Embed Size (px)

Citation preview

Vinod Kothari

1012 Krishna224 AJC Bose RoadKolkata 700 017

222 Ashoka Shopping CenterLT RoadMumbai

www.vinodkothari.comEmail: [email protected]

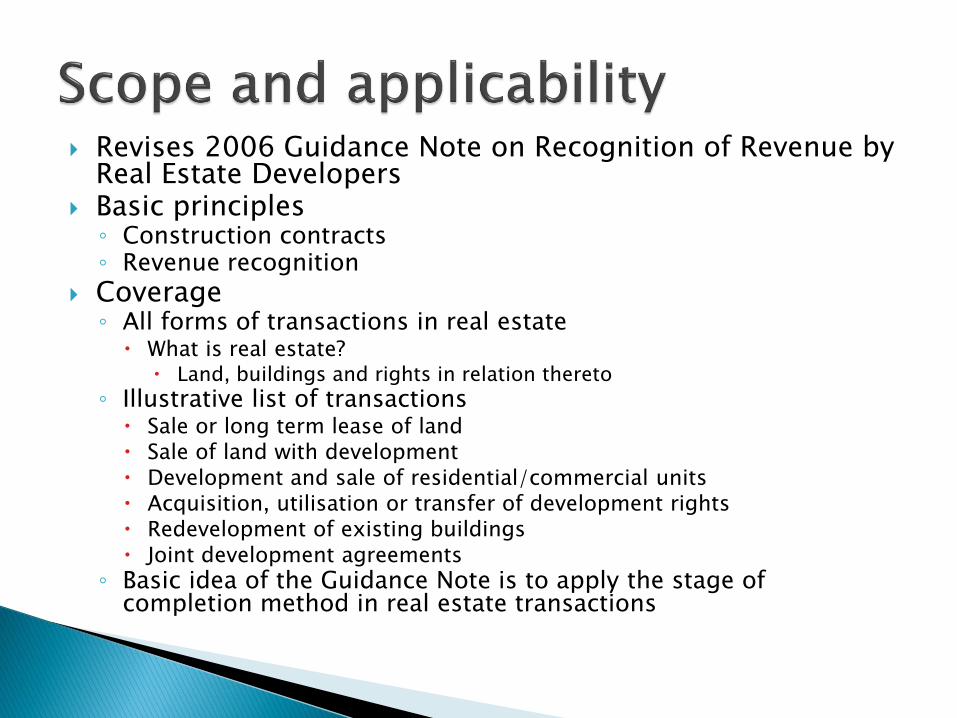

Revises 2006 Guidance Note on Recognition of Revenue by Real Estate Developers

Basic principles◦ Construction contracts◦ Revenue recognition

Coverage◦ All forms of transactions in real estate What is real estate?

Land, buildings and rights in relation thereto

◦ Illustrative list of transactions Sale or long term lease of land Sale of land with development Development and sale of residential/commercial units Acquisition, utilisation or transfer of development rights Redevelopment of existing buildings Joint development agreements

◦ Basic idea of the Guidance Note is to apply the stage of completion method in real estate transactions

Should revenue recognition be based on transfer of legal title, handing of possession or transfer of risks/rewards

