Embed Size (px)

Citation preview

Jl^o:^

VILLAGE OF LONGSTREET LONGSTREET, LOUISIANA

FINANCIAL REPORT

YEAR ENDED JUNE 30,2011

Under provisions of state law, this report is a public document. Acopy of the report has been submitted to the entity and other appropriate public officials. The report is avaiiable for public inspection at the Baton Rouge office of the LegislativeAuditor and, where appropriate, at the office of the parish clerk of .court.

R«...D« MOV 30 2011

(cMJ The CPA. Never Underestimate The Value?"

EUGENE W. FREMAUXII

CERTIFIED PUBLIC ACCOUNTANT

VILLAGE OF LONGSTREET LONGSTREET. LOUISIANA

JUNE 30.2011

TABLE OF CONTENTS

Accountants Compilation Report 1

Management's Discussion And Analysis 2

Statement Of Net Assets 5

Statement Of Activities ; 6

Govemmental Funds' Balance Sheet 7

Reconciliation Of The Govemmental Funds Balance Sheet To The Statement Of

Net Assets 8

Combined Statement Of Revenues, Expenditures, And Changes In Fund Balance

Govemmental Fund - General Fund 9

Reconciliation Of The Govemmental Funds Statement Of Revenues,

Expenditures, And Changes In Fund Balances To The Statement Of Activities 10

Notes To The Financial Statements 11

Other Reports Required By Govemment Auditing Standards 16

General Fund - Budgetary Comparison Schedule 17

Schedule Of Findings 18

Eugene W. FremaUX II p. O. BOX 134 270 Marthaville Road Certified Public Accountant Many, Louisiana 71449

318-256-0332 FAX 318-256-0389

fremaiixefg)helknuth net

ACCOUNTANT'S COMPILATION REPORT

Mayor Sue Fields and Members of the Board of Aldermen Village of Longstreet, Louisiana

I have compiled the accompanying basic fmancial statements of the Village of Longstreet, Louisiana as of June 30, 2011, and for the year then ended, as listed in the table of contents. I have not audited or reviewed the accompanying financial statements and, accordingly, do not express an opinion or provide any assurance about whether the fmancial statements are in accordance with accounting principles generally accepted in the United State of America.

The management of the Village of Longstreet, Louisiana, is responsible for the preparation and fair presentation of the fmancial statements in accordance with accounting principles generally accepted in the United States of America and for designing, implementing, and maintaining intemal control relevant to the preparation and fair presentation of the fmancial statements.

My responsibility is to conduct the compilation in accordance with Statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants. The objective of a compilation is to assist management in presenting fmancial information in the form of financial statements without undertaking to obtain or provide any assurance that there are no material modifications that should be made to the fmancial statements.

The management's discussion and analysis and budgetary comparison information, on pages 2 through 4 and 17, are not a required part of the basic financial statements but are supplementary information required by the Govemmental Accounting Standards Board. I have compiled the supplementary information from information that is the representation of management, without audit or review. Accordingly, I do not express an opinion or any other form of assurance on the supplementary information.

I am not independent with respect to the Village of Longstreet.

Eugene W. Fremaux II November 4, 2011

(£MJ Ttie CPA. Never Underestimate The Value?"

VILLAGE OF LONGSTREET LONGSTREET, LOUISIANA

MANAGEMENT'S DISCUSSION AND ANALYSIS JUNE 30, 2011

This section of the Village's armual financial report presents our discussion and analysis of the Village's financial performance during the fiscal year ended June 30, 2011. Please read it in conjunction with the transmittal letter at the front of this report and the Village's financial statements, which follow this section.

FINANCIAL HIGHLIGHTS

> The Village's net assets decreased $727 to $538,101. > Expenses for the year amounted to $43,754, an increase of $15,659. The increase results primarily

from higher depreciation and personnel expenses. > Revenues increased by $5,449 to $43,027. The increase primarily results from receipt of an

insurance settlement related to building damage sustained as a result of a car crashing into the building.

OVERVIEW OF FINANCIAL STATEMENTS

This annual report consists of three parts:

> Management's discussion and analysis > Basic financial statements > Supplementary information

The basic financial statements include two kinds of statements that present different views of the Village:

>• The first two statements are govemment-wide fmancial statements that provide both long-term and short-term information about the Village's overall financial status.

