Embed Size (px)

Citation preview

Friday, June 1, 2018

COMMENTARYTHE MARKET’S PERFORMANCE AMID this week’s volatility shows many municipal investors are in it for the long haul. They need that coupon. . . . . . . . . 3

THE REGIONSTHE PUERTO RICO SENATE REFUSED to give in to an Oversight Board demand on labor regu-lations, the latest episode in a struggle over policy measures intended to pull the territory out of recession and help in the payment of its debt. . . . 5

WEB EXCLUSIVESILLINOIS NEEDS A PLAN TO TACKLE its rising tab for pensions and other fixed costs like retiree healthcare and debt service or its risks a drop into specu-lative grade territory, Moody’s Investors Service warned in a new report published as law-makers were casting final votes on a budget package.

THE NONPROFIT PLAYHOUSE SQUARE Foundation is using some of the proceeds of a tax-exempt, $80 million junk-bond offering to finance a $139 million, 34-story luxury apartment tower in downtown Cleveland’s theater district.

THE OWNERS OF FLORIDA’S PRIVATELY owned Brightline-branded passenger train system have been given more time to issue $1.15 billion of private activity bonds to finance portions of the project.

PENNSYLVANIA’S TREASURER AND A lawmaker have begun a review of the state’s two largest pension funds, the Public School Employees’ Retirement System and the Pennsylvania State Employees’ Retirement System.

FRIDAYwww.bondbuyer.com

Vol. 390 No. F467 N.Y., N.Y. THE DAILY NEWSPAPER OF PUBLIC FINANCE

CORONADO, CALIF. – The 2008 financial crisis wrought radical changes in the municipal market, but those changes may not have prepared the market for its next challenge, analysts said Thurs-day.

The legacy of the calamitous fi-nancial meltdown of ten years ago was the subject of a panel discus-sion at the National Federation of Municipal Analysts’ annual con-ference. The wide-ranging conver-sation touched on the changes in market conditions, the technolog-ical advancements in the industry, and the regulatory changes born from the reaction to the crisis.

“The things that happened ten years ago, it’s hard to even remem-

How the Financial Crisis Altered the Muni MarketBy Kyle Glazier

Turn to Analysts page 3

Muni Sales Show Signs Of Recovery

Municipal bond issuance rose for the third month in a row in May, raising expectations that vol-ume is on a path toward normalcy.

May 2018 volume was still down to $30.92 billion from $38.71 billion a year earlier, according to Thomson Reuters data. Issuers completed 985 transactions, off from 1,203 in May 2017. One month from the halfway point of the year, muni volume is sitting at $125.60 bil-lion, roughly 22% lower than the $161.69 billion of muni sales at this point a year ago.

New-money issuance increased 53.3% to $23.82 billion in 820 deals, up from $15.60 billion in 794 deals a year earlier.

“The main trend is of course not surprising: refundings are down massively compared to last year, as a result of the elimination of advance refundings,” which were banned under the new Fed-eral tax law, said Mikhail Foux, director of municipal research at Barclays Capital. “Meanwhile,

By aaron Weitzman

Turn to Volume page 14

Seven.She founded the firm five years

ago with the aim of using climate change forecasting models to help companies understand the poten-tial physical impacts on their as-sets and how to prepare for natural disasters, Mazzacurati said.

“We had done a lot of work on the risks for equities and real as-sets – and expanded our work af-ter we discovered a large demand from fixed income investors,” Mazzacurati said.

The company’s first clients were large corporations with hun-dreds of facilities.

The firm expanded its offerings two years ago when investment

companies became interested in the potential impact on companies in their portfolios. A few months ago, that expanded again to mod-eling the risk for municipalities.

“Climate risk is increasingly a part of our credit analysis for mu-nicipal issuers across the country,” said Andrew Teras, senior analyst at Breckinridge in a statement. “The climate risk scores devel-oped by Four Twenty Seven pro-vide a comparable way to evaluate climate exposure and will give us another factor for assessing our investment universe.”

Though the bond rating agen-cies are increasingly integrating

Four Twenty Seven, a Berke-ley, California, company that de-veloped software to track climate change risks for private compa-nies, wants to help bond investors evaluate the risks to cities and counties.

Focusing on climate change-based economic risk analysis, the company created a software ap-plication using data to model the risks for cities and counties after it received a request from Breck-inridge Capital Advisors, a fixed income fund manager.

“Many of us think that climate change is the greatest socioeco-nomic danger out there and that there is a need for markets to un-derstand the risks,” said Emilie Mazzacurati, founder and chief executive officer of Four Twenty

“We discovered a large demand from fixed income investors,” said Em-ilie Mazzacurati, founder and CEO of Four Twenty Seven.

Tracking ImpactsOf Climate

Turn to Firm page 4

By Keeley WeBster

Four Twenty Seven

MMA President Tom Doe said the MSRB has effectively joined the vendor data pool with the growing amount of data it collects and disseminates.

THURSDAY’S YIELDS

Complete market coverage appears on page 2

2.8

3.3

3.8

4.3

4.8

5/315/255/225/17

The Bond Buyer 40

2.8

3.0

3.3

3.6

3.9

4.1

4.4

4.7

5.0

JMAMFJDNOSAJ

To Maturity3.94 Down 0.01

To Par Call3.68 Down 0.02

001_BB06011801 1 5/31/2018 5:11:08 PM

The Bond Buyer2 Friday, June 1, 2018

Brainard Says Policy May Become More Restrictive

With gradual tightening continuing, mon-etary policy will become slightly restrictive as the neutral rate remains low, Federal Reserve Board Gov. Lael Brainard said Thursday.

“This outlook suggests a policy path that moves gradually from modestly accommo-dative today to neutral — and, after some time, modestly beyond neutral — against the backdrop of a longer run neutral rate that is likely to remain low by historical standards,” Brainard said in remarks pre-pared for delivery in New York, released by the Fed.

While the neutral rate should rise over the medium term, but her long-term outlook for the neutral rate remains.

“I expect current tailwinds to boost the neutral rate gradually over the medium term but leave little imprint on the long-run neutral rate,” she said.

“I continue to view gradual increases in the federal funds rate as the appropriate path,” Brainard added, “although I will re-main vigilant for the emergence of risks and prepared to adjust if conditions change.”

Discussing the flattening yield curve, Brainard noted, “So while I will keep a close watch on the yield curve as an important signal on how tight financial conditions are becoming, I consider it as just one among several important indicators. Yield curve movements will need to be interpreted within the broader context of financial conditions and the outlook and will be one of many considerations informing my assessment of appropriate policy.”

Brainard also noted the forward-guidance language in the post-meeting statements that the fed funds rate is likely to remain be-low its long-run levels “is growing stale and may no longer serve its original purpose.”

— Gary E. Siegel

Personal Income Data Show Inflation Just Below Target

Nominal personal consumption expendi-tures rose 0.6% in April, a stronger gain that expected, while core PCE prices rose 0.2% to keep the year/year rate at 1.8% after a March revision, both factors that will weigh on the minds of analysts ahead of the June FOMC meeting, data released by the Bureau of Economic Analysis Thursday morning suggested.

The core price index’s 1.8% year/year rise in April was unchanged from March after that month’s year/year pace was revised down after rounding. Either way, it remains well above the 1.5% rate seen in the first two months of the year before a special factor in March 2017 rolled out of the calculation.

The 0.6% gain in current dollar PCE, well ahead of the 0.4% rise expected, followed an upward revised 0.5% gain in March. Spending on durable goods rose 0.3% in the month, while nondurable goods spend-ing jumped 0.9% on a 1.5% gain in energy prices. Services spending was up 0.5%.

Real PCE was up only 0.4% in April, as the overall PCE price index was up 0.2% due to that gain in energy prices. The overall price index was up 2.0% year/year, the same as in March.

— Market News International

U.S. Jobless Claims Decline, Remain Above Recent Lows

Initial claims for U.S. state unemploy-ment benefits fell by 13,000 to 221,000 in the May 26 week, below the 224,000 level expected.

The four-week moving average rose by 2,500 to 222,250.

The level of continuing claims fell by 16,000 to 1.726 million in the May 19 week after rising by 30,000 in the previ-ous week. The four-week average for con-tinuing claims fell 8,500 to 1.744 million, another decades-low level.

— Market News International

INBRIEF

Government Securities Prices 10-year: 10011/32 to yield 2.83%, up 3/32

30-year: 10215/32 to yield 3.00%, up 9/32

Municipal Bond Index 12624/32, up 5/32

The Bond Buyer’s Total: $12.576 billion, up $1.945 billion

30-Day Visible Supply Competitives: $5.503 billion, down $60.7 million

(as of 6/01) Negotiated: $7.073 billion, up $2.006 billion

TheMuniCenter List Offering Total: $19.608 billion, down $436.0 million

Thursday’s Data

Thursday’s Economic Indicators

Indicator Last Report Forecast Actual

Initial Jobless Claims 5/19: 234,000 5/26: 225,000 5/26: 221,000Continuing Claims 5/12: 1.742M 5/19: n/a 5/19: 1.726M

Personal Income March: +0.2% April: +0.3% April: +0.3%

Consumption March: +0.5% April: +0.4% April: +0.6%Core PCE March: +0.2% April: +0.1% April: +0.2%Chicago PMI April: 57.6 May: 58.0 May: 62.7

Pending Home Sales March: +0.6% April: +0.5% April: -1.3% Forecasts represent the median of estimates by economists polled by IFR Markets

$-3B

$-2B

$-1B

$0

$1B

$2B

$3B

Five in a rowTax-exempt money market fund flows

Source: The iMoneyNet fund report

April 3

April 10

April 17

April 24

May1

May8

May15

May22

May29

As the last of the week’s larger new issues came to market, municipal bonds finished stronger on Thursday. Munis held on to the gains made earlier in the week as Trea-sury bonds also strengthened, while stocks slumped.

“As of late, muni market participants have been actively discussing supportive market technicals,” said said Mikhail Foux, director of municipal research at Barclays Capital. “Large summer redemptions are not new, and net issuance is almost always negative from June until August. Nevertheless, tax-ex-empts have frequently been underperforming Treasuries during those months. We believe that it might be rather hard for high grade tax-exempts to outperform Treasuries in the near term, and this week’s price action proves this point.”

Municipal bonds were stronger on Thurs-day, according to a late read of the MBIS benchmark scale. Benchmark muni yields fell as much as two basis points in the one-

to 30-year matur-ities.

H i g h - g r a d e munis were also stronger, with yields calculated on MBIS’ AAA scale falling by as much as one basis point across the curve.

Municipal Mar-ket Data’s AAA benchmark scale was unchanged, with yields steady in the 10-year general obligation muni and flat in the 30-year muni maturity.

Treasury bonds were stronger, with both the 10- and 30-year maturities yielding under 3%. Stock prices traded lower throughout the day.

On Thursday, the 10-year muni-to-Trea-sury ratio was calculated at 84.8% while

Market News

Municipals Hang On to Gains as Week’s Last Deals Pricethe 30-year mu-ni-to-Treasury rat io s tood at 95.2%, according to MMD. The muni-to-Treasury ratio compares the yield of tax-ex-empt municipal bonds with the yield of taxable U.S. Treasury with comparable maturities. If the

muni/Treasury ratio is above 100%, munis are yielding more than Treasury; if it is below 100%, munis are yielding less.

Treasury yields were being pulled lower by concerns around the future of Italy’s fi-nances and its membership in the European Union, Bill Merz, a director of fixed income at U.S. Bank Wealth Management, said a Wednesday market comment. Currently, Treasury yields are trading below the key technical level of 3%.

“Fundamentals still support modestly higher bond yields due to Fed rate hikes, rising inflation expectations, robust Treasury

issuance and softer foreign demand for Trea-suries. We continue to prefer shorter maturity bonds across asset classes, which offer com-pelling yields with less price risk from rising rates,” Merz said.

“Large summer redemptions are not new, and net issuance is almost always negative from June until August. Nevertheless, tax-ex-empts have frequently been underperforming Treasuries during those months. We believe that it might be rather hard for high grade tax-exempts to outperform Treasuries in the near term, and this week’s price action proves this point.”

