Embed Size (px)

Citation preview

12/2/2008

1

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 1

Time SeriesTime Series EconometricsEconometrics

1010

VijayamohananVijayamohanan PillaiPillai NN

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 2

Panel Data AnalysisPanel Data Analysis

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 3

Badi H. BaltagiBadi H. Baltagi 20052005 Econometric Analysis of PanelEconometric Analysis of Panel

DataData, 3, 3rdrd Edition, John Wiley and Sons.Edition, John Wiley and Sons.

Cheng HsiaoCheng Hsiao 20032003 Analysis of Panel DataAnalysis of Panel Data, 2, 2ndnd

Edition, Cambridge University Press.Edition, Cambridge University Press.

Edward W FreesEdward W Frees 20042004 Longitudinal and Panel DataLongitudinal and Panel Data

Analysis and Applications in the Social SciencesAnalysis and Applications in the Social Sciences

Cambridge University Press.Cambridge University Press.

Panel Data AnalysisPanel Data Analysis

ReferencesReferences

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 4

Manuel ArellanoManuel Arellano 20032003 Panel Data EconometricsPanel Data Econometrics

Oxford University PressOxford University Press

Jeffrey M WooldridgeJeffrey M Wooldridge 20012001 Econometric Analysis ofEconometric Analysis of

Cross Section and Panel DataCross Section and Panel Data The MIT Press.The MIT Press.

Panel Data AnalysisPanel Data Analysis

ReferencesReferences

12/2/2008

2

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 5

Panel (Longitudinal) Data:Panel (Longitudinal) Data:

AA data setdata set containingcontaining observations on multipleobservations on multiple

phenomenaphenomena observed overobserved over multiple time periodsmultiple time periods..

TwoTwo--dimensional:dimensional:

Time seriesTime series andand

CrossCross--sectional.sectional.

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 6

xit refers to an independent variable for a given

case (i) and time point (t)

Often, i is referred to as n

Often talk about data as case, time

For example:

country, years

group, months

president, elections

NomenclatureNomenclature

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 7

CountryCountry YearYear PDYPDY PEPE Median HHYMedian HHY

UtopiaUtopia 19901990 65006500 50005000 125000125000

UtopiaUtopia 19911991 70007000 60006000 140000140000

………… ………… ………… ………… …………

………… ………… ………… ………… …………

UtopiaUtopia 20082008 1500015000 1100011000 455000455000

LilliputLilliput 19901990 15001500 13001300 2500025000

LilliputLilliput 19911991 17001700 16001600 2800028000

………… ………… ………… ………… …………

………… ………… ………… ………… …………

LilliputLilliput 20082008 54505450 50005000 980000980000

TroyTroy 19901990 22002200 18001800 4500045000

TroyTroy 19911991 24002400 20002000 6000060000

………… ………… ………… ………… …………

………… ………… ………… ………… …………

TroyTroy 20082008 85008500 75007500 125000125000

A Typical Panel Data SetA Typical Panel Data Set

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 8

Time is nested within the crossTime is nested within the cross--sectionsection

in this example.in this example.

PossiblePossible forfor thethe crosscross--sectionssections toto bebe nestednested

withinwithin timetime..

No missing valuesNo missing values

= the data set is a= the data set is a balanced panelbalanced panel,,

If there areIf there are missing valuesmissing values

= the data set is an= the data set is an unbalanced panelunbalanced panel..

Typical Panel Data SetTypical Panel Data Set

12/2/2008

3

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 9

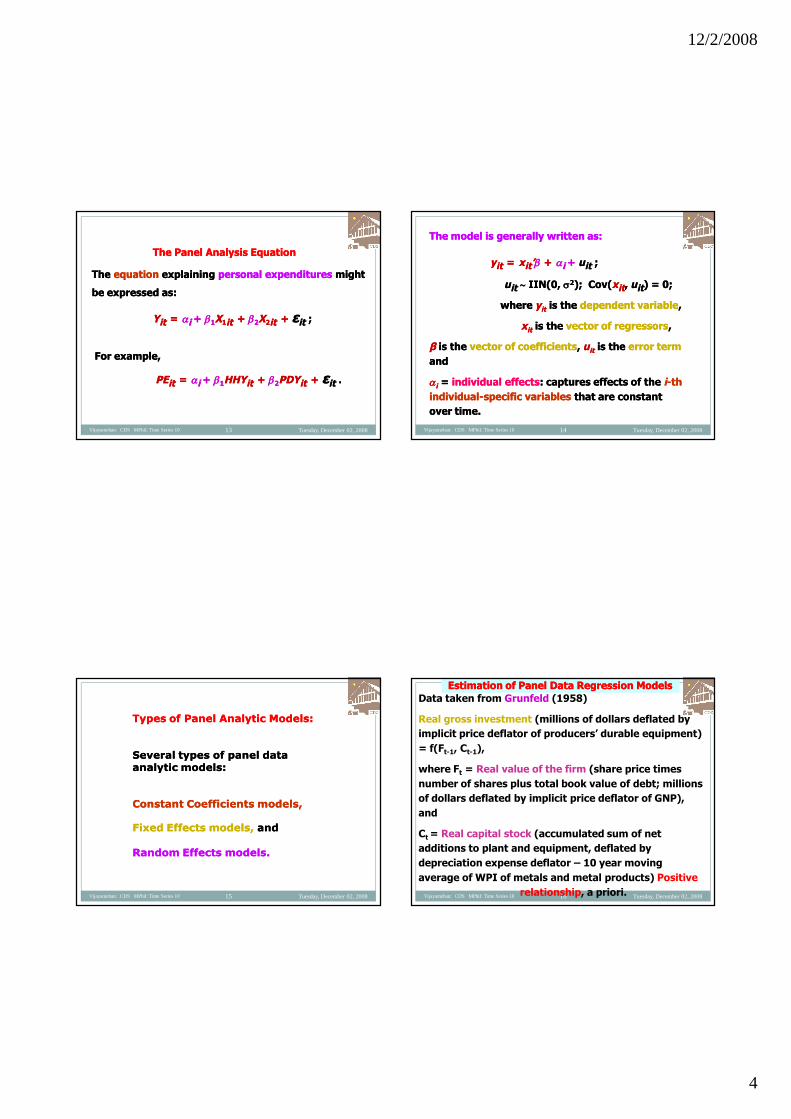

Balanced panelBalanced panel Unbalanced PanelUnbalanced Panel

PersonPersonSl NoSl No

YearYear IncomeIncome AgeAge SexSex PersonPersonSl NoSl No

YearYear IncomeIncome AgeAge SexSex

11 20062006 800800 4545 11 11 20072007 17501750 3232 11

11 20072007 900900 4646 11 11 20082008 25002500 3333 11

11 20082008 10001000 4747 11 22 20062006 20002000 4040 22

22 20062006 15001500 2929 22 22 20072007 25002500 4141 22

22 20072007 20002000 3030 22 22 20082008 28002800 4242 22

22 20082008 25002500 3131 22 33 20082008 25002500 2828 22

Balanced and Unbalanced PanelBalanced and Unbalanced Panel

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 10

Increases the number of observations

Multiply N by T

In one study, N = 50 cases, 29 years aggregated

monthly, creating 17,400 data points

Ability to model time and space as well as

generalize across them

Conceptually, this is very important

Time-series component increases one’s ability to

show/argue causation

Advantages of TSCSAdvantages of TSCS

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 11

Heteroskedasticity

Errors do not have the same variance

Autocorrelation

Errors are correlated

Last time period’s values affect current values

Spatial autocorrelation: shock in one country affects

neighboring countries

DisadvantagesDisadvantages

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 12

Typical heteroskedasticity and autocorrelation

Multiple cases increase the probability that you

will have heteroskedasticity

Cross-case autocorrelation

Correlation at same time point across cases (rise in oil

prices hits all nations)

Correlation at different time points across cases

(development aid from one country impacts another

country’s growth)

Disadvantages Specific to TSCSDisadvantages Specific to TSCS

12/2/2008

4

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 13

TheThe PanelPanel AnalysisAnalysis EquationEquation

TheThe equationequation explainingexplaining personalpersonal expendituresexpenditures mightmight

bebe expressedexpressed asas::

YYitit == ii ++ 11XX11itit ++ 22XX22itit ++ εεitit ;;

ForFor example,example,

PEPEitit == ii ++ 11HHYHHYitit ++ 22PDYPDYitit ++ εεitit ..

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 14

The model is generally written as:The model is generally written as:

yyitit == xxitit’’ ++ ii ++ uuitit ;;

uuitit IIN(0,IIN(0, 22); Cov(); Cov(xxitit,, uuitit) = 0;) = 0;

wherewhere yyitit is theis the dependent variabledependent variable,,

xxitit is theis the vector of regressorsvector of regressors,,

ββ is theis the vector of coefficientsvector of coefficients,, uuitit is theis the error termerror term

andand

ii == individual effectsindividual effects: captures effects of the: captures effects of the ii--thth

individualindividual--specific variablesspecific variables that are constantthat are constant

over time.over time.

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 15

TypesTypes ofof PanelPanel AnalyticAnalytic ModelsModels::

Several types of panel dataSeveral types of panel dataanalytic models:analytic models:

Constant Coefficients models,Constant Coefficients models,

Fixed Effects models,Fixed Effects models, andand

Random Effects models.Random Effects models.

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 16

Data taken from Grunfeld (1958)

Real gross investment (millions of dollars deflated by

implicit price deflator of producers’ durable equipment)

= f(Ft-1, Ct-1),

where Ft = Real value of the firm (share price times

number of shares plus total book value of debt; millions

of dollars deflated by implicit price deflator of GNP),

and

Ct = Real capital stock (accumulated sum of net

additions to plant and equipment, deflated by

depreciation expense deflator – 10 year moving

average of WPI of metals and metal products) Positive

relationship, a priori.

Estimation of Panel Data Regression ModelsEstimation of Panel Data Regression Models

12/2/2008

5

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 17

We consider only four companies:

General Electric (GE),

General Motor (GM),

US Steel (US) and

Westinghouse (WEST),

for the period 1935-1954.

Four cross sectional units

20 time periods – 80 observations.

Estimation of Panel Data Regression ModelsEstimation of Panel Data Regression Models

Data PDA.xls

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 18

Consider our model:Consider our model:

IIitit == ii ++ 11FFtt--11 ++ 22CCtt--11 ++ uuitit ;;

uuitit IIN(0,IIN(0, 22););

i = 1, 2, 3, 4; t = 1, 2, …, 20.

