Embed Size (px)

Citation preview

TWENTY-FIFTH ANNUAL SURVEY OF WHITE COLLAR CRIMEEDITOR’S NOTE

INTRODUCTORY ESSAYA PROPOSAL FOR A UNITED STATES DEPARTMENT OF JUSTICE FOREIGN CORRUPT

PRACTICES ACT LENIENCY POLICY

POLICY PROPOSALFEDERAL CRIMINAL PROSECUTIONS OF KICKBACK ARRANGEMENTS IN THE HEALTHCARE

SECTOR INVOLVING PRIVATE PAY PATIENTS

ARTICLESANTITRUST VIOLATIONSCOMPUTER CRIMESCORPORATE CRIMINAL LIABILITYELECTION LAW VIOLATIONSEMPLOYMENT-RELATED CRIMESENVIRONMENTAL CRIMESFALSE STATEMENTS AND FALSE CLAIMSFEDERAL CRIMINAL CONSPIRACYFINANCIAL INSTITUTIONS FRAUDFOREIGN CORRUPT PRACTICES ACTHEALTH CARE FRAUDINTELLECTUAL PROPERTY CRIMESMAIL AND WIRE FRAUDMONEY LAUNDERINGOBSTRUCTION OF JUSTICEPERJURYPUBLIC CORRUPTIONRACKETEER INFLUENCED AND CORRUPT ORGANIZATIONSSECURITIES FRAUDTAX VIOLATIONS

VOLUME 47 SPRING 2010 NUMBER 2

Published bythe Georgetown University Law Center

Twenty-Fifth Annual Survey of White Collar CrimeEditor in Chief

KEVIN R. GLANDON

Twenty-Fifth Annual Survey of White Collar CrimeManaging EditorMICHAEL W. HOLT

Senior Annual Survey EditorsROLLO C. BAKER JUSTIN ALEXANDER KASPRISIN JESSICA L. MCCURDY