Barclays Capital priced and repriced the Metropolitan Washington Airports Authori-ty’s $561.27 million of Series 2018A airport system revenue and refunding bonds subject to the alternative minimum tax.

Wells Fargo Securities priced and repriced Anchorage, Alaska’s $171.29 million of gen-eral obligation and GO refunding bonds.

In the competitive arena, the Virginia Transportation Board sold $149.61 million of Series 2018 transportation capital projects revenue bonds on Thursday.

Morgan Stanley won the bonds with a true interest cost of 3.3091%. q

By Chip Barnett & Christine alBano

002_BB06011801 2 5/31/2018 5:11:11 PM

www.bondbuyer.com 3Friday, June 1, 2018 Commentary

What Italy’s Government Machinations Mean for MunisThe recent government machinations in

Italy and the consequent market reactions in sovereign bonds and currencies are reminis-cent of the fallout earlier this decade from developments in Greece. Although Italy’s GDP is not growing as fast as officials would desire, the finances are not encountering as much difficulty as Greece. What are the im-plications for the municipal market?

The volatility that was on display earlier this week with Italian bonds could easily hap-pen here once again. We have a significant mid-term election that has the possibility of redirecting fiscal and monetary policy until 2020. Although we have a federal budget agreement for a couple of years, factors could change rapidly after that period of bipartisan agreement.

Of course, we are not concerned about any currency change, but we are focused on a stronger or weaker dollar. Though a some-what weaker dollar may serve to support more trade, it is far from clear whether we are going to have a renegotiated NAFTA and whether or not we will have much higher tariffs on foreign goods, including up to a potential 25% on imported vehicles.

Municipals rallied significantly along with Treasury equivalents as Italy has veered. In some aspects, municipals even out-rallied

the taxable markets. We reversed course after the last couple of days as the equity markets recovered from the initial shock.

The initial reactions in the municipal mar-ket could have been even more pronounced. Underlying the bid in the market and the

market tone is the sharp reduction in munic-ipal supply. Supply YTD is running about 22% below last year’s volume. This condition begs the question: what will happen when we have a spike in supply with one of the many percolating event risks taking place simul-taneously? I trust that you already know the answer. Spreads have the tendency to widen holding other factors constant.

The market has not violently overreacted because we know that the economy is in fine shape at the moment. Corporate earnings have been strong, as we have just witnessed through the cycle, and unemployment is at a decade-plus low. We are just ever vigilant about what domestic policies or global forces may upend the balance.

The bid side for municipal paper remains strong, in part due to the continuing positive flows to the mutual funds. In the new tax environment, even though some demand is undoubtedly affected by the reduced corpo-rate rate, many individuals leaving out high net worth individuals are more affected by the cap on SALT deductibility. There are few alternatives to the favorable status of the tax exemption.

The recent volatility has proven that many municipal investors are in the product for the long haul. They need that coupon. It hasn’t caused municipal investors to either pile in or to flee from the paper. The only real com-

ponent of the buyer base that can exhibit this behavior and to take advantage of disloca-tions is the institutional side.

There is no real fear of contagion in our market at present. Despite a cautious ap-proach to acting as principal and taking on more exposure, the broker-dealers have been providing ample liquidity. Bid lists are often posted and have been withdrawn or cancelled at times. The lists that are out there tend to be well bid. We do not see this changing, given the present tone.

Of course, the FED is a stabilizing force when the markets are in flux. The FED has been careful about tightening and slowing the application as the data dictates.

If the Eurozone is to be challenged by a potential exit by Italy, there is no doubt there would be a marked reaction in the markets. We would expect that municipals would re-act in a partially correlated way with the Treasury market. However, given the prob-able supply scenario remaining at a lower level, we would not expect municipals to overcompensate. What is instructive about the situation in Italy is that fiscal policy can be radically changed in swift fashion. We await the mid-terms for clues about the future course for the market.

John Hallacy is contributing editor of The Bond Buyer.

By John hallacy

Congratulations Ginny Housum!

UMB.com | 816.860.7000

UMB Bank congratulates Virginia (Ginny) Housum on her recognition at the NFMA 35th Annual Conference for her contributions to the municipal analyst industry.

Member FDIC

ber,” said Mary Colby, vice president and head of municipal research a Charles Schwab Investment Management. Colby said change has been so dramatic in the muni market from that time, noting for example the sharp decline in bond insurance coverage.

Tom Doe, president of Municipal Market Analytics, said that although the marketplace has access to far more data now than it did ten years ago, some of the fundamental chal-lenges have not gone away.

“Trading really hasn’t changed in terms of the volume,” Doe said. “Liquidity remains an issue. We don’t have more liquidity just because we have more offerings, more bonds available.”

Doe said that the market has not yet per-fected how to use all the data now available. A former Municipal Securities Rulemaking Board member, Doe said that the MSRB has now effectively joined the data vendor pool as the amount of data it collects and dissem-inates has grown over the years. “They are now a player in the vendor space,” Doe said, adding that he and others have speculated that the MSRB should split into rulemaking and data divisions.

Doe said current increases in risky issu-ances as a percentage of the overall market -- a product of the low interest rate environ-ment that has persisted since the crisis -- are somewhat similar to the run-up to the crisis when risky issuance became more common for several quarters.

The panelists also discussed the significant regulatory changes that occurred as a result of the crisis, saying that they were generally

well-intentioned but in some cases were not effective or were misguided.

“I think the concern with systemic risk was well-placed,” said Rick Cosgrove, a partner at the law firm of Chapman and Cut-ler. But despite the efforts of lawmakers to reduce systemic risk through the Dodd-Frank Act, Cosgrove said, some of the banks are larger than they were before the crisis.

Colby and Cosgrove also agreed that ten-der option bonds, or TOBs, were unfairly swept up in regulatory changes. The Volcker Rule, named for former Federal Reserve Board chairman Paul Volcker and part of Dodd-Frank, was aimed at restricting pro-prietary trading by banks. The rule restricted banks and their affiliates from sponsoring a TOB program or owning a residual certifi-cate issued by a TOB trust, forcing bankers to come up with new structures to cover the market. “A lot of us felt TOBs got mistreat-ed,” said Cosgrove.

Moderator Alex Wallace, a managing di-rector at U.S. Bank, said he thinks Dodd-Frank‘s creation of a municipal advisor regulatory regime was responsible for the popularity of bank direct lending over the past decade.

“The municipal advisor rule has been a significant change in our marketplace,” said Wallace. “I do believe that additional burden contributed to an increased interest in the direct purchase market.”

Panelists said they are not convinced the market is prepared for the next potential cri-sis.

“I think the jury is out, Doe said.“I think we have a lot of work to do,” Wal-

lace said. q

Analysts Reflect on Changes in Muni Market Since Financial CrisisContinued from page 1

The bid side for municipal paper remains strong amid international market volatiltiy, Hallacy writes.

003_BB06011801 3 5/31/2018 5:11:12 PM

The Bond Buyer4 Friday, June 1, 2018

TRENDS IN THE REGIONFar West

Firm Pinpoints Governments FacingGreatest Risks From Climate Change

climate risk into their municipal ratings, they lack concrete metrics that compare and assess how cities and counties are exposed to specific hazards, according to a report the company released last week.

Four Twenty Seven provides local cli-mate risk scores that provide comparable, forward-looking data to fill this gap, Maz-zacurati said.

“Each city and county is assigned a score based on how it ranks nationwide, which provides investors with comparable detail to complement the assessments of credit rating agencies,” according to the report.

The firm took global climate change models used by international research in-stitutions and created a set of scores for U.S. cities and counties above a certain population, she said.

The software application created by Four Twenty Seven processes trillions of bytes of data boiling it down to a few characteristics, she said. For instance, the firm can compare flooding problems in various counties and rank them on a risk basis.

The report outlines the firm’s approach to measuring exposure to climate hazards and pinpoints the cities and counties most exposed to the impacts of climate change.

“This new dataset provides a compre-hensive suite of risk scores to better inform ratings and pricing decisions,” Mazzacurati said. “The risk scores will be very helpful for all market participants, including muni bond investors, local governments, and ratings agencies.”

The research targets five major climate categories: cyclones and hurricanes, sea level rise, extreme rainfall, heat stress, and water stress. It covers all 3,143 U.S. coun-ties and 761 cities with populations over 50,000 as of 2015.

“This fits squarely in the realm of in-formation that the market wants to know – including us,” said Kurt Forsgren, an S&P Global Ratings analyst.

Four Twenty Seven appears to be the first to release this sort of data, but there are oth-er companies with similar efforts that are trying to provide such information down to zip codes, Forsgren said.

“As a market participant, we recognize there are credit risks associated with chang-es in the environment,” Forsgren said. “We would be a consumer of this information. Much as we look at long-term forecasts of financials and look at engineering reports to form credit views, we would be very interested in this information.”

S&P and Moody’s Investors Service both released reports in 2017 explaining their methodologies for incorporating climate change into their municipal credit ratings. Fitch Ratings just released a report Tuesday explaining its approach.

“Our earlier piece recognized that the muni market has had risks like this for years. There have always been hurricanes,” Forsgren said. “What is different is that we are getting more, and better information, of what those risks are, and we have begun to see what the exposures are if those risks are not addressed.”

The rating agencies all consider financial management, planning and the economic diversity of the municipalities in their ap-proaches.

But in the absence of forward-looking climate projections, the estimates used by the rating agencies “may grossly underes-timate the magnitude of future risks, or at least fail to characterize the type of climate risks that may eventually make it more dif-ficult for a municipality to meet its financial obligations,” according to the firm’s report.

Moody’s published a report in Novem-ber listing six indicators it uses “to assess the exposure and overall susceptibility of U.S. states to the physical effects of cli-mate change.” For instance, the indicators included the share of economic activity for the states that comes from coastal areas or homes located in a flood plain.

Fitch Ratings analysts wrote that they

consider environmental factors in their credit ratings through the lens of a fun-damental credit risk. Fitch also noted that “the federal government approved $130 billion in aid for natural disasters last year, a considerable 0.7% of the country’s $19.7 trillion economy.”

Fitch analysts said they don’t anticipate such a scenario, but added that if the federal government pulled back on its current level of aid it would be a credit negative for cities and counties.

The federal government’s role in disaster response is critical in mitigating natural disaster risk for ratings on state and local governments,” said Michael Rinaldi, a Fitch senior director.

With the exception of Hurricane Katrina in Louisiana, rating actions directly linked to climate change or natural disasters have historically been limited; but the kind of damage to vital infrastructure and wide-spread depopulation that occurred during Katrina have become more commonplace, most recently with the hurricanes that struck the southeast last year, Fitch said.

In addition to providing information to rating agencies and investors, the compa-ny’s analysis can also help municipalities better prepare for natural disasters, said Nik Steinberg, Four Twenty Seven’s director of analytics.

Every region of the country has unique vulnerabilities to weather-related disasters, according to the report.

The coastal areas with the highest ex-posure to problems from rising sea levels are the San Francisco Bay Area, the Pacific Northwest, New Jersey and Virginia in the mid-Atlantic region and North Carolina and Florida.

The southeast has the greatest exposure to cyclone and hurricane risk, which tend to be less frequent and weaker in the mid-At-lantic and Northeast. The Midwest has the greatest exposure to heightened flood risk due to changing rainfall patterns.

Drought and the potential for wildfires

falls in the “water stress” category – a con-dition expected to worsen in the Southwest, Pacific Northwest and Western Pacific.

Eight major cities in California could face downgrades in the absence of water supply alternatives and sustained cutbacks in use, according to the report.

Key watersheds for agricultural produc-tion such as the Central Valley aquifer sys-tem in California and the Ogallala Aquifer in the Great Plains are highly exposed to water stress.

The agriculturally-dominated areas of Bakersfield, Delano, and Visalia, Califor-nia, along the Central Valley Aquifer are among the ten cities most exposed to water stress. Similarly, municipalities along the Ogallala Aquifer in the Great Plains also rely heavily on agriculture and are among the most exposed to water stress.

