Embed Size (px)

Citation preview

Bulletin No. 2018-03

Bulletin No. 2018-03

Retention: May 31, 2018

To: Heads of Government Departments, Agencies, and Others Concerned

Subject: Implementation of SFFAS No. 47, Reporting Entity, to be effective fiscal year 2018

1. Purpose

This bulletin provides the Federal Accounting Standards Advisory Board’s (FASAB) SFFAS No. 47,Reporting Entity determinations received by the entities, reviewed by the Working Group, and approved bythe SFFAS No. 47 Steering Committee. The determinations are listed in Sections 6, 7, and 8 (ConsolidatedEntities, Disclosure Entities, and Related Party). Additional Governmentwide Financial Report System(GFRS) reporting guidance is provided for agencies with a determination of disclosure or related party.Transaction guidance is also included for agencies that use the Treasury Account Symbol (TAS) associatedwith the disclosure or related party entities.

SFFAS No. 47 was not written to rescind Statement of Federal Financial Accounting Concepts 2, Entity andDisplay, when addressing reporting entities and the criteria for inclusion. SFFAS No. 47 is to be used asadditional guidance to assist with making the determination of inclusion.

2. Authority

FASAB was created under the terms of the Federal Advisory Committee Act (FACA), as amended, (5U.S.C. app.) and is sponsored by the Comptroller General of the United States, the Director of the Office ofManagement and Budget (OMB), and the Secretary of the Treasury of the United States. In addition, since1999, FASAB has been the body designated by the American Institute of Certified Public Accountants(AICPA) to establish generally accepted accounting principles (GAAP) for federal government reportingentities.

3. Rescission

This Bulletin rescinds TFM Volume I Bulletin No. 2017-09: Implementation of SFFAS No. 47, ReportingEntity, to be effective fiscal year 2018.

4. Background

Page 1 of 29

SFFAS No. 47, Reporting Entity was published in December of 2014 with an effective date of fiscal year2018. Treasury, along with the SFFAS No. 47 Working Group (Working Group) and Steering Committee,has been engaged in achieving a successful implementation. A questionnaire was designed by compilingthe key deciding factors throughout FASAB Standard No. 47, and listing them in branch logic sequence.The document referenced the corresponding paragraphs in SFFAS No. 47 with each question. Thequestionnaire asked for the component reporting entity to be identified. Upon completion of the survey,the agency was led to a reporting determination of consolidation entity, disclosure entity, or relatedparty.

The SFFAS No. 47 questionnaire was distributed through email between August 2015 and March 2016.Multiple requests were emailed. If an agency did not respond, the Working Group made a determination forthe agency and emailed the agency a completed survey. The Working Group only asked for a negativeconfirmation of the survey determination. All surveys were reviewed by the Working Group and SteeringCommittee and discrepancies were addressed.

The survey supported the following determinations:

Component Reporting Entity—is used broadly to refer to a reporting entity within a largerreporting entity. Examples of component reporting entities include organizations such asexecutive departments, independent agencies, government corporations, legislative agencies,and federal courts. Component reporting entities would also include sub-components (thosecomponents included in the Government Purpose Federal Financial reports (GPFFR) of alarger component reporting entity) that may themselves prepare GPFFRs. An example would bea bureau that is within a larger department that prepares its own stand-alone GPFFR.Consolidation Entity—is an organization that should be consolidated in the financialstatements based on the assessment of "(a) is financed through taxes and other non-exchangerevenues (b) is governed by the Congress and/or the President (c) imposes or may imposerisks and rewards to the federal government and (d) provides goods and services on a non-market basis." It would also include organizations that would result in misleading or incompletefinancial statements if excluded.Disclosure Entity—is an organization with a greater degree of autonomy with the federalgovernment than a consolidation entity.Related Party—is an organization considered to be a related party in the GPFFR if the existingrelationship or one party to the existing relationship, and has the ability to exercise significantinfluence over the other party’s policy decisions.

The top down approach was used to identify entity determinations from a governmentwide perspective.Each component entity should perform an agency review to validate proper reporting at the agency level.For assistance in an agency level review, please contact Fiscal Service [email protected] to receive the SFFAS No. 47 Agency Analysis Excel workbook.

The Working Group also determined that certain entities should not be included in the reporting process.For other entities, a determination has not yet been made regarding their reporting category. These entitiesare listed in Sections 9 and 10 below, respectively.

SFFAS No. 47 agency review process was addressed during the May 18, 2017 CRT meeting byDepartment of Interior. This review may lead to additional consolidation, disclosure and related parties for acomponent entity. During this review, if any revisions/additions to SFFAS No. 47 Agency Determinations(Sections 6-10) are needed, please report all determination revisions/additions to Fiscal Service [email protected] and notate in the subject line “SFFAS No. 47”.

Page 2 of 29

5. Procedure/Requirements

In fiscal year 2018, agencies should report information based on the SFFAS No. 47 determination. SFFASNo. 47 determinations have been available for agency review on multiple websites over the last year(SFFAS No. 47 Q&A). SFFAS No. 47 Agency Determinations (sections 6-8) is the published version. Thisinformation will be used to report Appendix A: Reporting Entity of the Financial Report of the United StatesGovernment (FR) for fiscal year 2018. The SFFAS No. 47 Working Group will continue to address theDetermination Discrepancy/Not Submitted a Survey category outlined in SFFAS No. 47 AgencyDeterminations (section 10).

An agency with the determination of consolidated will provide financial information in the GovernmentwideTreasury Symbol Adjusted Trial Balance System (GTAS), unless other means are determined for financialreporting. This data will flow to the face of the governmentwide statements presented in the FR.

Agencies with a determination of disclosure or related party will continue to report Treasury AccountingSymbols (TAS), if applicable, but when utilizing the disclosure or related party TAS transactions must beprocessed as non-federal (N). Therefore, if you are doing business with a disclosure entity or relatedparty, make sure to report the federal or non-federal designation as non-federal. Financial informationfor these disclosures and related parties, if possible, will be provided in a note not linked to the financialstatements. The list of TAS associated with disclosure and related party entities are outlined in TAS toReport as Non-Federal w/Designation of Disclosure or Related Party (see below). Some disclosure andrelated party entities have no TAS association. If you feel a disclosure or related party entity has direct TASassociation, and it is not addressed in TAS to Report as Non-Federal w/Designation of Disclosure orRelated Party, please contact Fiscal Service at [email protected] and notate in thesubject line “SFFAS No. 47 Disclosure TAS”.

