Embed Size (px)

DESCRIPTION

Walker Real Estate Mortgage Package

Citation preview

Dear Client, We are Cindy and Amanda Walker, Licensed Mortgage Professionals with Dominion Lending Centres Leading Edge located at #201 15955 Fraser Hwy, Surrey, B.C. V4N 0Y3. We have access to a multiple mortgage products and services to meet your unique needs when it comes time to renew your mortgage, refinance to consolidate debt, take equity out of your home for renovation purposes, or even lease business-related equipment.

With have access to more than 90 lending institutions, including big banks, credit unions and trust companies. We are familiar with a vast array of available mortgage products – ranging from financing for the self-employed to financing for those with credit blemishes.

And, best of all, We work for you – not the lenders – ensuring you always receive the best mortgage product and rate to serve your specific needs. Based on the high volume of business we fund, lenders offer us better discounts on mortgages that we can further pass on to our clientele. With interest rates continuing to fall to historic lows, refinancing your existing mortgage and switching to a lower rate may save you a lot of money – possibly thousands of dollars per year. Imagine what you could do with the savings – anything from renovating or investing to going on a much-needed vacation or putting money towards your children’s education. By refinancing now and paying off high-interest debt, such as credit cards, you can put yourself and your family in a better financial position. If your current mortgage is up for renewal, you’re thinking of refinancing your mortgage or you’d like to discuss your options, please give us a call.

About Dominion Lending Centres

Dominion Lending Centres is Canada’s fastest-growing national mortgage brokerage and leasing company with more than 1,600 Mortgage Professionals spanning the country. Launched in January 2006, the company was named Best Newcomer (Mortgage Brokerage Firm) at the prestigious CMP Canadian Mortgage Awards 2008. And at the 2009 CMAs, the company received the Best Branding Award. Dominion Lending Centres was also ranked 23rd on the PROFIT HOT 50 list of emerging growth companies that appeared in the October 2009 issue of Profit Magazine. For more information, visit: www.dominionlending.ca Sincerely, Cindy Walker, AMP Amanda Walker, Licensed Assistant Dominion Lending Centres Leading Edge Tel: 604-889-5004; Fax: 604-541-0897 Email: [email protected] Website: www.whiterockwalker.com

Products & Services

Monthly Income (Net)

Salary -

Salary -

Rental

Other

Other

MONTHLY EXPENSES

Maintaining Your Home Maintaing Your Lifestyle

Mortgage/Rent Eating Out/Coffee

Property Taxes Concerts/Clubs/Movies/Plays

Strata Fees Magazines/Newspapers

Light/Water/Heating Religious/Charitable Donations

Home Insurance Sports/Gym/Club Membership

Cell Phone Gifts/Holiday Presents & Decorations

Cable/Internet/Home Phone Vacations/Travel

Computer Lease Clothing/Shoes

Home Repairs/Home Improvements Hair/Mani-Pedi/Spa/Massages

Home Security Music/Books

Other Other

Maintaining Your Family Maintaining Your Future

Groceries Disability Insurance

Dry Cleaning Critical Illness Insurance

Auto Repairs Long Term Care Insurance

Auto Insurance Life Insurance

Auto Lease/Payments Short Term Savings (Emergencies)

Auto Parking/Parking Tickets Major Purchase Savings (Eg. Home)

Auto Gas RRSP Contributions

Public Transportation/Taxi's Education/RESP Savings

Child Care/Nanny Credit Card Payments

Child Support/Alimony Investment Loan

House Cleaning Loan/Line of Credit Payments

Education (Tuition,Books,Other) Student Loans

Health and Dental Insurance (Private) Other

MSP Other

Drugs/Vision Care (Not Covered) Other

Animal Care Other

Other Other

Other Other

Other Other

Balance Sheet

Total Monthly Income 0

Total Monthly Expenses 0

Cash Flow Surplus/(Deficit) 0

MORTGAGE APPLICATION

Referral: ___________________________

Applicant Information: Full Name S.I.N. Date of Birth Dependants Marital Status

Present Address Postal Code Rent/Own No. Of Years

$

Previous Address: (if less than 3 years at current) Rent/Own No. Of Years

$

Home Phone: Home Fax: Cellular:

Bus Phone: Bus Fax: Email:

Current Employer Years Gross Annual Income Occupation

Previous Employer: (if less than 3 years at current) Years Gross Annual Income Occupation

1

2 Other Income: Source Years Income Occupation

Smoker? ____ Yes ____ No First Time Buyer? _____ Yes ____ No

Co-Applicant Information:

Full Name S.I.N. Date of Birth Marital Status

Address Postal Code Yrs

Home Phone: Home Fax: Cellular:

Business Phone: Bus Fax: Email:

Current Employer Years Gross Annual Income Occupation

Previous Employer: (if less than 3 years at current) Years Gross Annual Income Occupation