> The remaining statements are fund financial statements that focus on individual parts of the Village's operations in more detail than the govemment-wide statements. The Village has only one fund, the general fund.

VILLAGE OF LONGSTREET LONGSTREET, LOUISIANA

MANAGEMENT'S DISCUSSION AND ANALYSIS JUNE 30,2011

FINANCIAL ANALYSIS OF THE VILLAGE AS A WHOLE

Condensed Statement of Net Assets

Cunent assets Capital assets, net

Total assets

Cunent liabilities

Net assets:

Invested in capital assets

Unassigned

Total net assets

Total liabilitKs & net assets

June 30,

2011

$ 231,598 307.962

S 1.459

307,962

230.139

538.101

$ 539,560

June 30,

2010

$ 223,545

316.441

^ 5199}t6

1. 1.158

316,441

222J87

538.828

$ 539,986

Condensed Statement of Activities

E?q)enses

Program revenues

Year ended

June 30, June 30;

2011 2010

(43,754) $ (28,095)

31.206 30.043

Subtotal

General revenues

(12,548)

li.821

1,948

7.535

Change in net assets j m jm

> The Village's net assets decreased $727 during the year. Revenues increased $5,449 to $43,027, primarily due to receipt of an insurance settlement related to building damage sustained as a result of a car crashing into the building. Expenses for the year amounted to $43,754, an increase of $15,659. The increase results primarily from higher depreciation and personnel expenses.

FINANCIAL ANALYSIS OF THE FUNDS

The Village's govemmental fund balance increased $7,752 during die year. Revenues increased $5,449 to $43,027, primarily due to receipt of an insurance settlement related to building damage sustained as a result

VILLAGE OF LONGSTREET LONGSTREET, LOUISIANA

MANAGEMENT'S DISCUSSION AND ANALYSIS JUNE 30, 2011

of a car crashing into the building. Expenses increased $9,637 to $35,275 primarily due to increased personnel expense.

CAPITAL ASSETS

There were not additions or deletions to capital assets during the year.

ECONOMIC FACTORS AND NEXT YEAR'S BUDGETS AND RATES

The Village is highly dependent upon non-potable water sales, which comprise approximately 73% of total revenues. These sales are primarily made to drilling companies operating in the area. Drilling activity in the Haynesville shale geologic formation is expected to continue demand for the Village's non-potable water for the next few years; however the drilling companies have switched their focus to using groimd water, as opposed to well water, for major well completion projects, and monthly demand is highly volatile and very dependent upon drilling activity in the area. The Village does not expect any significant change in revenues or expenses for 2012.

CONTACTING THE VILLAGE'S FINANCLVL MANAGEMENT

This financial report is designed to provide our citizens, taxpayers, customers, and investors and creditors with a general overview of the Village's finances and to demonstrate the Village's accountability for the money it receives. If you have questions about this report or need additional financial information, contact Mayor Sue Fields, P.O. Box 3130, Longstreet, LA 71050.

ASSETS

VILLAGE OF LONGSTREET LONGSTREET, LOUISIANA

STATEMENT OF NET ASSETS

JUNE 30, 2011

Cash Receivables Prepaid expenses Capital assets, net of accumulated depreciation

228,691 2,129

778 307,962

TOTAL ASSETS 539,560

LIABILITIES

Accounts payable Payroll taxes payable

TOTAL LIABILITIES

609 850

1,459

NET ASSETS

Invested in capital assets Unassigned ^

TOTAL NET ASSETS

307,962 230,139

$ 538,101

See accompanying notes and accountant's compilation report

VILLAGE OF LONGSTREET LONGSTREET, LOUISIANA

STATEMENT OF ACTIVITIES

YEAR ENDED JUNE 30, 2011

Goverrmiental activities:

General govemment

Expenses

Program Revenues

Charges for Services

General Revenues: Taxes Other Interest

Total general revenues

Changes in net assets

Net assets, beginning of year

Net assets, end of year

Net (Expenses) Revenue and

Changes in Net Assets

Govemmental Unit

$ 43,754 $ 31,206 $

Total govemmental activities $ 43,754 $ 31,206 $

(12,548)

(12,548)

7,433 3,555

833

11,821

(727)

