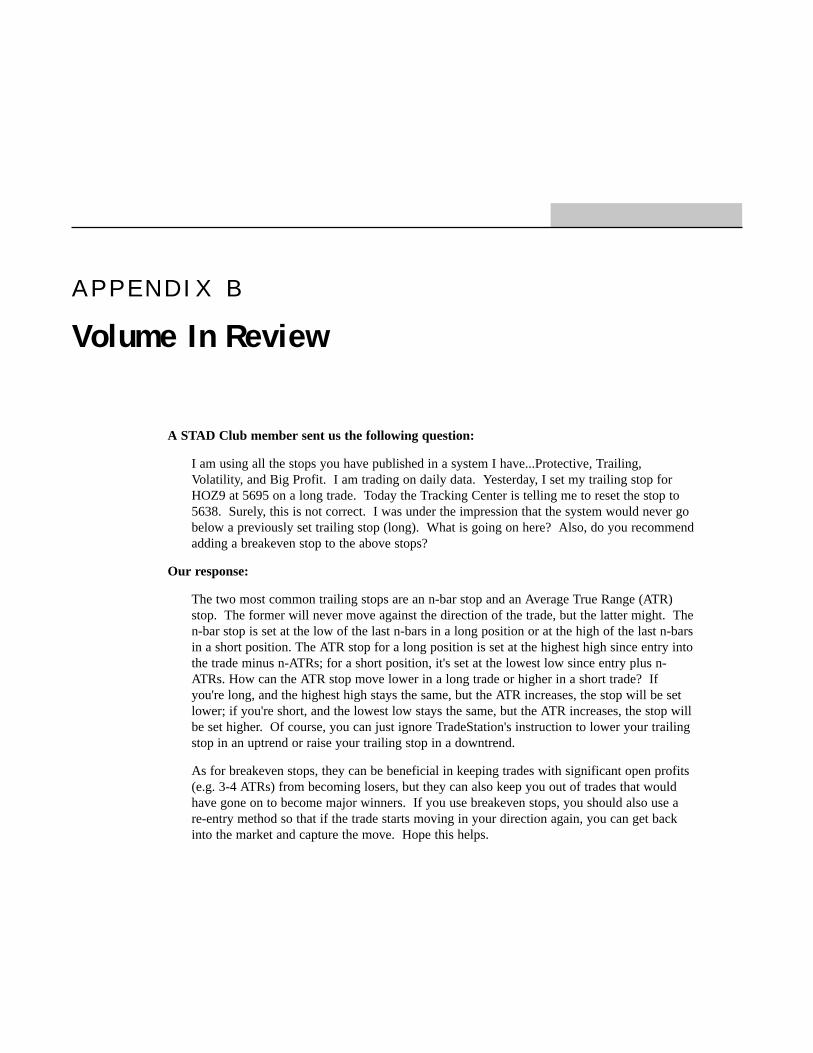

Embed Size (px)

Citation preview

V O L U M E 1 0

© 1999 . O M E G A R E S E A R C H , I N C . M I A M I , F L O R I D A .

Information in this document is subject to change without notice.

THE TRADING SYSTEMS IN THIS BOOK ARE EXAMPLES ONLY, AND HAVE BEEN INCLUDED SOLELY FOREDUCATIONAL PURPOSES. OMEGA RESEARCH DOES NOT RECOMMEND THAT YOU USE ANY SUCH TRADING

SYSTEM, AS THE USE OF ANY SUCH TRADING SYSTEM DOES NOT GUARANTEE THAT YOU WILL MAKEPROFITS, INCREASE PROFITS, OR MINIMIZE LOSSES. THE SOLE INTENDED USES OF THE TRADING SYSTEMSINCLUDED IN THIS BOOK ARE TO DEMONSTRATE THE WAYS IN WHICH EASYLANGUAGE CAN BE USED TO

DESIGN PERSONAL TRADING SYSTEMS AND TO SHOW SOME EXAMPLES OF HOW CERTAIN POPULAR, WELL-KNOWN TRADING STRATEGIES MAY BE INCORPORATED INTO PERSONAL TRADING SYSTEMS. OMEGA

RESEARCH, INC. IS NOT ENGAGED IN RENDERING ANY INVESTMENT OR OTHER PROFESSIONAL ADVICE.IF INVESTMENT OR OTHER PROFESSIONAL ADVICE IS REQUIRED, THE SERVICES OF A COMPETENT

PROFESSIONAL SHOULD BE SOUGHT.

Copyright © 1999 Omega Research Inc. All rights reserved. No part of this publication may be reproduced, stored in aretrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise,without prior written permission of Omega Research, Inc. Printed in the United States of America.

TradeStation® and SuperCharts® are registered trademarks of Omega Research, Inc. EasyLanguage, Portfolio Maximizer,PaintBar, ShowMe and SystemBuilder are trademarks of Omega Research, Inc. Microsoft is a registered trademark ofMicrosoft Corporation and MS-DOS, Windows, and Excel are trademarks of Microsoft Corporation. DBC Signal and BMIare trademarks of Data Broadcasting Corp. Price data supplied courtesy of Global Market Information, Inc.

Contents

INTRODUCTION Welcome to STAD 10..........................................................................................................5

Chapter 1: JK Monday We Trade........................................................................................................11

Chapter 2 The Serendipity Entry Trigger, by Chuck LeBeau ...........................................................19

Chapter 3 Serendipity System............................................................................................................21

Chapter 4 Eight Ball...........................................................................................................................31

Chapter 5 Measuring & Comparing Performance .............................................................................49

Chapter 6 Going In Style ...................................................................................................................55

Chapter 7 Who’s Minding The Store ................................................................................................69

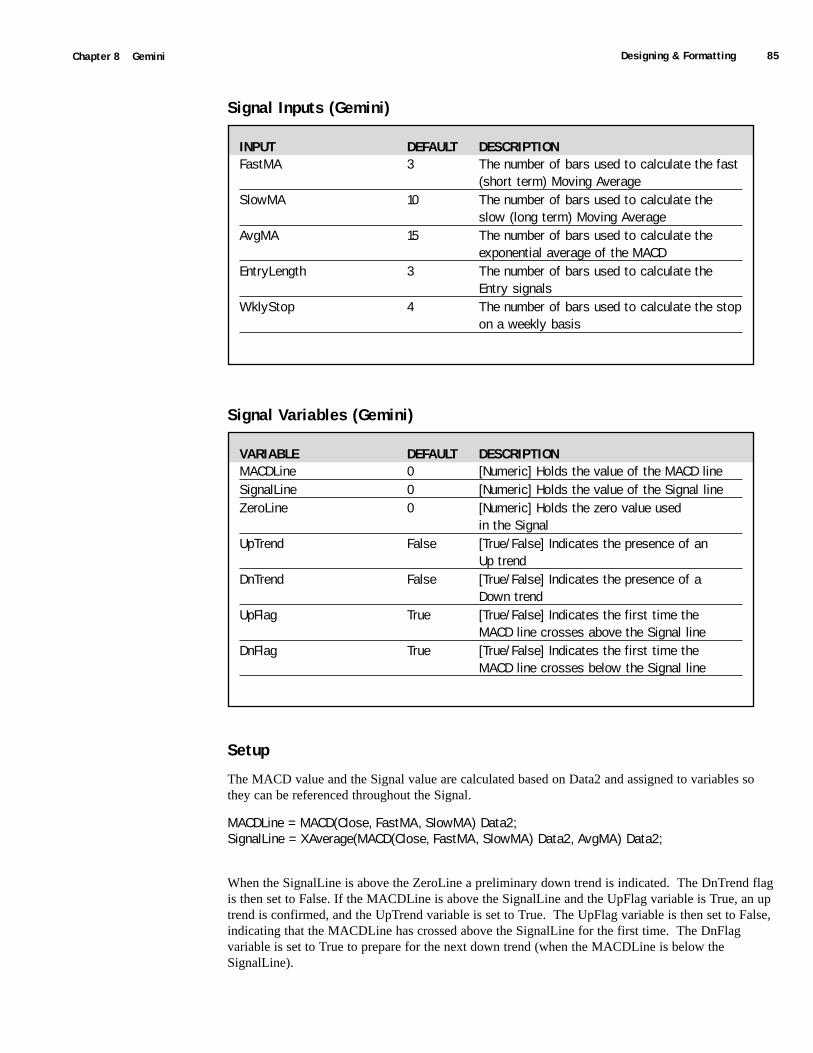

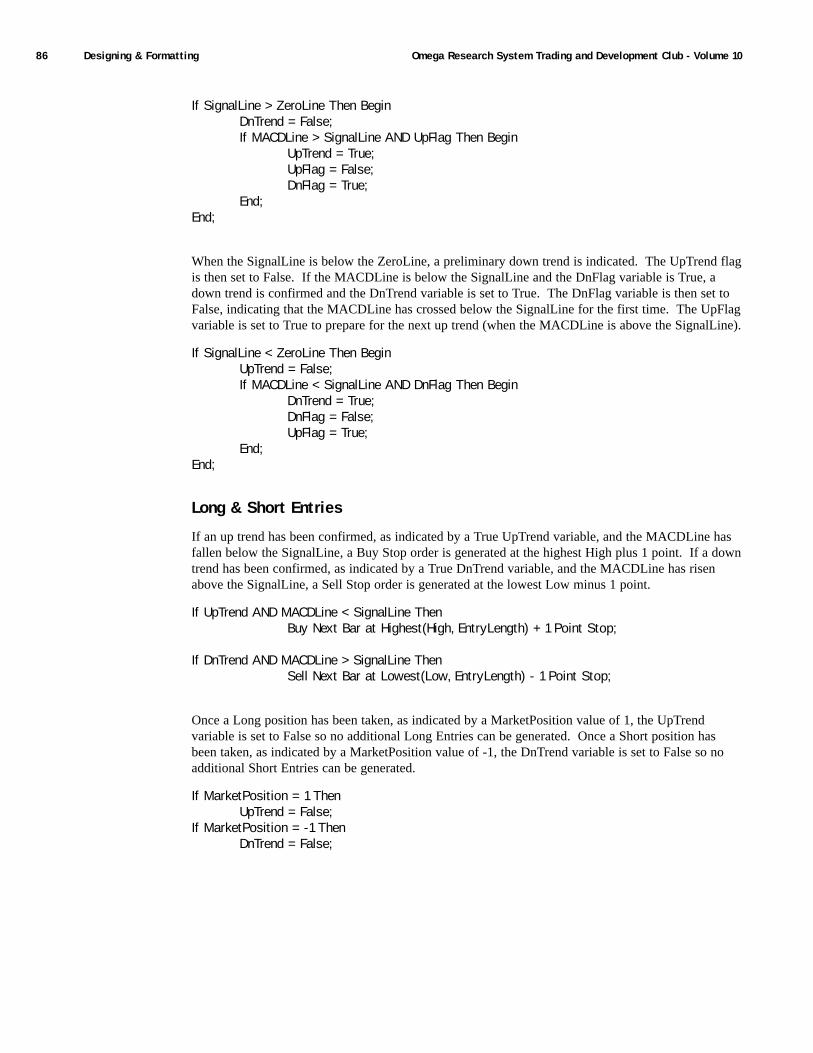

Chapter 8 Gemini ...............................................................................................................................81

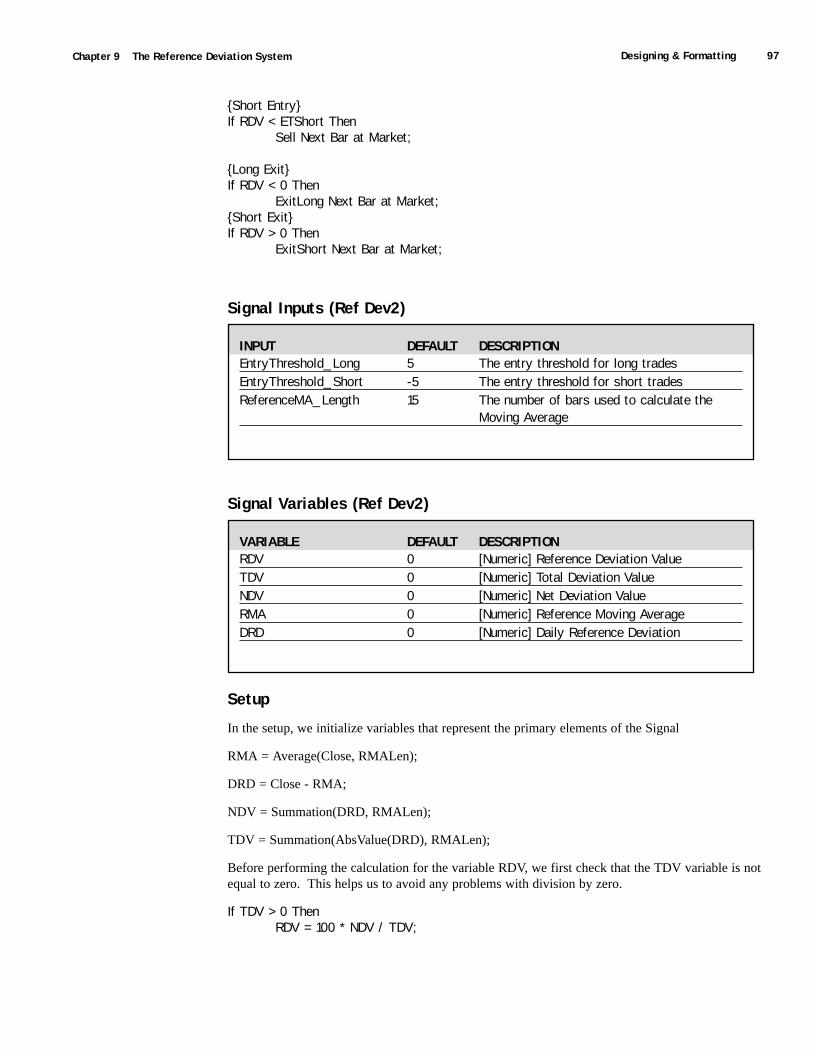

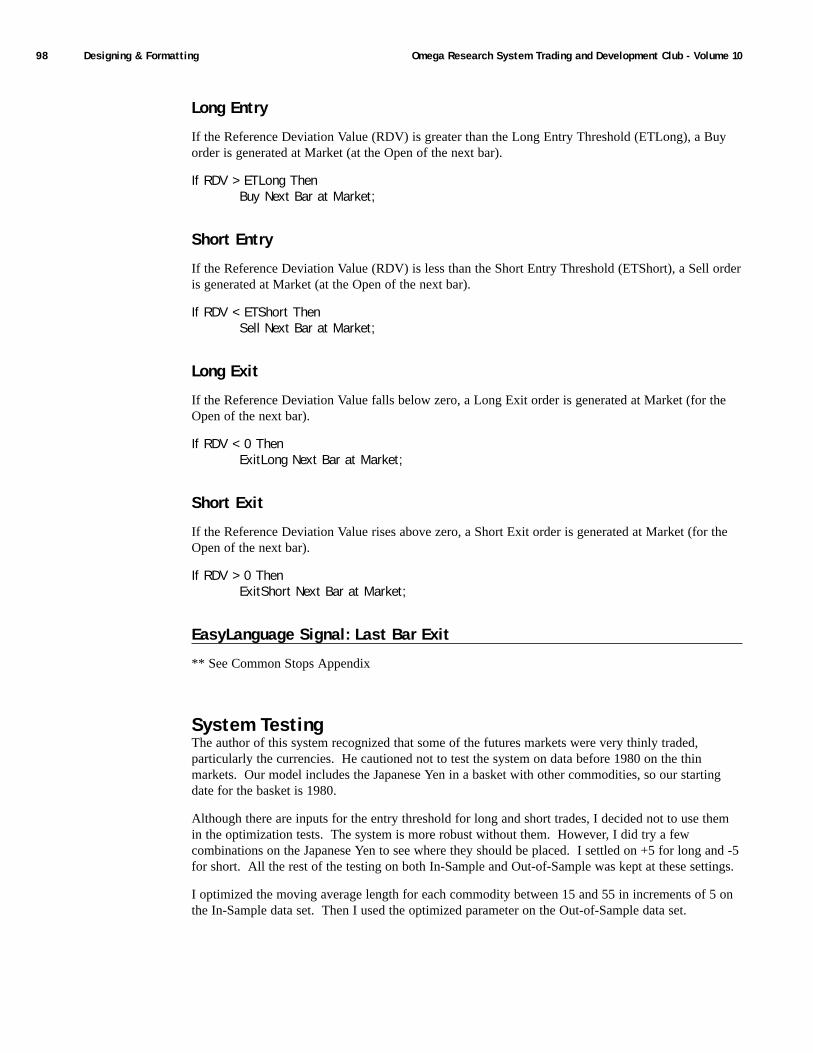

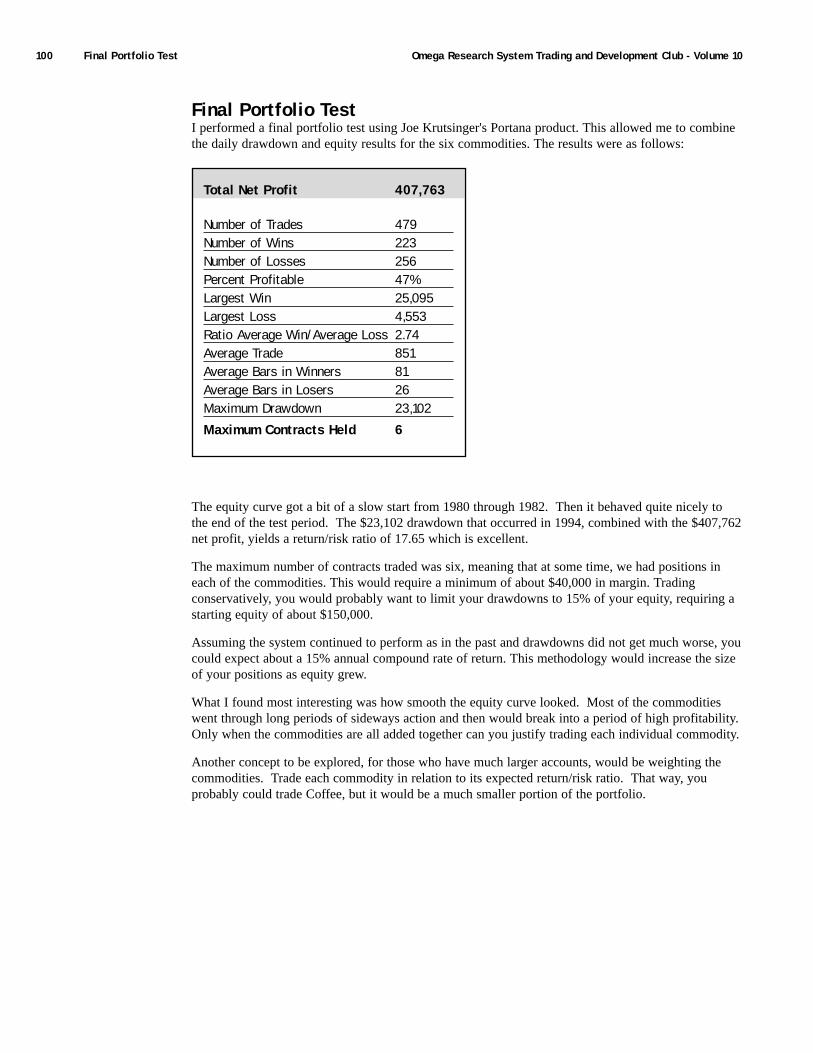

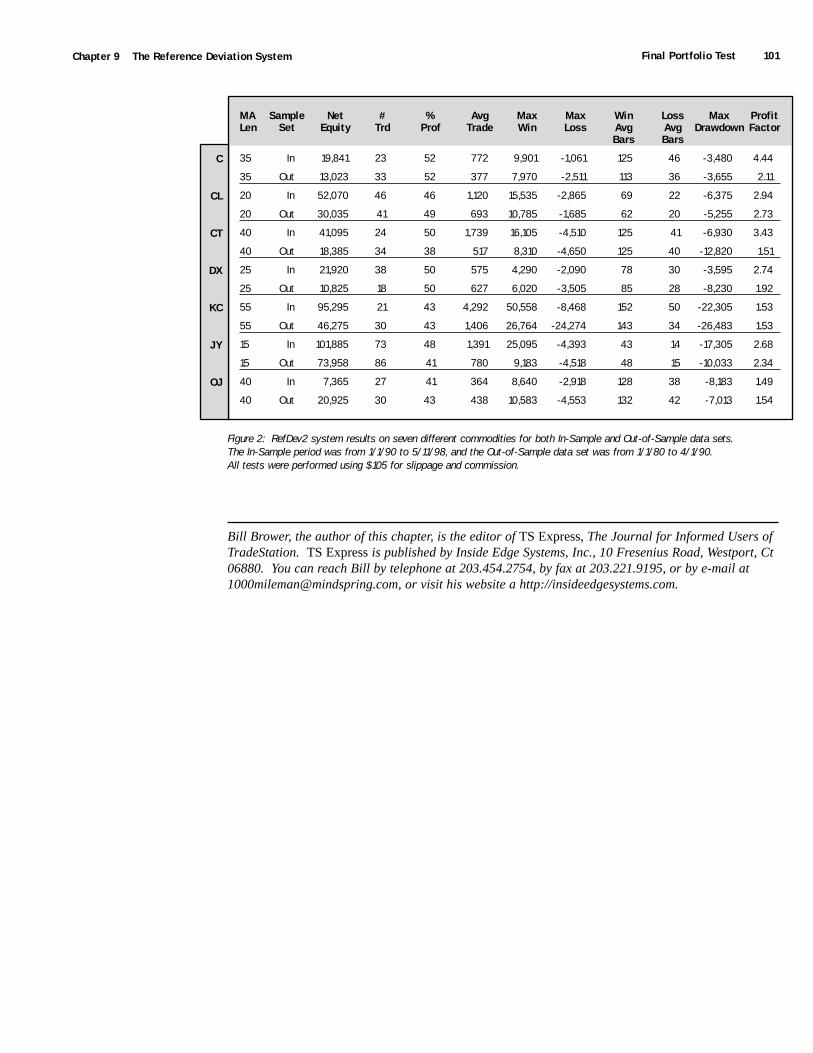

Chapter 9 The Reference Deviation System, By William Brower, CTA ..........................................95

Chapter 10 Superman ........................................................................................................................103

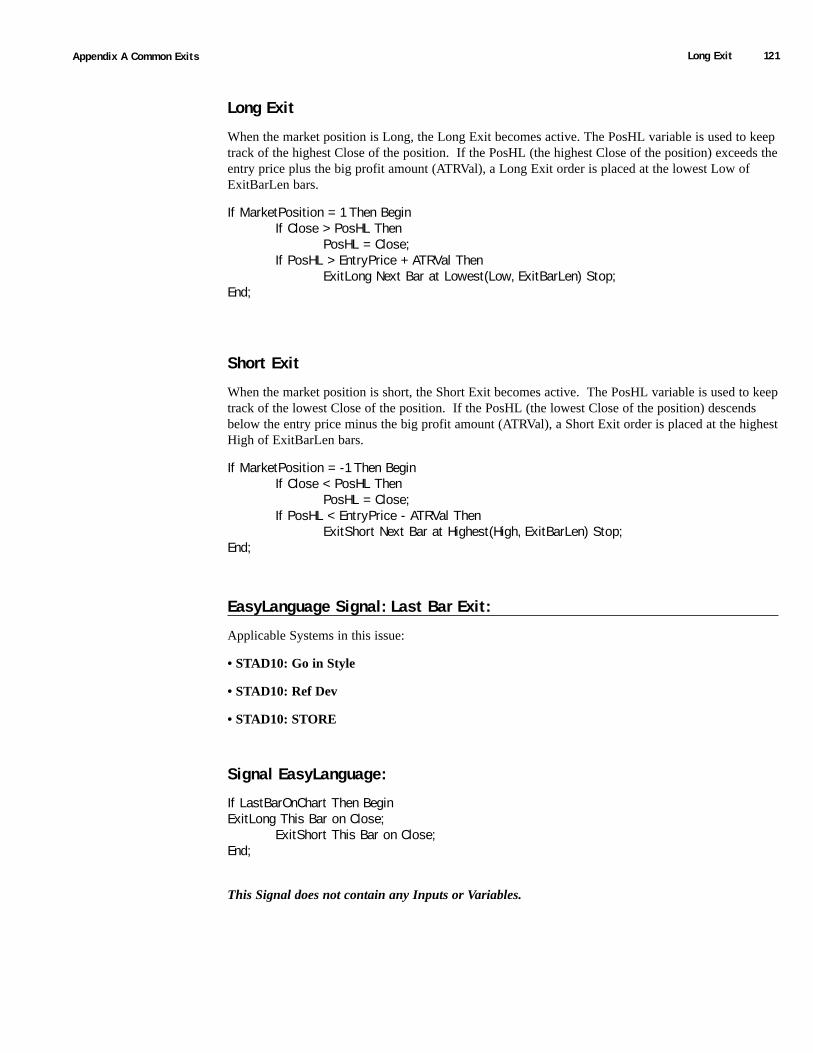

Appendix A: Common Exits .................................................................................................................115

Appendix B Volume in Review ...........................................................................................................123

Index...................................................................................................................................124

I N T R O D U C T I O N

Welcome to Volume 10

Welcome to Volume 10 of the Omega Research System Trading & DevelopmentClub. We're very glad to know that you're taking advantage of this uniquelearning tool to improve your understanding of trading systems and to increase

the bottom-line results of your trading.

