Embed Size (px)

Citation preview

1

Paper Prepared for the 11th ERF Conference on December 16-18, 2004

Volatility Regime-Switching and Linkage among GCC Stock Markets

Shawkat Hammoudeh Drexel University Philadelphia, PA

Kyongwook Choi Ohio University

Athens, OH

Abstract. The GCC stock markets vary in terms of sensitivity to the magnitude of return

volatility and the duration of volatility, regardless of the volatility regime and the return

component. Among the GCC market, risk-averse investors and traders in the Oman and

Saudi Arabia markets should particularly demand higher premiums for the extra volatility

sensitivity during fad times than investors in the other markets. In terms of duration of

volatility, investors and policy makers in the Kuwait, Bahrain and Saudi Arabia should be

aware of the longer duration of this volatility during the fad times. All GCC returns move

in the same direction whether in terms of total return, fundamentals or fads under both

volatility regimes. Correlations of the stock returns and their components with each other

and with the oil price return are also weak, suggesting that country particularities in

addition to the oil price return influence the stock component returns.

JEL Classification: C22; F3; Q49 Keywords: Volatility; Markov switching; Permanent and transitory components; Transition Probability

2

Volatility Regime-Switching and Linkage among GCC Stock Markets

1. Introduction

Fads or speculative attacks are short- lived phenomena that affect the world’s

stock markets such as the October 1997 crash of the US market and the 1982 crash of the

Kuwait market. In these crashes the markets experience large drop in stock prices and

dramatic jump in volatility. Shocks in the fads are caused by noisy trades how bid prices

away from the fundamentals due to changes in price misperceptions (De Long et al,

1990). Although the fad volatility usually reverts to normal levels quickly, this transitory

volatility can cause tremendous damage to wealth and social wellbeing. Moreover,

increases in risk would raise the cost of capital and may retard economic growth in the

long-run. Therefore, it is important to consider an economic variable such as a stock

return in terms of its permanent or fundamental component, and its transitory or fad

components to determine the expected durability of the fad volatility relative to the

fundamental volatility and examine the impact of each of these components on the

volatility of the return.

The recent literature also studies the decomposition of the stock return within the

state-space framework that allows for volatility transition between regimes for the return

itself and for each of its components. Several authors have proposed different methods of

decomposing a time series into permanent and transitory components. Nelson and Plosser

(1982) matched a model consisting of transitory and permanent components to an

autocorrelation function to determine the relative sizes of these two components. Watson

3

(1986) and Clark (1987) used the conventional unobserved component model (without

Markov-switching) to decompose GNP into these two components. Campbell and

Mankiw (1987), employing an ARMA representation of a time series, estimated the

impact of a shock on long-run forecasts to weigh up he relative importance of the two

components.

More recent methods examined the decomposition by focusing on mean reversion

in stock returns. Fama and French (1988) used an autoregressive test and found mixed

results on the existence of mean reversion in the transitory and permanent components.

Kim and Kim (1996) and Kim and Nelson (1999) examined the relative importance of the

two components within the framework of the space state model with Markov-switching

heteroscedasticity. This model can capture the short term dynamics that might not

otherwise be captured by the other methods such as the autoregression test of Fama and

French (1988) and the conventional unobserved component models of Watson (1986) and

Clark (1987). Bhar and Hamori (2004) applied Kim and Kim (1996) model to the some

of OECD countries. Other studies that use the space-state model with a Markov regime-

switching process to model volatility and shifts in return regimes but without the

component decomposition include Hamilton and Susman (1994)1, McCarthy and Najand

(1995), Chu et al (1996), Schaller and van Norden (1997) and among others.

This study uses the empirical model of Kim and Kim (1996) and Bhar and

Hamori (2004) to examine the volatility of the decomposed stock returns of members of

the Gulf Cooperation Council (GCC). The six-member GCC includes: Bahrain, Kuwait,

1 For earlier research, see Hamilton (1989), Turner et al (1989) and Glosten et al (1993).

4

Oman, Qatar, Saudi Arabia and United Arab Emirates (UAE)2. The market capitalization

of the GCC markets as a group was about US$ 172 billion at the end of 2002, and since

then has been rapidly rising because of high oil prices and of strong movement towards

privatization. These markets have strong future gain potential because of their ownership

of huge oil reserves. They together account for 16% of the world output and possess 47%

of the world’s oil reserves. In 2002 when most of the world’s stock markets dropped

drastically and realized huge losses, most of the GCC countries made substantial gains

and have continued this strong gain through 2004.

Recent research on the GCC stock markets uses the error-correction model to

examine co-movements and interactions of the returns (Hammoudeh and Eleisa, 2004;

and Malik and Hammoudeh, 2004). No attempt has been made to examine the mean

reversion of the two components that make up the returns of these GCC markets while

allowing for volatility regime switching. Therefore, the desired objectives of this paper

can be summarized as follows:

1. To decompose the stock returns of the GCC stock markets into permanent and

transitory components;

2. To measure the switch in volatility between the high and low variance regimes for

both the permanent and transitory components of the stock returns;

3. To measure the expected duration of the volatility, in terms of trading weeks, of

the high and low variance regimes of the transitory component.

2 Qatar is not included because its stock market was established in 1997, which does not provide an appropriate long enough time series.