538,828

538,101

See accompanying notes and accountant's compilation report

VILLAGE OF LONGSTREET LONGSTREET, LOUISIANA

GOVERNMENTAL FUNDS - BALANCE SHEET

JUNE 30, 2011

Cash Receivables Prepaid expenses

Total Assets

$ 228,691 2,129

778_

$ 231,598

LIABILITIES AND FUND BALANCE

Liabilities: Accounts payable Payroll taxes payable

Total Liabilities

Fimd balance - unassigned

Total liabilities and fimd balance

$ 609 850

1,459

230,139

$ 231,598

See accompanying notes and accountant's compilation report

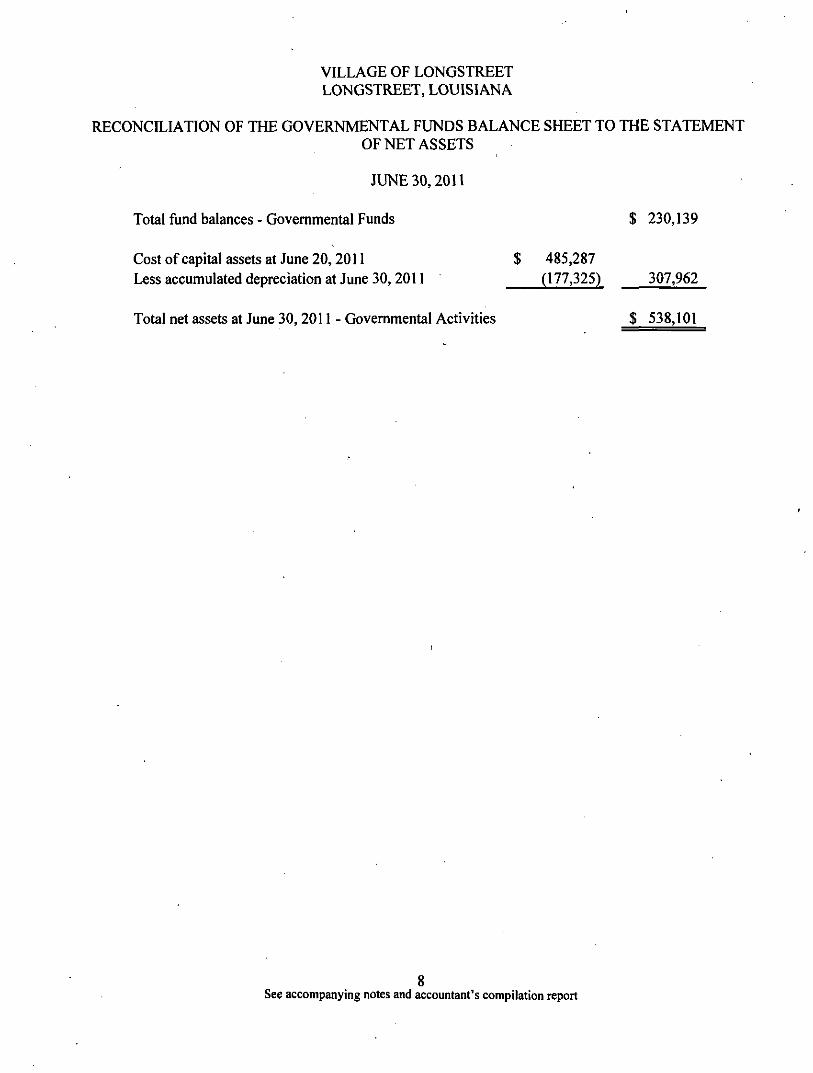

VILLAGE OF LONGSTREET LONGSTREET, LOUISIANA

RECONCILIATION OF THE GOVERNMENTAL FUNDS BALANCE SHEET TO THE STATEMENT

OF NET ASSETS

JUNE 30,2011

Total fund balances - Govemmental Funds $ 230,139

Cost of capital assets at June 20,2011 $ 485,287 Lessaccumulateddepreciationat June 30,2011 (177,325) 307,962

Total net assets at June 30, 2011 - Govemmental Activities $ 538,101

8 See accompanying notes and accountant's compilation report

VILLAGE OF LONGSTREET LONGSTREET, LOUISIANA

COMBINED STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCE

GOVERNMENTAL FUND - GENERAL FUND

YEAR ENDED JUNE 30,2011

Revenues:

Franchise tax $ 4,032 Occupational licenses 3,401 Water sales 31,206 Other income 3,555 Interest income 833

