Embed Size (px)

Citation preview

WABERER’S INTERNATIONAL Nyrt. | October 2017

Waberer’s Investor Presentation

This presentation may contain forward-looking statements. Statements that are not historical facts, including statements

about our beliefs and expectations, are forward-looking statements. These statements are based on current plans,

estimates and projections, and therefore should not have undue reliance placed upon them. Forward-looking statements

speak only as of the date they are made, and we undertake no obligation to update publicly any of them in light of new

information or future events.

Forward-looking statements involve inherent risks and uncertainties. We caution you that a number of important factors

could cause actual results to differ materially from those contained in any forward-looking statement. Such factors are

described in, among other things, the prospectus dated 15 June 2017, which was approved for publication by the National

Bank of Hungary in its resolution No. H-KE-III-426/2017, dated 16 June 2017, and available on our website for investors at

http://www.waberers.com/en/investors.

Forward-looking statements

| 2

Agenda

| Waberer’s Highlights

| A Compelling Investment Proposition – Delivering Growth

| The European Leader in FTL Transportation

| Divisional Overview: International and Regional

| Consistent Top Line Growth with Stable Profit Generation

| Capital Market Overview

| Investment Case

| Appendix

| 3

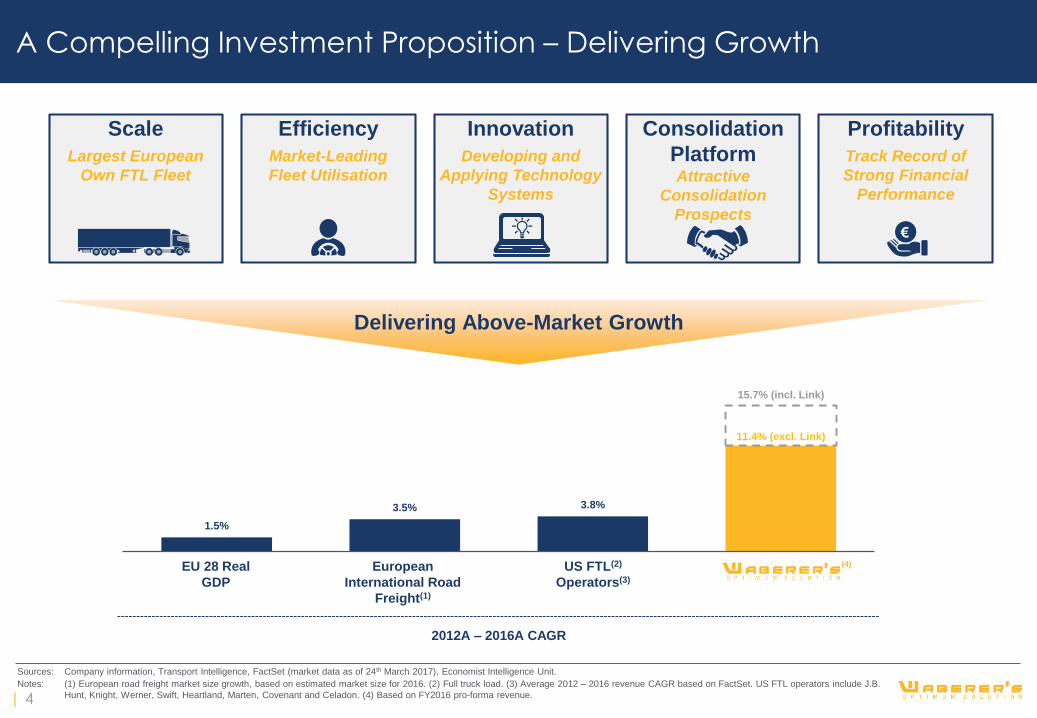

11.4% (excl. Link)

1.5%

3.5% 3.8%

15.7% (incl. Link)

A Compelling Investment Proposition – Delivering Growth

Sources: Company information, Transport Intelligence, FactSet (market data as of 24th March 2017), Economist Intelligence Unit.

Notes: (1) European road freight market size growth, based on estimated market size for 2016. (2) Full truck load. (3) Average 2012 – 2016 revenue CAGR based on FactSet. US FTL operators include J.B.

Hunt, Knight, Werner, Swift, Heartland, Marten, Covenant and Celadon. (4) Based on FY2016 pro-forma revenue.

Delivering Above-Market Growth

2012A – 2016A CAGR

European

International Road

Freight(1)

US FTL(2)

Operators(3)

(4)EU 28 Real

GDP

Scale

Largest European

Own FTL Fleet

Efficiency

Market-Leading

Fleet Utilisation

Profitability

Track Record of

Strong Financial

Performance

€

Consolidation

PlatformAttractive

Consolidation

Prospects

Innovation

Developing and

Applying Technology

Systems

| 4

2016A2000A

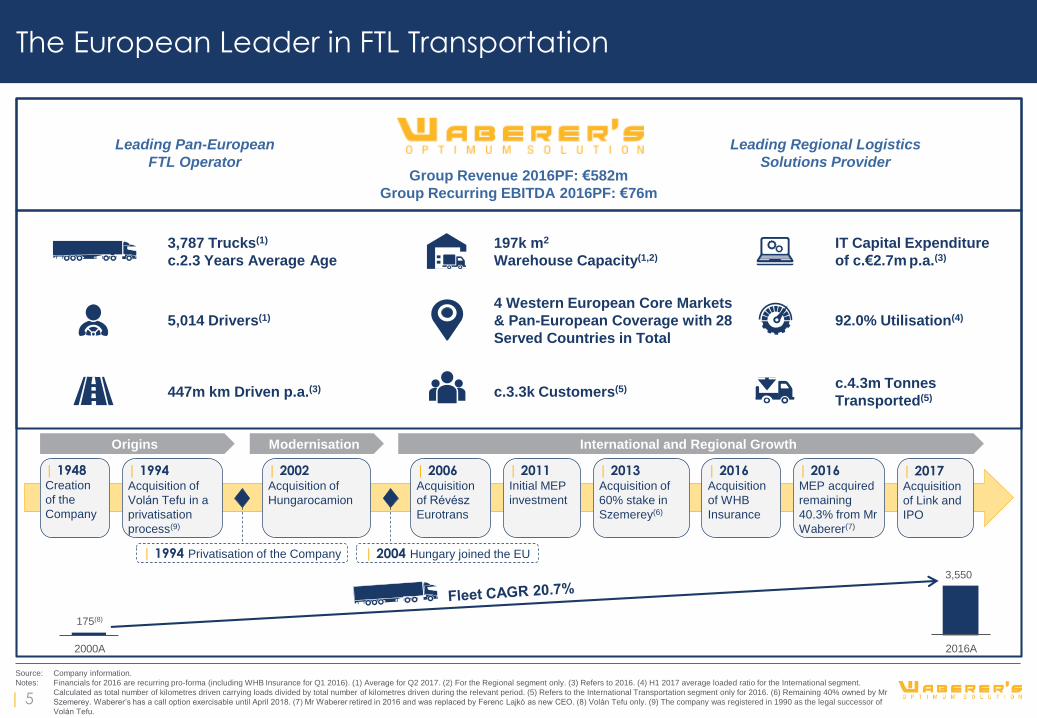

The European Leader in FTL Transportation

Leading Pan-European

FTL Operator

Leading Regional Logistics

Solutions Provider

175(8)

3,550

3,787 Trucks(1)

c.2.3 Years Average Age

5,014 Drivers(1)

447m km Driven p.a.(3)

197k m2

Warehouse Capacity(1,2)

4 Western European Core Markets

& Pan-European Coverage with 28

Served Countries in Total

c.3.3k Customers(5)

IT Capital Expenditure

of c.€2.7m p.a.(3)

92.0% Utilisation(4)

c.4.3m Tonnes

Transported(5)

Group Revenue 2016PF: €582m

Group Recurring EBITDA 2016PF: €76m

Source: Company information.

Notes: Financials for 2016 are recurring pro-forma (including WHB Insurance for Q1 2016). (1) Average for Q2 2017. (2) For the Regional segment only. (3) Refers to 2016. (4) H1 2017 average loaded ratio for the International segment.

Calculated as total number of kilometres driven carrying loads divided by total number of kilometres driven during the relevant period. (5) Refers to the International Transportation segment only for 2016. (6) Remaining 40% owned by Mr

Szemerey. Waberer’s has a call option exercisable until April 2018. (7) Mr Waberer retired in 2016 and was replaced by Ferenc Lajkó as new CEO. (8) Volán Tefu only. (9) The company was registered in 1990 as the legal successor of

Volán Tefu.

| 1948Creation

of the

Company

| 2011Initial MEP

investment

| 2013Acquisition of

60% stake in

Szemerey(6)

| 2016Acquisition

of WHB

Insurance

| 2016MEP acquired

remaining

40.3% from Mr

Waberer(7)

| 1994Acquisition of

Volán Tefu in a

privatisation

process(9)

| 2002Acquisition of

Hungarocamion

| 2006Acquisition

of Révész

Eurotrans

| 1994 Privatisation of the Company | 2004 Hungary joined the EU

Origins Modernisation International and Regional Growth

| 2017Acquisition

of Link and

IPO

| 5

Divisional Overview: International and Regional

International Regional

|Overview(1)

#1 own-fleet player in European FTL with

3,123(2) own trucks

Pan-European network and capacity

availability

Benchmark service offering at a competitive

price point

Fleet utilisation of 92.0%(3) as measured by

loaded ratio

|Overview(1)

#1 in road transport and logistics services in Hungary

Large dedicated domestic fleet of 844 own trucks(2)

and warehousing capacity of 197k m² (2) (dry and

refrigerated)

Full range of logistics capabilities across the

value chain

Regional transportation comprises FTL

transportation, LTL(4) distribution, container

transportation as well as warehousing

17%

17%

76%

77%

Revenue Split(5)

Group Revenue: €582m Group EBITDA: €76m (Margin: 13.1%)

Other

|Overview(1)

Comprising revenues and profits from third party

insurance

Acquisition of insurance business has internalised

insurance services, reducing exposure to further

premium increases

7%

6%

Revenue

€41m

EBITDA

€5m

Margin

11.9%

Own Fleet 80.5%

Revenue

€97m

EBITDA

€13m

Margin

13.4%

Revenue

€443m

EBITDA

€58m

Margin

13.2%

Freight Forwarding 19.5%

Source: Company information.

