Embed Size (px)

Citation preview

$2.0B

Presented by:• Ashima(50801012)• Alpa(50801007)• Hina (50801030)• Himanshu Watta(50801029)

“ “ Virtual Integration From DELLVirtual Integration From DELLStrategy That Revolutionized an Industry ” Strategy That Revolutionized an Industry ”

www.dell.com 2

Background

Ten years ago , the companies that were the stars in the Digital Equipment of this world, had to build massive structures to produce everything a computer needed.

As a small start-up, Dell couldn’t afford to create every piece of the value chain. But more to the point, why should we want to?

Dell concluded that they’d be better off leveraging the investments others have made and focusing on delivering solutions and systems to customers.

www.dell.com 3

As said by Michael Dell

• “If you’ve got a race with 20 players that are all vying to produce the fastest graphics chip in the world, do you want to be the twenty-first horse, or do you want to evaluate the field of 20 and pick the best one”?

And that’s how Michael Dell coined Virtual Integration

www.dell.com 4

VIRTUAL INTEGRATION

“Virtual integration means you basically stitch together a business with partners that are treated as if they’re inside the company.”

Michael Dell

www.dell.com 5

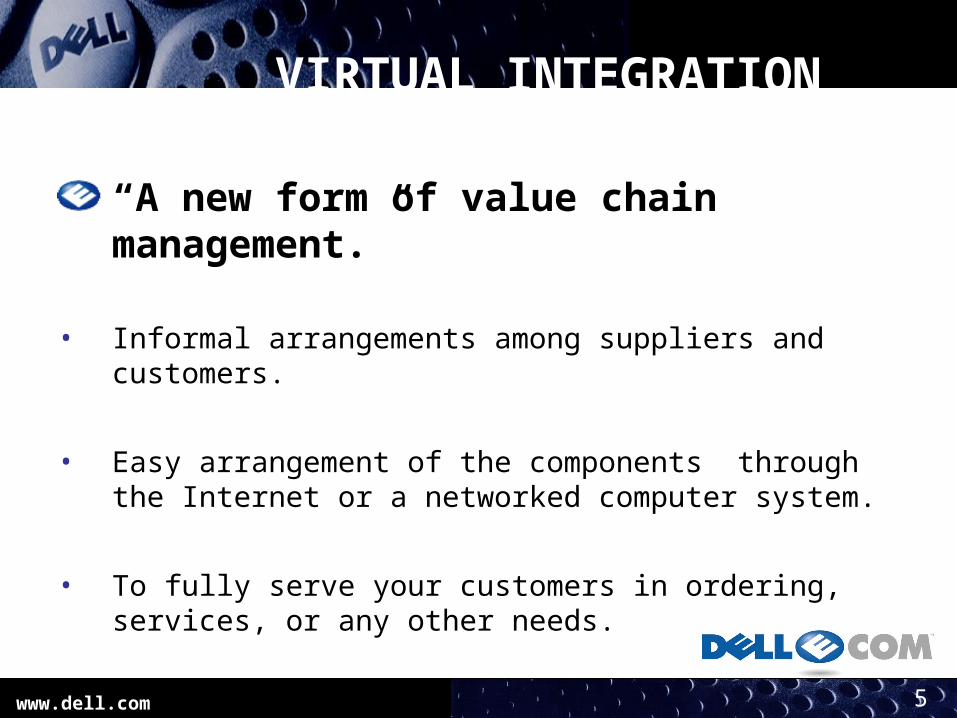

VIRTUAL INTEGRATION

“A new form of value chain management.”

• Informal arrangements among suppliers and customers.

• Easy arrangement of the components through the Internet or a networked computer system.

• To fully serve your customers in ordering, services, or any other needs.

www.dell.com 6

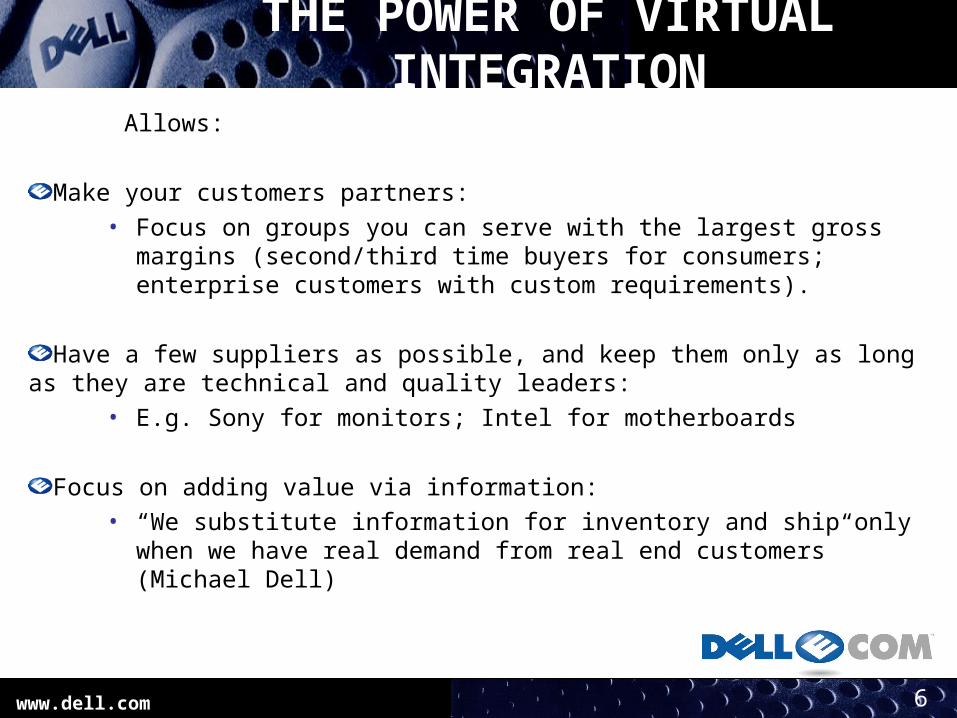

THE POWER OF VIRTUAL INTEGRATION

Allows:

Make your customers partners:• Focus on groups you can serve with the largest gross margins (second/third time

buyers for consumers; enterprise customers with custom requirements).

