Embed Size (px)

Citation preview

Tuesday

April 5, 2016

www.bloombergbriefs.com

Trade Balance; Non-Manufacturing ISM; JoltsBEN BARIS AND JAMES BATTY, BLOOMBERG BRIEF EDITORS

WHAT TO WATCH: The is to widen to a $46.2 billion U.S. trade balance forecastdeficit in February, up from $45.7 billion in January, 8:30 a.m. The ISM non-

is expected to rise to 54.2 in March from 53.4 in February, which manufacturing indexwould mark the first improvement in U.S. services industry growth in five months. 10 a.m. The print may show a seasonally adjusted 5.49 million new job openings in JOLTSFebruary, 10 a.m.

ECONOMICS: Chicago Fed President said Charles Evans it will be appropriate for the U.S. central bank to make two more rate hikes this year and “follow a very gradual

at the Credit Suisse Asian Investment Conference in path of rate increases thereafter” Hong Kong last night. Bank of Canada Senior Deputy Governor Carolyn Wilkinsspeaks to the Vancouver Board of Trade at 3 p.m.

GOVERNMENT: Wisconsin holds Republican and Democratic presidential primaries. Bloomberg hosts the in Buenos Aires, with scheduled Argentina Summit speakers including Finance Minister and Central Bank President Alfonso Prat-Gay

, beginning at 7 a.m.Federico Sturzenegger

MARKETS: Global stocks fell with emerging-market currencies.

(All times local for New York.)

Click to view a live version of this chart on the Bloomberg terminal.here

Adam Posen@AdamPosen

Good point that many large @anatadmatiBank HCs are largely nonbanks and can acquire nonbanks competitors with cheap funding #EndingTBTFDetails

COMMENTARY IN THIS ISSUE

Outside of non-farm payrolls, a decline in average hourly earnings, a slight uptick in the unemployment rate and a drop in hiring plans all contributed to another lackluster picture of : employmentBloomberg Intelligence Economists.

Wage growth is more robust by some measures than commonly acknowledged due to changes in the composition of the workforce: Jana Randow.

Bayerische Landesbank was named asthe top of major currencies forecaster again. See who else was among the most accurate for FX calls in the first quarter of 2016.

NUMBER OF THE DAY

—$24 trillion The amount of the that could be world’s financial assets

hit by rising temperatures and extreme weather events, according to one of the first studies using an economic model to calculate the cost of climate change. Read more on the Bloomberg .terminal

QUOTE OF THE DAY

"We calculate that this decline [in market-based measures of inflation expectations] is not likely to be short-lived, but should be resolved over the medium- to long-term."

— Jens Christensen and Jose Lopez of the San

Francisco Fed, in an Economic Letter to posted

the bank's website

TWEET OF THE DAY

WAGE GROWTH JANA RANDOW, BLOOMBERG NEWS

Treasuries Volatility Plunges as Rate Outlooks Converge

Volatility in the $13.3 trillion market for U.S. Treasuries is plunging, approaching the lowest since 2014, as traders wager yields will remain in a narrow range amid broad-based demand for U.S. debt and assurances that policy makers will raise interest rates gradually. Federal Reserve Chair Janet Yellen’s latest commitment to “proceed cautiously’’ with tightening U.S. monetary policy pushed traders to pare bets on when and how often the central bank will boost rates this year. A Bank of America Merrill Lynch index measuring price swings bond traders expect over the next year declined for a fourth day, touching the lowest this year.

— Eliza Ronalds-Hannon, Bloomberg News

April 5, 2016 Bloomberg Brief Economics 2

WAGE GROWTH JANA RANDOW, BLOOMBERG NEWS

Wages Are Imperfect Window Into Health of U.S. Labor MarketThe true strength of the American labor

market may be disguised.Wage growth — described as slow and

unconvincing by Federal Reserve officials plotting their path to higher interest rates — is more robust by some measures than commonly acknowledged due to changes in the composition of the workforce. With unemployment close to the lowest in eight years, accelerating pay gains would force Fed Chair Janet Yellen to step up her gradual approach to lifting borrowing costs if inflation starts to rise.

