Embed Size (px)

Citation preview

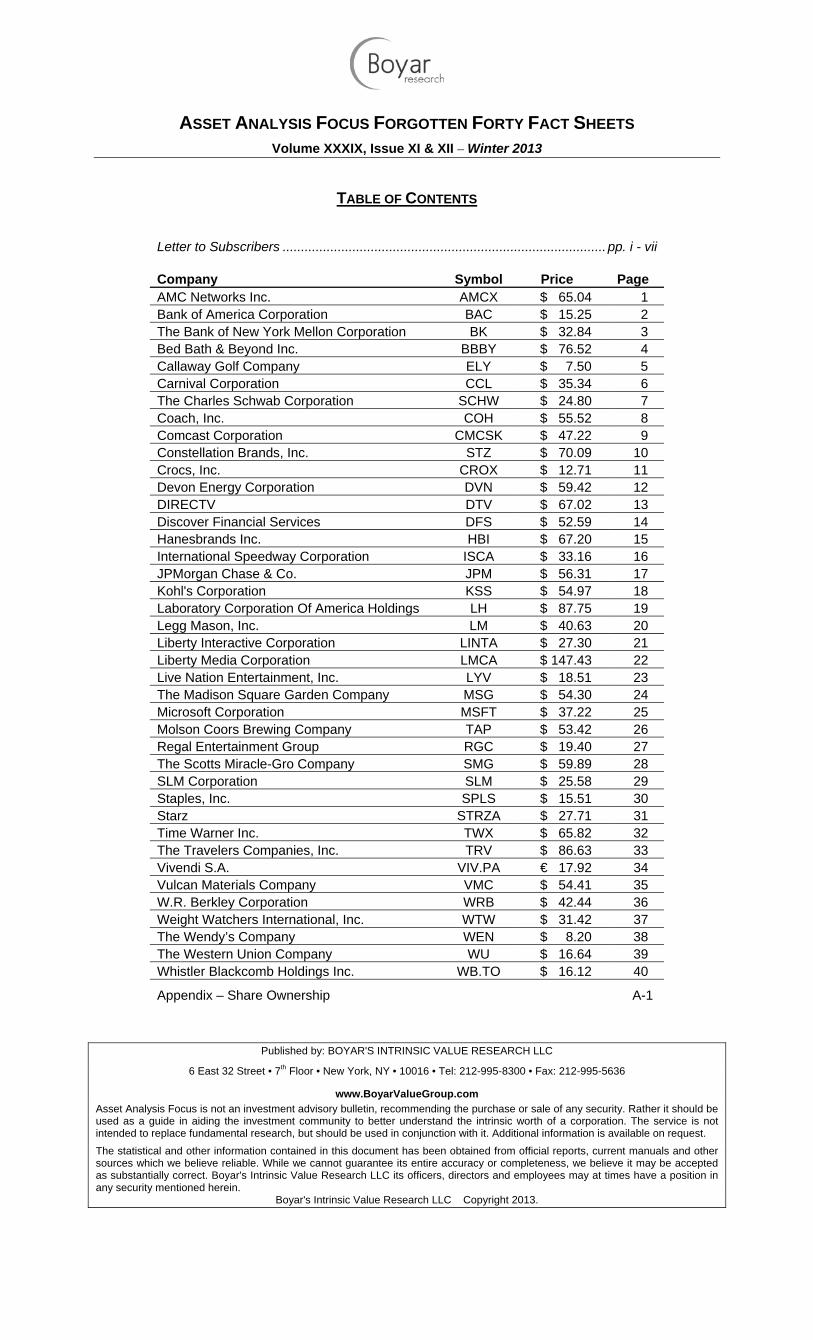

ASSET ANALYSIS FOCUS FORGOTTEN FORTY FACT SHEETS

Volume XXXIX, Issue XI & XII – Winter 2013

TABLE OF CONTENTS

Letter to Subscribers ........................................................................................ pp. i - vii

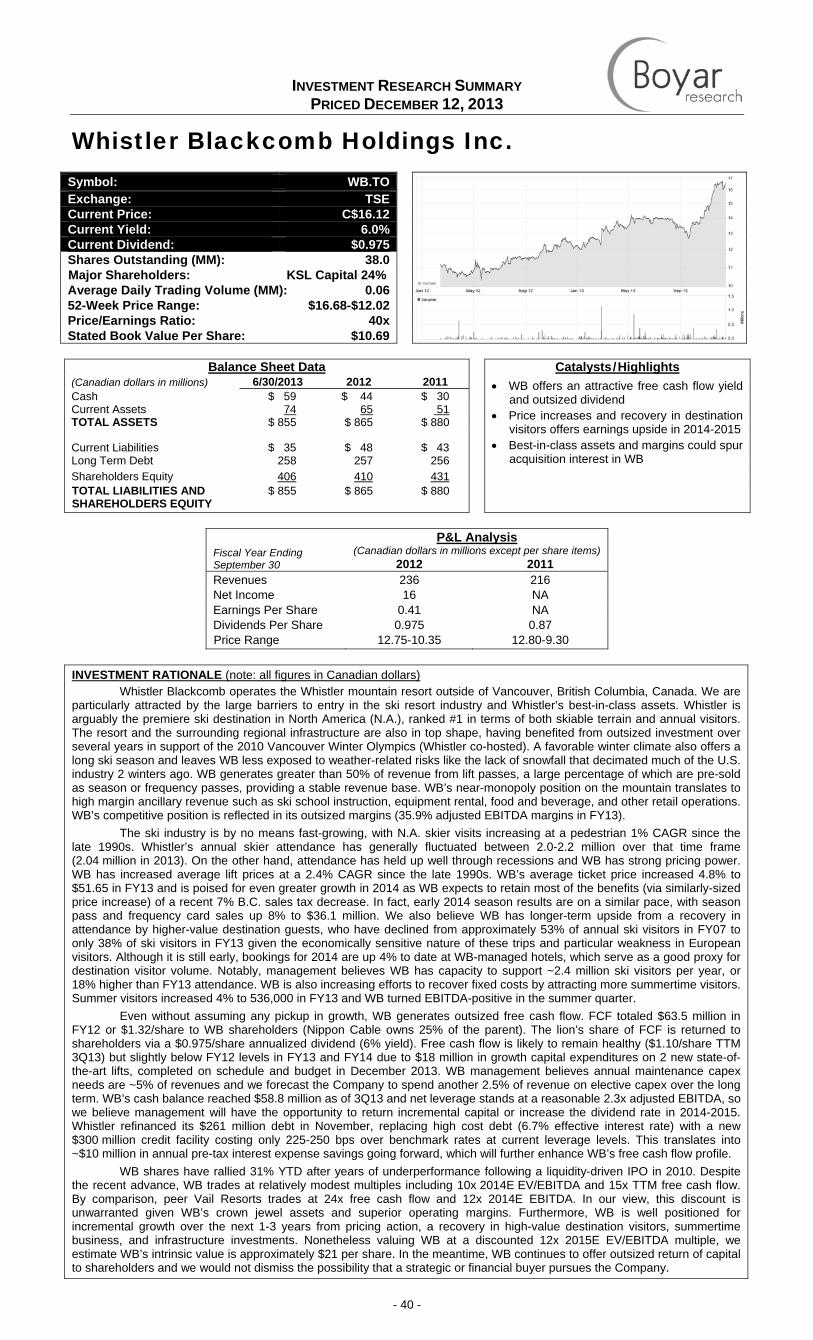

Company Symbol Price Page AMC Networks Inc. AMCX $ 65.04 1 Bank of America Corporation BAC $ 15.25 2 The Bank of New York Mellon Corporation BK $ 32.84 3 Bed Bath & Beyond Inc. BBBY $ 76.52 4 Callaway Golf Company ELY $ 7.50 5 Carnival Corporation CCL $ 35.34 6 The Charles Schwab Corporation SCHW $ 24.80 7 Coach, Inc. COH $ 55.52 8 Comcast Corporation CMCSK $ 47.22 9 Constellation Brands, Inc. STZ $ 70.09 10 Crocs, Inc. CROX $ 12.71 11 Devon Energy Corporation DVN $ 59.42 12 DIRECTV DTV $ 67.02 13 Discover Financial Services DFS $ 52.59 14 Hanesbrands Inc. HBI $ 67.20 15 International Speedway Corporation ISCA $ 33.16 16 JPMorgan Chase & Co. JPM $ 56.31 17 Kohl's Corporation KSS $ 54.97 18 Laboratory Corporation Of America Holdings LH $ 87.75 19 Legg Mason, Inc. LM $ 40.63 20 Liberty Interactive Corporation LINTA $ 27.30 21 Liberty Media Corporation LMCA $ 147.43 22 Live Nation Entertainment, Inc. LYV $ 18.51 23 The Madison Square Garden Company MSG $ 54.30 24 Microsoft Corporation MSFT $ 37.22 25 Molson Coors Brewing Company TAP $ 53.42 26 Regal Entertainment Group RGC $ 19.40 27 The Scotts Miracle-Gro Company SMG $ 59.89 28 SLM Corporation SLM $ 25.58 29 Staples, Inc. SPLS $ 15.51 30 Starz STRZA $ 27.71 31 Time Warner Inc. TWX $ 65.82 32 The Travelers Companies, Inc. TRV $ 86.63 33 Vivendi S.A. VIV.PA € 17.92 34 Vulcan Materials Company VMC $ 54.41 35 W.R. Berkley Corporation WRB $ 42.44 36 Weight Watchers International, Inc. WTW $ 31.42 37 The Wendy’s Company WEN $ 8.20 38 The Western Union Company WU $ 16.64 39 Whistler Blackcomb Holdings Inc. WB.TO $ 16.12 40

Appendix – Share Ownership A-1

Published by: BOYAR'S INTRINSIC VALUE RESEARCH LLC

6 East 32 Street • 7th Floor • New York, NY • 10016 • Tel: 212-995-8300 • Fax: 212-995-5636

www.BoyarValueGroup.com Asset Analysis Focus is not an investment advisory bulletin, recommending the purchase or sale of any security. Rather it should be used as a guide in aiding the investment community to better understand the intrinsic worth of a corporation. The service is not intended to replace fundamental research, but should be used in conjunction with it. Additional information is available on request. The statistical and other information contained in this document has been obtained from official reports, current manuals and other sources which we believe reliable. While we cannot guarantee its entire accuracy or completeness, we believe it may be accepted as substantially correct. Boyar's Intrinsic Value Research LLC its officers, directors and employees may at times have a position in any security mentioned herein.

Boyar's Intrinsic Value Research LLC Copyright 2013.

MMAARRKK AA.. BBOOYYAARR

6 EAST 32ND STREET 7TH FLOOR NEW YORK, NY 10016 (212) 995-8300 FAX: (212) 995-5636

WWW.BOYARVALUE.COM

“The outstanding characteristics of financial markets are shortness of memory and ignorance of history.”

– John Kenneth Galbraith

A Look Back at Our 2013 Predictions

1) Revisiting the Fiscal Cliff As we anticipated, the “kick the can” approach to the federal budget crisis continued in

2013 with several partial budget acts and temporary debt ceiling extensions culminating in the September-October fiasco and partial government shutdown. Another 3-month extension was passed in October, although Congress is reportedly closer to reaching a “long term” (i.e. 2-year) solution just in time for winter recess. On the other hand, our prediction that the stock market would continue to weather any short-term federal budget related setbacks also came true. The S&P 500 barely reacted to the 2013 budget crises and has continued its ascent to all-time highs.

2) Investors Continue to Shun Equities for Bonds We have been highlighting the potential bubble in the bond market for some time now,

and this was among the issues we raised in our 2013 Forgotten Forty predictions. The historic shift from equities to bonds was large and extended in scope, reflecting lingering investor anxiety created by the market volatility of recent years. After examining the overall market landscape in 2013 and the robust performance of equities, it appears this heavy emphasis on fixed income is beginning to abate. Certainly, a second year of double-digit appreciation of the S&P 500 helps to illustrate the change in investor sentiment. Importantly, the shift into equities is also illustrated by flow activity within the mutual fund industry. According to a December 2013 report by Morningstar, overall equity funds have received $198 billion in net inflows during 2013 (through the end of November), positioning the equity fund industry to realize its best year since 2000. Conversely, year-to-date outflows from bond mutual funds have exceeded $70 billion, and are projected to realize their first year of net outflows in roughly a decade. These respective fund flow figures reflect an important new reality: Retail investors are shifting their assets back into the equity market again, and this may be just the beginning.

3) Geopolitical Uncertainty In last year’s edition we observed that the world continued to be a scary place in terms

of geopolitical stock market risk. There was the danger/uncertainty of escalating tensions between China and Japan, regime change in Venezuela, and European economic malaise. We noted however, as value investors it is important to ignore the “noise” and focus on individual companies’ business fundamentals. Investors would have been wise to heed our advice as the U.S. stock market continued its upward trajectory despite the above-referenced issues, as well as continued conflict in the Middle East, the constant talk of a “taper,” and other ugly headlines that make you want to hoard cash. So to quote again from Warren Buffett’s 2008 Op-Ed that appeared in the New York Times (we quoted from a different section of this same piece in last year’s edition of The Forgotten Forty):

“Let me be clear on one point: I can’t predict the short-term movements of the stock market. I haven’t the faintest idea as to whether stocks will be higher or lower a month — or a year — from now. What is likely, however, is that the market will move higher, perhaps substantially so, well before either sentiment or the economy turns up. So if you wait for the robins, spring will be over.”