We believe that STAD Club Volume 10 contains something for everyone, from the beginner tothe advanced systems trader. The systems in this issue incorporate popular and importantconcepts such as using both setup conditions and entry techniques to find and then confirmtrading opportunities, and managing positions with several exit strategies — each one performingits own crucial function.

Here's a quick rundown of what you'll see in this volume: Monday We Trade isolates the one dayeach week that is best for trading the stock indices (guess which day), the Serendipity EntryTrigger improves a widely used entry technique by changing just one word in the EasyLanguagecode, and the Serendipity System turns that entry technique into a complete system by adding theRSI, two stops and a profit target.

Our Eight-Ball system uses two exponential moving averages to identify the long and short-termtrends, a volatility trigger to confirm the setup, and a series of stops to manage the trade. Goingin Style adds a volatility expansion condition and the Parabolic stop to enhance a price channelbreakout system. Who's Minding the Store integrates a classic chart pattern and the Stochasticoscillator to find winning trades.

The Gemini system relies on two data series from different time periods: one for the setup, theother for timing the entry, while our Superman system evaluates both the strength and the speedof a market to find reliable trading opportunities. A system from TradeStation guru Bill Brower-the RefDev2 System-builds on a smoothed momentum function to produce a solid-performingtrendfollowing system. Finally, a new RadarScreen indicator will let you know instantly andautomatically which stocks have made the greatest % change and which have lagged behind.

We think STAD 10 is one of our best volumes so far. How much you learn and how much youactually apply to your own trading are, of course, up to you. As always, we wish you good luckand good trading.

IMPORTANT NOTICE: The trading systems in this book are examples only, and they havebeen included solely for educational purposes. Omega Research does not recommend thatyou use any such trading system, as the use of any such trading system does not guaranteethat you will make profits, increase profits, or minimize losses. The sole intended use of thetrading systems included in this book are to demonstrate the ways in which EasyLanguagecan be used to design personal trading systems and to show some examples of how certainpopular, well-known trading strategies may be incorporated into personal trading systems.

Omega Research System Trading and Development Club - Volume 106 Contents at a Glance

Contents at a Glance! Chapter 1: JK Monday We Trade

! Chapter 2: The Serendipity Entry Trigger, by Chuck LeBeau

! Chapter 3: Serendipity System

! Chapter 4: Eight Ball

! Chapter 5: Measuring & Comparing Performance

! Chapter 6: Going In Style

! Chapter 7: Who’s Minding The Store

! Chapter 8: Gemini

! Chapter 9: The Reference Deviation System, by William Brower, CTA

! Chapter 10: Superman

! Appendix A: Common Exits

! Appendix B: Volume in Review

! Index

Additional Educational ServicesOmega Research is committed to enhancing individual trading potential through quality education. To learn more about systemtrading, an Omega Research product, or EasyLanguage, visit our web site at www.omegaresearch.com or call (800) 439-7995(outside US 305-485-7000) and ask about the following educational services:

WorkshopsOmega Research offers a variety of workshops on Omega Research 2000i products and technical analysis. Workshops are anexcellent way to learn how to use the products, learn about technical analysis and system trading and/or EasyLanguage. Spend aday with a Product Training Specialist and exchange ideas with other users like yourself. All workshops provide a 100%satisfaction guarantee. Call now for more information or to register — space is limited!

EasyLanguage Resource CenterOne of the best ways to learn is by example, and the EasyLanguage Resource Center on our web site is an excellent source ofexamples. In this Resource Center, we list all the analysis techniques — indicators and trading systems — published in theTechnical Analysis of Stocks and Commodities magazine, as well as popular analysis techniques worth taking a look at. Access tothis Resource Center is free of charge. Feel free to download and review any of the analysis techniques and their descriptions. Ourweb site address is www.omegaresearch.com.

Getting StartedTo begin reviewing your systems, transfer the analysis techniques into your TradeStation® library and then apply the system youwant to review to a chart. Use the System Report to view the system results and take a look at the EasyLanguage instructions byopening the system in the PowerEditor™.

To transfer the analysis techniques into TradeStation:

1. Place the System Trading and Development Club CD in the CD-ROM drive.

2. Start the PowerEditor. In Windows, click Start, choose Programs, choose OmegaResearch (OMGA) and choose EasyLanguage PowerEditor.

Obtaining Technical Support 7Introduction

3. In the PowerEditor, use the File - Import and Export menu sequence.

4. Select the Import EasyLanguage Archive File (ELA and ELS) option and click NEXT.

5. Click Scan.

6. In the Enter drive letter to scan edit box, enter the drive letter for your CD-ROM drive(normally D), and click OK.

7. Choose STAD10.ELS from the list and click NEXT.

8. Below the Analysis Types box choose the Select All button and click NEXT.

9. Below the Available Analysis Techniques box choose the Select All button and clickFINISH.

10. Once the files are transferred and verified, a dialog box appears informing you that thetransfer was performed successfully. Click OK.

For your convenience, the names of the systems in this volume all begin with STAD10 (although the signals will not have this prefix).You can now open the systems in the PowerEditor and view the EasyLanguage instructions and/or apply them to a chart in TradeStation.You can remove your CD from the CD-ROM drive and store it in a safe place. As you apply the systems and work with them, refer tothis book for detailed explanations of the systems and the EasyLanguage used to create them. For instructions on applying systems andviewing the System Report, please refer to your TradeStation User's Manual.

Note to SuperCharts® Users: To transfer the systems into SuperCharts, use the Tools - QuickEditor menu sequence and select Transfer.Keep in mind, however, that although you can apply the systems in SuperCharts, you will not be able to view the EasyLanguageinstructions in the QuickEditor. This is because the systems were designed in the PowerEditor. Also, if you are using SuperCharts Endof Day, some of the systems will not apply as they are designed for intraday trading. Since the purpose of the Club is to provide youwith a learning tool, and viewing the EasyLanguage instructions is an essential part of this learning process, the use of this club forSuperCharts users is limited.

Note to TradeStation or SuperCharts 3.x Users: The systems for the Club were designed using TradeStation 2000i. As such, some ofthe features used, such as automatic drawing of trendlines and/or text, are not available in previous versions of TradeStation (orSuperCharts). An effort is made to provide a variety of systems that incorporate both long standing and new features; however, keep inmind that as new features are developed, we will naturally want to showcase and educate users on these features; therefore, users of themost recent version of our software will be able to make the most use of the Club.

Obtaining Technical SupportDepending on your question, there are two resources at your disposal: the EasyLanguage Support Department and the STAD ClubE-Mail Address.

EasyLanguage Support DepartmentThe EasyLanguage Support Department provides EasyLanguage support via fax and is designed to help you troubleshoot ananalysis technique or trading system you are currently working on. For example, if you are incorporating a trading system from theClub into your own and have a question about the implementation, the EasyLanguage Support Department can answer it.

Please keep in mind that while this department can answer any EasyLanguage question, it cannot answer questions about the STADClub specifically, such as the theory behind a system in the Club, why a system was developed a certain way, or why the system is notperforming as you expect it to, etc.

Fax Number: (305) 485-7598

E-Mail Address: [email protected]

Omega Research System Trading and Development Club - Volume 108 Benefits of System trading

Be sure to include the following information in your fax or e-mail:

! Name

! Security Block or Customer ID Number

! Telephone Number

! Fax Number

! Product you own

! EasyLanguage instructions you are working on

! Detailed description of your problem

Please allow 48 hours for a response.

STAD Club E-Mail AddressAnother resource at your disposal is the STAD Club e-mail address.

Please realize that when you send a message to this e-mail address, you will not receive a response directly; your message will bereviewed and the answer incorporated into the next volume of the STAD Club, when applicable. Therefore, if you need technicalsupport on EasyLanguage, please use the above fax number or e-mail address.

Please send any comment, suggestion, or question regarding the systems in the Club to the STAD Club e-mail address, and in eachsubsequent volume we will publish the most common suggestions and questions.

Benefits of System TradingThere are at least five major benefits of trading in a systematic manner as opposed to trading in a discretionary manner:

1. You’ll have a system that is compatible with your own personality and trading style — a system that you are comfortable with andthat you can follow.

2. You will eliminate overly emotional trading and reduce the stress of constantly making subjective, spur-of-the-moment tradingdecisions.

3. You will have objective entry and exit criteria that have been validated by historical testing of quantifiable data.

4. You will know the maximum peak-to-valley drawdown that your system has experienced in the past, and you can make sure that youare adequately capitalized (both financially and psychologically) to withstand another worst-case drawdown.

5. You will gain confidence in both your system and yourself, thus strengthening your ability to follow your system and to trade in ahighly disciplined manner.

As you continue to become more proficient as a systems trader, you will almost certainly discover even more benefits of a systematicapproach.

Getting Ideas For SystemsWe can easily think of at least five great ways to get ideas for trading systems. You’ll probably come up with at least a few more. Here’sour quick list:

1. SuperCharts and TradeStation’s built-in indicators, ShowMeTM studies, PaintBarsTM, and systems

2. Trading As A Business by Charlie Wright (available from Omega Research)

3. Jack Schwager’s Complete Guide to Designing and Testing Trading Systems (12 videos, CD, manual; available from OmegaResearch)

Getting Ideas for Systems 9Introduction

4. OmegaWorld (June, 2000, New York City)

5. And, of course, Omega System Trading & Development Club (ten new trading ideas with manual and CD, published six times peryear. Club members also receive a password for Omega’s STAD Club online forum.)

Once we’re convinced that systems trading is more likely to generate consistent profits than discretionary trading, and once we have anidea for a trading system, how do we progress from an idea to a complete system?

Building a Trading System

We hope the following ten-step plan will prove useful:

1. Write your trading idea as a ShowMe study. Scroll through several years of data to develop a sense of how your idea performs.

2. Write a very simple system based on your idea. For example, you could write a system that enters a position based on your idea andexits the position automatically after n-days. Alternatively, you could write a stop-and-reverse system that uses your idea to enter,exit, and reverse positions.

3. Design a setup for your system. A setup alerts you that a trading opportunity has developed. Setups don’t get you into a trade, butthey do tell you that market conditions have become favorable for a trade. An example of a buy setup is a market posting twoconsecutive closes above a moving average. An example of a sell setup is the Relative Strength Index (RSI) crossing from above 70to below 70.

4. Design an entry for your system. An entry is the criterion that must be met after a setup for a trade to be initiated. An example of abuy entry is a market rallying one average daily range above yesterday’s close. An example of a sell entry is a market’s declinebelow the previous week’s low.

5. Design an exit for your system. An exit is the criterion by which a trade is closed out. Trailing stops, profit targets, and exitconditions will account for most of your system’s exits.

A trailing stop is set below the current price for a long position and above the current price for a short position. When you are in a longposition, you raise the trailing stop as the market trades higher to lock in profits; while short, you lower the trailing stop as the markettrades lower, locking in profits.

An alternative to exiting on a trailing stop is exiting at a profit target. A profit target closes out a trade when the price reaches aspecified objective. One example of a profit-target exit is to close out a position on the second close above the high of the entry day.Another example is to automatically close out a trade when open profits equal three times the initial risk on the trade.

An exit condition gets you out of a trade when a market no longer justifies an open position. Good traders do not always rely on stopsto exit their trades. If the technical condition that got you into a trade (e.g. a rising moving average) is no longer in effect, you shouldexit the trade immediately rather than waiting for your stop to be hit.

6. Select the data on which you will test your system. For example, you might choose to test your system on continuous, back-adjusteddata on U.S. Treasury Bonds from January, 1978 through December, 1997.

7. Divide the test data into five equal parts. Since you are going to test your system on 20 years of data, each part consists of four years.The first four years (01/02/78 - 12/31/81) are reserved for the backward test, and the last four years (01/02/94 - 12/31/97) arereserved for the forward test. The middle 12 years (01/02/82 - 12/31/93) are the data on which you will test and optimize yoursystem.

8. Test and optimize your system on the large, middle section of data. To evaluate the results of testing and optimizing, you shouldconsider several factors including equity curve, net profit, percent profitable, profit factor (dollars won per dollar lost), average trade,and maximum drawdown.

9. Backward and forward test your system on the out-of-sample data you reserved. The test results will probably not be as good as theresults on the data for which your system was optimized. However, for your system to be tradable, the backward and forward testsshould yield favorable results. Your system is unlikely to perform better in the future than it did on the out-of-sample data. Checkyour system’s performance on the same key factors that you evaluated during your test of the sample data (equity curve, net profit,percent profitable, profit factor, average trade, and maximum drawdown).

10. Trade your system with consistency, confidence, and courage.

C H A P T E R 1 :

JK Monday We Trade

Joe Krutsinger, a long-time friend of Omega Research, contributed the Monday We Trade(MWT) system to STAD Club. MWT is a fine example of how a simple system-based on asound idea-can generate extraordinary profits.

MWT trades the stock indices. Joe tested it on the NASDAQ 100, and we tested it on the S&P500. Out of curiosity, we also tested it on an individual stock — IBM. (Test results can be foundbelow.) Here's the entire system: if it's Friday and the close is above a two-day simple movingaverage, buy at the open on Monday, set a money-management stop, and exit on the close; if it'sFriday and the close is below a two-day simple moving average, sell short at the open onMonday, set a money-management stop, and exit on the close. (If the market's not open onMonday, take the trade on Tuesday.)

Omega Research System Trading and Development Club - Volume 1012 Defining Our Trading Rules

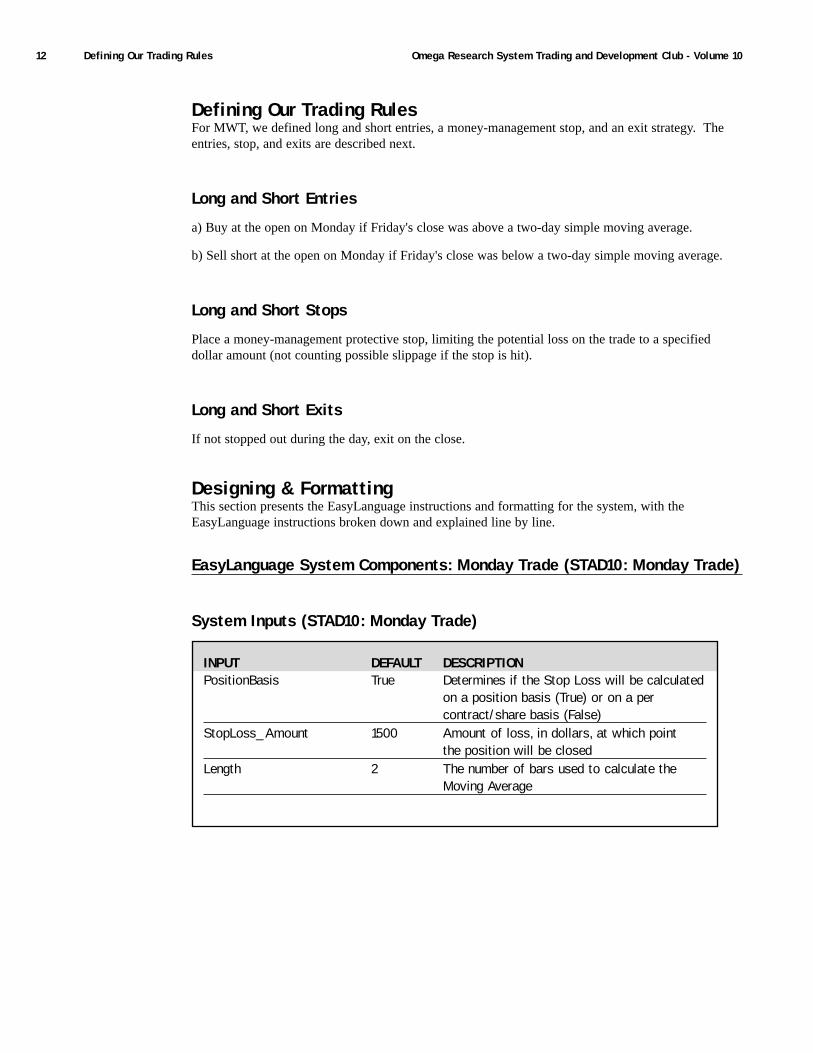

Defining Our Trading RulesFor MWT, we defined long and short entries, a money-management stop, and an exit strategy. Theentries, stop, and exits are described next.

Long and Short Entries

a) Buy at the open on Monday if Friday's close was above a two-day simple moving average.

b) Sell short at the open on Monday if Friday's close was below a two-day simple moving average.

Long and Short Stops

Place a money-management protective stop, limiting the potential loss on the trade to a specifieddollar amount (not counting possible slippage if the stop is hit).

Long and Short Exits

If not stopped out during the day, exit on the close.