Total revenues 43,027

Expenditures: General govemment: Office supplies 2,760 Maintenance 9,246 Miscellaneous 5,574 Salaries 11,115 Payroll taxes 843 Utilities 5,737

Total general govemment 35,275

Total Expenditures 35,275

Excess (deficiency) of revenues over expenditures 7,752

Fund balance, beginning of year 222,387

Fund balance, end of year $ 230,139

9 See accompanying notes and accountant's compilation report

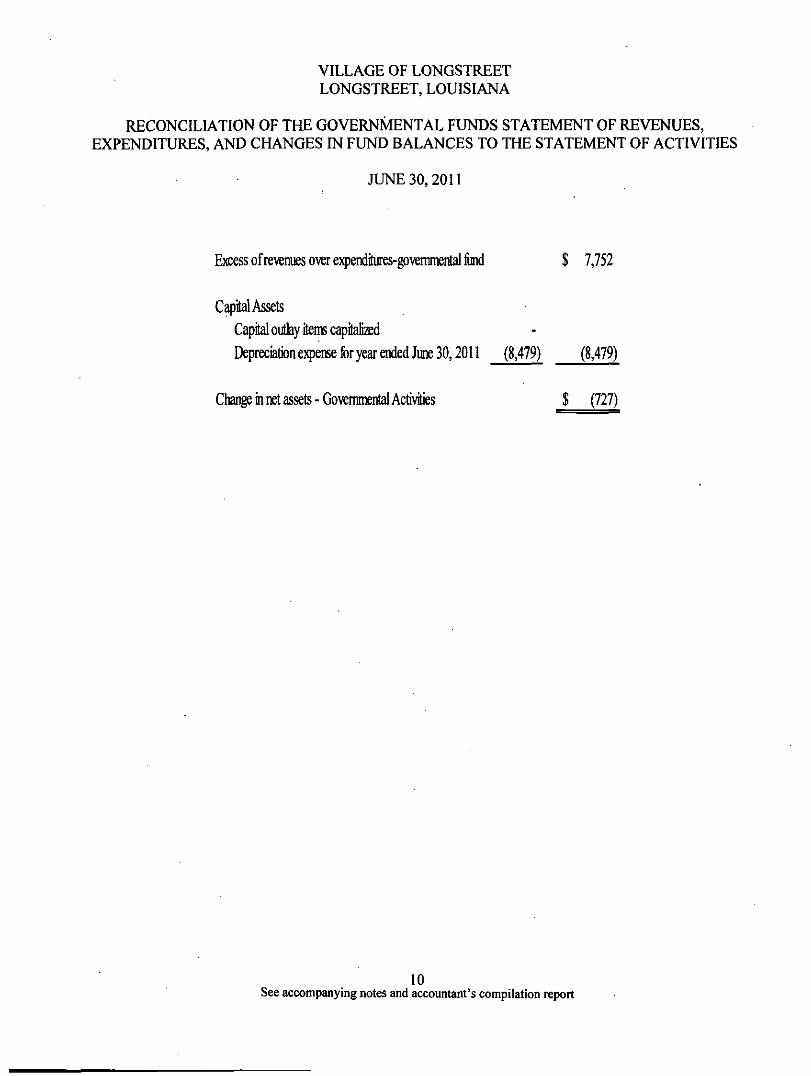

VILLAGE OF LONGSTREET LONGSTREET, LOUISIANA

RECONCILIATION OF THE GOVERNMENTAL FUNDS STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES EM FUND BALANCES TO THE STATEMENT OF ACTIVITIES

JUNE 30, 2011

Excess of revenues over e)q)enditiires-gpvemmental fond $ 7,752

Capital Assets

Capital outlay items capitaHzed

Depreciation ejgjense for year ended June 30,2011 (8,479) (8,479)

Change in net assets-Govemmental Activities $ (727)

10 See accompanying notes and accountant's compilation report

VILLAGE OF LONGSTREET LONGSTREET, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTS JUNE 30, 2011

(I) Summary of significant accounting policies

Village of Longstreet, Louisiana, was incorporated under the provisions of the Lawrason Act and operates under a Mayor/Board of Aldermen form of govemment. The Govemmental Accounting Standards Board (GASB) is the accepted standard setting body for establishing govemmental accounting and financial reporting principles.

