Embed Size (px)

Citation preview

Volume XV, Issue 1

April 2016

Volume XV, Issue 1 April 2016

Economic Policy Group

Monetary Authority of Singapore

ISSN 0219-8908

Published in April 2016

Economic Policy Group Monetary Authority of Singapore

http://www.mas.gov.sg

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanised, photocopying, recording or otherwise, without the prior written permission of the copyright owner except in accordance with the provisions of the Copyright Act (Cap. 63). Application for the copyright owner's written permission to reproduce any part of this publication should be addressed to:

Economic Policy Group Monetary Authority of Singapore 10 Shenton Way MAS Building Singapore 079117

Printed by Xpress Print Singapore

Monetary Authority of Singapore Economic Policy Group

Contents

Preface i

Monetary Policy Statement ii-iv

1 The International Economy 2 1.1 G3 Economies 3

1.2 Asia 8

1.3 Global Inflation 13

Box A: China And The Global Export Slowdown 15

2 The Singapore Economy 18 2.1 Recent Economic Developments 19

2.2 Economic Outlook 28

Box B: Evaluating Probability Forecasts From The 34

MAS Survey Of Professional Forecasters

3 Labour Market And Inflation 42 3.1 Labour Market 43

3.2 Consumer Price Developments 49

4 Macroeconomic Policy 58 4.1 Monetary Policy 59

4.2 Fiscal Policy 67

Special Features Special Feature A: Singapore’s Monetary History: The Quest 78

For A Nominal Anchor

Box C: A Model-based Ex-post Evaluation Of 84

Singapore’s Monetary Policy

Special Feature B: The Great Recession: Earthquake For Macroeconomics 87

Special Feature C: Corporate Governance And The Finance Sector: 97

An Asian Perspective

Statistical Appendix 112

Macroeconomic Review, April 2016

Monetary Authority of Singapore Economic Policy Group

LIST OF ABBREVIATIONS

3MMA three-month moving average

ACU Asian Currency Unit

AE advanced economies

ASEAN Association of Southeast Asian Nations

BOJ Bank of Japan

COE Certificate of Entitlement

CPF Central Provident Fund

CPI consumer price index

DBU Domestic Banking Unit

ECB European Central Bank

EIA Energy Information Administration

EPG Economic Policy Group

FI Fiscal Impulse

FOMC Federal Open Market Committee

GFC Global Financial Crisis

GFCF gross fixed capital formation

GOS gross operating surplus

GST Goods and Services Tax

ICT information and communications technology

IMF International Monetary Fund

IT information technology

ITP Industry Transformation Programme

LIBOR London interbank offered rate

MMS Monetary Model of Singapore

MNC multinational corporation

m-o-m month-on-month

NEA Northeast Asian economies

NEER nominal effective exchange rate

OECD Organisation for Economic Cooperation and Development

OPEC Organisation of the Petroleum Exporting Countries

PBOC People’s Bank of China

PMET professionals, managers, executives and technicians

PMI Purchasing Managers’ Index

PPI producer price index

q-o-q quarter-on-quarter

REER real effective exchange rate

SA seasonally adjusted

SAAR seasonally adjusted annualised rate

SIBOR Singapore interbank offered rate

SME small and medium enterprise

SPF Survey of Professional Forecasters

TFP total factor productivity

UBC unit business cost

ULC unit labour cost

WTO World Trade Organisation

y-o-y year-on-year

Preface i

Monetary Authority of Singapore Economic Policy Group

Preface The Macroeconomic Review is published twice a year in conjunction with the release of the MAS Monetary Policy Statement. The Review documents the Economic Policy Group’s (EPG) analysis and assessment of macroeconomic developments in the Singapore economy, and shares with market participants, analysts and the wider public, the basis for the policy decisions conveyed in the Monetary Policy Statement. It also features in-depth studies undertaken by EPG on important economic issues facing Singapore. In this 45th year of the MAS, Special Feature A provides a broad historical narrative of Singapore’s search for a nominal anchor from the early 19th century up to the present, including the considerations leading to the adoption of the unique exchange-rate centred monetary policy framework. We are pleased to have Professor Lawrence Christiano of Northwestern University write Special Feature B in this issue, titled “The Great Recession: Earthquake for Macroeconomics”. We are also grateful to Professor Randall Morck of University of Alberta Business School and Professor Bernard Yeung of NUS Business School for contributing Special Feature C, which provides an Asian perspective on corporate governance with some focus on the role of the financial sector. The Review was edited by Associate Professor Peter Wilson. The data used in the Review was drawn from the following government agencies, unless otherwise stated: BCA, CAAS, CPF Board, DOS, EDB, IDA, IE Singapore, LTA, MOF, MOM, MND, MPA, MTI, STB and URA. The Review can be accessed in PDF format on the MAS website: http://www.mas.gov.sg/Monetary-Policy-and-Economics/Monetary- Policy/Macroeconomic-Review. Hard copies of the Review may also be purchased at major bookstores, ordered online (http://www.marketasiabooks.com), or on an annual subscription basis (details can be found on the last page).

ii Macroeconomic Review, April 2016

Monetary Authority of Singapore Economic Policy Group

14 April 2016

Monetary Policy Statement

INTRODUCTION 1. In October 2015, MAS kept the Singapore dollar nominal effective exchange rate (S$NEER) policy band on a modest and gradual appreciation path, but reduced its rate of appreciation slightly. There was no change to the width of the policy band or the level at which it was centred. This policy stance was assessed to be supportive of economic growth into 2016, while ensuring price stability over the medium term.

Chart 1

S$ Nominal Effective Exchange Rate (S$NEER)

2. Since October 2015, the S$NEER has fluctuated around a strengthening trend, appreciating from below the mid-point of the policy band to the upper half of the band. Following a bout of depreciation pressures in January 2016 amid heightened global risk aversion, the S$NEER strengthened on broad-based US$ weakness, as financial markets revised downwards their expectations of the US Federal Reserve’s pace of interest rate normalisation. However, the average level of the S$NEER over the last six months as a whole has been unchanged compared to the six months prior to October 2015. 3. The three-month S$ SIBOR rose from 1.07% as at end-October 2015 to 1.25% by end-January 2016, before edging down to 1.06% as at end-March 2016.

OUTLOOK

4. Compared to expectations in October 2015, the Singapore economy is now projected to expand at a more modest pace this year, against the backdrop of a less favourable external environment. MAS Core Inflation is likely to pick up gradually over 2016 as the disinflationary effects of Budgetary and

98

100

102

104

106

108

Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr

Ind

ex (

2–5

Ap

r 2

01

2 A

vera

ge =

100

)

2012

Appreciation

Depreciation

indicates release of Monetary Policy Statement

20142013 2015 2016

Monetary Policy Statement iii

Monetary Authority of Singapore Economic Policy Group

other one-off measures fade. However, the increase in core inflation will be milder than earlier expected, on account of a downward revision in the outlook for global oil prices, a reduction in labour market tightness, and weaker consumer sentiment. CPI-All Items inflation will remain negative throughout 2016. Over the medium term, core inflation is expected to average slightly below 2%.

Growth

5. According to the Advance Estimates released by the Ministry of Trade and Industry today, the Singapore economy registered 0% growth on a quarter-on-quarter seasonally adjusted annualised basis in Q1 2016, following the 6.2% expansion in Q4 2015. While output in the manufacturing sector increased after six quarters of contraction, this largely reflected a temporary ramp-up in pharmaceutical production in January. The performance of the rest of manufacturing and the trade-related services sectors continued to be held down by sluggish external conditions. Re-export volumes registered sequential contraction on average over the first two months of 2016. There was also a pullback in financial services activity from the previous quarter, amid the slowdown in bank lending to the region. 6. The outlook for the global economy has dimmed since October. The pace of expansion in the US economy is expected to be more modest than earlier anticipated on account of weakening investment and exports, even as the strengthening labour market continues to underpin private consumption. In the Eurozone and Japan, economic activity will be dampened by their appreciating currencies and weak external demand, notwithstanding recent efforts to boost growth through more accommodative monetary policy. China’s growth momentum is likely to moderate, as its services sector expansion is unlikely to be sufficiently strong to offset faltering industrial activity, amid supply gluts and weak global demand. The slower pace of growth in the G3 and China will in turn weigh on trade-related activity in the rest of Asia. 7. In the quarters ahead, subdued growth in Singapore’s major trading partners will continue to pose cyclical headwinds to the external-oriented sectors. Within manufacturing, the transport engineering and some precision engineering clusters will be hampered by the cutback in oil exploration activities, while the weakness in IT production and its supporting industries will also persist due to tepid final demand and ongoing corporate restructuring. In comparison, the domestic-oriented sectors should continue to provide some support to the economy, underpinned by sustained demand for healthcare and education services, as well as public infrastructure spending. The retail and real estate segments, however, are likely to soften as economic sentiment weakens. Overall, the Singapore economy is likely to grow at a modest pace of 1–3% in 2016, and the level of activity will be slightly below potential.

