Embed Size (px)

Citation preview

VOLVO CAR GROUP

FY 2017 resultS

Patrik Tolf, Deputy CFO & head of Group Finance Hans Oscarsson, Senior vice president finance & CFO

Nils Mösko, vice president & Head of investor relations

By accepting this document, the person to whom it is provided (the “Recipient”) agrees to be bound by the following obligations and limitations.

This document has been prepared and issued by Volvo Car AB (together with its subsidiaries, “Volvo Cars”).

The information contained in this document is derived from sources that have not been independently verified. Except in the case of fraudulent misrepresentation, no responsibility or liability is accepted by Volvo Cars or by any of its respective officers, employees, affiliates or agents in relation to the accuracy, completeness or sufficiency of any information contained herein or any other written or oral information made available by Volvo Cars in connection therewith or any data which any such information generates, or for any loss whatsoever arising from or in connection with the use of or reliance on this document and any such liability is expressly disclaimed. Analyses and opinions contained herein may be based on assumptions that, if altered, can change the analyses or opinions expressed. This document speaks as of the date hereof and in providing this document, Volvo Cars gives no undertaking and is under no obligation to provide the Recipient with access to any additional information or to update this document or to correct any inaccuracies in it which may become apparent. Volvo Cars’ past performance is not necessarily indicative of future results and nothing contained herein shall constitute any representation or warranty as to future performance of Volvo Cars or any security, credit, currency, rate or other market or economic measure. Nor does this document constitute a recommendation with respect to any securities.