Two cases:

Case 1: Heterogeneous intercepts (ii jj ),

homogeneous slope (ii == jj) :) :

Case 2:

Heterogeneous intercepts and slopes

(ii jj ); (ii jj))

Estimation of Panel Data Regression ModelsEstimation of Panel Data Regression Models

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 19

Esti

ma

tio

no

fP

an

el

Da

taE

sti

ma

tio

no

fP

an

el

Da

ta

Re

gre

ssio

nM

od

els

Re

gre

ssio

nM

od

els

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 20

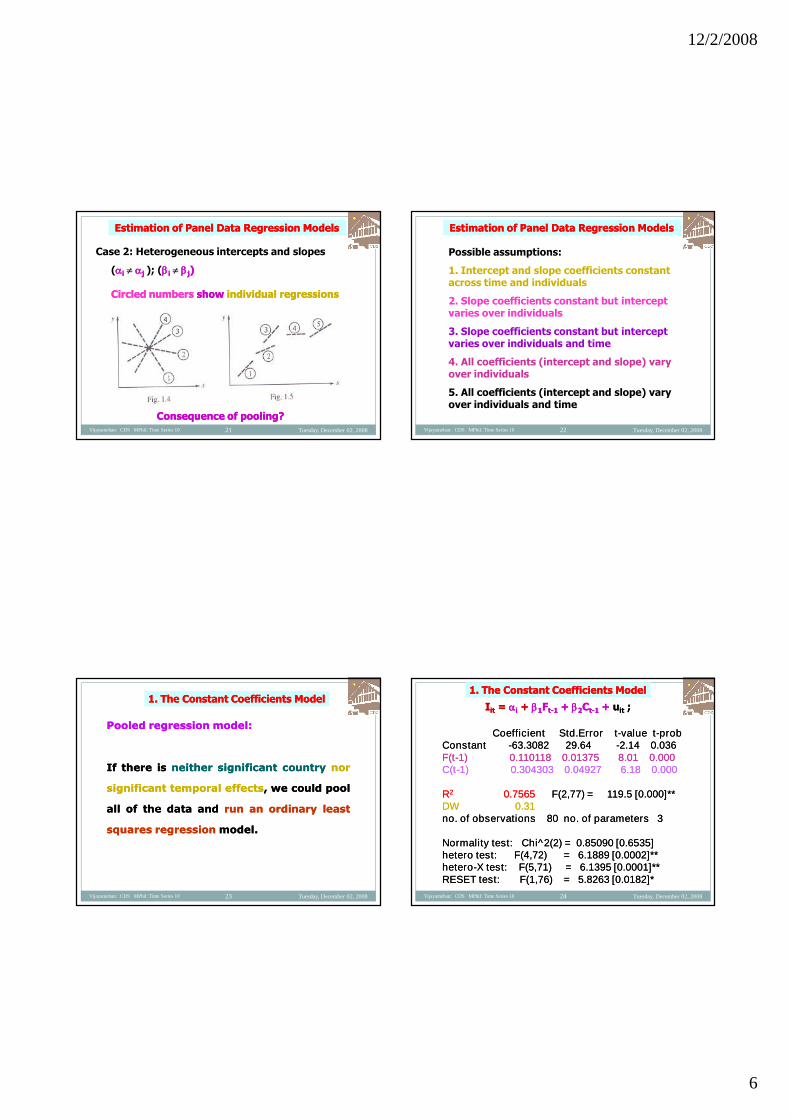

Case 1: (ii jj ), and (ii == jj)) ::

BrokenBroken line ellipsesline ellipses –– point scatter for eachpoint scatter for each individualindividual

//firmfirm over timeover time

BrokenBroken straight linestraight line –– individual regressionsindividual regressions

SolidSolid lineline –– Pooled regression with NT observationsPooled regression with NT observations

ConsequenceConsequence of pooling?of pooling?

Estimation of Panel Data Regression ModelsEstimation of Panel Data Regression Models

12/2/2008

6

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 21

Case 2: Heterogeneous intercepts and slopes

(ii jj ); (ii jj))

Circled numbersCircled numbers showshow individual regressionsindividual regressions

ConsequenceConsequence of pooling?of pooling?

Estimation of Panel Data Regression ModelsEstimation of Panel Data Regression Models

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 22

Possible assumptions:

1. Intercept and slope coefficients constantacross time and individuals

2. Slope coefficients constant but interceptvaries over individuals

3. Slope coefficients constant but interceptvaries over individuals and time

4. All coefficients (intercept and slope) varyover individuals

5. All coefficients (intercept and slope) varyover individuals and time

Estimation of Panel Data Regression ModelsEstimation of Panel Data Regression Models

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 23

PooledPooled regressionregression modelmodel::

IfIf therethere isis neitherneither significantsignificant countrycountry nornor

significantsignificant temporaltemporal effectseffects,, wewe couldcould poolpool

allall ofof thethe datadata andand runrun anan ordinaryordinary leastleast

squaressquares regressionregression modelmodel..

1. The Constant Coefficients Model1. The Constant Coefficients Model

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 24

CoefficientCoefficient Std.ErrorStd.Error tt--value tvalue t--probprobConstantConstant --63.3082 29.6463.3082 29.64 --2.14 0.0362.14 0.036F(tF(t--1) 0.110118 0.01375 8.01 0.0001) 0.110118 0.01375 8.01 0.000C(tC(t--1) 0.304303 0.04927 6.18 0.0001) 0.304303 0.04927 6.18 0.000

RR22 0.75650.7565 F(2,77) = 119.5 [0.000]**F(2,77) = 119.5 [0.000]**DW 0.31DW 0.31no. of observations 80 no. of parameters 3no. of observations 80 no. of parameters 3

Normality test: Chi^2(2) = 0.85090 [0.6535]Normality test: Chi^2(2) = 0.85090 [0.6535]hetero test: F(4,72) = 6.1889 [0.0002]**hetero test: F(4,72) = 6.1889 [0.0002]**heterohetero--X test: F(5,71) = 6.1395 [0.0001]**X test: F(5,71) = 6.1395 [0.0001]**RESET test: F(1,76) = 5.8263 [0.0182]*RESET test: F(1,76) = 5.8263 [0.0182]*

1. The Constant Coefficients Model1. The Constant Coefficients Model

IIitit == ii ++ 11FFtt--11 ++ 22CCtt--11 ++ uuitit ;;

12/2/2008

7

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 25

No significant temporal effects,

But significant differences among companies.

That is, a linear regression model in which the

intercept terms vary over individual units:

yit = xit + i + uit ;

uit IIN(0, 2);

Cov(xit, uis) = 0; t and s

2. The Fixed Effects Model:2. The Fixed Effects Model:(Least Squares Dummy Variable Model):(Least Squares Dummy Variable Model):

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 26

yyitit == xxitit ++ ii ++ uuitit ;;

Possible toPossible to include a dummy variableinclude a dummy variable forfor eacheach

unitunit ii in the model:in the model:

yyitit == xxitit ++ iiddii ++ uuitit ;;

Four Companies:Four Companies:

Three dummiesThree dummies

Additive

2. The Fixed Effects Model:2. The Fixed Effects Model:

Constant Slope; Variable InterceptConstant Slope; Variable Intercept

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 27

yyitit == xxitit ++ iiddii ++ uuitit ;;

For example,For example,

YYitit ==11 ++22DD22ii ++33DD33ii ++44DD44ii ++ 11XX11itit ++ 22XX22itit ++ εεitit ;;

wherewhere DD22ii = 1 for GM; and= 1 for GM; and zero otherwisezero otherwise..

DD33ii = 1 for US; and= 1 for US; and zero otherwisezero otherwise..

DD44ii = 1 for WEST; and= 1 for WEST; and zero otherwisezero otherwise..

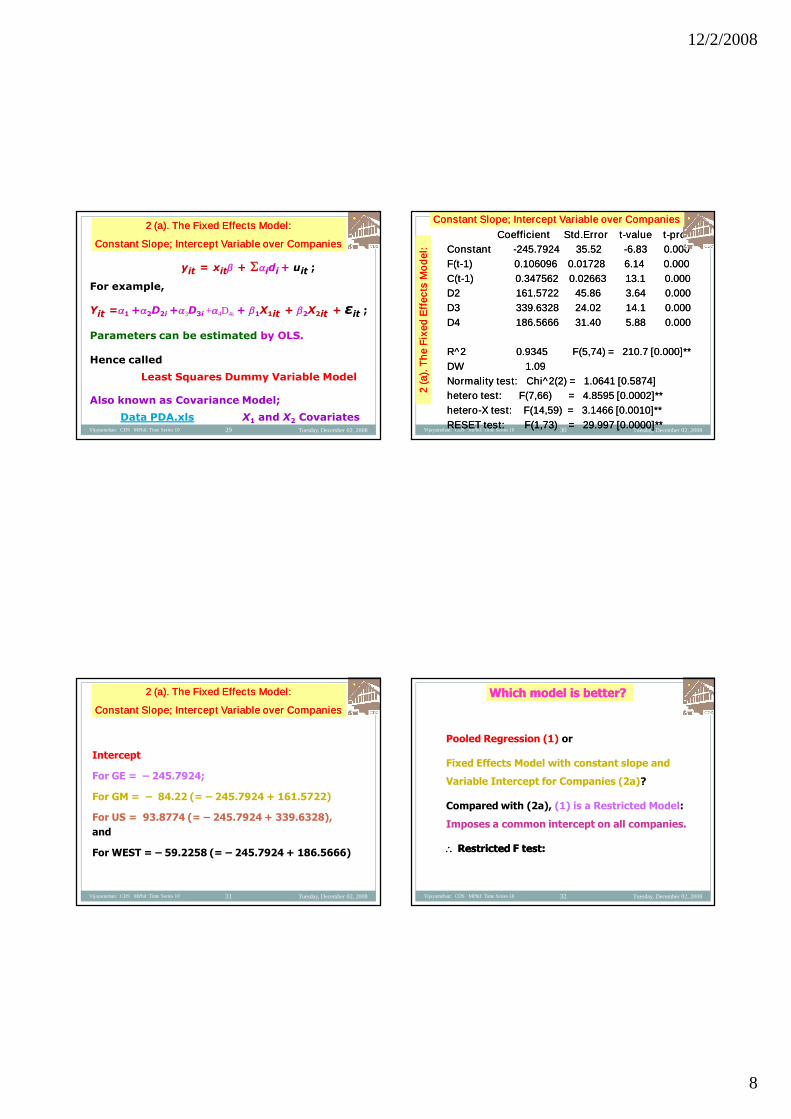

2 (a). The Fixed Effects Model:2 (a). The Fixed Effects Model:

Constant Slope; Intercept Variable over CompaniesConstant Slope; Intercept Variable over Companies

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 28

YYitit ==11 ++22DD22ii ++33DD33ii ++44DD44ii ++ 11XX11itit ++ 22XX22itit ++ εεitit ;;

Base company: GE

Intercept for GE = 11

If all s statistically significant, differential intercepts.

For example, if 11 and 22 significant,

intercept for GM = 11 ++22

2 (a). The Fixed Effects Model:2 (a). The Fixed Effects Model:

Constant Slope; Intercept Variable over CompaniesConstant Slope; Intercept Variable over Companies

12/2/2008

8

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 29

yit = xit + idi + uit ;

For example,

Yit =1 +2D2i +3D3i +4D4i + 1X1it + 2X2it + εit ;

Parameters can be estimated by OLS.

