Embed Size (px)

Citation preview

Walker Sigismund, FSA Risk Policy 1

Using Harm to anticipate and regulate Liquidity Risk

By Walker SigismundFSA Risk Policy

Imperial Risk Management Laboratory

Liquidity: Pricing and Risk Management Bank of England, 23-24 June 2008

Walker Sigismund, FSA Risk Policy 2

Troubles with Liquidity Concept

• During the last couple years I have been troubled by– The frequent absence of any clear let alone consistent definition of

“Liquidity Risk” in most academic and industry papers or discussions, in which it is used to mean many different and contradictory things

– Whether Liquidity is merely a symptom of the crystallisation of other types of risk—market, credit and operational—or a risk in its own right (& whether Basle captures it or not)

– Why firms think Liquidity is Firm rather than Market-centric– What are the Triggers & Early Warning Indicators– How to manage and regulate Liquidity– Whether the only regulatory concern is the Time transformation of

deposits, or if it includes Market Confidence and other factors…?

• The following derivative model of a firm/market and extensive empirical results help resolve these and many other Liquidity and Financial Stability problems

Walker Sigismund, FSA Risk Policy 3

Abstract

• The relationship of Liquidity to Asset Prices and the crystallisation of Market, Credit, Operational and Strategic Risks within firms can be clearly analysed by using Derivative pricing techniques to mark-to-market the balance sheets of each firm.

• The analysis defines Distress to be the risk that these risks crystallise, and defines Harm to be the losses incurred by non-shareholders as a result.

• These tools and definitions show why many of the principles and techniques used to manage Liquidity have only marginal affect.

• Marking-to-Market every Balance Sheet using these techniques, will dispel most of the current lack of transparency and help ensure that each firm get the right risk adjustment from the market.

• We have computed this risk for thousands of firms, across sectors and most major markets world-wide.

Walker Sigismund, FSA Risk Policy 4

– Liquidity Definition –

Accounting v

Marking to Market of Entire Balance Sheet—

DistressHarm

Walker Sigismund, FSA Risk Policy 5

FSA Discussion Paper December 2007 07/7 [2.2]

• “We define liquidity risk as the risk that a firm, although balance-sheet solvent, cannot maintain or generate sufficient cash resources to meet its payment obligations in full as they fall due, or can only do so at materially disadvantageous terms.

• The corollary is that liquidity risk management means mitigating the risk that a bank is not able to do this. This in turn requires reliable access to enough cash resources, at unpredictable times and to unpredictable extents, to meet uncertain cash flow obligations.

• Such access – and indeed the cash flow obligations themselves – depends on market and other external events and on other agents’ behaviour. Even during normal conditions this can be far from straightforward; stressed conditions, which are themselves often unpredictable, make it even more challenging and add extra layers of uncertainty to a task already surrounded by uncertainty.”

Walker Sigismund, FSA Risk Policy 6

Basle: Principles for .. Liquidity… June 2008

• “Liquidity is the ability of a bank to fund increases in assets and meet obligations as they come due, at reasonable cost.”

Walker Sigismund, FSA Risk Policy 7

What does reasonable mean?

• Asset prices change relative to other asset classes– Fundamental shifts in economy

– Store-of-Value/Speculative interests ebb and flow

• The firm may have to pay more because it has/is – The wrong mix of Assets and/or Liabilities

– Weaker than its competition

– Not very well run… has credit and market risk problems

– Unclear set of Strategic or other Risks

• Because of this ‘Distress’ the Market– Requires a greater (or lower) Risk premium

• Questions– Why is that unreasonable?

– What can firms do to manage these risks

– What--if anything--should regulators do?

Walker Sigismund, FSA Risk Policy 8

Distress Definition

• Distress– Occurs when losses are expected by non-shareholders

– In the simple Binomial model used here, the Market Value of Assets is less than or equal to the Face Value of all Debt

• If the firm were immediately wound up, it would be insolvent• When long-term debt is present, default will not occur until later

– In other words, the firm is or getting nearer to being ‘insolvent’ on a marked-to-market basis (assuming immediate wind up) but not necessarily in an accounting or legal sense until default is actually triggered by the inability to repay the long-term debt

• Consequences– Assets sell at a greater discount

– Loans cost more

Walker Sigismund, FSA Risk Policy 9

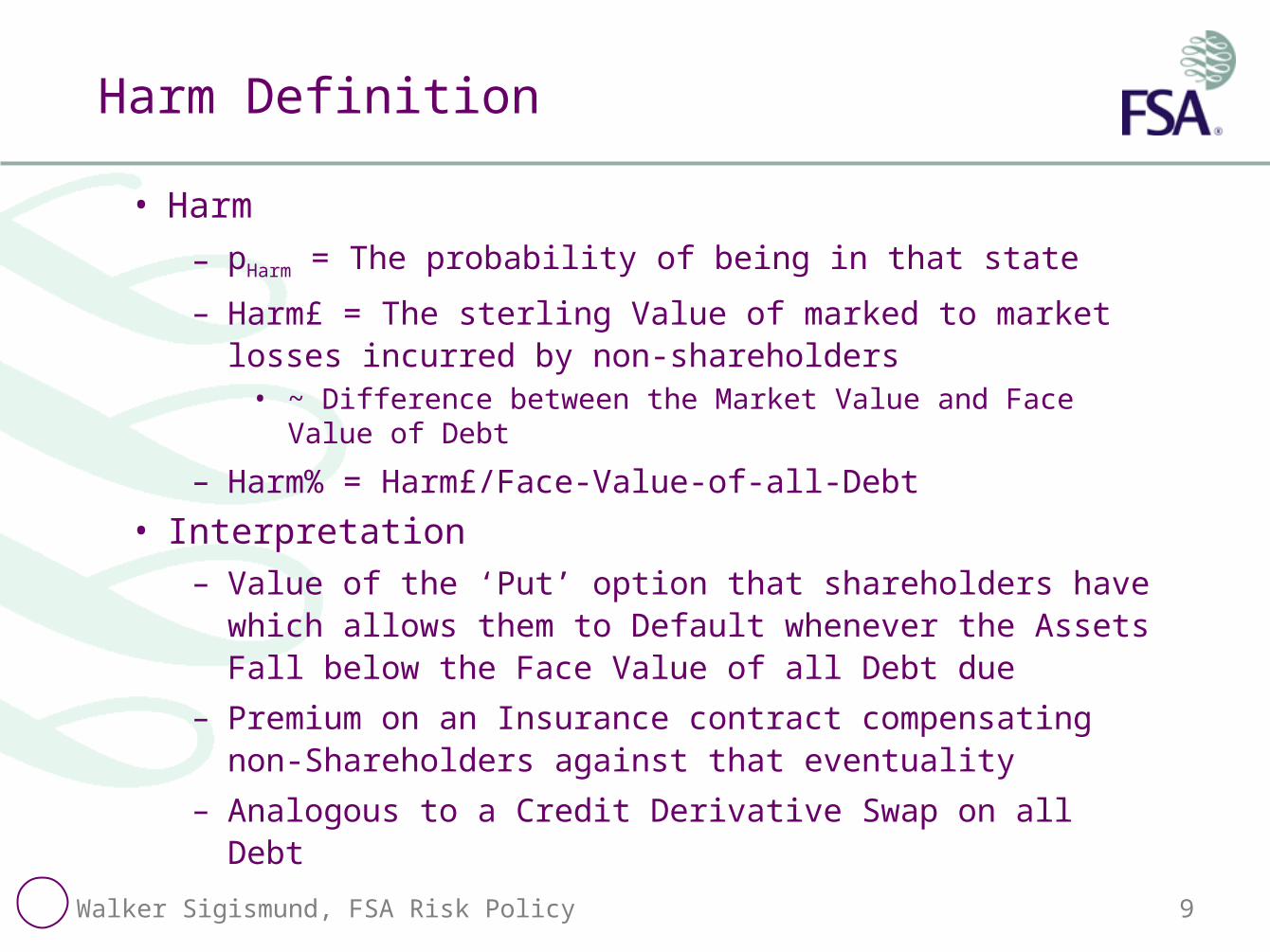

Harm Definition

• Harm

– pHarm = The probability of being in that state

– Harm£ = The sterling Value of marked to market losses incurred by non-shareholders

• ~ Difference between the Market Value and Face Value of Debt

– Harm% = Harm£/Face-Value-of-all-Debt

• Interpretation– Value of the ‘Put’ option that shareholders have which

allows them to Default whenever the Assets Fall below the Face Value of all Debt due

– Premium on an Insurance contract compensating non-Shareholders against that eventuality

– Analogous to a Credit Derivative Swap on all Debt

Walker Sigismund, FSA Risk Policy 10

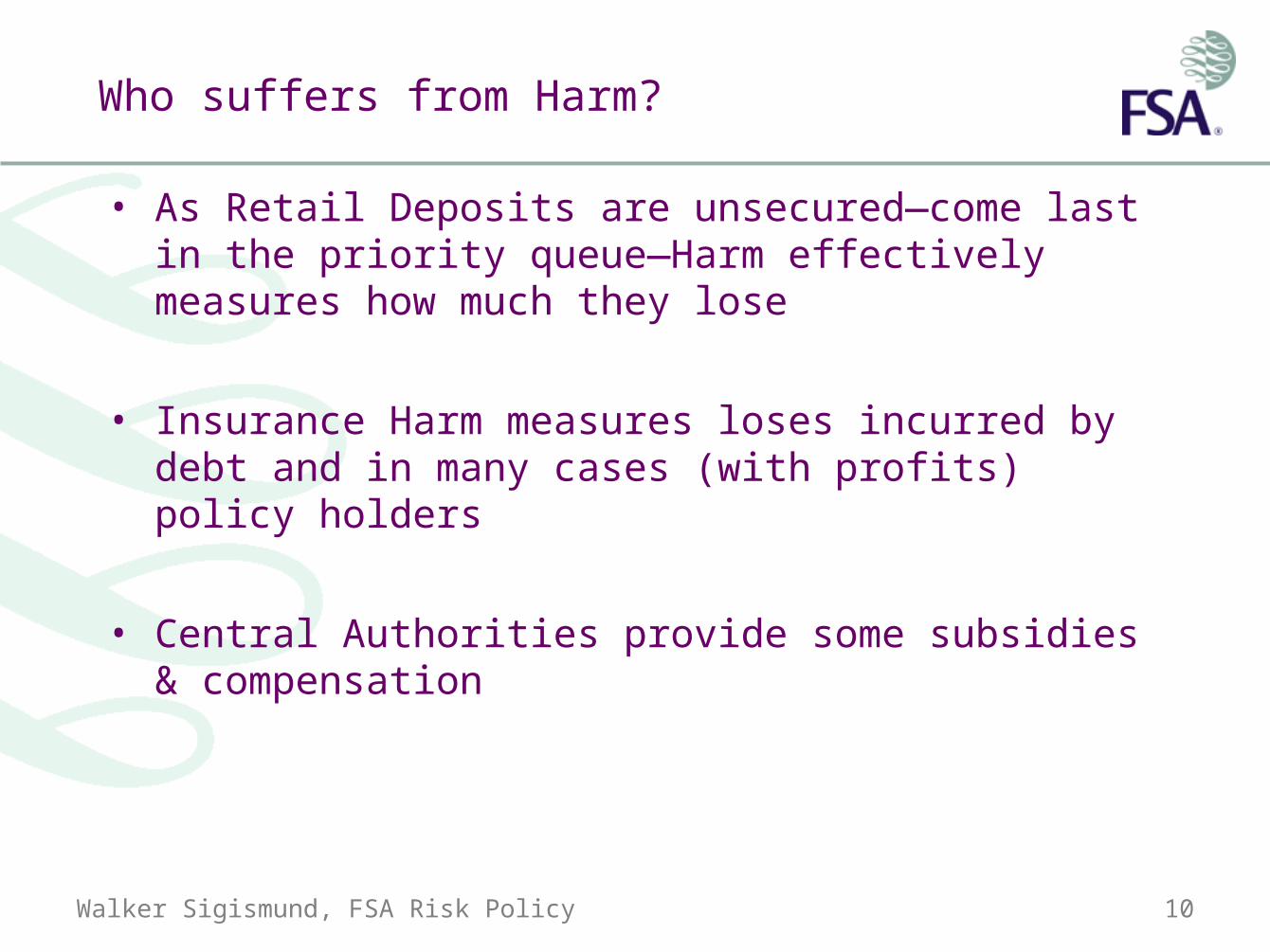

Who suffers from Harm?