Inflation

8. MAS Core Inflation, which excludes the costs of private road transport and accommodation, has been subdued. The slight uptick in core inflation to 0.4% y-o-y in January–February 2016 from 0.2% in Q4 2015 was largely due to the smaller decline in the prices of oil-related items on a year-ago basis, as well as the dissipation of temporary disinflationary effects from Budgetary and other one-off measures, such as the enhanced medication subsidies introduced at the beginning of 2015. Meanwhile, CPI-All Items inflation remained muted at −0.7% y-o-y in January–February, as housing rentals and car prices fell further.

iv Macroeconomic Review, April 2016

Monetary Authority of Singapore Economic Policy Group

9. External sources of inflation will stay benign given ample supply buffers in the commodity markets and weak global demand conditions. Since October 2015, global oil prices have fallen considerably and despite the recent pickup, are likely to average lower for the whole of 2016 compared to last year. Domestic cost pressures are also expected to moderate in line with emerging slack in the economy. The domestic labour market is expected to see slightly reduced tightness, with wage growth projected to slow further over the course of 2016 amid softer employment conditions. While the resident unemployment rate has been fairly stable in recent quarters, it could increase slightly in the period ahead alongside a gradual rise in redundancies and declining job vacancies. At the same time, the pass-through of business costs to consumer prices will be constrained by the subdued growth environment. All in, MAS Core Inflation will rise over the course of this year at a milder pace than earlier anticipated. For the whole of 2016, it should come in within the lower half of the 0.5–1.5% forecast range, barring upside surprises to global oil prices. Over the medium term, core inflation is likely to average slightly below 2%. 10. Car prices and housing rentals will continue to dampen overall inflation amid the expected increase in the supply of COEs and newly-completed housing units, respectively. The 2016 forecast for CPI-All Items inflation was revised down to −1.0–0% in February, taking into account the step-down in global oil prices in late 2015 and the sharp decline in COE premiums at the beginning of this year. This forecast for headline inflation remains unchanged.

MONETARY POLICY

11. The Singapore economy is projected to expand at a more modest pace in 2016 than envisaged in the October policy review. MAS Core Inflation should also pick up more gradually over the course of 2016 than previously anticipated, and is now likely to fall below 2% on average over the medium term. 12. MAS will therefore set the rate of appreciation of the S$NEER policy band at zero percent, beginning 14 April 2016. This is not a policy to depreciate the domestic currency, and only removes the modest and gradual appreciation path of the S$NEER policy band that was in place. 13. The width of the policy band and the level at which it is centred will be unchanged. 14. This move to a neutral policy stance of zero percent appreciation follows the measured steps that MAS has taken to reduce the rate of appreciation of the policy band in January and October 2015 respectively.1 The actual outcome of S$NEER movements over the six months since October 2015 has in fact been a zero percent appreciation compared to the preceding six-month period. The cumulative effects of past S$NEER movements and the new policy path will continue to ensure price stability over the medium term.

1 MAS had adopted a modest and gradual appreciation path for the S$NEER policy band since April 2010.

Chapter1TheInternationalEconomy

2 Macroeconomic Review, April 2016

Monetary Authority of Singapore Economic Policy Group

1 The International Economy

Global Growth To Remain Subdued In 2016

The global economy slowed in Q4 2015, as growth decelerated in the advanced economies while remaining below trend in Asia ex-Japan. Economic activity in the US and Japan was dampened, in part, by weather-related factors, even as the Eurozone maintained a steady pace of growth. Meanwhile, China’s ongoing restructuring has put its economy on a weakening growth trajectory, with a pullback in industrial output only partially compensated by a better-performing services sector. Elsewhere in the region, economic activity was weighed down by the turning of the financial, credit and commodity cycles. Nevertheless, generally resilient domestic demand has helped to support growth, with policy stimulus providing a further boost in some countries. In 2016, the outlook is lacklustre growth and low inflation globally. The post-GFC years have been characterised by low nominal GDP growth in many advanced economies. Confronted with weak demand from these economies, as well as China, growth in the rest of emerging Asia is expected to stay tepid. Moreover, with the tightening of global financial conditions, domestic demand growth in the region will be impeded by rising debt service burdens. The softness in emerging Asia’s growth will, in turn, spill back into activity in the advanced economies. Consequently, the prospects for the global economy have dimmed, as compared to the last Review. Growth is projected at 3.8% in 2016, slightly below the 3.9% recorded last year, before edging up marginally to 4.0% in 2017. (Table 1.1) Meanwhile, global inflation is likely to stay muted in 2016, but may rise further next year, alongside the mild pickup in economic activity.

Table 1.1 Global GDP Growth

(%)

Q3 2015 Q4 2015 2015 2016F 2017F

q-o-q SAAR y-o-y

Total* 4.0 3.7 3.9 3.8 4.0

G3* 1.5 0.8 1.6 1.5 1.7 US 2.0 1.4 2.4 2.0 2.4 Japan 1.4 −1.1 0.5 0.6 0.5 Eurozone 1.2 1.3 1.5 1.5 1.6

NEA-3* 2.1 1.7 1.9 1.8 2.3 Hong Kong 2.2 0.9 2.4 1.7 2.0 Korea 5.0 2.7 2.6 2.6 2.8 Taiwan −0.2 2.2 0.7 1.4 2.3

y-o-y

ASEAN-4* 4.5 4.6 4.6 4.4 4.7 Indonesia 4.7 5.0 4.8 5.0 5.3 Malaysia 4.7 4.5 5.0 4.2 4.4 Philippines 6.1 6.3 5.8 6.0 5.9 Thailand 2.9 2.8 2.8 2.9 3.3

China 6.9 6.8 6.9 6.5 6.3 India** 7.7 7.3 7.2 7.6 7.7

Source: CEIC, Consensus Economics, Apr 2016 and EPG, MAS estimates

* Weighted by shares in Singapore’s NODX.

** Figures are reported on a Financial Year basis; FY2017 refers to the period from April

2016 to March 2017.

The International Economy 3

Monetary Authority of Singapore Economic Policy Group

1.1 G3 Economies

Low Inflation Amid Growth Underperformance

The G3 economies ended 2015 on a subdued note, with weaker-than-expected GDP outturns in Q4. This reflected, to some extent, the impact of one-off factors such as unusual weather, which held back spending on warm clothing and utilities in the US and Japan. Nonetheless, expectations are for the US to expand at a moderate pace this year, on the back of a strong labour market and modest income growth. Concerns over the strength of the recovery in Japan remain, given tentative signs that the pullback in economic activity has carried over into Q1 this year. In the Eurozone, domestic demand will be supported by additional monetary easing measures, but external demand will be adversely impacted by the slowdown in emerging markets. On the whole, GDP growth in the G3 is projected to come in at 1.5% in 2016 and tick up slightly to 1.7% in 2017. This sub-par expansion in output, coupled with below-target inflation, implies that nominal GDP growth in the G3 will stay low in the near term, thus necessitating concerted policy responses.

Growth in the US eased towards the end of 2015 …

US GDP growth slackened to 1.4% q-o-q SAAR in Q4 2015, from 2.0% in the preceding quarter. The slowdown in economic activity was broad-based, with a moderation in personal consumption expenditure growth, a sharper pullback in fixed investment spending, and weaker exports. Consumer spending, which had been the lynchpin of growth through most of 2015, rose by a softer 2.4% q-o-q SAAR in Q4, from 3.0% in the previous quarter. This was partly due to transitory factors, such as unusually warm weather, which lowered utilities spending. Meanwhile, non-residential fixed investment contracted for the first time since Q3 2012, by 2.1% q-o-q SAAR in Q4, as a pullback in oil drilling caused structures and equipment expenditure to decline sharply by 5.1% and 2.1%, respectively. (Chart 1.1) Moreover, the strength of the US dollar, alongside soft global demand, continued to weigh on net exports in Q4, which subtracted 0.1% point from GDP growth.

… but the core strengths of the economy should reassert themselves as the year progresses.

Economic indicators point to modest growth in Q1 2016, with a stronger pickup expected only later this year. There have been sustained improvements in the labour market in the early months of 2016, with employment growth averaging 209,000 jobs per month over Jan–Mar. This strength in hiring has, in turn, drawn more people back into the workforce, resulting in a rise in the labour force participation rate to 63.0% in March this year. (Chart 1.2) Indeed, the participation

Chart 1.1

Decomposition of US Non-residential Fixed Investment Growth in 2015

Source: Haver Analytics and EPG, MAS estimates

Chart 1.2 Change in US Non-farm Payrolls and

Labour Force Participation Rate

Source: Haver Analytics and EPG, MAS estimates

-3

-2

-1

0

1

2

3

4

Ave Q1–Q3 Q4

% P

oin

t C

on

trib

uti

on

to

QO

Q S

AA

R G

row

th

Equipment

Intellectual Property

-3-2-101234

Ave Q1-Q3 2015 Q4

% P

oin

t C

on

trib

uti

on

to

QO

Q S

AA

R

Gro

wth

Equipment

Intellectual Property

Structures

Non-residential Fixed Investments

50

150

250

350

62

63

64

65

2012 2013 2014 2015 2016

Pe

rso

ns

(Th

ou

san

d, 3

MM

A)

Pe

r C

ent

Mar

Labour Force Participation Rate

Change in Non-farmPayrolls (RHS)