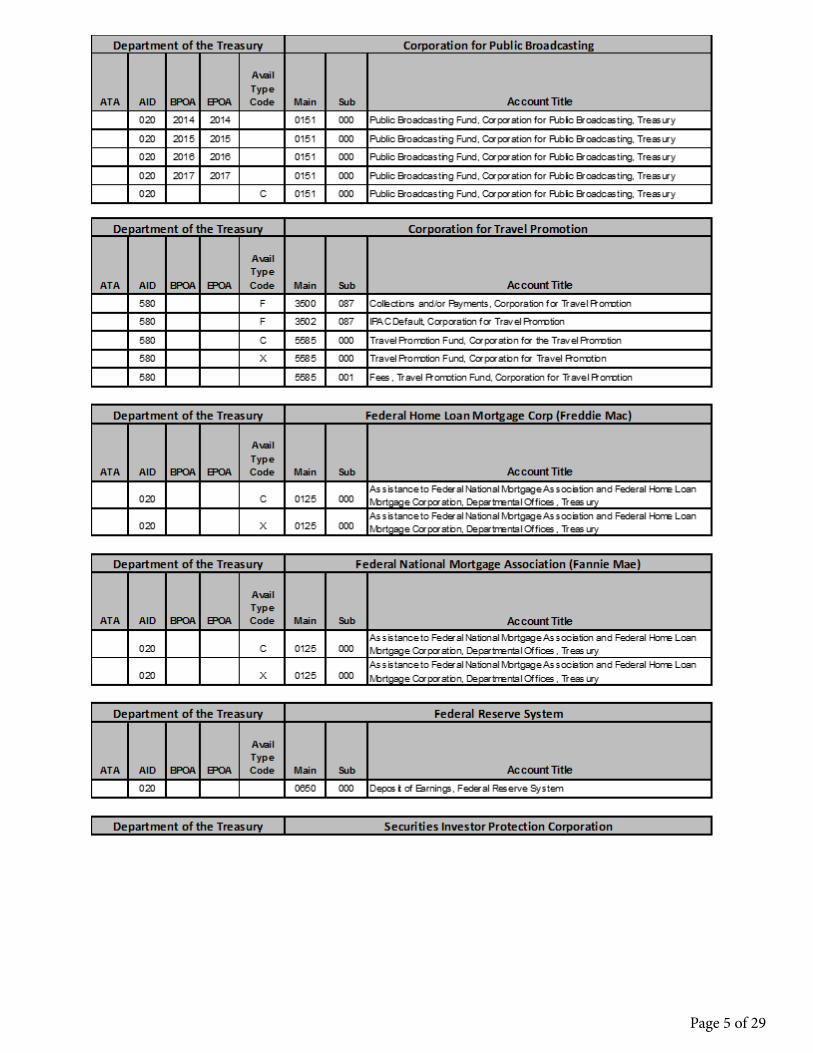

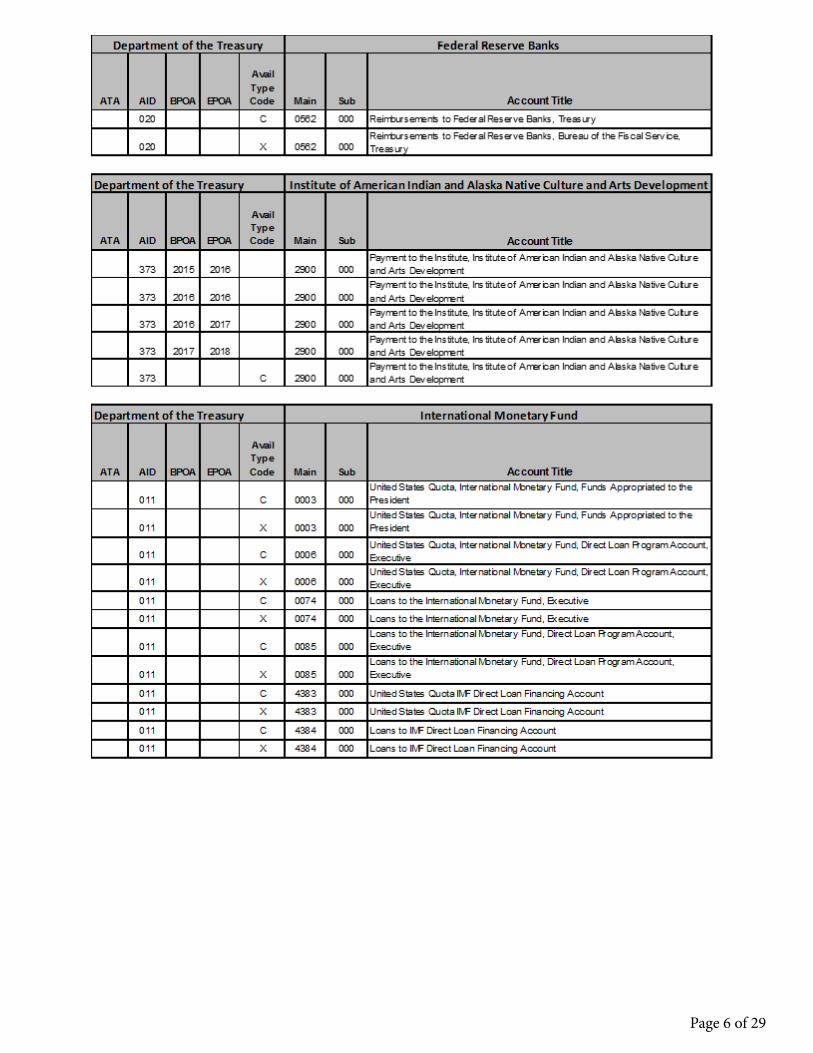

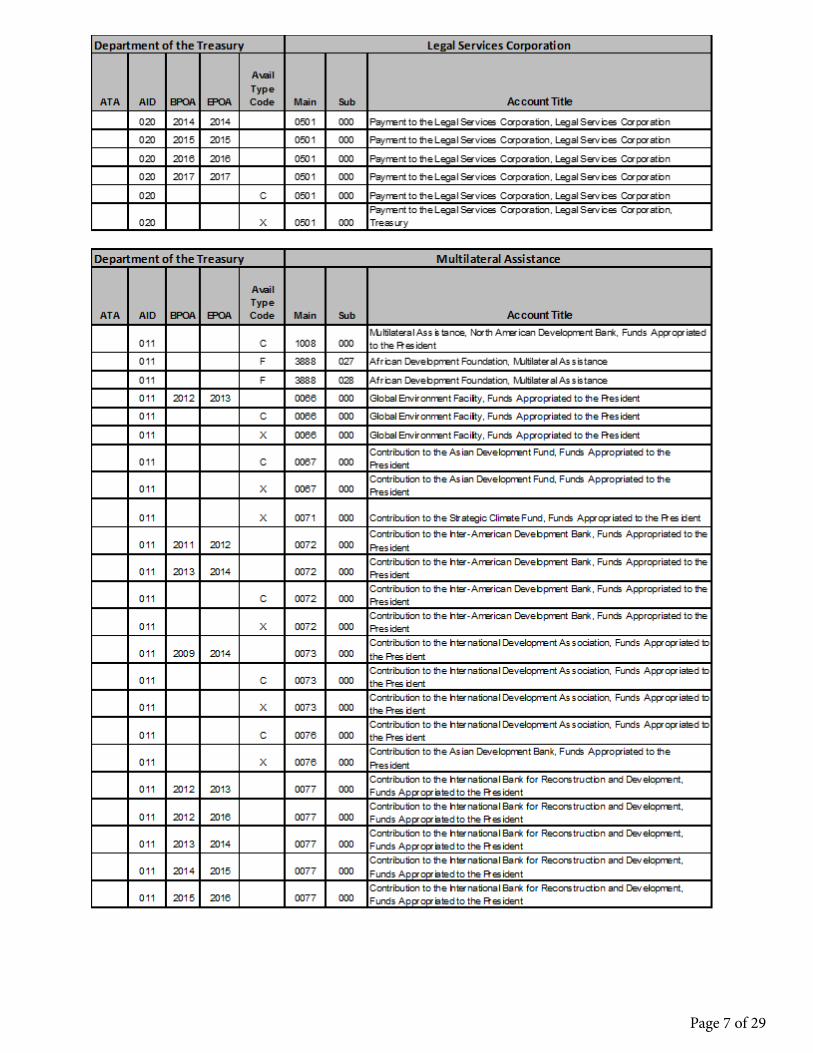

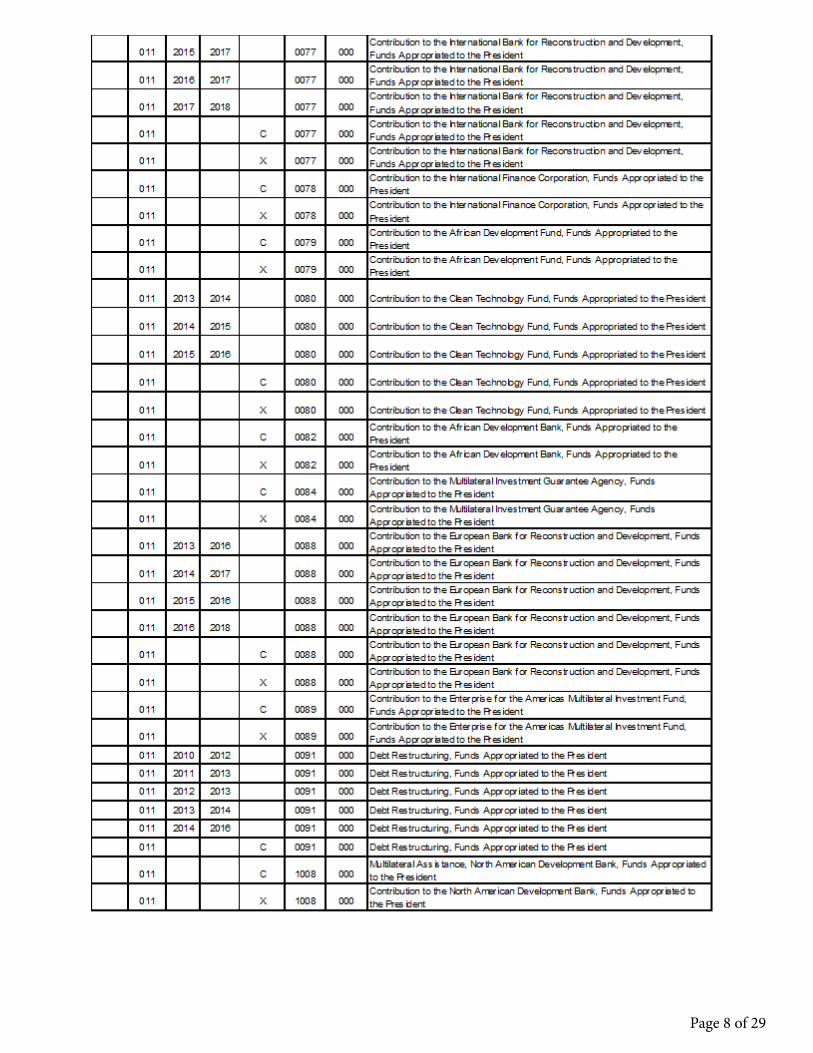

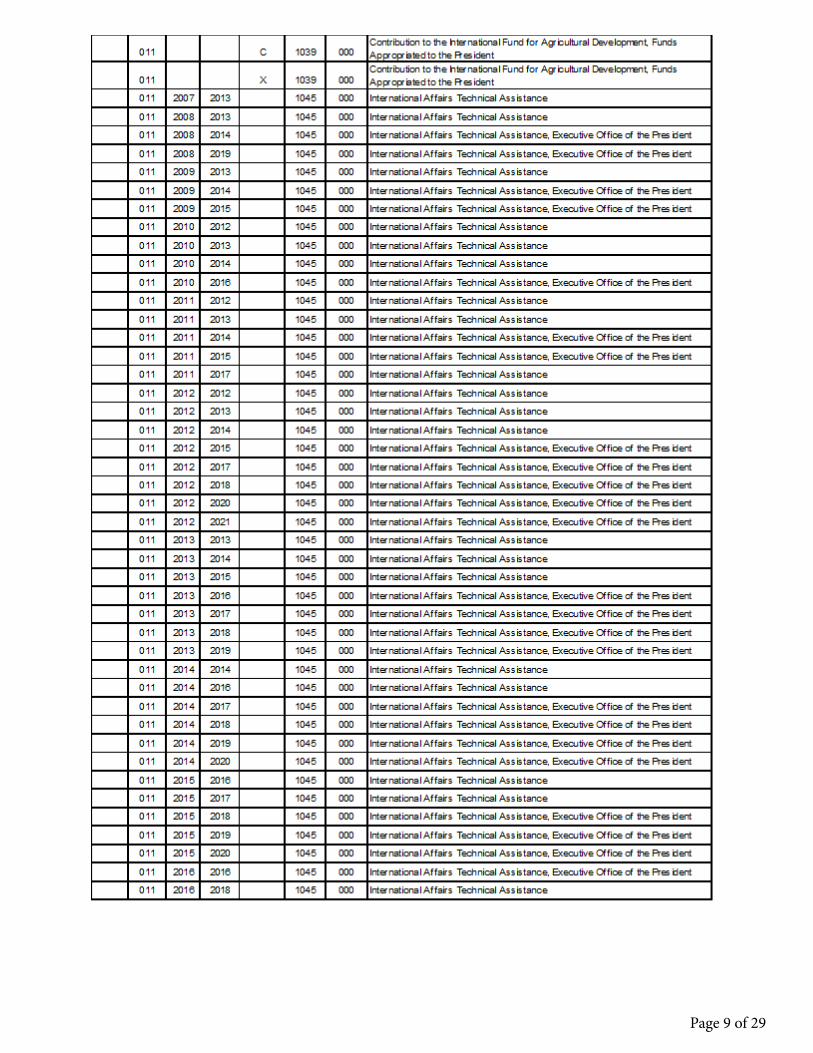

TAS to Report as Non-Federal w/Designation of Disclosure Entity or Related Party

Page 3 of 29

Page 4 of 29

Page 5 of 29

Page 6 of 29

Page 7 of 29

Page 8 of 29

Page 9 of 29

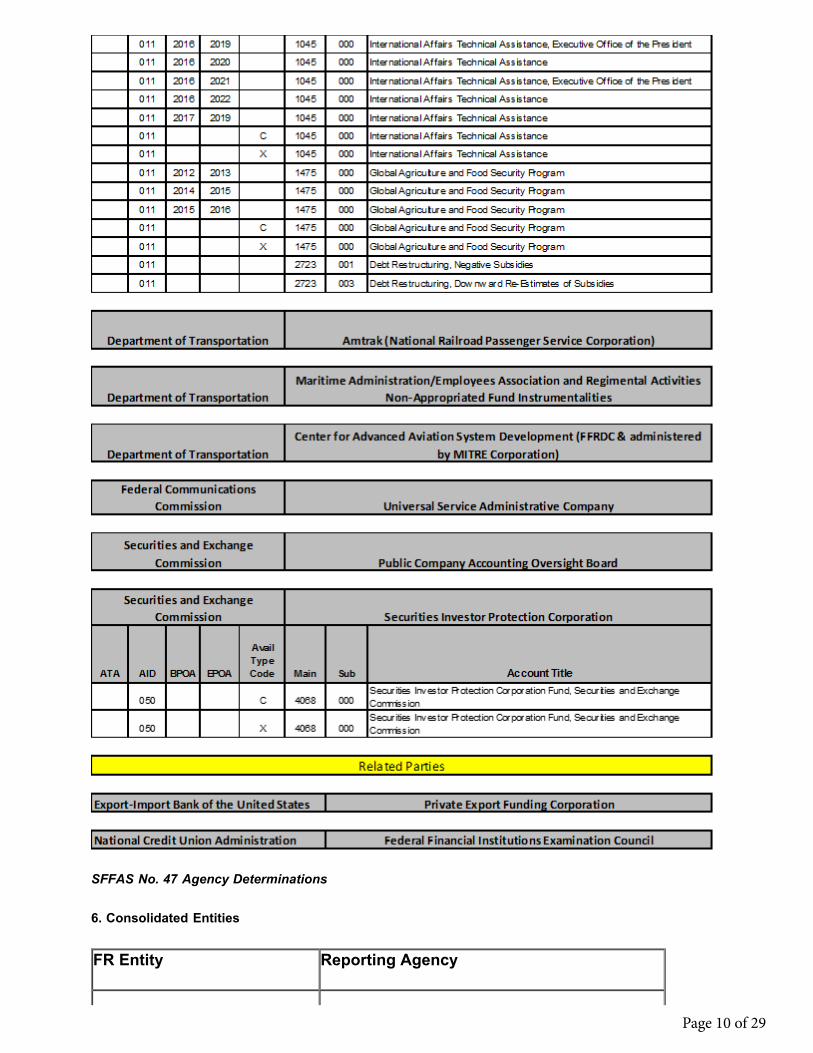

SFFAS No. 47 Agency Determinations

6. Consolidated Entities

FR Entity Reporting Agency

Page 10 of 29

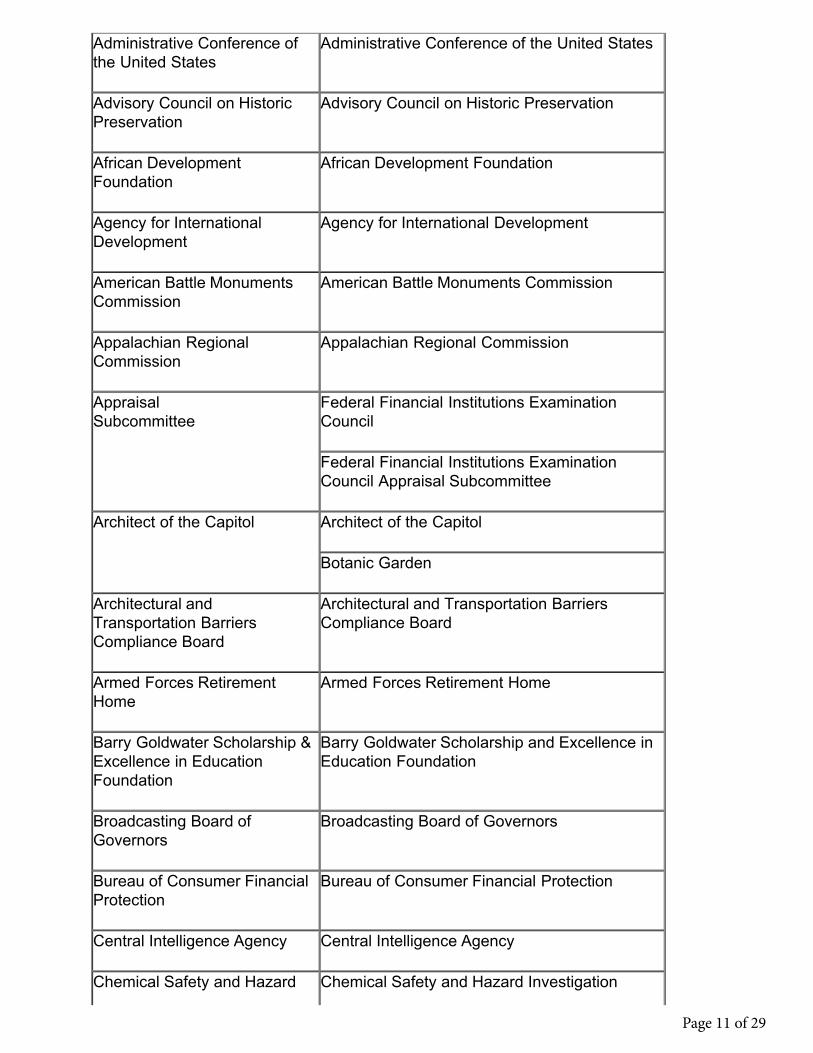

Administrative Conference ofthe United States

Administrative Conference of the United States

Advisory Council on HistoricPreservation

Advisory Council on Historic Preservation

African DevelopmentFoundation

African Development Foundation

Agency for InternationalDevelopment

Agency for International Development

American Battle MonumentsCommission

American Battle Monuments Commission

Appalachian RegionalCommission

Appalachian Regional Commission

AppraisalSubcommittee

Federal Financial Institutions ExaminationCouncil

Federal Financial Institutions ExaminationCouncil Appraisal Subcommittee

Architect of the Capitol Architect of the Capitol

Botanic Garden

Architectural andTransportation BarriersCompliance Board

Architectural and Transportation BarriersCompliance Board

Armed Forces RetirementHome

Armed Forces Retirement Home

Barry Goldwater Scholarship &Excellence in EducationFoundation

Barry Goldwater Scholarship and Excellence inEducation Foundation

Broadcasting Board ofGovernors

Broadcasting Board of Governors

Bureau of Consumer FinancialProtection

Bureau of Consumer Financial Protection

Central Intelligence Agency Central Intelligence Agency

Chemical Safety and Hazard Chemical Safety and Hazard Investigation

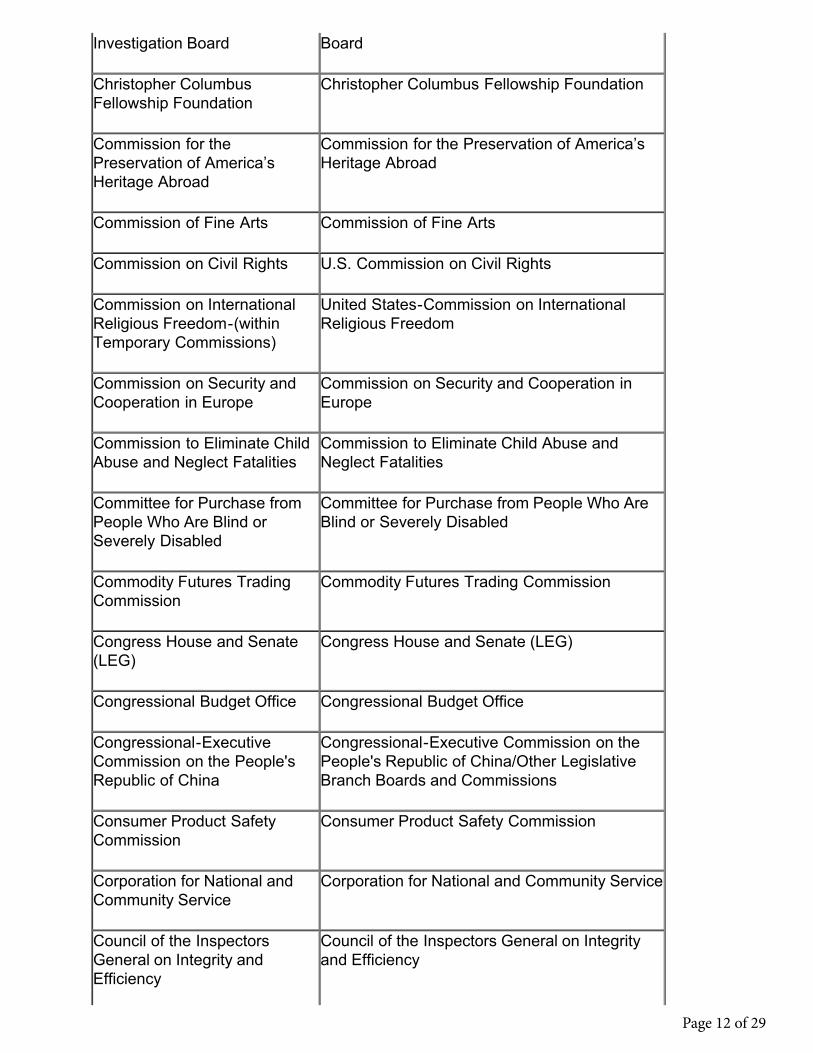

Page 11 of 29

Investigation Board Board

Christopher ColumbusFellowship Foundation

Christopher Columbus Fellowship Foundation

Commission for thePreservation of America’sHeritage Abroad

Commission for the Preservation of America’sHeritage Abroad

Commission of Fine Arts Commission of Fine Arts

Commission on Civil Rights U.S. Commission on Civil Rights

