Embed Size (px)

Citation preview

InvestorMetrolina

JULY 2009VOLUME 12, ISSUE 7

Metrolina REIA Winner of the 2009 National REIA Award of Excellence www.MetrolinaREIA.org

In This IssueHow to Keep a Positive Perspective in a Negative Market . . . . . . . . 4

Summer Reading . . . . . . . . . . . 6

TOP TEN “Deductions for Landlords” . . . . . . . . . . . . 10

7 Ways to Flip a Property . . . . 11

Invest in Your Own Debts - A 23% Return . . . . . . . . . . . . . 12

How to Create Your Own Personal Investment Criteria . . . . . . . . . . . . . . . . . 13

PHP Saturday . . . . . . . . . . . . 14

Events Calendar & Sub-Group Meeting Info . . . . . 15

Be sure to wear your REIA name

badge to the main meeting.

Starting in May all members

not wearing their badge will be

charged $5. The money collected

will be donated to charity.

Join Us As We Celebrate Winning the National REIA

NATIONAL AWARD OF EXCELLENCE!

The Main REIA Meeting Will Feature...

PHP Housing

CertificationGraduation!

Award of

Excellence

Celebration

Expert Q & A Panel

Thursday, July 16Doors open at 5:30

Networking & RefreshmentsMeeting Starts at 6:30pm

Hilton HotelCharlotte Executive Park

5624 Westpark Dr.I-77 & Tyvola Rd.

Bring a GuestMembers bring this cover and receive FREE admissionfor one guest ($15 value)Valid only for the July 16, 2009Main Meeting.

2 www.MetrolinaREIA.org

Metrolina Investoris a Publication of

Metrolina Real Estate Investors Association

122 W. Woodlawn Rd., Suite D-101Charlotte, NC 28217

(704) 523-1570www.MetrolinaREIA.org

Executive DirectorJC Underwood

President: Tom Latimer [email protected]

Vice President: Tim Spyridon [email protected]

Secretary: Sherry Fredenberg [email protected]

Treasurer: Ki Shin [email protected]

Board MembersDonna BordeauxCherrathee HagerLeon HumphreyTyler McCracken

Jay ParkerDoug DeShieldsKimberly Shelton

Metrolina REIA Board is run by volunteers who are committed to the mission of the Metrolina REIA. Elections are held annually each November.

Newsletter Design and ProductionRaynell Swanson

The mission of the Metrolina Real Estate Investors Association (Metrolina REIA) is to actively promote wealth building with real estate through education, mentoring and networking. The Metrolina REIA is dedicated to helping it’s membership excel in the real estate investment arena in Charlotte, NC and the surrounding Metrolina area.

The Metrolina Real Estate Investors Association, Inc. is a professional organization dedicated to providing networking, and education programs for real estate investors.

The information presented at our meetings, on our website, and in our publications should not be construed as legal or tax advice. Legal advice should be obtained from an attorney. Tax advice should be sought from tax professionals.

The Metrolina REIA exists to expose its members to ideas that may be beneficial as they plan their business. We do not render legal, tax, or investment advice except in educational discussions and disclaim all liability for the actions or inactions taken or not taken as a result of communications from and/or to its members, officers, directors, and any employee.

The opinions expressed by the speakers and published articles are not necessarily those of Metrolina REIA.

Each individual should consult their own counsel, accountant, and other advisors as to legal, tax, investment, and economic matters concerning

real estate and other investments.

REIACharlotte, NC

Declaration of Metrolina REIA

AD SIZE

1/8 page

1/4 page

1/2 page

Full Page

1 Month

$45.00

$57.00

$95.00

$185.00

3 Months

$115.00

$148

$245.00

$483.00

1 Year

$300.00

$516.00

$840.00

$1680.00

InvestorMetrolina

For more information about vendor membership, advertising and reserving ad space contact: Deanna Valeo,

Vendor membership Chairperson at 704-366-7711 office •

704-488-1421 mobile • [email protected]

AdvE

rtis

inG

rAtE

s

Metrolina REIA Winner of the 2009 National REIA Award of Excellence 3

ARROW DISPOSAL Inc.Serving the Central North Carolina Area Since 2000

SAME DAY SERVICEDelivery or pickup in most of the greater

Charlotte and surrounding areas.

DUMPSTERS10, 15, & 20 yard cans available — Open tops, Roll-offs

Containers with walk-in gate for easy accessGreat for Do-It Yourselfers • Large or Small Remodels

Garage / Attic / House / Yard Clean-outs • Roof tear-offs

OWNER ANSWERS ALL CALLS

7 0 4 . 4 6 7 . 7 7 4 4w w w. A r r o w D i s p o s a l . c o m

4 www.MetrolinaREIA.org

Suppor t Our Vendor Members! AccountingBordeaux & Bordeaux, Certified Public AccountantsChadwick Bordeaux, CPADonna Bordeaux, CPAPhone: 704-752-9845www.yourcpapartners.com/ Smith and Shin, Certified Public Accountants, LLCPhone: 864-322-8995Brandon Smith, CPA, MBAKi Shin, CPAwww.smithandshin.net

concrete ServiceSA&W Concrete Services, Inc.Phone: 704-843-4587Cary Williamswww.awconcrete.com

contrActorSLowery ConstructionPhone: 704-364-3234Chuck Lowery, Jr.

contrActorS con’tMr. Sandless - CharlotteAshley Allen Phone: 704-231-5311www.mrsandless.com DiSpoSAl ServiceSArrow Disposal, Inc.Phone: 704-467-7744Jerry Frakeswww.arrowdisposal.com eDucAtionLarry GoinsPhone: (803) 831-0056Larry Goinswww.larrygoins.com www.larrygoinsfreeoffer.com

