Embed Size (px)

Citation preview

CONCEPT NOTE

Virtual Knowledge-sharing Platform for Insurance Regulators and Supervisors

Gaby Ramm, 14th October 2013

Commissioned by the GIZ RFPI Asia

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 2

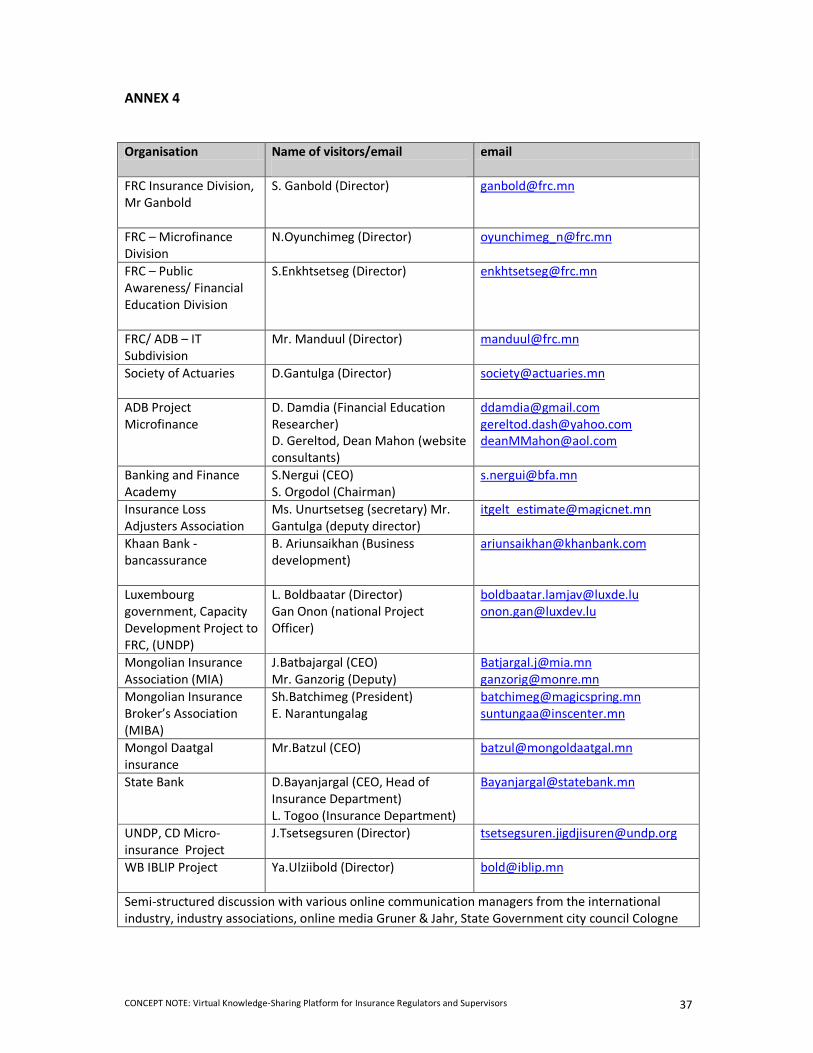

Table of Contents List of Abbreviations 3 List of Boxes 3 List of Tables 3 1. Introduction 4 1.1 Background 4 1.2 Methodology 5 2. Knowledge-sharing themes 6 2.1 Introduction to inclusive insurance 6 2.2 Product development 7 2.3 Distribution channels 8 2.4 Microinsurance business operation 11 2.5 Consumer Protection 11 2.6 Insurance regulation and legislation 11 3. Other capacity development issues 13 4. Considerations for designing the KSP 14 4.1 Expectations and objectives 14 4.2 Current user behaviour – scope for using the KSP 14 4.3 ‘Knowledge Management’ approach 15 4.3.1 Actions for promoting an effective use of the KSP 16 4.3.2 Strategic management considerations 17 4.4 KSP tools for knowledge generating, sharing and learning 18 5. Recommendations 20 5.1 KSP design 20 5.2 KSP development – initial steps 21 5.3 KSP content and tools 21 5.4 KSP management structure 23 5.5 Monitoring and Evaluation of the KSP 25 Bibliography 27 ANNEXES Annex 1: Results of the TNA questionnaire 28 Annex 2: Assessment of FRC Content Needs for Knowledge-Sharing – Questionnaire 30 Annex 3: Questions pertaining to virtual KSP methods: FRC and GIZ 36 Annex 4: List of resource persons and respondents 37

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 3

List of Abbreviations ADB Asian Development Bank CUMIC Central Union of Mongolian Industrial Cooperatives CUMCC Central Union of Mongolian Consumers Cooperatives RFPI Asia Regulatory Framework Promotion of Pro-poor Insurance Markets in Asia FRC Financial Regulatory Commission GIZ Deutsche Gesellschaft fuer Internationale Zusammenarbeit GmbH KSP Knowledge-Sharing Platform MCTIC Mongolian Cooperative Training and Information Center MIA Mongolian Insurers Association MOCCU National Confederation of Savings and Credit Cooperatives MoF Ministry of Finance MNCA Mongolian National Cooperative Association MSMEs Micro, Small and Medium Enterprises NAMAC National Association of Mongolian Agricultural Cooperatives SCCs Savings and Credit Cooperatives SDC Swiss Development Corporation SME Small and Medium Enterprises TNA Training Needs Assessment UMPSC Union of Mongolian Production and Service Cooperatives UNDP United Nations Development Programme List of Boxes Box 1: Examples of interlinking capacity development of traditional and inclusive insurance 4 Box 2. Key aspects of building an effective loss-adjustment system 8 Box 3: Potential role of Universities in capacity development 13 Box 4. Dealing with different languages 15 Box 5: Setting of online facilitation 18 Box 6: Potential online tools for other countries or set up at a later stage 20 Box 7: KPS management structure 23 List of Tables Table 1: Proposed KSP design 20 Table 2: Summary of contents and KSP features 22 Table 3: Example of performance indicators 26

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 4

1. Introduction 1.1 Background The Financial Regulatory Commission (FRC) was established in 2006 consisting of eight sub departments1, one being the FRC Insurance Division with its three sub-divisions: I) Policy planning; II) non-life insurance; and III) life insurance & motor third party liability insurance, licensing intermediaries & loss adjusters. The FRC acts according to the Law on Insurance (2004) which regulates all insurance activities except those defined by other laws (e.g. the Civil Code or Law on Insurance Intermediaries). The Insurance Law includes provisions for definitions of insurance classes and forms, rights and duties of the insurer and insured, regulation and licensing of insurance companies (incl. approving and supervising insurers business plans), capitalisation and solvency, accounting and auditing, roles and responsibilities of actuaries, regulation and licensing of reinsurance, and the right of the FRC to collect data and impose sanctions (Country Diagnosis, 2011). Many of these details are very general, and although specifications contain a part of insurance regulations and guidelines key insurance stakeholders stated a strong need for further clarification (see following sections). Accordingly, the FRC Insurance Division is responsible for the following tasks (selection according to their relevance for inclusive insurance): x Encouraging market development and stability, x Classification of products and premium calculations, x Granting and revoking licences, x Organising insurance training, x Defining code of conduct for insurance intermediaries. Since the private insurance business is relatively new in Mongolia the FRC requested capacity development in selected areas of traditional insurance. Furthermore, inclusive insurance is unknown to the market and requires additional knowledge and skills (see also TNA assessment Annex 1). As knowledge in traditional insurance is a prerequisite for inclusive insurance both need to be supported but for most issues both areas can be interlinked (see Box 1). Box 1: Examples of interlinking capacity development of traditional and inclusive insurance

x Rules for ‘entities’ that act as insurers: If FRC further defines rules for (commercial) insurance providers in traditional insurance business, they could discuss standards and rules for non-insurance institutions that intend to offer in inclusive insurance, if agreeable. Such small organisations may operate mixed businesses but should transfer the insurance operation into a separate entity.

x Product development: Since FRC classifies products and premium calculations and intends to obtain data of traditional insurance products, they can use this basis for defining products for the low-income market under the inclusive insurance concept. Actuarial training for traditional product can be complemented by actuarial pricing for low-income market products.

Knowledge-sharing objectives for FRC: In line with these tasks, the information to be provided to the FRC Insurance Division will have to address two main objectives: x To inform and orient the staff about inclusive insurance thereby enhancing their appreciation

and enabling their “buy in” of its concepts and principles 1 FRC sub departments: Administration, Securities Market Development, Insurance Market Division, Microfinance Department, Financial reporting & quality control, Legal Division, International Cooperation, Information Technology Division.