• As Retail Deposits are unsecured—come last in the priority queue—Harm effectively measures how much they lose

• Insurance Harm measures loses incurred by debt and in many cases (with profits) policy holders

• Central Authorities provide some subsidies & compensation

Walker Sigismund, FSA Risk Policy 11

Liquidity Redefinition

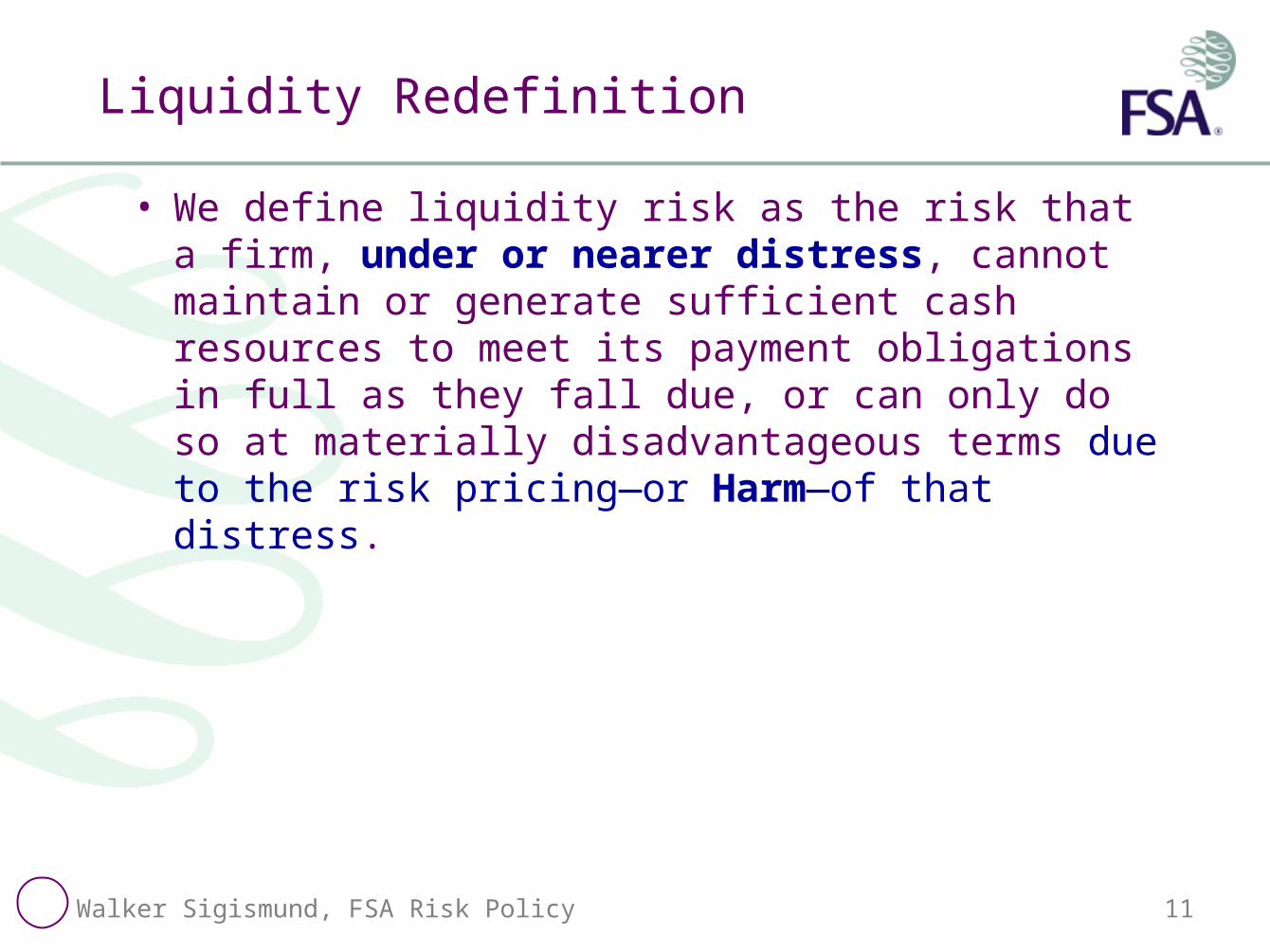

• We define liquidity risk as the risk that a firm, under or nearer distress, cannot maintain or generate sufficient cash resources to meet its payment obligations in full as they fall due, or can only do so at materially disadvantageous terms due to the risk pricing—or Harm—of that distress.

Walker Sigismund, FSA Risk Policy 12

– Unravelling Liquidity –Marking-to-Market Balance Sheet

Repricing of Risk

Liquidity Risk is a symptom of Market/Credit Risk

Walker Sigismund, FSA Risk Policy 13

Marking to Market of entire Balance sheets

• The market prices it Assets and Liabilities– The most important lesson from this analysis is that

marking-to-market the entire balance sheet of each firm provides the transparency required to know, at each point in time, the risk adjusted value of

• Assets which need to be sold• Liabilities that the firm seeks to raise

• Firms cannot manage Liquidity Risk alone– They have to reveal to the market enough information for

the market to mark its entire balance sheet to market

– They cannot count prices to remain stable (“reasonable”) due to constant Repricing of Risk

Walker Sigismund, FSA Risk Policy 14

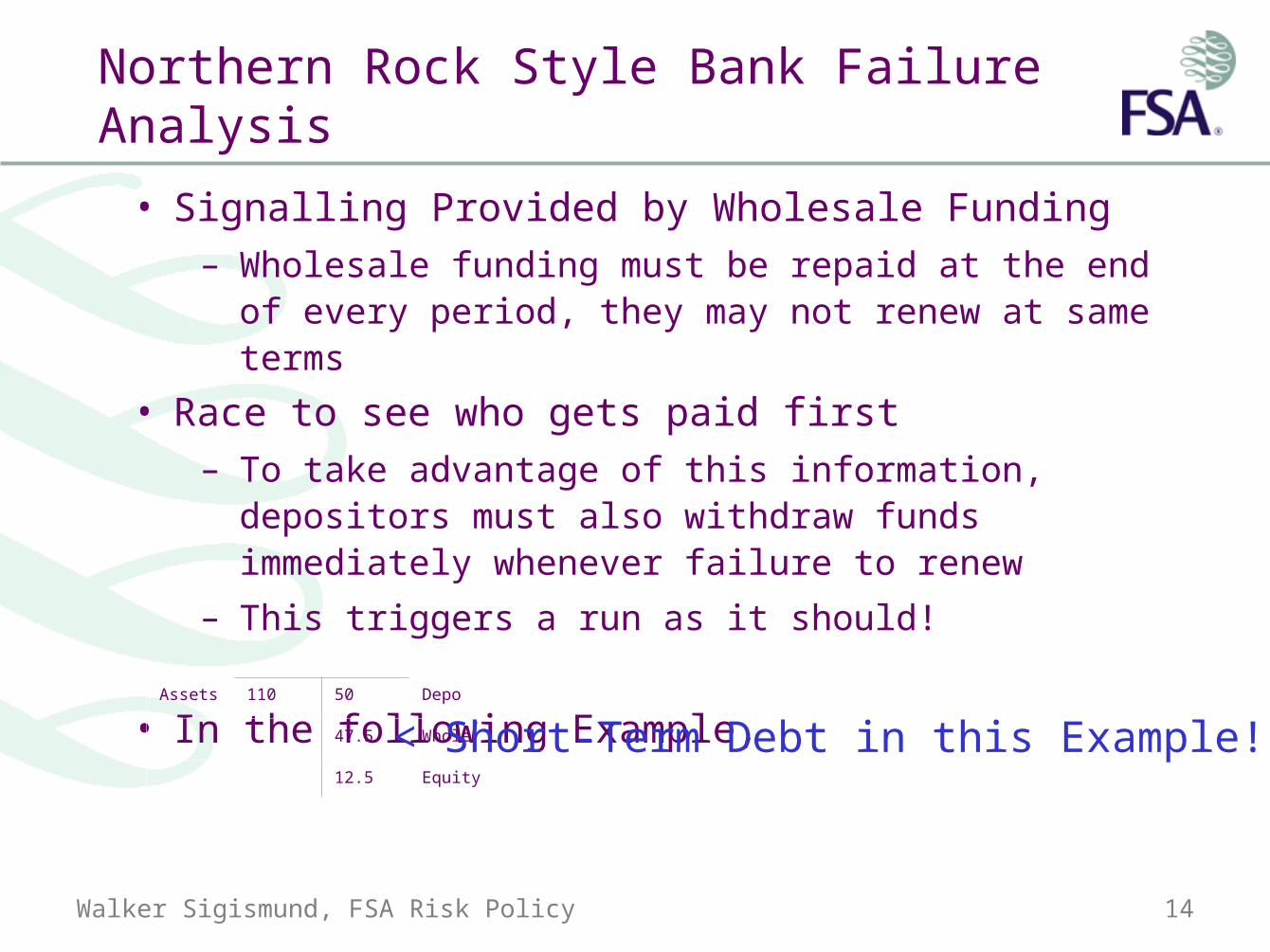

Northern Rock Style Bank Failure Analysis

• Signalling Provided by Wholesale Funding– Wholesale funding must be repaid at the end of every

period, they may not renew at same terms

• Race to see who gets paid first– To take advantage of this information, depositors must

also withdraw funds immediately whenever failure to renew

– This triggers a run as it should!

• In the following Example,Assets 110 50 Depo

47.5 Whole

12.5 Equity

< Short-Term Debt in this Example!

Walker Sigismund, FSA Risk Policy 15

130 50

50

30

140 50

50

40

110 50

50

10

90 45?

50?

0

120 50

50

20

100 50

50

0

80 30?

50?

0

120 50

50

20

100 47.5?

50?

2.5?

110 48.75?

50.00?

11.25?

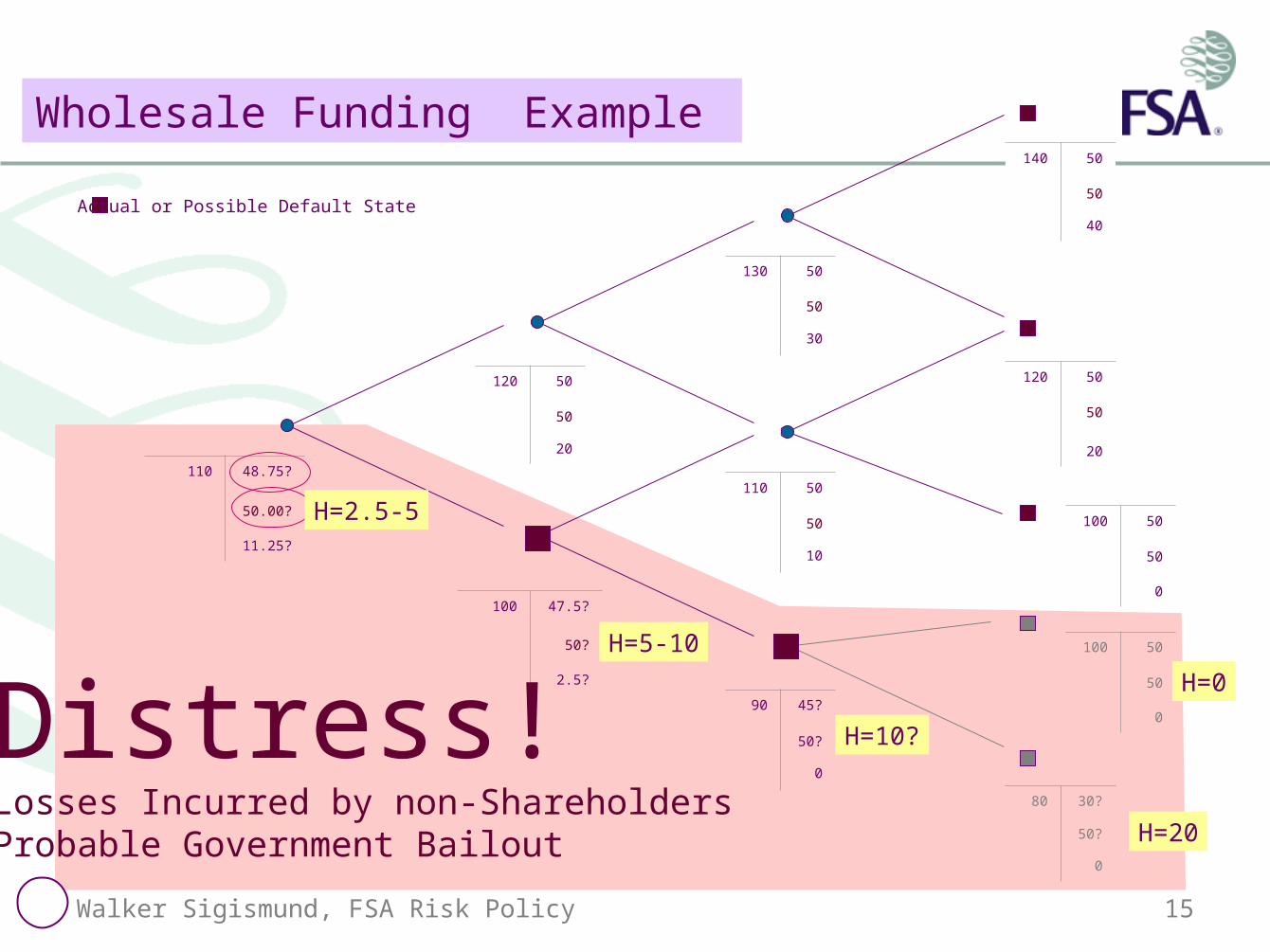

Distress!Losses Incurred by non-ShareholdersProbable Government Bailout

Wholesale Funding Example

100 50

50

0

Actual or Possible Default State

H=0

H=20

H=10?

H=5-10

H=2.5-5

Walker Sigismund, FSA Risk Policy 16

130 50

50

30

140 50

50

40

110 50

50

10

90 45?

50?

0

120 50

50

20

100 50

50

0

80 30?

50?

0

120 50

50

20

100 47.5?

50?

2.5?

110 48.75?

50.00?

11.25?