National REIAPhone: 859-261-3335Rebecca McLeanwww.nationalreia.com

HArD Money lenDerSEquity Development Corp.Phone: 757-460-9096Milton Kalligaridis704-650-1072www.equitydevelopmentcorp.com

InvestwellPhone: 888-497-3239Jennifer Castaldiwww.investwell.com

South Street FundingPhone: 704-987-9393Bill Worsleywww.southstreetfunding.com

inforMAtion ServiceSCourthouse Retrieval SystemRon Ayers 704-526-9599 www.crsdata.com

inSurAnceLarry Hale InsurancePhone: 704-847-4500Larry Halewww.larryhaleinsurance.com

MortgAge lenDerSCunningham & Company/ The Valeo-Croy TeamPhone: 704 488-1421Deanna Valeo and Todd Croywww.valeocroyteam.com

property MAnAgeMentCLT Property ManagementPhone: 704-529-RENT (7368)Allon Thompson, GRI, PHPCharles Lamere, Broker

Materna Gray704-526-5966Rami Alkhatib www.maternagray.com

reAl eStAte AgentS/BroKerSElite Buyer AgentsScott Patterson704-334-2100www.elitebuyeragents.com

Genesis Realty Company704-933-5000Gewn and John Chubirko

QuickMLS Realty, LLC803-746-4841Carmen Cunha

reSiDentiAl & coMMericAl cleAningMarr Clean Corporation704-556-7840Maria Ramirez

Self-DirecteD irAsEntrust Carolinas, LLC(828) 257-4949Sean McKay

“Whether you think you can or you think you can’t, you are right” – Henry Ford

I am sure you’ve heard the expression, “Attitude is everything.” This is very true. Right now, it’s simply your attitude and mentality that will give you the edge over others who are trying to invest in this highly violatile market. You’ve un-doubtedly heard the importance of think-ing positive and having the right attitude. Most people are intelligent enough to know that this statement is true. Some people reading this will argue that a posi-tive attitude doesn’t always work. Well, maybe not, but I know one thing for sure - negative thinking and a negative atti-tude NEVER works! So your only choice and your only chance for success in this market are to pick the positive things in life and maintain a positive attitude at all times.

I once read a fortune cookie that said, “An optimist is someone who tells you to cheer up when things are going his way”. I know that if you are reading this article, times may be difficult and you need seri-

ous answers to your burning questions such as, “How I profit in a slow market”? There are many answers to this ques-tion, but first I need to impart to you some relative perspective.

A History Lesson on Real Estate Cycles

About every ten to twelve years, as an average, real estate values tend to dou-ble in most major metropolitan areas. For example, in the 1920’s, the origi-nal colonial homes sold for just under $2,500 in Long Island, New York. Since then, real estate prices have doubled al-most eight times over the last 80 years. That averages out to a 100% increase approximately every ten years. An inter-esting note to this is that about every ten to twelve years, real estate values must correct before they enter their next “doubling cycle”.

It’s Not a Matter of If, It’s a Matter of When

The evolutionary process is three steps forward and one step backwards.

How to Keep a Positive Perspective in a Negative Market

For example, imagine a 100% increase occurring in three steps of one-third parts each. The last market cycle of the 1980’s was one in which real estate val-ues doubled, followed by a correction of the early 1990’s, which equated to a 20-30% decrease over a three to five year period. This cycle was then followed by the post-millennium cycle boom of 100% from the last high point of the previous cycle. We are now in the naturally-occur-ring phase of a correction in the cycle. This essential and beneficial adjustment gives the market pause to reflect and re-gather momentum and strength for the next doubling cycle. This has occurred time and time again because the long-term demand for housing is growing an exponential rate based on population growth to almost double in the United States by 2050. This will continue to drive prices higher as it has for the last 100 years.

Since we now know based on history that nearly all real estate prices will

continued on page 10

Metrolina REIA Winner of the 2009 National REIA Award of Excellence 5

6 www.MetrolinaREIA.org

After the Fall: Opportunities and Strategies for Real Estate Invest-ing in the Coming Decade by Steve BergsmanAmazon Rating - 5 stars

The subprime mortgage melt-down and subsequent credit crisis has not only destroyed investor wealth, but altered the landscape of real estate investing. While some of yesterday’s most favored strategies will not work going forward, today’s savvy real estate investor can still find great oppor-

tunities for growth and profits—if they understand how recent events could shape this industry over the next few years, and into the coming decade.

In After the Fall, real estate expert Steve Bergsman offers a detailed look at the state of various market sectors—including commercial, residential, and leisure real estate—and provides direction as to where they are headed, so you can make the right decisions on property investments during the coming years. According to Bergsman, the next decade will produce multiple investment currents. This reliable resource will help you find the right current and stay the course for a long, profitable ride. By separating the asset classes that will remain stable from those that will continue to lose value going forward, Bergsman provides much-needed guidance on the changing real estate marketplace.

Divided into five comprehensive parts, and filled with in-terviews of experienced professionals in this fast-moving field, After the Fall puts numerous individual asset classes in perspective—from office and retail to single-family homes and condominiums—and touches upon “megatrends” such as the green revolution and infill development that will be a big part of this industry’s future.

Focusing on the forces that have affected the market, Bergs-man skillfully addresses individual real estate sectors based on historical paths, movement of data fundamentals, market analysis, and collective opinion. With this information in hand, he takes the time to answer essential questions about each sector, including: When might they finally reach the bottom? How long will the climb back take? When will the next peak occur? And which asset classes won’t bounce back?

