Embed Size (px)

Citation preview

VIMO SEWA SEWA’S MICROINSURANCE PROGRAMME

FOR WOMEN WORKERS OF THE INFORMAL ECONOMY

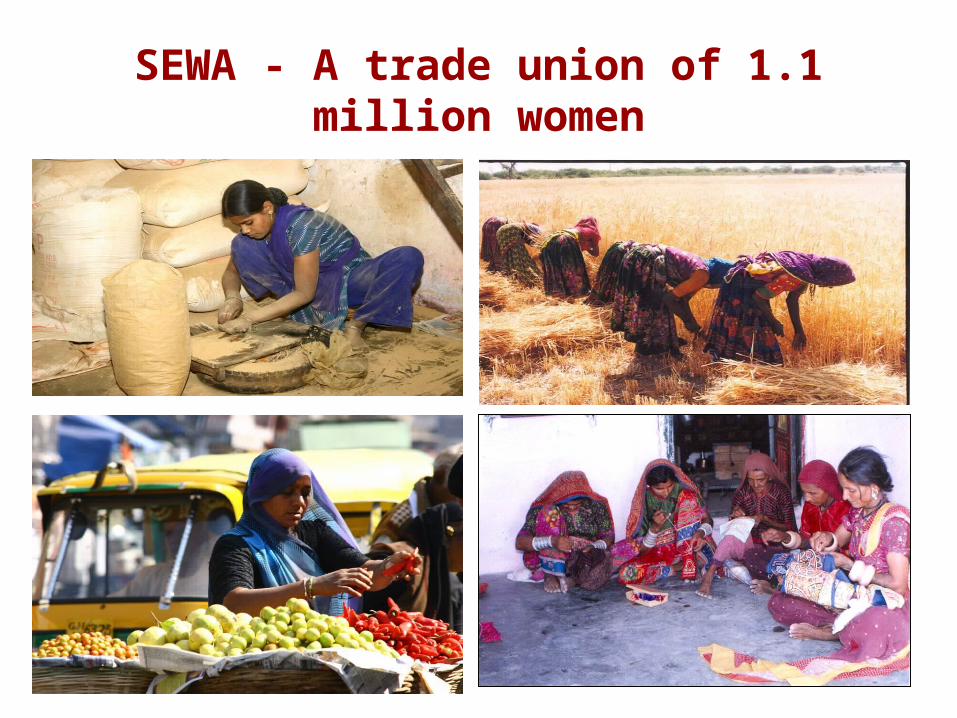

SEWA - A trade union of 1.1 million women

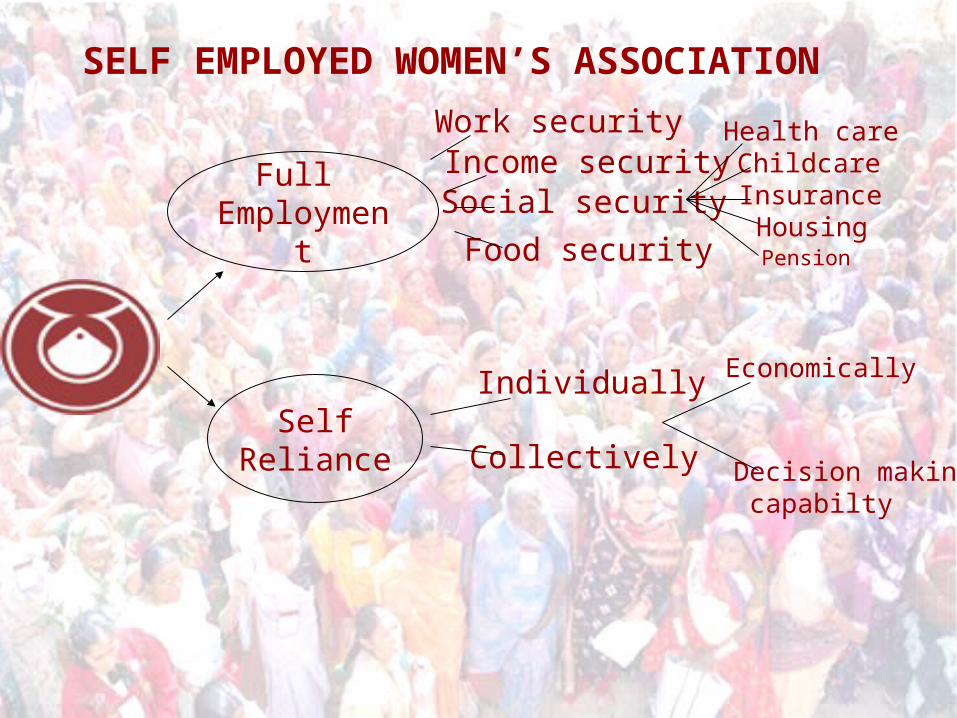

Full Employme

nt

SelfReliance

Work securityIncome securitySocial security

Food security

Individually

Collectively

Economically

Decision making capabilty

Health careChildcareInsuranceHousing

SELF EMPLOYED WOMEN’S ASSOCIATION

