Embed Size (px)

Citation preview

Vision

Monthly Economicand Financial Monitor

February 2019

Research Analysts

Administration

Ihor Danyliuk 416-869-7522Head of Research

Caroline Jukes 416-869-8039Administrative Manager

Tanya Bouchard 416-869-7934Supervisory Analyst

Research Publications

Vanda Bright 416-869-7141Manager, Publishing Services

Wayne Chau 416-869-7140Publishing Associate

Information

Giuseppe Saltarelli 514-879-5357 [email protected]

Economics & Strategy Stéfane Marion 514-879-3781Chief Economist and Strategist

Matthieu Arseneau 514-879-2252Deputy Chief Economist

Kyle Dahms 514-879-3195Economist

Angelo Katsoras 514-879-6458Geopolitical Analyst

Jocelyn Paquet 514-412-3693Economist

Paul-André Pinsonnault 514-879-3795Senior Fixed Income Economist

Marc Pinsonneault 514-879-2589Senior Economist

Krishen Rangasamy 514-879-3140Senior Economist

Banking & InsuranceGabriel Dechaine 416-869-7442Associate: Will Flanigan 416-507-8006Associate: Ganesh Kannan 416-507-9555

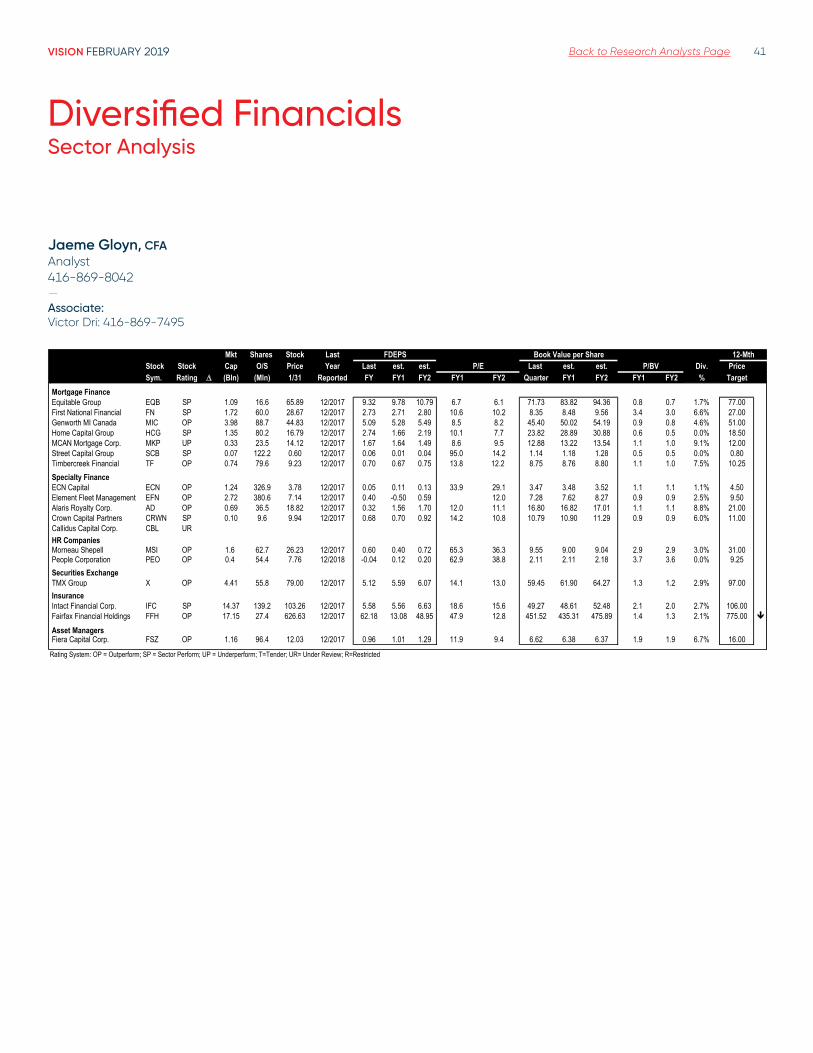

Diversified FinancialsJaeme Gloyn 416-869-8042Associate: Victor Dri 416-869-7495

Energy Services & AgricultureGreg Colman 416-869-6775Assoc: Anthony Linton 416-507-9054Assoc: Michael Storry-Robertson 416-507-8007

ETFs & Financial Products Daniel Straus 416-869-8020Ling Zhang 416-869-7942

Associate: Linda Ma 416-507-8801Associate: Tiffany Zhang 416-869-8022

Healthcare & BiotechnologyEndri Leno 416-869-8047Associate: Stephen Kwai 416-869-7571

Industrial Products Maxim Sytchev 416-869-6517Associate: Adam Staszewski 416-869-7937Associate: Troy Sun 416-869-6754

Merchandising & Consumer ProductsVishal Shreedhar 416-869-7930Associate: Ryan Li 416-869-6767

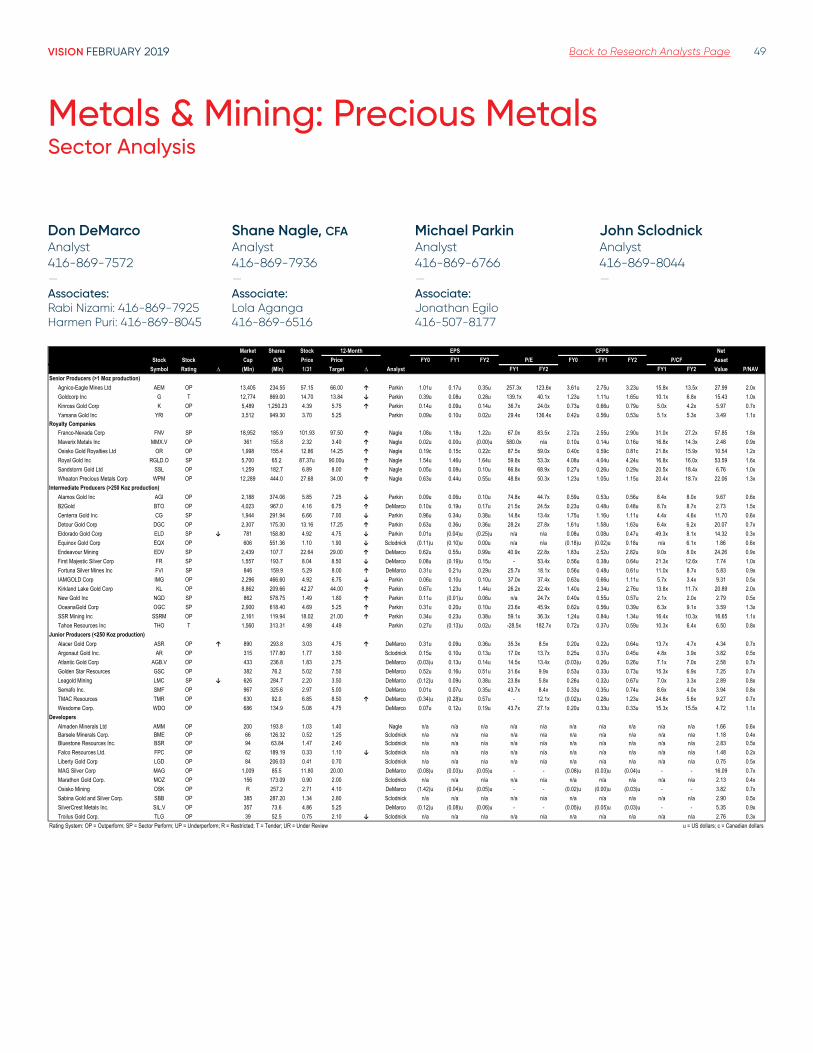

Metals & MiningDon DeMarco 416-869-7572Associate: Rabi Nizami 416-869-7925Associate: Harmen Puri 416-869-8045

Shane Nagle 416-869-7936Associate: Lola Aganga 416-869-6516

Michael Parkin 416-869-6766Associate: Jonathan Egilo 416-507-8177

John Sclodnick 416-869-8044

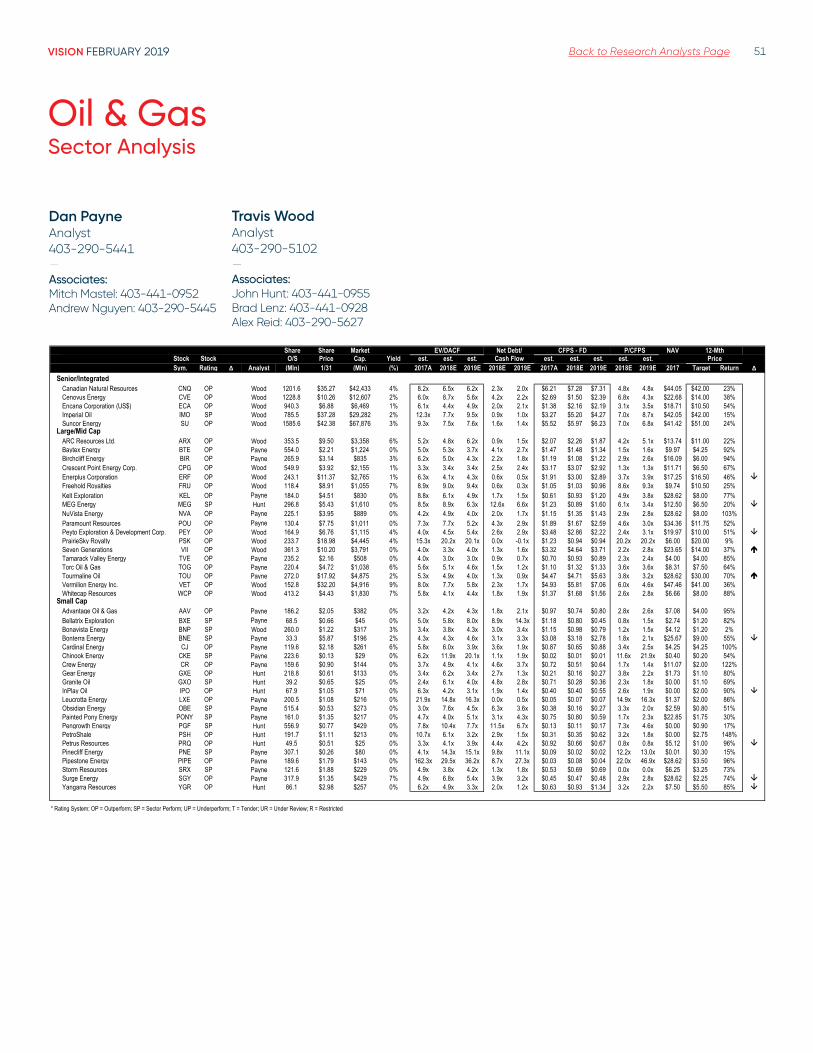

Oil & Gas› Intermediate Oil & Gas

Dan Payne 403-290-5441 Associate: Mitch Mastel 403-441-0952 Associate: Andrew Nguyen 403-290-5445

› Large Cap Oil & Gas

Travis Wood 403-290-5102 Associate: John Hunt 403-441-0955 Associate: Brad Lenz 403-441-0928 Associate: Alex Reid 403-290-5627

Pipelines, Utilities & Energy InfrastructurePatrick Kenny 403-290-5451Associate: Amber Brown 403-290-5624

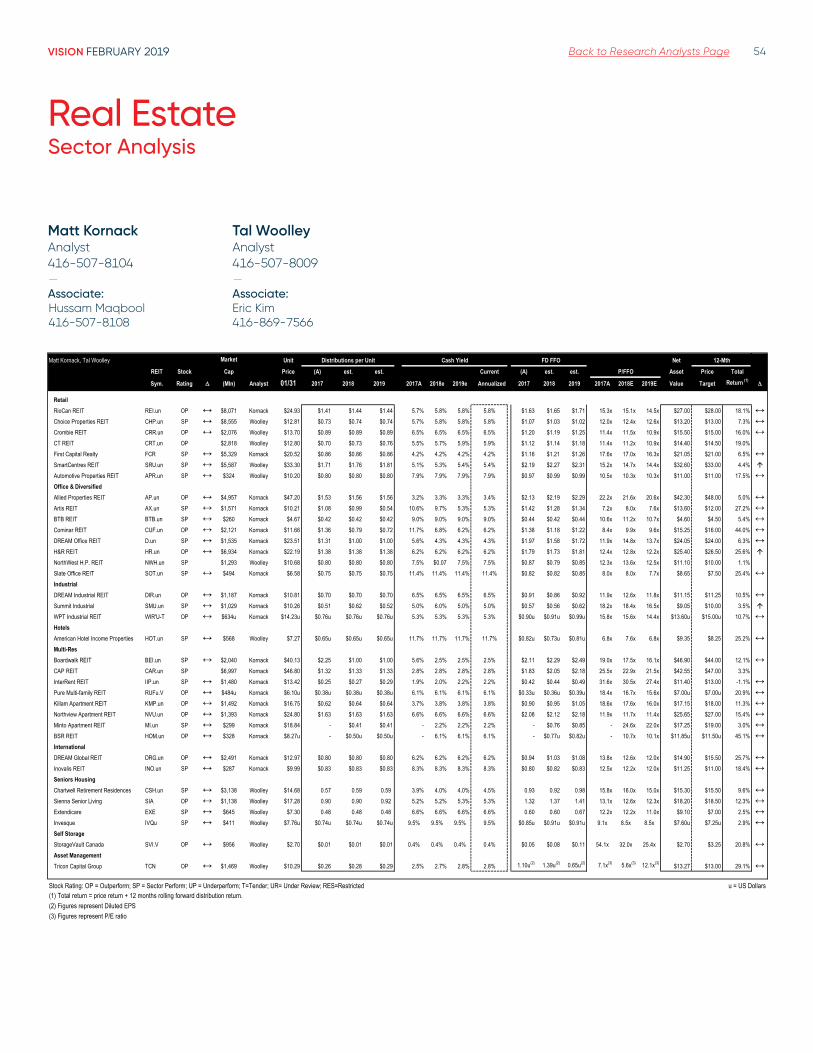

Real EstateMatt Kornack 416-507-8104Associate: Hussam Maqbool 416-507-8108

Tal Woolley 416-507-8009 Associate: Eric Kim 416-869-7566

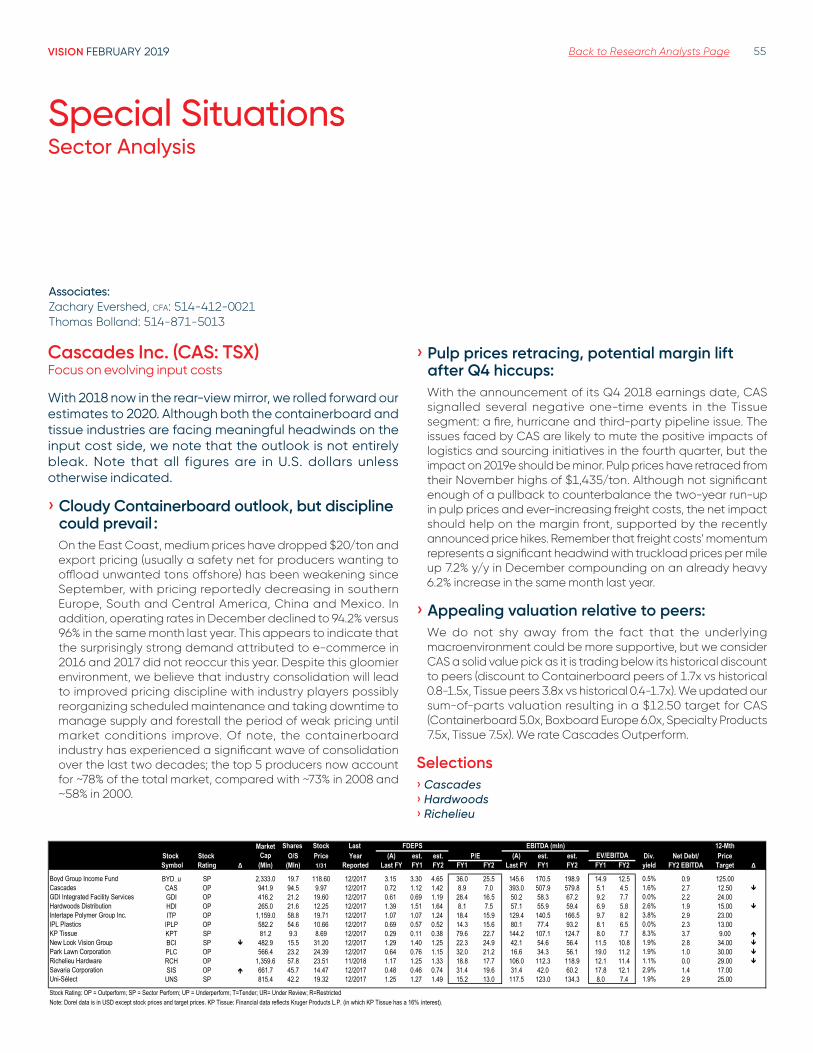

Special SituationsAssociate: Zachary Evershed 514-412-0021Associate: Thomas Bolland 514-871-5013

Endri Leno 416-869-8047Associate: Stephen Kwai 416-869-7571

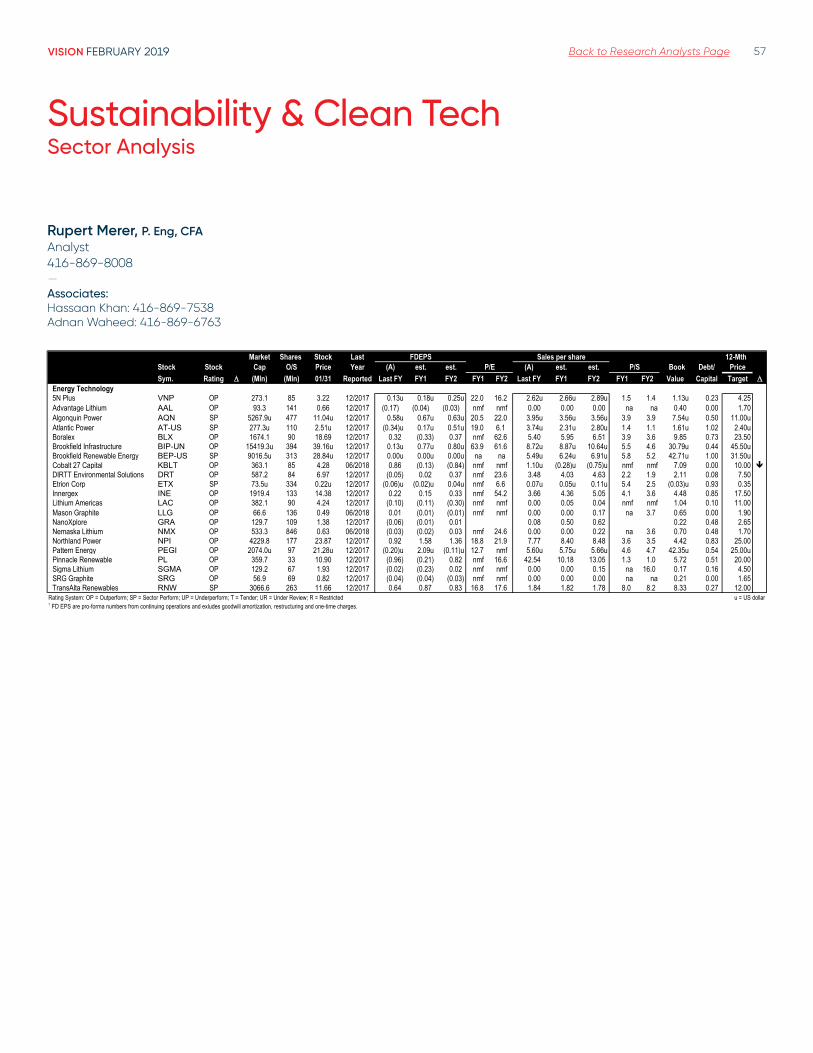

Sustainability & Clean Tech Rupert Merer 416-869-8008Associate: Hassaan Khan 416-869-7538Associate: Adnan Waheed 416-869-6763