Commission on InternationalReligious Freedom-(withinTemporary Commissions)

United States-Commission on InternationalReligious Freedom

Commission on Security andCooperation in Europe

Commission on Security and Cooperation inEurope

Commission to Eliminate ChildAbuse and Neglect Fatalities

Commission to Eliminate Child Abuse andNeglect Fatalities

Committee for Purchase fromPeople Who Are Blind orSeverely Disabled

Committee for Purchase from People Who AreBlind or Severely Disabled

Commodity Futures TradingCommission

Commodity Futures Trading Commission

Congress House and Senate(LEG)

Congress House and Senate (LEG)

Congressional Budget Office Congressional Budget Office

Congressional-ExecutiveCommission on the People'sRepublic of China

Congressional-Executive Commission on thePeople's Republic of China/Other LegislativeBranch Boards and Commissions

Consumer Product SafetyCommission

Consumer Product Safety Commission

Corporation for National andCommunity Service

Corporation for National and Community Service

Council of the InspectorsGeneral on Integrity andEfficiency

Council of the Inspectors General on Integrityand Efficiency

Page 12 of 29

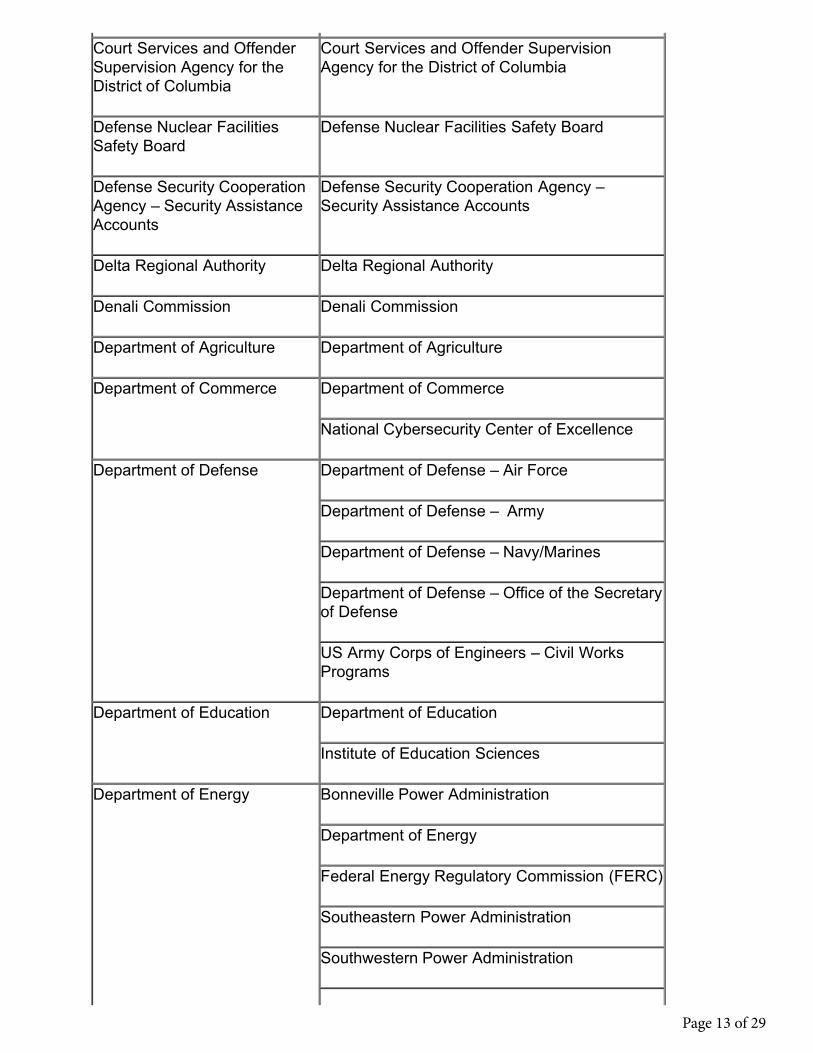

Court Services and OffenderSupervision Agency for theDistrict of Columbia

Court Services and Offender SupervisionAgency for the District of Columbia

Defense Nuclear FacilitiesSafety Board

Defense Nuclear Facilities Safety Board

Defense Security CooperationAgency – Security AssistanceAccounts

Defense Security Cooperation Agency –Security Assistance Accounts

Delta Regional Authority Delta Regional Authority

Denali Commission Denali Commission

Department of Agriculture Department of Agriculture

Department of Commerce Department of Commerce

National Cybersecurity Center of Excellence

Department of Defense Department of Defense – Air Force

Department of Defense – Army

Department of Defense – Navy/Marines

Department of Defense – Office of the Secretaryof Defense

US Army Corps of Engineers – Civil WorksPrograms

Department of Education Department of Education

Institute of Education Sciences

Department of Energy Bonneville Power Administration

Department of Energy

Federal Energy Regulatory Commission (FERC)