4) Dividend Paying Stocks In last year’s Forgotten Forty we noted that even though many pundits believed the tax

on dividends would increase in 2013, high dividend payers, as measured by the Vanguard Dividend Appreciation ETF, outperformed the S&P 500 as a whole from the period immediately following the U.S. presidential election through last year’s Forgotten Forty publication date. We speculated that the outperformance was caused in part by companies issuing dividends early or declaring onetime special dividends to combat the tax uncertainty in Washington. In 2013 that trend has reversed itself and that same ETF advanced approximately 22% this year, underperforming the S&P by about 300 basis points. That trend also demonstrated itself in this year’s Forgotten Forty performance as none of the top ten performing names had outsized dividend yields.

ii

5) First Year Market Performance of an Incumbent President As we mentioned in the last edition of the Forgotten Forty, market performance for the

first year of an incumbent president has been mixed from a historical perspective. Market movements were positive following the re-elections of Presidents Reagan, Clinton, and Bush (up 20% on average), while returns following the re-elections of Presidents Eisenhower and Nixon were decidedly weaker (average declines of approximately 15%). Clearly, many other factors can impact returns outside of presidential elections, but the past year has been a robust one within this political context. With a likely appreciation of well over 20% for the S&P 500 during 2013, the market performance during President Obama’s first year of his incumbency will rival some of his best performing peers of the past 50 years.

6) Where Have All the Housing Names Gone? In last year’s Forgotten Forty, we noted that while we still found the housing sector to be

somewhat inexpensive from a valuation perspective, we did not include any of the names featured in our 2011 Summer Issue detailing how to profit from an eventual U.S. housing recovery. We reasoned that while some of those names were still somewhat inexpensive, we saw better opportunities in names in ancillary sectors that would benefit from a U.S. housing recovery. We said companies like JPM, BAC, BRK, CVC, and CMCSA would be beneficiaries of a housing rebound and in our opinion were the more attractive way to participate in this particular trend. Clearly we were wrong. You would have been much better off investing in names we highlighted in our 2011 housing issue such as Whirlpool, or Mohawk that had more direct exposure to U.S. housing than the ancillary names we featured.

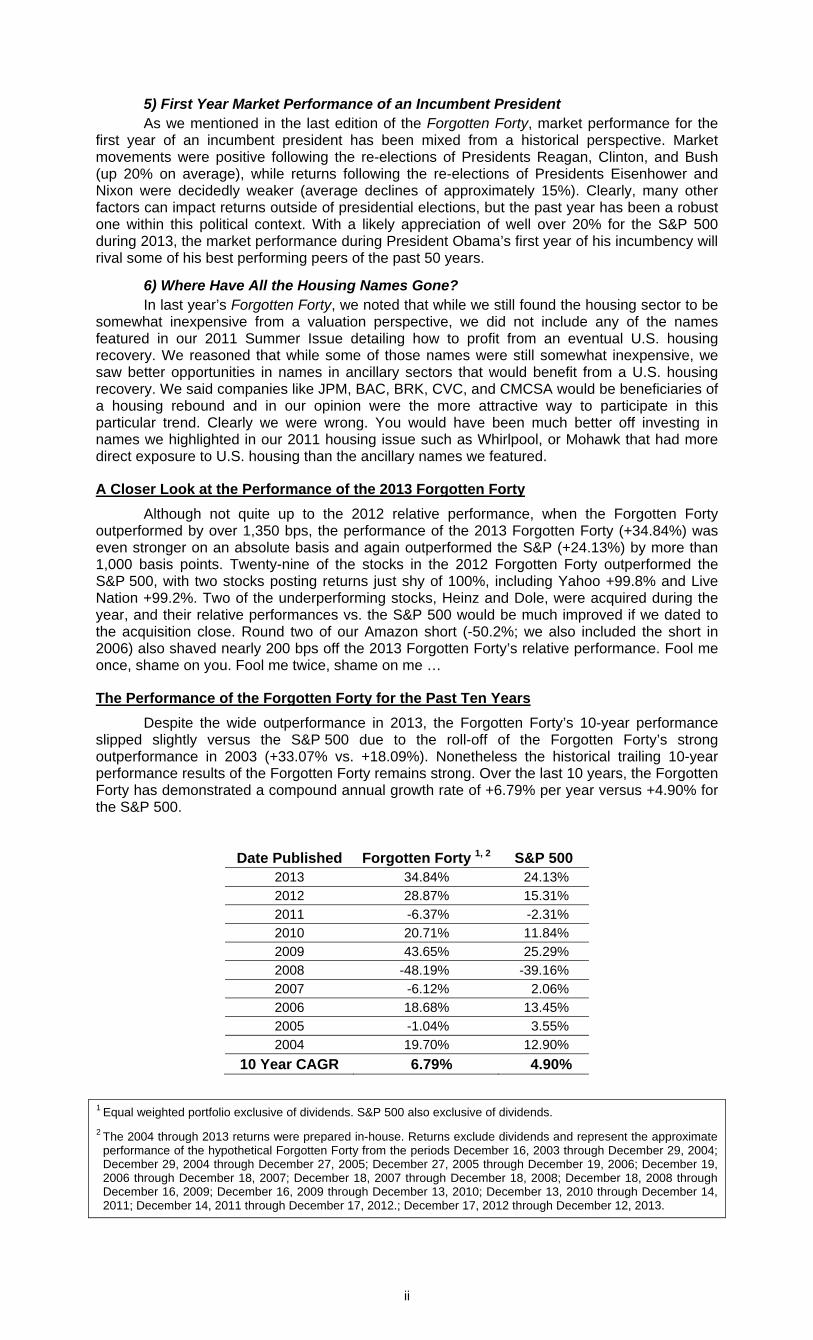

A Closer Look at the Performance of the 2013 Forgotten Forty Although not quite up to the 2012 relative performance, when the Forgotten Forty

outperformed by over 1,350 bps, the performance of the 2013 Forgotten Forty (+34.84%) was even stronger on an absolute basis and again outperformed the S&P (+24.13%) by more than 1,000 basis points. Twenty-nine of the stocks in the 2012 Forgotten Forty outperformed the S&P 500, with two stocks posting returns just shy of 100%, including Yahoo +99.8% and Live Nation +99.2%. Two of the underperforming stocks, Heinz and Dole, were acquired during the year, and their relative performances vs. the S&P 500 would be much improved if we dated to the acquisition close. Round two of our Amazon short (-50.2%; we also included the short in 2006) also shaved nearly 200 bps off the 2013 Forgotten Forty’s relative performance. Fool me once, shame on you. Fool me twice, shame on me …

The Performance of the Forgotten Forty for the Past Ten Years Despite the wide outperformance in 2013, the Forgotten Forty’s 10-year performance

slipped slightly versus the S&P 500 due to the roll-off of the Forgotten Forty’s strong outperformance in 2003 (+33.07% vs. +18.09%). Nonetheless the historical trailing 10-year performance results of the Forgotten Forty remains strong. Over the last 10 years, the Forgotten Forty has demonstrated a compound annual growth rate of +6.79% per year versus +4.90% for the S&P 500.

Date Published Forgotten Forty 1, 2 S&P 500 2013 34.84% 24.13% 2012 28.87% 15.31% 2011 -6.37% -2.31% 2010 20.71% 11.84% 2009 43.65% 25.29% 2008 -48.19% -39.16% 2007 -6.12% 2.06% 2006 18.68% 13.45% 2005 -1.04% 3.55% 2004 19.70% 12.90%

10 Year CAGR 6.79% 4.90%

1 Equal weighted portfolio exclusive of dividends. S&P 500 also exclusive of dividends. 2 The 2004 through 2013 returns were prepared in-house. Returns exclude dividends and represent the approximate

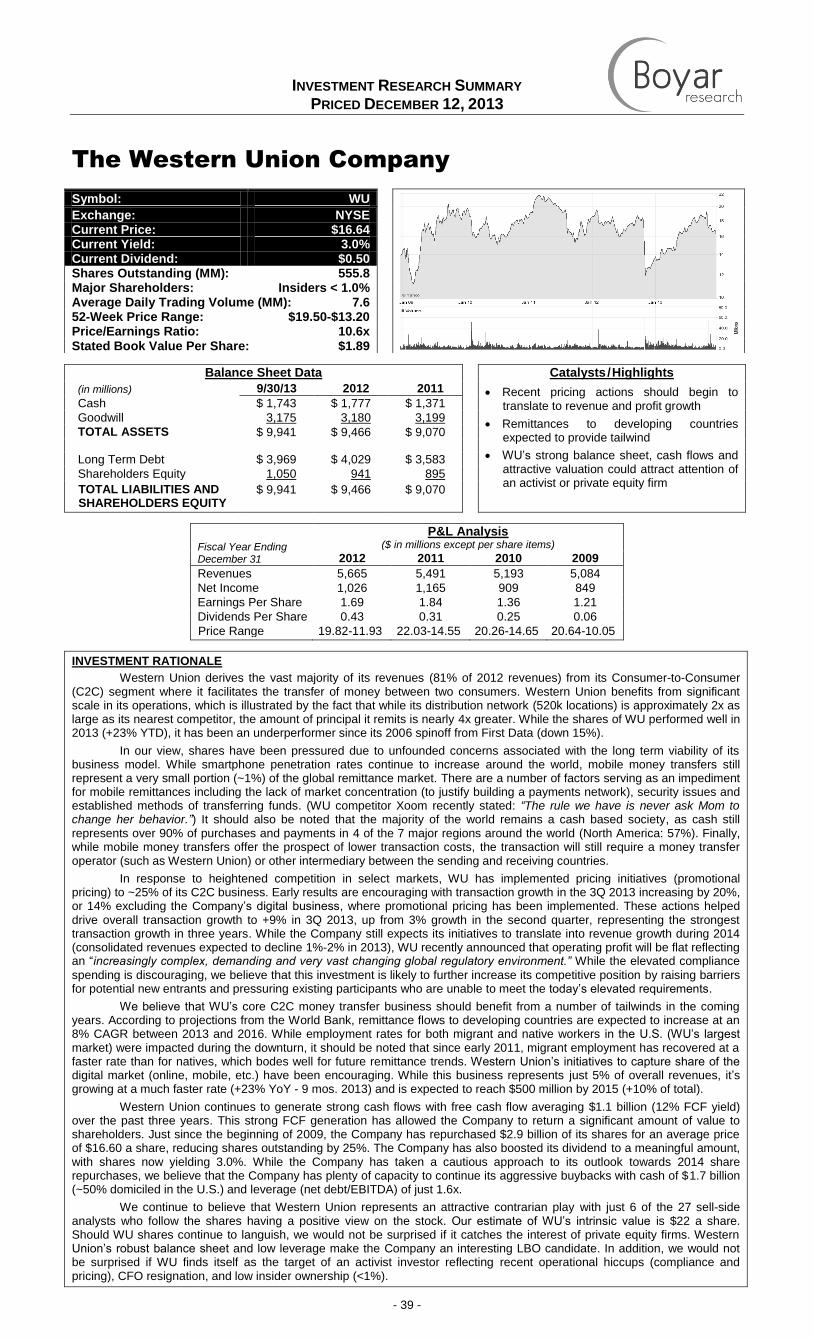

performance of the hypothetical Forgotten Forty from the periods December 16, 2003 through December 29, 2004; December 29, 2004 through December 27, 2005; December 27, 2005 through December 19, 2006; December 19, 2006 through December 18, 2007; December 18, 2007 through December 18, 2008; December 18, 2008 through December 16, 2009; December 16, 2009 through December 13, 2010; December 13, 2010 through December 14, 2011; December 14, 2011 through December 17, 2012.; December 17, 2012 through December 12, 2013.

iii

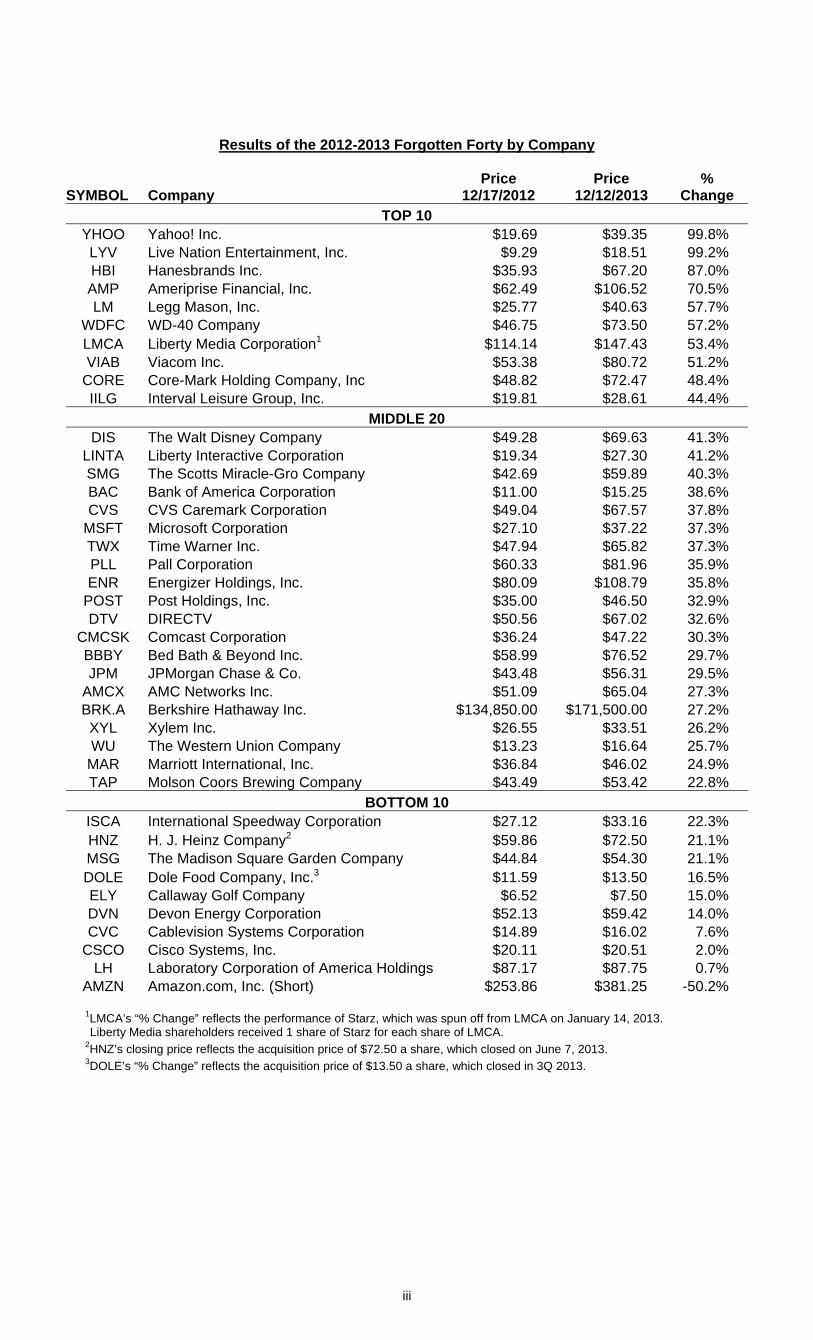

Results of the 2012-2013 Forgotten Forty by Company

SYMBOL Company Price

12/17/2012 Price

12/12/2013 %

Change TOP 10

YHOO Yahoo! Inc. $19.69 $39.35 99.8% LYV Live Nation Entertainment, Inc. $9.29 $18.51 99.2% HBI Hanesbrands Inc. $35.93 $67.20 87.0% AMP Ameriprise Financial, Inc. $62.49 $106.52 70.5% LM Legg Mason, Inc. $25.77 $40.63 57.7%