Hence called

Least Squares Dummy Variable Model

Also known as Covariance Model;

Data PDA.xls X1 and X2 Covariates

2 (a). The Fixed Effects Model:2 (a). The Fixed Effects Model:

Constant Slope; Intercept Variable over CompaniesConstant Slope; Intercept Variable over Companies

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 30

CoefficientCoefficient Std.ErrorStd.Error tt--value tvalue t--probprob

ConstantConstant --245.7924 35.52245.7924 35.52 --6.83 0.0006.83 0.000

F(tF(t--1) 0.106096 0.01728 6.14 0.0001) 0.106096 0.01728 6.14 0.000

C(tC(t--1) 0.347562 0.02663 13.1 0.0001) 0.347562 0.02663 13.1 0.000

D2 161.5722 45.86 3.64 0.000D2 161.5722 45.86 3.64 0.000

D3 339.6328 24.02 14.1 0.000D3 339.6328 24.02 14.1 0.000

D4 186.5666 31.40 5.88 0.000D4 186.5666 31.40 5.88 0.000

R^2 0.9345 F(5,74) = 210.7 [0.000]**R^2 0.9345 F(5,74) = 210.7 [0.000]**

DW 1.09DW 1.09

Normality test: Chi^2(2) = 1.0641 [0.5874]Normality test: Chi^2(2) = 1.0641 [0.5874]

hetero test: F(7,66) = 4.8595 [0.0002]**hetero test: F(7,66) = 4.8595 [0.0002]**

heterohetero--X test: F(14,59) = 3.1466 [0.0010]**X test: F(14,59) = 3.1466 [0.0010]**

RESET test: F(1,73) = 29.997 [0.0000]**RESET test: F(1,73) = 29.997 [0.0000]**2

(a).

Th

eF

ixe

dE

ffe

cts

Mo

de

l2

(a).

Th

eF

ixe

dE

ffe

cts

Mo

de

l::

ConstantConstant Slope; Intercept Variable over CompaniesSlope; Intercept Variable over Companies

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 31

Intercept

For GE = – 245.7924;

For GM = – 84.22 (= – 245.7924 + 161.5722)

For US = 93.8774 (= – 245.7924 + 339.6328),

and

For WEST = – 59.2258 (= – 245.7924 + 186.5666)

2 (a). The Fixed Effects Model:2 (a). The Fixed Effects Model:

Constant Slope; Intercept Variable over CompaniesConstant Slope; Intercept Variable over Companies

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 32

Pooled Regression (1) or

Fixed Effects Model with constant slope and

Variable Intercept for Companies (2a)?

Compared with (2a), (1) is a Restricted Model:

Imposes a common intercept on all companies.

Restricted F test:Restricted F test:

Which model is better?Which model is better?

12/2/2008

9

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 33

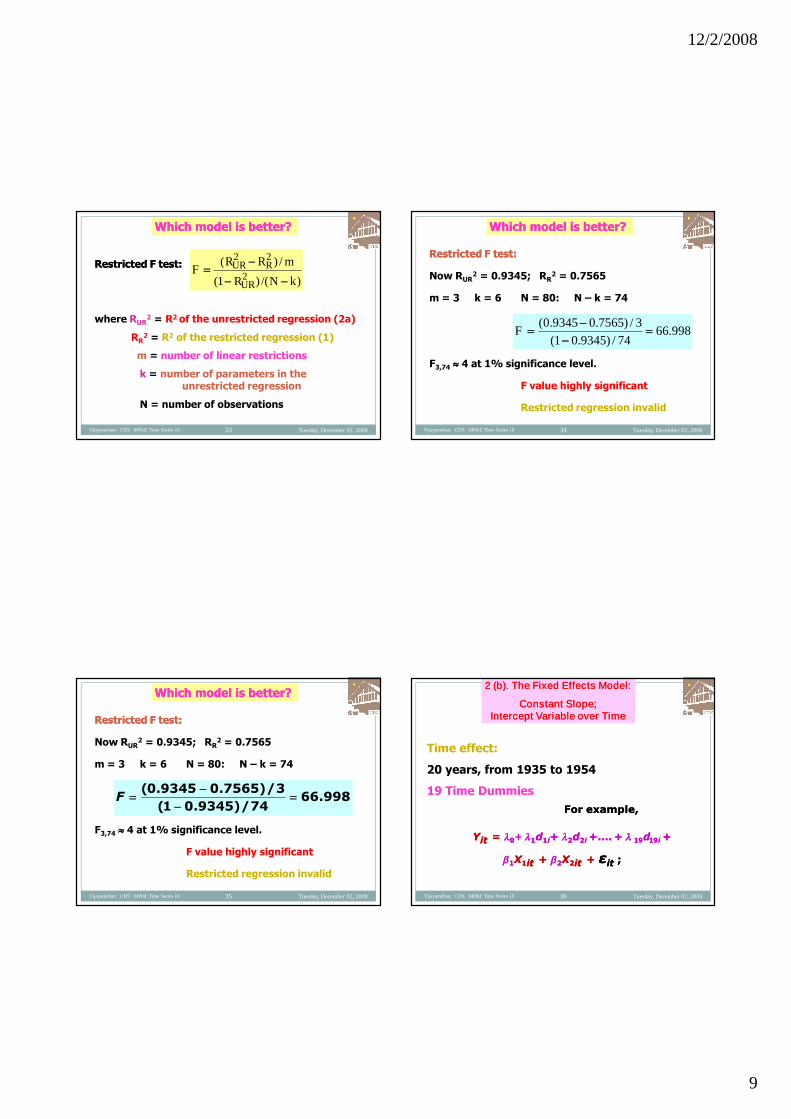

Restricted F test:Restricted F test:

where RUR2 = R2 of the unrestricted regression (2a)

RR2 = R2 of the restricted regression (1)

m = number of linear restrictions

k = number of parameters in theunrestricted regression

N = number of observations

)/()1(

/)(2

22

kNR

mRRF

UR

RUR

Which model is better?Which model is better?

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 34

Restricted F test:Restricted F test:

Now RUR2 = 0.9345; RR

2 = 0.7565

m = 3 k = 6 N = 80: N – k = 74

F3,74 4 at 1% significance level.

F value highly significant

Restricted regression invalid

998.6674/)9345.01(

3/)7565.09345.0(

F

Which model is better?Which model is better?

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 35

Restricted F test:Restricted F test:

Now RUR2 = 0.9345; RR

2 = 0.7565

m = 3 k = 6 N = 80: N – k = 74

F3,74 4 at 1% significance level.

F value highly significant

Restricted regression invalid

998.6674/)9345.01(

3/)7565.09345.0(

F

Which model is better?Which model is better?

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 36

Time effect:

20 years, from 1935 to 1954

19 Time Dummies

For example,For example,

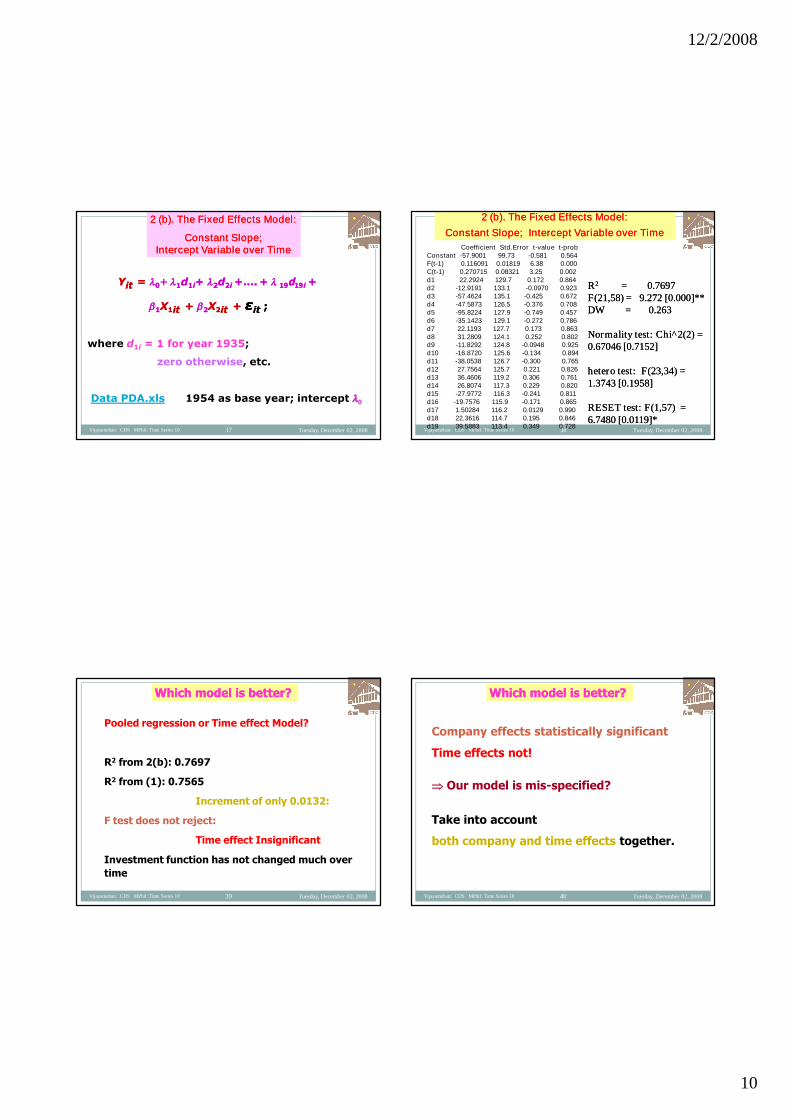

YYitit == 00+ 11dd11ii++ 22dd22ii +….+…. ++ 1919dd1919ii ++

11XX11itit ++ 22XX22itit ++ εεitit ;;

2 (b). The Fixed Effects Model:2 (b). The Fixed Effects Model:

Constant Slope;Constant Slope;Intercept Variable over TimeIntercept Variable over Time

12/2/2008

10

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 37

YYitit == 00+ 11dd11ii++ 22dd22ii +….+…. ++ 1919dd1919ii ++

11XX11itit ++ 22XX22itit ++ εεitit ;;

where d1i = 1 for year 1935;

zero otherwise, etc.

Data PDA.xls 1954 as base year; intercept 00

2 (b). The Fixed Effects Model:2 (b). The Fixed Effects Model:

Constant Slope;Constant Slope;Intercept Variable over TimeIntercept Variable over Time

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 38

Coefficient Std.Error t-value t-probConstant -57.9001 99.73 -0.581 0.564F(t-1) 0.116091 0.01819 6.38 0.000C(t-1) 0.270715 0.08321 3.25 0.002d1 22.2924 129.7 0.172 0.864d2 -12.9191 133.1 -0.0970 0.923d3 -57.4624 135.1 -0.425 0.672d4 -47.5873 126.5 -0.376 0.708d5 -95.8224 127.9 -0.749 0.457d6 -35.1423 129.1 -0.272 0.786d7 22.1193 127.7 0.173 0.863d8 31.2809 124.1 0.252 0.802d9 -11.8292 124.8 -0.0948 0.925d10 -16.8720 125.6 -0.134 0.894d11 -38.0538 126.7 -0.300 0.765d12 27.7564 125.7 0.221 0.826d13 36.4606 119.2 0.306 0.761d14 26.8074 117.3 0.229 0.820d15 -27.9772 116.3 -0.241 0.811d16 -19.7576 115.9 -0.171 0.865d17 1.50284 116.2 0.0129 0.990d18 22.3616 114.7 0.195 0.846d19 39.5883 113.4 0.349 0.728

RR22 = 0.7697= 0.7697F(21,58) =F(21,58) = 9.272 [0.0009.272 [0.000]**]**DW = 0.263DW = 0.263

Normality test: Chi^2(2) =Normality test: Chi^2(2) =0.67046 [0.7152]0.67046 [0.7152]

hetero test: F(23,34) =hetero test: F(23,34) =1.37431.3743 [[0.1958]0.1958]

RESET test: F(1,57) =RESET test: F(1,57) =6.74806.7480 [[0.0119]*0.0119]*

2 (b). The Fixed Effects Model:2 (b). The Fixed Effects Model:

Constant Slope;Constant Slope; InterceptIntercept Variable over TimeVariable over Time

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 39

Pooled regression or Time effect Model?

