Embed Size (px)

Citation preview

Korea Midland Power Co., Ltd.Management Presentation toStandard & Poor’s

November 14, 2002

2

AgendaAgenda

Executive summaryExecutive summary

KOMIPO overview

Key profit drivers and KOMIPO advantages

Assessment of deregulation and privatization

Robust financial profile

3

Issue Key objectives

Credit ratingObtain confidential long-term foreign currency issuer ratings for Korea Midland Power Co., Ltd from S&P

Establish a ratings platform for future fund-raising activities in the global debt market

Information Memorandum

Highlight KOMIPO’s exceptional creditworthiness through its: forward-looking management approach to changes in the industry leading market position due to its superior operating efficiency and cost control

strategy very strong cash flows resulting from the most competitive unit cost of generation; and strong financial discipline and sound debt protection measures

KOMIPO seeks to obtain confidential foreign currency issuer credit ratings from S&PKOMIPO seeks to obtain confidential foreign currency issuer credit ratings from S&P

4

Key highlights of KOMIPO’s business profile

KOMIPO represents the gencos on 10 of 14 deregulation committees

KOMIPO represents the gencos on 10 of 14 deregulation committees

Proximity to major end-user markets

Seoul and Jeju plants play key local roles

Proximity to major end-user markets

Seoul and Jeju plants play key local roles

Plants under construction will enhance KOMIPO’s competitiveness in 2005, 2006 and 2008

Plants under construction will enhance KOMIPO’s competitiveness in 2005, 2006 and 2008

Active fuel supply management

Active fuel supply management

Base and middle load plants among Korea’s most competitive

Base and middle load plants among Korea’s most competitive

Boryeong Thermal is Korea’s lowest unit cost thermal power plant

Overall efficiency will increase with new Boryeong CC

Boryeong Thermal is Korea’s lowest unit cost thermal power plant

Overall efficiency will increase with new Boryeong CC

Robustdemand for power

Quality of personnel

Strategicallysited

facilities

Attractivebase load/peak load

mix

Solid operatingefficiency

Competitive, low-cost

fuel supply

KOMIPO is distinguished by its operational competitiveness and structural advantages …

KOMIPO is distinguished by its operational competitiveness and structural advantages …

5

KOMIPO stands at the leading edge of Korea’s thermal generation sector as differences in credit quality become increasingly clear

KOMIPO stands at the leading edge of Korea’s thermal generation sector as differences in credit quality become increasingly clear

1 FFO = Net income + Depreciation and AmortizationIncludes capitalized interest

Key highlights of KOMIPO’s financial profile

Actual, 9 mths to Actual, 6 mths to Projected, full yearYear ended Dec 31, 2001 Jun 30, 2002 FY2002

Credit statistics

EBIT interest coverage (x) 2.8 3.8 5.0

EBITDA interest coverage (x) 4.9 6.1 7.1

FFO1/total debt (%) 34.2 47.0 59.4

Capex/capital (%) 3.4 5.7 9.6

EBIT return on capital (%) 8.0 12.5 17.3

EBITDA margin (%) 36.2 38.1 39.5

Debt/capital (%) 46.7 38.0 31.4

Debt/EBITDA (x) 3.4 1.9 1.3

… which are underscored by KOMIPO’s industry-leading financial performance… which are underscored by KOMIPO’s industry-leading financial performance

6

AgendaAgenda

Executive summary

KOMIPO overviewKOMIPO overview

Key profit drivers and KOMIPO advantages

Assessment of deregulation and privatization

Robust financial profile

7

Seocheon(400)

Boryeong CC(1,800)

Boryeong(3,000)

Incheon(1,150)

Incheon CC(450)

Seoul (387.5)

Seoul

Incheon

BukJeju(255)

Seoul ThermalOnly power plant located in Seoul City

Valuable contributor of heat and power

Strategic location

Incheon ThermalEnvironmentally-friendly

Incheon CCTo be completed by 2005Low variable unit cost

Boryeong ThermalNamed as world’s best coal power plant

Track record of lowest unit costs

Seocheon ThermalUses domestic anthracite coal

Strategic to local industry

Boryeong CCKorea’s largest LNG combined-cycle plant

Low variable unit costHigh utilization

Jeju ThermalCaptive demandRapid economic growthWill benefit from unbundling of transmission costs

Yangyang(1,000)

Yangyang Hydro•To be completed by 2006

•Korea’s largest pumped-storage power plant

Each of KOMIPO’s plants contribute valuable operational and strategic strengthsEach of KOMIPO’s plants contribute valuable operational and strategic strengths