Pension

History of VIMO SEWA

• Started in 1992 from SEWA Bank• Collaborated with insurance companies from

start.• Need based composite package for women• Initially insured 7000 members of SEWA• Evolved according to the needs of insured

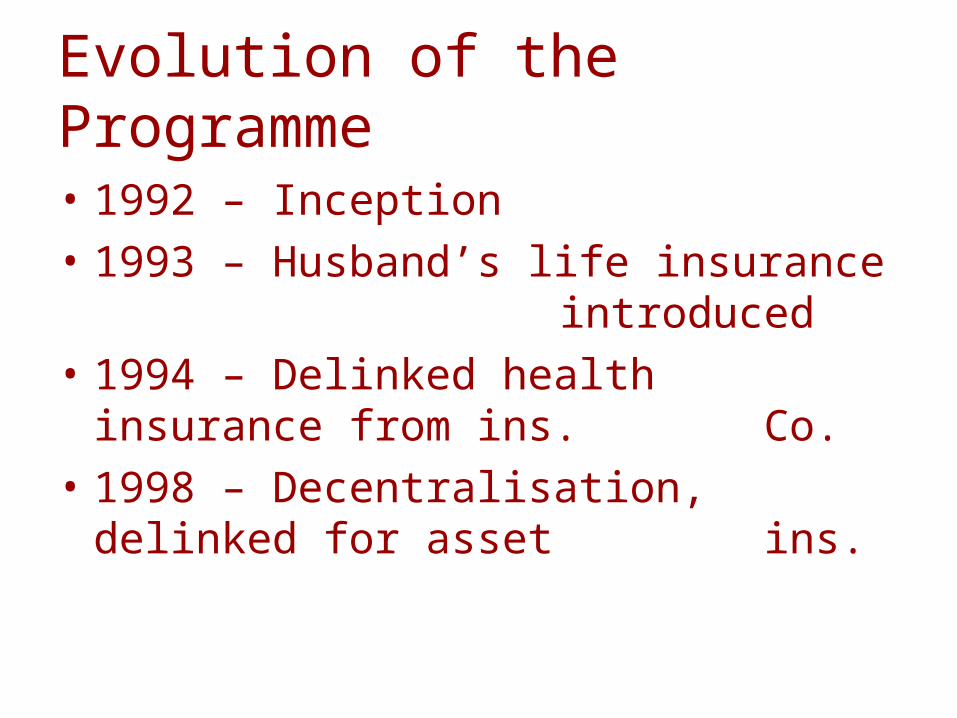

Evolution of the Programme

• 1992 – Inception

• 1993 – Husband’s life insurance introduced

• 1994 – Delinked health insurance from ins. Co.

• 1998 – Decentralisation, delinked for asset ins.