1

2

Other Income Years Gross Annual Income Occupation

Smoker? ____ Yes ____ No First Time Buyer? _____ Yes ____ No

Assets: Bank: Location: Type: Balance: $

Bank: Location: Type: Balance: $

RRSP: Value: $

Stocks/Bonds/GIC: Value: $

Automobile: Value: $

Automobile: Value: $

Other Assets: Value: $

Other Assets: Value: $

Other Assets: Value: $

Household Goods: Value: $

Liabilities: Bank Loan/LOC Balance: $ Payment: $

Bank Loan/LOC Balance: $ Payment: $

Bank Loan/LOC Balance: $ Payment: $

Credit Card Type: Balance: $ Payment: $

Credit Card Type: Balance: $ Payment: $

Credit Card Type: Balance: $ Payment: $

Credit Card Type: Balance: $ Payment: $

Other Debt: Balance: $

Other Debt: Balance: $

Current Mortgages/Properties Owned: Address: Property Value: $

Existing Mortgage Bank/Lender: First: Second:

Mortgage Rate: % Monthly Payments: $ Rental Income: $ Mortgage Balance: $

Address: Property Value: $

Existing Mortgage Bank/Lender: First: Second:

Mortgage Rate: % Monthly Payments: $ Rental Income: $ Mortgage Balance: $

Address: Property Value: $

Existing Mortgage Bank/Lender: First: Second:

Mortgage Rate: % Monthly Payments: $ Rental Income: $ Mortgage Balance: $

Signature: Date:

Signature: Date:

Verbal Consent - By Broker Date:

Notes:

Inco

me

Typ

e

Det

aile

d R

equ

irem

ents

Sa

lary

/Ho

url

y W

e w

ill

req

uir

e a

lett

er f

rom

yo

ur

emp

loy

er o

n c

om

pan

y l

ette

rhea

d s

tati

ng

yo

ur

star

t d

ate,

po

siti

on

an

d m

inim

um

sal

ary

. W

e a

lso

re

qu

ire

a cu

rren

t p

ay s

tub

.

If y

ou

r d

eal w

as a

pp

rov

ed o

n t

he

bas

is o

f y

ou

pro

vid

ing

min

imal

inco

me

con

firm

atio

n (

Sta

ted

In

com

e P

rog

ram

), y

ou

nee

d t

o p

rov

ide

a le

tter

of

emp

loy

men

t co

nfi

rmin

g y

ou

r st

art

dat

e a

nd

po

siti

on

alo

ng

wit

h y

ou

r m

ost

rec

ent

No

tice

of

Ass

essm

ent

that

co

nfi

rms

no

in

com

e ta

x ar

rear

s.

Co

mm

issi

on

W

e w

ill

req

uir

e a

lett

er f

rom

yo

ur

emp

loy

er o

n c

om

pan

y l

ette

rhea

d s

tati

ng

yo

ur

star

t d

ate

and

po

siti

on

alo

ng

wit

h y

ou

r N

oti

ce o

f A

s-se

ssm

ent

for

the

last

tw

o y

ears

th

at c

on

firm

s y

ou

r in

com

e.

Bu

sin

ess

fo

r Se

lf

We

wil

l re

qu

ire

Per

son

al T

ax A

sses

smen

t N

oti

ces

for

the

last

tw

o y

ears

co

nfi

rmin

g y

ou

r in

com

e as

wel

l as

fin

an

cial

sta

tem

ents

fro

m

the

bu

sin

ess

for

tho

se s

ame

two

yea

rs.

If y

ou

r m

ort

gag

e is

an

in

sure

d d

eal

wit

h G

enw

ort

h o

r C

MH

C (

see

yo

ur

com

mit

men

t to

co

nfi

rm),

we

wil

l req

uir

e 2

yea

rs N

oti

ce o

f A

s-se

ssm

ent

con

firm

ing

yo

ur

inco

me

as w

ell a

s o

ne

of

the

foll

ow

ing:

Bu

sin

ess

Cre

dit

Rep

ort

, tw

o y

ears

GS

T r

etu

rns,

co

nfi

rmat

ion

of

acti

ve

bu

sin

ess

ban

k a

cco

un

ts in

dic

atin

g tw

o y

ears

sat

isfa

cto

ry o

per

atio

ns

or

two

yea

rs a

ud

ited

or

acco

un

tan

t p

rep

ared

fin

anc

ial

stat

emen

ts.

If y

ou

r d

eal w

as a

pp

rov

ed o

n t

he

bas

is o

f y

ou

pro

vid

ing

min

imal

inco

me

con

firm

atio

n (

Sta

ted

In

com

e P

rog

ram

), y

ou

wil

l b

e re

qu

ired

to

pro

vid

e o

ne

of

the

foll

ow

ing

to c

on

firm

a m

inim

um

of

two

yea

rs b

usi

nes

s fo

r se

lf:

Bu

sin

ess

Cre

dit

Rep

ort

, Bu

sin

ess

Lic

ense

, GST

re

turn

, Art

icle

s o

f In

corp

ora

tio

n, A

cco

un

tan

t p

rep

ared

T1

Gen

eral

s al

on

g w

ith

Sta

tem

ent

of

Bu

sin

ess

Act

ivit

ies.