The Southeast and the Midwest, concen-trated in Missouri and western Illinois and fanning out to the Great Plains, Mississippi River Basin and Florida, have the greatest exposure to heat stress.

Rising temperatures pose “serious risks to the nation’s energy infrastructure and labor force,” according to the report.

The highest heat stress scores in the re-port tend to be centered in the Southeast and Midwest, concentrated in Missouri and western Illinois and then fanning out to the Great Plains, Mississippi River Basin, and Florida. The desert Southwest and agricul-turally-dominated counties in the Sacra-mento Valley and southeastern Washington State also had high heat scores.

Extreme temperatures grounded flights in Phoenix last July and could drive up en-ergy costs for car manufacturers that have moved to Missouri, the report said. q

For more content about this region, visit the Regional News tab on BondBuyer.com.

Continued from page 1

Alaska Aa3/AA/AA 1.68 2.18 2.76 2.87

California Aa3/AA–/AA– 1.58 1.97 2.42 2.89

Hawaii Aa1/AA+/AA 1.65 2.05 2.53 3.03

Idaho Aa1/AA+/AA+ 1.63 2.10 2.59 3.06

Montana Aa1/AA/AA+ 1.63 2.08 2.58 3.06

Nevada Aa2/AA/AA+ 1.66 2.09 2.61 3.11

Oregon Aa1/AA+/AA+ 1.63 2.02 2.48 2.96

Washington Aa1/AA+/AA+ 1.65 2.05 2.58 3.07

Wyoming NR/AA+/NR 1.63 2.03 2.46 2.94

State Ratings One-Year Five-Year 10-Year 30-Year

General ObliGatiOn Yield Curves fOr MaY 30, 2018

Sources: Municipal Market Data, Moody’s Investors Service, Standard & Poor’s, Fitch Ratings

Alaska 1 $164,860 1 $164,860 $0

California 9 2,135,670 8 583,014 1,552,656

Hawaii 0 0 0 0 0

Idaho 1 3,485 2 86,285 –82,800

Montana 0 0 0 0 0

Nevada 2 296,520 1 100,000 196,520

Oregon 0 0 0 0 0

Washington 3 396,080 5 91,455 304,625

Wyoming 0 0 0 0 0Sources: Ipreo, The Bond Buyer

May 31, 2018 May 24, 2018State Issues Amount Issues Amount Chg in Amt

visible supplY bY state

Dollar amounts are in thousands

004_BB06011801 4 5/31/2018 5:11:12 PM

www.bondbuyer.com 5Friday, June 1, 2018 Regions

Settlement is in Sight for Harvey Pension Intercept DisputeCHICAGO – Harvey, Illinois, and its

pension funds are working to finalize a settlement that would free up some state-intercepted revenues for the fis-cally distressed city while satisfying the funds’ demands for overdue contri-butions.

A court hearing scheduled Thursday before Cook County Circuit Court Judge Raymond Mitchell on a preliminary injunction involving the status of $2.3 million intercepted by state Comptroller Susana Mendoza was moved to Tuesday.

“Hopefully, we are there,” said Har-vey’s attorney, Bob Fioretti of Roth Fio-retti LLC. “We are working to satisfy the statutory pension requirements by 2040 and meet the needs of the city.”

Fioretti cautioned that the deal was far from final and the city has seen pre-vious settlements it thought were on firm ground fall apart.

The percentages each would receive from the pot of about $7 million in state collected city revenues also could change.

The police fund has agreed to the lat-est settlement version and the firefight-ers’ fund board was slated to consider it by the end of the week so it could be presented to the judge Tuesday.

Firefighters’ fund attorney Andrew

Schwartz, of Schwartz & Kanyock LLC, confirmed the fund was working on a settlement but declined any further com-ment. The police fund’s lawyer, Michael Moirano, of Moirano Gorman Kenny LLC, did not respond to a request for comment.

The fiscally distressed city had been seeking to keep at least 75% of its funds to cover payroll and critical services but the latest settlement version requires the city to give up more.

“The city is tightening its budget” to address the higher amount it would forgo, Fioretti said.

The Harvey fund diversions are the first to take place under a 2011 public safety pension funding law that allows for “state funds” to be intercepted to pay overdue actuarially based contri-butions to pension funds. The police fund was the first to file to cover a $7 million judgment and firefighters soon after filed requesting payment on a $12 million judgment.

The city challenged the police fund’s certified diversion request.

Mendoza concluded her review last week of the city’s protest, finding that the police fund was eligible to receive the city’s share of state sales taxes and other funds.

The office has concluded it has no discretion under the law to divvy up the

revenue between the pension funds or the city.

The judge granted a temporary re-straining order last week blocking the comptroller’s distribution of the $2.3 million to the police fund. The court did free up the city’s share of home rule sales taxes after the comptroller’s con-cluded they don’t count as “state funds.”

Those funds had previously been go-ing directly to the trustee -- Amalgam-ated Bank of Chicago -- on $6 million of city revenue bonds along with the city’s share of state sales taxes. State sales taxes are now subject to intercep-tion, but the freed-up home rule reve-nue should be sufficient to cover about $600,000 in annual debt service.

The settlement is complicated by con-flicts between the police and firefighter funds. The police fund was the first to submit an official claim and has argued it should receive priority status. The firefighters’ fund argues it should share in the funds. The individual boards are also divided among retiree members and working members who have divergent interests.

Mitchell has made clear during recent hearings of his preference for a settle-ment and the comptroller’s office, which is represented by Attorney General Lisa Madigan, hopes also for a settlement or guidance on how to manage claims.

Market participants are watching closely to see how the Harvey case plays out because it raises short- and long-term questions. Rating agencies have warned a flood of other pension funds could follow the Harvey funds’ lead and there are several hundred that have been shorted by their government sponsors.

The intercept also has sparked wor-ries that bondholders’ legal claims will fall behind pensioners and could lead to impairment as distressed governments look for ways to preserve funding for critical services.

Moody’s Investors Service warned this week in a report that certification of the police fund’s diversion represented a credit negative for all of the state’s lo-cal governments as it further reinforces the idea that holders of Illinois local government bonds fall behind pension funds.

If a settlement is finalized, Harvey’s lawsuit challenging the legality of the diversion of funds will be dropped so questions over the law’s enforcement and priority status won’t be settled un-less there is a challenge in another city.

Harvey’s lawsuit argues that critical services and bondholders have a supe-rior claim to the pension judgments and its revenues can’t be diverted to cover judgments. q

By yvette ShieldS

BB 20-Bond Index BB Revenue Bond IndexBB 11-Bond Index

3.0

3.5

4.0

4.5

5.0

5/315/24

5/175/10

5/34/26

4/194/12

4/53/28

3/223/15

3/82.5

3.0

3.5

4.0

4.5

5/315/24

5/175/10

5/34/26

4/194/12

4/53/28

3/223/15

3/83.7

3.9

4.2

4.4

4.7

5/315/24

5/175/10

5/34/26

4/194/12

4/53/28

3/223/15

3/8

BB Municipal Bond Index Yield to Maturity

4.0

4.3

4.7

5.1

5.5

5/315/24

5/175/10

5/34/26

4/194/12

4/53/28

3/223/15

3/8

Figures are weekly averages for daily yields from the BB40 ending Thursday

3.78%Down 0.12

3.26%Down 0.12

4.27%Down 0.12 3.96%

Down 0.06

The Bond Buyer Indexes

The Puerto Rico Senate refused to give in to an Oversight Board demand on labor regulations, the latest episode in a struggle over policy measures intended to pull the territory out of recession and help in the payment of its debt.

The Senate on Wednesday voted 22-9 for a measure that would introduce at-will employment only for employees entering the workforce in the future. The Oversight Board had demanded a repeal of Law 80 — which since 1976 has allowed Puerto Rico employees to appeal terminations — for all of the island’s workers.

The repeal of the law was part of a May 20 compromise between the board and

Gov. Ricardo Rosselló over the board’s April-approved fiscal plan. The board agreed to drop the plan’s elimination of the Christmas bonus and reductions to mandatory vacation and sick days. In ex-change, the governor agreed to introduce at-will employment on the island.

In the agreement with the board, the governor said that he would approve at-will employment on or before June 27 and that the new status would become effective on Jan. 1, 2019.

Senators from the governor’s New Progressive Party voted in favor of the watered down termination law change. Members of the Popular Democratic Party, one member of the Independence Party, and one unaffiliated Senator cast the op-

position votes.“We said that we were not going to re-

peal Law 80 and we did not repeal it, we said that we were going to protect the workers and we are doing it, this remains clear,” said Senate President Thomas Ri-vera Schatz, a member of the NPP with the governor.

On Thursday the board said that the Senate’s action is “inconsistent with the understanding reached with the govern-ment and with the revised Fiscal Plan.”

It remains to be seen how the conflict over the employment laws plays out.

However, on Thursday, board Chairman José Carrión, said, “The [fiscal plan’s] fiscal and structural reforms, including the changes proposed by the governor which

are contingent on the approval of legisla-tion by the end of this fiscal year to make Puerto Rico an ‘at-will employment’ juris-diction (repeal of Law 80) for current and new employees, will help return growth to our island’s economy.”

On Thursday the board released a re-certified fiscal plan with changes to labor reforms and other sections from the April-approved plan. If Puerto Rico’s gov-ernment were not to repeal Law 80, the board could conceivably try to force the local government’s hand on the matter and also return to the April plan’s stricter approach on other labor policies.

The board said it agreed to the new re-certified fiscal plan by unanimous writ-ten consent. q

Puerto Rico Oversight Board, Senate Clash Over At-Will Labor DemandBy RoBeRt Slavin

005_BB06011801 5 5/31/2018 5:11:14 PM

The Bond Buyer6 Friday, June 1, 2018Legal Notices

NOTICE OF SALE

TOWNSHIP OF MAPLEWOOD, IN THE COUNTY OF ESSEX, NEW JERSEY

$17,130,000* GENERAL IMPROVEMENT BONDS(Book-Entry-Only Bonds)/(Callable)/(Not Bank Qualified)

SUMMARY

Dated: Date of Delivery – On or about June 28, 2018Bid Date and Time: June 12, 2018 at 10:30 a.m. to 10:45 a.m.Type of Sale: Electronic Open Auction Interest: Multiple Interest Rates - multiples of 1/8 or 1/20 of 1% Legal Opinion: McManimon, Scotland & Baumann, LLC, Roseland, NJMaturity Schedule: February 15 as set forth in the following table:

Year Principal Amount Year Principal Amount 2019 $860,000 2025 $1,720,000 2020 $860,000 2026 $1,720,000 2021 $860,000 2027 $1,720,000 2022 $880,000 2028 $1,720,000 2023 $1,675,000 2029 $1,720,000 2024 $1,675,000 2030 $1,720,000

Preliminary Official Statement, Notice of Sale and other details available at www.GrantStreet.com

*Preliminary, subject to change, as described herein.

United StateS diStrict coUrt For the diStrict oF PUerto ricoIn re:The FInancIal OversIghT and ManageMenT BOard FOr PuerTO rIcO, as representative ofThe cOMMOnWealTh OF PuerTO rIcO, et al. debtors.