8

15% 15%9%

1%

-2%

20% 21%12% 11%

6%

KOMIPO KOSEPCO KOWEPO KOSPO KEWESPO

2H2001 1H2002

36% 33% 29% 30% 30%38% 36% 33%

38%33%

KOMIPO KOSEPCO KOWEPO KOSPO KEWESPO

2H2001 1H2002EBITDA margin

Net income margin

2H2001 and 1H2002 genco margin comparison

KOMIPO is one of Korea’s strongest and most profitable generation companiesKOMIPO is one of Korea’s strongest and most profitable generation companies

9

KOMIPO is organized along two co-ordinating business divisionsKOMIPO is organized along two co-ordinating business divisions

KOMIPO’s organizational structure

President & CEO

Executive Auditor

Administration Division Engineering Division

Corporate Planning

Department

Administration Department

Business Department

Power Generation Department

Power Construction Department

Boryeong Thermal Power

Seoul Thermal Power

Incheon Thermal Power

Seocheon Thermal Power

Jeju Thermal Power

Yangyang Pumped Storage Power

10

Cost reduction

Implement eGen system to optimize facility operation and management

Preparation for electricity trading under TWBP

Strengthening internal capability

2001 - 04 2004 - 09 2009 and after

Securing competitive position

Optimize efficiency together with cost reduction

Improve overall organization and management system to enhance competitiveness

Global best practices

Raise overall capacities to global standards

Growing market share as new facilities are completed

Start privatization process for five gencos

Start privatization process for five gencos

Split transmissio

n companies

from KEPCO

Split transmissio

n companies

from KEPCO

Adopt full scale of retail contestability

Adopt full scale of retail contestability

Begin two way bidding pool system

Begin two way bidding pool system

KOMIPO is currently in the first phase of its medium-term business planKOMIPO is currently in the first phase of its medium-term business plan

11

18,337 18,856

13,407

16,71815,767

3,948

11,8088,588

25,151 24,355

1,548

8,433

25,215

19,885

22,804

KOMIPO KOSEPCO KOWEPO KOSPO KEWESPO

Base Peak

2001 net generationGWh

3,400 3,5653,066 3,000 2,900

3,593

2,000

4,280 4,6001,000

1,600 1,800

7,565 7,500

2,765

600

7,9467,993

7,165

KOMIPO KOSEPCO KOWEPO KOSPO KEWESPO

Base Peak Expansion

Installed capacity of gencos1

MW

1 Includes capacity under constructionNote: Base = all coal-fired (imported and domestic) plants, Peak = Oil, LNG and Hydro plants

KOMIPO’s share of peak load generation will increase as new competitive power plants under construction are completed, such as Boryeong CC and Incheon CC

KOMIPO enjoys an attractive slice of the base load marketKOMIPO enjoys an attractive slice of the base load market

12

1H02 sales revenue by power plant

9%

9%

67%

6% 4%5%

SeoulIncheonJ ejuSeocheonBoryeong combinedBoryeong

1H02 sales volume by power plant

Source: Company data, January to June 2002

6%

5%

81%

4%1%

3%

SeoulIncheonJ ejuSeocheonBoryeong combinedBoryeong

GWh KRW bn

The Boryeong power plant is KOMIPO’s flagship facility and major earnings driverThe Boryeong power plant is KOMIPO’s flagship facility and major earnings driver

13

Power projects under construction

Power projects under consideration

Yang Yang Pumped Water Power Project (1,000MW)

Incheon Combined Cycle Project (450MW)

Boryeong Thermal Power Project (1,000MW)

Unit Fuel Capacity Completion

#1~4 250MW/unit 2006

Unit Fuel Capacity Completion

#1 LNG 450MW/unit 2005

Unit Fuel Capacity Completion

#7,8 Bituminous coal 500MW/unit 2007

Boryeong Thermal Power Project (1,600MW)Unit Fuel Capacity Completion

#9,10 Bituminous coal 800MW/unit 2010

KOMIPO’s capacity will expand from 2005 onwardsKOMIPO’s capacity will expand from 2005 onwards

14

AgendaAgenda

Executive summary

KOMIPO overview

Key profit drivers and KOMIPO advantagesKey profit drivers and KOMIPO advantages

Assessment of deregulation and privatization

Robust financial profile

15

KOMIPO has demonstrated strong results with its “power up, cost down” approach

Increased power generation

Reduced operating expenses

Robustdemand for power

Quality of personnel

Strategicallysited

facilities

Attractivebase load/peak load

mix

Solid operatingefficiency

Competitive, low-cost fuel supply

Profitable generation is determined by a genco’s ability to increase utilization and reduce costs