Technology Richard Tse 416-869-6690Associate: Andrew McGee 416-869-8049Associate: John Shao 416-869-7938

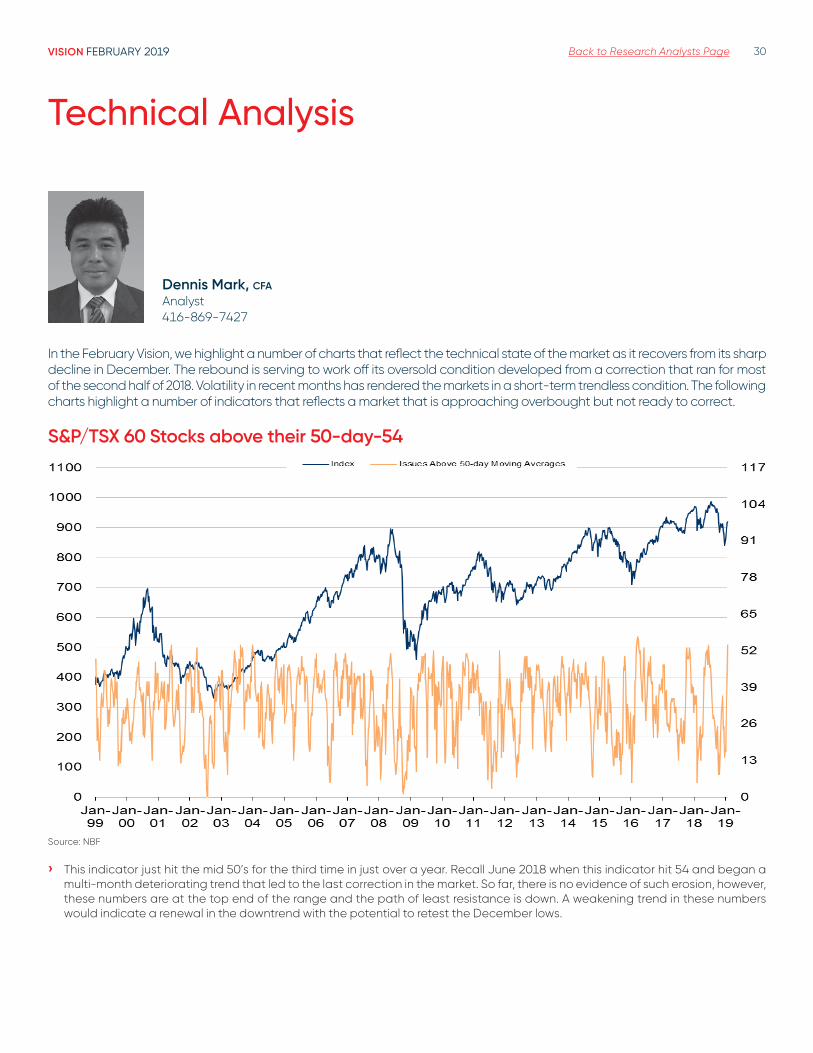

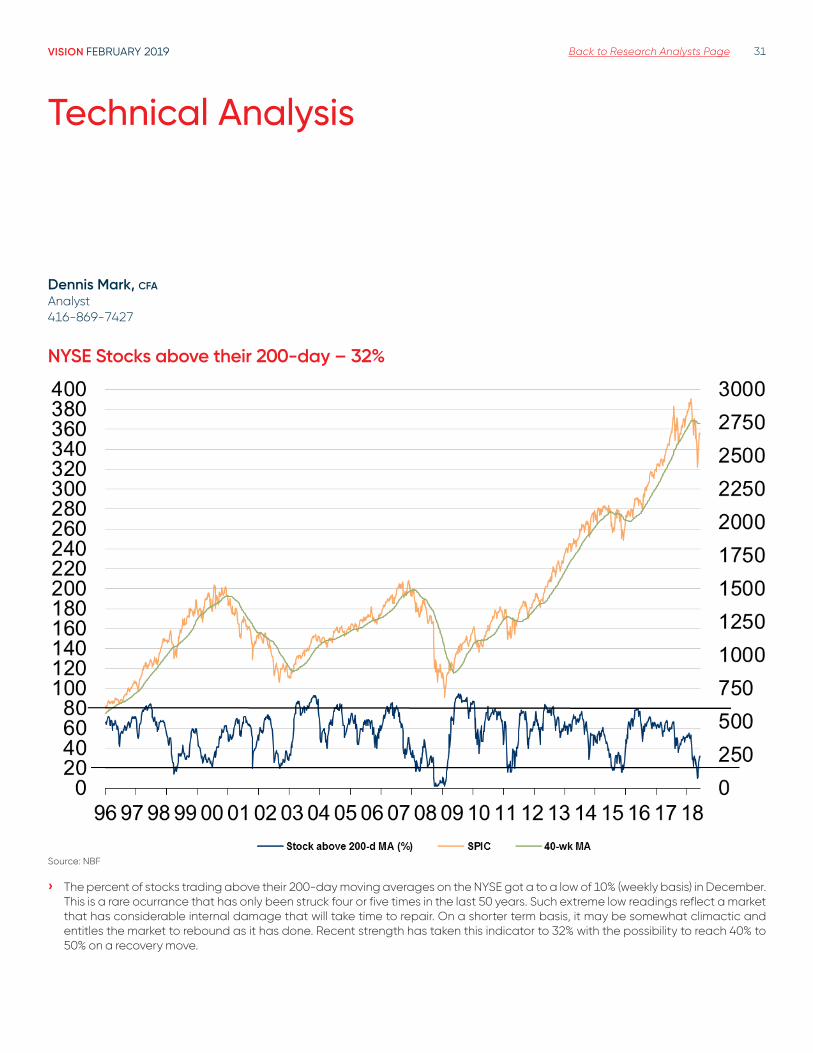

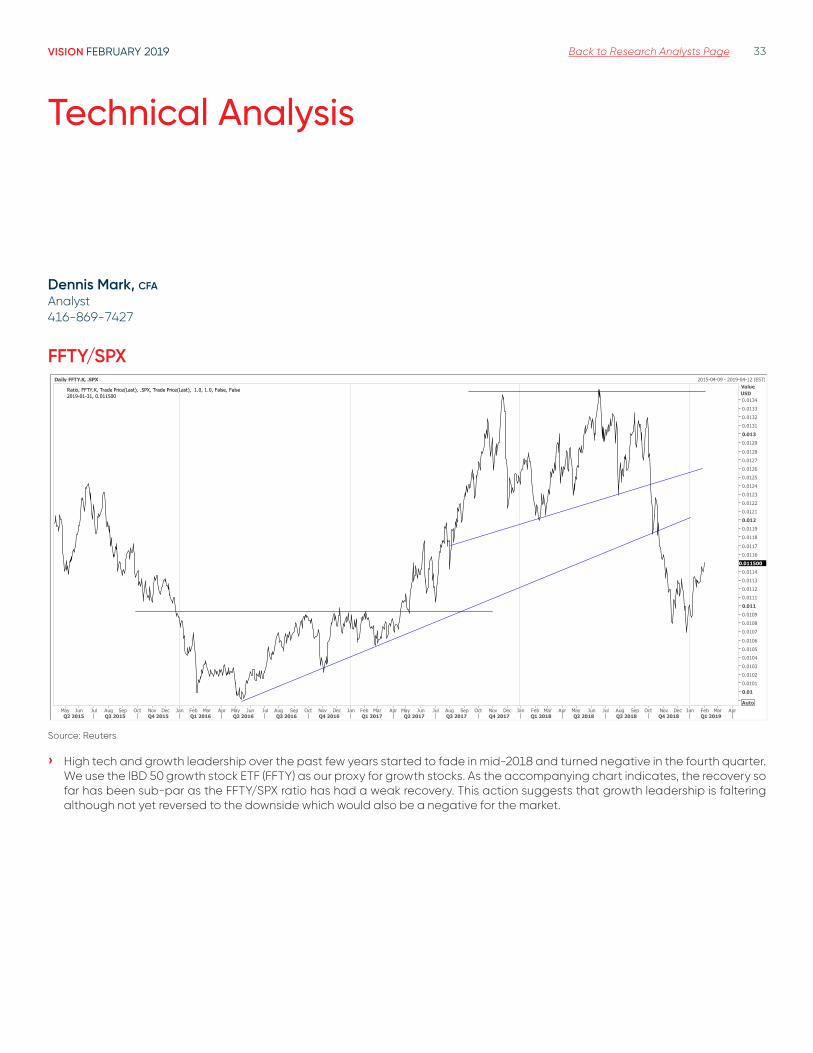

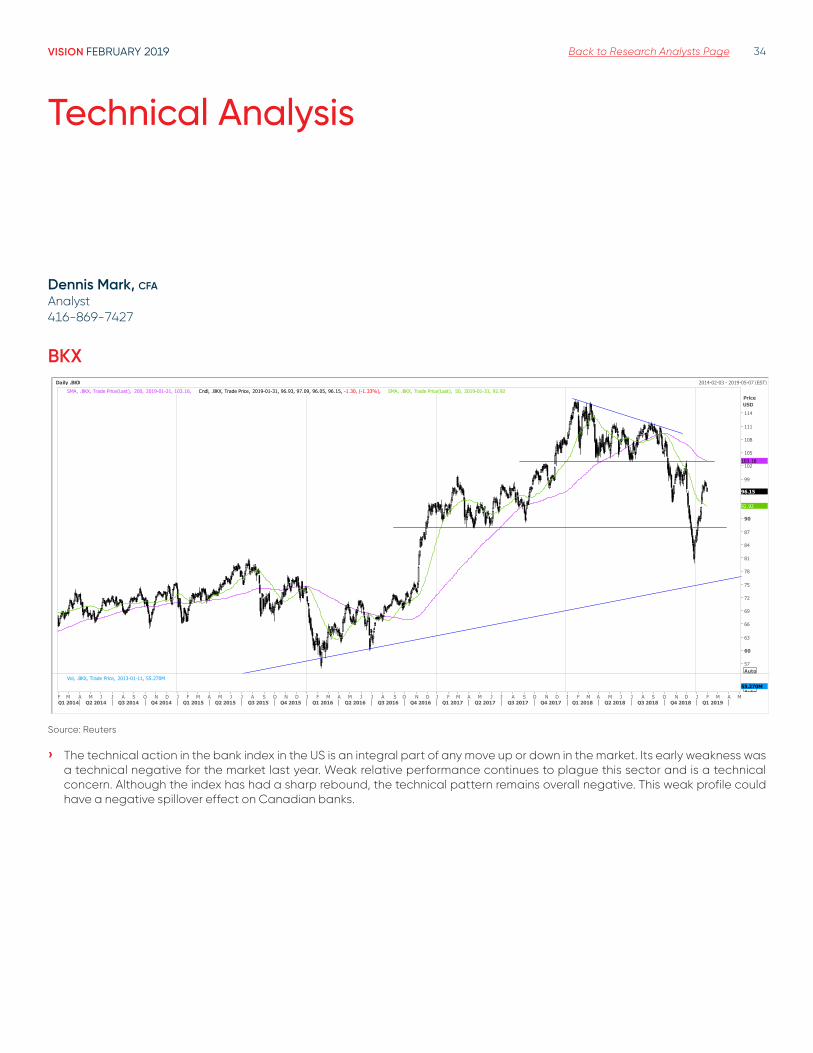

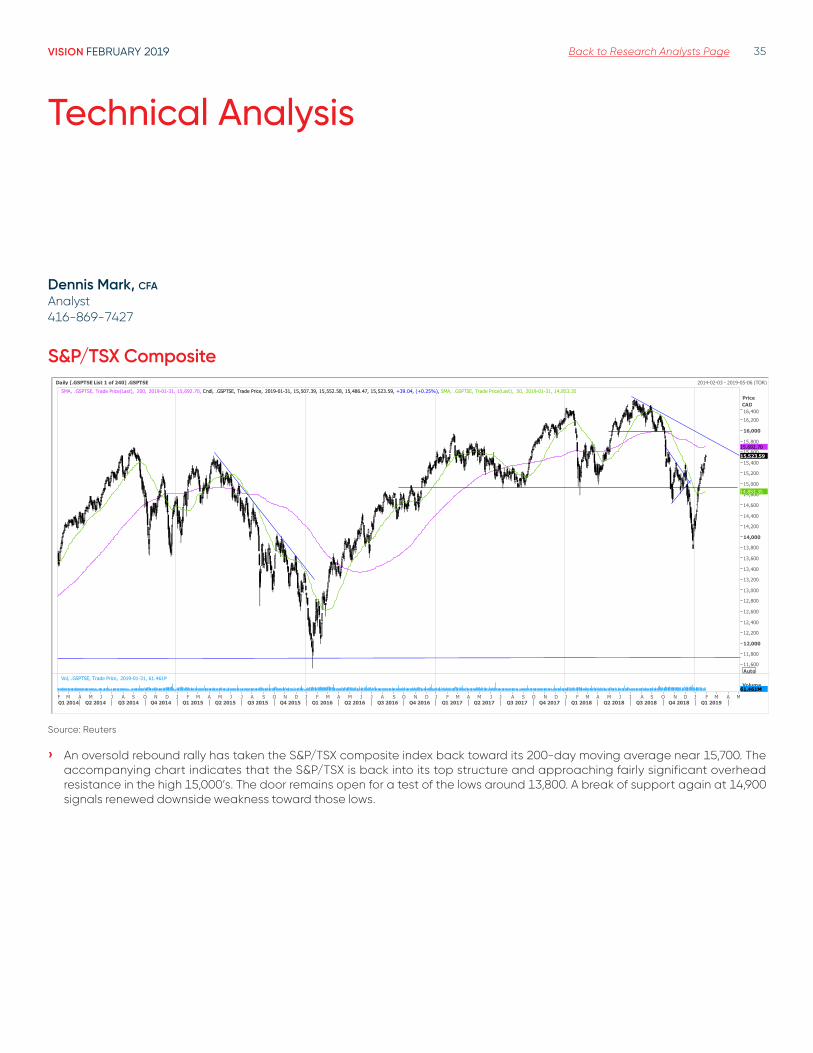

Technical AnalysisDennis Mark 416-869-7427

Telecom & MediaAdam Shine 514-879-2302Associate: Ahmed Abdullah 514-879-2564Associate: Luc Troiani 416-869-6585

Transportation & Industrial ProductsCameron Doerksen 514-879-2579Associate: Albert Matousek 514-390-7825

Back to Research Analysts Page 03

Table of Contents

Highlights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 04

The Economy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 06

Interest Rates and Bond Markets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Stock Market and Portfolio Strategy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Technical Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

Sector Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

› NBF Selection List . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

› Analysts' Tables Glossary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

› Analyst Recommendations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

› Alphabetical Listing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

NBF Disclosures, please visit URL: http://www .nbcn .ca/contactus/disclosures .html

VISION FEBRUARY 2019 Back to Research Analysts Page 04

Economy› With China and the Eurozone seemingly on the ropes, it’s difficult to

be optimistic about the global economy’s performance this year. Fortunately, the persistence of low inflation should allow major central banks to keep monetary policy accommodative while some governments, including China’s, also have room to dispatch fiscal stimulus should downside risks to growth materialize.

› While last month`s government shutdown will temporarily restrain Q1 output, we are leaving our 2019 forecast for U.S. GDP growth unchanged at 2.3% expecting a subsequent rebound. Concerns about a trade war, a slowing housing market and the possibility of an inverted yield curve should keep the Federal Reserve in pause mode for a while.

› Canada’s economy is decelerating in synch with a softening housing market and related fading wealth effects which are curtailing consumption spending, the latter already under pressure from rising interest rates and a low household savings rate. Barring fiscal relief from the federal government in 2019, consumption growth is on track for its worst year in a decade.

Interest rates and currency› In late January Fed chair Jerome Powell basically acknowledged

that unresolved government policy issues, ranging from ongoing trade negotiations and uncertainty about how long the government will avoid another shutdown, meant that he could not have strong conviction about the U.S. economic outlook. Neither can we. Much will depend on how politicians play their cards in coming weeks and months. We are optimistic as we wait for time to tell. In the meantime, we are leaving our interest-rate forecasts unchanged from last month. We continue to see one Fed rate hike in September and the 10-year Treasury yield ending the year around 3.34%. If U.S. economic growth turns out softer – say closer to 1.5% than to our base case scenario of 2.3% – then 10-year Treasuries could easily end the year closer to 2.25% or lower.

› Like the Bank of Canada, we project an acceleration of the Canadian economy after a weak first quarter. Assuming that the spot price of West Texas Intermediate crude ends the year at about US$63 and that trade tensions ease, we continue to see GDP growth of 1.8% in 2019 and headline inflation averaging 1.7% but returning to 2% by late 2019. We accordingly keep our interest-rate forecast unchanged: two BoC hikes and 10-year Canadas trading at 2.67% by year end. As with our U.S. forecast, our conviction about that outlook is less than strong.

› Amid a backdrop of decelerating domestic demand, there’s arguably little need for an aggressive monetary policy stance from the Bank of Canada. That’s not to say the Canadian dollar will necessarily struggle this year. The influence of Canada-U.S. interest rate spreads on the loonie is waning, in sharp contrast with oil which is now reasserting itself as the main driver of the Canadian currency. If we’re right about further increases for WTI oil and unimpeded global trade flows, USDCAD could move closer to our mid-year target of 1.27.

Recommended asset mix and stock market› Global equity markets rebounded smartly in January. The

7.1% jump of the MSCI ACWI was the biggest monthly increase since October 2015. Deteriorating earnings expectations have combined with a stock market rebound to push the MSCI ACWI forward P/E back up to 14 from a December 24 low of 12.4. In other words, the rise of equity indexes in recent weeks is due entirely to P/E expansion. So what’s fuelling the current optimism of equity markets? Dovish central banks and expectations of a trade deal between the U.S. and China.

› U.S. equity markets, after anticipating a major economic slowdown just a few weeks ago, are rebounding on the back of better-than-expected economic data. This is not to say GDP growth won’t slow in 2019 – we expect 1.9% Q4/Q4, down from 3.1% in 2018 – but we don’t see a contraction. With earnings showing signs of stabilizing, companies are less likely to cut back on investment and headcounts. That is key to keeping the economic expansion going. At this writing, the bottom-up consensus of equity analysts expects S&P 500 earnings per share to grow 5.7% in 2019. This estimate is in line with that for sales growth, implying no profit-margin expansion in 2019 (as we have been forecasting for the past few months). We find these expectations to be reasonable, especially in a time of USD depreciation.