Recent developments have hurt many real estate investors, but they have also opened the door to potentially profitable new opportunities down the road. Filled with in-depth insights and expert advice, After the Fall offers effective strategies for taking advantage of this situation and making the most of your time in such a dynamic market.

About the AuthorSteve Bergsman is a real estate, financial, and travel writer with more than twenty years’ experience and visitations to 120 coun-tries. His news stories and travel articles have been published in more than 100 publications around the world, and he has appeared on local and national radio and television. Bergsman is also the author of three previous real estate books, Maverick Real Estate Financing, Maverick Real Estate Investing, and Pass-port to Exotic Real Estate, all published by Wiley.

What Every Real Estate Investor Needs to Know About Cash Flow... And 36 Other Key Financial Mea-suresby Frank GallinelliFormulas that make the difference between making profits and losing equityAmazon Rating: 4.6 stars

The only way to win the real estate investing game is by master-ing the numbers. This revised and updated edition of the popular refer-ence shows how to target the best

investments in the present market. It answers all your real estate questions, and provides new discussions of capital accumulation and internal rate of return. This book’s basic formulas will help you measure critical aspects of real estate investments, including:

* Discounted Cash Flow * Net Present Value * Capitalization Rate * Cash-on-Cash Return * Net Operating Income * Internal Rate of Return * Profitability Index * Return on Equity

From the AuthorCan a book filled with numbers possibly be exciting? If you’re

truly interested in real estate investing then you must first realize that investing in income properties is all about the numbers. It’s about discounted cash flow and rates of return and net operating income and cap rates. If you understand how these and other key concepts work, then you’re on your way to success – and that’s exciting.

I also believe you’ll find the presentation of this material entertaining. I sought to write this in a way that would make it accessible to beginners and professionals alike.

I present more than three dozen key concepts and calcula-tions. The book is peppered with “Rules of Thumb” that you can use as benchmarks when you evaluate potential investment prop-erties. I also provide numerous examples and sample problems that you can use to check your understanding. As you progress you’ll learn how to read a property’s vital signs and how to put financial concepts to work for successful investing in real estate.

As important as these financial measures are, some can be tedious to perform manually. For those I show you how to use simple spreadsheet models to accomplish those tasks. I also provide you with a link to a special website we created where readers of the book can download many of these models as well as other valuable tools.

I hope that you’ll find many good ideas here and that you’ll use what you learn to help you make solid investment choices.

Summer Reading

Metrolina REIA Winner of the 2009 National REIA Award of Excellence 7

Your hometown hard money lender

HARD MONEY LOANS

100% FINANCING AVAILABLE

For Investment Property Purchase and Rehab

704-987-9393www.southstreetfunding .com

8 www.MetrolinaREIA.org

No landlord would pay more than nec-essary for utilities or other operating expenses for a rental property. But, ev-ery year, millions of landlords pay more taxes on their rental income than they have to. Why? Because they fail to take advantage of all the tax deductions avail-able for owners of rental property.

Rental real estate provides more tax benefits than almost any other invest-ment. Often, these benefits make the difference between losing money and earning a profit on a rental property. But tax deductions are worthless if you don’t take advantage of them. Here are the top ten tax deductions for owners of small residential rental property.

1. Interest. Interest is often a land-lord’s single biggest deductible expense. Common examples of interest that land-lords can deduct include mortgage inter-est payments on loans used to acquire or improve rental property and interest on credit cards for goods or services used in a rental activity.

2. Depreciation. The actual cost of a house, apartment building, or other rental property is not fully deductible in the year in which you pay for it. Instead, landlords get back the cost of real es-tate through depreciation. This involves deducting a portion of the cost of the property over several years. Residential rental property must be depreciated over 27.5 years.

3. Repairs. The cost of repairs to rental property (provided the repairs are ordinary, necessary, and reasonable in amount) are fully deductible in the year in which they are incurred. Good examples of deductible repairs include repainting, fixing gutters or floors, fixing leaks, plas-tering, and replacing broken windows.

4. Local travel. Landlords are entitled to a tax deduction whenever they drive anywhere for their rental activity. For example, when you drive to your rental building to deal with a tenant complaint or go to the hardware store to purchase a part for a repair, you can deduct your travel expenses. If you drive a car, SUV, van, pickup, or panel truck for your rental activity (as most landlords do), you have

two options for deducting your vehicle ex-penses: You can use the standard mile-age rate (40.5 cents per mile in 2005), or you can deduct your actual expenses (gasoline, upkeep, repairs).

5. Long distance travel. If you travel overnight for your rental activity, you can deduct your air fare, hotel bills, meals, and other expenses. If you plan your trip carefully, you can even mix landlord business with pleasure and still take a deduction. However, IRS auditors closely scrutinize deductions for overnight travel, and many taxpayers get caught claiming these deductions without proper records to back them up. To stay within the law (and avoid unwanted attention from the IRS), you need to properly document your long distance travel expenses.

6. Home office. Provided they meet certain minimal requirements, landlords may deduct their home office expenses from their taxable income. This deduc-tion applies not only to space devoted to office work, but also to a workshop or any other home workspace you use for your rental business. This is true wheth-er you own your home or apartment or are a renter.

7. Employees and independent con-tractors. Whenever you hire anyone to perform services for your rental activity, you can deduct their wages as a rental business expense. This is so whether the worker is an employee (for example, a resident manager) or an independent contractor (for example, a repair per-son).

8. Casualty and theft losses. If your rental property is damaged or destroyed from a sudden event like a fire or flood, you may be able to obtain a tax deduction for all or part of your loss. These types of losses are called “casualty” losses. You usually won’t be able to deduct the entire cost of property damaged or destroyed by a casualty. How much you may deduct depends on how much of your property was destroyed and whether the loss was covered by insurance.