4 Macroeconomic Review, April 2016

Monetary Authority of Singapore Economic Policy Group

rate has been increasing steadily since September 2015, after being on a downtrend following the GFC. Nevertheless, wage growth has been relatively weak, indicating the presence of residual slack in the labour market. On the whole, consumer spending is likely to maintain a moderate pace of expansion and provide the key support to GDP growth in 2016. In comparison, sectors of the US economy that are sensitive to external demand or energy prices will continue to weigh on growth. Net exports will likely be a drag on account of the substantial appreciation of the US dollar in real trade-weighted terms since mid-2014, accentuated by weak foreign demand. Notably, with the exception of the Eurozone, demand for US exports from all other regions, especially China and ASEAN-4, deteriorated further in Q4 2015. (Chart 1.3) In December 2015, the US Federal Reserve raised the Federal funds rate, after maintaining it at near-zero for seven years. The median expectation among FOMC members at that time was for another four rate hikes, amounting to a cumulative 100 bps increase, over the course of 2016. However, at the latest policy meeting in March, the FOMC members slightly lowered their growth and inflation forecasts for 2016 and cut back on the projected number of rate hikes to just two this year. Although core inflation has picked up more recently, the strength of the US dollar is anticipated to help keep inflation in check and there appears to be room for further employment growth before marked increases in labour costs are triggered. All in, US GDP growth is expected to come in at 2.0% in 2016, before rising to 2.4% in 2017.

Eurozone growth was steady in Q4.

Eurozone GDP expanded by 1.3% q-o-q SAAR in Q4 2015, similar to the outturn in the previous quarter. Although this was marginally higher than the average of 1.2% since the recovery from the sovereign debt crisis in Q2 2013, growth momentum decelerated through the course of 2015, from an average of 1.9% in H1 to 1.2% in H2. In terms of expenditure, robust domestic demand continued to be offset by the negative effect from trade, although there was a discernible shift in the former’s underlying composition. Private consumption growth—the main driver of the recovery thus far—eased across the four major Eurozone economies, in spite of a pickup in wage

Chart 1.3 Growth in US Exports by Region

Source: Haver Analytics and EPG, MAS estimates

* North America refers to Canada and Mexico.

2015 Q2 Q3 Q4

-40

-30

-20

-10

0

10

20

30

% Q

OQ

SA

AR

ASEAN-4 NEA-3 China Eurozone North America*

The International Economy 5

Monetary Authority of Singapore Economic Policy Group

growth and lower oil prices. (Chart 1.4) Notably, consumer spending in France fell into outright contraction in the aftermath of the Paris terror attacks in November. In contrast, investment spending in the Eurozone, which has been subdued over the past two years, rebounded strongly (except in Spain), to 5.4% in Q4, from 1.7% in the previous quarter. This was due to a rise in construction-related activity, albeit from a low base, as well as a tentative pickup in machinery and equipment investment across the region as business confidence improved.

A challenging external environment will pose a drag on Eurozone growth.

The Eurozone economy should expand at a modest pace in 2016, with growth underpinned by private consumption and a slightly expansionary fiscal impulse. Notwithstanding the recent dent in consumer confidence caused by elevated financial volatility earlier this year, household spending should continue to be supported by moderate wage growth, low oil prices and steady employment gains. Moreover, the fiscal stance will be fairly accommodative, in view of refugee-related spending in Germany, alongside some easing of fiscal tightening measures in Italy and Spain. Nonetheless, the region faces a challenging external environment. Exports from the Eurozone to large emerging markets, such as China and Russia, as well as shipments to advanced economies such as the US, may continue to underperform. The ECB had noted that risks to growth are tilted to the downside, which could exacerbate deflationary pressures. In response, the ECB eased monetary policy further in March 2016: interest rates were lowered, including the rate on the deposit facility, which was cut by 10 bps to an unprecedented −0.4% (Chart 1.5); the asset purchase programme was expanded to €80 billion per month and will include purchases of investment-grade bonds issued by non-bank corporations; and a series of four targeted longer-term refinancing operations (TLTRO II) was launched. In order to spur economic activity and raise the inflation rate back to target, ECB President Draghi has committed to keep interest rates “very low, for a long period of time”. On balance, growth projections for the Eurozone are 1.5% this year and 1.6% in 2017.

Chart 1.4

Eurozone Private Consumption and Investment

Source: Eurostat

Chart 1.5 Eurozone’s Key Policy Rates and

Asset Purchase Programme

Source: ECB

-2

0

2

4

6

8

QO

Q S

AA

R %

Gro

wth

Q3 2015 Q4 2015

Consumption Investment

2014 May Sep 2015 May Sep 2016

0

400

800

1200

-0.5

0.0

0.5

1.0€

Bill

ion

% P

er

An

nu

m

Holdings under Asset Purchase Programme (RHS)Deposit RateRefinancing RateMarginal Lending Rate

Mar

6 Macroeconomic Review, April 2016

Monetary Authority of Singapore Economic Policy Group

Growth prospects for Japan have been downgraded.

Following an expansion of 1.4% q-o-q SAAR in Q3 2015, Japan’s economy contracted by 1.1% in Q4 due to a pullback in private consumption, with unusually warm weather dampening spending on winter goods and heating. (Charts 1.6 and 1.7) Meanwhile, aggregate investment spending increased by 0.8% q-o-q SAAR in Q4, supported mainly by the non-residential segment, while residential investment contracted by 4.7%, following three quarters of increase. Overall exports fell by 3.3%, as a decline in shipments to Asian markets more than offset a pickup in volumes to the advanced economies. Private spending has been lacklustre in Japan, especially after the consumption tax hike in April 2014. Slower wage growth and higher food prices have also curtailed real household expenditure on non-food consumption items, as more spending was channelled to food expenses. (Chart 1.7) Against this backdrop of flagging domestic demand and lower-than-expected inflation outcomes, the Bank of Japan (BOJ) enhanced its Quantitative and Qualitative Monetary Easing (QQE) policy in October 2014 with higher asset purchases. This was followed by a further move in January 2016 to introduce a negative interest rate policy, which will apply to financial institutions’ funds in excess of average outstanding balances at the central bank in 2015 and selected portions of reserves. Working in tandem with asset purchases, the policy aims to further reduce rates across the entire yield curve and spur spending by firms and households. Looking ahead, domestic demand is projected to recover, albeit gradually, on the back of healthy corporate profits as well as a modest pickup in wage growth. The further loosening of financial conditions through negative interest rates is also expected to have some stimulative effects, especially on investment. However, risks to Japan’s growth outlook include heightened uncertainty in the global economy and the recent appreciation of the yen, which could adversely affect firms’ profits and hold back the pace of capital expenditure and wage increases. All in, the Japanese economy is projected to grow by 0.6% in 2016, before easing to 0.5% in 2017, mainly due to the effects of the planned consumption tax hike.

Chart 1.6

Contribution to Japan’s GDP Growth

Source: CEIC

Chart 1.7

Real Household Expenditure in Japan

Source: CEIC

-15

-10

-5

0

5

10

2012 2013 2014 2015 Q4

% P

oin

t C

on

trib

uti

on

to

Q

OQ

SA

AR

Gro

wth

Private Consumption Govt Consumption

Investment Net Exports

GDP

85

90

95

100

105

110

2010 2011 2012 2013 2014 2015

Ind

ex

(20

10

=10

0),

SA

Q4

Total Expenditure

FoodExpenses

Fuel Charges

Clothes

The International Economy 7

Monetary Authority of Singapore Economic Policy Group

Slow growth and low inflation necessitate concerted policy responses by

the advanced economies.

More than seven years after the collapse of Lehman Brothers, a strong recovery has yet to materialise in the advanced economies. In the aftermath of the GFC, debt overhang, sluggish investment and hysteresis effects associated with increases in long-term unemployment have contributed to a reduction in trend real GDP growth, as well as a notable decline in nominal GDP growth rates in the G3. (Chart 1.8) The deceleration in nominal growth, reflecting both low growth and muted inflation, is of particular concern given the elevated stock of private and public sector debt in these economies. (Chart 1.9) With nominal interest rates largely constrained by the zero lower bound, low (and at times negative) inflation implies that the real rate of interest remains too high. Apart from restraining current spending, high real interest rates also raise debt servicing and repayment obligations, especially with a slowdown in nominal GDP growth depressing corporate revenues. Going forward, more needs to be done by the G3 economies on the policy front to raise growth prospects over the longer term. While monetary policy has shouldered most of the burden in supporting aggregate demand in the short term, there is insufficient progress on improving supply-side growth drivers, without which sustained long-term growth will not be achievable. A concerted and coordinated package of measures that includes monetary accommodation, fiscal stimulus and structural reforms, aimed at enhancing economic efficiency and removing impediments to growth (such as labour and product market rigidities), will have a better chance of lifting investment and economic growth.

Chart 1.8

G3 Nominal GDP Growth

Source: CEIC and EPG, MAS estimates

Note: The slight uptick in nominal GDP growth in Japan in 2014 and 2015 was due, in large part, to the 3% points hike in the consumption tax to 8% in April 2014, which led to a one-off increase in the price level.