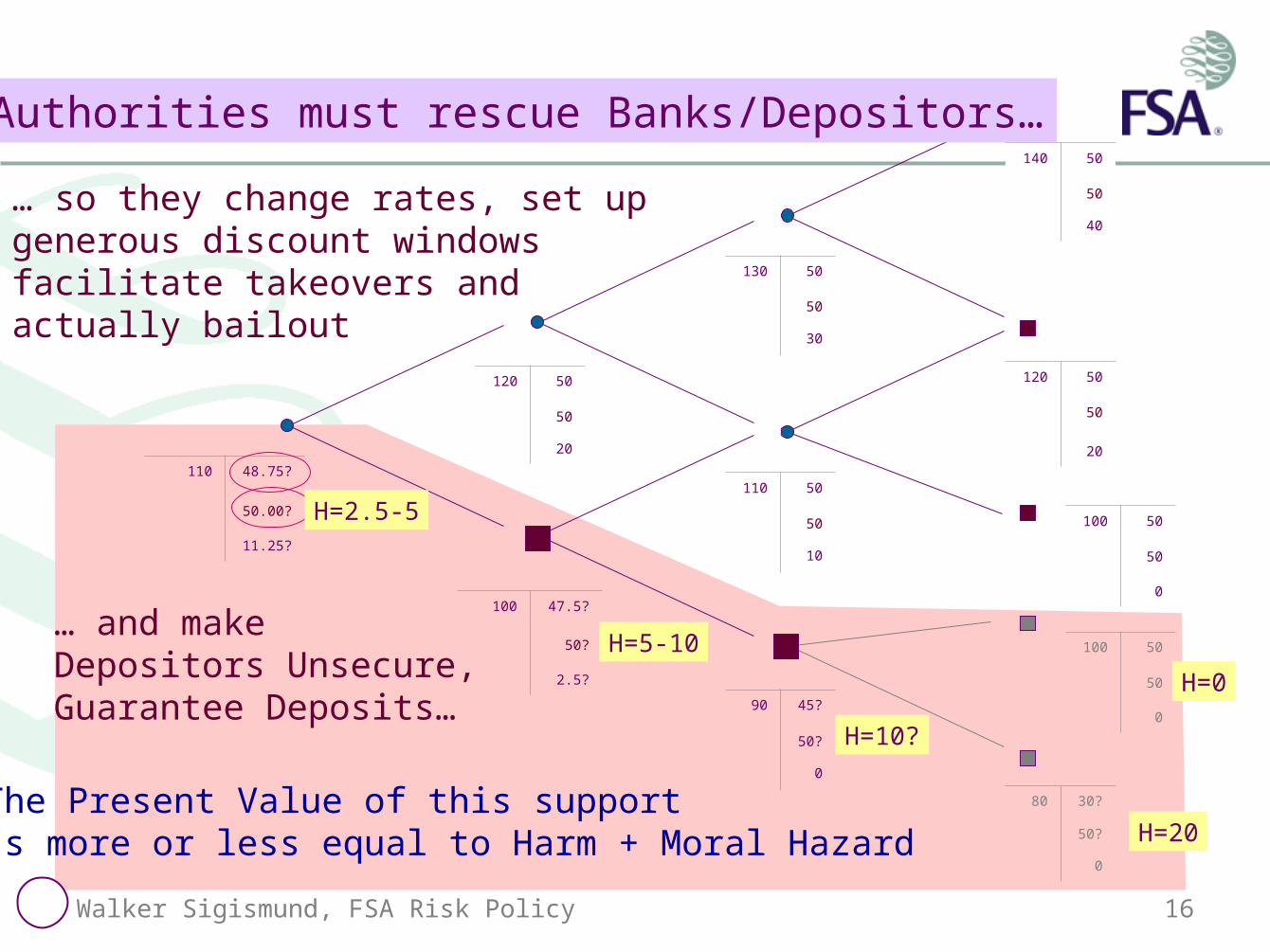

Authorities must rescue Banks/Depositors…

100 50

50

0

H=0

H=20

H=10?

H=5-10

H=2.5-5

… so they change rates, set up generous discount windowsfacilitate takeovers andactually bailout

The Present Value of this supportIs more or less equal to Harm + Moral Hazard

… and makeDepositors Unsecure,Guarantee Deposits…

Walker Sigismund, FSA Risk Policy 17

130 50

50

30

140 50

50

40

110 50

50

10

100 50?

50?

0

120 50

50

20

100 50

50

0

100 50

50

0

120 50

50

20

100 50?

50?

0 0

110 50

50

10

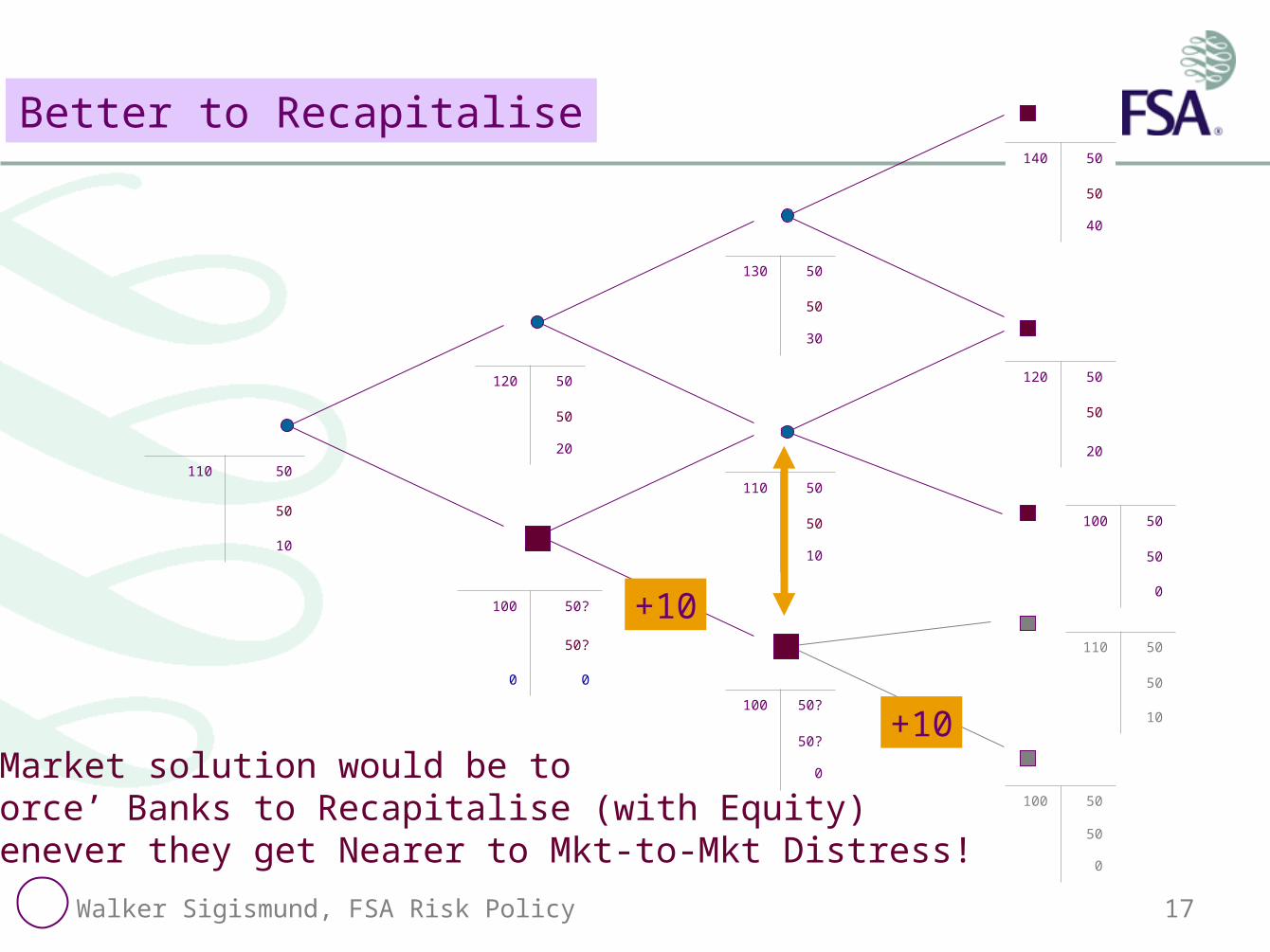

Better to Recapitalise

110 50

50

10

A Market solution would be to‘force’ Banks to Recapitalise (with Equity)Whenever they get Nearer to Mkt-to-Mkt Distress!

+10

+10

Walker Sigismund, FSA Risk Policy 18

Lessons from Northern Rock

• Wholesale funding – Acts like a trigger, keeping the whole system fair, almost as if all

funding were short term

– Possible delay, allowing further distress—or Harm—to develop

• Central Bank subsidies– Changes in Rates and lending windows subsidise banks

– These are frequently changed to suit the financial community (rather than the real economy)

– This also means that the tree is not Arbitrage Free!

• Forbearance– The fact that the tree is not Arbitrage-free means that there can be