5

4. To measure the correlation between the volatilities of the individual GCC stock

markets to ascertain whether or not these markets move in the same or opposite

direction; and

5. To measure the correlation of volatility of the individual GCC stock markets and

oil markets to determine if they move in the same direction.

The findings suggest that there are two significant volatility-switching regimes in

both components of the stock returns for all the GCC countries. They also show

differences in the sensitivity to the return volatility and the duration of volatility across

regimes and return components and across the markets. In particular the results

emphasize the sensitivity of the Oman and Saud i markets to shocks during fad times in

the high volatility regime which is of particular interest to this study. Shocks also persist

longer in the Kuwait, Bahrain and Oman markets in the high volatility fad regime. We

should also note that shocks in the fundamentals have very long expected durations

exceeding the durations of shocks in the fads. Overall, these results suggest that the GCC

countries are very different when it comes to return on financial investment. Thus,

investors should do their homework before investing in these countries. Moreover, the

persistence and magnitude of extra volatility in certain markets (e.g., Oman and Kuwait)

calls on policy makers to introduce financial hedge instruments (e.g., options, futures) to

help investors ride the volatility waves that could persist for several months. They should

reduce volatility because of its impact on the cost of capital and economic growth.

Traders should also demand higher premiums for investing in stock markets that are

relatively more volatile such as the Oman market. The findings will provide traders and

6

investors in the GCC markets with information that may enable them to distinguish

between markets and ask for higher compensations in some markets than others.

The results also indicate that the markets are not highly correlated in the return itself,

and the permanent and transitory components between the GCC markets, compared for

example with Germany, Japan, UK and the United States (Bhar and Hamori, 2004).

These results suggest there are some gains from portfolio diversification among particular

GCC markets particula rly between Saudi Arabia and UAE, and between and Oman and

Bahrain.

The correlations of the returns and their components with the oil price for the

countries are also weak, suggesting that country particularities also influence the

component returns. The weakest correlation is between the oil price return and the Oman

and Kuwait total returns. The Kuwait market has a negative correlation with the oil price

return in the fads, emphasizing the importance of speculative attacks and the presence of

hot hands in this market. This information is useful for local as well as for international

investors

2. Descriptive Statistics

The Gulf Cooperation Council (GCC) consists of six members including Bahrain,

Kuwait, Oman, Qatar, Saudi Arabia and United Arab Emirates. We used in this study

weekly time series on the Bahrain Stock Exchange index (BSE), Kuwait Stock Exchange

index (KSE), the Oman Muscat Securities Market index (MSM), the Saudi stock market

index (Tadawal) and the UAE National Bank of Abu Dhabi index (NBAD). As indicated

above, the market capitalization of the GCC markets as a group was about US$ 172

7

billion at the end of 2002. These stock markets display low to moderate valuations

compared to the stock markets in the United States and other major world markets

(Hammoudeh and Eleisa, 2004)

The series for these indices were directly obtained from the respective stock

exchanges. The data for these series covers the period February 15, 1994 to December

25, 2001. The sample period was determined primarily by the availability of the data on

the five Gulf equity markets. Still, this sample period includes the Mexican 1994 crisis,

the July 1997 East Asian crisis, the 1998 collapse of oil prices, the 1999 oil price and

Asian economy recovery, the adoption of the target zone oil pricing mechanism in

February 2000, and the New York September 2001 bombing. The rate of return on for

each country’s each stock index is calculated as a log-differenced

prices, 1(log( ) log( )) 100t t tr P P −= − × , where tP is the stock price index for each country.