Southeastern Power Administration

Southwestern Power Administration

Page 13 of 29

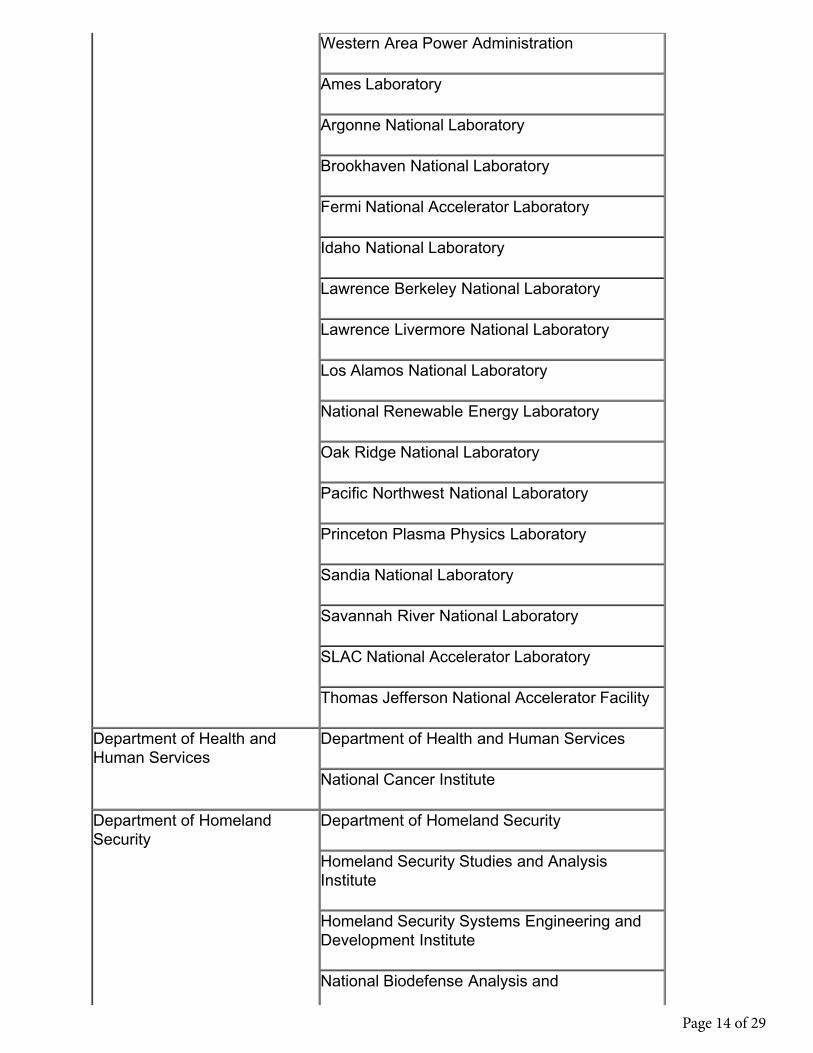

Western Area Power Administration

Ames Laboratory

Argonne National Laboratory

Brookhaven National Laboratory

Fermi National Accelerator Laboratory

Idaho National Laboratory

Lawrence Berkeley National Laboratory

Lawrence Livermore National Laboratory

Los Alamos National Laboratory

National Renewable Energy Laboratory

Oak Ridge National Laboratory

Pacific Northwest National Laboratory

Princeton Plasma Physics Laboratory

Sandia National Laboratory

Savannah River National Laboratory

SLAC National Accelerator Laboratory

Thomas Jefferson National Accelerator Facility

Department of Health andHuman Services

Department of Health and Human Services

National Cancer Institute

Department of HomelandSecurity

Department of Homeland Security

Homeland Security Studies and AnalysisInstitute

Homeland Security Systems Engineering andDevelopment Institute

National Biodefense Analysis and

Page 14 of 29

Countermeasures Center

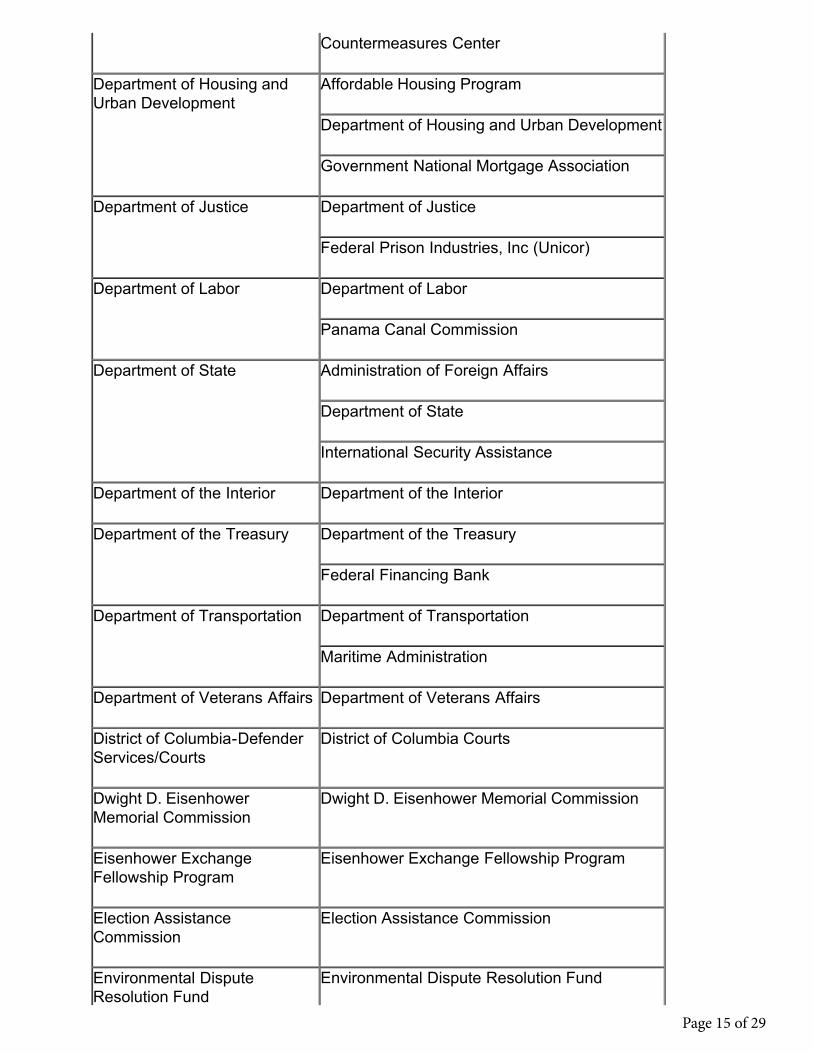

Department of Housing andUrban Development

Affordable Housing Program

Department of Housing and Urban Development

Government National Mortgage Association

Department of Justice Department of Justice

Federal Prison Industries, Inc (Unicor)

Department of Labor Department of Labor

Panama Canal Commission

Department of State Administration of Foreign Affairs

Department of State

International Security Assistance

Department of the Interior Department of the Interior

Department of the Treasury Department of the Treasury

Federal Financing Bank

Department of Transportation Department of Transportation

Maritime Administration

Department of Veterans Affairs Department of Veterans Affairs

District of Columbia-DefenderServices/Courts

District of Columbia Courts

Dwight D. EisenhowerMemorial Commission

Dwight D. Eisenhower Memorial Commission

Eisenhower ExchangeFellowship Program

Eisenhower Exchange Fellowship Program

Election AssistanceCommission

Election Assistance Commission

Environmental DisputeResolution Fund

Environmental Dispute Resolution Fund

Page 15 of 29

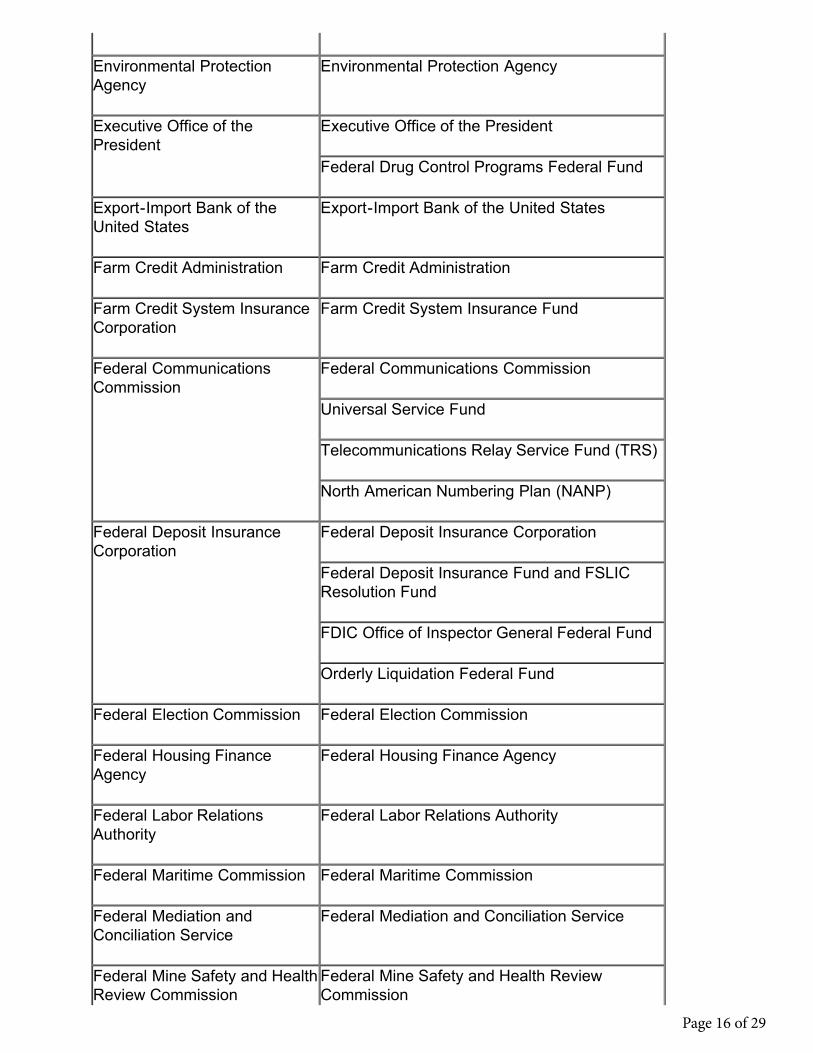

Environmental ProtectionAgency

Environmental Protection Agency

Executive Office of thePresident

Executive Office of the President

Federal Drug Control Programs Federal Fund

Export-Import Bank of theUnited States

Export-Import Bank of the United States

Farm Credit Administration Farm Credit Administration

Farm Credit System InsuranceCorporation

Farm Credit System Insurance Fund

Federal CommunicationsCommission

Federal Communications Commission

Universal Service Fund

Telecommunications Relay Service Fund (TRS)