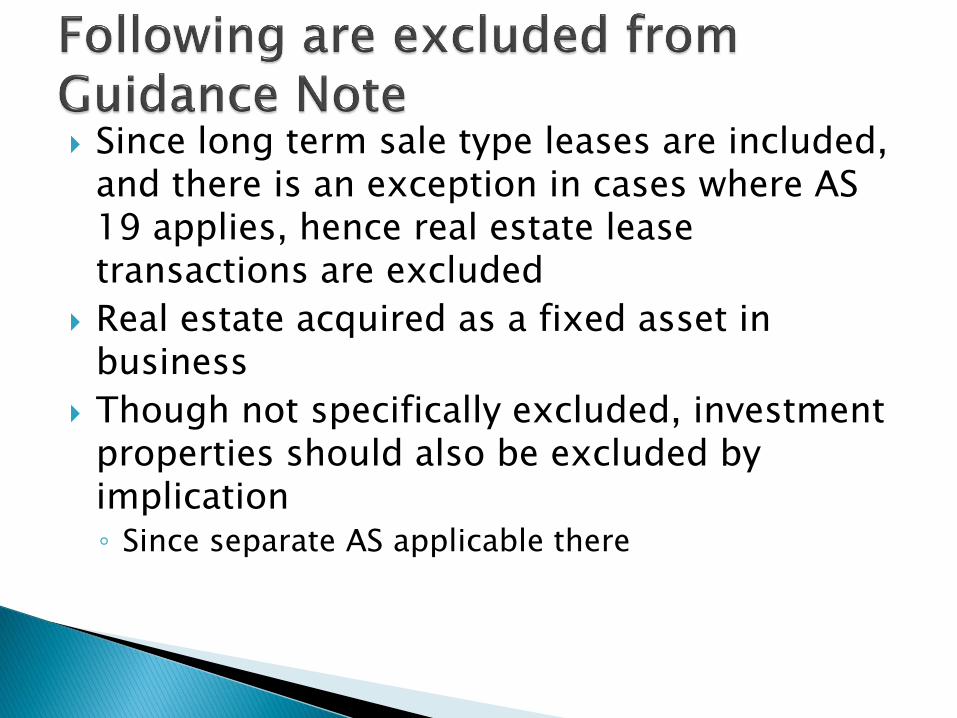

Since long term sale type leases are included, and there is an exception in cases where AS 19 applies, hence real estate lease transactions are excluded

Real estate acquired as a fixed asset in business

Though not specifically excluded, investment properties should also be excluded by implication◦ Since separate AS applicable there

All projects commenced on or after 1st April 2012◦ Since the reference is to a project –it obviously

implies construction

◦ Definition of “project” applies

Or ongoing projects where revenue is being recognised for the first time on or after 1st

April 2012

Project◦ Almost like the definition of an operating unit a smallest unit linked with a common set of amenities The common amenities are essential to put the property to

intended effective use

◦ Example A tower in a complex Common amenity is the lift, electricity, water, etc

Project cost◦ Cost of land and cost of development rights Includes stamp duty, development rights, brokerage, etc

◦ Borrowing costs As per AS 16, direct costs or apportioned costs

◦ Construction and development costs Direct costs or costs attributable to project

(a) land conversion costs, betterment charges, municipal sanction fee and other charges for obtaining building permissions;

(b) site labour costs, including site supervision; (c) costs of materials used in construction or development of property; (d) depreciation of plant and equipment used for the project ; (e) costs of moving plant, equipment and materials to and from

the project site; (f) costs of hiring plant and equipment; (g) costs of design and technical assistance that is directly

related to the project; (h) estimated costs of rectification and guarantee work, includingexpected warranty costs; and (i) claims from third parties.

(a) General administration costs;

(b) selling costs;

(c) research and development costs;

(d) depreciation of idle plant and equipment;

(e) cost of unconsumed or uninstalled material delivered at site; and

(f) payments made to sub-contractors in advance of work performed.

(a) insurance;

(b) costs of design and technical assistance that is not directly related to a specific project;

(c) construction or development overheads; and

(d) borrowing costs.

How are these costs allocated: systematic and rational basis, based on normal level of project activity

Revenues from sale of plots, undivided share in land, sale of finished and semi-finished structures,

consideration for construction, consideration for amenities and interiors,

consideration for parking spaces and sale of development rights.