WDFC WD-40 Company $46.75 $73.50 57.2% LMCA Liberty Media Corporation1 $114.14 $147.43 53.4% VIAB Viacom Inc. $53.38 $80.72 51.2%

CORE Core-Mark Holding Company, Inc $48.82 $72.47 48.4% IILG Interval Leisure Group, Inc. $19.81 $28.61 44.4%

MIDDLE 20 DIS The Walt Disney Company $49.28 $69.63 41.3%

LINTA Liberty Interactive Corporation $19.34 $27.30 41.2% SMG The Scotts Miracle-Gro Company $42.69 $59.89 40.3% BAC Bank of America Corporation $11.00 $15.25 38.6% CVS CVS Caremark Corporation $49.04 $67.57 37.8%

MSFT Microsoft Corporation $27.10 $37.22 37.3% TWX Time Warner Inc. $47.94 $65.82 37.3% PLL Pall Corporation $60.33 $81.96 35.9% ENR Energizer Holdings, Inc. $80.09 $108.79 35.8%

POST Post Holdings, Inc. $35.00 $46.50 32.9% DTV DIRECTV $50.56 $67.02 32.6%

CMCSK Comcast Corporation $36.24 $47.22 30.3% BBBY Bed Bath & Beyond Inc. $58.99 $76.52 29.7% JPM JPMorgan Chase & Co. $43.48 $56.31 29.5%

AMCX AMC Networks Inc. $51.09 $65.04 27.3% BRK.A Berkshire Hathaway Inc. $134,850.00 $171,500.00 27.2% XYL Xylem Inc. $26.55 $33.51 26.2% WU The Western Union Company $13.23 $16.64 25.7%

MAR Marriott International, Inc. $36.84 $46.02 24.9% TAP Molson Coors Brewing Company $43.49 $53.42 22.8%

BOTTOM 10 ISCA International Speedway Corporation $27.12 $33.16 22.3% HNZ H. J. Heinz Company2 $59.86 $72.50 21.1% MSG The Madison Square Garden Company $44.84 $54.30 21.1% DOLE Dole Food Company, Inc.3 $11.59 $13.50 16.5% ELY Callaway Golf Company $6.52 $7.50 15.0% DVN Devon Energy Corporation $52.13 $59.42 14.0% CVC Cablevision Systems Corporation $14.89 $16.02 7.6%

CSCO Cisco Systems, Inc. $20.11 $20.51 2.0% LH Laboratory Corporation of America Holdings $87.17 $87.75 0.7%

AMZN Amazon.com, Inc. (Short) $253.86 $381.25 -50.2%

1LMCA’s “% Change” reflects the performance of Starz, which was spun off from LMCA on January 14, 2013. Liberty Media shareholders received 1 share of Starz for each share of LMCA.

2HNZ’s closing price reflects the acquisition price of $72.50 a share, which closed on June 7, 2013. 3DOLE’s “% Change” reflects the acquisition price of $13.50 a share, which closed in 3Q 2013.

iv

A Look Ahead

1) Where Do We Go From Here? It is hard to believe but it has been over 5 years since the collapse of Lehman Brothers.

Stocks certainly have had quite a run since that period, advancing by approximately 162%, as measured by the S&P 500 from its March 2009 lows.

Time has a way of dulling the pain from traumatic shocks such as the most recent financial crisis (making investors more risk averse, and allowing new speculative bubbles to emerge). It is clearly more difficult to find bargains today than when stocks like CBS traded for $6 per share (current price $58.17), or when Saks was trading at a $1.85 per share (recently acquired for $16 per share). For the moment (at least in our opinion), the days of six or seven baggers are over. So where do we go from here?

• The current bull market is ~57 months long; the average bull market since 1921 lasted 29 months.

• The average price increase from the bottom in the past 17 bull markets has been ~153% vs. the ~162% jump in the S&P 500 from March 9, 2009.

• The longest and strongest bull market which ended with the bursting of the tech bubble lasted 113 months and climbed 417%.

• Two of the four bull markets since 1982 have seen significantly better stock market advances than the one we are currently experiencing. As mentioned above, one bull market saw a 417% advance, and the bull market from 1982 to 1987 saw an advance of 229%.

• The average price to earnings ratio since 1999 has approximated 16.6x. The projected 2014 P/E of the S&P 500 is currently around 14.6x.

Typically bull markets come to an end following a period of extraordinary performance. As Mark Hulbert in Barron’s observed, “some of a bull market’s best returns occur right before it dies.” Remember the NASDAQ’s performance in the 4th quarter of 1999 when it advanced ~48%? The NASDAQ hit its all-time high four months later, just before the party ended. In the months leading to market tops there are striking similarities that often occur. Growth stocks outperform value stocks and small capitalization stocks outperform their larger brethren. There are early signs today that such a trend has commenced.

So let us revisit the grand daddy of all bull markets, the Internet craze and NASDAQ 5000 to see if there are any similarities with today’s richest companies in terms of stock market valuations and the leaders of that era. Bill Gates aptly once stated:

“I think the multiples of technology stocks should be quite a bit lower than the multiples of stocks like Coke and Gillette, because we are subject to complete changes in the rules. I know very well that in the next ten years, if Microsoft is still a leader, we will have to weather at least three crises.”

The magnitude of Internet stocks’ price increases and market valuations in the late 1990s dwarfed what longtime market watchers recall in previous speculative frenzies like that for biotechnology stocks in 1991. Compared with AOL’s P/E of 418, the 95x earnings Polaroid sold for in the late 1960s was a model of value investing.

Currently there are a number of companies that have captured Wall Street’s fancy, each with multiples of 100x or more. They include names like Netflix, Zillow and LinkedIn. Tesla is another example of a high multiple stock (with no current earnings). The company delivered just 1400 cars in July or about 1% of Ford Motor Company’s sales for the same month. Today Tesla commands a market valuation of ~ $18 billion. This is about 30% of Ford’s market capitalization.

Before the dot com bubble imploded, Yahoo! commanded a price multiple of more than 400x earnings. So when it purchased Mark Cuban’s fledgling Broadcast.com for $5.9 billion, the acquisition price, based on future potential, was not widely criticized. This site is now defunct and redirects to Yahoo!’s home page. Yahoo! also purchased GeoCities during that era, paying $3.65 billion for a company that is no longer in business. Did Yahoo! make the same mistake yet again? Just recently it purchased blogging site Tumblr ($13 million in sales last year) for $1.3 billion.

Although there are some early indications that the U.S. equity market is getting somewhat frothy, it could still have some more room to run. Yes, it is true the more speculative technology-laden NASDAQ and the small capitalization Russell 2000 have become the market leaders. Momentum stocks, such as Tesla (even with the recent pullback and based on forward earnings) and Netflix, each with triple-digit P/E ratios, have also become market darlings.

On the other hand during the 1990s large capitalization stocks such as Microsoft, Pfizer, Cisco and Intel commanded outsized price/earnings multiples of 40x to 150x. Today, the P/E ratios of these same companies average approximately 12x, well below the multiples of most of

v

the companies within the S&P 500. These companies also yield 3% or more, with the capability of multiple dividend increases during the next five years.

There are a number of other factors that could help continue the stock market’s advance for at least a while longer. While this report was going to press the Federal Reserve announced that it will begin a modest taper of $10 billion per month and stated it will continue to taper even more if the economy shows sustained improvement. However even after the initial tapering begins, the amount of bonds the government is buying each month is still massive. In addition, it appears as if the Federal Reserve intends to keep short-term rates low for an extended period of time. So for now it appears as if the green light is still flashing to purchase riskier assets such as stocks, but we do not know when the light will change. What gives us great concern is the violent reaction in terms of both interest rates and stock market performance that occurred in May of this year (the S&P declined by 6.3% while long-term government bonds lost approximately 6%) when the market thought the Fed would begin to taper in earnest. We do not know what will happen when the market believes the Fed is close to a significant, and what would appear to be a permanent, wind down in purchasing securities.

Until recently, individual investors had not taken the Fed’s bait. And who can blame them? Over the last decade or so they have been badly bruised by three financial bubbles bursting: First came the Internet bubble, followed by a real estate collapse of monumental proportion and finally the financial meltdown which almost destroyed the entire economic system.

Individual investors usually show up late for the party, but they usually do show up. As a result of both individual and institutional investors fleeing the equity markets en masse during the 2007-2009 period, common stocks are currently under-owned, while bonds have a much higher weighting than normally is the case. A higher asset allocation into stocks could prolong the stock market advance.

To summarize, the overall stock market is probably fairly valued. Stocks are not on the bargain basement table as they were in 2008-2009. Temper your expectations in terms of expected future returns, and be wary of momentum stocks with triple-digit P/E ratios (or no current earnings at all). A higher cash balance might also be appropriate.

2) Where to Look For Opportunities in Current Market This has certainly (at least in our view) turned into a stock picker’s market. The broad

market is not blatantly overvalued, but is close to being fairly valued. This is the hardest time to be in the investment business, as you really do not know whether you should be playing offense or defense. While the overall market may be somewhat picked over, that does not mean there are not opportunities for good old fashioned stock picking. We think turnarounds that are starting to show signs of progress (such as Callaway, which is regaining market share) are interesting places to search for investment ideas. Other potential turnarounds such as Weight Watchers that have not yet shown signs of progress, but have a significant margin of safety in terms of valuation, a great consumer franchise, and an identifiable catalyst are worth looking further into. Another example of a company that we believe presents an attractive opportunity is Carnival Cruise Lines. The Company has not participated in the broad stock market advance, is hated by Wall Street, has problems that we believe can be remedied and is looking to cut costs after being run by the son of the Company’s founder for more than three decades.

Spinoffs continue to be a fertile ground to find investment ideas. Recent spinoffs that were featured in last year’s Forgotten Forty such as LMC/Starz, AMC, and Post Holdings, significantly outperformed the market and were among the best performers in the 2012-2013 Forgotten Forty class. In 2014, we will continue to scour the market for spinoff opportunities, such as reviewing the upcoming Time Inc. spinout. Time Warner has enhanced shareholder value under Jeff Bewkes tremendously by spinning out both AOL and Time Warner Cable and repurchasing a significant amount of stock at attractive prices. Look for TWX to possibly sell their valuable NYC headquarters in 2014. It would be our “dream” that TWX will continue its spin-out spree and take advantage of the high value that the market is currently placing on Netflix and spin-out HBO. While we know of no plans for them to do this, we believe that the market would assign a premium valuation to HBO as a standalone entity.

3) IPOs and Insiders Signaling Bubbly Conditions In recent months, The Boyar Value Group has made several mentions of the sky-high

valuations attached to a certain group of new technology stocks and recent IPOs. We think it is particularly noteworthy that even the CEOs of some of these companies have recently voiced concerns with the exuberance attached to their stocks. In his 3Q 2013 letter to investors, Netflix CEO Reed Hastings compared Netflix shares’ recent performance to 2003 when “momentum-fueled investor euphoria” made Netflix the top NASDAQ performer during the year. Netflix shares went on to decline by 77% in 2004. This October, Tesla CEO Elon Musk also went so far as to say about his shares, “The stock price that we have is more than we have any right to deserve.” While long-term shareholders of some of the current high-flyers may be rewarded, we fear the ride will be too bumpy for many to stomach.

vi

In another sign of the times, there were 222 IPOs in 2013 to date, the highest number since the year 2000. This partially reflects the end result of the pre-crisis LBO boom, and IPOs are still far below the 400-500 annual count reached during the tech bubble, but recent IPO performance gives us pause. IPOs averaged a remarkable 17% first-day rise in 2013 and the Renaissance IPO Composite Index is up 59% YTD or well over 2x the S&P 500. IPOs tend to come in waves, and the recent performance could spur even more issuers next year. But while IPOs historically exhibited positive abnormal short-term returns, they also exhibit negative abnormal long-term returns. Given their unusually strong outperformance in 2013, we would remain on the sidelines with the current batch of IPOs.