Notes: Financials are FY2016 recurring pro-forma (including WHB Insurance for Q1 2016) figures. (1) % contribution represents 2016 Revenue and EBITDA. (2) Q2 2017 average. (3) H1 2017 average.

(4) Less than truckload. (5) Freight forwarding also includes groupage and other revenue. | 6

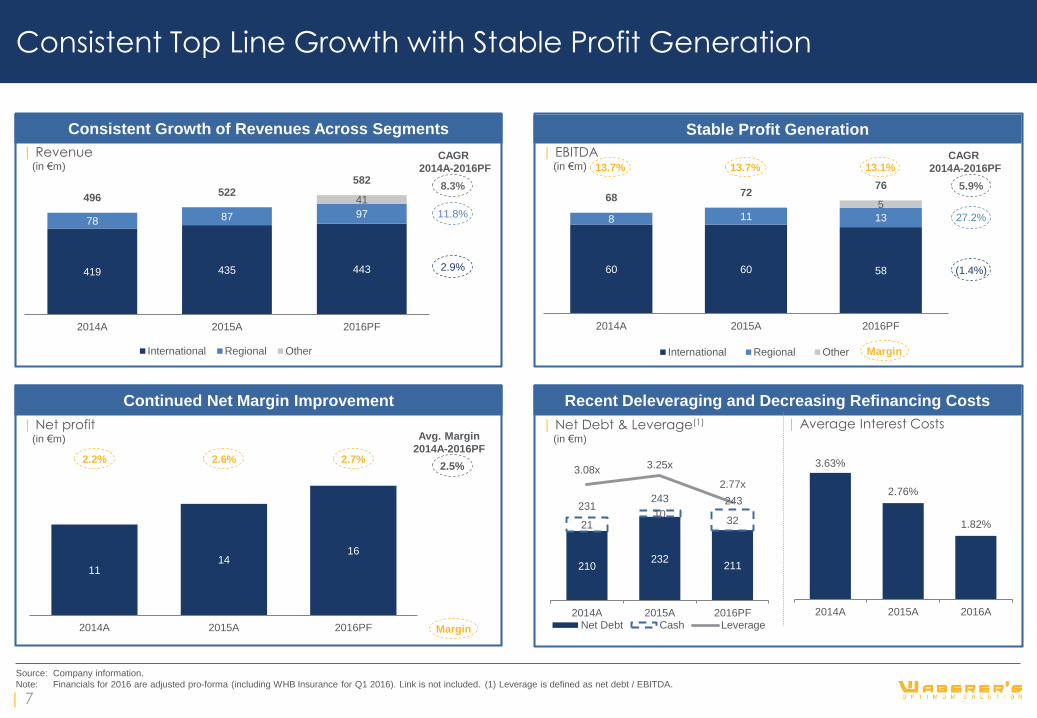

11 14

16

2014A 2015A 2016PF

60 60 58

8 11 13

568 72

76

2014A 2015A 2016PF

International Regional Other

Consistent Top Line Growth with Stable Profit Generation

Source: Company information.

Note: Financials for 2016 are adjusted pro-forma (including WHB Insurance for Q1 2016). Link is not included. (1) Leverage is defined as net debt / EBITDA.

Stable Profit Generation

Recent Deleveraging and Decreasing Refinancing Costs

Consistent Growth of Revenues Across Segments

Continued Net Margin Improvement

| EBITDA(in €m)

| Net profit(in €m)

| Revenue(in €m)

| Net Debt & Leverage(1)

(in €m)

CAGR

2014A-2016PF

2.9%

11.8%

8.3%

(1.4%)

27.2%

5.9%

13.7% 13.7% 13.1%CAGR

2014A-2016PF

2.2% 2.6% 2.7%2.5%

Avg. Margin

2014A-2016PF

419 435 443

78 87 97

41496522

582

2014A 2015A 2016PF

International Regional Other Margin

Margin

| 7

210232

211

2110

32

231243 243

3.08x3.25x

2.77x

2014A 2015A 2016PFNet Debt Cash Leverage

3.63%

2.76%

1.82%

2014A 2015A 2016A

| Average Interest Costs

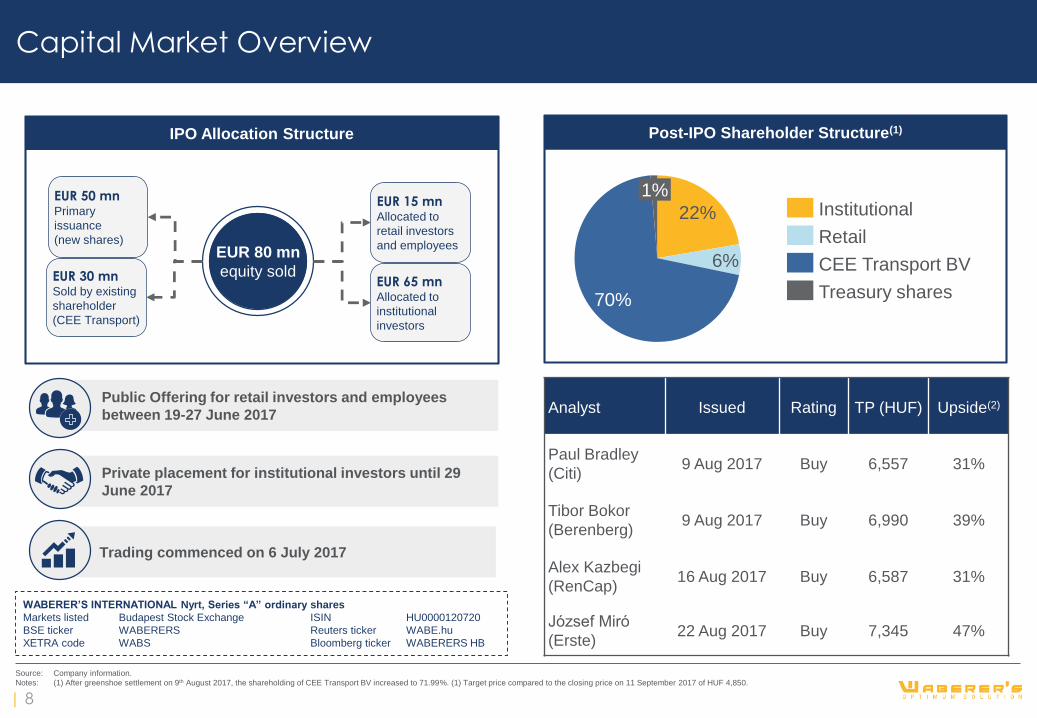

Trading commenced on 6 July 2017

Private placement for institutional investors until 29

June 2017

Public Offering for retail investors and employees

between 19-27 June 2017

Capital Market Overview

| 8

1%

70%

6%

22%

CEE Transport BV

Treasury shares

Retail

Institutional

Post-IPO Shareholder Structure(1)

Source: Company information.

Notes: (1) After greenshoe settlement on 9th August 2017, the shareholding of CEE Transport BV increased to 71.99%. (1) Target price compared to the closing price on 11 September 2017 of HUF 4,850.