› After a dismal performance in 2018, the S&P/TSX surged more than 8% in January, the best beginning of a year in 32 years. As we go to press, the S&P/TSX is trading at about 13.7 times forward earnings, up from less than 12 on December 24, 2018. That’s a 14% increase! In fact it was the largest P/E expansion among global regions so far in 2019.

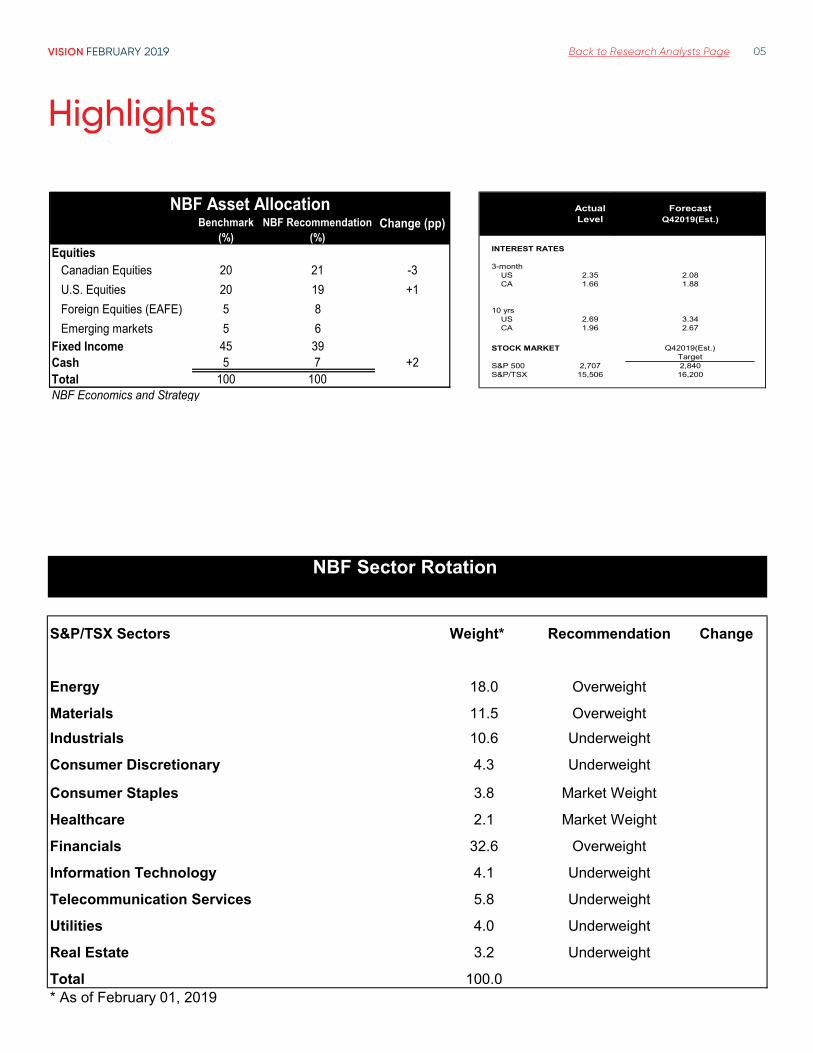

› The recent surge has left the S&P/TSX closing in on our target and a consensus outlook of EPS growth exceeding ours (9.6% vs. 6%). With upside less compelling, we are scaling back our S&P/TSX position, while keeping it slightly overweight because of our currency forecast of 1.27CAD/USD. We recommend using some of the proceeds from this trade to reduce our underweighting of the S&P 500 (where EPS and sales growth are now better aligned). We are also raising our cash recommendation to slightly overweight as we await confirmation of a U.S.-China trade truce/deal that will avert the imposition of new tariffs on March 1.

Highlights

Stéfane Marion Chief Economist and Strategist 514-879-3781

VISION FEBRUARY 2019 Back to Research Analysts Page 05

Highlights

Benchmark (%)

NBF Recommendation (%)

Change (pp)

EquitiesCanadian Equities 20 21 -3U.S. Equities 20 19 +1Foreign Equities (EAFE) 5 8Emerging markets 5 6

Fixed Income 45 39Cash 5 7 +2Total 100 100NBF Economics and Strategy

NBF Asset Allocation Actual ForecastLevel Q42019(Est.)

INTEREST RATES

3-month US 2.35 2.08 CA 1.66 1.88

10 yrs US 2.69 3.34 CA 1.96 2.67

STOCK MARKET Q42019(Est.)Target

S&P 500 2,707 2,840S&P/TSX 15,506 16,200

S&P/TSX Sectors Weight* Recommendation Change

Energy 18.0 Overweight

Materials 11.5 OverweightIndustrials 10.6 Underweight

Consumer Discretionary 4.3 Underweight

Consumer Staples 3.8 Market Weight

Healthcare 2.1 Market Weight

Financials 32.6 Overweight

Information Technology 4.1 Underweight

Telecommunication Services 5.8 Underweight

Utilities 4.0 Underweight

Real Estate 3.2 Underweight

Total 100.0* As of February 01, 2019

NBF Sector Rotation

VISION FEBRUARY 2019 Back to Research Analysts Page 06

The Economy

VISION FEBRUARY 2019 Back to Research Analysts Page 07

The Economy

Krishen Rangasamy Senior Economist 514-879-3140

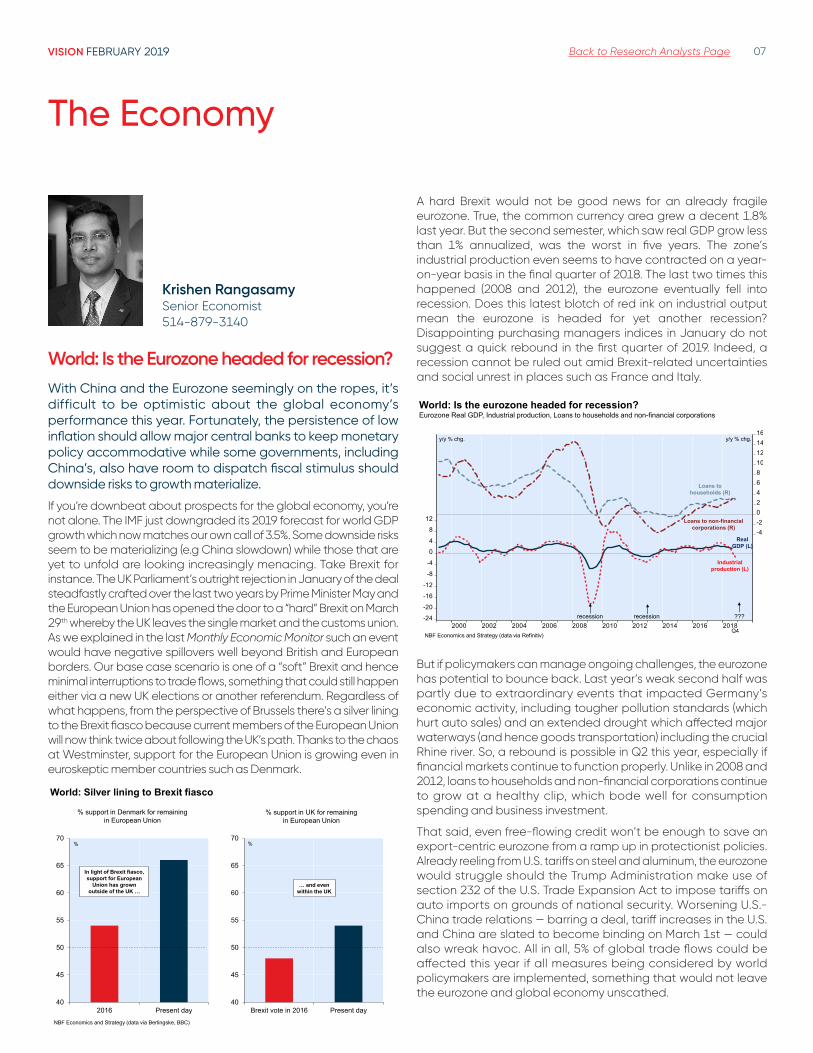

World: Is the Eurozone headed for recession?With China and the Eurozone seemingly on the ropes, it’s difficult to be optimistic about the global economy’s performance this year. Fortunately, the persistence of low inflation should allow major central banks to keep monetary policy accommodative while some governments, including China’s, also have room to dispatch fiscal stimulus should downside risks to growth materialize.

If you’re downbeat about prospects for the global economy, you’re not alone. The IMF just downgraded its 2019 forecast for world GDP growth which now matches our own call of 3.5%. Some downside risks seem to be materializing (e.g China slowdown) while those that are yet to unfold are looking increasingly menacing. Take Brexit for instance. The UK Parliament’s outright rejection in January of the deal steadfastly crafted over the last two years by Prime Minister May and the European Union has opened the door to a “hard” Brexit on March 29th whereby the UK leaves the single market and the customs union. As we explained in the last Monthly Economic Monitor such an event would have negative spillovers well beyond British and European borders. Our base case scenario is one of a “soft” Brexit and hence minimal interruptions to trade flows, something that could still happen either via a new UK elections or another referendum. Regardless of what happens, from the perspective of Brussels there’s a silver lining to the Brexit fiasco because current members of the European Union will now think twice about following the UK’s path. Thanks to the chaos at Westminster, support for the European Union is growing even in euroskeptic member countries such as Denmark.

40

45

50

55

60

65

70

2016 Present day40

45

50

55

60

65

70

Brexit vote in 2016 Present day

World: Silver lining to Brexit fiasco

%

NBF Economics and Strategy (data via Berlingske, BBC)

% support in Denmark for remaining in European Union

% support in UK for remaining in European Union

In light of Brexit fiasco, support for European

Union has grown outside of the UK …

… and even within the UK

%

A hard Brexit would not be good news for an already fragile eurozone. True, the common currency area grew a decent 1.8% last year. But the second semester, which saw real GDP grow less than 1% annualized, was the worst in five years. The zone’s industrial production even seems to have contracted on a year-on-year basis in the final quarter of 2018. The last two times this happened (2008 and 2012), the eurozone eventually fell into recession. Does this latest blotch of red ink on industrial output mean the eurozone is headed for yet another recession? Disappointing purchasing managers indices in January do not suggest a quick rebound in the first quarter of 2019. Indeed, a recession cannot be ruled out amid Brexit-related uncertainties and social unrest in places such as France and Italy.

-24

-20

-16

-12

-8

-4

0

4

8

12

-4-20246810121416

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018NBF Economics and Strategy (data via Refinitiv)

World: Is the eurozone headed for recession?Eurozone Real GDP, Industrial production, Loans to households and non-financial corporations

Real GDP (L)

Industrial production (L)

y/y % chg.

Q4

y/y % chg.

Loans to non-financialcorporations (R)

Loans to households (R)

recession recession ???

But if policymakers can manage ongoing challenges, the eurozone has potential to bounce back. Last year’s weak second half was partly due to extraordinary events that impacted Germany’s economic activity, including tougher pollution standards (which hurt auto sales) and an extended drought which affected major waterways (and hence goods transportation) including the crucial Rhine river. So, a rebound is possible in Q2 this year, especially if financial markets continue to function properly. Unlike in 2008 and 2012, loans to households and non-financial corporations continue to grow at a healthy clip, which bode well for consumption spending and business investment.

That said, even free-flowing credit won’t be enough to save an export-centric eurozone from a ramp up in protectionist policies. Already reeling from U.S. tariffs on steel and aluminum, the eurozone would struggle should the Trump Administration make use of section 232 of the U.S. Trade Expansion Act to impose tariffs on auto imports on grounds of national security. Worsening U.S.-China trade relations — barring a deal, tariff increases in the U.S. and China are slated to become binding on March 1st — could also wreak havoc. All in all, 5% of global trade flows could be affected this year if all measures being considered by world policymakers are implemented, something that would not leave the eurozone and global economy unscathed.

VISION FEBRUARY 2019 Back to Research Analysts Page 08

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

2018q1 2018q2 2018q3 2018q4 2019q1 2019q2 2019q3 2019q4NBF Economics and Strategy (data via World Bank)

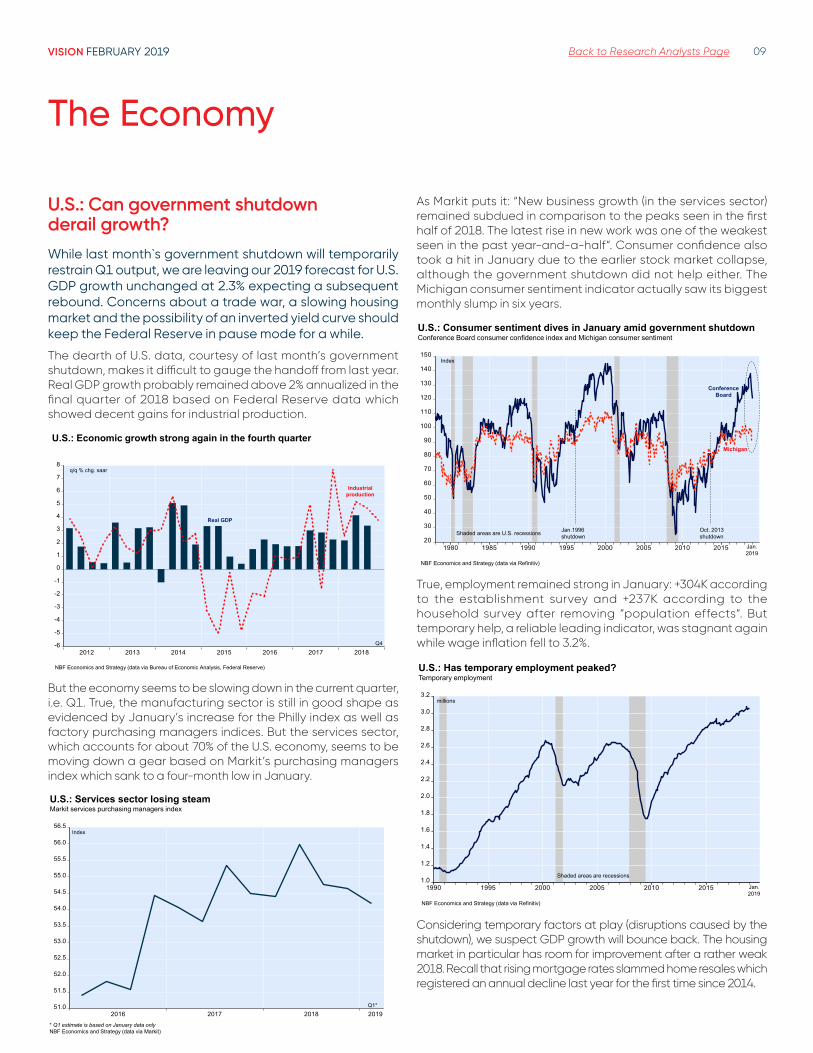

World: Ramp up of protectionism in 2019?Imports affected by tariffs

U.S.

Rest of the world

% of world goods imports Measures being considered by policymakers

Rest of the world

U.S.

China’s slowdown is also hurting investor confidence. While the world’s second largest economy grew a decent 6.6% last year, that was the lowest GDP growth print since 1990. The deceleration should, however, not be surprising all things considered. Actions by Beijing to curtail risks posed by shadow banking, while necessary for long term stability of the financial system, have capped credit expansion. Social financing, the broad measure of credit flows in China, totalled 19.3 trillion yuan in 2018, or roughly 3 trillion yuan lower than the preceding year. Investment outlays (including real estate), and hence GDP growth, were restrained as a result. We suspect a similar outcome in 2019.

0

2

4

6

8

10

12

14

16

18

20

22

24

2002 2004 2006 2008 2010 2012 2014 2016 2018NBF Economics and Strategy (data via Refinitiv)

World: Why is China’s economy slowing?Social financing

New bank loans

Other credit

Trillion yuan

Trade was also a drag on China’s growth last year as imports grew faster than exports. Because of an elevated real effective yuan, we’re not expecting that dynamic to change in 2019, even if a trade deal is struck with the U.S. But that’s not to say China’s GDP growth is about to collapse. The central government has proven in the past that it can support the economy via fiscal and monetary policy stimulus. Announcements in January including tax relief for small businesses and cuts to the reserve requirement ratio are likely to be followed by additional measures should growth fall short of Beijing’s expectations. As such we continue to expect China to post annual growth rates north of 6% this year and next.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018NBF Economics and Strategy (data via Refinitiv)

China: Goods trade surplus falls for third consecutive yearGoods trade by year

Exports

Imports

US$ trillion

Balance

World Economic Outlook

Forecast

2018 2019 2020Advanced countries 2.3 1.9 1.8United States 2.9 2.3 1.9Euroland 1.8 1.6 1.7Japan 0.9 1.1 0.5UK 1.4 1.5 1.6Canada 2.0 1.8 1.7Australia 3.2 2.7 2.7New Zealand 3.1 2.7 3.1Hong Kong 3.8 2.4 3.0Korea 2.8 2.5 2.8Taiwan 2.7 2.2 2.3Singapore 2.9 2.6 2.7

Emerging Asia 6.5 6.3 6.3China 6.6 6.3 6.2India 7.3 7.4 7.7Indonesia 5.1 5.1 5.2Malaysia 4.7 4.5 4.8Philippines 6.5 6.3 6.6Thailand 4.6 3.8 3.7

Latin America 1.1 1.8 2.0Mexico 2.1 1.9 2.2Brazil 1.3 2.4 2.2Argentina -2.6 -1.1 2.2Venezuela -18.0 -12.8 -2.0Colombia 2.8 3.4 3.7

Eastern Europe and CIS 3.0 2.0 2.1Russia 1.7 1.5 1.7Czech Rep. 3.1 2.9 2.5Poland 4.4 3.7 3.0Turkey 3.5 -0.2 2.6

Middle East and N. Africa 2.1 2.5 3.0

Sub-Saharan Africa 3.1 3.7 3.9

Advanced economies 2.3 1.9 1.8Emerging economies 4.6 4.6 4.7World 3.7 3.5 3.5

Source: NBF Economics and Strategy

The Economy

VISION FEBRUARY 2019 Back to Research Analysts Page 09

U .S .: Can government shutdown derail growth?While last month`s government shutdown will temporarily restrain Q1 output, we are leaving our 2019 forecast for U.S. GDP growth unchanged at 2.3% expecting a subsequent rebound. Concerns about a trade war, a slowing housing market and the possibility of an inverted yield curve should keep the Federal Reserve in pause mode for a while.

The dearth of U.S. data, courtesy of last month’s government shutdown, makes it difficult to gauge the handoff from last year. Real GDP growth probably remained above 2% annualized in the final quarter of 2018 based on Federal Reserve data which showed decent gains for industrial production.

-6

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

2012 2013 2014 2015 2016 2017 2018

U.S.: Economic growth strong again in the fourth quarter

NBF Economics and Strategy (data via Bureau of Economic Analysis, Federal Reserve)

q/q % chg. saar

Industrial production

Real GDP

Q4

But the economy seems to be slowing down in the current quarter, i.e. Q1. True, the manufacturing sector is still in good shape as evidenced by January’s increase for the Philly index as well as factory purchasing managers indices. But the services sector, which accounts for about 70% of the U.S. economy, seems to be moving down a gear based on Markit’s purchasing managers index which sank to a four-month low in January.