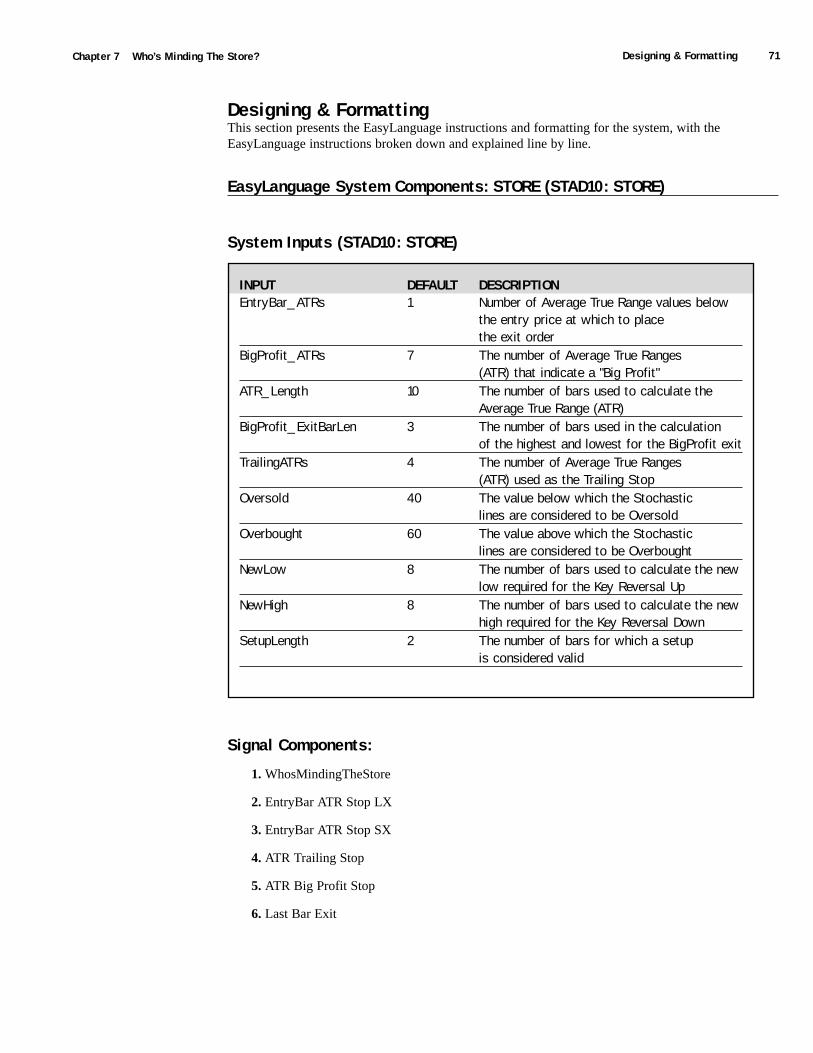

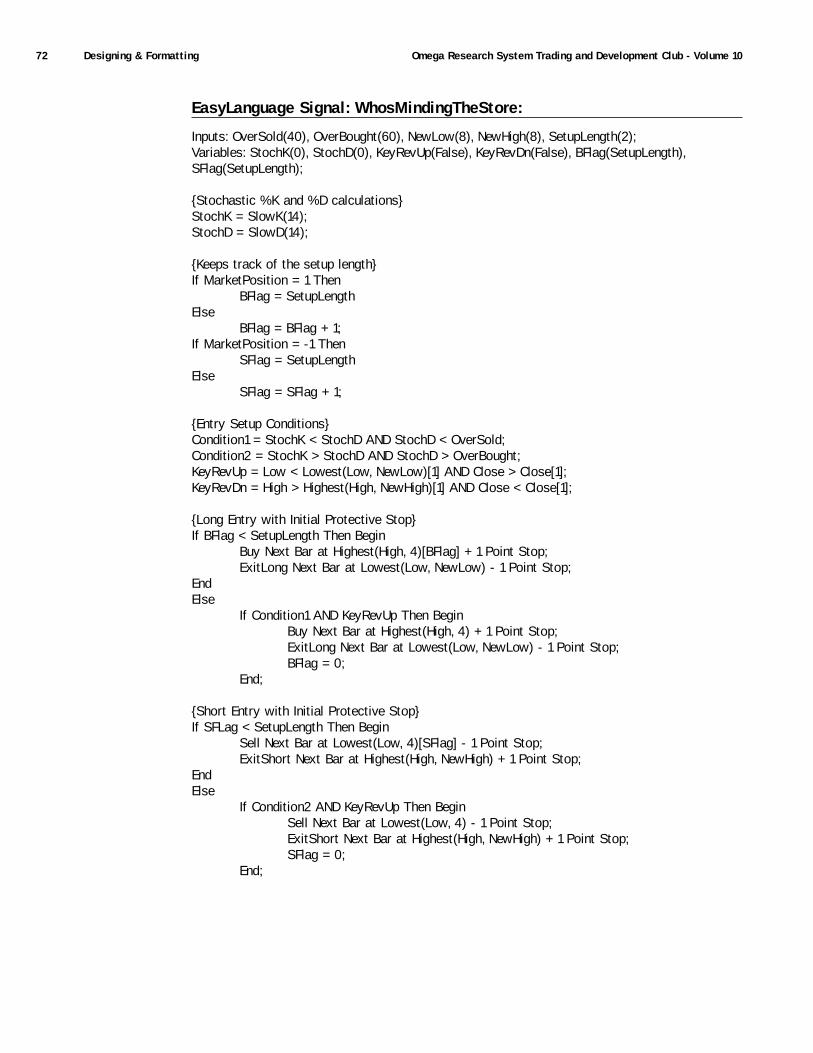

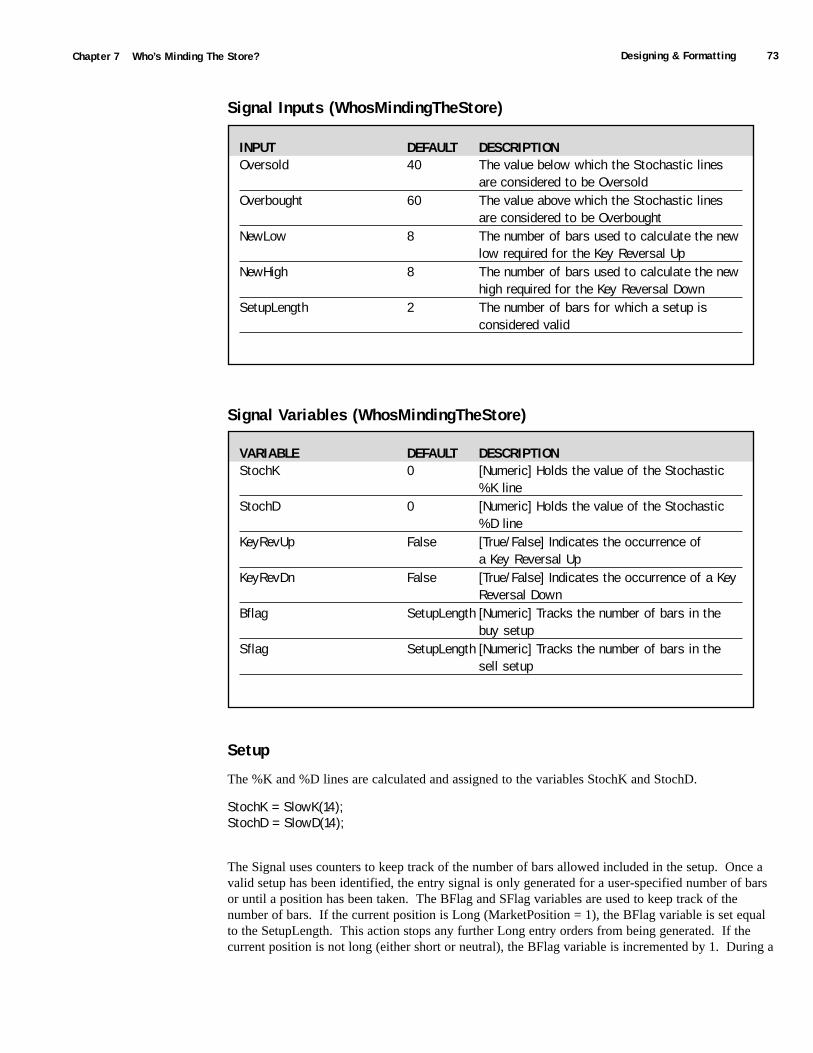

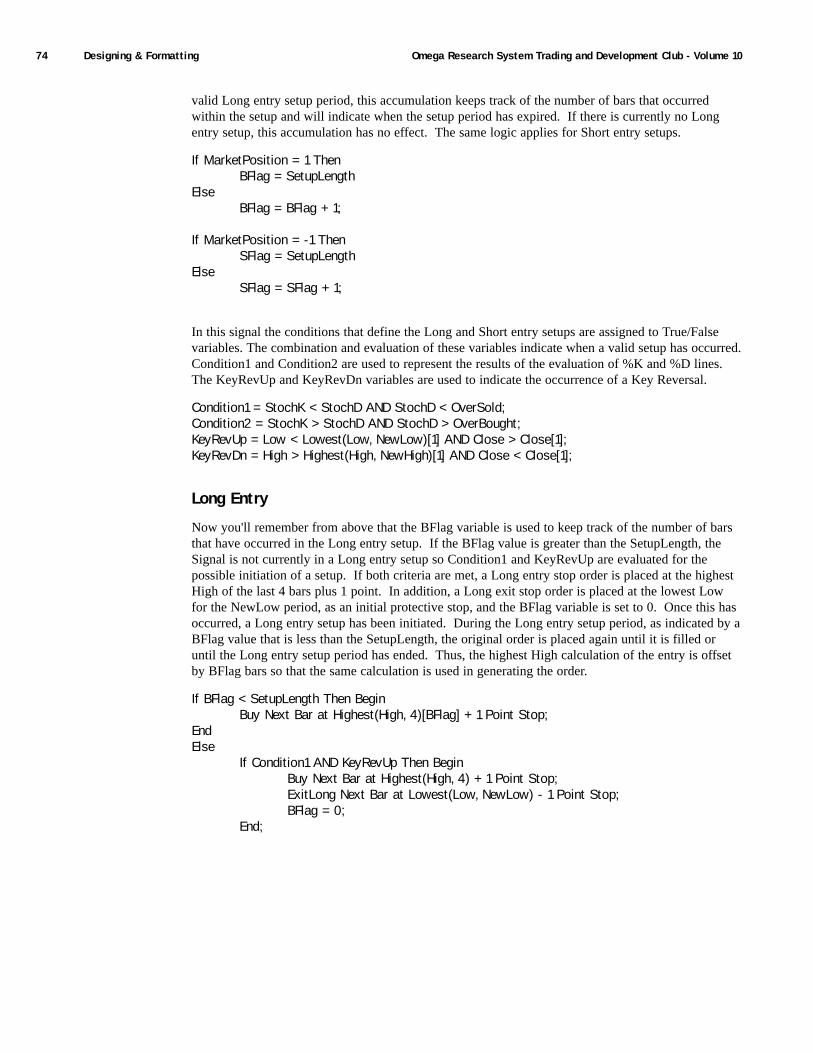

Designing & FormattingThis section presents the EasyLanguage instructions and formatting for the system, with theEasyLanguage instructions broken down and explained line by line.

EasyLanguage System Components: Monday Trade (STAD10: Monday Trade)

System Inputs (STAD10: Monday Trade)

INPUT DEFAULT DESCRIPTIONPositionBasis True Determines if the Stop Loss will be calculated

on a position basis (True) or on a percontract/share basis (False)

StopLoss_Amount 1500 Amount of loss, in dollars, at which pointthe position will be closed

Length 2 The number of bars used to calculate theMoving Average

Designing & Formatting 13Chapter 1 JK Monday We Trade

Signal Components:

1. JK Monday We Trade!

2. Stop Loss

3. Close at end of day

EasyLanguage Signal: JK Monday We Trade!:

Input: Length(5);

If DayOfWeek(Date) = Friday AND Close > Average(Close, Length) Then Buy Next Bar at Market;

If DayOfWeek(Date) = Friday AND Close <= Average(Close, Length) ThenSell Next Bar at Market;

Signal Inputs (JK Monday We Trade!)

Long Entry

If the current day of the week is Friday, and the Close is greater than the 2 bar Average of the Close, aBuy order is placed on the open of the next bar (Market), Monday.

If DayOfWeek(Date) = Friday AND Close > Average(Close, Length) Then Buy Next Bar at Market;

Short Entry

If the current day of the week is Friday, and the Close is less than the 2 bar Average of the close, aSell order is placed on the Open of the next bar (Market), Monday.

If DayOfWeek(Date) = Friday AND Close <= Average(Close, Length) ThenSell Next Bar at Market;

EasyLanguage Signal: Close at end of day

This Signal simply uses an EasyLanguage keyword called SetExitOnClose to trigger an Exit, eitherLong or Short, at the end of the trading day.

SetExitOnClose;

INPUT DEFAULT DESCRIPTIONLength 2 The number of bars used to calculate the

Moving Average

Omega Research System Trading and Development Club - Volume 1014 Designing & Formatting

EasyLanguage Signal: StopLoss

** See Common Stops Appendix

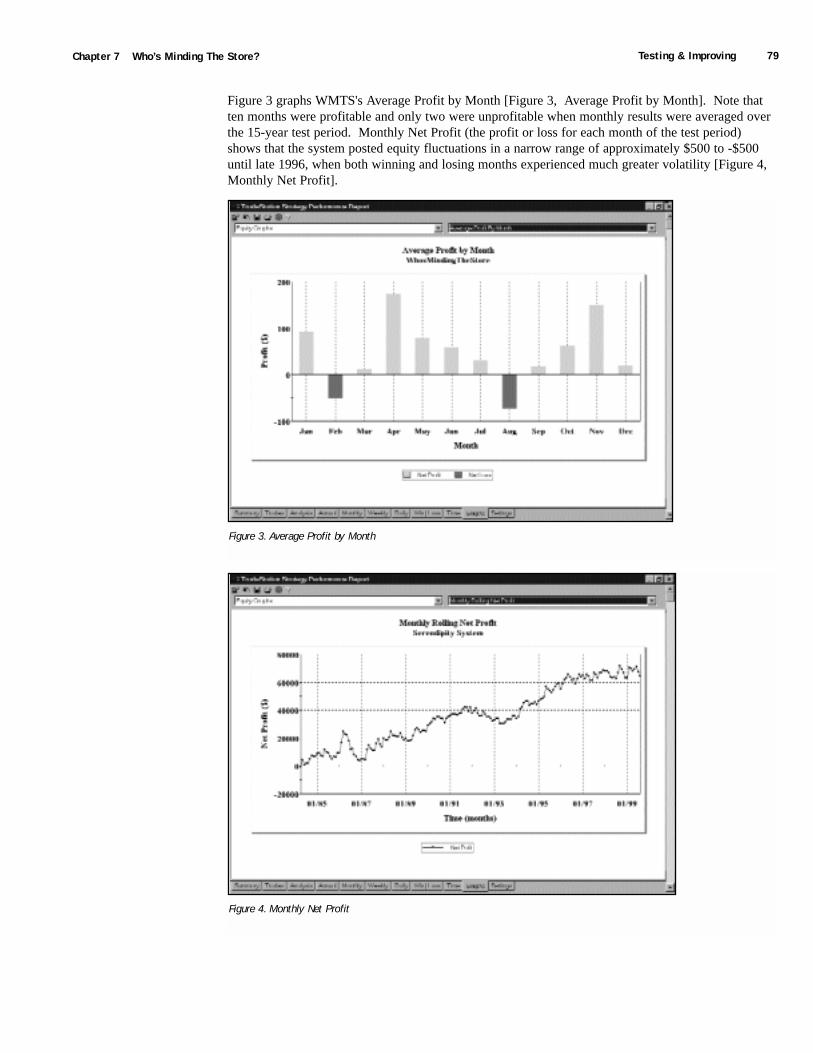

Testing & ImprovingJoe Krutsinger tested Monday We Trade on daily data for the NASDAQ 100 Index from 4/96 to 8/99.No deductions were made for slippage or commission. The total net profit was $107,035 on 167trades. 59% of the trades were profitable. The largest winning trade earned $15,000, while thelargest losing trade lost only $1,300. The average win was 1.68 times the size of the average loss, at$1,827 and -$1,087 respectively. The Profit Factor of 2.45 indicates that MWT gained $2.45 for each$1.00 it lost. Surprisingly (since stocks have been in an historic bull market for several years), thesystem made more money on the short side than on the long side: $45,955 long and $61,080 short.The average long trade earned $468 compared to an average short trade of $885.

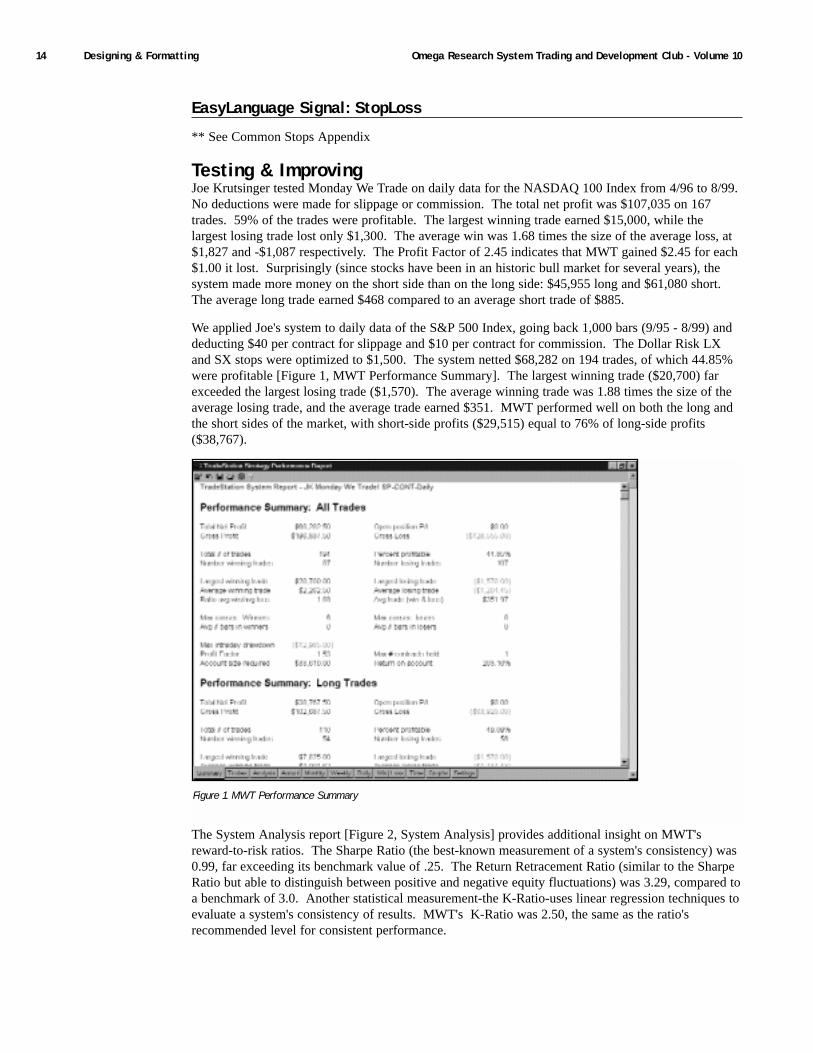

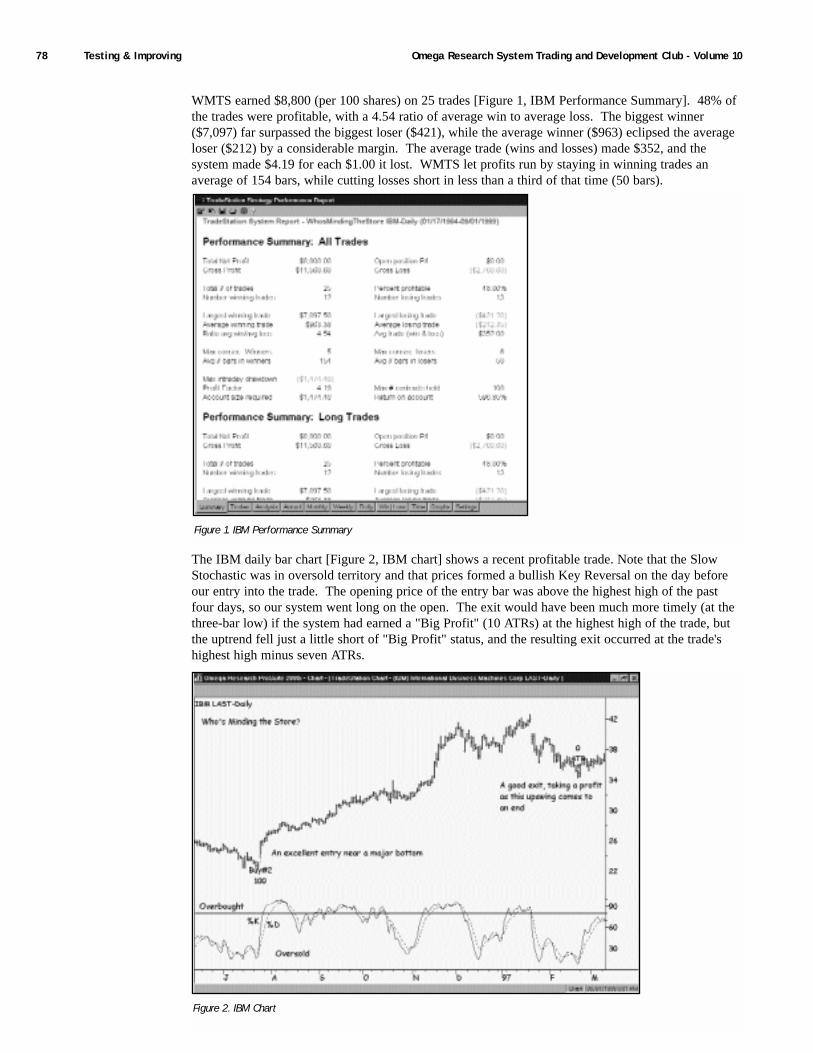

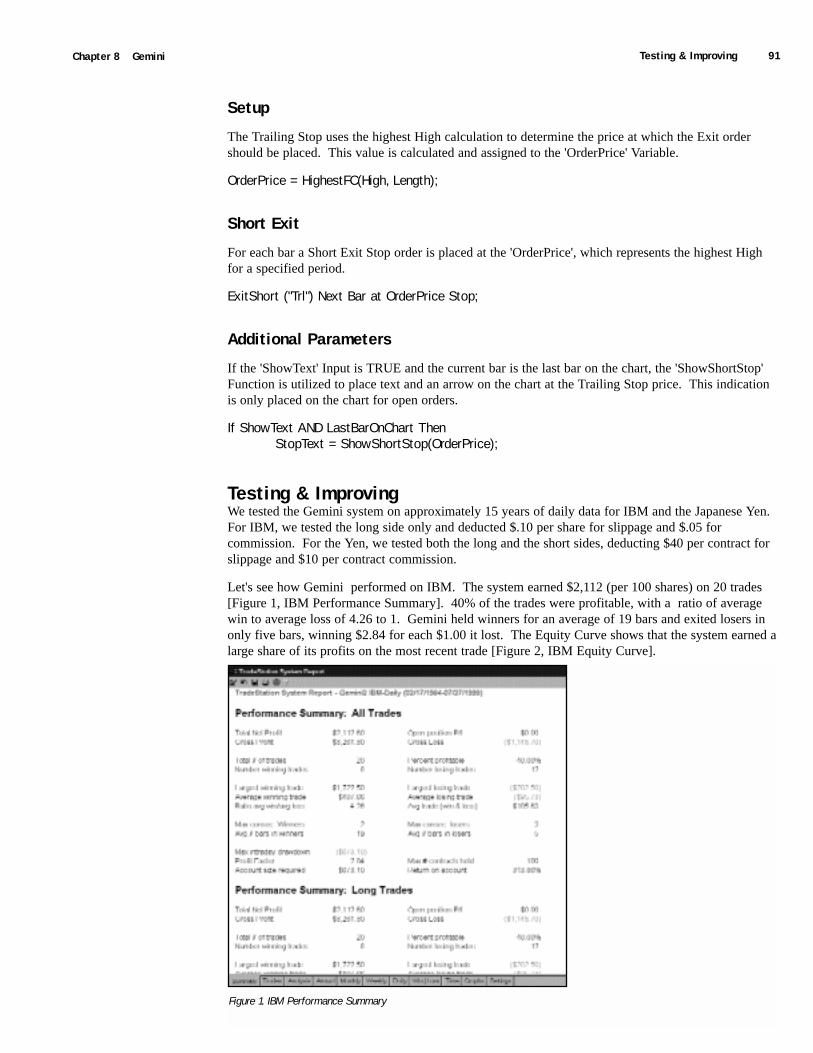

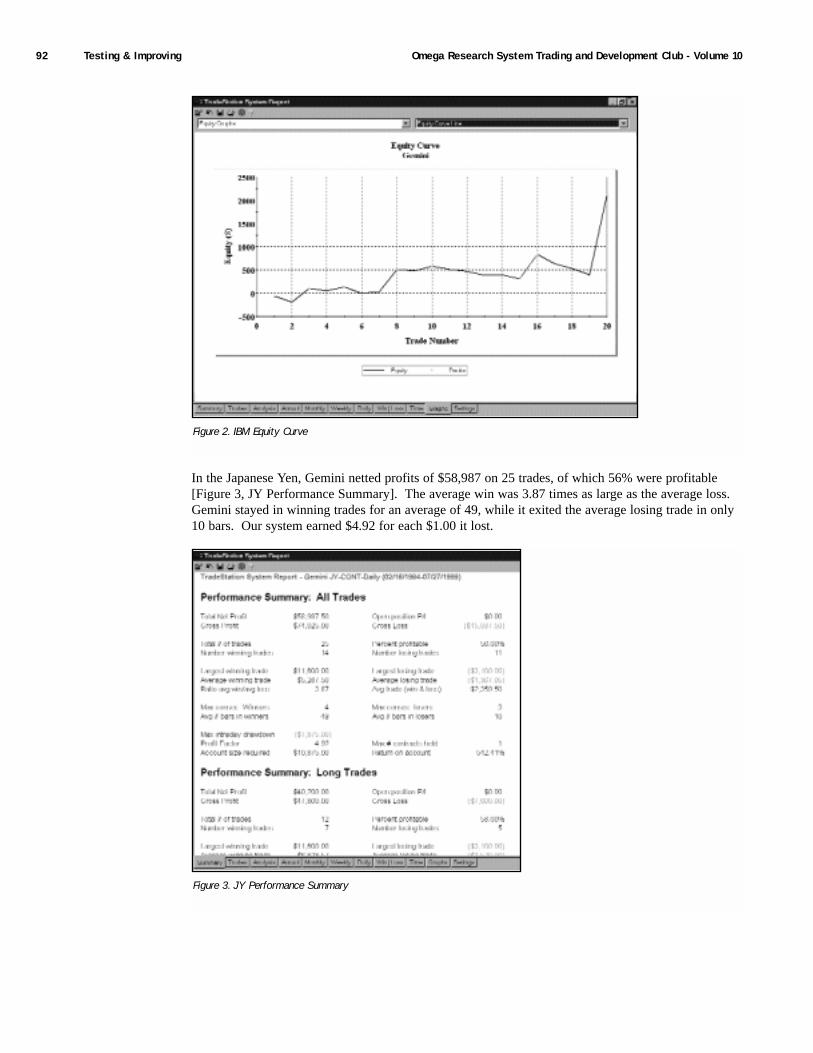

We applied Joe's system to daily data of the S&P 500 Index, going back 1,000 bars (9/95 - 8/99) anddeducting $40 per contract for slippage and $10 per contract for commission. The Dollar Risk LXand SX stops were optimized to $1,500. The system netted $68,282 on 194 trades, of which 44.85%were profitable [Figure 1, MWT Performance Summary]. The largest winning trade ($20,700) farexceeded the largest losing trade ($1,570). The average winning trade was 1.88 times the size of theaverage losing trade, and the average trade earned $351. MWT performed well on both the long andthe short sides of the market, with short-side profits ($29,515) equal to 76% of long-side profits($38,767).