Annual Survey EditorsLYDIA CHAO

THERESA M. COUGHLIN

JONATHAN B. KRISCH

ALLISON L. FRUMIN

KATHERINE T. KLEINDIENST

RICK KOZELL

ABIGAIL H. LIPMAN

LISA C. PEARLSTEIN

MARK A. PROVOST

CRAIG THEDWALL

Editor in ChiefAIYSHA S. HUSSAIN

Senior Articles EditorBRIAN A. FOX

Managing EditorALLISON C. WHITE

Administrative EditorKATHERINE S. DUMOUCHEL

Executive EditorsTRISTAN S. BREEDLOVE

ERIC D. OLSON

Notes EditorsJOSEPH W. CORMIER

CRAIG FRANCIS DUKIN

Articles EditorsBETH CORRIGAN

COLLEEN B. DIXON

JILL K. PASQUARELLA

HEATHER J. SIGLER

Article Development EditorsBENJAMIN J. WOLINSKY

CRAIG THEDWALL

Article & Note EditorsSTEPHEN M. BLANK

KEVIN M. DAVIS

EMILY S. FULLER

SUNEEL J. NELSON

Note Development EditorsCAROLYN A. DELONE

DAVID E. DWORSKY

SPENCER GWARTNEY

ANDREA C. HALVERSON

MATTHEW R. KING

NATHANIEL D. SHAFER

CHRISTOPHER J. STUART

MEGHAN K. WOODSOME

PUBLISHED BY

The Georgetown University Law Center

VOLUME 47 SPRING 2010 NUMBER 2

AMERICANCRIMINAL

LAW REVIEW

EDITORIAL BOARD

INTRODUCTORY ESSAY

A PROPOSAL FOR A UNITED STATES DEPARTMENT OFJUSTICE FOREIGN CORRUPT PRACTICES ACT

LENIENCY POLICY

Robert W. Tarun & Peter P. Tomczak1

INTRODUCTION

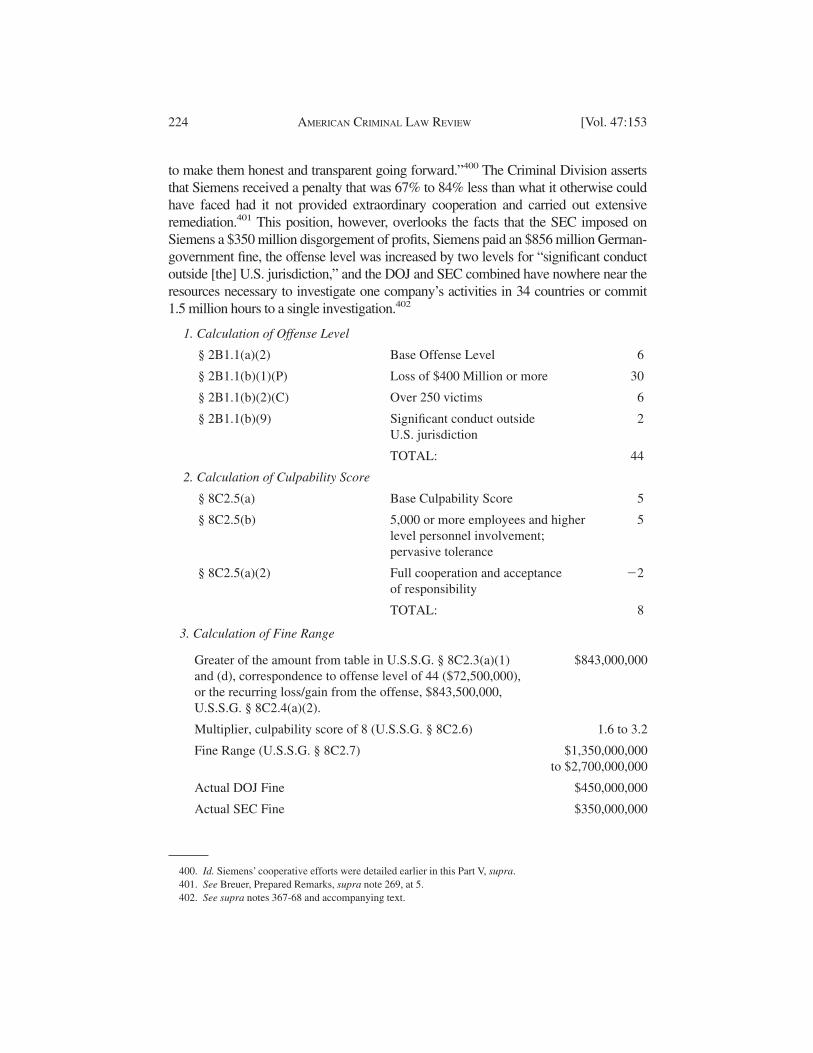

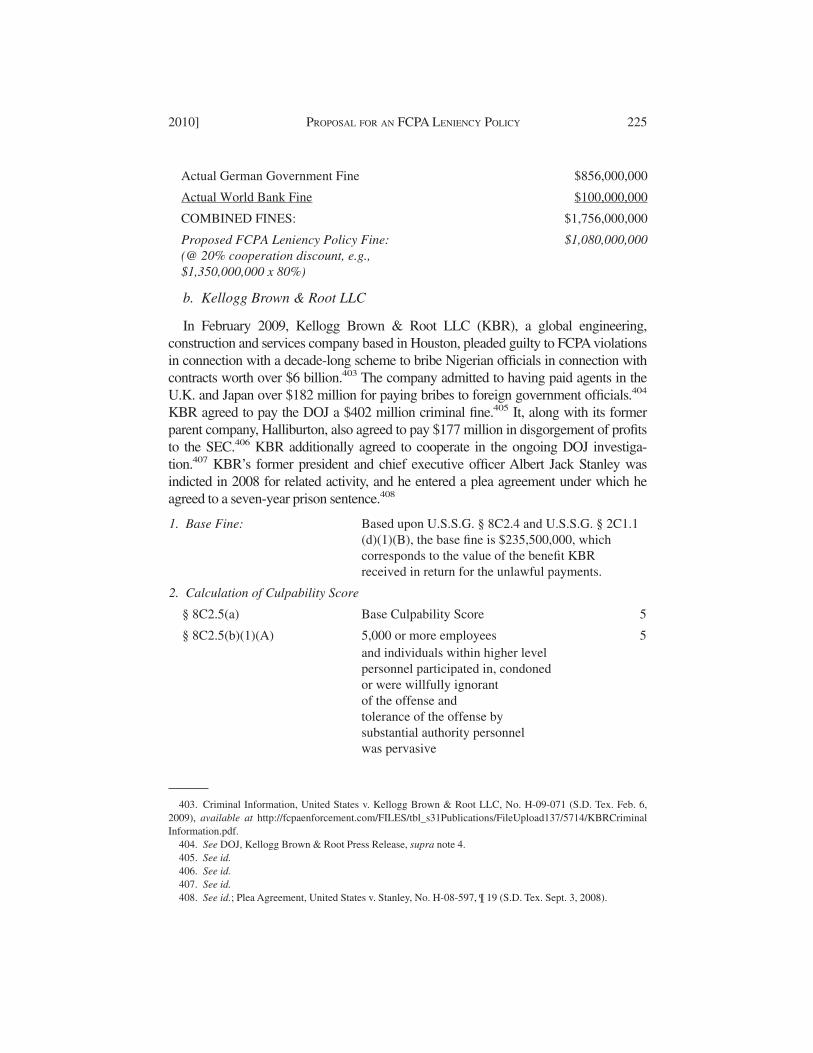

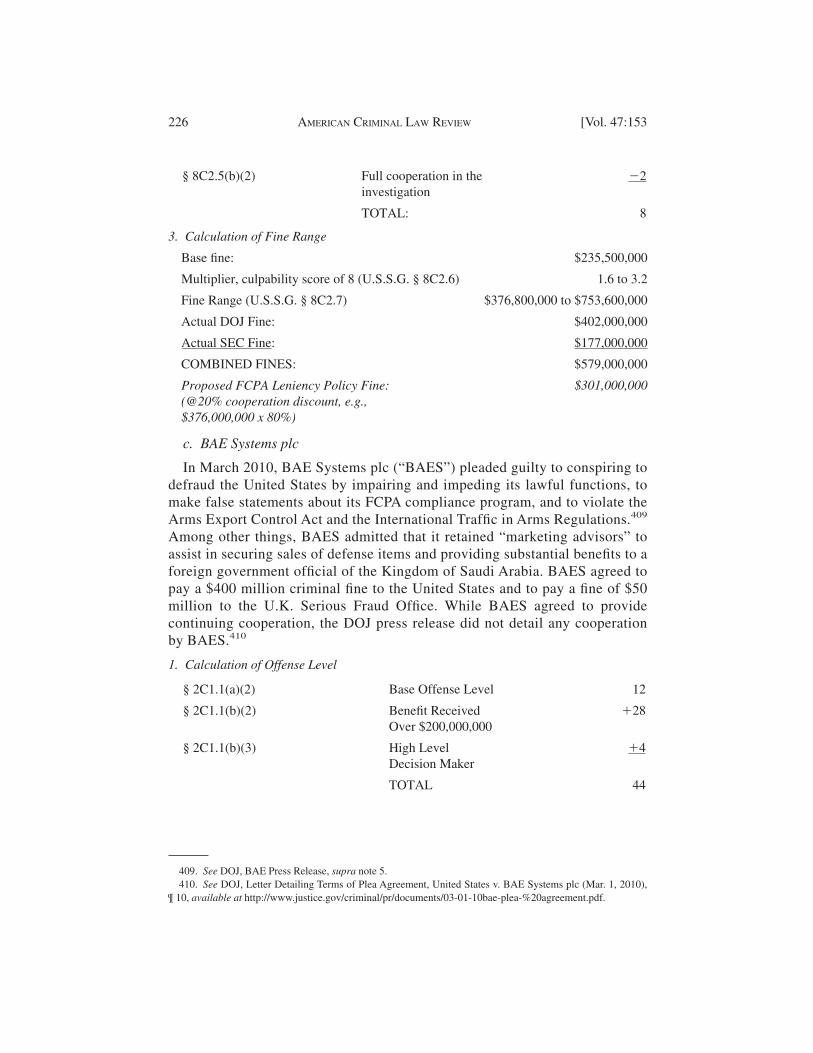

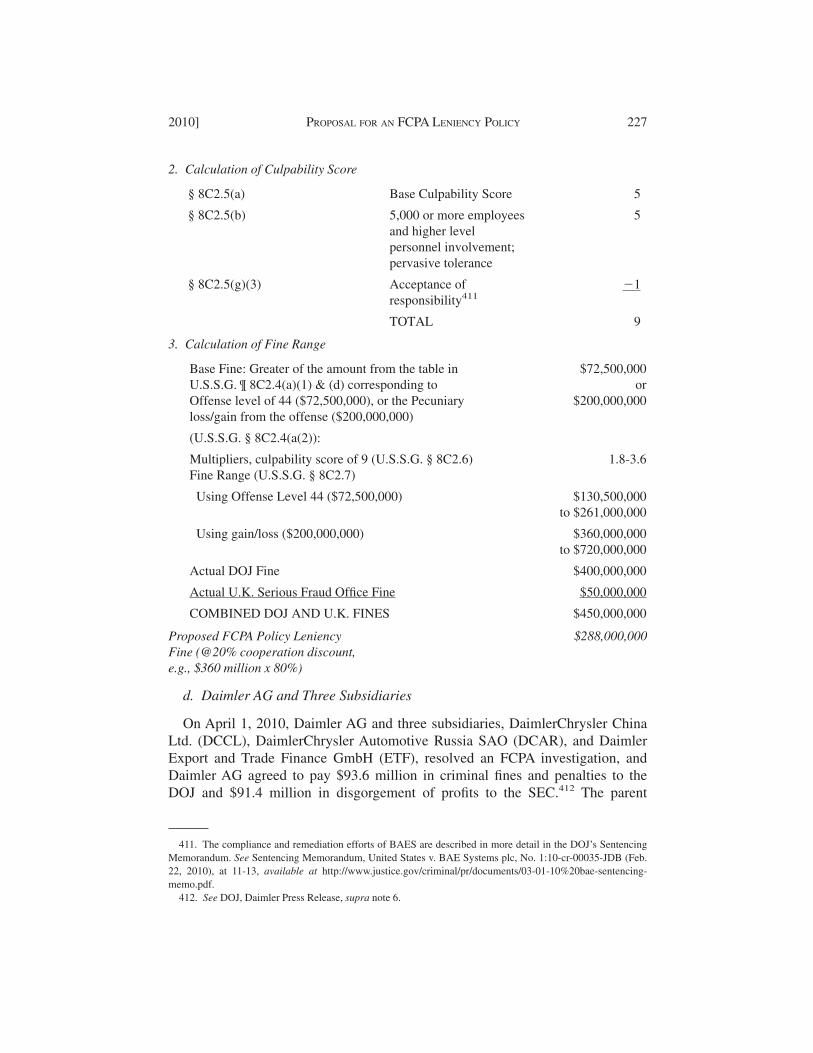

On December 15, 2008, the Fraud Section of the United States Department ofJustice (“DOJ”) and the United States Securities and Exchange Commission(“SEC”) announced that Siemens AG had pleaded guilty to violating the ForeignCorrupt Practices Act (“FCPA”)2 for a far-reaching and long-lasting briberyscheme of international scope, and had agreed, among other things, to payapproximately $1.6 billion in sanctions to United States and German law enforce-ment.3 On February 11, 2009, the DOJ and the SEC reported that Kellogg Brown& Root LLC had pleaded guilty to violating the FCPA in a decade-long briberyscheme, and had agreed with its present and former parent companies, amongother things, to pay $579 million in criminal fines and disgorged profits.4 OnMarch 1, 2010, the DOJ disclosed that BAE Systems plc had pleaded guilty toFCPA-related charges, and had agreed, among other things, to pay fines ofapproximately $400 million and $50 million to law enforcement authorities in the

1. Robert W. Tarun is a Principal, and Peter P. Tomczak is a Partner, in the San Francisco and Chicago offices,respectively, of Baker & McKenzie LLP. Mr. Tarun served as a federal prosecutor in the Northern District ofIllinois from 1976 to 1985, and as the Executive Assistant U.S. Attorney there from 1982 to 1985. The authorswish to thank Jay Martin of Houston, Texas, for his editorial insights, and Eileen T. Flynn, Linda F. Braggs andJames F. Brown of Baker & McKenzie LLP for their assistance in preparing edits to this Article. The views andopinions expressed in and any shortcomings of this Article are solely those of the authors. © 2010, Robert W.Tarun and Peter P. Tomczak.

2. Foreign Corrupt Practices Act of 1977, Pub. L. No. 95-213, 91 Stat. 1494 (codified as amended at 15 U.S.C.§ 78m, 78dd-1 to 78dd-3, 78ff).

3. See Press Release, DOJ, Siemens AG and Three Subsidiaries Plead Guilty to Foreign Corrupt Practices ActViolations and Agree to Pay $450 Million in Combined Criminal Fines (Dec. 15, 2008) [hereinafter DOJ, SiemensPress Release], available at http://www.justice.gov/opa/pr/2008/December/08-crm-1105.html; Press Release,SEC, SEC Charges Siemens AG for Engaging in Worldwide Bribery (Dec. 15, 2008) [hereinafter SEC, SiemensPress Release], available at http://www.sec.gov/news/press/2008/2008-294.htm.

4. See Press Release, DOJ, Kellogg Brown & Root LLC Pleads Guilty to Foreign Bribery Charges and Agreesto Pay $402 Million Criminal Fine (Feb. 11, 2009) [hereinafter DOJ, Kellogg Brown & Root Press Release],available at http://www.justice.gov/opa/pr/2009/February/09-crm-112.html; Press Release, SEC, SEC ChargesKBR and Halliburton for FCPA Violations (Feb. 11, 2009) [hereinafter SEC, KBR and Halliburton Press Release],available at http://www.sec.gov/news/press/2009/2009-23.htm.

153

United States and the United Kingdom, respectively.5 On April 1, 2010, the DOJannounced that Daimler AG and three of its subsidiaries had resolved FCPAinvestigations, and had agreed to pay the DOJ $93.6 million and the SEC $91.4million.6 Undoubtedly, the immense sanctions imposed on these four companiesconveyed a message: FCPA misconduct will be punished severely.7

Massive penalties like those noted above may deter corporate crimes.8 How-ever, because of how corporations9 respond to criminal sanctions, under somecircumstances, such measures may dissuade corporations from investigatingpurported misconduct and reporting detected crimes. In regards to FCPA viola-tions, corporations that must decide whether to report voluntarily bribery conductconfront considerable uncertainty as to the benefits (in the form of reducedsanctions) of self-reporting and cooperation.10 While self-reporting corrupt pay-ment activities results in indeterminate benefits, it does assure that law enforce-ment will know of the misconduct and, thus, in many instances, some sanction willbe imposed.11

Whether a corporation should undertake a costly internal investigation, self-report its employees or agents’ FCPA bribery conduct and cooperate fully with lawenforcement is a highly contextual decision that is not invariably answered in the

5. See Press Release, DOJ, BAE Systems plc Pleads Guilty and Ordered to Pay $400 Million Criminal Fine(Mar. 1, 2010) [hereinafter DOJ, BAE Press Release], available at www.justice.gov/opa/pr/2010/March/10-crm-209.html.

6. See Press Release, DOJ, Daimler AG and Three Subsidiaries Resolve Foreign Corrupt Practices ActInvestigation and Agree to Pay $93.6 Million in Criminal Penalties (Apr. 1, 2010) [hereinafter DOJ, DaimlerPress Release], available at www.justice.gov/opa/pr/2010/April/10-crm-360.html.

7. See SEC, KBR and Halliburton Press Release, supra note 4 (“‘FCPA violations have been and will continueto be dealt with severely by the SEC and other law enforcement agencies,’ said SEC Chairman Mary L.Schapiro.”); SEC, Siemens Press Release, supra note 3 (“‘The $1.6 billion in combined sanctions that Siemenswill pay in the U.S. and Germany should make clear that these corrupt business practices will be rooted outwherever they take place, and the sanctions for them will be severe.’” quoting Associate Director of the SEC’sDivision of Enforcement Cheryl J. Scarboro)). Interestingly, if the sanctions imposed on Siemens AG and KelloggBrown & Root LLC are removed from the analysis, the total fines imposed against corporations in a given yeardecreased from 2007 to 2009. See Shearman & Sterling LLP, FCPA Digest: Recent Trends & Patterns in FCPAEnforcement (Mar. 2010) [hereinafter 2010 Trends & Patterns], at 7, available at http://www.shearman.com/files/upload/FCPA-Trends-and-Patterns-Spring-2010.pdf.

8. This is a stated goal of the DOJ. See SEC, KBR and Halliburton Press Release, supra note 4 (quoting ActingAssistant Attorney General Rita M. Glavin of the Criminal Division of the DOJ as warning that, “‘[t]he successfulprosecution of KBR, and its agreement to pay a more than $400 million fine, demonstrates that no one is above thelaw, and that the Department is determined to seek penalties that are commensurate with, and will deter, this kindof serious criminal misconduct’”). Scholars have debated whether imposing liability on corporations deterscrime—a debate that is beyond the scope of this Article. See Miriam Hechler Baer, Insuring Corporate Crime, 83IND. L. J. 1035, 1036 n. 2 (2008) (collecting sources).

9. Unless otherwise indicated by the context, we refer throughout this Article to business enterprises,regardless of their form of legal entity, as “corporations”.