North American Numbering Plan (NANP)

Federal Deposit InsuranceCorporation

Federal Deposit Insurance Corporation

Federal Deposit Insurance Fund and FSLICResolution Fund

FDIC Office of Inspector General Federal Fund

Orderly Liquidation Federal Fund

Federal Election Commission Federal Election Commission

Federal Housing FinanceAgency

Federal Housing Finance Agency

Federal Labor RelationsAuthority

Federal Labor Relations Authority

Federal Maritime Commission Federal Maritime Commission

Federal Mediation andConciliation Service

Federal Mediation and Conciliation Service

Federal Mine Safety and HealthReview Commission

Federal Mine Safety and Health ReviewCommission

Page 16 of 29

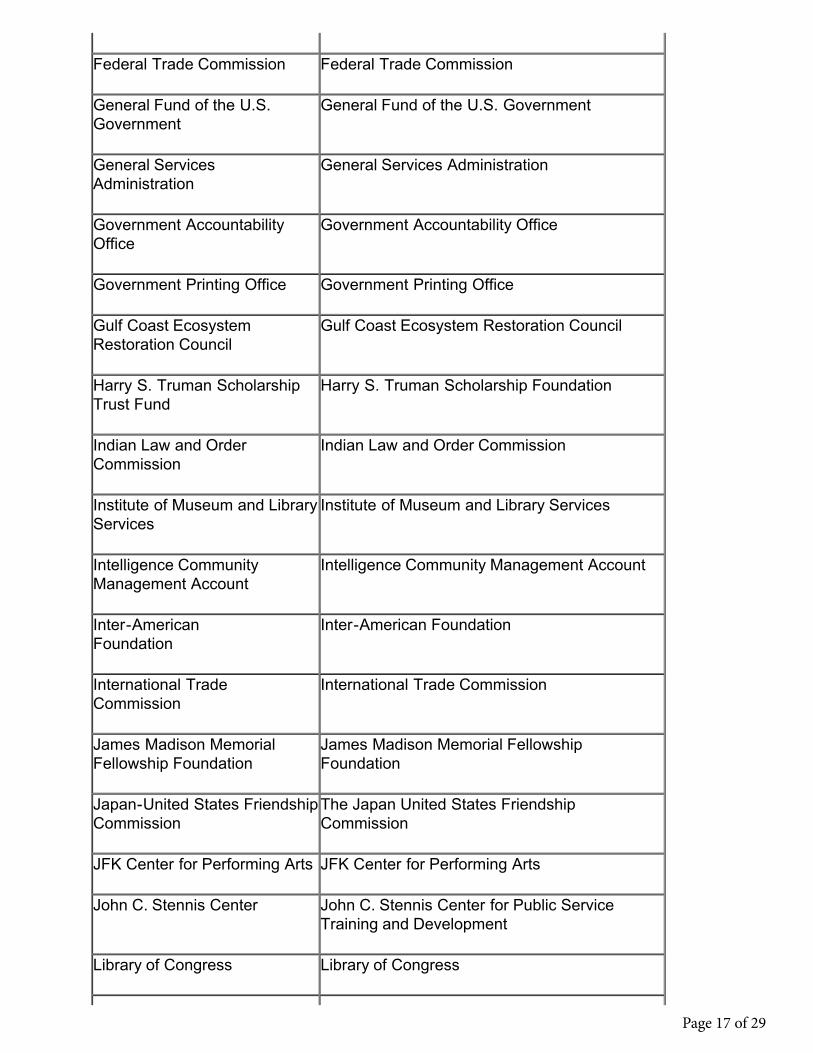

Federal Trade Commission Federal Trade Commission

General Fund of the U.S.Government

General Fund of the U.S. Government

General ServicesAdministration

General Services Administration

Government AccountabilityOffice

Government Accountability Office

Government Printing Office Government Printing Office

Gulf Coast EcosystemRestoration Council

Gulf Coast Ecosystem Restoration Council

Harry S. Truman ScholarshipTrust Fund

Harry S. Truman Scholarship Foundation

Indian Law and OrderCommission

Indian Law and Order Commission

Institute of Museum and LibraryServices

Institute of Museum and Library Services

Intelligence CommunityManagement Account

Intelligence Community Management Account

Inter-AmericanFoundation

Inter-American Foundation

International TradeCommission

International Trade Commission

James Madison MemorialFellowship Foundation

James Madison Memorial FellowshipFoundation

Japan-United States FriendshipCommission

The Japan United States FriendshipCommission

JFK Center for Performing Arts JFK Center for Performing Arts

John C. Stennis Center John C. Stennis Center for Public ServiceTraining and Development

Library of Congress Library of Congress

Page 17 of 29

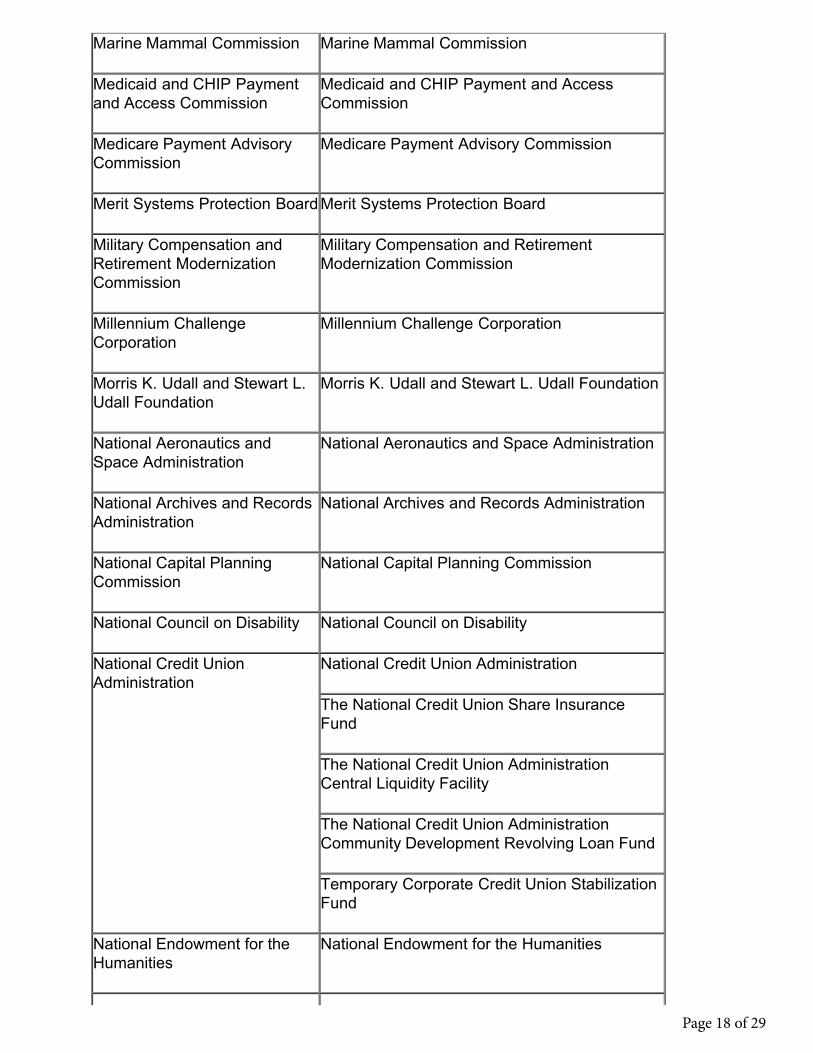

Marine Mammal Commission Marine Mammal Commission

Medicaid and CHIP Paymentand Access Commission

Medicaid and CHIP Payment and AccessCommission

Medicare Payment AdvisoryCommission

Medicare Payment Advisory Commission

Merit Systems Protection Board Merit Systems Protection Board

Military Compensation andRetirement ModernizationCommission

Military Compensation and RetirementModernization Commission

Millennium ChallengeCorporation

Millennium Challenge Corporation

Morris K. Udall and Stewart L.Udall Foundation

Morris K. Udall and Stewart L. Udall Foundation

National Aeronautics andSpace Administration

National Aeronautics and Space Administration

National Archives and RecordsAdministration

National Archives and Records Administration

National Capital PlanningCommission

National Capital Planning Commission

National Council on Disability National Council on Disability

National Credit UnionAdministration

National Credit Union Administration

The National Credit Union Share InsuranceFund

The National Credit Union AdministrationCentral Liquidity Facility

The National Credit Union AdministrationCommunity Development Revolving Loan Fund

