Embed Size (px)

Citation preview

m^4

VILLAGE OF SIMPSON

Financial Slalcmcnls

Year Ended June 30, 2012

Unc'er p-ovis.ons z\ s*aie iaw ihis lepoa is a pLiblic document Acopy of the report has been subi-nitted to the entity and other app/opriate p!.:b)(C ox\\c\a\'̂ The report is available for public inspection at tiie Baton Rouge office of the Legislative Auditor and where appropriate at the office of ihe parish clerk of court

FEB 0 6 2013 Release Date

TABLE OF CONTENTS

Independent Auditor's Report 1 - 2

BASIC FINANCIAL STATEMENTS 3

GOVERNMENT-WIDE FINANCIAL STATEMENTS (GWFS) 4

Statement of net assets 5

Statement ol activities 6

FUND FINANCIAL STATEMENTS (FFS) 7 - 8

Balance sheet - governmental funds 9

Rcconcilialion ol llie governmental funds balance sheet to the statement of net asscls 10

Statement of revenues, expenditures, and changes in fund balances - governmental funds 11

Reconciliation ol the stalement of revenues, expenditures, and changes in fund balances

lo the statement of activities 12

Statement ol nel asscls - proprietary funds 13

Stalement ol revenues, expenditures, and changes in fund nel assets - proprietary funds 14

Stalement ol cash Hows - proprietary lunds 15

Notes lo basic financial statemenls 16 - 27

INTERNAL CONTROL, COMPLIANCE AND OTHER MATTERS 28

Report on Internal Control Over Financial Reporting and on Compliance and

Other Mailers Based on an Audit of Financial Statements Performed in Accordance

wah Government Aiuhtifify Standards 29 - 30

Summary schedule of current and prior year audit findings and management's

corrective action plan 31 - 33

ELLIOTT & ASSOCIATES, INC. A Professional Actoiintin}^ Corporation

P O Box 1287

LeesviIIe, Louisiana 71496-1287

(•̂ 37) 239-2S3S W Mitlical lilholi, CPA

(337)238-SnS

Tax 239-2295

INDEPENDENT AUDITOR'S REPORT

The Honorable Roger Bennett, Mayor and Members of the Board ol Aldermen

Village of Simpson

1 have audited the accompanying financial statements ol ihe governmental activities, the business-type activiiies and each major fund of the Village ol Simpson (ihe Village), as of and for Ihe year ended June 30, 2012, which collectively comprise the Village's basic financial statements, as listed m the table of contents These linancial statemenls arc the responsibility of the Village of Simpson's management My responsibility is lo express an opinion on these basic financial slatemenls based on my audit

I conducted my audit in accordance with auditing standards generally accepted in the United States of America and ihe standards applicable lo financial audits contained in Government Auditing Standards, issued by the Complroller General of Ihe United Stales Those standards require ihat I plan and perform the audit to obtain reasonable assurance about whether the basic financial stdtements are free of material misstatement An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial slalcmcnls An audit also includes assessing the accounting principles used and the significant estimales made by managemenl, as well as evaluating the overall basic fmancial statement presentation 1 believe that my audit provides a reasonable basis lor my opinion

In my opinion, the linancial slatemenls referred to above present lairly, in all material respects, the respective linancial position of the governmental activities, the business-type activiiics, and each major lund ol ihc Village of Simpson as ot June 30, 2012, and the respective changes in linancial pt>silu>n, and, where applicable, cash flows for the year then ended in conformity with accounting principles generally accepted in the United Stales of America

In accordance wiih Government Auditing Standards, I have also issued my repv r̂l dated December 17, 20J2 on my consideration of the Village of Simpson's internal control over financial reporting and my tests of Its compliance with certain provision ol laws, regulations, contracts, and grants The purpose ol that report is to describe the scope ol my testing of internal control over financial reporting and compliance and the results ol that testing, and not to provide an opinion on internal control over financial reporting or on compliance That report is an integral part of an audit performed in accordance with Government Auditing Standards and should be read in conjunction with this report in considering the result of my audit

Management has not presented management's discussion and analysis and budgetary comparison information that governmental accounting principles generally accepted in the United States of America require to be presented to supplement the basic financial statements Such missing inlormalion, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or histoncal context My opinion on ihe basic financial statemenls is not affected by this missmg information

LeesviIIe, Louisiana

December 17,2012

BASIC FINANCIAL STATEMENTS

GOVERNMENT-WIDE FINANCIAL STATEMENTS (GWFS)

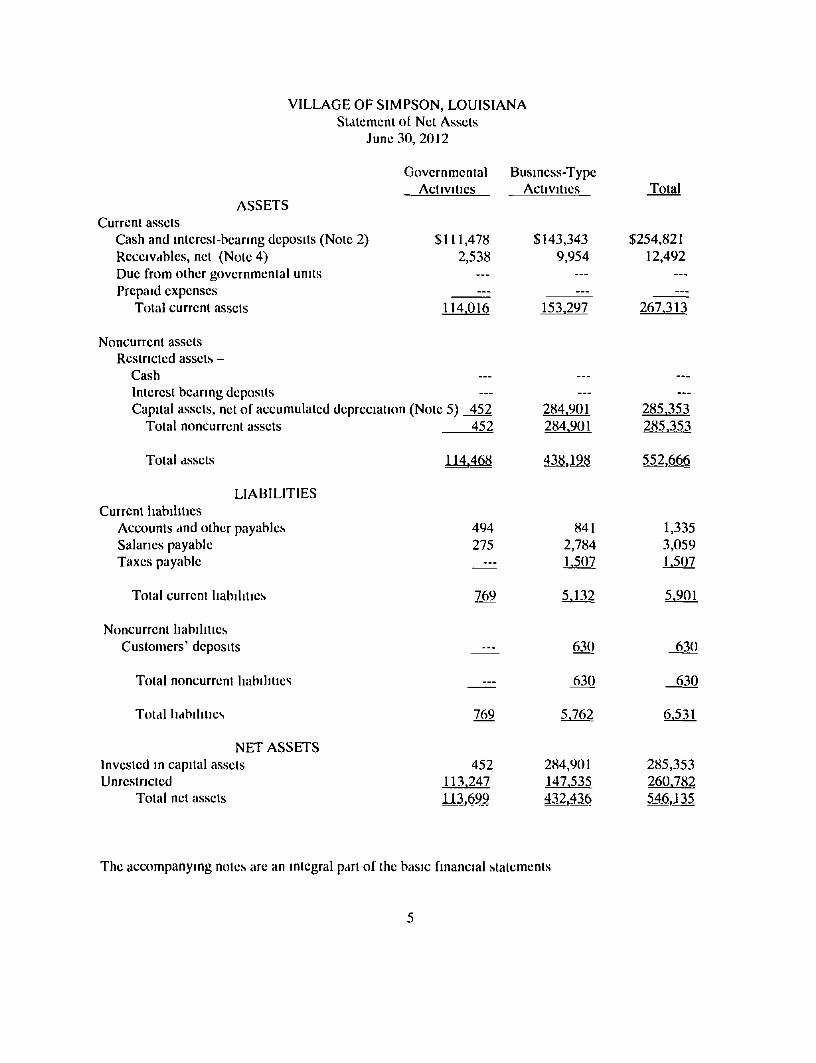

VILLAGE OF SIMPSON, LOUISIANA Statement ot Net Assets

June 30, 2012

ASSETS Current assets

Cash and interest-bearing deposits (Note 2) Receivables, nel (Note 4) Due from other governmental units Prepaid expenses

Total current assets

Governmental Activities

$111,478 2,538

— —

114,016

Business-Type Activities

$143,343 9,954

— —

153,297

Total

$254,821 12,492

— —

267,313

114,46M

Noncurrent asscls Restricted assets -

Cash Inlerest bearing deposits Capital assets, net of accumulated depreciation (Note 5) 452

Total noncurrent assets 452

Total assets

LIABILITIES Current liabilities

Accounts and other payables Salaries payable Taxes payable

Total current liabilities

Noncurrent liabilities Customers' deposits

Total noncurrent liabilities

Total liabilities

NET ASSETS Invested in capital assets Unrestricted

Total net assets

284,901 284,901

43.8,19.8

285.353 285,353

5.5.2,6_6_6

494 275

769

—

—

769

452 113,247

841 2,784 1,507

5,132

630

630

5,762

284,901 147,535 432,436

1,335 3,059 1,507

5,901

630

630

6,531

285,353 260,782 546,J35.

The accompanying notes are an integral part of the basic financial statements

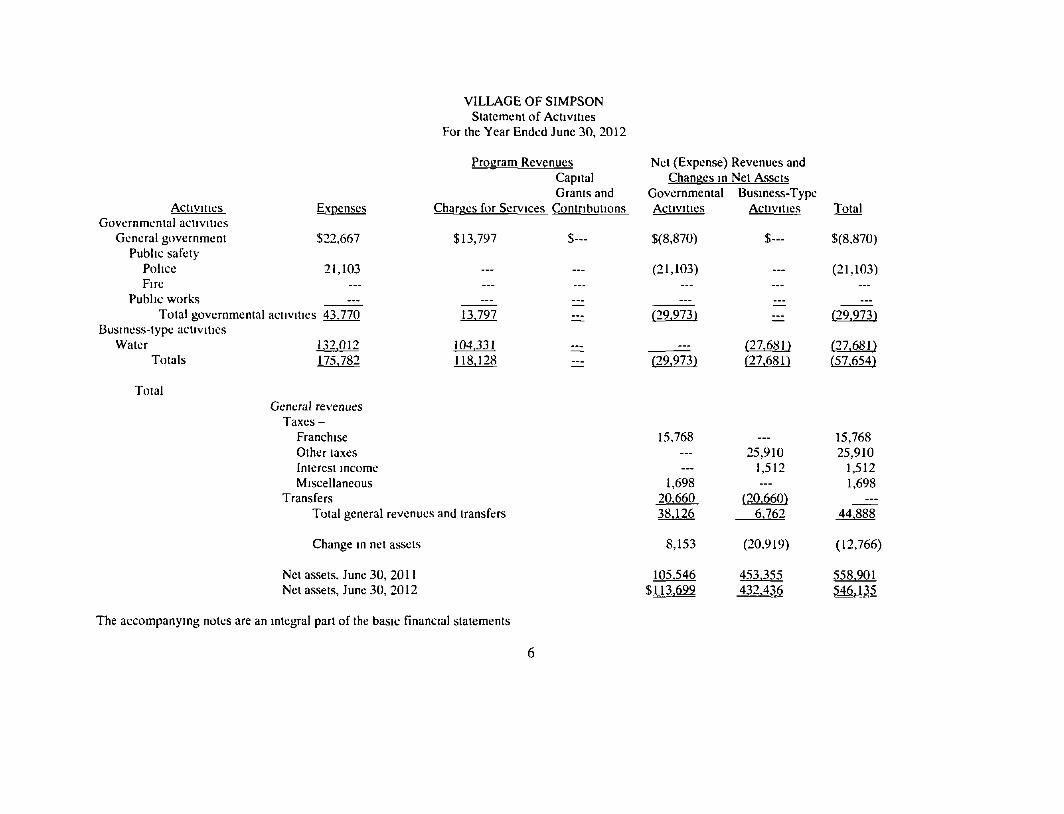

VILLAGE OF SIMPSON Statement of ActiviUes

For the Year Ended June 30, 2012

Activiiics Govornmenlal aciiviiics

General government Public safety

Police Fire

Public works — Total governmental activities 43.770

Business-type activities

Expenses

$22,667

2K103

Procram Revenues Capital Grants and

Charues for Services Contributions

$13,797 S—

— —

Net (Expense) Chanaesin

Governmental Activities

$(8,870)

(21,103)

Revenues and Net Assets

Business-Type Activities

$ -

Total

$(8,870)

(21,103)

Water Totals

Total

132.012 175.782

13.797

104.331 118.128

General revenues Taxes -

Franchise Other laxes Interest income Miscellaneous

Transfers Total general revenues and transfers

Change in net assets

Netassets. June 30, 2011 Netassets, June 30, 2012

(29.973)

(29.973) (27.681) (27.68 n

(29.973)

(27.681) (57.654)

15,768 ___ ...