10. See infra Part III.C.11. See infra at III.B-C.

154 AMERICAN CRIMINAL LAW REVIEW [Vol. 47:153

affirmative.12 For example, if the underlying FCPA misconduct is egregious,bound to become public (such as through the federal securities laws’ disclosureregime or a whistleblower’s report) and subject to severe sanctions (such asdebarment), then a corporate decision-making body comprised of risk-adverseindividuals is significantly incentivized under the current legal sanction regime,including the Federal Sentencing Guidelines for Organizations (“SentencingGuidelines”),13 to self-report such misconduct and try to seize any possibility of amore lenient sentence. However, if that underlying misconduct is neither systemicnor likely to be independently detected by law enforcement, and the corporationbelieves that it will receive an insubstantial reduction in the sanction for self-reporting or be required to pay other costs in connection with self-reporting (suchas the costs of an internal investigation or those attendant to additional inquiriesfrom law enforcement), then a corporate decision-making body comprised of risk-neutral individuals may decide not to voluntarily report such misconduct. Themore difficult self-reporting decisions involve factual scenarios between these twoextreme ends of the sanctioning spectrum.14

Thus, situations exist in which corporations rationally and responsibly choose toremedy bribery conduct internally and not self-report misconduct. But if corpora-tions fail to report voluntarily the FCPA violations that they detect, then societycannot realize the substantial benefits from corporations self-reporting theiremployees and agents’ wrongdoing.15 Significantly, inducing corporations to bring

12. To be clear, we are not advocating that corporations always decline to report, more so ever undertake activesteps to conceal, wrongdoing by their employees or agents that they discover. Companies must, in allcircumstances, immediately stop any improper conduct and promptly undertake measures to prevent itsrecurrence. See In re Caremark Int’l Inc. Deriv. Litig., 698 A.2d 959, 971 (Del. Ch. 1996) (“In order to show thatthe Caremark directors breached their duty of care by failing adequately to control Caremark’s employees,plaintiffs would have to show either (1) that the directors knew or (2) should have known that violations of lawwere occurring and, in either event, (3) that the directors took no steps in a good faith effort to prevent or remedythat situation, and (4) that such failure proximately resulted in the losses complained of, although . . . this lastelement may be thought to constitute an affirmative defense.”). Nor do we claim that there is no incentive tovoluntarily report misconduct and, in certain circumstances, existing “carrots” of mitigated sanctions and/oravoidance of indictment are strong motivations to self-report detected malfeasance, particularly in light ofpotential disclosure obligations under the federal securities laws, see infra Part III.C.1.b, and disclosures by thirdparties, such as whistleblowers, see infra id. Nevertheless, these and other factors do not assure that allcorporations will under all circumstances fully investigate and voluntarily report each and every FCPA violationthat they uncover. See infra Part III.C.

13. 18 U.S.C. §§ 3551-3742 (2006); 28 U.S.C. § 991-98 (2006). On April 7, 2010, the Sentencing Guidelineswere amended, effective November 1, 2010. See infra note 62. Under United States v. Booker, the SentencingGuidelines are advisory and not mandatory. 543 U.S. 220, 245 (2005).

14. See infra Part III.D (discussing various factual scenarios and the incentives for a corporation to self-reportFCPA bribery conduct to law enforcement or remedy the misconduct internally).

15. See Louis Kaplow & Steven Shavell, Optimal Law Enforcement with Self-Reporting of Behavior, 102J. POL. ECON. 583, 584-596 (1994) (demonstrating that an optimal legal regime with self reporting is superior toan optimal legal regime without self-reporting for both one act and multiple act models); see also Robert Innes,Self-Reporting in Optimal Law Enforcement when Violators Have Heterogeneous Probabilities of Apprehension,29 J. LEGAL STUD. 287, 287-288, 291-96 (2000) (showing the benefits of self-reporting regimes). Certainly,“bribery of public officials abroad is, for the most part, harmful to the citizens of the particular country. The

2010] PROPOSAL FOR AN FCPA LENIENCY POLICY 155

FCPA bribery conduct to the attention of law enforcement agencies saves onenforcement costs.16 These savings are considerable in regards to FCPA investiga-tions, which “are the most challenging of all corporate investigations because thepotential misconduct is serious, many countries in which most misconduct mayhave occurred are distant and tolerant of corruption, interviewees are frequentlyhostile and indifferent to U.S. laws, and, in limited cases, there is personal risk toinvestigating counsel.”17 This Article therefore proposes a Fraud Section FCPAleniency policy modeled after the Antitrust Division’s well-recognized CorporateLeniency Program.

To date, the Fraud Section has declined to promulgate an FCPA leniency policyon likely three grounds. First, unlike with an Antitrust Division leniency applicant,a corporation that is engaged in improper payment activity usually cannot establisha criminal agreement with another corporate entity and thereby make a criminalcase against that other corporate entity for the Fraud Section.18 Therefore, thebenefit to law enforcement from a corporation’s investigation and cooperation isperceived to be neither as substantial to the Fraud Section nor as great to theAntitrust Division.19 However, corporate self-reporting of bribery conduct may

literature on corruption appears to have defeated the notion that bribery is efficient or desirable, and regimechange in certain corrupt countries has helped debunk that myth as well.” Philip Segal, Coming Clean on DirtyDealing: Time for a Fact-Based Evaluation of the Foreign Corrupt Practices Act, 18 FLA. J. INT’L L. 169, 172 &nn. 10-11 (2006) (collecting authorities and examples).

16. See Kaplow & Shavell, supra note 15, at 584 (explaining that this is “because those who commit harmfulacts are induced to report their behavior, enforcement effort need not be spent identifying them”).

17. ROBERT W. TARUN, THE FOREIGN CORRUPT PRACTICES ACT HANDBOOK: A PRACTICAL GUIDE FOR

MULTINATIONAL GENERAL COUNSEL, TRANSACTIONAL LAWYERS AND WHITE COLLAR CRIMINAL PRACTITIONERS 161(2010); see also Federal Bureal of Investigation, Bribes Beyond the Border: Stemming the Export of Corruption(Feb. 5, 2007) [hereinafter Bribes Beyond the Border], available at http://www.fbi.gov/page2/feb07/fcpa020507.htm (“FCPA cases are often complicated and difficult to prosecute. Overseas bribes are typically wellhidden in complex contracts and other procurement processes. The days of someone ‘accidentally’ leaving abriefcase full of money sitting on the floor after a business meeting to help grease the skids are long gone.”); cf.Brandon L. Garrett, Structural Reform Prosecution, 93 VA. L. REV. 853, 880-81 (2007) (“[O]rganizationalprosecutions require a substantial investment due to their complexity, the organizations’ greater ability to concealinformation, attorney-client privilege issues, access to very highly paid defense counsel, and the factualcomplexity of such cases.”).

18. James R. Doty, a former SEC General Counsel, has asserted that the corrupt practices and paymentsprohibited by the FCPA are similar to insider trading activities. See James R. Doty, Toward a Reg. FCPA: AModest Proposal for Change in Administering the Foreign Corrupt Practices Act, 62 BUS. LAW. 1233, 1240(2007).

19. By providing for leniency to self-reporting wrongdoers, law enforcement attempts to create a prisoner’sdilemma for colluding wrongdoers, thereby “undermining trust [between them] by shaping incentives to play oneparty against the other(s). . . .” Paolo Buccirossi & Giancarlo Spagnolo, Leniency Policies and Illegal Transac-tions, 90 J. PUBLIC ECON. 1281, 1282 (2006). In this manner, the antitrust leniency program deters the formation ofcartels, and speeds the demise of existing cartels. See generally Christopher R. Leslie, Trust, Distrust, andAntitrust, 82 TEX. L. REV. 515 (2004); Bruce H. Kobayashi, Antitrust, Agency and Amnesty: An EconomicAnalysis of the Criminal Enforcement of the Antitrust Laws Against Corporations, 69 GEO. WASH. L. REV. 715,728-31 (2001). The prisoner’s dilemma “has been very influential as a simple illustration of how’s people rationalpursuit of their individual best interests can lead to outcomes that are bad for all of them.” ROGER B. MYERSON,GAME THEORY: ANALYSIS OF CONFLICT 98 (Harvard Univ. Press 2002) (1991). In a single-play prisoner’s

156 AMERICAN CRIMINAL LAW REVIEW [Vol. 47:153

enable the Fraud Section to prosecute individual wrongdoers, including employeesand agents of the confessing corporation, and their co-conspirators.20 Corporateself-reporting may also enable U.S. and foreign law enforcement to prosecutecorrupt foreign government officials.21

Second, the Fraud Section may argue that public companies must already reportimproper payment activity under the federal securities laws and, in particular, theobligations imposed by the Sarbanes-Oxley Act of 2002 (“SOX”).22 However, notall bribery conduct will be required to be disclosed. As important, multinationalcompanies required to report under the federal securities laws may provide inmany instances extraordinary cooperation leading to the exposure of internationalcorruption that, absent corporate investigative efforts, would likely never havecome to the light given the limited resources of law enforcement and internationallegal hurdles. Extraordinary investigation and cooperation by multinational corpo-rations warrant extraordinary credit akin to that offered under the AntitrustDivision’s Corporate Leniency Program.

Third, the Fraud Section may contend that it currently treats cooperatingcompanies with leniency by, for example: limiting the conduct, countries and/ortime frames that cooperating companies need investigate; negotiating what con-duct will be part of the final sentencing-fine calculus; and, in limited instances,offering deferred or non-prosecution agreements.23 Such informal leniency is not

dilemma, the dominating strategy for each of the two prisoner-players is to confess on the other, so that the uniqueNash equilibrium is that of both prisoners confessing on each other. See id. at 97 (discussing R. D. LUCE AND H.RAIFFA, GAMES AND DECISIONS (1957)). However, this results in a greater punishment being imposed on bothprisoner-players than if they had both adopted the strategy of refusing to confess. See id. at 97-98.

20. Indeed, the DOJ has increasingly focused on prosecuting individuals engaged in FCPA misconduct,particularly in light of the perceived substantial deterrent effect of such prosecutions. Mark Mendelsohn, formerDeputy Chief of the DOJ’s Criminal Division, Fraud Section, has stated that “‘[t]o really achieve the kind ofdeterrent effect we’re shooting for, you have to prosecute individuals. . . . If the only sanctions out there aremonetary, penalties against companies could be interpreted as the cost of doing business. . . . But when people’sliberty is at stake, it resonates in new ways.’” Posting of Nathan Koppel, Now It’s Personal: The DOJ TargetsIndividuals in Prosecuting Bribery, WALL ST. J., Oct. 8, 2009, available at http://blogs.wsj.com/law/2009/10/08/now-its-personal-the-doj-targets-individuals-in-prosecuting-bribery/tab/print.

In this regard, though the FCPA context is not readily susceptible to making a case against another corporatedefendant, corporate and individual leniency programs may in some ways create a prisoner’s dilemma betweenthe corporation and certain of its employees and agents, thereby preventing bribery conduct. See generallyChristopher R. Leslie, Cartels, Agency Costs, and Finding Virtue in Faithless Agents, 49 WM. & MARY L. REV.1621 (2008) (focusing on links between cartel participants and their employees, as opposed to the relationshipsbetween corporate cartel participants, towards destabilizing cartels).