Measured as consideration received or receivable

Significant estimation is required here –hence, estimates may change over time

Key to recognition of revenue is Para 11 of AS 9◦ Recognition of risks and rewards

What are risks/rewards◦ The agreement is typically for purchase of a property◦ Hence, risk is the risk of decrease in the price, reward is reward

for appreciation of the price◦ Hence, a fixed price contract presumably transfers risks/rewards

to the buyer

Agreement for sale prima facie transfers risks/rewards◦ Subject to legal enforceability – every agreement is prima facie

legally enforceable◦ Satisfaction of conditions signifying transfer of risks/rewards

Transfer of legal title or handing of possession is not necessary

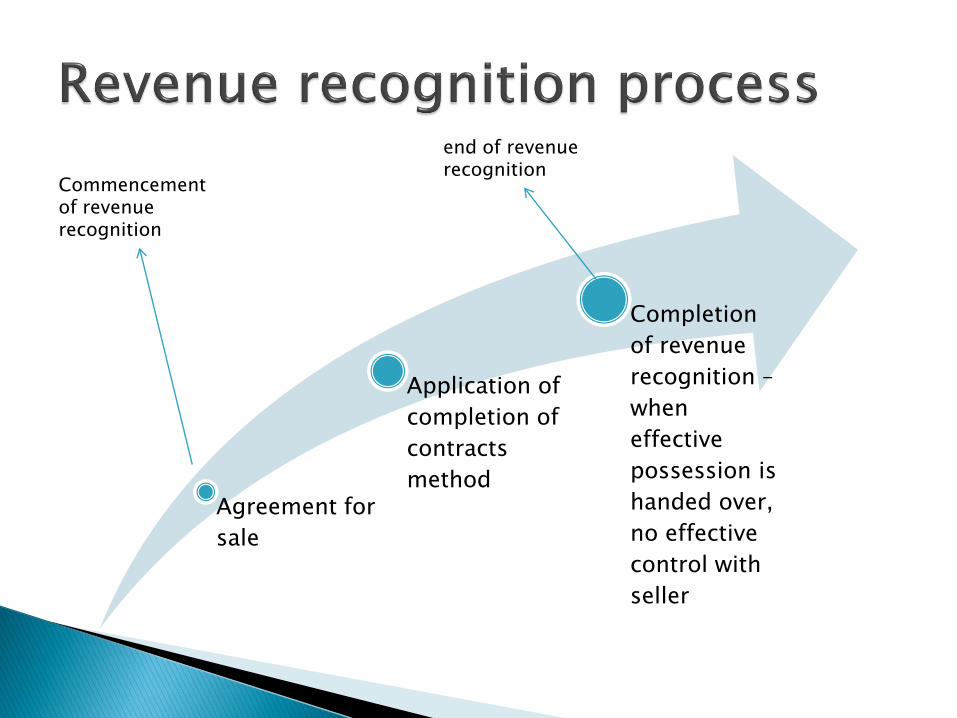

Agreement for

sale

Application of

completion of

contracts

method

Completion

of revenue

recognition –

when

effective

possession is

handed over,

no effective

control with

seller

Commencement of revenue recognition

end of revenue recognition

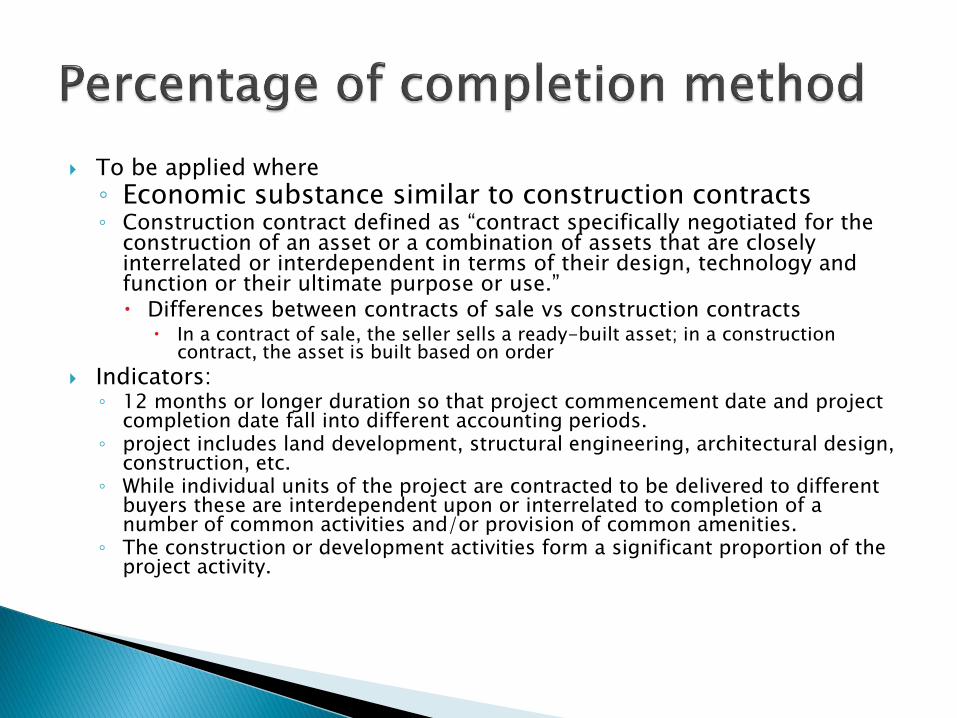

To be applied where

◦ Economic substance similar to construction contracts◦ Construction contract defined as “contract specifically negotiated for the

construction of an asset or a combination of assets that are closely interrelated or interdependent in terms of their design, technology and function or their ultimate purpose or use.” Differences between contracts of sale vs construction contracts