1,698 20.660 38,126

8J53

105.546 $113,622

__. 25,910

1,512 ___

(20,660) 6.762

(20,919)

453,355 i 3 2 ^ 6

15,768 25,910

1,512 1,698

— 44.888

(12,766)

558,901 5Af̂ .m

The accompanying notes are an integral part of the basic financial statements

FUND FINANCIAL STATEMENTS (FFS)

FUND DESCRIPTIONS

General Fund

The General Fund is used to account for resources traditionally associated with governments which are not required to be accounted for in another fund

Enterprise Fund

Uulitv Fund

To account for the provision ol gas, water, and sewerage services to residents of the Villiige All activities necessary lo provide such services are accounted for in this lund, including, but not limited to, administration, operations, maintenance, financing, and related debt service, and billing and collection

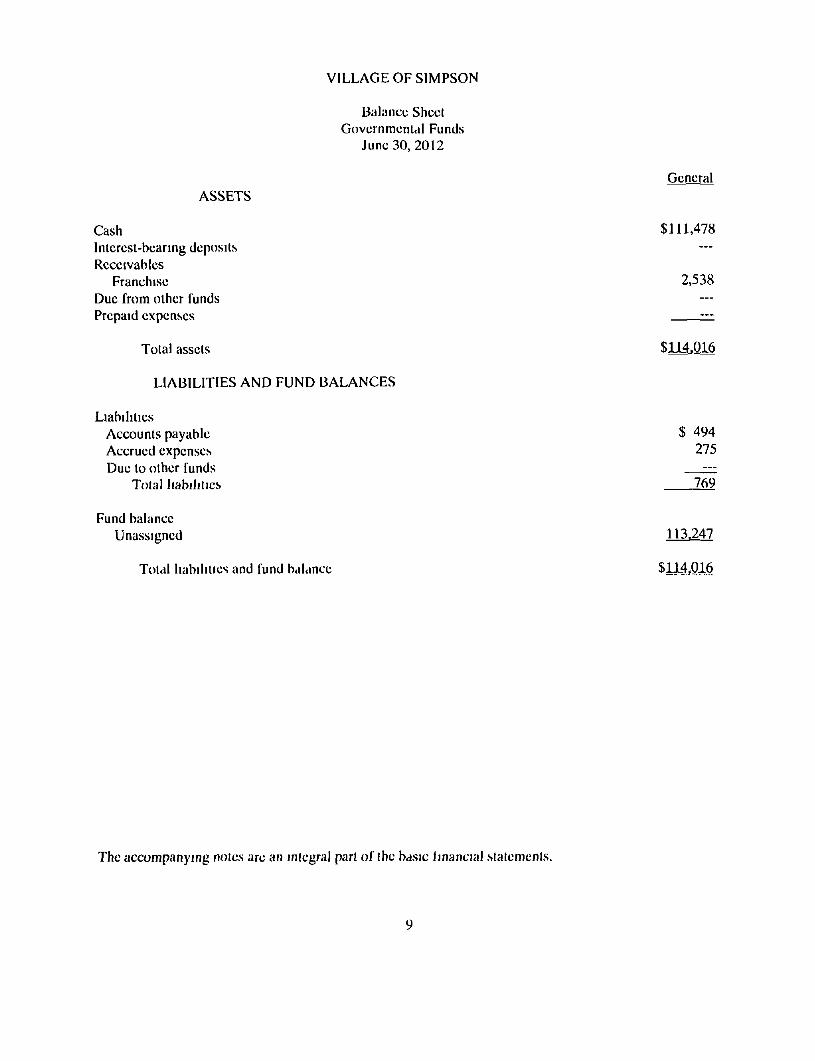

VILLAGE OF SIMPSON

Balance Sheet Governmental Funds

June 30, 2012

ASSETS

Cash Interest-bearing deposits Receivables

Franchise Due from other funds Prepaid expenses

Total assets

LIABILITIES AND FUND BALANCES

Liabilities Accounts payable Accrued expenses Due to other funds

Total liabilities

Fund balance Unassigned

Total liabilities and fund balance

General

$111,478

2,538

$114,016

$ 494 275

769

113.247

S11-4.Q16

The accompanying notes are an miegral part of the basic iinancial statements.

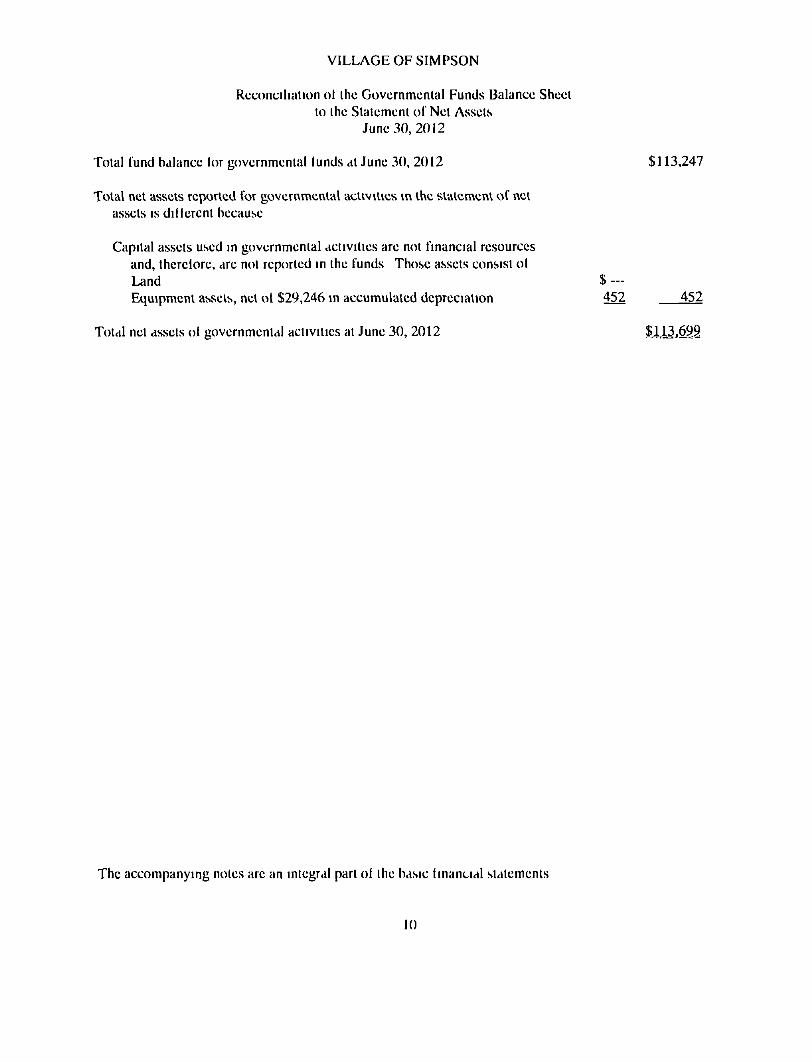

VILLAGE OF SIMPSON

Reconciliation ol the Governmental Funds Balance Sheet to the Statement of Net Assets

June 30, 2012

Total fund balance lor governmental lunds at June 30, 2012 $113,247

Total net assets reported for governmental activities in the slatement of net assets IS dillerent because

Capital assets used in governmental activities are not financial resources and, therelore, are not reported in the funds Those assets consist ol Liind $ — Equipment assets, nel ol $29,246 in accumulated dcprccialion 452 452

Total nel assets oi governmental activities at June 30, 2012 S113,6g9

The accompanying notes arc an integral pari ol ihe basic financial slatemenls

10

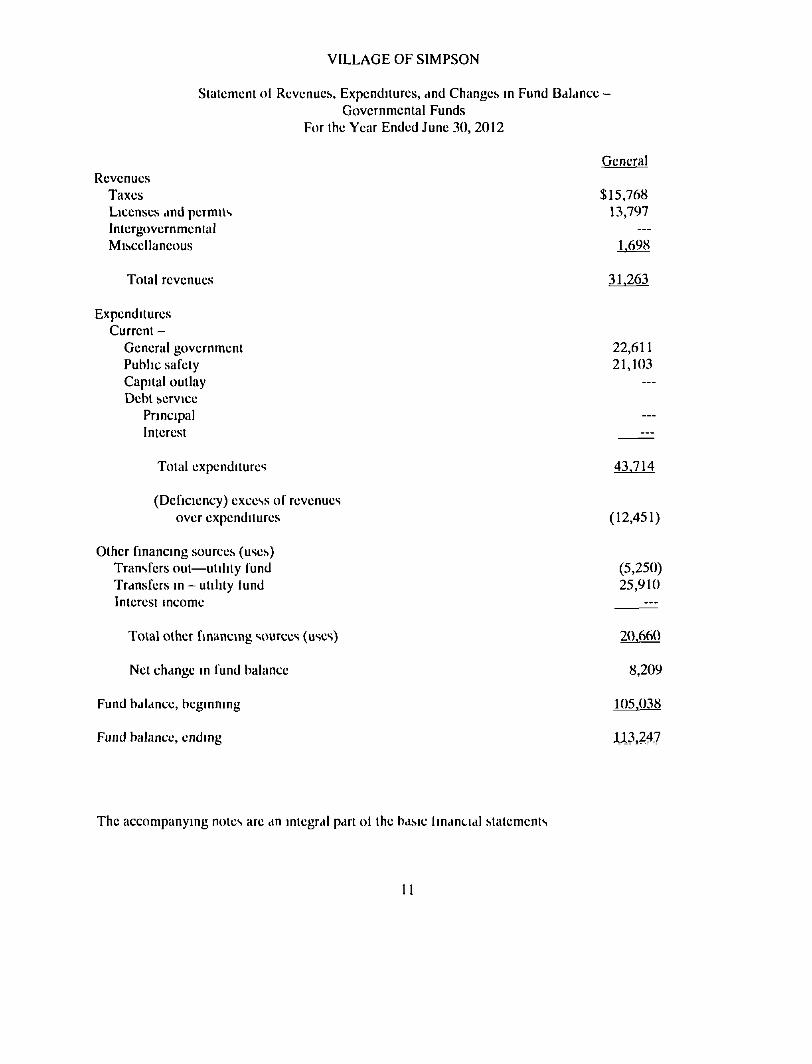

VILLAGE OF SIMPSON

Statement ol Revenues, Expenditures, and Changes in Fund Bal Governmental Funds

For the Year Ended June 30, 2012

tince

Revenues Taxes Licenses and permits Intergovernmental Miscellaneous

Total revenues

Expenditures Current -

General government Public safety Capital outlay Debt service

Principal Interest

Total expenditures

(Deficiency) excess of revenues over expendilures

Other financing sources (uses) Transfers out—utility fund Transfers in - utility lund Interest income