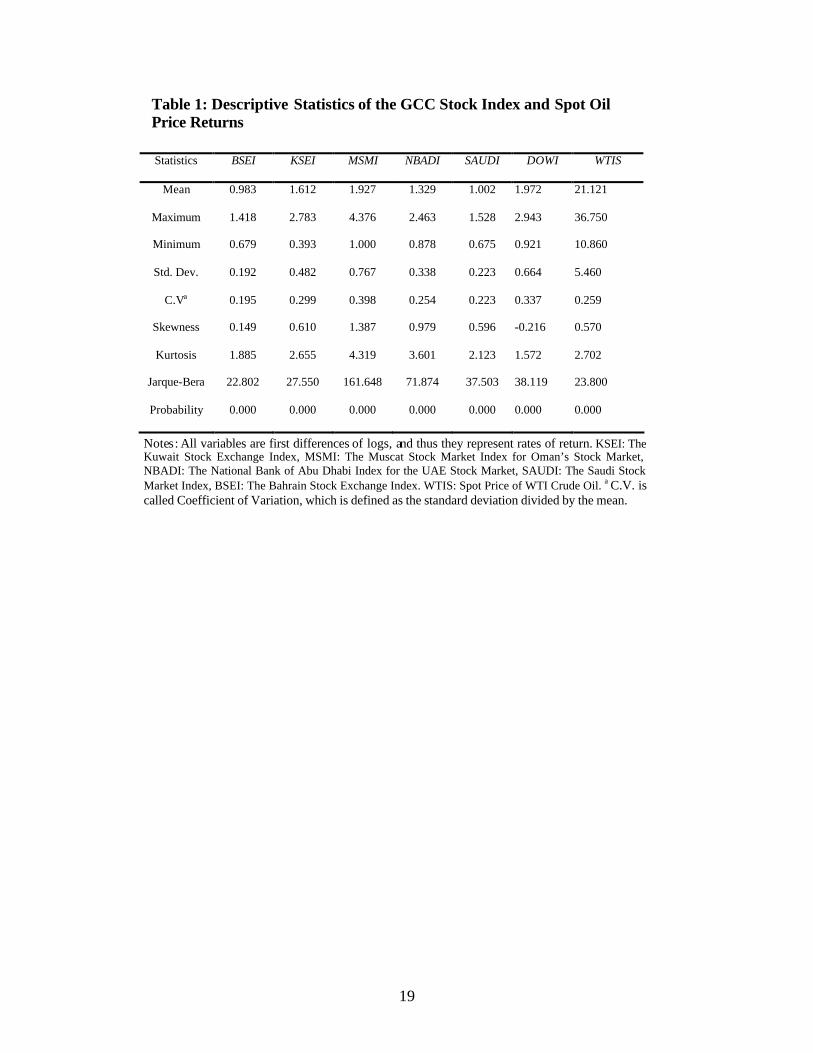

Comparing the volatilities of the five GCC stock indices and the Dow as defined

by the coefficient of variation, Table 1 shows that the GCC stock returns on average are

less volatile than the DOW which could be due to the isolation of these markets and the

difference in the types of traders participating in them; the only exception is the Omani

index (MSM) which is the most volatile of them all. It also shows that the six stock

returns are generally more volatile than the five spot and futures oil price returns.

However, the US DOW return is highly skewed to the left, while the GCC returns are

moderately skewed to the right. This means that there is a higher probability for investors

to get positive returns from the GCC markets rather than negative returns, as is the case

in developed and some other emerging markets (Harvey and Siddique, 1999). An

expectation of positive rather than negative returns in a portfolio of oil-sensitive GCC

8

stocks is a manifestation of anticipated higher compensation for the higher risk associated

with a narrowly diversified portfolio.

A stylized fact of individual financial time series is that they are non-stationary in

levels and stationary in the first differences; that is, they are I(1). In particular, shocks in

the level of an I(1) series are permanent whereas shocks to the first difference are

transitory. Two unit root tests, namely the augmented Dickey-Fuller (ADF) test and the

Phillips-Perron (PP) test, are utilized to test for the I(1) property3. Both of these tests

investigate the presence of a stochastic trend in the individual series.

The tests are first conducted in the natural logarithms of the levels of the spot oil

price variable and the five GCC stock index variables. Both tests show that all of the oil

and financial series are non-stationary in levels at the 5% significance level. They are

then carried out in first differences of the logarithms and the results of the tests suggest

that all of the individual series in first differences are stationary at the 5% significance

level4. In conclusion, all the series have a single unit root or are integrated of degree one,

I (1). Thus, all classical regressions using the level data, instead of first differences, will

produce spurious estimation results.

3. Empirical Model

As indicated above, we use the unobserved-component model with Markov-

switching heteroskedasticity (UC-MS model) by Kim (1993) and Kim and Kim (1996).

There are several benefits to adapting this model. First, we can incorporate regime shifts

3 We also used the KPSS test (1992), which confirmed that all the individual series are I(1), except MSMI. 4 The results of both the ADF and PP test are available on request.

9

in variance structures within the permanent and transitory framework. Second, Kim

(1993) points out that the ARCH and Markov-switching heteroskedasticity is that in the

case of the former the unconditional variance is constant but the latter for the

unconditional variance itself is subject to the regime change. Kim (1993) applied the

model to investigate the link between inflation and its uncertainty. He assumes that

inflation consists of a permanent and transitory component and decomposes two

components by UC-MS model. Kim and Kim (1996) also use the UC-MS

heteroskedasticity of stock returns. Their model is as follows:

* ,t t tP P z= + (1)

* * 21 , ~ (0, ),t t t t etP P e e Nµ σ−= + + (2)

2( ) , ~ (0, ),t t t utz L u u N σ= Ψ (3)

where tP is the natural log of stock price and *tP is the “fundamental” (permanent)

component and tz is fad (transitory) component. The stock return is given by

1 1( ).t t t t t tr P P e z zµ− −= − = + + − (4)

Equation (4) suggests that the stock return series consists of a constant mean plus noise

and transitory component tz . They assume that tz follows AR(2) process and propose a

model using UC-MC model by

1

[1 1] ,tt t

t

zr e

zµ

−

= + − +

(5)

11 2

1 2

.1 0 0

t t t

t t

z z uz z

φ φ −

− −

= +

(6)

Equation (5) and (6) is called the measurement equation and transition equation

respectively and we can rewrite equation (5) and (6) as the matrix form

10

t t ty H eµ β= + + (7)

1t t tF vβ β −= + (8)

where Markov-switching variances are two shocks related to the permanent and

transitory components.

2 2 21 1 1(1 ) ,et t et t eS Sσ σ σ= − + (9)

2 2 22 0 21(1 ) ,ut t u utS Sσ σ σ= − + (10)

where the two independent unobserved state variables, 1tS and 2tS , evolve according to

first order, discrete, two-state Markov processes with following transition probabilities

which determine the regime.