PrOMesa Title III

case no. 17 BK 3283-lTs(Jointly administered)

notice oF eXtended deadLineS For FiLinG ProoFS oF cLaiM

deadLine eXtenSionto aLL creditorS oF the deBtorS, and to other PartieS in intereSt, PLeaSe taKe notice oF the FoLLoWinG:

The Financial Oversight and Management Board for Puerto rico has filed voluntary petitions under section 304(a) of the Puerto Rico Oversight, Management, and Economic Stability Act (“PrOMesa”),1 initiating Title III cases under PrOMesa (each, a “Title III case” and collectively, the “Title III cases”) for the debtors listed below (each, a “debtor” and collectively, the “debtors”). You may be a creditor of one of the debtors, and you may be required to file a proof of claim (“Proof of claim”).

the deadline to file a proof of claim has been extended to June 29, 2018 at 4:00 p.m. (atlantic time).if you have already filed a Proof of claim, no further action is required unless directed by court order, notice,

or otherwise. a list of the names of the debtors, their case numbers, and the commencement date of the debtors’ Title III cases is as follows:

title iii cases Federal tax id no. case no. commencement datecommonwealth of Puerto rico 3481 17 BK 3283 May 3, 2017Puerto rico sales Tax Financing corporation (“cOFIna”) 8474 17 BK 3284 May 5, 2017employees retirement system of the government of the commonwealth of Puerto rico (“ers”)

9686 17 BK 3566 May 21, 2017

Puerto rico highways and Transportation authority (“hTa”) 3808 17 BK 3567 May 21, 2017Puerto rico electric Power authority (“PrePa”) 3747 17 BK 4780 July 2, 2017

Key Points• InaTitleIIIproceedingunderPROMESA,creditorsmayberequiredtofileclaimformsstatingtheamountofmoneyowedto

them as of the day the Title III proceeding was filed. This notice explains how to file claims.• Many creditors in the title iii cases are not required to file a claim. For more information, please refer to the

claims agent’s website at https://cases.primeclerk.com/puertorico/, call the claims agent at (844) 822-9231 (toll free for u.s. and Puerto rico) or (646) 486-7944 (for international callers), available 10:00 a.m. to 7:00 p.m. (atlantic standard Time) (spanish available), or email at [email protected].

• if you are not required to file a claim, you do not need to complete and return a claim form, and you will still keep your rights to vote on a plan of adjustment and receive payments under the plan. a plan of adjustment is a document that explains how a debtor proposes to pay the amounts it owes to its creditors. Once filed, this plan will be available for creditors to review. Who gets to vote on the plan will be determined at a later date. The amount you may receive under the plan also will be determined later.

• if you are required to file a claim against any of the debtors, the deadline to do so has been extended to June 29, 2018 at 4:00 p.m., atlantic Standard time. To obtain a form that you may use to file your claim, refer to the contact infor-mation below.

• Claims may be filed (a) electronically on the Claims Agent’s website at https://cases.primeclerk.com/puertorico/EPOC-Index, (b) by overnight courier to commonwealth of Puerto rico claims Processing center c/o Prime clerk, llc, 850 Third avenue, suite 412, Brooklyn, nY 11232, (c) by first class mail to commonwealth of Puerto rico, claims Processing center, c/o Prime clerk llc, grand central station, P.O. Box 4708, new York, nY 10163-4708, or (d) by hand delivery at the claim Form drop-Off locations identified in the Information center on the claims agent’s website at https://cases.primeclerk.com/puertorico/ePOc-Index.

Afterreadingthisnotice,ifyourequireadditionalinformation,youmaycontacttheClaimsAgentat(844)822-9231(tollfreefor u.s. and Puerto rico) or (646) 486-7944 (for international callers), available 10:00 a.m. to 7:00 p.m. (atlantic standard Time) (spanish available), or by email at [email protected]. Please note that the people answering the phone number arenotabletoprovidelegaladvice.Ifyouhavequestionsaboutyourlegalrights,includingwhetheryouneedtofileaclaim,youshould talk to an attorney.1 PrOMesa is codified at 48 u.s.c. §§ 2101-2241.

006_BB06011801 6 5/31/2018 2:03:39 PM

www.bondbuyer.com 7Friday, June 1, 2018

For more inFormation, contact:

John hester (212)-849-5125James Kellum (212) 849-5156

• Full service electronic document delivery and tracking system

www.i-dealprospectus.com

I-DEAL PROSPECTUS ELECTRONIC OFFICIAL STATEMENTSNegotiated

Garland (city oF), tX combo taX & rev coo, series 2018massachusetts housinG Finance aGency, ma housinG bonds, series 2018 a&bhouston isd, tX ltd taX schoolhouse bonds, series 2018 houston isd, tX maintenance taX notes, series 2018 northwest isd, tX unltd taX school bldG bonds, series 2018sienna Plantation manaGement district, tX unlimited taX reFundinG bonds, srs 2018 san marcos (city oF), tX Go bonds & combo taX & revenue coo, series 2018 Katy isd, tX unlimited taX school buildinG bonds, series 2018mesa (city oF), aZ General obliGation bonds, series 2018 **Pos suPPlement has been added**houston isd, tX variable rate limited taX reFundinG bonds, series 2012houston isd, tX variable rate limited taX schoolhouse bonds, srs 2013bhouston isd, tX variable rate ltd taX schoolhouse bonds, series 2014a-1bst. martin (Parish oF), la hosPital service dist no. 2, Go bonds, srs 2018**s&P ratinGs rePort has been added**anderson county, tX unlimited taX road bonds, series 2018bucKeye (city oF), aZ roosevelt street imProv dist imProvement bonds, series 2018leander (city oF), tX General obliGation reFundinG bonds, series 2018st. martin (Parish oF), la hosPital service dist no. 2, Go bonds, srs 2018shrevePort (city oF), la water & sewer revenue bonds, Junior lien srs 2018cGarland (city oF), tX water & sewer system revenue reFundinG bonds, new series 2018el Paso isd, tX unlimited taX reFundinG bonds, series 2018FranKlin (county oF), oh various PurPose sales taX revenue bonds, series 2018venus (city oF), tX combination taX & rev coo, series 2018Garland (city oF), tX electric utility system rev reF bonds, new series 2018revenue authority oF Prince GeorGe’s county, md lease rev reF bonds, srs 2018a&bmesa (city oF), aZ General obliGation bonds, series 2018mesa (city oF) aZ, utility systems revenal bonds, srs 2018 Goodyear (city oF), aZ mcdowell road commercial corridor imProv dist reF bonds, srs 2018sPrinG branch isd, tX unlimited taX schoolhouse bonds, series 2018mesquite (city oF), tX ww&ss rev reF & imProv bonds, series 2018 mesquite (city oF), tX Go reF&imPrv bonds & combo taX<d surPlus rev coo, srs 2018 northside isd, tX unlimited taX reFundinG bonds, series 2018 tennessee hda, tn residential Finance ProGram bonds, issue 2018-2 (non-amt)montGomery county, tX unlimited taX road bonds, series 2018Fort bend isd, tX unlimted taX reFundinG bonds, series 2018lewisville isd, tX unlimited taX reFundinG bonds, series 2018Gilbert (town oF), aZ wrmPc senior lien utility sys rev bonds, srs 2018hutto isd, unlimited taX school buildinG bonds, series 2018conroe (city oF), tX limited taX reFundinG bonds, series 2018hutto economic develoPment corP tyPe b, tX sales taX rev bonds, taXable srs 2018temPle isd, tX unltd taX school buildinG bonds, series 2018

I-DEAL PROSPECTUSELECTRONIC OFFICIAL STATEMENTSCompetitive

6/11-harris county mud no. 537, tX unlimited taX road bonds, series 20186/12-arlinGton (city oF), tX municiPal drainaGe utility system rev bonds, series 20186/12- arlinGton (city oF), tX water & wasterwater system revenue bonds, series 2018a5/30-Fort worth (city oF), tX water & sewer system revenue bonds, series 2018 6/5-Fort atKinson (city oF), wi Go corPorate PurPose bonds, 20186/5-harris-waller counties mud no. 2, tX unlimited taX bonds, series 20186/6-berGen county, nJ ban & Go bonds, series 2018a&b6/11-carlisle community school district, ia Go school bonds, series 2018 6/11-east benard isd, tX unlimited taX school buildinG bonds, series 20186/12-south buda wc&id no. 1, tX unltd taX bonds, series 20186/12-cibolo (city oF), tX Genetal obliGation bonds, series 20186/5-Prairie du chien (city oF), Go corP PurP bonds, srs 2018c & nans, srs 2018d6/6-PulasKi community school distrist, wi Go sch bldG & imProv bonds6/6-harris county mud no. 495, tX unlimited taX bonds, series 20186/7-Jersey city (city oF), nJ notes, srs 2018b (taXable) & srs 2018c&d6/7-irvinG (city oF), tX Go bonds & taX notes, series 20186/7-irvinG (city oF), tX ww&ss new lien revenue imProvement bonds, srs 2018 6/7-oranGe usd, ca Go bonds, election oF 2016, series 20186/11-oKoboJi community school district, ia Go school bonds, series 20186/12-cibolo (city oF), tX Genetal obliGation bonds, series 2018**s&P ratinGs rePort has been added6/12-union (county oF), nJ Gen imPrv&county voc-tech school&county colleGe bonds, 2018 srs a&b7/10-GraettinGer-terril csd, ia Go school bonds, series 2018