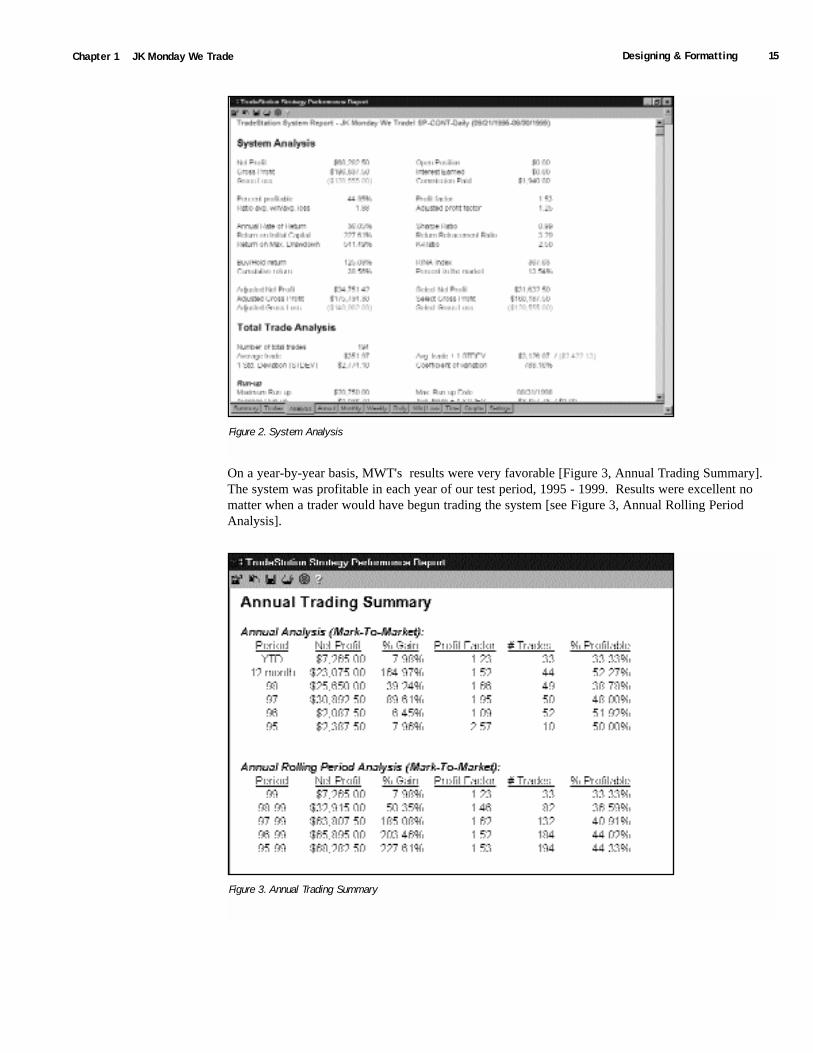

The System Analysis report [Figure 2, System Analysis] provides additional insight on MWT'sreward-to-risk ratios. The Sharpe Ratio (the best-known measurement of a system's consistency) was0.99, far exceeding its benchmark value of .25. The Return Retracement Ratio (similar to the SharpeRatio but able to distinguish between positive and negative equity fluctuations) was 3.29, compared toa benchmark of 3.0. Another statistical measurement-the K-Ratio-uses linear regression techniques toevaluate a system's consistency of results. MWT's K-Ratio was 2.50, the same as the ratio'srecommended level for consistent performance.

Figure 1. MWT Performance Summary

Designing & Formatting 15Chapter 1 JK Monday We Trade

On a year-by-year basis, MWT's results were very favorable [Figure 3, Annual Trading Summary].The system was profitable in each year of our test period, 1995 - 1999. Results were excellent nomatter when a trader would have begun trading the system [see Figure 3, Annual Rolling PeriodAnalysis].

Figure 2. System Analysis

Figure 3. Annual Trading Summary

Omega Research System Trading and Development Club - Volume 1016 Designing & Formatting

The Underwater Equity Curve is a deliberately pessimistic display of a system's performance [Figure4, Underwater Equity Curve]. The vertical axis indicates the percent drawdown the systemexperienced, while the horizontal axis indicates the time in months. The short vertical bars risingabove the 0 line represent new equity highs; obviously, they are not drawn to scale. The mostprominent features of the Underwater Equity Curve are the equity declines between new monthlyequity highs. Unlike the bars that represent the new equity highs, these equity dips are drawn toscale, giving the graph a very negative appearance. The MWT system did have one drawdown ofabout 24%, but its other drawdowns were all less than 14 percent.

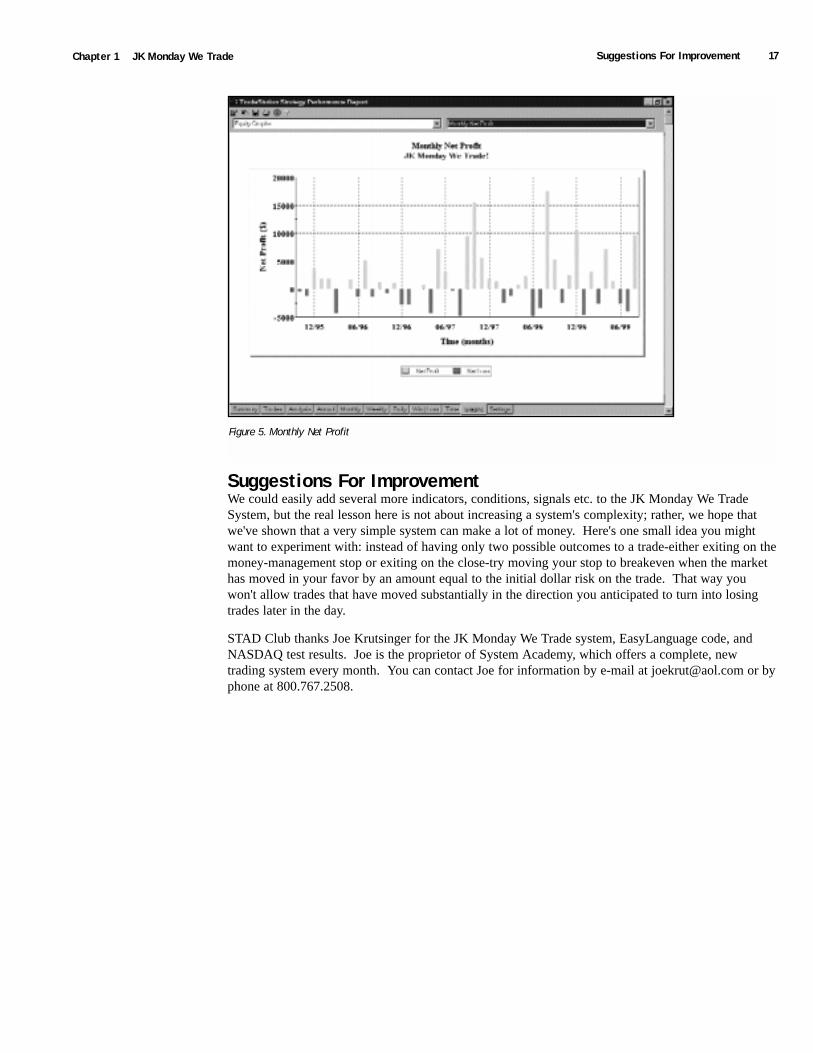

Monthly Net Profit is depicted in Figure 5 [Figure 5, Monthly Net Profit]. Note that there are severalmore winning months than losing months, and that several winning months are larger than any of thelosing months.

Although MWT was designed to trade stock indices, we also tested it on IBM. We tested the longside only on daily data from 1995 to 1999, deducting $.10 per share for slippage and $.05 per sharefor commission. Our optimization returned a money-management stop of $300 (per 100 contractstraded) and an eight-day simple moving average. Here are the test results for each day of the week: ifthe system bought on Tuesdays and exited on the close, it lost $259 over the approximately five-yeartest period; buying on Wednesdays earned $553; buying on Thursdays earned $1,037; buying onFridays earned $1,609; buying on Mondays earned $2,822.

Figure 4. Underwater Equity Curve

Suggestions For Improvement 17Chapter 1 JK Monday We Trade

Suggestions For ImprovementWe could easily add several more indicators, conditions, signals etc. to the JK Monday We TradeSystem, but the real lesson here is not about increasing a system's complexity; rather, we hope thatwe've shown that a very simple system can make a lot of money. Here's one small idea you mightwant to experiment with: instead of having only two possible outcomes to a trade-either exiting on themoney-management stop or exiting on the close-try moving your stop to breakeven when the markethas moved in your favor by an amount equal to the initial dollar risk on the trade. That way youwon't allow trades that have moved substantially in the direction you anticipated to turn into losingtrades later in the day.

STAD Club thanks Joe Krutsinger for the JK Monday We Trade system, EasyLanguage code, andNASDAQ test results. Joe is the proprietor of System Academy, which offers a complete, newtrading system every month. You can contact Joe for information by e-mail at [email protected] or byphone at 800.767.2508.

Figure 5. Monthly Net Profit

Omega Research System Trading and Development Club - Volume 1018

C H A P T E R 2

The Serendipity Entry TriggerBy Chuck LeBeau

Because we prefer to get our trades started in the right direction as soon as possible,we spend a great deal of time experimenting with various setup conditions and entrytriggers. If the setup conditions are favorable, we will often trigger the entry on the

long side of our trades based on an upward excursion from the opening price. We find thatmeasuring favorable movement from the opening price rather than from the previous closetends to produce reliable entry signals that offer a high probability of success. This particu-lar method of getting new trades started in the right direction is one of our personalfavorites, and it has been used as the entry trigger in several of our systems.

Late one evening, while testing entry triggers on a new system, we inadvertently coded the entryso that we would enter TOMORROW based on a specified price excursion from TODAY'SOPEN. We had originally intended to have the system enter tomorrow as the price movedupward from tomorrow's open. However, the miscoded entry that was based on today's openworked much better than we expected, and it substantially out-performed our intended entrytrigger. Our initial reaction to the outstanding test results was one of skepticism, and we naturallyassumed that this entry trigger might have been a mere fluke. We feared that perhaps we hadsimply stumbled into an accidental curve fit. However, when we tested this entry method onother systems and with other setup conditions, it continued to perform admirably. Because ourdiscovery of this entry method was quite accidental, we named it the Serendipity Entry Trigger,and we immediately began to investigate to see if there was any logic behind the entry that mightexplain why it seemed to work so well in our tests.

After carefully studying the patterns of the Serendipity Entry Trigger, we concluded that it isparticularly effective because it is based on two days of cumulative price movement rather thanthe typical one day or less of price movement that we would normally measure.

For the sake of this discussion, let's assume that our specific entry trigger is to buy the bondsTOMORROW on a stop that is 20/32nds above TODAY'S OPEN. Now, if we look carefully atthe relationship of today's close relative to today's open, it helps us to better understand what willbe required tomorrow to trigger an effective entry signal. If today is a strong day with a closethat is well above the opening, then we will be able to enter quickly tomorrow on just a smallamount of favorable price movement. In fact, if the close today is 20 or more points above theopening today, then we are very likely to be stopped into our new trade immediately ontomorrow's opening.

20 The Serendipity Entry Trigger Omega Research System Trading and Development Club - Volume 10

In our opinion, the Serendipity Entry Trigger works so well because it is almost like adding anelement of hindsight into the entry process. The precise sequence of price action on the setup daybecomes an important part of the final trigger mechanism.

We could, of course, simply require that the setup day be a strong day as a pre-entry condition.However, the Serendipity Trigger is more adaptive and robust than a setup condition because it isflexible enough to occasionally permit an entry even though the setup day is weak. A weak setup daycan occasionally be followed by an abnormally strong entry day, and the Serendipity Trigger wouldstill allow us to enter on this strength. If we were to use a more conventional entry trigger and makea strong setup day a pre-entry condition, there would be no entry signal on the following day even ifthe market showed remarkable strength.

The Serendipity Trigger offers an important operational advantage as well as contributing to improvedtiming. When using the conventional trigger that is based on tomorrow's opening price, our exactentry point cannot be calculated until after the opening trade has been posted. However, one of thebenefits of the Serendipity Trigger is that the exact entry order is available the day prior to the entry,and our stop order can be placed prior to the opening.

Conventional Entry Code

Buy("Long Entry") Open Tomorrow + 20 points stop;

Sell("Short Entry") Open Tomorrow - 20 points stop;

Serendipity Entry Code

Buy("Long Entry") Open + 20 points stop;

Sell("Short Entry") Open - 20 points stop;

Chuck LeBeau is the co-author of the highly regarded book, Computer Analysis of the FuturesMarket. He is also the proprietor of Chuck LeBeau's System Traders Club. The club's website addressis www.traderclub.com. You can contact Chuck by e-mail at [email protected].

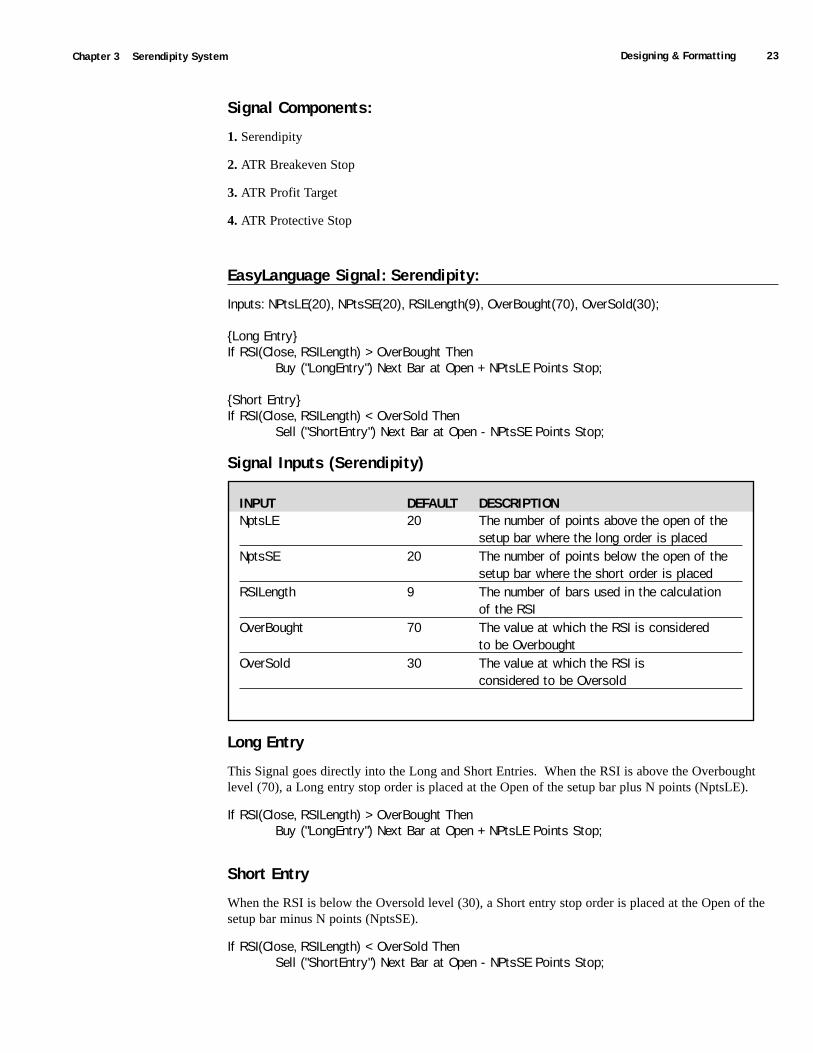

C H A P T E R 3

Serendipity System

Our Serendipity System begins with Chuck LeBeau's Serendipity entry trigger thenadds a momentum indicator, a protective stop, a breakeven stop, and a profit targetto complete the system.

Although the Relative Strength Index (RSI) is usually used to identify overbought and oversoldconditions, we use it as our trend indicator in Serendipity. When RSI climbs to 70 or higher, themarket is strong, and we get ready to buy; when RSI falls to 30 or lower, the market is weak, andwe get ready to sell short.

With a bullish RSI setup in place, we go long at the open plus n points. When a bearish RSIsetup is in effect, we sell short at the open minus n points. The unusual aspect of this system isthat we are referring to the open of the day before the entry bar, not the open of the entry bar (seethe Serendipity entry trigger, Chapter 2 in this volume).

Upon entering a new long position, we place a protective stop at our entry price minus a multipleof the Average True Range (ATR). When the market moves in our favor by n ATRs, we raise ourstop to breakeven and place an order to take profits at a target that is also calculated as a multipleof the ATR. For a new short position, we set our protective stop at the entry price plus a multipleof the ATR. When the market moves in our favor by n ATRs, we lower our stop to breakevenand place an order to take profits at a target n ATRs below our entry price.

22 Defining Our Trading Rules Omega Research System Trading and Development Club - Volume 10

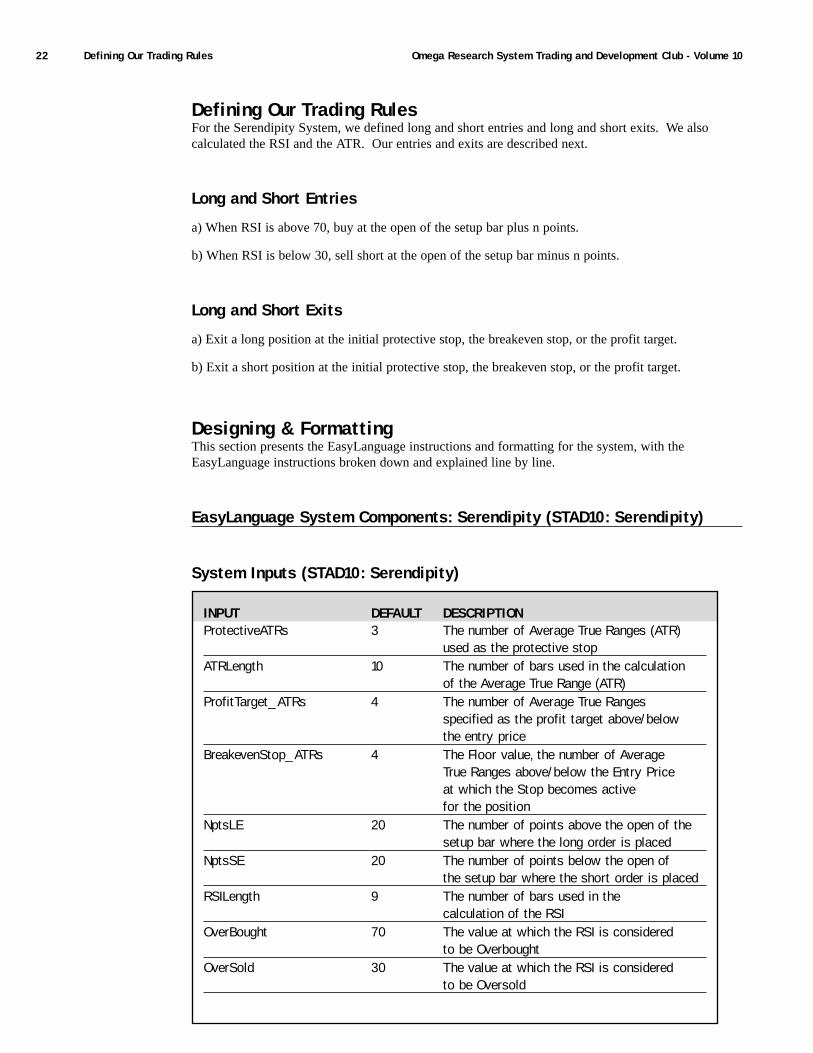

Defining Our Trading RulesFor the Serendipity System, we defined long and short entries and long and short exits. We alsocalculated the RSI and the ATR. Our entries and exits are described next.

Long and Short Entries

a) When RSI is above 70, buy at the open of the setup bar plus n points.

b) When RSI is below 30, sell short at the open of the setup bar minus n points.

Long and Short Exits

a) Exit a long position at the initial protective stop, the breakeven stop, or the profit target.

b) Exit a short position at the initial protective stop, the breakeven stop, or the profit target.

Designing & FormattingThis section presents the EasyLanguage instructions and formatting for the system, with theEasyLanguage instructions broken down and explained line by line.

EasyLanguage System Components: Serendipity (STAD10: Serendipity)

System Inputs (STAD10: Serendipity)

INPUT DEFAULT DESCRIPTIONProtectiveATRs 3 The number of Average True Ranges (ATR)

used as the protective stopATRLength 10 The number of bars used in the calculation

of the Average True Range (ATR)ProfitTarget_ATRs 4 The number of Average True Ranges

specified as the profit target above/belowthe entry price

BreakevenStop_ATRs 4 The Floor value, the number of AverageTrue Ranges above/below the Entry Priceat which the Stop becomes activefor the position

NptsLE 20 The number of points above the open of the setup bar where the long order is placed

NptsSE 20 The number of points below the open ofthe setup bar where the short order is placed

RSILength 9 The number of bars used in thecalculation of the RSI

OverBought 70 The value at which the RSI is consideredto be Overbought

OverSold 30 The value at which the RSI is consideredto be Oversold

Designing & Formatting 23Chapter 3 Serendipity System

Signal Components:

1. Serendipity

2. ATR Breakeven Stop

3. ATR Profit Target

4. ATR Protective Stop

EasyLanguage Signal: Serendipity:

Inputs: NPtsLE(20), NPtsSE(20), RSILength(9), OverBought(70), OverSold(30);

{Long Entry}If RSI(Close, RSILength) > OverBought Then

Buy ("LongEntry") Next Bar at Open + NPtsLE Points Stop;

{Short Entry}If RSI(Close, RSILength) < OverSold Then

Sell ("ShortEntry") Next Bar at Open - NPtsSE Points Stop;

Signal Inputs (Serendipity)

Long Entry

This Signal goes directly into the Long and Short Entries. When the RSI is above the Overboughtlevel (70), a Long entry stop order is placed at the Open of the setup bar plus N points (NptsLE).

If RSI(Close, RSILength) > OverBought ThenBuy ("LongEntry") Next Bar at Open + NPtsLE Points Stop;

Short Entry

When the RSI is below the Oversold level (30), a Short entry stop order is placed at the Open of thesetup bar minus N points (NptsSE).