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017

DISCLAIMER

2

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017

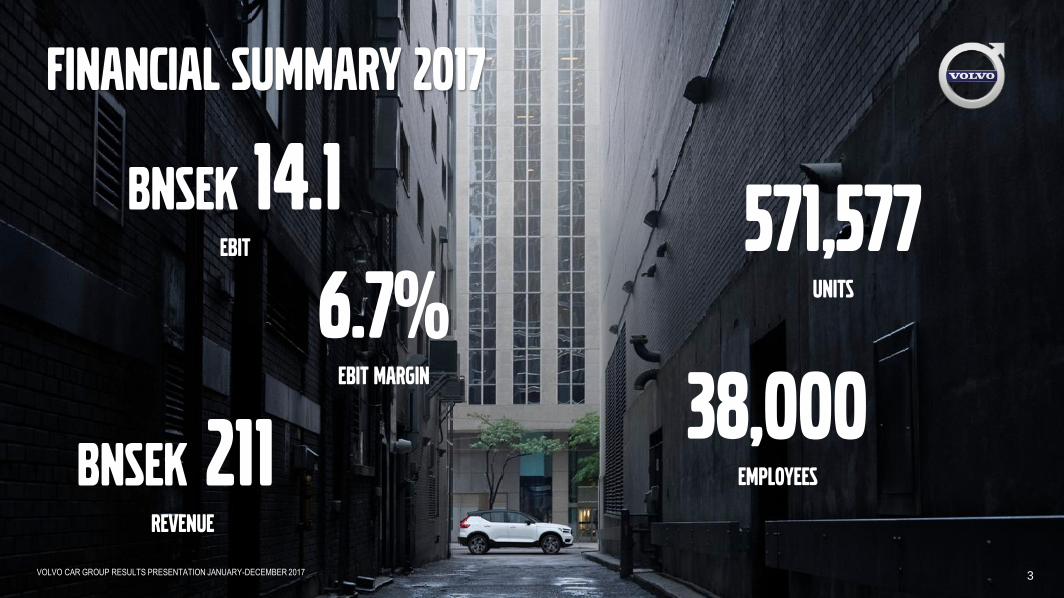

Financial Summary 2017

BNSEK 211 Revenue

BNSEK 14.1 ebit 571,577

units

6.7%Ebit margin

3

38,000EMPLOYEES

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017

Comparable period: Jan – Dec 2016

Europe is defined as EU + EFTA

US –1.5% China +25.8%

EUROPE +2.8%

Global growth +7.0%

Volvo Car Group Sales

4

2017 highlights

Torslanda plant - at full speed

S90 - worldwide export from China

Sales in China – first time over 100,000

XC40 - start of production in Gent

Clear electrification strategy – T8 sales up 30 %

Subscription model – Care by Volvo

Complete SUV line up

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017 5

Complete SUV Lineup

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017 6

Fastest growing industry segment

More than 50% of Volvo Cars’ revenue

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017

Financials

7

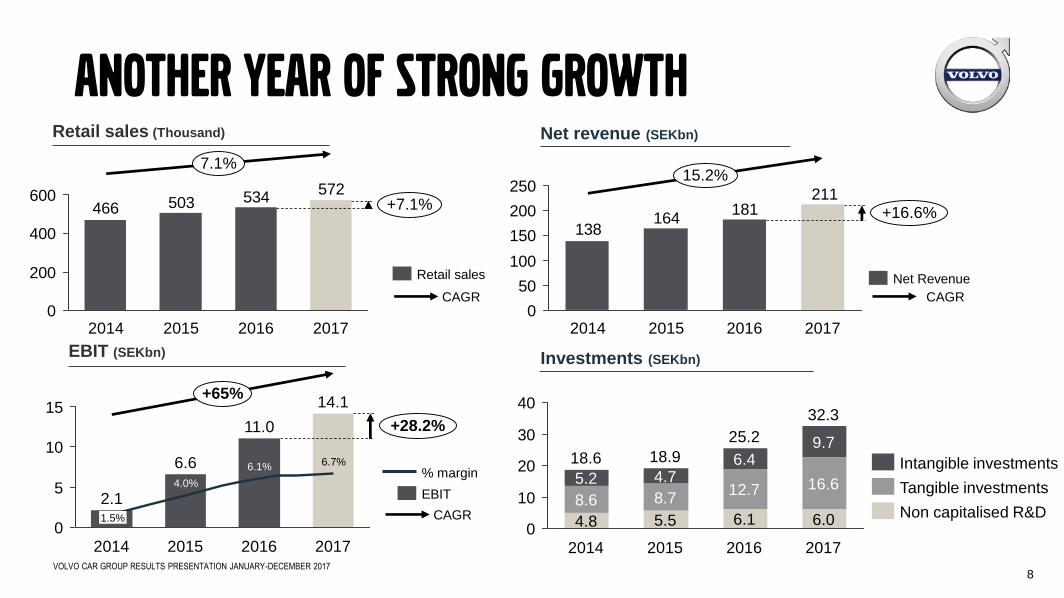

Another year of strong growthNet revenue (SEKbn)

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017

211181

164138

0

50

100

150

200

250

+16.6%

15.2%

2017201620152014

8

Net Revenue

CAGR

EBIT (SEKbn)

0

5

10

15+28.2%

+65%

2017

14.1

6.7%

2016

11.0

6.1%

2015

6.6

4.0%

2014

2.11.5%

EBIT

% margin

CAGR0

10

20

30

40

2017

32.3

6.0

16.6

9.7

2016

25.2

6.1

12.7

6.4

2015

18.9

5.5

8.7

4.7

2014

18.6

4.8

8.6

5.2

Non capitalised R&D

Tangible investments

Intangible investments

Investments (SEKbn)

Retail sales (Thousand)