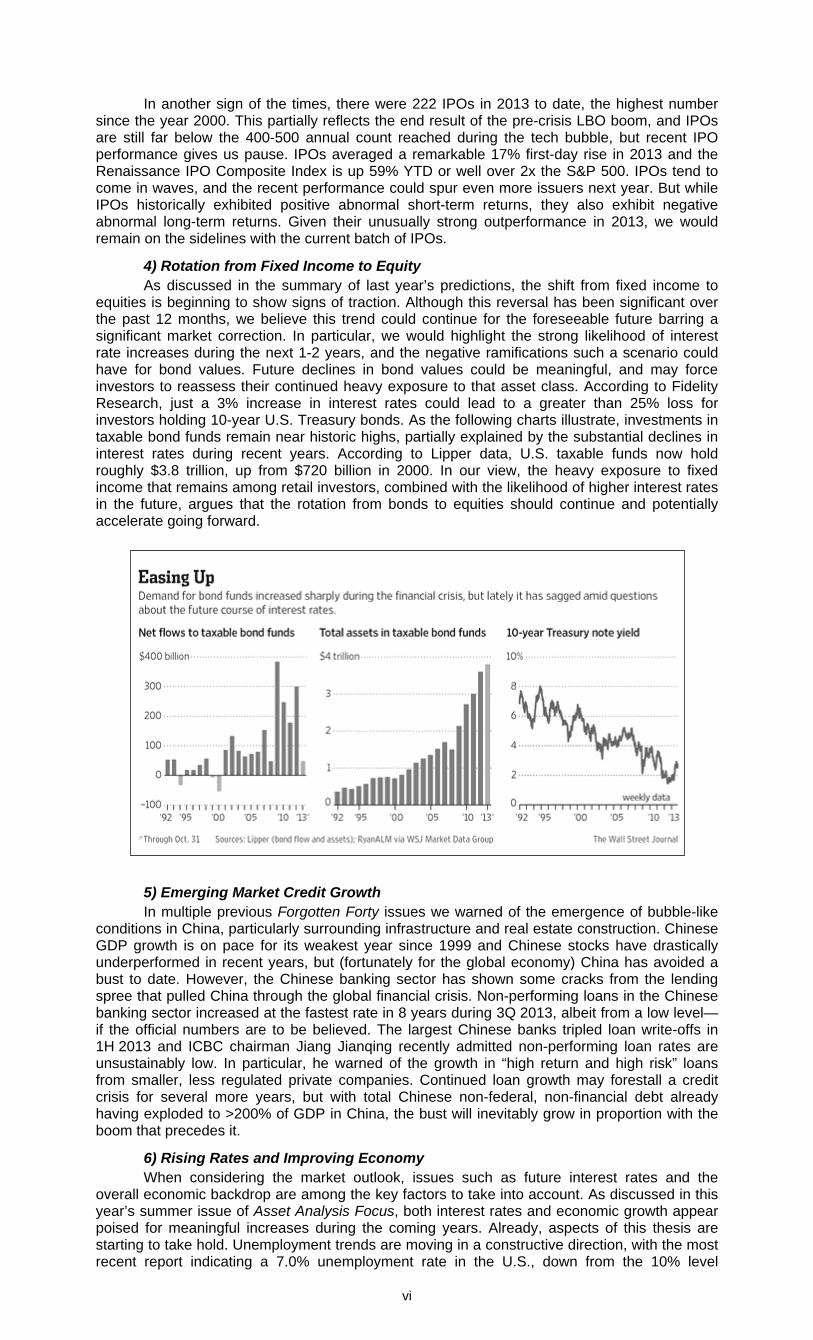

4) Rotation from Fixed Income to Equity As discussed in the summary of last year’s predictions, the shift from fixed income to

equities is beginning to show signs of traction. Although this reversal has been significant over the past 12 months, we believe this trend could continue for the foreseeable future barring a significant market correction. In particular, we would highlight the strong likelihood of interest rate increases during the next 1-2 years, and the negative ramifications such a scenario could have for bond values. Future declines in bond values could be meaningful, and may force investors to reassess their continued heavy exposure to that asset class. According to Fidelity Research, just a 3% increase in interest rates could lead to a greater than 25% loss for investors holding 10-year U.S. Treasury bonds. As the following charts illustrate, investments in taxable bond funds remain near historic highs, partially explained by the substantial declines in interest rates during recent years. According to Lipper data, U.S. taxable funds now hold roughly $3.8 trillion, up from $720 billion in 2000. In our view, the heavy exposure to fixed income that remains among retail investors, combined with the likelihood of higher interest rates in the future, argues that the rotation from bonds to equities should continue and potentially accelerate going forward.

5) Emerging Market Credit Growth In multiple previous Forgotten Forty issues we warned of the emergence of bubble-like

conditions in China, particularly surrounding infrastructure and real estate construction. Chinese GDP growth is on pace for its weakest year since 1999 and Chinese stocks have drastically underperformed in recent years, but (fortunately for the global economy) China has avoided a bust to date. However, the Chinese banking sector has shown some cracks from the lending spree that pulled China through the global financial crisis. Non-performing loans in the Chinese banking sector increased at the fastest rate in 8 years during 3Q 2013, albeit from a low level—if the official numbers are to be believed. The largest Chinese banks tripled loan write-offs in 1H 2013 and ICBC chairman Jiang Jianqing recently admitted non-performing loan rates are unsustainably low. In particular, he warned of the growth in “high return and high risk” loans from smaller, less regulated private companies. Continued loan growth may forestall a credit crisis for several more years, but with total Chinese non-federal, non-financial debt already having exploded to >200% of GDP in China, the bust will inevitably grow in proportion with the boom that precedes it.

6) Rising Rates and Improving Economy When considering the market outlook, issues such as future interest rates and the

overall economic backdrop are among the key factors to take into account. As discussed in this year’s summer issue of Asset Analysis Focus, both interest rates and economic growth appear poised for meaningful increases during the coming years. Already, aspects of this thesis are starting to take hold. Unemployment trends are moving in a constructive direction, with the most recent report indicating a 7.0% unemployment rate in the U.S., down from the 10% level

vii

experienced during the 2009-2010 period. Labor participation remains depressed from a historical perspective, but this metric should show gradual improvement as the labor market recovers. Other metrics such as GDP growth have shown steady advances during recent quarters, further suggesting that Federal Reserve monetary policy will likely be less accommodative going forward. We believe this scenario could have multiple beneficiaries from an investment perspective. Certainly, financial institutions with significant exposures to net interest income are among the prime examples (Forgotten Forty stocks such as Charles Schwab, Bank of New York, and Sallie Mae to name a few). Additionally, companies that provide economically sensitive commodities such as Devon Energy (oil and gas) and Vulcan Materials (construction aggregates) represent other ways for investors to capitalize on improving growth. Conversely, higher rates could create potential challenges. Several years of historically low interest rates have allowed firms to issue or refinance debt at very attractive levels. Going forward, higher rates could have negative ramifications for company balance sheets and cash flow, potentially diminishing the return of capital to shareholders via dividends and share repurchases. Moreover, companies that possess elevated levels of debt could face increased risk of financial distress.

We welcome your feedback at any time, and wish you a Happy, Healthy and Prosperous New Year.

Sincerely yours, Mark A. Boyar Chief Investment Officer

INVESTMENT RESEARCH SUMMARY PRICED DECEMBER 12, 2013

- 1 -

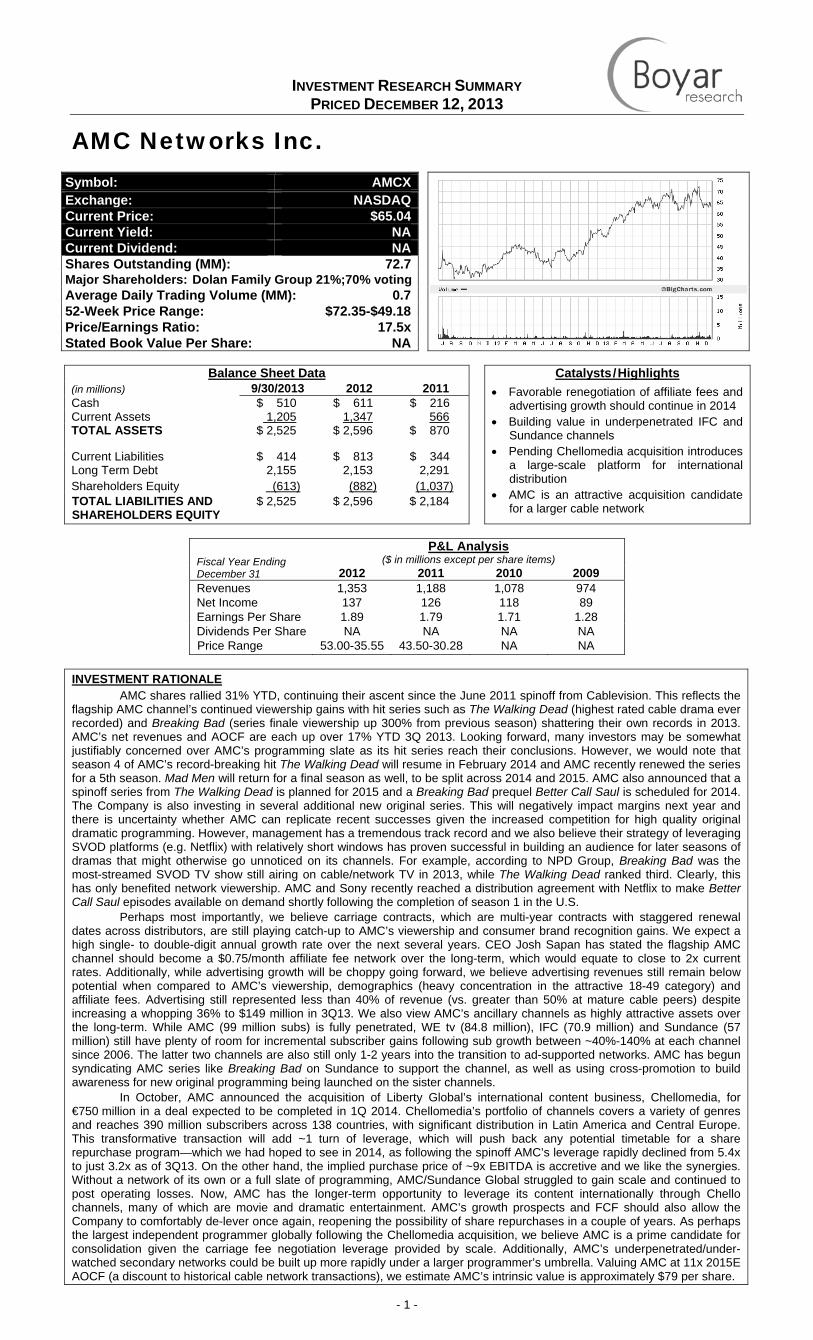

AMC Networks Inc.

Balance Sheet Data Catalysts/Highlights

(in millions) 9/30/2013 2012 2011 • Favorable renegotiation of affiliate fees and advertising growth should continue in 2014

• Building value in underpenetrated IFC and Sundance channels

• Pending Chellomedia acquisition introduces a large-scale platform for international distribution

• AMC is an attractive acquisition candidate for a larger cable network

Cash $ 510 $ 611 $ 216 Current Assets 1,205 1,347 566 TOTAL ASSETS $ 2,525 $ 2,596 $ 870 Current Liabilities $ 414 $ 813 $ 344 Long Term Debt 2,155 2,153 2,291 Shareholders Equity (613) (882) (1,037) TOTAL LIABILITIES AND SHAREHOLDERS EQUITY

$ 2,525 $ 2,596 $ 2,184

Fiscal Year Ending December 31

P&L Analysis ($ in millions except per share items)

2012 2011 2010 2009 Revenues 1,353 1,188 1,078 974 Net Income 137 126 118 89 Earnings Per Share 1.89 1.79 1.71 1.28 Dividends Per Share NA NA NA NA Price Range 53.00-35.55 43.50-30.28 NA NA