R2 from 2(b): 0.7697

R2 from (1): 0.7565

Increment of only 0.0132:

F test does not reject:

Time effect Insignificant

Investment function has not changed much over

time

Which model is better?Which model is better?

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 40

Company effects statistically significant

Time effects not!

Our model is mis-specified?

Take into account

both company and time effects together.

Which model is better?Which model is better?

12/2/2008

11

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 41

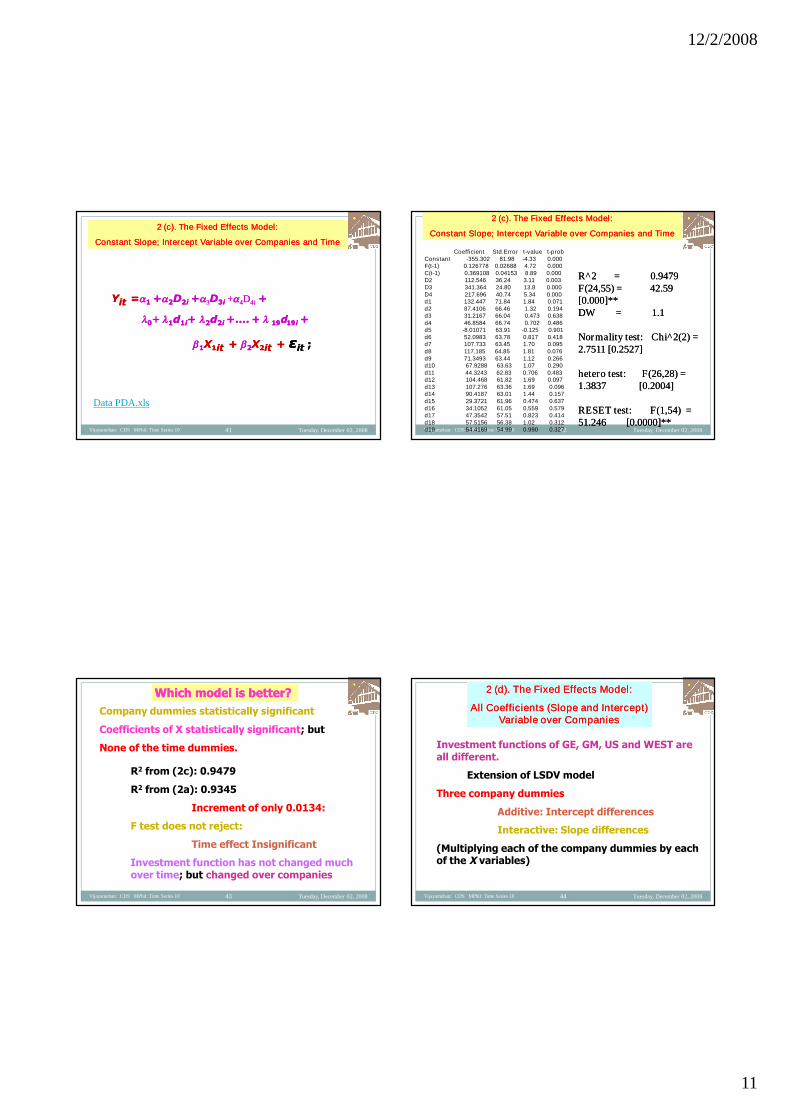

00+ 11dd11ii++ 22dd22ii +….+…. ++ 1919dd1919ii ++

11XX11itit ++ 22XX22itit ++ εεitit ;;

YYitit ==11 ++22DD22ii ++33DD33ii ++44DD44ii ++

2 (c). The Fixed Effects Model:2 (c). The Fixed Effects Model:

Constant Slope;Constant Slope; InterceptIntercept Variable over Companies and TimeVariable over Companies and Time

Data PDA.xls

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 42

Coefficient Std.Error t-value t-probConstant -355.302 81.98 -4.33 0.000F(t-1) 0.126778 0.02688 4.72 0.000C(t-1) 0.369108 0.04153 8.89 0.000D2 112.546 36.24 3.11 0.003D3 341.364 24.80 13.8 0.000D4 217.696 40.74 5.34 0.000d1 132.447 71.84 1.84 0.071d2 87.4106 66.46 1.32 0.194d3 31.2167 66.04 0.473 0.638d4 46.8584 66.74 0.702 0.486d5 -8.01071 63.91 -0.125 0.901d6 52.0983 63.78 0.817 0.418d7 107.733 63.45 1.70 0.095d8 117.185 64.85 1.81 0.076d9 71.3493 63.44 1.12 0.266d10 67.9288 63.63 1.07 0.290d11 44.3243 62.83 0.706 0.483d12 104.468 61.82 1.69 0.097d13 107.276 63.36 1.69 0.096d14 90.4187 63.01 1.44 0.157d15 29.3721 61.96 0.474 0.637d16 34.1052 61.05 0.559 0.579d17 47.3542 57.51 0.823 0.414d18 57.5156 56.38 1.02 0.312d19 54.4169 54.99 0.990 0.327

R^2 = 0.9479R^2 = 0.9479F(24,55) = 42.59F(24,55) = 42.59[0.000]**[0.000]**DW = 1.1DW = 1.1

Normality test: Chi^2(2) =Normality test: Chi^2(2) =2.7511 [0.2527]2.7511 [0.2527]

hetero test: F(26,28) =hetero test: F(26,28) =1.38371.3837 [0.2004][0.2004]

RESET test: F(1,54) =RESET test: F(1,54) =51.24651.246 [0.0000]**[0.0000]**

2 (c). The Fixed Effects Model:2 (c). The Fixed Effects Model:

Constant Slope;Constant Slope; InterceptIntercept Variable over Companies and TimeVariable over Companies and Time

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 43

Company dummies statistically significant

Coefficients of X statistically significant; but

None of the time dummies.

R2 from (2c): 0.9479

R2 from (2a): 0.9345

Increment of only 0.0134:

F test does not reject:

Time effect Insignificant

Investment function has not changed muchover time; but changed over companies

Which model is better?Which model is better?

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 44

Investment functions of GE, GM, US and WEST areall different.

Extension of LSDV model

Three company dummies

Additive: Intercept differences

Interactive: Slope differences

(Multiplying each of the company dummies by eachof the X variables)

2 (d). The Fixed Effects Model:2 (d). The Fixed Effects Model:

All Coefficients (Slope and Intercept)All Coefficients (Slope and Intercept)Variable over CompaniesVariable over Companies

12/2/2008

12

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 45

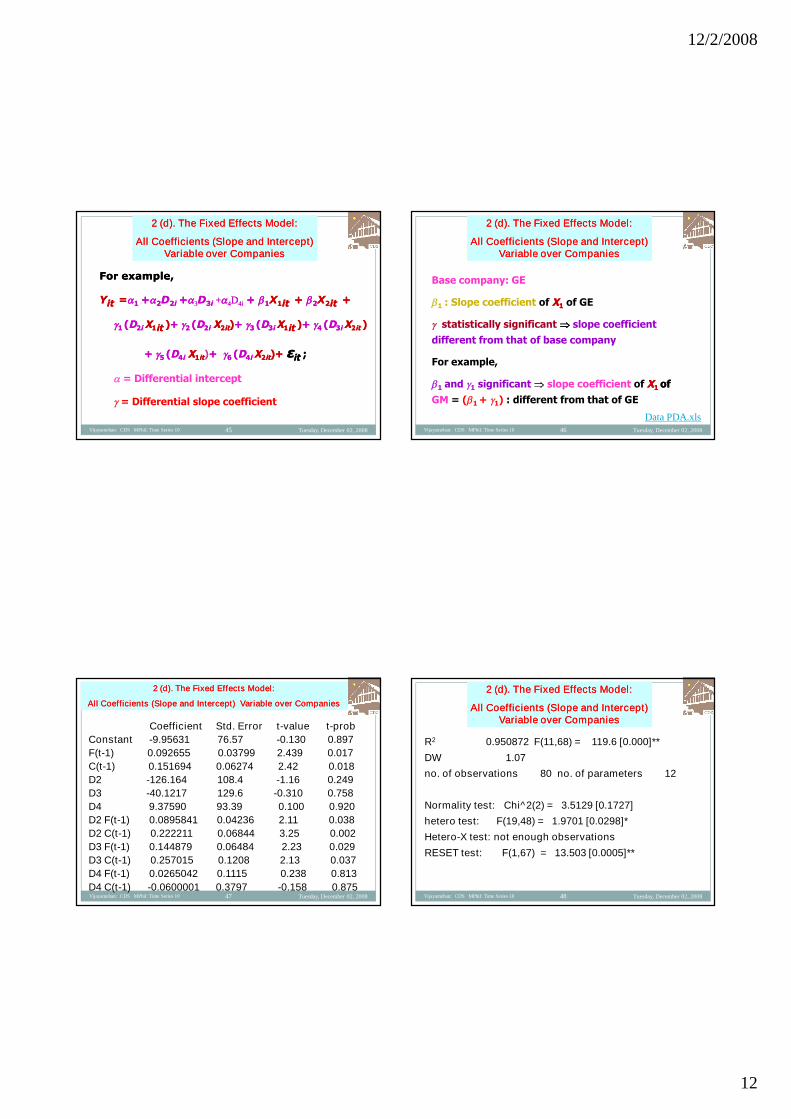

For example,For example,

YYitit ==11 ++22DD22ii ++33DD33ii ++44DD44ii ++ 11XX11itit ++ 22XX22itit ++

11 ((DD22ii XX11itit ))++ 22 ((DD22ii XX22itit))++ 33 ((DD33ii XX11itit ))++ 44 ((DD33ii XX22itit ))

++ 55 ((DD44ii XX11itit)++ 66 ((DD44ii XX22itit)+)+ εεitit ;;

= Differential intercept

= Differential slope coefficient

2 (d). The Fixed Effects Model:2 (d). The Fixed Effects Model:

All Coefficients (Slope and Intercept)All Coefficients (Slope and Intercept)Variable over CompaniesVariable over Companies

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 46

Base company: GE

1 : Slope coefficient of XX11 of GE

statistically significant slope coefficient

different from that of base company

For example,

1 and 1 significant slope coefficient of XX11 ofof

GM = (1 + 1) : different from that of GE

2 (d). The Fixed Effects Model:2 (d). The Fixed Effects Model:

All Coefficients (Slope and Intercept)All Coefficients (Slope and Intercept)Variable over CompaniesVariable over Companies

Data PDA.xls

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 47

Coefficient Std. Error t-value t-prob

Constant -9.95631 76.57 -0.130 0.897

F(t-1) 0.092655 0.03799 2.439 0.017

C(t-1) 0.151694 0.06274 2.42 0.018

D2 -126.164 108.4 -1.16 0.249

D3 -40.1217 129.6 -0.310 0.758

D4 9.37590 93.39 0.100 0.920

D2 F(t-1) 0.0895841 0.04236 2.11 0.038

D2 C(t-1) 0.222211 0.06844 3.25 0.002

D3 F(t-1) 0.144879 0.06484 2.23 0.029

D3 C(t-1) 0.257015 0.1208 2.13 0.037

D4 F(t-1) 0.0265042 0.1115 0.238 0.813

D4 C(t-1) -0.0600001 0.3797 -0.158 0.875

2 (d). The Fixed Effects Model:2 (d). The Fixed Effects Model:

All Coefficients (Slope and Intercept) Variable over CompaniesAll Coefficients (Slope and Intercept) Variable over Companies

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 48

R2 0.950872 F(11,68) = 119.6 [0.000]**

DW 1.07

no. of observations 80 no. of parameters 12

Normality test: Chi^2(2) = 3.5129 [0.1727]

hetero test: F(19,48) = 1.9701 [0.0298]*

Hetero-X test: not enough observations

RESET test: F(1,67) = 13.503 [0.0005]**

2 (d). The Fixed Effects Model:2 (d). The Fixed Effects Model:

All Coefficients (Slope and Intercept)All Coefficients (Slope and Intercept)Variable over CompaniesVariable over Companies

12/2/2008

13

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 49

2 (d). The Fixed Effects Model:2 (d). The Fixed Effects Model:

All Coefficients (Slope and Intercept)All Coefficients (Slope and Intercept)Variable over CompaniesVariable over Companies

It is significantly related to Ft-1 and Ct-1

Slope coefficients of Base company (GE) significant

Both the slope coefficients significant for GM and US

But not for WEST

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 50

1. Too many regressors:

Numerically unattractive.

df ; error variance

Possibility of multicollinearity

2. Unable to identify the impact of time-

invariant variables (sex, colour, ethnicity,

education – invariant over time)

2. The Fixed Effects (LSDV) Model: Problems2. The Fixed Effects (LSDV) Model: Problems

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 51

3. Assumption that the error term follows classical

assumptions: uit ~ N(0, 2):

For a given period, possible that the error term for

GM is correlated with the error term for, say, US

or both US and WEST.

the Seemingly Unrelated Regression (SURE)Seemingly Unrelated Regression (SURE)

modellingmodelling (Arnold Zellner; see Jan Kmenta 1986

Elements of Econometrics)

2. The Fixed Effects (LSDV) Model: Problems2. The Fixed Effects (LSDV) Model: Problems

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 52

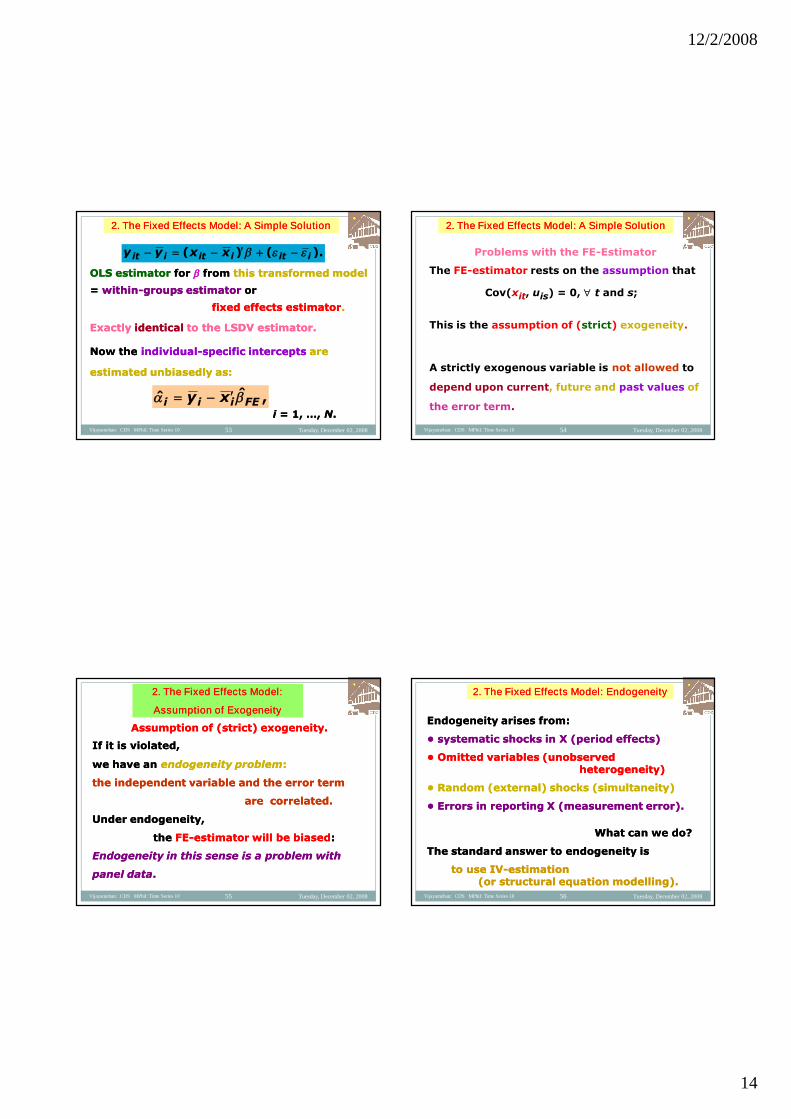

A Simple way:A Simple way:

TheThe same estimatorsame estimator forfor is obtainedis obtained if theif the

regressionregression is performedis performed inin deviations fromdeviations from

individual meansindividual means::

wherewhere

So we can writeSo we can write::

iiii xy

t iti yTy 1

).()( iitiitiit xxyy

2. The Fixed Effects (LSDV) Model: Problems2. The Fixed Effects (LSDV) Model: Problems

12/2/2008

14

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 53

OLS estimatorOLS estimator forfor fromfrom this transformed modelthis transformed model

== withinwithin--groups estimatorgroups estimator oror

fixed effects estimatorfixed effects estimator..

ExactlyExactly identicalidentical to the LSDV estimator.to the LSDV estimator.

Now theNow the individualindividual--specific interceptsspecific intercepts areare

estimated unbiasedly as:estimated unbiasedly as:

ii = 1, …,= 1, …, NN..

,ˆˆ FEiii xy

).()( iitiitiit xxyy

2. The Fixed Effects Model: A Simple Solution2. The Fixed Effects Model: A Simple Solution

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 54

Problems with the FE-Estimator

The FE-estimator rests on the assumption that

Cov(xit, uis) = 0, t and s;

This is the assumption of (strict) exogeneity.

A strictly exogenous variable is not allowed to

depend upon current, future and past values of

the error term.

2. The Fixed Effects Model: A Simple Solution2. The Fixed Effects Model: A Simple Solution

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 55

Assumption of (strict) exogeneity.Assumption of (strict) exogeneity.

If it is violated,If it is violated,

we have anwe have an endogeneity problemendogeneity problem::

the independent variable and the error termthe independent variable and the error term

are correlated.are correlated.

Under endogeneity,Under endogeneity,

thethe FEFE--estimator will be biasedestimator will be biased::

Endogeneity in this sense is a problem withEndogeneity in this sense is a problem with

panel datapanel data..

2. The Fixed Effects Model:2. The Fixed Effects Model:

Assumption of ExogeneityAssumption of Exogeneity

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 56

Endogeneity arises from:Endogeneity arises from:

• systematic shocks in X (period effects)• systematic shocks in X (period effects)

• Omitted variables (unobserved• Omitted variables (unobservedheterogeneity)heterogeneity)

• Random (external) shocks (simultaneity)• Random (external) shocks (simultaneity)

• Errors in reporting X (measurement error).• Errors in reporting X (measurement error).

What can we do?What can we do?

The standard answer to endogeneity isThe standard answer to endogeneity is

to use IVto use IV--estimationestimation(or structural equation modelling).(or structural equation modelling).

2. The Fixed Effects Model: Endogeneity2. The Fixed Effects Model: Endogeneity

12/2/2008

15

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 57

A regression with aA regression with a random constant termrandom constant term..

In regression:In regression: All factors that affectAll factors that affect yy butbut notnot

includedincluded can be summarized bycan be summarized by a random errora random error

termterm. So. So ii assumed to be random.assumed to be random.

yyitit == xxitit ++ ii ++ uuitit ;; uuitit IIN(0,IIN(0, uu22););

ii IIN(0,IIN(0, 22););

Cov(Cov(uuitit,,ii) = 0) = 0Cov(Cov(uuitit,, xxitit) = 0) = 0Cov(Cov(xxitit,,ii) = 0.) = 0.

The Random Effects ModelThe Random Effects Model

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 58

Intercept assumed not constant, but as a random

variable with a mean of :

ii = ++ ii ,, ii == 1, …,1, …, N.N.

TheThe sample of our four firms are drawn from thesample of our four firms are drawn from the

same populationsame population and haveand have a common mean value fora common mean value for

the intercept (the intercept (););

thethe individual differences in the intercept valuesindividual differences in the intercept values

of each companyof each company are reflectedare reflected in the error termin the error term ii

The Random Effects ModelThe Random Effects Model

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 59

yyitit == xxitit ++ ii ++ uuitit ;;

TheThe composite error termcomposite error term wwitit == ii ++ uuitit::

Two componentsTwo components::

ii : cross sectional (within) component;

uit: panel (between) component

hencehence Error components modelError components model

The Random Effects ModelThe Random Effects Model(Error Component Model)(Error Component Model)

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 60

yyitit == xxitit ++ ii ++ uuitit ;; uuitit IIN(0,IIN(0, uu22););

ii IIN(0,IIN(0, 22););

Cov(Cov(uuitit,,ii) = Cov() = Cov(uuitit,, xxitit) = Cov() = Cov(xxitit,,ii) = 0.) = 0.

Individual error components not correlatedIndividual error components not correlated

with each otherwith each other,,

andand not autocorrelated across both crossnot autocorrelated across both cross--

section and time series unitssection and time series units..

The Random Effects ModelThe Random Effects Model(Error Component Model)(Error Component Model)

12/2/2008

16

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 61

The composite error termThe composite error term wwitit == ii ++ uuitit::

E(E(wwitit) = 0) = 0;;

Var(Var(wwitit) =) = 22 ++ uu

22 (sum of within and between

unit variances)

If 22 = 0, no difference between pooled

regression model and RE model;

We can pool the data and run OLSWe can pool the data and run OLS

The Random Effects ModelThe Random Effects Model(Error Component Model)(Error Component Model)

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 62

TheThe composite error termcomposite error term wwitit == ii ++ uuitit::

E(E(wwitit) = 0) = 0;; Var(Var(wwitit) =) = uu22 ++

22..

HomoscedasticHomoscedastic;;

butbut serially correlatedserially correlated ((unlessunless 22 = 00).).

Cov(Cov(wwitit,, wwisis) =) = 22

Correlation coefficient of the composite error term

wit : r(wit, wis) = 22 /(uu

22 ++ 22)

The Random Effects ModelThe Random Effects Model(Error Component Model)(Error Component Model)

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 63

TheThe composite error termcomposite error term wwitit == ii ++ uuitit::

serially correlatedserially correlated ((unlessunless 22 = 00).).

SoSo SE for OLS estimatorSE for OLS estimator:: biased and inefficientbiased and inefficient;;

HenceHence GLS estimatorGLS estimator..

The Random Effects ModelThe Random Effects Model(Error Component Model)(Error Component Model)

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 64

If errors are nonspherical, OLS estimation can

be a problem.

In the TSCS/Panel context, it is often the case

that the assumptions above will not be

accurate.