CAGR

572534503466

0

200

400

600+7.1%

7.1%

2017201620152014

Retail sales

Net revenue 2017 – 17% Organic growth

9

MSEK

FY 2017

+17%211,000

Other

8,000

Sales Mix and Pricing

7,500

Volume

14,500

FY 2016

181,000

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017

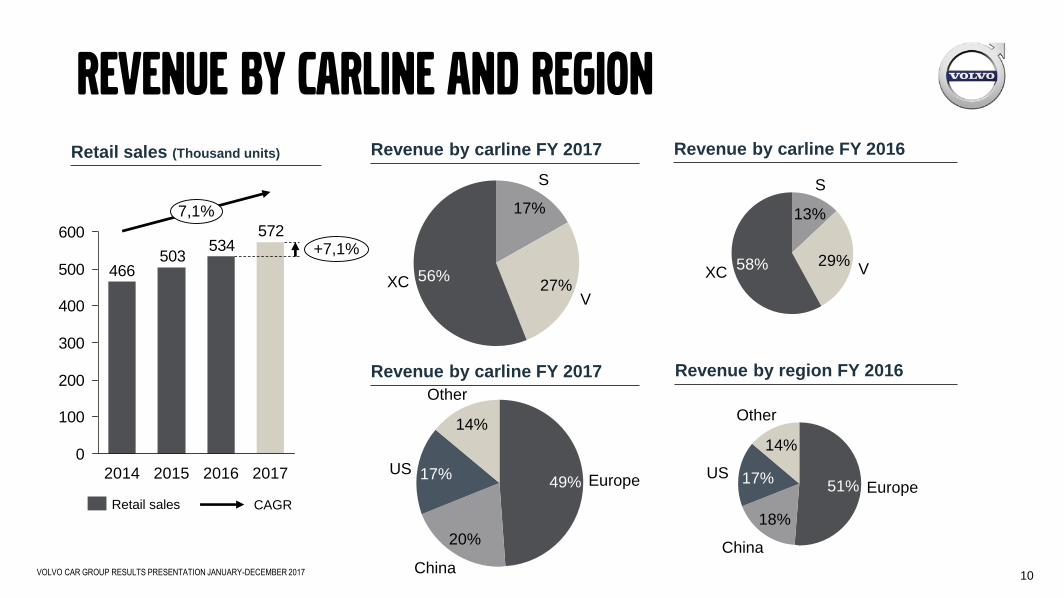

XC 56%

V27%

S

17%

49% Europe

20%

China

17%US

14%

Other

Revenue by carline FY 2017 Revenue by carline FY 2016

Revenue by carline and region

Revenue by carline FY 2017 Revenue by region FY 2016

17%

China

18%

Europe51%

14%

Other

US

XC58% V

29%

S

13%

10

Retail sales (Thousand units)

572534

503466

0

100

200

300

400

500

600+7,1%

7,1%

2017201620152014

Retail sales CAGR

ebit 2017 – 28% improvement in transition year

11

MSEK

-500

+28%

2017

14,100

Fixed cost, FX and OtherSales Mix and Pricing

-300

Volume

3,900

2016

11,000

6.1% EBIT

margin

6.7%EBIT

margin

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-JUNE 2017

Cash Flow – Investments financed

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017

* Change in inventories, accounts receivables and accounts payables, **Adjusted for interests and other items, *** Adjusted for exchange on cash

500

2017 FY Liquidity

54,600

35,400

4,000

15,200

Financing***Strategic

investments

-2,800

Operating

investments**

-24,300

Working capital*

-2,800

EBITDA

26,200

2016 FY Liquidity

49,600

38,600

4,700

6,300

CashMarketable securitiesUndrawn credit facilities

12

MSEK

Free cash flow from recurring

business MSEK -900

R&D Expenses (SEKbn)

0

2

4

6

8

10

12

8.8

5.4%

2014

7.2

2017

10.2

4.8%

2016

10.2

5.6%

2015

5.2%

R&D expenses% of Revenue

Investments (SEKbn)