Chart 1.9

G3 Non-financial Private Sector Debt

Source: Institute of International Finance

-10

-5

0

5

10

15

1980 1985 1990 1995 2000 2005 2010 2015

% Y

OY

US

Japan

Eurozone

40

60

80

100

120

140

2000 2005 2010 2015

% o

f G

DP US Households

Eurozone Households

Japan Non-financial Corporates

Japan Households

US Non-financial Corporates

Eurozone Non-financial Corporates

Q4

8 Macroeconomic Review, April 2016

Monetary Authority of Singapore Economic Policy Group

1.2 Asia

Growth Outlook Dims With Rising Financial Headwinds

In Asia ex-Japan, growth was underpinned by relatively resilient domestic demand in Q4 2015, which provided some buffer against lacklustre export performance. Although further pump-priming measures should help to put a floor on China’s growth in 2016, the economy’s rebalancing continues to impact the region through lower import demand. In the coming quarters, Asia ex-Japan is expected to register tepid growth, given further moderation in the Chinese economy and muted imports of investment goods from the advanced economies. However, the weakness in the export sector will be partly offset by a revival of public investment in most ASEAN economies and India. The outlook for private investment is much less sanguine. First, the turn in the global financial cycle, triggered by the US interest rate hike in December 2015, will raise the debt-servicing burden of corporates which had borrowed heavily during the upswing of the cycle amid low global interest rates. Second, credit growth has waned alongside intermittent capital outflows and tightening financial conditions. Third, the end of the commodity super-cycle has crimped corporate and fiscal revenues in a number of economies. This confluence of events has intensified the challenges facing the region, and growth in Asia ex-Japan is projected to slow to 4.6% in 2016 from 4.7% last year, before picking back up mildly to 4.7% in 2017.

China’s growth will be cushioned by policy easing.

The Chinese economy experienced a gradual slowdown over the course of 2015, as the divergence between its goods-producing and services industries widened. In Q4 2015, China’s GDP decelerated to 6.8% on a y-o-y basis and to 1.5% on a q-o-q SA basis, from 6.9% and 1.8% in Q3, respectively. (Chart 1.10) For the year as a whole, the manufacturing and construction sectors grew on average by a tepid 6.0%, weighed down by excess industrial capacity and sluggish demand. In comparison, growth in the services sector came in at 8.3% y-o-y, spurred by capital market-driven activity in the financial services sector.

China’s economy slowed further in Q1 2016 to 6.7% y-o-y, with sequential growth momentum easing to 1.1% q-o-q SA. Nonetheless, investment in fixed assets grew by 10.7% y-o-y in Q1, up from 10% in 2015, on the back of a property market recovery and faster infrastructure construction. Meanwhile, retail sales rose at a slightly slower pace of 10.3% y-o-y compared to 10.7% in 2015, alongside sluggish consumer confidence and a softer labour market. (Chart 1.11)

In the quarters ahead, the Chinese authorities are expected to continue to apply monetary and fiscal stimuli to the economy in a measured manner, to ease the adjustment costs arising from structural reforms and industrial layoffs. Besides successively lowering the

Chart 1.10 China’s GDP Growth

Source: CEIC and EPG, MAS estimates

Chart 1.11

Change in Employment in China by Sector

Source: CEIC

2012 2013 2014 2015 2016Q1

0.5

1.0

1.5

2.0

2.5

6.5

7.0

7.5

8.0

8.5

Pe

r C

en

t

Pe

r C

en

t

YOY

QOQ SA (RHS)

2009 2010 2011 2012 2013 2014 2015

-20

-15

-10

-5

0

5

10

15

20

Mill

ion

Tertiary Secondary Primary

The International Economy 9

Monetary Authority of Singapore Economic Policy Group

benchmark lending rate and the reserve requirement ratio for banks over the past year, the central government recently announced a more expansionary fiscal stance for 2016 by targeting a budget deficit amounting to 3% of its GDP. In addition, direct fiscal spending will be complemented by off-budget measures, such as local government bond issuances, the proceeds from which can be used to fund infrastructure works. Nonetheless, given weak domestic and external demand, the industrial sector faces continuing overcapacity in heavy industries and electronics. The hitherto robust expansion of the overall services sector will not be sufficient to offset the effects of sluggish exports and manufacturing output, as services are not fully insulated from the industrial weakness. Activities that move in sync with manufacturing, such as transportation and wholesale trade services, will be adversely affected. Increased layoffs in the heavy industries will also dampen wage growth and weigh on private consumption. Taking these factors into account, China’s growth is expected to come in at 6.5% this year, before slowing further to 6.3% in 2017. The deceleration in the Chinese economy has been a contributor to the weakness in global trade in the last few quarters, dampening the growth outcomes of key trading partners across the world. Box A highlights the differential impact of this development on various countries and regions.

India is the bright spot in the region.

India’s GDP expanded at a firm 7.3% y-o-y in Q4 2015, though this was a slight moderation from the 7.7% in the previous quarter. Household expenditure growth rose to 6.4% y-o-y from 5.6% over the same period, as higher urban discretionary spending more than compensated for weak rural demand. However, the investment recovery seen earlier faltered somewhat, as gross fixed capital formation growth slipped to 2.8% y-o-y in Q4 2015 from 7.6% in the preceding quarter, largely on account of weak private investment. (Chart 1.12) In the near term, the Indian economy will remain on a modest expansion path, despite a weak external environment. Economic activity will continue to be driven by private consumption, which has received a fillip from lower energy prices and higher real wages.

Chart 1.12

India’s Outstanding Investment by Ownership

Source: Centre for Monitoring Indian Economy

0

30

60

90

120

150

180

2011 2012 2013 2014 2015 Q4

INR

Tri

llio

n

Indian Private Sector Foreign Private Sector Government

10 Macroeconomic Review, April 2016

Monetary Authority of Singapore Economic Policy Group

Looking ahead, an increase in public infrastructure spending and official efforts to improve the business environment should gradually crowd in private investment. Encouragingly, foreign direct investment hit a record high of US$39 billion in 2015, a 37% surge from the previous year. Nonetheless, weakness in both corporate financial and public bank balance sheets will constrain a sharper pickup in growth. To date, Indian banks have passed on less than half of the Reserve Bank of India’s (RBI) cumulative 150 bps reduction in the policy rate since the beginning of 2015, with median base lending rates having fallen by only 60 bps. (Chart 1.13) Notwithstanding a challenging global growth environment, GDP growth is projected to come in at a solid 7.6% in FY2016 and rise further to 7.7% in the following year.

Growth projections for the NEA-3 have been revised down sharply.

The NEA-3 region as a whole grew by 1.7% q-o-q SAAR in Q4 2015, down from a 2.1% expansion in the preceding quarter. Weak external demand was behind the slowdown. In Korea and Taiwan, the weakness in shipments of capital goods and heavy equipment has extended to electronics, as industrial upgrading in China’s electronics industry reduced the mainland’s reliance on imported Korean and Taiwanese components. As a result, Korea’s growth decelerated to 2.7% q-o-q SAAR in Q4 from 5.0% in Q3. However, Taiwan’s GDP expansion picked up to 2.2% q-o-q SAAR on the back of stimulus-driven private consumption expenditure. Hong Kong’s growth eased to 0.9% q-o-q SAAR in Q4 from 2.2% in the previous quarter, owing to falling retail sales and shrinking tourist numbers, particularly from mainland China.

The persistently weak export performance of Korea and Taiwan is beginning to weigh on domestic economic activity, as shown by signs of softness in their manufacturing sectors and labour markets. Hong Kong, which has been a popular destination for mainland tourists and an important transhipment hub for China, is also likely to face challenges. The latest PMI reading for Hong Kong deteriorated further in March 2016, although those for Korea and Taiwan saw some improvement. (Chart 1.14) Overall, the short-term outlook for the NEA-3 has dimmed progressively, resulting in successive downgrades in growth projections for the region. (Chart 1.15) Accordingly, consensus growth forecasts for 2016 and 2017 have been lowered to 1.8% and 2.3%, respectively, from 2.2% and 2.5% in January.

Chart 1.13

India Interest Rates

Source: CEIC and EPG, MAS estimates

Chart 1.14 NEA-3 Manufacturing PMIs

Source: Markit

* Whole economy.

Chart 1.15 NEA-3 GDP Growth Projections for 2016

Source: Consensus Economics

1.0

1.5

2.0

2.5

3.0

3.5

5

7

9

11

13

15

2012 2013 2014 2015 2016

Pe

r C

ent

Pe

r C

ent

Spread between the Two Rates (RHS)

RBI Repo Rate

Five Major Bank Base Rate

Mar

44

46

48

50

52

54

2015 Mar May Jul Sep Nov 2016 Mar

Ind

ex,

>5

0=E

xpan

sio

n

Korea

Taiwan

Hong Kong*

0

1

2

3

4

Korea Hong Kong Taiwan

% Y

OY

Apr 15 Oct 15 Apr 16Projection as of:

The International Economy 11

Monetary Authority of Singapore Economic Policy Group

P

ASEAN-4 will deliver below-trend growth.