9. Insurance. You can deduct the pre-miums you pay for almost any insurance for your rental activity. This includes

TOP TEN “Deductions for Landlords”fire, theft, and flood insurance for rental property, as well as landlord liability in-surance. And if you have employees, you can deduct the cost of their health and workers’ compensation insurance.

10. Legal and professional services. Finally, you can deduct fees that you pay to attorneys, accountants, property man-agement companies, real estate invest-ment advisors, and other professionals. You can deduct these fees as operating expenses as long as the fees are paid for work related to your rental activity.

Did You Know?

Did you know that:

* Landlords can greatly increase the depreciation deductions they receive the first few years they own rental property by using “segmented” depreciation.

* Careful planning can permit you to deduct, in a single year, the cost of im-provements to rental property that you would otherwise have to deduct over 27.5 years.

* You can rent out a vacation home tax-free, in some cases.

* Most small landlords can deduct up to $25,000 in rental property losses each year.

* A special tax rule permits some landlords to deduct 100% of their rental property losses every year, no matter how much.

* People who rent property to their family or friends can lose virtually all of their tax deductions.

If you didn’t know one or more of these facts, you could be paying far more tax than you need to.

The information provided is not in-tended to be legal, tax or financial ad-vice. We hope you find this information useful, but we cannot guarantee that it is accurate, up-to-date or appropriate for your situation. You should consult with a qualified attorney or financial advisor to understand how the law applies to your particular circumstances or for financial information specific to your personal or business situation.

Metrolina REIA Winner of the 2009 National REIA Award of Excellence 9

• Full Service Property Management & much more! • Competitive Rates • Residential & Commercial

Contact us today for details!

CLT PROPERTYM ANAGEMEN T

704-529-RENT (7368)[email protected]

122 W Woodlawn Rd., Ste. D108 • Charlotte, NC 28217

10 www.MetrolinaREIA.org

positive perspective continued from page 4

double again, it’s not a matter of if, it’s a matter of when your existing houses will sell. Sharing these facts with your pro-spective buyers will put them in the right frame of mind to buy now versus next year if they plan on staying in the home more than five years. If a buyer is apprehensive about being the right time to invest, ask him if he’d like to buy his parent’s home for the price they paid for it – the answer will be obvi-ously “yes”.

Maintain a Positive Attitude Assuming a Negative Result

In “Winning Through Intimidation” author Robert Ringer talks of the importance of maintaining a positive attitude through the assumption of a negative result. In other words, Ringer suggests that you be prepared for the worst case scenario while at the same time putting your best foot forward to get the best possible result. This will take the mental pressure off of you and allow you to focus on getting the job done. This approach, I believe, allows you to be positive and realistic in your mental assessment buying and selling houses.

If it Bleeds, it Leads

There’s an old expression in the media business, “If it bleeds, it leads.” In other words, the media loves to cover neg-ative news more than positive because it sells better. When the real estate market is in turmoil, the media loves to run these negative headlines to keep reminding people how bad things are. When buyers hear the bad news, it affects demand because the negative news drives fear, which makes buyers worry about whether the time is right to buy a home.

Is the media simply reporting the news or does the media actually affect the news in this regard? The answer is obvi-ously both. The media reporting negative news alone can’t shape a real estate market. However, since perception is of-ten reality, when buyers are spooked, they may shy away from buying. This affects lenders, builders, real estate agents and other professionals who rely on the real estate business for their income. It becomes almost a self-fulfilling prophecy be-cause things get worse and the media again reminds us how bad things are.

But, are things really as bad as the media reports? At the time of this article (October 2008) the numbers certainly do reflect falling home prices and rising foreclosures. When you hear that foreclosures have doubled or even tripled in a par-ticular area, this may sound catastrophic at first until you real-ize that the vast majority of homes (97-99%, depending on the local market) are NOT in foreclosure. Despite the doom and gloom, there’s always a buyer for a well-kept home offered at the right price and terms. In short, don’t read the paper if you want to keep a positive attitude and sell your homes fast!

Ready Fire, Aim, Fire

Well done is better than well said – you have to take a whole lot of action to get your houses sold in s slow market. In a good real estate market, people can sell a house fast, so when things slow down, they figure, “Oh well, there’s nothing I can do.” Nothing could be further from the truth. Not only is there something you can do, but there’s a lot you MUST do to get

your house sold. However, it’s not just about working hard, it’s about working SMART. You need to do things in the right order and in the right way to get the proper results.

However, don’t focus too much on perfection before you take action. You’re probably familiar with the phenomenon of the “C” student who outperforms the “A” student in real life. This is because the “C” student is often satisfied with doing a mediocre job at something, but just getting it done. The “A” student mentality often leads to paralysis of analysis and inaction. In other words, the bottom line is getting your house exposed to as many buyers as possible, not necessarily get-ting it done perfectly. For example, many sellers want to show their house only when it’s convenient for them and the house is in perfect shape to be shown, instead of when a buyer is ready. While showing a house in its best condition is a priority, it doesn’t make sense to put off a ready, willing and able buyer for too long.

Fear

Many people reading this are prone to inaction because of fear of doing it incorrectly. Remember, it’s not a matter of doing it perfectly, but putting forth your best effort. As I dis-cussed earlier, a lot of effort at a “C” level beats doing less things at an “A” level.

Lack of knowledge certainly makes it difficult to sell a house fast in a slow market, and in fact is probably the single biggest drawback for the average person. Most people only have the opportunity to sell a few houses in their lifetime and often rely on professionals to do the work. Thus, the average home seller does not have enough practice to get really good at the job. In fact, most real estate agents who sell houses for a liv-ing are hardly good at it. The top 5% of agents in any market do the vast majority of the business.