Profitable generation is determined by a genco’s ability to increase utilization and reduce costs

16

Source: MOCIE, First Basic Plan for Demand and Supply of Electricity, 2002-2015, most probable plan

43 48 52 55 59 62 65 6851 55

76 79 77 7768

62

2001 2003 2005 2007 2009 2011 2013 2015

Peak load Capacity

15.1 13.716.8

21.325.3 24.9

18.9

13.7

0

5

10

15

20

25

30

2001 2003 2005 2007 2009 2011 2013 2015

Peak power demand and capacity projectionsGW

Reserve margin%

Robust demand

for power

The electricity industry is characterized by rapid demand growth and capacity growthThe electricity industry is characterized by rapid demand growth and capacity growth

Power demand is expected to grow rapidly at a rate of 3.3% p.a. from 2002-2010

Tight reserve margins of 15%

Planned capacity expansion of 23,813MW between 2002-2010

Tight reserve margins underline individual importance of all 6 power gencos to maintaining the stability of supply

17

Present installed capacity of gencosMW

1,000

450

450

6,393

6,993 6,993 6,993

7,943

8,443

500

2001 02E 03E 04E 05E 06E

Existing capacity Yang yang Inchon

KOMIPO forecast generation capacityMW

KOMIPO has started construction on an additional 1,000MW baseload thermal power plant in Boryeong and is considering another 1,600MW at the same site

Note: Base = all coal-fired (imported and domestic) plants, Peak = Oil, LNG and Hydro plantsSource: Company data

Robust demand

for power

3,565 3,000 3,400 3,066 2,900

2,0002,765

3,5934,280 4,600

5,565 5,765

6,9937,346 7,500

KO

SE

PC

O

KO

SP

O

KO

MIP

O

KO

WE

PO

KE

WE

SP

O

Base Peak

Construction underway will expand KOMIPO’s peak generation capacity in 2005 and 2006Construction underway will expand KOMIPO’s peak generation capacity in 2005 and 2006

18

Accumulated number of 1H2002 SMP merit order determination

Accumulated number of 1H2002 BLMP merit order determination

Source: KPX

After KHNP’s nuclear facilities, Boryeong is the country’s most efficient power plant

Attractive base load/

peak load mix

The flagship 3,000MW Boryeong Power Plant is Korea’s most competitive thermal generation facility

The flagship 3,000MW Boryeong Power Plant is Korea’s most competitive thermal generation facility