In a contract of sale, the seller sells a ready-built asset; in a construction contract, the asset is built based on order

Indicators:◦ 12 months or longer duration so that project commencement date and project

completion date fall into different accounting periods.◦ project includes land development, structural engineering, architectural design,

construction, etc.◦ While individual units of the project are contracted to be delivered to different

buyers these are interdependent upon or interrelated to completion of a number of common activities and/or provision of common amenities.

◦ The construction or development activities form a significant proportion of the project activity.

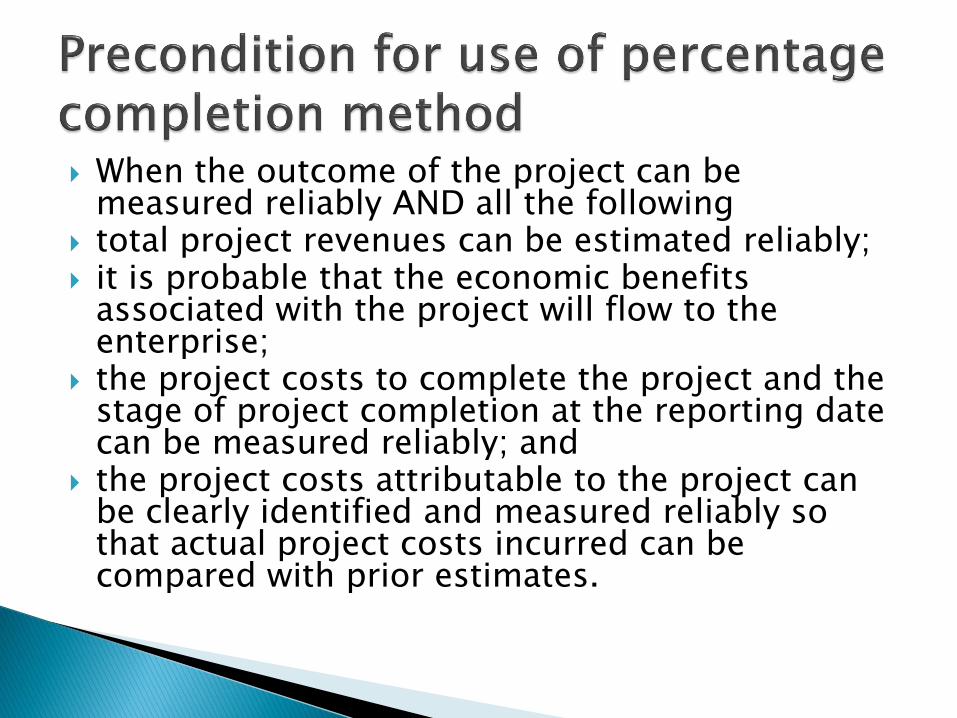

When the outcome of the project can be measured reliably AND all the following

total project revenues can be estimated reliably; it is probable that the economic benefits

associated with the project will flow to the enterprise;

the project costs to complete the project and the stage of project completion at the reporting date can be measured reliably; and

the project costs attributable to the project can be clearly identified and measured reliably so that actual project costs incurred can be compared with prior estimates.