[ ] [ ]1 1 1 00 1 1 1 11Pr 0 | , 0 ,P r 1 | , 1t t t tS S p S S p− −= = = = = =

2 2, 1 00 2 2, 1 11Pr 0 | 0 ,Pr 1 | 1t t t tS S q S S q− −= = = = = = (11)

We can estimate the parameters by Kalman filter and Kim (1993)’s mixed collapsing

method. For more detail estimation procedure, refer to Kim and Kim (1996), and Kim

and Nelson (1998).

To identify the permanent and transitory component and its relationship within

GCC countries, we set the model as follows:

t t tr cτ= + (12)

0 1 1( ) , (0,1),t t t tQ Q S Nτ µ ε ε= + + : (13)

0 1 2( ) ( ) , (0,1),t t t tL c h h S e e Nφ = + : (14)

where tτ is the permanent part of the return and tc is the transitory (or temporary) part of

the return and we assume that it follows AR(1) process. The parameter 1h and 1Q indicate

11

the variance changes during periods of high variance state. The two independent

unobserved state variables, 1tS and 2tS , evolve according to first order, discrete, two-state

Markov processes with following transition probabilities which determine the regime.

[ ] [ ]1 1 1 00 1 1 1 11Pr 0 | , 0 ,P r 1 | , 1t t t tS S p S S p− −= = = = = =

2 2, 1 00 2 2, 1 11Pr 0 | 0 ,Pr 1 | 1t t t tS S q S S q− −= = = = = = (15)

The difference between our model and Kim and Kim (1996) model is that we assume the

AR(1) process of transitory components because AR(2) parameter is not statistically

significant for all GCC countries.5

4. Empirical Results

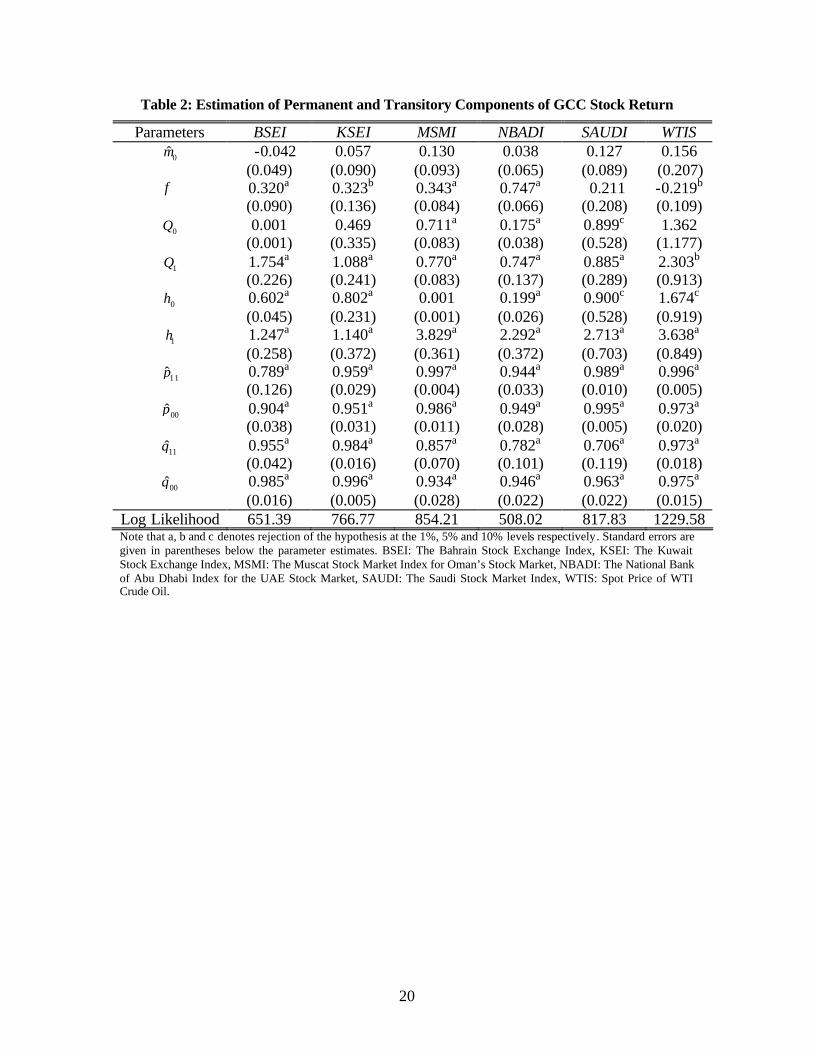

The estimates of the models suggest that two volatility return regimes exist in the

spot oil market and the stock markets of all the GCC countries except for Oman in the

low volatility state. This finding confirms the validity of using the Markov-switching

process in examining the return volatility in these markets. This finding is evident from

the statistical significance of the variances for both the low and high volatility regimes of

the two components as shown in Table 2. The estimates of transition probabilities for the

two regimes of both the permanent and transitory components are statistically significant

at the 1% level for all the countries. We find that the permanent component high

volatility regime variance, 1Q , is statistically significant for all countries. That is, when

the economy moves into the high volatility state, the variance of the permanent

5 More recently Bhar and Hamori (2004) use the same model as ours and applied their model to the stock markets of Germany, Japan, UK and the US.

12

component of the return increases for those countries significantly. We can evaluate the

magnitude of the overall variance of the permanent component variances by the adding

the low and high state variances. The permanent component of oil price return shows the

highest variance.