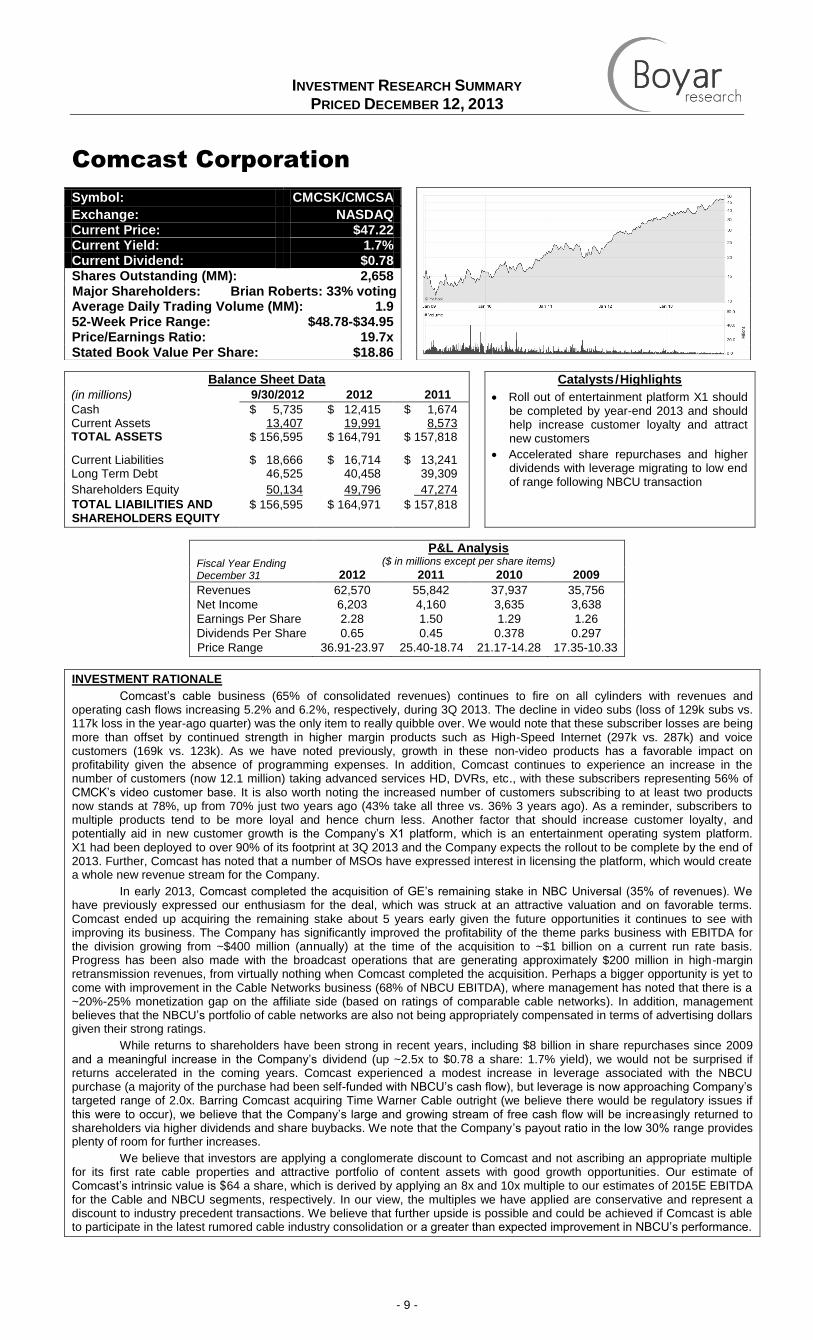

INVESTMENT RATIONALE

AMC shares rallied 31% YTD, continuing their ascent since the June 2011 spinoff from Cablevision. This reflects the flagship AMC channel’s continued viewership gains with hit series such as The Walking Dead (highest rated cable drama ever recorded) and Breaking Bad (series finale viewership up 300% from previous season) shattering their own records in 2013. AMC’s net revenues and AOCF are each up over 17% YTD 3Q 2013. Looking forward, many investors may be somewhat justifiably concerned over AMC’s programming slate as its hit series reach their conclusions. However, we would note that season 4 of AMC’s record-breaking hit The Walking Dead will resume in February 2014 and AMC recently renewed the series for a 5th season. Mad Men will return for a final season as well, to be split across 2014 and 2015. AMC also announced that a spinoff series from The Walking Dead is planned for 2015 and a Breaking Bad prequel Better Call Saul is scheduled for 2014. The Company is also investing in several additional new original series. This will negatively impact margins next year and there is uncertainty whether AMC can replicate recent successes given the increased competition for high quality original dramatic programming. However, management has a tremendous track record and we also believe their strategy of leveraging SVOD platforms (e.g. Netflix) with relatively short windows has proven successful in building an audience for later seasons of dramas that might otherwise go unnoticed on its channels. For example, according to NPD Group, Breaking Bad was the most-streamed SVOD TV show still airing on cable/network TV in 2013, while The Walking Dead ranked third. Clearly, this has only benefited network viewership. AMC and Sony recently reached a distribution agreement with Netflix to make Better Call Saul episodes available on demand shortly following the completion of season 1 in the U.S.

Perhaps most importantly, we believe carriage contracts, which are multi-year contracts with staggered renewal dates across distributors, are still playing catch-up to AMC’s viewership and consumer brand recognition gains. We expect a high single- to double-digit annual growth rate over the next several years. CEO Josh Sapan has stated the flagship AMC channel should become a $0.75/month affiliate fee network over the long-term, which would equate to close to 2x current rates. Additionally, while advertising growth will be choppy going forward, we believe advertising revenues still remain below potential when compared to AMC’s viewership, demographics (heavy concentration in the attractive 18-49 category) and affiliate fees. Advertising still represented less than 40% of revenue (vs. greater than 50% at mature cable peers) despite increasing a whopping 36% to $149 million in 3Q13. We also view AMC’s ancillary channels as highly attractive assets over the long-term. While AMC (99 million subs) is fully penetrated, WE tv (84.8 million), IFC (70.9 million) and Sundance (57 million) still have plenty of room for incremental subscriber gains following sub growth between ~40%-140% at each channel since 2006. The latter two channels are also still only 1-2 years into the transition to ad-supported networks. AMC has begun syndicating AMC series like Breaking Bad on Sundance to support the channel, as well as using cross-promotion to build awareness for new original programming being launched on the sister channels.

In October, AMC announced the acquisition of Liberty Global’s international content business, Chellomedia, for €750 million in a deal expected to be completed in 1Q 2014. Chellomedia’s portfolio of channels covers a variety of genres and reaches 390 million subscribers across 138 countries, with significant distribution in Latin America and Central Europe. This transformative transaction will add ~1 turn of leverage, which will push back any potential timetable for a share repurchase program—which we had hoped to see in 2014, as following the spinoff AMC’s leverage rapidly declined from 5.4x to just 3.2x as of 3Q13. On the other hand, the implied purchase price of ~9x EBITDA is accretive and we like the synergies. Without a network of its own or a full slate of programming, AMC/Sundance Global struggled to gain scale and continued to post operating losses. Now, AMC has the longer-term opportunity to leverage its content internationally through Chello channels, many of which are movie and dramatic entertainment. AMC’s growth prospects and FCF should also allow the Company to comfortably de-lever once again, reopening the possibility of share repurchases in a couple of years. As perhaps the largest independent programmer globally following the Chellomedia acquisition, we believe AMC is a prime candidate for consolidation given the carriage fee negotiation leverage provided by scale. Additionally, AMC’s underpenetrated/under-watched secondary networks could be built up more rapidly under a larger programmer’s umbrella. Valuing AMC at 11x 2015E AOCF (a discount to historical cable network transactions), we estimate AMC’s intrinsic value is approximately $79 per share.

Symbol: AMCX

Exchange: NASDAQCurrent Price: $65.04Current Yield: NACurrent Dividend: NAShares Outstanding (MM): 72.7Major Shareholders: Dolan Family Group 21%;70% votingAverage Daily Trading Volume (MM): 0.752-Week Price Range: $72.35-$49.18Price/Earnings Ratio: 17.5xStated Book Value Per Share: NA

INVESTMENT RESEARCH SUMMARY PRICED DECEMBER 12, 2013

- 2 -

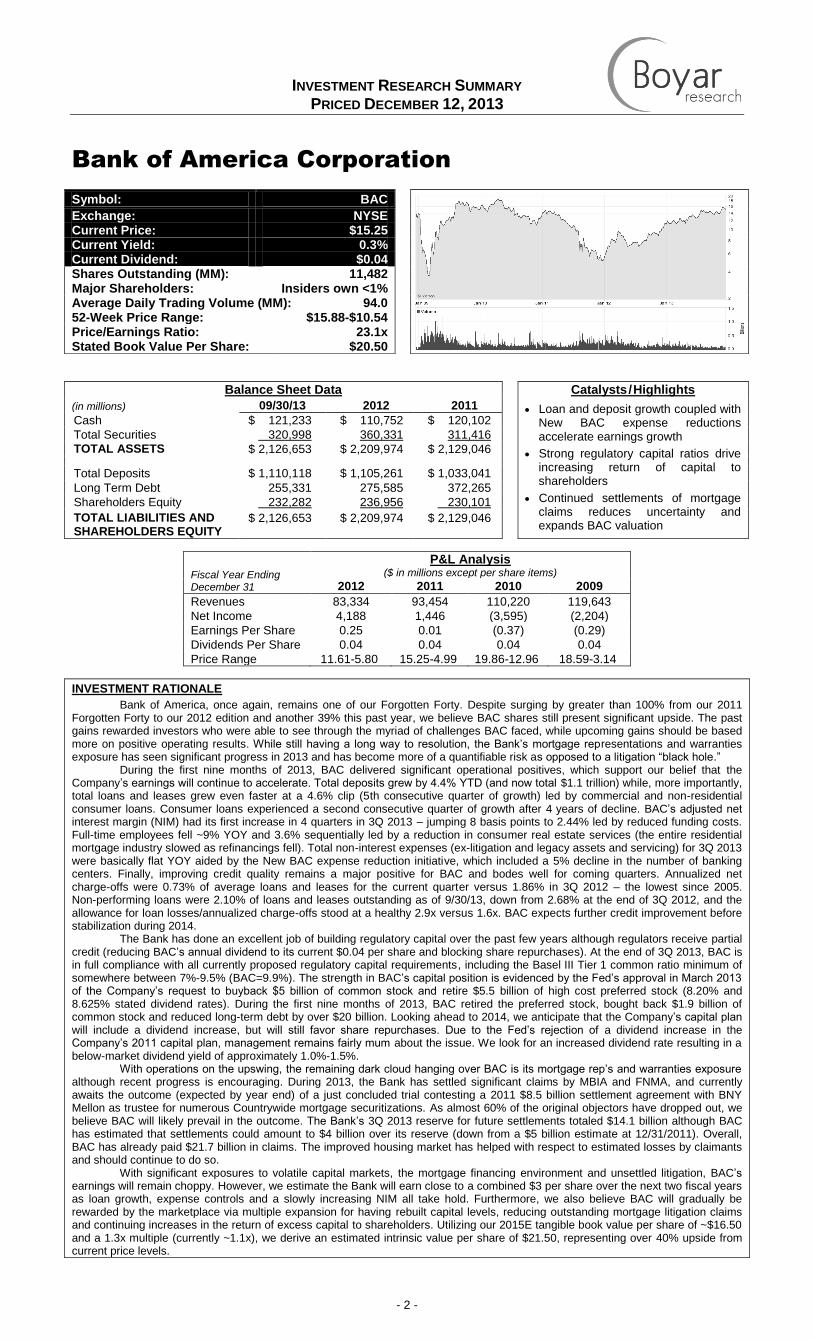

Bank of America Corporation

Balance Sheet Data Catalysts/Highlights

(in millions) 09/30/13 2012 2011 Loan and deposit growth coupled with New BAC expense reductions accelerate earnings growth

Strong regulatory capital ratios drive increasing return of capital to shareholders

Continued settlements of mortgage claims reduces uncertainty and expands BAC valuation

Cash $ 121,233 $ 110,752 $ 120,102

Total Securities 320,998 360,331 311,416

TOTAL ASSETS $ 2,126,653 $ 2,209,974 $ 2,129,046

Total Deposits $ 1,110,118 $ 1,105,261 $ 1,033,041

Long Term Debt 255,331 275,585 372,265

Shareholders Equity 232,282 236,956 230,101

TOTAL LIABILITIES AND SHAREHOLDERS EQUITY

$ 2,126,653 $ 2,209,974 $ 2,129,046

Fiscal Year Ending December 31

P&L Analysis ($ in millions except per share items)

2012 2011 2010 2009

Revenues 83,334 93,454 110,220 119,643

Net Income 4,188 1,446 (3,595) (2,204)

Earnings Per Share 0.25 0.01 (0.37) (0.29)

Dividends Per Share 0.04 0.04 0.04 0.04

Price Range 11.61-5.80 15.25-4.99 19.86-12.96 18.59-3.14

INVESTMENT RATIONALE

Bank of America, once again, remains one of our Forgotten Forty. Despite surging by greater than 100% from our 2011 Forgotten Forty to our 2012 edition and another 39% this past year, we believe BAC shares still present significant upside. The past gains rewarded investors who were able to see through the myriad of challenges BAC faced, while upcoming gains should be based more on positive operating results. While still having a long way to resolution, the Bank’s mortgage representations and warranties exposure has seen significant progress in 2013 and has become more of a quantifiable risk as opposed to a litigation “black hole.”

During the first nine months of 2013, BAC delivered significant operational positives, which support our belief that the Company’s earnings will continue to accelerate. Total deposits grew by 4.4% YTD (and now total $1.1 trillion) while, more importantly, total loans and leases grew even faster at a 4.6% clip (5th consecutive quarter of growth) led by commercial and non-residential consumer loans. Consumer loans experienced a second consecutive quarter of growth after 4 years of decline. BAC’s adjusted net interest margin (NIM) had its first increase in 4 quarters in 3Q 2013 – jumping 8 basis points to 2.44% led by reduced funding costs. Full-time employees fell ~9% YOY and 3.6% sequentially led by a reduction in consumer real estate services (the entire residential mortgage industry slowed as refinancings fell). Total non-interest expenses (ex-litigation and legacy assets and servicing) for 3Q 2013 were basically flat YOY aided by the New BAC expense reduction initiative, which included a 5% decline in the number of banking centers. Finally, improving credit quality remains a major positive for BAC and bodes well for coming quarters. Annualized net charge-offs were 0.73% of average loans and leases for the current quarter versus 1.86% in 3Q 2012 – the lowest since 2005. Non-performing loans were 2.10% of loans and leases outstanding as of 9/30/13, down from 2.68% at the end of 3Q 2012, and the allowance for loan losses/annualized charge-offs stood at a healthy 2.9x versus 1.6x. BAC expects further credit improvement before stabilization during 2014.