21. See 2010 Trends & Patterns, supra note 7, at 10-11 (summarizing two 2009 cases in which the DOJbrought non-FCPA charges against corrupt foreign government officials); Mike Koehler, The Foreign CorruptPractices Act in the Ultimate Year of Its Decade of Resurgence, 43 IND. L. REV. 389, 405-06 (2010) (same).

22. Pub. L. No. 107-204, 116 Stat. 745. Public companies may have reporting obligations in the wake ofantitrust violations, yet this has not deterred the Antitrust Division from expanding its leniency program and,indeed, promoting its criteria and principles to competition authorities around the world.

23. “Settlements without trial are the usual resolution of FCPA investigations and prosecutions.” Rebekah J.Poston et al., FCPA Due Diligence in Acquisitions, 43 REV. SEC. & COMMODITIES REG. 13, 14 (Jan. 20, 2010).Under a deferred prosecution agreement (DPA) and a non-prosecution agreement (NPA), “charges are filed and

2010] PROPOSAL FOR AN FCPA LENIENCY POLICY 157

transparent or instructive to decision-making bodies of corporations that are tryingto make informed decisions in the best interests of the corporations and theirshareholders about the benefits of fully investigating malfeasance, and voluntarilydisclosing it to and fully cooperating with law enforcement.24

In sum, while the typical inability of a leniency applicant to make a prosecutableFCPA case against another corporate entity, the potential obligation to disclosecertain FCPA violations under the federal securities laws and the current practiceof granting informal leniency may not weigh in favor of giving complete amnestyto a corporation that conducts a thorough, global investigation of potential FCPAmisconduct and discloses misconduct to and fully cooperates with law enforce-ment, it surely does not militate against the establishment of a clear, graduated, writtenleniency program for FCPA violations drawn from the Antitrust Division’s CorporateLeniency Program.25 The proposed FCPA leniency policy will provide much greaterclarity to corporations about the benefits and consequences of fully investigating andself-reporting FCPA violations. Finally, a U.S. anti-corruption leniency policy couldbecome, like it has in the case of theAntitrust Division’s Corporate Leniency Program, amodel for other law enforcement authorities, leading to greater global coordination incombating bribery of public officials.26

Part I of this Article summarizes the FCPA and the sanctions imposed oncorporations that, through their employees and agents, engage in bribery orcorruption in violation of the FCPA.27 Part II of this Article briefly reviews theSherman Act and its sanctions regime that punishes cartel behavior by corpora-

later dismissed (or in the case of an NPA, never filed at all), provided that the company adheres to the agreement’sother terms. With either agreement, no conviction ever occurs—which means that a federal judge never renders asentence, and Chapter 8 is never judicially applied.” Jay G. Martin & Ryan D. McConnell, How RevisedSentencing Guidelines Impact CCOs, COMPLIANCE WEEK (May 4, 2010), available at http://www.complianceweek.com/index.clm?fuseaction�article.viewArticle&articled�590388msg�. “‘The scope of things companies haveto worry about is enlarging all the time as the government asserts violations in circumstances where it’s unclear ifthey would prevail in court,’ says Lucinda Low, who has helped companies deal with the FCPA for years. ‘Youdon’t have the checks and balances you would normally have if you had more litigation.’” Nathan Vardi, TheBribery Racket, FORBES (May 24, 2010), at 74. Such agreements may be especially important to multinationalcorporations facing government debarment or suspension for felony bribery convictions. See infra notes 49 and341-42, and accompanying text, & note 393.

24. See generally F. Joseph Warin & Andrew S. Boutros, Response: Deferred Prosecution Agreements: A Viewfrom the Trenches and a Proposal for Reform, 93 VA. L. REV. IN BRIEF 121 (2007), available at http://virginialawreview.org/inbrief.php?s�2007/06/18/warin.

25. See infra note 135.26. See 2010 Trends & Patterns, supra note 7, at 15 (noting that “the DOJ approach is also reflected in the July

2009 ‘Approach of the Serious Fraud Office to Dealing with Overseas Corruption’ white paper issued by theU.K.’s [Serious Fraud Office]. In that paper, the [Serious Fraud Office] encourages self reporting and providesguidelines for reporting, investigation, and settlement.”); see also Doty, supra note 18, at 1251 n.57 andaccompanying text (noting influence of the FCPA on foreign anti-corruption laws).

27. The FCPA and the Sentencing Guidelines provide for punishment of individuals. In this Article, though, wefocus primarily on the punishment of corporations (“organizations”) and not individuals. For a brief discussion ofissues relating to the punishment of individuals under the FCPA, see Part V.A.1 of the FOREIGN CORRUPT

PRACTICES ACT article in this issue.

158 AMERICAN CRIMINAL LAW REVIEW [Vol. 47:153

tions, focusing upon the Corporate Leniency Program that the Antitrust Divisionhas successfully created and developed. Next, Part III of this Article reviews thearguments and evidence from academics and practitioners on the decision-makingprocess of corporations in regards to whether to self-report bribery conduct of theiremployees and agents. Finally, Part IV of this Article proposes an FCPA leniencypolicy based in substantial part on the Antitrust Division’s successful CorporateLeniency Program and criteria for the DOJ to adopt in rewarding, negotiating andlevying fines and other sanctions against corporate and employee violators of theFCPA anti-bribery laws.

I. A BRIEF OVERVIEW OF THE FCPA AND THE SANCTIONS IMPOSED FOR

VIOLATIONS OF THE FCPA

A. The Foreign Corrupt Practices Act

In 1977, in the wake of its inquiry into bribery of public officials in Japan andelsewhere by U.S. corporations, Congress enacted the FCPA to prohibit andcriminalize foreign bribery.28 The FCPA’s “anti-bribery” provisions expansivelyprohibit U.S. corporations and nationals, among other persons, from paying orgiving, or offering or promising to pay or give, directly or indirectly, money or anyother thing of value to any foreign government official, foreign political party orcandidate for foreign political office for the purpose of obtaining or retainingbusiness or some other unfair advantage.29 Further, the FCPA’s “accounting”provisions require “issuers” (as defined under the Securities Exchange Act of1934, as amended (the “Exchange Act”))30 to satisfy requirements governing thosecorporations’ recordkeeping and internal controls.31

Two law enforcement authorities, the DOJ and the SEC, are charged withenforcing the FCPA.32 The DOJ is solely responsible for the criminal enforcementof that statute.33 Specifically, the Fraud Section of the DOJ’s Criminal Divisioninvestigates and prosecutes bribery of foreign government officials and accounting

28. See Peter W. Schroth, American Law in a Time of Global Interdependence: U.S. National Reports to theXVIth International Congress of Comparative Law: Section V The United States and the International BriberyConventions, 50 AM. J. COMP. L. 593, 593-97 (2002). For a more detailed overview of the FCPA and itsprovisions, see generally TARUN, supra note 17, at 1-40, 207-09, 215-24, from which much of Part I is taken. For asummary of how the FCPA was born, see Judge Stanley Sporkin, Origins of the FCPA, Address at the ABA Nat’lInst. on the Foreign Corrupt Practices Act (Oct. 16, 2006) [hereinafter Judge Sporkin Speech], at 2-4 (on file withthe American Criminal Law Review) (describing FCPA’s origins in a voluntary disclosure program of the SEC).That program’s benefits were summarized in In re Sealed Case, 676 F. 2d 793, 818-19 (D.C. Cir. 1982).

29. See 15 U.S.C. §§ 78dd-1-dd-3 (2006).30. 15 U.S.C. § 78a et seq.; see also David E. Dworsky, Foreign Corrupt Practices Act, 46 AM. CRIM. L. REV.

671, 675-76 (2009) (explaining what corporations qualify as “issuers”).31. See 15 U.S.C. §§ 78m(b)(2)(A)-(B).32. See Dworsky, supra note 30, at 685 (citing, inter alia, S. REP. No. 95-114, at 11-12 (1977)); DOJ, Foreign

Corrupt Practices Act Antibribery Provisions Brochure [hereinafter DOJ Brochure], at 2, available at http://www.justice.gov/criminal/fraud/fcpa/docs/lay-persons-guide.pdf.

33. See DOJ Brochure, supra note 32, at 2.

2010] PROPOSAL FOR AN FCPA LENIENCY POLICY 159

violations under the books and records and internal controls provisions of theFCPA.34 FCPA bribery allegations are generally investigated by the FederalBureau of Investigation (“FBI”), which is required by internal regulation to bringalleged FCPA violations to the Fraud Section of the Criminal Division of theDOJ.35 No prosecution of an alleged FCPA violation may be brought without theexpress permission of the DOJ Criminal Division in Washington, D.C.36

The SEC is the “primary overseer and regulator of the U.S. securities mar-kets . . . .”37 Allegations of civil violations of the anti-bribery and recordkeepingprovisions are investigated by the SEC’s Division of Enforcement.38 In the case ofpublic companies, the SEC has regularly conducted parallel or joint FCPAinvestigations with the Fraud Section and sought civil penalties39 and, since 2004,disgorgement of profits and prejudgment interest.40 In 2009, the SEC EnforcementDivision announced the creation of an FCPA unit with staff around the countrydedicated to FCPA enforcement.41

The DOJ and SEC may jointly or separately initiate and conduct an FCPAinvestigation.42 They are increasingly conducting joint or parallel civil andcriminal investigations of the same FCPA allegations involving public compa-nies.43 The Fraud Section of the DOJ has FCPA expertise and frequently coordi-nates with the SEC Enforcement Division on FCPA matters, and vice versa.44 It

34. See Christopher A. Wray & Robert K. Hur, Corporate Criminal Prosecution in a Post-Enron World: TheThompson Memo in Theory and Practice, 43 AM. CRIM. L. REV. 1095, 1161 n.315 (2006) (citing U.S. DEP’T OF

JUSTICE, U.S. ATTORNEYS’ MANUAL, CRIMINAL RESOURCE MANUAL § 1018) (1997)). The Fraud Section isexpected to increase in size by as much as 50% in the near future. See David Hechler, DOJ Unit that ProsecutesFCPA to Bulk Up ‘Substantially,’ CORPORATE COUNSEL (Feb. 26, 2010), available at http://www.law.com/jsp/articlejsp?id�12024446/2530.

35. U.S. DEP’T OF JUSTICE, U.S. ATTORNEYS’ MANUAL, CRIMINAL RESOURCE MANUAL § 1015 (1997).[hereinafter U.S. ATTORNEYS’ MANUAL]. The FBI has established a team of special agents that focuses oninvestigating FCPA violations. See Bribes Beyond the Border, supra note 17. This dedicated team of agents hasinvestigated several, recent high-public FCPA cases. See, e.g., DOJ, BAE Press Release, supra note 5.