IPO Allocation Structure

EUR 80 mn

equity soldEUR 30 mnSold by existing

shareholder

(CEE Transport)

EUR 50 mnPrimary

issuance

(new shares)

EUR 65 mnAllocated to

institutional

investors

EUR 15 mnAllocated to

retail investors

and employees

WABERER’S INTERNATIONAL Nyrt, Series “A” ordinary shares

Markets listed Budapest Stock Exchange ISIN HU0000120720

BSE ticker WABERERS Reuters ticker WABE.hu

XETRA code WABS Bloomberg ticker WABERERS HB

Analyst Issued Rating TP (HUF) Upside(2)

Paul Bradley

(Citi)9 Aug 2017 Buy 6,557 31%

Tibor Bokor

(Berenberg)9 Aug 2017 Buy 6,990 39%

Alex Kazbegi

(RenCap)16 Aug 2017 Buy 6,587 31%

József Miró

(Erste)22 Aug 2017 Buy 7,345 47%

Agenda

| Waberer’s Highlights

| Investment Case

| Established Market Leadership Secured by Significant Barriers to Entry

| Attractive Growth and Consolidation Prospects – European Market

| Attractive Growth and Consolidation Prospects – Regional Market

| Focused Strategy, Underpinned by a Compelling Value Proposition,

Driving Above-Market Growth

| Industry-Leading Operational Performance

| Resilient Business Model

| Appendix

| 9

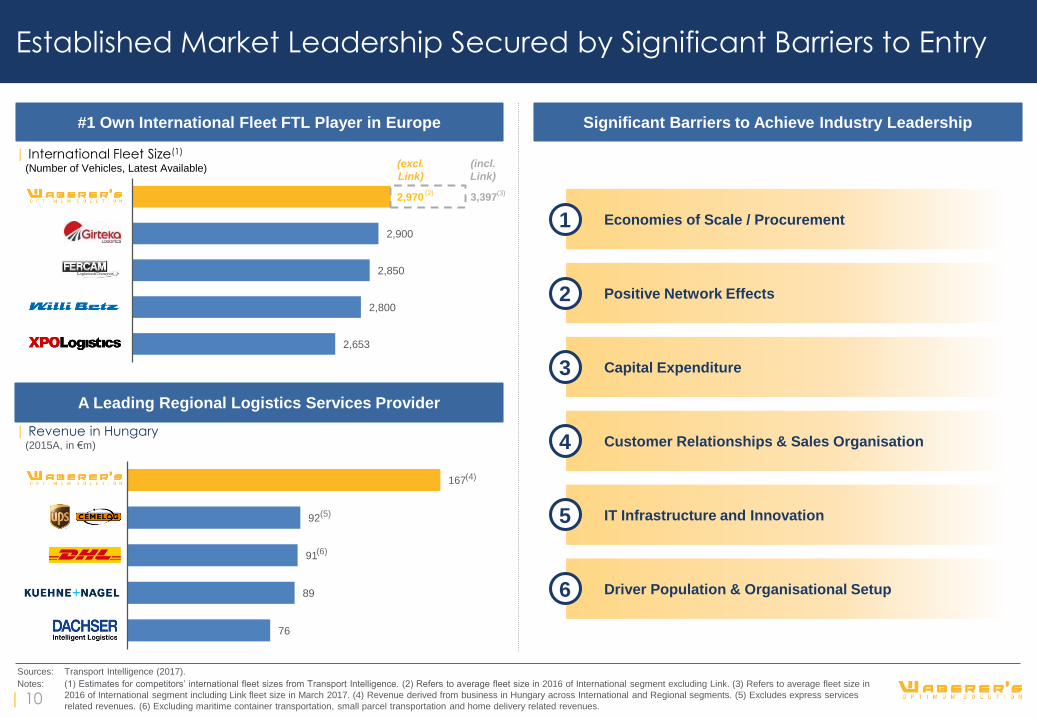

2,970

2,653

2,800

2,850

2,900

3,397

XPO Logistics

Wili Betz

Fercam

Girteka

Waberers

#1 Own International Fleet FTL Player in Europe

A Leading Regional Logistics Services Provider

Significant Barriers to Achieve Industry Leadership

| International Fleet Size(1)

(Number of Vehicles, Latest Available)

Economies of Scale / Procurement1

Positive Network Effects2

Capital Expenditure3

Customer Relationships & Sales Organisation4

IT Infrastructure and Innovation5

Driver Population & Organisational Setup6

Sources: Transport Intelligence (2017).

Notes: (1) Estimates for competitors’ international fleet sizes from Transport Intelligence. (2) Refers to average fleet size in 2016 of International segment excluding Link. (3) Refers to average fleet size in

2016 of International segment including Link fleet size in March 2017. (4) Revenue derived from business in Hungary across International and Regional segments. (5) Excludes express services

related revenues. (6) Excluding maritime container transportation, small parcel transportation and home delivery related revenues.

(2)

76

89

91

92

167

| Revenue in Hungary(2015A, in €m)

(4)

(5)

(6)

(excl.

Link)

(incl.

Link)

(3)

Established Market Leadership Secured by Significant Barriers to Entry

| 10

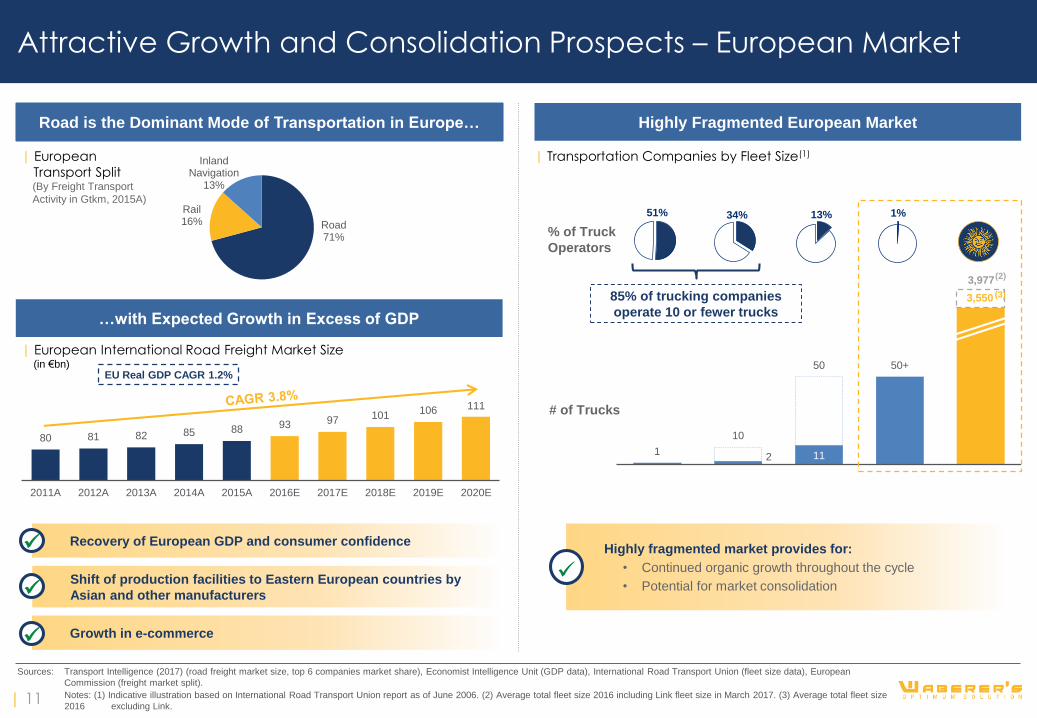

2 111

10

50 50+

3,977

3,550

80 81 82 85 88 93 97 101 106 111

2011A 2012A 2013A 2014A 2015A 2016E 2017E 2018E 2019E 2020E

Attractive Growth and Consolidation Prospects – European Market

Road is the Dominant Mode of Transportation in Europe…

…with Expected Growth in Excess of GDP

Highly Fragmented European Market

| European International Road Freight Market Size(in €bn)

Sources: Transport Intelligence (2017) (road freight market size, top 6 companies market share), Economist Intelligence Unit (GDP data), International Road Transport Union (fleet size data), European

Commission (freight market split).

Notes: (1) Indicative illustration based on International Road Transport Union report as of June 2006. (2) Average total fleet size 2016 including Link fleet size in March 2017. (3) Average total fleet size

2016 excluding Link.

Highly fragmented market provides for:

• Continued organic growth throughout the cycle

• Potential for market consolidation

| Transportation Companies by Fleet Size(1)

Growth in e-commerce

Recovery of European GDP and consumer confidence

EU Real GDP CAGR 1.2%

85% of trucking companies

operate 10 or fewer trucks

51% 34% 13% 1%

% of Truck

Operators

# of Trucks

(2)

| European

Transport Split(By Freight Transport

Activity in Gtkm, 2015A)

Road71%

Rail16%

Inland Navigation

13%

Shift of production facilities to Eastern European countries by

Asian and other manufacturers

(3)

| 11

1.8 1.8 1.92.1 2.1 2.2 2.2 2.3 2.4 2.5

2011A 2012A 2013A 2014A 2015A 2016E 2017E 2018E 2019E 2020E

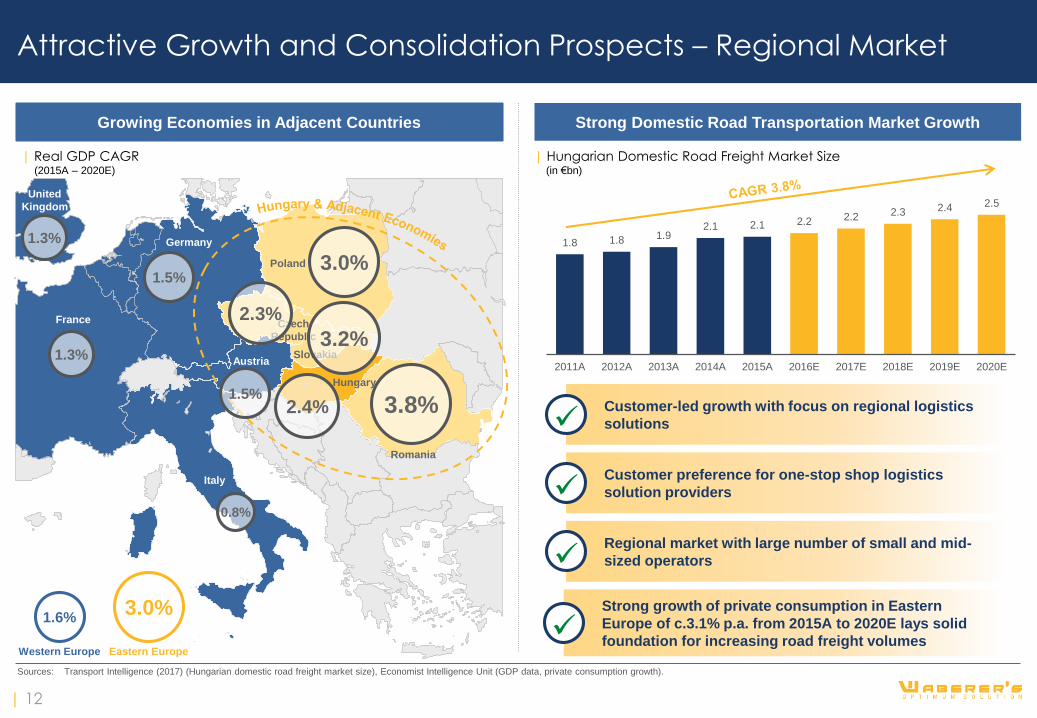

Attractive Growth and Consolidation Prospects – Regional Market

Growing Economies in Adjacent Countries Strong Domestic Road Transportation Market Growth

| Real GDP CAGR(2015A – 2020E)

Sources: Transport Intelligence (2017) (Hungarian domestic road freight market size), Economist Intelligence Unit (GDP data, private consumption growth).