Total other financing sources (uses)

Net change in fund balance

Fund balance, beginning

Fund balance, ending

General

$15,768

13,797

1.698

31,263

22,611 21,103

43,714

(12,451)

(5,250) 25,910

20.660

8,209

105.038

113,247

The accompanying notes are an integral part ol the basic financial statements

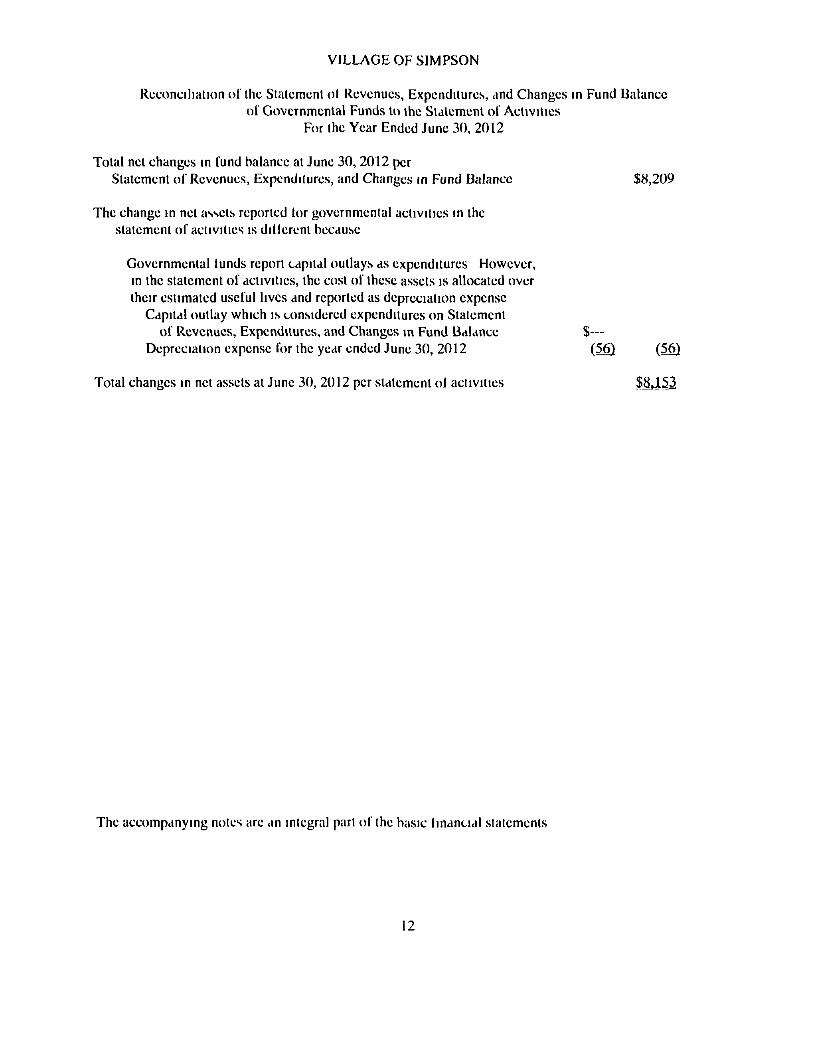

VILLAGE OF SIMPSON

Reconciliation of the Statement ol Revenues, Expenditures, and Changes in Fund Balance of Governmental Funds to the Slalemcnl of Activities

For the Year Ended June 30, 2012

Total net changes in fund balance at June 30, 2012 per Statement of Revenues, Expenditures, and Changes in Fund Balance $8,209

The change in net assets reported lor governmental activities in the statement of activities is dillerent because

Governmental lunds report capital outlays as expenditures However, in the statement of activities, the cosl of these assets is allocated over their estimated useful lives and reported as depreciation expense

Capital outlay which is considered expenditures on Slatement of Revenues, Expenditures, and Changes in Fund Balance $—

Depreciation expense for the year ended June 30, 2012 (56) (56)

Total changes in net assets at June 30, 2012 per statement ol activities $8,153

The accompanying notes are an integral part of the basic financial statements

12

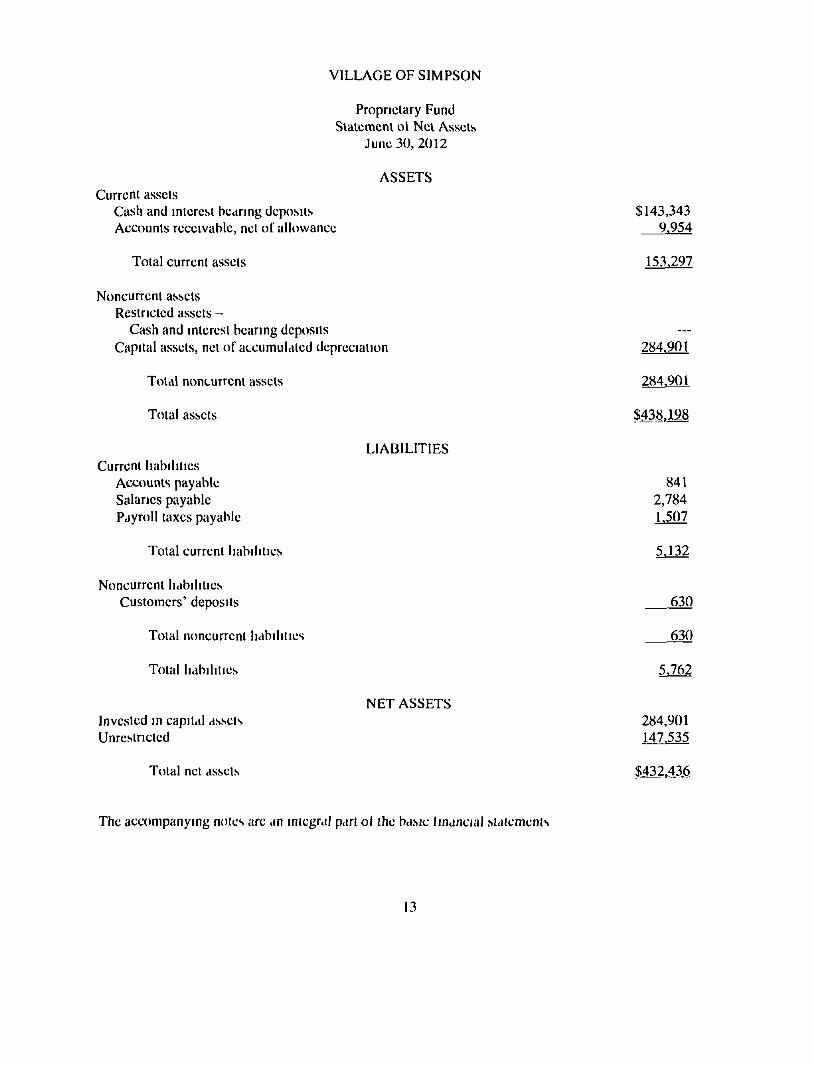

VILLAGE OF SIMPSON

Proprietary Fund Slalemcnl ot Nel Assets

June 30, 2012

ASSETS Current asscls

Cash and interest bearing dept)sils Accounts receivable, net of allowance

Total current assets

$143,343 9,954

153.297

Noncurrent assets Restricted assets -

Cash and interest bearing deposits Capital assets, nel of accumulated depreciation

Total noncurrent assets

Toial assets

Current liabilities Accounts payable Salaries payable Payroll taxes payable

Total current liabilities

Noncurrent liabilities Customers' deposits

Total noncurrent liabilities

Total liabilities

LIABILITIES

284.901

284.901

$A38.12§

841 2,784 1.507

5.132

630

630

5,762

Invested in capital assets Unrestricted

Total net assets

NET ASSETS 284,901 147.535

The accompanying notes are dn integral p<irt ol the basic linancial stalcmcnts

13

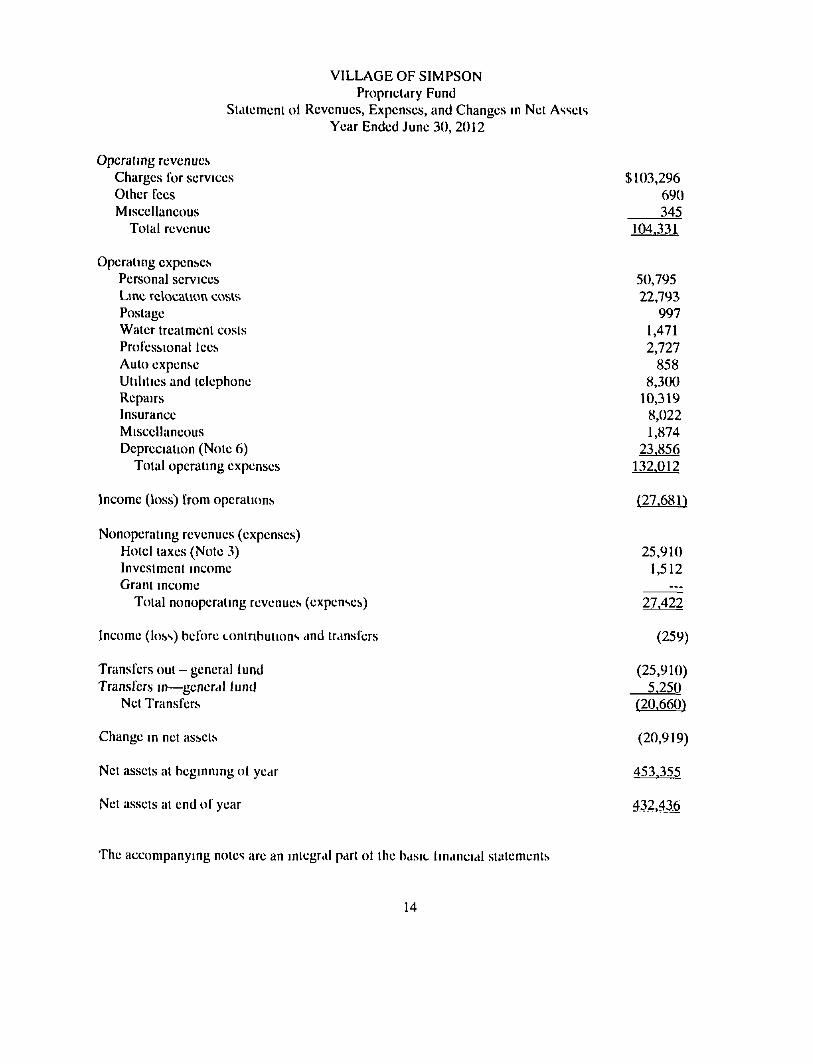

VILLAGE OF SIMPSON Proprietary Fund

Statement ol Revenues, Expenses, and Changes in Net Assets Year Ended June 30, 2012