Temporary Corporate Credit Union StabilizationFund

National Endowment for theHumanities

National Endowment for the Humanities

Page 18 of 29

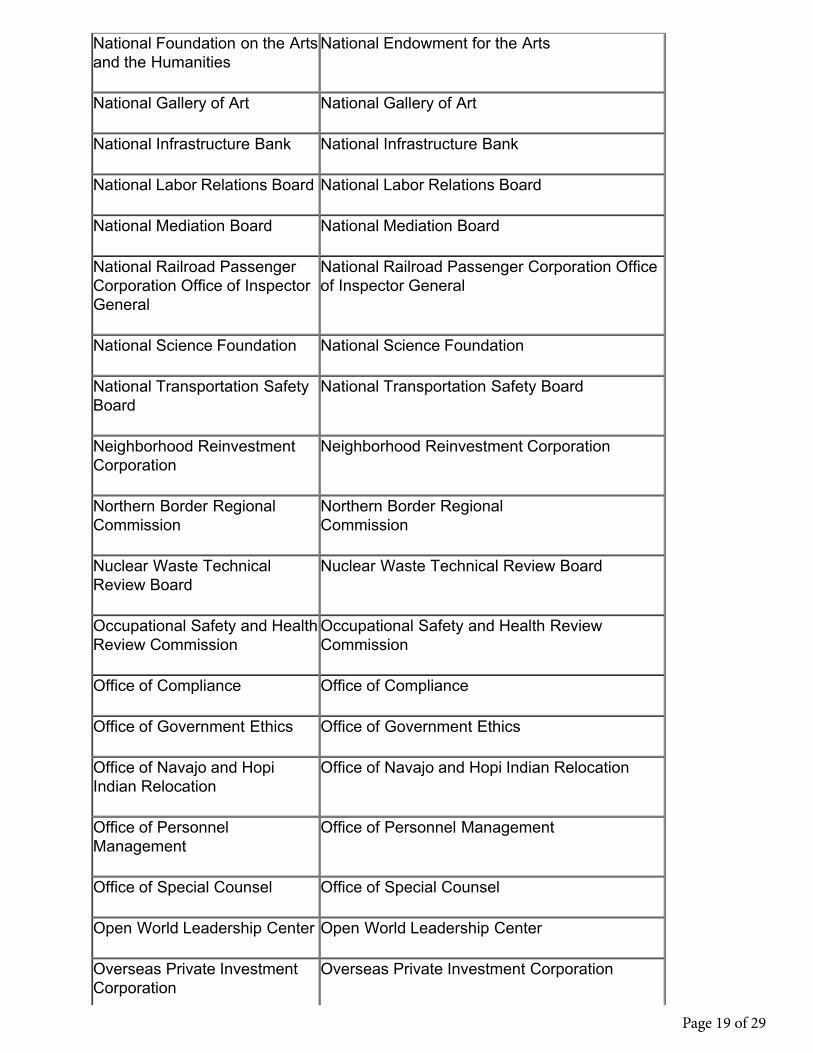

National Foundation on the Artsand the Humanities

National Endowment for the Arts

National Gallery of Art National Gallery of Art

National Infrastructure Bank National Infrastructure Bank

National Labor Relations Board National Labor Relations Board

National Mediation Board National Mediation Board

National Railroad PassengerCorporation Office of InspectorGeneral

National Railroad Passenger Corporation Officeof Inspector General

National Science Foundation National Science Foundation

National Transportation SafetyBoard

National Transportation Safety Board

Neighborhood ReinvestmentCorporation

Neighborhood Reinvestment Corporation

Northern Border RegionalCommission

Northern Border RegionalCommission

Nuclear Waste TechnicalReview Board

Nuclear Waste Technical Review Board

Occupational Safety and HealthReview Commission

Occupational Safety and Health ReviewCommission

Office of Compliance Office of Compliance

Office of Government Ethics Office of Government Ethics

Office of Navajo and HopiIndian Relocation

Office of Navajo and Hopi Indian Relocation

Office of PersonnelManagement

Office of Personnel Management

Office of Special Counsel Office of Special Counsel

Open World Leadership Center Open World Leadership Center

Overseas Private InvestmentCorporation

Overseas Private Investment Corporation

Page 19 of 29

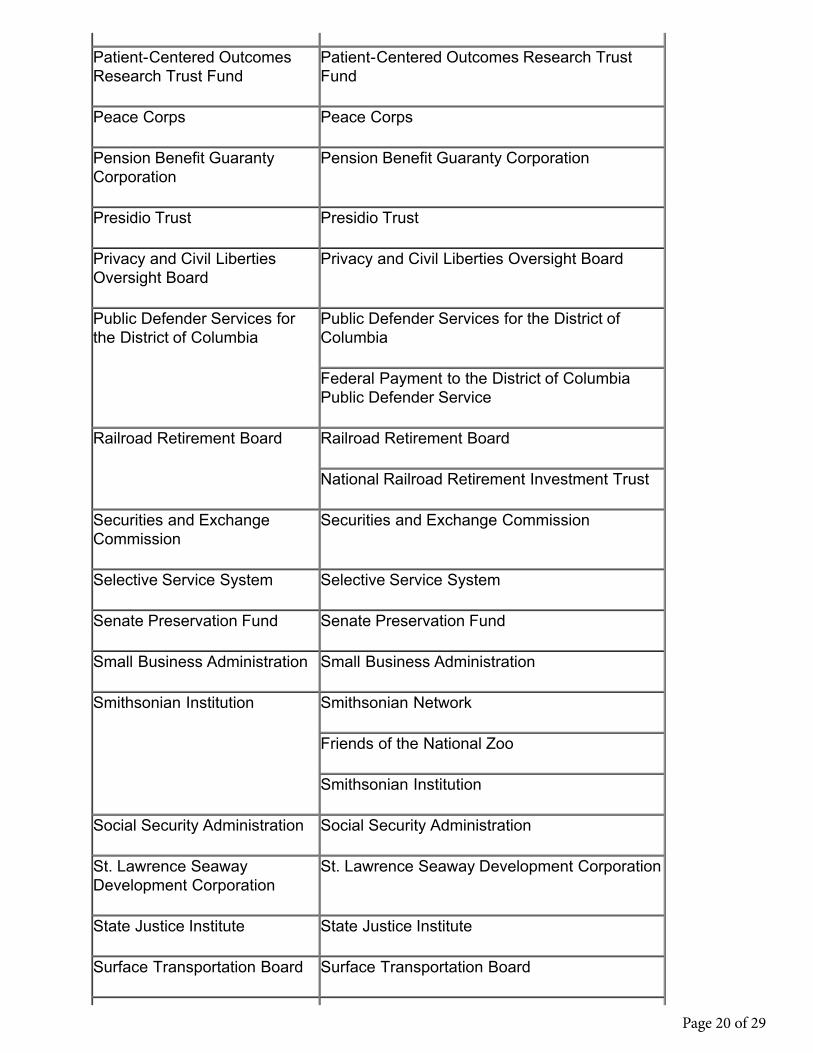

Patient-Centered OutcomesResearch Trust Fund

Patient-Centered Outcomes Research TrustFund

Peace Corps Peace Corps

Pension Benefit GuarantyCorporation

Pension Benefit Guaranty Corporation

Presidio Trust Presidio Trust

Privacy and Civil LibertiesOversight Board

Privacy and Civil Liberties Oversight Board

Public Defender Services forthe District of Columbia

Public Defender Services for the District ofColumbia

Federal Payment to the District of ColumbiaPublic Defender Service

Railroad Retirement Board Railroad Retirement Board

National Railroad Retirement Investment Trust

Securities and ExchangeCommission

Securities and Exchange Commission

Selective Service System Selective Service System

Senate Preservation Fund Senate Preservation Fund

Small Business Administration Small Business Administration

Smithsonian Institution Smithsonian Network

Friends of the National Zoo

Smithsonian Institution

Social Security Administration Social Security Administration

St. Lawrence SeawayDevelopment Corporation

St. Lawrence Seaway Development Corporation

State Justice Institute State Justice Institute

Surface Transportation Board Surface Transportation Board

Page 20 of 29

Tennessee Valley Authority Tennessee Valley Authority

The Judiciary Administrative Office of the United StatesCourts

Court of Appeals, District Courts, and otherJudicial Services

Judicial Retirement Fund

United States Court of Appeals for the FederalCircuit

United States Court of International Trade

Federal Judicial Center

United States Sentencing Commission

Judiciary Engineering and Modernization Center

Supreme Court of the United States

Thrift Savings Fund Federal Retirement Thrift Investment Board

Thrift Savings Fund

U.S. Capitol Police U.S. Capitol Police

U.S. Capitol PreservationCommission

U.S. Capitol Preservation Commission

U.S. Equal EmploymentOpportunity Commission

Equal Employment Opportunity Commission

U.S. Nuclear RegulatoryCommission

U.S. Nuclear Regulatory Commission

U.S. Postal Service U.S. Postal Service

U.S. Trade and DevelopmentAgency

Trade and Development Agency

United States Court of Appealsfor Veterans Claims

United States Court of Appeals for VeteransClaims

United States HolocaustMemorial

United States Holocaust MemorialMuseum

Page 21 of 29

Museum

United States Institute of Peace United States Institute of Peace

United States InteragencyCouncil on Homelessness

United States Interagency Council onHomelessness

United States Tax Court United States Tax Court

United States-China SecurityReview Commission-(withinTemporary Commissions)

United States-China Economic Security ReviewCommission

Vietnam Education Foundation Vietnam Education Foundation

Woodrow Wilson InternationalCenter for Scholars

Woodrow Wilson International Center forScholars

WWI Centennial Commission WWI Centennial Commission

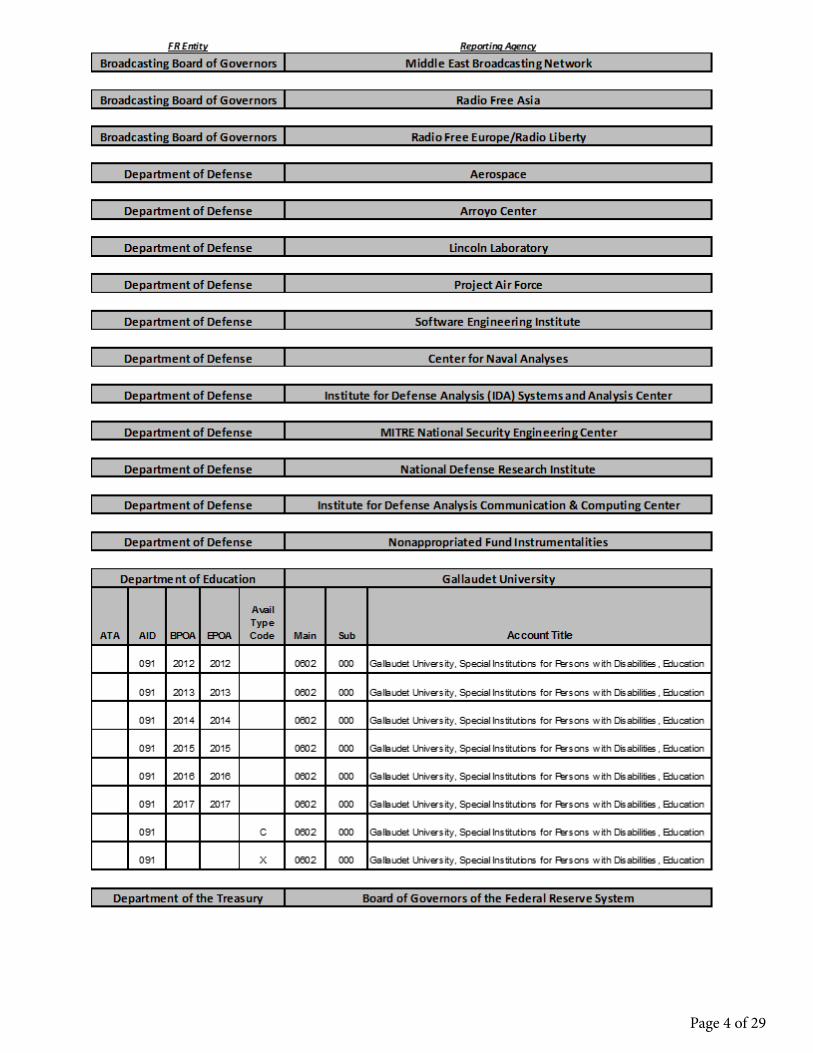

7. Disclosure Entities

FR Entity Reporting Agency

Broadcasting Board ofGovernors

Middle East Broadcasting Network

Radio Free Asia

Radio Free Europe/Radio Liberty

Department of Defense Aerospace

Arroyo Center

Lincoln Laboratory

Project Air Force

Software Engineering Institute

Center for Naval Analyses

Institute for Defense Analysis (IDA) Systemsand Analysis Center

MITRE National Security Engineering Center

Page 22 of 29

National Defense Research Institute

Institute for Defense Analysis Communication &Computing Center

Nonappropriated Fund Instrumentalities

Department of Education Gallaudet University

Department of the Treasury Board of Governors of the Federal ReserveSystem

Corporation for Public Broadcasting

Corporation for Travel Promotion

Federal Home Loan Mortgage Corp (FreddieMac)