The accounting and reporting policies of the Village conform to generally accepted accounting principles (GAAP) as applicable to govemments. The Govemmental Accounting Standards Board (GASB) is the accepted standard-setting body for establishing govemmental accounting and financial reporting principles. Such accounting and reporting procedures also conform to the requirements of Louisiana Revised Statutes 24:517 and to the guides set forth in the Louisiana Govemmental Audit Guide, and to the industry audit guide, Audits of State and Local Govemmental Units.

This financial report has been prepared in conformity with GASB Statement No. 34, Basic Financial Statements - and Management's Discussion and Analysis - f o r State and Local Governments, The following is a summary of certain significant accounting policies the Village follows:

Financial Reporting Entity

In evaluating how to define the Village for financial reporting purposes, management has considered all potential component units. The decision to include a potential component unit in the reporting entity was made by applying the criteria set forth in GAAP. The basic, but not only, criterion for including a potential component unit widiin the reporting entity is the goveming body's ability to exercise oversight responsibility. The most significant manifestation of this ability is fmancial interdependency. Other manifestations of the ability to exercise oversight responsibility include, but are not limited to, the selection of goveming authority, the designation of management, the ability to significantly influence operations, and accountability for fiscal matters. A second criterion used in evaluating potential component units is the scope of public service. Application of this criterion involves considering whether the activity benefits the govemment and/or its citizens, or whether the activity is conducted within the geographic boundaries of the govemment and is generally available to its citizens. A third criterion used to evaluate potential component units for inclusion or exclusion from the reporting entity is the existence of special financing relationships, regardless of whether the government is able to exercise oversight responsibilities. Based upon the application of these criteria, the financial statements of the Village consists of only the funds and account groups since the Village has no oversight responsibility for any other govemmental entity.

Govemmetvt-wide and fut\d financial statements

The govemment-wide financial statements (GWFS) (i.e., the statement of net assets and die statement of activities) report information on all of the non-fiduciary activities of the primary govemment. For the most part, the effect of inter-fund activity has been removed from these statements. Govemmental activities, which normally are supported by taxes, intergovemmental revenues, and other non-exchange transactions, are reported separately from business-type activities, which rely to a significant extent on fees and charges for support.

n

VILLAGE OF LONGSTREET LONGSTREET, LOUISIANA

NOTES TO FINANCIAL STATEMENTS JUNE 30,2011

The statement of net assets presents information on all of the Villages assets and liabilities, with the difference between the two reported as net assets. Over time, increases or decreases in net assets may serve as a useful indicator of whether the financial position of the Village is improving or deteriorating. The statement of activities demonstrates the degree, to which the direct expenses, of a given fimction or segment, are offset by program revenues.

Direct expenses are those that are clearly identifiable with a specific function or segment. Depreciation expense is identified by function and is included in the direct expense of each function. Interest on general long-term debt of govemmental activities is considered an indirect expense and is reported separately on the statement of activities. Interest on long-term debt of business-type activities is recorded as direct expenses. Program revenues include 1) charges to customers or applicants who purchase, use or directly benefit from goods, services, or privileges provided by a given function or segment; and 2) grants and contributions that are restricted to meeting the operation or capital requirements of a particular function or segment. Program revenues included in the Statement of Activities derive directly from sales of non-potable water; program revenues reduce the cost of the function to be financed from the Village's general revenues. Taxes and other items not properly included among program revenues are reported instead as general revenues.

Separate fund fmancial statements (FFS) are provided for govemmental funds and proprietary funds. Major individual govemmental and enterprise funds are reported as separate columns in the FFS. The Village has only a govemmental fund.

Measurement Focus, Basis of Accounting, and Financial Statement Representation

The govemment-wide fmancial statements are reported using the economic resources measurement focus and the accmal basis of accounting, as are proprietary fiind financial statements. Revenues are recorded when eamed and expenses are recorded when a liability is incurred, regardless of the fiming of related cash flows. Property taxes are recognized as revenues in the year for which they are levied. Grants and similar items are recognized as revenue as soon as all eligibility requirements have been met.

Govemment fund fmancial statements are reported using the current fmancial resources measurement focus and the modified accmal basis of accounting. Revenues are recognized as soon as they are both measurable and available. Revenues are considered to be available when they are collectible within the current period or soon enough thereafter to pay liabilities of the current period. The Village considers revenues to be available if they are collected within 60 days of the end of the current fiscal period. Expenditures generally are recorded when a liability is incurred, as under accmal accounting. However, debt service expenditures, as well as expenditures related to compensated absences are recorded only when payment is due.