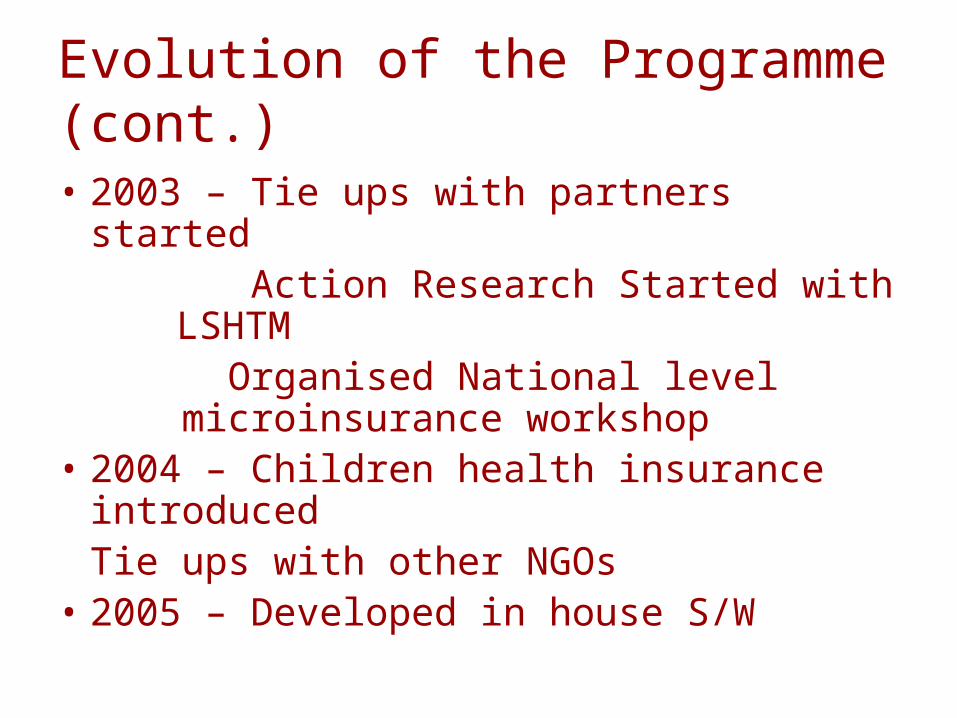

Evolution of the Programme (cont.)

• 1999 – A separate, autonomous unit, Vimo SEWA formed, plan for insurance cooperative

• 2000 – Husband’s health insurance started, expansion out of Gujarat

• 2001 – High increase in membership, linkages with insurance co. again for non life ins.

• 2002 – Computerisation started

Evolution of the Programme (cont.)

• 2003 – Tie ups with partners started Action Research Started with

LSHTM Organised National level microinsurance workshop

• 2004 – Children health insurance introduced

Tie ups with other NGOs• 2005 – Developed in house S/W

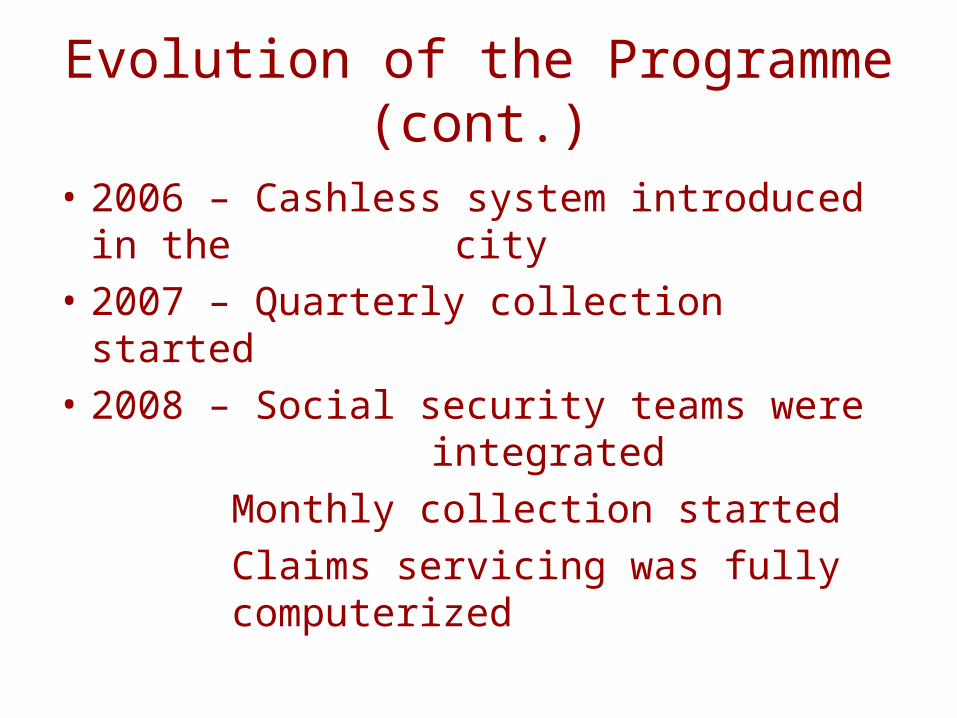

Evolution of the Programme (cont.)