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 5

x To educate the staff on the technical how-to’s of regulating and supervising inclusive insurance operations

1.2 Methodology As the GIZ RFPI Asia program focuses on regulators and supervisors, the relevant information and capacity building activities were identified on the basis of the FRC needs. However, to assure an effective and efficient functioning of the inclusive insurance market, knowledge gaps of the relevant industry stakeholders were considered to such an extent as they are relevant for FRC’s functions. In order to obtain information on the needs and priorities of information pertaining to inclusive insurance five types of sources were used as reference for this concept: x A training needs assessment (TNA) questionnaire was filled by 10 of the 13 members of the FRC

Insurance Division (see Annexes 1 and 2) x The comprehensive TNA for all the FRC divisions carried out by the capacity building project of

the Government of Luxembourg was reviewed and the (few) suggestions for the Insurance Division were integrated

x Discussion with all relevant categories of stakeholders for receiving an overview of the knowledge on inclusive insurance, incl. policy, products, services, experiences, and challenges

x Final feedback discussion with the Director of the FRC Insurance Division The following section briefly describes the situation of inclusive insurance around specific issues, setting the stage for the suggested content/information to be provided to the FRC via the virtual Knowledge Sharing Platform (KSP).

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 6

2. Knowledge-sharing themes 2.1 Introduction to inclusive insurance Inclusive insurance is an almost unknown concept in Mongolia and prone to different perceptions ranging from insurance for middle income people to microinsurance for the poor. As UNDP (health microinsurance) and the World Bank-supported index-based livestock project (IBLIP) are the only two products for neglected populations and the poor, inclusive insurance is closely connected with these approaches. Experience with ‘pilot projects’ reveal that the development of microinsurance often started under ‘exceptional conditions’ with the intention to explore the scope of the new approach for later implementation under ‘real’ circumstances – as a viable business model in collaboration with the insurance industry. This approach was followed by UNDP and set the notion of the requirement of heavy donor support. Now, in the current project phase, emphasis will be shifted to more sustainable practices. As the concept of inclusive insurance is not yet introduced in Mongolia, other ministries, especially the Ministry of Health and the Ministry of Human Development and Social Welfare, are rather critical about additional health microinsurance products as it may contradict their intention of making the social insurance system mandatory for all citizens. They perceive private (health) insurance for the low income market as a competing system to the current (subsidized) health insurance and other social welfare benefits. Hence, information dissemination should preferably include other relevant ministries (and actors) in order to support a consistent policy. With the intention to discuss issues that cut across jurisdictions of various government agencies, the FRC Insurance Division is intending to initiate a ‘joint working group’ consisting of, for instance, the Ministry of Finance (MoF) and the Central Bank. Still prevailing from the communist system is both a distrust of insurance, and a sense of entitlement to government support and social welfare. The FRC director mentioned peoples’ confusion that “insurance is a tax” to be paid without receiving any benefit and the cultural taboo of talking about ‘bad events’. Both aspects make it difficult to promote insurance and require strong effort in awareness building. The UNDP microinsurance project uses their Community Centres in their project regions (with the assistance of UN volunteers). The FRC-ADB microfinance project emphasises on virtual means through a financial education website (see details under 4.4). Relevant information in the context mentioned above: x Clarification of the concept of ‘inclusive insurance’ and its implication on product definition for

the low-income market2 x Sustainable insurance business models for the low-income market x Role of (micro)insurance and inclusive insurance for social protection, the inclusive finance policy

of the Ministry of Finance (MoF) and integrated risk management. As insurance is most successful when embedded into broader risk management measures an integrated approach covering the main risks of low-income persons will avoid further strain on the fiscal budget and the people. Herders are apparently extremely vulnerable to weather-related shocks, so is the related agriculture sector, the fodder growers, but also cereal and potato production will be increasingly affected by climate change. Insurance has to be combined with preventive activities incl. storage facilities. In urban areas fire of gers and productive assets are recorded and may be

2 Currently the term ‚microinsurance’ or low-income product is not defined. The FRC Director indicated a premium amount of MNT 50.000 premium/annum. The Country Diagnostic draft report (2011) refers to “internally the FRC considers policies with annual premium less than MNT 10,000 (USD 8) as microinsurance policies”.

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 7

combined with innovative heating facilities and energy saving technology for dwellers and Micro, Small and Medium Enterprises (MSMEs).

2.2 Product development Many stakeholders are not familiar with products for the low-income market and tend to perceive such products as downsized traditional products – which is not surprising as only two products were explored (UNDP health microinsurance and the World Bank supported livestock index product). All actors including the State Bank complained about the lack of innovative products (too many credit-linked insurance policies apart from compulsory driver’s liability auto insurance). The first Life (and only one) Insurance company was established in 2008 and life products are still in an ‘infancy stage’. Other non-life products cater to corporate clients with the retail market starting to sell both non-life and life insurance to the higher income segment. Recognising that there is little publicly available data for product design and pricing, the FRC intends to apply a new policy where products should be submitted to FRC either for approval or for information. With a similar intention UNDP started collecting data on existing insurance products and the Insurance Loss Adjustors Association initiated a product data base on auto insurance with seven commercial insurance providers. In such situations, all stakeholders were concerned about the low actuarial capacity for developing appropriate inclusive insurance products both within FRC and the insurance industry. Actuaries of non-life insurance providers were issued a license from FRC which does not comply with international standards. Only a few actuaries of the Society of Actuaries of Mongolia (2008) have international degrees – mostly from the UK. The insurance industry educates loss adjusters which are reported to partly overlap with the training for agents. To supplement the short programs of the Insurance Loss Adjustors Association (2012), with 10 licensed members, plans to organise additional training courses dealing with complicated products. The demand for training and further refinement of regulatory issues is high (see also Box 2 below). Relevant information in the context mentioned above: x Difference between traditional products and those for the low-income market, incl. demand-

based product design. x Group policies are an unknown concept in Mongolia and evoked interest within the insurance

industry, in particular among brokers. Comparable with the cooperatives, other organisations such as employers, workers’ organisations in the mining industry, or neighbourhood associations, may act as intermediaries for either selling or promoting the concept of group insurance. While group insurance would require an agreement with the FRC, the example of the Ard Insurance is an interesting proposition to work within the current jurisdiction and suffices the underlying idea of group insurance: The insurer offers apartment damage and liability coverage that is sold through apartment associations. As the association manages the billing for utilities to all of the apartments in the complex, they could add the insurance premium to the utility bill. Once the apartment association opts for insurance, coverage is mandatory for all apartment owners. For selling the product, the association had to be licensed as an insurance agent (Country Diagnostic, 2011).

x Information on the following product types which would enable the FRC to compare available products in Mongolia, assess their client value, and provide indication for innovative product development (with an emphasis on inclusive insurance policy)

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 8

o Life insurance: credit life, life & savings, accident & disability, remittances linked insurance (as the development of life insurance is new the interest is high)

o Insurance against catastrophic weather-related risks: index agriculture insurance and livestock, incl. the challenges offering indemnity-based products for low-income persons or households

o Property insurance for micro enterprises (and others such as people living in gers) o Health product issues: Product design for hospitalisation and out-of-pocket expenses (if

offered, such products need to be conceptualised in the context of the existing (partially subsidized health insurance)

o Information on product ‘packages’ (which are currently not permitted) x Materials needed for future training for actuaries within the FRC, in general but for inclusive