In

ad

dit

ion

to

on

e o

f th

e ab

ov

e, w

e w

ill a

lso

req

uir

e y

ou

r la

st y

ears

No

tice

of

Ass

essm

ent

that

co

nfi

rms

no

in

com

e ta

x ar

rear

s

Pen

sio

n

We

wil

l re

qu

ire

yo

ur

T4

A f

or

the

mo

st r

ecen

t ta

x y

ear

or

3 m

on

ths

ban

k s

tate

men

ts c

on

firm

ing

auto

mat

ic d

epo

sits

.

Ca

r A

llow

an

ce

We

wil

l re

qu

ire

a le

tter

fro

m y

ou

r em

plo

yer

co

nfi

rmin

g th

at t

he

car

allo

wan

ce i

s a

taxa

ble

in

com

e as

wel

l as

yo

ur

T4

fro

m la

st y

ear

to

con

firm

No

n-T

axab

le

We

wil

l re

qu

ire

on

e o

f th

e fo

llo

win

g co

nfi

rmin

g y

ou

r an

nu

al in

com

e is

no

n-t

axab

le i

nco

me:

a c

urr

ent

pay

stu

b, y

ou

r m

ost

rec

ent

No

-ti

ce O

f A

sses

smen

t, a

lett

er f

rom

th

e so

urc

e o

f y

ou

r in

com

e o

r y

ou

r m

ost

rec

ent

T5

00

7

Bo

nu

s/O

verti

me

W

e w

ill

req

uir

e y

ou

r jo

b le

tter

an

d T

4s

for

the

last

tw

o y

ears

or

No

tice

of

Ass

essm

ent

for

the

pas

t tw

o y

ears

co

nfi

rmin

g y

ou

r av

erag

e n

et in

com

e.

Oth

er In

com

e

We

wil

l re

qu

ire

a le

tter

fro

m y

ou

r em

plo

yer

sta

tin

g y

ou

r st

art

dat

e an

d p

osi

tio

n a

s w

ell a

s y

ou

r N

oti

ce o

f A

sses

smen

t fo

r th

e la

st t

wo

y

ears

co

nfi

rmin

g an

av

erag

e in

com

e.

Inve

stm

ent

We

wil

l re

qu

ire

yo

ur

No

tice

of

Ass

essm

ent

for

the

last

tw

o y

ears

co

nfi

rmin

g a

n a

ver

age

in

com

e

Rel

oca

tio

n

We

wil

l re

qu

ire

a co

py

of

yo

ur

relo

cati

on

lett

er o

r cu

rren

t p

ay s

tub

co

nfi

rmin

g y

ou

r an

nu

al s

alar

y.

If b

on

us

or

com

mis

sio

n i

nco

me

is

incl

ud

ed, a

co

py

of

yo

ur

last

tw

o y

ears

No

tice

of

Ass

essm

ent

or

T4

s to

dem

on

stra

te a

tw

o-y

ear

aver

age

wil

l als

o b

e re

qu

ired

.