Taking the time to learn what to do is a very important part of the success in selling a house. In the classic book “Think & Grow Rich”, Napoleon Hill writes about the importance of learning the right things. He distinguishes between general knowledge and specialized knowledge. Certainly, there’s a lot of general real estate knowledge in bookstores and floating around the Internet, but this book is unique because it of-fers the very specialized knowledge of how to sell a house … QUICKLY! Our experience in selling thousands of homes will reveal the very specialized knowledge you’ll need to get your house sold fast and at the highest price you can get for your market.

Excerpt from William Bronchick’s New Book

How to Sell a House Fast in a Slow Real Estate Market: A 30-Day Plan for Motivated Sellers (Paperback)by William Bronchick

Metrolina REIA Winner of the 2009 National REIA Award of Excellence 11

Flip Strategy #1: Buy, Fix and Flip

Let’s start with the most common form - the good, old “fix ‘n flip”. This process involves buying a property that needs work, fixing it up, then selling on the “retail” market, that is, to a per-son who will live in the property. This method is tried and true, and works very well. You can easily make $15 - $50k on one deal, depending on your market and how good you are at finding bargains.

The danger in fix and flips is either paying too much or underestimating re-pairs. Be very conservative in your fix-up costs and length of time it may take to resell. Also, make sure you include in your analysis the cost of paying a real estate agent to sell the property.

Flip Strategy #2: Buy, Refi & Lease/Option

Rather than sell the fixed up property for all cash, sell for terms. Once you have completed the rehab, refinance the property at its new appraised val-ue. If you did the math correctly, you should have little or no money in the deal. Sell the property on a lease with option to buy. The rent payment from your tenant/buyer should cover your mortgage payment (if not, consider an interest-only or adjustable rate loan that is fixed for 3 years). When your tenant exercises his option to pur-chase, you reap a larger profit, since you don’t have to pay a broker’s fee. If the tenant exercises his option after 12 months, you benefit from a lower capital gains tax rate.

Flip Strategy #3: Buy & Flip “As Is”

Don’t like to do fix-up work? Consider selling the property “as is” as a light fixer upper. If the local real estate mar-ket is hot, you should be able to sell the property in poor condition just a little below market. This is especially the case with houses in “transitioning” neighborhoods. Make sure, of course, that you acquire the property suffi-ciently cheap enough that you can sell it below market quickly and still profit.

Flip Strategy #4: Wholesale

Strategy #1, the fix and flip, is very popular, which means there are a lot of investors looking for rehabs. You can buy the property cheap and sell it for just a few thousand dollars more to an-other investor without doing any work. You won’t make nearly as much as the rehabber, but you will realize your profit quickly.

Flip Strategy #5: Pre-Construction

In very hot real estate markets, pric-es are appreciating as much as 2% per month. If you time things right, you can put a contract on a pre-construction house or condominium, then flip it to someone else when the development is complete. If it takes 12 months for the development to be complete, and the condo price is $500,000, you could make $100,000 or more in one year! Of course, the opposite is also true - you could end up losing money if the local economy tanks and you end up with a worthless condo that you can’t sell for more than you paid. Use this approach very carefully...

7 Ways to Flip a PropertyFlip Strategy #6: Scouting

The Scout is an information gatherer, so not technically a property flipper. He is the “bird dog” who finds poten-tial deals and sells the information to other investors. Many people get started as a Scout for other investors because it does not take any cash or prior knowledge to look for distressed properties. The Scout finds a property for sale, gathers the necessary infor-mation, and then provides this infor-mation to investors for a fee. The fee will vary depending on the price of the property and the profit potential. The Scout can expect to make five hundred to one thousand dollars each time he provides information that leads to a purchase by another investor.

Flip Strategy #7: Illegal Flipping

OK, no one is advocating this ap-proach, because it is illegal. Illegal property-flipping schemes work as follows: unscrupulous investors buy cheap, run-down properties in mostly low-income neighborhoods. They do shoddy renovations to the properties and sell them to unsophisticated buy-ers at inflated prices. In most cases, the investor, appraiser and mortgage broker conspire by submitting fraudu-lent loan documents and a bogus ap-praisal. The end result is a buyer that paid too much for a house and cannot afford the loan. Since many of these loans are federally insured, the gov-ernment authorities have investigated this practice and arrested many of the parties involved. As a result, the public perceives is flipping to be illegal.

12 www.MetrolinaREIA.org

Invest in Your Own Debts - A 23% Return by John McCarthy

“How to position yourself to make HUGE wealth-building profits!”

We live in a world that thrives on debt--the richest industry on planet earth--rigged for unlimited expansion!

Having grown up in a debt-ridden society, we tend not to put a lot of attention on debts, at least until something goes wrong. Very few people, if any, are debt free. In the US, very few people are solvent = they have sufficient cash resources to cover their debt load, a dangerous situation in anything but a thriving economy.

Debt is no friend to man, but does that mean all debt is bad? Being addicted to it, I doubt we will ever be totally rid of debt, but there are circumstances where debt does make sense. Debt used to create returns higher than the debt ser-vice (cash flow and/or profit) is totally acceptable providing there is sufficient finance in it to weather economic storms.

All other debt should be classified as a potential lethal weapon; it can and will be used against you.

We have not been well educated on the principles of cash, debt, or wealth management. Signs of this are everywhere. The average net worth of Americans is $250 (this was before the current economic downturn); we have a government bor-rowing trillions to pay off debts; companies are going bank-rupt in record numbers; governments are failing financially; and worldwide debt is over $40 Trillion and accelerating. This is not a healthy economic environment.