51.0

51.5

52.0

52.5

53.0

53.5

54.0

54.5

55.0

55.5

56.0

56.5

2016 2017 2018 2019

U.S.: Services sector losing steamMarkit services purchasing managers index

* Q1 estimate is based on January data only NBF Economics and Strategy (data via Markit)

Index

Q1*

As Markit puts it: “New business growth (in the services sector) remained subdued in comparison to the peaks seen in the first half of 2018. The latest rise in new work was one of the weakest seen in the past year-and-a-half“. Consumer confidence also took a hit in January due to the earlier stock market collapse, although the government shutdown did not help either. The Michigan consumer sentiment indicator actually saw its biggest monthly slump in six years.

20

30

40

50

60

70

80

90

100

110

120

130

140

150

1980 1985 1990 1995 2000 2005 2010 2015

NBF Economics and Strategy (data via Refinitiv)

Index

Jan. 2019

U.S.: Consumer sentiment dives in January amid government shutdown Conference Board consumer confidence index and Michigan consumer sentiment

Shaded areas are U.S. recessions Oct. 2013 shutdown

Jan.1996shutdown

Michigan

Conference Board

True, employment remained strong in January: +304K according to the establishment survey and +237K according to the household survey after removing “population effects“. But temporary help, a reliable leading indicator, was stagnant again while wage inflation fell to 3.2%.

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

3.0

3.2

1990 1995 2000 2005 2010 2015

U.S.: Has temporary employment peaked?Temporary employment

NBF Economics and Strategy (data via Refinitiv)

millions

Shaded areas are recessions

Jan. 2019

Considering temporary factors at play (disruptions caused by the shutdown), we suspect GDP growth will bounce back. The housing market in particular has room for improvement after a rather weak 2018. Recall that rising mortgage rates slammed home resales which registered an annual decline last year for the first time since 2014.

The Economy

VISION FEBRUARY 2019 Back to Research Analysts Page 10

4.04.24.4

4.64.85.0

5.25.45.6

3.6

4.0

4.4

4.8

5.2

5.6

6.0

6.4

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

U.S.: Home resales see annual decline for the first time since 2014Sales of existing homes versus Effective mortgage rate

Home resales (L)

Effective rate on 30-yr mortgage (R)

NBF Economics and Strategy (data via National Association of Realtors)

million units %

But with the Fed making clear that it is pacing down monetary policy tightening, home sales can recover in 2019. For clues about the sensitivity of home buyers to rates, one just needs to look at the surge in mortgage applications which coincided with the recent drop in long rates. Also supporting our positive view of the U.S. housing market is the fact that over the last decade the gap between resale price inflation and income growth hasn’t diverged a whole lot, unlike the excesses observed before the 2006 crash. Positive housing wealth effects, a high savings rate, and the best household balance sheet in 34 years (see January’s Monthly Economic Monitor) bode well for consumption spending this year.

-10.0-7.5-5.0-2.50.02.55.07.5

10.012.515.0 3

4

5

6

7

8

9

10

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

U.S.: Housing market in a better position than in 2006 Case-Shiller house price index, disposable income and personal savings rate

Case-Shiller (L)Disposable income (L)

NBF Economics and Strategy (data via Refinitiv)

y/y % chg. %

Savings rate (R)

That’s not to say the U.S. is in the clear. As we’ve pointed out before, another financial crisis cannot be ruled out, more so considering a bubbly-looking corporate bond market. The U.S. government is ironically also a threat to growth. January’s shutdown has already shown that politicians are willing to sacrifice prosperity for popularity. Another shutdown is possible in February (when the temporary truce ends) or later in the year when the debt ceiling debate heats up. Reckless trade policies could also be implemented by Washington to gain votes. While popular in “Rust Belt” states, protectionist

measures could backfire on the U.S. economy, and not just through retaliatory tariffs from slighted trade partners. According to the Federal Reserve Bank of San Francisco, the local content of imports into the U.S. is roughly 43% on average. In other words, 43% of U.S. expenditures on goods made in foreign countries stays in America either through payments to retailers or for logistics. At 56%, the local content of “made in China” is even larger than the average.

0

10

20

30

40

50

60

TOTAL China Mexico Canada Japan Euro

U.S.: More than half of spending on “made in China” goods stays in U.S.Share of local content of U.S. imports

%

NBF Economics and Strategy (data via Federal Reserve Bank of San Francisco)

56% of spending on “made in China” goods stays in U.S.

China has been trying to de-escalate tensions by reportedly agreeing to boost its imports from the U.S. enough to eliminate the bilateral trade deficit by the end of 2024. Recall that last year’s U.S. goods trade deficit with China amounted to more than US$420 billion. Cutting that massive tally to zero in six years would entail an unprecedented combination of strong growth of U.S. exports to China and weak growth of U.S. imports from China. Even if U.S. imports from China remain flat from now through 2024, exports would have to grow at least 29% every year for six years to erase the trade deficit. Such pace of sustained growth for U.S. exports to China has never happened before, not even when China’s real GDP growth was in double digits. In other words, Beijing is unlikely to deliver on its promises, which suggests the ongoing trade war is far from over.

-440

-400

-360

-320

-280

-240

-200

-160

-120

-80

-40

0

1995 2000 2005 2010 2015 2020 2025

U.S.: Can the trade deficit with China be erased by 2024? U.S. goods trade balance with China

NBF Economics and Strategy (data via U.S. Census Bureau, NBF calculations)

US$ bn If imports remain unchanged (i.e. 0%

growth), exports have to grow 29%

every year

If imports grow 10% annually, exports have to grow 42%

every year

Scenarios to balance trade by 2024

If imports grow 5% annually, exports have to grow 35%

every year

The Economy

VISION FEBRUARY 2019 Back to Research Analysts Page 11

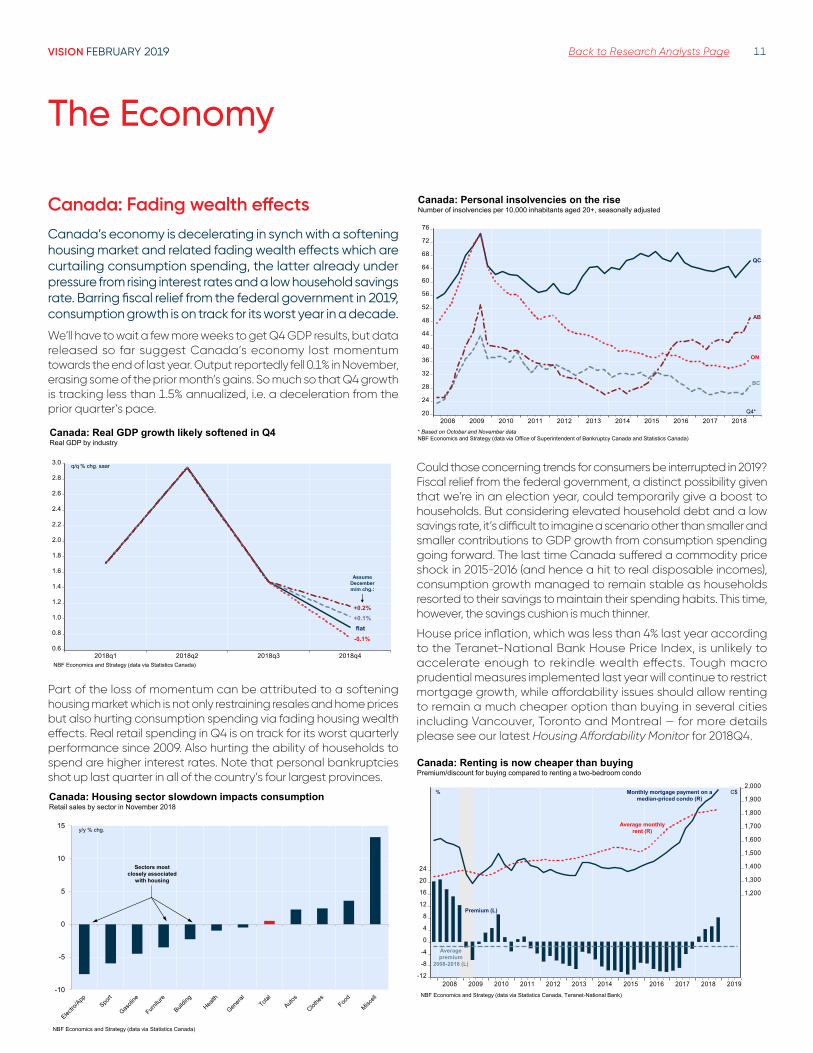

Canada: Fading wealth effectsCanada’s economy is decelerating in synch with a softening housing market and related fading wealth effects which are curtailing consumption spending, the latter already under pressure from rising interest rates and a low household savings rate. Barring fiscal relief from the federal government in 2019, consumption growth is on track for its worst year in a decade.

We’ll have to wait a few more weeks to get Q4 GDP results, but data released so far suggest Canada’s economy lost momentum towards the end of last year. Output reportedly fell 0.1% in November, erasing some of the prior month’s gains. So much so that Q4 growth is tracking less than 1.5% annualized, i.e. a deceleration from the prior quarter’s pace.

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

3.0

2018q1 2018q2 2018q3 2018q4

Canada: Real GDP growth likely softened in Q4Real GDP by industry

q/q % chg. saar

NBF Economics and Strategy (data via Statistics Canada)

-0.1%

+0.1%flat

Assume December m/m chg.:

+0.2%

Part of the loss of momentum can be attributed to a softening housing market which is not only restraining resales and home prices but also hurting consumption spending via fading housing wealth effects. Real retail spending in Q4 is on track for its worst quarterly performance since 2009. Also hurting the ability of households to spend are higher interest rates. Note that personal bankruptcies shot up last quarter in all of the country’s four largest provinces.

-10

-5

0

5

10

15

Canada: Housing sector slowdown impacts consumptionRetail sales by sector in November 2018

y/y % chg.

NBF Economics and Strategy (data via Statistics Canada)

Sectors most closely associated

with housing

20

24

28

32

36

40

44

48

52

56

60

64

68

72

76

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Canada: Personal insolvencies on the riseNumber of insolvencies per 10,000 inhabitants aged 20+, seasonally adjusted

QC

ON

Q4*

AB

BC

* Based on October and November data NBF Economics and Strategy (data via Office of Superintendent of Bankruptcy Canada and Statistics Canada)

Could those concerning trends for consumers be interrupted in 2019? Fiscal relief from the federal government, a distinct possibility given that we’re in an election year, could temporarily give a boost to households. But considering elevated household debt and a low savings rate, it’s difficult to imagine a scenario other than smaller and smaller contributions to GDP growth from consumption spending going forward. The last time Canada suffered a commodity price shock in 2015-2016 (and hence a hit to real disposable incomes), consumption growth managed to remain stable as households resorted to their savings to maintain their spending habits. This time, however, the savings cushion is much thinner.

House price inflation, which was less than 4% last year according to the Teranet-National Bank House Price Index, is unlikely to accelerate enough to rekindle wealth effects. Tough macro prudential measures implemented last year will continue to restrict mortgage growth, while affordability issues should allow renting to remain a much cheaper option than buying in several cities including Vancouver, Toronto and Montreal — for more details please see our latest Housing Affordability Monitor for 2018Q4.

-12

-8

-4

0

4

8

12

16

20

24

1,200

1,300

1,400

1,500

1,600

1,700

1,800

1,900

2,000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Canada: Renting is now cheaper than buyingPremium/discount for buying compared to renting a two-bedroom condo

NBF Economics and Strategy (data via Statistics Canada, Teranet-National Bank)

C$Monthly mortgage payment on a median-priced condo (R)

Average monthlyrent (R)

Premium (L)

Averagepremium

2008-2018 (L)

%

The Economy

VISION FEBRUARY 2019 Back to Research Analysts Page 12

Fortunately for consumers, not all is bleak. The labour market is expected to continue generating jobs in 2019, albeit at a slower pace than last year. The Bank of Canada’s latest Business Outlook Survey indeed suggested firms were still willing to expand headcount to address shortages in some areas. At the end of 2018, the balance of opinion on hiring (over the next 12 months) rose to 41. In the past, such levels of intention translated into decent job growth.

-200-150-100-50

050

100150200250300350400450500550

-15

-10

-5

0

5

10

15

20

25

30

35

40

45

50

55

60

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Canada: Firms positive about hiring plans Employment according to Labour Force Survey versus Balance of opinion* on hiring over the next 12 months

* Share of firms that expect increased employment over the next 12 months minus share expecting lower employment NBF Economics and Strategy (data via Statistics Canada, Bank of Canada)

y/y chg. in thousands Employment (L)

Balance of opinion* on hiring at the end of previous year (R)

Also limiting the damage somewhat on consumers is the likelihood of a slower pace of monetary policy tightening by the Bank of Canada. The central bank indeed expressed concerns about the economic outlook and downgraded its 2019 growth forecast last month for Canada to just 1.7% (roughly in line with our own call of 1.8%). And with the central bank’s projected GDP growth forecast over 2019-2020 averaging close to the estimated potential of 1.8%, the output gap is set to remain open for several quarters. As such we expect the Bank of Canada’s overnight rate to remain unchanged through at least the first half this year.

-4.0

-3.5

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Canada: Output gap likely to remain open for several quarters Bank of Canada’s estimate of the output gap (average of Integrated framework and Extended multivariate filter)

* Projections based on BoC’s GDP growth forecasts and Potential GDP growth of 1.8% over forecast horizon NBF Economics and Strategy (data via Bank of Canada)

% Projections*

Just a few days after the Bank of Canada published its downgraded growth forecasts, Statistics Canada provided more bad news with updated data on business creation, one of Governor Poloz’s “favourite

variables”. The number of private sector firms in Q3 last year was up just 0.7% compared to the same quarter the previous year. That’s about half a percentage point lower than the average since 2001. The softness in business formation is in part due to declines in the population of firms in hard-hit sectors such as mining and oil & gas, but also in retailing, wholesaling and utilities. The tepid pace of business creation coupled with depressed commodity prices does not bode well for business investment spending going forward.

-0.8

-0.4

0.0

0.4

0.8

1.2

1.6

2.0

2.4

2.8

3.2

3.6

2002 2004 2006 2008 2010 2012 2014 2016 2018

Canada: Business formation stalls Number of active employer businesses in the private sector

NBF Economics and Strategy (data via Statistics Canada)

y/y % chg.

Q3

Average2001-2018

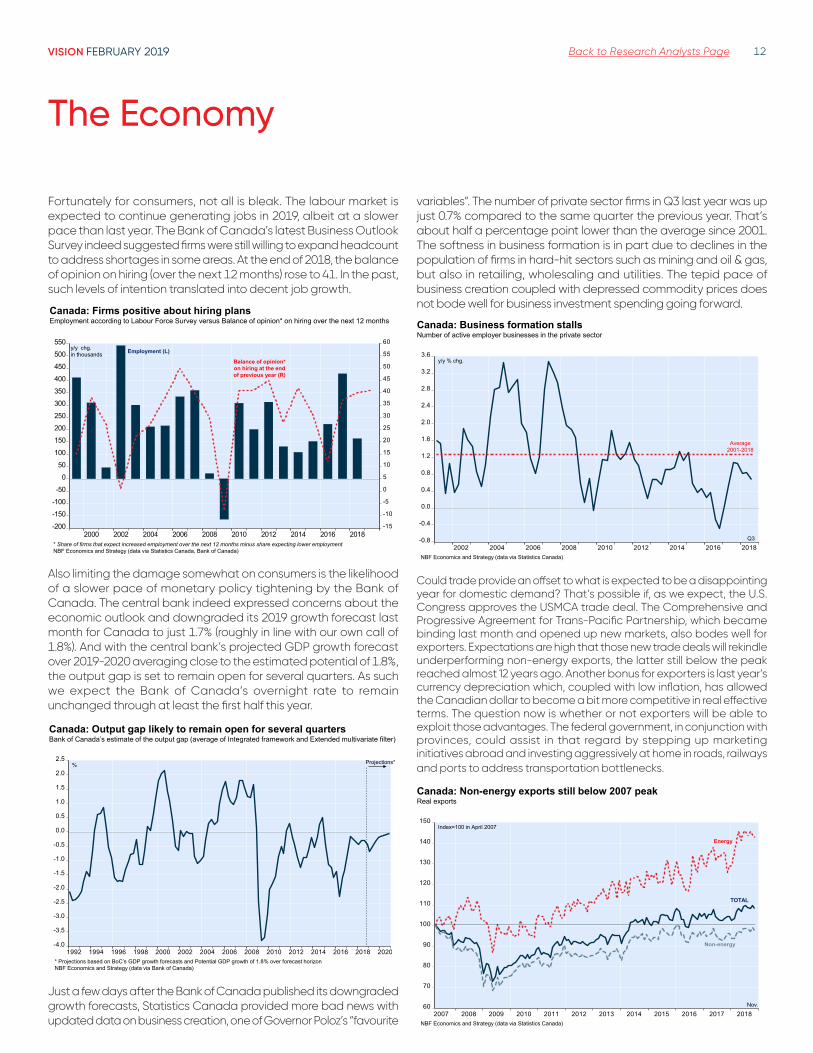

Could trade provide an offset to what is expected to be a disappointing year for domestic demand? That’s possible if, as we expect, the U.S. Congress approves the USMCA trade deal. The Comprehensive and Progressive Agreement for Trans-Pacific Partnership, which became binding last month and opened up new markets, also bodes well for exporters. Expectations are high that those new trade deals will rekindle underperforming non-energy exports, the latter still below the peak reached almost 12 years ago. Another bonus for exporters is last year’s currency depreciation which, coupled with low inflation, has allowed the Canadian dollar to become a bit more competitive in real effective terms. The question now is whether or not exporters will be able to exploit those advantages. The federal government, in conjunction with provinces, could assist in that regard by stepping up marketing initiatives abroad and investing aggressively at home in roads, railways and ports to address transportation bottlenecks.

60

70

80

90

100

110

120

130

140

150

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Canada: Non-energy exports still below 2007 peak Real exports

NBF Economics and Strategy (data via Statistics Canada)

Index=100 in April 2007

Nov.