If we knew the shape of the errors (their

variance-covariance matrix) we could simply

use it to modify our usual estimation (this would

be GLS, generalized least squares).

The Random Effects ModelThe Random Effects Model(Error Component Model)(Error Component Model)

12/2/2008

17

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 65

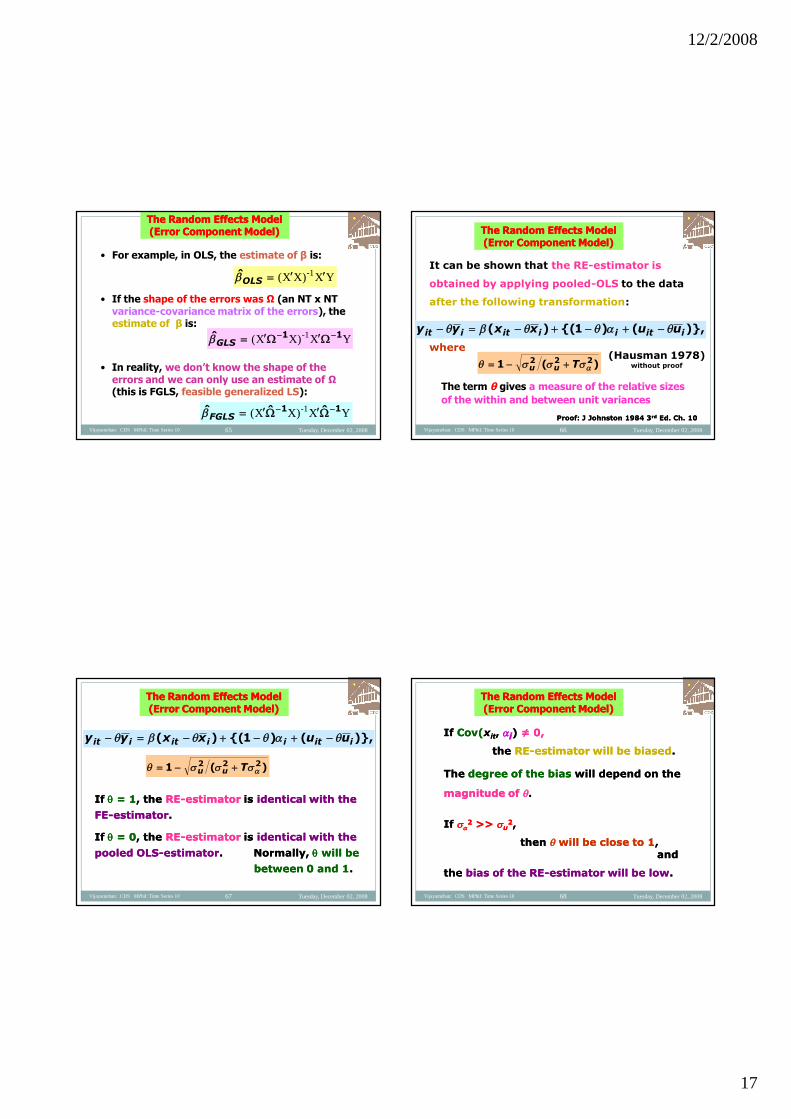

• For example, in OLS, the estimate of β is:

• If the shape of the errors was Ω (an NT x NTvariance-covariance matrix of the errors), theestimate of β is:

• In reality, we don’t know the shape of theerrors and we can only use an estimate of Ω(this is FGLS, feasible generalized LS):

YXXX -1)(OLS

YXXX 11ˆ -1)(GLS

YXXX 11 ˆˆˆ -1)(FGLS

The Random Effects ModelThe Random Effects Model(Error Component Model)(Error Component Model)

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 66

It can be shown that the RE-estimator is

obtained by applying pooled-OLS to the data

after the following transformation:

where

)},()1{()( iitiiitiit uuxxyy

)(1 222 Tuu

(Hausman 1978)without proof

Proof: J Johnston 1984 3Proof: J Johnston 1984 3rdrd Ed. Ch. 10Ed. Ch. 10

The Random Effects ModelThe Random Effects Model(Error Component Model)(Error Component Model)

The term θ gives a measure of the relative sizes

of the within and between unit variances

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 67

IfIf == 11, the, the RERE--estimatorestimator isis identical with theidentical with the

FEFE--estimatorestimator..

IfIf == 00, the, the RERE--estimatorestimator isis identical with theidentical with the

pooled OLSpooled OLS--estimatorestimator. Normally,. Normally, will bewill be

between 0 and 1between 0 and 1..

)},()1{()( iitiiitiit uuxxyy

)(1 222 Tuu

The Random Effects ModelThe Random Effects Model(Error Component Model)(Error Component Model)

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 68

IfIf Cov(Cov(xxitit,, ii)) ≠ 0,≠ 0,

thethe RERE--estimator will be biasedestimator will be biased..

TheThe degree of the biasdegree of the bias will depend on thewill depend on the

magnitude ofmagnitude of ..

IfIf 22 >>>> uu

22,,

thenthen will be close to 1will be close to 1,,andand

thethe bias of the REbias of the RE--estimator will be lowestimator will be low..

The Random Effects ModelThe Random Effects Model(Error Component Model)(Error Component Model)

12/2/2008

18

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 69

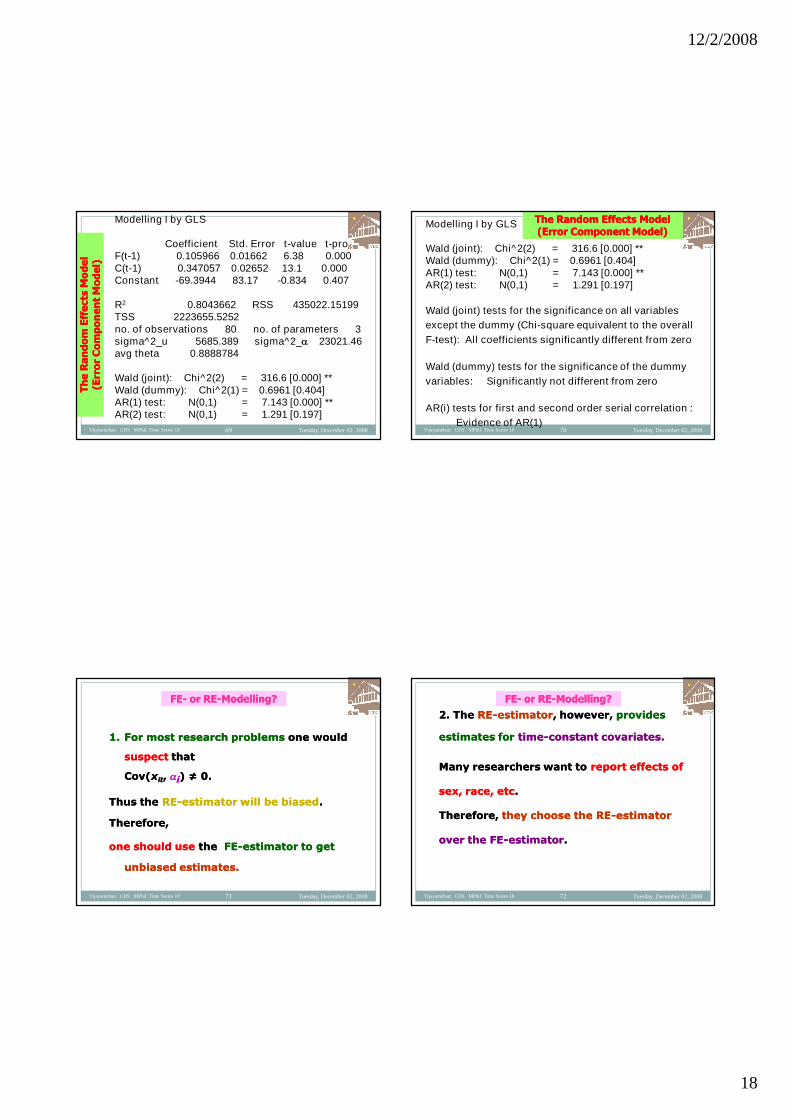

Modelling I by GLS

Coefficient Std. Error t-value t-probF(t-1) 0.105966 0.01662 6.38 0.000C(t-1) 0.347057 0.02652 13.1 0.000Constant -69.3944 83.17 -0.834 0.407

R2 0.8043662 RSS 435022.15199TSS 2223655.5252no. of observations 80 no. of parameters 3sigma^2_u 5685.389 sigma^2_ 23021.46avg theta 0.8888784

Wald (joint): Chi^2(2) = 316.6 [0.000] **Wald (dummy): Chi^2(1) = 0.6961 [0.404]AR(1) test: N(0,1) = 7.143 [0.000] **AR(2) test: N(0,1) = 1.291 [0.197]

Th

eR

an

do

mE

ffe

cts

Mo

de

lT

he

Ra

nd

om

Eff

ects

Mo

de

l(E

rro

rC

om

po

ne

nt

Mo

de

l)(E

rro

rC

om

po

ne

nt

Mo

de

l)

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 70

Modelling I by GLS

Wald (joint): Chi^2(2) = 316.6 [0.000] **Wald (dummy): Chi^2(1) = 0.6961 [0.404]AR(1) test: N(0,1) = 7.143 [0.000] **AR(2) test: N(0,1) = 1.291 [0.197]

Wald (joint) tests for the significance on all variables

except the dummy (Chi-square equivalent to the overall

F-test): All coefficients significantly different from zero

Wald (dummy) tests for the significance of the dummy

variables: Significantly not different from zero

AR(i) tests for first and second order serial correlation :

Evidence of AR(1)

The Random Effects ModelThe Random Effects Model(Error Component Model)(Error Component Model)

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 71

1.1. For most research problemsFor most research problems one wouldone would

suspectsuspect thatthat

Cov(Cov(xxitit,, ii) ≠ 0. ) ≠ 0.

Thus theThus the RERE--estimator will be biasedestimator will be biased..

Therefore,Therefore,

one should useone should use thethe FEFE--estimator to getestimator to get

unbiased estimates.unbiased estimates.

FEFE-- or REor RE--Modelling?Modelling?

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 72

2. The2. The RERE--estimatorestimator, however,, however, providesprovides

estimates forestimates for timetime--constant covariates.constant covariates.

Many researchers want toMany researchers want to report effects ofreport effects of

sex, race, etcsex, race, etc..

Therefore,Therefore, they choose the REthey choose the RE--estimatorestimator

over the FEover the FE--estimatorestimator..

FEFE-- or REor RE--Modelling?Modelling?