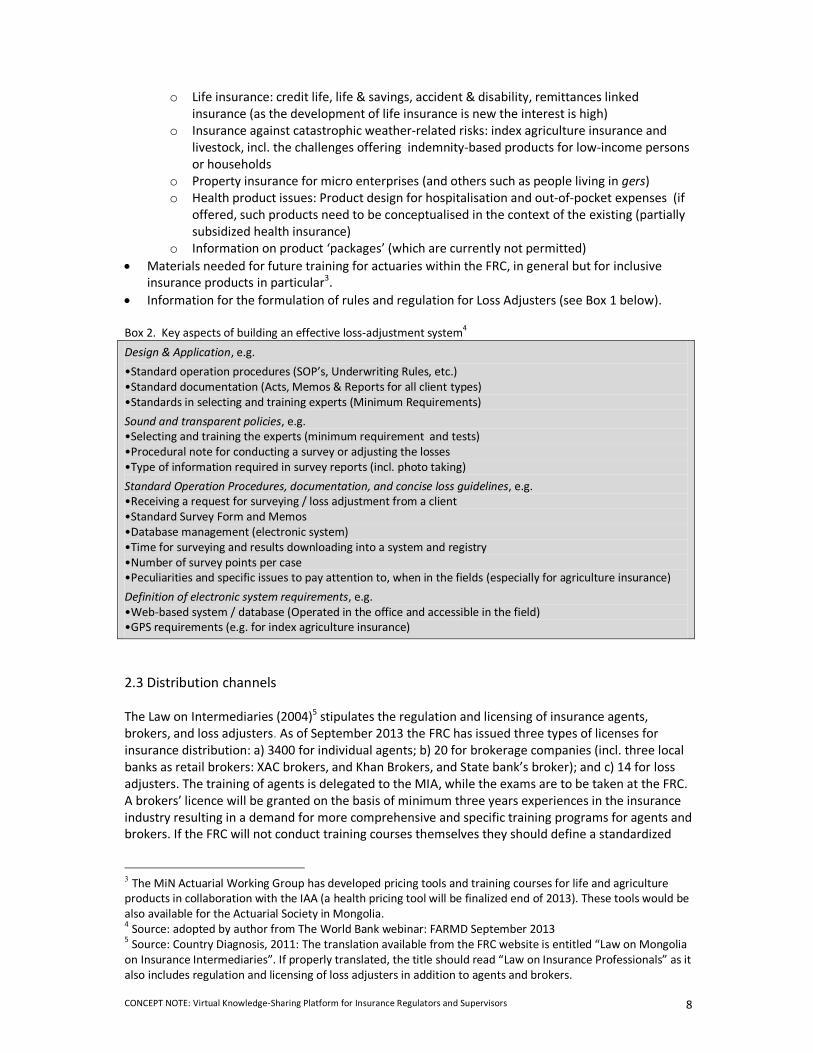

insurance products in particular3. x Information for the formulation of rules and regulation for Loss Adjusters (see Box 1 below). Box 2. Key aspects of building an effective loss-adjustment system4 Design & Application, e.g. •Standard operation procedures (SOP’s, Underwriting Rules, etc.) •Standard documentation (Acts, Memos & Reports for all client types) •Standards in selecting and training experts (Minimum Requirements) Sound and transparent policies, e.g. •Selecting and training the experts (minimum requirement and tests) •Procedural note for conducting a survey or adjusting the losses •Type of information required in survey reports (incl. photo taking) Standard Operation Procedures, documentation, and concise loss guidelines, e.g. •Receiving a request for surveying / loss adjustment from a client •Standard Survey Form and Memos •Database management (electronic system) •Time for surveying and results downloading into a system and registry •Number of survey points per case •Peculiarities and specific issues to pay attention to, when in the fields (especially for agriculture insurance) Definition of electronic system requirements, e.g. •Web-based system / database (Operated in the office and accessible in the field) •GPS requirements (e.g. for index agriculture insurance)

2.3 Distribution channels The Law on Intermediaries (2004)5 stipulates the regulation and licensing of insurance agents, brokers, and loss adjusters. As of September 2013 the FRC has issued three types of licenses for insurance distribution: a) 3400 for individual agents; b) 20 for brokerage companies (incl. three local banks as retail brokers: XAC brokers, and Khan Brokers, and State bank’s broker); and c) 14 for loss adjusters. The training of agents is delegated to the MIA, while the exams are to be taken at the FRC. A brokers’ licence will be granted on the basis of minimum three years experiences in the insurance industry resulting in a demand for more comprehensive and specific training programs for agents and brokers. If the FRC will not conduct training courses themselves they should define a standardized

3 The MiN Actuarial Working Group has developed pricing tools and training courses for life and agriculture products in collaboration with the IAA (a health pricing tool will be finalized end of 2013). These tools would be also available for the Actuarial Society in Mongolia. 4 Source: adopted by author from The World Bank webinar: FARMD September 2013 5 Source: Country Diagnosis, 2011: The translation available from the FRC website is entitled “Law on Mongolia on Insurance Intermediaries”. If properly translated, the title should read “Law on Insurance Professionals” as it also includes regulation and licensing of loss adjusters in addition to agents and brokers.

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 9

curriculum for insurance agents and brokers’ incl. selling products to the low income population as there is a significant knowledge gap.

Cost-effective distribution is a key challenge in Mongolia given the large distances, reaching out to potential individual low-income clients, manual premium collection and other administrative processes such as signing insurance policies by both the parties on paper (although the Ministry of Justice and Internal Affairs ratified an e-signature concept paper as a basis for drafting a future law). Insurance providers sell insurance through their local branches and individual agents but there are no efficient and effective means for reaching out to low-income persons. For brokers, who are based in Ulaanbaatar, it is not feasible to operate at province or district levels (at least not for low-premium products). They could only reach out to the countryside if cooperating with regional distribution channels – an option recommended by various industry stakeholders. Even local banks, which have a much higher presence in rural areas than insurance providers, are not yet equipped to sell other than compulsory auto insurance or credit-linked products - though their infrastructure constitutes an opportunity as many rural people holding bank accounts. However, they would not be in a position to build insurance awareness, inform people about products suitable for their situation, or assist them with claim submission. The Khan Bank (largest commercial bank) started its banc assurance in June 2013 selling insurance through booklets, website, and simple products such as credit-linked insurance and compulsory auto insurance by bank staff. Yet, effective and efficient mechanisms are not in place for a broader spectrum of voluntary products. Another constraint is the low information on insurance and its acceptance as a risk management mechanism. Financial and insurance literacy is an absolutely new field which is not yet taken up by any organisation except the UNDP microinsurance project and the World Bank supported IBLIP program. The ADB-supported microfinance project in collaboration with the FRC Microfinance Department is currently developing a financial education website with similar objectives as the RFPI Asia – FRC platform though with broader issues. This Ulaanbaatar-based FRC-ADB initiative provides scope for exchange or future collaboration. New delivery channels could play the role of a ‘missing link’ between licensed sales force and potential customers for e.g. awareness building, premium collection, or claims assistance. The present regulation, however, does not provide for mechanisms that would make sales more efficient such as mobile banking for automate premium payments in rural areas, electronic signatures, or additional distribution organisations. Since the present delivery channels are a crucial bottleneck for enhancing the penetration of insurance services this section receives special attention. This refers to the consideration of potential innovative distribution mechanisms mentioned below and the subsequent need for information to the FRC: x Local government: The local administration has the broadest outlet in rural areas and people

interact often with the local officials who provide social welfare benefits and other services. Several institutions such as the Actuary Society and UNDP suggested an enhanced coordination in the area of inclusive insurance. FRC at provincial level: The FRC’s local part-time representatives are placed in the provincial local government and could organise awareness programmes and events. UNDP conducts educational programs for local staff of the Ministry of Human Development and Social Welfare. Insurance awareness building to potential customers is being done through the UNDP Information Centres. Considering the current segmentation between insurance, social protection and financial systems development, local government officials (including provincial FRC and social workers) could play a promoting role in financial/insurance education and could support people to access insurance and financial services, assuming they are appropriately trained. They may not be in a position to

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 10

sell private insurance but they could prepare ‘the ground’ for giving low-income people the choice and work in line with the concept of inclusive insurance.

x Savings and Credit Cooperatives (SCCs) and its national Confederation of Savings and Credit Cooperatives – MOCCU (2007): Approximately 200 SCCs are licensed by the FRC. They focus on savings and lending, and are not permitted to sell insurance. Since the SCCs hold accounts at the local banks, they are most suited for providing insurance awareness and financial literacy to their members (as currently supported by the ADB). If the FRC considers amending the present conditions they could moreover apply for an agent licence. Involving the SCCs in either ways has an advantage that their national MCTIC training centre could enhance SCCs insurance capacity. In addition, the MOCCU offers a national infrastructure for implementing capacity developing programs in an efficient way (for details please see separate report on Local Training Institutions).

x The Mongolian National Cooperative Association (MNCA): The 2008-established association with its current seven member organisations (including the Confederation of Savings and Credit Cooperatives) operates nationwide. They represent a broad spectrum of non-government organisations 6and could be used for reaching out to its members in a similar way as described above regarding the SCCs and the MOCCU (e.g. the World Bank supported IBLIP index project works with the Herders Cooperatives).

x Other organisations that have an infrastructure in provincial and district towns reaching out to rural areas such as the Red Cross, SME business associations (if they are relevant).

x Technology-based delivery: Given the limitations of the current distribution channels and the dispersed population, the expectations of mobile phone-based sales are extremely high. Admittedly, the penetration rate of cell phones is high but the low insurance education and acceptance restricts the sales of voluntary products at this stage - except if this channel would be complemented by organisations that disseminate the relevant insurance information. However, for services such as premium payments, renewals, or claim submission mobile phones or e-signature could reduce the administrative costs but need adjustment of the current FRC policy and should be viewed in the context of consumer protection.