Energy

TOTAL

Non-energy

The Economy

VISION FEBRUARY 2019 Back to Research Analysts Page 13

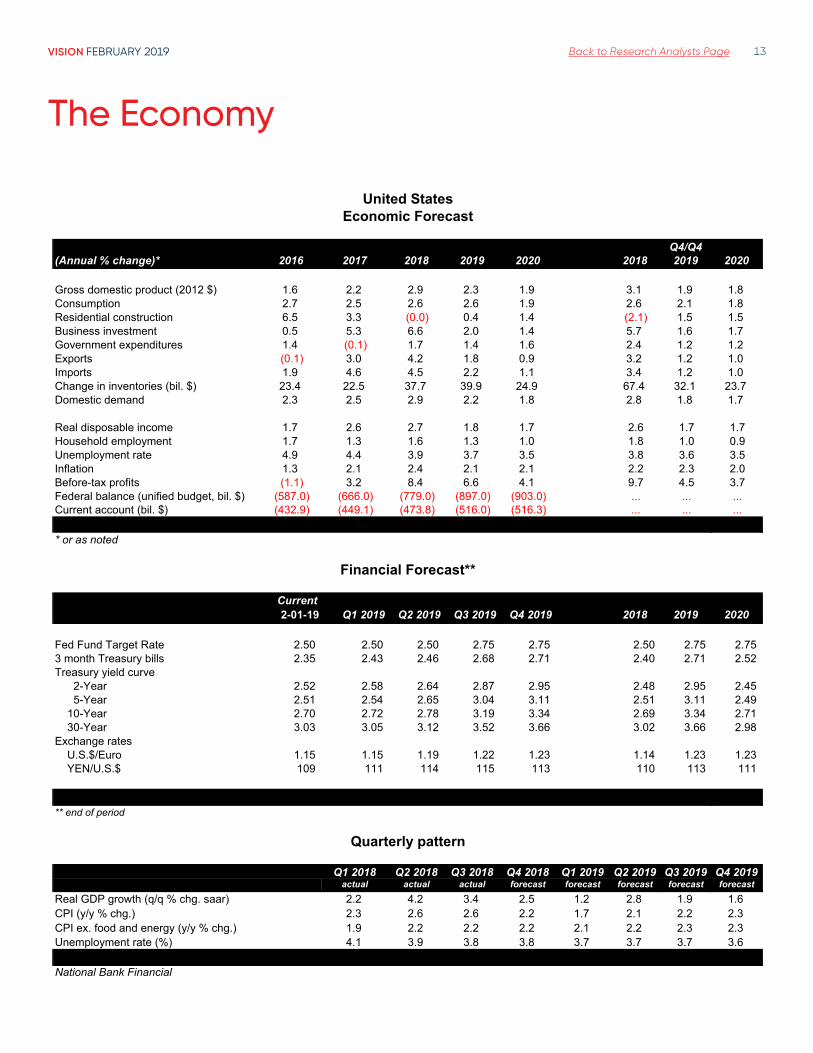

Q4/Q4(Annual % change)* 2016 2017 2018 2019 2020 2006 2018 2019 2020

Gross domestic product (2012 $) 1.6 2.2 2.9 2.3 1.9 3.1 1.9 1.8Consumption 2.7 2.5 2.6 2.6 1.9 2.6 2.1 1.8Residential construction 6.5 3.3 (0.0) 0.4 1.4 (2.1) 1.5 1.5Business investment 0.5 5.3 6.6 2.0 1.4 5.7 1.6 1.7Government expenditures 1.4 (0.1) 1.7 1.4 1.6 2.4 1.2 1.2Exports (0.1) 3.0 4.2 1.8 0.9 3.2 1.2 1.0Imports 1.9 4.6 4.5 2.2 1.1 3.4 1.2 1.0Change in inventories (bil. $) 23.4 22.5 37.7 39.9 24.9 67.4 32.1 23.7Domestic demand 2.3 2.5 2.9 2.2 1.8 2.8 1.8 1.7

Real disposable income 1.7 2.6 2.7 1.8 1.7 2.6 1.7 1.7Household employment 1.7 1.3 1.6 1.3 1.0 1.8 1.0 0.9Unemployment rate 4.9 4.4 3.9 3.7 3.5 3.8 3.6 3.5Inflation 1.3 2.1 2.4 2.1 2.1 2.2 2.3 2.0Before-tax profits (1.1) 3.2 8.4 6.6 4.1 9.7 4.5 3.7Federal balance (unified budget, bil. $) (587.0) (666.0) (779.0) (897.0) (903.0) ... ... ...Current account (bil. $) (432.9) (449.1) (473.8) (516.0) (516.3) ... ... ...

-304* or as noted

Current Q4 2018 Q4 2019 Q4 20202-01-19 Q1 2019 Q2 2019 Q3 2019 Q4 2019 2018 2019 2020

Fed Fund Target Rate 2.50 2.50 2.50 2.75 2.75 2.50 2.75 2.75 3 month Treasury bills 2.35 2.43 2.46 2.68 2.71 2.40 2.71 2.52 Treasury yield curve 2-Year 2.52 2.58 2.64 2.87 2.95 2.48 2.95 2.45 5-Year 2.51 2.54 2.65 3.04 3.11 2.51 3.11 2.49 10-Year 2.70 2.72 2.78 3.19 3.34 2.69 3.34 2.71 30-Year 3.03 3.05 3.12 3.52 3.66 3.02 3.66 2.98 Exchange rates U.S.$/Euro 1.15 1.15 1.19 1.22 1.23 1.14 1.23 1.23 YEN/U.S.$ 109 111 114 115 113 110 113 111

** end of period

Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019actual actual actual forecast forecast forecast forecast forecast

Real GDP growth (q/q % chg. saar) 2.2 4.2 3.4 2.5 1.2 2.8 1.9 1.6CPI (y/y % chg.) 2.3 2.6 2.6 2.2 1.7 2.1 2.2 2.3CPI ex. food and energy (y/y % chg.) 1.9 2.2 2.2 2.2 2.1 2.2 2.3 2.3Unemployment rate (%) 4.1 3.9 3.8 3.8 3.7 3.7 3.7 3.6

National Bank Financial

Financial Forecast**

Quarterly pattern

United StatesEconomic Forecast

The Economy

VISION FEBRUARY 2019 Back to Research Analysts Page 14

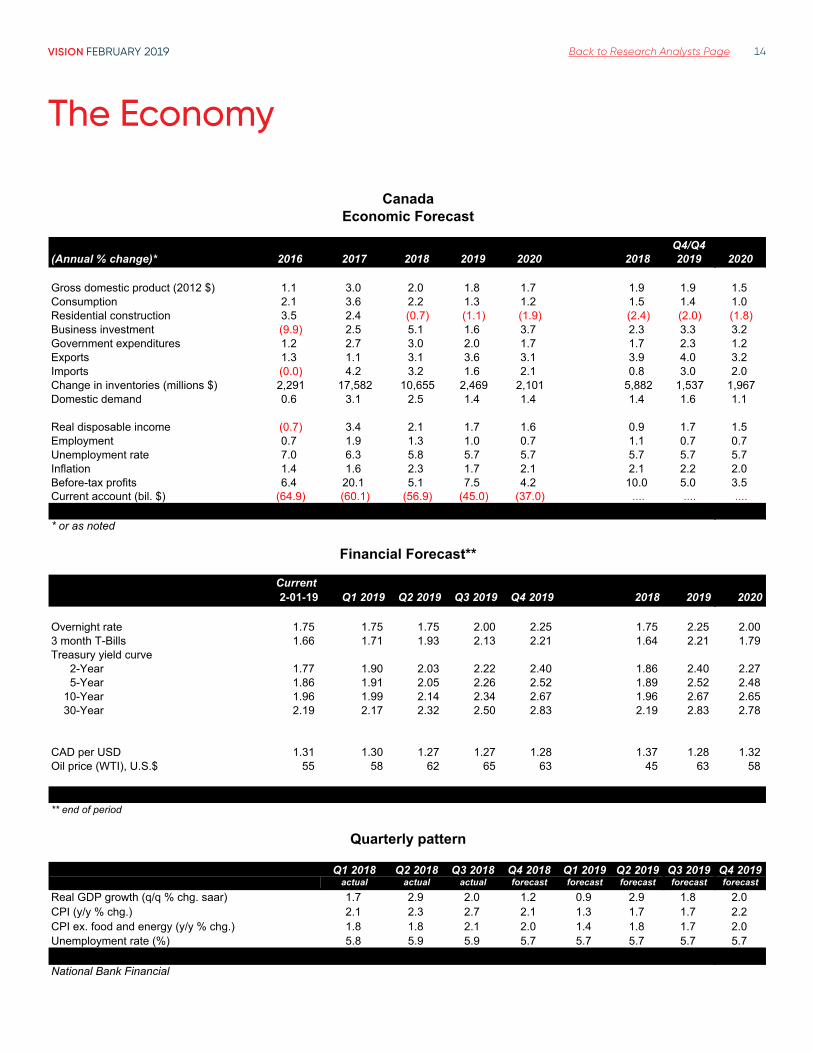

Q4/Q4(Annual % change)* 2016 2017 2018 2019 2020 2018 2019 2020

Gross domestic product (2012 $) 1.1 3.0 2.0 1.8 1.7 1.9 1.9 1.5Consumption 2.1 3.6 2.2 1.3 1.2 1.5 1.4 1.0Residential construction 3.5 2.4 (0.7) (1.1) (1.9) (2.4) (2.0) (1.8)Business investment (9.9) 2.5 5.1 1.6 3.7 2.3 3.3 3.2Government expenditures 1.2 2.7 3.0 2.0 1.7 1.7 2.3 1.2Exports 1.3 1.1 3.1 3.6 3.1 3.9 4.0 3.2Imports (0.0) 4.2 3.2 1.6 2.1 0.8 3.0 2.0Change in inventories (millions $) 2,291 17,582 10,655 2,469 2,101 5,882 1,537 1,967Domestic demand 0.6 3.1 2.5 1.4 1.4 1.4 1.6 1.1

Real disposable income (0.7) 3.4 2.1 1.7 1.6 0.9 1.7 1.5Employment 0.7 1.9 1.3 1.0 0.7 1.1 0.7 0.7Unemployment rate 7.0 6.3 5.8 5.7 5.7 5.7 5.7 5.7Inflation 1.4 1.6 2.3 1.7 2.1 2.1 2.2 2.0Before-tax profits 6.4 20.1 5.1 7.5 4.2 10.0 5.0 3.5Current account (bil. $) (64.9) (60.1) (56.9) (45.0) (37.0) .... .... ....

* or as noted

Current Q4 2018 Q4 2019 Q4 20202-01-19 Q1 2019 Q2 2019 Q3 2019 Q4 2019 2018 2019 2020

Overnight rate 1.75 1.75 1.75 2.00 2.25 1.75 2.25 2.00 3 month T-Bills 1.66 1.71 1.93 2.13 2.21 1.64 2.21 1.79 Treasury yield curve 2-Year 1.77 1.90 2.03 2.22 2.40 1.86 2.40 2.27 5-Year 1.86 1.91 2.05 2.26 2.52 1.89 2.52 2.48 10-Year 1.96 1.99 2.14 2.34 2.67 1.96 2.67 2.65 30-Year 2.19 2.17 2.32 2.50 2.83 2.19 2.83 2.78

CAD per USD 1.31 1.30 1.27 1.27 1.28 1.37 1.28 1.32 Oil price (WTI), U.S.$ 55 58 62 65 63 45 63 58

** end of period

Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019actual actual actual forecast forecast forecast forecast forecast

Real GDP growth (q/q % chg. saar) 1.7 2.9 2.0 1.2 0.9 2.9 1.8 2.0CPI (y/y % chg.) 2.1 2.3 2.7 2.1 1.3 1.7 1.7 2.2CPI ex. food and energy (y/y % chg.) 1.8 1.8 2.1 2.0 1.4 1.8 1.7 2.0Unemployment rate (%) 5.8 5.9 5.9 5.7 5.7 5.7 5.7 5.7

National Bank Financial

CanadaEconomic Forecast

Financial Forecast**

Quarterly pattern

The Economy

VISION FEBRUARY 2019 Back to Research Analysts Page 15

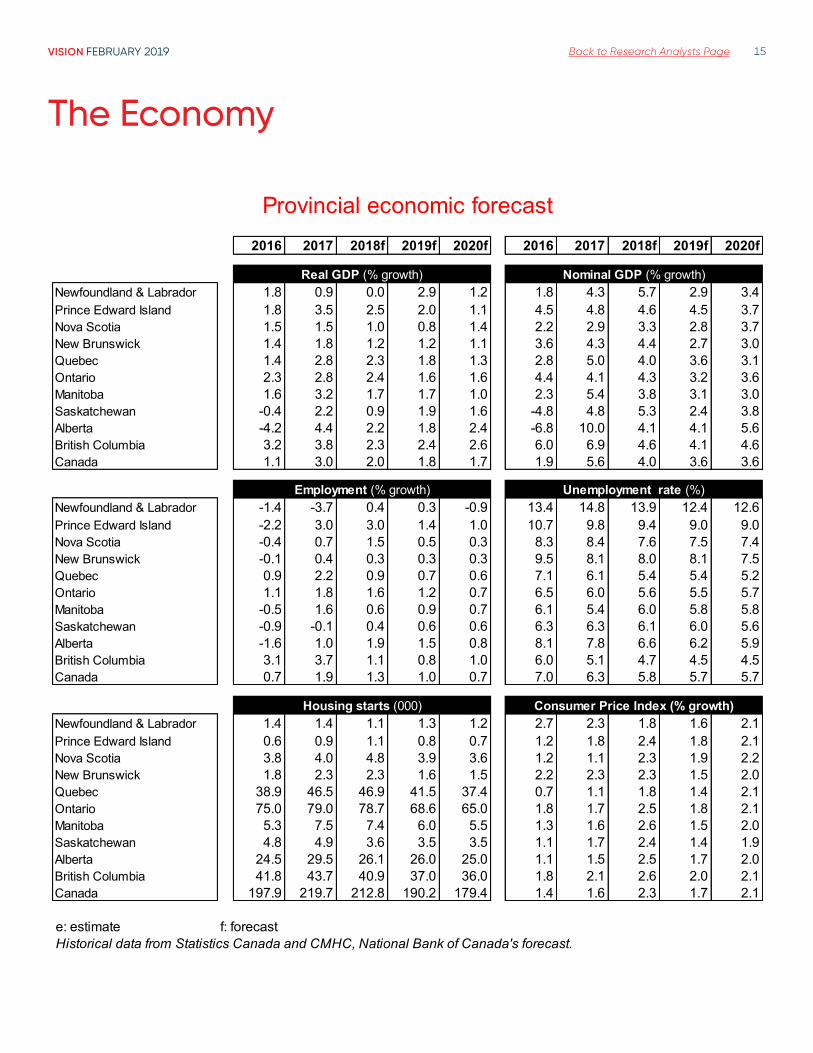

Provincial economic forecast2016 2017 2018f 2019f 2020f 2016 2017 2018f 2019f 2020f

Real GDP (% growth) Nominal GDP (% growth)Newfoundland & Labrador 1.8 0.9 0.0 2.9 1.2 1.8 4.3 5.7 2.9 3.4Prince Edward Island 1.8 3.5 2.5 2.0 1.1 4.5 4.8 4.6 4.5 3.7Nova Scotia 1.5 1.5 1.0 0.8 1.4 2.2 2.9 3.3 2.8 3.7New Brunswick 1.4 1.8 1.2 1.2 1.1 3.6 4.3 4.4 2.7 3.0Quebec 1.4 2.8 2.3 1.8 1.3 2.8 5.0 4.0 3.6 3.1Ontario 2.3 2.8 2.4 1.6 1.6 4.4 4.1 4.3 3.2 3.6Manitoba 1.6 3.2 1.7 1.7 1.0 2.3 5.4 3.8 3.1 3.0Saskatchewan -0.4 2.2 0.9 1.9 1.6 -4.8 4.8 5.3 2.4 3.8Alberta -4.2 4.4 2.2 1.8 2.4 -6.8 10.0 4.1 4.1 5.6British Columbia 3.2 3.8 2.3 2.4 2.6 6.0 6.9 4.6 4.1 4.6Canada 1.1 3.0 2.0 1.8 1.7 1.9 5.6 4.0 3.6 3.6

Employment (% growth) Unemployment rate (%)Newfoundland & Labrador -1.4 -3.7 0.4 0.3 -0.9 13.4 14.8 13.9 12.4 12.6Prince Edward Island -2.2 3.0 3.0 1.4 1.0 10.7 9.8 9.4 9.0 9.0Nova Scotia -0.4 0.7 1.5 0.5 0.3 8.3 8.4 7.6 7.5 7.4New Brunswick -0.1 0.4 0.3 0.3 0.3 9.5 8.1 8.0 8.1 7.5Quebec 0.9 2.2 0.9 0.7 0.6 7.1 6.1 5.4 5.4 5.2Ontario 1.1 1.8 1.6 1.2 0.7 6.5 6.0 5.6 5.5 5.7Manitoba -0.5 1.6 0.6 0.9 0.7 6.1 5.4 6.0 5.8 5.8Saskatchewan -0.9 -0.1 0.4 0.6 0.6 6.3 6.3 6.1 6.0 5.6Alberta -1.6 1.0 1.9 1.5 0.8 8.1 7.8 6.6 6.2 5.9British Columbia 3.1 3.7 1.1 0.8 1.0 6.0 5.1 4.7 4.5 4.5Canada 0.7 1.9 1.3 1.0 0.7 7.0 6.3 5.8 5.7 5.7

Housing starts (000) Consumer Price Index (% growth)Newfoundland & Labrador 1.4 1.4 1.1 1.3 1.2 2.7 2.3 1.8 1.6 2.1Prince Edward Island 0.6 0.9 1.1 0.8 0.7 1.2 1.8 2.4 1.8 2.1Nova Scotia 3.8 4.0 4.8 3.9 3.6 1.2 1.1 2.3 1.9 2.2New Brunswick 1.8 2.3 2.3 1.6 1.5 2.2 2.3 2.3 1.5 2.0Quebec 38.9 46.5 46.9 41.5 37.4 0.7 1.1 1.8 1.4 2.1Ontario 75.0 79.0 78.7 68.6 65.0 1.8 1.7 2.5 1.8 2.1Manitoba 5.3 7.5 7.4 6.0 5.5 1.3 1.6 2.6 1.5 2.0Saskatchewan 4.8 4.9 3.6 3.5 3.5 1.1 1.7 2.4 1.4 1.9Alberta 24.5 29.5 26.1 26.0 25.0 1.1 1.5 2.5 1.7 2.0British Columbia 41.8 43.7 40.9 37.0 36.0 1.8 2.1 2.6 2.0 2.1Canada 197.9 219.7 212.8 190.2 179.4 1.4 1.6 2.3 1.7 2.1

e: estimate f: forecastHistorical data from Statistics Canada and CMHC, National Bank of Canada's forecast.

The Economy

VISION FEBRUARY 2019 Back to Research Analysts Page 16

Interest Ratesand Bond Markets

VISION FEBRUARY 2019 Back to Research Analysts Page 17

Interest Rates and Bond Markets

Paul-André Pinsonnault Senior Fixed Income Economist 514-879-3795

Faced with weakening of global growth, central bankers talk patienceThe rhetoric of central bankers has taken a dovish turn. In the U.S., with inflation pressures still mild, Fed officials have made clear they think they can afford to be patient in their normalizing of monetary policy. In Japan, the latest BoJ quarterly outlook shows a 2-tick downward revision of inflation forecasts for both 2019 and 2020. The Bank of Canada adjusted its narrative in early January, revising its growth forecast for 2019 down substantially from 2.1% to 1.7%. In Europe, the ECB assesses risks to the Eurozone economy as skewed to the downside.

In recognition that economic momentum is likely to be weaker in the near term than first expected, discussion among forecasters is focusing on the factors in the current softening of the outlook and how persistent they might prove.