If RSI(Close, RSILength) < OverSold ThenSell ("ShortEntry") Next Bar at Open - NPtsSE Points Stop;

INPUT DEFAULT DESCRIPTIONNptsLE 20 The number of points above the open of the

setup bar where the long order is placedNptsSE 20 The number of points below the open of the

setup bar where the short order is placedRSILength 9 The number of bars used in the calculation

of the RSIOverBought 70 The value at which the RSI is considered

to be OverboughtOverSold 30 The value at which the RSI is

considered to be Oversold

24 Designing & Formatting Omega Research System Trading and Development Club - Volume 10

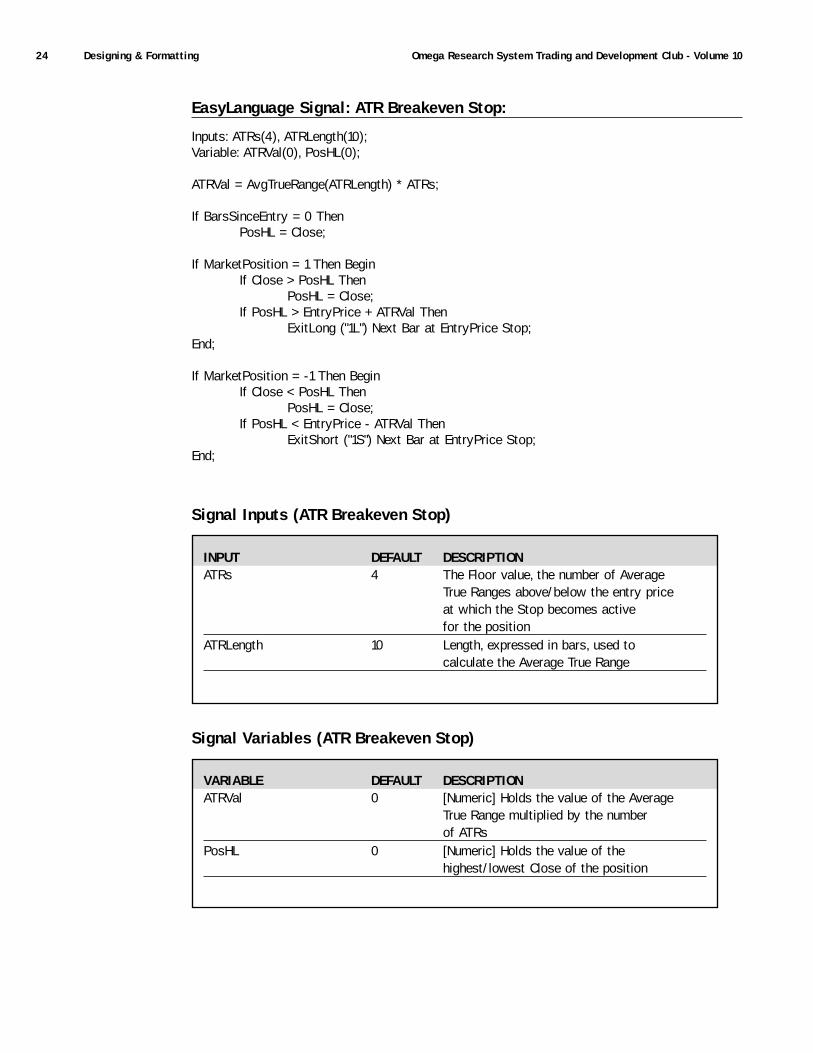

EasyLanguage Signal: ATR Breakeven Stop:

Inputs: ATRs(4), ATRLength(10);Variable: ATRVal(0), PosHL(0);

ATRVal = AvgTrueRange(ATRLength) * ATRs;

If BarsSinceEntry = 0 ThenPosHL = Close;

If MarketPosition = 1 Then BeginIf Close > PosHL Then

PosHL = Close;If PosHL > EntryPrice + ATRVal Then

ExitLong ("1L") Next Bar at EntryPrice Stop;End;

If MarketPosition = -1 Then BeginIf Close < PosHL Then

PosHL = Close;If PosHL < EntryPrice - ATRVal Then

ExitShort ("1S") Next Bar at EntryPrice Stop;End;

Signal Inputs (ATR Breakeven Stop)

Signal Variables (ATR Breakeven Stop)

INPUT DEFAULT DESCRIPTIONATRs 4 The Floor value, the number of Average

True Ranges above/below the entry priceat which the Stop becomes activefor the position

ATRLength 10 Length, expressed in bars, used tocalculate the Average True Range

VARIABLE DEFAULT DESCRIPTIONATRVal 0 [Numeric] Holds the value of the Average

True Range multiplied by the numberof ATRs

PosHL 0 [Numeric] Holds the value of thehighest/lowest Close of the position

Designing & Formatting 25Chapter 3 Serendipity System

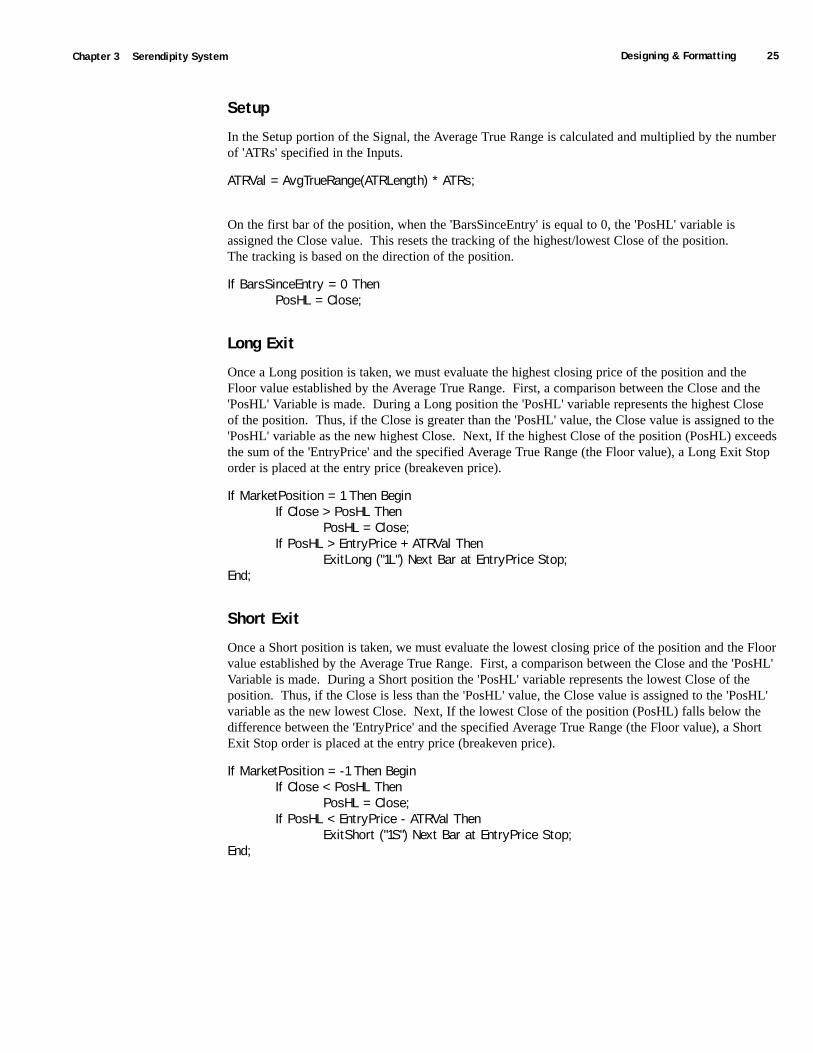

Setup

In the Setup portion of the Signal, the Average True Range is calculated and multiplied by the numberof 'ATRs' specified in the Inputs.

ATRVal = AvgTrueRange(ATRLength) * ATRs;

On the first bar of the position, when the 'BarsSinceEntry' is equal to 0, the 'PosHL' variable isassigned the Close value. This resets the tracking of the highest/lowest Close of the position.The tracking is based on the direction of the position.

If BarsSinceEntry = 0 ThenPosHL = Close;

Long Exit

Once a Long position is taken, we must evaluate the highest closing price of the position and theFloor value established by the Average True Range. First, a comparison between the Close and the'PosHL' Variable is made. During a Long position the 'PosHL' variable represents the highest Closeof the position. Thus, if the Close is greater than the 'PosHL' value, the Close value is assigned to the'PosHL' variable as the new highest Close. Next, If the highest Close of the position (PosHL) exceedsthe sum of the 'EntryPrice' and the specified Average True Range (the Floor value), a Long Exit Stoporder is placed at the entry price (breakeven price).

If MarketPosition = 1 Then BeginIf Close > PosHL Then

PosHL = Close;If PosHL > EntryPrice + ATRVal Then

ExitLong ("1L") Next Bar at EntryPrice Stop;End;

Short Exit

Once a Short position is taken, we must evaluate the lowest closing price of the position and the Floorvalue established by the Average True Range. First, a comparison between the Close and the 'PosHL'Variable is made. During a Short position the 'PosHL' variable represents the lowest Close of theposition. Thus, if the Close is less than the 'PosHL' value, the Close value is assigned to the 'PosHL'variable as the new lowest Close. Next, If the lowest Close of the position (PosHL) falls below thedifference between the 'EntryPrice' and the specified Average True Range (the Floor value), a ShortExit Stop order is placed at the entry price (breakeven price).

If MarketPosition = -1 Then BeginIf Close < PosHL Then

PosHL = Close;If PosHL < EntryPrice - ATRVal Then

ExitShort ("1S") Next Bar at EntryPrice Stop;End;

26 Designing & Formatting Omega Research System Trading and Development Club - Volume 10

EasyLanguage Signal: ATR Profit Target:

Inputs: ATRs(4), ATRLength(10);Variable: ATRVal(0), EntryATR(0);

ATRVal = AvgTrueRange(ATRLength) * ATRs;

If BarsSinceEntry = 0 ThenEntryATR = ATRVal;

If MarketPosition = 1 ThenExitLong ("2L") Next Bar at EntryPrice + EntryATR Limit;

If MarketPosition = -1 ThenExitShort ("2S") Next Bar at EntryPrice - EntryATR Limit;

If LastBarOnChart Then Beginvalue1 = ShowLongStop(EntryPrice + EntryATR);value1 = ShowShortStop(EntryPrice - EntryATR);

End;

Signal Inputs (ATR Profit Target)

Signal Variables (ATR Profit Target)

INPUT DEFAULT DESCRIPTIONATRs 4 The number of Average True Ranges

specified as the profit target above/belowthe entry price

ATRLength 10 Length, expressed in bars, used tocalculate the Average True Range

VARIABLE DEFAULT DESCRIPTIONATRVal 0 [Numeric] Holds the value of the Average

True Range multiplied by the numberof ATRs

EntryATR 0 [Numeric] Holds the value of the AverageTrue Range on the first bar of the position

Designing & Formatting 27Chapter 3 Serendipity System

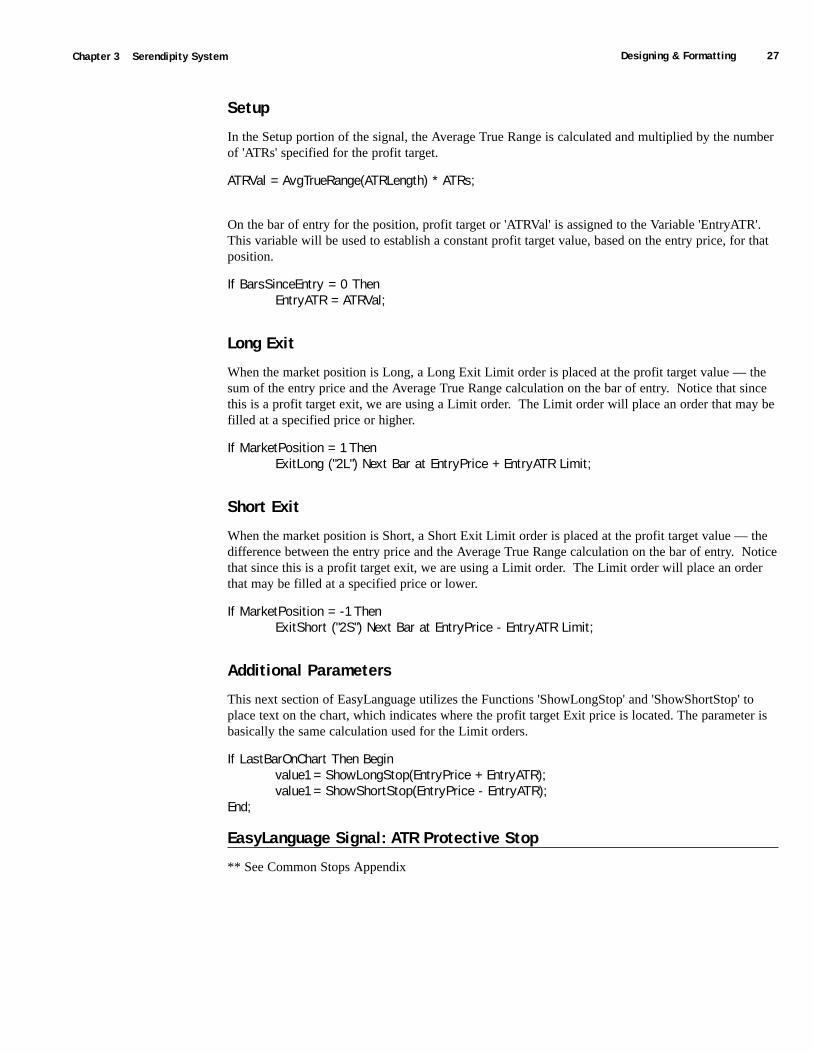

Setup

In the Setup portion of the signal, the Average True Range is calculated and multiplied by the numberof 'ATRs' specified for the profit target.

ATRVal = AvgTrueRange(ATRLength) * ATRs;

On the bar of entry for the position, profit target or 'ATRVal' is assigned to the Variable 'EntryATR'.This variable will be used to establish a constant profit target value, based on the entry price, for thatposition.

If BarsSinceEntry = 0 ThenEntryATR = ATRVal;

Long Exit

When the market position is Long, a Long Exit Limit order is placed at the profit target value — thesum of the entry price and the Average True Range calculation on the bar of entry. Notice that sincethis is a profit target exit, we are using a Limit order. The Limit order will place an order that may befilled at a specified price or higher.

If MarketPosition = 1 ThenExitLong ("2L") Next Bar at EntryPrice + EntryATR Limit;

Short Exit

When the market position is Short, a Short Exit Limit order is placed at the profit target value — thedifference between the entry price and the Average True Range calculation on the bar of entry. Noticethat since this is a profit target exit, we are using a Limit order. The Limit order will place an orderthat may be filled at a specified price or lower.

If MarketPosition = -1 ThenExitShort ("2S") Next Bar at EntryPrice - EntryATR Limit;

Additional Parameters

This next section of EasyLanguage utilizes the Functions 'ShowLongStop' and 'ShowShortStop' toplace text on the chart, which indicates where the profit target Exit price is located. The parameter isbasically the same calculation used for the Limit orders.

If LastBarOnChart Then Beginvalue1 = ShowLongStop(EntryPrice + EntryATR);value1 = ShowShortStop(EntryPrice - EntryATR);

End;

EasyLanguage Signal: ATR Protective Stop

** See Common Stops Appendix

28 Testing & Improving Omega Research System Trading and Development Club - Volume 10

Testing & Improving

We tested Serendipity on approximately 15 years of daily data for US Treasury Bonds, deducting $40per contract for slippage and $10 per contract for commission.

Let's see how Serendipity fared on the Bonds. The optimized values are as follows:

ATR Protective Stop (ProtectiveATRs) = 2

ATR Length (ATRLength) = 10

ATR Profit Target (ProfitTarget_ATRs) = 8

ATR Breakeven Stop (BreakevenStop_ATRs) = 5

NptsLE = 20

NptsSE = 5

RSI Length = 11

Overbought = 60

Oversold = 35

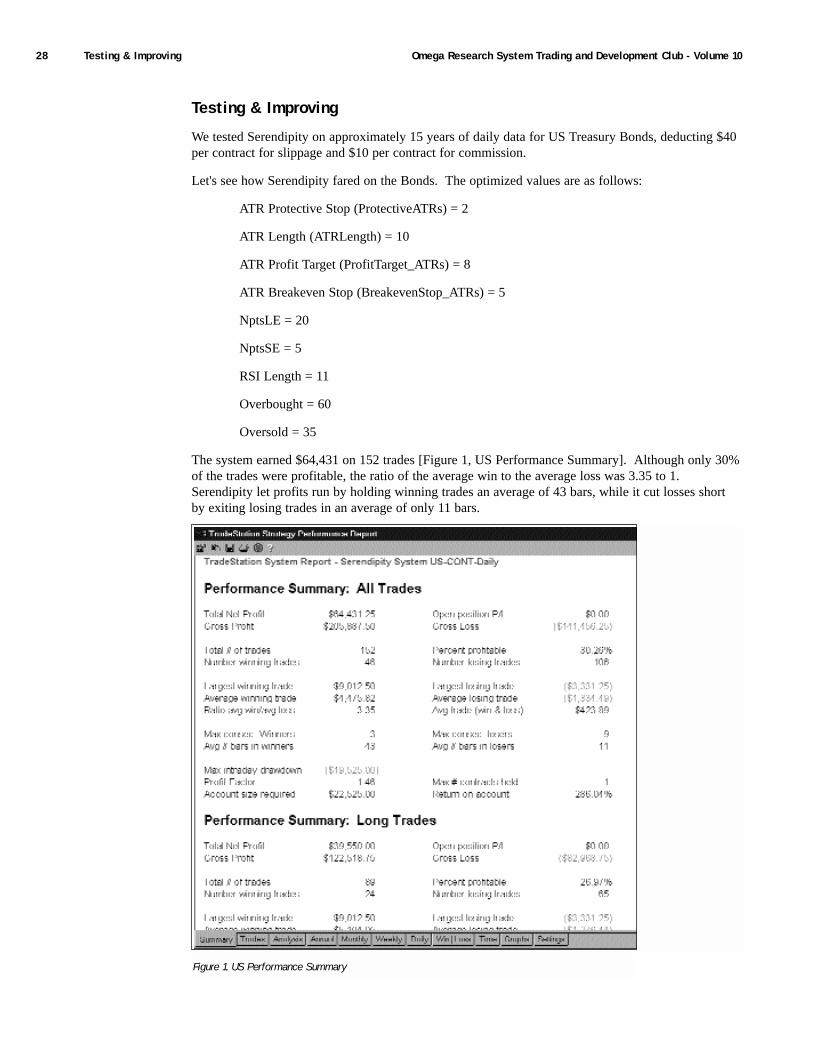

The system earned $64,431 on 152 trades [Figure 1, US Performance Summary]. Although only 30%of the trades were profitable, the ratio of the average win to the average loss was 3.35 to 1.Serendipity let profits run by holding winning trades an average of 43 bars, while it cut losses shortby exiting losing trades in an average of only 11 bars.

Figure 1. US Performance Summary

Testing & Improving 29Chapter 3 Serendipity System

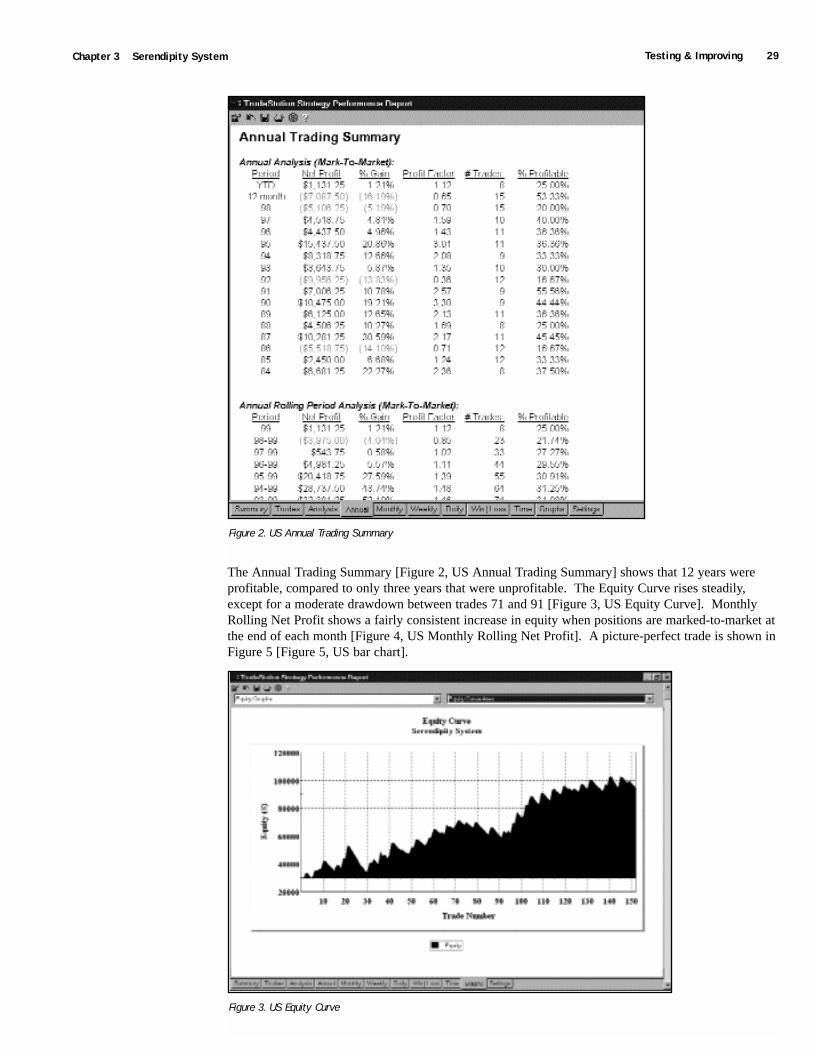

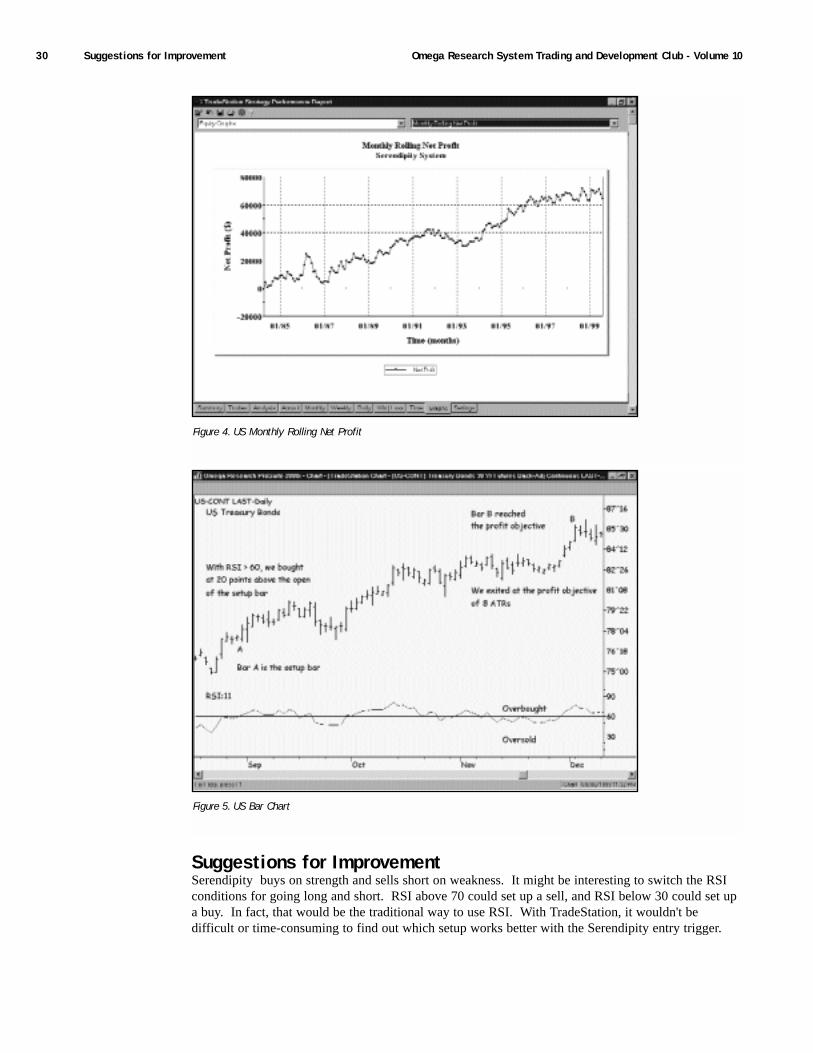

The Annual Trading Summary [Figure 2, US Annual Trading Summary] shows that 12 years wereprofitable, compared to only three years that were unprofitable. The Equity Curve rises steadily,except for a moderate drawdown between trades 71 and 91 [Figure 3, US Equity Curve]. MonthlyRolling Net Profit shows a fairly consistent increase in equity when positions are marked-to-market atthe end of each month [Figure 4, US Monthly Rolling Net Profit]. A picture-perfect trade is shown inFigure 5 [Figure 5, US bar chart].

Figure 2. US Annual Trading Summary

Figure 3. US Equity Curve

30 Suggestions for Improvement Omega Research System Trading and Development Club - Volume 10

Suggestions for ImprovementSerendipity buys on strength and sells short on weakness. It might be interesting to switch the RSIconditions for going long and short. RSI above 70 could set up a sell, and RSI below 30 could set upa buy. In fact, that would be the traditional way to use RSI. With TradeStation, it wouldn't bedifficult or time-consuming to find out which setup works better with the Serendipity entry trigger.

Figure 4. US Monthly Rolling Net Profit

Figure 5. US Bar Chart

C H A P T E R 4

Eight Ball

The Eight-Ball system employs two exponential moving averages, a volatility trigger,and four stops. The moving averages identify the long-term and short-term trends.The volatility trigger looks for a strong move off the opening price in the direction of

the anticipated trade. The four stops limit our initial risk, lock in profits, limit our exposurewhen volatility increases suddenly, and maximize our gains when we catch a powerful trend.We named the system Eight Ball simply because eight bars was frequently the best value forthe length of the short-term moving average in our preliminary testing and optimizing.