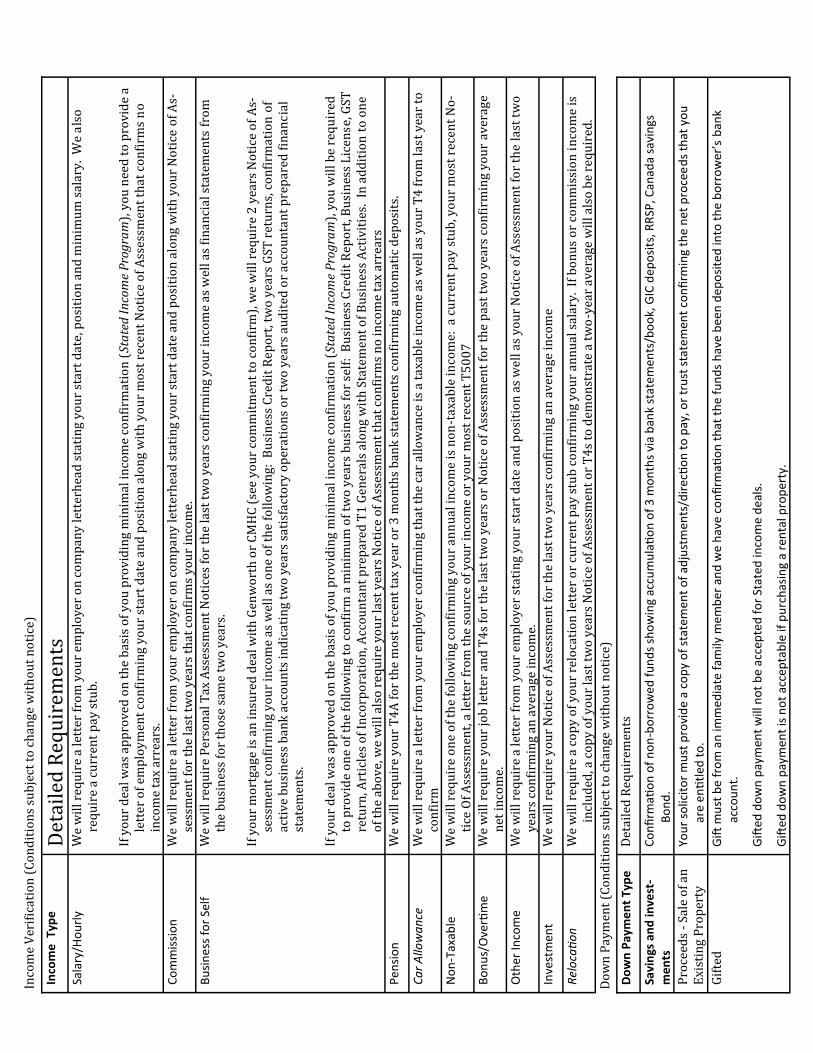

Do

wn

Pay

me

nt

Typ

e

Det

aile

d R

equ

irem

ents

Sa

vin

gs a

nd

inve

st-

me

nts

C

on

firm

atio

n o

f n

on

-bo

rro

we

d f

un

ds

sho

win

g ac

cum

ula

tio

n o

f 3

mo

nth

s vi

a b

ank

stat

em

ents

/bo

ok,

GIC

dep

osi

ts, R

RSP

, Can

ada

savi

ngs

B

on

d.

Pro

ceed

s -

Sale

of

an

Exi

stin

g P

rop

erty

Yo

ur

solic

ito

r m

ust

pro

vid

e a

cop

y o

f st

atem

ent

of

adju

stm

ents

/dir

ecti

on

to

pay

, or

tru

st s

tate

men

t co

nfi

rmin

g th

e n

et p

roce

ed

s th

at y

ou

ar

e en

titl

ed t

o.

Gif

ted

Gift

mu

st b

e fr

om

an

imm

edia

te f

amily

me

mb

er a

nd

we

hav

e co

nfi

rmati

on

th

at t

he

fun

ds

hav

e b

een

dep

osi

ted

into

th

e b

orr

ow

er’s

ban

k ac

cou

nt.

Gift

ed d

ow

n p

aym

ent

will

no

t b

e ac

cep

ted

fo

r St

ated

inco

me

dea

ls.

Gift

ed d

ow

n p

aym

ent

is n

ot

acce

pta

ble

if p

urc

has

ing

a re

nta

l pro

per

ty.

Inco

me

Ver

ific

atio

n (

Co

nd

itio

ns

sub

ject

to

ch

ang

e w

ith

ou

t n

oti

ce)

Do

wn

Pay

men

t (C

on

dit

ion

s su

bje

ct t

o c

han

ge

wit

ho

ut

no

tice

)