Time will tell. High on everyone’s list of key risks to the global economy are the outcome of trade negotiations and the evolution of financial conditions in coming quarters. Most forecasts assume that trade divergences/tensions will be more or less ironed out. The consensus sees 2019 global growth averaging 3.5%, compared to the 3.7% estimated by the IMF for 2018.

The BoC projects acceleration of the Canadian economy after a weak first quarter. In the view of BoC governor Stephen Poloz, its soft patch is temporary and insufficient to affect inflation materially in the medium term. But the Bank recognizes significant uncertainties in its projections. How will U.S.-China trade relations evolve? Will Congressional ratification of the USMCA be delayed? How long will oil prices stay soft? How will investment, terms of trade and national income be affected? And finally, the Canadian housing market has been softer than the BoC expected. It is unclear how much of this is due to various municipal or provincial measures as well as federal macroprudential initiatives. Higher mortgage rates have obviously taken a toll. Any of these items on the Bank of Canada watch list could influence its monetary policy decisions.

Since GDP forecasts necessarily make assumptions about exogenous economic variables and the behaviour of politicians, discrepancies between what is forecast on the eve of a new year and the actual growth over that year are hardly surprising.

-4

-3

-2

-1

0

1

2

3

4

5

6

1990 1995 2000 2005 2010 2015 2020

Canada: Actual GDP growth vs. beginning-of-year consensus forecastMedian absolute forecast error since the last recession: 0.6 percentage points

% y/y

NBF Economics and Strategy (data via Refinitiv)

Forecast

Actual

The median absolute error of consensus forecasts since the last recession is significant. Forecast error was particularly eye-catching in the 2015-2017 period, one main factor being the unexpected oil shock and the extent of the energy sector rebound in 2017.

75

80

85

90

95

100

105

110

115

120

125

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Canada: Perspective on Canadian economy since 2007Real gross domestic product, constant 2007 dollars

NBF Economics and Strategy (data via Statistics Canada)

Rest of the economy(84% of the economy)

Energy(9% of the economy)

Non-energy commodities

(7% of the economy)25-bp BcCrate cuts

25-bp BcCrate hikes

January 2007 = 100

However numerous the potential sources of forecasting error may be, they do not dispense us from providing point estimates for the overnight rate and the shape of the yield curve. First, some of the assumptions in our base case scenario: The spot price of West Texas Intermediate crude will end the year at about US$63 compared to the current US$53.17. The CAD will trade around 1.28 to the USD by year end compared to 1.3277 at this writing. On the political front, we join the consensus view that trade tensions are likely to ease. On these assumptions, we continue to see the Canadian economy growing 1.8% in 2019 and headline inflation averaging 1.7% but returning to 2% by late 2019.

In other words, our base case scenario has not changed. We accordingly keep our interest-rate forecast unchanged: two BoC hikes and 10-year Canadas trading at 2.67% by year end.

VISION FEBRUARY 2019 Back to Research Analysts Page 18

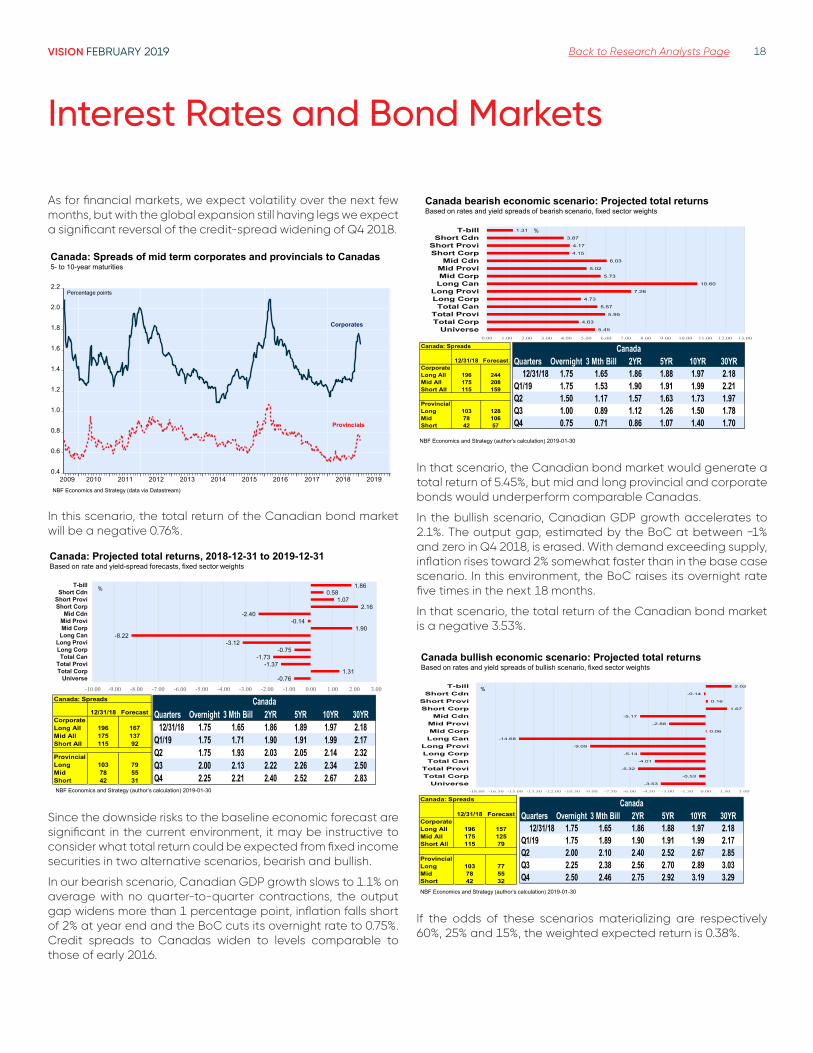

As for financial markets, we expect volatility over the next few months, but with the global expansion still having legs we expect a significant reversal of the credit-spread widening of Q4 2018.

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019NBF Economics and Strategy (data via Datastream)

Percentage points

Canada: Spreads of mid term corporates and provincials to Canadas5- to 10-year maturities

Corporates

Provincials

In this scenario, the total return of the Canadian bond market will be a negative 0.76%.

%

Canada: Projected total returns, 2018-12-31 to 2019-12-31Based on rate and yield-spread forecasts, fixed sector weights

NBF Economics and Strategy (author’s calculation) 2019-01-30

Canada: Spreads

12/31/18 ForecastCorporateLong All 196 167Mid All 175 137Short All 115 92

ProvincialLong 103 79Mid 78 55Short 42 31

-0.761.31

-1.37-1.73

-0.75-3.12

-8.221.90

-0.14-2.40

2.161.07

0.581.86

-10.00 -9.00 -8.00 -7.00 -6.00 -5.00 -4.00 -3.00 -2.00 -1.00 0.00 1.00 2.00 3.00

UniverseTotal CorpTotal Provi

Total CanLong CorpLong Provi

Long CanMid CorpMid Provi

Mid CdnShort CorpShort Provi

Short CdnT-bill %

Quarters Overnight 3 Mth Bill 2YR 5YR 10YR 30YR12/31/18 1.75 1.65 1.86 1.89 1.97 2.18

Q1/19 1.75 1.71 1.90 1.91 1.99 2.17Q2 1.75 1.93 2.03 2.05 2.14 2.32Q3 2.00 2.13 2.22 2.26 2.34 2.50Q4 2.25 2.21 2.40 2.52 2.67 2.83

Canada

Since the downside risks to the baseline economic forecast are significant in the current environment, it may be instructive to consider what total return could be expected from fixed income securities in two alternative scenarios, bearish and bullish.

In our bearish scenario, Canadian GDP growth slows to 1.1% on average with no quarter-to-quarter contractions, the output gap widens more than 1 percentage point, inflation falls short of 2% at year end and the BoC cuts its overnight rate to 0.75%. Credit spreads to Canadas widen to levels comparable to those of early 2016.

5.45

4.63

5.95

5.57

4.73

7.26

10.60

5.73

5.02

6.03

4.15

4.17

3.87

1.31

0.00 1.00 2.00 3.00 4.00 5.00 6.00 7.00 8.00 9.00 10.00 11.00 12.00 13.00

UniverseTotal CorpTotal Provi

Total CanLong CorpLong Provi

Long CanMid CorpMid Provi

Mid CdnShort CorpShort Provi

Short CdnT-bill %

Canada bearish economic scenario: Projected total returnsBased on rates and yield spreads of bearish scenario, fixed sector weights

NBF Economics and Strategy (author’s calculation) 2019-01-30

Canada: Spreads

12/31/18 ForecastCorporateLong All 196 244Mid All 175 208Short All 115 159

ProvincialLong 103 128Mid 78 106Short 42 57

Quarters Overnight 3 Mth Bill 2YR 5YR 10YR 30YR12/31/18 1.75 1.65 1.86 1.88 1.97 2.18

Q1/19 1.75 1.53 1.90 1.91 1.99 2.21Q2 1.50 1.17 1.57 1.63 1.73 1.97Q3 1.00 0.89 1.12 1.26 1.50 1.78Q4 0.75 0.71 0.86 1.07 1.40 1.70

Canada

In that scenario, the Canadian bond market would generate a total return of 5.45%, but mid and long provincial and corporate bonds would underperform comparable Canadas.

In the bullish scenario, Canadian GDP growth accelerates to 2.1%. The output gap, estimated by the BoC at between −1% and zero in Q4 2018, is erased. With demand exceeding supply, inflation rises toward 2% somewhat faster than in the base case scenario. In this environment, the BoC raises its overnight rate five times in the next 18 months.

In that scenario, the total return of the Canadian bond market is a negative 3.53%.

-3.53

-0.53

-5.32

-4.01

-5.14

-9.09

-14.68

0.06

-2.88

-5.17

1.67

0.16

-0.14

2.02

-18.00 -16.50 -15.00 -13.50 -12.00 -10.50 -9.00 -7.50 -6.00 -4.50 -3.00 -1.50 0.00 1.50 3.00

UniverseTotal CorpTotal Provi

Total CanLong CorpLong Provi

Long CanMid CorpMid Provi

Mid CdnShort CorpShort Provi

Short CdnT-bill

Canada: Spreads

12/31/18 ForecastCorporateLong All 196 157Mid All 175 125Short All 115 79

ProvincialLong 103 77Mid 78 55Short 42 32

Canada bullish economic scenario: Projected total returnsBased on rates and yield spreads of bullish scenario, fixed sector weights

NBF Economics and Strategy (author’s calculation) 2019-01-30

%

Quarters Overnight 3 Mth Bill 2YR 5YR 10YR 30YR12/31/18 1.75 1.65 1.86 1.88 1.97 2.18

Q1/19 1.75 1.89 1.90 1.91 1.99 2.17Q2 2.00 2.10 2.40 2.52 2.67 2.85Q3 2.25 2.38 2.56 2.70 2.89 3.03Q4 2.50 2.46 2.75 2.92 3.19 3.29

Canada

If the odds of these scenarios materializing are respectively 60%, 25% and 15%, the weighted expected return is 0.38%.

Interest Rates and Bond Markets

VISION FEBRUARY 2019 Back to Research Analysts Page 19

… and in the U .S .As widely expected, the Federal Reserve left the fed funds rate unchanged at 2.25-2.50% in January. The FOMC changed its communication significantly by removing from its press release the sentence about further gradual increases in the fed funds rate. The Fed now says “the Committee will be patient as it determines what future adjustments to the target range for the federal funds rate may be appropriate” to support “sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee's symmetric 2 percent objective.” At the post-rate-announcement press conference, Fed chair Jerome Powell said the FOMC sees the outlook as generally favourable but noted that indicators such as business confidence surveys are sending warning signals. The FOMC intends to let the data clarify what adjustments to the policy stance will be required over time, but has no strong a priori view on rates at this stage, Mr. Powell said.

In other words, the data will determine how long the Fed will be patient. We note that the FOMC press release expressed sensitivity to “muted inflation pressures” and downside risks to the global economy. All in all, the Fed’s statement of January 30 does not change our view that there will be no more than one interest rate hike this year.

A fair portion of Mr. Powell’s post-rate-announcement press conference was devoted to the FOMC’s plans for normalization of its balance sheet. The Committee is still evaluating the right size for the Fed’s balance sheet and expects to complete its evaluation over coming meetings. However, it has formally decided that it will “continue to implement monetary policy in a regime in which an ample supply of reserves ensures” that the fed funds rate will be controlled primarily through the setting of administered rates.

Bottom line At that January 30 press conference, Mr. Powell basically acknowledged that unresolved government policy issues, ranging from ongoing trade negotiations and uncertainty about how long the government will avoid another shutdown, meant that he could not have strong conviction about the U.S. economic outlook. Moreover, growth has slowed in some major foreign economies at a time when the risk of a hard Brexit is on the rise.

For the same reasons, our own conviction about our baseline scenario is no stronger (60% odds). Much will depend on how politicians play their cards in coming weeks and months. We are optimistic as we wait for time to tell. Meanwhile, with inflation muted and the fed funds target range above core PCE inflation, the Fed has the luxury of waiting and seeing.

So we leave our interest-rate forecasts unchanged from last month. We continue to see one Fed rate hike in September and the 10-year Treasury yield ending the year around 3.34%. If economic growth turns out softer – say closer to 1.5% than to our base case scenario of 2.3% – then 10-year Treasuries could easily end the year closer to 2.25%.

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

3.0

3.2

3.4

3.6

3.8

4.0

4.2

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019NBF Economics and Strategy (data via Bloomberg) 2019-01-31

3.76

3.25

2.83

2.54

2.25

1.89

1.32

%

10-year Treasury yield at year end: 3.375% or 2.125%?The Fed lacked economic visibility to hazard a balance-of-risks assessment in its press release

Interest Rates and Bond Markets

VISION FEBRUARY 2019 Back to Research Analysts Page 20

Interest Rates and Bond Markets

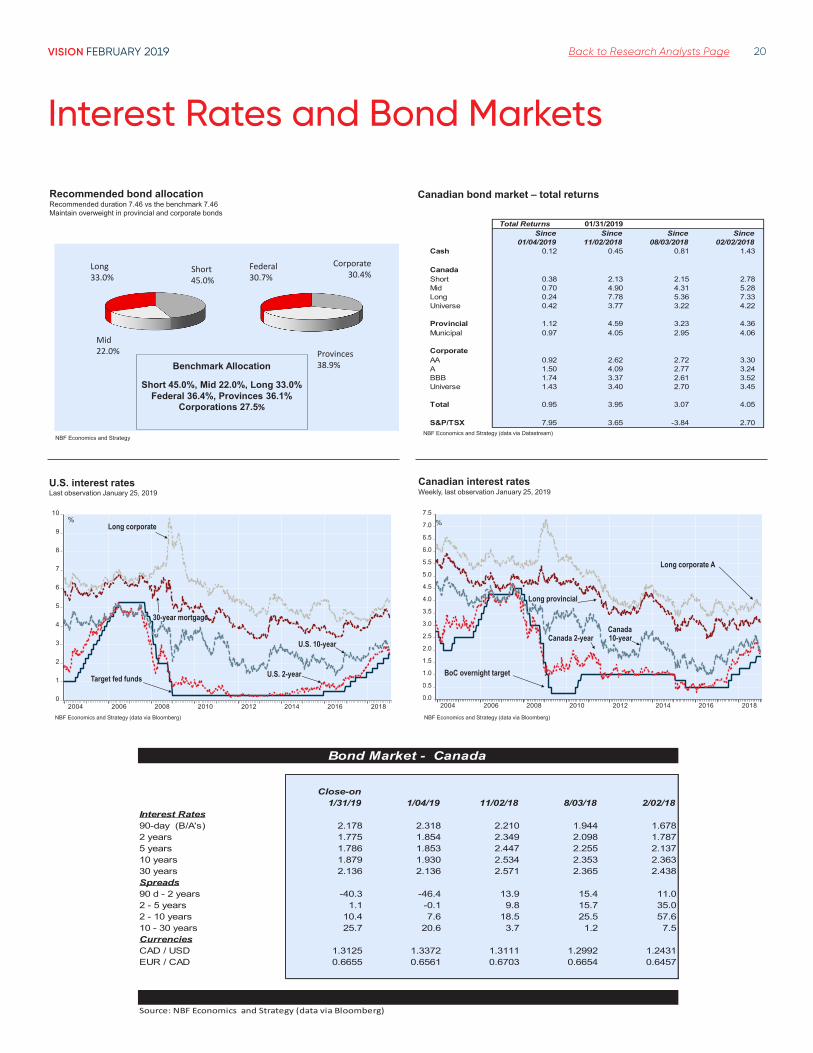

Long33.0%

Short45.0%

Mid22.0%

Federal30.7%

Corporate30.4%

Provinces38.9%Benchmark Allocation

Short 45.0%, Mid 22.0%, Long 33.0%Federal 36.4%, Provinces 36.1%

Corporations 27.5%

Recommended bond allocationRecommended duration 7.46 vs the benchmark 7.46 Maintain overweight in provincial and corporate bonds

NBF Economics and Strategy

0

1

2

3

4

5

6

7

8

9

10

2004 2006 2008 2010 2012 2014 2016 2018

U.S. interest ratesLast observation January 25, 2019

%Long corporate

U.S. 10-year

U.S. 2-yearTarget fed funds

30-year mortgage

NBF Economics and Strategy (data via Bloomberg)

Canadian bond market – total returns

NBF Economics and Strategy (data via Datastream)

Total Returns 01/31/2019 Since Since Since Since

01/04/2019 11/02/2018 08/03/2018 02/02/2018Cash 0.12 0.45 0.81 1.43

CanadaShort 0.38 2.13 2.15 2.78Mid 0.70 4.90 4.31 5.28Long 0.24 7.78 5.36 7.33Universe 0.42 3.77 3.22 4.22

Provincial 1.12 4.59 3.23 4.36Municipal 0.97 4.05 2.95 4.06

CorporateAA 0.92 2.62 2.72 3.30A 1.50 4.09 2.77 3.24BBB 1.74 3.37 2.61 3.52Universe 1.43 3.40 2.70 3.45

Total 0.95 3.95 3.07 4.05

S&P/TSX 7.95 3.65 -3.84 2.70

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

2004 2006 2008 2010 2012 2014 2016 2018

Canadian interest ratesWeekly, last observation January 25, 2019

%

Long corporate A

Long provincial

Canada10-yearCanada 2-year

BoC overnight target

NBF Economics and Strategy (data via Bloomberg)

Bond Market - Canada

Close-on1/31/19 1/04/19 11/02/18 8/03/18 2/02/18

Interest Rates90-day (B/A's) 2.178 2.318 2.210 1.944 1.6782 years 1.775 1.854 2.349 2.098 1.7875 years 1.786 1.853 2.447 2.255 2.13710 years 1.879 1.930 2.534 2.353 2.36330 years 2.136 2.136 2.571 2.365 2.438Spreads90 d - 2 years -40.3 -46.4 13.9 15.4 11.02 - 5 years 1.1 -0.1 9.8 15.7 35.02 - 10 years 10.4 7.6 18.5 25.5 57.610 - 30 years 25.7 20.6 3.7 1.2 7.5CurrenciesCAD / USD 1.3125 1.3372 1.3111 1.2992 1.2431EUR / CAD 0.6655 0.6561 0.6703 0.6654 0.6457

Source: NBF Economics and Strategy (data via Bloomberg)