Substantially all non-intergovemmental revenues are susceptible to accmal and are recognized when eamed or the underlying transaction occurs. Those revenues susceptible to accmal are, franchise taxes, interest revenue, licenses, intergovemmental revenues, and charges for services. Permits, penalties and interest, and miscellaneous revenues are not susceptible to accmal because generally they are not measurable until received in cash. Grants and similar items are recognized as revenues as soon as all eligibility requirements have been met. In reimbursement type programs, monies must be expended on the specific purpose or

12

VILLAGE OF LONGSTREET LONGSTREET, LOUISIANA

NOTES TO FINANCIAL STATEMENTS JUNE 30,2011

project before any amounts will be paid to the Village; therefore revenues are recognized based upon the expenditures recorded. In other programs in which monies are virtually unrestricted as to purpose of expenditure and are usually revocable only for failure to comply with prescribed compliance requirements, the resources are reflected as revenues at the time of receipt or earlier if the susceptible to accmal criteria are met and all other eligibility requirements are met.

The accounts of the Village are organized on the basis of funds, each of which Is considered a separate accounting entity. The operations of each fund are accounted for with a separate set of self-balancing accounts that comprise its assets, liabilities, fimd balance/net assets, revenues expenditures/expenses and other changes in fund balance/net assets. The various fimds are summarized by type in the financial statements. The Village has only one fund, as follows:

Govemmental Funds -

General Fund

The General Fund is the general operating fund of the Village. It is used to account for all financial resources except those required to be accounted for in another fund.

The Village applies all applicable GASB pronouncements in accounting and reporting for its govemment-wide and business-type activities and its enterprise fiinds as well as the following pronouncements issued on or before November 30, 1989, unless those pronouncements conflict with or contradict GASB pronouncements, Financial Accounting Standards Board Statements and interpretations. Accounting Principles Board opinions, and Accounting Research Bulletins.

When both restricted and unrestricted resources are available for use, it is the Village's policy to use unrestricted resources first, the restricted resources as they are needed.

Capital assets

Capital assets which include property, plant, equipment and infrastmcture assets are reported in the applicable govemmental or business-type activities columns in the govemment-wide financial statements. Capital assets are capitalized at historical cost or estimated historical cost based upon like items. The Village, a phase 3 govemment, in accordance with GASB 34, has not retroactively reported infrastmcture assets. As of July 1, 2008, the Village implemented a policy of capitalizing all infrastmcture assets with a cost of $10,000 or more. All other assets are capitalized based on thresholds of $1,500 to $10,000, depending on asset classification, except land and constmction in progress which are capitalized at cost.

Capital assets are not reported in the govemmental fund financial statements.

The cost of normal maintenance and repairs that do not extend the assets lives or add value are not capitalized.

13

VILLAGE OF LONGSTREET LONGSTREET, LOUISIANA

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2011

Depreciation has been provided over the estimated useful lives using the straight-line method. The estimated useful lives vary from 25 to 60 years.

Budget practices

Prior to July 1, the Mayor submits to the Board of Aldermen a proposed budget for the ensuing fiscal year that includes proposed expenditures and the means of financing them. The budget is enacted through the passage of a resolution.

Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect certain reported amounts and disclosures. Accordingly, actual results could differ from those estimates.

(2) Pending Litigation

The Village of Longstreet is not involved in any litigation at June 30, 2011.

(3) Cash

All bank deposits are secured through federal depository insurance.

(4) Compensation paid to Mayor and Council

The following refiects compensation paid to the Mayor and members of the Village Council for the year ended June 30,2011:

Mayor Sue Fields $ 2,400

Council Members: Queenie Rogers 1,200 Billy G Lee 900 Connie Jackson 1,200

(5) Accounts Receivable

Accounts receivable at June 30,2011, consisted of revenue from non-potable water sales and franchise fees.