BiDCOMP®/Parity®

www.newissuehome.i-deal.com

6/4 - City of Elkhorn (WI), WI

6/4 - City of Elkhorn (WI), WI

6/4 - Ankeny Community School District, IA

6/4 - White County (TN), TN

6/4 - Village of Oregon, WI

6/4 - Village of Oregon, WI

6/4 - Independent School District No. 318 (Itasca County), MN

6/4 - City of Manvel, TX

6/4 - City of Dayton (TX), TX

6/4 - Village of Cottage Grove, WI

6/4 - Independent School District No. 277 (Westonka), MN

6/4 - City of Gardner (KS), KS

6/4 - City of Lakefield, MN

6/4 - Town of Credit River Township (MN), MN

6/5 - City of Seattle, WA

6/5 - Town of Grand Chute, WI

6/5 - Town of Grand Chute, WI

6/5 - Brillion Public School District (WI), WI

6/5 - City of Greensboro, NC

6/5 - City of Greensboro, NC

6/5 - State of Ohio (OH), OH

6/5 - Hilton Central School District, NY

6/5 - City of Edina, MN

6/5 - County of Suffolk, NY

6/5 - Town of Clinton (MA), MA

6/5 - County of Brunswick, NC

6/5 - Town of Braintree, MA

6/5 - City School District of the City of Hudson, NY

6/5 - Independent School District No. 33 of Creek County (Sapulpa), OK

6/5 - Cambridge Central School District, NY

6/5 - Linn County (IA), IA

6/5 - Linn County (IA), IA

6/6 - Winterset Community School District, IA

6/6 - City of Emporia, KS

6/6 - City of Portsmouth (NH), NH

6/6 - Wayne County (OH), OH

6/6 - Village of Westbury, NY

6/6 - County of Bergen, NJ

6/6 - City School District of the City of Auburn, NY

6/7 - City of Blaine (MN), MN

6/7 - Town of Henrietta, NY

007_BB06011801 7 5/31/2018 2:03:40 PM

The Bond Buyer8 Friday, June 1, 2018

d36735_BB_Midwest _Keynote Bond Buyer_Print_Ad.indd 2 5/8/18 1:23 PM

008_BB06011801 8 5/31/2018 2:28:56 PM

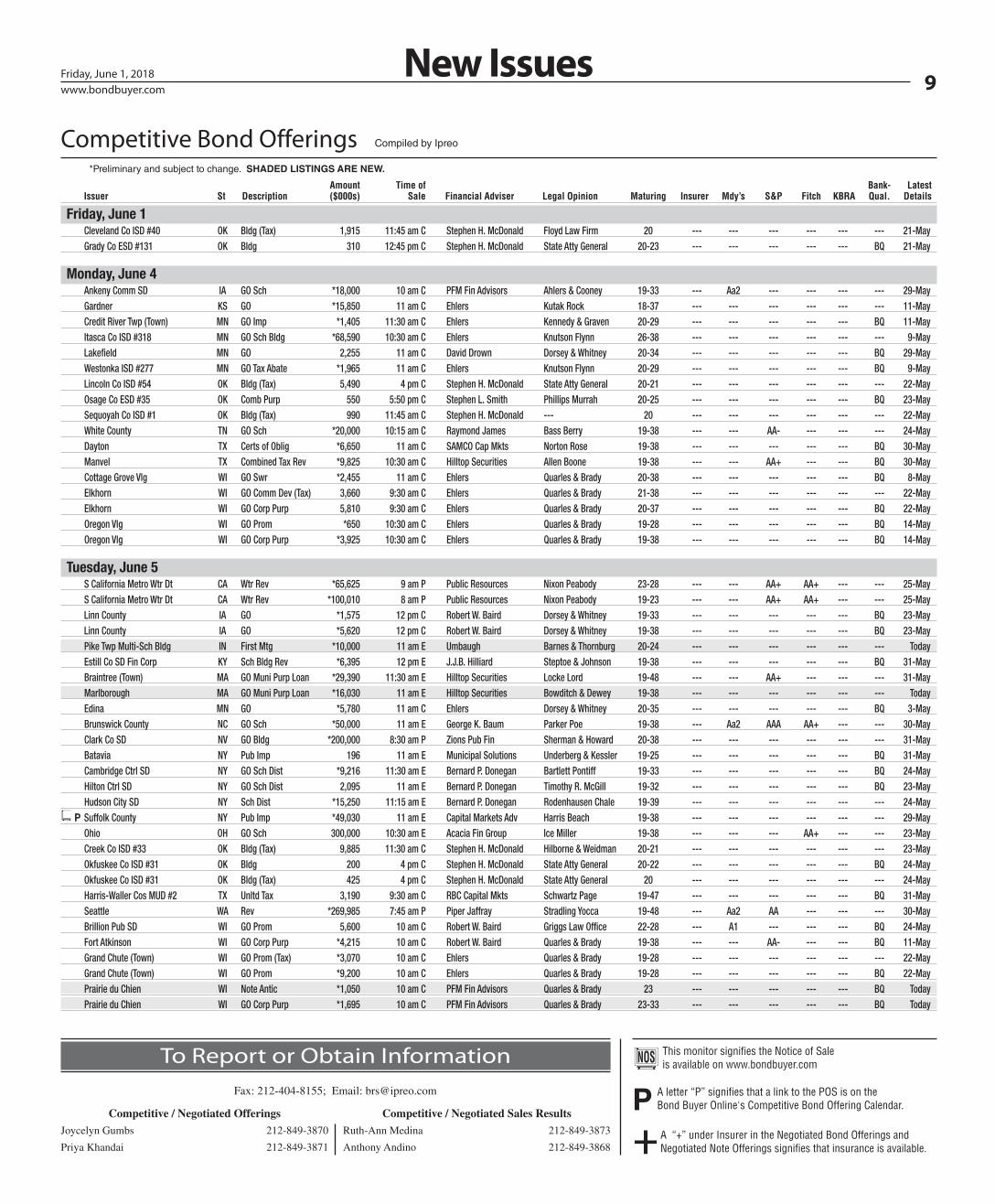

9www.bondbuyer.comFriday, June 1, 2018

Amount Time of Bank- Latest Issuer St Description ($000s) Sale Financial Adviser Legal Opinion Maturing Insurer Mdy’s S&P Fitch KBRA Qual. Details

Competitive Bond Offerings *Preliminary and subject to change. SHADED LISTINGS ARE NEW.

Compiled by Ipreo

New Issues

A letter “P” signifies that a link to the POS is on the Bond Buyer Online's Competitive Bond Offering Calendar.

This monitor signifies the Notice of Sale is available on www.bondbuyer.comTo Report or Obtain Information

Competitive / Negotiated Offerings

Joycelyn Gumbs 212-849-3870

Priya Khandai 212-849-3871

Competitive / Negotiated Sales Results

Ruth-Ann Medina 212-849-3873

Anthony Andino 212-849-3868A “+” under Insurer in the Negotiated Bond Offerings and Negotiated Note Offerings signifies that insurance is available.

Fax: 212-404-8155; Email: [email protected]

Friday, June 1 Cleveland Co ISD #40 OK Bldg (Tax) 1,915 11:45 am C Stephen H. McDonald Floyd Law Firm 20 --- --- --- --- --- --- 21-May Grady Co ESD #131 OK Bldg 310 12:45 pm C Stephen H. McDonald State Atty General 20-23 --- --- --- --- --- BQ 21-May

Monday, June 4 Ankeny Comm SD IA GO Sch *18,000 10 am C PFM Fin Advisors Ahlers & Cooney 19-33 --- Aa2 --- --- --- --- 29-May Gardner KS GO *15,850 11 am C Ehlers Kutak Rock 18-37 --- --- --- --- --- --- 11-May Credit River Twp (Town) MN GO Imp *1,405 11:30 am C Ehlers Kennedy & Graven 20-29 --- --- --- --- --- BQ 11-May Itasca Co ISD #318 MN GO Sch Bldg *68,590 10:30 am C Ehlers Knutson Flynn 26-38 --- --- --- --- --- --- 9-May Lakefield MN GO 2,255 11 am C David Drown Dorsey & Whitney 20-34 --- --- --- --- --- BQ 29-May Westonka ISD #277 MN GO Tax Abate *1,965 11 am C Ehlers Knutson Flynn 20-29 --- --- --- --- --- BQ 9-May Lincoln Co ISD #54 OK Bldg (Tax) 5,490 4 pm C Stephen H. McDonald State Atty General 20-21 --- --- --- --- --- --- 22-May Osage Co ESD #35 OK Comb Purp 550 5:50 pm C Stephen L. Smith Phillips Murrah 20-25 --- --- --- --- --- BQ 23-May Sequoyah Co ISD #1 OK Bldg (Tax) 990 11:45 am C Stephen H. McDonald --- 20 --- --- --- --- --- --- 22-May White County TN GO Sch *20,000 10:15 am C Raymond James Bass Berry 19-38 --- --- AA- --- --- --- 24-May Dayton TX Certs of Oblig *6,650 11 am C SAMCO Cap Mkts Norton Rose 19-38 --- --- --- --- --- BQ 30-May Manvel TX Combined Tax Rev *9,825 10:30 am C Hilltop Securities Allen Boone 19-38 --- --- AA+ --- --- BQ 30-May Cottage Grove Vlg WI GO Swr *2,455 11 am C Ehlers Quarles & Brady 20-38 --- --- --- --- --- BQ 8-May Elkhorn WI GO Comm Dev (Tax) 3,660 9:30 am C Ehlers Quarles & Brady 21-38 --- --- --- --- --- --- 22-May Elkhorn WI GO Corp Purp 5,810 9:30 am C Ehlers Quarles & Brady 20-37 --- --- --- --- --- BQ 22-May Oregon Vlg WI GO Prom *650 10:30 am C Ehlers Quarles & Brady 19-28 --- --- --- --- --- BQ 14-May Oregon Vlg WI GO Corp Purp *3,925 10:30 am C Ehlers Quarles & Brady 19-38 --- --- --- --- --- BQ 14-May

Tuesday, June 5 S California Metro Wtr Dt CA Wtr Rev *65,625 9 am P Public Resources Nixon Peabody 23-28 --- --- AA+ AA+ --- --- 25-May S California Metro Wtr Dt CA Wtr Rev *100,010 8 am P Public Resources Nixon Peabody 19-23 --- --- AA+ AA+ --- --- 25-May Linn County IA GO *1,575 12 pm C Robert W. Baird Dorsey & Whitney 19-33 --- --- --- --- --- BQ 23-May Linn County IA GO *5,620 12 pm C Robert W. Baird Dorsey & Whitney 19-38 --- --- --- --- --- BQ 23-May Pike Twp Multi-Sch Bldg IN First Mtg *10,000 11 am E Umbaugh Barnes & Thornburg 20-24 --- --- --- --- --- --- Today Estill Co SD Fin Corp KY Sch Bldg Rev *6,395 12 pm E J.J.B. Hilliard Steptoe & Johnson 19-38 --- --- --- --- --- BQ 31-May Braintree (Town) MA GO Muni Purp Loan *29,390 11:30 am E Hilltop Securities Locke Lord 19-48 --- --- AA+ --- --- --- 31-May Marlborough MA GO Muni Purp Loan *16,030 11 am E Hilltop Securities Bowditch & Dewey 19-38 --- --- --- --- --- --- Today Edina MN GO *5,780 11 am C Ehlers Dorsey & Whitney 20-35 --- --- --- --- --- BQ 3-May Brunswick County NC GO Sch *50,000 11 am E George K. Baum Parker Poe 19-38 --- Aa2 AAA AA+ --- --- 30-May Clark Co SD NV GO Bldg *200,000 8:30 am P Zions Pub Fin Sherman & Howard 20-38 --- --- --- --- --- --- 31-May Batavia NY Pub Imp 196 11 am E Municipal Solutions Underberg & Kessler 19-25 --- --- --- --- --- BQ 31-May Cambridge Ctrl SD NY GO Sch Dist *9,216 11:30 am E Bernard P. Donegan Bartlett Pontiff 19-33 --- --- --- --- --- BQ 24-May Hilton Ctrl SD NY GO Sch Dist 2,095 11 am E Bernard P. Donegan Timothy R. McGill 19-32 --- --- --- --- --- BQ 23-May Hudson City SD NY Sch Dist *15,250 11:15 am E Bernard P. Donegan Rodenhausen Chale 19-39 --- --- --- --- --- --- 24-May

P Suffolk County NY Pub Imp *49,030 11 am E Capital Markets Adv Harris Beach 19-38 --- --- --- --- --- --- 29-May Ohio OH GO Sch 300,000 10:30 am E Acacia Fin Group Ice Miller 19-38 --- --- --- AA+ --- --- 23-May Creek Co ISD #33 OK Bldg (Tax) 9,885 11:30 am C Stephen H. McDonald Hilborne & Weidman 20-21 --- --- --- --- --- --- 23-May Okfuskee Co ISD #31 OK Bldg 200 4 pm C Stephen H. McDonald State Atty General 20-22 --- --- --- --- --- BQ 24-May Okfuskee Co ISD #31 OK Bldg (Tax) 425 4 pm C Stephen H. McDonald State Atty General 20 --- --- --- --- --- --- 24-May Harris-Waller Cos MUD #2 TX Unltd Tax 3,190 9:30 am C RBC Capital Mkts Schwartz Page 19-47 --- --- --- --- --- BQ 31-May Seattle WA Rev *269,985 7:45 am P Piper Jaffray Stradling Yocca 19-48 --- Aa2 AA --- --- --- 30-May Brillion Pub SD WI GO Prom 5,600 10 am C Robert W. Baird Griggs Law Office 22-28 --- A1 --- --- --- BQ 24-May Fort Atkinson WI GO Corp Purp *4,215 10 am C Robert W. Baird Quarles & Brady 19-38 --- --- AA- --- --- BQ 11-May Grand Chute (Town) WI GO Prom (Tax) *3,070 10 am C Ehlers Quarles & Brady 19-28 --- --- --- --- --- --- 22-May Grand Chute (Town) WI GO Prom *9,200 10 am C Ehlers Quarles & Brady 19-28 --- --- --- --- --- BQ 22-May Prairie du Chien WI Note Antic *1,050 10 am C PFM Fin Advisors Quarles & Brady 23 --- --- --- --- --- BQ Today Prairie du Chien WI GO Corp Purp *1,695 10 am C PFM Fin Advisors Quarles & Brady 23-33 --- --- --- --- --- BQ Today