Relevant information in the context mentioned above: a) Institutional distribution channels for the low-income market x Partner-agent model in collaboration with the commercial insurance industry

o Agents and brokers for the low-income market x Other delivery channels

o Role of technology o Non-insurance institutions and mechanisms o Public Private Partnership

x Developing sales force and incentives b) Licensing of distribution channels x Requirements for the provision of good services to low-income people x Training contents for delivery channels reaching out to the low-income population x Clear instruction for licensing agents and brokers when dealing with the low-income market x If bancassurance will play a larger role the FRC need to develop a respective guidelines and ToTs

for brokers (who currently invite international experts for their own capacity enhancement). 6 The MNCA consist of the following members: The Central Union of Mongolian Consumers Cooperatives (CUMCC), Central Union of Mongolian Industrial Cooperatives (CUMIC), National Association of Mongolian Agricultural Cooperatives (NAMAC), Union of Mongolian Production and Service Cooperatives (UMPSC), Association of Private Herders Cooperatives (APHC), Mongolian Cooperative Training and Information Center (MCTIC), Mongolian Confederation of Savings and Credit Cooperatives (MOCCU)

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 11

2.4 Microinsurance business operation Since the first UNDP microinsurance health project was confronted with several problems (e.g. adverse selection, moral hazard, and extremely high claims ratios) the FRC is showing significant interest in the issues mentioned below. They reflect also the view of the insurance industry, the Broker Association, and the Loss Adjusters Association. Relevant information in the context mentioned above: a) (Micro)insurance operations7 x Business planning x Marketing and sales methods x Anti selection, fraud & moral hazard detection and controls x Premium payments for low-income customers (in rural areas) x Claims processes (incl. documentation) as the current processes are not suitable for (dispersed)

low-income customers b) Valuable services x Requirements for the provision and assessment of good services to low-income customers x Creating an insurance culture x Educating clients on product value and usage 2.5 Consumer protection Consumer protection should be seen in the context of client value mentioned above. The Law on Insurance (2004) refers to the Civil Code which regulates insurance contracts and includes minimal standards for policy contracts and minimum disclosure to clients. The contracts do not have to specify where and how to make a claim, or provide details about complaint processes (Country Diagnostic draft report, 2011). Taking this situation into account and combined with customer dissatisfaction (though not documented), the FRC-ADB microfinance project considers adding a ‘complaint section’ on its virtual financial education platform which is currently limited to financial products and services but there seems a scope for extending it to insurance and is subject to further discussion with the FRC financial education unit and the ADB project office in Ulaanbaatar. Relevant information in the context mentioned above x Industry-wide dispute resolution mechanism (e.g. Ombudsman) x Regulations that address ethics and market conduct of insurers, agents & brokers serving the

low-income market x Detailed information are provided in the draft ‘Discussion Paper - Consumer Protection in

Microinsurance’ (2012) 2.6 Insurance regulation and legislation Mongolia neither has a specific microinsurance regulation nor a regulation or policy on inclusive insurance and the interest of information from other Asian countries is high. 7 Interestingly, the KPI and Social Performance Indicators were not ranked high at the TNA questionnaire. This contradicts the interest of receiving information on ‘valuable services’. It can be assumed that the concept of the (microinsurance) ‘Key Performance Indicators’ (KPI) and ‘Social Performance Indicators’ (SPI) are not known to the FRC.

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 12

The Diagnostic Country study indicates the concern that “… with a small market for insurance, there is a tendency for insurers and even distributors to employ practices that would undercut other players just to get a bigger share of the market. In view of this, some insurers called for the establishment of rules and guidelines that will prevent underpricing and unfair market practices. With appropriate guidelines, insurers, agents and brokers should be able to deliver the right product with the right price.“ Additional aspects for adjusting the present regulation, related legislation and guidelines in particular pertaining to inclusive insurance are stated in the draft report (2011). During the September 2013 visit, all actors stated the need for further specification and clarification of existing legislation and regulations (incl. further guidelines for ensuring cost effective insurance services for the low-income population). The most common issues are already indicated above. Some additional issues are mentioned below reflecting the specific interest of the different stakeholders, namely the MIA, the Brokers Association and banks. Relevant information in the context mentioned above: x Legal documents on regulation that would promote inclusive insurance products and services

and risk-based supervision. The information should address market conduct of insurers, agents and brokers.

x Material of innovative distribution channels, if permitted at a later stage. Licensing of civil society organisations. non-insurance mechanisms, and technology need specific attention. This would have implications on the concerned laws and regulations such as the Cooperative Law (amended in 2010), the Non-Banking Financial Institutions Law (2002) as well as for legislation pertaining to the role of technology.

x Concepts of additional institutions which may play a role as ‘aggregators’ or ‘promoters’ but not as sales agents. Guidelines and examples that clarify these roles including the official mandate to be given to them.

x Regulatory options for cost-effective distribution mechanisms to open the insurance market for low-income customers. The MIA (and brokers) stated the following challenges:

o Insurance products are subject to a product fee which is suggested to be either waived or deducted for products targeting the low-income market.

o Fee for licensing insurance agents (UB 5.000, in rural areas lower amount) may be reduced for agents reaching out to low-income customers?

x Experiences with carefully designed policies for motivating private insurers to enter the low-income market (e.g. documenting the benefits of inclusive insurance for private sector, good practises, incentives).

x A standardized common insurance glossary and Mongolian/English translation was requested for instance by the Loss Adjusters Association, the MIA, the Actuarial Society, and the Brokers Association who conduct training workshops on the clarifications of terms which are also needed for (financial) reporting.

x Guidelines and good practises of appropriate standardization of products and processes (the standardized auto insurance was stated as a positive example).

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 13

3. Other capacity development issues There is a correlation between FRC’s capacity building needs and those of the insurance industry and other relevant ministries (though more indirect depending on the ministry and the issue). The following aspects highlight a few issues for discussion with a future ‘Joint Working Group’ and other industry actors who is supposed to formulate and develop cross-cutting policies and strategies for inclusive insurance market development. x Consultation processes: Although FRC organises annual dialogue meetings with the MIA and

seeks feedback on insurance issues from others such as the Brokers Association, all actors expressed the need for a structured dialogue and systematic consultation. Such a structured consultation process was introduced by the World Bank supported IBLIP project when developing a separate law for index livestock insurance which had to be passed in parliament: A legal working group of different stakeholders’, incl. sub-groups, was set up (consisting of the insurance industry and the concerned government agencies) followed by a defined process of drafting the law for index insurance with inputs from local and international experts until the paper was submitted to the Ministry of Justice and the cabinet.

x Capacity enhancement of the insurance industry: Due to the limited period of commercial insurance experience in Mongolia the demand for capacity enhancement of all actors is significant - though MIA provides some staff training and the Brokers Association invites international experts for their capacity development. Both the organisations cooperate with the FRC and the MoF. The capacity building needs in the area of inclusive insurance is much higher and corresponds to a large extent with that of the FRC though the emphasis differ (e.g. broadly divided in policy issues for the FRC and technical operations tools for the insurance industry):

x Financial & insurance literacy for potential clients (incl. micro entrepreneurs): According to FRC the concept of ‘insurance’ causes misunderstandings and is associated with ‘taxes’ or is closely linked to the social welfare system requiring marginal contributions (if any). This hampers the promotion of insurance and was the reason for the FRC-ADB microfinance project to develop a financial education website.

x Training of local government officials: Even if the local government will not directly sell insurance, their potential for involvement in awareness-building and risk management literacy should be explored. UNDP has trained government officials in their project regions which resulted in enhanced knowledge and administrative support for the project (e.g. for the Information Centres).

x The National University’s insurance curriculum is in its infancy and can presently not satisfy the needs of the insurance market (let alone inclusive insurance). Since the insurance training needs are significant and the insurance market is expected to grow, the RFPI Asia may explore a pragmatic joint support with other multi- and bilateral organisations. For instance, the Netherlands Senior Expert Service, who sent already insurance specialists to Mongolia, could support the insurance faculty with (short-term) lecturers.

Box 3: Potential role of Universities in capacity development Provider Outreach Strengths Risks Potential

Offerings Business Model & Needs

Universities and business schools

Students looking for high quality learning Participation of insurance industry members to be explored

Credibility/Brand infrastructure Inclusive insurance relevant to existing offerings (not yet in Mongolia

Demand for inclusive insurance has to be raised Lack of skilled faculty

Courses, Training of Trainers Content development & Certification

Up front funding for development of new offerings End user (learner, insurance company) pay or funding for participants

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 14

4. Considerations for designing the KSP As GIZ RFPI-Asia program promotes partnership with the initial six countries from MEFIN, the development of a virtual knowledge sharing platform (KSP) is only one of several mechanisms in the context of capacity building for the promotion of inclusive insurance (for more details please see chapter 2). The platform will serve as the online tool housing information and lessons generated by the partner countries, the RFPI-Asia program and others. In addition, the platform shall provide venues for knowledge exchange among regulators/supervisors (prime users) and secondary target participants, such as the Ministry of Finance in Mongolia. In order to ensure active usage of the KSP, a semi-structured questionnaire was developed (see Annex 2) for receiving feedback on the following broad areas: x Expectations x Current and potential user behaviour x Suitable methods of the KSP x Administrative issues x Technical details (need to be clarified by the KSP developer) 4.1 Expectations and objectives It seems that the expectations of the virtual KSP were not discussed in detail within the FRC Insurance Division. The director strongly appreciated the rich resources accessible through a virtual platform. However, he indicated his preference for face-to-face interaction and expressed certain reluctance on the complex features a KSP can offer (“FRC staff is busy with day-to-day work”; “Staff cannot be pushed to use KSP”). These concerns have to be taken into consideration when selecting the contents and developing a platform with a focus on accessibility and a user friendly GUI (Graphical User Interface). Objectives: The partner countries are striving toward inclusive insurance and are at different stages of this process. To ensure that lessons generated by core stakeholders are consolidated and made readily available to other regulators and supervisors, the KSP aims at providing a single-window platform for defined topics which will be shared by the primary and secondary users in the partner countries for promoting improved inclusive insurance policy. Benefits of the KSP: By accessing and exchanging knowledge through a suggested wiki-based online platform it is expected to x Shorten the learning curve, make work easier and contribute to faster decisions; x Enhance the quality of solutions by receiving feedback and discussing relevant topics; x Increase the pool of human resources with high quality knowledge to whom partner countries

can refer to. 4.2 Current user behaviour – scope for using the KSP Currently the FRC staff members8 focus on the use of Emails and some internet research (google). They are not familiar with distant learning. Their digital office systems are in the process of being further developed and there is a lack of database (e.g. for insurance products).