Have a few suppliers as possible, and keep them only as long as they are technical and quality leaders:

• E.g. Sony for monitors; Intel for motherboards

Focus on adding value via information:• “We substitute information for inventory and ship only when we have real demand

from real end customers” (Michael Dell)

www.dell.com 7

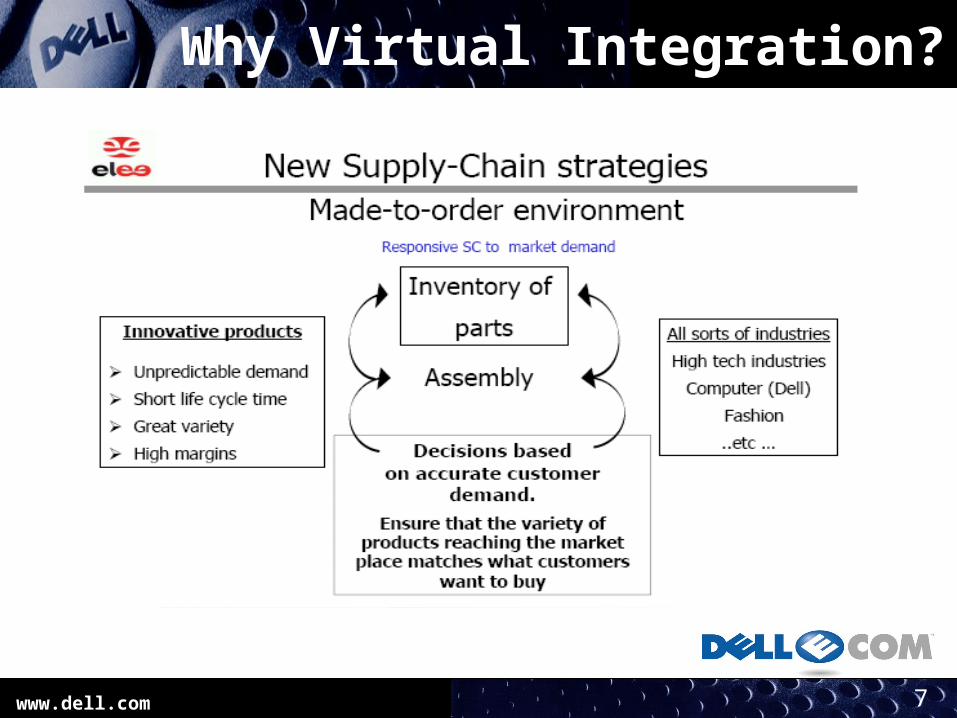

Why Virtual Integration?

www.dell.com 8

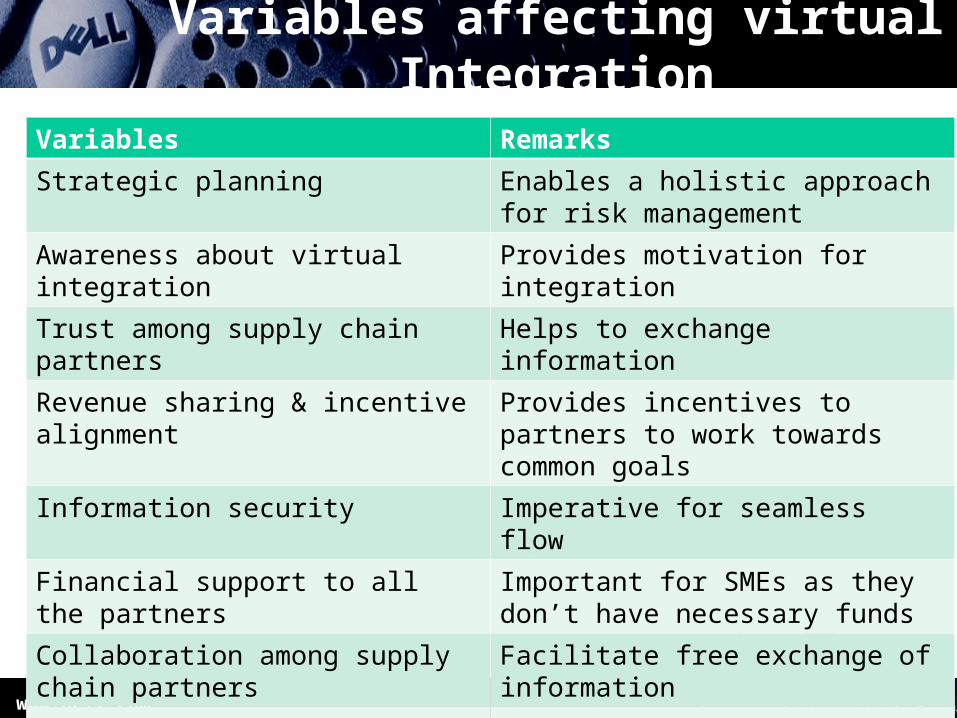

Variables affecting virtual Integration

Variables RemarksStrategic planning Enables a holistic approach for risk

managementAwareness about virtual integration Provides motivation for integrationTrust among supply chain partners Helps to exchange informationRevenue sharing & incentive alignment Provides incentives to partners to work

towards common goalsInformation security Imperative for seamless flowFinancial support to all the partners Important for SMEs as they don’t have