A maxim of technical analysis is that prices move in trends (up, down, or sideways), and thattrends are more likely to continue than to reverse. Analyzing a chart can be tricky, however,because trends of various lengths are always present on the same chart. In Eight Ball, wedetermine the long-term and short-term trends by averaging closing prices over two lengths ofdata and defining the trend as the current direction or slope of the averages. The system's defaultvalues are a long-term moving average of 40 bars and a short-term moving average of eight bars.To set up an entry, both averages must be pointing in the same direction. The actual entry occurswhen a market moves off its opening price by a specified multiple of its Average True Range(ATR). (An ATR is the largest of the following: today's high minus today's low, yesterday's closeminus today's low, or today's high minus yesterday's close.) This system's default values are a10-bar ATR and an entry trigger of one. Therefore, if both moving averages are rising, and themarket climbs one 10-bar ATR above its open, we go long; if both moving averages are falling,and the market drops one 10-bar ATR below its open, we go short.

Once we've entered a new position, we need to place an initial protective stop. The stop is set atthe entry price minus a multiple of the ATR for a long position and at the entry price plus amultiple of the ATR for a short position. This system's default value for the initial protective stopis 3: we'll exit a long position if the market falls to our entry price minus three ATRs; we'll exit ashort position if the market rallies to our entry price plus three ATRs.

The second stop in the Eight-Ball system is the ATR trailing stop, which has a default value offive ATRs. If we're in a long position, we'll set the trailing stop at the highest high since ourentry into the trade minus five ATRs; if we're in a short position, we'll set the stop at the lowestlow since our entry into the trade plus five ATRs.

32 Defining Our Trading Rules Omega Research System Trading and Development Club - Volume 10

The Eight-Ball system's third stop is a volatility stop with a default value of three. Our volatility stopis set at the previous day's closing price minus three ATRs for a long position and plus three ATRs fora short position. It's generally wise to exit a position when a market is moving against us withexpanding volatility. In this system, we define expanding volatility as a move three ATRs below theprevious day's close if we're long and three ATRs above the previous day's close if we're short.

The fourth stop in the Eight-Ball system is the "big profit" stop. When our open profits in a trade aregreater than or equal to a specified number of ATRs, we'll tighten our stop to make sure that we keepa larger than usual portion of the profits. The "big profit" default value in this system is 10 ATRs: ifwe're long, and the close is greater than or equal to our entry price plus 10 ATRs, we'll raise our stopto the four-bar low; if we're short, and the close is less than or equal to our entry price minus 10ATRs, we'll lower our stop to the four-bar high.

Defining Our Trading RulesFor the Eight-Ball system, we defined long and short entries and exits. We also calculated twoexponential moving averages and the Average True Range. The entries and exits are described next.

Long and Short Entries

a) If the long-term and short-term moving averages are both greater than on the previous bar, buy attomorrow's open plus the entry trigger.

b) If the long-term and short-term moving averages are both less than on the previous bar, sell short attomorrow's open minus the entry trigger.

Long and Short Exits

a) Exit a long position at the initial protective stop, the trailing stop, the volatility stop, or the big-profit stop.

b) Exit a short position at the initial protective stop, the trailing stop, the volatility stop, or the big-profit stop.

Designing & FormattingThis section presents the EasyLanguage instructions and formatting for the system, with theEasyLanguage instructions broken down and explained line by line.

Designing & Formatting 33Chapter 4 Eight Ball

EasyLanguage System Components: Eight Ball (STAD10: Eight Ball)

System Inputs (STAD10: Eight Ball)

Signal Components:

1. Eight Ball

2. ATR Big Profit Stop

3. ATR Protective Stop

4. ATR Trailing Stop

5. ATR Volatility Stop

EasyLanguage Signal: Eight Ball:

Inputs: Length1(40), Length2(8), Trigger(1); Variables: ATR(0), Avg1(0), Avg2(0);

ATR = AvgTrueRange(10);SlowAvg = XAverage(Close, Length1);FastAvg = XAverage(Close, Length2);

INPUT DEFAULT DESCRIPTIONVolatilityATRs 2 The number of Average True Ranges (ATR)

used in the Volatility StopATRLength 10 The number of bars used to calculate the

Average True Range (ATR)TrailingATRs 4 The number of Average True Ranges (ATR)

used as the Trailing StopProtectiveATRs 3 The number of Average True Ranges (ATR)

used as the protective stopBigProfitATRs 7 The number of Average True Ranges (ATR)

that indicate a "Big Profit"BigProfit_ExitBarLen 3 The number of bars used in the calculation of

the highest and lowest for the BigProfit exitSlowLen 40 The number of bars used to calculate the

Slow Exponential Moving AverageFastLen 8 The number of bars used to calculate the Fast

Exponential Moving AverageTrigger 1 The number of Average True Ranges

above/below the open of the next bar at which the order will be placed

34 Designing & Formatting Omega Research System Trading and Development Club - Volume 10

Condition1 = SlowAvg > SlowAvg[1] AND FastAvg < FastAvg[1];Condition2 = SlowAvg < SlowAvg[1] AND FastAvg > FastAvg[1];

{Long Entry}If Condition1 Then

Buy ("Long Entry") Next Bar at Open Tomorrow + Trigger * ATR Stop;{Short Entry}If Condition2 Then

Sell ("Short Entry") Next Bar at Open Tomorrow - Trigger * ATR Stop;

Signal Inputs (Eight Ball)

Signal Variables (Eight Ball)

Setup

In the first part of the setup, the most commonly used values are assigned to variables. These valuesinclude the Average True Range (ATR), as well as the Slow and Fast Moving Averages (Avg1 &Avg2).

ATR = AvgTrueRange(10);SlowAvg = XAverage(Close, Length1);FastAvg = XAverage(Close, Length2);

INPUT DEFAULT DESCRIPTIONSlowLen 40 The number of bars used to calculate the

Slow Exponential Moving AverageFastLen 8 The number of bars used to calculate the

Fast Exponential Moving AverageTrigger 1 The number of Average True Ranges

above/below the Open of the next bar at which th order will be placed

VARIABLE DEFAULT DESCRIPTIONATR 0 [Numeric] The calculation of the Average

True RangeSlowAvg 0 [Numeric] The value of the Slow

Moving AverageFastAvg 0 [True/False] The value of the

Fast Moving Average

Designing & Formatting 35Chapter 4 Eight Ball

Once the variables have been initialized, Condition1 and Condition2 are used to identify the primaryconditions of the Signal. If the value of SlowAvg is greater than on the previous bar, and the value ofFastAvg is less than on the previous bar, Condition1 is true. If the value of SlowAvg is less than onthe previous bar, and the value of FastAvg is greater than on the previous bar, Condition2 is true.

Condition1 = SlowAvg > SlowAvg[1] AND FastAvg < FastAvg[1];Condition2 = SlowAvg < SlowAvg[1] AND FastAvg > FastAvg[1];

Long Entry

If Condition1 is true, based on the criteria specified above, a Long entry stop order is placed at theOpen of the next bar, plus the product of ‘Trigger’ and a factor of the Average True Range (ATR).

If Condition1 ThenBuy ("Long Entry") Next Bar at Open Tomorrow + Trigger * ATR Stop;

Short Entry

If Condition2 is true, based on the criteria specified above, a Short entry stop order is placed at theOpen of the next bar, minus the product of ‘Trigger’ and a factor of the Average True Range (ATR).

If Condition2 ThenSell ("Short Entry") Next Bar at Open Tomorrow - Trigger * ATR Stop;

EasyLanguage Signal: ATR Volatility Stop:

Inputs: VolatilityATRs(2), ATRLength(10);Variable: ATRVal(0);

ATRVal = AvgTrueRange(ATRLength) * VolatilityATRs;

If MarketPosition = 1 ThenExitLong Next Bar at EntryPrice - ATRVal Stop;

If MarketPosition = -1 ThenExitShort Next Bar at EntryPrice + ATRVal Stop;

Signal Inputs (ATR Volatility Stop)

INPUT DEFAULT DESCRIPTIONVolatilityATRs 2 The number of Average True Ranges that are

used to determine the required volatility to place an Exit order

ATRLength 10 Length, expressed in bars, used to calculate the Average True Range

36 Designing & Formatting Omega Research System Trading and Development Club - Volume 10

Signal Variables (ATR Volatility Stop)

Setup

In the setup portion of this signal, the Average True Range is calculated and multiplied by the numberof VolatilityATRs specified in the Inputs.

ATRVal = AvgTrueRange(ATRLength) * VolatilityATRs;

Long Exit

When the market position is Long, a Long Exit is placed at the entry price minus the VolatilityAverage True Range calculation (ATRVal)

If MarketPosition = 1 ThenExitLong Next Bar at EntryPrice - ATRVal Stop;

Short Exit

When the market position is Short, a Short Exit is placed at the entry price plus the Volatility AverageTrue Range calculation (ATRVal).

If MarketPosition = -1 ThenExitShort Next Bar at EntryPrice + ATRVal Stop;

EasyLanguage Signal: ATR Big Profit Stop

** See Common Stops Appendix

EasyLanguage Signal: ATR Trailing Stop

** See Common Stops Appendix

EasyLanguage Signal: ATR Protective Stop

** See Common Stops Appendix

VARIABLE DEFAULT DESCRIPTIONATRVal 0 [Numeric] Holds the value of the Average True

Range multiplied by the number ofVolatility ATRs

Testing & Improving 37Chapter 4 Eight Ball

Testing & ImprovingWe tested the Eight-Ball system on approximately 15 years of daily data for IBM, Bonds, and theSwiss Franc. On IBM, we tested the long side only and deducted $.10 per share for slippage and $.05per share for commission. On Bonds and the Swiss Franc, we tested both the long and short sides,deducting $40 per contract for slippage and $10 per contract for commission.

Here are the optimized values for IBM:

Volatility Stop (VolatilityATRs) = 2

ATR Length (ATRLength) = 10

ATR Trailing Stop (TrailingATRs) = 4

Initial Protective Stop (ProtectiveATRs) = 2

Big Profit Stop (BigProfitATRs) = 10

N bar Stop (BigProfit_ExitBarLen) = 3

Moving Average Slow (SlowLen) = 30

Moving Average Fast (FastLen) = 10

Volatility Trigger (Trigger) = 1.5

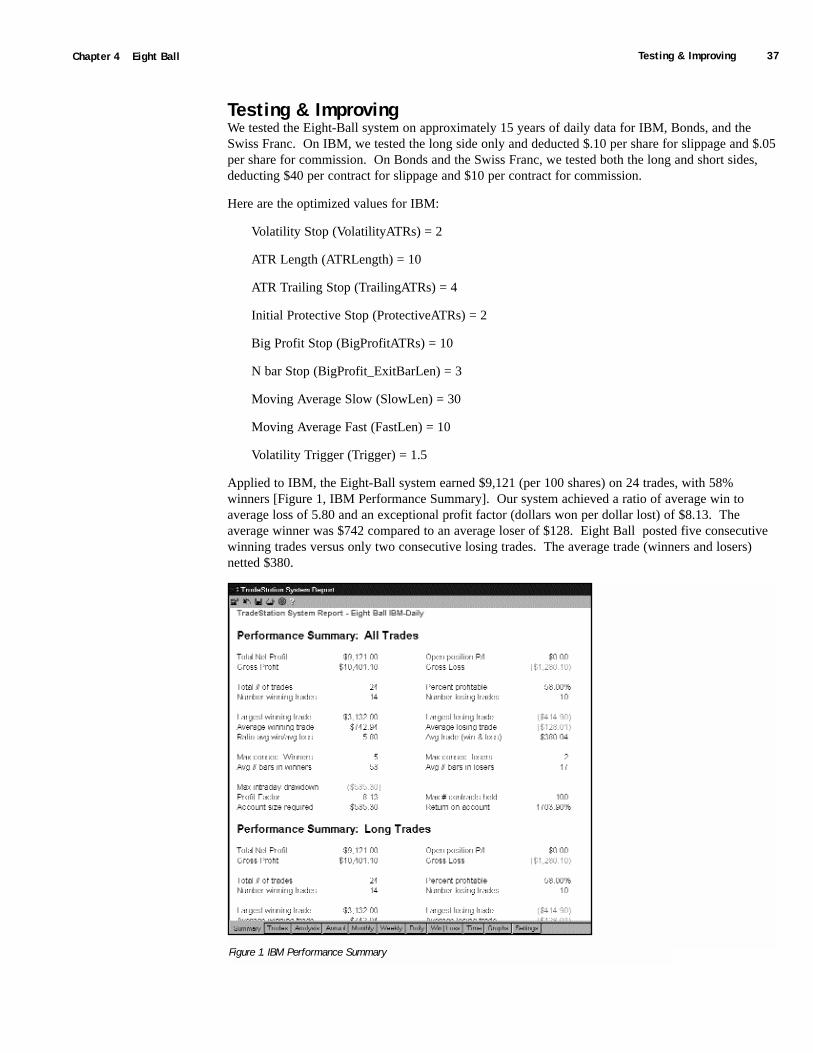

Applied to IBM, the Eight-Ball system earned $9,121 (per 100 shares) on 24 trades, with 58%winners [Figure 1, IBM Performance Summary]. Our system achieved a ratio of average win toaverage loss of 5.80 and an exceptional profit factor (dollars won per dollar lost) of $8.13. Theaverage winner was $742 compared to an average loser of $128. Eight Ball posted five consecutivewinning trades versus only two consecutive losing trades. The average trade (winners and losers)netted $380.

Figure 1. IBM Performance Summary

38 Testing & Improving Omega Research System Trading and Development Club - Volume 10

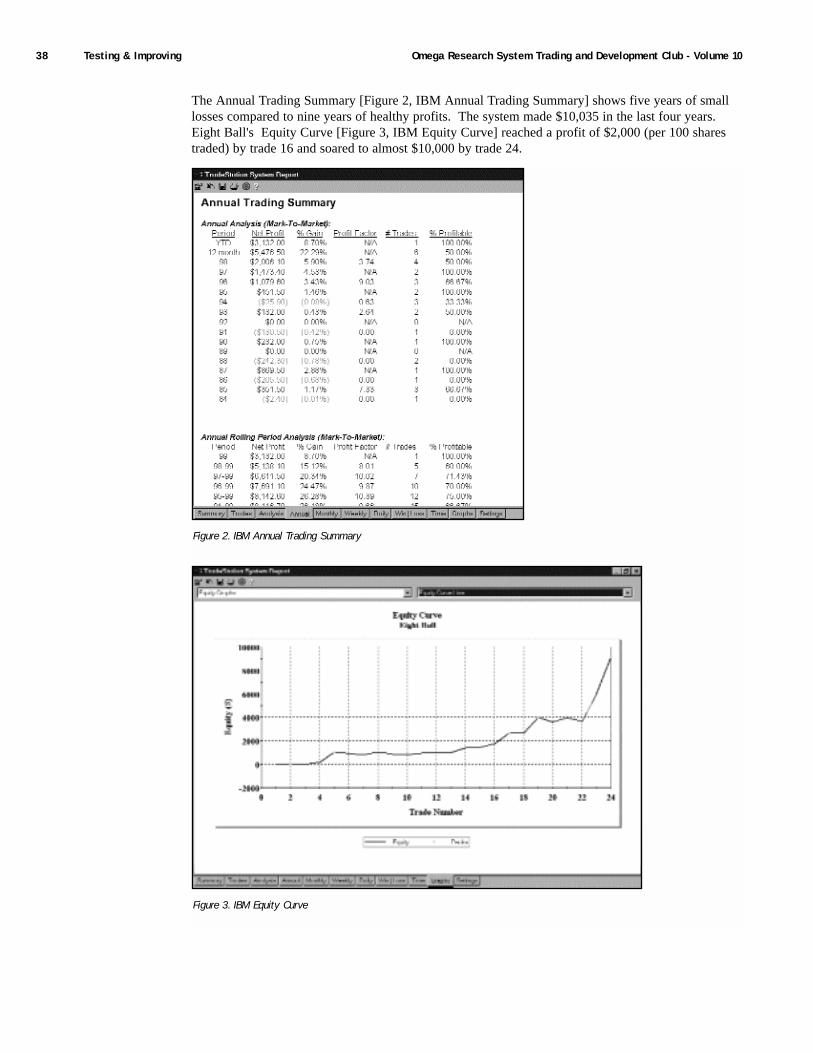

The Annual Trading Summary [Figure 2, IBM Annual Trading Summary] shows five years of smalllosses compared to nine years of healthy profits. The system made $10,035 in the last four years.Eight Ball's Equity Curve [Figure 3, IBM Equity Curve] reached a profit of $2,000 (per 100 sharestraded) by trade 16 and soared to almost $10,000 by trade 24.

Figure 2. IBM Annual Trading Summary

Figure 3. IBM Equity Curve

Testing & Improving 39Chapter 4 Eight Ball

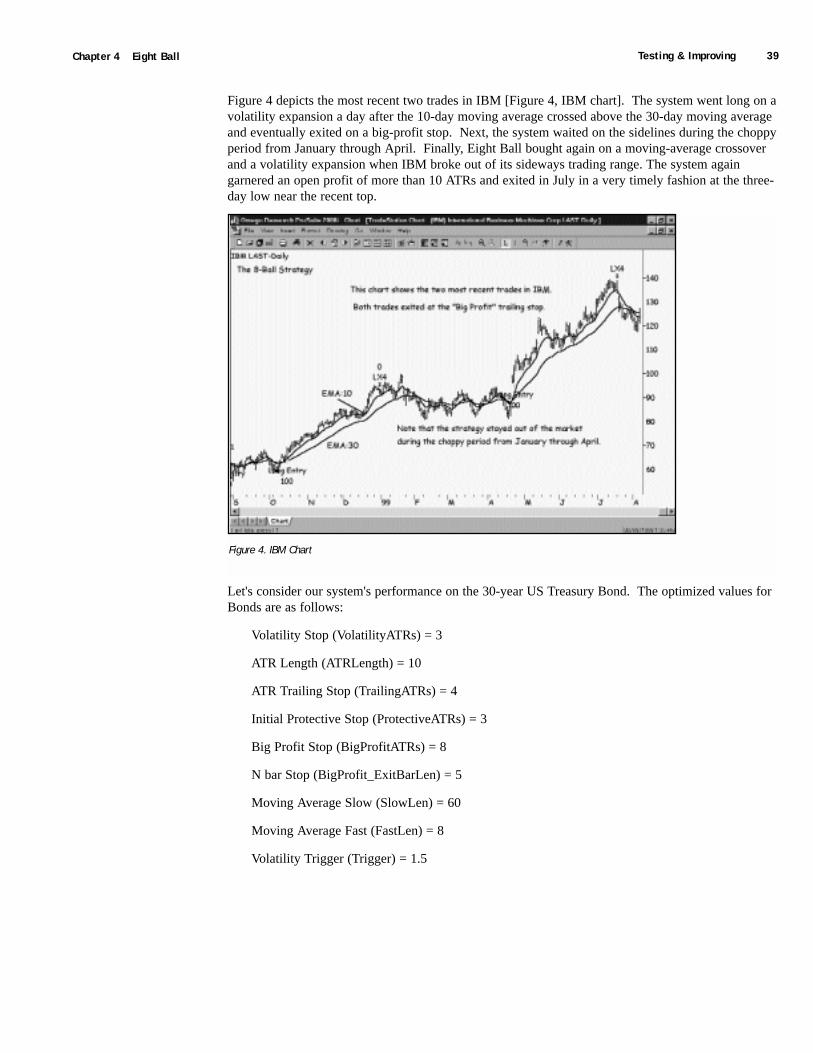

Figure 4 depicts the most recent two trades in IBM [Figure 4, IBM chart]. The system went long on avolatility expansion a day after the 10-day moving average crossed above the 30-day moving averageand eventually exited on a big-profit stop. Next, the system waited on the sidelines during the choppyperiod from January through April. Finally, Eight Ball bought again on a moving-average crossoverand a volatility expansion when IBM broke out of its sideways trading range. The system againgarnered an open profit of more than 10 ATRs and exited in July in a very timely fashion at the three-day low near the recent top.

Let's consider our system's performance on the 30-year US Treasury Bond. The optimized values forBonds are as follows:

Volatility Stop (VolatilityATRs) = 3

ATR Length (ATRLength) = 10

ATR Trailing Stop (TrailingATRs) = 4

Initial Protective Stop (ProtectiveATRs) = 3

Big Profit Stop (BigProfitATRs) = 8

N bar Stop (BigProfit_ExitBarLen) = 5

Moving Average Slow (SlowLen) = 60

Moving Average Fast (FastLen) = 8

Volatility Trigger (Trigger) = 1.5

Figure 4. IBM Chart

40 Testing & Improving Omega Research System Trading and Development Club - Volume 10

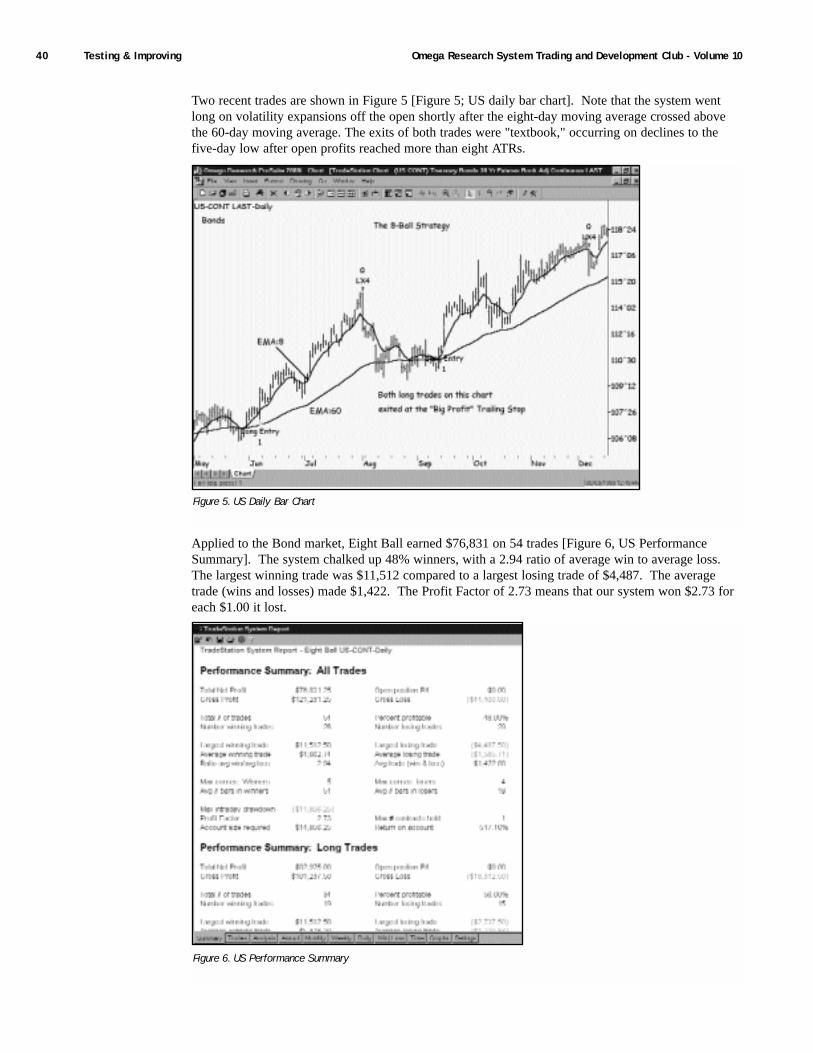

Two recent trades are shown in Figure 5 [Figure 5; US daily bar chart]. Note that the system wentlong on volatility expansions off the open shortly after the eight-day moving average crossed abovethe 60-day moving average. The exits of both trades were "textbook," occurring on declines to thefive-day low after open profits reached more than eight ATRs.

Applied to the Bond market, Eight Ball earned $76,831 on 54 trades [Figure 6, US PerformanceSummary]. The system chalked up 48% winners, with a 2.94 ratio of average win to average loss.The largest winning trade was $11,512 compared to a largest losing trade of $4,487. The averagetrade (wins and losses) made $1,422. The Profit Factor of 2.73 means that our system won $2.73 foreach $1.00 it lost.