no agreement About the exact nature and pricing within the tree

– No Reliable (unambiguous) threshold conditions

– The best is arguably Distress and Harm to Depositors

Walker Sigismund, FSA Risk Policy 19

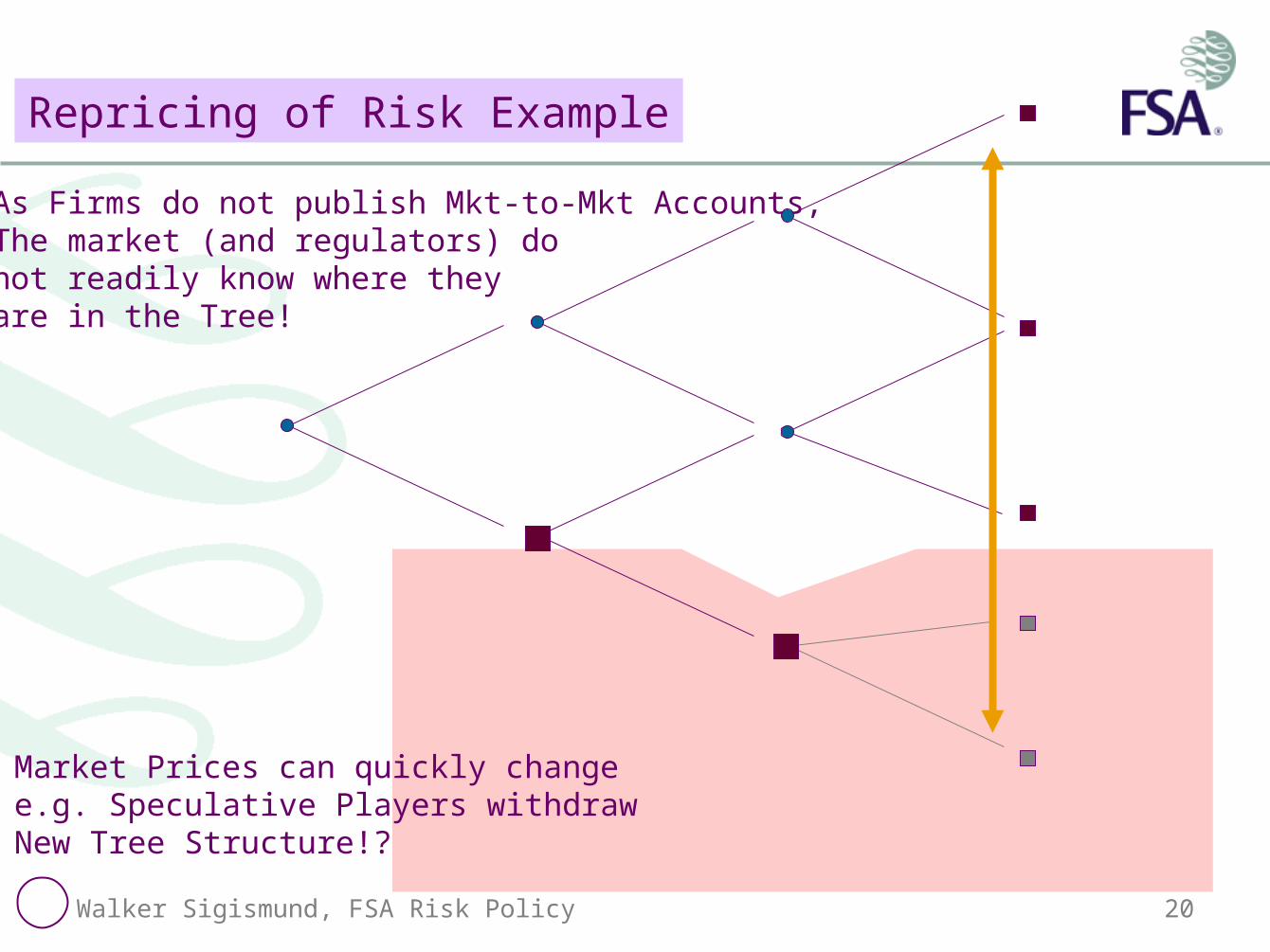

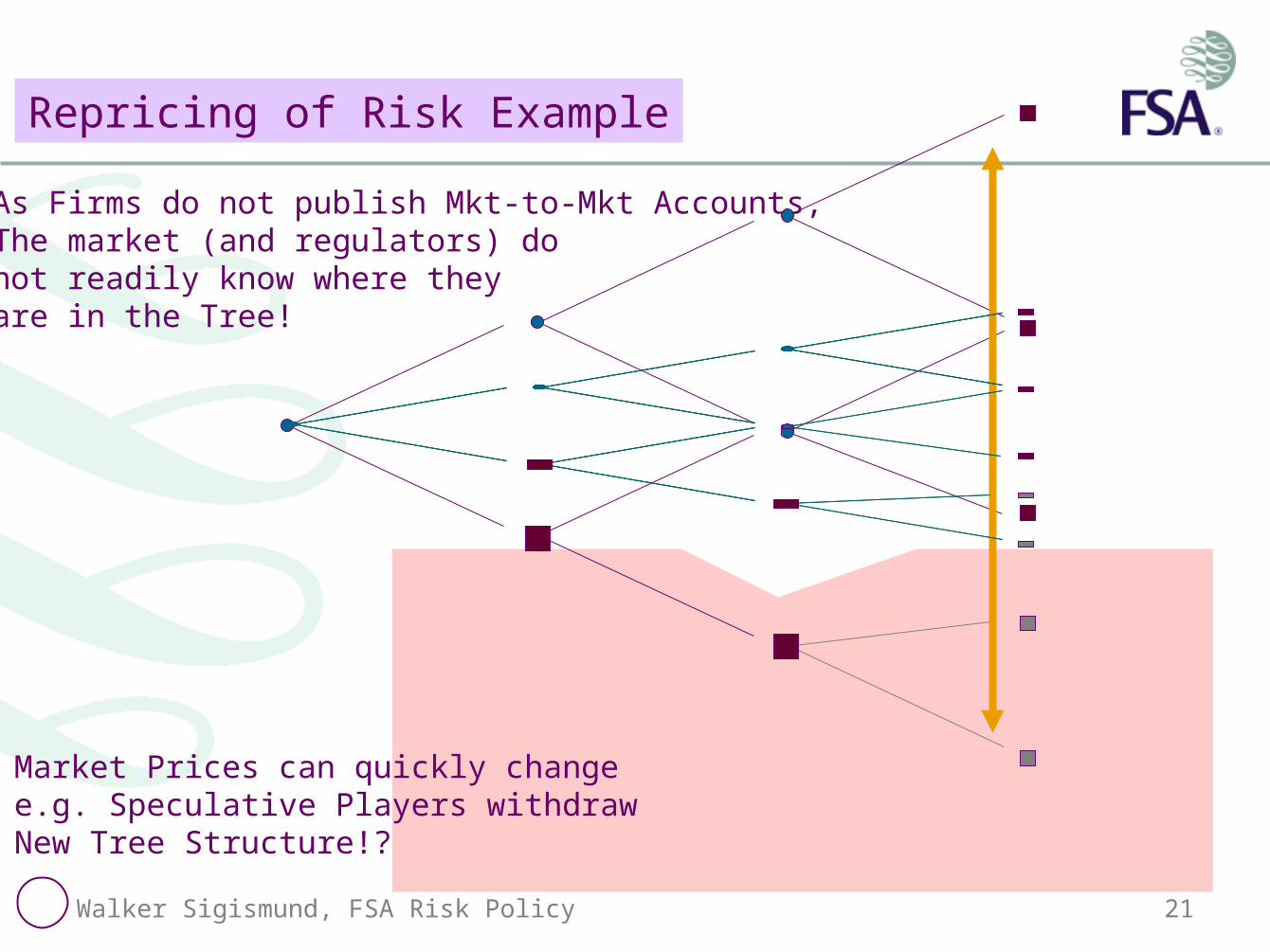

Repricing of Risk Example

As Firms do not publish Mkt-to-Mkt Accounts,The market (and regulators) donot readily know where theyare in the Tree!

Market Prices can quickly changee.g. Speculative Players withdrawNew Tree Structure!?

Walker Sigismund, FSA Risk Policy 20

Repricing of Risk Example

As Firms do not publish Mkt-to-Mkt Accounts,The market (and regulators) donot readily know where theyare in the Tree!

Market Prices can quickly changee.g. Speculative Players withdrawNew Tree Structure!?

Walker Sigismund, FSA Risk Policy 21

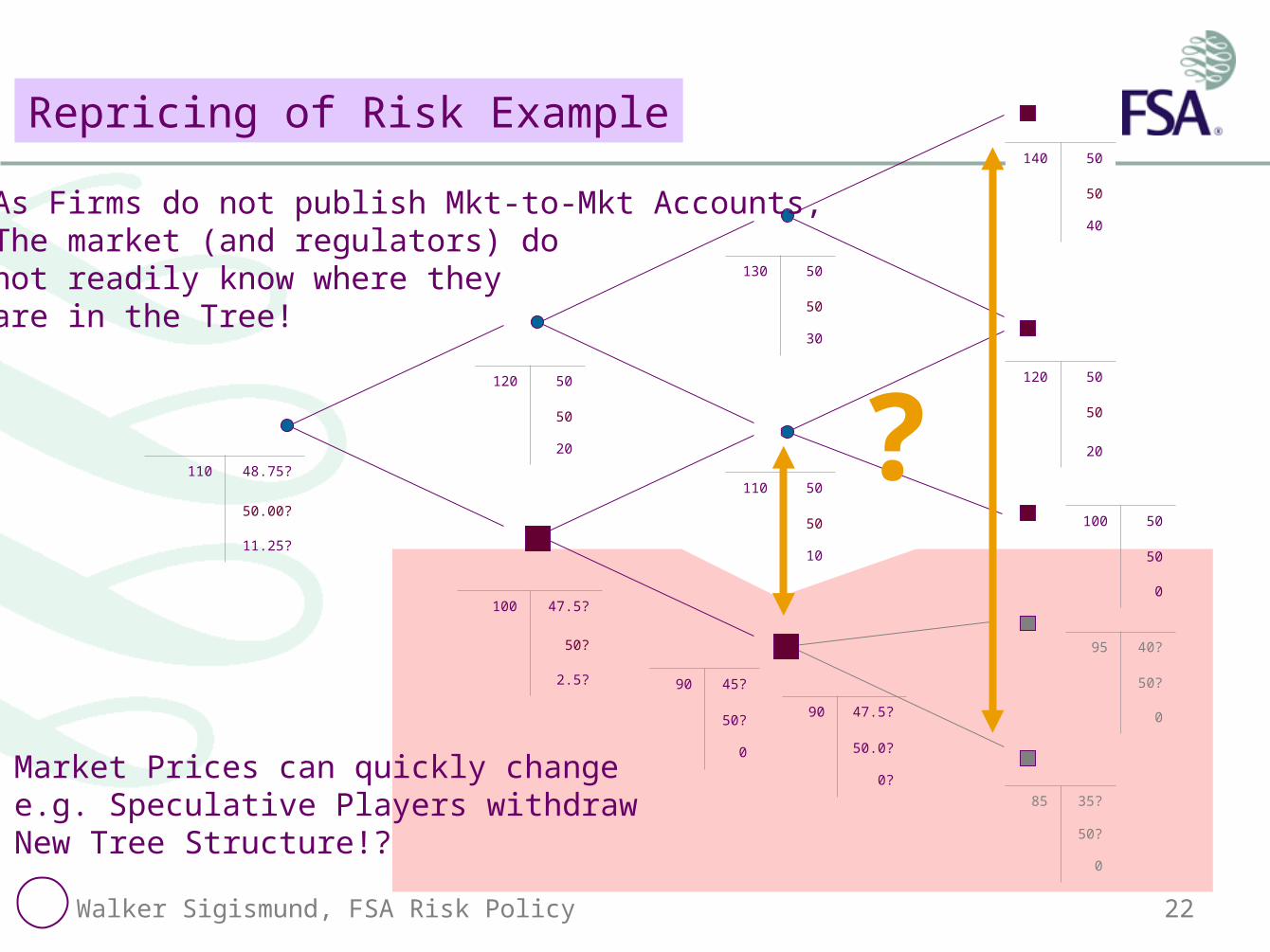

Repricing of Risk Example

As Firms do not publish Mkt-to-Mkt Accounts,The market (and regulators) donot readily know where theyare in the Tree!

Market Prices can quickly changee.g. Speculative Players withdrawNew Tree Structure!?

Walker Sigismund, FSA Risk Policy 22

130 50

50

30

140 50

50

40

110 50

50

10

90 45?

50?

0

120 50

50

20

100 50

50

0

85 35?

50?

0

120 50

50

20

100 47.5?

50?

2.5?

110 48.75?

50.00?

11.25?

Repricing of Risk Example

95 40?

50?

0

As Firms do not publish Mkt-to-Mkt Accounts,The market (and regulators) donot readily know where theyare in the Tree!

90 47.5?

50.0?

0?

?

Market Prices can quickly changee.g. Speculative Players withdrawNew Tree Structure!?

Walker Sigismund, FSA Risk Policy 23

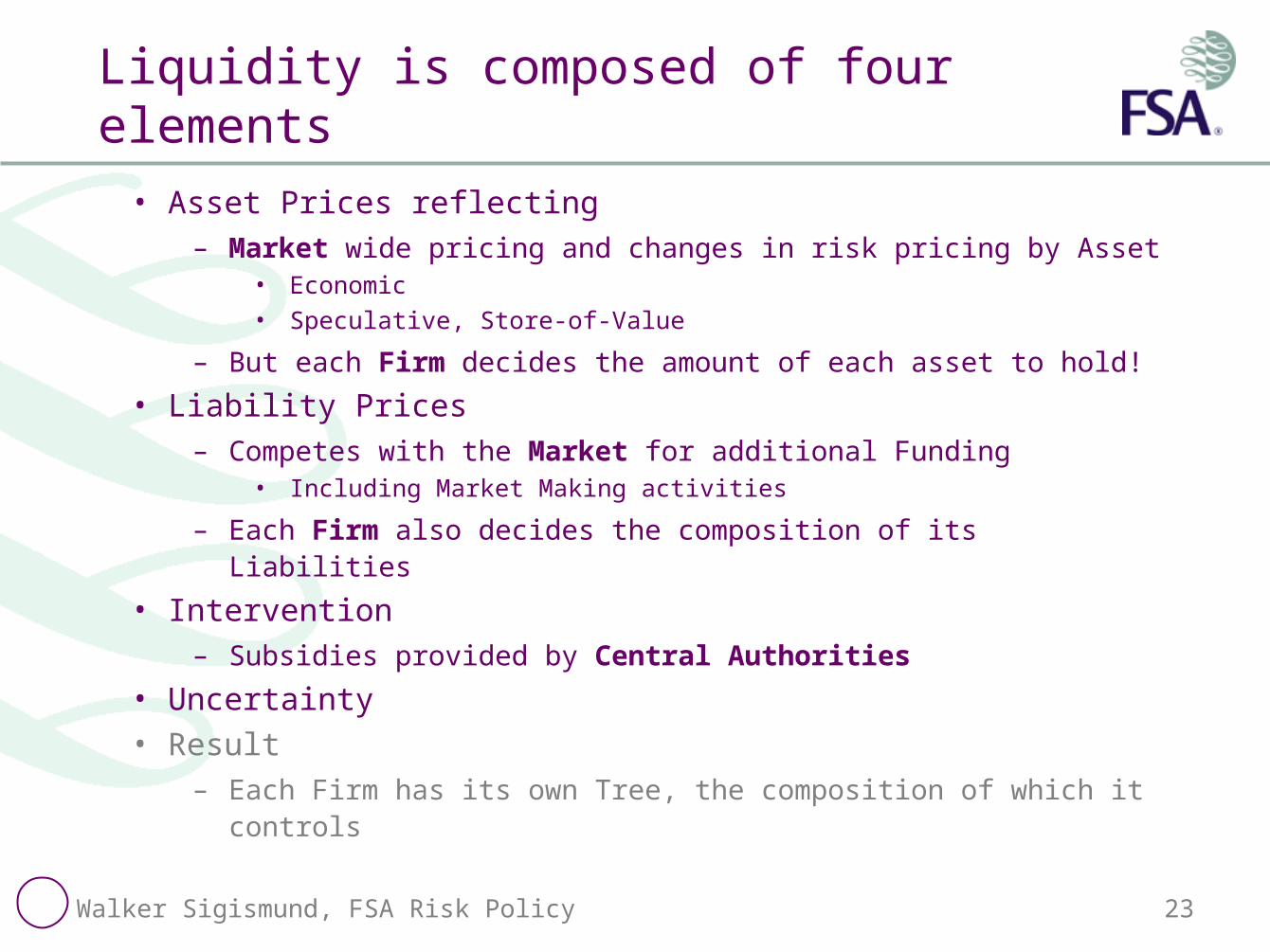

Liquidity is composed of four elements

• Asset Prices reflecting– Market wide pricing and changes in risk pricing by Asset

• Economic• Speculative, Store-of-Value

– But each Firm decides the amount of each asset to hold!