necessary fundsCollaboration among supply chain partners

Facilitate free exchange of information

Compatible IT infrastructure Assists integration of partners in a supply chain

www.dell.com 9

Benefits of Virtual Integration

Better understand customer needs

Customers receive exactly what they want: not standard solution

Minimized inventory

New technology delivered immediately

www.dell.com 10

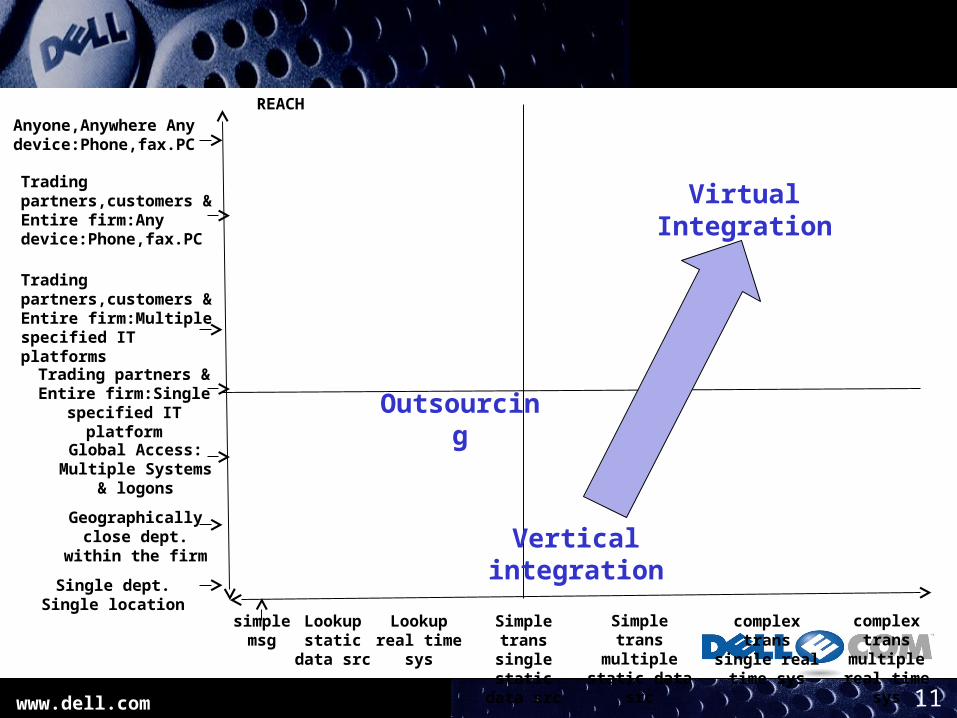

Vertical integration vs. outsourcing vs. Virtual Integration

www.dell.com 11

Single dept. Single location

Geographically close dept. within

the firm

Global Access: Multiple Systems &

logons

Trading partners & Entire firm:Single

specified IT platform

Trading partners,customers & Entire firm:Multiple specified IT platforms

Trading partners,customers & Entire firm:Any device:Phone,fax.PC

Anyone,Anywhere Any device:Phone,fax.PC

REACH

simple msg

Lookup static

data src

Lookup real time sys

Simple trans single static

data src

Simple trans multiple static

data src

complex trans single real time sys

complex trans multiple real time sys

RANGE

Vertical integration

Outsourcing

Virtual Integration

www.dell.com 12

Examples of Virtual Integration

www.dell.com 13

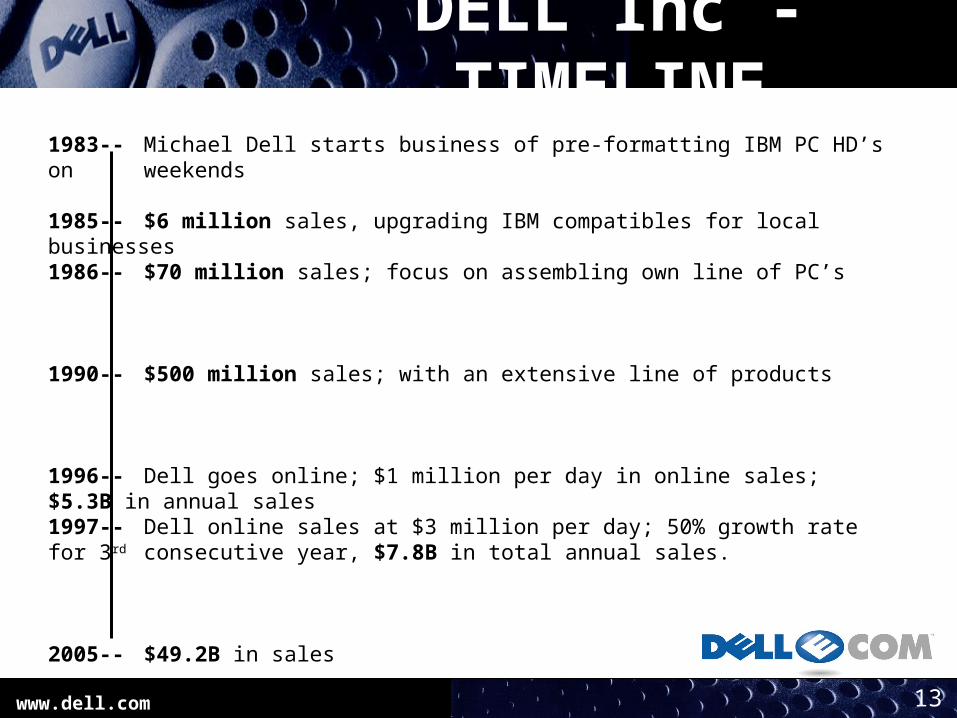

DELL Inc - TIMELINE

1983-- Michael Dell starts business of pre-formatting IBM PC HD’s on weekends

1985-- $6 million sales, upgrading IBM compatibles for local businesses1986-- $70 million sales; focus on assembling own line of PC’s

1990-- $500 million sales; with an extensive line of products

1996-- Dell goes online; $1 million per day in online sales; $5.3B in annual sales1997-- Dell online sales at $3 million per day; 50% growth rate for 3rd consecutive year, $7.8B in total annual sales.