8 If not mentioned otherwise the term ‘FRC’ refers to the Insurance Division of FRC and not to other FRC Departments.

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 15

Another constraint is the English language skill. Out of 13 FRC Insurance staff members four are relatively fluent while only a few can read English documents. According to the Director, this will result in staff’s reluctance of sharing ‘badly written’ English information and hampers real-time interaction on the KPS. It seems the interaction within the KSP will focus more on asynchronous methods (e.g. email, forum, online library) than on synchronous communication (audio, moderated discussion, chats). The full complexity of online mechanisms will be limited to very few staff members and the Director. Box 4: Dealing with different languages

It is suggested that x FRC staff members concerned attend the English classes offered by the Luxembourg

Government (other FRC members are more active than their colleagues from the Insurance Division);

x Only important documents should be translated as it is expensive to translate large numbers of papers into the relevant working languages;

x Translating summaries of selected discussions and documents in several languages. If the intended ‘joint working group’ will be established and could serve as a venue for discussing issues that cut across jurisdictions of various government departments, they will also use the KSP. Hence, the RFPI-Asia program needs to discuss these issues with them as well. 4.3 ‘Knowledge Management’ approach There are various definitions of ‘Knowledge Management’ available. For the RFPI Asia KSP it seems to be most useful to define Knowledge Management as the use of practises to identify and obtain different types of information and make knowledge available to people (as defined above) who need it at the appropriate time. The KSP is linked to institutional learning and incorporates the sharing of knowledge and lessons learnt. The RFPI Asia KSP will consist of two key components: a) Knowledge collection that will allow the users to

x easily retrieve needed materials anytime x upload relevant documents and tools useful in inclusive insurance practice x document lessons in a more structured and simple way

b) Knowledge sharing to x comment on shared documents of inclusive insurance topics x discuss with other partners on critical issues related to inclusive insurance, incl. some

assistance through peers or the facilitator x connect with people or organizations providing the experience the KSP users are looking for

This process can be organised through the following steps:

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 16

4.3.1 Actions for promoting an effective use of the KSP 1. Generating knowledge x Confirm core users fully understand the concept of “KSP” x Ensure selected users/participants are open to learn, and are capable and willing to share

learnings x Orient users/participants to select relevant information and prepare simple project

documentation on defined issues preferably according to jointly defined formats x Facilitate the management of the KSP and provide guidance to the users/participants when

needed 2. Eliciting & extracting knowledge x Mobilize persons to extract lessons from project partners x Organise eliciting knowledge from outside the RFPI Asia program x Use reports and other communication by the RFPI Asia program for extracting knowledge (if not

confidential) 3. Synthesizing and analyzing knowledge x Lessons across partner countries (and beyond) will be analyzed to enrich the formulation of

inclusive insurance regulation and related practices x KSP entries on defined topics will be synthesized for easy use by other users 4. Consolidating & packaging knowledge x Package the knowledge in a way that can be (quickly) read and summarize the most relevant

learnings

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 17

x Produce information in a way that can be understood by various users (e.g. informed management, administrative staff; fluent English speakers, those with little English knowledge)

x Categorize the information according to defined relevant topics and present them in formats that are easy to use

5. Sharing & communicating knowledge x A searchable database of information and lessons will be available online x Periodic exchanges will be conducted for both regulators & supervisors and other experts (e.g.

through time-bound discussion forums) x Peer groups will be encouraged for joint learnings and feedback 6. Depending on the complexity of the KSP a tool for ‘realizing knowledge needs’ could be integrated x ‘Realizing knowledge needs’ helps an organisation to become aware its knowledge gaps and

enables the management to take corrective action (e.g. obtaining information in identified sectors). An online self assessment tool could assist FRC to diagnose its capacity building needs. This feature requires additional effort which may overload the KSP management initially.

4.3.2 Strategic management considerations Regardless of the complexity of the virtual KSP, several processes have to be defined: x Hosting of the KSP: Who will host the KSP – one platform or being hosted at the partner

countries with automatic linkages (if systems are compatible)? x Quality control: Who will decide about the initial contents, updating of contents, and adoption of

contents – an effective structure is a prerequisite otherwise it will prolong the process of uploading (bottleneck)?

x Quick availability: Should new information be immediately available (probably depending on the relevance)? If uploads can be done decentralised (through country managers?), the platform is potentially more up-to-date though the quality control is less (consideration could be given to a defined section of the KSP which could be open to the members while the core platform will be centrally managed).

x Access: The RFPI Asia and the partner countries may decide on an extended audience such as the future ‘joint working group’ in Mongolia or/and selected actors from the insurance industry who could benefit from the KSP The decision also depends on the duration of the platform: Is it intended to operate the KSP beyond the RFPI Asia program duration? If yes, it makes sense extending the user group. The KSP may house different sections for different access levels (with the prime users having access to all spaces, including peer discussion groups).

x Pre-testing: KSP must be pre-tested before going online. Knowledge collection and sharing requires maintenance of the platform, facilitation and coordination with contributors and users. While a KSP system administrator ensures the technical operation, a good online facilitator “should engage, guide and motivate learners, and provide a safe and conducive environment for learning and communication exchange for all learners regardless of their prior experience and predisposition” (Australian flexible learning framework). This is in particular important as the knowledge, the experience, and the language gap between the KSP users is high. The online facilitator acts also as a knowledge manager and engages the user in the learning process (particularly at the beginning) and assists the user group to define its goals; assess the demand for information, assist in delivering the requested materials, (if feasible), answering questions, and provide feedback. The wider the knowledge gap, digital experience and language gap is, the more

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 18

asynchronous communication will take place and the more facilitation is required. The facilitator needs contact persons in the partner countries for in-country coordination. In addition to these ‘soft skills’ an effective online facilitator should x be knowledgeable about the subject and have an overview about relevant information, x be in a position to assess the relevance of information, incl. linkages to international sources x be able to answer questions or to forward them to selected experts. Box 5: Setting of online facilitation

Swiss Development Corporation (SDC): Good Practice: E-Facilitation, 2011:

Online dialogues – especially email-based interactions – can help us do our work in an inclusive and efficient way, as well as learn from the experience of others. However, online group interactions often do not happen spontaneously. Once they have been set up, they require care and nurturing. E-facilitators can help create ownership and trust, as well as make online communication more efficient, results-oriented and participatory. What is special about e-facilitation? In online spaces – just as in offline community spaces – people interact for various reasons, e.g., to communicate, share information, build knowledge around a practice or carry out a project. E-facilitation for what? In the SDC context, online dialogues are used in various ways. For example, a network member may have a question on a specific aspect of his/her work that is sent to the group, for which a quick response is received (Q&A). Alternatively a network member may have a challenge or thematic issue for which a broader range of more detailed responses is sought. Other network members formulate various responses and the exchange can then be summarised (experience capitalisation through consolidated reply). Third, scheduled discussions – usually lasting 2-3 weeks – are held online in order to clarify thematic issues and build a consensus within the network (consultation). Also, e-discussions can be used for collective problem solving (e-cooperation). Finally, online exchanges might be used to prepare a f2f event of the network or to follow up on it (see guide on linking face to face and online dialogues). As is the case with other activities within a network, key online dialogues should be planned and conducted to achieve desired objectives.