009_BB06011801 9 5/31/2018 3:49:52 PM

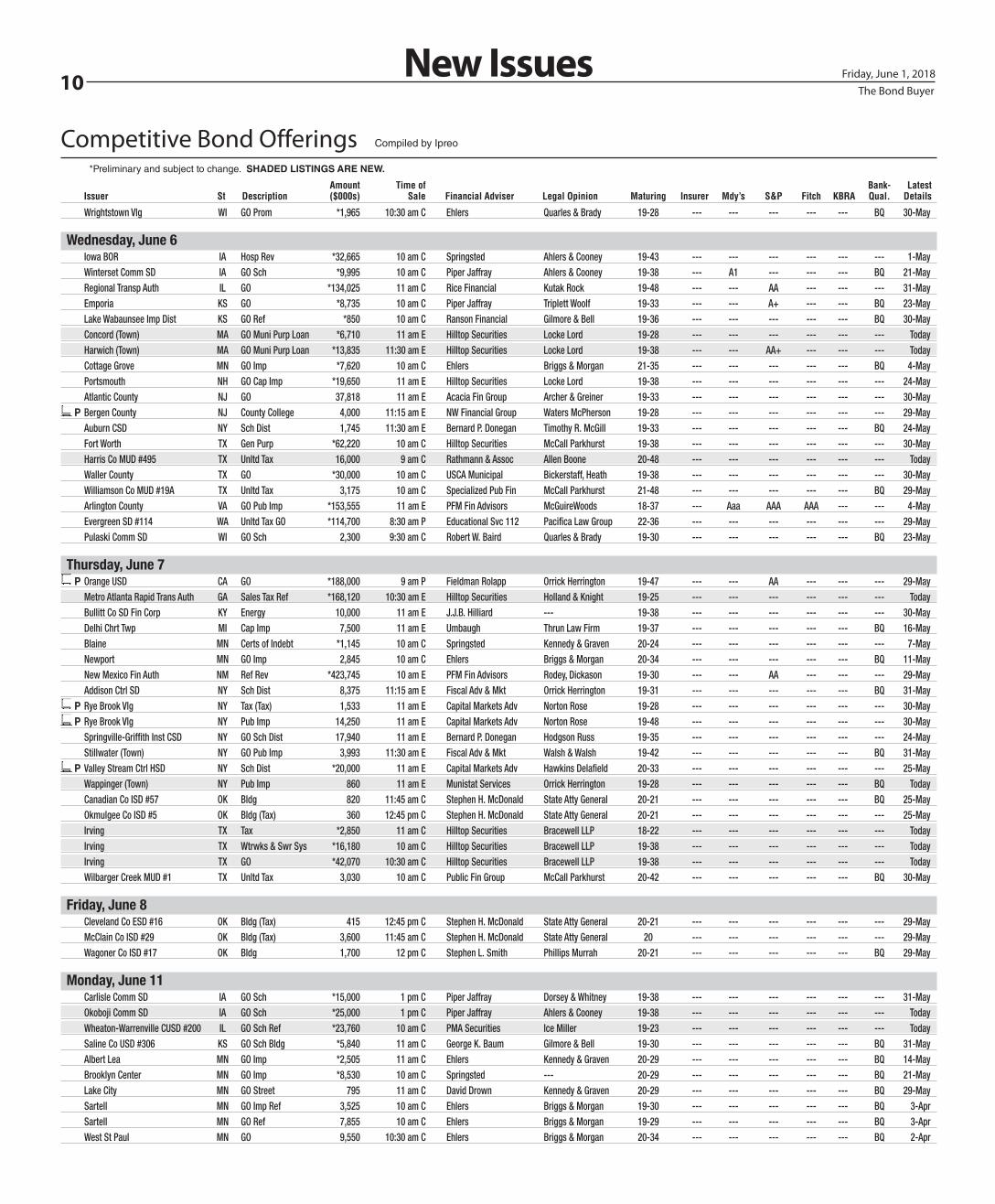

10 The Bond Buyer

Friday, June 1, 2018

Amount Time of Bank- Latest Issuer St Description ($000s) Sale Financial Adviser Legal Opinion Maturing Insurer Mdy’s S&P Fitch KBRA Qual. Details

Competitive Bond Offerings *Preliminary and subject to change. SHADED LISTINGS ARE NEW.

Compiled by Ipreo

New Issues

Wrightstown Vlg WI GO Prom *1,965 10:30 am C Ehlers Quarles & Brady 19-28 --- --- --- --- --- BQ 30-May

Wednesday, June 6 Iowa BOR IA Hosp Rev *32,665 10 am C Springsted Ahlers & Cooney 19-43 --- --- --- --- --- --- 1-May Winterset Comm SD IA GO Sch *9,995 10 am C Piper Jaffray Ahlers & Cooney 19-38 --- A1 --- --- --- BQ 21-May Regional Transp Auth IL GO *134,025 11 am C Rice Financial Kutak Rock 19-48 --- --- AA --- --- --- 31-May Emporia KS GO *8,735 10 am C Piper Jaffray Triplett Woolf 19-33 --- --- A+ --- --- BQ 23-May Lake Wabaunsee Imp Dist KS GO Ref *850 10 am C Ranson Financial Gilmore & Bell 19-36 --- --- --- --- --- BQ 30-May Concord (Town) MA GO Muni Purp Loan *6,710 11 am E Hilltop Securities Locke Lord 19-28 --- --- --- --- --- --- Today Harwich (Town) MA GO Muni Purp Loan *13,835 11:30 am E Hilltop Securities Locke Lord 19-38 --- --- AA+ --- --- --- Today Cottage Grove MN GO Imp *7,620 10 am C Ehlers Briggs & Morgan 21-35 --- --- --- --- --- BQ 4-May Portsmouth NH GO Cap Imp *19,650 11 am E Hilltop Securities Locke Lord 19-38 --- --- --- --- --- --- 24-May Atlantic County NJ GO 37,818 11 am E Acacia Fin Group Archer & Greiner 19-33 --- --- --- --- --- --- 30-May

P Bergen County NJ County College 4,000 11:15 am E NW Financial Group Waters McPherson 19-28 --- --- --- --- --- --- 29-May Auburn CSD NY Sch Dist 1,745 11:30 am E Bernard P. Donegan Timothy R. McGill 19-33 --- --- --- --- --- BQ 24-May Fort Worth TX Gen Purp *62,220 10 am C Hilltop Securities McCall Parkhurst 19-38 --- --- --- --- --- --- 30-May Harris Co MUD #495 TX Unltd Tax 16,000 9 am C Rathmann & Assoc Allen Boone 20-48 --- --- --- --- --- --- Today Waller County TX GO *30,000 10 am C USCA Municipal Bickerstaff, Heath 19-38 --- --- --- --- --- --- 30-May Williamson Co MUD #19A TX Unltd Tax 3,175 10 am C Specialized Pub Fin McCall Parkhurst 21-48 --- --- --- --- --- BQ 29-May Arlington County VA GO Pub Imp *153,555 11 am E PFM Fin Advisors McGuireWoods 18-37 --- Aaa AAA AAA --- --- 4-May Evergreen SD #114 WA Unltd Tax GO *114,700 8:30 am P Educational Svc 112 Pacifica Law Group 22-36 --- --- --- --- --- --- 29-May Pulaski Comm SD WI GO Sch 2,300 9:30 am C Robert W. Baird Quarles & Brady 19-30 --- --- --- --- --- BQ 23-May

Thursday, June 7 P Orange USD CA GO *188,000 9 am P Fieldman Rolapp Orrick Herrington 19-47 --- --- AA --- --- --- 29-May

Metro Atlanta Rapid Trans Auth GA Sales Tax Ref *168,120 10:30 am E Hilltop Securities Holland & Knight 19-25 --- --- --- --- --- --- Today Bullitt Co SD Fin Corp KY Energy 10,000 11 am E J.J.B. Hilliard --- 19-38 --- --- --- --- --- --- 30-May Delhi Chrt Twp MI Cap Imp 7,500 11 am E Umbaugh Thrun Law Firm 19-37 --- --- --- --- --- BQ 16-May Blaine MN Certs of Indebt *1,145 10 am C Springsted Kennedy & Graven 20-24 --- --- --- --- --- --- 7-May Newport MN GO Imp 2,845 10 am C Ehlers Briggs & Morgan 20-34 --- --- --- --- --- BQ 11-May New Mexico Fin Auth NM Ref Rev *423,745 10 am E PFM Fin Advisors Rodey, Dickason 19-30 --- --- AA --- --- --- 29-May Addison Ctrl SD NY Sch Dist 8,375 11:15 am E Fiscal Adv & Mkt Orrick Herrington 19-31 --- --- --- --- --- BQ 31-May

P Rye Brook Vlg NY Tax (Tax) 1,533 11 am E Capital Markets Adv Norton Rose 19-28 --- --- --- --- --- --- 30-May P Rye Brook Vlg NY Pub Imp 14,250 11 am E Capital Markets Adv Norton Rose 19-48 --- --- --- --- --- --- 30-May

Springville-Griffith Inst CSD NY GO Sch Dist 17,940 11 am E Bernard P. Donegan Hodgson Russ 19-35 --- --- --- --- --- --- 24-May Stillwater (Town) NY GO Pub Imp 3,993 11:30 am E Fiscal Adv & Mkt Walsh & Walsh 19-42 --- --- --- --- --- BQ 31-May

P Valley Stream Ctrl HSD NY Sch Dist *20,000 11 am E Capital Markets Adv Hawkins Delafield 20-33 --- --- --- --- --- --- 25-May Wappinger (Town) NY Pub Imp 860 11 am E Munistat Services Orrick Herrington 19-28 --- --- --- --- --- BQ Today Canadian Co ISD #57 OK Bldg 820 11:45 am C Stephen H. McDonald State Atty General 20-21 --- --- --- --- --- BQ 25-May Okmulgee Co ISD #5 OK Bldg (Tax) 360 12:45 pm C Stephen H. McDonald State Atty General 20-21 --- --- --- --- --- --- 25-May Irving TX Tax *2,850 11 am C Hilltop Securities Bracewell LLP 18-22 --- --- --- --- --- --- Today Irving TX Wtrwks & Swr Sys *16,180 10 am C Hilltop Securities Bracewell LLP 19-38 --- --- --- --- --- --- Today Irving TX GO *42,070 10:30 am C Hilltop Securities Bracewell LLP 19-38 --- --- --- --- --- --- Today Wilbarger Creek MUD #1 TX Unltd Tax 3,030 10 am C Public Fin Group McCall Parkhurst 20-42 --- --- --- --- --- BQ 30-May

Friday, June 8 Cleveland Co ESD #16 OK Bldg (Tax) 415 12:45 pm C Stephen H. McDonald State Atty General 20-21 --- --- --- --- --- --- 29-May McClain Co ISD #29 OK Bldg (Tax) 3,600 11:45 am C Stephen H. McDonald State Atty General 20 --- --- --- --- --- --- 29-May Wagoner Co ISD #17 OK Bldg 1,700 12 pm C Stephen L. Smith Phillips Murrah 20-21 --- --- --- --- --- BQ 29-May

Monday, June 11 Carlisle Comm SD IA GO Sch *15,000 1 pm C Piper Jaffray Dorsey & Whitney 19-38 --- --- --- --- --- --- 31-May Okoboji Comm SD IA GO Sch *25,000 1 pm C Piper Jaffray Ahlers & Cooney 19-38 --- --- --- --- --- --- Today Wheaton-Warrenville CUSD #200 IL GO Sch Ref *23,760 10 am C PMA Securities Ice Miller 19-23 --- --- --- --- --- --- Today Saline Co USD #306 KS GO Sch Bldg *5,840 11 am C George K. Baum Gilmore & Bell 19-30 --- --- --- --- --- BQ 31-May Albert Lea MN GO Imp *2,505 11 am C Ehlers Kennedy & Graven 20-29 --- --- --- --- --- BQ 14-May Brooklyn Center MN GO Imp *8,530 10 am C Springsted --- 20-29 --- --- --- --- --- BQ 21-May Lake City MN GO Street 795 11 am C David Drown Kennedy & Graven 20-29 --- --- --- --- --- BQ 29-May Sartell MN GO Imp Ref 3,525 10 am C Ehlers Briggs & Morgan 19-30 --- --- --- --- --- BQ 3-Apr Sartell MN GO Ref 7,855 10 am C Ehlers Briggs & Morgan 19-29 --- --- --- --- --- BQ 3-Apr West St Paul MN GO 9,550 10:30 am C Ehlers Briggs & Morgan 20-34 --- --- --- --- --- BQ 2-Apr