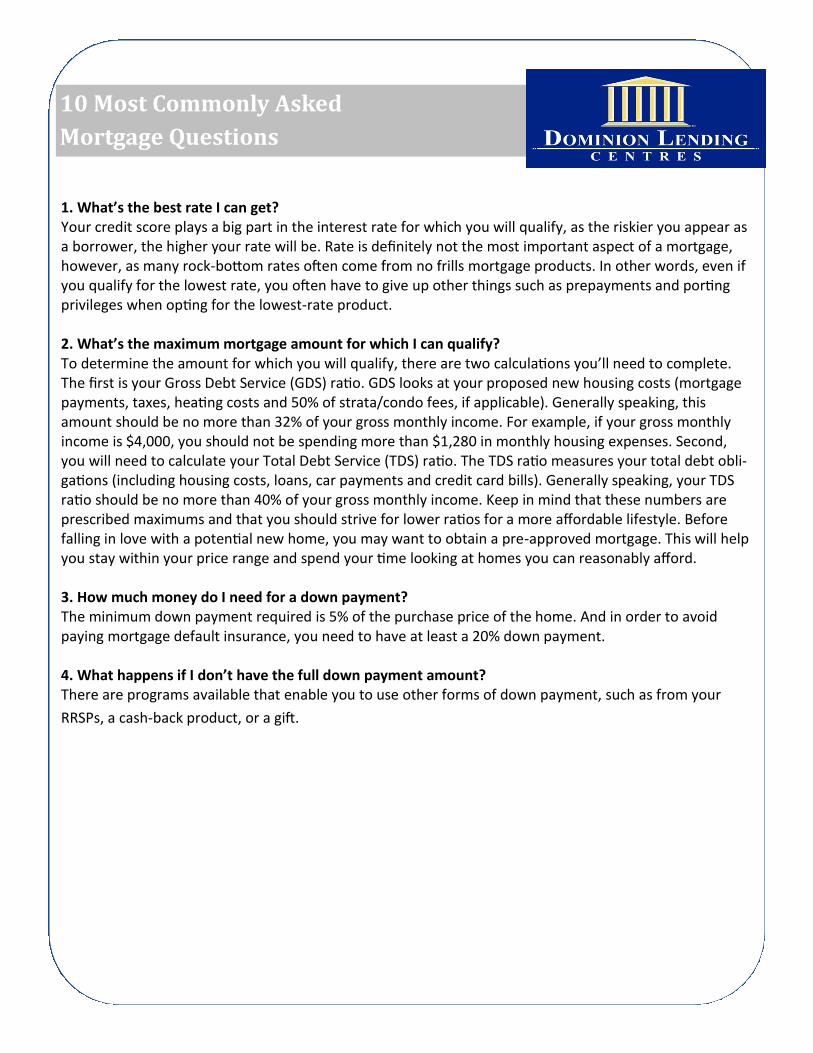

10 Most Commonly Asked

Mortgage Questions

1. What’s the best rate I can get? Your credit score plays a big part in the interest rate for which you will qualify, as the riskier you appear as a borrower, the higher your rate will be. Rate is definitely not the most important aspect of a mortgage, however, as many rock-bottom rates often come from no frills mortgage products. In other words, even if you qualify for the lowest rate, you often have to give up other things such as prepayments and porting privileges when opting for the lowest-rate product. 2. What’s the maximum mortgage amount for which I can qualify? To determine the amount for which you will qualify, there are two calculations you’ll need to complete. The first is your Gross Debt Service (GDS) ratio. GDS looks at your proposed new housing costs (mortgage payments, taxes, heating costs and 50% of strata/condo fees, if applicable). Generally speaking, this amount should be no more than 32% of your gross monthly income. For example, if your gross monthly income is $4,000, you should not be spending more than $1,280 in monthly housing expenses. Second, you will need to calculate your Total Debt Service (TDS) ratio. The TDS ratio measures your total debt obli-gations (including housing costs, loans, car payments and credit card bills). Generally speaking, your TDS ratio should be no more than 40% of your gross monthly income. Keep in mind that these numbers are prescribed maximums and that you should strive for lower ratios for a more affordable lifestyle. Before falling in love with a potential new home, you may want to obtain a pre-approved mortgage. This will help you stay within your price range and spend your time looking at homes you can reasonably afford. 3. How much money do I need for a down payment? The minimum down payment required is 5% of the purchase price of the home. And in order to avoid paying mortgage default insurance, you need to have at least a 20% down payment. 4. What happens if I don’t have the full down payment amount? There are programs available that enable you to use other forms of down payment, such as from your

RRSPs, a cash-back product, or a gift.

10 Most Commonly Asked

Mortgage Questions

5. What will a lender look at when qualifying me for a mortgage? Most lenders look at five factors when determining whether you qualify for a mortgage: 1. Income; 2. Debts; 3. Employment History; 4. Credit history; and 5. Value of the Property you wish to purchase. One of the first things a lender will consider is how much of your total income you’ll be spending on housing. This helps the lender decide whether you can comfortably afford a house. A lender will then look at your debts, which generally include monthly house payments as well as payments on all loans, credit cards, child support, etc. A history of steady employment, usually within the same job for several years, helps you qualify. But a short history in your current job shouldn’t prevent you from getting a mortgage, as long as there have been no gaps in income over the past two years. Good credit is also very important in qualify-ing for a mortgage. The lender will also want to know that the house is worth the price you plan to pay. 6. Should I go with a fixed- or variable-rate mortgage? The answer to this question depends on your personal risk tolerance. If, for instance, you’re a first-time homebuyer and/or you have a set budget that you can comfortably spend on your mortgage, it’s smart to lock into a fixed mortgage with predictable payments over a specific period of time. If, however, your financial situation can handle the fluctuations of a variable-rate mortgage, this may save you some money over the long run. Another option is to opt for a variable rate, but make payments based on what you would have paid if you selected a fixed rate. Finally, there are also 50/50 mortgage options that enable you to split your mortgage into both fixed and variable portions. 7. What credit score do I need to qualify? Generally speaking, you’re a prime candidate for a mortgage if your credit score is 680 and above. The

higher you can get above 700 the better, as you will qualify for the lowest rates. These days almost anyone

can obtain a mortgage, but the key for those with lower credit scores is the size of the down payment. If you

have a sufficient down payment, you can reduce the risk to the lender providing you with the mortgage.

Statistics show that default rates on mortgages decline as the down payment increases.

10 Most Commonly Asked

Mortgage Questions

8. What happens if my credit score isn’t great? There are several things you can do to boost your credit fairly quickly. Following are five steps you can use to help attain a speedy credit score boost: 1) Pay down credit cards. The number one way to increase your credit score is to pay down your credit cards so they’re below 70% of your limits. Revolving credit like cred-it cards seems to have a more significant impact on credit scores than car loans, lines of credit, and so on. 2) Limit the use of credit cards. Racking up a large amount and then paying it off in monthly instalments can hurt your credit score. If there is a balance at the end of the month, this affects your score – credit for-mulas don’t take into account the fact that you may have paid the balance off the next month. 3) Check credit limits. If your lender is slower at reporting monthly transactions, this can have a significant impact on how other lenders view your file. Ensure everything’s up to date as old bills that have been paid can come back to haunt you. Some financial institutions don’t even report your maximum limits. As such, the credit bureau is left to only use the balance that’s on hand. The problem is, if you consistently charge the same amount each month – say $1,000 to $1,500 – it may appear to the credit-scoring agencies that you’re regularly maxing out your cards. The best bet is to pay your balances down or off before your statement periods close. 4) Keep old cards. Older credit is better credit. If you stop using older credit cards, the issuers may stop updating your accounts. As such, the cards can lose their weight in the credit formula and, therefore, may not be as valuable – even though you have had the cards for a long time. Use these cards periodically and then pay them off. 5) Don’t let mistakes build up. Always dispute any mistakes or situations that may harm your score. If, for instance, a cell phone bill is incorrect and the company will not amend it, you can dispute this by making the credit bureau aware of the situation.