19

Attractive base load/ peak load

mix

Merit order as of October 2002

Source: KPX

# Plant name TypeIGP

(KRW/kWh) Owner

1 Tangjin Coal 12.21 KEWESPO

2 Boryeong #3-6 Coal 12.29 KOMIPO

3 Hadong Coal 12.45 KOSPO

4 Samchunpo #5,6 Coal 12.60 KOSEPCO

5 Taeahn Coal 12.99 KOWEPO

6 Boryeong #1,2 Coal 13.01 KOMIPO

7 Samchunpo #1,2 Coal 13.39 KOSEPCO

8 Samchunpo #3,4 Coal 13.43 KOSEPCO

9 Honam Coal 18.91 KEWESPO

10 Tonghae Domestic coal 37.90 KEWESPO

11 Boryeong CC LNG 42.47 KOMIPO

12 Ulsan #4-6 Heavy oil 44.47 KEWESPO

13 Seocheon Domestic coal 45.32 KOMIPO

14 Incheon CC LNG 45.52 KOSPO

15 Ulsan CC #2,3 LNG 45.89 KEWESPO

16 SeoIncheon CC LNG 47.56 KOWEPO

17 Youngnam Heavy oil 47.92 KOSPO

18 Ilsan CC #2 LNG 48.21 KEWESPO

19 Youngdong #2 Domestic coal 49.04 KOSPO

# Plant name TypeIGP

(KRW/kWh) Owner

20 Ulsan #1-3 Heavy oil 50.03 KEWESPO

21 Ilsan CC #1 LNG 51.03 KEWESPO

22 Yosu #1 Heavy oil 51.50 KOSEPCO

23 Youngdong #1 Domestic coal 51.96 KOSEPCO

24 NamJeju Heavy oil 52.85 KOSPO

25 Pyongtaek CC LNG 53.04 KOWEPO

26 Pundang CC #2 LNG 53.22 KOSEPCO

27 Pyongtaek Heavy oil 54.98 KOWEPO

28 Yosu #2 Heavy oil 55.26 KOSEPCO

29 Pundang CC #1 LNG 55.88 KOSEPCO

30 Jeju #2,3 Heavy oil 58.84 KOMIPO

31 Incheon #1,2 LNG 63.57 KOMIPO

32 Seoul #5 LNG 63.79 KOMIPO

33 Seoul #4 LNG 66.94 KOMIPO

34 Incheon #3,4 LNG 67.45 KOMIPO

35 NamJeju Heavy oil 77.69 KOSPO

36 Jeju #1 Heavy oil 77.92 KOMIPO

37 Jeju Light oil 85.89 KOMIPO

38 Hanlim CC Light oil 90.72 KOSPO

39 Jeju GT #3 Light oil 114.94 KOMIPO

Attractive base load/

peak load mix

KOMIPO enjoys good representation across base, middle and peak load segmentsKOMIPO enjoys good representation across base, middle and peak load segments

20

# Plant name Owner Type Unit # # of prices set Price (KRW/kWh)

Samchunpo KOSEPCO #3 14 16.4231 Boryeong KOMIPO #5 3 16.4632 Honam Honam #1 25 19.0933 Honam Honam #2 46 19.3034 Tonghae KEWESPO #2 9 38.1835 Ulsan KEWESPO #4 15 38.9136 Tonghae KEWESPO #1 55 39.7637 Yongnam KOSPO #2 54 40.6338 Ulsan KEWESPO #6 11 41.1439 Yongnam KOSPO #1 131 41.8240 Seocheon KOMIPO #2 51 44.9941 Ulsan KEWESPO #5 38 45.2942 Seocheon KOMIPO #1 8 45.6143 Boryeong CC KOMIPO #2 34 46.9244 Yongdong KOSEPCO #2 139 47.0045 Pyongtaek KOWEPO #3 66 48.7346 Boryeong CC KOMIPO #4 2 49.0547 Yosu KEWESPO #1 71 49.1448 Pyongtaek KOWEPO #1 101 49.5449 Yongdong KOSEPCO #1 169 49.9050 Inchon CC #1 39 50.35Total 4344 48.13

Source: KPX

1H 2002 SMP merit order

Attractive base load/

peak load mix

The Boryeong CC and Seocheon plants also have a solid position in the middle and peak load markets

The Boryeong CC and Seocheon plants also have a solid position in the middle and peak load markets

21

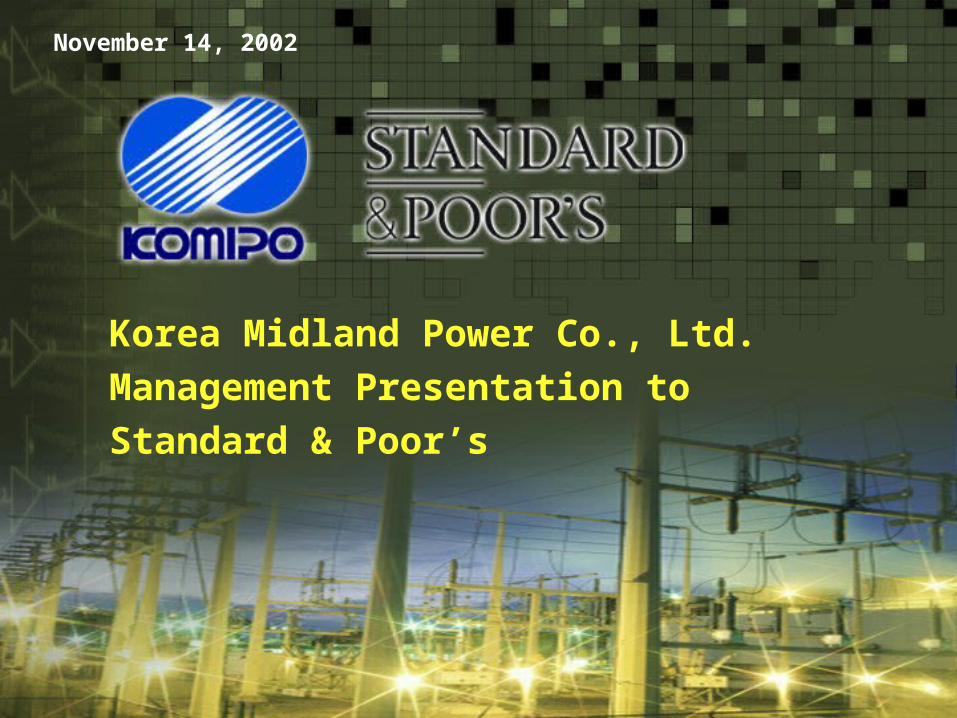

Unbundling of transmission costs

Lower transmission costs: particularly Seoul, Incheon and Jeju island

Peak periods of transmission congestion

Trend of power sold by province

Advantages of location

Cheongpyong(79.6)