Operating revenues Charges for services Other fees Miscellaneous

Total revenue

Operating expenses Personal services Line relocation costs Postage Water treatment costs Professional lees Auto expense Utilities and telephone Repairs Insurance Miscellaneous Depreciation (Note 6)

Total operating expenses

Income (loss) from operations

Nonoperating revenues (expenses) Hotel taxes (Note 3) Investment income Grant income

Total nonoperating revenues (expenses)

Income (loss) before contributions and transfers

Transfers out - general lund Transfers in—general lund

Net Transfers

Change in nel assets

Net assets at beginning ol year

Net assets at end of year

$103,296 690 345

104.331

50,795 22,793

997 1,471 2,727

858 8,300

10,319 8,022 1,874

23,856 132.012

(27.68n

25,910 1,512

27.422

(259)

(25,910) 5.250

(20.660)

(20,919)

453.355

4.32,4_3.6

The accompanying noles are an integral part ol the basic financial statements

14

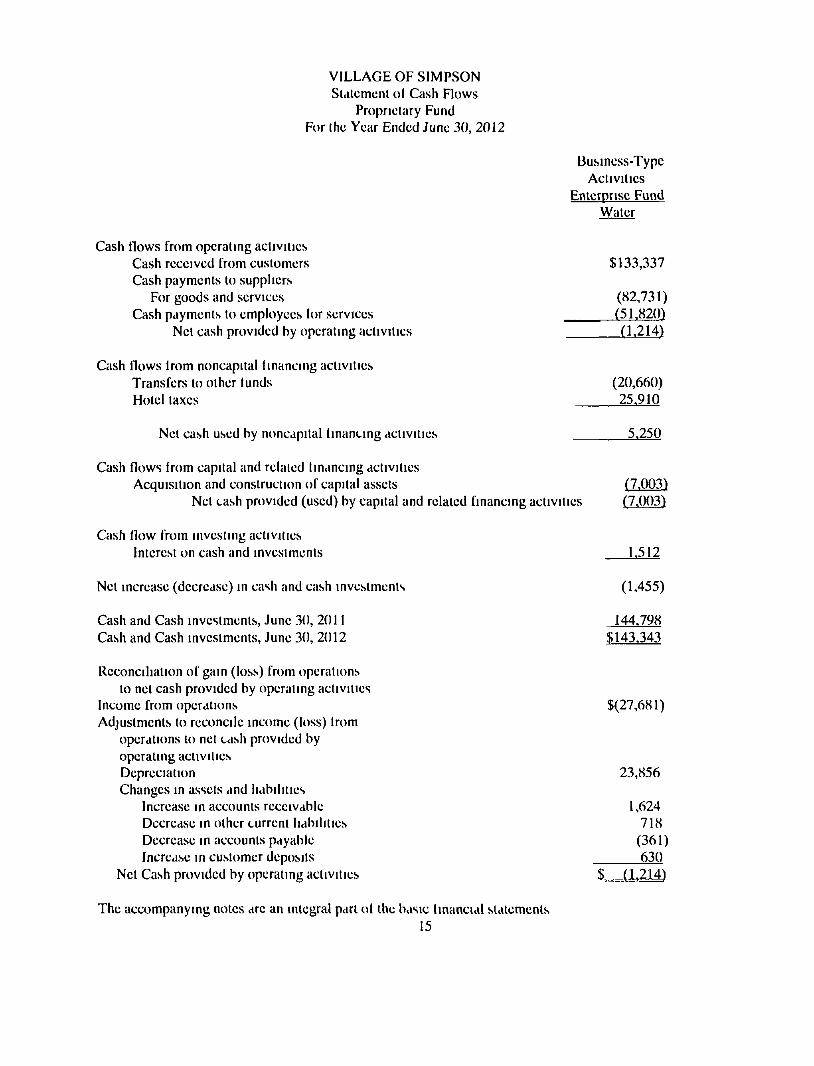

VILLAGE OF SIMPSON Statement ol Cash Flows

Proprietary Fund For the Year Ended June 30, 2012

Business-Type Activities

Enterprise Fund Water

Cash Hows from operating activities Cash received from customers Cash payments to suppliers

For goods and services Cash payments to employees lor services

Net cash provided by operating activities

$133,337

(82,731) (51,820) (1,214)

Cash Hows Irom noncapital financing activities Transfers lo other lunds Hotel taxes

(20,660) 25.910

Net cash used by noncapital financing activities 5,250

Cash Hows Irom capital and related financing activities Acquisition and construction of capital assets (7.003)

Net cash provided (used) by capital and related financing activities (7.003)

Cash How from investing activities Interest on cash and investments 1,512

Net increase (decrease) in cash and cash investments (1,455)

Cash and Cash investments, June 30, 2011 Cash and Cash investments, June 30, 2012

144.798 $143.343

Reconciliation of gain (loss) from operations lo nel cash provided by operating activiiics

Income from operations Adjustments to reconcile income (loss) Irom

operations lo net cash provided by operating activities Depreciation Changes in assets and liabilities

Increase in accounts receivable Decrease in other current liabilities Decrease in accounts payable Increase in customer deposits

Net Cash provided by operating activities

$(27,681)

23,856

1,624 718

(361) 630

The accompanying notes are an integral part ol the basic financial statements 15

VILLAGE OF SIMPSON

Notes lo Basic Financial Stalcmcnts

(1) Summary of Significant Accounting Policies

The accompanying financial statements of the Village of Simpson (the Village) have been prepared in conformity with generally accepted accounting principles (GAAP) as applied to governmental units GAAP includes all relevant Governmental Accounting Standards Board (GASB) pronouncements. The accounting and reportmg framework and the more significant accounting policies arc discussed in subsequent subsections of these notes

A, Financial Reporting Entity

The Village was originally formed as a Village on August 28, 1967 and operates under the provisions of the Lawrson Act The Village operates under a Mayor-Board of Aldermen form of government The financial reporting entity consists of (a) the primary government, (b) organizations for which the primary government is financially accountable, and (c) other organizations for which the primary government is not accountable, but for which the nature and significance of Iheir relationship with the primary government are such that exclusion would cause the reportmg entity's financial statements to be misleading or incomplete Component units are legally separate organizations for which the elected officials of the primary government are financially accountable In addition, component units can be other organizations for which the nature and significance of their relationship with the primary government are such that exclusion would cause the reporting entity's financial statements to be misleading or incomplete The Village of Simpson has no such component units

B Basis of Presentation

Government-Wide Financial Statements (GWFS)

The statement of net assets and statement of activities display information about the Village, the primary government, as a whole They include all funds of the reporting entity, except fiduciary funds and component units that are fiduciary in nature The statements distinguish between governmental and business-type activities Governmental activities generally are financed through taxes, intergovernmental revenues, and other nonexchange revenues Business-type activities are financed in whole or in part by fees charged to external parties for goods or services

16

VILLAGE OF SIMPSON

Noles to Basic Financial Statemenls (Continued)

The slatement of activities presenls a comparison between direct expenses and program revenues for the business-type activities of the Village and for each function of the Village's governmental activities Direct expenses arc those that arc specifically associated with a program or function and, therefore, arc clearly identifiable to a particular function Program revenues include (a) fees, fines, and charges paid by the recipients of goods or services offered by the programs, and (b) grants and contributions that are restricted to meeting the operational or capital requirements of a particular program. Revenues that are not classified as program revenues, including all taxes, are presented as general revenues

Fund Financial Statements

The accounts of the Village are organized and operated on the basis of funds. A fund IS an independent fiscal and accounting entity with a separate set of self-balancing accounts. Fund accounting segregates funds according to their intended purpose and is used to aid management in demonstrating compliance with finance-related legal and contractual provisions The minimum number of funds is maintained consistent with legal and managerial requirements. Fund financial statements report detailed information about the Village

The various funds of the Village are classified into two categories: governmental and proprietary. The emphasis on fund financial statements is on major governmental and enterprise funds, each displayed in a separate column. A fund is considered major if it is the primary operating fund of the Village or meets the following criteria

a. Total assets, liabilities, revenues, or expenditures/expenses of that individual governmental or enterprise fund are at least 10 percent of the corresponding total for all funds of that category or type: and

b Total assets, liabilities, revenues, or expenditures/expenses of the individual governmental or enterprise fund are at least 5 percent of the corresponding total for all governmental and enterprise funds combined

The major funds of the Village are described below

Governmental Funds -

The General Fund is the general operating fund of the Village. It is used to account for all financial resources except those required to be accounted for in another fund.

17

VILLAGE OF SIMPSON

Notes lo Basic Financial Statements (Continued)

Additionally, the Village reports the following fund types

Proprietary Funds -

Proprietary funds are used lo account for ongoing organizations and activities that arc similar to those often found in the private sector The measurement focus is based upon determination of net income, financial position, and cash flows

Enterprise funds

Enterprise funds are used to account for operations (a) that are financed and operated in a manner similar to private business enterprises - where the intent of the governing body is that the costs (expenses, including depreciation) of providing goods or services to the general public on a continuing basis be financed or recovered primarily through user charges; or (b) where the governing body has decided that periodic determination of revenues earned, expenses incurred, and/or net income is appropriate for capital maintenance, public policy, management control, accountability, or other purposes.

The Village's enterprise fund is the Utility Fund

C. Measurement Focus/Basis of Accounting

Measurement focus is a term used to describe "which" transactions are recorded within the vanous financial statements Basis of accounting refers lo "when" transactions are recorded regardless of the measurement focus applied.

Measurement Focus

On the government-wide statement of net assets and the stalement of activities, both governmental and business-type activities are presented using the economic resources measurement focus as defined in item b. below

In the fund financial statements, the "current financial resources" measurement focus or the "economic resources" measurement focus is used as appropriate.

All governmental funds utilize a "current financial resources'' measurement focus Only current financial assets and liabilities are generally included on their balance sheets Their operating statements present sources and uses of available spendable financial resources during a given period. These funds use fund balance as their measure of available spendable financial resources at the end of the period.