VISION FEBRUARY 2019 Back to Research Analysts Page 21

Stock Market and Portfolio Strategy

VISION FEBRUARY 2019 Back to Research Analysts Page 22

Stock Market and Portfolio Strategy

Stéfane Marion Chief Economist and Strategist 514-879-3781

Matthieu Arseneau Deputy Chief Economist 514-879-2252

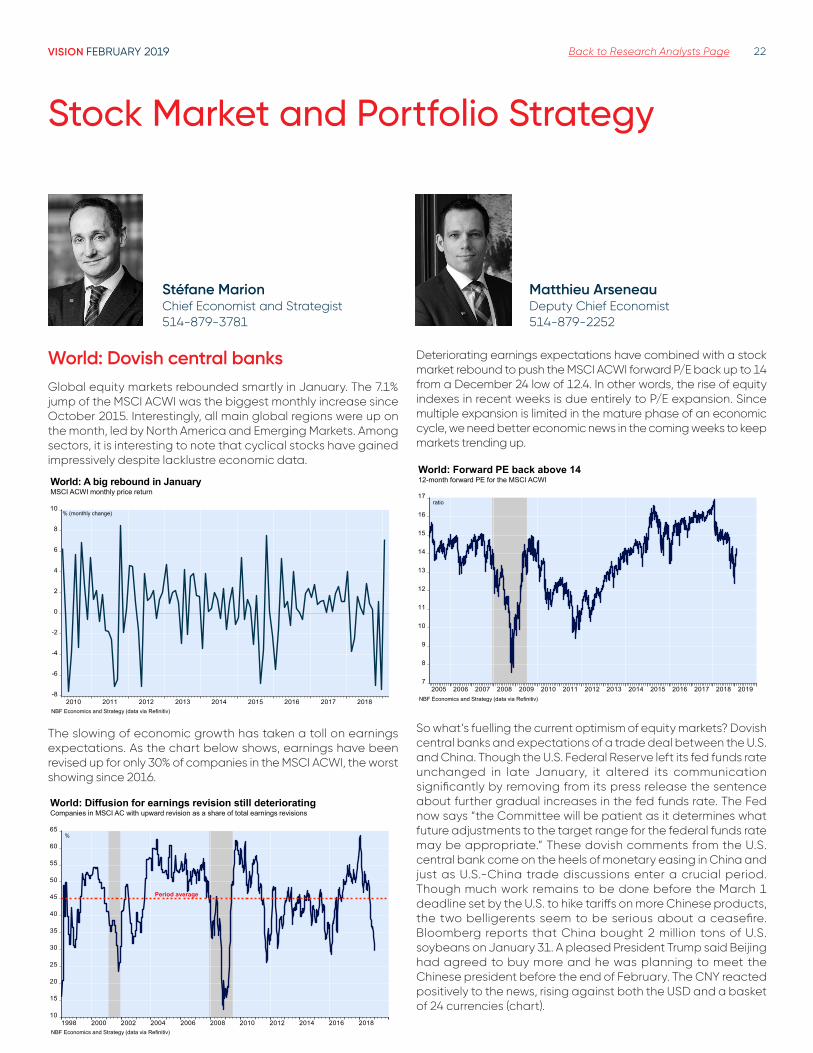

World: Dovish central banksGlobal equity markets rebounded smartly in January. The 7.1% jump of the MSCI ACWI was the biggest monthly increase since October 2015. Interestingly, all main global regions were up on the month, led by North America and Emerging Markets. Among sectors, it is interesting to note that cyclical stocks have gained impressively despite lacklustre economic data.

-8

-6

-4

-2

0

2

4

6

8

10

2010 2011 2012 2013 2014 2015 2016 2017 2018

World: A big rebound in JanuaryMSCI ACWI monthly price return

NBF Economics and Strategy (data via Refinitiv)

% (monthly change)

The slowing of economic growth has taken a toll on earnings expectations. As the chart below shows, earnings have been revised up for only 30% of companies in the MSCI ACWI, the worst showing since 2016.

10

15

20

25

30

35

40

45

50

55

60

65

1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

%

World: Diffusion for earnings revision still deterioratingCompanies in MSCI AC with upward revision as a share of total earnings revisions

NBF Economics and Strategy (data via Refinitiv)

Period average

Deteriorating earnings expectations have combined with a stock market rebound to push the MSCI ACWI forward P/E back up to 14 from a December 24 low of 12.4. In other words, the rise of equity indexes in recent weeks is due entirely to P/E expansion. Since multiple expansion is limited in the mature phase of an economic cycle, we need better economic news in the coming weeks to keep markets trending up.

7

8

9

10

11

12

13

14

15

16

17

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

ratio

World: Forward PE back above 1412-month forward PE for the MSCI ACWI

NBF Economics and Strategy (data via Refinitiv)

So what’s fuelling the current optimism of equity markets? Dovish central banks and expectations of a trade deal between the U.S. and China. Though the U.S. Federal Reserve left its fed funds rate unchanged in late January, it altered its communication significantly by removing from its press release the sentence about further gradual increases in the fed funds rate. The Fed now says “the Committee will be patient as it determines what future adjustments to the target range for the federal funds rate may be appropriate.” These dovish comments from the U.S. central bank come on the heels of monetary easing in China and just as U.S.-China trade discussions enter a crucial period. Though much work remains to be done before the March 1 deadline set by the U.S. to hike tariffs on more Chinese products, the two belligerents seem to be serious about a ceasefire. Bloomberg reports that China bought 2 million tons of U.S. soybeans on January 31. A pleased President Trump said Beijing had agreed to buy more and he was planning to meet the Chinese president before the end of February. The CNY reacted positively to the news, rising against both the USD and a basket of 24 currencies (chart).

VISION FEBRUARY 2019 Back to Research Analysts Page 23

Stock Market and Portfolio Strategy

88

90

92

94

96

98

100

102

104

106

2015 2016 2017 2018 2019

China: Currency is strengtheningTrade-weighted index of RMB vs. 24 currencies vs. the CNY/USD index

NBF Economics and Strategy (Federal Reserve data via Refinitiv)

Index (Dec. 2014 =100)

CFETS RMB index

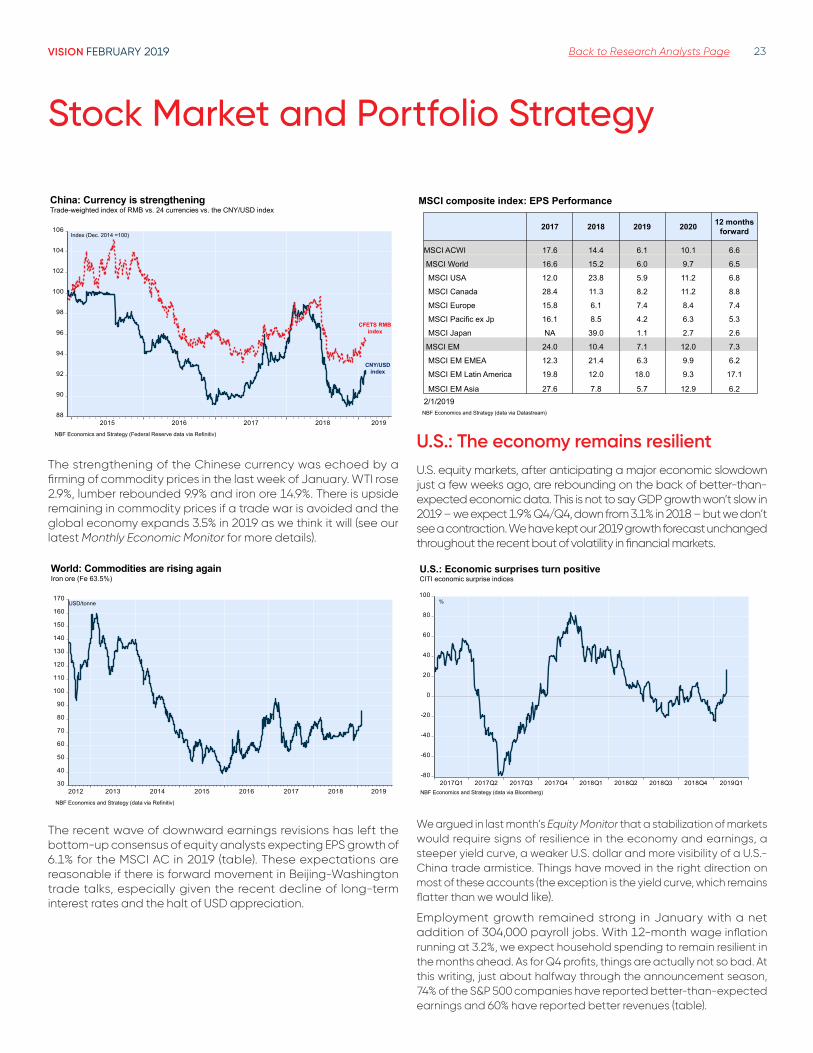

CNY/USDindex

The strengthening of the Chinese currency was echoed by a firming of commodity prices in the last week of January. WTI rose 2.9%, lumber rebounded 9.9% and iron ore 14.9%. There is upside remaining in commodity prices if a trade war is avoided and the global economy expands 3.5% in 2019 as we think it will (see our latest Monthly Economic Monitor for more details).

30

40

50

60

70

80

90

100

110

120

130

140

150

160

170

2012 2013 2014 2015 2016 2017 2018 2019

World: Commodities are rising againIron ore (Fe 63.5%)

NBF Economics and Strategy (data via Refinitiv)

USD/tonne

The recent wave of downward earnings revisions has left the bottom-up consensus of equity analysts expecting EPS growth of 6.1% for the MSCI AC in 2019 (table). These expectations are reasonable if there is forward movement in Beijing-Washington trade talks, especially given the recent decline of long-term interest rates and the halt of USD appreciation.

MSCI composite index: EPS Performance

NBF Economics and Strategy (data via Datastream)

2017 2018 2019 2020 12 months forward

MSCI ACWI 17.6 14.4 6.1 10.1 6.6

MSCI World 16.6 15.2 6.0 9.7 6.5

MSCI USA 12.0 23.8 5.9 11.2 6.8

MSCI Canada 28.4 11.3 8.2 11.2 8.8

MSCI Europe 15.8 6.1 7.4 8.4 7.4

MSCI Pacific ex Jp 16.1 8.5 4.2 6.3 5.3

MSCI Japan NA 39.0 1.1 2.7 2.6

MSCI EM 24.0 10.4 7.1 12.0 7.3

MSCI EM EMEA 12.3 21.4 6.3 9.9 6.2

MSCI EM Latin America 19.8 12.0 18.0 9.3 17.1

MSCI EM Asia 27.6 7.8 5.7 12.9 6.22/1/2019

U .S .: The economy remains resilientU.S. equity markets, after anticipating a major economic slowdown just a few weeks ago, are rebounding on the back of better-than-expected economic data. This is not to say GDP growth won’t slow in 2019 – we expect 1.9% Q4/Q4, down from 3.1% in 2018 – but we don’t see a contraction. We have kept our 2019 growth forecast unchanged throughout the recent bout of volatility in financial markets.

-80

-60

-40

-20

0

20

40

60

80

100

2017Q1 2017Q2 2017Q3 2017Q4 2018Q1 2018Q2 2018Q3 2018Q4 2019Q1

%

U.S.: Economic surprises turn positiveCITI economic surprise indices

NBF Economics and Strategy (data via Bloomberg)

We argued in last month’s Equity Monitor that a stabilization of markets would require signs of resilience in the economy and earnings, a steeper yield curve, a weaker U.S. dollar and more visibility of a U.S.-China trade armistice. Things have moved in the right direction on most of these accounts (the exception is the yield curve, which remains flatter than we would like).

Employment growth remained strong in January with a net addition of 304,000 payroll jobs. With 12-month wage inflation running at 3.2%, we expect household spending to remain resilient in the months ahead. As for Q4 profits, things are actually not so bad. At this writing, just about halfway through the announcement season, 74% of the S&P 500 companies have reported better-than-expected earnings and 60% have reported better revenues (table).

VISION FEBRUARY 2019 Back to Research Analysts Page 24

Industry (ICB) Positive Inline Negative % Positive Inline Negative %All Securities 235 / 500 140 0 95 0.57% 172 4 57 2.84%> Oil & Gas 10 / 30 7 0 3 1.23% 7 0 2 22.62%> Basic Materials 10 / 17 1 0 9 -3.04% 5 0 5 -3.05%> Industrials 53 / 88 37 0 16 1.58% 48 0 5 3.28%> Consumer Goods 22 / 59 11 0 11 -1.66% 13 1 7 3.23%> Health Care 26 / 52 20 0 6 0.82% 21 0 5 2.43%> Consumer Services 24 / 67 16 0 8 1.29% 21 0 3 5.60%> Telecommunications 2 / 3 0 0 2 -0.79% 1 1 0 1.23%> Utilities 5 / 27 3 0 2 -3.66% 2 0 3 -0.65%> Financials 59 / 103 32 0 27 -0.36% 34 2 23 -0.56%> Technology 23 / 52 12 0 11 0.24% 19 0 4 2.51%

Sales Surprise Earnings SurpriseReported

U.S.: Q4 2018 earnings seasonS&P 500 earnings season

Bloomberg (as of February 1, 2019)

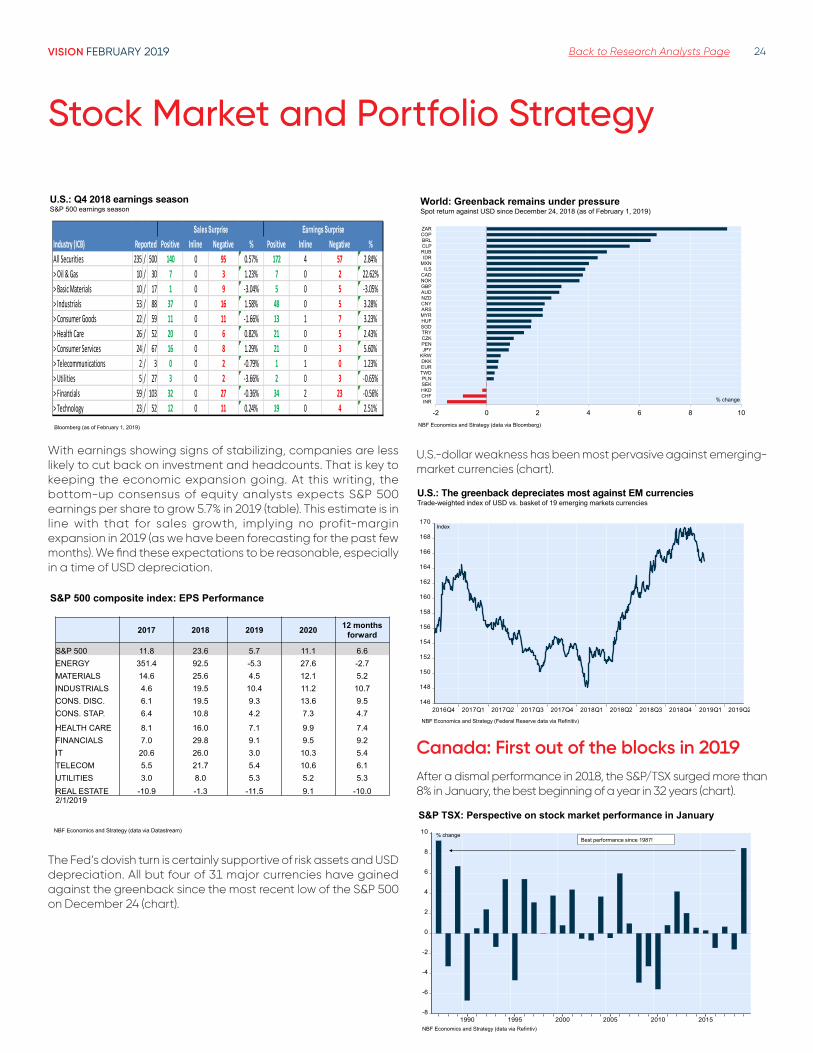

With earnings showing signs of stabilizing, companies are less likely to cut back on investment and headcounts. That is key to keeping the economic expansion going. At this writing, the bottom-up consensus of equity analysts expects S&P 500 earnings per share to grow 5.7% in 2019 (table). This estimate is in line with that for sales growth, implying no profit-margin expansion in 2019 (as we have been forecasting for the past few months). We find these expectations to be reasonable, especially in a time of USD depreciation.

S&P 500 composite index: EPS Performance

NBF Economics and Strategy (data via Datastream)

2017 2018 2019 2020 12 months forward

S&P 500 11.8 23.6 5.7 11.1 6.6ENERGY 351.4 92.5 -5.3 27.6 -2.7MATERIALS 14.6 25.6 4.5 12.1 5.2INDUSTRIALS 4.6 19.5 10.4 11.2 10.7CONS. DISC. 6.1 19.5 9.3 13.6 9.5CONS. STAP. 6.4 10.8 4.2 7.3 4.7

HEALTH CARE 8.1 16.0 7.1 9.9 7.4FINANCIALS 7.0 29.8 9.1 9.5 9.2IT 20.6 26.0 3.0 10.3 5.4TELECOM 5.5 21.7 5.4 10.6 6.1UTILITIES 3.0 8.0 5.3 5.2 5.3REAL ESTATE -10.9 -1.3 -11.5 9.1 -10.02/1/2019

The Fed’s dovish turn is certainly supportive of risk assets and USD depreciation. All but four of 31 major currencies have gained against the greenback since the most recent low of the S&P 500 on December 24 (chart).

-2 0 2 4 6 8 10INR

CHFHKDSEKPLN

TWDEURDKK

KRWJPYPENCZKTRYSGDHUFMYRARSCNYNZDAUDGBPNOKCAD

ILSMXNIDR

RUBCLPBRLCOPZAR

World: Greenback remains under pressureSpot return against USD since December 24, 2018 (as of February 1, 2019)

NBF Economics and Strategy (data via Bloomberg)

% change

U.S.-dollar weakness has been most pervasive against emerging-market currencies (chart).

146

148

150

152

154

156

158

160

162

164

166

168

170

2016Q4 2017Q1 2017Q2 2017Q3 2017Q4 2018Q1 2018Q2 2018Q3 2018Q4 2019Q1 2019Q2

U.S.: The greenback depreciates most against EM currenciesTrade-weighted index of USD vs. basket of 19 emerging markets currencies

NBF Economics and Strategy (Federal Reserve data via Refinitiv)

Index

Canada: First out of the blocks in 2019After a dismal performance in 2018, the S&P/TSX surged more than 8% in January, the best beginning of a year in 32 years (chart).

-8

-6

-4

-2

0

2

4

6

8

10

1990 1995 2000 2005 2010 2015

S&P TSX: Perspective on stock market performance in January

% change

NBF Economics and Strategy (data via Refintiv)

Best performance since 1987!