• 2006 – Cashless system introduced in the city

• 2007 – Quarterly collection started

• 2008 – Social security teams were integrated

Monthly collection started

Claims servicing was fully computerized

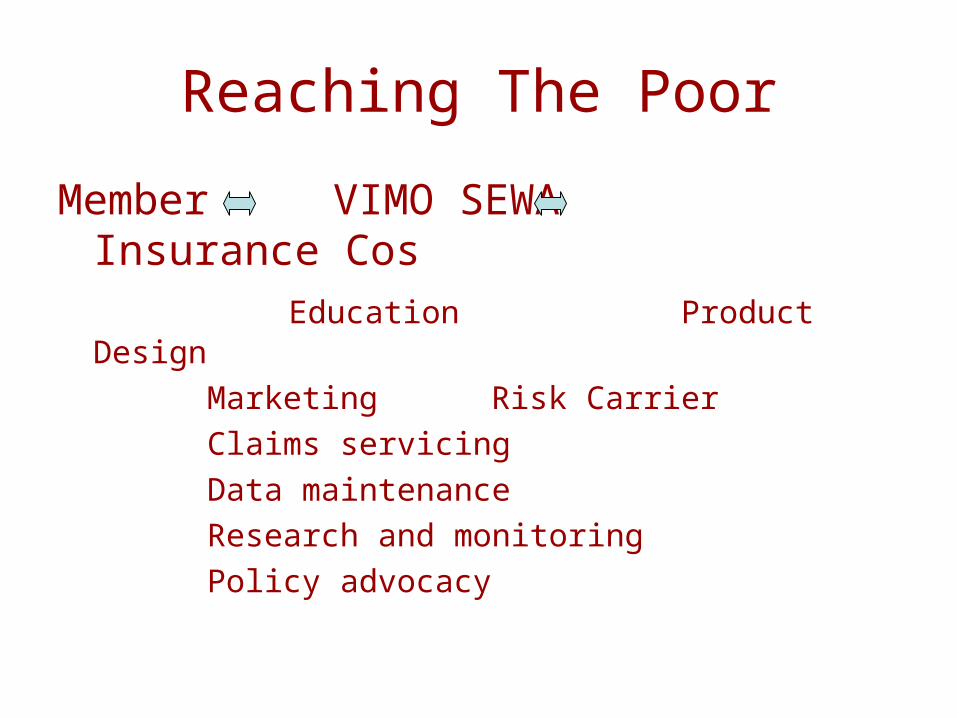

Reaching The Poor

Member VIMO SEWA Insurance Cos Education Product Design

Marketing Risk Carrier

Claims servicing

Data maintenance

Research and monitoring

Policy advocacy

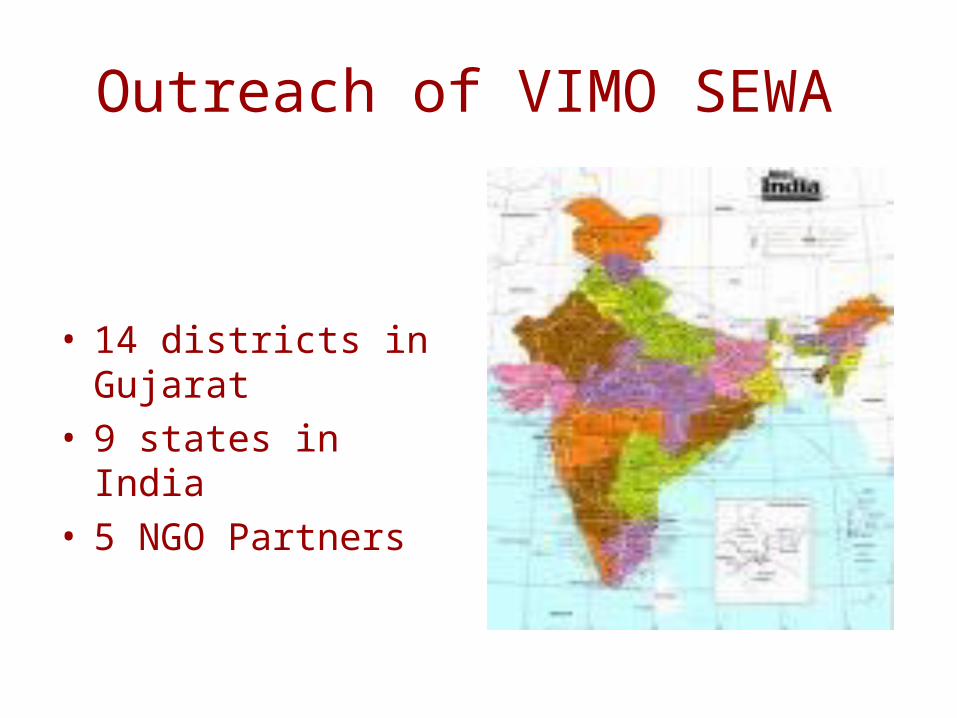