10 Most Commonly Asked

Mortgage Questions

9. How much will I have to pay for closing costs? As a general rule of thumb, it’s recommended that you put aside at least 1.5% of the purchase price (in addition to the down payment) strictly to cover closing costs. There are several items you should budget for when it comes to closing costs. Property Transfer Tax is charged whenever a property is purchased. The tax will vary from jurisdiction to jurisdiction, but I can help with the calculation. GST/HST is only charged on new homes, and does not affect homes priced at less than $400,000. Even homes that exceed the price threshold are only taxed on the portion that exceeds $400,000. Certain conditions may apply. Please contact you lawyer/notary for more detailed information. Your lawyer/notary will charge you a fee for drawing up the mortgage and conveyance of title. The amount of the fee will depend on the individual that you use. The typical cost is $900. If you’re purchasing a single-family home, you’ll need to give your lender a survey certificate showing where the property sits within the property lines. Some exceptions are made, however, on low loan-to-value deals and acreage properties. A survey will cost approximately $300-$350, but the lender will often accept a copy of an existing survey. Other costs include such things as an appraisal fee (approximately $200), title insurance and a home inspection (approximately $350).

10. How much will my mortgage payments be? Monthly mortgage payments vary based on several factors, including: the size of your mortgage; whether you’re paying mortgage default insurance; your mortgage amortization; your interest rate; and your frequency of making mortgage payments. You can view some useful calculators to find out your specific mortgage payments: www.dominionlending.ca/mortgage-calculators

10 Questions Mortgage Brokers

Should Ask But Often Don’t

1. If I have mortgage default insurance do I also need mortgage life insurance? Yes. Mortgage life insurance is a life insurance policy on a homeowner, which will allow your family or dependents to pay off the mortgage on the home should something tragic happen to you. Mortgage default insurance is something lenders require you to purchase to cover their own assets if you have less than a 20% down payment. Mortgage life insurance is meant to protect the family of a homeowner and not the mortgage lender itself. 2. What steps can I take to maximize my mortgage payments and own my home sooner? There are many ways to pay down your mortgage sooner that could save you thousands of dollars in interest payments throughout the term of your mortgage. Most mortgage products, for instance, include prepayment privileges that enable you to pay up to 20% of the principal (the true value of your mortgage minus the interest payments) per calendar year. This will also help reduce your amortization period (the length of your mortgage). Another way to reduce the time it takes to pay off your mortgage involves changing the way you make your payments by opting for accelerated bi-weekly mortgage payments. Not to be confused with semi-monthly mortgage payments (24 payments per year), accelerated bi-weekly mortgage payments (26 payments per year) will not only pay your mortgage off quicker, but it’s guaranteed to save you a significant amount of money over the term of your mortgage. With accelerated bi-weekly mortgage payments, you’re making one additional monthly payment per year. In addition to increased payment options, most lenders offer the opportunity to make lump-sum payments on your mortgage (as much as 20% of the original borrowed amount each year). Please note, however, that some lenders will only let you make these lump-sum payments on the anniversary date of your mortgage while others will allow you to spread out the lump-sum payments to the maximum allowable yearly amount. 3. Can I make lump-sum or other prepayments on my mortgage, or will I be penalized? Most lenders enable lump-sum payments and increased mortgage payments to a maximum amount per

year. But, since each lender and product is different, it’s important to check stipulations on prepayments

prior to signing your mortgage papers. Most “no frills” mortgage products offering the lowest rates often

do not allow for prepayments.

10 Questions Mortgage Brokers

Should Ask But Often Don’t

4. How do I ensure my credit score enables me to qualify for the best possible rate? There are several things you can do to ensure your credit remains in good standing. Following are five steps you can follow: 1) Pay down credit cards. The number one way to increase your credit score is to pay down your credit cards so they’re below 70% of your limits. Revolving credit like credit cards seems to have a more significant impact on credit scores than car loans, lines of credit, and so on. 2) Limit the use of credit cards. Racking up a large amount and then paying it off in monthly instalments can hurt your credit score. If there’s a balance at the end of the month, this affects your score – credit formulas don’t take into account the fact that you may have paid the balance off the next month. 3) Check credit limits. If your lender is slower at reporting monthly transactions, this can have a significant impact on how other lenders view your file. Ensure everything’s up to date as old bills that have been paid can come back to haunt you. Some financial institutions don’t even report your maximum limits. As such, the credit bureau is left to only use the balance that’s on hand. The problem is, if you consistently charge the same amount each month – say $1,000 to $1,500 – it may appear to the credit-scoring agencies that you’re regularly maxing out your cards. The best bet is to pay your balances down or off before your statement periods close. 4) Keep old cards. Older credit is better credit. If you stop using older credit cards, the issuers may stop updating your accounts. As such, the cards can lose their weight in the credit formula and, therefore, may not be as valuable – even though you have had the cards for a long time. Use these cards periodically and then pay them off. 5) Don’t let mistakes build up. Always dispute any mistakes or situations that may harm your score. If, for instance, a cell phone bill is incorrect and the company will not amend it, you can dispute this by making the credit bureau aware of the situation. 5. What amortization will work best for me? While the lending industry’s benchmark amortization period is 25 years, and this is the standard that is