4.4 KSP tools for knowledge generating, sharing and learning One of the major challenges of the joint KSP is the diversity of users in terms of x Digital affinity and experience x Implementing stages of inclusive insurance x Language skills With the diverse user audience in the six countries, the RFPI Asia program must avoid sub-challenging or overcharging the participants. This pertains to complexity of contents, forms of digital communication (user friendliness of KSP and extend of usage) and language. While a certain divide can be already noticed in Mongolia across the FRC directorate and staff, the situation is even more diverse between countries like the Philippines and Mongolia. This balancing act implies more efforts in user-specific selection of information, adoption and packaging of knowledge; developing appropriate digital formats on the KSP, and translation of selected papers and summaries of online discussions. In Mongolia the KSP will not be available on smart phones (which otherwise would need additional adaptation). A wiki-based platform allows a broad range of interactive options9 and can be configured according to the needs of the partner countries (see Table 1 Proposed KSP Design). It builds on the concept of

9 Wiki-based system allows language selection (if relevant for the KSP), commenting & editing documents and track changes, modifying text by users and allow to re-establishing earlier versions, chats, blogs, monitor & control contents, search function, information about news posted through e.g. RSS feeds.

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 19

‘Good practice’ which combines two elements: a) knowledge database (connecting people with information) and b) methods for sharing knowledge such as (virtual) communities of practice (connecting people with people). Depending on the financial and human resources available, the KSP can contain tools beyond an online database/library, feedback functions, discussion forums, or moderated or guided learning sessions. Complex learning mechanisms require additional inputs: x Peer tutoring or peer assistance support each other and learn from each other’s work x Job aids or facilitation provide in-time knowledge, usually quick answers to specific questions,

helping users accomplish their tasks x Learning platforms are a set of interactive online services that provide users with access to

information and resources to support educational delivery and management through the Internet. For instance

o Virtual learning environments (VLEs), are used to simulate traditional face-to-face classroom activities and facilitate teaching and learning with a strong collaborative component. VLE supports facilitated online learning and allows tutors and learner to share content and create links to outside sources. There are many virtual learning platforms which can be used for online and blended solutions delivery (some technical details under 4.5.2).

o Learning management system (LMS) solution facilitates delivery and management of all learning mechanisms, incl. virtual classroom and instructor-led courses but with an emphasis on training.

o Learning content management systems (LCMSs) focuses mainly on creating e-learning content. Though these reduce development efforts and allow digital content to be easily available, existing documents (e.g. in the online library) cannot automatically serve as e-learning materials but need to be transformed into specific formats. For example, a PowerPoint presentation developed for face-to-face sessions is not e-learning content, because it does not include the explanations and examples of the trainer, a study is not e-learning content because the way it is designed does not automatically match specific learning objectives.

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 20

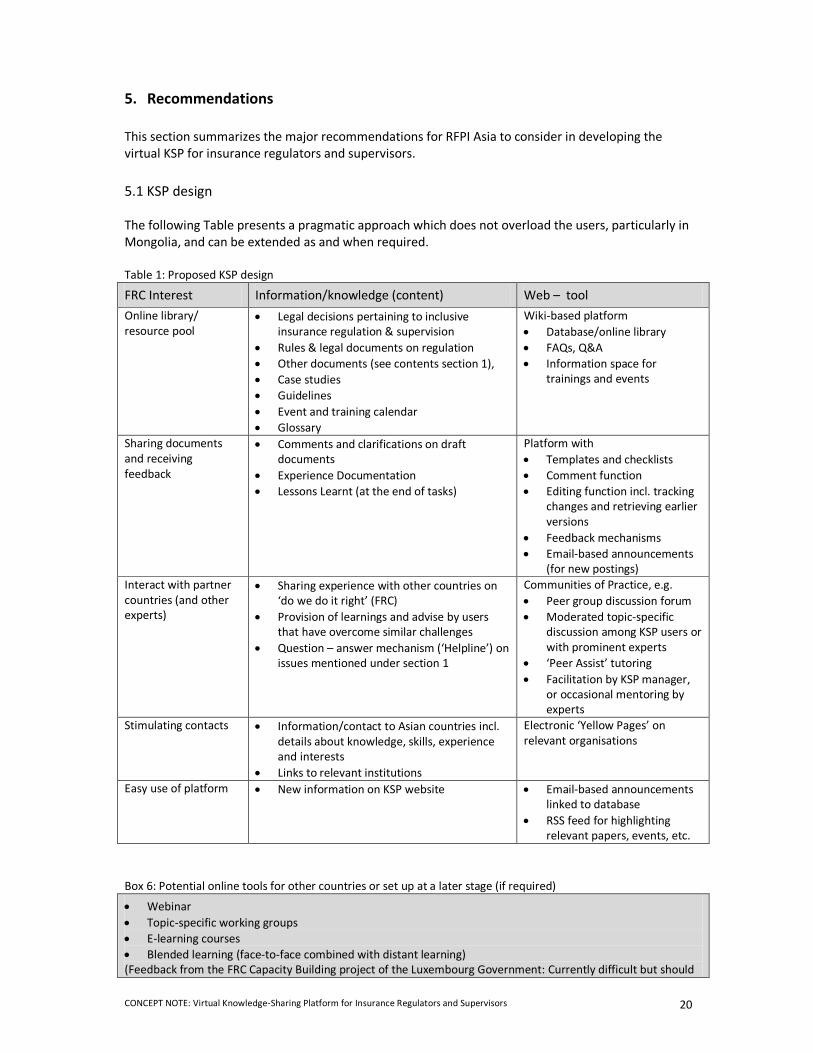

5. Recommendations This section summarizes the major recommendations for RFPI Asia to consider in developing the virtual KSP for insurance regulators and supervisors. 5.1 KSP design The following Table presents a pragmatic approach which does not overload the users, particularly in Mongolia, and can be extended as and when required. Table 1: Proposed KSP design

FRC Interest Information/knowledge (content) Web – tool Online library/ resource pool

x Legal decisions pertaining to inclusive insurance regulation & supervision

x Rules & legal documents on regulation x Other documents (see contents section 1), x Case studies x Guidelines x Event and training calendar x Glossary

Wiki-based platform x Database/online library x FAQs, Q&A x Information space for

trainings and events

Sharing documents and receiving feedback

x Comments and clarifications on draft documents

x Experience Documentation x Lessons Learnt (at the end of tasks)

Platform with x Templates and checklists x Comment function x Editing function incl. tracking

changes and retrieving earlier versions

x Feedback mechanisms x Email-based announcements

(for new postings) Interact with partner countries (and other experts)

x Sharing experience with other countries on ‘do we do it right’ (FRC)

x Provision of learnings and advise by users that have overcome similar challenges

x Question – answer mechanism (‘Helpline’) on issues mentioned under section 1

Communities of Practice, e.g. x Peer group discussion forum x Moderated topic-specific

discussion among KSP users or with prominent experts

x ‘Peer Assist’ tutoring x Facilitation by KSP manager,

or occasional mentoring by experts

Stimulating contacts x Information/contact to Asian countries incl. details about knowledge, skills, experience and interests

x Links to relevant institutions

Electronic ‘Yellow Pages’ on relevant organisations

Easy use of platform x New information on KSP website x Email-based announcements linked to database

x RSS feed for highlighting relevant papers, events, etc.

Box 6: Potential online tools for other countries or set up at a later stage (if required)

x Webinar x Topic-specific working groups x E-learning courses x Blended learning (face-to-face combined with distant learning) (Feedback from the FRC Capacity Building project of the Luxembourg Government: Currently difficult but should

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 21

be strongly supported incl. required guidance. There a many ways of e-learning methods that would exceed the scope of the paper. So far only a few FRC members, though nobody from the Insurance Division, attended the e-learning English language course offered by the Luxembourg Government. The Loss Adjuster Association will apply an e-learning approach for their members and recommended a wider spread of distance learning methods)

The following initiatives can stimulate the KSP participants to use the platform, e.g. x As the communication be primarily asynchronous (largely due to language problems or time

difference), trust among the KSP key users stimulates active participation. Joint face-to-face meeting(s) could be helpful to kick-start the KSP (e.g. Jakarta Microinsurance conference, further Toronto Centre training courses).

x A short introductory video could explain the value-addition for the KSP participants and how the platform can be used (embedded from streaming platform is even better than a link to other server).

x Configure the browser in a way that the KSP is always ‘visible’ (e.g. place a KSP icon on the homepage of the respective country websites for easy opening and as a constant reminder)

x A RSS feed can inform the KSP users of new information which could be supplemented by detailed email announcements of new entries, interesting events, or short learnings.

x Add content of high interest to the members – which must not necessarily be linked to inclusive insurance but motivate potential users to open the KSP (e.g. all relevant contact details/phone numbers, relevant articles/official announcements, or more ‘entertaining’ issues).