Policy makers have identified wages as one of the most disappointing features in a labor-market recovery that has seen the biggest back-to-back annual payroll gains in 16 years, the jobless rate cut in half and a recent surge in the labor force. The data are being distorted by the retirement of highly paid baby boomers just as lower-wage workers re-enter the workforce after being sidelined during the last recession, according to Fed analysts.

“The signal is muddied so we shouldn’t use it as an indicator that the labor market is weaker than we observe when we look at the unemployment rate,” Mary Daly, associate director of research at the San Francisco Fed, said in an interview. “Absent the changes in labor-force composition, we would have seen wage growth come up more consistently with the decline of unemployment.”

Measures of the state of the labor market are abundant and range from job openings to hiring, layoffs to voluntary quits, and payrolls to various forms of underemployment and joblessness.

Yellen’s dashboard contains nine indicators, not including the vast array of wage-growth gauges such as unit-labor costs, the employment-cost index, compensation per hour and average hourly earnings. The latter, which rose 2.3 percent in March from a year earlier, is probably the best yardstick for inflation because it tracks employers’ total wage bill — but also one that masks underlying trends that Daly has zeroed in on.

In a recent research paper with Bart Hobijn, an economics professor at Arizona State University, and Benjamin Pyle, a research associate at the San Francisco Fed, she argued that the disproportionate firing of low-wage

Read the full analysis with additional live charts on the Bloomberg terminal . here

workers during the 2008-2009 recession propped up aggregate wage measures at the time. Bringing those workers back into the labor force is now a drag on pay growth. It’s amplified by the retirement of those born during the baby boom between 1946 and 1964, who make up more than 20 percent of the American population.

Gauges focusing on those continuously employed may thus better capture pay dynamics. The Atlanta Fed’s wage-growth tracker is one such measure. In February, the last month for which data are available, it signaled gains of 3.2 percent, compared with an average of 2.8 percent over the past decade.

“We almost look at it as another sign of relative tightness in the labor market,” John Robertson, a research economist and senior policy adviser at the Atlanta Fed, said in an interview. “It doesn’t allow us however to connect that wage growth to inflation because for a business it’s really about the total wage bill at the end of the month.”

Yellen has acknowledged anecdotal evidence and said that “quite a number of reports” show wages are picking up, but the aggregate data don’t yet reflect it.

“I do see broad-based improvement in the labor market, and I’m somewhat surprised that we’re not seeing more of a pickup in wage growth,” she said March 16. “That suggests to me that there is

continued slack in the labor market.”That assessment is crucial for

monetary policy. Typically, wages pick up when the jobless rate drops significantly as employers boost pay to fill vacancies and retain staff. That, in turn, would fuel inflation as they raise prices to offset the higher costs, increasing the need for higher interest rates.

Wage growth, by any standard, has in the most recent recovery been below the 3.5 percent to 4 percent range historically observed. With the Fed’s preferred inflation gauge currently running at half the central bank’s 2 percent target rate, and last year’s increase in productivity a mere quarter of the average over the past two decades, it could be that current pay gains actually aren’t out of line with those economic fundamentals.

Even though inflation and productivity are expected to pick up, Daly predicts wages won’t resume their past path of expansion for another two to four years as lower-skilled workers are integrated into the labor force. With those employees likely to be less productive than those who retire, the labor market may be getting tighter than comparatively tepid wage growth would suggest.

“We don’t have any perfect measure of wage growth,” Daly said. “It’s time for people to turn their attention to it and dig in. We’re just starting to discuss these issues.”