Outreach of VIMO SEWA

• 14 districts in Gujarat• 9 states in India• 5 NGO Partners

Current membership

• Women: 63,386• Men : 19,252 • Children: 18,926

• Total : 1,01,564

Current Products of VIMO SEWA

• Life

• Health

• House and Assets

• Accident

• Rainfall

• 17 schemes

Premium CollectionPremium Collection

- House-to-house

- Through self-help groups

-Annual – quarterly – monthly

Fixed deposit

Annual pay

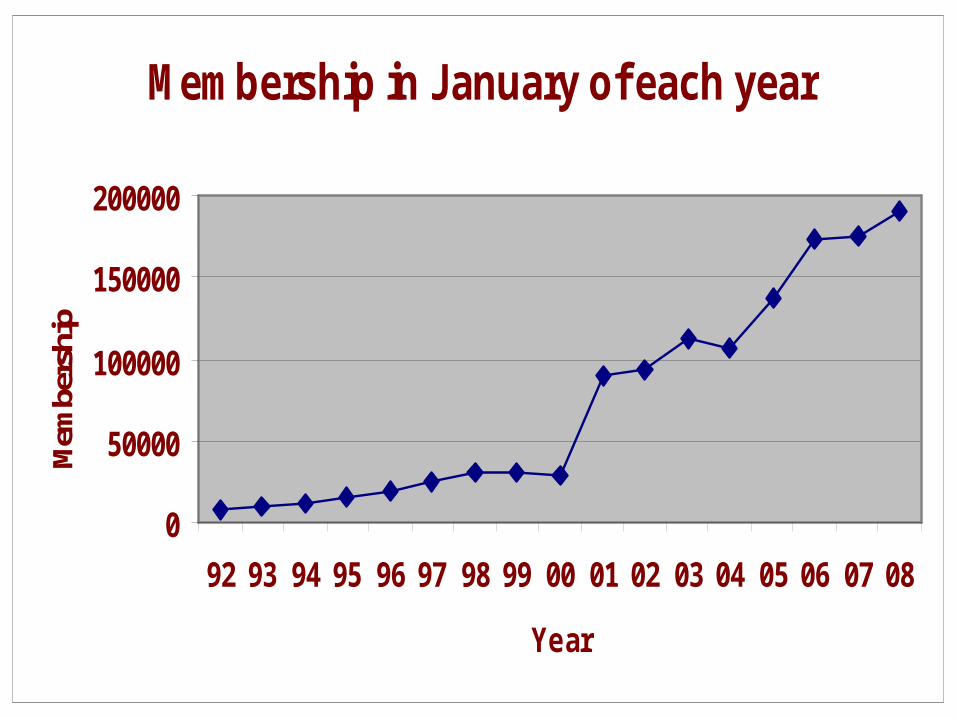

Membership in January of each year

0

50000

100000

150000

200000

92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

Year

Mem

bers

hip

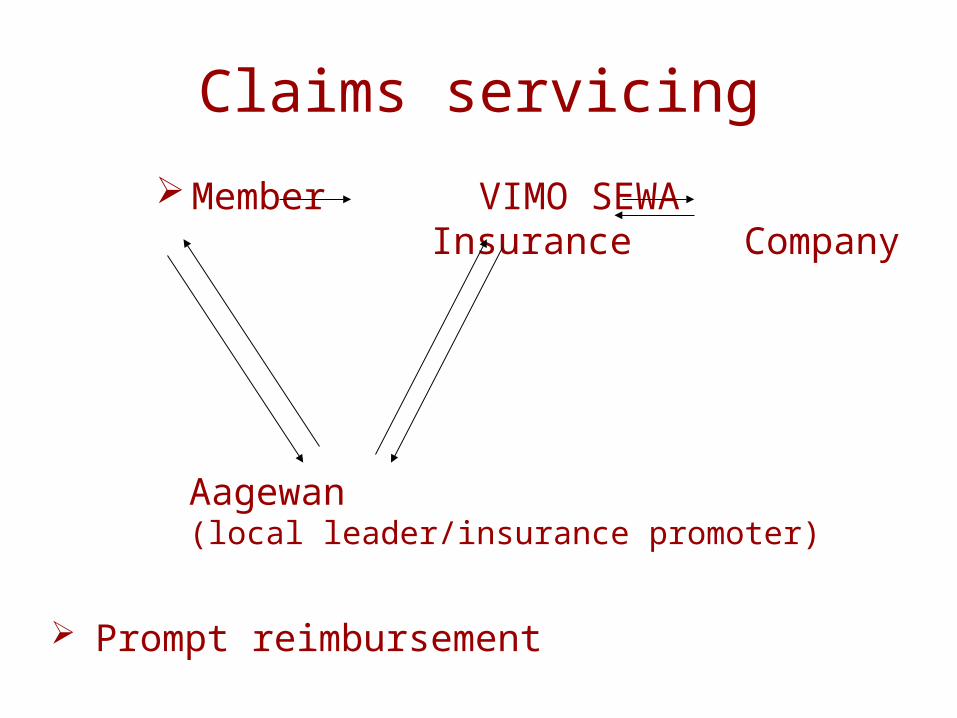

Claims servicing

Member VIMO SEWA Insurance Company

Aagewan(local leader/insurance promoter)

Prompt reimbursement

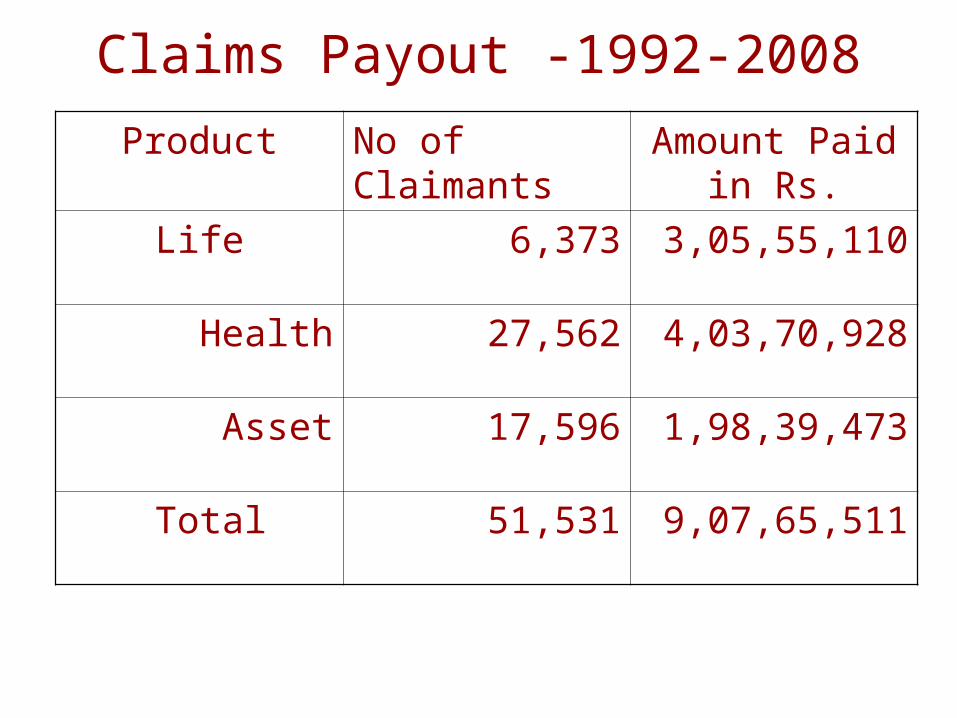

Claims Payout -1992-2008

Product No of Claimants Amount Paid in Rs.