Customer-led growth with focus on regional logistics

solutions

Customer preference for one-stop shop logistics

solution providers

Regional market with large number of small and mid-

sized operators

| Hungarian Domestic Road Freight Market Size(in €bn)

Hungary

2.4%

Italy

0.8%

Germany

1.5%

Austria

1.5%

Czech

Republic

2.3%

Slovakia3.2%

Poland 3.0%

3.8%

Romania

3.0%1.6%

Western Europe Eastern Europe

France

1.3%

Strong growth of private consumption in Eastern

Europe of c.3.1% p.a. from 2015A to 2020E lays solid

foundation for increasing road freight volumes

United

Kingdom

1.3%

| 12

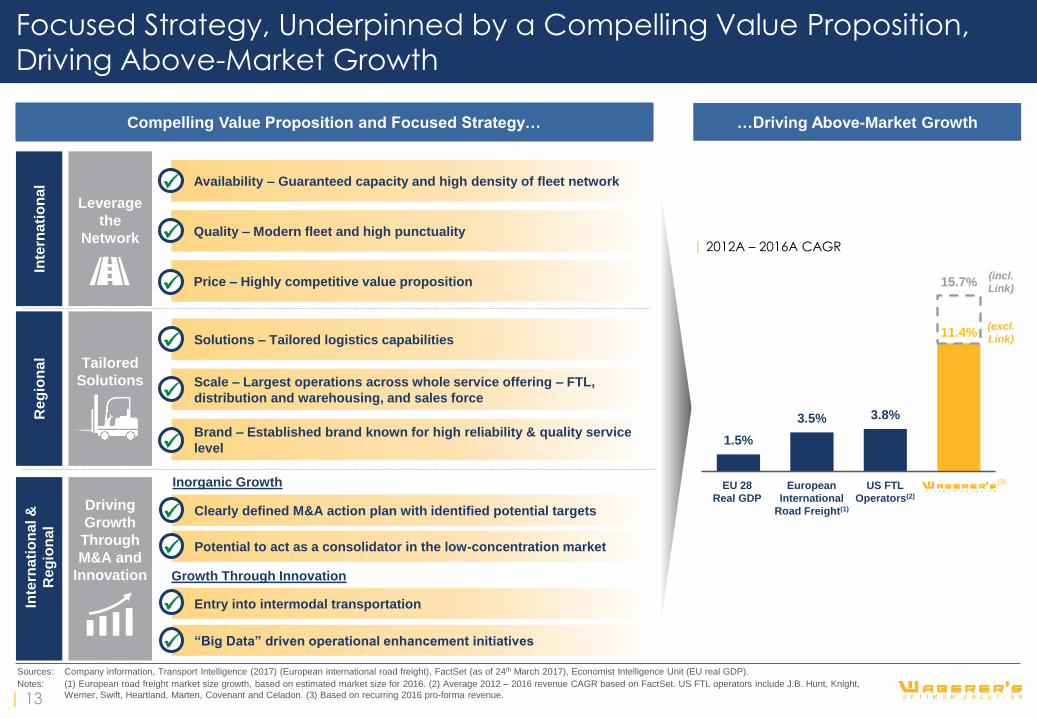

Focused Strategy, Underpinned by a Compelling Value Proposition,

Driving Above-Market Growth

Compelling Value Proposition and Focused Strategy… …Driving Above-Market Growth

Leverage

the

Network

Tailored

Solutions

Driving

Growth

Through

M&A and

Innovation

Solutions – Tailored logistics capabilities

Scale – Largest operations across whole service offering – FTL,

distribution and warehousing, and sales force

Brand – Established brand known for high reliability & quality service

level

11.4%

1.5%

3.5% 3.8%

15.7%

Clearly defined M&A action plan with identified potential targets

Potential to act as a consolidator in the low-concentration market

Entry into intermodal transportation

“Big Data” driven operational enhancement initiatives

Inorganic Growth

Growth Through Innovation

Sources: Company information, Transport Intelligence (2017) (European international road freight), FactSet (as of 24th March 2017), Economist Intelligence Unit (EU real GDP).

Notes: (1) European road freight market size growth, based on estimated market size for 2016. (2) Average 2012 – 2016 revenue CAGR based on FactSet. US FTL operators include J.B. Hunt, Knight,

Werner, Swift, Heartland, Marten, Covenant and Celadon. (3) Based on recurring 2016 pro-forma revenue.

| 2012A – 2016A CAGR

European

International

Road Freight(1)

US FTL

Operators(2)

(3)EU 28

Real GDP

Availability – Guaranteed capacity and high density of fleet network

Quality – Modern fleet and high punctuality

Price – Highly competitive value proposition

Inte

rna

tio

na

lR

eg

ion

al

Inte

rna

tio

na

l &

Re

gio

na

l

(excl.

Link)

(incl.

Link)

| 13

High Density of

Coverage(3)

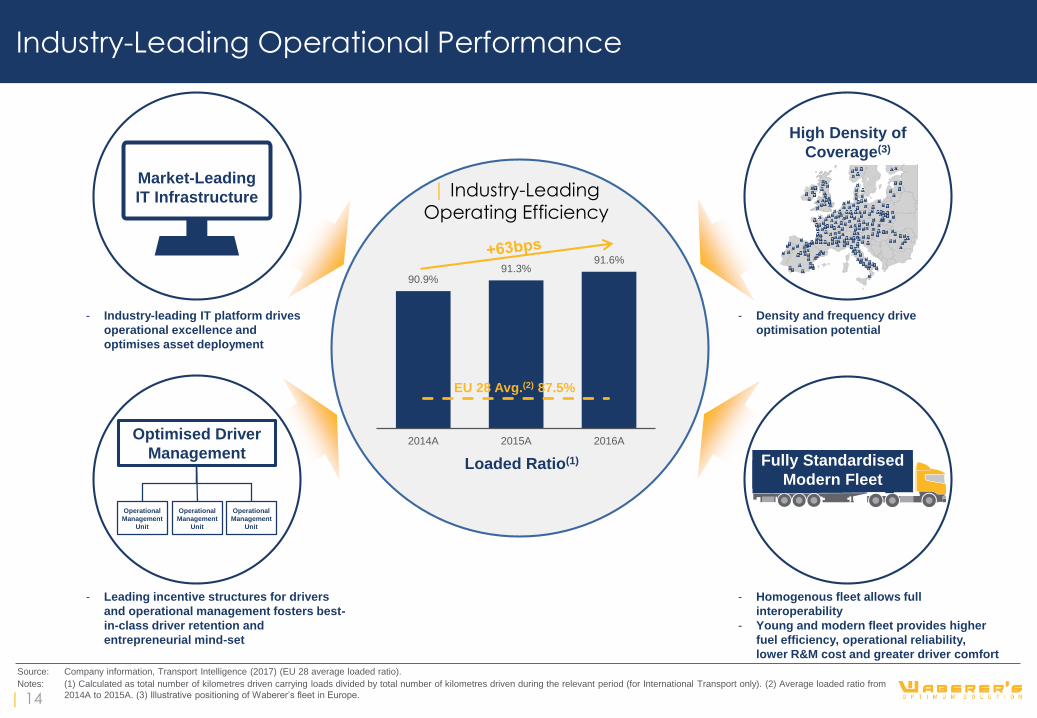

Industry-Leading Operational Performance

| Industry-Leading Operating Efficiency

Loaded Ratio(1)

Source: Company information, Transport Intelligence (2017) (EU 28 average loaded ratio).

Notes: (1) Calculated as total number of kilometres driven carrying loads divided by total number of kilometres driven during the relevant period (for International Transport only). (2) Average loaded ratio from

2014A to 2015A. (3) Illustrative positioning of Waberer’s fleet in Europe.