The Bank has done an excellent job of building regulatory capital over the past few years although regulators receive partial credit (reducing BAC’s annual dividend to its current $0.04 per share and blocking share repurchases). At the end of 3Q 2013, BAC is in full compliance with all currently proposed regulatory capital requirements, including the Basel III Tier 1 common ratio minimum of somewhere between 7%-9.5% (BAC=9.9%). The strength in BAC’s capital position is evidenced by the Fed’s approval in March 2013 of the Company’s request to buyback $5 billion of common stock and retire $5.5 billion of high cost preferred stock (8.20% and 8.625% stated dividend rates). During the first nine months of 2013, BAC retired the preferred stock, bought back $1.9 billion of common stock and reduced long-term debt by over $20 billion. Looking ahead to 2014, we anticipate that the Company’s capital plan will include a dividend increase, but will still favor share repurchases. Due to the Fed’s rejection of a dividend increase in the Company’s 2011 capital plan, management remains fairly mum about the issue. We look for an increased dividend rate resulting in a below-market dividend yield of approximately 1.0%-1.5%.

With operations on the upswing, the remaining dark cloud hanging over BAC is its mortgage rep’s and warranties exposure although recent progress is encouraging. During 2013, the Bank has settled significant claims by MBIA and FNMA, and currently awaits the outcome (expected by year end) of a just concluded trial contesting a 2011 $8.5 billion settlement agreement with BNY Mellon as trustee for numerous Countrywide mortgage securitizations. As almost 60% of the original objectors have dropped out, we believe BAC will likely prevail in the outcome. The Bank’s 3Q 2013 reserve for future settlements totaled $14.1 billion although BAC has estimated that settlements could amount to $4 billion over its reserve (down from a $5 billion estimate at 12/31/2011). Overall, BAC has already paid $21.7 billion in claims. The improved housing market has helped with respect to estimated losses by claimants and should continue to do so.

With significant exposures to volatile capital markets, the mortgage financing environment and unsettled litigation, BAC’s earnings will remain choppy. However, we estimate the Bank will earn close to a combined $3 per share over the next two fiscal years as loan growth, expense controls and a slowly increasing NIM all take hold. Furthermore, we also believe BAC will gradually be rewarded by the marketplace via multiple expansion for having rebuilt capital levels, reducing outstanding mortgage litigation claims and continuing increases in the return of excess capital to shareholders. Utilizing our 2015E tangible book value per share of ~$16.50 and a 1.3x multiple (currently ~1.1x), we derive an estimated intrinsic value per share of $21.50, representing over 40% upside from current price levels.

Symbol: BAC

Exchange: NYSE Current Price: $15.25 Current Yield: 0.3% Current Dividend: $0.04 Shares Outstanding (MM): 11,482 Major Shareholders: Insiders own <1% Average Daily Trading Volume (MM): 94.0 52-Week Price Range: $15.88-$10.54 Price/Earnings Ratio: 23.1x Stated Book Value Per Share: $20.50

INVESTMENT RESEARCH SUMMARY PRICED DECEMBER 12, 2013

- 3 -

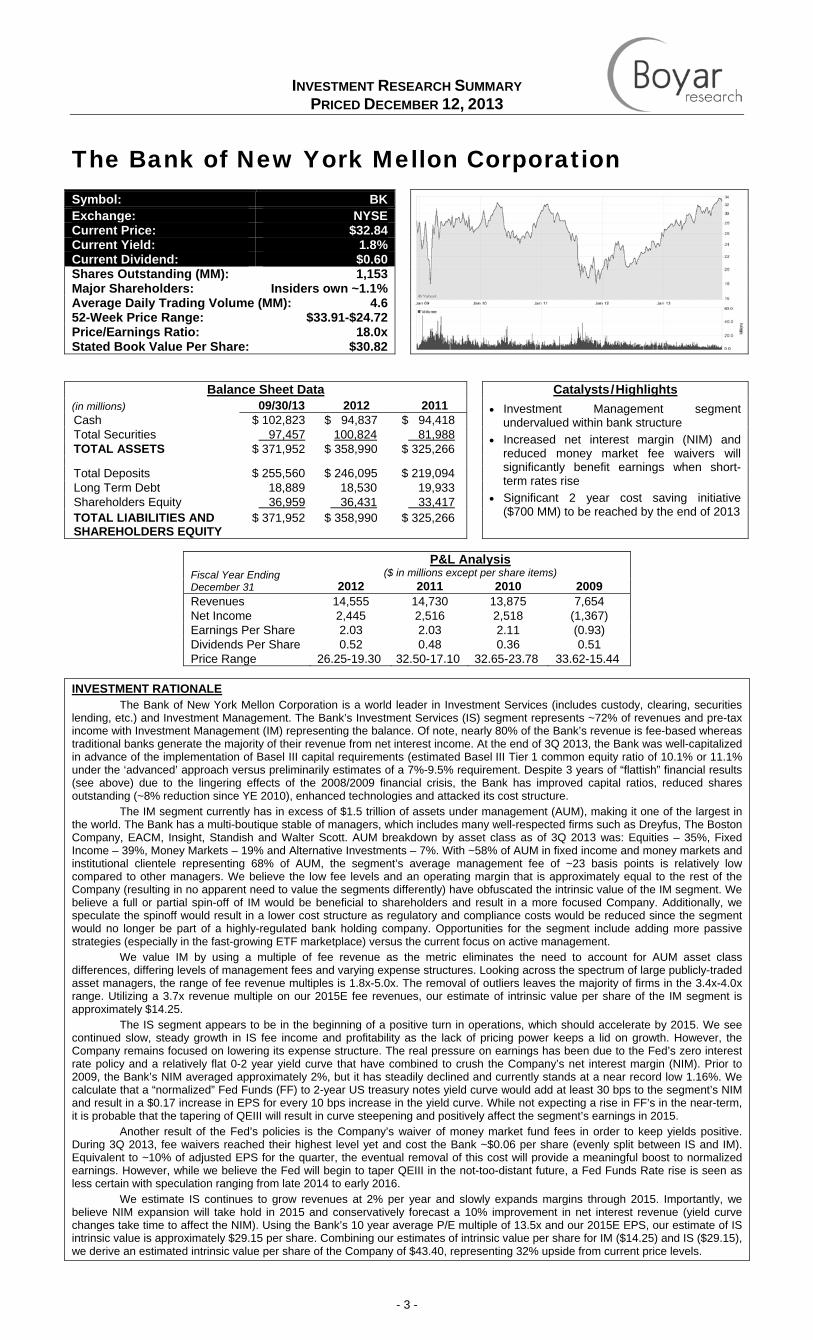

The Bank of New York Mellon Corporation

Balance Sheet Data Catalysts/Highlights (in millions) 09/30/13 2012 2011 • Investment Management segment

undervalued within bank structure • Increased net interest margin (NIM) and

reduced money market fee waivers will significantly benefit earnings when short-term rates rise

• Significant 2 year cost saving initiative ($700 MM) to be reached by the end of 2013

Cash $ 102,823 $ 94,837 $ 94,418 Total Securities 97,457 100,824 81,988 TOTAL ASSETS $ 371,952 $ 358,990 $ 325,266

Total Deposits $ 255,560 $ 246,095 $ 219,094 Long Term Debt 18,889 18,530 19,933 Shareholders Equity 36,959 36,431 33,417 TOTAL LIABILITIES AND SHAREHOLDERS EQUITY

$ 371,952 $ 358,990 $ 325,266

Fiscal Year Ending December 31

P&L Analysis ($ in millions except per share items)

2012 2011 2010 2009 Revenues 14,555 14,730 13,875 7,654 Net Income 2,445 2,516 2,518 (1,367) Earnings Per Share 2.03 2.03 2.11 (0.93) Dividends Per Share 0.52 0.48 0.36 0.51 Price Range 26.25-19.30 32.50-17.10 32.65-23.78 33.62-15.44

INVESTMENT RATIONALE

The Bank of New York Mellon Corporation is a world leader in Investment Services (includes custody, clearing, securities lending, etc.) and Investment Management. The Bank’s Investment Services (IS) segment represents ~72% of revenues and pre-tax income with Investment Management (IM) representing the balance. Of note, nearly 80% of the Bank’s revenue is fee-based whereas traditional banks generate the majority of their revenue from net interest income. At the end of 3Q 2013, the Bank was well-capitalized in advance of the implementation of Basel III capital requirements (estimated Basel III Tier 1 common equity ratio of 10.1% or 11.1% under the ‘advanced’ approach versus preliminarily estimates of a 7%-9.5% requirement. Despite 3 years of “flattish” financial results (see above) due to the lingering effects of the 2008/2009 financial crisis, the Bank has improved capital ratios, reduced shares outstanding (~8% reduction since YE 2010), enhanced technologies and attacked its cost structure.

The IM segment currently has in excess of $1.5 trillion of assets under management (AUM), making it one of the largest in the world. The Bank has a multi-boutique stable of managers, which includes many well-respected firms such as Dreyfus, The Boston Company, EACM, Insight, Standish and Walter Scott. AUM breakdown by asset class as of 3Q 2013 was: Equities – 35%, Fixed Income – 39%, Money Markets – 19% and Alternative Investments – 7%. With ~58% of AUM in fixed income and money markets and institutional clientele representing 68% of AUM, the segment’s average management fee of ~23 basis points is relatively low compared to other managers. We believe the low fee levels and an operating margin that is approximately equal to the rest of the Company (resulting in no apparent need to value the segments differently) have obfuscated the intrinsic value of the IM segment. We believe a full or partial spin-off of IM would be beneficial to shareholders and result in a more focused Company. Additionally, we speculate the spinoff would result in a lower cost structure as regulatory and compliance costs would be reduced since the segment would no longer be part of a highly-regulated bank holding company. Opportunities for the segment include adding more passive strategies (especially in the fast-growing ETF marketplace) versus the current focus on active management.

We value IM by using a multiple of fee revenue as the metric eliminates the need to account for AUM asset class differences, differing levels of management fees and varying expense structures. Looking across the spectrum of large publicly-traded asset managers, the range of fee revenue multiples is 1.8x-5.0x. The removal of outliers leaves the majority of firms in the 3.4x-4.0x range. Utilizing a 3.7x revenue multiple on our 2015E fee revenues, our estimate of intrinsic value per share of the IM segment is approximately $14.25.

The IS segment appears to be in the beginning of a positive turn in operations, which should accelerate by 2015. We see continued slow, steady growth in IS fee income and profitability as the lack of pricing power keeps a lid on growth. However, the Company remains focused on lowering its expense structure. The real pressure on earnings has been due to the Fed’s zero interest rate policy and a relatively flat 0-2 year yield curve that have combined to crush the Company’s net interest margin (NIM). Prior to 2009, the Bank’s NIM averaged approximately 2%, but it has steadily declined and currently stands at a near record low 1.16%. We calculate that a “normalized” Fed Funds (FF) to 2-year US treasury notes yield curve would add at least 30 bps to the segment’s NIM and result in a $0.17 increase in EPS for every 10 bps increase in the yield curve. While not expecting a rise in FF’s in the near-term, it is probable that the tapering of QEIII will result in curve steepening and positively affect the segment’s earnings in 2015.

Another result of the Fed’s policies is the Company’s waiver of money market fund fees in order to keep yields positive. During 3Q 2013, fee waivers reached their highest level yet and cost the Bank ~$0.06 per share (evenly split between IS and IM). Equivalent to ~10% of adjusted EPS for the quarter, the eventual removal of this cost will provide a meaningful boost to normalized earnings. However, while we believe the Fed will begin to taper QEIII in the not-too-distant future, a Fed Funds Rate rise is seen as less certain with speculation ranging from late 2014 to early 2016.

We estimate IS continues to grow revenues at 2% per year and slowly expands margins through 2015. Importantly, we believe NIM expansion will take hold in 2015 and conservatively forecast a 10% improvement in net interest revenue (yield curve changes take time to affect the NIM). Using the Bank’s 10 year average P/E multiple of 13.5x and our 2015E EPS, our estimate of IS intrinsic value is approximately $29.15 per share. Combining our estimates of intrinsic value per share for IM ($14.25) and IS ($29.15), we derive an estimated intrinsic value per share of the Company of $43.40, representing 32% upside from current price levels.