Muju PS(600)

Seocheon(400)

Boryeong CC(1,800)

Boryeong(3,000)

Taean(3,000) Tangjin

(3,000)

Pyongtaek(1,880)

Pundang (900)

Cheongpyong PS (400)

Incheon(1,150)

Youngheung(1,600)

Puchon(450)

Incheon CC(450)

SeoIncheon 3,4 (1,800)

SeoIncheon 1,2 (1,800)

Hanhwa (1,500)

Anyang(450)

Seoul (387.5)

IIsan (900)

Seoul

Incheon HPaldang

(120)

Strategically sited facilities

KOMIPO’s facilities are close to Korea’s major energy end-user marketsKOMIPO’s facilities are close to Korea’s major energy end-user markets

22

27,874

30,821

34,21735,740 35,340

37,669

2001 02E 03E 04E 05E 06E

Power generation forecast

GWh

4952

5658

56 57

39 40 40 4038

40

2001 02E 03E 04E 05E 06E

Utilization rate Thermal efficiency

Utilization and thermal efficiency forecast%

Source: Company data

Decrease due to completion of Yang

Yang hydro and Incheon CC in 2005/6

Solid operating efficiency

Going forward, efficiency is expected to increase as the new Boryeong CC increases its generation

Going forward, efficiency is expected to increase as the new Boryeong CC increases its generation

* Note that Yangyang Hydro distorts utilization rate because of its size (1,000MW). Hydro power plants do not typically operate beyond a 10% utilization rate* ‘05E and ‘06E utilization rates exclude Yang Yang

23

e-Gen planning committee was formed in Jan. 2002

Task force teams have been formed

Responsibility for repair, maintenance management and improved procurement of raw materials

In the next step, KOMIPO will appoint a consulting firm

Setup of a 2-phase Employee Information System

Development of a “one-stop” generation maintenance management system

Establishment of an integrated management system

Full electronic purchasing

Core strategic objectivese-Gen master plan

The e-Gen management strategy will integrate and optimize all management systems in operation and maintenance of power plants, mobilization of materials and fuel, power trading, and financial affairs and accounting

Solid operating efficiency

KOMIPO’s e-Gen initiative will help to catalyze further improvements in efficiency while lowering costs

KOMIPO’s e-Gen initiative will help to catalyze further improvements in efficiency while lowering costs

24

KOMIPO LNG usage

280 280 360190

660

1,210 1,2701,380

1,570

1998 1999 2000 2001¹ 2002 2003 2004 2005 2006

Thousand tons

KOMIPO bituminous coal usage

7.318.00

8.66

6.24

8.42 8.118.59

8.26 8.45

1998 1999 2000 2001¹ 2002 2003 2004 2005 2006

1 April-December 2001

LNG consumption is expected to increase as Boryeong CC comes onstream

Competitive, low-cost fuel

supply

KOMIPO’s fuel requirements are expected to grow steadily as generation capacity increases

KOMIPO’s fuel requirements are expected to grow steadily as generation capacity increases

KOMIPO anthracite coal usage

1.000.87 0.81 0.85 0.88 0.85 0.82 0.80 0.78

1998 1999 2000 2001¹ 2002 2003 2004 2005 2006

Million tons Million tons

KOMIPO heavy oil/crude petroleum usage

203 185

270320

432 436 418 412 418

1998 1999 2000 2001¹ 2002 2003 2004 2005 2006

Thousand kL

25

Source: Company reports

Comparison of operating expenses (1H 2002)

% of sales

Competitive, low-cost fuel

supply

KOMIPO’s active fuel supply management provides a cost advantage over the other thermal gencos

KOMIPO’s active fuel supply management provides a cost advantage over the other thermal gencos

Bituminous coal. Fuel procurement strategy takes advantage of current market dynamics and the projected industry cycle to lock in fuel prices at low prices

Anthracite coal. Determined by the Korean government

Oil. Calculated as FOB (linked to the spot market price) + an additional bid cost, determined quarterly through a competitive contract

LNG. Procured from KOGAS through a long-term contract

KOMIPO minimizes fuel supply risk by diversifying suppliers, daily verifying inventory volume and imposing penalties on short supply

26

6,474

6,7326,765

6,839

6,920

KO

MIP

O

KO

SPO

KO

WEPO

KEW

ES

PO

KO

SEPC

O

Procurement cost per Gcal Jan-Jul 2002Bituminous coalKRW/Gcal

The fuel purchase price of each company depends on its purchasing techniques and experience. The keys to success are timing and volume