010_BB06011801 10 5/31/2018 3:49:53 PM

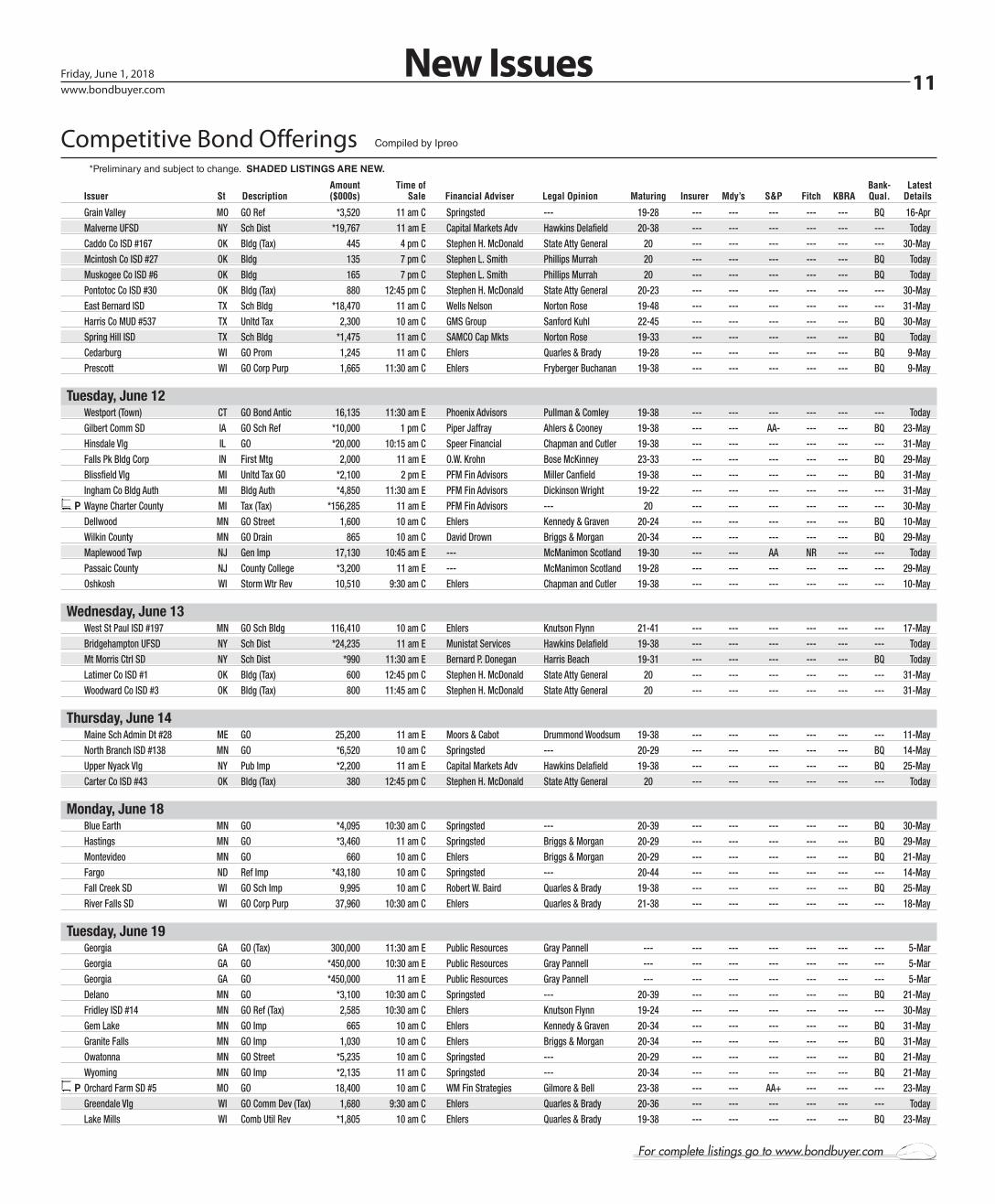

11www.bondbuyer.comFriday, June 1, 2018 New Issues

Amount Time of Bank- Latest Issuer St Description ($000s) Sale Financial Adviser Legal Opinion Maturing Insurer Mdy’s S&P Fitch KBRA Qual. Details

Competitive Bond Offerings *Preliminary and subject to change. SHADED LISTINGS ARE NEW.

Compiled by Ipreo

Grain Valley MO GO Ref *3,520 11 am C Springsted --- 19-28 --- --- --- --- --- BQ 16-Apr Malverne UFSD NY Sch Dist *19,767 11 am E Capital Markets Adv Hawkins Delafield 20-38 --- --- --- --- --- --- Today Caddo Co ISD #167 OK Bldg (Tax) 445 4 pm C Stephen H. McDonald State Atty General 20 --- --- --- --- --- --- 30-May Mcintosh Co ISD #27 OK Bldg 135 7 pm C Stephen L. Smith Phillips Murrah 20 --- --- --- --- --- BQ Today Muskogee Co ISD #6 OK Bldg 165 7 pm C Stephen L. Smith Phillips Murrah 20 --- --- --- --- --- BQ Today Pontotoc Co ISD #30 OK Bldg (Tax) 880 12:45 pm C Stephen H. McDonald State Atty General 20-23 --- --- --- --- --- --- 30-May East Bernard ISD TX Sch Bldg *18,470 11 am C Wells Nelson Norton Rose 19-48 --- --- --- --- --- --- 31-May Harris Co MUD #537 TX Unltd Tax 2,300 10 am C GMS Group Sanford Kuhl 22-45 --- --- --- --- --- BQ 30-May Spring Hill ISD TX Sch Bldg *1,475 11 am C SAMCO Cap Mkts Norton Rose 19-33 --- --- --- --- --- BQ Today Cedarburg WI GO Prom 1,245 11 am C Ehlers Quarles & Brady 19-28 --- --- --- --- --- BQ 9-May Prescott WI GO Corp Purp 1,665 11:30 am C Ehlers Fryberger Buchanan 19-38 --- --- --- --- --- BQ 9-May

Tuesday, June 12 Westport (Town) CT GO Bond Antic 16,135 11:30 am E Phoenix Advisors Pullman & Comley 19-38 --- --- --- --- --- --- Today Gilbert Comm SD IA GO Sch Ref *10,000 1 pm C Piper Jaffray Ahlers & Cooney 19-38 --- --- AA- --- --- BQ 23-May Hinsdale Vlg IL GO *20,000 10:15 am C Speer Financial Chapman and Cutler 19-38 --- --- --- --- --- --- 31-May Falls Pk Bldg Corp IN First Mtg 2,000 11 am E O.W. Krohn Bose McKinney 23-33 --- --- --- --- --- BQ 29-May Blissfield Vlg MI Unltd Tax GO *2,100 2 pm E PFM Fin Advisors Miller Canfield 19-38 --- --- --- --- --- BQ 31-May Ingham Co Bldg Auth MI Bldg Auth *4,850 11:30 am E PFM Fin Advisors Dickinson Wright 19-22 --- --- --- --- --- --- 31-May

P Wayne Charter County MI Tax (Tax) *156,285 11 am E PFM Fin Advisors --- 20 --- --- --- --- --- --- 30-May Dellwood MN GO Street 1,600 10 am C Ehlers Kennedy & Graven 20-24 --- --- --- --- --- BQ 10-May Wilkin County MN GO Drain 865 10 am C David Drown Briggs & Morgan 20-34 --- --- --- --- --- BQ 29-May Maplewood Twp NJ Gen Imp 17,130 10:45 am E --- McManimon Scotland 19-30 --- --- AA NR --- --- Today Passaic County NJ County College *3,200 11 am E --- McManimon Scotland 19-28 --- --- --- --- --- --- 29-May Oshkosh WI Storm Wtr Rev 10,510 9:30 am C Ehlers Chapman and Cutler 19-38 --- --- --- --- --- --- 10-May

Wednesday, June 13 West St Paul ISD #197 MN GO Sch Bldg 116,410 10 am C Ehlers Knutson Flynn 21-41 --- --- --- --- --- --- 17-May Bridgehampton UFSD NY Sch Dist *24,235 11 am E Munistat Services Hawkins Delafield 19-38 --- --- --- --- --- --- Today Mt Morris Ctrl SD NY Sch Dist *990 11:30 am E Bernard P. Donegan Harris Beach 19-31 --- --- --- --- --- BQ Today Latimer Co ISD #1 OK Bldg (Tax) 600 12:45 pm C Stephen H. McDonald State Atty General 20 --- --- --- --- --- --- 31-May Woodward Co ISD #3 OK Bldg (Tax) 800 11:45 am C Stephen H. McDonald State Atty General 20 --- --- --- --- --- --- 31-May

Thursday, June 14 Maine Sch Admin Dt #28 ME GO 25,200 11 am E Moors & Cabot Drummond Woodsum 19-38 --- --- --- --- --- --- 11-May North Branch ISD #138 MN GO *6,520 10 am C Springsted --- 20-29 --- --- --- --- --- BQ 14-May Upper Nyack Vlg NY Pub Imp *2,200 11 am E Capital Markets Adv Hawkins Delafield 19-38 --- --- --- --- --- BQ 25-May Carter Co ISD #43 OK Bldg (Tax) 380 12:45 pm C Stephen H. McDonald State Atty General 20 --- --- --- --- --- --- Today

Monday, June 18 Blue Earth MN GO *4,095 10:30 am C Springsted --- 20-39 --- --- --- --- --- BQ 30-May Hastings MN GO *3,460 11 am C Springsted Briggs & Morgan 20-29 --- --- --- --- --- BQ 29-May Montevideo MN GO 660 10 am C Ehlers Briggs & Morgan 20-29 --- --- --- --- --- BQ 21-May Fargo ND Ref Imp *43,180 10 am C Springsted --- 20-44 --- --- --- --- --- --- 14-May Fall Creek SD WI GO Sch Imp 9,995 10 am C Robert W. Baird Quarles & Brady 19-38 --- --- --- --- --- BQ 25-May River Falls SD WI GO Corp Purp 37,960 10:30 am C Ehlers Quarles & Brady 21-38 --- --- --- --- --- --- 18-May

Tuesday, June 19 Georgia GA GO (Tax) 300,000 11:30 am E Public Resources Gray Pannell --- --- --- --- --- --- --- 5-Mar Georgia GA GO *450,000 10:30 am E Public Resources Gray Pannell --- --- --- --- --- --- --- 5-Mar Georgia GA GO *450,000 11 am E Public Resources Gray Pannell --- --- --- --- --- --- --- 5-Mar Delano MN GO *3,100 10:30 am C Springsted --- 20-39 --- --- --- --- --- BQ 21-May Fridley ISD #14 MN GO Ref (Tax) 2,585 10:30 am C Ehlers Knutson Flynn 19-24 --- --- --- --- --- --- 30-May Gem Lake MN GO Imp 665 10 am C Ehlers Kennedy & Graven 20-34 --- --- --- --- --- BQ 31-May Granite Falls MN GO Imp 1,030 10 am C Ehlers Briggs & Morgan 20-34 --- --- --- --- --- BQ 31-May Owatonna MN GO Street *5,235 10 am C Springsted --- 20-29 --- --- --- --- --- BQ 21-May Wyoming MN GO Imp *2,135 11 am C Springsted --- 20-34 --- --- --- --- --- BQ 21-May

P Orchard Farm SD #5 MO GO 18,400 10 am C WM Fin Strategies Gilmore & Bell 23-38 --- --- AA+ --- --- --- 23-May Greendale Vlg WI GO Comm Dev (Tax) 1,680 9:30 am C Ehlers Quarles & Brady 20-36 --- --- --- --- --- --- Today Lake Mills WI Comb Util Rev *1,805 10 am C Ehlers Quarles & Brady 19-38 --- --- --- --- --- BQ 23-May