Stock Market and Portfolio Strategy

VISION FEBRUARY 2019 Back to Research Analysts Page 25

Stock Market and Portfolio Strategy

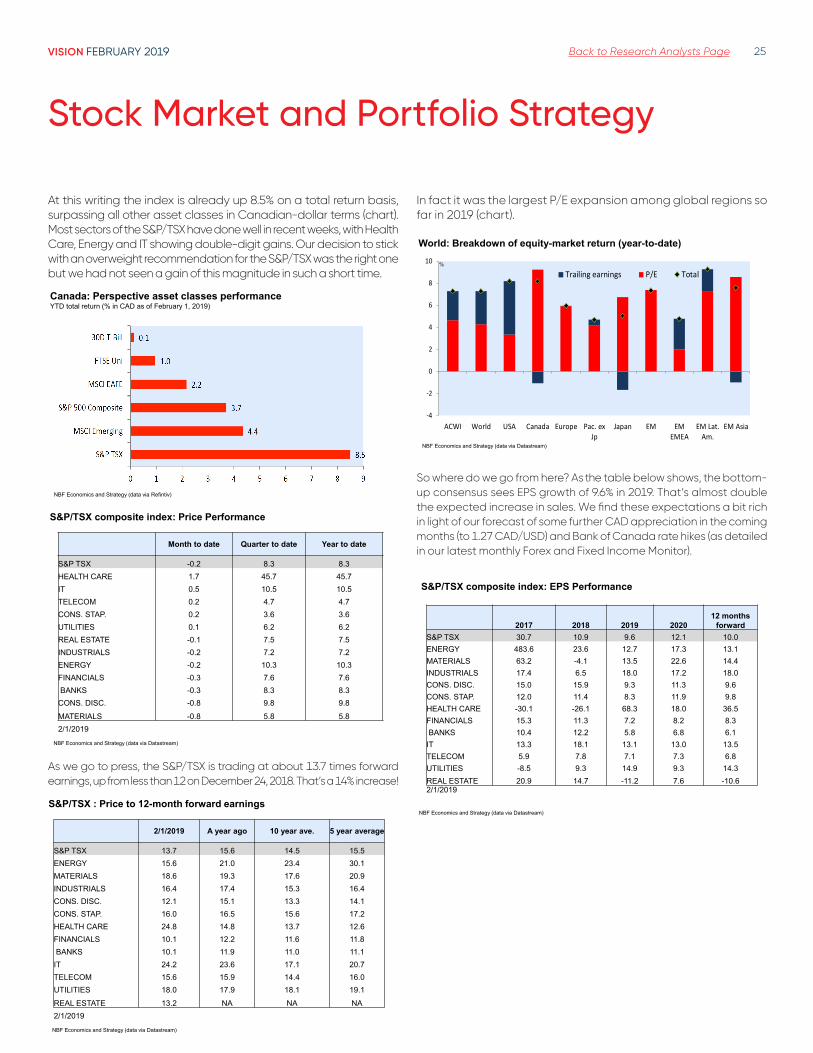

At this writing the index is already up 8.5% on a total return basis, surpassing all other asset classes in Canadian-dollar terms (chart). Most sectors of the S&P/TSX have done well in recent weeks, with Health Care, Energy and IT showing double-digit gains. Our decision to stick with an overweight recommendation for the S&P/TSX was the right one but we had not seen a gain of this magnitude in such a short time.

Canada: Perspective asset classes performanceYTD total return (% in CAD as of February 1, 2019)

NBF Economics and Strategy (data via Refintiv)

S&P/TSX composite index: Price Performance

NBF Economics and Strategy (data via Datastream)

Month to date Quarter to date Year to date

S&P TSX -0.2 8.3 8.3HEALTH CARE 1.7 45.7 45.7IT 0.5 10.5 10.5TELECOM 0.2 4.7 4.7CONS. STAP. 0.2 3.6 3.6UTILITIES 0.1 6.2 6.2REAL ESTATE -0.1 7.5 7.5INDUSTRIALS -0.2 7.2 7.2ENERGY -0.2 10.3 10.3FINANCIALS -0.3 7.6 7.6BANKS -0.3 8.3 8.3

CONS. DISC. -0.8 9.8 9.8MATERIALS -0.8 5.8 5.82/1/2019

As we go to press, the S&P/TSX is trading at about 13.7 times forward earnings, up from less than 12 on December 24, 2018. That’s a 14% increase!

S&P/TSX : Price to 12-month forward earnings

NBF Economics and Strategy (data via Datastream)

2/1/2019 A year ago 10 year ave. 5 year average

S&P TSX 13.7 15.6 14.5 15.5ENERGY 15.6 21.0 23.4 30.1MATERIALS 18.6 19.3 17.6 20.9INDUSTRIALS 16.4 17.4 15.3 16.4CONS. DISC. 12.1 15.1 13.3 14.1CONS. STAP. 16.0 16.5 15.6 17.2HEALTH CARE 24.8 14.8 13.7 12.6FINANCIALS 10.1 12.2 11.6 11.8BANKS 10.1 11.9 11.0 11.1

IT 24.2 23.6 17.1 20.7TELECOM 15.6 15.9 14.4 16.0UTILITIES 18.0 17.9 18.1 19.1REAL ESTATE 13.2 NA NA NA2/1/2019

In fact it was the largest P/E expansion among global regions so far in 2019 (chart).

%

-4

-2

0

2

4

6

8

10

ACWI World USA Canada Europe Pac. exJp

Japan EM EMEMEA

EM Lat.Am.

EM Asia

Trailing earnings P/E Total

World: Breakdown of equity-market return (year-to-date)

NBF Economics and Strategy (data via Datastream)

%

So where do we go from here? As the table below shows, the bottom-up consensus sees EPS growth of 9.6% in 2019. That’s almost double the expected increase in sales. We find these expectations a bit rich in light of our forecast of some further CAD appreciation in the coming months (to 1.27 CAD/USD) and Bank of Canada rate hikes (as detailed in our latest monthly Forex and Fixed Income Monitor).

S&P/TSX composite index: EPS Performance

NBF Economics and Strategy (data via Datastream)

2017 2018 2019 202012 months

forwardS&P TSX 30.7 10.9 9.6 12.1 10.0ENERGY 483.6 23.6 12.7 17.3 13.1MATERIALS 63.2 -4.1 13.5 22.6 14.4INDUSTRIALS 17.4 6.5 18.0 17.2 18.0CONS. DISC. 15.0 15.9 9.3 11.3 9.6CONS. STAP. 12.0 11.4 8.3 11.9 9.8HEALTH CARE -30.1 -26.1 68.3 18.0 36.5FINANCIALS 15.3 11.3 7.2 8.2 8.3BANKS 10.4 12.2 5.8 6.8 6.1

IT 13.3 18.1 13.1 13.0 13.5TELECOM 5.9 7.8 7.1 7.3 6.8UTILITIES -8.5 9.3 14.9 9.3 14.3REAL ESTATE 20.9 14.7 -11.2 7.6 -10.62/1/2019

VISION FEBRUARY 2019 Back to Research Analysts Page 26

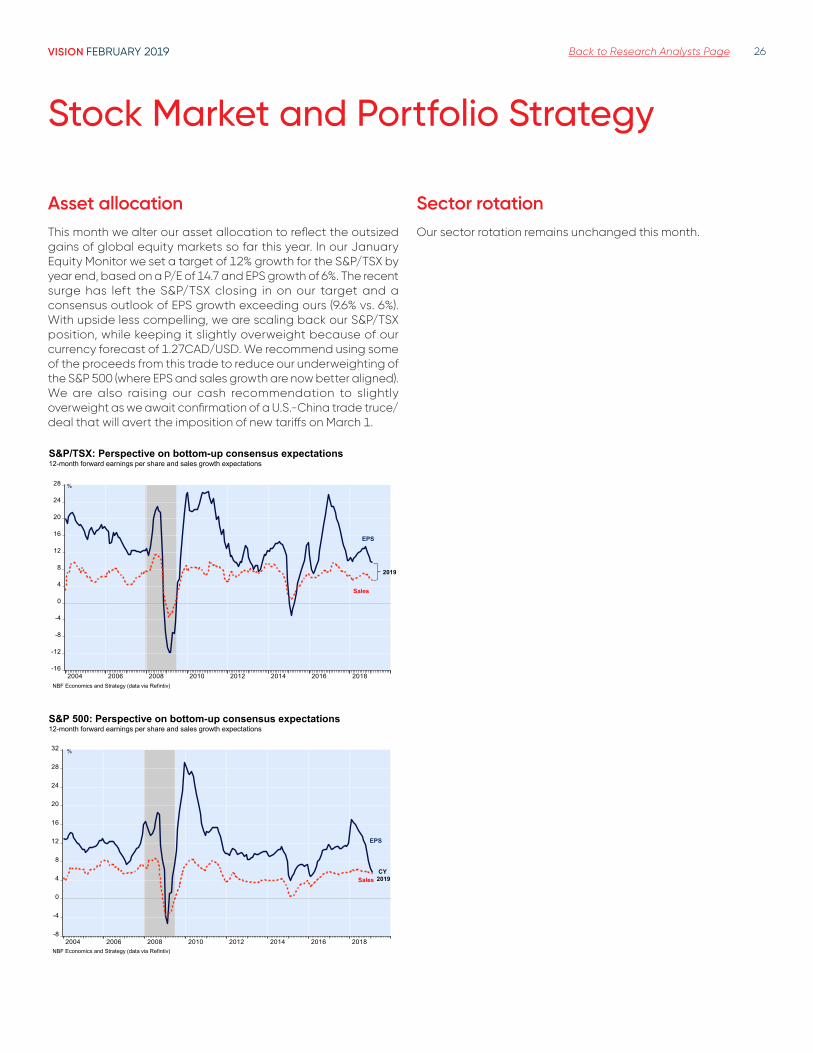

Asset allocationThis month we alter our asset allocation to reflect the outsized gains of global equity markets so far this year. In our January Equity Monitor we set a target of 12% growth for the S&P/TSX by year end, based on a P/E of 14.7 and EPS growth of 6%. The recent surge has left the S&P/TSX closing in on our target and a consensus outlook of EPS growth exceeding ours (9.6% vs. 6%). With upside less compelling, we are scaling back our S&P/TSX position, while keeping it slightly overweight because of our currency forecast of 1.27CAD/USD. We recommend using some of the proceeds from this trade to reduce our underweighting of the S&P 500 (where EPS and sales growth are now better aligned). We are also raising our cash recommendation to slightly overweight as we await confirmation of a U.S.-China trade truce/deal that will avert the imposition of new tariffs on March 1.

-16

-12

-8

-4

0

4

8

12

16

20

24

28

2004 2006 2008 2010 2012 2014 2016 2018

S&P/TSX: Perspective on bottom-up consensus expectations12-month forward earnings per share and sales growth expectations

%

NBF Economics and Strategy (data via Refintiv)

Sales

EPS

2019

-8

-4

0

4

8

12

16

20

24

28

32

2004 2006 2008 2010 2012 2014 2016 2018

S&P 500: Perspective on bottom-up consensus expectations12-month forward earnings per share and sales growth expectations

%

NBF Economics and Strategy (data via Refintiv)

Sales

EPS

CY2019

Sector rotationOur sector rotation remains unchanged this month.

Stock Market and Portfolio Strategy

VISION FEBRUARY 2019 Back to Research Analysts Page 27

Stock Market and Portfolio Strategy

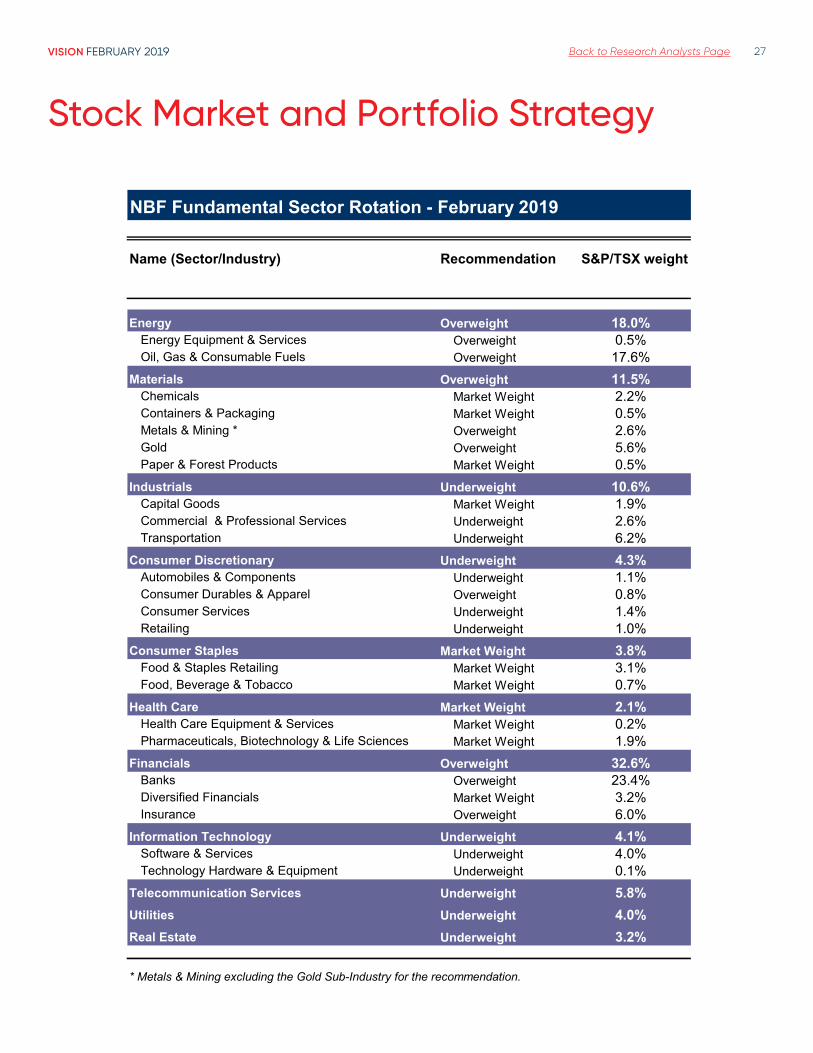

NBF Fundamental Sector Rotation - February 2019

Name (Sector/Industry) Recommendation S&P/TSX weight

Energy Overweight 18.0%Energy Equipment & Services Overweight 0.5%Oil, Gas & Consumable Fuels Overweight 17.6%

Materials Overweight 11.5%Chemicals Market Weight 2.2%Containers & Packaging Market Weight 0.5%Metals & Mining * Overweight 2.6%Gold Overweight 5.6%Paper & Forest Products Market Weight 0.5%

Industrials Underweight 10.6%Capital Goods Market Weight 1.9%Commercial & Professional Services Underweight 2.6%Transportation Underweight 6.2%

Consumer Discretionary Underweight 4.3%Automobiles & Components Underweight 1.1%Consumer Durables & Apparel Overweight 0.8%Consumer Services Underweight 1.4%Retailing Underweight 1.0%

Consumer Staples Market Weight 3.8%Food & Staples Retailing Market Weight 3.1%Food, Beverage & Tobacco Market Weight 0.7%

Health Care Market Weight 2.1%Health Care Equipment & Services Market Weight 0.2%Pharmaceuticals, Biotechnology & Life Sciences Market Weight 1.9%

Financials Overweight 32.6%Banks Overweight 23.4%Diversified Financials Market Weight 3.2%Insurance Overweight 6.0%

Information Technology Underweight 4.1%Software & Services Underweight 4.0%Technology Hardware & Equipment Underweight 0.1%

Telecommunication Services Underweight 5.8%Utilities Underweight 4.0%Real Estate Underweight 3.2%

* Metals & Mining excluding the Gold Sub-Industry for the recommendation.

VISION FEBRUARY 2019 Back to Research Analysts Page 28

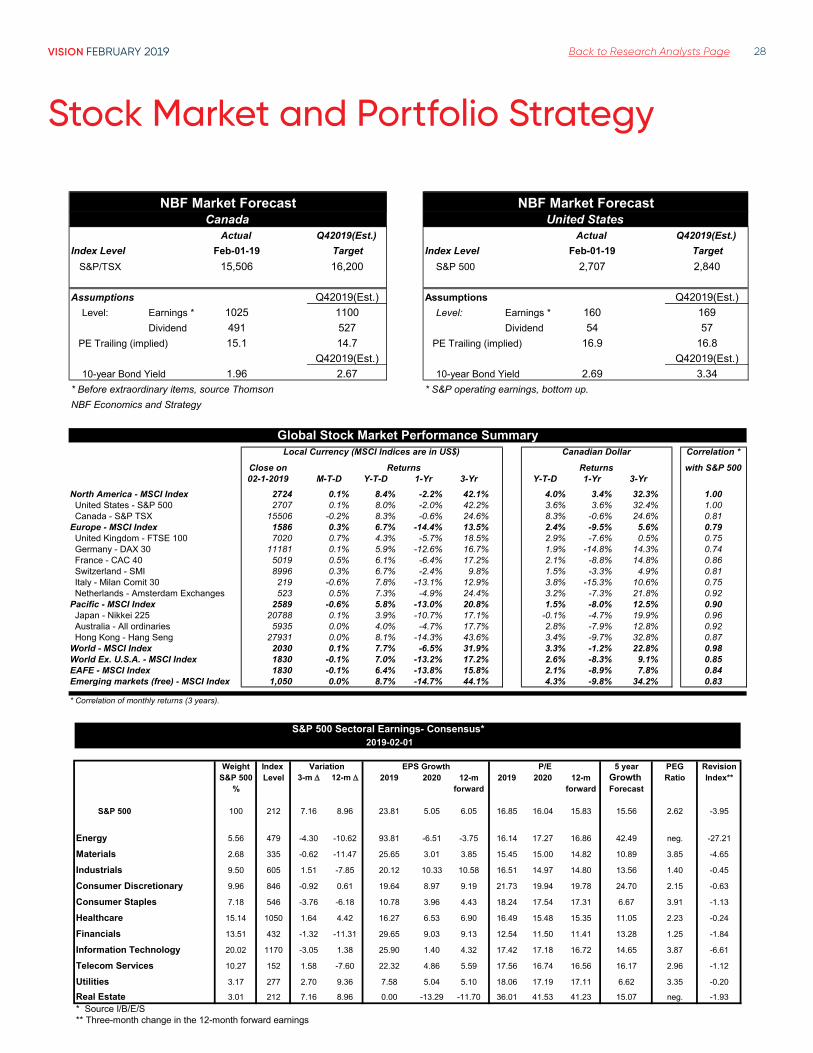

Actual Q42019(Est.) Actual Q42019(Est.)Index Level Feb-01-19 Target Index Level Feb-01-19 Target S&P/TSX 15,506 16,200 S&P 500 2,707 2,840

Assumptions Q42019(Est.) Assumptions Q42019(Est.) Level: Earnings * 1025 1100 Level: Earnings * 160 169

Dividend 491 527 Dividend 54 57PE Trailing (implied) 15.1 14.7 PE Trailing (implied) 16.9 16.8

Q42019(Est.) Q42019(Est.) 10-year Bond Yield 1.96 2.67 10-year Bond Yield 2.69 3.34* Before extraordinary items, source Thomson * S&P operating earnings, bottom up.NBF Economics and Strategy

NBF Market Forecast NBF Market ForecastCanada United States

Stock Market and Portfolio Strategy

Local Currency (MSCI Indices are in US$) Canadian Dollar Correlation *

Close on with S&P 50002-1-2019 M-T-D Y-T-D 1-Yr 3-Yr Y-T-D 1-Yr 3-Yr