• Liability Prices– Competes with the Market for additional Funding

• Including Market Making activities

– Each Firm also decides the composition of its Liabilities

• Intervention– Subsidies provided by Central Authorities

• Uncertainty

• Result– Each Firm has its own Tree, the composition of which it controls

Walker Sigismund, FSA Risk Policy 24

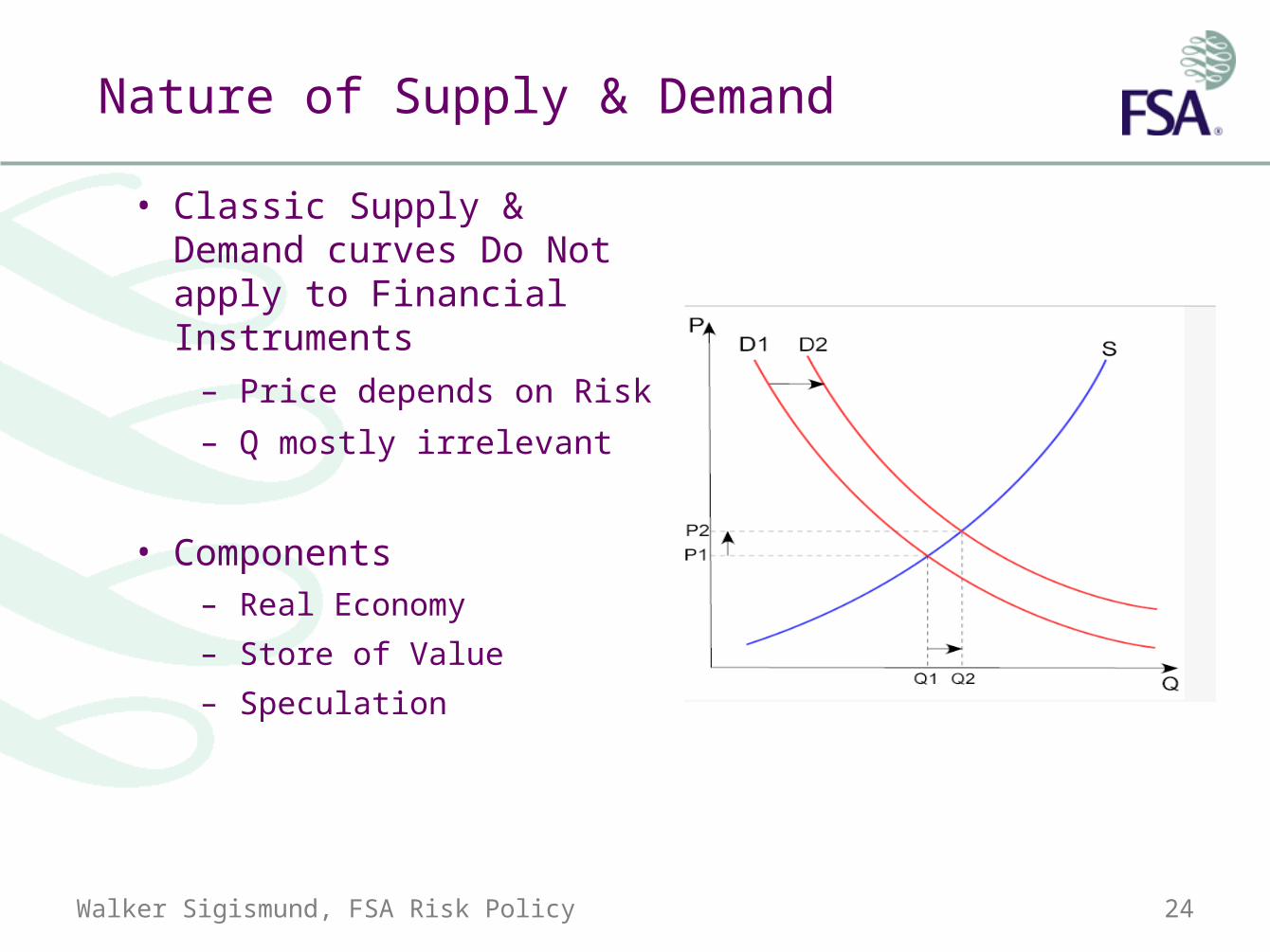

Nature of Supply & Demand

• Classic Supply & Demand curves Do Not apply to Financial Instruments

– Price depends on Risk

– Q mostly irrelevant

• Components– Real Economy

– Store of Value

– Speculation

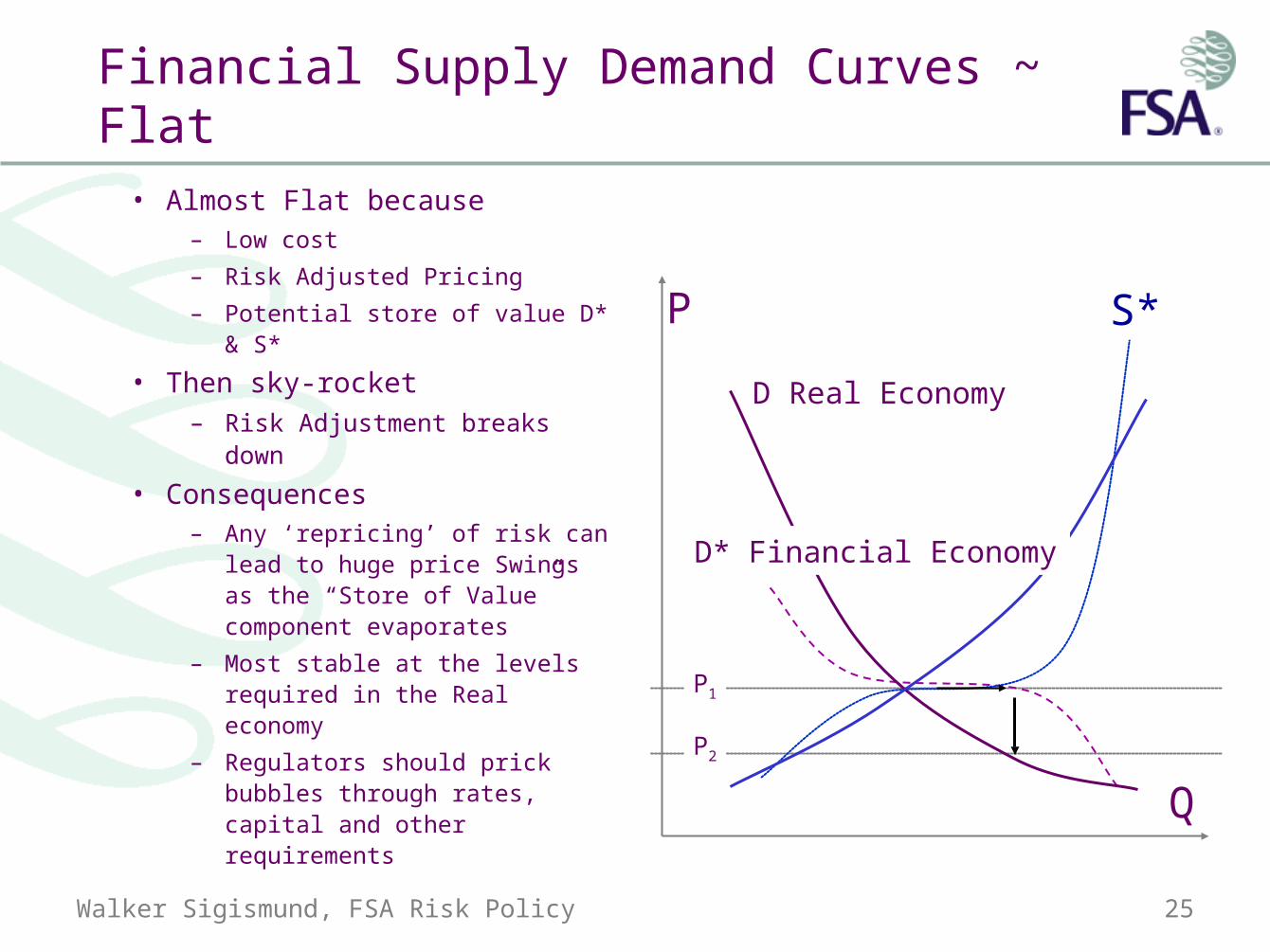

Walker Sigismund, FSA Risk Policy 25

Financial Supply Demand Curves ~ Flat

• Almost Flat because– Low cost

– Risk Adjusted Pricing

– Potential store of value D* & S*

• Then sky-rocket– Risk Adjustment breaks down

• Consequences– Any ‘repricing’ of risk can lead

to huge price Swings as the “Store of Value” component evaporates

– Most stable at the levels required in the Real economy

– Regulators should prick bubbles through rates, capital and other requirements

P

Q

P1

P2

D Real Economy

D* Financial Economy

S*

Walker Sigismund, FSA Risk Policy 26

Lessons to be Learned

• Market Centric Liquidity– There is a market-wide tree for each asset class– The Real economy needs limited amounts of each asset class– Financial firms often over supply the market (which in many cases will absorb this

excess due to ‘storage of wealth’ made possible via ‘equilibrium’ risk pricing no matter the economic supply/demand need)

– The market goes through phases where certain types of assets are favoured over others, which can rapidly fall into disfavour as a store of wealth and thus in great economic oversupply

– Under market wide distress (disenchantment with certain asset classes and liability structures) a type of “musical chairs” take place where some sectors and firms are favoured over others

• Firm Centric Liquidity– The Trees of ‘similar’ firms differ both in the quality of the assets generating the

forward prices, but also the strength or weakness of the Liabilities generating backward prices

– A firm demonstrably in control of its market, credit and operational risk—relative to its peers—can have little if any Liquidity Risk

– A firm with a massive position in a given asset class—Metallgesellschaft, LTCM…—are always prone to Liquidity shocks