So, what we can we do about it?

As a real estate investor, you are in the unique position to profit from almost any economic environment wayward bank-ers can throw at you. Providing you have the skills to do this, the only other things that can get in your way is lack of cash flow, lack of equity, and low credit scores, and probably the last place you look for solutions is in your own backyard.

Increasing one’s income is always the best solution, but one of the fastest ways you can improve your financial situation is to simply pay your debts down quickly. To fully understand this, you need to look at how debts affect you financially:

* Debts eat up cash flow;

* They encumber your equity;

* They reduce your net worth;

* If too high or too many, they affect your credit scores

These are the very tools that you need to successfully build wealth.

Also, looking at the future, debts play another destruc-tive wealth building role: They tie up huge amounts of future income in interest expense that could be used to super-accel-erate your wealth building activities.

You are no doubt aware of how much mortgage interest you will pay over the next 30 years. Did you know that you could--

* Save up to $7.00 in future interest for every extra $1.00 you pay down on mortgage principal?

* Save up 75% or more in future interest payments by paying off your mortgage in 10 years instead of 30?

As a note to substantiate this, I have clients who have been using my debt elimination software for a number of years now and they are saving on average over $300,000 in future interest payments with an average pay off time of just over eight years. What could you accomplish as an investor with an extra $300,000?

By the way, if you look at the savings created as a return on investment, the average annual return would be over 23%.

Okay, so you don’t want to wait 10 years before you can start investing in real estate. I agree! But if you are not in a position to invest in real estate right now then do yourself the biggest favor you could ever do and start investing in your own debts. If you do, here’s what will happen:

* Your cash flow will increase;

* You will free up some equity;

* Your net worth will improve;

* Your credit scores will improve

Now, let’s assume that you have no funds available for debt investment. Well fear not, there is a way that you can still do this. It’s a little slower, but no less effective (and this is a subject thoroughly covered in my book Debt-2-Riches and far too lengthy for this article).

Even if you can invest in real estate right now, investing some of your funds in personal debt elimination will enhance all of your wealth-building activities.

The point here is you can turn things in your favor relatively quickly (from months to a year or two), and start on the road to greater future riches, and never have to look back. Here’s a rule that you should carry forward with you into every trans-action you ever do:

Never minimize your financial strength!

And the best way to do that per-sonally is--get out of debt!

Debt-2-Riches: 7 Steps To Debt-Free Living

by John McCarthy & Gary Knutson

Metrolina REIA Winner of the 2009 National REIA Award of Excellence 13

In this article, I want to share with you the concept of creat-ing your own personal investing criteria. Why is this so impor-tant? I’m glad you asked! Here’s my best answer: Four rea-sons to put your investing criteria in writing

Reason One: It helps you immediately know if a potential investment fits or does not fit. This saves you a tremendous amount of time sorting through which deals you are even going to take a closer look at.

Reason Two: It sharpens your focus and chances of finding great deals to begin with. How can you find what you want if you haven’t clearly defined what in fact you are looking for? How can you get other people to bring you great deals if you can’t clearly communicate what you are, in fact, looking for?

Reason Three: It allows you compare your criteria with other investors to learn from them, network, synergize, etc.

Reason Four: It helps show you how you are evolving over time as an investor. You can look at your written criteria as it has changed over time to see the ways you are growing.

Now I would like to share with you my personal criteria for investment deals. I share this with you because it gives you an idea of what your investment criteria might look like in prin-ciple. What size deals are you looking for? What kind? etc. What do good deals look like for you?

David’s personal investing criteria

1.) If I don’t understand the investment, I don’t make the in-vestment, period.

2.) I invest in areas where I have expertise and the advantage to make a superior investment with minimal time and effort and energy. This lowers my risk, magnifies my returns, and saves me time and effort (by my skill, my systems, my team, and amortizing costs over many similar deals). If I’m not go-ing to do multiple deals in an area or niche, it rarely pays to become an expert.

3.) I don’t put lots of capital at risk. If I am going to put money into a deal, I make sure it is a low-risk deal or medium-risk deal, and not a high-risk deal. I’m not comfortable taking a high risk with my money.

I look closely at how I’m secured in the deal. The greater the risk, the more I work to carve out and isolate those risks.

4.) If I am taking a medium risk in a deal, I expect to get a healthy cash on cash return, conservatively 15%, aggressively 30% - 40% or higher annual rate of return on my money de-pending on the degree of risk.

Plus, if the amount or deal is such that I want an extra layer of protection, I work to have some kind of meaningful input and insight on the deal (board of directors seat--with proper liability insurance in place to protect).

5.) Has the person selling me the investment bought himself or herself? If not, I pass. If so, it’s a necessary--but not suf-ficient criterion for me to invest. I may or may not invest after my due diligence.

How to Create Your Own Personal Investment Criteria BY David Finkel

6.) The game has to be worth playing. This means that if the deal isn’t big enough, why bother? Every deal requires due diligence of some sort. Deals where I put money at risk or take on personal liability have the highest need for due diligence. So, if the return is not there, the upside is not there on the whole, then I pass and don’t even get involved in the deal from the start.

7.) I look for ways I can bring increased value to the table be-sides just putting money into a deal to earn a founder’s share of the deal. For example, my skills in negotiation; or my skills of big picture business strategy and structuring; or my con-tacts; or my experience with making other deals happen.

Ultimately, I like to invest in my own deals best of all. I have more control, more influence, and I’ve already done my due diligence.

8.) If I am going to leverage my contacts to make an invest-ment work, or if I am asking other people to put in money or resources, then I better make sure through good, quality due diligence that the deal is right. I’m staking a tremendous amount on that deal, which is my word and my reputation in the business community.