5.2 KSP development – initial steps Developing a Knowledge Sharing Platform is not ‘an overnight’ task and can absorb significant resources. It is, therefore, suggested to apply a step-wise-approach: Starting with an online library containing the (most) relevant information and simple interactive online tools (see Tables 1 and 2). In due course of time and after analysing the use of the KSP other content and web tools can be added (e.g. webinars, e-learning tools). For pre-testing and gaining experience, RFPI Asia may consider to take Mongolia as a starting point before rolling it out at a large scale in all other partner countries. Apart from higher investments into content management, due to the limited information on (inclusive) insurance in Mongolia, this approach has some advantages: x It is a small market and feedback can be obtained easily. x There is a high demand for information expressed by all industry stakeholders. x The few existing (micro)insurance projects are facing the same problem of identifying effective

and efficient ways of information dissemination for insurance education and learnings – a joint collaboration (e.g. with UNDP, IBLIP- World Bank) would be most effective and efficient in reaching out to a larger user group.

x The FRC- ADB microfinance project started developing a financial education website in partnership with the Ministry of Finance and the Bank of Mongolia. Although it will be designed for the ‘general public’ incl. ministries and financial institutions, various sections will be similar to that of the RFPI Asia Knowledge Sharing Platform. Both, the FRC-ADB project and the recently established FRC - Financial Education Unit (2013) are interested to coordinate their efforts with the KSP of the FRC Insurance Division and the RFPI Asia program. As most of the questions pertaining to the management of the wiki-based website are not yet answered, an early dialog with the FRC-ADB is recommended.

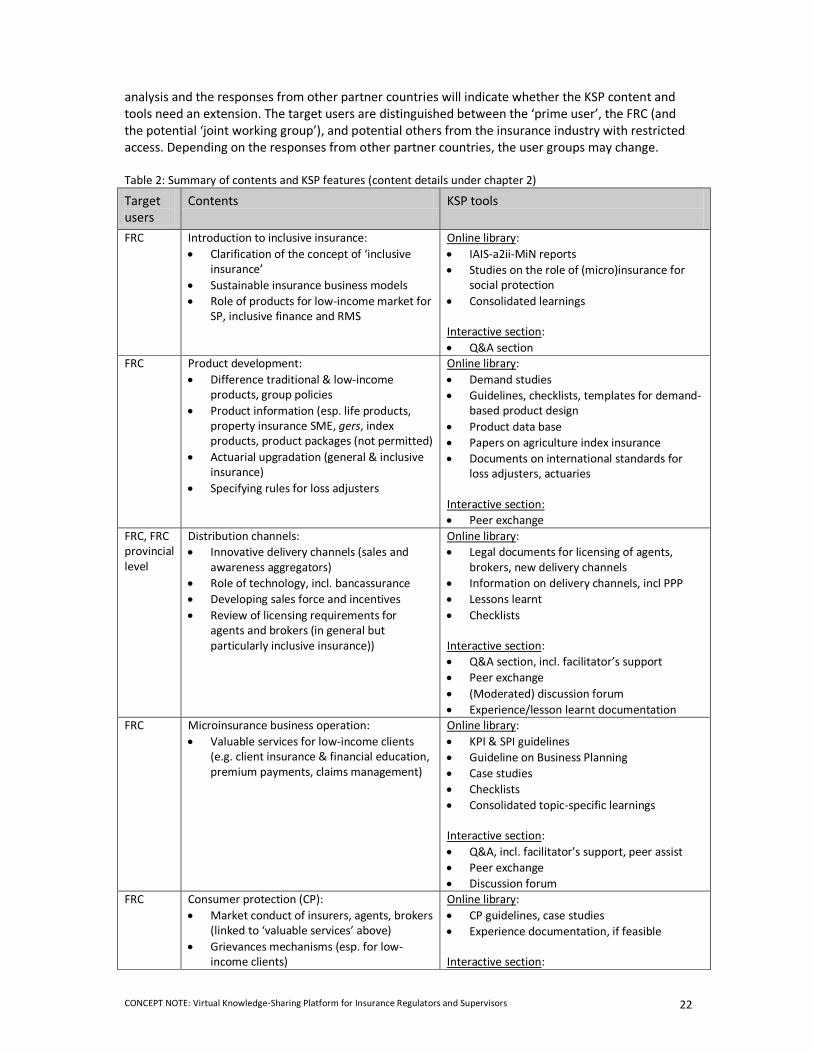

5.3 KSP content and tools The table below displays a summary of contents presented through various tools on the KSP focusing on asynchronous communication initially due to the reasons mentioned above. The monitoring

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 22

analysis and the responses from other partner countries will indicate whether the KSP content and tools need an extension. The target users are distinguished between the ‘prime user’, the FRC (and the potential ‘joint working group’), and potential others from the insurance industry with restricted access. Depending on the responses from other partner countries, the user groups may change. Table 2: Summary of contents and KSP features (content details under chapter 2)

Target users

Contents KSP tools

FRC Introduction to inclusive insurance: x Clarification of the concept of ‘inclusive

insurance’ x Sustainable insurance business models x Role of products for low-income market for

SP, inclusive finance and RMS

Online library: x IAIS-a2ii-MiN reports x Studies on the role of (micro)insurance for

social protection x Consolidated learnings Interactive section: x Q&A section

FRC Product development: x Difference traditional & low-income

products, group policies x Product information (esp. life products,

property insurance SME, gers, index products, product packages (not permitted)

x Actuarial upgradation (general & inclusive insurance)

x Specifying rules for loss adjusters

Online library: x Demand studies x Guidelines, checklists, templates for demand-

based product design x Product data base x Papers on agriculture index insurance x Documents on international standards for

loss adjusters, actuaries Interactive section: x Peer exchange

FRC, FRC provincial level

Distribution channels: x Innovative delivery channels (sales and

awareness aggregators) x Role of technology, incl. bancassurance x Developing sales force and incentives x Review of licensing requirements for

agents and brokers (in general but particularly inclusive insurance))

Online library: x Legal documents for licensing of agents,

brokers, new delivery channels x Information on delivery channels, incl PPP x Lessons learnt x Checklists Interactive section: x Q&A section, incl. facilitator’s support x Peer exchange x (Moderated) discussion forum x Experience/lesson learnt documentation

FRC Microinsurance business operation: x Valuable services for low-income clients

(e.g. client insurance & financial education, premium payments, claims management)

Online library: x KPI & SPI guidelines x Guideline on Business Planning x Case studies x Checklists x Consolidated topic-specific learnings Interactive section: x Q&A, incl. facilitator’s support, peer assist x Peer exchange x Discussion forum

FRC Consumer protection (CP): x Market conduct of insurers, agents, brokers

(linked to ‘valuable services’ above) x Grievances mechanisms (esp. for low-

income clients)

Online library: x CP guidelines, case studies x Experience documentation, if feasible Interactive section:

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 23

x Feedback of drafts/laws etc. x Peer exchange/forum x Q&A, Facilitator’s support Moderated expert discussion

FRC Insurance regulation & legislation (linked to issues above): x Legal documents, regulations for inclusive

insurance x Insurance glossary x Good practices on inclusive insurance

Online library: x Legal documents, regulations on inclusive

insurance x Glossary x Case studies Interactive section: x Feedback function (on draft documents, etc.) x Peer assist (‘do we do it right’)

Potential other users

Actuarial Society, Loss Adjuster

x Actuarial upgradation (general & inclusive insurance)

x Deepening training for loss adjuster

Face to face training or e-learning courses, IAA MI pricing training , access to KSP on product development section

MIA, Banks, Brokers

Distribution channels: x Innovative delivery channels (sales or

awareness aggregators) x Role of technology, incl. bancassurance x Developing sales force and incentives x Review of licensing requirements for

agents and brokers (contents of training – in general but particularly inclusive insurance)

x Consumer protection

Access to KSP on distribution channels and product development, business operations and consumer protection section Dialog programs (face to face, conference on delivery channels)

5.4 KSP management structure Hosting of the KSP: It is suggested to use a central host and a central management including a facilitator for the KSP operations. If other country-specific platforms exist, like the future FRC-ADB financial education website, the KSP could be linked to this website coordinated by the FRC ‘country platform manager’ (CM) and assisted by the central facilitator. If the RFPI Asia enters into a cooperation with the UNDP Microinsurance project, the FRC-ADB Microfinance program, or even the IBLIP supported be the World Bank, the management structure is likely to be adopted. Quality control: Quality control will take place at different levels: a) decision on documents for the online library at the time when developing the platform, b) ongoing decisions when updating the KSP (distinguishing between country information and general documents), c) monitoring and facilitating the interactive section of the platform (e.g. discussion forum, peer-assist section). This issue is closely linked to the question of ‘access’ (see below). Online library: Taking the list of identified contents into account, a number of documents will be politically sensitive (e.g. drafts of regulations, laws, or policy decisions). This calls for a careful decision on the uploaded documents. In order to develop ownership and obtain information on the relevant material, each country may nominate one ‘country platform manager’ (CM) who will become a member of a ‘KSP committee’ (composition see below) for joint decision taking of the content (when establishing the platform). As the information are of strategic nature rather than of immediate need, this initial slightly time consuming process may be acceptable. The ongoing update can be done by the central facilitator as he/she participated in the initial decision making process and should have developed the required ‘sensitivity’.