• Distress and Harm measures the degree of this risk

Walker Sigismund, FSA Risk Policy 27

– Liquidity Indicators –

Early Warning Indicators

Walker Sigismund, FSA Risk Policy 28

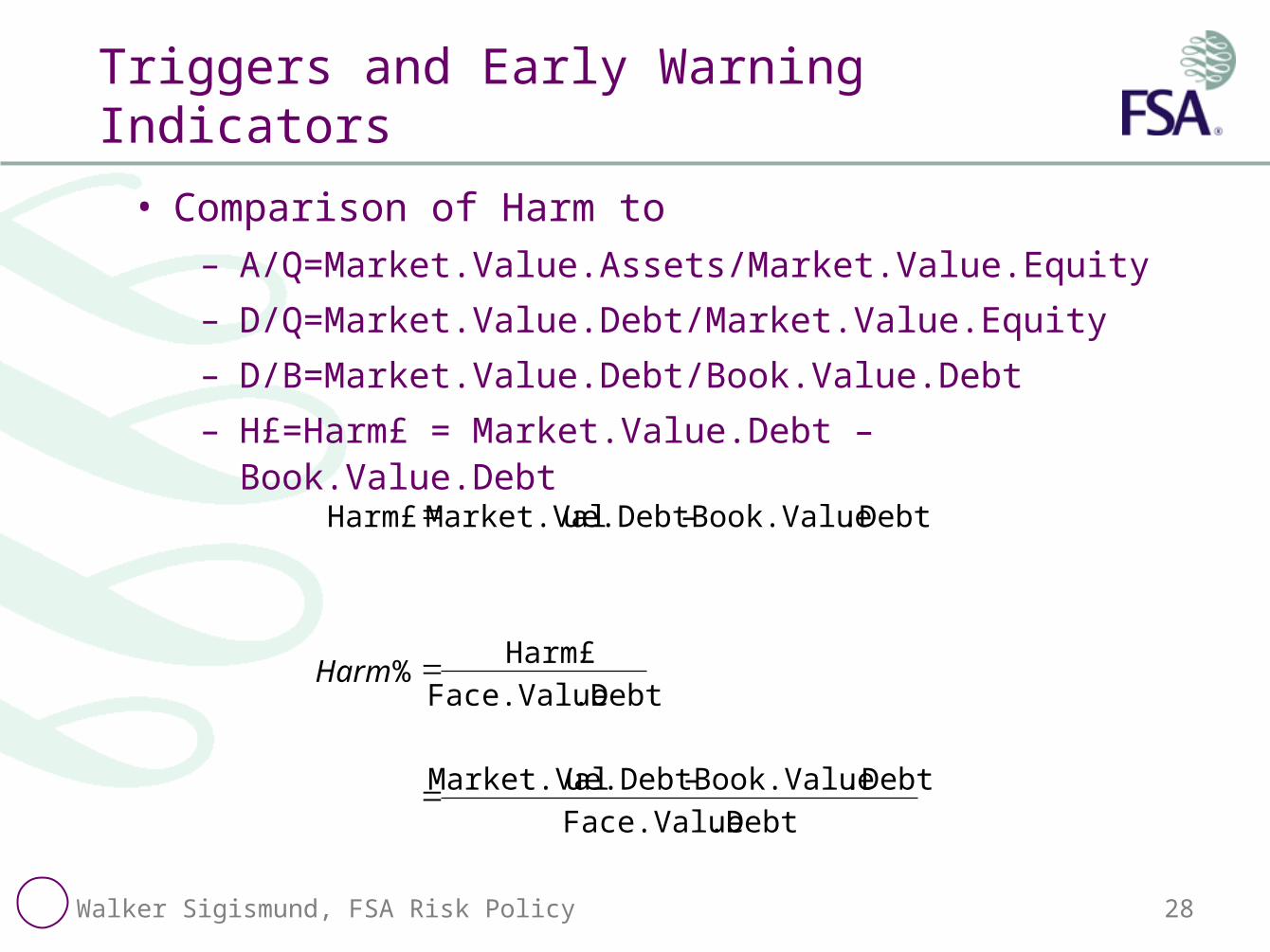

Triggers and Early Warning Indicators

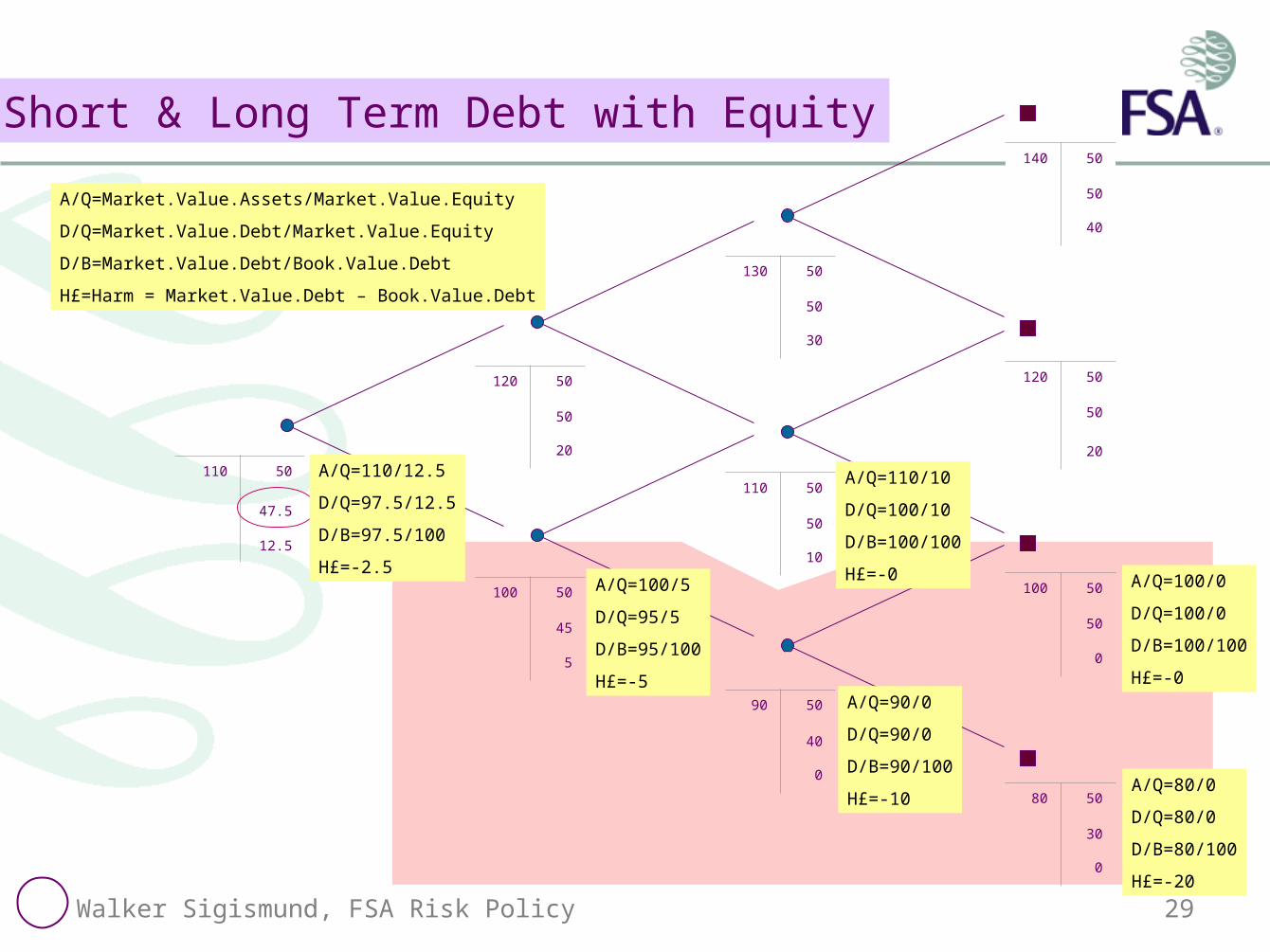

• Comparison of Harm to– A/Q=Market.Value.Assets/Market.Value.Equity

– D/Q=Market.Value.Debt/Market.Value.Equity

– D/B=Market.Value.Debt/Book.Value.Debt

– H£=Harm£ = Market.Value.Debt – Book.Value.Debt

.DebtFace.Value

.DebtBook.Value– ue.Debt Market.Val

.DebtFace.Value

Harm£%

.DebtBook.Value– ue.Debt Market.ValHarm£

Harm

Walker Sigismund, FSA Risk Policy 29

130 50

50

30

140 50

50

40

110 50

50

10

90 50

40

0

120 50

50

20

100 50

50

0

80 50

30

0

120 50

50

20

100 50

45

5

110 50

47.5

12.5

Short & Long Term Debt with Equity

A/Q=110/12.5

D/Q=97.5/12.5

D/B=97.5/100

H£=-2.5A/Q=100/5

D/Q=95/5

D/B=95/100

H£=-5

A/Q=110/10

D/Q=100/10

D/B=100/100

H£=-0

A/Q=90/0

D/Q=90/0

D/B=90/100

H£=-10A/Q=80/0

D/Q=80/0

D/B=80/100

H£=-20

A/Q=Market.Value.Assets/Market.Value.Equity

D/Q=Market.Value.Debt/Market.Value.Equity

D/B=Market.Value.Debt/Book.Value.Debt

H£=Harm = Market.Value.Debt – Book.Value.Debt

A/Q=100/0

D/Q=100/0

D/B=100/100

H£=-0

Walker Sigismund, FSA Risk Policy 30

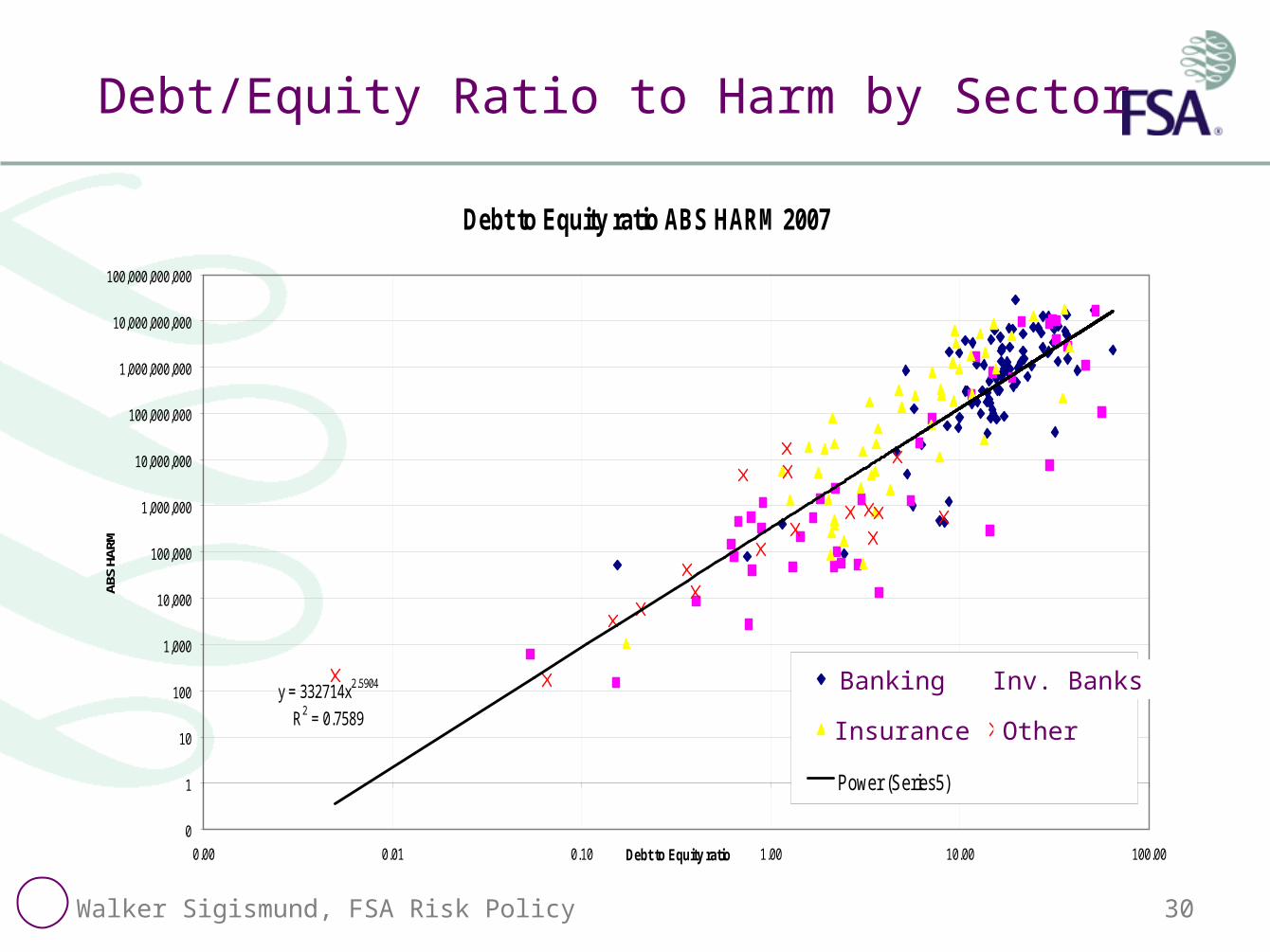

Debt/Equity Ratio to Harm by Sector

Debt to Equity ratio ABS HARM 2007

y = 332714x2.5904

R2 = 0.7589

0

1

10

100

1,000

10,000

100,000

1,000,000

10,000,000

100,000,000

1,000,000,000

10,000,000,000

100,000,000,000

0.00 0.01 0.10 1.00 10.00 100.00Debt to Equity ratio

ABS

HARM

6000 to 6200 6201 to 6300

6301 to 6500 6000

Power (Series5)

Banking Inv. Banks

Insurance Other

Walker Sigismund, FSA Risk Policy 31

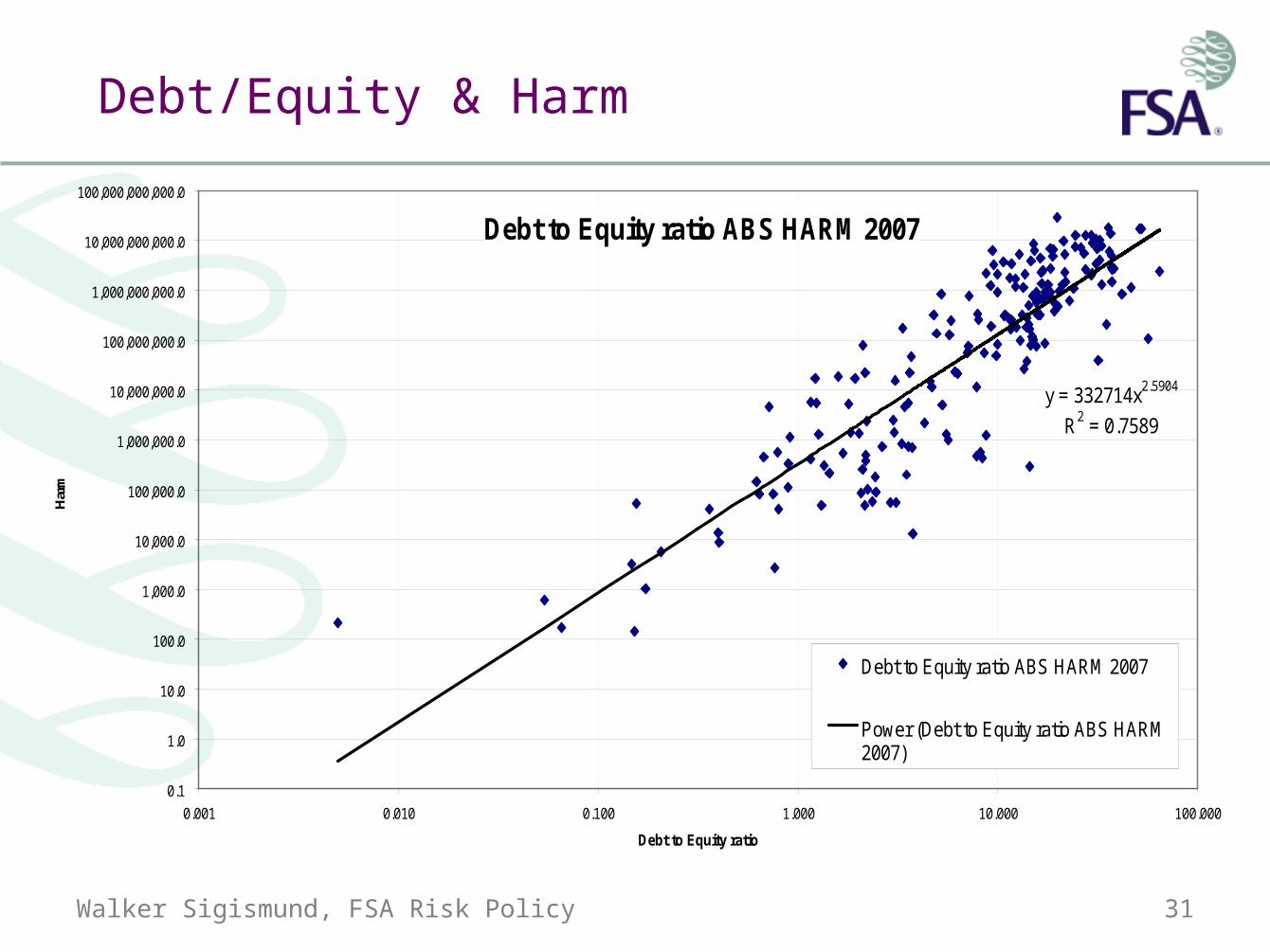

Debt/Equity & Harm

Debt to Equity ratio ABS HARM 2007

y = 332714x2.5904

R2 = 0.7589

0.1

1.0

10.0

100.0

1,000.0

10,000.0

100,000.0

1,000,000.0

10,000,000.0

100,000,000.0

1,000,000,000.0

10,000,000,000.0

100,000,000,000.0

0.001 0.010 0.100 1.000 10.000 100.000

Debt to Equity ratio

Har

m

Debt to Equity ratio ABS HARM 2007

Power (Debt to Equity ratio ABS HARM2007)