Life 6,373 3,05,55,110

Health 27,562 4,03,70,928

Asset 17,596 1,98,39,473

Total 51,531 9,07,65,511

Lessons Learned

• Working with Insurance Cos Life : LIC, AVIVA,OMKM, Bajaj Allianze General : UIIC, NIA, NIC, ICICI, Reliance

• Effective Tools for collaboration with Insurance Cos :Credibility of the organisationSystems and mechanisms Human resourcesTransparency

Lessons Learned (cont.)• Life : simple term policy is

easy to operate Endowment product requires

long term commitment, complex

• Health : Linkage with health programme enhances the viability of the programme

• It creates demand for government health services

• It increases health seeking behavior amongst poor specially women

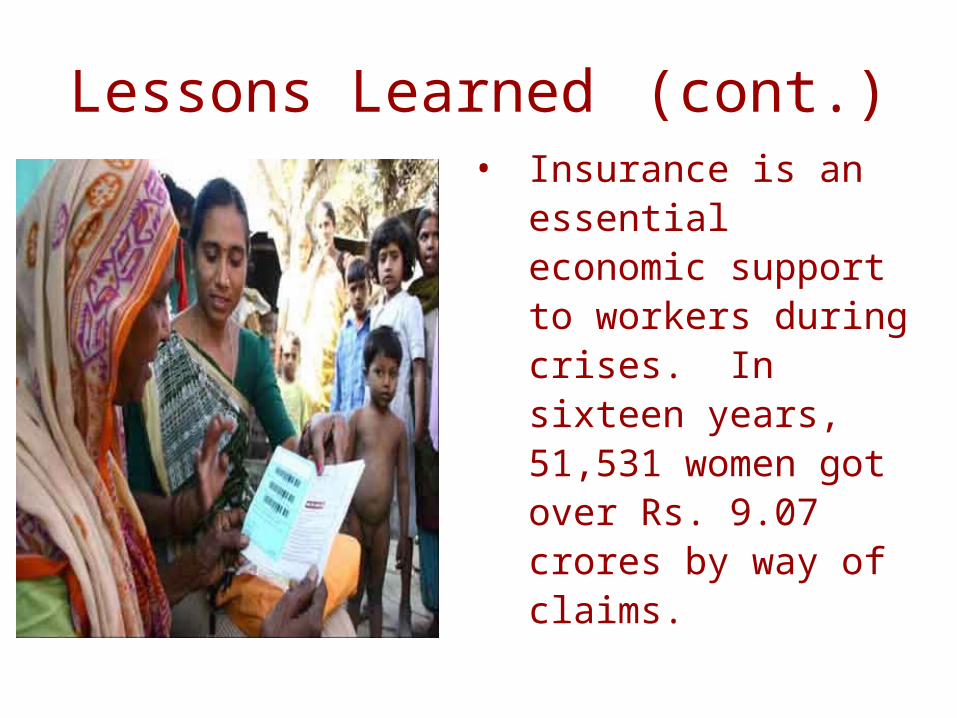

Lessons Learned (cont.)• Insurance is an

essential economic support to workers during crises. In sixteen years, 51,531 women got over Rs. 9.07 crores by way of claims.

Lessons Learned (cont.)

• Need based, affordable, bundled products

• Community based doorstep and one window quality service

• Linkages with other services and economic activities

• Linking insurance to other financial services (savings and credit) promotes long-term insurance coverage

Lessons Learned (cont.)

• Insurance by and for workers,

encourages their organizing and

contributes to their economic security.

• A combination of increased outreach

(especially to families and entire

communities), increased renewals and

cost containment leads to viability.

Challenges

1. Viability – which depends on: • Increasing Outreach • Spreading risk (other states), • Family coverage, deepening• Cost reduction

2. Education3. Product development4. Balance between social and business

objective

Future Action

• Increase outreach

• Work with MFIs, NGO partners

• Partner with government’s health programme. (RSBY)

• Multi-state cooperative (VimoSEWA) with reduced capital requirement