LABOR RICHARD YAMARONE, CARL RICCADONNA AND YELENA SHULYATYEVA, BLOOMBERG INTELLIGENCE ECONOMISTS

Alternative Wage Gauges May Better Capture Pay Dynamics

April 5, 2016 Bloomberg Brief Economics 3

LABOR RICHARD YAMARONE, CARL RICCADONNA AND YELENA SHULYATYEVA, BLOOMBERG INTELLIGENCE ECONOMISTS

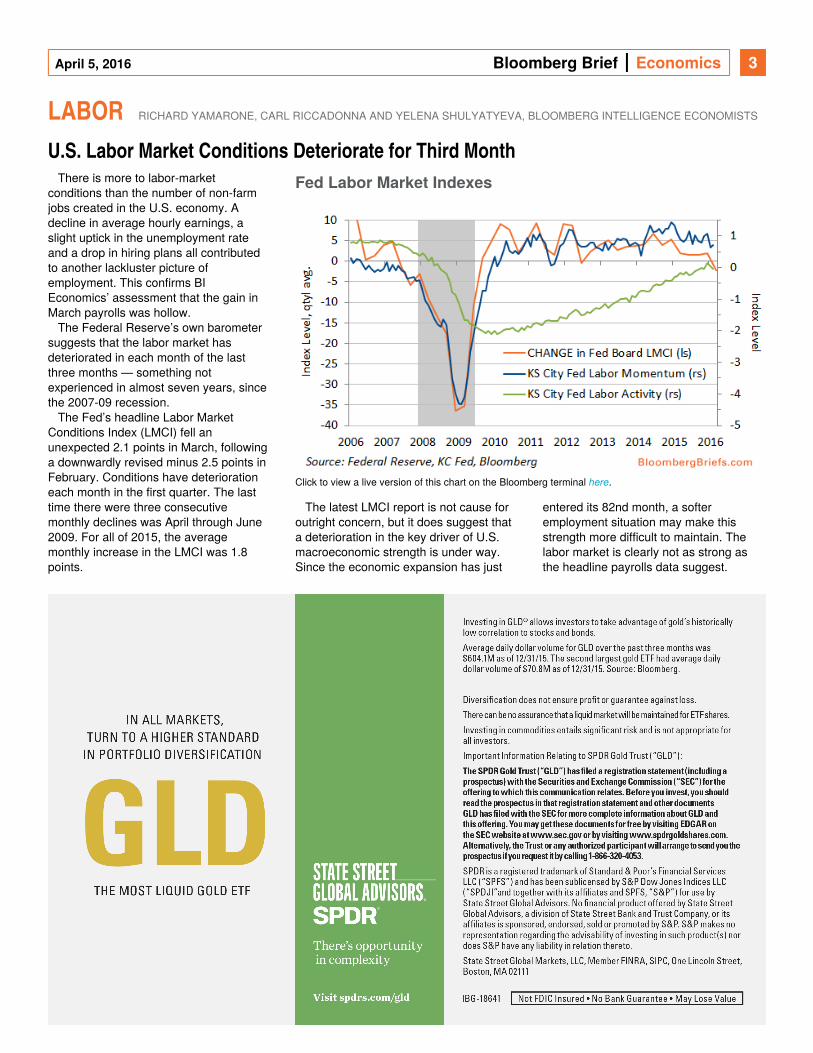

U.S. Labor Market Conditions Deteriorate for Third MonthThere is more to labor-market

conditions than the number of non-farm jobs created in the U.S. economy. A decline in average hourly earnings, a slight uptick in the unemployment rate and a drop in hiring plans all contributed to another lackluster picture of employment. This confirms BI Economics’ assessment that the gain in March payrolls was hollow.

The Federal Reserve’s own barometer suggests that the labor market has deteriorated in each month of the last three months — something not experienced in almost seven years, since the 2007-09 recession.

The Fed’s headline Labor Market Conditions Index (LMCI) fell an unexpected 2.1 points in March, following a downwardly revised minus 2.5 points in February. Conditions have deterioration each month in the first quarter. The last time there were three consecutive monthly declines was April through June 2009. For all of 2015, the average monthly increase in the LMCI was 1.8 points.