Figure 5. US Daily Bar Chart

Figure 6. US Performance Summary

Testing & Improving 41Chapter 4 Eight Ball

The TradeStation System Report [Figure 7, System Report] presents several items of interest. EightBall's Sharpe Ratio, a standard measure of consistency of monthly returns compared to risk, was .24-very close to the desired rating of .25. The K- Ratio (which is similar to the Sharpe Ratio, but whichuses linear regression to evaluate a system's consistency of returns over time) came in at 3.68, muchbetter than the recommended reference point of 2.50. Two widely used reward-to-risk ratios alsoposted excellent results when Eight Ball was applied to the Bond market: Net Profit / Largest Losswas 17.12, and Net Profit / Maximum Drawdown was 17.31. The reference points for goodperformance in these ratios are 7 and 5, respectively.

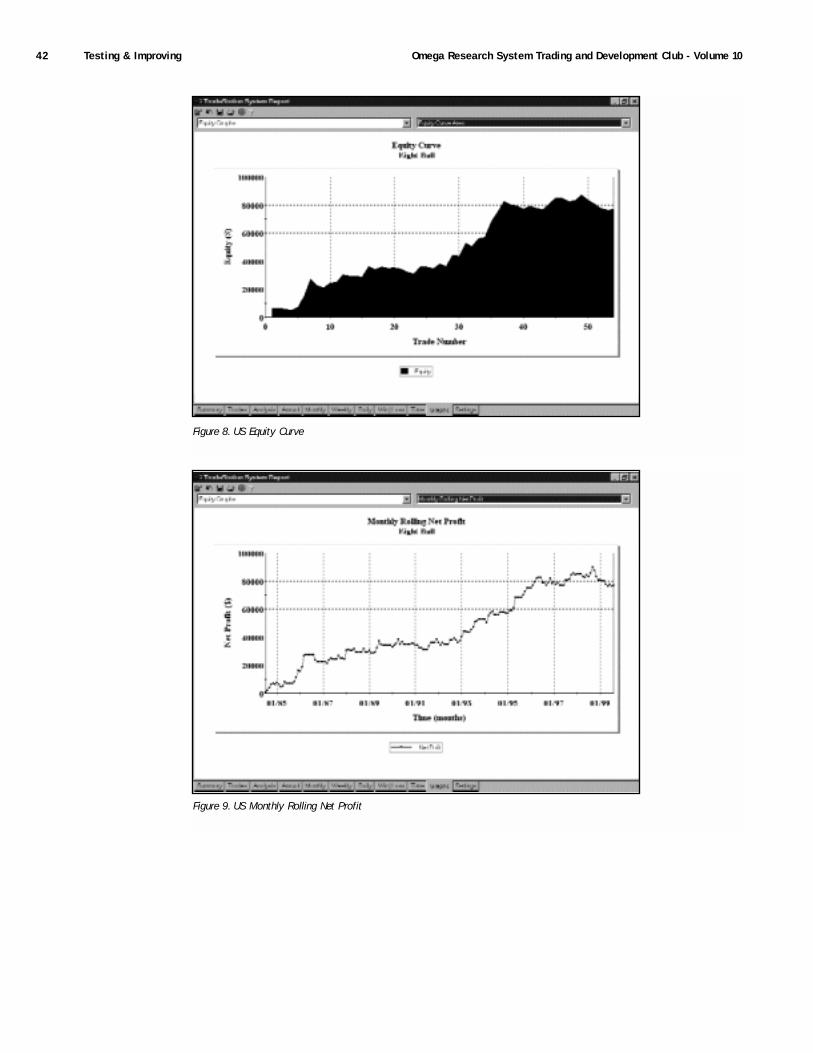

The system's Equity Curve represents fairly steady growth through trade 38 and a period of levelingoff since then to trade 54 [Figure 8, US Equity Curve]. The graph of Monthly Rolling Net Profitshows how the equity curve would look if trades were closed out at the end of each month [Figure 9,US Monthly Rolling Net Profit], and a snapshot was taken of the trading account. In other words, theaccount is "marked-to-market" on the last trading day of each month, and the end-of-month equity isposted to the graph.

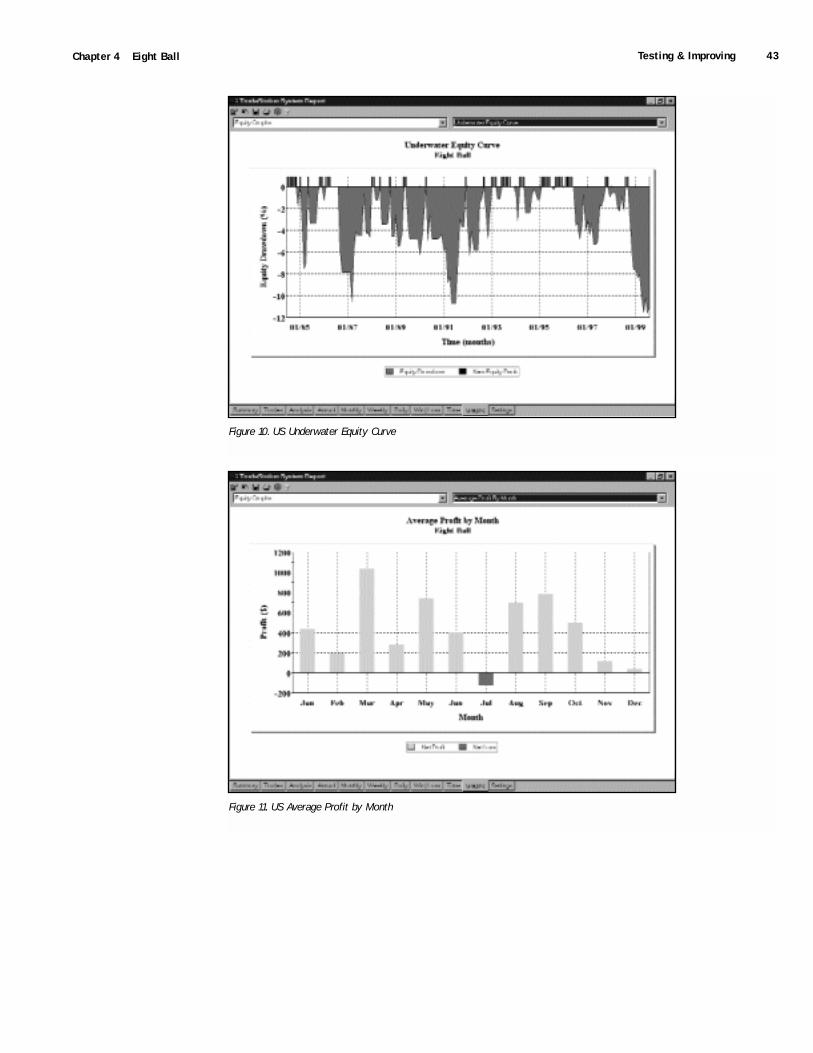

The Underwater Equity Curve [Figure 10, US Underwater Equity Curve] actually looks fairly goodwhen you consider that it was designed to paint a very negative picture of performance. The newequity highs (the short, vertical bars rising above the 0 line) obviously are not drawn to scale, but theareas of drawdown between the equity peaks are drawn very large. In reality, there were only threedrawdowns greater than 10 percent in the 15-year test period, with a largest drawdown of only 11 3/4percent.

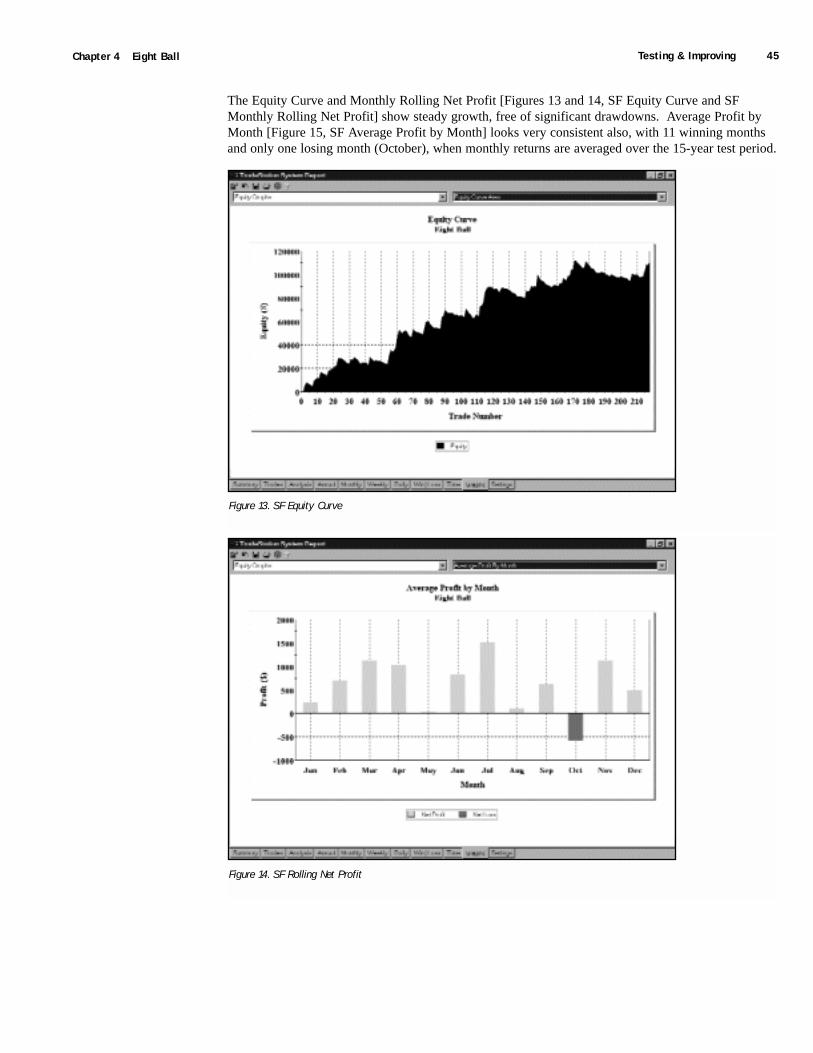

The Average Profit by Month graph for the Eight-Ball system applied to Bonds is just about as goodas can be, with 11 winning months and only one small losing month when monthly returns areaveraged over the test period [Figure 11, US Average Profit by Month].

Figure 7. System Report

42 Testing & Improving Omega Research System Trading and Development Club - Volume 10

Figure 8. US Equity Curve

Figure 9. US Monthly Rolling Net Profit

Testing & Improving 43Chapter 4 Eight Ball

Figure 10. US Underwater Equity Curve

Figure 11. US Average Profit by Month

44 Testing & Improving Omega Research System Trading and Development Club - Volume 10

Next, let's see how Eight Ball handled the Swiss Franc. The optimized values are as follows:

Volatility Stop (VolatilityATRs) = 3

ATR Length (ATRLength) = 10

ATR Trailing Stop (TrailingATRs) = 5

Initial Protective Stop (ProtectiveATRs) = 2

Big Profit Stop (BigProfitATRs) = 8

N bar Stop (BigProfit_ExitBarLen) = 2

Moving Average Slow (SlowLen) = 60

Moving Average Fast (FastLen) = 6

Volatility Trigger (Trigger) = 0

Applied to the Swiss Franc, our system generated profits of $110,412 on 218 trades, with an averagetrade (wins and losses) of $506 per contract [Figure 12, SF Performance Summary]. Although only33% of the trades were profitable, the average win was 3.71 times as large as the average loss. Thebiggest winning trade made $11,612, while the biggest losing trade lost only $3,287. The averagewinning trade earned $3,523 versus an average losing trade of just $950. Eight Ball let profits run byholding winners for an average of 38 days and cut losses short by exiting losers in an average of onlyseven days.

Figure 12. SF Performance Summary

Testing & Improving 45Chapter 4 Eight Ball

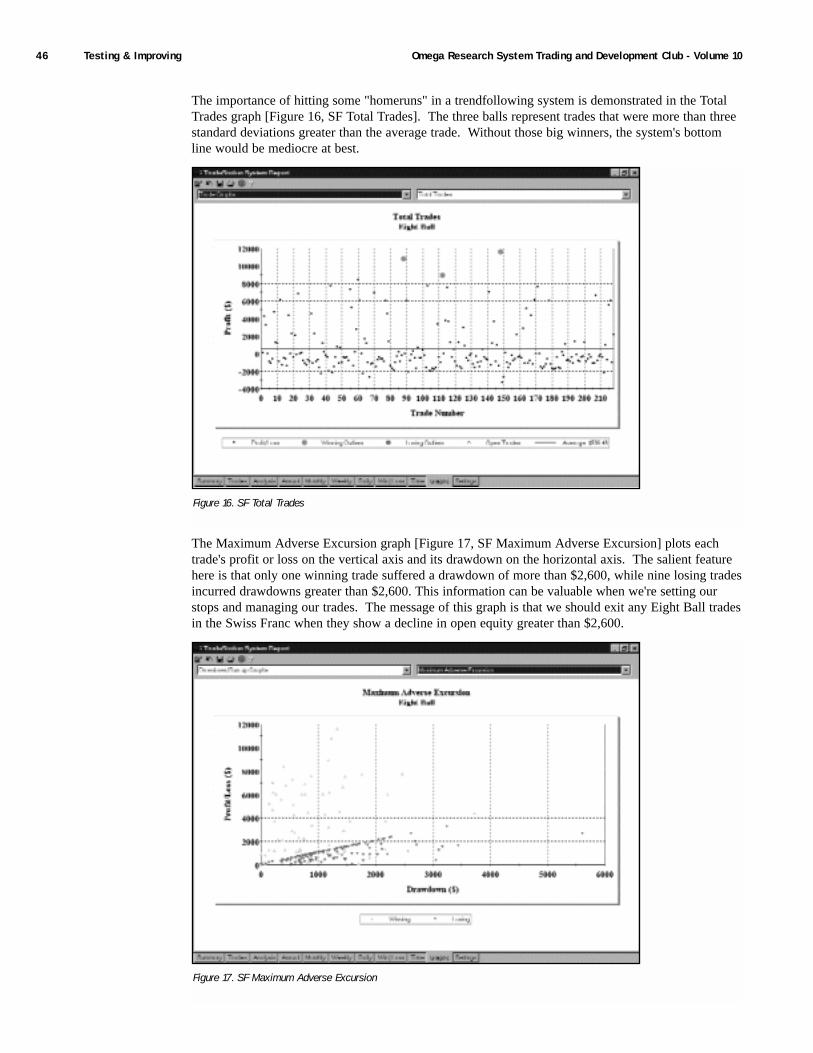

The Equity Curve and Monthly Rolling Net Profit [Figures 13 and 14, SF Equity Curve and SFMonthly Rolling Net Profit] show steady growth, free of significant drawdowns. Average Profit byMonth [Figure 15, SF Average Profit by Month] looks very consistent also, with 11 winning monthsand only one losing month (October), when monthly returns are averaged over the 15-year test period.

Figure 13. SF Equity Curve

Figure 14. SF Rolling Net Profit

46 Testing & Improving Omega Research System Trading and Development Club - Volume 10

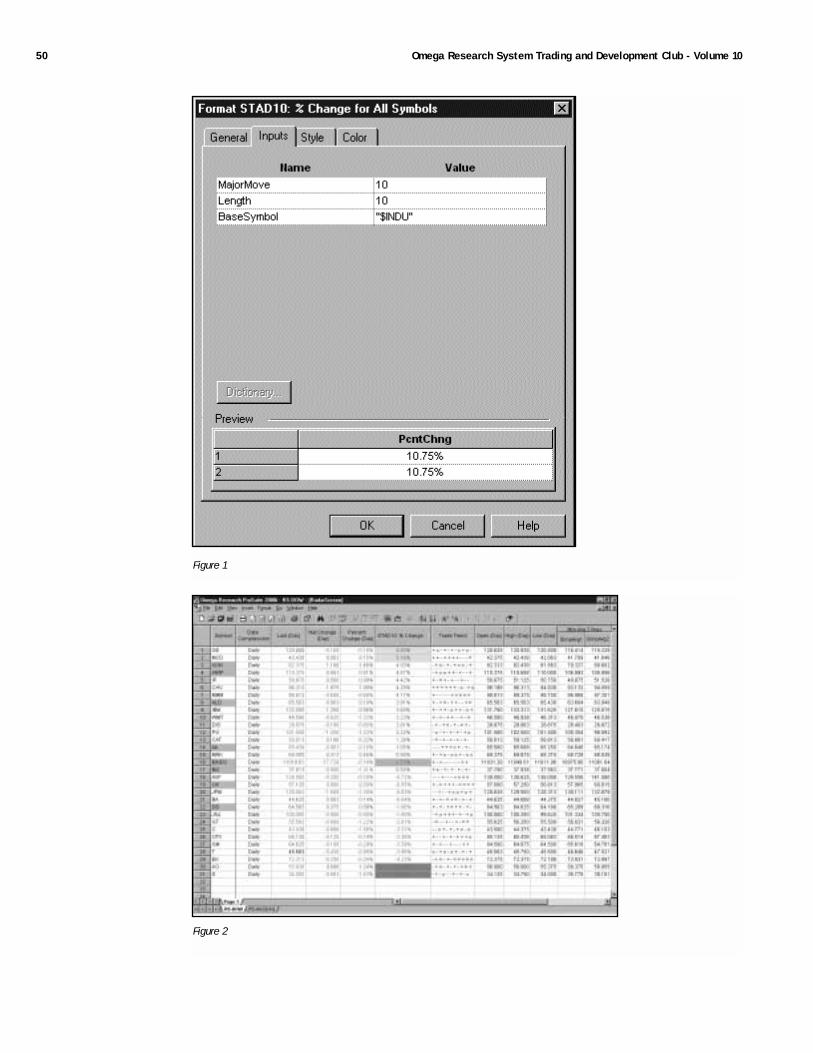

The importance of hitting some "homeruns" in a trendfollowing system is demonstrated in the TotalTrades graph [Figure 16, SF Total Trades]. The three balls represent trades that were more than threestandard deviations greater than the average trade. Without those big winners, the system's bottomline would be mediocre at best.

The Maximum Adverse Excursion graph [Figure 17, SF Maximum Adverse Excursion] plots eachtrade's profit or loss on the vertical axis and its drawdown on the horizontal axis. The salient featurehere is that only one winning trade suffered a drawdown of more than $2,600, while nine losing tradesincurred drawdowns greater than $2,600. This information can be valuable when we're setting ourstops and managing our trades. The message of this graph is that we should exit any Eight Ball tradesin the Swiss Franc when they show a decline in open equity greater than $2,600.

Figure 16. SF Total Trades

Figure 17. SF Maximum Adverse Excursion

Suggestions for Improvement 47Chapter 4 Eight Ball

Suggestions for ImprovementThe system is working very well. Can we improve it? With four types of stops managing its exits,the exits would probably be hard to improve. Let's look at the entries. Currently, the system enters aposition on a move off the open in the direction of the desired trade when the two moving averagespoint in the same direction. That way both the long-term and short-term trends are in agreement.However, a market may be overbought when both averages point up and oversold when both averagespoint down. What would happen if we changed the setup for a buy to the following: if the long-termmoving average is rising, and the short-term moving average is declining? That way the long-termtrend would be up, but the short-term trend would be down. We'd be buying after a countertrenddecline, and our entry trigger of a strong move off the open in the direction of the desired trade wouldindicate that the decline had run its course.

Similarly, when both moving averages are pointing down, a market might be oversold and ready tostage a countertrend rally. If the long-term moving average is falling, but the short-term average isrising, we'd have a setup to sell short on a resumption of the downtrend. A sharp downward move offthe open could signal an end to the countertrend rally and a resumption of the downtrend.

It's easy to modify the EasyLanguage for this idea. In the PowerEditor, find Eight Ball's condition1.Change the second part to the following:

And FastAvg < FastAvg [1];

Next, find condition2 and change the second part to:

And FastAvg > FastAvg [1];

Finally, retest and reoptimize Eight Ball to find out if the revised version improves the originalversion.

48 Omega Research System Trading and Development Club - Volume 10

C H A P T E R 5

Measuring & Comparing Performance inRadarScreen 2000iBy Gaston Sanchez

RadarScreen was designed to answer the question "What to Buy and Sell?" Thereare many ways, using many Indicators, that this question can be answered. In thischapter, I will be showing you a unique approach to setting up and sorting your

RadarScreen window to show you those stocks that are out-performing, as well as under-performing, a particular market index.

In this chapter I have taken advantage of RadarScreen's unique ability to create and sort based oncustom analysis techniques developed an excellent tool for benchmarking the performance of alist of stocks to a market index. Very simply put, the Indicator just calculates the Percent Changebased on a user-defined length. Even though the idea is simple, strength of this technique is reallybrought out by RadarScreen. Using the sorting capabilities in RadarScreen, my entire list ofstocks is sorted in such a way so as to show me those stocks that are over/under performing theselected market index. In addition, it also displays for me which are over/under performing themarket by a specific amount. This allows me to easily recognize which are the strongest stocks inmy window, relative to the selected market index. Basically a very valuable tool for determiningwhat I might want to Buy or Sell. This tool has shown such promise that it is likely that you maysee it added to the default work area at some point in the future.

We begin with a very simple example, say using the Dow 30 stocks. All 30 stocks can be easilyloaded into our RadarScreen window using the built-in symbol list. We will also load the DowJones Industrial Average ($INDU - the symbology may vary between feeds). The DJIA is whatwe will call the 'BaseSymbol'. The 'BaseSymbol' is a symbol that will serve as a benchmark forall the other symbols in our list. The next step is to apply the STAD10: % Change Indicator toyour RadarScreen window. When applying the Indicator, it is very important that you enter theappropriate symbol for the DJIA in quotes for the 'BaseSymbol' Input [Figure 1]. Once you haveapplied the Indicator to your chart, you can then double-click the column heading to sort the list.Once the list is sorted, you will notice that the DJIA or the 'BaseSymbol' is highlighted in yellow.Those stocks that are outperforming the DJIA for the period specified will appear above the cellhighlighted in yellow, and those that are under-performing the DJIA for the period specified willappear below the cell highlighted in yellow cell in the column. Any symbols that have aparticularly strong percent change, either positive or negative (as indicated by the MajorMoveInput) will be highlighted with a different color [Figure 2].

50 Omega Research System Trading and Development Club - Volume 10

Figure 1

Figure 2

EasyLanguage Indicator 51Chapter 5 Measuring & Comparing Performance in RadarScreen 2000i

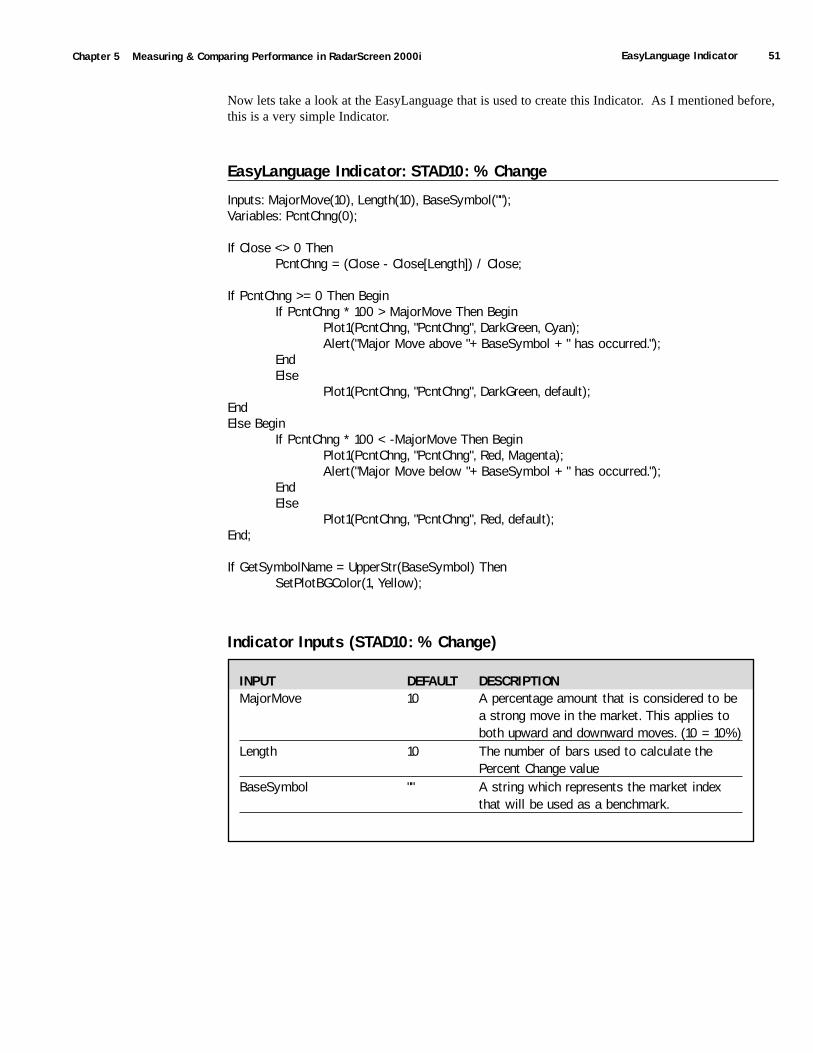

Now lets take a look at the EasyLanguage that is used to create this Indicator. As I mentioned before,this is a very simple Indicator.