18

VILLAGE OF SIMPSON

Noles lo Basic Financial Statements (Continued)

The proprietary fund utilizes an "economic resources" measurement focus The accounting objectives of this measurement focus are the determination of operating income, changes in net assets (or cost recovery), financial position, and cash flows All assets and liabilities (whether current or noncurrent) associated with their activities are reported Proprietary fund equity is classified as net assets

Basis of Accounting

In the govcrnmenl-wide statemenl ol net assets and slalemcnl of activities, both governmental and business-type activities are presented using the accrual basis ol accounting Under the accrual basis of accounting, revenues are recognized when earned and expenses are recorded when the liability is incurred or economic asset used Revenues, expenses, gains, losses, assets, and liabilities resulting from exchange and exchange-like transactions are recognized when ihe exchange takes place

Governmental lund financial statements are reported using the current financial resources measuremenl focus and ihc modified accrual basis oi accounting Revenues are recognized as soon as ihcy arc both measurable and available Revenues are considered lo be available when they are collectible wilhin the current period or soon enough thereafter to pay liabilities of ihc current period For this purpose, the government considers revenues lo be available if they are collected within 60 days of the end of the current fiscal period Expenditures (including capital outlay) generally are recorded when a liability is incurred, as under accrual accounting However, debt service expenditures are recorded only when payment is due

The proprietary fund utilizes the accrual basis of accounting Under ihe accrual basis of accounting, revenues are recognized when earned and expenses are recorded when the liability is incurred or economic asset used

Program revenues

Program revenues included in the Statement of Activities are derived directly from ihe program itself or from parties outside the Village's taxpayers or citi/enry, as a whole, program revenues reduce the cosl of the function to be financed from the Village's general revenues

Allocation ol indirect expenses

The Village reports all direct expenses by lunction in ihe Statement of Activities Direct expenses are those that are clearly idenlifiable with a lunction Depreciation expense is specifically ideniified by function and is included in the direct expense ol each function

VILLAGE OF SIMPSON

Notes to Basic Financial Stalements (Continued)

D Assets. Liabilities, and Equilv

Cash and interest-bearing deposits

For purposes of the Slatement of Net Assets, cash and interest-bearing deposits include all demand accounts, savings accounts, and cerlificales of deposits of the Village For the purpose of the proprietary fund statement of cash flows, "cash and cash equivalents" include all demand and savings accounls, and certificates of deposit or short-term investments with an original maturity of three months or less when purchased See Note (2) for additional GASB No 3 disclosures

Inveslmenls

Under slate law the Village may deposit funds with a fiscal agent organized under the laws of the State of Louisiana, the laws of any other stale in the union, or the laws of the United States The Village may invest in United Slates bonds, treasury notes and bills, government backed agency securities, or cerlificales and lime deposits of slate banks organized under Louisiana law and national banks having principal offices in Louisiana

Interfund receivables and payables

During the course of operations, numerous transactions occur between individual funs that may result in amounts owed between funds Those related lo goods and services type transactions arc classified as '*due to and from other funds '' Short-term interfund loans arc reported as 'interfund receivables and payables '' Long-term inerfund loans (noncurrent portion) are reported as '^advances from and to other funds " Interfund receivables and payables between funds within governmental activities arc eliminated m the Statemenl of Nel Assets

Receivables

In the government-wide statements, receivables consist ol all revenues earned at year-end and not yet received Major receivable balances lor the governmental activities include ad valorem and franchise laxes Business-type activities report customer's utility service receivables as their major receivables

20

VILLAGE OF SIMPSON

Notes to Basic Financial Statements (Continued)

Prepaid Items

Payments made lo vendors lor services thai will benefit periods beyond June 30, 2012, if any, are recorded as prepaid items

Capital Assets

Capital assets, which include properly, plant, equipment, and inlrastructure asscls, are reported in the applicable governmental or business-type activities columns in the government-wide or financial slalcmcnls Capital assets are capitalized at historical cosl or estimated cosl il historical is not available Donated assets are recorded as capital assets at their estimated lair market value at the date of donation The Village maintains a threshold level of $500 or more for capitalizing capital assets

The costs of normal maintenance and repairs that do not add to the value of ihe assel or materially extend assets' lives are not capitalized Prior to January I, 2003, governmental funds' infrastructure assets were not capitalized These assets have been valued at estimated historical cost

Depreciation of all exhaustible capital assets is recorded as an allocated expense in the slatement of activities, with accumulated depreciation refiected m the statement of net asscls Depreciation is provided over the assets' estimated uselul lives using the straighl-hne method of depreciation Umd and construction in progress are not depreciated The range ol estimated uselul lives by type of assel is as lollows

Equipment 5 - 1 5 years Plant, Well, and Extensions 10 -50 years

In the fund financial statements, capital asscls used in governmental fund operations are accounted for as capital outlay expenditures of the governmental fund upon acquisition Capital assets used in propnetary fund operations are accounted for the same as in the government-wide slatemenls

Compensated Absences

The Village does not award compensated absences to Us employees

Long-term debt (if any)

The accounting treatment of long-term debt depends on whether the assets are used in governmental fund operations or proprietary fund t>peralions and whether they are reported in the govcrnmenl-widc or tund financial statements

VILLAGE OF SIMPSON

Noles lo Basic Financial Slatemenls (Continued)

All long-term debt lo be repaid from governmental and business-type resources arc reported as liabilities in the government-wide statements The long-term debt consists primarily of utility meter deposits payable

Long-term debt lor governmental lunds is not reported as liabililies in the fund financial stalcmcnts The debt proceeds are reported as olher financing sources and payment of principal and interest repi^rtcd as expendilures The accounting for proprietary fund long-term debt is the same in ihe lund statements as it is in the governmenl-widc statements

Equity Classificalions

In the governmcnl-wide slatemenls, equity is classified as net assets and displayed in three components

a Invested in capital assets, net of related debt - consists ol capital assets including restricted capital asscls, net of accumulated depreciation and reduced by the outstanding balances of any bonds, mortgages, notes, or other borrowing that are attributable lo the acquisition, construction, or improvement of those assets

b Restricted net assets - consists of ncl assets with constraints placed on the use either by (1) external groups, such as credilors, grantors, contributors, or laws or regulations of other governments, or (2) law through constitutional provisions or enabling legislation

c. Unrestricted nel assets - all olher net assets that do nol meet the definition of "restricted" or "invested in capital assets, net of related debt "

Beginning with fiscal year 2011, the Village implemented GASB Statement No 54, "Fund Balance Reporting and Governmental Fund Type Definitions '* This Statement provides more clearly defined lund balance categories to make the nature and extent of the constraints placed on a government's fund balances more transparent The following classifications describe the relative strength of the spending constraints

Nonspendable Fund Balance - amounts that are nol in nonspendable form (such as inventory) or are required to be maintained intact

Restricted Fund Balance - amounts constrained lo specific purposes by their providers (such as grantors, bondholders, and higher levels ol government), though constitutional provision, or by enabling legislation

Committed Fund Balance - amounts constrained to specific purposes by the Village itself, using its highest level ol decision-making authority To be reported as commuted, amounts cannot be used lor any other purpose unless the Village lakes the same highest level action to remove or change the constraint

Assigned Fund Balance - amounts the Village intends lo use for a specific purpose Intenl is expressed by the Village

Unassigned Fund Balance - amounts that are available for any purpose Positive amounts are reported only in the general fund

At year-end, the Village only had unassigned fund balance

22

VILLAGE OF SIMPSON

Noles to Basic Financial Statements (Continued)

E Revenues. Expenditures, and Expenses

Operating Revenues and Expenses

Operating revenues and expenses for proprietary funds are those that result Irom providing services and producing and delivering goods and/or services It also includes all revenue and expenses not related to capital and related financing, noncapilal financing, or investing aclivities

Expenditures/Expenses

In the government-wide financial statemenls, expenses are classified by function lor both governmental and business-type activities

In the lund financial slatemenls, expenditures are classified as follows

Governmental Funds - by Character Proprietary Fund - by Operating and Nonoperating

In the fund financial slalcmcnls, govcrnmenlal funds report expendilures of financial resources Proprietary funds report expenses relating lo use of economic resources

Interfund Translers

Permanent reallocations of resources between funds ol the reporting entity are classified as interlund translers For the purposes ol the statement of activities, all interfund transfers between individual governmental funds have been eliminated

F Budgets and Budgetary Accounling

The Village follows these procedures in establishing the budgetary dala renected in the financial statements

1 The Village prepares a proposed operating budget for the fiscal year and submits it lo Ihe Mayor and Board of Aldermen not later than lifieen days prior to the beginning of each fiscal year

2 A summary ot the proposed budget is published and the public notified that the proposed budget is available for public inspection At the same lime, a public hearing is called

3 A public hearing is held on the proposed budget at leasl ten days alter publication of the call lor the hearing

4 Alter the holding of the public hearing and completion ol all action necessary to finalize and implement the budget, the budget is adopted through passage ol a resolution prior to the commencemenl ol the fiscal year lor which the budget is being adopted

5 Budgetary amendments involving the transfer of funds from one department, program, or lunction to another or involving increases in expendilures resulting Irom revenues exceeding amounts eslimated require the approval of the Board ol Aldermen

23

VILLAGE OF SIMPSON

Noles to Basic Financial Statements (Continued)

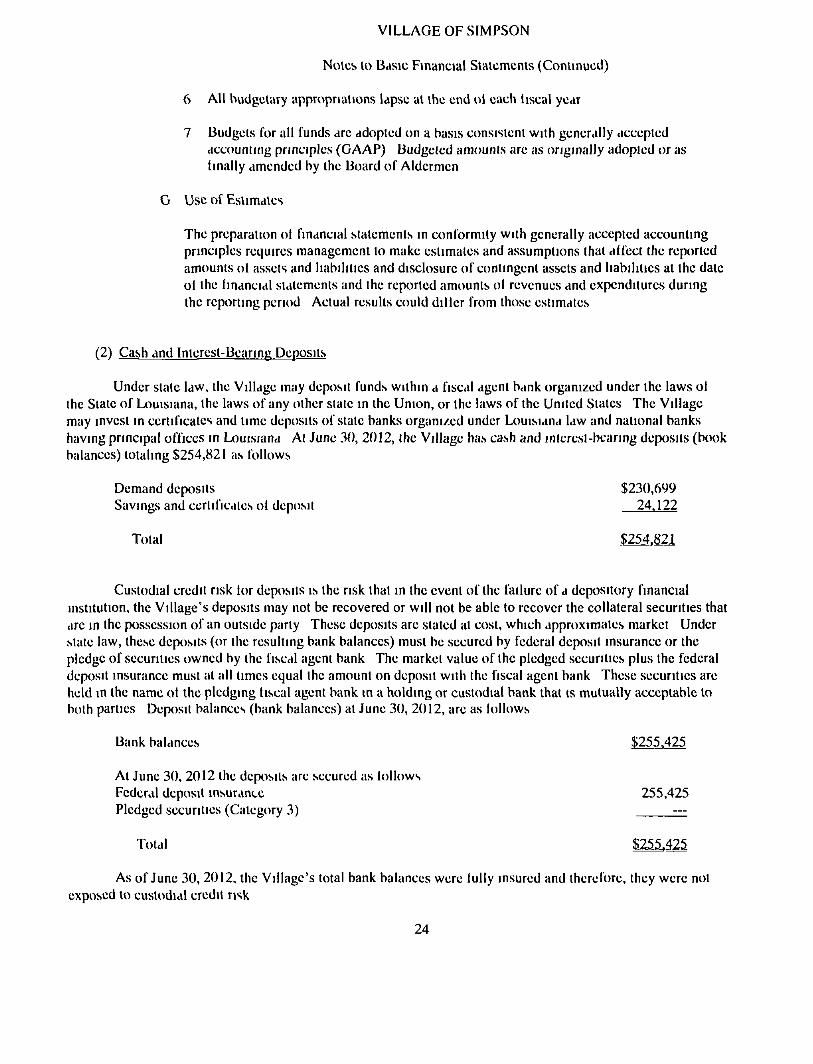

6 All budgetary appropriations lapse at the end ol each liscal year

7 Budgets for all funds arc adopted on a basis consistent with generally accepted accounting principles (GAAP) Budgeted amounts are as originally adopted or as finally amended by the Board of Aldermen