36. U.S. ATTORNEYS’ MANUAL § 9-47.110 (1997).37. See SEC, The Investor’s Advocate: How the SEC Protects Investors, Maintains Market Integrity, and

Facilitates Capital Formation, available at http://www.sec.gov/about/whatwedo.shtml (last visited Mar. 9, 2010).38. See Dworsky, supra note 30, at 685; David C. Weiss, Note, The Foreign Corrupt Practices Act, SEC

Disgorgement of Profits, and the Evolving International Bribery Regime: Weighing Proportionality, Retribution,and Deterrence, 30 MICH. J. INT’L L. 471, 478 (2009).

39. See Dworsky, supra note 30, at 685-86; Weiss, supra note 38, at 478.40. See Weiss, supra note 38 at 484. For examples of parallel proceedings resulting in the imposition of

criminal fines by the DOJ as well as civil disgorgement by the SEC, see Doty, supra note 18, at 1237 n.11.41. Robert Khuzami, Dir., SEC Div. of Enforcement, Remarks Before the New York City Bar: My First 100

Days as Director of Enforcement (Aug. 5, 2009), available at http://www.sec.gov/news/speech/2009/spch080509rk.htm (announcing formation of specialized Foreign Corrupt Practices Act Unit of the SEC).

42. See SEC v. Dresser Indus., Inc., 628 F.2d 1368, 1379 (D.C. Cir. 1980); Weiss, supra note 38, at 478.43. See, e.g., SECURITIES INVESTIGATIONS, ch. 5, Cooperation in SEC and DOJ Cases (Richard J. Morvillo ed.

2009).44. See SEC, KBR and Halliburton Press Release, supra note 4 (Director of SEC’s Division of Enforcement

Linda Chatman Thomsen stating: “‘This case demonstrates the close and cooperative working relationships thathave developed in FCPA investigations among the SEC, the U.S. Department of Justice, and foreign law

160 AMERICAN CRIMINAL LAW REVIEW [Vol. 47:153

has become common for the DOJ and SEC to announce settlements of FCPAinvestigations simultaneously.45

In 1994, the then largest DOJ corporate fine in an FCPA prosecution was the$24.8 million penalty imposed on Lockheed.46 In December 2008, the FraudSection, in conjunction with German authorities and the SEC, obtained recordanti-corruption penalties totaling approximately $1.6 billion from Siemens AG andthree of its foreign subsidiaries.47 Seven months later, the World Bank sanctionedSiemens AG and obtained an additional $100 million fine, resulting in a total fineof $1.7 billion.48

B. FCPA Violations: Criminal Penalties and the Sentencing Guidelines

The FCPA establishes maximum fines that may be imposed against corporationsthat violate its anti-bribery and accounting provisions. The statutory maximumcriminal penalties49 for corporations are: (i) $2,000,000 for each violation of theFCPA’s anti-bribery provisions;50 and (ii) $25,000,000 for each violation of theFCPA’s accounting provisions.51 Moreover, under the Alternative Fines Act, a fineequal to twice the gross gain or gross loss resulting from the offense, whichever isgreatest, may be imposed.52 In numerous cases, U.S. law enforcement agencieshave successfully imposed penalties and sanctions that, in aggregate, exceed thestatutory maximums.53 The criminal provisions of the FCPA have always providedfor felony conviction.

1. The Corporate Sentencing Calculus

For the DOJ as well as defendant corporations, the potential corporate finestarting point in corporate prosecutions is the Sentencing Guidelines and, in

enforcement agencies and securities regulators.’”). These investigations may entail working in conjunction withother agencies, such as the Internal Revenue Service and U.S. Immigration and Customs Enforcement. SeeMarsha Z. Gerber et al., Voluntary Disclosure of FCPA Violations, 43 REV. SEC. & COMMODITIES REG. 55, 59(2010) (describing the investigations of Gerald and Patricia Green, and Shu Quan-Sheng).

45. See, e.g., supra notes 3-4.46. See United States v. Lockheed Corp., No. CR.A. 194CR226MHS, 1995 WL 17064259 (N.D. Ga. Jan. 9,

1995) (discussing indictment against Lockheed Corporation, Allen R. Love, and Suleiman A. Nassar).47. See supra note 3 and accompanying text.48. See Vanessa Fuhrmans, Siemens Settles with World Bank on Bribes, WALL ST. J., July 3, 2009, at B1.49. The FCPA also provides for civil penalties. See Dworsky, supra note 30, at 689-90. In addition,

corporations that violate the FCPA may be debarred from doing business with the U.S. government, or have theirexport licenses revoked. See id. at 690; see also id. at 687 (citing, inter alia, U.S. DEP’T OF STATE, FIGHTING

GLOBAL CORRUPTION: BUS. RISK MGMT. (2001), at 28, available at http://www.ogc.doc.gov/pdfs/Fighting_Global_Corruption.pdf (“The President has directed that no executive agency shall allow any party to participate in anyprocurement or nonprocurement activity if any agency has debarred, suspended, or otherwise excluded that partyfrom participation in a procurement or nonprocurement activity.”)).

50. 15 U.S.C. § 78dd-2(g) (2006).51. 15 U.S.C. § 78ff(a) (2006).52. 15 U.S.C. § 78dd-2(g); 18 U.S.C. § 3571(a) (2006).53. See Dworsky, supra note 30, at 689 (collecting examples).

2010] PROPOSAL FOR AN FCPA LENIENCY POLICY 161

particular, Chapter 8, which governs the sentencing of “organizations.”54 Ingeneral, the fine range is a product of the seriousness of the offense and theculpability of the corporation. A corporate fine is based on a five-step process.55

“First, the seriousness of the offense . . . is computed and reflected in a numbercalled the ‘Base Fine.’”56 This equals “the greatest of: (1) the amount from a tablecorresponding to a calculation under the individual Guidelines; (2) the pecuniarygain to the [corporation] from the offense; or (3) the pecuniary loss from theoffense caused by the [corporation], to the extent” caused intentionally, knowinglyor recklessly.57

“Second, the culpability of the [corporation] is assessed by adding up the[corporation’s] ‘Culpability Score.’ One begins the computation with a score offive.”58 Points may be added depending upon: the size of the corporation; the leveland degree of discretionary authority of individuals who participated in ortolerated the criminal activity; whether the corporation had a fairly recent historyof similar misconduct; whether the offense violated a judicial order, injunction, orcondition of probation; or whether the corporation willfully obstructed or at-tempted to obstruct justice during the investigation, prosecution or sentencing ofthe offense.59 Points may be subtracted if: (1) the offense occurred even though thecorporation had in place a compliance and ethics program; or (2) the corporationself-reports, cooperates, and accepts responsibility.60

As noted, a corporation may receive a lesser sanction with a three-pointdeduction from its culpability score if its employees or agents violated the FCPA“even though the organization had in place at the time of the offense an effectivecompliance and ethics program. . . .”61 The Sentencing Guidelines set forth the

54. See Martin & McConnell, supra note 23 (“Despite Booker and the rise of DPAs/NPAs, Chapter 8 remains acritical consideration for corporate compliance programs because every corporate criminal prosecution (regard-less of any conviction) begins with a charging decision and a fine calculation under the guidelines.”).

55. See JULIE O’SULLIVAN, FEDERAL WHITE COLLAR CRIME (3d ed. 2007) at 209-216 (describing in greaterdetail the five-step process summarized in this Article).

56. Id. at 209.57. Id. (citing U.S. SENTENCING GUIDELINES MANUAL § 8C2.4 (2009) [hereinafter U.S.S.G. MANUAL]). In

many FCPA cases, the pecuniary gain to the corporation will be the greatest amount.58. Id. at 210.59. See id., § 8C2.5(b-e).60. See id., § 8C2.5(f-g).61. Id. § 8C2.5(f)(1). Commentators contend that the Sentencing Guidelines helped create a self-serving

compliance industry. See, e.g., Miriam Hechler Baer, Governing Corporate Compliance, 50 B.C.L. REV. 949,993-99 (2009); Frank O. Bowman, III, Drifting Down the Dnieper With Prince Potemkin: Some SkepticalReflections About the Place of Compliance Programs in Federal Criminal Sentencing, 39 WAKE FOREST L. REV.671, 679-90 (2004). Others have posited that compliance programs, if merely cosmetic, may lead to inefficientcorporate monitoring structures. See generally Kimberly D. Krawiec, Cosmetic Compliance and the Failure ofNegotiated Governance, 81 WASH. U.L.Q. 487 (2003). The BAE enforcement action, however, demonstrates thatcorporations who misrepresent the efficiency of their internal controls and compliance programs do so at theirperil. See DOJ, BAE Press Release, supra note 5 (“Despite BAES’s representations to the U.S. government to thecontrary, BAES knowingly and willfully failed to create sufficient compliance mechanisms to prevent and detectviolations of the anti-bribery provisions of the FCPA.”).

162 AMERICAN CRIMINAL LAW REVIEW [Vol. 47:153

criteria for an effective compliance and ethics program for purposes of theculpability score, and currently requires, among other things, that:

(1) The organization shall establish standards and procedures to prevent anddetect criminal conduct.(2) (A) The organization’s governing authority shall be knowledgeable aboutthe content and operation of the compliance and ethics program and shallexercise reasonable oversight with respect to the implementation and effective-ness of the compliance and ethics program.

(B) High-level personnel of the organization shall ensure that the organiza-tion has an effective compliance and ethics program, as described in thisguideline. . . .(3) The organization shall use reasonable efforts not to include within thesubstantial authority personnel of the organization any individual whom theorganization knew, or should have known through the exercise of due dili-gence, has engaged in illegal activities or other conduct inconsistent with aneffective compliance and ethics program.(4) (A) The organization shall take reasonable steps to communicate periodi-cally and in a practical manner its standards and procedures, and other aspectsof the compliance and ethics program, [throughout the organization and asappropriate, the organization’s agents] by conducting effective training pro-grams and otherwise disseminating information appropriate to such individu-als’ respective roles and responsiblities. . . .(5) The organization shall take reasonable steps—(A) to ensure that theorganization’s compliance and ethics program is followed, including monitor-ing and auditing to detect criminal conduct; (B) to evaluate periodically theeffectiveness of the organization’s compliance and ethics program; and (C) tohave and publicize a system, which may include mechanisms that allow foranonymity or confidentiality, whereby the organization’s employees and agentsmay report or seek guidance regarding potential or actual criminal conductwithout fear of retaliation.(6) The organization’s compliance and ethics program shall be promoted andenforced consistently throughout the organization through (A) appropriateincentives to perform in accordance with the compliance and ethics program;and (B) appropriate disciplinary measures for engaging in criminal conductand for failing to take reasonable steps to prevent or detect criminal conduct.(7) After criminal conduct has been detected, the organization shall takereasonable steps to respond appropriately to the criminal conduct and toprevent further similar criminal conduct, including making any necessarymodifications to the organization’s compliance and ethics program.62