13.6%

2014

18.6

4.8

8.6

5.2

25.2

6.1

12.7

6.4

13.9%

2015 2016

15.3%

9.7

18.9

5.5

8.7

4.7

11.5%

2017

6.0

32.3

16.6

Tangible investments

Non capitalised R&DIntangible investments

% of Revenue

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017 13

Investments and R&D

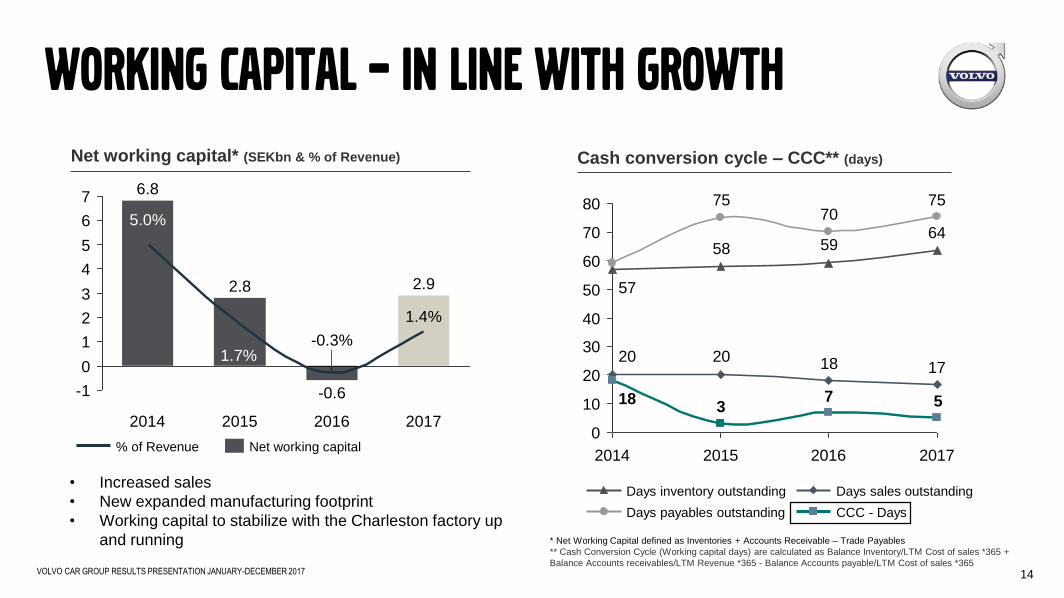

Net working capital* (SEKbn & % of Revenue)

* Net Working Capital defined as Inventories + Accounts Receivable – Trade Payables

** Cash Conversion Cycle (Working capital days) are calculated as Balance Inventory/LTM Cost of sales *365 +

Balance Accounts receivables/LTM Revenue *365 - Balance Accounts payable/LTM Cost of sales *365

Cash conversion cycle – CCC** (days)

-1

0

1

2

3

4

5

6

7

2017

2.9

1.4%

-0.6

-0.3%

2.8

1.7%

2016

6.8

5.0%

20152014

Net working capital% of Revenue

645958

57

7570

75

17182020

573

18

0

10

20

30

40

50

60

70

80

2014 2015 2016 2017

CCC - Days

Days sales outstanding

Days payables outstanding

Days inventory outstanding

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017 14

Working capital – in line with growth

• Increased sales

• New expanded manufacturing footprint

• Working capital to stabilize with the Charleston factory up

and running

Liquidity & debt – comfortable net cash position

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017

27,700

Debt

26,900

6,700

7,400

12,800

Liquidity

54,600

35,400

4,000

15,200

12,500

Short-term Debt

Bonds

Long-term Debt

Cash & Cash Equivalents

Marketable Securities

Undrawn Credit Facilities

MSEK

Net cash position of SEK 12,5bn

(2016 SEK18.9bn)