9.) I look closely at how the deal is creating value. If there is no clear way that the people who are doing the deal are creating a tremendous increase in value somehow in the deal, then I question how they are going to make a great return.

They can create that tremendous value by: • turning around a property that was under performing • taking a property and getting it for low value because they are changing the owner-ship circumstances • taking a business and making it better through innovation or salesmanship, marketing skills, better contacts, better business management.

But somehow, they are going to have to increase or create value--either through better use of the property, or by changing the way something is positioned in a business environment; otherwise the deal can’t be a real deal.

10.) It has to be a business or investment that I feel good about, that I think does good things in the world: • provide comfortable housing • provide quality office space • provide a valuable service or commodity to the marketplace

11.) The people with whom I invest have to be people I want to be in business with. They have character, competence, and experience. I verify this in my due diligence.

About the author...

David Finkel is an ex-Olympic level athlete turned real es-tate millionaire and one of the leading investing experts in the nation. He is a Wall Street Journal and Business Week best-selling author of over 40 business and investing books and courses, including the wildly successful, Real Estate Fast-Track and The Maui Millionaires.

His website, www.MauiMillionaires.com, is a popular site for investors and entrepreneurs on the web and has dozens of free wealth tools and ebooks.

14 www.MetrolinaREIA.org

Saturday JUNE 11th

8:30am–1:00pm

“ Wealth through Knowledge”

To Attend Register online in advance at www.MetrolinaREIA.org

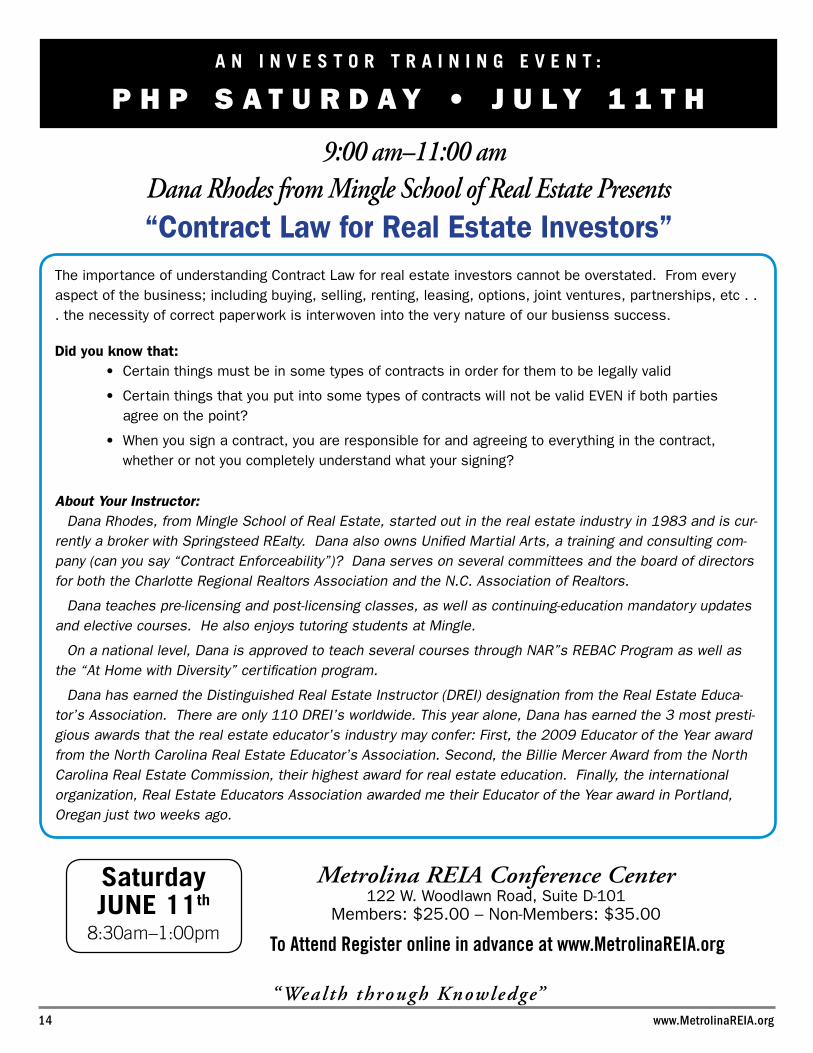

A N I N v E S t o r t r A I N I N g E v E N t :

P H P S A T U R D A Y • J U l Y 1 1 T H

Metrolina REIA Conference Center 122 W. Woodlawn Road, Suite D-101

Members: $25.00 – Non-Members: $35.00

9:00 am–11:00 am Dana Rhodes from Mingle School of Real Estate Presents “Contract Law for Real Estate Investors”

The importance of understanding Contract Law for real estate investors cannot be overstated. From every aspect of the business; including buying, selling, renting, leasing, options, joint ventures, partnerships, etc . . . the necessity of correct paperwork is interwoven into the very nature of our busienss success.

Did you know that:• Certain things must be in some types of contracts in order for them to be legally valid

• Certain things that you put into some types of contracts will not be valid EVEN if both parties agree on the point?

• When you sign a contract, you are responsible for and agreeing to everything in the contract, whether or not you completely understand what your signing?

About Your Instructor:Dana Rhodes, from Mingle School of Real Estate, started out in the real estate industry in 1983 and is cur-

rently a broker with Springsteed REalty. Dana also owns Unified Martial Arts, a training and consulting com-pany (can you say “Contract Enforceability”)? Dana serves on several committees and the board of directors for both the Charlotte Regional Realtors Association and the N.C. Association of Realtors.