GDP growth in the ASEAN-4 held steady at 4.6% y-o-y in Q4 2015, as a pickup in domestic demand alleviated the negative impact of a slowdown in exports. Across the region, private consumption growth held firm or strengthened, supported by resilient labour markets and the boost to real incomes from a renewed decline in oil prices. In Malaysia and Thailand, household spending was also lifted by the frontloading of vehicle purchases ahead of tax revisions in 2016. Bolstered by robust growth in government development expenditure, investment surged in Indonesia and Thailand, and rose at a creditable pace in the Philippines. (Chart 1.16) Trade performance, however, diverged across the region, largely reflecting variations in the composition of exports. Goods exports from Malaysia and the Philippines expanded in the past two quarters, supported by firmer demand for high-tech products. (Chart 1.17) In comparison, goods exports declined in Indonesia and Thailand, weighed down by falling shipments of mining and agricultural products, respectively, while exports of lower value-added manufactured goods stayed weak. The Philippines benefited from solid growth in services exports, due to higher tourism receipts and business services earnings. In comparison, the surge in Thailand’s services exports faded in Q4 2015 as tourist arrivals slowed following the rebound in Q1–Q3. Economic growth in the ASEAN-4 region is expected to ease further this year, given the downbeat global outlook and slowing domestic demand in some economies. Increased government outlays on infrastructure, however, will provide some support in the near term. Malaysia and Thailand will be the most affected by continued softness in external demand, given their greater external orientation and exposure to China’s slowing economy. Meanwhile, Indonesia and the Philippines face firmer growth prospects, with domestic demand underpinned by improving consumer and investor sentiments. In addition, the monetary easing undertaken by Indonesia early this year will provide support to economic activity, while growth in the Philippines will be bolstered by additional fiscal expenditures in the run-up to the presidential election in May. Overall, GDP growth in the ASEAN-4 is projected to slow from 4.6% last year to 4.4% in 2016, before rising to 4.7% in 2017.

Chart 1.16 Growth in ASEAN-4 Public

Capital Expenditure in 2015

Source: CEIC and EPG, MAS estimates

Chart 1.17 Growth in ASEAN-4 Real Exports in 2015

Source: CEIC and EPG, MAS estimates

* Malaysia’s national accounts data does not have a quarterly breakdown into goods and services exports.

Indonesia Malaysia Philippines Thailand

-10

0

10

20

30

40

50

60

70

% Y

OY

Q2 Q3 Q4

Q3 Q4 Q3 Q4 Q3 Q4 Q3 Q4

Indonesia Malaysia* Philippines Thailand

-4

-2

0

2

4

-8

-4

0

4

8

% P

oin

t C

on

trib

uti

on

to

GD

P G

row

th

% Y

OY

Goods Exports Services Exports

Goods & Services Exports Total Export Growth (RHS)

12 Macroeconomic Review, April 2016

Monetary Authority of Singapore Economic Policy Group

Growth in Asia ex-Japan will be hampered by the sharp run-up in debt post-GFC.

The Asia ex-Japan region as a whole is presently adjusting to the turn in the global financial, credit and commodity cycles. For several years following the GFC, low interest rates in the advanced economies, accompanied by quantitative easing and large capital outflows, led to a rapid escalation in debt accumulation in parts of Asia. While the flood of global liquidity helped to fuel growth, the resultant debt build-up is now unravelling at a time when commodity prices have slumped and global interest rates are set to rise. This deleveraging process, combined with slowing activity, could result in a period of weak investment and consumption growth. The increase in leverage is most pronounced in China, where debt rose largely because of a rapid build-up of non-financial corporate borrowing. This reflected, in part, the Chinese government’s efforts to support growth in the aftermath of the GFC through monetary easing. (Chart 1.18) In Korea, Thailand, and Malaysia, household debt has also climbed significantly, to around 70–90% of GDP. In these, and some other Asia ex-Japan countries, debt service ratios in the private non-financial sectors have trended up over the past several years to above pre-GFC levels. (Chart 1.19) Further, countries with a significant proportion of US dollar-denominated debt may face some refinancing difficulties ahead, given the ongoing trend appreciation in the US dollar. (Chart 1.20) In sum, the tightening of global financial conditions in the aftermath of a credit boom in the region could pose a significant drag on growth, although the impact would vary across countries.

Chart 1.18 Asian Debt by Sector

Source: Institute of International Finance and EPG, MAS estimates

Chart 1.19

Selected Asian Debt Service Ratios

Source: Bank for International Settlements

Chart 1.20

US Dollar-denominated Debt in Asia

Source: Haver Analytics, Institute of International Finance, World Bank and EPG, MAS estimates

0

50

100

150

200

250

300

350

% o

f G

DP

050

100150200250300

China Indonesia Korea Malaysia Thailand

% o

f G

DP

HouseholdNon-financial CorporatesGovernmentFinancial Corporates

HouseholdNon-financial CorporatesGovernment

Q3 2007

Financial Corporates

050

100150200250300350

China Indonesia Korea Malaysia Thailand

% o

f G

DP

HouseholdNon-financial CorporatesGovernmentFinancial Corporates

HouseholdNon-financial CorporatesGovernment

Q4 2015

Financial Corporates

China Indonesia Korea Malaysia Thailand

0

5

10

15

20

25

30

2005 2007 2009 2011 2013 2015

Pe

r C

en

t

Malaysia

Thailand

Hong Kong

India

Korea

Q3

0

2

4

6

8

10

12

14

16

China India Indonesia Malaysia Thailand

% o

f G

DP

Public and Publicly Guaranteed Non-financial Corporates

The International Economy 13

Monetary Authority of Singapore Economic Policy Group

1.3 Global Inflation

Weak Global Demand Will Keep Inflation Low

Global inflation has been muted in the last two years, with low oil prices exerting a strong dampening effect and sluggish aggregate demand restraining price pressures. In 2016, headline global inflation is expected to rise slightly to 1.4%, after coming in at 0.9% last year. While underlying price pressures are likely to stay weak on account of subdued growth, the energy-related drag should dissipate with the anticipated stabilisation of oil prices. However, in India and the ASEAN economies, where food forms a larger proportion of the CPI basket, a pickup in food prices due to the El Niño weather phenomenon may contribute to some inflationary pressures. In 2017, global inflation is projected to increase further to 2.1%, as economic activity strengthens and the direct and indirect impact of low energy prices fade.

Inflation remains below target in the G3.

Inflation has begun to rise slightly in the US, while staying muted in the Eurozone and Japan. (Chart 1.21) US headline inflation rose to 1.1% in Q1 2016 from 0.5% in the previous quarter, as the disinflationary effects from energy prices eased further. Core inflation was also higher at 2.2% in Q1 2016, up from 2.0% in the previous quarter, reflecting continued improvements in labour and housing market conditions. In the Eurozone, headline inflation eased, coming in flat in Q1, from 0.2% the quarter before. Despite the recent turnaround in oil prices early this year, muted core inflation prints of 1.0% y-o-y over the past two quarters suggest that the unwinding of excess capacity in the region remains incomplete. Meanwhile, Japan’s headline CPI inflation came in at 0.3% y-o-y in Q4 2015, slightly higher than the 0.2% recorded in the preceding quarter. Lingering downward pressure from low oil prices will continue to depress inflation in 2016, alongside slow GDP growth. Overall, G3 inflation is projected to rise from 0.2% in 2015 to 0.8% in 2016.

Asia ex-Japan inflation is not expected to rise significantly in 2016.

Inflation in Asia ex-Japan is likely to remain muted in the quarters ahead. Energy prices are still low despite some pickup since the beginning of this year (Chart 1.22), which will offset higher import prices caused by the depreciation of some Asian currencies, as well as higher food prices owing to the El Niño weather phenomenon. Accordingly, inflation in Asia ex-Japan is

Chart 1.21

G3 CPI Inflation

Source: CEIC and EPG, MAS estimates

Chart 1.22 Global Oil and Food Price Indices

Source: IMF

* Average of UK Brent, Dubai and West Texas Intermediate oil prices.

2008 2010 2012 2014 2016Q1

-4

-2

0

2

4

6

% Y

OY G3

US

JapanEurozone

2014 Apr Jul Oct 2015 Apr Jul Oct 2016

20

40

60

80

100

120

Ind

ex (

2014

Jan

=100

) Food & Beverages

Oil*

Mar

14 Macroeconomic Review, April 2016

Monetary Authority of Singapore Economic Policy Group

expected to come in at 2.5% this year, close to the 2.4% recorded in 2015. (Chart 1.23) In China, headline inflation tapered alongside falling core inflation, from 1.7% y-o-y in Q3 2015 to 1.5% in Q4, due to a milder rise in food prices. However, in Q1 this year, pork prices surged anew by an average of 24.2%, lifting headline inflation to 2.1%. After worsening to 5.9% in Q4 2015, Chinese PPI deflation slowed in Q1 2016, with the index declining by 4.8% y-o-y. For 2016, China’s headline CPI inflation is projected to average 1.9%. India’s CPI inflation rose to 5.3% y-o-y in Q4 2015 from 3.9% in Q3, largely on account of higher cost of food items. Nonetheless, headline inflation remained unchanged in Q1 2016 as food price inflation held steady. High food prices have been reined in over the past two years, aided by improved food management policies by the government. Consequently, CPI inflation in India is expected to decline further to 5.2% in FY2017. In the NEA-3, inflation ticked up to 1.5% y-o-y in Q1 2016 from 1.1% in the preceding quarter. A cold spell at the turn of the year pushed food prices higher even as low energy prices continued to suppress inflation in the region. Consequently, food price inflation edged up in Korea, Taiwan and Hong Kong in Q1 2016. On the whole, inflation in the NEA-3 is expected to increase to 1.3% in 2016 as the base effect from low oil prices dissipates. Headline inflation in the ASEAN-4 region stayed low in Q1 2016, at 3.0% y-o-y, partly due to weak energy prices, especially in Indonesia. Inflation in Thailand was in negative territory for the fifth consecutive quarter, as sub-par growth depressed underlying price pressures, and energy costs continued to fall sharply. In the Philippines, inflationary pressures stayed weak, held down by low food prices. Meanwhile, Malaysia saw a surge in inflation in Q1, due to the implementation of the Goods and Services Tax (GST) in April 2015, and upward adjustments to administrative prices. For the ASEAN-4 region as a whole, inflation is forecast to come in at 3.2% this year.