G Use of Estimates

The preparation ol financial statemenls in conformity with generally accepted accounting principles requires management lo make estimates and assumptions that alfect the reported amounts ol assets and habililies and disclosure of conlingent assets and liabilities at the date ol the financial statements and the reported amounts ol revenues and expenditures during the reporting period Actual results could dillcr from those estimates

(2) Cash and Interest-Bearing Deposits

Under state law, the Village may deposit funds within a fiscal agent bank organized under the laws ol the Stale of Louisiana, the laws of any olher state in the Union, or the laws of the United Stales The Village may invest in certificates and time deposits of stale banks organized under Louisiana law and national banks having principal offices in Louisiana At June 30, 2012, the Village has cash and inleresl-beanng deposils (book balances) totaling $254,821 as follows

Demand deposits $230,699 Savings and certificates ol deposit 24.122

Total $25,4,821

Custodial credit risk lor deposits is the risk that in the event of the failure of a depository financial institution, the Village's deposits may not be recovered or will not be able to recover the collateral securities that tire in the possession of an outside party These deposits are staled at cost, which approximates market Under stale law, these deposits (or the resulting bank balances) must be secured by federal deposit insurance or the pledge of securities owned by the fiscal agent bank The market value of the pledged securities plus the federal deposit insurance must at all times equal the amount on deposit with the fiscal agent bank These securities are held in the name ol the pledging fiscal agent bank m a holding or custodial bank that ts mutually acceptable to both parties Deposil balances (bank balances) at June 30, 2012, are as lollows

Bank balances $255,425

At June 30, 2012 the deposits are secured as loMows Federal deposit insurance 255,425 Pledged securities (Category 3) zzz

Total $255,425

As of June 30, 2012, the Village's total bank balances were lully insured and iherelbre, they were not exposed to custodial credit nsk

24

VILLAGE OF SIMPSON

Notes to Basic Financial Statements (Continued)

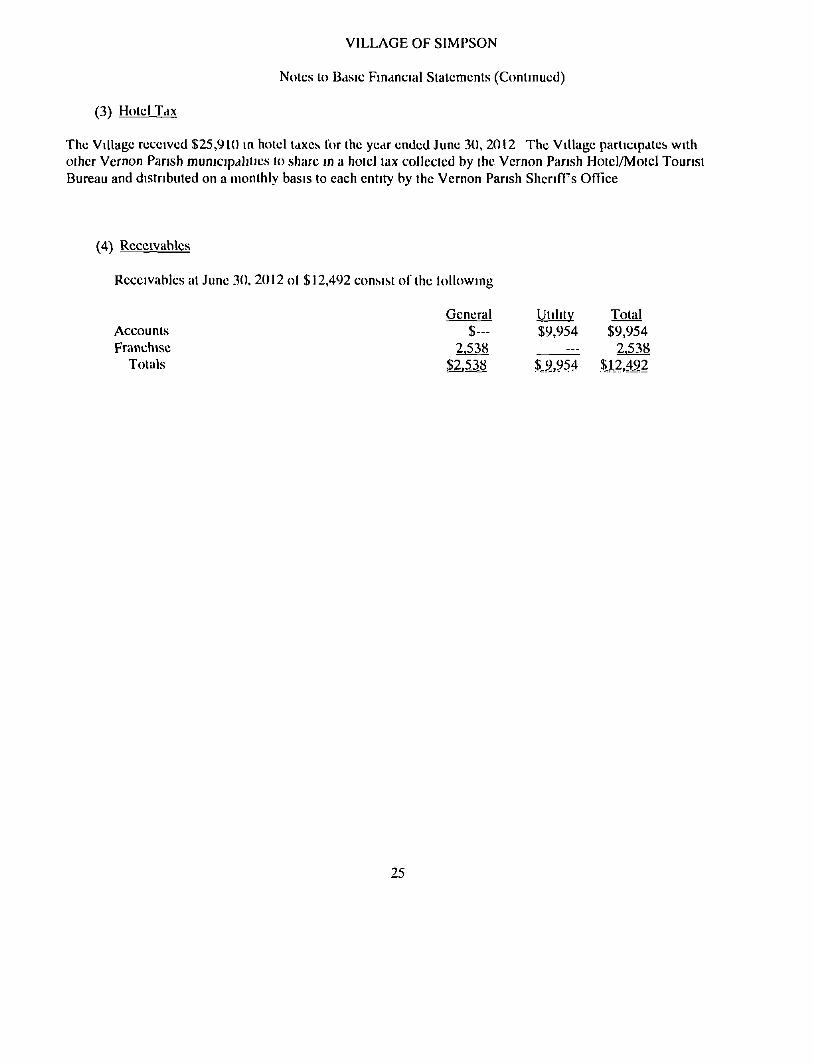

(3) Hotel Tax

The Village received $25,910 in hotel taxes for the year ended June 30, 2012 The Village participates with olher Vernon Parish municipalilies lo share in a hole! lax collecled by the Vernon Parish Hotel/Molcl Tourist Bureau and distributed on a monthly basis to each entity by the Vernon Parish Sheriffs Ofilce

(4) Receivables

Receivables at June 30, 2012 ol $12,492 consist of the lollowing

General Utility Total Accounls $— $9,954 $9,954 Franchise 2,538 -j:^ 2.538

Totals $2,538 $.9,954 $12,4J2

25

VILLAGE OF SIMPSON

Notes to Basic Financial Statemenls (Continued)

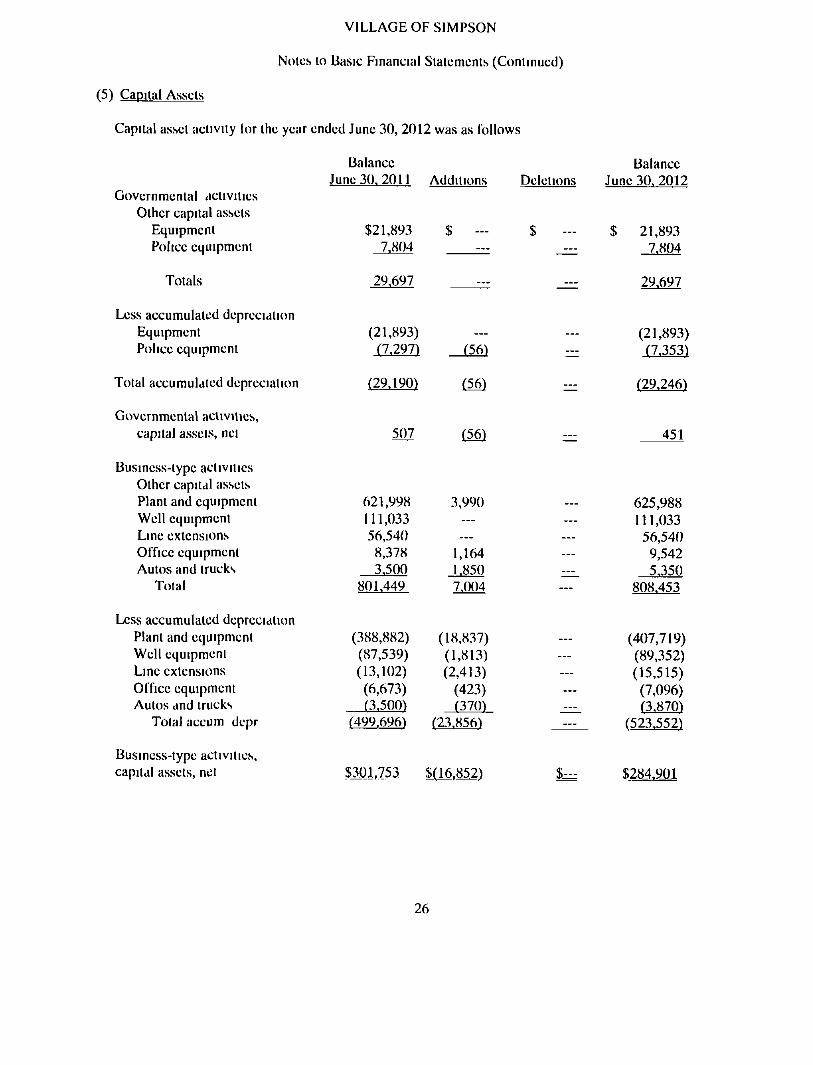

(5) Capital Assets

Capital assel activity lor the year ended June 30, 2012 was as follows

Governmental activities Other capital assets

Equipment Police equipment

Totals

Less accumulated depreciation Equipment Police equipment

Total accumulated depreciation

Governmental acliviiics, capital assets, nel

Balance June 30, 2011

$21,893 7,804

29,697

(21,893) (7,297)

(29.190)

507

Add

$

ilions

(56)

(56)

(56)

Deletions

S -

I I I

Balance June 30. 2012

$ 21,893 7,804

29,697

(21,893) (7,353)

(29.246)

451

Business-type activities Other capital assets Plant and equipment Well equipment Line extensions Office equipment Autos and trucks

Total

Less accumulated depreciation Plant and equipment Well equipment Line extensions Office equipment Autos and trucks

Total accum depr

Business-type activities. capital assets, net

621,998 111,033 56,540 8,378 3,500

801,449

(388,882) (87,539) (13,102) (6,673) (3.500)

(499.696)

5301,753

3,990 ___ -..

1,164 1,850 7,004

(18,837) (1,813) (2,413)

(423) (370)

(23.856)

$(16,852)

___ ___ ___ ___ ___ —

— ___ — ... ___ —

$zzz

625,988 111,033 56,540 9,542 5,.350

808,453

(407,719) (89,352) (15,515) (7,096) (3.870)

(523.552)

$284.9.01

26

VILLAGE OF SIMPSON

Notes to Basic Financial Statements (Continued)

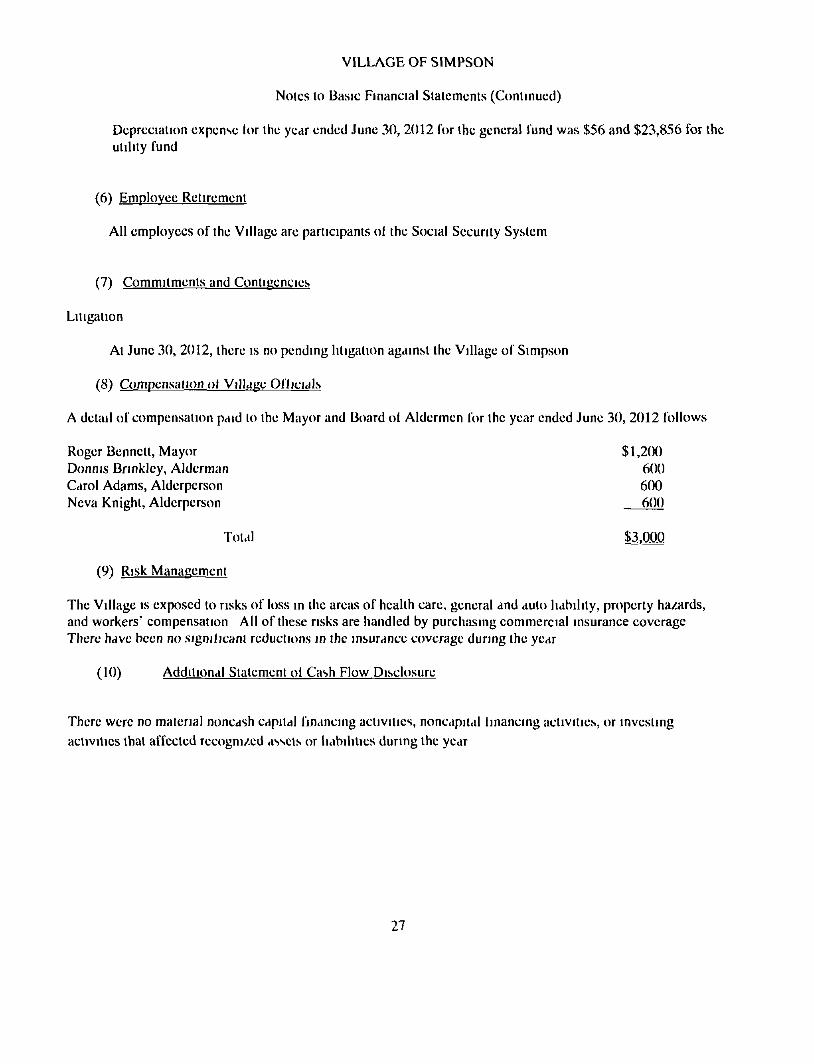

Depreciation expense lor the year ended June .30, 2012 for the general fund was $56 and $23,856 for the utility fund