KOMIPO has a demonstrated competitive advantage in fuel supply management. In 2001, the company enjoyed the second-lowest unit cost of generation (KRW7,300/Gcal, versus KOWEPO’s KRW7,290/Gcal)

In 2002, KOMIPO has secured the lowest fuel purchase prices overall

For 2003, KOMIPO has already secured 1,320,000 metric tons of coal at low market prices

Competitive, low-cost fuel

supply

As a result, KOMIPO enjoys the lowest variable unit cost of generation among the thermal gencos

As a result, KOMIPO enjoys the lowest variable unit cost of generation among the thermal gencos

27

KEPCO experience. KOMIPO has a large proportion of former KEPCO specialists

Recognized leadership. KOMIPO represents the gencos on 10 committees out of a total of 14 committees, including the genco expense evaluation committee and transmission fee committee

Innovation. KOMIPO was the first genco to develop a settlement program for power trading

Location advantages. KOMIPO is highly sought after due to its plant locations

Management commitment. KOMIPO is focused on human resource development: by providing overseas

exposure or spot study opportunities to junior resources

KOMIPO subsidizes 50% of the total tuition for selected workers who go to business school

Attracting and retaining talent

Exceptional experience

KOMIPO will capitalize on its understanding of power market dynamics as it models power demand, supply and its own bidding strategy

Quality of personnel

KOMIPO’s experienced personnel are a key advantage as it forms its prepares for increased market deregulation

KOMIPO’s experienced personnel are a key advantage as it forms its prepares for increased market deregulation

28

Training

Internal External

Collective training

On-site training

Rotational training

Domestic

Abroad

Central Training Center Generation Training Center Specialist Training Agencies

Orientation Training

Personal Development

Training

Strategy/ Management

Training

Cultivation of Core Specialists

Working Level Specialist Training

New employees Senior

employees– New junior

managers– New mid-level

managers

Management strategy

Organizational culture

Understanding reform

Business management

Quality management

Manager course

Business management

Labor-management relations

Power exchange Financial

management Project

management

Senior management

General employees

Functional employees

Government employees

E-learning– Job– Language– Others

Quality of personnel

KOMIPO aims to cultivate its human resource competitiveness through its training system KOMIPO aims to cultivate its human resource competitiveness through its training system

29

KOMIPO hopes to further build upon its competitive advantages going forwardKOMIPO hopes to further build upon its competitive advantages going forward

•Strengthening management analyses for efficient resource allocation

•Strengthening management analyses for efficient resource allocation

•Managing new capacity construction

•Managing new capacity construction

•Focusing on negotiating lower prices

•Focusing on negotiating lower prices

•Leverage experienced personnel in TWBP preparation

•Leverage experienced personnel in TWBP preparation

Robustdemand for power

Quality of personnel

Strategicallysited

facilities

Attractivebase load/peak load

mix

Solid operatingefficiency

Competitive, low-cost fuel

supply

• Improved understanding of industry demand for TWBP

• Improved understanding of industry demand for TWBP

• Improving maintenance programs and shutdowns

• Improving maintenance programs and shutdowns

30

AgendaAgenda

Executive summary

KOMIPO overview

Key profit drivers and KOMIPO advantages

Assessment of deregulation and privatizationAssessment of deregulation and privatization

Robust financial profile

31

Wholesale market

Discos

Retail

Market regulation

Gencos

Phase I Phase II Phase III Phase IV

1999 2001 2004 2009

Preparation of Cost Based Pool (“CBP”)

Establishment of KPX Launch of CBP Preparation of Two-

way Bidding Pool (“TWBP”)

Launch of TWBP Vesting contracts

Separation of assets into Gencos

Separation of Gencos effective

First phase of Genco sales program

Second phase of Genco sales program

Establishment of separate distribution companies

Disco sales program Continuation of Disco sales program (if not completed in Phase III)

Implementation of new T&D tariff

Full fledged retail competition

Establishment of KOREC

Introduction of retail competition

Necessary legislation enacted

Note: KOREC: Korean Electricity Commission KPX: Korea Power ExchangeCBP: Cost Based PoolTWBP: Two-way Bidding Pool

The electricity industry restructuring plan will introduce competition in the power sector

The electricity industry restructuring plan will introduce competition in the power sector

32

Forecast and management of new capacity

Power industry growth projections are detailed in the First Basic Plan. KOMIPO makes its own plans/forecasts accordingly, which are reviewed every two years

The decision to construct new facilities at Incheon and Yang Yang was decided by KEPCO. In contrast, KOMIPO independently decided to build Boryeong #7 and #8, and #9 and #10 are under consideration