EasyLanguage Indicator: STAD10: % Change

Inputs: MajorMove(10), Length(10), BaseSymbol("");Variables: PcntChng(0);

If Close <> 0 ThenPcntChng = (Close - Close[Length]) / Close;

If PcntChng >= 0 Then BeginIf PcntChng * 100 > MajorMove Then Begin

Plot1(PcntChng, "PcntChng", DarkGreen, Cyan);Alert("Major Move above "+ BaseSymbol + " has occurred.");

EndElse

Plot1(PcntChng, "PcntChng", DarkGreen, default);EndElse Begin

If PcntChng * 100 < -MajorMove Then BeginPlot1(PcntChng, "PcntChng", Red, Magenta);Alert("Major Move below "+ BaseSymbol + " has occurred.");

EndElse

Plot1(PcntChng, "PcntChng", Red, default);End;

If GetSymbolName = UpperStr(BaseSymbol) ThenSetPlotBGColor(1, Yellow);

Indicator Inputs (STAD10: % Change)

INPUT DEFAULT DESCRIPTIONMajorMove 10 A percentage amount that is considered to be

a strong move in the market. This applies to both upward and downward moves. (10 = 10%)

Length 10 The number of bars used to calculate the Percent Change value

BaseSymbol "" A string which represents the market index that will be used as a benchmark.

52 EasyLanguage Indicator Omega Research System Trading and Development Club - Volume 10

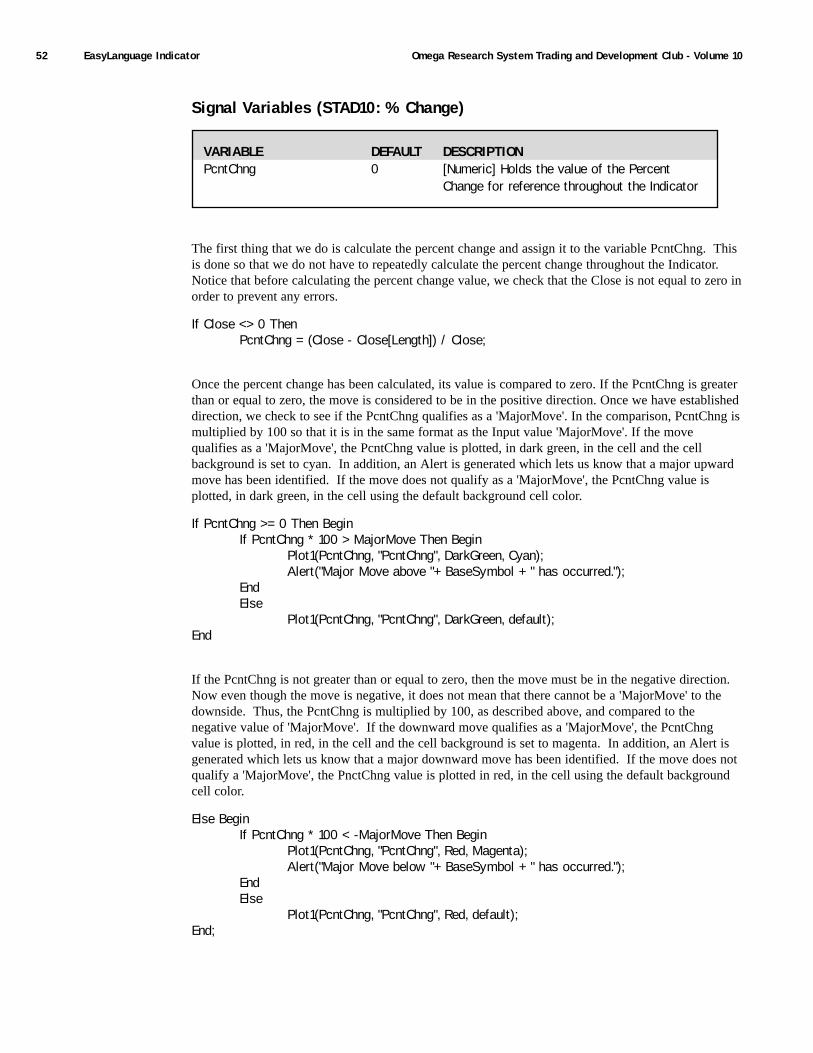

Signal Variables (STAD10: % Change)

The first thing that we do is calculate the percent change and assign it to the variable PcntChng. Thisis done so that we do not have to repeatedly calculate the percent change throughout the Indicator.Notice that before calculating the percent change value, we check that the Close is not equal to zero inorder to prevent any errors.

If Close <> 0 ThenPcntChng = (Close - Close[Length]) / Close;

Once the percent change has been calculated, its value is compared to zero. If the PcntChng is greaterthan or equal to zero, the move is considered to be in the positive direction. Once we have establisheddirection, we check to see if the PcntChng qualifies as a 'MajorMove'. In the comparison, PcntChng ismultiplied by 100 so that it is in the same format as the Input value 'MajorMove'. If the movequalifies as a 'MajorMove', the PcntChng value is plotted, in dark green, in the cell and the cellbackground is set to cyan. In addition, an Alert is generated which lets us know that a major upwardmove has been identified. If the move does not qualify as a 'MajorMove', the PcntChng value isplotted, in dark green, in the cell using the default background cell color.

If PcntChng >= 0 Then BeginIf PcntChng * 100 > MajorMove Then Begin

Plot1(PcntChng, "PcntChng", DarkGreen, Cyan);Alert("Major Move above "+ BaseSymbol + " has occurred.");

EndElse

Plot1(PcntChng, "PcntChng", DarkGreen, default);End

If the PcntChng is not greater than or equal to zero, then the move must be in the negative direction.Now even though the move is negative, it does not mean that there cannot be a 'MajorMove' to thedownside. Thus, the PcntChng is multiplied by 100, as described above, and compared to thenegative value of 'MajorMove'. If the downward move qualifies as a 'MajorMove', the PcntChngvalue is plotted, in red, in the cell and the cell background is set to magenta. In addition, an Alert isgenerated which lets us know that a major downward move has been identified. If the move does notqualify a 'MajorMove', the PnctChng value is plotted in red, in the cell using the default backgroundcell color.

Else BeginIf PcntChng * 100 < -MajorMove Then Begin

Plot1(PcntChng, "PcntChng", Red, Magenta);Alert("Major Move below "+ BaseSymbol + " has occurred.");

EndElse

Plot1(PcntChng, "PcntChng", Red, default);End;

VARIABLE DEFAULT DESCRIPTIONPcntChng 0 [Numeric] Holds the value of the Percent

Change for reference throughout the Indicator

EasyLanguage Indicator 53Chapter 5 Measuring & Comparing Performance in RadarScreen 2000i

Finally, as the entire RadarScreen window is evaluated, once the symbol that serves as the benchmark(BaseSymbol) is identified, the background color for that cell is set to yellow. Notice that thecomparison includes UpperStr() for the BaseSymbol. This is done in the event that the BaseSymbolis not entered as all CAPS in the Input.

If GetSymbolName = UpperStr(BaseSymbol) ThenSetPlotBGColor(1, Yellow);

Lets look at another example of this Indicator. In this example, the Indicator has been applied to aRadarScreen window, which contains the NASDAQ 100. The 'BaseSymbol' is tied to the NASDAQ100 index (NDX) [Figure 3].

Figure 3. Those stocks that were outperforming the NDX appear above the highlighted cell. Anystocks with a percent change that was greater than 7% are highlighted. By having RadarScreenkeep the list of symbols sorted, you can always know which stocks are on top of the market, aswell as how they compare to a specific market index.

54 EasyLanguage Indicator Omega Research System Trading and Development Club - Volume 10

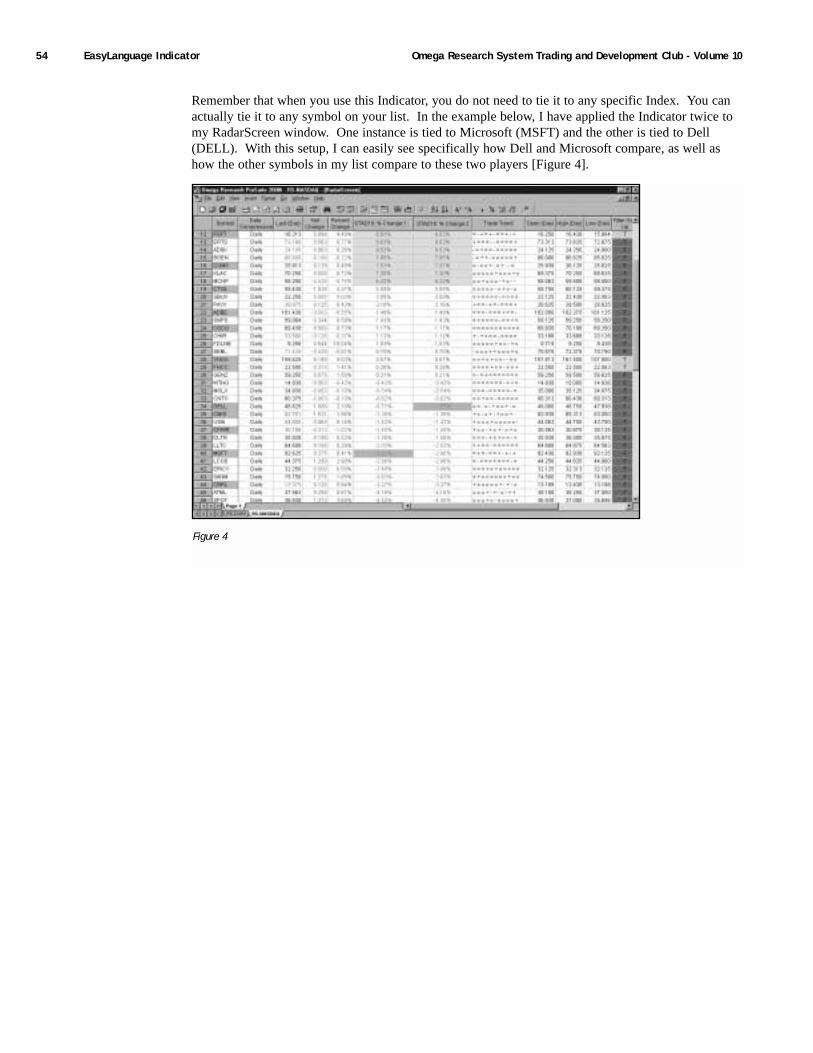

Remember that when you use this Indicator, you do not need to tie it to any specific Index. You canactually tie it to any symbol on your list. In the example below, I have applied the Indicator twice tomy RadarScreen window. One instance is tied to Microsoft (MSFT) and the other is tied to Dell(DELL). With this setup, I can easily see specifically how Dell and Microsoft compare, as well ashow the other symbols in my list compare to these two players [Figure 4].

Figure 4

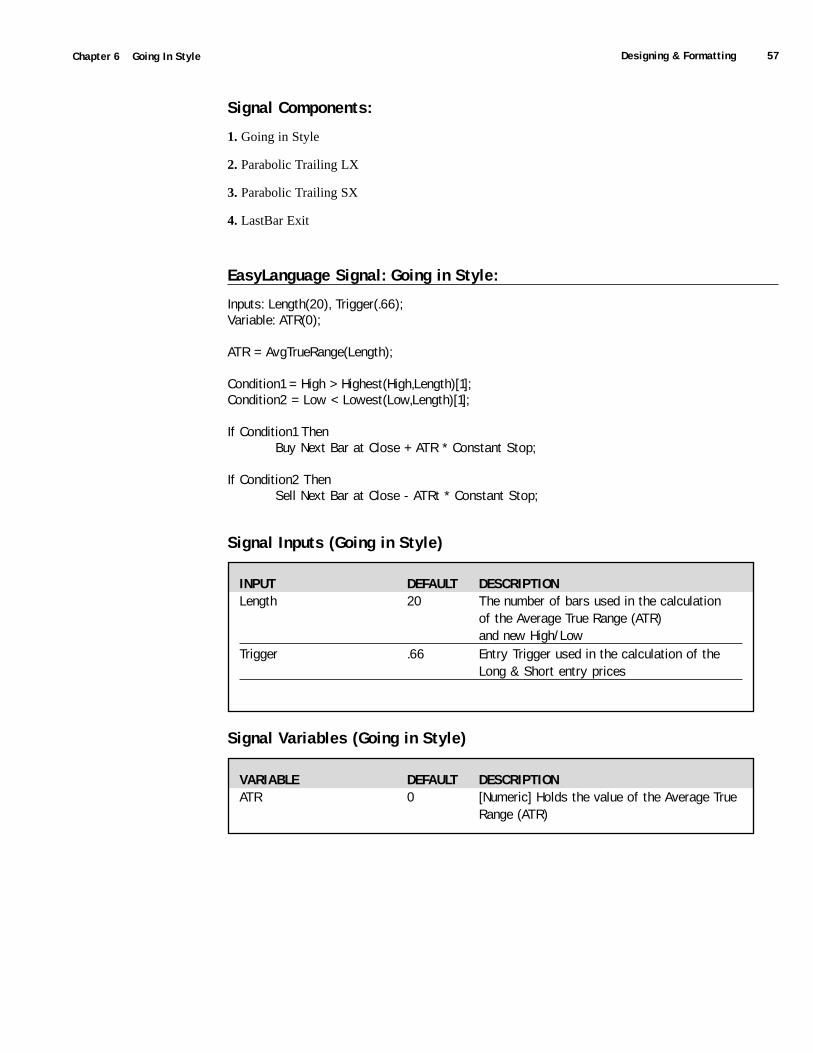

C H A P T E R 6

Going In Style

Price channel breakouts are very simple: you buy when a market makes a new n-barhigh; you sell when a market makes a new n-bar low. Add a few money-managementand trade-management rules, and you may have a profitable system. In the Going in

Style system, we'll use a price channel breakout as a setup and a multiple of the AverageTrue Range (ATR) added to or subtracted from the close as an entry.

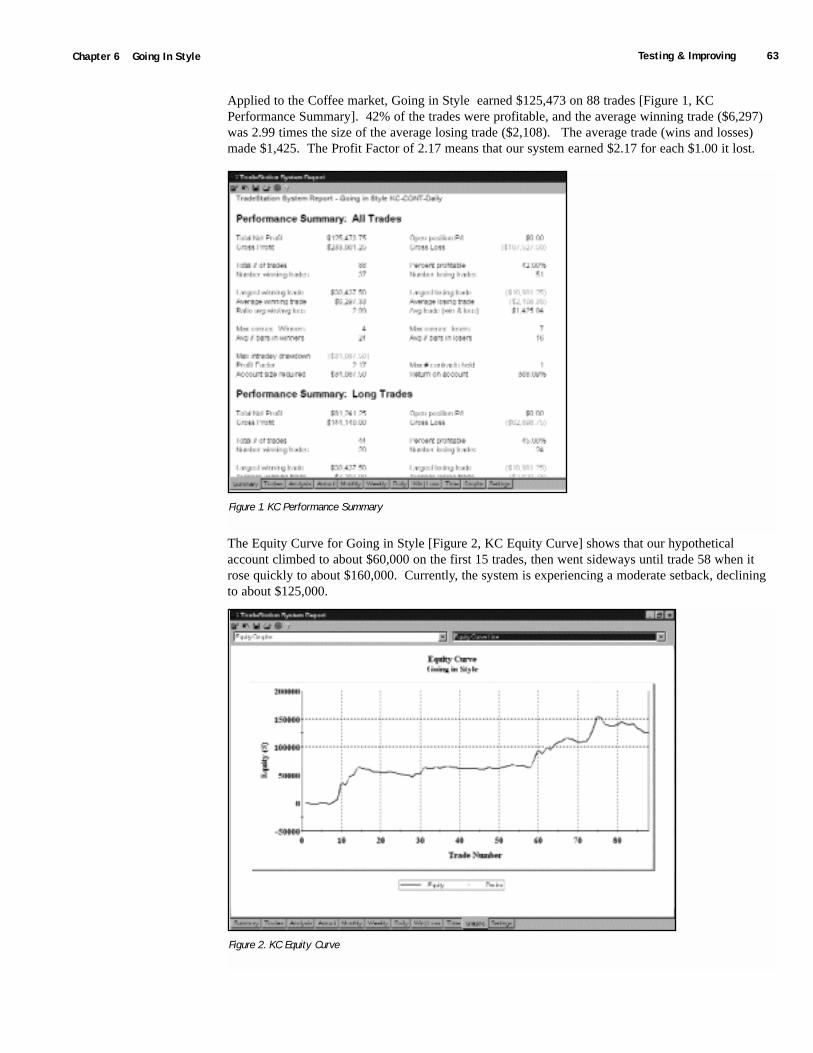

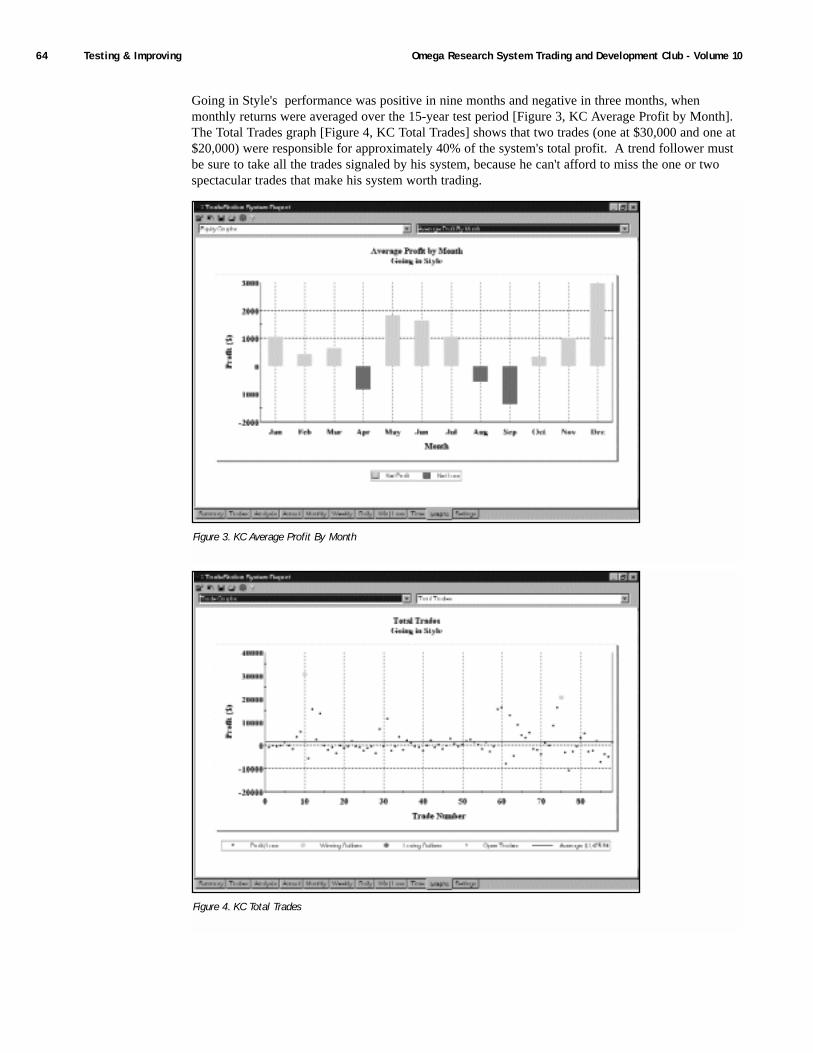

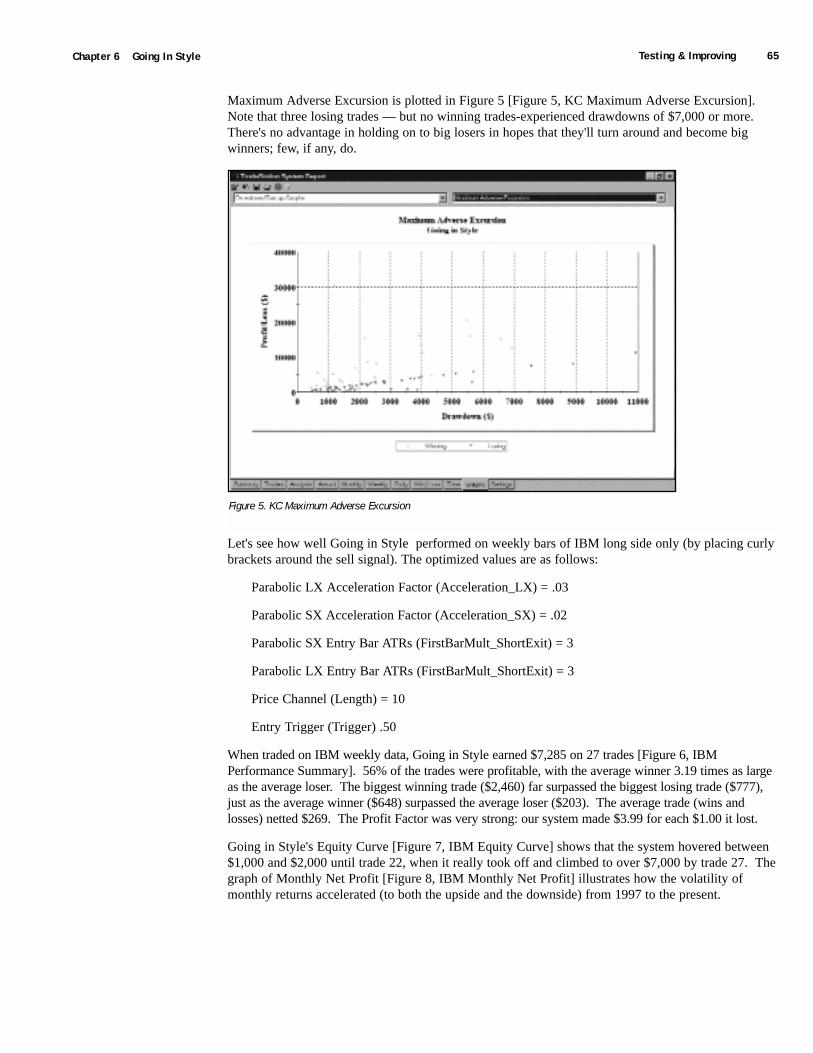

In other words, we'll identify a price channel breakout but defer our entry into the trade untilprices stage a confirming rally (in the case of a potential long position) or a confirming decline(for a potential short position). We named this system Going in Style because we're requiringthat a market not only break out of a price channel, but that it also does so with style-makinganother strong move on the bar following the breakout.