(6) Employee Retirement

All employees of the Village are participants ol the Social Security System

(7) Commitments and Contigencies

Litigation

At June 30, 2012, there is no pending litigation against ihe Village of Simpson

(8) Compensation ol Village Oflicials

A detail of compensation paid lo the Mayor and Board oi Aldermen for the year ended June 30, 2012 follows

Roger Bennett, Mayor $ 1,200 Donnis Brinklcy, Alderman 600 Carol Adams, Alderperson 600 Neva Knight, Alderperson 600

Total $3.aO.Q

(9) Risk Management

The Village is exposed to risks of loss in the areas of health care, general and auto liability, property hazards, and workers' compensation All of these risks are handled by purchasing commercial insurance coverage There have been no significant reductions m the insurance coverage during the year

(10) Additional Statement ot Cash Flow Disclosure

There were no material noncash capital financing activiiics, noncapilal financing activiiics, or investing acliviiics that affected recogni/ed asscls or liabilities during the year

27

INTERNAL CONTROL, COMPLIANCE, AND OTHER MATTERS

28

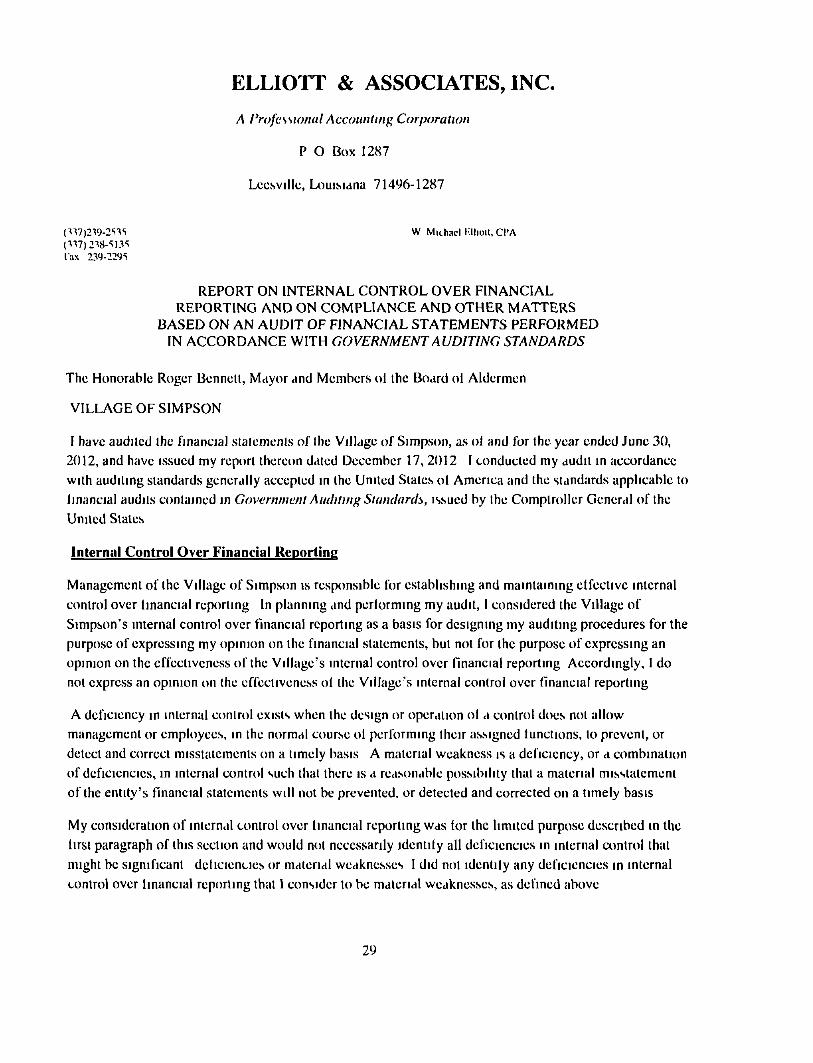

ELLIOTT & ASSOCIATES, INC.

A Professional Accounting Corporation

P O Box 1287

LeesviIIe, Louisiana 71496-1287

("^"^7)2^9-2'^'^S W Mithiicl I'lliolt.CI'A (•^"^7)3^8-^13^ \ \ \ \ 23M-229S

REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS

BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

The Honorable Roger Bennett, Mayor and Members ol the Board ol Aldermen

VILLAGE OF SIMPSON

I have audited the financial stalements of the Village of Simpson, as ol and \'or the year ended June 30, 2012, and have issued my report ihereon dated December 17, 2012 I conducted my audit in accordance with auditing standards generally accepted in the United Stales ol America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United Stales

Internal Control Over Financial Reporting

Management of the Village of Simpson is responsible for establishing and maintaining elfective internal control over financial reporting In planning and perlorming my audit, I considered the Village of Simpson's internal control over financial reporting as a basis for designing my auditing procedures for the purpose of expressing my opinion on the financial statements, bul not for the purpose of expressing an opinion on the effectiveness of the Village's internal control over financial reporting Accordingly, I do not express an opinion on the effectiveness ol the Village's internal control over financial reporting

A deficiency in internal control exists when the design or operation ol a control does nol allow management or employees, in the normal course ol performing their assigned lunclions, lo prevent, or detect and correct misstatements on a timely basis A material weakness is a deficiency, or a combination of deficiencies, in internal control such that there is a reasonable possibility that a material misstatement of the entity's financial statements will not be prevented, or detected and corrected on a timely basis

My consideration of internal control over financial reporting was lor the limited purpose described in the lirsi paragraph of this section and would nol necessarily identity all deficiencies in internal control that might be significant deficiencies or material weaknesses I did nol identity any deficiencies in internal control over financial reporting that 1 consider lo be material weaknesses, as defined above

29

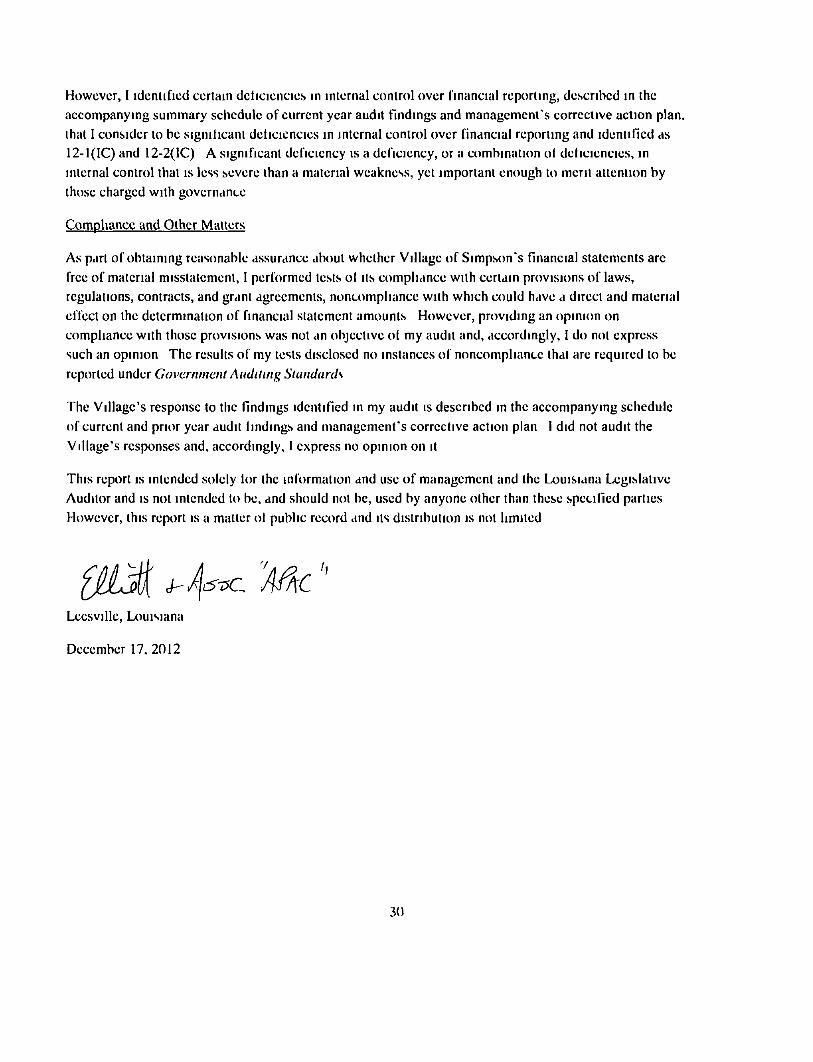

However, I identified certain deficiencies in internal control over financial reporting, described in the accompanying summary schedule of current year audit findings and management's corrective action plan, that I consider lo be significant deficiencies in internal control over financial reporting and identified as 12-1(IC) and 12-2(IC) A significant deficiency is a deficiency, or a combination ol deficiencies, in inlernal control that is less severe than a material weakness, yet important enough lo meril allenlion by those charged with governance

Compliance and Other Mailers

As part of obtaining reasonable assurance aboul whether Village of Simpson's financial statements arc free of material misslalemenl, I performed lesls ol Us compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the dclerminalion of financial statement amounts However, providing an opinion on compliance with those provisions was nol an objeclivc ol my audit and, accordingly, I do not express such an opinion The results of my tests disclosed no instances of noncompliance that are required lo be reported under Government Auditing Standards

The Village's response to the findings identified in my audit is described in the accompanying schedule of current and prior year audit findings and management's corrective action plan 1 did not audit the Village's responses and, accordingly, I express no opinion on it

This report is intended solely lor the information and use of management and the Louisiana Legislative Auditor and is not intended to be, and should nol be, used by anyone other than these specified parties However, this report is a mailer ol public record and its distribution is nol limited