90.9%91.3%

91.6%

2014A 2015A 2016A

EU 28 Avg.(2) 87.5%

- Industry-leading IT platform drives

operational excellence and

optimises asset deployment

- Leading incentive structures for drivers

and operational management fosters best-

in-class driver retention and

entrepreneurial mind-set

- Density and frequency drive

optimisation potential

- Homogenous fleet allows full

interoperability

- Young and modern fleet provides higher

fuel efficiency, operational reliability,

lower R&M cost and greater driver comfort

Fully Standardised

Modern Fleet

Optimised Driver

Management

Operational

Management

Unit

Operational

Management

Unit

Operational

Management

Unit

Market-Leading

IT Infrastructure

| 14

FMCG23%

Automotive16%

Electronics12%

Freight Forwarders

11%

Retail5%

Construction & Packaging

2%

Non-Classified31%

3,433

2,765

668 785

117

3,550

Fleet 2015 Replacement Expansion Fleet 2016

Continuous fleet

renewal programme

Established OEM

buyback scheme

Allows re-scalability

and re-configuration

of fleet

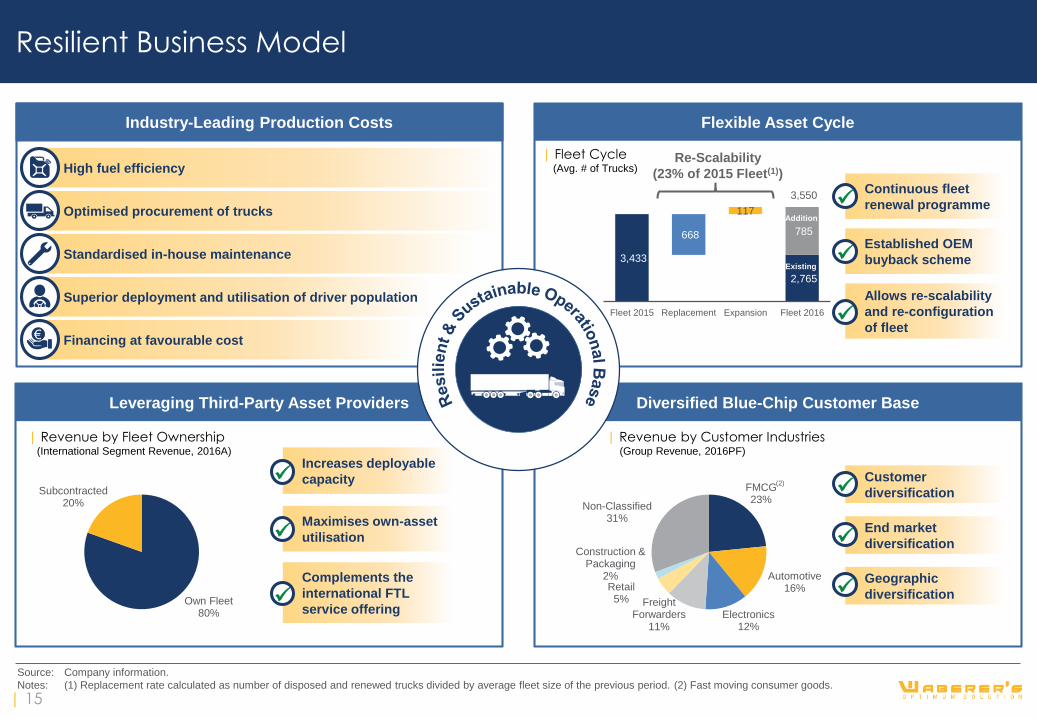

Resilient Business Model

Source: Company information.

Notes: (1) Replacement rate calculated as number of disposed and renewed trucks divided by average fleet size of the previous period. (2) Fast moving consumer goods.

Industry-Leading Production Costs

Leveraging Third-Party Asset Providers

Flexible Asset Cycle

Diversified Blue-Chip Customer Base

High fuel efficiency

Optimised procurement of trucks

Standardised in-house maintenance

| Revenue by Fleet Ownership(International Segment Revenue, 2016A)

Customer

diversification

End market

diversification

Geographic

diversification

| Fleet Cycle(Avg. # of Trucks)

Increases deployable

capacity

Maximises own-asset

utilisation

Complements the

international FTL

service offering

Re-Scalability

(23% of 2015 Fleet(1))

Addition

Existing

Superior deployment and utilisation of driver population

Financing at favourable cost

| Revenue by Customer Industries(Group Revenue, 2016PF)

(2)

Own Fleet80%

Subcontracted20%

€

| 15

Agenda

| Waberer’s Highlights

| Investment Case

| Appendix

| H1 2017 Results Highlights

| Diversified, Blue-Chip Customer Base

| Platform for Growth Through M&A

| Identified M&A Selection Criteria

| Polish Acquisition

| Industry Recognised and Highly Regarded Board of Directors

| Financial Statements

| 16

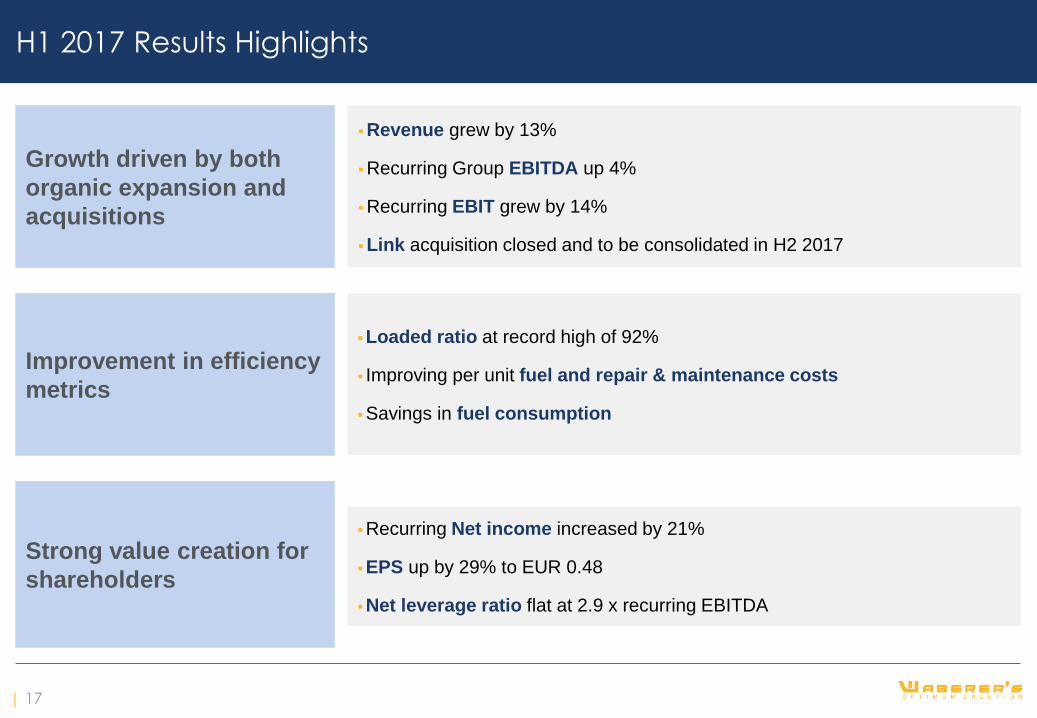

H1 2017 Results Highlights

Revenue grew by 13%

Recurring Group EBITDA up 4%

Recurring EBIT grew by 14%

Link acquisition closed and to be consolidated in H2 2017

Growth driven by both

organic expansion and

acquisitions

Strong value creation for

shareholders

Recurring Net income increased by 21%

EPS up by 29% to EUR 0.48

Net leverage ratio flat at 2.9 x recurring EBITDA

Improvement in efficiency

metrics

Loaded ratio at record high of 92%

Improving per unit fuel and repair & maintenance costs

Savings in fuel consumption

| 17

FMCG23%

Automotive16%

Electronics12%

Freight Forwarders

11%

Retail5%

Construction & Packaging

2%

Non-Classified31%

Freight Forwarders

10%

BCO90%

Hungary Regional17%

Hungary International

12%

United Kingdom12%

Germany12%

France11%

Italy6%

Netherlands5%

Spain5%

Austria3%

Slovakia3%

Other7%

3rd Party Insurance 6%

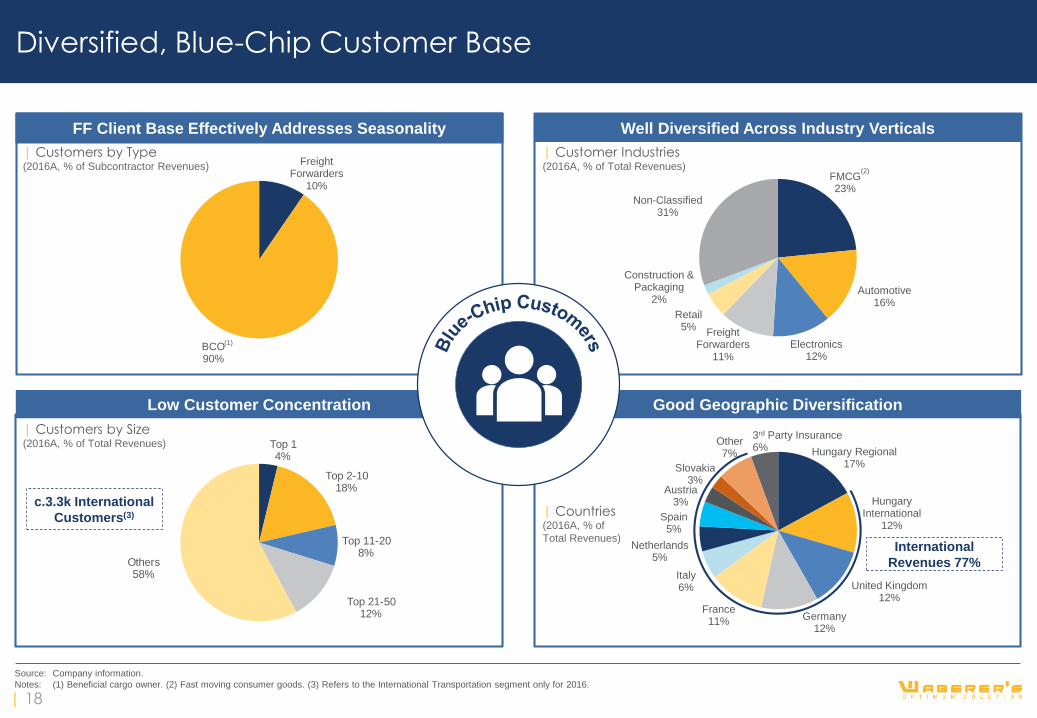

Diversified, Blue-Chip Customer Base

Source: Company information.