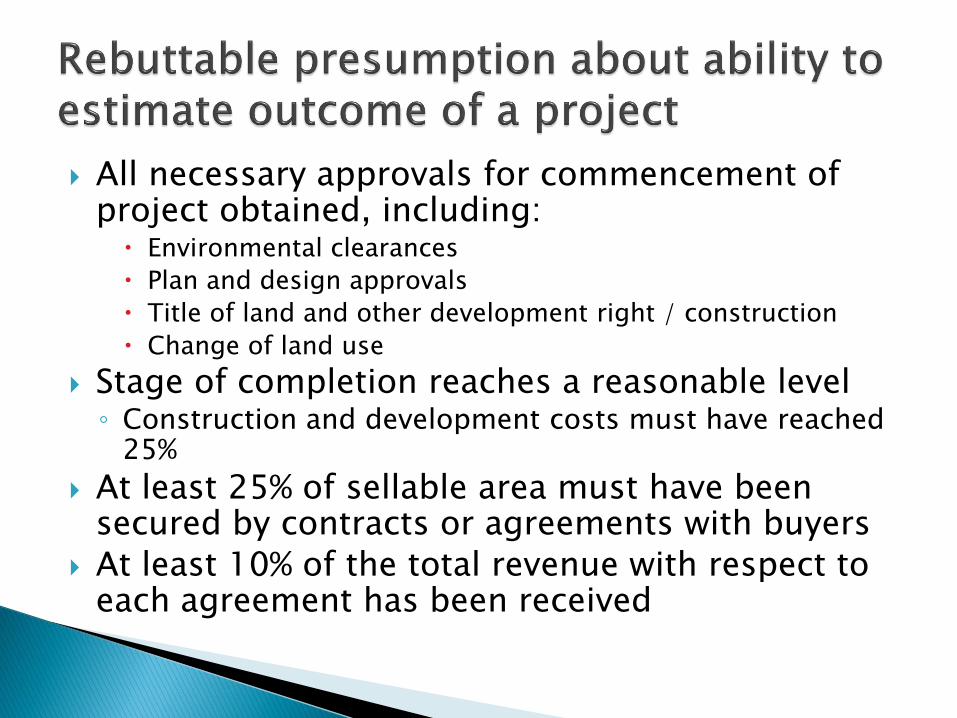

All necessary approvals for commencement of project obtained, including: Environmental clearances

Plan and design approvals

Title of land and other development right / construction

Change of land use

Stage of completion reaches a reasonable level◦ Construction and development costs must have reached

25%

At least 25% of sellable area must have been secured by contracts or agreements with buyers

At least 10% of the total revenue with respect to each agreement has been received