2005-- $49.2B in sales

www.dell.com 14

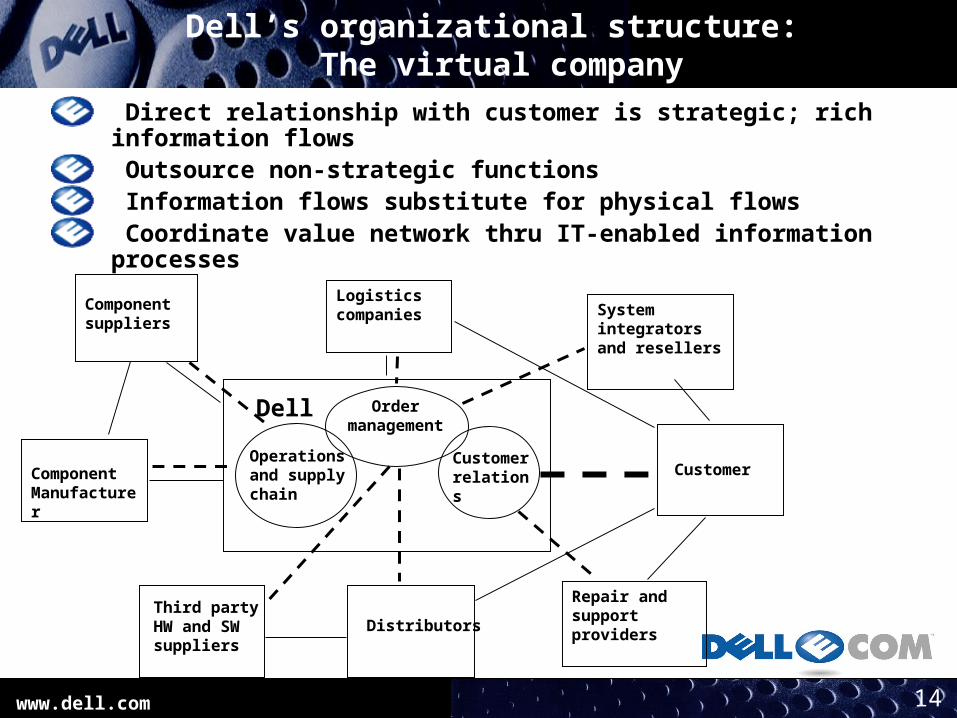

Dell’s organizational structure: The virtual company

Direct relationship with customer is strategic; rich information flows Outsource non-strategic functions Information flows substitute for physical flows Coordinate value network thru IT-enabled information processes

System integrators and resellers

Dell Order management

Customer relations

Operations and supply chain

ComponentManufacturer

Componentsuppliers

Third party HW and SW suppliers

Distributors

Logistics companies

Repair and support providers

Customer

www.dell.com 15

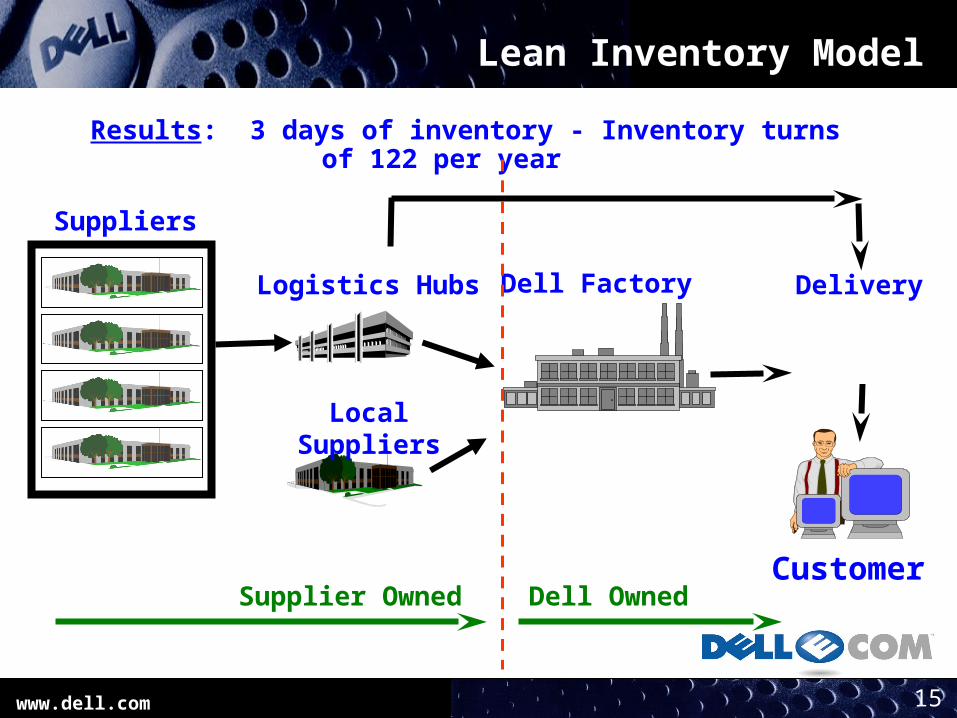

Customer

Local Suppliers

Dell Factory

Lean Inventory Model

Logistics Hubs

Suppliers

Results: 3 days of inventory - Inventory turns of 122 per year

Delivery

Supplier Owned Dell Owned

www.dell.com 16

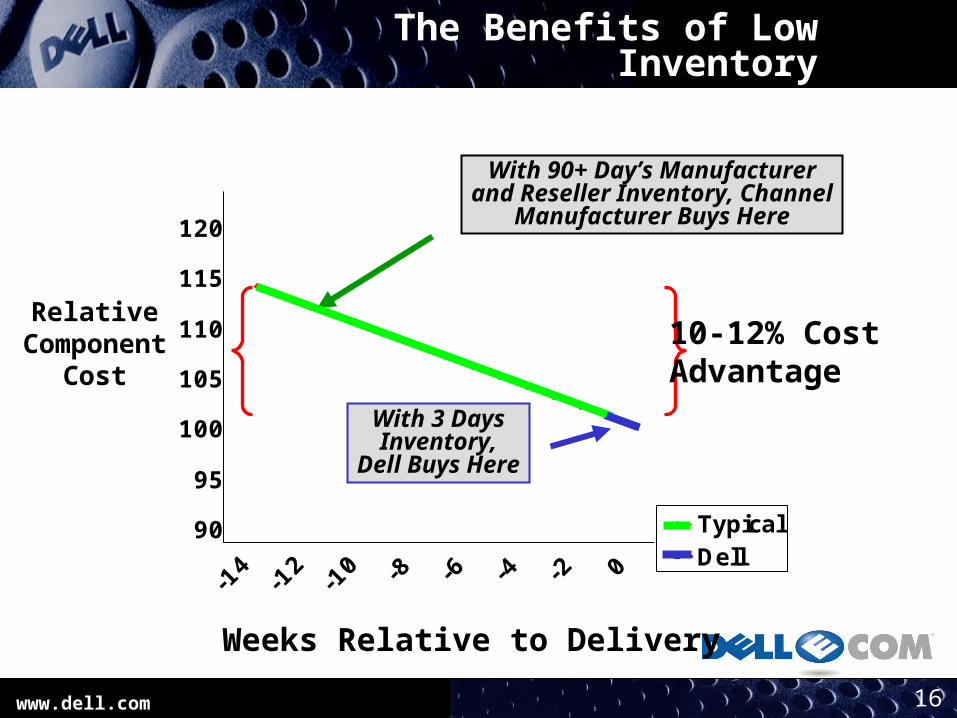

The BenefitsBenefits of Low Inventory

90

95

100

105

110

115

120

-14 -12 -10 -8 -6 -4 -2 0TypicalDell

RelativeComponent

Cost

Weeks Relative to Delivery

With 3 DaysInventory,

Dell Buys Here

With 90+ Day’s Manufacturerand Reseller Inventory, Channel

Manufacturer Buys Here

10-12% Cost Advantage

www.dell.com 17

Benefits of Virtual Integration to Dell

www.dell.com 18

Dell brings products to market faster than its competitors

• Dell uses direct sales via Internet, whereas Traditional PC manufacturers previously assemble PCs ready for purchase at retail stores.