Walker Sigismund, FSA Risk Policy 32

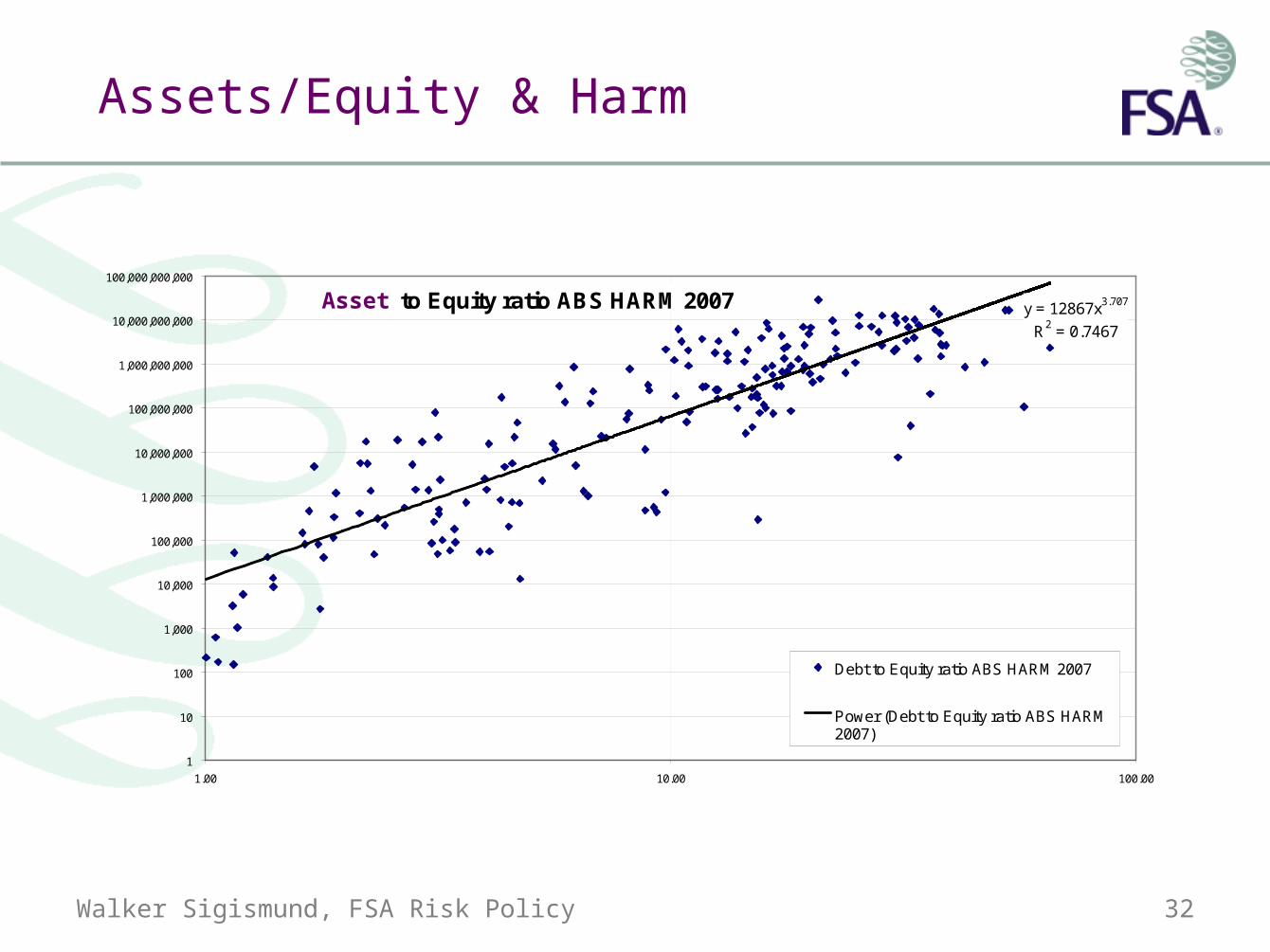

Assets/Equity & Harm

Debt to Equity ratio ABS HARM 2007 y = 12867x3.707

R2 = 0.7467

1

10

100

1,000

10,000

100,000

1,000,000

10,000,000

100,000,000

1,000,000,000

10,000,000,000

100,000,000,000

1.00 10.00 100.00

Debt to Equity ratio ABS HARM 2007

Power (Debt to Equity ratio ABS HARM2007)

Asset

Walker Sigismund, FSA Risk Policy 33

– Extensive Data Analysis –

Empirical Results from 5000+ firms

Across all major markets

Links to Accounting and Regulatory Returns

Supply/Demand Model

Walker Sigismund, FSA Risk Policy 34

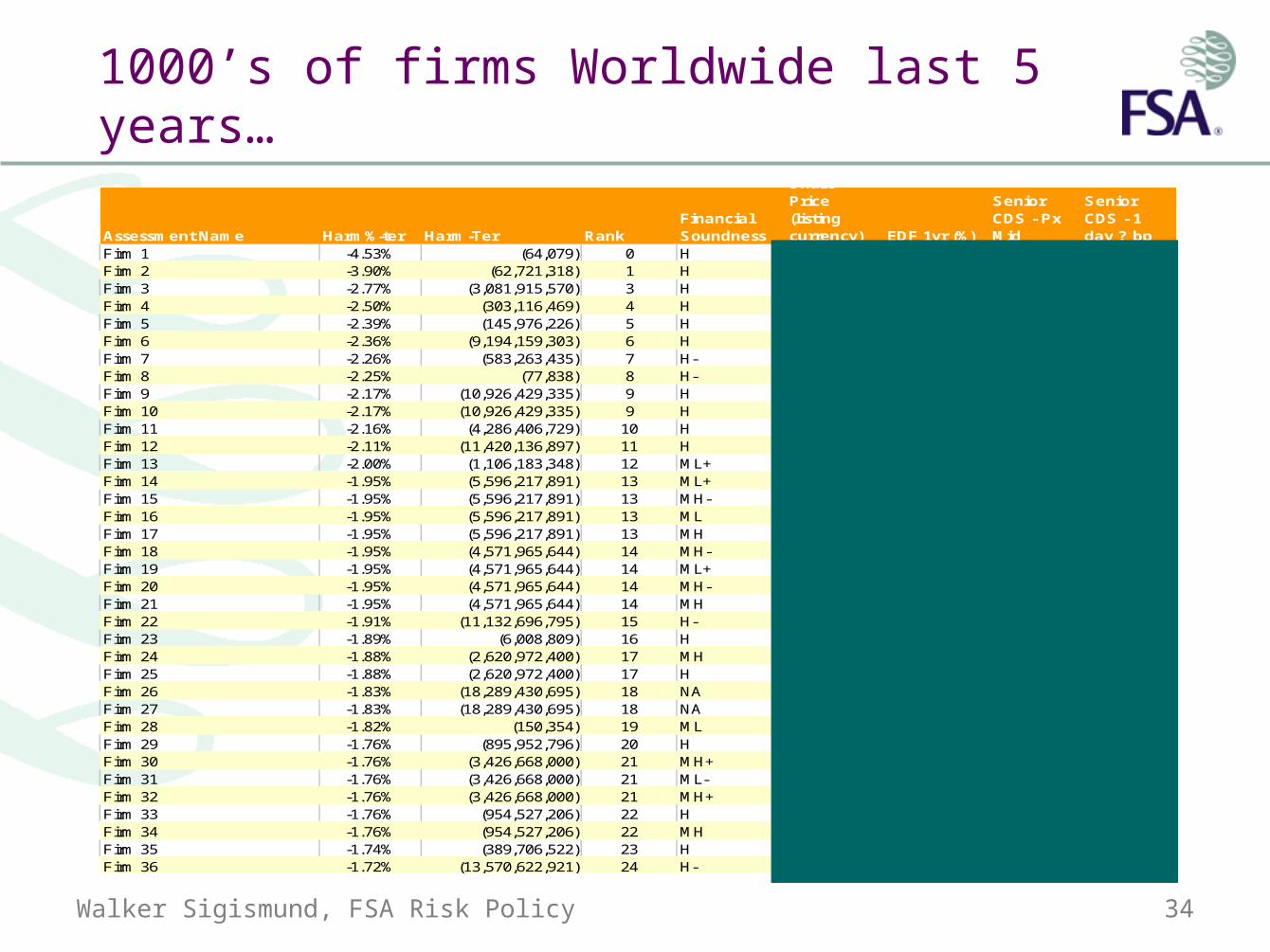

1000’s of firms Worldwide last 5 years…

Assessment Name Harm%-ter Harm-Ter RankFinancial Soundness

Share Price (listing currency) EDF 1yr (%)

Senior CDS - Px Mid

Senior CDS - 1 day ? bp

Firm 1 -4.53% (64,079) 0 H 1.75 24.5 #N/A #N/AFirm 2 -3.90% (62,721,318) 1 H 0.38 32.49 2742.37 97.10Firm 3 -2.77% (3,081,915,570) 3 H 0.11 143.63 -0.39Firm 4 -2.50% (303,116,469) 4 H 1.90 20.72 1778.65 -3.37Firm 5 -2.39% (145,976,226) 5 H 30.32 #N/A #N/AFirm 6 -2.36% (9,194,159,303) 6 H 23.75 0.19 282.76 27.97Firm 7 -2.26% (583,263,435) 7 H- 3.50 3.91 630.00 0.00Firm 8 -2.25% (77,838) 8 H- 14.00 11.54 #N/A #N/AFirm 9 -2.17% (10,926,429,335) 9 H 0.11 #N/A #N/AFirm 10 -2.17% (10,926,429,335) 9 H 35.46 0.11 205.11 8.52Firm 11 -2.16% (4,286,406,729) 10 H 9.33 0.46 87.77 1.16Firm 12 -2.11% (11,420,136,897) 11 H 37.13 0.12 187.98 8.29Firm 13 -2.00% (1,106,183,348) 12 ML+ 551.00 0.02 #N/A #N/AFirm 14 -1.95% (5,596,217,891) 13 ML+ 573.50 0.09 108.57 -3.99Firm 15 -1.95% (5,596,217,891) 13 MH- 0.09 #N/A #N/AFirm 16 -1.95% (5,596,217,891) 13 ML 0.09 #N/A #N/AFirm 17 -1.95% (5,596,217,891) 13 MH 0.09 #N/A #N/AFirm 18 -1.95% (4,571,965,644) 14 MH- 0.07 #N/A #N/AFirm 19 -1.95% (4,571,965,644) 14 ML+ 0.07 #N/A #N/AFirm 20 -1.95% (4,571,965,644) 14 MH- 9.08 0.07 121.62 -3.71Firm 21 -1.95% (4,571,965,644) 14 MH 0.07 #N/A #N/AFirm 22 -1.91% (11,132,696,795) 15 H- 162.40 0.08 117.74 6.80Firm 23 -1.89% (6,008,809) 16 H 8.35 19.07 #N/A #N/AFirm 24 -1.88% (2,620,972,400) 17 MH 0.09 #N/A #N/AFirm 25 -1.88% (2,620,972,400) 17 H 234.00 0.09 #N/A #N/AFirm 26 -1.83% (18,289,430,695) 18 NA 0.04 #N/A #N/AFirm 27 -1.83% (18,289,430,695) 18 NA 22.02 0.04 66.13 1.63Firm 28 -1.82% (150,354) 19 ML 15.50 10.4 #N/A #N/AFirm 29 -1.76% (895,952,796) 20 H 67.00 2.61 208.33 0.52Firm 30 -1.76% (3,426,668,000) 21 MH+ 611.00 0.02 64.93 1.05Firm 31 -1.76% (3,426,668,000) 21 ML- 0.02 #N/A #N/AFirm 32 -1.76% (3,426,668,000) 21 MH+ 0.02 #N/A #N/AFirm 33 -1.76% (954,527,206) 22 H 116.40 0.14 131.00 0.00Firm 34 -1.76% (954,527,206) 22 MH 0.14 #N/A #N/AFirm 35 -1.74% (389,706,522) 23 H 4.85 13.26 1718.93 -4.20Firm 36 -1.72% (13,570,622,921) 24 H- 0.08 #N/A #N/A