12/2/2008

19

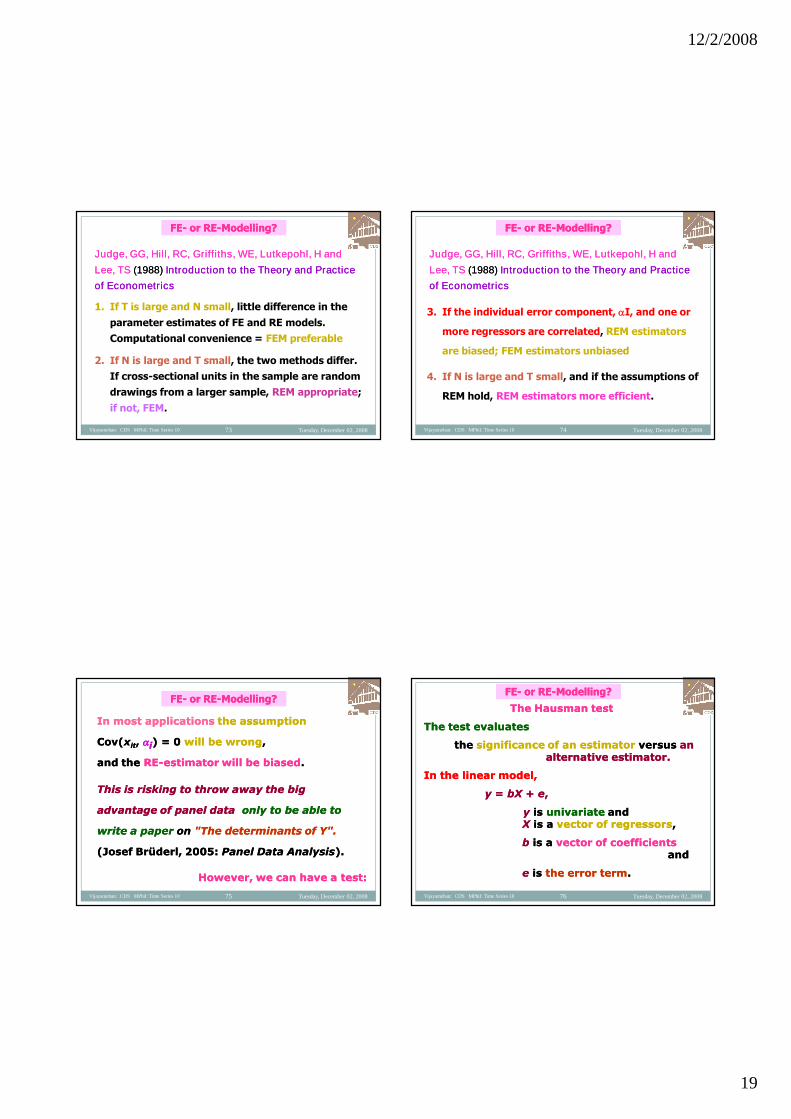

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 73

Judge, GG, Hill, RC, Griffiths, WE, Lutkepohl, H andJudge, GG, Hill, RC, Griffiths, WE, Lutkepohl, H and

Lee, TSLee, TS (1988)(1988) Introduction to the Theory and PracticeIntroduction to the Theory and Practice

of Econometricsof Econometrics

1. If T is large and N small, little difference in the

parameter estimates of FE and RE models.

Computational convenience = FEM preferable

2. If N is large and T small, the two methods differ.

If cross-sectional units in the sample are random

drawings from a larger sample, REM appropriate;

if not, FEM.

FEFE-- or REor RE--Modelling?Modelling?

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 74

3. If the individual error component, I, and one or

more regressors are correlated, REM estimators

are biased; FEM estimators unbiased

4. If N is large and T small, and if the assumptions of

REM hold, REM estimators more efficient.

FEFE-- or REor RE--Modelling?Modelling?

Judge, GG, Hill, RC, Griffiths, WE, Lutkepohl, H andJudge, GG, Hill, RC, Griffiths, WE, Lutkepohl, H and

Lee, TSLee, TS (1988)(1988) Introduction to the Theory and PracticeIntroduction to the Theory and Practice

of Econometricsof Econometrics

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 75

In most applicationsIn most applications the assumptionthe assumption

Cov(Cov(xxitit,, ii) = 0) = 0 will be wrongwill be wrong,,

and theand the RERE--estimator will be biasedestimator will be biased..

This is risking to throw away the bigThis is risking to throw away the big

advantage of panel dataadvantage of panel data only to be able toonly to be able to

write a paperwrite a paper onon "The determinants of Y"."The determinants of Y".

(Josef Brüderl, 2005:(Josef Brüderl, 2005: Panel Data AnalysisPanel Data Analysis).).

However, we can have a test:However, we can have a test:

FEFE-- or REor RE--Modelling?Modelling?

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 76

The Hausman testThe Hausman test

The test evaluatesThe test evaluates

thethe significance of an estimatorsignificance of an estimator versusversus ananalternative estimator.alternative estimator.

In the linear model,In the linear model,

yy == bXbX ++ ee,,

yy isis univariateunivariate andandXX is ais a vector of regressorsvector of regressors,,

bb is ais a vector of coefficientsvector of coefficientsandand

ee isis the error termthe error term..

FEFE-- or REor RE--Modelling?Modelling?

12/2/2008

20

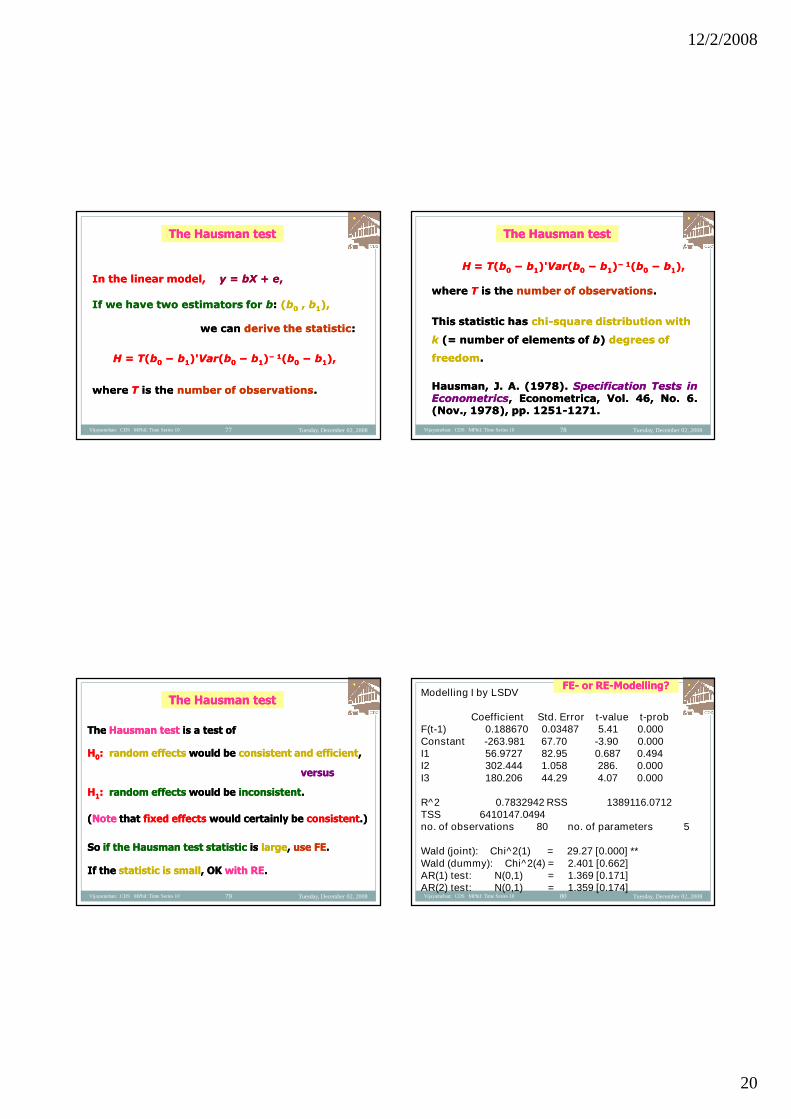

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 77

In the linear model,In the linear model, yy == bXbX ++ ee,,

If we have two estimators forIf we have two estimators for bb:: ((bb00 ,, bb11),),

we canwe can derive the statisticderive the statistic::

HH == TT((bb00 −− bb11)')'VarVar((bb00 −− bb11))− 1− 1((bb00 −− bb11),),

wherewhere TT is theis the number of observationsnumber of observations..

The Hausman testThe Hausman test

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 78

HH == TT((bb00 −− bb11)')'VarVar((bb00 −− bb11))− 1− 1((bb00 −− bb11),),

wherewhere TT is theis the number of observationsnumber of observations..

This statistic hasThis statistic has chichi--square distribution withsquare distribution with

kk (= number of elements of(= number of elements of bb)) degrees ofdegrees of

freedomfreedom..

Hausman,Hausman, JJ.. AA.. ((19781978)).. SpecificationSpecification TestsTests ininEconometricsEconometrics,, Econometrica,Econometrica, VolVol.. 4646,, NoNo.. 66..(Nov(Nov..,, 19781978),), pppp.. 12511251--12711271..

The Hausman testThe Hausman test

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 79

TheThe Hausman testHausman test is a test ofis a test of

HH00:: random effectsrandom effects would bewould be consistent and efficientconsistent and efficient,,

versusversus

HH11:: random effectsrandom effects would bewould be inconsistentinconsistent..

((NoteNote thatthat fixed effectsfixed effects would certainly bewould certainly be consistentconsistent.).)

SoSo if the Hausman test statisticif the Hausman test statistic isis largelarge,, use FEuse FE..

If theIf the statistic is smallstatistic is small, OK, OK with REwith RE..

The Hausman testThe Hausman test

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 80

FEFE-- or REor RE--ModellingModelling??Modelling I by LSDV

Coefficient Std. Error t-value t-probF(t-1) 0.188670 0.03487 5.41 0.000Constant -263.981 67.70 -3.90 0.000I1 56.9727 82.95 0.687 0.494I2 302.444 1.058 286. 0.000I3 180.206 44.29 4.07 0.000

R^2 0.7832942 RSS 1389116.0712TSS 6410147.0494no. of observations 80 no. of parameters 5

Wald (joint): Chi^2(1) = 29.27 [0.000] **Wald (dummy): Chi^2(4) = 2.401 [0.662]AR(1) test: N(0,1) = 1.369 [0.171]AR(2) test: N(0,1) = 1.359 [0.174]

12/2/2008

21

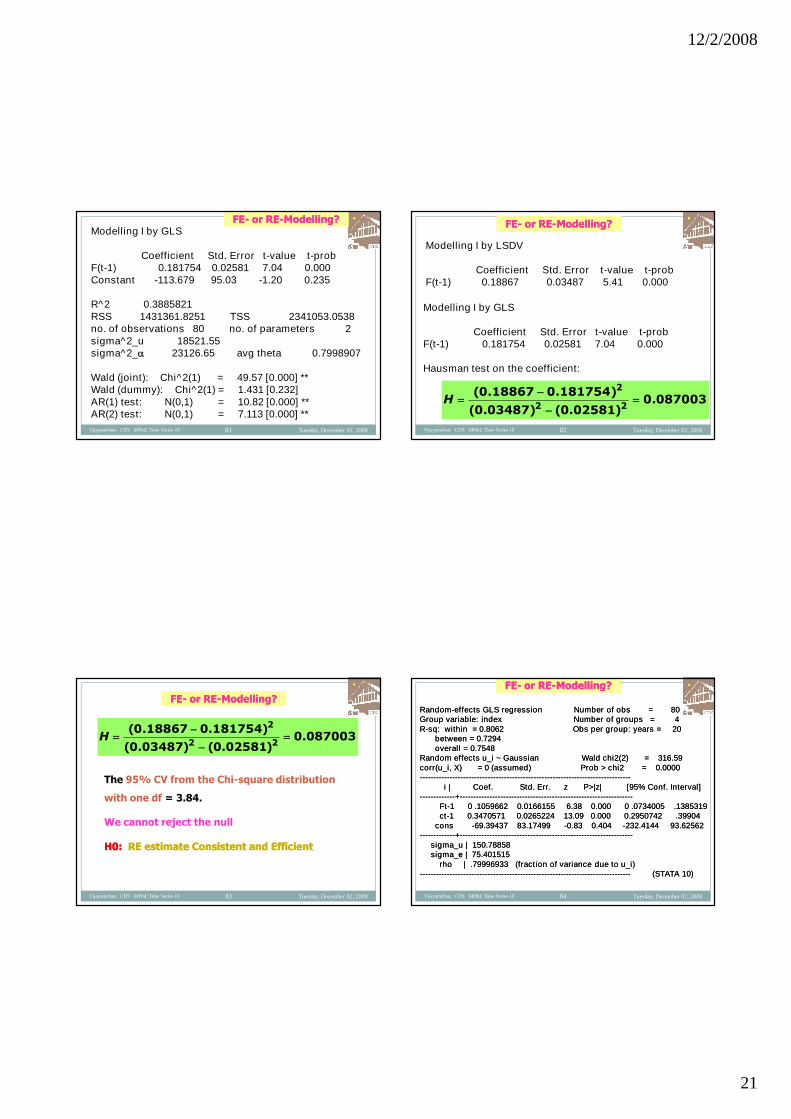

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 81

Modelling I by GLS

Coefficient Std. Error t-value t-probF(t-1) 0.181754 0.02581 7.04 0.000Constant -113.679 95.03 -1.20 0.235