Click to view a live version of this chart on the Bloomberg terminal . here

The latest LMCI report is not cause for outright concern, but it does suggest that a deterioration in the key driver of U.S. macroeconomic strength is under way. Since the economic expansion has just

entered its 82nd month, a softer employment situation may make this strength more difficult to maintain. The labor market is clearly not as strong as the headline payrolls data suggest.

TOP FORECASTERS WEI LU, BLOOMBERG NEWS DATA

Fed Labor Market Indexes

April 5, 2016 Bloomberg Brief Economics 4

TOP FORECASTERS WEI LU, BLOOMBERG NEWS DATA

Bloomberg FX Forecast Accuracy Ranking — Major Currencies, 1Q 2016Bayerische Landesbank was the top foreign-exchange forecaster for major currencies in the first quarter of 2016, according to data

compiled by Bloomberg. The Munich-based bank took the top spot for the second straight quarter. See the full rankings on the terminal , as well as the top currency forecasters for , and .here Asia ex-Japan EMEA Latin America

Overall (Major Currencies)

Rank Firm Score

1 Bayerische Landesbank 61.88

2 Bank Julius Baer 60.03

3 National Bank Financial 58.91

4 Wells Fargo 57.02

5 BMO Capital Markets 55.84

EURUSD

Rank Firm Score

1 Aletti Gestielle SGR 75.38

2 Mizuho Bank 71.58

3 Bank Julius Baer 69.51

4 CIB Bank 67.55

5 RHB OSK Securities 66.25

GBPUSD

Rank Firm Score

1 Validus Risk Management 72.30

2 National Bank Financial 71.55

3 Societe Generale 69.64

4 Ebury 67.93

5 HSBC Holdings 67.29

USDCNY

Rank Firm Score

1 ABN Amro Bank N.V. 67.41

2 Landesbank Baden-Wuerttemberg 67.20

3 Jyske Bank 62.39

4 Cinkciarz.pl 61.07

5 HSBC Holdings 60.77

USDJPY

Rank Firm Score

1 Bank Julius Baer 78.12

2 Sumitomo Mitsui Trust Bank 76.87

3 Australia & New Zealand Banking 72.04

4 Rand Merchant Bank 71.22

5 Day By Day 68.46

USDCAD

Rank Firm Score

1 Day By Day 80.09

2 Mizuho Bank 74.09

3 Klarity FX 71.02

4 TMS Brokers 66.86

5 RBC Capital Markets 64.18

AUDUSD

Rank Firm Score

1 UniCredit 71.36

2 Maybank Singapore 67.77

3 Lloyds Bank Commercial Banking 64.30

4 Ebury 62.34

5 Silicon Valley 60.41

EURGBP

Rank Firm Score

1 Banco Santander 72.87

2 Prestige Economics LLC 68.91

3 Bank Julius Baer 67.57

4 Validus Risk Management 65.67

5 Casa De Bolsa Ve Por Mas SA de CV 65.64

EURCHF

Rank Firm Score

1 Landesbank Baden-Wuerttemberg 81.18

2 TMS Brokers 79.92

3 Bayerische Landesbank 78.06

4 Lloyds Bank Commercial Banking 77.71

5 DNB 73.84

USDCHF

Rank Firm Score

1 Maybank Singapore 75.18

2 Silicon Valley 74.40

3 TD Securities 69.12

4 Rand Merchant Bank 68.32

5Canadian Imperial Bank ofCommerce

67.75

Source: Bloomberg

NZDUSD

Rank Firm Score

1 UniCredit 83.84

2 HSBC Holdings 76.34

3 Swissquote Bank 63.15

4 Standard Chartered 62.25

5 Bank of America Merrill Lynch 60.93

EUDJPY

Rank Firm Score

1 Investec 76.19

2 Bayerische Landesbank 76.03

3 Alpha Bank 75.10

4 National Bank Financial 73.88

5 Societe Generale 73.06

Methodology: Q1’2016 FX forecasters are ranked based on three criteria: margin of error, timing (for identical forecasts, earlier ones received more credit) and

directional accuracy (whether the movements with the currency’s overall direction). The ranking above, which was based on Bloomberg’s foreign exchange

forecasts (FXFC), was for the forecasters provided forecasts for Q1’2016 in at least three of the four preceding quarters but no later than one month prior to March,