• PCs have life cycles of only a few months

• Thus, Dell enjoys early-to-market advantage.

www.dell.com 19

Customization and quick response

• Dell• uses the Internet to sell its products• offers a virtually unlimited variety of PC

configurations.

• Buyers can click through Dell and assemble a computer system piece by piece, based on their budgets and needs

www.dell.com 20

Attract large business customers

• To facilitate B2B sales, the Dell site offers each corporate customer an individualized interface called “Premier page”• purchasing managers log on and order using an interface

customized for their company's needs

• While Dell’s consumer sales are highly visible, its business sales are a much bigger revenue source • “About 15 percent of our total revenue is consumer business and

the rest is B2B” says Bob Kaufman, Media Relations manager of Dell.

www.dell.com 21

Reduce Bullwhip Effect

• Dell constracts special Web pages for suppliers, allowing them to view orders for components they produce.

• This allows suppliers to plan based on customer demand

www.dell.com 22

Collecting the payments

• Because of direct sales, Dell can collect payments in averagely 5 days after they are sold.

• However, Dell continues to pay their suppliers according to the traditional billing schedules.

• Low level of inventory and negative working capital helps Dell increase its performance.

www.dell.com 23

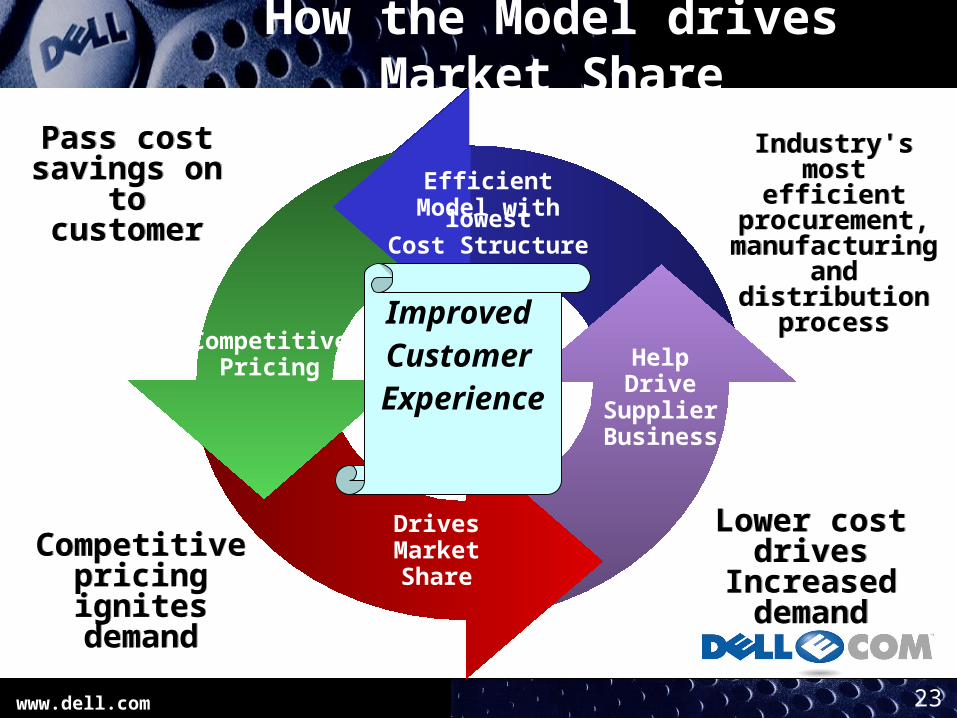

Pass cost savings on

to customer

Competitive pricing ignites demand

Lower cost drives

Increased demand

Industry's most efficient procurement, manufacturin

g and distribution

process

How the Model drives Market Share

CompetitivePricing

EfficientModel with lowest

Cost Structure

HelpDrive

SupplierBusiness

DrivesMarketShare

Improved Customer Experience

www.dell.com 24

CORDINATION WITH STRATEGIC PARTNERS

www.dell.com 25

Coordinating the virtual company with IT and e-networks

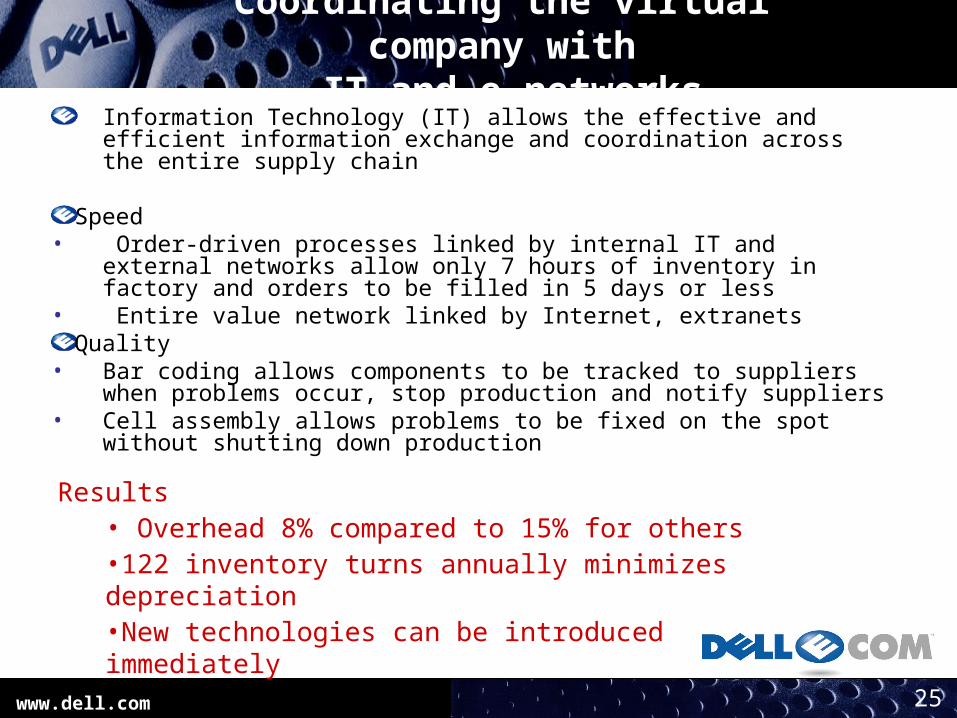

Information Technology (IT) allows the effective and efficient information exchange and coordination across the entire supply chain