Federal National Mortgage Association (FannieMae)

Federal Reserve System

Securities Investor Protection Corporation

Federal Reserve Banks

Institute of American Indian and Alaska NativeCulture and Arts Development

International Monetary Fund

Legal Services Corporation

Multilateral Assistance

Department of Transportation Amtrak (National Railroad Passenger ServiceCorp)

Maritime Administration/Employees Associationand Regimental Activities Non-AppropriatedFund Instrumentalities

Center for Advanced Aviation SystemDevelopment (FFRDC & administered by MITRECorporation)

Page 23 of 29

Federal CommunicationsCommission

Universal Service Administrative Company

Securities and ExchangeCommission

Public Company Accounting Oversight Board

Securities Investor Protection Corporation

8. Related Party

FR Entity Reporting Agency

Export-Import Bank of theUnited States

Private Export Funding Corporation

National Credit UnionAdministration

Federal Financial Institutions ExaminationCouncil

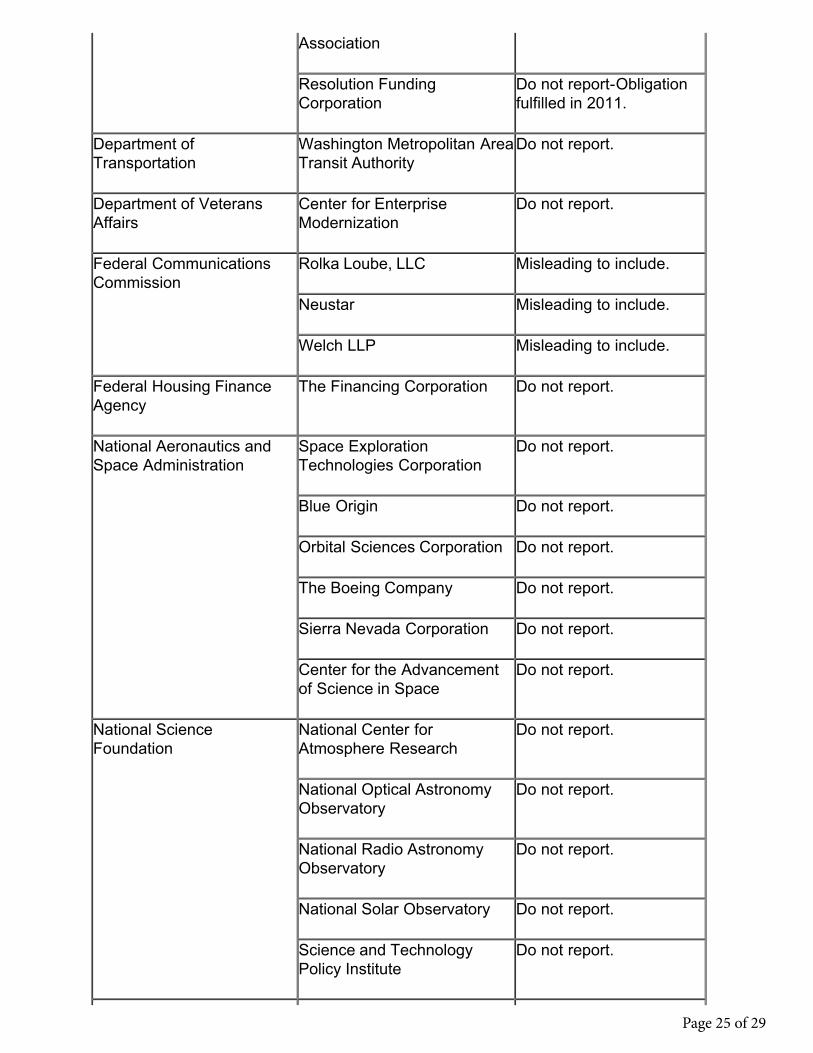

9. Misleading to Include/Do Not Report Entities

FR Entity Reporting Agency Determination

Office of the FederalCoordinator for AlaskaNatural Gas TransportationProjects

Office of the FederalCoordinator for Alaska NaturalGas Transportation Projects

Do not report-Entityclosed on March 7, 2015due to lack of funding.

Department of Education American Printing House forthe Blind

Do not report.

Howard University Do not report.

National Technical Institute forthe Deaf

Do not report.

Department of Energy Electric ReliabilityOrganization

Do not report.

United States EnrichmentCorporation Fund

Do not report.

Department of theInterior/OSMRE

United Mine Workers ofAmerica Benefit Funds

Do not report.

Department of the Treasury Federal Home Loan Banks Misleading to include.

Student Loan Marketing Do not report.

Page 24 of 29

Association

Resolution FundingCorporation

Do not report-Obligationfulfilled in 2011.

Department ofTransportation

Washington Metropolitan AreaTransit Authority

Do not report.

Department of VeteransAffairs

Center for EnterpriseModernization

Do not report.

Federal CommunicationsCommission

Rolka Loube, LLC Misleading to include.

Neustar Misleading to include.

Welch LLP Misleading to include.

Federal Housing FinanceAgency

The Financing Corporation Do not report.

National Aeronautics andSpace Administration

Space ExplorationTechnologies Corporation

Do not report.

Blue Origin Do not report.

Orbital Sciences Corporation Do not report.

The Boeing Company Do not report.

Sierra Nevada Corporation Do not report.

Center for the Advancementof Science in Space

Do not report.

National ScienceFoundation

National Center forAtmosphere Research

Do not report.

National Optical AstronomyObservatory

Do not report.

National Radio AstronomyObservatory

Do not report.

National Solar Observatory Do not report.

Science and TechnologyPolicy Institute

Do not report.

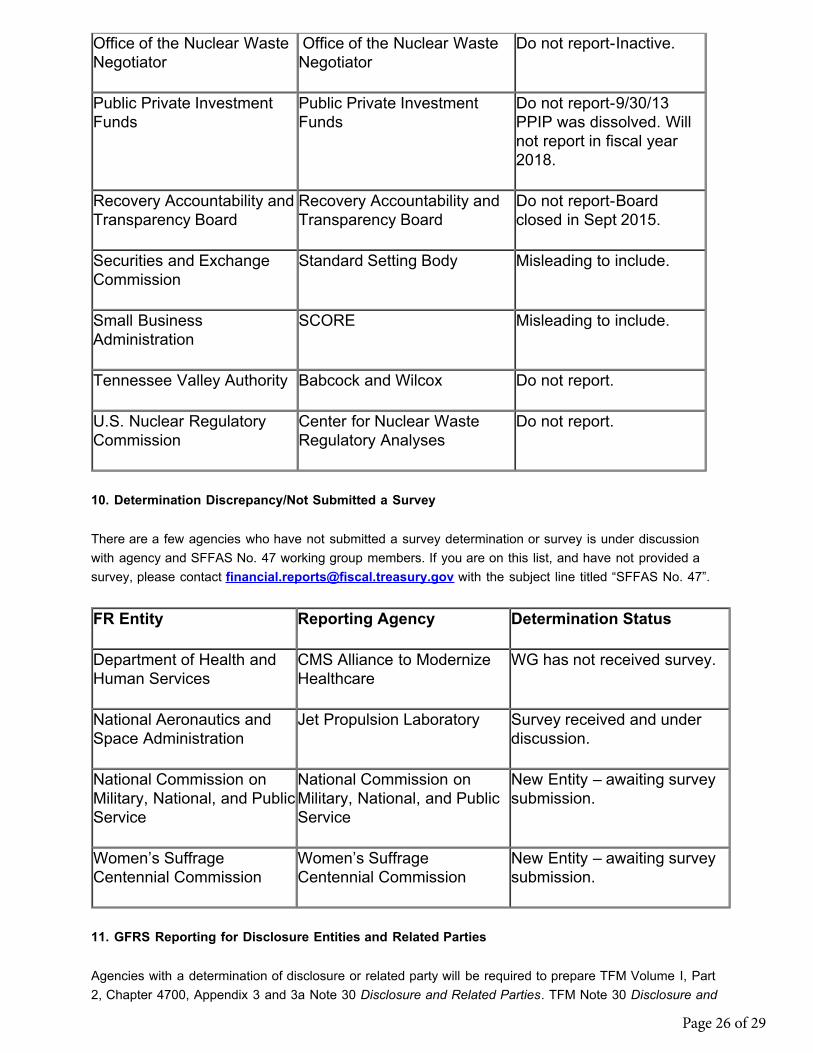

Page 25 of 29

Office of the Nuclear WasteNegotiator

Office of the Nuclear WasteNegotiator

Do not report-Inactive.

Public Private InvestmentFunds

Public Private InvestmentFunds

Do not report-9/30/13PPIP was dissolved. Willnot report in fiscal year2018.

Recovery Accountability andTransparency Board

Recovery Accountability andTransparency Board

Do not report-Boardclosed in Sept 2015.

Securities and ExchangeCommission

Standard Setting Body Misleading to include.

Small BusinessAdministration

SCORE Misleading to include.

Tennessee Valley Authority Babcock and Wilcox Do not report.

U.S. Nuclear RegulatoryCommission

Center for Nuclear WasteRegulatory Analyses

Do not report.

10. Determination Discrepancy/Not Submitted a Survey

There are a few agencies who have not submitted a survey determination or survey is under discussionwith agency and SFFAS No. 47 working group members. If you are on this list, and have not provided asurvey, please contact [email protected] with the subject line titled “SFFAS No. 47”.

FR Entity Reporting Agency Determination Status

Department of Health andHuman Services

CMS Alliance to ModernizeHealthcare

WG has not received survey.

National Aeronautics andSpace Administration

Jet Propulsion Laboratory Survey received and underdiscussion.

National Commission onMilitary, National, and PublicService

National Commission onMilitary, National, and PublicService

New Entity – awaiting surveysubmission.

Women’s SuffrageCentennial Commission

Women’s SuffrageCentennial Commission

New Entity – awaiting surveysubmission.

11. GFRS Reporting for Disclosure Entities and Related Parties

Agencies with a determination of disclosure or related party will be required to prepare TFM Volume I, Part2, Chapter 4700, Appendix 3 and 3a Note 30 Disclosure and Related Parties. TFM Note 30 Disclosure and

Page 26 of 29

Related Parties (see below) outlines the questions that will be asked during the fiscal year 2018 GFRSsubmission. In May 2018 the TFM Volume I, Part 2, Chapter 4700 will be published with the updates fordisclosure and related parties.