Chart 1.23

Asia ex-Japan Inflation

Source: CEIC and EPG, MAS estimates

2008 2010 2012 2014 2016Q1

-4

0

4

8

12

16

% Y

OY

ASEAN-4

NEA-3

China

India

The International Economy 15

Monetary Authority of Singapore Economic Policy Group

Box A

China And The Global Export Slowdown

Introduction

Global trade growth slowed markedly in 2015, with emerging economies recording their first year of contraction in merchandise trade volumes since the GFC. A slowdown in China’s imports, particularly in commodities, has been widely regarded as a key factor behind the trade slowdown. This Box examines developments in China’s imports in recent years and the impact of the deceleration in the country’s growth on the global economy, including across different countries and regions.

Decomposing China’s Import Demand

Despite perceptions that sharply falling Chinese demand was responsible for the plunging prices of commodities, such as oil, the country’s total merchandise import volume contracted only marginally in 2015. After stripping out price effects, imports in real terms fell by 0.7% last year after rising by 3.7% in 2014. (Chart A1) This suggests that other factors, including structural shifts, were also important in explaining the deceleration in global trade growth.

Chart A1 China’s Merchandise Import Growth:

Volume and Price Effects, 2007–15

Chart A2 China’s Import Growth by Selected Products:

Volume and Price Effects in 2015

Source: CEIC, IMF and EPG, MAS estimates

Source: China General Administration of Customs and EPG, MAS estimates

Chart A3 China’s Nominal Merchandise

Import Growth by Country

Chart A4 Exposure to China’s Import

Demand in 2011

Source: CEIC and EPG, MAS estimates

* Asia-9 comprises Hong Kong, Indonesia, Korea, Malaysia, the Philippines, Singapore, Taiwan, Thailand and Vietnam.

Source: OECD-TiVA Database and EPG, MAS estimates

-20

-10

0

10

20

30

40

2007 2008 2009 2010 2011 2012 2013 2014 2015

% P

oin

t C

on

trib

uti

on

to

Im

po

rt G

row

th

Volume Effect Price Effect Total Imports

-60

-40

-20

0

20

% P

oin

t C

on

trib

uti

on

to

Im

po

rt G

row

th

Volume Effect Price Effect Import Value

-15

-10

-5

0

5

10

2013 2014 2015

% P

oin

t C

on

trib

uti

on

to

Im

po

rt G

row

th

Asia-9*

Africa, Middle East & Latin America

G3

ROW

Total Imports

0

2

4

6

8

NEA-3& SGP

ASEAN-4 Japan Eurozone UK US

% o

f D

om

est

ic N

om

ina

l G

DP

Goods Services

16 Macroeconomic Review, April 2016

Monetary Authority of Singapore Economic Policy Group

China’s customs trade data show that trends in import volumes and values varied considerably across major products in 2015. Although the country imported larger quantities of crude oil, LPG, and iron ore, their unit prices fell by around 40%, resulting in lower import values for these products. (Chart A2) Conversely, China imported smaller quantities of manufactured products such as computers, display screens and cars, which contributed, in part, to the slump in intra-regional trade since early 2015. Meanwhile, Chinese imports of coal fell in both volume and price terms. In terms of geographical impact, the bulk of the decline in China’s nominal imports last year was due to goods shipped from the Middle East, Latin America and Africa combined, while Asia-9 and the G3 accounted for smaller proportions. (Chart A3)

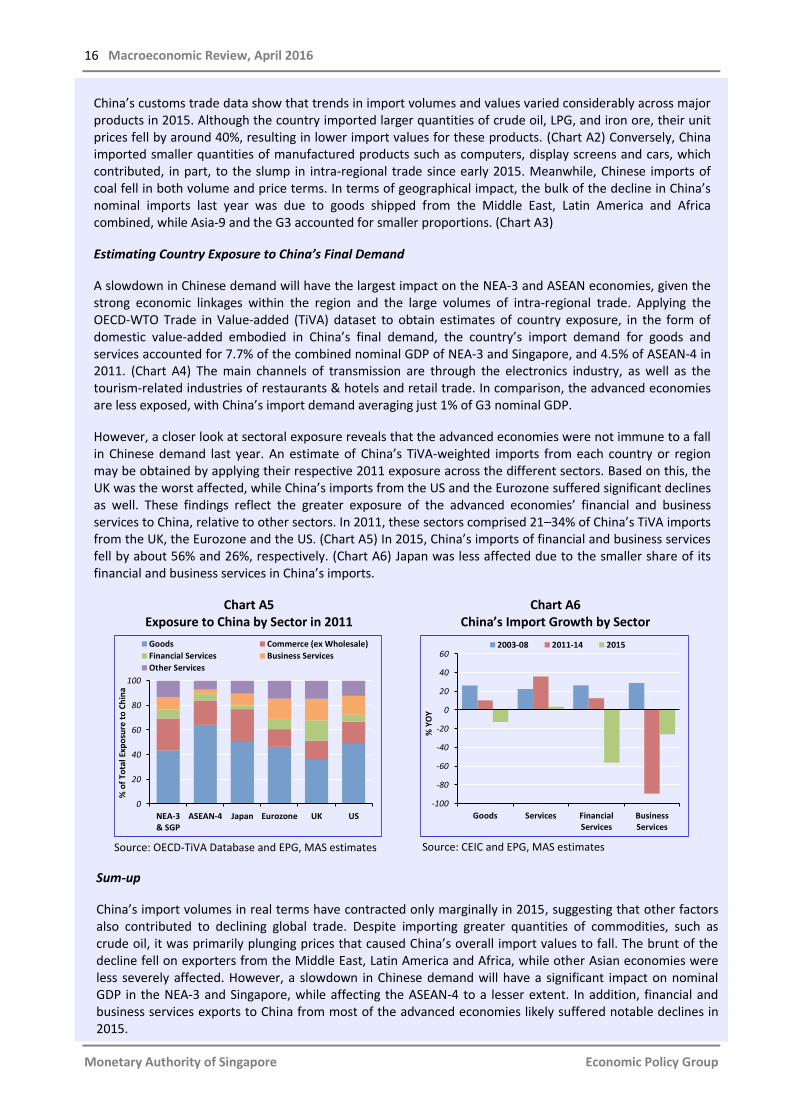

Estimating Country Exposure to China’s Final Demand

A slowdown in Chinese demand will have the largest impact on the NEA-3 and ASEAN economies, given the strong economic linkages within the region and the large volumes of intra-regional trade. Applying the OECD-WTO Trade in Value-added (TiVA) dataset to obtain estimates of country exposure, in the form of domestic value-added embodied in China’s final demand, the country’s import demand for goods and services accounted for 7.7% of the combined nominal GDP of NEA-3 and Singapore, and 4.5% of ASEAN-4 in 2011. (Chart A4) The main channels of transmission are through the electronics industry, as well as the tourism-related industries of restaurants & hotels and retail trade. In comparison, the advanced economies are less exposed, with China’s import demand averaging just 1% of G3 nominal GDP.

However, a closer look at sectoral exposure reveals that the advanced economies were not immune to a fall in Chinese demand last year. An estimate of China’s TiVA-weighted imports from each country or region may be obtained by applying their respective 2011 exposure across the different sectors. Based on this, the UK was the worst affected, while China’s imports from the US and the Eurozone suffered significant declines as well. These findings reflect the greater exposure of the advanced economies’ financial and business services to China, relative to other sectors. In 2011, these sectors comprised 21–34% of China’s TiVA imports from the UK, the Eurozone and the US. (Chart A5) In 2015, China’s imports of financial and business services fell by about 56% and 26%, respectively. (Chart A6) Japan was less affected due to the smaller share of its financial and business services in China’s imports.