62. U.S.S.G. MANUAL § 8B2.1(b)(1-7). These requirements have been in place, with minor modifications,since 2004. On April 7, 2010, the U.S. Sentencing Commission approved changes to the Sentencing Guidelines,effective November 1, 2010, that amend the definition of what constitutes an effective compliance program. SeeU.S. Sentencing Commission, Amendments to the Sentencing Guidelines [hereinafter 2010 Amendments to theSentencing Guidelines], available at http://www.ussc.gov/2010guid/finalamend10.pdf. Among other things, the

2010] PROPOSAL FOR AN FCPA LENIENCY POLICY 163

This downward departure is not available, however, “if, after becoming aware ofan offense, the [corporation] unreasonably delayed reporting the offense toappropriate governmental authorities.”63 The downward departure for effectivecompliance and ethics programs also is not, or a rebuttable presumption exists thatit is not, available if certain high-level officials “participated in, condoned, or[were] willfully ignorant of the offense.”64

Downward departures of one, two or five points off of a corporation’s culpabil-ity score are also available for varying degrees of self-reporting, cooperation, andacceptance of responsibility by the corporation.65 The report “must be made underthe direction of the” corporation.66 A cooperating corporation must be “both timelyand thorough” and “disclose all pertinent information known by the” corporationto receive a downward departure under the Sentencing Guidelines.67

Third, after the culpability score is calculated, it is assigned a minimummultiplier and a maximum multiplier.68 The two multipliers “are then applied tothe Base Fine amount, and the result is a fine range.”69

Fourth, a sentencing court should consider in determining the amount of the finewithin the applicable range such factors as the corporation’s “role in the offense,any nonpecuniary loss caused or threatened by the offense, prior [corporate]misconduct . . . not previously counted, and any prior criminal record of high-levelpersonnel in the” corporation and whether it failed to have, at the time of theoffense, an effective compliance and ethics program.70

Fifth, a sentencing court may consider other factors in granting an upward ordownward departure, including “substantial assistance to the authorities in theinvestigation or prosecution ‘of another organization that has committed anoffense, or in the investigation and prosecution of an individual not directly

2010 Amendments to the Sentencing Guidelines clarified what is a reasonable corporate response to criminalactivity. See id. at 17 (adding new Application Note 6 to Section 8B2.1 of the Sentencing Guidelines). For adiscussion of the impact of these amendments, see generally Martin & McConnell, supra note 23.

63. U.S.S.G. MANUAL § 8C2.5(f)(2).64. Id., § 8C2.5(f)(3). The 2010 Amendments to the Sentencing Guidelines relax this condition, and provide

that a corporation’s compliance program may be deemed as “effective,” despite the involvement of high levelcorporate employees in the wrongdoing, if, inter alia, the compliance program meets certain criteria. See Martin& McConnell, supra note 23.

65. See id., § 8C2.5(g).66. Id., § 8C2.5 cmt.11.67. Id., § 8C2.5 cmt.12.68. See O’SULLIVAN, supra note 55, at 213 (citing U.S.S.G. MANUAL § 8C2.6).69. Id. (citing U.S.S.G. MANUAL § 8C2.7).70. See id. at 214 (citing U.S.S.G. MANUAL § 8C2.8) (“Determining the Fine within the Range (Policy

Statement)”). A court must add to this calculated fine “any gain to the [corporation] from the offense that has notand will not be paid as restitution or by way of other remedial measures.” Id., § 8C2.9. This guideline usuallyapplies to offenses that lack identifiable victims. See id., § 8C2.9 cmt. 1. Notwithstanding its availability, theAntitrust Division regularly has not sought restitution orders in corporate plea agreements. See, e.g., PleaAgreement, United States v. Epson Imaging Devices Corp., No. 3:09-cr-00854-SI, ¶ 12 (N.D. Cal. Oct. 23, 2009);Plea Agreement, United States v. LG Display Co., No. CR 08-0803-SI, ¶ 12 (N.D. Cal. Dec. 8, 2008).

164 AMERICAN CRIMINAL LAW REVIEW [Vol. 47:153

affiliated with the defendant who has committed an offense,’”71 “threats tonational security”72 or “to a market flowing from the offense,”73 and “remedialcosts that greatly exceed the gain from the offense.”74 In practice, these fourth andfifth steps are rarely applicable to either Antitrust Division or Fraud Sectioncorporate pleas, as those final fines are usually numbers negotiated between theUnited States and the corporate defendants, e.g., the aggravating or mitigatingfactors in steps 4 and 5.

Further, under the Alternative Fines Act, a fine may be imposed equal to twicethe gross gain or twice the gross loss resulting from the offense, whichever is thegreater.75 (Of course, the Antitrust Division follows its Corporate LeniencyProgram in negotiating and reaching an agreed fine figure.) While the DOJ and acorporate target may negotiate over various sentencing enhancements, the primarydriver in a serious bribery case remains either the amount of the bribes or, morecommonly, the pecuniary gain to the corporation. Pecuniary gain to the corpora-tion is defined in the Commentary to the Sentencing Guidelines as “the additional,before-tax profit to the defendant resulting from the relevant conduct of theoffense.”76

The Sentencing Guidelines thus offer mitigated sanctions to corporations thatundertake certain measures in order to induce their adoption by corporations.77 Incontrast to the Antitrust Division,78 the Fraud Section has not promulgated anyleniency guidelines, leaving companies and their counsel to review DOJ and SECFCPA resolutions and often speculate about the ultimate monetary benefits ofvoluntary disclosure and corporate cooperation with the Fraud Section and SECFCPA unit.79

2. SEC Settlements

Settlements reached in many FCPA cases involve payments to not only theDOJ, but the SEC,80 though limitations on the SEC’s authority generally causethe SEC to seek penalties and disgorgement against parent company, publicissuers.81 These SEC penalties typically include: (i) a civil penalty; and (ii)disgorgement of ill-gotten gains (e.g., profits derived or losses avoided by the

71. See O’SULLIVAN, supra note 55, at 215 (quoting U.S.S.G. MANUAL § 8C4.1).72. Id. (quoting U.S.S.G. MANUAL § 8C4.3).73. Id. (quoting U.S.S.G. MANUAL § 8C4.5).74. Id. (quoting U.S.S.G. MANUAL § 8C4.9).75. 18 U.S.C. § 3571(d) (2006).76. U.S.S.G. MANUAL § 8A1.2 cmt. 3(h).77. See John S. Baker, Jr., Reforming Corporations Through Threats of Federal Prosecution, 89 CORNELL L.

REV. 310, 317 (2004).78. See infra Part II.B.79. See infra Part III.C.80. See Doty, supra note 18, at 1237.81. See id. at 1236 n.9.

2010] PROPOSAL FOR AN FCPA LENIENCY POLICY 165

misconduct), together with prejudgment interest. Signally, SEC disgorgementand civil fine settlements may approach the DOJ settlement criminal finefigure.82

Disgorgement to the SEC is a relatively new phenomenon in FCPA enforce-ment,83 the SEC having first insisted upon this remedy in a 2004 FCPAresolution.84 The amount of disgorged profits secured by the SEC, neverthe-less, has been significant.85 The legality of disgorgement of profits in the FCPAcontext has yet to be resolved in a published court decision.86 However, thestatutory authorization for obtaining disgorgement of profits in the FCPAcontext, even if based on SOX in addition to the FCPA itself, may bequestioned.87 The complexities in calculating the profits that are directlyattributable to bribery conduct caution against using disgorgement as a majorenforcement tool under the FCPA.88

C. Current DOJ and SEC General Charging Criteria

1. United States Attorneys’ Manual

The decision of federal prosecutors to charge an individual or a corporation isguided by the United States Attorneys’ Manual.89 Beginning in 1980, the DOJpublished Principles of Federal Prosecution to guide federal prosecutors incharging individuals.90 These principles, which are incorporated into the UnitedStates Attorneys’ Manual, list seven factors for determining whether a substantialfederal interest would be served by prosecution.91 Those factors have remainedthe general criteria for criminally charging individuals in federal court for thirtyyears.

In regards to the factors guiding the decision to charge corporations, in 1999,then Deputy Attorney General Eric H. Holder, Jr., issued a memorandum entitled

82. See, e.g., DOJ, Daimler Press Release, supra note 6; SEC v. UTStarcom, Inc., SEC Litigation Release No.21357 (2009); see also infra note 336.

83. See Weiss, supra note 38, at 486.84. See SEC v. ABB Ltd., No. 1:04-CV-01141 (D.D.C. 2004).85. See Weiss, supra note 38, at 486; see also infra note 336 (describing amounts disgorged by Titan Corp.,

Baker Hughes, Inc., Siemens AG, and Halliburton Co).86. See Doty, supra note 18, at 1237 n.13 (defining the issue as “[w]hether Congress intended the equitable

disgorgement remedy to subsume the FCPA’s express fining provisions”).87. See Weiss, supra note 38, at 496-499 (though not arguing that the disgorgement remedy is statutorily

inpermissible or undesirable per se).88. See id., at 509-511. This general uncertainty may be exacerbated by the rule that the SEC, in general, need

only show a reasonable approximation of the amount of profits to be disgorged. See id. at 510.89. See U.S. ATTORNEYS’ MANUAL § 9-27.120.90. DEP’T OF JUSTICE, PRINCIPLES OF FEDERAL PROSECUTION (1980).91. U.S. ATTORNEYS’ MANUAL § 9-27.230.

166 AMERICAN CRIMINAL LAW REVIEW [Vol. 47:153

“Federal Prosecution of Corporations.”92 After several iterations,93 in 2008, thecorporate charging policy became part of the United States Attorneys’ Manual.94

The nine general criteria that today guide all federal prosecutors in decidingwhether to charge corporations are:

1. the nature and seriousness of the offense, including the risk of harm to thepublic, and applicable policies and priorities, if any, governing the prosecutionof corporations for particular categories of crime;2. the pervasiveness of wrongdoing within the corporation, including thecomplicity in, or the condoning of, the wrongdoing by corporate management;3. the corporation’s history of similar misconduct, including prior criminal,civil, and regulatory enforcement actions against it;4. the corporation’s timely and voluntary disclosure of wrongdoing and itswillingness to cooperate in the investigation of its agents;5. the existence and effectiveness of the corporation’s pre-existing complianceprogram;6. the corporation’s remedial actions, including any efforts to implement aneffective corporate compliance program or to improve an existing one, toreplace responsible management, to discipline or terminate wrongdoers, to payrestitution, and to cooperate with the relevant government agencies;7. collateral consequences, including whether there is disproportionate harmto shareholders, pension holders, employees, and others not proven personallyculpable, as well as impact on the public arising from the prosecution;8. the adequacy of the prosecution of individuals responsible for the corpora-tion’s malfeasance; and9. the adequacy of remedies such as civil or regulatory enforcement actions.95

Because of the profound and harsh consequences arising from indictment, corpora-tions often seek to reach a resolution with the DOJ before charges are filed.96

2. SEC Enforcement Criteria

In 2001, the SEC issued a Section 21(a) report, commonly referred to as the

92. Memorandum from U.S. Deputy Attorney General Eric H. Holder, Jr., Federal Prosecution of Corpora-tions (June 16, 1999), available at http://www.justice.gov/criminal/fraud/documents/reports/1999/charging-corps.pdf.