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 24

Interactive KSP section: A distinction is required between a) the prime users and b) selected others (e.g. the future ‘joint working group’) and c) other industry actors. While there is no need to steer the discussion forum among the prime users (regulators and supervisors), the postings of potential other users need to be monitored by the facilitator. The ‘peer assist’ section require a prior reading and some facilitation (e.g with additional information from worldwide experience on specific issues). Access: When investing significant resources in establishing and operating the platform, it is suggested to provide access to an extended group within the industry. This can be steered by housing different sections for different access levels. While the prime users will have access to all spaces the extended group would have restricted access but can use the online ‘public library’, the public-moderated discussion on selected topics, etc.). Box 7: KPS management structure

KSP Management Structure

KSP committee• Decisions online library

(development phase)• Strategic decisions (as and

when required)

General KSP

Facilitator assistedby CM

• Online library updates (country information)

• Online library updates (other information)Online

library

Links to other relevant websites

(e.g. FRC-ADB financial education, Mongolia)• Relevant experts/contacts

• Links to other organisations & webistes

Prime user (unrestricted access)•Discussion forum (no control)•Feedback section (no control)•Peer assist (cross check by facilitator)•Q&A facility among prime users & facilitator

External user (restricted access)•Public section of online library•Public moderated topic-specific discussion

Interactive sectionFacilitator

x KSP committee members (central level) – responsible for the initial contents of the online library:

o representation from RFPI Asia, GIZ o representation from the regulator(s)/supervisor(s), o central level facilitator, o country platform manager (CP)

x Central level facilitator & content manager – responsible for managing the centrally hosted KSP. Since the content requirements are high in Mongolia, the value addition of the KSP is related to ‘advisory services’ both by peers but particularly by the facilitator and other

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 25

experts to whom the facilitator could address the questions (for instance Q&A and guided/moderated discussion forum). Such service require additional resources and depends on the RFPI Asia budget or/and the collaboration with other agencies like UNDP and the ADB.

It would be most effective if the facilitator could also fulfil the function of a content manager (updating the platform and managing the interactive section). This task could be either done by RFPI Asia (depending on the GIZ RFPI staff availability) or by outsourcing to person(s)/consultancy firm fulfilling the requirements mentioned under 4.3.2. If both the functions cannot be done by one person, the tasks have to be separated and supported

o by the country manager for country-specific content, and o probably by somebody for international information (occasionally)

x Country platform manager – responsible for obtaining country-specific contents to be submitted to the central facilitator.

o If other relevant country-specific virtual platforms are operational, the CM should coordinate with such organisations e.g. the FRC-ADB financial education website, assisted by the central facilitator depending on the nature of the cooperation.

x System administrator – if the platform is centrally hosted in the Philippines, it would be most

efficient if the GIZ system administrator could be assigned for the KSP. As the KSP will be used by in six countries, the knowledge of the bandwidth limitations is needed for choosing the right delivery format. The following is a rough estimate of connection speeds required by various e-learning formats10

o Screen sharing with text and images: from 128 Kbps to 300 Kbps o E-mail, Chat, discussion forums: from 56 Kbps to 128 Kbps o Video conferencing, live webcasting: from 100 Kbps to 1800 Kbps o Audio conferencing: from 56 Kbps to 128 Kbps.

Once the RFPI Asia introduces extended e-learning methods, decisions on appropriate learning platforms need to be taken. Learning platforms exist as proprietary software or open source: One of many other open-source learning platforms is Moodle (Modular Object-Oriented Dynamic Learning Environment) which is widely used, and free of charge. Moodle has more than 73 million users and almost 87 000 registered sites in 239 countries (as of September 2013)11. Numerous modules extend its functionalities (e.g. graphical themes, authentication and enrolment methods, games and activities and resources). Moodle runs without modification on Unix, Windows, MacOS and many other systems that support PHP scripting language and a database compliant with SCORM and AICC standards. Iits installation requires certain technical proficiency of PHP technology. But there are many other open-source LMS solutions

5.5 Monitoring and Evaluation of the KSP Monitoring of the KSP will provide valuable information about acceptance of the platform, preferred contents and features which could be used for improving this facility. It is recommended to start with a basic monitoring plan (see Table x) containing data from site statistics which can be retrieved automatically from server logs (if configured accordingly). The indicators can be refined at a later stage (e.g. adding conversion rate12). A later evaluation could assess the satisfaction rate of users and for instance the number of assistance services provided by the facilitator.

10 Source: http://support.apple.com/kb/ht2020 (last visited 16 October 2013) 11 https://moodle.org/stats/ (last visited 16 October 2013) 12 Conversion rate is a call for action, e.g., when webinar announced and call for registration= effective number of registration.

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 26

Table 3: Example of performance indicators Indicators

Website - general Number of visitors on the KSP , number of clicks on contents

Online library/ documents

Number of clicks pertaining to different documents Number of downloaded documents Number of clicks on FAQ section Number of uploads and clicks on information space for training and events Number of RSS feeds posted

Sharing documents/ feedback facility

Number of documents posted for sharing and commenting Number of comments / feedback Number of downloaded templates/checklists Number of Email based announcements

Interaction Number of participants using the Q-A functions and the ‘helpline’ Number of (moderated) peer group discussion and participants in peer group discussion, moderated chats/discussion Number of forums and Number of participants at forums

Contact stimulation

Number of clicks on this site Number of contacts Number of clicks on links to referred institutions

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 27

Bibliography http://support.apple.com/kb/ht2020 (last visited 14 October 2013) All Things in Moderation Company: Running E-tivity plenaries, London 2011 Australian Flexible Learning Framework: Effective Online Facilitation, October 2003 Batchuluun, A.: Financial Literacy among Members of Savings and Credit Cooperatives and the General Population in Mongolia., Asian Development Bank; Ulaanbaatar, Mongolia 2010. FAO: E-learning methodologies, FAO; Rome 2011 Forum for Agricultural Risk Management in Development (FARMD): Global loss adjustment practice in agriculture. Key principles of building an effective system, Swiss Government (SECO), Dutch Government, The World Bank; webinar September 2013 FRC, Department of Cooperatives: Draft Law on Savings and Credit Cooperatives - Introduction (Eng). Ulaanbaatar, Mongolia, 2010 IAIS: Application Paper on Regulation and Supervision supporting Inclusive Insurance Markets, IAIS-joint working group/MicroInsurance Network/ the Access to Insurance Initiative, October 2012 ILO Microinsurance Innovation Facility (internal capacity building papers), Geneva 2010-2012 Law of Mongolia on Insurance Intermediaries, Ulaanbaatar, Mongolia, 30 April 2004 (unofficial translation) MNCA Activity REPORT 2010, Ulaanbaatar, Mongolia, 2011 https://moodle.org/stats/ (last visited 14 October 2013) National VET E-learning Strategy 2012–2015, Australian Government, Department of Industry, Innovation, Science, Research and Tertiary Education Rendeck, K., Wiedmaier-Pfister, M.: Developing the Market for Microinsurance in Mongolia, Draft, December 2011 SDC L&N, Knowledge Management Tools, http://www.sdc-learningandnetworking.ch/en/Home/SDC_KM_Tools, (October 4th, 2013) Swiss Development Corporation (SDC): Good Practice: E-Facilitation, 2011

UNDP: Capacity Building for the Micro-insurnce Market Project. Assessment of the policy and regulatory framework on micro-insurnace industry in Mongolia, UNDP, Ulaanbaatar, Mongolia, December 2009

CONCEPT NOTE: Virtual Knowledge-Sharing Platform for Insurance Regulators and Supervisors 28

ANNEX 1

Results of the TNA questionnaire leading to the following contents13: Cross-checking the importance of topics mentioned in Annex 2 with information already available reveal the results below. It is important to note that we could not verify the available information provided by the FRC staff members. As a sample size of 10 persons is not sufficient for statistical analysis the following topics also reveal the discussion with the different stakeholders.14 Introduction to inclusive insurance/microinsurance: x Low-income market, inclusive sustainable insurance business models(2.3 – 2.0) x Group policies and individually sold products (2.6 – 2.5) x (role of microinsurance for social protection, inclusive finance and integrated risk management

(2.4 – 2.0) Product development for the low-income market x Introductory principles for low-income customers (2.2 – 2.4) x Data availability on low-income customers required for product development (2.4 – 2.3) Information on the following product types x Agriculture insurance against catastrophic weather-related risks (3.1 – 2.5) x Livestock index insurance (2.8 – 2.5) x Challenges of indemnity-based products for the low-income market (2.9 – 2.6) x Property insurance for micro enterprises (2.6 – 2.6) x Product design for hospitalisation and out-of-pocket expenses cover (3.1 – 2.7) x Importance of health care providers and infrastructure (3.5 – 2.9) x Life insurance: credit life, life & savings, accident & disability, remittances linked insurance (3.2 –