Symbol: BK Exchange: NYSECurrent Price: $32.84Current Yield: 1.8%Current Dividend: $0.60 Shares Outstanding (MM): 1,153Major Shareholders: Insiders own ~1.1%Average Daily Trading Volume (MM): 4.652-Week Price Range: $33.91-$24.72Price/Earnings Ratio: 18.0xStated Book Value Per Share: $30.82

INVESTMENT RESEARCH SUMMARY PRICED DECEMBER 12, 2013

- 4 -

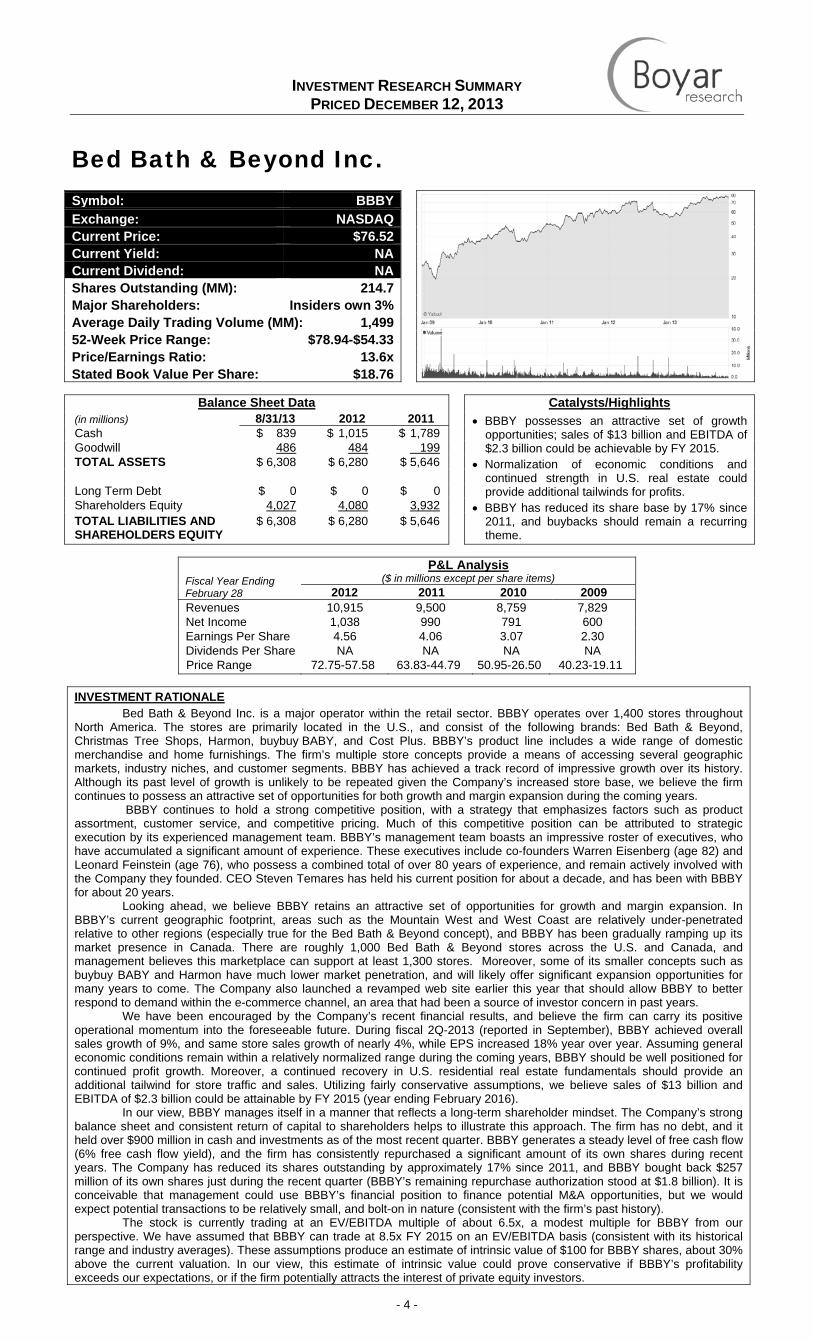

Bed Bath & Beyond Inc.

Balance Sheet Data Catalysts/Highlights

(in millions) 8/31/13 2012 2011 • BBBY possesses an attractive set of growth opportunities; sales of $13 billion and EBITDA of $2.3 billion could be achievable by FY 2015.

• Normalization of economic conditions and continued strength in U.S. real estate could provide additional tailwinds for profits.

• BBBY has reduced its share base by 17% since 2011, and buybacks should remain a recurring theme.

Cash $ 839 $ 1,015 $ 1,789 Goodwill 486 484 199 TOTAL ASSETS $ 6,308 $ 6,280 $ 5,646 Long Term Debt $ 0 $ 0 $ 0 Shareholders Equity 4,027 4,080 3,932 TOTAL LIABILITIES AND SHAREHOLDERS EQUITY

$ 6,308 $ 6,280 $ 5,646

Fiscal Year Ending February 28

P&L Analysis ($ in millions except per share items)

2012 2011 2010 2009 Revenues 10,915 9,500 8,759 7,829 Net Income 1,038 990 791 600 Earnings Per Share 4.56 4.06 3.07 2.30 Dividends Per Share NA NA NA NA Price Range 72.75-57.58 63.83-44.79 50.95-26.50 40.23-19.11

INVESTMENT RATIONALE

Bed Bath & Beyond Inc. is a major operator within the retail sector. BBBY operates over 1,400 stores throughout North America. The stores are primarily located in the U.S., and consist of the following brands: Bed Bath & Beyond, Christmas Tree Shops, Harmon, buybuy BABY, and Cost Plus. BBBY’s product line includes a wide range of domestic merchandise and home furnishings. The firm’s multiple store concepts provide a means of accessing several geographic markets, industry niches, and customer segments. BBBY has achieved a track record of impressive growth over its history. Although its past level of growth is unlikely to be repeated given the Company’s increased store base, we believe the firm continues to possess an attractive set of opportunities for both growth and margin expansion during the coming years.

BBBY continues to hold a strong competitive position, with a strategy that emphasizes factors such as product assortment, customer service, and competitive pricing. Much of this competitive position can be attributed to strategic execution by its experienced management team. BBBY’s management team boasts an impressive roster of executives, who have accumulated a significant amount of experience. These executives include co-founders Warren Eisenberg (age 82) and Leonard Feinstein (age 76), who possess a combined total of over 80 years of experience, and remain actively involved with the Company they founded. CEO Steven Temares has held his current position for about a decade, and has been with BBBY for about 20 years.

Looking ahead, we believe BBBY retains an attractive set of opportunities for growth and margin expansion. In BBBY’s current geographic footprint, areas such as the Mountain West and West Coast are relatively under-penetrated relative to other regions (especially true for the Bed Bath & Beyond concept), and BBBY has been gradually ramping up its market presence in Canada. There are roughly 1,000 Bed Bath & Beyond stores across the U.S. and Canada, and management believes this marketplace can support at least 1,300 stores. Moreover, some of its smaller concepts such as buybuy BABY and Harmon have much lower market penetration, and will likely offer significant expansion opportunities for many years to come. The Company also launched a revamped web site earlier this year that should allow BBBY to better respond to demand within the e-commerce channel, an area that had been a source of investor concern in past years.

We have been encouraged by the Company’s recent financial results, and believe the firm can carry its positive operational momentum into the foreseeable future. During fiscal 2Q-2013 (reported in September), BBBY achieved overall sales growth of 9%, and same store sales growth of nearly 4%, while EPS increased 18% year over year. Assuming general economic conditions remain within a relatively normalized range during the coming years, BBBY should be well positioned for continued profit growth. Moreover, a continued recovery in U.S. residential real estate fundamentals should provide an additional tailwind for store traffic and sales. Utilizing fairly conservative assumptions, we believe sales of $13 billion and EBITDA of $2.3 billion could be attainable by FY 2015 (year ending February 2016).

In our view, BBBY manages itself in a manner that reflects a long-term shareholder mindset. The Company’s strong balance sheet and consistent return of capital to shareholders helps to illustrate this approach. The firm has no debt, and it held over $900 million in cash and investments as of the most recent quarter. BBBY generates a steady level of free cash flow (6% free cash flow yield), and the firm has consistently repurchased a significant amount of its own shares during recent years. The Company has reduced its shares outstanding by approximately 17% since 2011, and BBBY bought back $257 million of its own shares just during the recent quarter (BBBY’s remaining repurchase authorization stood at $1.8 billion). It is conceivable that management could use BBBY’s financial position to finance potential M&A opportunities, but we would expect potential transactions to be relatively small, and bolt-on in nature (consistent with the firm’s past history).

The stock is currently trading at an EV/EBITDA multiple of about 6.5x, a modest multiple for BBBY from our perspective. We have assumed that BBBY can trade at 8.5x FY 2015 on an EV/EBITDA basis (consistent with its historical range and industry averages). These assumptions produce an estimate of intrinsic value of $100 for BBBY shares, about 30% above the current valuation. In our view, this estimate of intrinsic value could prove conservative if BBBY’s profitability exceeds our expectations, or if the firm potentially attracts the interest of private equity investors.

Symbol: BBBY Exchange: NASDAQCurrent Price: $76.52Current Yield: NACurrent Dividend: NAShares Outstanding (MM): 214.7Major Shareholders: Insiders own 3%Average Daily Trading Volume (MM): 1,49952-Week Price Range: $78.94-$54.33Price/Earnings Ratio: 13.6xStated Book Value Per Share: $18.76

INVESTMENT RESEARCH SUMMARY PRICED DECEMBER 12, 2013

- 5 -

Callaway Golf Company

Balance Sheet Data Catalysts/Highlights

(in millions) 9/30/13 2012 2011 • Ongoing market share gains are translating into improved top and bottom line performance

• As profitability improves, ELY should generate an outsized amount of FCF due to significant operating loss carryforwards

• Elimination of high cost preferred stock should remove valuation overhang

Cash $ 38 $ 43 $ 43 Current Assets 410 387 419 TOTAL ASSETS $ 651 $ 638 $ 727

Current Liabilities $ 163 $ 162 $ 68 Long Term Debt 108 107 0 Shareholders Equity 335 322 513 TOTAL LIABILITIES AND SHAREHOLDERS EQUITY

$ 651 $ 638 $ 727

Fiscal Year Ending December 31

P&L Analysis ($ in millions except per share items)

2012 2011 2010 2009 Revenues 834 887 968 951 Net Income (123) (172) (19) (15) Earnings Per Share (1.96) (2.82) (0.46) (0.33) Dividends Per Share 0.04 0.04 0.04 0.10 Price Range 7.29-5.17 8.37-4.70 10.19-5.80 10.31-4.66

INVESTMENT RATIONALE We believe that Callaway is in the early stages of executing a successful turnaround as the Company is regaining market

share, which is translating into significantly improved top and bottom line results. Between 2007 and 2012, Callaway’s hard goods (woods, irons, putters, wedges and balls) market share in the U.S. steadily declined from 19.6% in 2007 to 13.9% in 2012. However, Callaway has begun to recapture share thanks to its strong new product development and improved marketing initiatives intended to revitalize the iconic Callaway brand. Year-to-date (August 2013), Callaway’s hard goods market share stood at 15.1%, up 110 basis points on a Y-o-Y basis and management has noted that its fairway wood market share in the U.S. doubled in 2013, which has contributed to a 26% increase in Callaway’s total woods sales (~32% of ELY’s total sales). It is worth noting that the Company’s market share gains are not confined to the U.S. market with the Company recording share gains in key markets including Japan (18% of ELY’s sales) and the U.K, which is Callaway’ largest market in Europe (15% of total). Notably, the Company’s YTD market share gains in Japan of 350 basis points represented the highest share gain for any golf brand in that country helping to drive 31% local currency growth through the first 9 months of 2013.

A key component of Callaway’s turnaround plan has been improving the image of its iconic brand. As part of its plan to make the Callaway brand more relevant, especially with avid golfers, Callaway has invested heavily in signing tour players to endorse its brand with an emphasis on attracting “long-hitting, young dynamic professionals.” New Callaway staff members for 2013 included Gary Woodland, Ryo Ishikawa, Nicolas Colsaerts and Chris Kirk. Notably, Callaway had two of its endorsers in the top ten in driving distance on each of the PGA and European tour at the end of the 2013 season. The Company’s initiatives to make the brand resonate with consumers are showing success with ELY experiencing brand strength for the first time in many years according to a recent Attitude and Usage survey conducted by industry researcher Golf Datatech.

Callaway’s 3Q 2013 results suggest that not only is a turnaround unfolding, but it is actually gaining momentum with quarterly and YTD revenues increasing by 38% (constant currency) and 13%, respectively. Results in both time periods imply that Callaway is outpacing the industry as conditions in the U.S. and Europe, two of the Company’s largest markets accounting for 64% of sales, continue to be soft. The strong results prompted the Company to increase its full year outlook (the first boost in many years) for revenue with the Company now expecting to generate $836 million up from a prior outlook of $810-$820 million, which would represent a 13% increase on a pro forma basis. The Company’s improved top line, aided by less discounting and new product success, coupled with ongoing cost reduction and manufacturing efficiency initiatives to further streamline the organization are also translating into significantly enhanced profitability. For the first nine months of 2013, Callaway’s gross margins on a pro forma basis were 41%, up 350 basis points while operating expenses on a pro forma basis declined by 11% to $248 million compared with $279 million. As a result of Callaway’s progress this year, the Company expects to post positive net income on a pro forma basis during 2013, which would be ELY’s first annual profit since 2008.

In addition to its operational improvements, Callaway has made significant progress with its capital structure, which should help reduce expenses and bolster the Company’s financial flexibility. During 2013, Callaway redeemed the remainder of its high cost (7.5%) convertible preferred stock. In our view the convertible preferred security has served as a valuation overhang on the shares in recent years. While the Company still has $108 million of preferred stock outstanding, it carries a much lower coupon (3.5%) than the convertible stock that was recently redeemed. In addition, as the Company’s profitability continues to improve, ELY is likely to generate an outsized amount of free cash flow thanks to $273 million in operating loss carryforwards at the end of 2012. With future tax payments likely to be minimal, ELY should be well positioned to further improve its capital structure and have the ability to begin returning value to shareholders via higher dividends or share buybacks.

We believe Callaway’s operating momentum should continue under the auspices of CEO Chip Brewer, who appears to be leading Callaway in the right direction and successfully orchestrated a prior golf industry turnaround while at Adams Golf. The pace of new product introductions is set to accelerate under Brewer (the Big Bertha is back), which should help the Company sustain its recent operating momentum. Our estimate of Callaway’s intrinsic value is $12 a share, which is derived by applying discounted multiples (relative to recent golf industry transactions) to our estimate of 2016 sales and profitability. We note that CEO Brewer is heavily incentivized to see through a successful turnaround as he is in possession of 800k ELY stock options (avg. exercise price: $6.48 a share) and 300k restricted stock units that he received upon joining the Company as part of “make-whole” agreement for incentives he was forfeiting at his prior employer.

Symbol: ELY Exchange: NYSECurrent Price: $7.50Current Yield: 0.5%Current Dividend: $0.04Shares Outstanding (MM): 72.6Major Shareholders: Insiders 2.3%Average Daily Trading Volume (MM): 0.852-Week Price Range: $8.97-$6.15Price/Earnings Ratio: N/AStated Book Value Per Share: $4.61

INVESTMENT RESEARCH SUMMARY PRICED DECEMBER 12, 2013

- 6 -

Carnival Corporation

Balance Sheet Data Catalysts/Highlights

(in millions) 8/31/2013 2012 2011 • The Company is in the early stages of undergoing a complete transformation with regard to its operating philosophy.