Notes: (1) Beneficial cargo owner. (2) Fast moving consumer goods. (3) Refers to the International Transportation segment only for 2016.

Top 14%

Top 2-1018%

Top 11-208%

Top 21-5012%

Others58%

Low Customer Concentration Good Geographic Diversification

| Customer Industries(2016A, % of Total Revenues)

| Customers by Size(2016A, % of Total Revenues)

| Countries(2016A, % of

Total Revenues)

| Customers by Type(2016A, % of Subcontractor Revenues)

(1)

FF Client Base Effectively Addresses Seasonality Well Diversified Across Industry Verticals

(2)

c.3.3k International

Customers(3)

International

Revenues 77%

| 18

Platform for Growth Through M&A

Source: Company information.

M&A Objectives

Extended geographical coverage to access new labour

and customer markets

Build incremental FTL scale

Expand customer base

Expand regional offering to new industry verticals and

value-added services

Applying industry-leading technology to harvest

synergies and extract value

Industry-leading operating platform

Committed to Inorganic Growth

| Successfully acquired and integrated several companies in the

past, both domestically and internationally

| Committed to act as a consolidator to capitalise on the potential

opportunities in the highly fragmented international and regional

markets

─ Team in place that continuously monitors the market for relevant

acquisition opportunities

| Several targets identified:

─ Structured approach to selection

─ Coherence with growth, margin and operational targets ensured

2002

Acquisition of Hungarocamion(1,200 trucks acquired)

2007

Acquisition of Révész Eurotrans

(424 trucks acquired)

2013

Acquisition of Szemerey

(465 trucks acquired)

2016

Acquisition of

WHB Insurance

CEO joined the group,

i.e. participating in

successful integration

of several targets

2017

Acquisition of Link

(427 trucks acquired)

| 19

English as

corporate language

English as

corporate language

Identified M&A Selection Criteria

Source: Company information.

| Size– Focus on mid-sized

operators

– Quality book

of business

– Scope for operational

improvement

– Economies of scale

Revenue:

>€50mEquity Value:

€30–50m

| Geography

– Expansion into

high-growth CEE

economies key priority

| Business Focus

– Operational focus on

standardised asset-based

operations

– Coherence with

existing strategy of

international segment

| Management

– Compatibility with Waberer’s

management, organisation and

location is key

– Ensure ease of integration and

subsequent operation

Strong FTL

expertise

Geographic

accessibility

FTL

1

2

3

4

CEE contract logistics

for standardised cargo

| Size

– Focus on small and

mid-sized

logistics providers

– Quality book

of business

Revenue:

€20–50mEquity Value:

Up to €50m

| Geography

– Regional expansion

– High-growth adjacent

countries

| Business Focus

– Expansion into new

industry verticals

– Operations focussed around

warehousing and

value-added services

| Management

– Compatibility with Waberer’s

management, organisation and

location is key

– Ensure ease of integration and

subsequent operation

Strong logistics

expertise

Geographic

accessibility

Warehousing

Value

Added

Services

Distribution

Electronics

Automotive

Fresh

Retail

1

2

3

4

Regional LogisticsInternational Transportation

FMCG

Fleet Size:

>300 Trucks

Number of Identified Potential Targets: c.20 – 25

Healthy diversification

of customer baseHealthy diversification

of customer base

PL SKCZ PL SISK

| 20

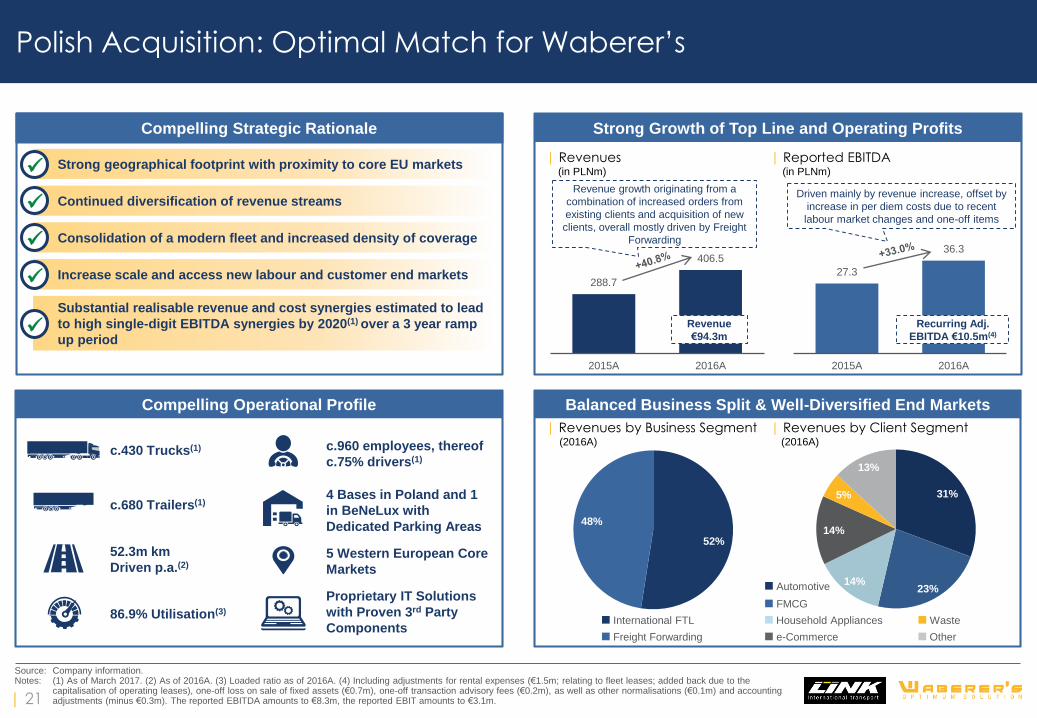

31%

23% 14%

14%

5%

13%

52%

48%

27.3

36.3

2015A 2016A

288.7

406.5

2015A 2016A

Source: Company information.Notes: (1) As of March 2017. (2) As of 2016A. (3) Loaded ratio as of 2016A. (4) Including adjustments for rental expenses (€1.5m; relating to fleet leases; added back due to the

capitalisation of operating leases), one-off loss on sale of fixed assets (€0.7m), one-off transaction advisory fees (€0.2m), as well as other normalisations (€0.1m) and accounting adjustments (minus €0.3m). The reported EBITDA amounts to €8.3m, the reported EBIT amounts to €3.1m.

| Revenues by Client Segment(2016A)

Automotive

FMCG

Othere-Commerce

Household Appliances Waste

| Revenues by Business Segment(2016A)

International FTL

Freight Forwarding

Balanced Business Split & Well-Diversified End Markets

Strong Growth of Top Line and Operating Profits

| Revenues(in PLNm)

| Reported EBITDA(in PLNm)

Revenue

€94.3m

Recurring Adj.

EBITDA €10.5m(4)

Driven mainly by revenue increase, offset by

increase in per diem costs due to recent

labour market changes and one-off items

Revenue growth originating from a

combination of increased orders from

existing clients and acquisition of new

clients, overall mostly driven by Freight

Forwarding

Polish Acquisition: Optimal Match for Waberer’s

Compelling Strategic Rationale

c.960 employees, thereof

c.75% drivers(1)

4 Bases in Poland and 1

in BeNeLux with

Dedicated Parking Areas

c.430 Trucks(1)

c.680 Trailers(1)

Proprietary IT Solutions

with Proven 3rd Party

Components

Compelling Operational Profile

52.3m km

Driven p.a.(2)

86.9% Utilisation(3)