Speed• Order-driven processes linked by internal IT and external networks allow

only 7 hours of inventory in factory and orders to be filled in 5 days or less• Entire value network linked by Internet, extranets

Quality • Bar coding allows components to be tracked to suppliers when problems

occur, stop production and notify suppliers• Cell assembly allows problems to be fixed on the spot without shutting

down production

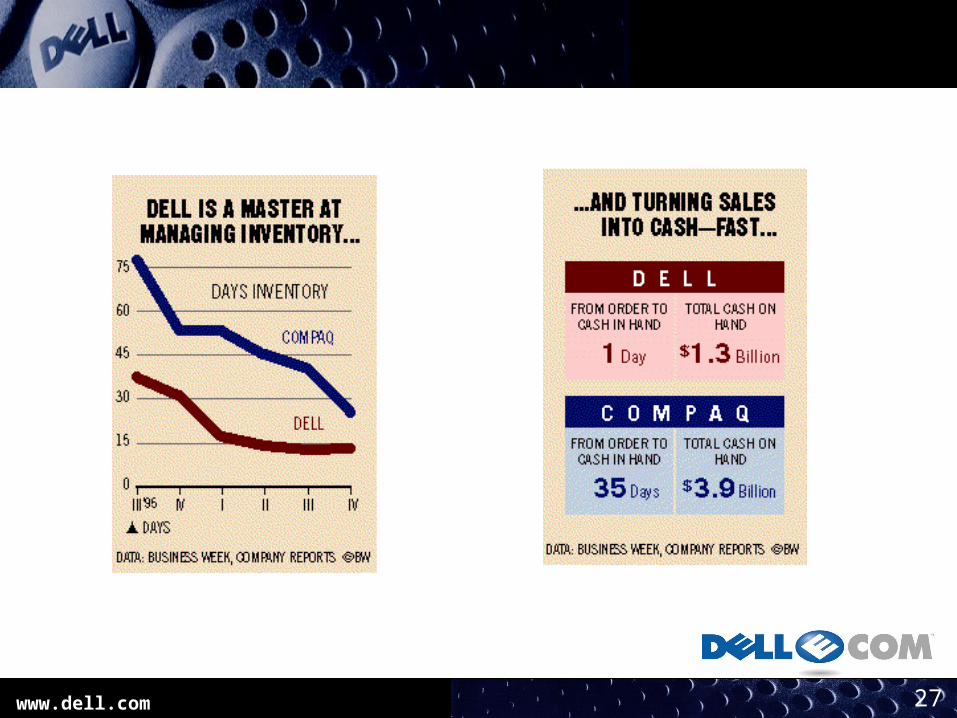

Results• Overhead 8% compared to 15% for others •122 inventory turns annually minimizes depreciation•New technologies can be introduced immediately

www.dell.com 26

DELL PERFORMANCE AS A RESULT OF VIRTUAL INTEGRATION

www.dell.com 27

www.dell.com 28

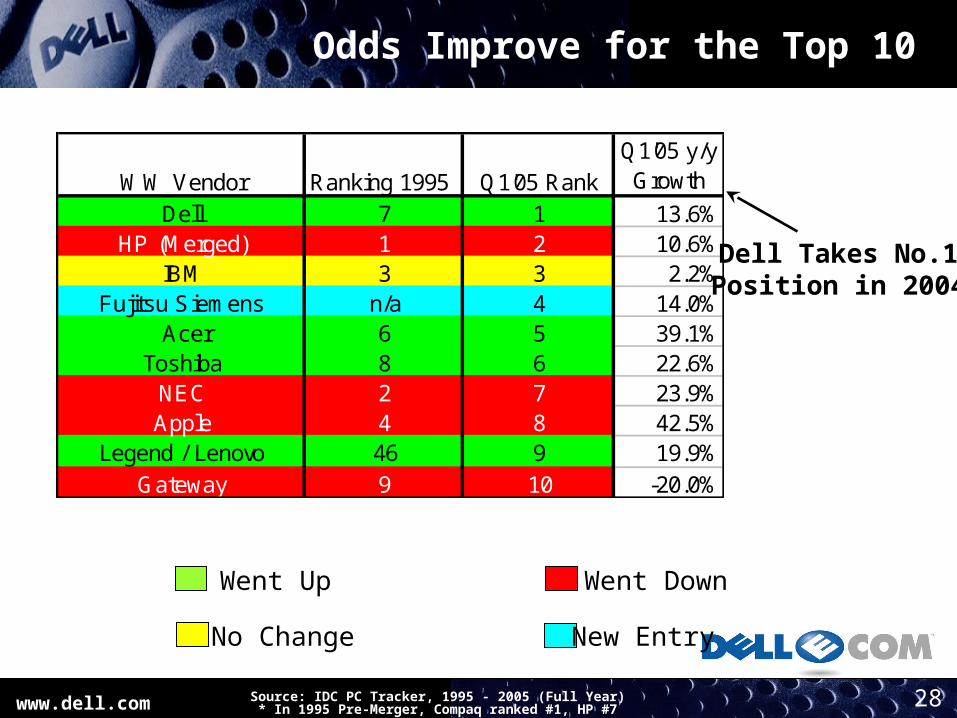

Odds Improve for the Top 10

Source: IDC PC Tracker, 1995 - 2005 (Full Year)* In 1995 Pre-Merger, Compaq ranked #1, HP #7

Went UpNo Change

Went DownNew Entry

WW Vendor Ranking 1995 Q1'05 RankQ1'05 y/y Growth

Dell 7 1 13.6%HP (Merged) 1 2 10.6%

IBM 3 3 2.2%Fujitsu Siemens n/a 4 14.0%

Acer 6 5 39.1%Toshiba 8 6 22.6%

NEC 2 7 23.9%Apple 4 8 42.5%

Legend / Lenovo 46 9 19.9%Gateway 9 10 -20.0%

Dell Takes No.1Position in 2004

www.dell.com 29(Annualized)