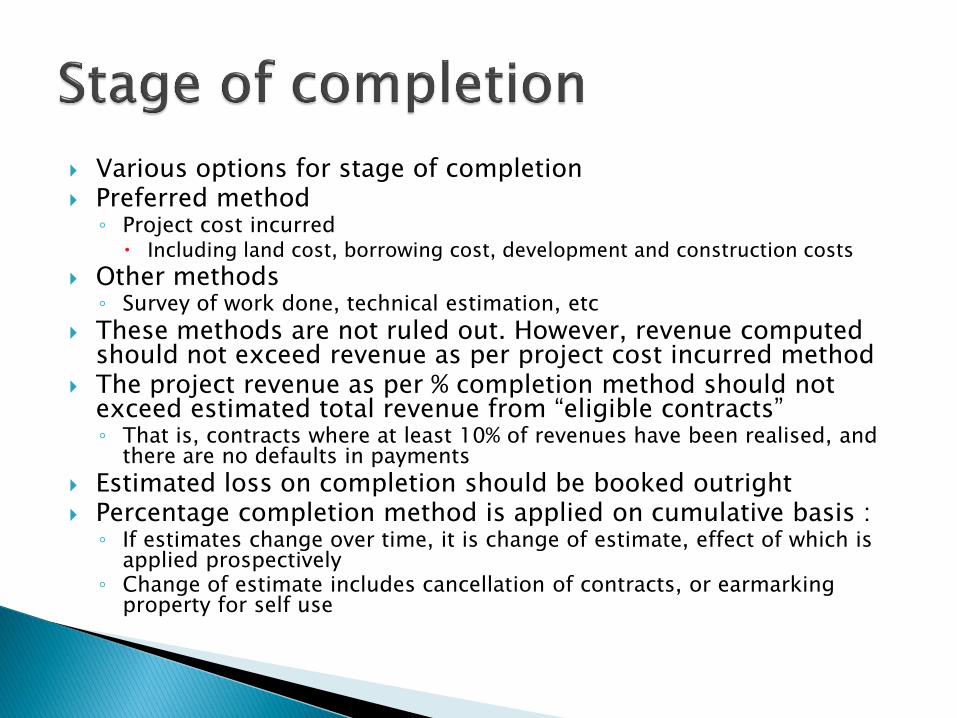

Various options for stage of completion Preferred method

◦ Project cost incurred Including land cost, borrowing cost, development and construction costs

Other methods◦ Survey of work done, technical estimation, etc

These methods are not ruled out. However, revenue computed should not exceed revenue as per project cost incurred method

The project revenue as per % completion method should not exceed estimated total revenue from “eligible contracts”◦ That is, contracts where at least 10% of revenues have been realised, and

there are no defaults in payments

Estimated loss on completion should be booked outright Percentage completion method is applied on cumulative basis :

◦ If estimates change over time, it is change of estimate, effect of which is applied prospectively

◦ Change of estimate includes cancellation of contracts, or earmarking property for self use

Revenue from sale of plot/land may be booked when risk/rewards transferred◦ That is, transfer of legal title, conveyance or

possession are not pre-requisite

In case agreement for sale of developed land, percentage completion method to be applied

Cost of acquiring TDRs should be added to the cost of construction

In case of transfer fo TDRs, revenue should be booked◦ When title is transferred

◦ It is not unreasonable to expect realisation

If there is a contract for supply of goods or services in addition to construction contract◦ Those parts will be segregated

◦ Composite consideration shall be segregated in proportion to fair market value

Revenue related disclosures:◦ the amount of project revenue recognised as revenue in the

reporting period;◦ the methods used to determine the project revenue recognised in

the reporting period; and◦ the method used to determine the stage of completion of the

project.

An enterprise should also disclose each of the following for projects in progress at the end of the reporting period:

(a) the aggregate amount of costs incurred and profits recognised (less recognised losses) to date;

(b) the amount of advances received; (c) the amount of work in progress and the value of

inventories; and (d) Excess of revenue recognised over actual bills raised

(unbilled revenue).

Accounting

Taxation◦ MAT

◦ Regular income tax

9/21/2012Free template from

www.brainybetty.com 23

IAS 11 Construction contracts

Snapshot◦ Key objective: Construction contracts normally span more than one accounting

period – hence, the costs/revenues are scattered; the standard provides for allocation of revenue/costs to the period

Scope exception

9/21/2012Free template from

www.brainybetty.com 24

Construction contract◦ Contract for construction of an asset

or group of assets that are interdependent or interrelated A contract for a group of assets should be treated as separate if separate bids

have been submitted, the contract may be accepted/rejected for any one or more assets, and costs/revenues of each may be found separately

If these conditions are not satisfied, the group contract should be taken as single contract

◦ Contract for rendering services relating to contracts such as project managers, architects, are also regarded as construction contracts