Prepare for Two-Way Bidding Pool

KOMIPO believes that the key to successful bidding is the ability to understand and forecast system demand under a competitive pool market

The Electricity Supply/Demand Comprehensive System is being adjusted for the TWBP

KOMIPO team members include members formerly from the KEPCO forecasting team

Expectations on vesting contracts

Prepare for large-scale contracts with customers in the next 3-5 years Vesting contracts will be enacted as a transition toward an open and stable

market. Volume and price of vesting contracts will be determined in 2003, and vesting contracts are expected to go into effect April 2004. Vesting contracts will initially account for about 95% of sales, then gradually decline as they are phased out by 2009

Key next steps

KOMIPO has begun to prepare for the next stage of industry deregulationKOMIPO has begun to prepare for the next stage of industry deregulation

33

AgendaAgenda

Executive summary

KOMIPO overview

Key profit drivers and KOMIPO advantages

Assessment of deregulation and privatization

Robust financial profile

34

KOMIPO base case financial projections (2002-2006)

Stable revenues Healthy margins Low gearing High liquidity

8.711.416.818.3

31.420

02F

2003

F

2004

F

2005

F

2006

F

35.134.83636.4

39.5

2002

F

2003

F

2004

F

2005

F

2006

F

0.31

0.79

0.47 0.500.37

2002

F

2003

F

2004

F

2005

F

2006

F

0.70

0.640.660.65

0.62

2002

F

2003

F

2004

F

2005

F

2006

F

Revenue growth%

1.98

1.571.79 1.82 1.85

2002

F

2003

F

2004

F

2005

F

2006

F

RevenueKRW tr

EBITDA margin%

EBITDAKRW tr

Total debt/capital%

DebtKRW tr

7.1

13.6 15.017.3

21.2

2002

F

2003

F

2004

F

2005

F

2006

F

EBITDA interest coveragex

13.8

1.7 1.8

N.A. 6.9

2002F

2003F

2004F

2005F

2006F

5.0

9.611.0

12.5 13.2

2002

F

2003

F

2004

F

2005

F

2006

F

EBIT interest coveragex

KOMIPO’s solid financials are expected to rapidly strengthen further over the near term

KOMIPO’s solid financials are expected to rapidly strengthen further over the near term

35

KOMIPO base case financial projections (2002-2006)

Key underlying assumptionsKey underlying assumptions

2002E 2003E 2004E 2005E 2006E

Inputs

Revenue growth 13.6% 1.7% 1.8% 6.9%

Fuel costs (% of revenues) 46.6% 51.2% 51.9% 52.0% 52.5%Personnel costs (% of revenues) 4.4% 3.4% 3.5% 3.6% 3.6%Retirement provisions(% of revenues)

0.4% 0.3% 0.3% 0.3% 0.3%

Depreciation (% of revenues) 11.8% 10.7% 9.4% 9.6% 13.1%Maintenance and repair(% of revenues)

5.0% 5.0% 4.5% 5.2% 4.6%

Interest expense (% of revenues) 2.8% 0.8% 0.5% 0.5% 0.5%Other expenses (% of revenues) 4.0% 3.2% 3.3% 3.5% 3.1%

Tax rate 29.70% 29.70% 29.70% 29.70% 29.70%

36

Debt/capital

Below 30% (currently 38%)1

EBITDA interest coverage

Above 10.0 x (currently 6.1x)1

Return on equity

Above 10.5% (currently 18.4%)1

Key financial targets

KOMIPO believes its business profile can support a conservative financial policyKOMIPO believes its business profile can support a conservative financial policy