The estimates of the parameters of the weekly transitory component suggest

several implications. First, the transitional probability for both high and low volatility

regimes are statistically significant for all countries and the oil price returns. Second, in

our sample, the transitory low variance state, 00q is higher than 11q which suggest that the

low volatility state dominates the high volatility state. In other words, the transitory shock

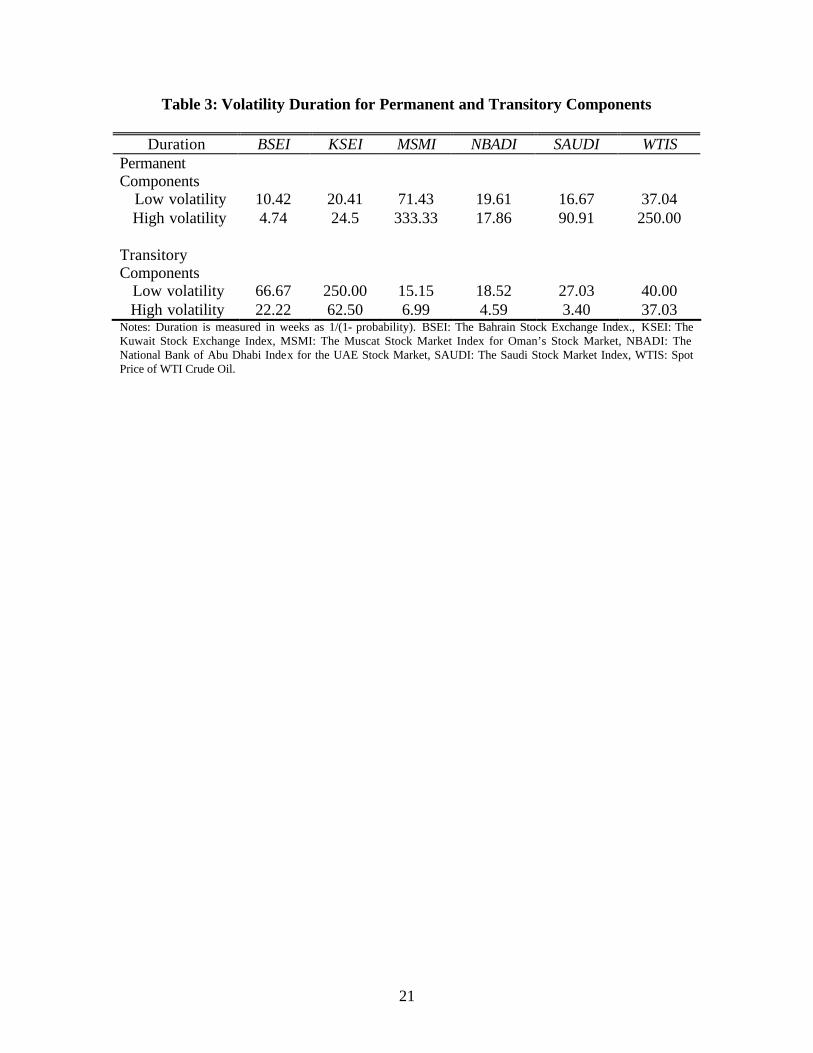

is short lived. The expected durations of the high volatility state (of transitory

component) for Bahrain, Kuwait, Oman, UAE, and Saudi are 22.2, 62.5, 7.0, 4.6 and 3.4

weeks, respectively as shown in Table 3, having an average of about 19.9. On the other

hand, the expected durations of the low volatility state (of transitory component) for

Bahrain, Kuwait, Oman, UAE, and Saudi are 66.7, 250.0, 15.2, 18.5 and 27.0 weeks,

respectively, having an average of about 75.4 weeks. The high volatility state variance is

higher than the low volatility state variance for all countries and it is clear that during the

high volatility state the uncertainty is much higher for those stock markets.