For complete listings go to www.bondbuyer.com

011_BB06011801 11 5/31/2018 3:49:53 PM

12 The Bond Buyer

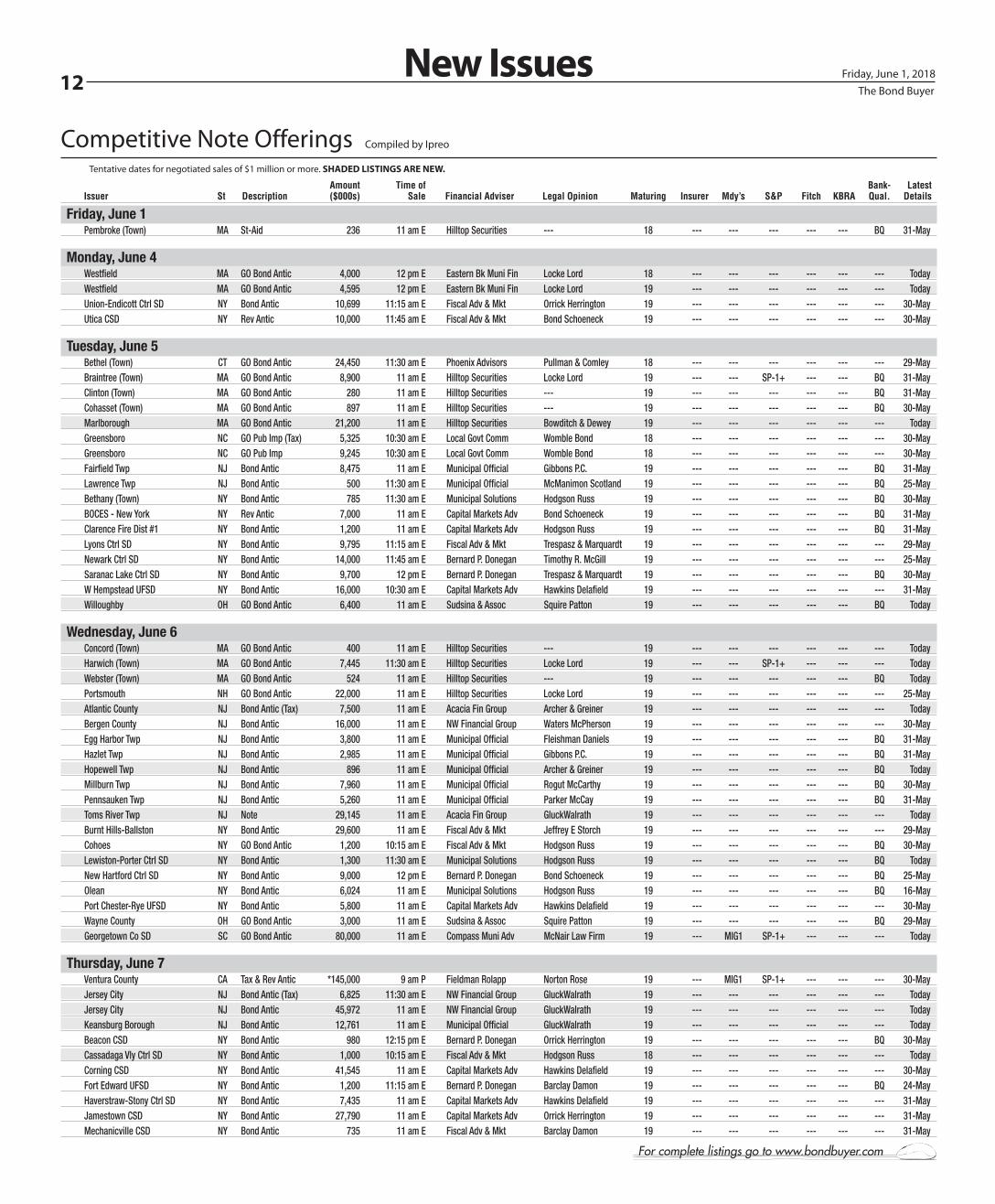

Friday, June 1, 2018

Amount Time of Bank- Latest Issuer St Description ($000s) Sale Financial Adviser Legal Opinion Maturing Insurer Mdy’s S&P Fitch KBRA Qual. Details

Competitive Note Offerings Tentative dates for negotiated sales of $1 million or more. SHADED LISTINGS ARE NEW.

Compiled by Ipreo

New Issues

Friday, June 1 Pembroke (Town) MA St-Aid 236 11 am E Hilltop Securities --- 18 --- --- --- --- --- BQ 31-May

Monday, June 4 Westfield MA GO Bond Antic 4,000 12 pm E Eastern Bk Muni Fin Locke Lord 18 --- --- --- --- --- --- Today Westfield MA GO Bond Antic 4,595 12 pm E Eastern Bk Muni Fin Locke Lord 19 --- --- --- --- --- --- Today Union-Endicott Ctrl SD NY Bond Antic 10,699 11:15 am E Fiscal Adv & Mkt Orrick Herrington 19 --- --- --- --- --- --- 30-May Utica CSD NY Rev Antic 10,000 11:45 am E Fiscal Adv & Mkt Bond Schoeneck 19 --- --- --- --- --- --- 30-May

Tuesday, June 5 Bethel (Town) CT GO Bond Antic 24,450 11:30 am E Phoenix Advisors Pullman & Comley 18 --- --- --- --- --- --- 29-May Braintree (Town) MA GO Bond Antic 8,900 11 am E Hilltop Securities Locke Lord 19 --- --- SP-1+ --- --- BQ 31-May Clinton (Town) MA GO Bond Antic 280 11 am E Hilltop Securities --- 19 --- --- --- --- --- BQ 31-May Cohasset (Town) MA GO Bond Antic 897 11 am E Hilltop Securities --- 19 --- --- --- --- --- BQ 30-May Marlborough MA GO Bond Antic 21,200 11 am E Hilltop Securities Bowditch & Dewey 19 --- --- --- --- --- --- Today Greensboro NC GO Pub Imp (Tax) 5,325 10:30 am E Local Govt Comm Womble Bond 18 --- --- --- --- --- --- 30-May Greensboro NC GO Pub Imp 9,245 10:30 am E Local Govt Comm Womble Bond 18 --- --- --- --- --- --- 30-May Fairfield Twp NJ Bond Antic 8,475 11 am E Municipal Official Gibbons P.C. 19 --- --- --- --- --- BQ 31-May Lawrence Twp NJ Bond Antic 500 11:30 am E Municipal Official McManimon Scotland 19 --- --- --- --- --- BQ 25-May Bethany (Town) NY Bond Antic 785 11:30 am E Municipal Solutions Hodgson Russ 19 --- --- --- --- --- BQ 30-May BOCES - New York NY Rev Antic 7,000 11 am E Capital Markets Adv Bond Schoeneck 19 --- --- --- --- --- BQ 31-May Clarence Fire Dist #1 NY Bond Antic 1,200 11 am E Capital Markets Adv Hodgson Russ 19 --- --- --- --- --- BQ 31-May Lyons Ctrl SD NY Bond Antic 9,795 11:15 am E Fiscal Adv & Mkt Trespasz & Marquardt 19 --- --- --- --- --- --- 29-May Newark Ctrl SD NY Bond Antic 14,000 11:45 am E Bernard P. Donegan Timothy R. McGill 19 --- --- --- --- --- --- 25-May Saranac Lake Ctrl SD NY Bond Antic 9,700 12 pm E Bernard P. Donegan Trespasz & Marquardt 19 --- --- --- --- --- BQ 30-May W Hempstead UFSD NY Bond Antic 16,000 10:30 am E Capital Markets Adv Hawkins Delafield 19 --- --- --- --- --- --- 31-May Willoughby OH GO Bond Antic 6,400 11 am E Sudsina & Assoc Squire Patton 19 --- --- --- --- --- BQ Today

Wednesday, June 6 Concord (Town) MA GO Bond Antic 400 11 am E Hilltop Securities --- 19 --- --- --- --- --- --- Today Harwich (Town) MA GO Bond Antic 7,445 11:30 am E Hilltop Securities Locke Lord 19 --- --- SP-1+ --- --- --- Today Webster (Town) MA GO Bond Antic 524 11 am E Hilltop Securities --- 19 --- --- --- --- --- BQ Today Portsmouth NH GO Bond Antic 22,000 11 am E Hilltop Securities Locke Lord 19 --- --- --- --- --- --- 25-May Atlantic County NJ Bond Antic (Tax) 7,500 11 am E Acacia Fin Group Archer & Greiner 19 --- --- --- --- --- --- Today Bergen County NJ Bond Antic 16,000 11 am E NW Financial Group Waters McPherson 19 --- --- --- --- --- --- 30-May Egg Harbor Twp NJ Bond Antic 3,800 11 am E Municipal Official Fleishman Daniels 19 --- --- --- --- --- BQ 31-May Hazlet Twp NJ Bond Antic 2,985 11 am E Municipal Official Gibbons P.C. 19 --- --- --- --- --- BQ 31-May Hopewell Twp NJ Bond Antic 896 11 am E Municipal Official Archer & Greiner 19 --- --- --- --- --- BQ Today Millburn Twp NJ Bond Antic 7,960 11 am E Municipal Official Rogut McCarthy 19 --- --- --- --- --- BQ 30-May Pennsauken Twp NJ Bond Antic 5,260 11 am E Municipal Official Parker McCay 19 --- --- --- --- --- BQ 31-May Toms River Twp NJ Note 29,145 11 am E Acacia Fin Group GluckWalrath 19 --- --- --- --- --- --- Today Burnt Hills-Ballston NY Bond Antic 29,600 11 am E Fiscal Adv & Mkt Jeffrey E Storch 19 --- --- --- --- --- --- 29-May Cohoes NY GO Bond Antic 1,200 10:15 am E Fiscal Adv & Mkt Hodgson Russ 19 --- --- --- --- --- BQ 30-May Lewiston-Porter Ctrl SD NY Bond Antic 1,300 11:30 am E Municipal Solutions Hodgson Russ 19 --- --- --- --- --- BQ Today New Hartford Ctrl SD NY Bond Antic 9,000 12 pm E Bernard P. Donegan Bond Schoeneck 19 --- --- --- --- --- BQ 25-May Olean NY Bond Antic 6,024 11 am E Municipal Solutions Hodgson Russ 19 --- --- --- --- --- BQ 16-May Port Chester-Rye UFSD NY Bond Antic 5,800 11 am E Capital Markets Adv Hawkins Delafield 19 --- --- --- --- --- --- 30-May Wayne County OH GO Bond Antic 3,000 11 am E Sudsina & Assoc Squire Patton 19 --- --- --- --- --- BQ 29-May Georgetown Co SD SC GO Bond Antic 80,000 11 am E Compass Muni Adv McNair Law Firm 19 --- MIG1 SP-1+ --- --- --- Today

Thursday, June 7 Ventura County CA Tax & Rev Antic *145,000 9 am P Fieldman Rolapp Norton Rose 19 --- MIG1 SP-1+ --- --- --- 30-May Jersey City NJ Bond Antic (Tax) 6,825 11:30 am E NW Financial Group GluckWalrath 19 --- --- --- --- --- --- Today Jersey City NJ Bond Antic 45,972 11 am E NW Financial Group GluckWalrath 19 --- --- --- --- --- --- Today Keansburg Borough NJ Bond Antic 12,761 11 am E Municipal Official GluckWalrath 19 --- --- --- --- --- --- Today Beacon CSD NY Bond Antic 980 12:15 pm E Bernard P. Donegan Orrick Herrington 19 --- --- --- --- --- BQ 30-May Cassadaga Vly Ctrl SD NY Bond Antic 1,000 10:15 am E Fiscal Adv & Mkt Hodgson Russ 18 --- --- --- --- --- --- Today Corning CSD NY Bond Antic 41,545 11 am E Capital Markets Adv Hawkins Delafield 19 --- --- --- --- --- --- 30-May Fort Edward UFSD NY Bond Antic 1,200 11:15 am E Bernard P. Donegan Barclay Damon 19 --- --- --- --- --- BQ 24-May Haverstraw-Stony Ctrl SD NY Bond Antic 7,435 11 am E Capital Markets Adv Hawkins Delafield 19 --- --- --- --- --- --- 31-May Jamestown CSD NY Bond Antic 27,790 11 am E Capital Markets Adv Orrick Herrington 19 --- --- --- --- --- --- 31-May Mechanicville CSD NY Bond Antic 735 11 am E Fiscal Adv & Mkt Barclay Damon 19 --- --- --- --- --- --- 31-May

For complete listings go to www.bondbuyer.com

012_BB06011801 12 5/31/2018 3:49:54 PM

13www.bondbuyer.comFriday, June 1, 2018 New Issues

Amount First Issuer St Description ($000s) Lead Manager Financial Adviser Insurer Mdy’s S&P Fitch KBRA Appeared

Negotiated Bond Offerings Tentative dates for negotiated sales of $1 million or more. A “+” under Insurer signifies that insurance is available. SHADED LISTINGS ARE NEW.

Compiled by Ipreo

Friday, June 1 Ferris ISD TX Sch Bldg & Ref 16,395 UMB Bank George K. Baum PSF --- A+ --- --- 25-May