1 As of June 30, 2002

37

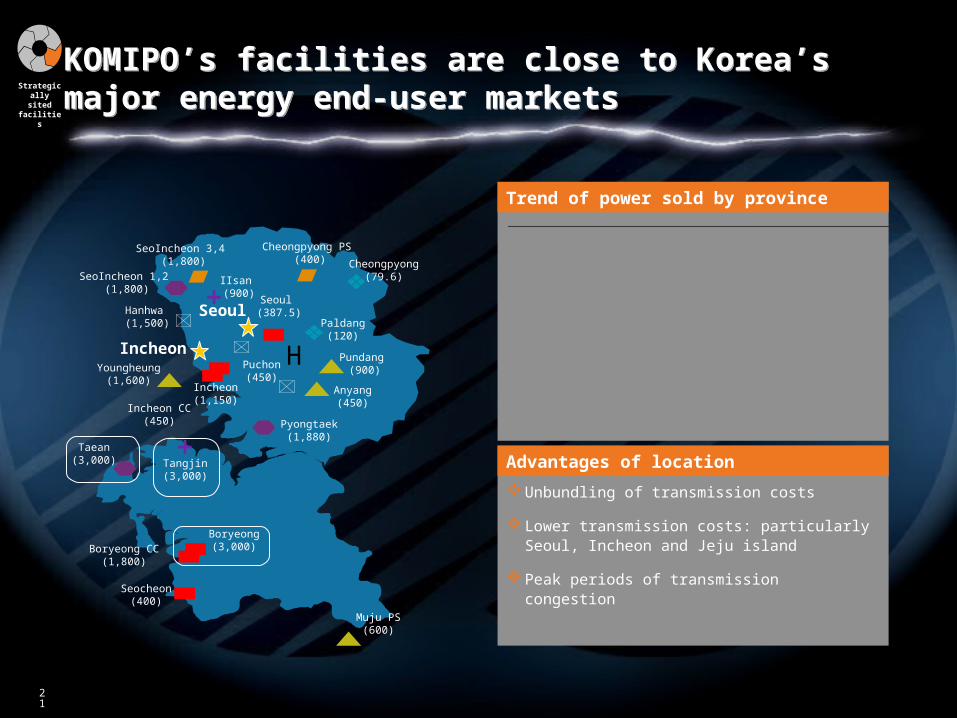

KRW mm

2002E 2003E 2004E 2005E 2006E

Inputs

Boryeong CC 58,300 14,400 - - -Incheon CC 1,500 27,472 204,300 54,100 -Kunjang site 16,500 - - - -Yangyang pumped storagepower plant

88,800 116,230 152,600 61,100 44,900

Boryeong #7, #8 700 7,891 82,900 167,400 333,700Total new construction 165,800 165,993 455,200 282,600 378,600

Facility maintenance/ repair 45,100 29,100 46,000 17,400 20,800Other 9,200 8,200 7,500 7,500 7,600Total operating investment 54,300 37,300 53,500 24,900 28,400

Total investment 220,100 203,293 508,700 307,500 407,000

EBITDA 621,854 651,643 656,259 644,995 695,122Net income from operations 280,681 380,024 413,285 402,250 395,485

CAPEX and investment planCAPEX and investment plan

KOMIPO will remain free cash flow positive over the medium-term

38

KRW mm

2002E 2003E 2004E 2005E 2006E

InputsTotal revenue 1,595,800 1,812,749 1,843,523 1,876,724 2,005,552EBITDA 621,854 651,643 656,259 644,995 695,122D&A 187,832 193,302 172,393 180,929 262,015EBIT 434,022 458,341 483,865 464,066 433,107Gross interest expense 87,644 47,964 43,881 37,210 32,801Income tax expense 118,581 160,550 174,602 169,941 167,083Net income from operations 280,681 380,024 413,285 402,250 395,485

Total debt 788,891 466,825 498,859 368,593 306,059Shareholders' equity 1,725,500 2,015,100 2,306,500 2,563,600 2,773,400Total capitalization 2,704,700 2,688,900 3,034,400 3,170,500 3,328,200

Credit statisticsEBIT Interest coverage 5.0 9.6 11.0 12.5 13.2EBITDA Interest coverage 7.1 13.6 15.0 17.3 21.2FFO / total debt 59.4% 122.8% 117.4% 158.2% 214.8%EBIT Return on capital 17.3% 18.0% 16.3% 14.4% 12.3%EBITDA margin 39.5% 36.4% 36.0% 34.8% 35.1%Debt/capital 31.4% 18.3% 16.8% 11.4% 8.7%

Key financial data and credit statisticsKey financial data and credit statistics

39

AAA

AA

A

Business and financial profiles of generation companies

Belowaverage

Average

Strong

Strong Average Below average

Financial profile

Business profile

TransAlta New Zealand Ltd. KHNP KEPCO

Singapore Power Ltd.

A

BB

AA

BBB

BBB

A

Chugoku Electric Power Co. Inc.

Manila Electric Co. National Power Corp.

Tenaga Nasional Berhad

Chubu Electric Power Co. Inc. Tokyo Electric Power Co. Inc. Taiwan Power Co.

SPI PowerNet Pty Ltd. Australian Gas Light Co. (The) Hongkong Electric Co. Ltd. CLP Power Hong Kong Ltd.

EGAT

Huaneng Power International Inc.

KOSPO KEWESPO KOWEPO

KOMIPO

KOMIPO believes that its financial profile, driven by strong operations, is a key differentiating factor

KOMIPO believes that its financial profile, driven by strong operations, is a key differentiating factor

40

Thank you

We thank S&P for taking the time to understand our financial and business profileWe thank S&P for taking the time to understand our financial and business profile