5 Western European Core

Markets

Strong geographical footprint with proximity to core EU markets

Continued diversification of revenue streams

Consolidation of a modern fleet and increased density of coverage

Substantial realisable revenue and cost synergies estimated to lead

to high single-digit EBITDA synergies by 2020(1) over a 3 year ramp

up period

Increase scale and access new labour and customer end markets

| 21

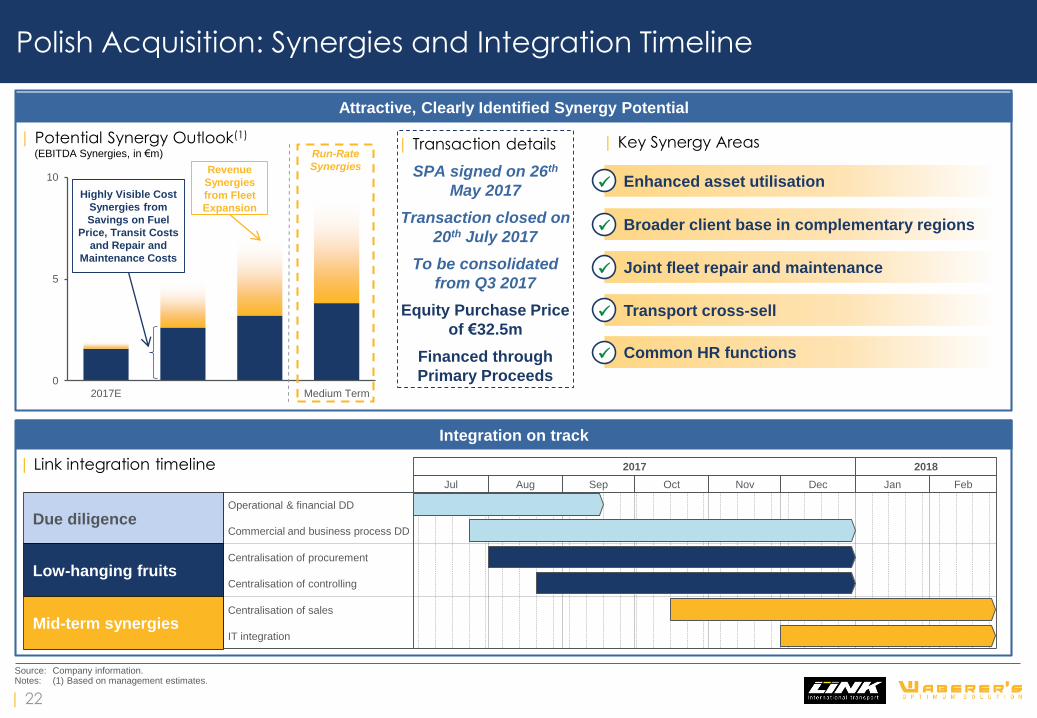

0

5

10

2017E Medium Term

Polish Acquisition: Synergies and Integration Timeline

Source: Company information.Notes: (1) Based on management estimates.

Attractive, Clearly Identified Synergy Potential

Integration on track

Broader client base in complementary regions

Joint fleet repair and maintenance

Common HR functions

Transport cross-sell

| Key Synergy Areas| Potential Synergy Outlook(1)

(EBITDA Synergies, in €m) Run-Rate

Synergies

Highly Visible Cost

Synergies from

Savings on Fuel

Price, Transit Costs

and Repair and

Maintenance Costs

Revenue

Synergies

from Fleet

Expansion

| Transaction details

SPA signed on 26th

May 2017

Transaction closed on

20th July 2017

To be consolidated

from Q3 2017

Equity Purchase Price

of €32.5m

Financed through

Primary Proceeds

Enhanced asset utilisation

2017 2018

Jul Aug Sep Oct Nov Dec Jan Feb

IT integration

Centralisation of procurement

Commercial and business process DD

Operational & financial DD

Centralisation of sales

Centralisation of controlling

Due diligence

Low-hanging fruits

Mid-term synergies

| 22

| Link integration timeline

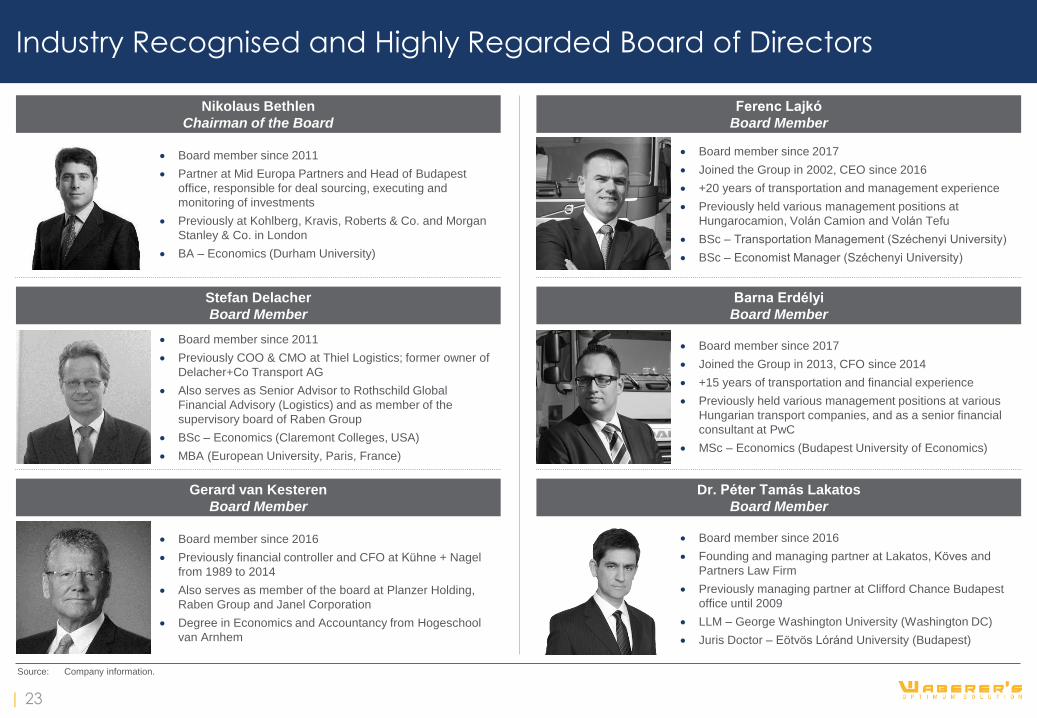

Board member since 2017

Joined the Group in 2002, CEO since 2016

+20 years of transportation and management experience

Previously held various management positions at

Hungarocamion, Volán Camion and Volán Tefu

BSc – Transportation Management (Széchenyi University)

BSc – Economist Manager (Széchenyi University)

Ferenc Lajkó

Board Member

Board member since 2017

Joined the Group in 2013, CFO since 2014

+15 years of transportation and financial experience

Previously held various management positions at various

Hungarian transport companies, and as a senior financial

consultant at PwC

MSc – Economics (Budapest University of Economics)

Barna Erdélyi

Board Member

Board member since 2011

Previously COO & CMO at Thiel Logistics; former owner of

Delacher+Co Transport AG

Also serves as Senior Advisor to Rothschild Global

Financial Advisory (Logistics) and as member of the

supervisory board of Raben Group

BSc – Economics (Claremont Colleges, USA)

MBA (European University, Paris, France)

Stefan Delacher

Board Member

Board member since 2016

Previously financial controller and CFO at Kühne + Nagel

from 1989 to 2014

Also serves as member of the board at Planzer Holding,

Raben Group and Janel Corporation

Degree in Economics and Accountancy from Hogeschool

van Arnhem

Source: Company information.

Industry Recognised and Highly Regarded Board of Directors

Gerard van Kesteren

Board Member

Board member since 2011

Partner at Mid Europa Partners and Head of Budapest

office, responsible for deal sourcing, executing and

monitoring of investments

Previously at Kohlberg, Kravis, Roberts & Co. and Morgan

Stanley & Co. in London

BA – Economics (Durham University)

Nikolaus Bethlen

Chairman of the Board

Board member since 2016

Founding and managing partner at Lakatos, Köves and

Partners Law Firm

Previously managing partner at Clifford Chance Budapest

office until 2009

LLM – George Washington University (Washington DC)

Juris Doctor – Eötvös Lóránd University (Budapest)

Dr. Péter Tamás Lakatos

Board Member

| 23

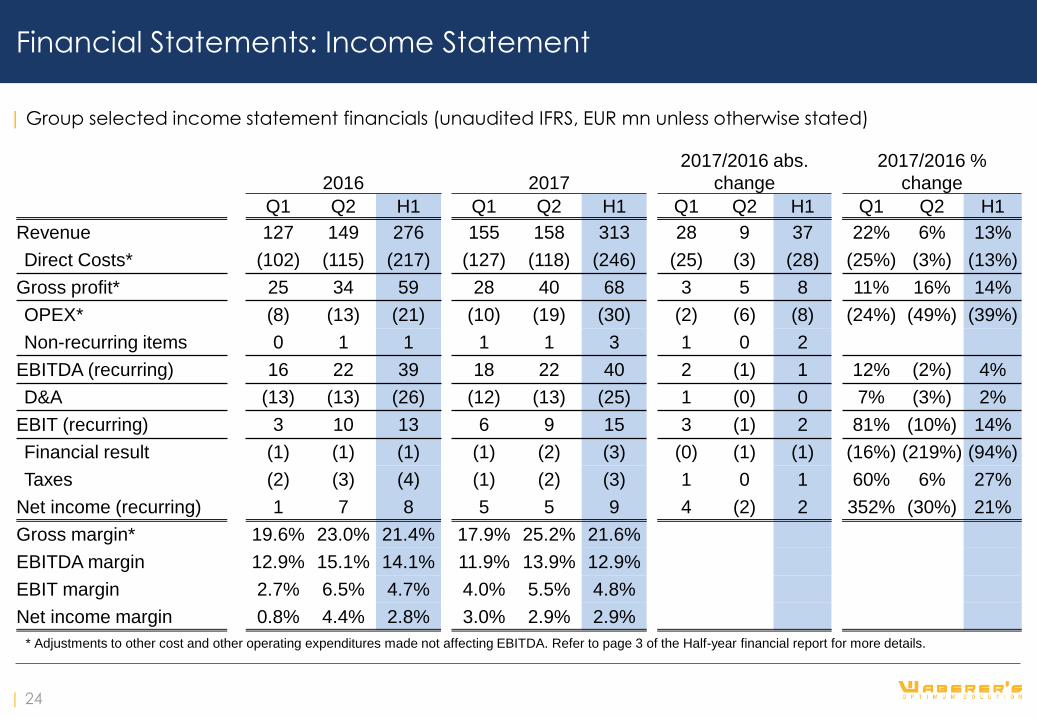

Financial Statements: Income Statement

| Group selected income statement financials (unaudited IFRS, EUR mn unless otherwise stated)