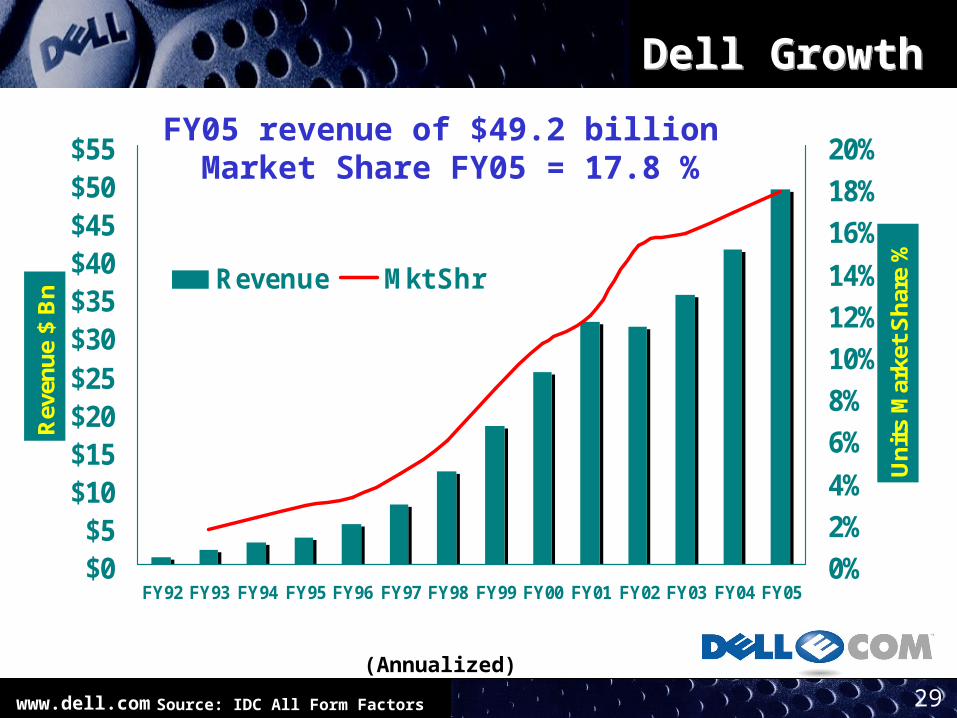

Dell Growth

$0$5

$10$15$20$25$30$35$40$45$50$55

FY92 FY93 FY94 FY95 FY96 FY97 FY98 FY99 FY00 FY01 FY02 FY03 FY04 FY05

Reve

nue

$ Bn

0%2%4%6%8%10%12%14%16%18%20%

Units

Mar

ket S

hare

%Revenue Mkt Shr

FY05 revenue of $49.2 billion Market Share FY05 = 17.8 %

Source: IDC All Form Factors

www.dell.com 30

Three golden rules at Dell : Three golden rules at Dell :

`Disdain inventory' `Disdain inventory' `Listen to the customer' `Listen to the customer'

`Never sell indirect' `Never sell indirect'

Learnings

www.dell.com 31

FORD CASE

www.dell.com 32

Introduction

Founded by Henry Ford on June 16, 1903, in Dearborn, Michigan.Second largest industrial corporation in the worldWith revenues of more than 144 billion and about 370,000 employees, operation spanned 200 countriesWorld's second largest motor vehicle manufacturer.Produces cars and trucks, and many of the vehicles plastic, glass and electronic components, and replacement parts.Core business: design & manufacture auto for sales