Dana teaches pre-licensing and post-licensing classes, as well as continuing-education mandatory updates and elective courses. He also enjoys tutoring students at Mingle.

On a national level, Dana is approved to teach several courses through NAR”s REBAC Program as well as the “At Home with Diversity” certification program.

Dana has earned the Distinguished Real Estate Instructor (DREI) designation from the Real Estate Educa-tor’s Association. There are only 110 DREI’s worldwide. This year alone, Dana has earned the 3 most presti-gious awards that the real estate educator’s industry may confer: First, the 2009 Educator of the Year award from the North Carolina Real Estate Educator’s Association. Second, the Billie Mercer Award from the North Carolina Real Estate Commission, their highest award for real estate education. Finally, the international organization, Real Estate Educators Association awarded me their Educator of the Year award in Portland, Oregan just two weeks ago.

Advanced InvestorMeets 3rd Thurs. – 9:00 amJonathan’s Restaurant10630 Independence Pointe Pkwy., Matthews, NCContact: Chuck Wiedenhoeft 704-236-1130

Charlotte Landlord AssociationNo Meetings in June & July Meets 2nd Wed. – 6:00 pmMetrolina REIA Conf. Center122 W. Woodlawn Ave., Char-lotte — Turn in between IHOP & Tres PesosContact: Allon Thompson 704-364-8966

HickoryMeets 3rd Mon. – 6:00 pmHickory Elks Lodge356 Main Ave. NW, Hickory, NCContact: David Meier828-962-7946

Lake NormanMeets 1st Tues. – 6:30 pmAcropolis Restaurant 20659 Catawba Ave. Cornelius, NCContact: Mitch Young704-421-5950

MatthewsMeets Every Tues. – 6:00 pmJonathan’s Restaurant10630 Independence Pointe Pkwy., Matthews, NCContact: Tom Amann 704-668-1157

ConcordMeets 1st Thurs. – 6:00 pmLogan’s RoadHouse I-85 & Dale Earnhardt Blvd. Exit 60 off of I-852431 Wonder Dr., Kannapolis, NCContact: Cherrathee HagerTwinOakProperties4U @yahoo.com 704-490-2001

Gaston CountyMeets 2nd Mon. – 6:00 pmRyans Restaurant2900 E. Franklin Blvd. Gastonia, NCContact: Candy Tashiro704-691-0591

* Please note: Dates & Times of Sub-Groups meetings are subject to change. Confirm with Sub-Group leader prior to the meeting. Dates and times are correct at the time the newsletter is printed.

New Member Orientation5:30pm, prior to the Main MeetingHilton Hotel5624 Westpark Drive Charlotte, NC — I-77 at Tyvola Contact: Kimberly Shelton 704-877-8777 or email:[email protected]

Rock HillMeets 1st Thurs. – 6:00 pmFireBonz BBQ & Grill2445 Cherry Rd., Rock Hill, SCContact: Grady & Susan Denton – 704-905-8469

SUNDAY MONDAY TUESDAY WEDNESDAY THURSDAY FRIDAY SATURDAY

1 2 3 4

5 6 7 8 9 10 11

12 13 14 15 16 17 18

19 20 21 22 23 24 25

26 27 28 29 30 31

July 2009 Events Calendar

Gaston Co – 6pm

Hickory – 6pm

Matthews – 6pm

Lk. Norm – 6:30pm

Advanced – 9amMAin Meeting–6pMNew Member – 5:30pmVisitor Info – 6:00pm

PHP Saturday 9am – 1pmsee page 14 for details

Matthews – 6pm Sonrisers – 7am

Matthews – 6pm

Matthews – 6pm

Sub-Groups are a great way for you to learn more about real estate investing in a smaller group and network. As a guest you may attend two meetings and on the third you must join the association to continue attending meetings. *

HAPPY INDEPENDENCEDAY!

SonRisersMeets the 3rd Fri. – 7:00 amLight Rail Family Restaurant8045 South Blvd. Charlotte, NCContact: Leon Humphrey 704-460-4933

Visitor Information Session6:00pm, prior to the Main MeetingHilton Hotel5624 Westpark Drive Charlotte, NC — I-77 at Tyvola Contact: Kimberly Shelton 704-877-8777 or email:[email protected]

Rock Hill – 6pm

Concord – 6pm

All Day with Than Merrill see page 13 for details

N E W M E M B E r P r o g r A M g I v E S Y o U

f A S t S t A r t t o S U c c E S S

Metrolina Real Estate Investors Association122 W. Woodlawn Road, Suite D-101Charlotte, NC 28217

This New Member Program is designed to get each and every new member off to a good start. After completing a few basic requirements, each new member will be recognized and awarded a certificate.

The “Fast start To Success” steps are: • Attend the New Member Orientation • Attend a main meeting • Attend a subgroup meeting • Volunteer at an event • Register and attend a PHP Saturday • Complete the member profile on the website.

RSVP to Kimberly Shelton at 704.877.8777 or [email protected]. The “Fast Start to Success” is held each month prior to the Main Meeting from 6:00–6:20pm.

IS YOUR PROFILE UP-to-DATE on the Metrolina REIA Website?Your membership is important to us. To get the most out of the Metrolina REIA, please to log on to our website

and update your profile. Go to www.MetrolinaREIA.org and here’s the instructions:

1st click on Members on the left side of the page in the grey area - the one on the bottom. That will take you to the log in page. Update your information and add your photo.

It is very important for us to have up-to-date info on each and every one of our members so we can communicate with you on all of the upcoming events and news.

If you don’t have your log in info email Kimberly Shelton at [email protected].