percent

Web surf/email

Online Gaming

Pay-per-view games

Broadband Gaming Service

Download new games/levels

High Interest Responses to Potential Connectivity Applications

Source: IDC's 2001 Videogame Survey

Predominately male, 21 years, 2 ½ hours per day

Key: Content, New and Compelling Experience

© 2001 Peter Louis. All Rights Reserved

40

Is 20 per cent growth still

achievable?

© 2001 Peter Louis. All Rights Reserved

41

Yes…

© 2001 Peter Louis. All Rights Reserved

42

but only if

Disney continues to both:

1. Innovate

2. Update the competitive advantage

© 2001 Peter Louis. All Rights Reserved

43

Recommendations

© 2001 Peter Louis. All Rights Reserved

44

Recommendations

Reduce the attrition of executives

Licence (or buy) innovative content

Develop innovative local content

Create an Interactive Games Division (to

target the “serious gamer”)

© 2001 Peter Louis. All Rights Reserved

45

Reduce the attrition of executives

Survey executives

– Use independent consultants, say Holzschu, Jordan, Schiff & Associates

– Determine causal factors (moral, culture fit, remuneration, lack of authority, change of location, etc.)

Review findings at board level

Implement recommendations

Create future guidelines

© 2001 Peter Louis. All Rights Reserved

46

Licence (or buy) innovative

content

Source innovative international content (e.g.

programs, comic characters, cartoons, etc.)

– Transferable to the US market (e.g. The Weakest Link)

– Can be leveraged internationally (e.g. Walking With

Dinosaurs)

Seek extension opportunities (e.g. Teletubbies)

– Program Cartoon Video Park theme ?

© 2001 Peter Louis. All Rights Reserved

47

Develop innovative local content

Leverage the rich cultural heritage of host regions to

create local themes and programs (e.g. Japan)

– Themes include movies (The Seven Samurai or Yojimbo),

unique shopping experiences, etc

– Create characters that can be leveraged internationally (e.g.

Pokemon)

Seek extension opportunities (e.g. Power Rangers)

– Program Movie Cartoon Park theme ?

© 2001 Peter Louis. All Rights Reserved

48

Create an Interactive Games

Division

Purchase an established publisher like Electronic Arts (fiscal revenue of $1.3 billion, 2001)

Develop games for successful movie releases

– Con Air, Pearl Harbor

Use new video expertise to create new Disney themes that are:

– Interactive, immersive or simulations

Leverage publisher to position for emerging subscription based Web gaming services that allow:

– Individual, cooperative or combative play

© 2001 Peter Louis. All Rights Reserved

49

Conclusions

© 2001 Peter Louis. All Rights Reserved

50

Conclusions

Disney can achieve 20 per cent ROE. However, this

requires a focused strategy that:

– Allows effective managers to manage (à la GE)

– Realizes brand values

– Kindles internal and external innovation

– Exploits areas of growth

– Realizes synergies, and

– Maintains incremental revenue growth (e.g. gate receipts)

© 2001 Peter Louis. All Rights Reserved

51

Thank you

© 2001 Peter Louis. All Rights Reserved

52

About the author

Peter is the Founder and CEO of p2people

(http://www.p2people.co.uk), the innovative micro

outsourcing service.

Formerly a freelance consultant, Peter has extensive

international experience in data warehousing and IT

& HR outsourcing.

Peter has an MBA (Instituto de Empresa) and MSc

in Knowledge Management (Cranfield).

© 2001 Peter Louis. All Rights Reserved

53

The Walt Disney Company

“Content is King”

By Peter Louis

Instituto de Empresa

December 2001