R^2 0.3885821RSS 1431361.8251 TSS 2341053.0538no. of observations 80 no. of parameters 2sigma^2_u 18521.55sigma^2_ 23126.65 avg theta 0.7998907

Wald (joint): Chi^2(1) = 49.57 [0.000] **Wald (dummy): Chi^2(1) = 1.431 [0.232]AR(1) test: N(0,1) = 10.82 [0.000] **AR(2) test: N(0,1) = 7.113 [0.000] **

FEFE-- or REor RE--ModellingModelling??

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 82

Modelling I by LSDV

Coefficient Std. Error t-value t-probF(t-1) 0.18867 0.03487 5.41 0.000

Modelling I by GLS

Coefficient Std. Error t-value t-probF(t-1) 0.181754 0.02581 7.04 0.000

Hausman test on the coefficient:

087003.0)02581.0()03487.0(

)181754.018867.0(22

2

H

FEFE-- or REor RE--ModellingModelling??

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 83

087003.0)02581.0()03487.0(

)181754.018867.0(22

2

H

The 95% CV from the Chi-square distribution

with one df = 3.84.

We cannot reject the null

H0:H0: RE estimate Consistent and EfficientRE estimate Consistent and Efficient

FEFE-- or REor RE--Modelling?Modelling?

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 84

FEFE-- or REor RE--Modelling?Modelling?

RandomRandom--effects GLS regression Number of obs = 80effects GLS regression Number of obs = 80Group variable: index Number of groups = 4Group variable: index Number of groups = 4RR--sq: within = 0.8062 Obs per group: years = 20sq: within = 0.8062 Obs per group: years = 20

between = 0.7294between = 0.7294overall = 0.7548overall = 0.7548

Random effects u_i ~ Gaussian Wald chi2(2) = 316.59Random effects u_i ~ Gaussian Wald chi2(2) = 316.59corr(u_i, X) = 0 (assumed) Prob > chi2 = 0.0000corr(u_i, X) = 0 (assumed) Prob > chi2 = 0.0000------------------------------------------------------------------------------------------------------------------------------------------------------------

i | Coef. Std. Err. z P>|z| [95% Conf.i | Coef. Std. Err. z P>|z| [95% Conf. Interval]Interval]--------------------------++--------------------------------------------------------------------------------------------------------------------------------

FtFt--1 0 .1059662 0.0166155 6.38 0.000 0 .0734005 .13853191 0 .1059662 0.0166155 6.38 0.000 0 .0734005 .1385319ctct--1 0.3470571 0.0265224 13.09 0.000 0.2950742 .399041 0.3470571 0.0265224 13.09 0.000 0.2950742 .39904

conscons --69.39437 83.1749969.39437 83.17499 --0.83 0.4040.83 0.404 --232.4144 93.62562232.4144 93.62562--------------------------++--------------------------------------------------------------------------------------------------------------------------------

sigma_u | 150.78858sigma_u | 150.78858sigma_e | 75.401515sigma_e | 75.401515

rho | .79996933 (fraction of variance due to u_i)rho | .79996933 (fraction of variance due to u_i)------------------------------------------------------------------------------------------------------------------------------------------------------------ (STATA 10)(STATA 10)

12/2/2008

22

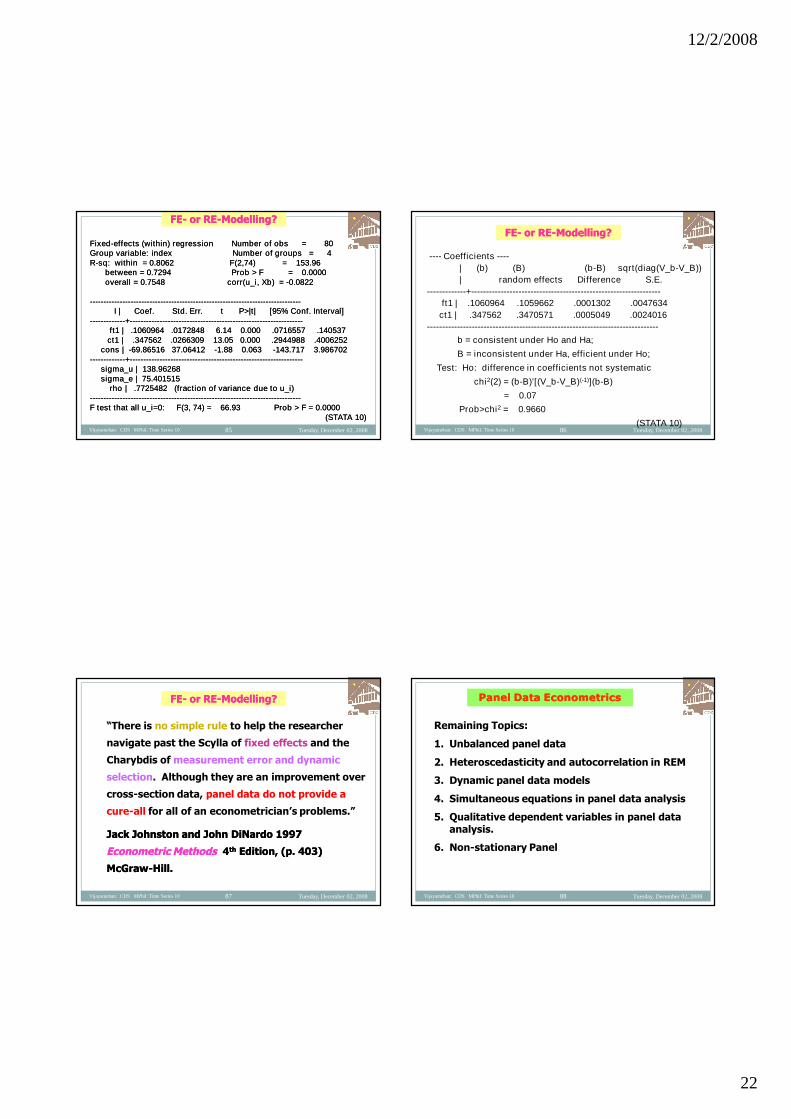

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 85

FEFE-- or REor RE--Modelling?Modelling?

FixedFixed--effects (within) regression Number of obs = 80effects (within) regression Number of obs = 80Group variable: index Number of groups = 4Group variable: index Number of groups = 4RR--sq: within = 0.8062 F(2,74) = 153.96sq: within = 0.8062 F(2,74) = 153.96

between = 0.7294between = 0.7294 Prob > F = 0.0000Prob > F = 0.0000overall = 0.7548overall = 0.7548 corr(u_i, Xb) =corr(u_i, Xb) = --0.08220.0822

------------------------------------------------------------------------------------------------------------------------------------------------------------I | Coef.I | Coef. Std. Err. t P>|t| [95% Conf.Std. Err. t P>|t| [95% Conf. Interval]Interval]

--------------------------++--------------------------------------------------------------------------------------------------------------------------------ft1 | .1060964 .0172848 6.14 0.000 .0716557 .140537ft1 | .1060964 .0172848 6.14 0.000 .0716557 .140537

ct1 | .347562 .0266309 13.05 0.000 .2944988 .4006252ct1 | .347562 .0266309 13.05 0.000 .2944988 .4006252cons |cons | --69.86516 37.0641269.86516 37.06412 --1.88 0.0631.88 0.063 --143.717 3.986702143.717 3.986702

--------------------------++--------------------------------------------------------------------------------------------------------------------------------sigma_u | 138.96268sigma_u | 138.96268sigma_e | 75.401515sigma_e | 75.401515

rho | .7725482 (fraction of variance due to u_i)rho | .7725482 (fraction of variance due to u_i)------------------------------------------------------------------------------------------------------------------------------------------------------------F test that all u_i=0: F(3, 74) = 66.93 Prob > F = 0.0000F test that all u_i=0: F(3, 74) = 66.93 Prob > F = 0.0000

(STATA 10)(STATA 10)

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 86

FEFE-- or REor RE--Modelling?Modelling?

---- Coefficients ----

| (b) (B) (b-B) sqrt(diag(V_b-V_B))

| random effects Difference S.E.

-------------+----------------------------------------------------------------

ft1 | .1060964 .1059662 .0001302 .0047634

ct1 | .347562 .3470571 .0005049 .0024016

------------------------------------------------------------------------------

b = consistent under Ho and Ha;

B = inconsistent under Ha, efficient under Ho;

Test: Ho: difference in coefficients not systematic

chi2(2) = (b-B)'[(V_b-V_B)(-1)](b-B)

= 0.07

Prob>chi2 = 0.9660

(STATA 10)

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 87

“There is no simple rule to help the researcher

navigate past the Scylla of fixed effects and the

Charybdis of measurement error and dynamic

selection. Although they are an improvement over

cross-section data, panel data do not provide a

cure-all for all of an econometrician’s problems.”

Jack Johnston and JohnJack Johnston and John DiNardoDiNardo 19971997

Econometric MethodsEconometric Methods 44thth Edition, (p. 403)Edition, (p. 403)

McGrawMcGraw--Hill.Hill.

FEFE-- or REor RE--Modelling?Modelling?

Tuesday, December 02, 2008Vijayamohan: CDS MPhil: Time Series 10 88

Remaining Topics:

1. Unbalanced panel data

2. Heteroscedasticity and autocorrelation in REM

3. Dynamic panel data models

4. Simultaneous equations in panel data analysis

5. Qualitative dependent variables in panel dataanalysis.

6. Non-stationary Panel

Panel Data EconometricsPanel Data Econometrics

12/2/2008

23

Tuesday, December 02,2008

Vijayamohan: CDS MPhil: TimeSeries 10

89

![[S.o. pillai] objective_physics_for_medical_and_e(book_fi.org)](https://img.pdfslide.us/doc/110x75/555f2609d8b42a93658b4f8a/so-pillai-objectivephysicsformedicalandebookfiorg.jpg)