• In our opinion, profits are well below potential relative to its own historic pricing as well as that of its competitors.

• We believe CCL’s private market value is at least 40% above its current market price.

Cash $ 981 $ 465 $ 450 Current Assets 2,634 1,821 1,312 TOTAL ASSETS $ 40,393 $ 39,161 $ 38,637 Current Liabilities $ 7,488 $ 7,340 $ 6,105 Long Term Debt 7,792 7,168 8,053 Shareholders Equity 24,260 23,929 23,832 TOTAL LIABILITIES AND SHAREHOLDERS EQUITY

$ 40,393 $ 39,161 $ 38,637

Fiscal Year Ending November 30

P&L Analysis ($ in millions except per share items)

2012 2011 2010 2009 Revenues 15,382 15,793 14,469 13,157 Net Income 1,298 1,912 1,978 1,790 Earnings Per Share 1.67 2.42 2.47 2.23 Dividends Per Share 1.00 1.00 0.40 Nil Price Range 39.95-29.15 48.14-28.52 47.22-29.68 34.95-16.80

INVESTMENT RATIONALE Investing in turnaround situations is not only complicated, but in the vast majority of instances requires

significant amounts of patience. However, once an underachieving company finally fesses up to its past sins by cutting costs, paying down debt, eliminating unprofitable or non-core businesses, and intelligently articulates a new business plan, the result is often a rapid rise in its share price (Home Depot and McDonald’s are relatively recent examples of this phenomenon). Furthermore, if the plan is orchestrated by a newly appointed CEO, the common shares tend to advance even sooner.

Carnival, the world’s largest cruise operator, was clearly in crisis mode throughout 2012 and 2013. Its Costa Concordia vessel ran aground near the Italian coast in 2012, killing 32 people and generating an immense amount of bad media coverage. That was followed by more negative incidents in 2013, including a fire aboard the Carnival Triumph in February that further tarnished the Company’s image.

As a result of the aforementioned, Micky Arison, the son of the Company's founder and the Company’s chief executive officer for 34 years, resigned and was replaced by Arnold Donald. Donald, who has been a Carnival board member for 12 years, is a highly regarded entrepreneur and has resigned all of his private equity positions so he can devote his energy to literally “righting the ship.”

In the past CCL’s key growth drivers have been adding new vessels and penetrating new markets. CCL started with a few ships, grew to a fleet, and now has an armada. The Company is in the early stages of undergoing a complete transformation with regard to its operating philosophy. One in which it is transitioning from focusing on unit growth in favor of significant cost cutting and retrofitting existing ships. As the Company adds fewer new ships in the future, revenue growth will emanate from adding new cabins and innovative dining and bar concepts to existing vessels. Retrofitting will only be done if a satisfactory return on capital can be attained.

Other initiatives being implemented by Donald include focusing on collaboration between the many brands under the Carnival umbrella, something that was lacking in the past. Redundancies will be eliminated, and cross marketing will be initiated. Donald has already met with travel agents to repair relations that have frayed in recent years. CCL has simplified its fare structure and incentivized those agents. A more aggressive campaign to win over more travelers (currently about 35% who have never cruised before) has begun, as well as one intended to revitalize its tarnished brand.

Carnival will continue to discount prices throughout a good part of 2014 in order to fill its ships. As credibility is restored a more aggressive pricing policy will be implemented. Investor expectations in terms of earnings and stock price have been sufficiently diminished to create a margin of safety. In our opinion, profits are well below potential relative to its own historic pricing as well as that of its competitors. By fiscal 2015 EPS could reach $2.70 versus street estimates of $1.60 for the fiscal year ended Nov 30, 2013. Potential earning power based on CCL’s peak 2008 net yield to its current fleet and expense structure is over $4.50 and even higher if compared to competitors.

We believe CCL’s private market value is at least 40% above its current market price. We reach this number by projecting future profit potential, as well as taking into consideration the difficult barriers to entry, and the unique consumer franchise that has been created over multiple decades.

Symbol: CCL Exchange: NYSECurrent Price: $35.34Current Yield: 2.8%Current Dividend: $1.00Shares Outstanding (MM): 776Major Shareholders: Micky Arison~22%Average Daily Trading Volume (MM): 4.852-Week Price Range: $39.95-31.44Price/Earnings Ratio: 22.3xStated Book Value Per Share: $31.26

INVESTMENT RESEARCH SUMMARY PRICED DECEMBER 12, 2013

- 7 -

The Charles Schwab Corporation

Balance Sheet Data Catalysts/Highlights

(in millions) 9/30/2013 2012 2011 • Increased short term interest rates will have favorable impact on SCHW’s spread-based businesses and eliminate MMF fee waivers

• Traction with new platforms including Schwab Index Advantage, Schwab ETF OneSource and the upcoming/pending launch of Schwab’s ETF 401 (k) plans

• SCHW is well capitalized, which should allow it to repurchase shares and increase its dividend

Cash $ 7,362 $ 12,663 $ 8,679 Total Securities 80,566 64,953 49,666 TOTAL ASSETS $ 140,211 $ 133,637 $ 108,553 Total Deposits $ 91,187 $ 79,377 $ 60,854 Long Term Debt 1,904 1,632 2,001 Shareholders Equity 10,053 9,589 7,714 TOTAL LIABILITIES AND SHAREHOLDERS EQUITY

$ 140,211 $ 133,637 $ 108,553

Fiscal Year Ending December 30

P&L Analysis ($ in millions except per share items)

2012 2011 2010 2009 Revenues 4,883 4,691 4,248 4,193 Net Income 928 864 454 787 Earnings Per Share 0.69 0.70 0.38 0.68 Dividends Per Share N/A N/A N/A N/A Price Range 15.38-11.61 19.45-10.75 19.88-12.76 19.49-11.34

INVESTMENT RATIONALE The Charles Schwab Corporation provides its clients a number of services including securities brokerage, banking, money

management and financial advisory. Over the past two decades, Schwab has successfully transformed its business model from commission dependent to one that derives the vast majority of its revenues and profitability from either fee based or spread based businesses. At 3Q 2013, asset management and administration fees (42% of 3Q 2013 net revenues) and net interest revenue (37%) accounted for nearly 80% of SCHW’s total net revenues. Meanwhile, transactional based revenues (commissions, etc.) now represent just 16% of total net revenues, down from 60% as recently as 1998.

By all accounts, the current Charles Schwab bears little resemblance to the upstart brokerage firm that successfully challenged the full service model during the early 1970s. New assets entering Schwab’s various platforms are increasingly generating fees for the Company based on asset levels rather than commissions. Between 2009 and 2012, the Company’s asset management and administration fees (excluding money market fund fees) increased to $1.7 billion from $1.1 billion, representing a 17% CAGR. It should also be noted that nearly half of Schwab’s total client assets ($1 trillion out of $2.2 trillion) at 3Q 2013 were receiving some type of ongoing advice and hence generating an ongoing revenue stream for the Company.

We believe Charles Schwab will be a primary beneficiary of what we view as a rising interest rate environment. Persistently low rates have been particularly challenging for Schwab and have masked its true earnings power. Approximately 75% of SCHW’s interest-earning assets are currently tied to short-term rates. In addition to the pressure on net interest revenue, low interest rates have forced the Company to provide fee waivers for its money market funds in order for investors in these products to earn a positive return. During 2012, fee waivers totaled a whopping $587 million, representing nearly 30% of SCHW’s asset management and administration fees. As a result, as short term rates begin to increase this revenue component should experience a significant acceleration and have a disproportionate impact on SCHW’s overall profitability.

In the wake of the financial crisis with its competitors struggling, Schwab made a strategic decision to continue to invest in its client capabilities. It’s hard to argue that this was not the right decision. Between 2008 and 2012, Schwab attracted $500 billion in assets, which is $200 billion more than its top four publicly traded competitors combined. While expenses continued to remain elevated, tracking in line with revenue growth in recent years, management recently stated that expense growth during 2014 should be “muted” and trail revenue growth by ~300 to 500 bps. We believe this outlook is realistic reflecting Schwab’s asset gathering progress (YTD-3Q 2013, SCHW’s core net new assets of $108.8 billion represent an annualized growth rate of approximately 7.4%), the prospect for higher rates, and the Company’s disciplined expense management.

Schwab has recently embarked on a number of initiatives to further accelerate its fee based revenues. During 2012, the Company launched Schwab Index Advantage to become a much greater participant in the $5 trillion 401 (k) market by offering low cost mutual funds as well as professional advice. Recent results have been encouraging as Schwab was able to attract $4 billion from 50 employers in just its first year. An ETF only 401 (k) program is also scheduled to launch shortly that should allow Schwab to make further inroads in the 401 (k) market. Schwab’s recent decision to offer a marketplace of commission-free ETFs should also help accelerate fee based revenues. While Schwab foregoes a commission payment, it now generates an attractive long-term recurring revenue stream tied to asset levels. According to Schwab management, early indications are that the flows into the ETF OneSource platform are coming out of commission oriented ETFs or commission equities rather than cannibalizing Schwab’s profitable Mutual Fund OneSource program.

Schwab is well capitalized and is poised to return a significant amount of value to shareholders in our view. At September 30, 2013, Schwab Bank boasted a Tier 1 Risk-Based Capital ratio of 18.5%, well above the 6% level deemed to be well capitalized. While the current interest rate environment has created its share of headwinds, SCHW has taken advantage of historically low rates to secure capital at attractive rates. As earnings growth accelerates, we would not be surprised if Schwab boosts its dividend and begins repurchasing shares as soon as the Company receives more clarity on future capital requirements.

Utilizing a sum-of-the-parts valuation, our estimate of Schwab’s intrinsic value is $32 a share, representing 29% upside from current levels. We would not be surprised if this proves conservative, especially as SCHW’s true earnings power emerges. In addition, don’t rule out the potential for a takeout. Company founder Charles Schwab is 75 years old and controls over 14% of the stock. We believe that SCHW’s fee based business would be attractive for a number of large financial institutions.

Symbol: SCHW Exchange: NYSECurrent Price: $24.80Current Yield: N/ACurrent Dividend: N/AShares Outstanding (MM): 1,296Major Shareholders: Charles Schwab: 14.1%Average Daily Trading Volume (MM): 8.852-Week Price Range: $25.36-$14.00Price/Earnings Ratio: 35.4Stated Book Value Per Share: $7.76

INVESTMENT RESEARCH SUMMARY PRICED DECEMBER 12, 2013

- 8 -

Coach, Inc.

Balance Sheet Data Catalysts/Highlights

(in millions) 9/30/13 2012 2011 • Despite a slowdown in growth, COH continues to possess a strong market position, attractive margins, and solid cash flow.

• Recent sales weakness in North America has penalized share performance, serving to overshadow future growth opportunities.

• We believe COH is approaching an inflection point in terms of growth expectations and valuation, creating a very favorable risk/reward scenario for long-term investors.

Cash $ 855 $ 1,135 $ 917 Goodwill 373 345 376 TOTAL ASSETS $ 3,487 $ 3,532 $ 3,104 Long Term Debt $ 0 $ 1 $ 1 Shareholders Equity 2,379 2,409 1,993 TOTAL LIABILITIES AND SHAREHOLDERS EQUITY

$ 3,487 $ 3,532 $ 3,104

Fiscal Year Ending June 30

P&L Analysis ($ in millions except per share items)

2013 2012 2011 2010 Revenues 5,075 4,763 4,159 3,608 Net Income 1,034 1,039 881 735 Earnings Per Share 3.61 3.53 2.92 2.33 Dividends Per Share 1.24 0.98 0.68 0.38 Price Range 61.94-45.87 79.70-48.24 69.20-45.70 58.55-32.96

INVESTMENT RATIONALE

Coach Inc. is a well established provider of high-end accessories and gifts for men and women, such as leather handbags, travel accessories, shoes, watches, jewelry and other related items. Much of Coach’s notable track record has been characterized by robust growth and profitability. However, COH’s stock performance and operational trajectory have significantly moderated during more recent years due to investor concerns about slowing growth and increased competition in the North American market (69% of total sales). Although past growth rates are unlikely to be repeated (EBIT CAGRs over 20%), we believe the Company’s competitive position and future growth outlook are being overlooked. Moreover, the stock’s weak recent performance (down over 10% since early 2013) has created an opportunity to own an attractive business at a very reasonable price.

Just within the past 10-20 years, new competitors such as Kate Spade, Michael Kors, and Tory Burch have established themselves as successful operators within the U.S. market for luxury handbags and accessories. However, it is important to recognize that COH has faced its share of challenges in the past, and it has a record of successfully adapting to a changing environment. COH’s current strategy is designed to provide customers with innovative and unique products through its well established distribution channels (both direct and wholesale), that are consistent with COH’s well known market identity. The Company has an industry presence characterized by both a leading market share and global reach (about a third of sales are derived from overseas). The firm continues to hold #1 share in the U.S. luxury handbag market, and is the leading foreign firm in Japan.

Looking ahead, a combination of international opportunities and product line expansion will likely be the Company’s primary growth drivers. We would highlight the Asian market as an area of particular interest that will likely attract continued attention. The overall size of the market for premium handbags and accessories in Asia now stands at approximately $12 billion, and the growth rates in many of the region’s emerging markets remain in the double-digits.The Chinese market is an especially important growth driver, and COH has been building its presence there for several years. The number of COH stores in China has more than doubled since just FY 2010, and longer-term prospects in other emerging markets such as Latin America are also promising.