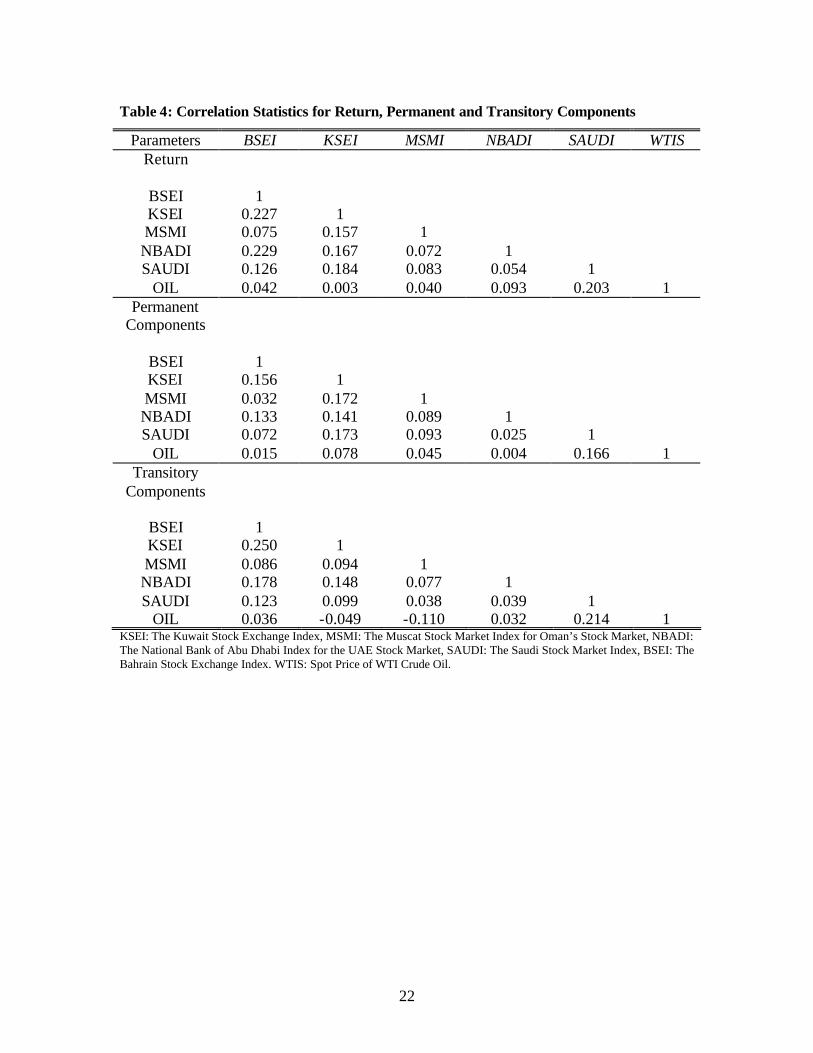

Table 4 shows the weekly correlation patterns for the return itself and its

permanent and transitory components between individual GCC countries. The correlation

patterns are positive for all the three returns measures, implying that these returns move

together in the short- and long-runs. This should not be surprising because these countries

are located in the same geographical region and share many common social and

economic characteristics including high dependence on the oil revenues. The highest

13

correlation in returns is between Bahrain and UAE (0.229), and between Bahrain and

Kuwait (0.227), implying that these two countries have the highest, same direction

movements in returns which makes these markets the least eligible candidates among the

GCC markets for portfolio diversification. Kuwaiti and UAE companies are listed on the

Bahrain stock Exchange. Still these return correlations are significantly low if compared

to those between Germany, Japan, UK and the US as reported in Bhar and Hamori

(2004), in the light of the GCC ‘s high dependence on oil. The lowest return correlation is

between Saudi and UAE (0.054), implying that these two countries are better candidate to

be combined in diversification-based portfolios when returns are in the high volatility

regime. However, the correlations for the permanent components provide different

results. The highest fundamental correlation is between Kuwait and Saudi Arabia (0.173).

This may be explained by the relatively high correlation between these countries’

fundamentals and that of the oil price. The lowest fundamental correlation is between

Saudi Arabia and UAE. In contrast to Saudi Arabia, the UAE fundamental has very low

correlation with the oil price returns. In terms of the transitory component, the highest

correlation is between Bahrain and Kuwait (0.250), and the lowest is between Oman and

Saudi Arabia (0.038).

As mentioned above, the GCC weekly return correlations with the oil spot price

return are surprisingly low for all GCC countries. This means that the oil price is only

one factor that moves the GCC stock markets on a weekly basis. The highest correlation

with the oil price return is for Saudi Arabia, which is the largest oil exporter in the world.

This correlation in terms of: the stock return itself is 0.203; the fundamental is 0.166; and

the transitory is 0.214. The lowest oil correlation for the fundamental is for UAE which is

14

also affected by regional tourism as well as by oil revenues. UAE has only one emirate

among its six united emirates that is a major oil exporter. It is surprising that Kuwait has

the lowest correlation for the return itself. However, it is possible that on weekly basis

and in a market that is highly sensitive to fads that the oil connection is weak.

5. Conclusions

Since the study clearly shows that there exist two volatility regimes in the two

components of all stock returns of the GCC countries, then risk-averse investors should

demand different compensations depending on the state of the economy and the shocks in

the components. Those GCC investors should ask for higher compensation in the high

volatility state regardless whether the shock hits the fundaments or the fads. Moreover,

sensitivity to return volatility during fad times is much higher than the volatility

sensitivity due to shocks in the fundamentals regardless of the return regime. It seems

that at times of increases in fads and speculative attacks noisy traders experience changes

in price misperceptions and that considerably increases the risk in all the GCC markets.

Thus those investors should ask for much higher premiums during fad times. .

Since sensitivity to return volatility varies across the GCC markets depending on

the state of the economy and the component of the return, the risk-averse investors in the

Oman market should particularly ask for the highest premium among the five GCC

markets during the high volatility state of the fad component, followed by investors in the

Saudi and the UAE markets. The Omani market should consider introducing financial

hedge instruments that can protect investors during fad times. The lowest fad premium

15

should go to investors in the Bahrain market which is more integrated with the world

stock market than the other GCC markets.

The spot oil market plays a very important factor in determining the returns of the

GCC stocks particularly during changes in the fundamentals and the fads. The additional

oil variance for both components is higher than that fo r most of the GCC markets. This

may explain why Bahrain, which is basically a non oil producing country, has the lowest

volatility sensitivity during fads.