Chart A5 Exposure to China by Sector in 2011

Chart A6 China’s Import Growth by Sector

Source: OECD-TiVA Database and EPG, MAS estimates

Source: CEIC and EPG, MAS estimates

Sum-up

China’s import volumes in real terms have contracted only marginally in 2015, suggesting that other factors also contributed to declining global trade. Despite importing greater quantities of commodities, such as crude oil, it was primarily plunging prices that caused China’s overall import values to fall. The brunt of the decline fell on exporters from the Middle East, Latin America and Africa, while other Asian economies were less severely affected. However, a slowdown in Chinese demand will have a significant impact on nominal GDP in the NEA-3 and Singapore, while affecting the ASEAN-4 to a lesser extent. In addition, financial and business services exports to China from most of the advanced economies likely suffered notable declines in 2015.

0

20

40

60

80

100

NEA-3& SGP

ASEAN-4 Japan Eurozone UK US

% o

f T

ota

l Exp

osu

re t

o C

hin

a

Goods Commerce (ex Wholesale)

Financial Services Business Services

Other Services

Goods Services FinancialServices

BusinessServices

-100

-80

-60

-40

-20

0

20

40

60

% Y

OY

2003-08 2011-14 2015

Chapter2TheSingaporeEconomy

18 Macroeconomic Review, April 2016

Monetary Authority of Singapore Economic Policy Group

2 The Singapore Economy

Cyclical Factors Weigh On Near-term Growth

The Singapore economy grew by an average of 3.1% q-o-q SAAR in Q4 2015 and Q1 2016. However, the underlying sectoral growth profile was uneven over the past six months. Against the downshift in the external environment and volatile financial markets early this year, economic activity appears to have weakened across more sectors into Q1. Besides pockets of the trade-related industries, the modern services and consumer-facing services sectors also turned in a muted performance. For the rest of the year, the softening of growth prospects across a number of Singapore’s key trading partners is expected to dampen activity in the external-oriented sectors. Notably, growth of capital formation in the G3 is likely to be lower than last year. This is expected to have a negative impact on pockets of trade-related industries, such as precision engineering, which have a relatively high exposure to the global investment cycle. Further, some signs of weakness have emerged in the domestic corporate landscape, with forward-looking business expectations pointing to softer conditions in H1 2016. Alongside the deterioration in activity, firms have responded by consolidating their operations, as evident in the step-down in business loan growth as well as the uptick in redundancies. Nonetheless, these corporate adjustments appear to be contained within specific clusters of firms at this stage. Given the subdued outlook, the Singapore economy is expected to see modest gains in the quarters ahead, culminating in 1–3% growth for this year as a whole.

The Singapore Economy 19

Monetary Authority of Singapore Economic Policy Group

2.1 Recent Economic Developments

Economic Activity Weakened Across More Sectors

The Singapore economy continued to chart a volatile growth profile over the past two quarters. A strong showing by modern services and the domestic-oriented cluster boosted GDP in Q4 2015, although the trade-related industries were buffeted by cyclical headwinds. In early 2016, the weakness widened to more industries. The pullback was most evident within the modern services cluster, with financial sector activity hit by falling credit demand and lower fee income from fund management after a surge at year-end. The more subdued economic environment also dampened pockets of domestic-oriented activity, although the cluster remained relatively resilient as a whole.

The Singapore economy has been on a three-speed trajectory in recent years, although the differences have narrowed more recently.

The performance of the domestic economy over the past six months or so has been modest and uneven, as in recent years. Economic activity picked up in the final quarter of 2015, with GDP rising by a stronger-than-expected 6.2% q-o-q SAAR to bring the year to a close on a high note. (Chart 2.1) However, this was transitory, with the latest Advance Estimates pointing to a flat growth outturn in early 2016. The underlying drivers in the economy can be related to developments in three distinct clusters: (i) modern services, which consist of finance & insurance, information & communications and business services; (ii) the trade-related cluster, comprising manufacturing, transportation & storage, and wholesale trade; and (iii) the domestic cluster, made up of construction, retail trade, utilities, other goods industries, and other services. Over the last few years, the modern services cluster has expanded strongly while trade-related industries stagnated. Meanwhile, domestic-oriented activities have been on a relatively slow, but steady, uptrend. (Chart 2.2) This three-speed trajectory was most evident in Q4 last year. Overall growth was supported by a buoyant modern services cluster and steady expansion in the domestic-oriented sectors, offsetting the deterioration in the trade-related industries.

Modern services was the main pillar of support in Q4 2015.

Following a relatively muted performance in Q3 2015, the modern services sectors experienced a broad-based

Chart 2.1

Singapore’s GDP Growth

* Advance Estimates.

Chart 2.2 Growth Drivers by Cluster

Source: EPG, MAS estimates

2013 2014 2015 2016 Q1*

-2

0

2

4

6

8

10

Pe

r C

en

t

QOQ SAAR

YOY

95

100

105

110

115

120

125

2012 2013 2014 2015

Ind

ex (

2012

=100

), S

A

Domestic

Trade-related

Modern Services

Q4

20 Macroeconomic Review, April 2016

Monetary Authority of Singapore Economic Policy Group

strengthening in Q4. The financial sector turned in a strong performance, with growth surging by 34.1% q-o-q SAAR. Notably, the fund management segment registered a strong increase in net fees and commissions towards the end of the year, while the insurance industry posted healthy gains from an uptick in life insurance sales. (Chart 2.3) The strength of these activities helped to offset the sluggishness in the financial intermediation segments, where domestic and offshore non-bank loan volumes contracted by 1.4% and 3.3% q-o-q, respectively, in Q4. Softer trade and economic growth in the region, as well as concerns over rising interest rates, led to a moderate decline in loan demand. Concomitantly, the information & communications sector expanded firmly by 6.4% q-o-q SAAR in Q4. This was partly due to a rebound in the telecommunications segment as the number of wireless broadband subscriptions increased. Stronger corporate demand for professional services, such as accounting and consultancy, provided a fillip to the business services sector.

A step-up in domestic-oriented activities gave further impetus to growth.

The domestic-oriented sectors also saw an increase in growth momentum in Q4 2015. This was underpinned in part by construction activity that grew robustly by 6.0% q-o-q SAAR, supported by a steady stream of civil engineering projects, including Changi Airport Terminal 5. (Chart 2.4) At the same time, supply-side developments in the healthcare industry, including the opening of Yishun Community Hospital, provided a boost to growth. Indeed, the health & social services segment added 1,600 jobs during the quarter, accounting for 10% of employment gains in the economy in Q4.

The trade-related industries were buffeted by lacklustre external demand.

In contrast, the trade-related industries languished amid persistent weakness in the external environment. In particular, the manufacturing sector shrank by 4.9% q-o-q SAAR in its fourth consecutive quarter of decline, mainly weighed down by dismal outturns in the electronics and biomedical segments.

Chart 2.3 New Business of Life Insurance Companies

Chart 2.4 Certified Construction Payments

Source: EPG, MAS estimates

80

100

120

140

160

180

200

2013 Q3 2014 Q3 2015

Ind

ex

(Q1

20

13

=1

00

)