◦ Destruction/restoration contracts also included

Cost plus contract: reimbursement for all allowable costs + margin

Fixed price contract: fixed contract price or fixed price per unit of output

9/21/2012Free template from

www.brainybetty.com 25

Contract revenues◦ Initial contracted revenue◦ Variations, to the extent they are probable, and can reliably be measured E.g., impact of escalation clauses

Impact of penalties

Incentive payments – if the contract has reached a stage where incentive payment looks highly probable, and may be reliably measured

Contract costs◦ Direct costs Site labor, materials, depreciation of plant used for the contract, cost of hiring plant,

design and technical assistance, warranty costs, rectification costs, claims of third parties

◦ Costs attributable to the contract activity and can be allocated to the contract Insurance, design or technical assistance not directly on the specific contract,

construction overheads

These can be systematically allocated based on normal level of construction activity

◦ Costs that are specifically chargeable to the customer as per contract◦ Following costs are NOT included General admin costs for which reimbursement is not allowed in contract

Selling costs

R & D costs for which reimbursement is not specified in contract

Depreciation of idle plant, not used for the contract

9/21/2012Free template from

www.brainybetty.com 26

When the outcome of the contract may be measured reliably◦ Expected loss on the contract should be booked immediately◦ Revenues/costs should be split based on stage of completion

When is the outcome reliably measurable◦ In fixed price contracts: all the following The contract revenue can be measured reliably

Economic benefits from the contract (that is, consideration) will flow to the entity

Costs to complete the contract and the stage of completion can be measured reliaby

Actual contract costs can be compared with estimated costs

◦ cost plus contracts, all the following Economic benefits from the contract (that is, consideration) will flow to the entity

Contract costs that are reimbursable may reliably be measured

If the outcome of the contract is not reliably measurable◦ Revenues should be recognised only to the extent of the costs◦ Expected loss should be expensed straightaway

When the uncertainties that prevented the contract from being recognised on the percentage completion method cease to exist, the contract should be accounted using percentage completion method

9/21/2012Free template from

www.brainybetty.com 27

Depending on the contract, the stage of completion may be found based◦ Percentage of construction cost incurred

◦ Survey

◦ Physical completion

9/21/2012Free template from

www.brainybetty.com 28

As per AS 16 (4) (e), to the extent foreign currency differences are treated as adjustment of borrowing cost, they are a part of borrowing cost◦ Borrowing cost attributable to acquisition,

construction or production of a qualifying asset to be capitalised

ASI 10 clarifies that to the extent the foreign currency borrowing cost is cheaper than domestic currency, the loss on exchange rates is adjustment to borrowing cost

9/21/2012Free template from

www.brainybetty.com 29

Foreign operations are◦ Integral◦ Non-integral

Integral operations are like an extension of the enterprise – it simply acts as a postman◦ Its activities are so organised that they have an immediate

effect on the cashflows of the reporting enterprise◦ Integral enterprises typically do not hold cash or assets

Non integral operations are those that have their own individual assets/liabilities◦ Hence, there is no direct effect on change in the value of

the assets/liabilities of non-integral operation on the reporting enterprise

9/21/2012Free template from

www.brainybetty.com 30

The activities of the foreign operation are carried out with a significant degree of autonomy

transactions with the reporting enterprise are not a high proportion of the foreign operation’s activities;

the activities of the foreign operation are financed autonomously

Operating exps and other components of the foreign operation’s products or services are primarily paid or settled in the local currency rather than in the reporting currency;

the foreign operation’s sales are mainly in currencies other than the reporting currency;

cash flows of the reporting enterprise are insulated from the day-to-day activities of the foreign operation

sales prices for the foreign operation’s products are not primarily responsive on a short-term basis to changes in exchange rates but are determined more by local competition or local government regulation

there is an active local sales market for the foreign operation’s products,

9/21/2012Free template from

www.brainybetty.com 31

Assets and liabilities at closing rates Incomes and exps at the rates (or average

rates) prevailing at the timing of such incomes/exps

All resulting foreign exchange differences should be accumulated in a foreign currency translation reserve, until disposal of foreign operations

Incorporation of a foreign operation into domestic operation follows consolidation principles