14

VILLAGE OF LONGSTREET LONGSTREET, LOUISIANA

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2011

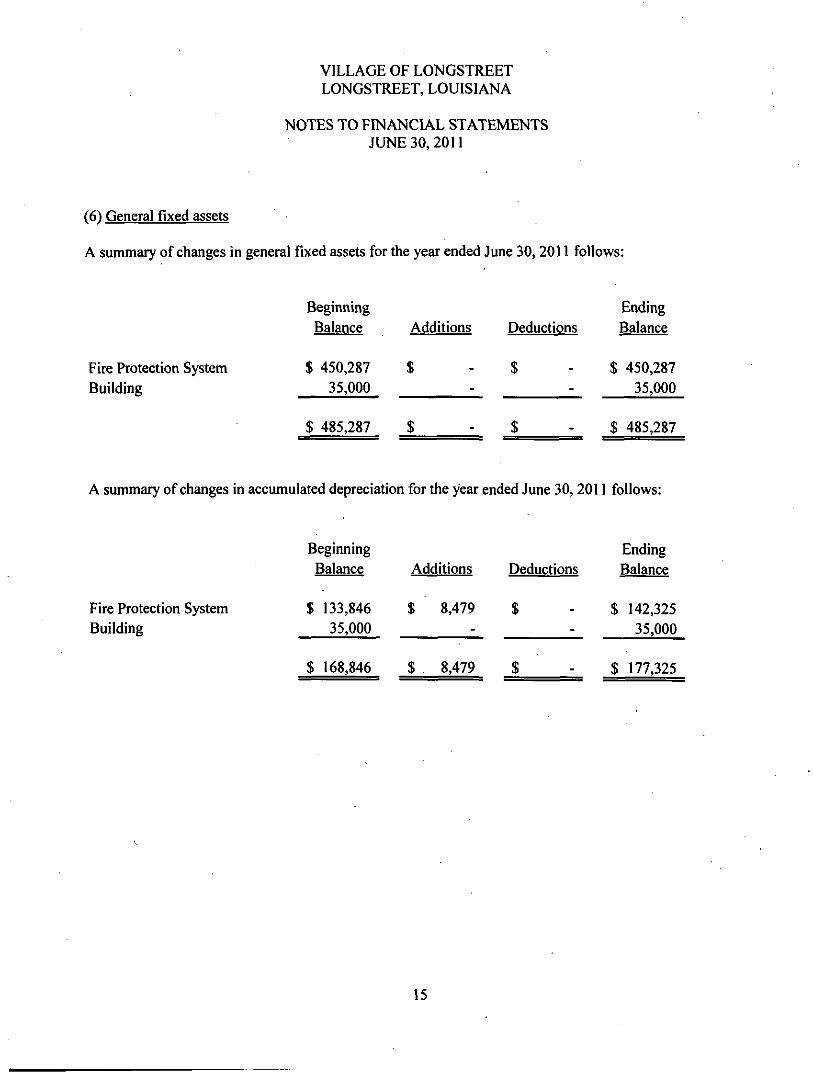

(6) General fixed assets

A summary of changes in general fixed assets for the year ended June 30,2011 follows:

Beginning Ending Balance Additions Deductions Balance

Fire Protection System $ 450,287 $ - $ - $ 450,287 Building 35,000 -__ -_ 35,000

$ 485,287 $ - $ - $ 485,287

A summary of changes in accumulated depreciation for the year ended June 30, 2011 follows:

Beginning Ending Balance Additions Deductions Balance

Fire Protection System $ 133,846 $ 8,479 $ - $ 142,325 Building 35,000 - - 35,000