www.dell.com 33

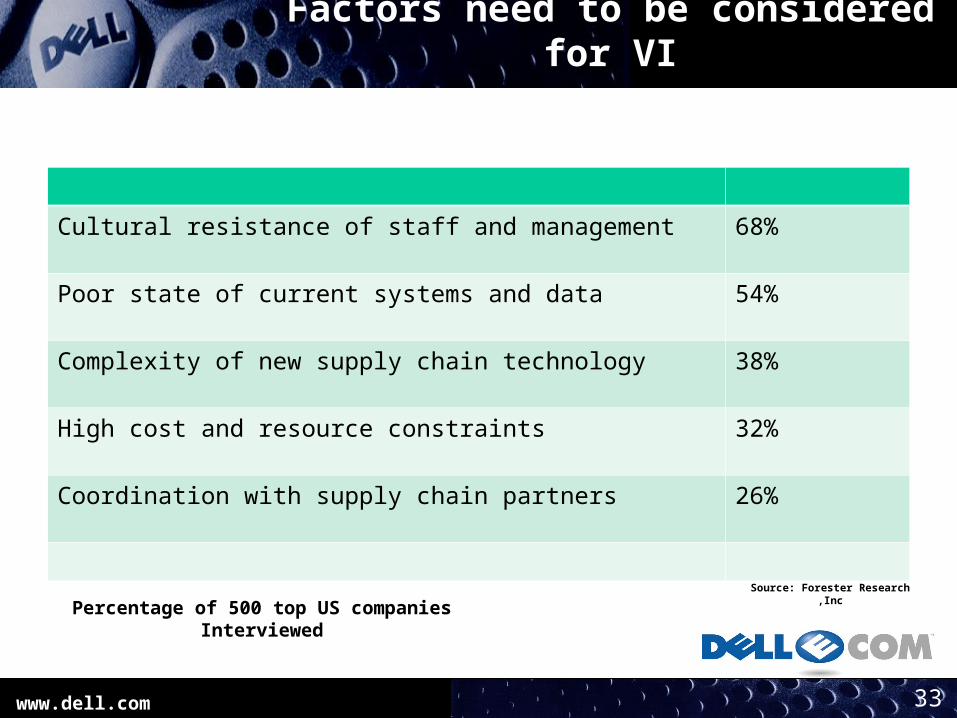

Factors need to be considered for VI

Cultural resistance of staff and management 68%

Poor state of current systems and data 54%

Complexity of new supply chain technology 38%

High cost and resource constraints 32%

Coordination with supply chain partners 26%

Source: Forester Research ,Inc

Percentage of 500 top US companies Interviewed

www.dell.com 34

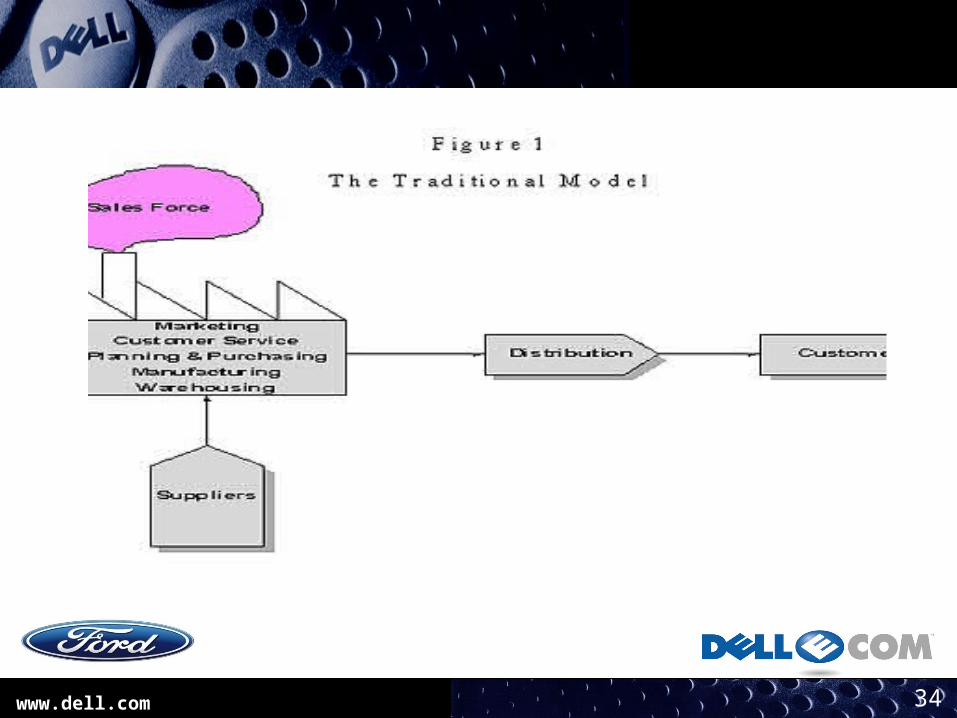

Ford Traditional supply chain model

www.dell.com 35

Problems

change to Ford's supply chain structure could also be very costly if not properly managed. Ford has a complex network of suppliers and does not have the IT knowledge cars require more components to build than a computer doesFord sells most of its cars through traditional dealerships, the selling process is not as efficient as Dell's direct sales model.Significant changes to Ford's factories, vehicle design, logistics, forecasting methods and other processes would have to be made.re-train employees to handle the new procedures and information technology.

www.dell.com 36

www.dell.com 37

Results of VI in ford

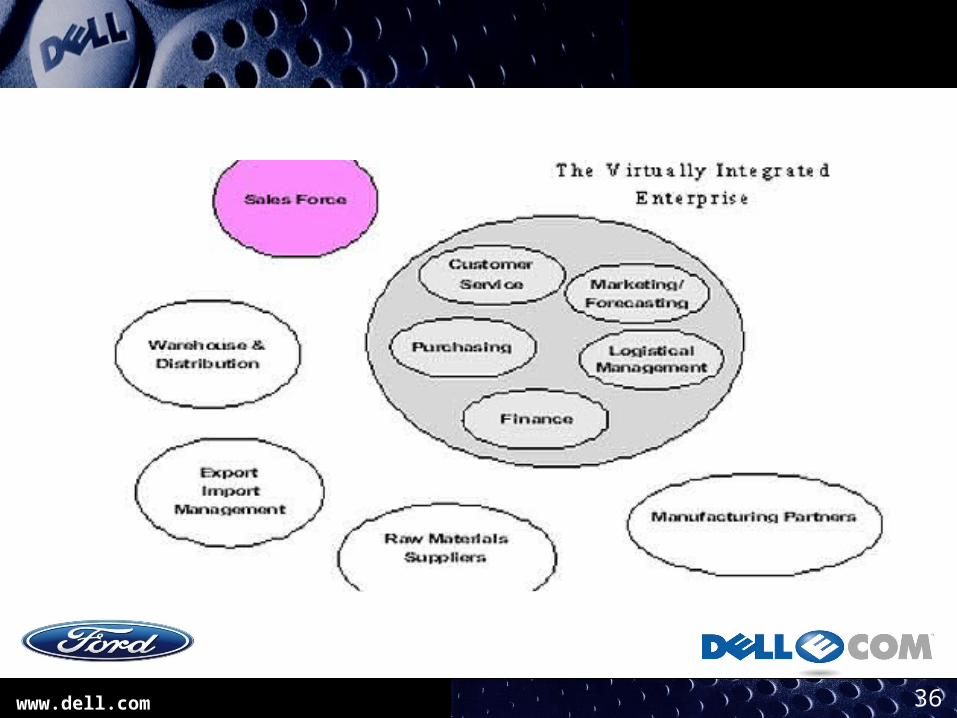

loose affiliations of companies organized as a supply networkphysical assets are replaced by information manufacturing continues to be controlled by the company’s planning departmentprovides logistics management and forecasts for demand and receiptsno longer delivers finished goods to the customersallows partners to be located far apart from each other

www.dell.com 38

Alternative solutions

The first possibility is to keep its existing supply chain as it is and not make any major changes.

To extend Ford's E-business strategy with customers and suppliers and make a partial jump towards virtual integration.

To have a total jump to a virtually integrated supply chain based completely on Dell's model.

www.dell.com 39

Benefits to ford

Strategic partnershipsDecreased holding costs,Increased flexibilityLess inventoryOpening up new ways to get vehicles to the market more quicklyTo compete with the smaller, more agile, players in the automobile market.Convenience for customers, and developing relationships with customersEnsures a continuous flow of materials and reduced buffer stock requirements.

www.dell.com 40

RECOMMENDATIONS FOR TRANSITION TO VIRTUAL ORGANIZATION

Develop strong Demand Chain to meet & exceed customer satisfactions

Better Relationship Management through out the value chain

Drive the organization for more efficiency

www.dell.com 41

Virtual Integration

Suppliers Customers

““No Boundaries”No Boundaries”

www.dell.com 42

THANK YOU