93. See, e.g., Memorandum from U.S. Deputy Attorney General Larry D. Thompson, Principles of FederalProsecutionofBusinessOrganizations(Jan.20,2003),availableathttp://www.justice.gov/dag/cftf/corporate_guidelines.htm); Memorandum from U.S. Deputy Attorney General Paul J. McNulty, Principles of Federal Prosecution ofBusiness Organizations (Dec. 12, 2006) [hereinafter McNulty Memorandum], available at http://www.justice.gov/dag/speeches/2006/mcnulty_memo.pdf.

94. Memorandum from U.S. Deputy Attorney General Mark R. Filip, Principles of Federal Prosecution ofBusiness Organizations (Aug. 28, 2008), available at http://www.justice.gov/opa/documents/corp-charging-guidelines.pdf.

95. U.S. ATTORNEYS’ MANUAL § 9-28.300.96. See Baer, supra note 8, at 1062-63. This regime has been criticized as not being transparent or predictable.

See infra notes 379-80.

2010] PROPOSAL FOR AN FCPA LENIENCY POLICY 167

Seaboard Report, that outlined thirteen non-exhaustive criteria the SEC considersin deciding whether to bring an enforcement action against a corporation.97 Thosefactors are:

1. What is the nature of the misconduct involved? Did it result from inadvert-ence, honest mistake, simple negligence, reckless or deliberate indifference toindicia of wrongful conduct, willful misconduct or unadorned venality? Werethe company’s auditors misled?2. How did the misconduct arise? Is it the result of pressure placed onemployees to achieve specific results, or a tone of lawlessness set by those incontrol of the company? What compliance procedures were in place to preventthe misconduct now uncovered? Why did those procedures fail to stop orinhibit the wrongful conduct?3. Where in the organization did the misconduct occur? How high up in thechain of command was knowledge of, or participation in, the misconduct? Didsenior personnel participate in, or turn a blind eye toward, obvious indicia ofmisconduct? How systemic was the behavior? Is it symptomatic of the way theentity does business, or was it isolated?4. How long did the misconduct last? Was it a one-quarter, or one-time, event,or did it last several years? In the case of a public company, did the misconductoccur before the company went public? Did it facilitate the company’s abilityto go public?5. How much harm has the misconduct inflicted upon investors and othercorporate constituencies? Did the share price of the company’s stock dropsignificantly upon its discovery and disclosure?6. How was the misconduct detected and who uncovered it?7. How long after discovery of the misconduct did it take to implement aneffective response?8. What steps did the company take upon learning of the misconduct? Did thecompany immediately stop the misconduct? Are persons responsible for anymisconduct still with the company? If so, are they still in the same positions?Did the company promptly, completely and effectively disclose the existenceof the misconduct to the public, to regulators and to self-regulators? Did thecompany cooperate completely with appropriate regulatory and law enforce-ment bodies? Did the company identify what additional related misconduct islikely to have occurred? Did the company take steps to identify the extent ofdamage to investors and other corporate constituencies? Did the companyappropriately recompense those adversely affected by the conduct?9. What processes did the company follow to resolve many of these issues andferret out necessary information? Were the Audit Committee and the Board ofDirectors fully informed? If so, when?

97. See Report of Investigation Pursuant to Section 21(a) of the Securities Exchange Act of 1934, as amended,and Commission Statement on the Relationship of Cooperation to Agency Enforcement Decisions, Exchange ActRelease No. 44,969, Accounting and Auditing Enforcement Release No. 1,470 (Oct. 23, 2001), available athttp://www.sec.gov/litigation/investreport/34-44969.htm.

168 AMERICAN CRIMINAL LAW REVIEW [Vol. 47:153

10. Did the company commit to learn the truth, fully and expeditiously? Did itdo a thorough review of the nature, extent, origins and consequences of theconduct and related behavior? Did management, the Board or committeesconsisting solely of outside directors oversee the review? Did companyemployees or outside persons perform the review? If outside persons, had theydone other work for the company? Where the review was conducted by outsidecounsel, had management previously engaged such counsel? Were scopelimitations placed on the review? If so, what were they?11. Did the company promptly make available to our staff the results of itsreview and provide sufficient documentation reflecting its response to thesituation? Did the company identify possible violative conduct and evidencewith sufficient precision to facilitate prompt enforcement actions against thosewho violated the law? Did the company produce a thorough and probingwritten report detailing the findings of its review? Did the company voluntarilydisclose information our staff did not directly request and otherwise might nothave uncovered? Did the company ask its employees to cooperate with ourstaff and make all reasonable efforts to secure such cooperation?12. What assurances are there that the conduct is unlikely to recur? Did thecompany adopt and ensure enforcement of new and more effective internalcontrols and procedures designed to prevent a recurrence of the misconduct?Did the company provide our staff with sufficient information for it to evaluatethe company’s measures to correct the situation and ensure that the conductdoes not recur?13. Is the company the same company in which the misconduct occurred, orhas it changed through a merger or bankruptcy reorganization?98

These thirteen non-exhaustive criteria offer guidance on whether the SEC shouldbring an enforcement action, but do not provide specifics about what credit acharged corporation will receive for its investigation, disclosure, cooperation andremedial efforts. For this and other reasons, much uncertainty existed under theSeaboard factors as to the benefits arising from cooperating with the SEC.99

The SEC recently announced a series of measures aimed at increasing coopera-tion of corporations and individuals in SEC investigations and enforcementactions.100 Notably, to incentivize corporations and individuals to report violationsof the federal securities laws, the SEC’s Division of Enforcement is now empow-ered to use cooperation agreements, deferred prosecution agreements and non-

98. See id. (footnote omitted).99. See Ropes & Gray LLP, The New Era in SEC Enforcement: Fostering Cooperation (Feb. 12, 2010), at 2,

available at http://www.ropesgray.com/secenforcementfosteringcooperation (follow hyperlink at top of page forpdf version). (“Most important, it was unclear what credit the SEC actually gave for cooperation under theSeaboard factors. The Seaboard factors were barely mentioned in the Enforcement Manual in existence prior toJanuary 2010, and many practitioners doubted the SEC gave any real credit for cooperation.”).

100. See Press Release, SEC, SEC Announces Initiative to Encourage Individuals and Companies toCooperate and Assist in Investigations (Jan. 13, 2010), available at http://www.sec.gov/news/press/2010/2010-6.htm.

2010] PROPOSAL FOR AN FCPA LENIENCY POLICY 169

prosecution agreements that, previously, were not formally available in SECenforcement matters.101 The cooperation initiative also establishes a regime forindividuals similar to that provided for in the Seaboard Report in regard tocorporations.102 In addition, the 2010 SEC Enforcement Manual, though notsupplanting the Seaboard Report, highlighted four of its factors: (i) self-policingprior to the discovery of the misconduct; (ii) self-reporting of misconduct when itis discovered; (iii) remediation; and (iv) cooperation with law enforcement.103

Therefore, although it may be too soon to predict with certainty how thesedevelopments will play out in practice, corporations and their legal counsel will,without specific clarification, continue to be uncertain as to the benefits ofcooperating with the SEC in FCPA cases.

D. Prior FCPA Reform Proposals

In light of these uncertainties and shortcomings, this Article proposes a leniencypolicy for FCPA violations, specifically, those that involve bribery conduct.Promulgation of such a leniency policy by the Fraud Section would be a timelydevelopment: recently, a respected financial publication remarked critically that“[s]till, nobody in Washington is rethinking enhanced FCPA enforcement. There isno movement for different approaches, such as a corporate amnesty program orless severe punishment.”104

This Article’s proposed FCPA policy also shares the goals of, though differs inseveral material respects from, three additional, noteworthy, reform proposalsoffered by preeminent lawyers. First, James R. Doty, former General Counsel ofthe SEC, has advocated “for a new approach to administration of the FCPA, onethat would provide a measure of regulatory certainty to public companies regard-ing the elements of good faith compliance” in the form of a proposed “Reg.FCPA.”105 Modeled after precedent SEC regulation such as Regulation D andRules 144 and 144A, Reg. FCPA would establish a permissive filing regime,created through SEC rule-making, under which participating corporations wouldestablish, implement and attest to the reasonable discharge of obligations providedunder an FCPA Compliance Program drawn from, inter alia, the criteria for aneffective compliance and ethics program set forth in the Sentencing Guidelines.106

Participating corporations would make a public portion of a filing (“Part I”) thatdiscloses, inter alia, the corporation’s code of conduct, the implementation and

101. See id.102. See id.103. See SEC ENFORCEMENT MANUAL § 6.1.2, at 127 (2010) [hereinafter SEC ENFORCEMENT MANUAL],

available at http://www.sec.gov/divisions/enforce/enforcementmanual.pdf. Indeed, the 2010 SEC EnforcementManual refers SEC staff to the Seaboard Report “[f]or greater detail regarding the analytical framework used bythe Commission to evaluate cooperation by companies . . . .” See id., § 6.1.2, at 128.

104. Vardi, supra note 23, at 77.105. Doty, supra note 18, at 1233.106. See id. at 1244.

170 AMERICAN CRIMINAL LAW REVIEW [Vol. 47:153

communication of an FCPA Compliance Program, and related internal controlsand procedures for testing and monitoring that program’s effectiveness.107 Corpo-rations could also seek confidential treatment of a non-public portion of the filing(“Part II”), which would contain certain proprietary and confidential informationof the corporation.108 “[B]y making the filing, a registrant would benefit from aregulatory presumption of compliance.”109 Specifically, Reg. FCPA would alsoidentify the components of an FCPA Compliance Program that permit a corpora-tion to avail itself of a safe harbor.110 If a corporation met its burden to demonstratethat the safe-harbor requirements had been satisfied, then it “would be presumednot to have violated the statute”—a presumption that “could be rebutted by apreponderance of the evidence.”111

Drawing from the successes of the voluntary program that existed for foreignbribery in the 1970s, in a 2006 address, Judge Stanley Sporkin, a former Directorof Enforcement at and General Counsel of the SEC, proposed an “FCPA Immuni-zation-Inoculation Program”—a voluntary disclosure program that would grantlimited amnesty to corporations for FCPA violations.”112 Under that program, aparticipating corporation would “conduct a full and complete review of [its]compliance with the FCPA for the previous 3 years,” such review to be accom-plished by a law firm and a major or specialized forensic accounting firm.113

Moreover, the corporation would agree to conduct a similar review annually for atleast five years.114 It then would report the results of this review by its legalcounsel and accounting firm to its stakeholders, the SEC and the public.115 Thecorporation would remediate any violations and establish controls to prevent therecurrence of any violations discovered in the review; in particular, the corporationwould need to establish the position of “FCPA compliance officer”—an officerwho would focus exclusively on FCPA compliance by the corporation.116 If aparticipating corporation satisfied these conditions, then it would receive from theSEC and DOJ “qualified assurances that no actions would be brought for violationsexposed by the review.”117 This limited amnesty, however, would not be available

107. See id.108. See id. at 1246-47.109. Id. at 1234.110. See id. at 1245.111. Id. Mr. Doty concludes that the benefits of Reg. FCPA include, among other things, guidance to registrants

on the establishment of anti-bribery policies, more generalized adoption of best practices, improved complianceby corporations, and greater transparency. See id. at 1234, 1246, 1248-54.