Walker Sigismund, FSA Risk Policy 35

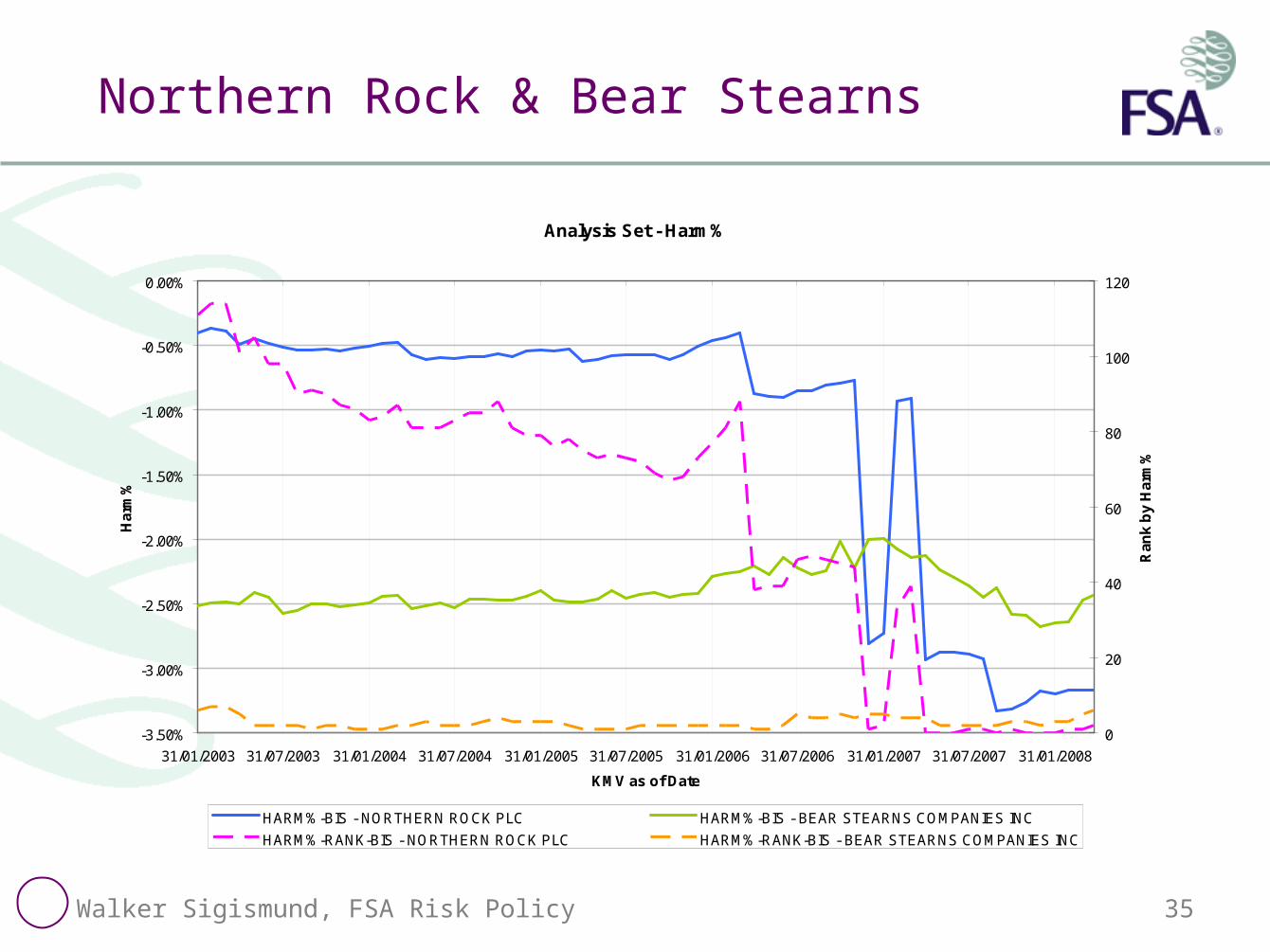

Northern Rock & Bear Stearns

Analysis Set - Harm%

-3.50%

-3.00%

-2.50%

-2.00%

-1.50%

-1.00%

-0.50%

0.00%

31/01/2003 31/07/2003 31/01/2004 31/07/2004 31/01/2005 31/07/2005 31/01/2006 31/07/2006 31/01/2007 31/07/2007 31/01/2008

KMV as of Date

Har

m%

0

20

40

60

80

100

120

Ran

k b

y H

arm

%

HARM%-BIS - NORTHERN ROCK PLC HARM%-BIS - BEAR STEARNS COMPANIES INC

HARM%-RANK-BIS - NORTHERN ROCK PLC HARM%-RANK-BIS - BEAR STEARNS COMPANIES INC

Walker Sigismund, FSA Risk Policy 36

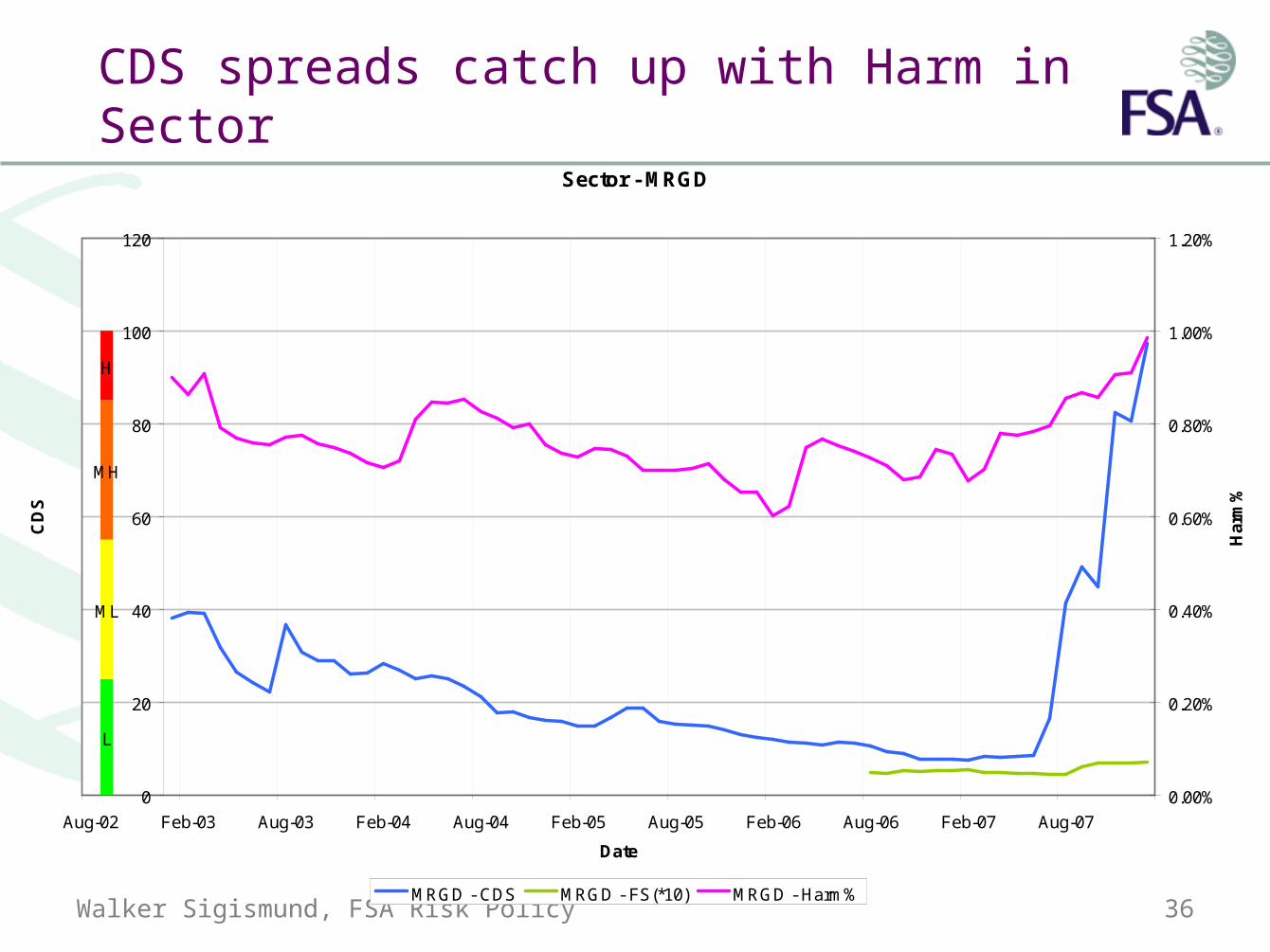

CDS spreads catch up with Harm in Sector

Sector - MRGD

L

ML

MH

H

0

20

40

60

80

100

120

Aug-02 Feb-03 Aug-03 Feb-04 Aug-04 Feb-05 Aug-05 Feb-06 Aug-06 Feb-07 Aug-07

Date

CD

S

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

Har

m%

MRGD - CDS MRGD - FS(*10) MRGD - Harm%

Walker Sigismund, FSA Risk Policy 37

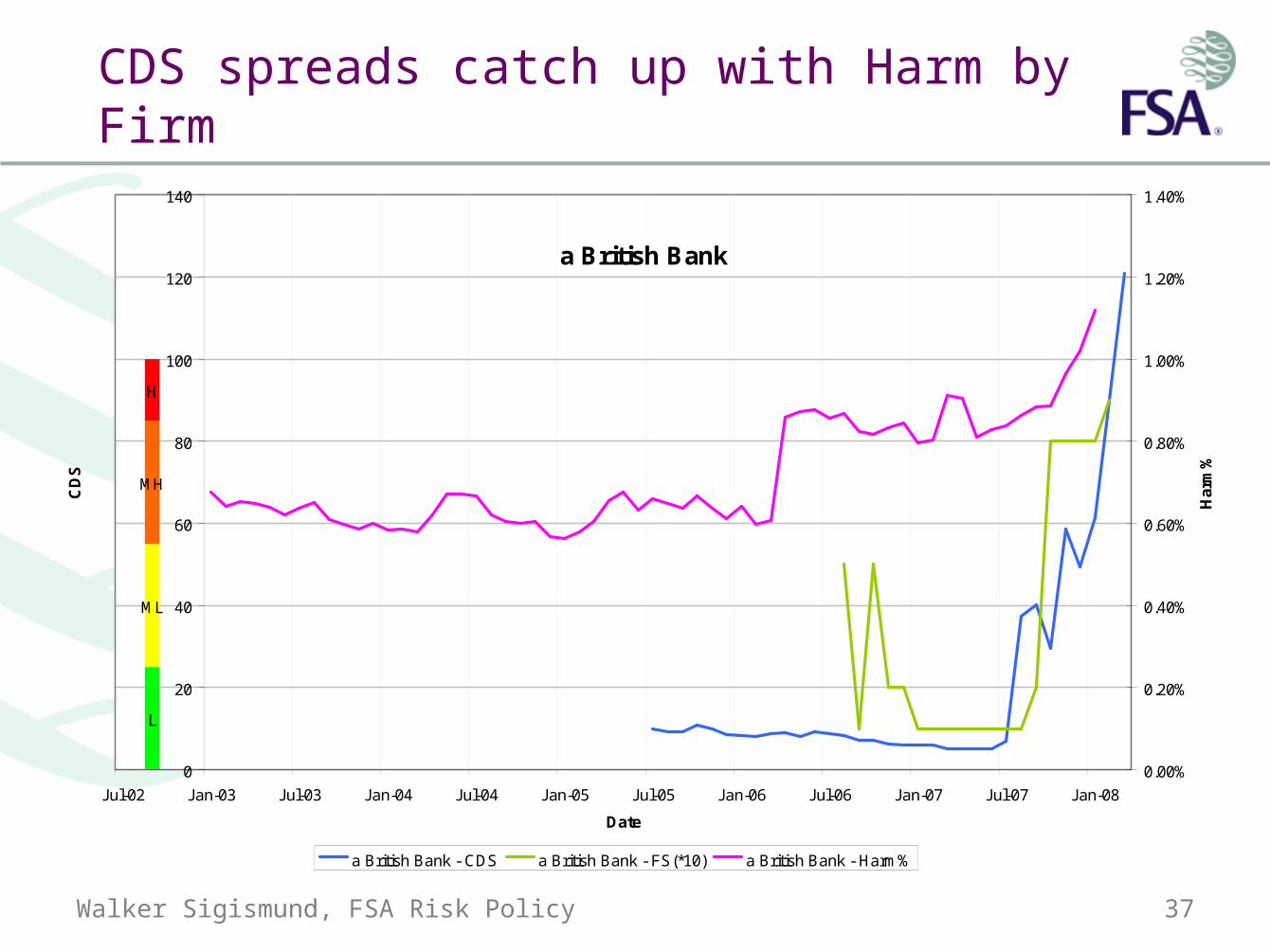

CDS spreads catch up with Harm by Firm

a British Bank

L

ML

MH

H

0

20

40

60

80

100

120

140

Jul-02 Jan-03 Jul-03 Jan-04 Jul-04 Jan-05 Jul-05 Jan-06 Jul-06 Jan-07 Jul-07 Jan-08

Date

CD

S

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

Har

m%

a British Bank - CDS a British Bank - FS(*10) a British Bank - Harm%

Walker Sigismund, FSA Risk Policy 38

Pattern of Riskiness by Sector

(35,000,000,000)

(30,000,000,000)

(25,000,000,000)

(20,000,000,000)

(15,000,000,000)

(10,000,000,000)

(5,000,000,000)

-

-5.0% -4.5% -4.0% -3.5% -3.0% -2.5% -2.0% -1.5% -1.0% -0.5% 0.0%

Life Insurers Retail Banks Wholesale Banks: EEA Wholesale Investment Banks: Group 1 Wholesale Investment Banks: Group 2

Walker Sigismund, FSA Risk Policy 39

Empirical Results

• Powerful Warning Indicator– NRK to be Riskiest firm up to 1 year before event

– Bear-Stearns… near top for a long time

– Seemingly all ‘problem’ firms at the top (various discussions with US and other regulators)

• Risk by Sector– Investment Banks, Insurance, Retail Banking… Real

Economy

• Risk by major market– Total Harm£ over £368Billion and rising

• Statistical and Logical Links to – Accounting and Regulatory Returns

Walker Sigismund, FSA Risk Policy 40

– End –

![[Clarinet_Institute] Neukomm, Sigismund - Clarinet Quintet, Op. 8.pdf](https://img.pdfslide.us/doc/110x75/552ef8214a795978658b4acf/clarinetinstitute-neukomm-sigismund-clarinet-quintet-op-8pdf.jpg)