used by lenders when discussing mortgage offers, and usually the basis for mortgage calculators and

payment tables, shorter or longer timeframes are available – to a maximum of 30 years. The main reason

to opt for a shorter amortization period is that you’ll become mortgage-free sooner. And since you’re

agreeing to pay off your mortgage in a shorter period of time, the interest you pay over the life of the

mortgage is, therefore, greatly reduced. A shorter amortization also affords you the luxury of building up

equity in your home sooner. Equity is the difference between any outstanding mortgage on your home and

its market value. While it pays to opt for a shorter amortization period, other considerations must be made

before selecting your amortization. Because you’re reducing the actual number of mortgage payments you

make to pay off your mortgage, your regular payments will be higher. So if your income is irregular because

you’re paid commission or if you’re buying a home for the first time and will be carrying a large mortgage,

a shorter amortization period that increases your regular payment amount and ties up your cash flow may

not be the best option for you.

10 Questions Mortgage Brokers

Should Ask But Often Don’t

6. What mortgage term is best for me? Selecting the mortgage term that’s right for you can be a challenging proposition for even the savviest of homebuyers, as terms typically range from six months up to 10 years. The first consideration when comparing various mortgage terms is to understand that a longer term generally means a higher corresponding interest rate. And, a shorter term generally means a lower corresponding interest rate. While this generalization may lead you to believe that a shorter term is always the preferred option, this isn’t always the case. Sometimes there are other factors – either in the financial markets or in your own life – that you’ll also have to take into consideration when selecting the length of your mortgage term. If paying your mortgage each month places you close to the financial edge of your comfort zone, you may want to opt for a longer mortgage term, such as five or 10 years, so that you can ensure that you’ll be able to afford your mortgage payments should interest rates increase. By the end of a five- or 10-year mortgage term, most buyers are in a better financial situation, have a lower outstanding principal balance and, should interest rates have risen throughout the course of your term, you’ll be able to afford higher mortgage payments. 7. Is my mortgage portable? Fixed-rate products usually have a portability option. Lenders often use a “blended” system where your

current mortgage rate stays the same on the mortgage amount ported over to the new property and the

new balance is calculated using the current rate. With variable-rate mortgages, however, porting is usually

not available. This means that when breaking your existing mortgage, a three-month interest penalty will

be charged. This charge may or may not be reimbursed with your new mortgage. While porting typically

ensures no penalty will be charged when you sell your existing property and buy a new one, it’s best to

check with your mortgage broker for specific conditions. Some lenders allow you to port your mortgage,

but your sale and purchase have to happen on the same day, while others offer extended periods.

8. If I want to move before my mortgage term is up, what are my options? The answer to this question often depends on your specific lender and what type of mortgage you have.

While fixed mortgages are often portable, variable are not. Some lenders allow you to port your mortgage,

but your sale and purchase have to happen on the same day, while others offer extended periods. As long

as there’s not too much time between the sale of your existing home and the purchase of the new home,

as a rule of thumb most lenders will allow you to port the mortgage. In other words, you keep your existing

mortgage and add the extra funds you need to buy the new house on top. The interest rate is a blend

between your existing mortgage rate and the current rate at the time you require the extra money.