[MM ^ ^ ^ "M-c LeesviIIe, Louisiana

December 17,2012

30

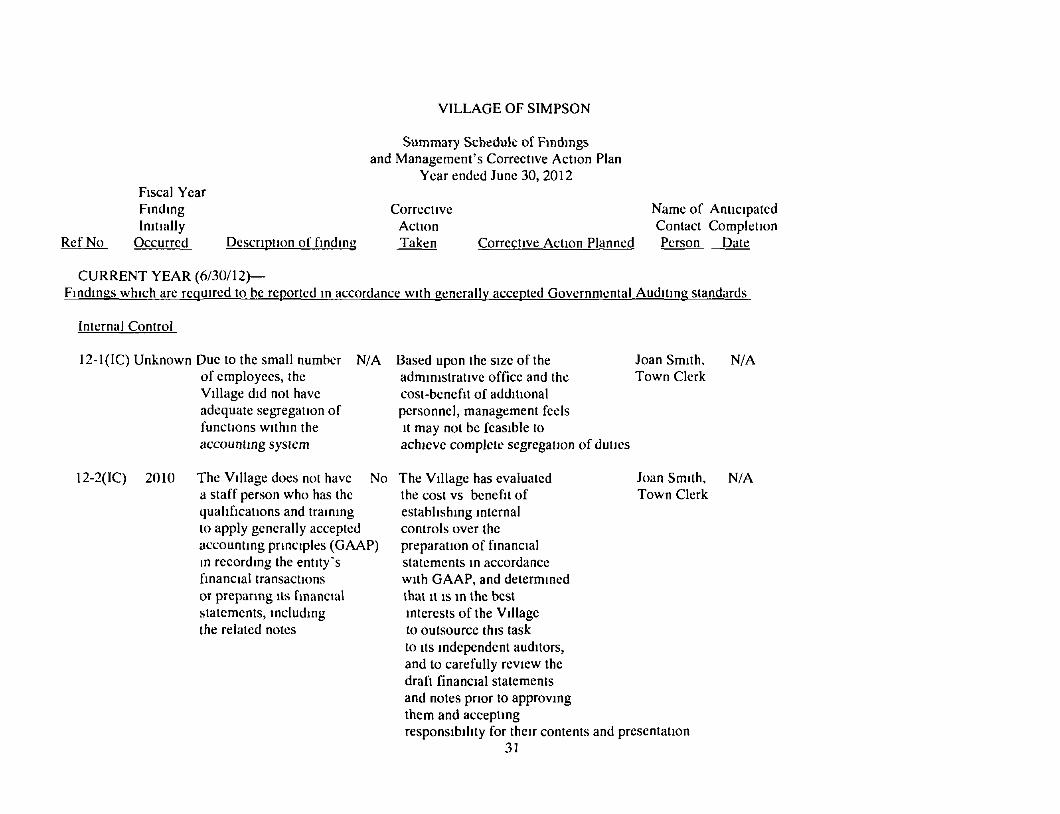

VILLAGE OF SIMPSON

Summary Schedule of Findings and Management's Corrective Action Plan

Yearended June 30, 2012 Fiscal Year Finding Corrective Name of Anticipated Initially Action Contact Completion

Ref No Occurred Description of finding Taken Corrective Action Planned Person Date

CURRENT YEAR (6/30/12)— Findings which are required lo be reported in accordance with generally accepted Governmental Auditing standards

Interna! Control

12-1(IC) Unknown Due to the small number N/A Based upon the size of the of employees, the Village did not have adequate segregation of functions within the accounting system

administrative office and the cost-benefit of additional personnel, management feels It may not be feasible to achieve complete segregation of duties

Joan Smith, Town Clerk

N/A

12-2(IC) 2010 The Village does nol have No a staff person who has the qualifications and training to apply generally accepted accounting principles (GAAP) in recording the entity's financial transactions or preparing its financial statements, including the related notes

The Village has evaluated Joan Smith, the cost vs benefit of Town Clerk establishing internal controls over the preparation of financial statements in accordance with GAAP, and determined that It is in the best interests of the Village to outsource this task to Its independent auditors, and to carefully review the draft financial statements and notes prior to approving them and accepting responsibility for their contents and presentation

31

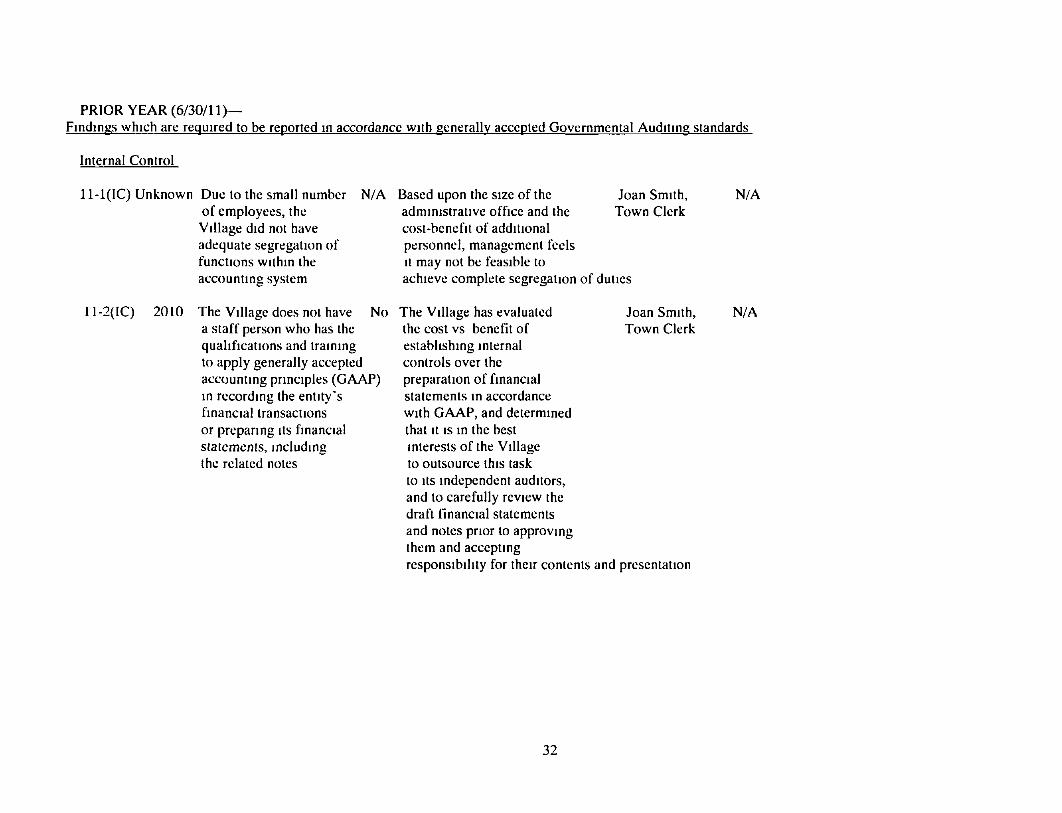

N/A

PRIOR YEAR (6/30/11; Findings which are required to be reported in accordance with generally accepted Governmental Auditing standards

Inlernal Control

1 l-l(IC) Unknown Due to the small number N/A Based upon the size of the Joan Smith, N/A

11-2(IC) 2010

of employees, the Village did nol have adequate segregation of functions within the accounting system

No The Village does not have a staff person who has the qualifications and training to apply generally accepted accounting principles (GAAP) in recording the entity's financial transactions or preparing its financial statements, including the related notes

administrative office and the Town Clerk cost-benefit of additional personnel, management feels It may not be feasible lo achieve complete segregation of duties

The Village has evaluated Joan Smith, the cost vs benefit of Town Clerk establishing internal controls over the preparation of financial statements in accordance with GAAP, and determined that It IS in the best interests of the Village to outsource this task to Its independent auditors, and to carefully review the draft financial statements and notes prior to approving them and accepting responsibility for their contents and presentation

N/A

32

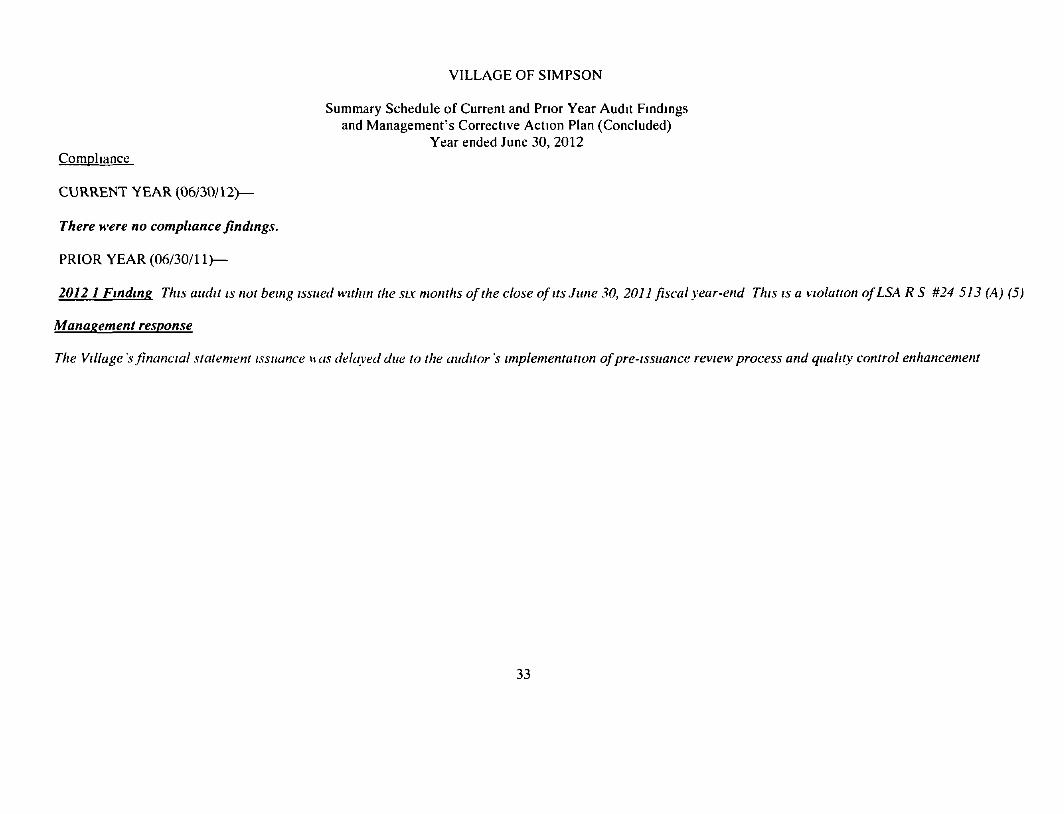

VILLAGE OF SIMPSON

Summary Schedule of Current and Prior Year Audit Findings and Management's Corrective Action Plan (Concluded)

Year ended June 30, 2012 Compliance

CURRENT YEAR (06/30/12)—

There were no compliance findings.

PRIOR YEAR (06/30/11)—

2012 1 Finding This audit is not being issued within the six months of the close of its June 30, 2011 fiscal year-end This is a violation ofLSA R S ^24 513 (A) (5)

Manasement response

The Village's financial statement issuance w as delayed due to the auditor \s implementation of pre-issitance review process and quality control enhancement

33