112. See Judge Sporkin Speech, supra note 28, at 7-8.113. Id. at 7.114. See id. at 8.115. See id. at 7.116. See id. at 7-8.117. Id. at 8.

2010] PROPOSAL FOR AN FCPA LENIENCY POLICY 171

to and exculpate flagrant or egregious FCPA violations.118

Finally, in a June 2010 speech in Washington, D.C., former Deputy AttorneyGeneral George J. Terwilliger became the third preeminent lawyer to proposesome form of an FCPA leniency policy.119 Noting the uncertain benefits arisingfrom self-reporting of FCPA violations, and the success of the Antitrust Division’sCorporate Leniency Program, Mr. Terwilliger outlined in his prepared remarks anamnesty policy “whereby there would be a presumption against criminal prosecu-tion or disposition for organizations that voluntarily disclose wrongdoing andthereafter cooperate with the government by, for example, providing the results ofan itnernal investigation and/or cooperating with additional government investiga-tion.”120 In addition, Mr. Terwilliger observed that such a policy “would still haveto provide forbearance from some aspects of non-criminal monetary penalties forviolations voluntarily disclosed,” which could be achieved through a complemen-tary “formula to determine the fine or financial punishment, or a range thereof, thatshould be imposed for violations.”121 While his “skeletal outline”122 leniencyprogram did not propose implementing statutory language or specific discounts,123

Mr. Terwilliger captures the sentiment of many corporations and FCPA counselthat “[t]he opportunity to receive ‘meaningful credit’ is too much promise and toolittle policy.”124

II. A BRIEF OVERVIEW OF THE SHERMAN ACT, SANCTIONS IMPOSED FOR

VIOLATIONS OF THE SHERMAN ACT, AND THE ANTITRUST DIVISION’SSUCCESSFUL CORPORATE LENIENCY PROGRAM

A. The Sherman Act: Criminal Penalties

Enacted in 1890, Section 1 of the Sherman Act prohibits certain forms ofanti-competitive behavior, including price fixing, bid rigging and market alloca-

118. See id. Judge Sporkin observes that his “Immunization-Inoculation” regime ultimately would incentivizecorporations to establish and implement rigorous ethical and compliance standards, and decrease the number ofcases for and investigative efforts undertaken by law enforcement. Id.

119. George J. Terwilliger III, Prepared Remarks for the Marcus Evans FCPA & Anti-Corruption ComplianceConference: Proposed Change in DOJ Policy: Presumption of No Criminal Disposition for Voluntary Disclosure(June 23, 2010) (on file with the American Criminal Law Review).

120. Id. at 2.121. Id. at 3.122. Id.123. Previously, Alexandros Zervos proposed for small scale bribery a graduated penalty scheme that would

allow companies to investigate and report such violations under a safe harbor which would shield participatingcorporations from prosecution. See Alexandros Zervos, Amending the Foreign Corrupt Practices Act: Repealingthe Exemption for “Routine Government Action” Payments, 25 PENN ST. INT’L L. REV. 251, 286 (2006).

124. Terwilliger, supra note 119, at 2. Mr. Terwilliger notes that the benefits of the proposed leniency policy toinclude, among others: (i) clearly establishing that there is a benefit to self-reporting FCPA violations; (ii)promoting investigation and self-reporting of FCPA violations by corporations; and (iii) counteracting thenegative consequences from self-reporting. See id. at 2.

172 AMERICAN CRIMINAL LAW REVIEW [Vol. 47:153

tion.125 For nearly a century, violations of the Sherman Act were criminallypunishable by only misdemeanor penalties.126 In 1974, Congress amended theSherman Act to make such misconduct a felony.127 The maximum criminal penaltyfor violations of the Sherman Act has been adjusted upwards from time to time; in2004, Congress increased the maximum criminal penalty for violations of Section1 of the Sherman Act from $10 million to $100 million.128 The maximum criminalpenalty for corporations for violations of Section 1 of the Sherman Act currentlyincludes, among other penalties, a fine of $100 million, or twice the gross gain ortwice the gross loss resulting from the offense, whichever is the greater.129

The amount of criminal fines collected by the Antitrust Division has expandeddramatically. In 1997, the Antitrust Division obtained criminal fines totaling $205million, which then was 500% higher than that which had been collected in anyprevious given year.130 Since then, the division has collected fines exceeding $5billion,131 including numerous corporate fines each exceeding $10 million.132 Thisincrease in fines preceded that experienced by the Fraud Section by a half-decadeor more,133 and is likely the result of at least five factors: (1) promulgation in 1991of the Sentencing Guidelines;134 (2) the issuance of Antitrust Division leniencypolicies for corporations (the Corporate Leniency Policy)135 that have beencontinuously refined and elucidated in position papers authored and speeches

125. 15 U.S.C. § 1 (2006).126. Sherman Act, ch. 647, §§ 1-2, 26 Stat. 209 (1890).127. See Antitrust Procedures and Penalties Act, Pub. L. No. 93-528, 88 Stat. 1706, 1708 (1974).128. See Antitrust Criminal Penalty Enhancement and Reform Act of 2004, Pub. L. No. 108-237, 118 Stat.

661, 668 (2004); see also Kobayashi, supra note 19, at 717 (listing increases in the maximum criminal penalty forcorporations from 1890 until 2001, at which time it equaled $10 million).

129. See 15 U.S.C. § 1 (2006); 18 U.S.C. § 3571(d) (2006).130. See Scott D. Hammond, Deputy Assistant Attorney Gen. for Criminal Enforcement, DOJ Antitrust Div.,

Recent Developments, Trends and Milestones in the Antitrust Division’s Criminal Enforcement Program,Presented at the 56th Annual Spring meeting of the ABA Section of Antitrust Law (Mar. 26, 2008) [hereinafterHammond, Recent Developments], at 11, available at http://www.justice.gov/atr/public/speeches/232716.pdf.

131. See Scott D. Hammond, Deputy Assistant Attorney Gen. for Criminal Enforcement, DOJ Antitrust Div.,The Evolution of Criminal Antitrust Enforcement Over the Last Two Decades, Presented at the 24th AnnualNational Institute on White Collar Crime (Feb. 25, 2010) [hereinafter Hammond, Evolution of Criminal AntitrustEnforcement], at 5-6, available at http://www.justice.gov/atr/public/speeches/255515.pdf.

132. See DOJ Antitrust Div., Sherman Act Violations Yielding a Corporate Fine of $10 Million or More,available at http://www.justice.gov/atr/public/criminal/sherman10.pdf.

133. See id.134. See Kobayashi, supra note 19, at 723-28.135. The Corporate Leniency Policy may be found at http://www.justice.gov/atr/public/guidelines/0091.pdf.

In 1994, the Antitrust Division promulgated an Individual Leniency Policy, which is available at www.justice.gov/atr/public/criminal/sherman10.htm. Though it addresses the leniency afforded to a corporate applicant’s directors,officers, and employees under the Corporate Leniency Program, this Article does not examine the IndividualLeniency Policy.

Former Deputy Assistant General Gary R. Spratling is widely recognized as the architect of the modernAntitrust Division corporate and individual leniency programs.

2010] PROPOSAL FOR AN FCPA LENIENCY POLICY 173

given by the Antitrust Division and its senior officials for the past 15 years;136 (3)informal and formal exchanges of information between U.S. and foreign competi-tion authorities pursuant to Mutual Lateral Assistance Treaties and other agree-ments;137 (4) increased focus by the DOJ on enforcement against large, interna-tional cartels that affect a more substantial amount of commerce, with closercooperation between U.S. and foreign competition authorities;138 and (5) theaforedescribed increases in the maximum criminal fine for corporations, and theintroduction of potential alternative fines.139

B. The Antitrust Division’s Corporate Leniency Program

The DOJ has established and promoted leniency policies to incentivize corpora-tions and individuals to report antitrust violations to and cooperate with lawenforcement. The Antitrust Division first implemented a leniency program in1978.140 In 1993, the Division significantly revised and greatly improved theleniency program with the issuance of the Corporate Leniency Program.141 Underthe Division’s Corporate Leniency Program, “a corporation can avoid criminalconviction and fines . . . by being the first to confess participation in a criminalantitrust violation, fully cooperating with the Antitrust Division and meeting other

136. See, e.g., Hammond, Evolution of Criminal Antitrust Enforcement, supra note 131; Scott D. Hammond,Deputy Assistant Attorney Gen. for Criminal Enforcement, DOJ Antitrust Div., & Belinda A. Barnett, SeniorCounsel, DOJ Antitrust Div., Frequently Asked Questions regarding the Antitrust Division’s Leniency Program’sModel Leniency Letters, Presented at the 24th Annual National Institute on White Collar Crime (Nov. 19, 2008),available at http://www.justice.gov/atr/public/criminal/239583.pdf; Hammond, Recent Developments, supranote 130; Scott D. Hammond, Deputy Assistant Attorney Gen. for Criminal Enforcement, DOJ Antitrust Div.,Measuring the Value of Second-In Cooperation in Corporate Plea Negotiations, Address at the 54th Annual ABASection of Antitrust Law Spring Meeting (Mar. 29, 2006) [hereinafter Hammond, Second-In Cooperation],available at http://www.justice.gov/atr/public/speeches/215514.pdf; Scott D. Hammond, Deputy Assistant Attor-ney Gen. for Criminal Enforcement, DOJ Antitrust Div., Charting New Waters in International Cartel Prosecu-tions, Presented at the 20th Annual National Institute on White Collar Crime (Mar. 2, 2006) [hereinafterHammond, Charting New Waters], available at http://www.justice.gov/atr/public/speeches/214861.pdf; Scott D.Hammond, Director of Criminal Enforcement, DOJ Antitrust Division, Cornerstones of an Effective LeniencyProgram, Presented at the ICN Workshop on Leniency Programs (Nov. 22-23, 2004) [hereinafter Hammond,Cornerstones], available at http://www.justice.gov/atr/public/speeches/206611.pdf; Gary R. Spratling & D.Jarrett Arp, The International Leniency Revolution: The Transformation of International Cartel EnforcementDuring the First Ten Years of the United States’ 1993 Corporate Amnesty/Immunity Policy, Presented at theAmerican Bar Association Section of Antitrust Law 2003 Annual Meeting (Aug. 12, 2003), at 4-5 nn.16 & 19,available at http://media.gibsondunn.com/fstore/documents/pubs/Sprating-Arp%20ABA2003_Paper.pdf.