31, 2016. Scores were calculated each quarter for the three criteria, which were weighted 60 percent, 30 percent and 10 percent, respectively. The final score for

each currency pair was the time-weighted average of the four quarterly scores. The Best Overall forecasters were identified by averaging the individual scores for

each firm on all 13 currency pairs and all four quarters. Forecasters had to be ranked in at least eight of the 13 pairs to qualify for the overall ranking. 63 firms

qualified. The ranking tables above display the top five forecasters for 11 currency pairs; the full tables for all 13 currency pairs, which can be accessed , rank here

the top 20 percent of forecasters who were eligible to a maximum of 10 names.

DATA & EVENTS

April 5, 2016 Bloomberg Brief Economics 5

DATA & EVENTS

TIME COUNTRY EVENT SURVEY PRIOR

8:30 U.S. Trade Balance -$46.2b -$45.7b

8:30 Canada Int'l Merchandise Trade -0.90b -0.66b

9:00 Brazil Markit Brazil PMI Composite — 39

9:00 Brazil Markit Brazil PMI Services — 36.9

9:00 Mexico Gross Fixed Investment 1.00% 1.10%

9:45 U.S. Markit US Services PMI 51.2 51

9:45 U.S. Markit US Composite PMI — 51.1

10:00 U.S. ISM Non-Manf. Composite 54.2 53.4

10:00 U.S. IBD/TIPP Economic Optimism 47 46.8

10:00 U.S. JOLTS Job Openings 5490 5541

11:00 World Aggregate JPMorgan Global Services PMI — 50.7

11:00 World Aggregate JPMorgan Global Composite PMI — 50.6

21:45 China Caixin China PMI Services — 51.2

21:45 China Caixin China PMI Composite — 49.4Source: Bloomberg. Surveys updated at 5:25 a.m. New York.

Click to view a live version of this chart on the Bloomberg terminal.here

CALENDAR

Click on the to see the full range of economists' forecasts on the terminal. highlighted releases

OVERNIGHT

The euro-area economy grew slower than initially anticipated at the end of the first quarter, according to Markit

, which revised down a key Economicsindex of activity. Markit said its composite

rose to Purchasing Managers Index53.1 in March from 53 in February. While that’s above the 50 level that divides expansion from contraction, it’s below the initial reading of 53.7 published March 22.

German factory orders unexpectedly fell in February in a sign that a global trade slowdown is weighing on Europe’s largest economy. Orders, adjusted for seasonal swings and inflation, dropped 1.2 percent from the prior month, when they rose a revised 0.5 percent, data from the in Berlin Economy Ministryshowed today.

Global uncertainty and the upcoming referendum are European Union

weighing on the economy and U.K.growth will remain subdued this quarter, according to . Markit Economics In a report published today, Markit said its monthly surveys indicate expansion slowed to 0.4 percent in the first quarter from 0.6 percent in the last three months of 2015. While its services Purchasing

rose in March from a Managers Index three-year low, it remains below its long-run average.

Japanese Finance Minister Taro Asobegan outlining how the government will bring forward spending in the current budget to the first half of the year as the Abe administration seeks to bolster an economy that’s struggling to recover from a slump at the end of 2015. "We aim to sign contracts on about 80 percent of the 12.1 trillion yen ($110 billion) in public works in the budget in the first half of the fiscal year," Aso said today. The government also urged ministries to spend the money from last year’s extra budget as quickly as possible, Aso said.