10 Questions Mortgage Brokers

Should Ask But Often Don’t

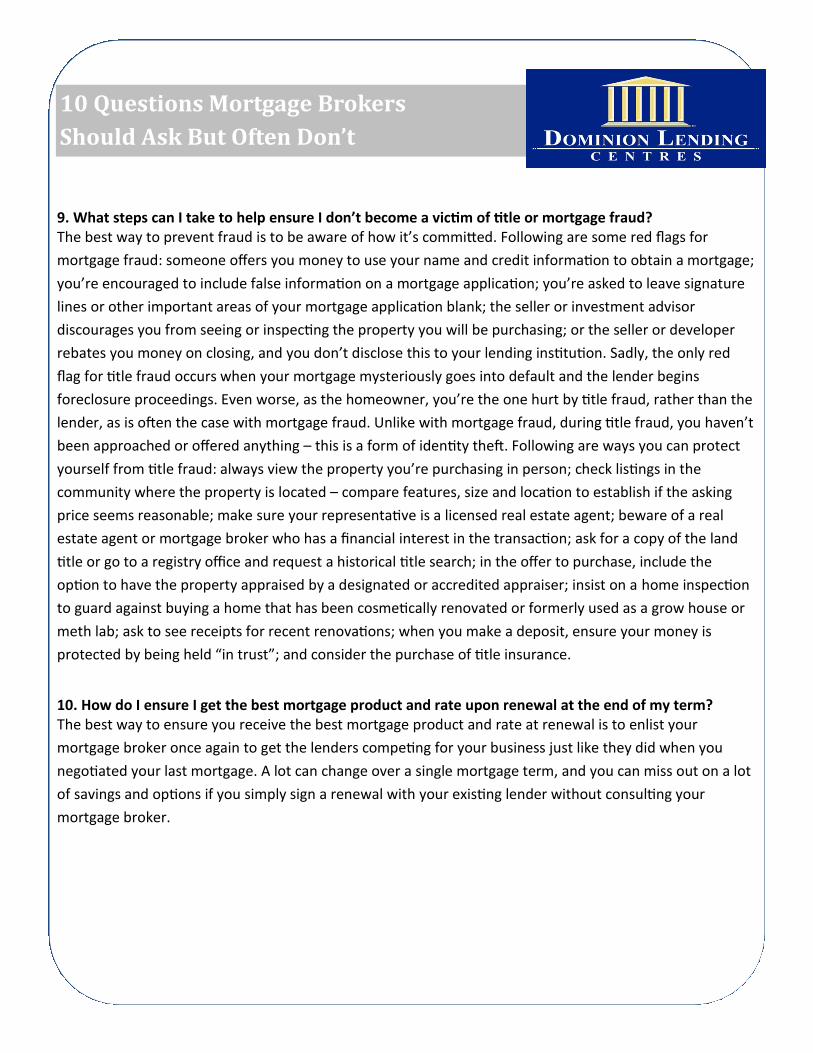

9. What steps can I take to help ensure I don’t become a victim of title or mortgage fraud? The best way to prevent fraud is to be aware of how it’s committed. Following are some red flags for

mortgage fraud: someone offers you money to use your name and credit information to obtain a mortgage;

you’re encouraged to include false information on a mortgage application; you’re asked to leave signature

lines or other important areas of your mortgage application blank; the seller or investment advisor

discourages you from seeing or inspecting the property you will be purchasing; or the seller or developer

rebates you money on closing, and you don’t disclose this to your lending institution. Sadly, the only red

flag for title fraud occurs when your mortgage mysteriously goes into default and the lender begins

foreclosure proceedings. Even worse, as the homeowner, you’re the one hurt by title fraud, rather than the

lender, as is often the case with mortgage fraud. Unlike with mortgage fraud, during title fraud, you haven’t

been approached or offered anything – this is a form of identity theft. Following are ways you can protect

yourself from title fraud: always view the property you’re purchasing in person; check listings in the

community where the property is located – compare features, size and location to establish if the asking

price seems reasonable; make sure your representative is a licensed real estate agent; beware of a real

estate agent or mortgage broker who has a financial interest in the transaction; ask for a copy of the land

title or go to a registry office and request a historical title search; in the offer to purchase, include the

option to have the property appraised by a designated or accredited appraiser; insist on a home inspection

to guard against buying a home that has been cosmetically renovated or formerly used as a grow house or

meth lab; ask to see receipts for recent renovations; when you make a deposit, ensure your money is

protected by being held “in trust”; and consider the purchase of title insurance.

10. How do I ensure I get the best mortgage product and rate upon renewal at the end of my term? The best way to ensure you receive the best mortgage product and rate at renewal is to enlist your

mortgage broker once again to get the lenders competing for your business just like they did when you

negotiated your last mortgage. A lot can change over a single mortgage term, and you can miss out on a lot

of savings and options if you simply sign a renewal with your existing lender without consulting your

mortgage broker.

Tips To Keep In Mind Between Your

Mortgage Approval and Funding Dates

In light of the new market realities and tightening of credit underwriting standards by both lenders and

mortgage default insurers as of late, keep in mind that now – more than ever – it’s important to be careful

what you do between the time your mortgage is approved and when it funds.

A few mortgage lenders and insurers have been doing something lately that they have not done in a long time

– pulling new credit bureaus prior to funding, especially if there is a long period between the time of your

approval and when the mortgage actually funds.

Following are eight tips to keep in mind between your mortgage approval and funding dates:

1. Don’t buy a new car or trade-up to a more expensive lease.

2. Don’t quit your job or change jobs. Even if it’s a better-paying job, you still are likely to be on a

probationary period. If in doubt, call your mortgage professional and they can let you know if this may

jeopardize your approval.

3. Don’t change industries, decide to become self-employed or accept a contract position even if it’s

within the same industry. Delay the start of your new job, self-employment or contract status until after the

funding date of your mortgage.

4. Don’t transfer large sums of money between bank accounts. Lenders get especially skittish about this

one because it looks like you’re borrowing money. Be ready to document cash transactions or money

movements.

5. Don’t forget to pay your bills, even ones that you’re disputing. This can be a real deal-breaker. If the

lender pulls your credit bureau prior to closing and sees a collection or a delinquent account, the best you can

hope for is that they make you pay off the account before they will fund. You don’t want to have to scramble

to pay off a debt at the last minute!

6. Don’t open new credit cards. Again, just wait until after your funding date.

7. Don’t accept a cash gift without properly documenting it – even if this is from proceeds of a wedding.

If you have a bunch of cash to deposit before your funding date, give your mortgage professional a call

before you deposit it.

Don’t buy furniture on the “Do not pay for XX years plan” until after funding. Even though you don’t

have to pay now, it will still be reported on your credit bureau, and will become an issue – especially if your

approval was tight to begin with.

While you may not risk losing your mortgage approval because you have broken one of these rules, it’s

always best to talk to your mortgage professional before doing any of the above just to make sure!