The GCC markets also vary in the duration of volatility across regimes and for the

two components. Oman and Saudi Arabia have longer volatility durations as a result of

shocks in the fundaments such as the oil market than all those markets. In this case risk–

averse investors and traders in these two countries should opt for longer term investments

than in the other market to ride the volatility. Macroeconomic policy makers in these

countries should also be aware of the longer volatility and makes policies in times of fads

that stabilize the stock markets especially during speculative attacks in the oil market.

In terms of movements of the returns, all GCC returns move in the same direction

whether in terms of total return, fundamentals or fads under both volatility regimes,

suggesting that they are commoved by a common factor such as political stability,

liquidity and/or the oil price in the short and long-runs. The highest movements are

between Kuwait and Bahrain, and Bahrain and UAE which makes these markets the least

eligible candidates for portfolio diversification among the GCC markets. There are also

relatively high correlation between Kuwait and Saudi Arabia. Overall the correlations

among the GCC whether in terms of to the return itself, the fundamental and the fad are

low, suggesting that these countries are very different when it comes to return on

16

financial investment. Thus, investors should do their homework before investing in these

countries. Saudi Arabia has the highest correlation with the spot oil price but in general

the oil correlation weak, confirming the above point that there are country particularities

that influence the stock returns in addition to the oil price.

17

References:

Bhar, R. and Hamori, S. 2004. Empirical characteristics of the permanent and transitory components of stock returns: Analysis in a Markov-switching heteroscedasticity framework. Economic letters, forthcoming. Campbell, J. Y and Mankiew, N. G. 1987. Are output fluctuation transitory? Quarterly Journal of Economics 102, 857-880. Chu, C.-S., Santoni, G. J., and Liu, T. 1996. Stock market volatility and regime shifts in returns. Information Sciences 94, 179-190. Clark, P. K. 1987. The cyclical component of the US economic activity, Quarterly Journal of Economics 102, 797-814. De Lond, J. B., Shleifer, A., L. H., Summes, L. H. and Waldmann, R. J., 1990. Noise trader risk in financial markets. Journal of political economy, 98, 703-738. Fama, E. F. and French, K. R. 1988. Permanent and temporary components of stock prices. Journal of political economy, 96, 246-273. Glosten, L. K., Jagannathan, R. and Runkle, D. E. 1993. On the relation between the expected value and the volatility of the nominal excess return on stocks. Journal of Finance 48(5), 1779-1801. Hamilton, J. D. 1989. A new approach to the economic analysis of nopnstationary time series and the business cycle. Econometrica 57(2), 357-384. Hamilton J.D. and Susmel, R., 1994. Autoregressive conditional heteroscedasticity and changes in regime. Journal of Econometrics 64, 307–333. Hammoudeh, S. and Elesia, E. 2004. Dynamic relationships among GCC stock markets and NYMEX oil futures. Contemporary Economic Policy 22 (2), 250-269.

Hammoudeh, S. and Malik, F. 2004, Shock and volatility transmission in the NYMEX oil, US and Gulf equity markets. Paper presented at the Middle East Economic Association Meeting, San Diego, CA. Harvey, C. R. znd A. Siddique, 1999. Autoregressive conditional skewness. Journal of Financial Quantitative Analysis 43, 465 –487. Kim, C. J. 1993. Unobserved-component time series models with Markov-switching: Changes in regime and the link between inflation rates and inflation uncertainty. Journal of Business and Economic Statistics 11, 341-349.

18

Kim, C.J., and Kim, M. J. 1996. Transient fads and the crash of ’87. Journal of Applied Econometrics 11, 41-58. Kim, C. J., and Nelson, C. R. 1999. State Space Models with Regime Switching, Classical and Gibbs Sampling Approach with Application. The MIT Press, Cambridge, MA. Nelsson, C. R., and Plosser, C. I. 1982. Trends and Random walks in macroeconomic time series: Some evidence and implications. Journal of Monetary Economics 10, 139-162. McCarthy, J. and Najand, N.1995. State space modeling of linkages among international markets. Journal of Multinational Financial Management 5, 1-9. Porterba, J. M. and Summers, L. H. 1988. Mean reversion in stock prices: Evidence and implications. Journal of Financial Economics 22, 27-59. Schaller, H. and van Norden, S. 1997. Regime-switching in stock market returns. Applied Financial Economics 7, 177-191. Turner, R. F., Startz, R. and Nelson, C. F. 1989. A Markov model of heteroskedasticity, risk, and learning in the stock market, Journal of Financial Economics. 25, 3-22 . Watson, M. W. 1986.Univariate detrending methods with stochastic trends. Journal of Monetary Economics 18, 49-75.

19

Table 1: Descriptive Statistics of the GCC Stock Index and Spot Oil Price Returns

Notes: All variables are first differences of logs, and thus they represent rates of return. KSEI: The Kuwait Stock Exchange Index, MSMI: The Muscat Stock Market Index for Oman’s Stock Market, NBADI: The National Bank of Abu Dhabi Index for the UAE Stock Market, SAUDI: The Saudi Stock Market Index, BSEI: The Bahrain Stock Exchange Index. WTIS: Spot Price of WTI Crude Oil. a C.V. is called Coefficient of Variation, which is defined as the standard deviation divided by the mean.