2016 2017

2017/2016 abs.

change

2017/2016 %

change

Q1 Q2 H1 Q1 Q2 H1 Q1 Q2 H1 Q1 Q2 H1

Revenue 127 149 276 155 158 313 28 9 37 22% 6% 13%

Direct Costs* (102) (115) (217) (127) (118) (246) (25) (3) (28) (25%) (3%) (13%)

Gross profit* 25 34 59 28 40 68 3 5 8 11% 16% 14%

OPEX* (8) (13) (21) (10) (19) (30) (2) (6) (8) (24%) (49%) (39%)

Non-recurring items 0 1 1 1 1 3 1 0 2

EBITDA (recurring) 16 22 39 18 22 40 2 (1) 1 12% (2%) 4%

D&A (13) (13) (26) (12) (13) (25) 1 (0) 0 7% (3%) 2%

EBIT (recurring) 3 10 13 6 9 15 3 (1) 2 81% (10%) 14%

Financial result (1) (1) (1) (1) (2) (3) (0) (1) (1) (16%) (219%) (94%)

Taxes (2) (3) (4) (1) (2) (3) 1 0 1 60% 6% 27%

Net income (recurring) 1 7 8 5 5 9 4 (2) 2 352% (30%) 21%

Gross margin* 19.6% 23.0% 21.4% 17.9% 25.2% 21.6%

EBITDA margin 12.9% 15.1% 14.1% 11.9% 13.9% 12.9%

EBIT margin 2.7% 6.5% 4.7% 4.0% 5.5% 4.8%

Net income margin 0.8% 4.4% 2.8% 3.0% 2.9% 2.9%

* Adjustments to other cost and other operating expenditures made not affecting EBITDA. Refer to page 3 of the Half-year financial report for more details.

| 24

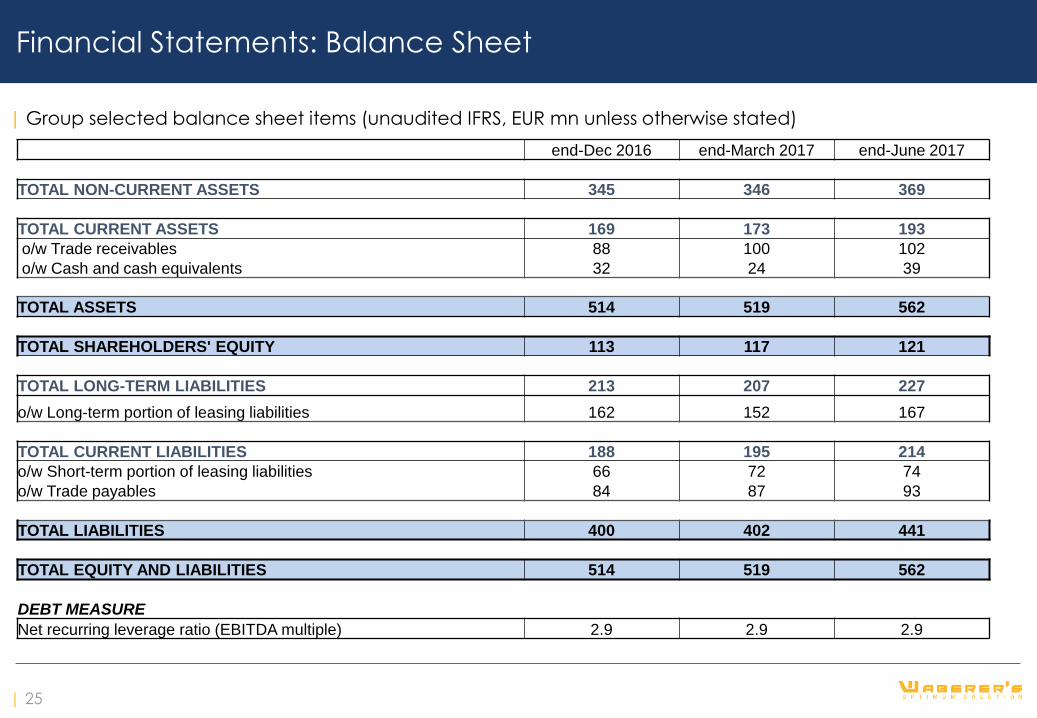

Financial Statements: Balance Sheet

| Group selected balance sheet items (unaudited IFRS, EUR mn unless otherwise stated)

end-Dec 2016 end-March 2017 end-June 2017

TOTAL NON-CURRENT ASSETS 345 346 369

TOTAL CURRENT ASSETS 169 173 193

o/w Trade receivables 88 100 102

o/w Cash and cash equivalents 32 24 39

TOTAL ASSETS 514 519 562

TOTAL SHAREHOLDERS' EQUITY 113 117 121

TOTAL LONG-TERM LIABILITIES 213 207 227

o/w Long-term portion of leasing liabilities 162 152 167

TOTAL CURRENT LIABILITIES 188 195 214

o/w Short-term portion of leasing liabilities 66 72 74

o/w Trade payables 84 87 93

TOTAL LIABILITIES 400 402 441

TOTAL EQUITY AND LIABILITIES 514 519 562

DEBT MEASURE

Net recurring leverage ratio (EBITDA multiple) 2.9 2.9 2.9

| 25

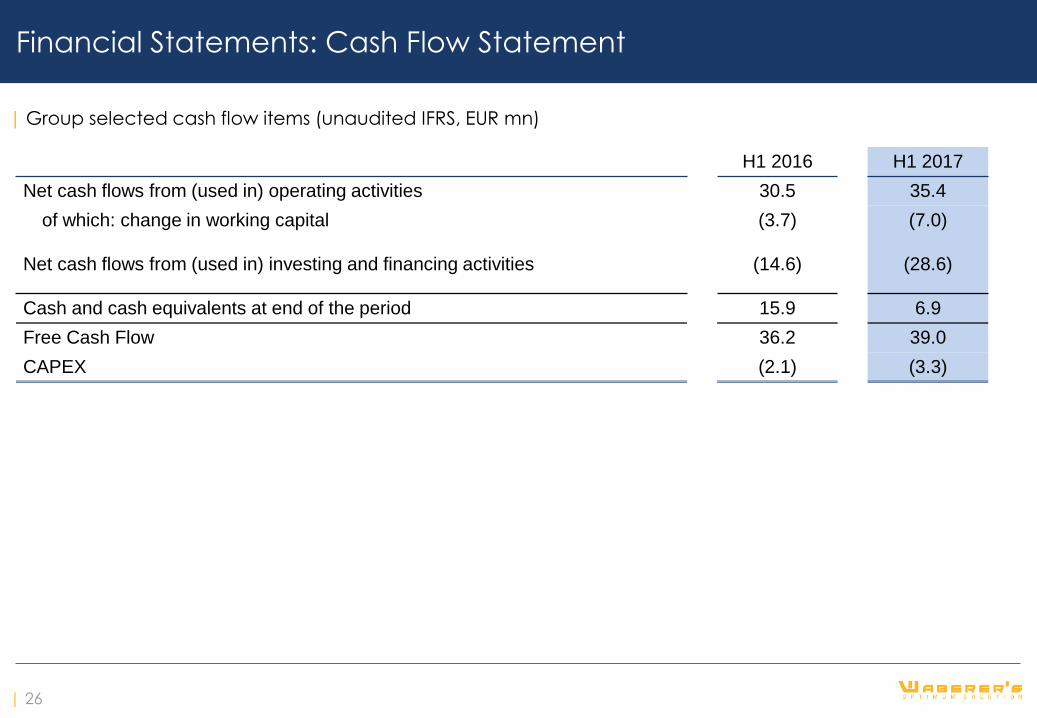

Financial Statements: Cash Flow Statement

| Group selected cash flow items (unaudited IFRS, EUR mn)

H1 2016 H1 2017

Net cash flows from (used in) operating activities 30.5 35.4

of which: change in working capital (3.7) (7.0)

Net cash flows from (used in) investing and financing activities (14.6) (28.6)

Cash and cash equivalents at end of the period 15.9 6.9

Free Cash Flow 36.2 39.0

CAPEX (2.1) (3.3)

| 26

WABERER’S INTERNATIONAL Nyrt.

H-1239 Budapest, Nagykőrösi út 351.

Tel: +36 1 421 6300

E-mail: [email protected]

![INTRODUCTION 1 - AC Transit · [13] Consolidated Budget (in US$ thousands) Budget Period Ending June 30 2013A 2014A 2015A 2016B 2017E 2018E 2019E 2020E 2021E Line Revenue 1 Operating](https://img.pdfslide.us/doc/110x75/5e015cde4742db518308cf27/introduction-1-ac-13-consolidated-budget-in-us-thousands-budget-period-ending.jpg)