15

Balanced Amortisation schedule

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017

5,800

1,200

2017

Dec 31

54,600

4,900

1,800

2020

3,000

2019

7,000

1,450

6,700

2018

4,900

3,000

202520222021

Repayment of CDB EUR loanLoansLiquidity Bonds

MSEK

16

51% 49% BondsLoans

Funding by type

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017 17

Looking ahead

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017 18

Volvo Car Group

Volvo Cars Polestar Zenuity Lynk & CoSubscription

Business

Outlook 2018

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017 19

Further sales progress - complete SUV line up

New disruption business opportunities

Complete product portfolio renewal

Truly global manufacturing footprint

Continued strong growth and improved profits

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017

Questions

20

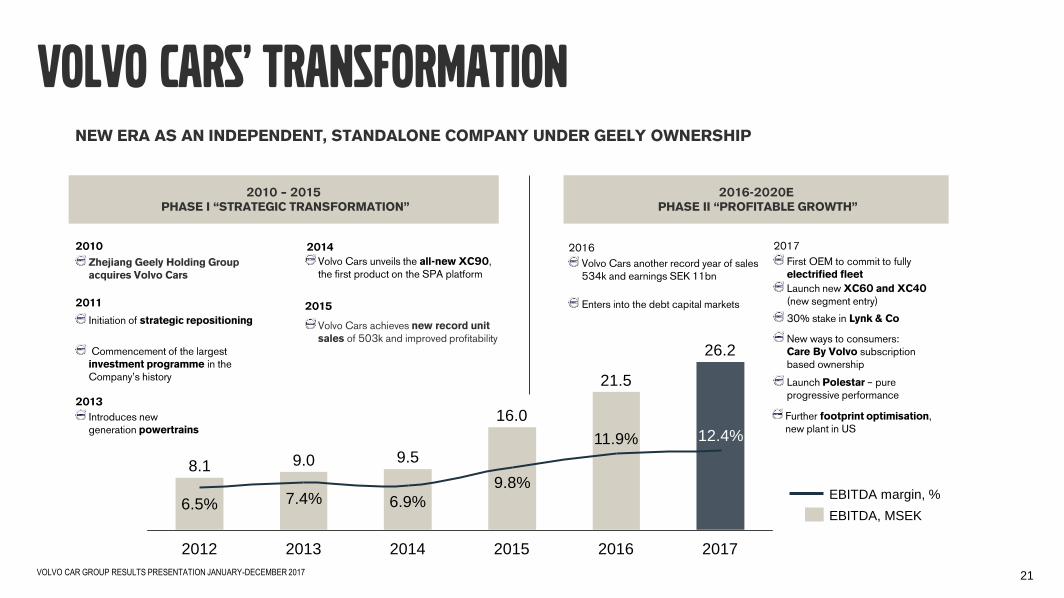

NEW ERA AS AN INDEPENDENT, STANDALONE COMPANY UNDER GEELY OWNERSHIP

Zhejiang Geely Holding Group acquires Volvo Cars

2010

2013

Volvo Cars unveils the all-new XC90, the first product on the SPA platform

2014

Volvo Cars achieves new record unit sales of 503k and improved profitability

2015

Further footprint optimisation, new plant in US

Initiation of strategic repositioning

Commencement of the largest investment programme in the Company’s history

2011

2010 – 2015PHASE I “STRATEGIC TRANSFORMATION”

2016-2020EPHASE II “PROFITABLE GROWTH”

Introduces new generation powertrains

2016

Volvo Cars another record year of sales 534k and earnings SEK 11bn

Enters into the debt capital markets

Launch Polestar – pure progressive performance

Launch new XC60 and XC40 (new segment entry)

2017

First OEM to commit to fully electrified fleet

New ways to consumers:Care By Volvo subscription based ownership

30% stake in Lynk & Co

Volvo Cars’ Transformation

2017

26.2

12.4%

2016

21.5

11.9%

2015

16.0

9.8%

2014

9.5

6.9%

2013

9.0

7.4%

2012

8.1

6.5%EBITDA margin, %

EBITDA, MSEK

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017 21

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017

Jan-Dec

2017 total

Working

Capital

-2,800

Payables

8,200

Receivables

-1,500

Inventory

-9,500

2017

Dec 31

5.0

Payables

-5.4

Receivables

-1.2

Inventory

4.6

2016

Dec 31

7.0

Change in Working capital (MSEK) 12 months rolling CCC* days

Appendix 1:

Working Capital and CCC days

22

* Cash Conversion Cycle (Working capital days) are calculated as Balance Inventory/LTM Cost of sales *365 +

Balance Accounts receivables/LTM Revenue *365 - Balance Accounts payable/LTM Cost of sales *365

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017

Appendix 2:

Number of employees

23

* Cash Conversion Cycle (Working capital days) are calculated as Balance Inventory/LTM Cost of sales *365 +

Balance Accounts receivables/LTM Revenue *365 - Balance Accounts payable/LTM Cost of sales *365

Number of employees* (Thousand)

30.000

10.000

20.000

0

5.000

25.000

15.000

40.000

35.000

13,5%

2017

+25,0%

38.000

26.00028.100

2014 2015

30.400

2016

Sweden

Other

China

Americas

Europe, other

CAGR

Appendix 3:

Retail sales

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017 24

Appendix 4:

Key figures

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017 25

Appendix 5:

Definitions of performance measures

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017 26

Appendix 6:

Reconciliation tables of performance measures

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017 27

Appendix 7:

Reconciliation tables of performance measures contd.

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017 28

VOLVO CAR GROUP RESULTS PRESENTATION JANUARY-DECEMBER 2017 29