$ 168,846 $ 8,479 $ - $ 177,325

15

OTHER REPORTS REQUIRED BY GOVERNMENT AUDITING STANDARDS

16

VILLAGE OF LONGSTREET LONGSTREET, LOUISIANA

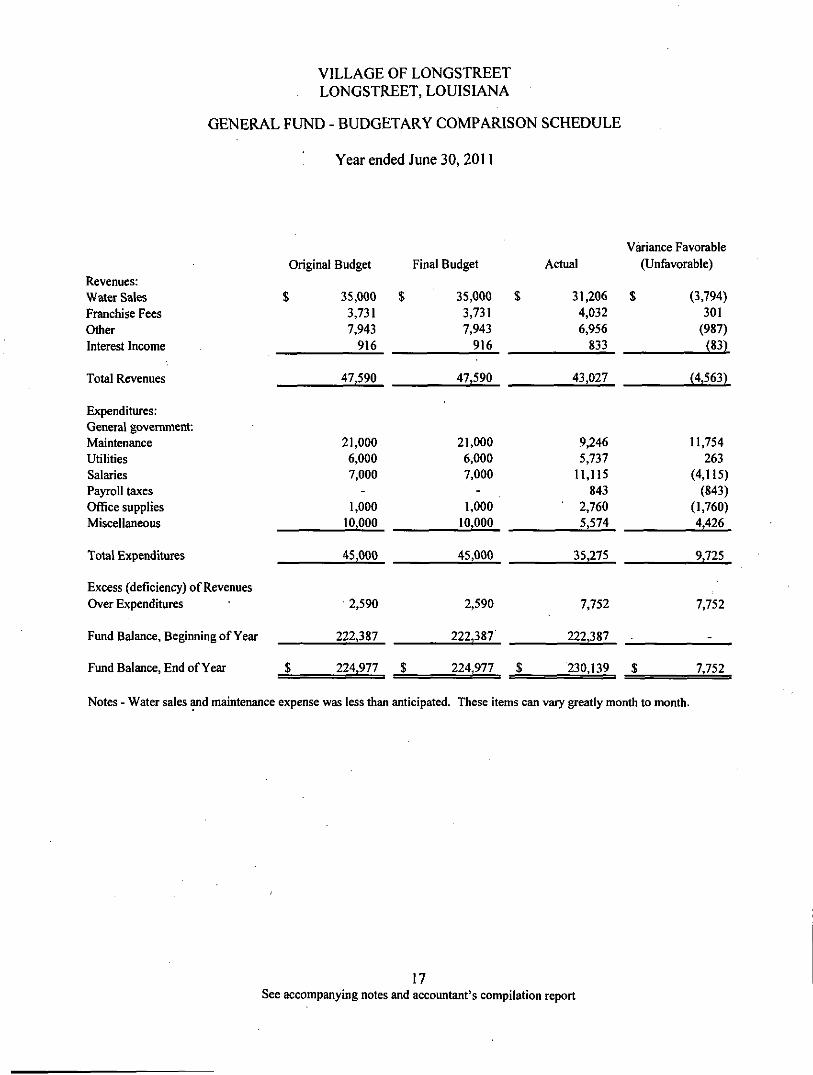

GENERAL FUND - BUDGETARY COMPARISON SCHEDULE

Year ended June 30, 2011

Revenues: Water Sales Franchise Fees Other Interest Income

Total Revenues

Expenditures: General govemment: Maintenance Utilities Salaries Payroll taxes Office supplies Miscellaneous

Total Expenditures

Excess (deficiency) of Revenues Over Expenditures

Fund Balance, Beginning of Year

Fund Balance, End of Year

Original Budget

$

$

35,000 3,731 7,943

916

47,590

21,000 6,000 7,000

-1,000

10,000

45,000

2,590

222,387

224,977

Final Budget

$ 35,000 $ 3,731 7,943

916

47,590

21,000 6,000 7,000

-1,000

10,000

45,000

2,590

222,387

$ 224,977 S

Actual

31,206 4,032 6,956

833

43,027

9,246 5,737

11,115 843

• 2,760 5,574

35,275

7,752

222,387

230,139

Variance Favorable (Unfavorable)

$ (3,794) 301

(987) (83)

(4,563)

11,754 263

(4,115) (843)

(1,760) 4,426

9,725

7,752

_

$ 7,752

Notes - Water sales and maintenance expense was less than anticipated. These items can vary greatly month to month.

17 See accompanying notes and accountant's compilation report

VILLAGE OF LONGSTREET LONGSTREET, LOUISIANA

SCHEDULE OF FINDINGS JUNE 30, 2011

PRIOR YEAR FINDINGS

None

CURRENT YEAR FINDINGS

Finding number 201 l-I

Actual revenues for the year were 9.6% below the Village's budget; therefore the Village was not in compliance with the State Budget Law. If actual revenues are expected to fall below 5% of the budgeted revenues, the law requires the budget to be amended, however the budget was not amended. The Village revenues consist primarily of sales of non-potable water to drilling companies and these revenues can vary significantly from month to month, thereby making it difficult to project revenues.

Recommendation

The Village Council should amend the budget, if appropriate, to comply with the State Budget Law.

Action taken

The Council will amend, if appropriate, the budget to comply with the State Budget Law.

18