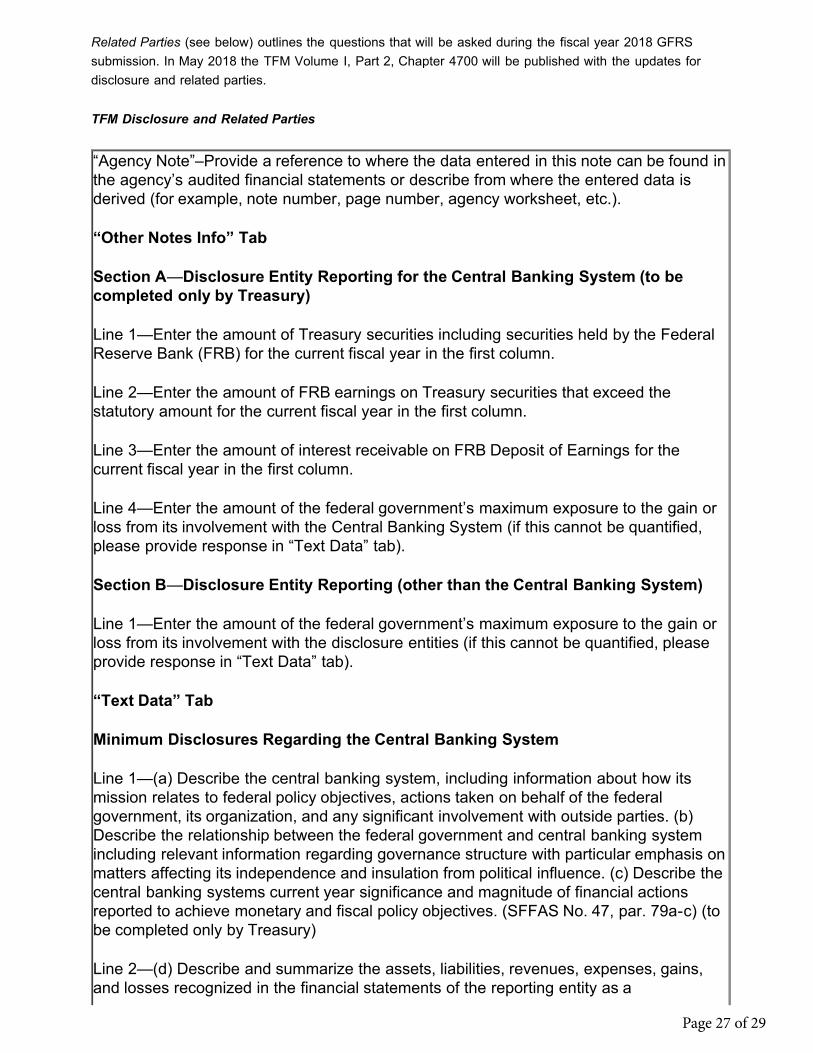

TFM Disclosure and Related Parties

“Agency Note”–Provide a reference to where the data entered in this note can be found inthe agency’s audited financial statements or describe from where the entered data isderived (for example, note number, page number, agency worksheet, etc.).

“Other Notes Info” Tab

Section A—Disclosure Entity Reporting for the Central Banking System (to becompleted only by Treasury)

Line 1—Enter the amount of Treasury securities including securities held by the FederalReserve Bank (FRB) for the current fiscal year in the first column.

Line 2—Enter the amount of FRB earnings on Treasury securities that exceed thestatutory amount for the current fiscal year in the first column.

Line 3—Enter the amount of interest receivable on FRB Deposit of Earnings for thecurrent fiscal year in the first column.

Line 4—Enter the amount of the federal government’s maximum exposure to the gain orloss from its involvement with the Central Banking System (if this cannot be quantified,please provide response in “Text Data” tab).

Section B—Disclosure Entity Reporting (other than the Central Banking System)

Line 1—Enter the amount of the federal government’s maximum exposure to the gain orloss from its involvement with the disclosure entities (if this cannot be quantified, pleaseprovide response in “Text Data” tab).

“Text Data” Tab

Minimum Disclosures Regarding the Central Banking System

Line 1—(a) Describe the central banking system, including information about how itsmission relates to federal policy objectives, actions taken on behalf of the federalgovernment, its organization, and any significant involvement with outside parties. (b)Describe the relationship between the federal government and central banking systemincluding relevant information regarding governance structure with particular emphasis onmatters affecting its independence and insulation from political influence. (c) Describe thecentral banking systems current year significance and magnitude of financial actionsreported to achieve monetary and fiscal policy objectives. (SFFAS No. 47, par. 79a-c) (tobe completed only by Treasury)

Line 2—(d) Describe and summarize the assets, liabilities, revenues, expenses, gains,and losses recognized in the financial statements of the reporting entity as a

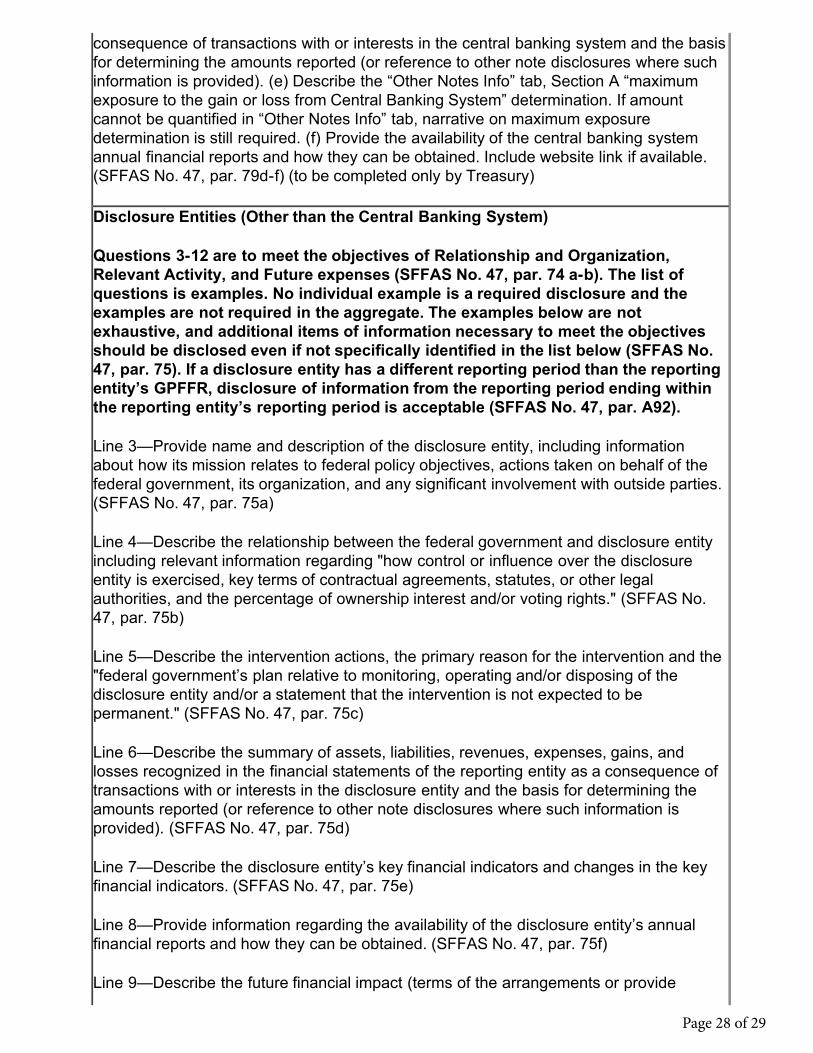

Page 27 of 29

consequence of transactions with or interests in the central banking system and the basisfor determining the amounts reported (or reference to other note disclosures where suchinformation is provided). (e) Describe the “Other Notes Info” tab, Section A “maximumexposure to the gain or loss from Central Banking System” determination. If amountcannot be quantified in “Other Notes Info” tab, narrative on maximum exposuredetermination is still required. (f) Provide the availability of the central banking systemannual financial reports and how they can be obtained. Include website link if available.(SFFAS No. 47, par. 79d-f) (to be completed only by Treasury)

Disclosure Entities (Other than the Central Banking System)

Questions 3-12 are to meet the objectives of Relationship and Organization,Relevant Activity, and Future expenses (SFFAS No. 47, par. 74 a-b). The list ofquestions is examples. No individual example is a required disclosure and theexamples are not required in the aggregate. The examples below are notexhaustive, and additional items of information necessary to meet the objectivesshould be disclosed even if not specifically identified in the list below (SFFAS No.47, par. 75). If a disclosure entity has a different reporting period than the reportingentity’s GPFFR, disclosure of information from the reporting period ending withinthe reporting entity’s reporting period is acceptable (SFFAS No. 47, par. A92).

Line 3—Provide name and description of the disclosure entity, including informationabout how its mission relates to federal policy objectives, actions taken on behalf of thefederal government, its organization, and any significant involvement with outside parties.(SFFAS No. 47, par. 75a)

Line 4—Describe the relationship between the federal government and disclosure entityincluding relevant information regarding "how control or influence over the disclosureentity is exercised, key terms of contractual agreements, statutes, or other legalauthorities, and the percentage of ownership interest and/or voting rights." (SFFAS No.47, par. 75b)

Line 5—Describe the intervention actions, the primary reason for the intervention and the"federal government’s plan relative to monitoring, operating and/or disposing of thedisclosure entity and/or a statement that the intervention is not expected to bepermanent." (SFFAS No. 47, par. 75c)

Line 6—Describe the summary of assets, liabilities, revenues, expenses, gains, andlosses recognized in the financial statements of the reporting entity as a consequence oftransactions with or interests in the disclosure entity and the basis for determining theamounts reported (or reference to other note disclosures where such information isprovided). (SFFAS No. 47, par. 75d)

Line 7—Describe the disclosure entity’s key financial indicators and changes in the keyfinancial indicators. (SFFAS No. 47, par. 75e)

Line 8—Provide information regarding the availability of the disclosure entity’s annualfinancial reports and how they can be obtained. (SFFAS No. 47, par. 75f)

Line 9—Describe the future financial impact (terms of the arrangements or provide

Page 28 of 29

financial support and liquidity, including events or circumstances that could expose thefederal government to a loss) to disclosure entities generated by contractual agreements,statues, or other legal authorities. (SFFAS No. 47, par. 75g)

Line 10—Describe the nature of, and changes in, the risks and benefits associated withthe control of, or other involvement with, the disclosure entity during the period. (SFFASNo. 47, par. 75h)

Line 11—Describe the “Other Notes Info” tab, Section B “maximum exposure to the gainor loss from the agencies involvement with the disclosure entity”. If amount cannot bequantified in “Other Notes Info” tab, narrative on maximum exposure determination is stillrequired including how the maximum exposure is determined. (SFFAS No. 47, par. 75i)

Line 12—Describe other information that would provide an understanding of the potentialfinancial impact, including financial-related exposures to risk of loss or potential gain tothe reporting entity, resulting from the disclosure entity’s operations including importantexisting, currently-known demands, risks, uncertainties, events, conditions, and trends-both favorable and unfavorable. (SFFAS No. 47, par. 75j)

Related Party Relationships

Line 13—Describe the nature of the federal government’s relationship with the relatedparty, including the name of the party or if aggregated, a description of the related parties.Such information also would include, as appropriate, the percentage of ownershipinterest. (SFFAS No. 47, par. 89a)

Line 14—Describe other information that would provide an understanding of therelationship and potential financial reporting impact, including financial-related exposuresto risk of loss or potential gain to the reporting entity resulting from the relationship.(SFFAS No. 47, par. 89b)

Effective Date

This bulletin is effective immediately.

Inquiries

Direct inquiries concerning this bulletin to:

Financial Reports and Advisory DivisionBureau of the Fiscal ServiceDepartment of the TreasuryPO Box 1328Parkersburg, WV 26106-1328Telephone: 304-480-6485Email: [email protected]

Date: March 29, 2018

Page 29 of 29