Q4

Total Premiums

Individual Policies

2014 Q2 Q3 Q4 2015 Q2 Q3 Q4

-6

-4

-2

0

2

4

6

8

% P

oin

t C

on

trib

uti

on

to

Q

OQ

SA

Gro

wth

Residential Non-residential

Civil Engineering Overall

The Singapore Economy 21

Monetary Authority of Singapore Economic Policy Group

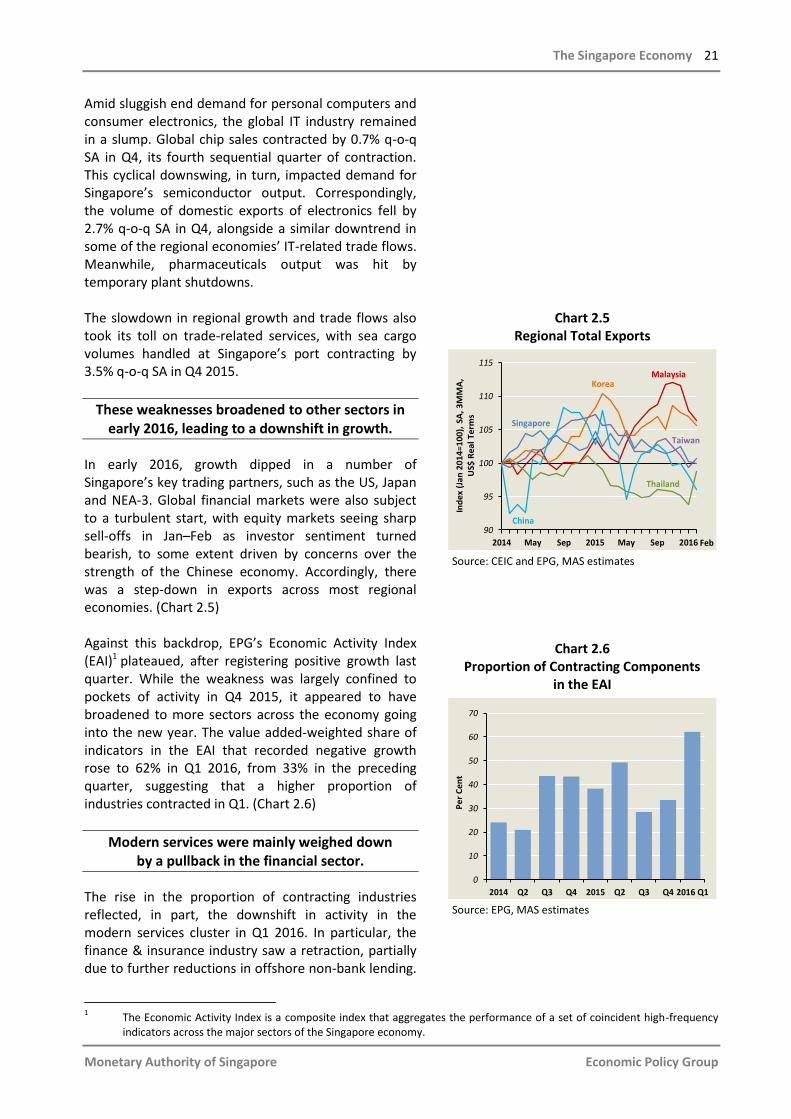

Amid sluggish end demand for personal computers and consumer electronics, the global IT industry remained in a slump. Global chip sales contracted by 0.7% q-o-q SA in Q4, its fourth sequential quarter of contraction. This cyclical downswing, in turn, impacted demand for Singapore’s semiconductor output. Correspondingly, the volume of domestic exports of electronics fell by 2.7% q-o-q SA in Q4, alongside a similar downtrend in some of the regional economies’ IT-related trade flows. Meanwhile, pharmaceuticals output was hit by temporary plant shutdowns. The slowdown in regional growth and trade flows also took its toll on trade-related services, with sea cargo volumes handled at Singapore’s port contracting by 3.5% q-o-q SA in Q4 2015.

These weaknesses broadened to other sectors in early 2016, leading to a downshift in growth.

In early 2016, growth dipped in a number of Singapore’s key trading partners, such as the US, Japan and NEA-3. Global financial markets were also subject to a turbulent start, with equity markets seeing sharp sell-offs in Jan–Feb as investor sentiment turned bearish, to some extent driven by concerns over the strength of the Chinese economy. Accordingly, there was a step-down in exports across most regional economies. (Chart 2.5) Against this backdrop, EPG’s Economic Activity Index (EAI)1 plateaued, after registering positive growth last quarter. While the weakness was largely confined to pockets of activity in Q4 2015, it appeared to have broadened to more sectors across the economy going into the new year. The value added-weighted share of indicators in the EAI that recorded negative growth rose to 62% in Q1 2016, from 33% in the preceding quarter, suggesting that a higher proportion of industries contracted in Q1. (Chart 2.6)

Modern services were mainly weighed down by a pullback in the financial sector.

The rise in the proportion of contracting industries reflected, in part, the downshift in activity in the modern services cluster in Q1 2016. In particular, the finance & insurance industry saw a retraction, partially due to further reductions in offshore non-bank lending.

Chart 2.5 Regional Total Exports

Source: CEIC and EPG, MAS estimates

Chart 2.6 Proportion of Contracting Components

in the EAI

Source: EPG, MAS estimates

1 The Economic Activity Index is a composite index that aggregates the performance of a set of coincident high-frequency

indicators across the major sectors of the Singapore economy.

2014 May Sep 2015 May Sep 2016

90

95

100

105

110

115

Ind

ex

(Ja

n 2

01

4=

10

0),

SA

, 3

MM

A,

US$

Re

al T

erm

s

Feb

China

Thailand

Singapore

MalaysiaKorea

Taiwan

0

10

20

30

40

50

60

70

2014 Q2 Q3 Q4 2015 Q2 Q3 Q4 2016 Q1

Pe

r C

en

t

22 Macroeconomic Review, April 2016

Monetary Authority of Singapore Economic Policy Group

Total ACU non-bank loan volumes fell by an average of 1.3% m-o-m in Jan–Feb 2016, extending the 1.1% decline recorded in the preceding quarter. From a geographical perspective, this stemmed primarily from a continued contraction in loans extended to East Asia, as the regional growth and trade slowdown constrained demand for credit, including trade financing. (Chart 2.7) The volatility in the earnings of fund managers also played a role. Following the lump-sum recognition of performance bonuses at the end of last year, which had contributed to a surge in value added, the fund management industry is likely to see a sequential moderation in Q1 2016. Meanwhile, the subdued business sentiment impacted corporate demand for ICT and business services, such as rental & leasing and consultancy.

Likewise, the domestic-oriented cluster lost some momentum ...

The domestic-oriented cluster remained a relatively stable source of support for the overall economy, despite a softening of aggregate growth. This was largely because of the construction industry, which saw a sequential step-up in certified progress payments for non-residential developments in Jan–Feb, including Project Jewel, a large-scale commercial project consisting of a new retail and lifestyle complex at Changi Airport. However, consumer-facing services, such as domestic retail trade, were affected by tepid consumer sentiment. According to the MasterCard Index of Consumer Confidence, there was a significant deterioration in the outlook for H1 2016 in Singapore. (Chart 2.8) In Jan–Feb, the volume of discretionary items sold, such as watches and jewellery, contracted. (Chart 2.9) Nevertheless, the magnitude of the decline was milder than during previous periods of heightened macroeconomic uncertainty.

… but idiosyncratic factors lifted the performance of the trade-related sector.

The trade-related cluster posted a surprising upturn in Q1, largely as a result of idiosyncratic events in the manufacturing sector, as external demand remained soft. After six consecutive quarters of contraction, manufacturing output rose by 2.6% q-o-q SA in Q1 2016. The typically volatile pharmaceuticals segment

Chart 2.7 ACU Non-bank Lending

Chart 2.8 MasterCard Index of Consumer Confidence

(Outlook for the Next Six Months)

Source: MasterCard

Note: A value of 0 represents maximum pessimism, while 100 represents maximum optimism and 50 represents neutrality.

* H2 2015 reading represents outlook for H1 2016.

Chart 2.9 Retail Sales Volumes

Source: EPG, MAS estimates

2014 Q2 Q3 Q4 2015 Q2 Q3 Q4 2016

-4

-2

0

2

4

6

% P

oin

t C

on

trib

uti

on

to

QO

Q G

row

th

East Asia Europe Americas

Jan–Feb

40

45

50

55

60

65

70

2012 H2 2013 H2 2014 H2 2015 H2*

Ind

ex

More Optimistic

80

85

90

95

100

105

2008 2009 2010 2011 2012 2013 2014 2015 2016

Ind

ex

(Q1

20

14

=1

00

), S

A

Discretionary

Non-discretionary

Jan–Feb

Overall excluding Motor Vehicle Sales

The Singapore Economy 23

Monetary Authority of Singapore Economic Policy Group

saw a 20.8% q-o-q SA surge in output over the quarter as firms switched to a more favourable product mix. Trade-related services continued to turn in a muted performance, with Singapore’s total export volume shrinking by 3.0% q-o-q SA in Q1.

2015 In Perspective: Further Growth Moderation

The domestic economy slowed in 2015 …

The Singapore economy grew by 2.0% in 2015, a step-down from the 3.3% in 2014 and lower than the average of 3.9% over 2012–14. At the same time, there was a higher proportion of industries (38% of the 58 industry segments) experiencing negative growth in 2015, compared with 24% the year before. (Chart 2.10)

… continuing the moderating growth trend since 2011.

Since 2011, the domestic economy has gradually settled on a more modest growth path, reflecting a confluence of cyclical and structural factors. Notably, Singapore’s underlying trend GDP2 growth has been moderating over 2011–15. (Chart 2.11) Part of this decline was due to the manufacturing sector, with the electronics, precision engineering and general manufacturing clusters facing the most intense structural challenges. MNCs have been rationalising their global operations in the post-GFC era, with electronics firms in particular scaling back on mass manufacturing in Singapore, while at the same time shifting towards higher local value-added niche production as well as manufacturing-related services, such as design and marketing. The consolidation process, in turn, has had spillover effects on supporting industries, such as precision engineering. These secular trends have been highlighted in previous issues of the Review. Growth in some services sectors has also eased, with business services and other services registering reduced contributions to the expansion of the overall economy. (Chart 2.11) In comparison, the support from wholesale & retail and financial services has held

Chart 2.10

Distribution of Industry VA Growth*

Source: EPG, MAS estimates

* Estimated using a kernel smoother.

Chart 2.11 Sectoral Contribution to

Estimated Trend GDP Growth

Source: EPG, MAS estimates

2 Singapore’s underlying trend GDP is estimated from a weighted average of three methods—a structural vector

autoregression (SVAR) approach using the Blanchard-Quah decomposition, the Friedman variable span smoother and a simple univariate Hodrick-Prescott filter. The sectoral contributions were estimated using an average of the Christiano-Fitzgerald, Hodrick-Prescott and Butterworth filters.

0

0.02

0.04

0.06

0.08

-30 -20 -10 0 10 20 30 40 50

De

nsi

ty

% YOY

2015

2014

0

2

4

6

8

2009 2010 2011 2012 2013 2014 2015

% P

oin

t C

on

trib

uti

on

Manufacturing ConstructionBusiness Services Other ServicesWholesale & Retail FinancialOthers Trend

24 Macroeconomic Review, April 2016

Monetary Authority of Singapore Economic Policy Group