Europe

Asia

MARKET INDICATORS

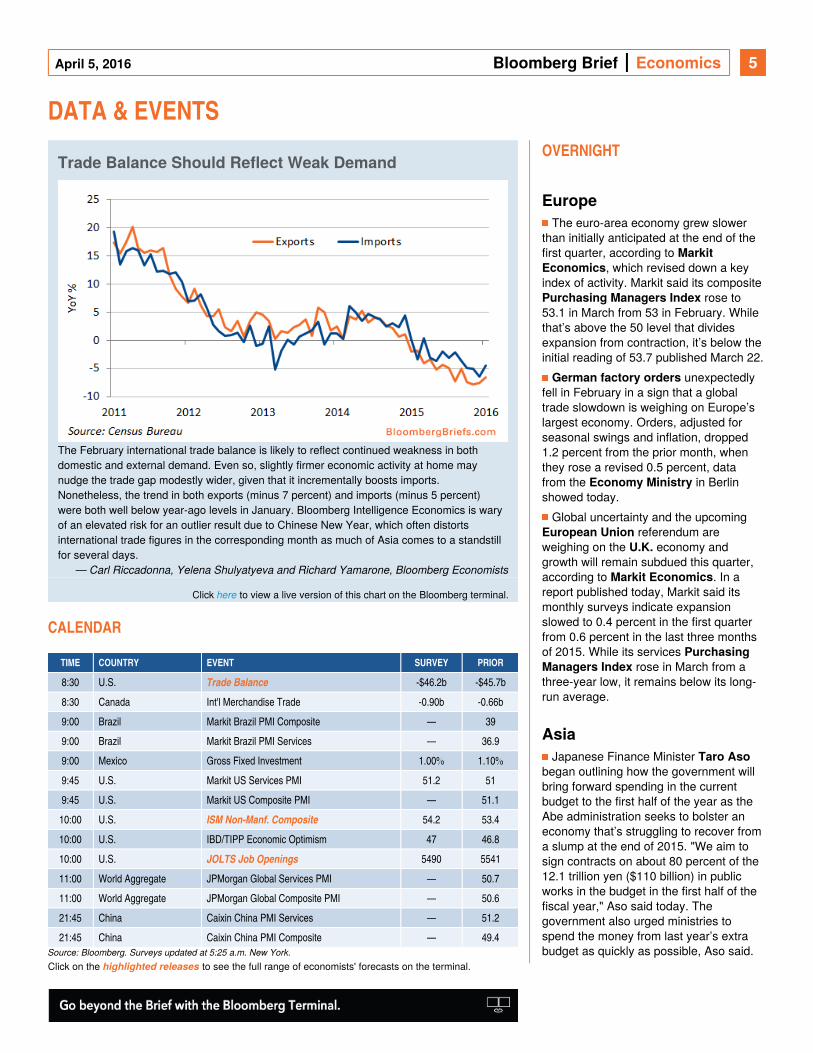

Trade Balance Should Reflect Weak Demand

The February international trade balance is likely to reflect continued weakness in both domestic and external demand. Even so, slightly firmer economic activity at home may nudge the trade gap modestly wider, given that it incrementally boosts imports. Nonetheless, the trend in both exports (minus 7 percent) and imports (minus 5 percent) were both well below year-ago levels in January. Bloomberg Intelligence Economics is wary of an elevated risk for an outlier result due to Chinese New Year, which often distorts international trade figures in the corresponding month as much of Asia comes to a standstill for several days.

— Carl Riccadonna, Yelena Shulyatyeva and Richard Yamarone, Bloomberg Economists

April 5, 2016 Bloomberg Brief Economics 6

MARKET INDICATORS

SURVEILLANCE

Source: Bloomberg. Updated 5:30 a.m. New York time.