Statistics BSEI KSEI MSMI NBADI SAUDI DOWI WTIS

Mean 0.983 1.612 1.927 1.329 1.002 1.972 21.121

Maximum 1.418 2.783 4.376 2.463 1.528 2.943 36.750

Minimum 0.679 0.393 1.000 0.878 0.675 0.921 10.860

Std. Dev. 0.192 0.482 0.767 0.338 0.223 0.664 5.460

C.Va 0.195 0.299 0.398 0.254 0.223 0.337 0.259

Skewness 0.149 0.610 1.387 0.979 0.596 -0.216 0.570

Kurtosis 1.885 2.655 4.319 3.601 2.123 1.572 2.702

Jarque-Bera 22.802 27.550 161.648 71.874 37.503 38.119 23.800

Probability 0.000 0.000 0.000 0.000 0.000 0.000 0.000

20

Table 2: Estimation of Permanent and Transitory Components of GCC Stock Return

Parameters BSEI KSEI MSMI NBADI SAUDI WTIS 0µ̂ -0.042

(0.049) 0.057

(0.090) 0.130

(0.093) 0.038

(0.065) 0.127

(0.089) 0.156 (0.207)

φ 0.320a (0.090)

0.323b (0.136)

0.343a (0.084)

0.747a (0.066)

0.211 (0.208)

-0.219b (0.109)

0Q 0.001 (0.001)

0.469 (0.335)

0.711a (0.083)

0.175a (0.038)

0.899c (0.528)

1.362 (1.177)

1Q 1.754a (0.226)

1.088a (0.241)

0.770a (0.083)

0.747a (0.137)

0.885a (0.289)

2.303b (0.913)

0h 0.602a (0.045)

0.802a (0.231)

0.001 (0.001)

0.199a (0.026)

0.900c (0.528)

1.674c (0.919)

1h 1.247a (0.258)

1.140a (0.372)

3.829a (0.361)

2.292a (0.372)

2.713a (0.703)

3.638a (0.849)

11p̂ 0.789a (0.126)

0.959a (0.029)

0.997a (0.004)

0.944a (0.033)

0.989a (0.010)

0.996a (0.005)

00p̂ 0.904a (0.038)

0.951a (0.031)

0.986a (0.011)

0.949a (0.028)

0.995a (0.005)

0.973a (0.020)

11q̂ 0.955a (0.042)

0.984a (0.016)

0.857a (0.070)

0.782a (0.101)

0.706a (0.119)

0.973a (0.018)

00q̂ 0.985a (0.016)

0.996a (0.005)

0.934a (0.028)

0.946a (0.022)

0.963a (0.022)

0.975a (0.015)

Log Likelihood 651.39 766.77 854.21 508.02 817.83 1229.58 Note that a, b and c denotes rejection of the hypothesis at the 1%, 5% and 10% levels respectively. Standard errors are given in parentheses below the parameter estimates. BSEI: The Bahrain Stock Exchange Index, KSEI: The Kuwait Stock Exchange Index, MSMI: The Muscat Stock Market Index for Oman’s Stock Market, NBADI: The National Bank of Abu Dhabi Index for the UAE Stock Market, SAUDI: The Saudi Stock Market Index, WTIS: Spot Price of WTI Crude Oil.

21

Table 3: Volatility Duration for Permanent and Transitory Components

Duration BSEI KSEI MSMI NBADI SAUDI WTIS Permanent Components

Low volatility 10.42 20.41 71.43 19.61 16.67 37.04 High volatility 4.74 24.5 333.33 17.86 90.91 250.00

Transitory Components

Low volatility 66.67 250.00 15.15 18.52 27.03 40.00 High volatility 22.22 62.50 6.99 4.59 3.40 37.03

Notes: Duration is measured in weeks as 1/(1- probability). BSEI: The Bahrain Stock Exchange Index., KSEI: The Kuwait Stock Exchange Index, MSMI: The Muscat Stock Market Index for Oman’s Stock Market, NBADI: The National Bank of Abu Dhabi Index for the UAE Stock Market, SAUDI: The Saudi Stock Market Index, WTIS: Spot Price of WTI Crude Oil.

22

Table 4: Correlation Statistics for Return, Permanent and Transitory Components

Parameters BSEI KSEI MSMI NBADI SAUDI WTIS Return

BSEI 1 KSEI 0.227 1 MSMI 0.075 0.157 1 NBADI 0.229 0.167 0.072 1 SAUDI 0.126 0.184 0.083 0.054 1

OIL 0.042 0.003 0.040 0.093 0.203 1 Permanent

Components

BSEI 1 KSEI 0.156 1 MSMI 0.032 0.172 1 NBADI 0.133 0.141 0.089 1 SAUDI 0.072 0.173 0.093 0.025 1

OIL 0.015 0.078 0.045 0.004 0.166 1 Transitory

Components

BSEI 1 KSEI 0.250 1 MSMI 0.086 0.094 1 NBADI 0.178 0.148 0.077 1 SAUDI 0.123 0.099 0.038 0.039 1

OIL 0.036 -0.049 -0.110 0.032 0.214 1 KSEI: The Kuwait Stock Exchange Index, MSMI: The Muscat Stock Market Index for Oman’s Stock Market, NBADI: The National Bank of Abu Dhabi Index for the UAE Stock Market, SAUDI: The Saudi Stock Market Index, BSEI: The Bahrain Stock Exchange Index. WTIS: Spot Price of WTI Crude Oil.