April 5, 2016 Bloomberg Brief Economics 7

Bloomberg Brief: Economics

SURVEILLANCE

Carl Weinberg, founder and chief economist of

High Frequency Economics, speaks with

Bloomberg's Tom Keene and Caroline Hyde

about domestic growth in the first quarter,

inflation pressures and central banker policy

options.

Q: As you begin the second quarter, what are you focused on?A: The world economy I think is decaying. And I think that we want to look for those trends to see whether they're going to continue. I think it's all related to commodity prices and if commodity prices stay where they are, we'll continue to see headwinds and that of course has a big impact on Fed policy. [Our chief U.S. economist] Jim O'Sullivan is writing about how the Fed is increasingly concerned about what's going on abroad.

Q: Atlanta Fed GDP now is a horrific number, under 1 percent for 1Q in the U.S. Is that a one off or do we extrapolate that out into the rest of the year?A: Jim is looking for generally good economic growth across the country although there are going to be pockets of trouble. You know it's interesting that you mentioned that because Jim also cites higher CPI figures and wage figures coming out of the Atlanta region in his notes on the United States economy this morning. Jim overall is looking for the

unemployment rate to continue to fall and more importantly for employment gains to persist at a high rate and he thinks that's going to keep the Fed going despite potential regional issues.

Q: Do you have concerns about inflation risks and the lack thereof? Or indeed do you see inflation starting to build?A: Jim did a real micro-detailed breakdown of the sources contributing to the CPI increase. And right now it's concentrated in health care. But 2/3 of it comes from non-health care, 2/3 of the increase of core CPI. So Jim has an eye on the fact that there are inflation pressures starting to appear and the theory of course tells us that we really don't see much inflation pressure until we get to that NAIRU level and we're just creeping up on that right now. So we're expecting to see continued acceleration of prices as we move forward. It's going to be very gentle but it's going to be very real. And it's going to have the attention of the Fed to act soon so that, as Stanley Fischer warns, we don't have to have bigger, more aggressive action later that could hurt the economy.

Q: When I look at the world economy, it is about central bankers adapting and adjusting. Are they theoretically exhausted?A: I think monetary policy is reaching the

limits of what it can do. And central bankers are very willing to accept that point. You know, that they've pushed their interest rates as low as they can go. Some of them have pushed quantitative easing. And while they might insist that they might have more easing they can do, the reality is that they're limited. We're hearing now calls coming for fiscal policy responses. That's a hard thing to do in the current global environment. But I think that that has to be the next move if things continue to deteriorate.

Q: Can there be a trade policy response? We're flat on our back like we were in the 1980s on global exports. What's a policy maker to do?A: Policy makers should first of all recognize and admit that world trade is totally in the garbage can. The drop in world trade that we're currently seeing — and the January figure I believe was about 12 percent lower year over year — is the biggest decline in world trade we've seen in the post-war period other than the 2008 shock. It's a drop of historic consequence and its roots are, I believe, in the commodity price decline. And I think that this is what policy makers are missing right now. That this drop in commodity prices is not a windfall for the world economy, it is instead a profound event that decreases world GDP and world income and provides a shock of potentially historic consequences.

This interview has been edited and condensed.

Bloomberg Brief Managing Editor

Jennifer Rossa

Economics Editors

Ben Baris

James Crombie

Global Director Economic

Research & Chief Economist

Michael McDonough

Chief U.S. Economist

Carl Riccadonna

U.S. Economists

Richard Yamarone

Yelena Shulyatyeva

Reprints & Permissions

Lori Husted

+1-717-505-9701 x2204

Marketing & Partnership Director

Johnna Ayres

+1-212-617-1833

Advertising

Christopher Konowitz

+1-212-617-4694

Economics Terminal Sales

Matthew Traum

+1-212-617-4671

Interested in learning more about

the Bloomberg terminal? Request a

free demo .here

© 2016 Bloomberg LP.

All rights reserved. This newsletter

and its contents may not be

forwarded or redistributed without

the prior consent of Bloomberg.

Please contact our reprints group

listed left for more information.