Embed Size (px)

Citation preview

Vijay Chugh Principal Chief General Manager

Dept. of Payment & Settlement Systems Disclaimer: Views are personal

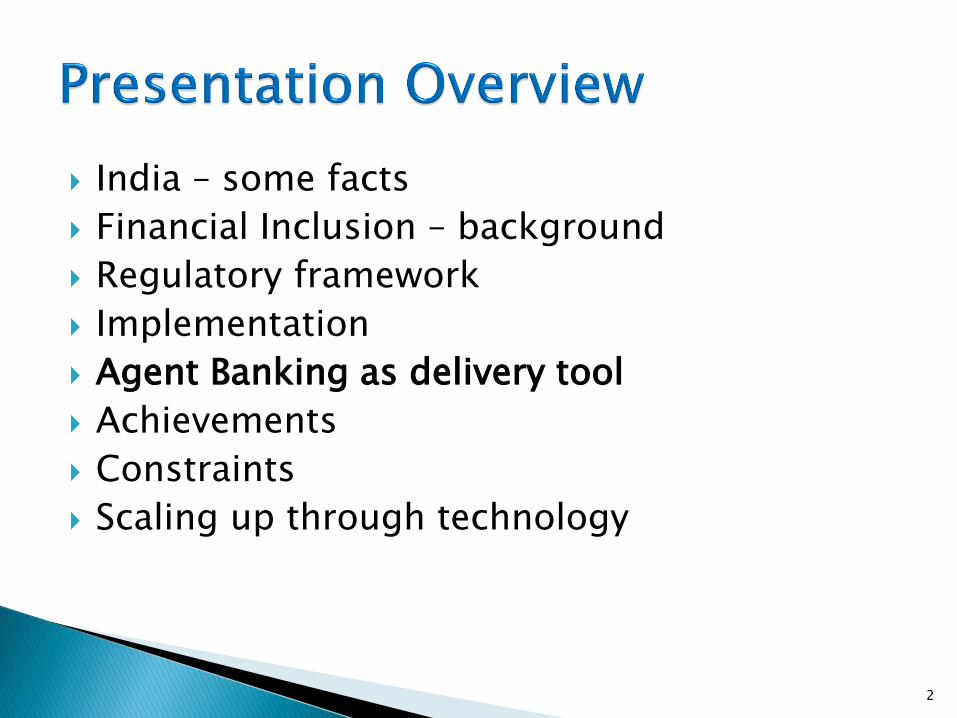

India – some facts

Financial Inclusion – background

Regulatory framework

Implementation

Agent Banking as delivery tool

Achievements

Constraints

Scaling up through technology

2

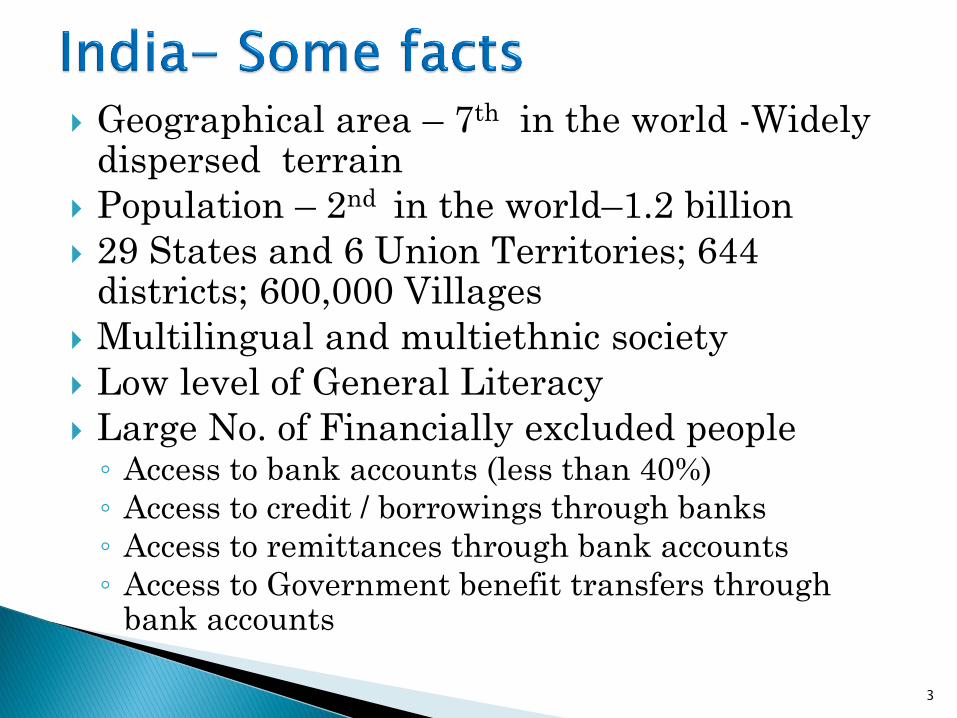

Geographical area – 7th in the world -Widely dispersed terrain

Population – 2nd in the world–1.2 billion

29 States and 6 Union Territories; 644 districts; 600,000 Villages

Multilingual and multiethnic society

Low level of General Literacy

Large No. of Financially excluded people ◦ Access to bank accounts (less than 40%)

◦ Access to credit / borrowings through banks

◦ Access to remittances through bank accounts

◦ Access to Government benefit transfers through bank accounts

3

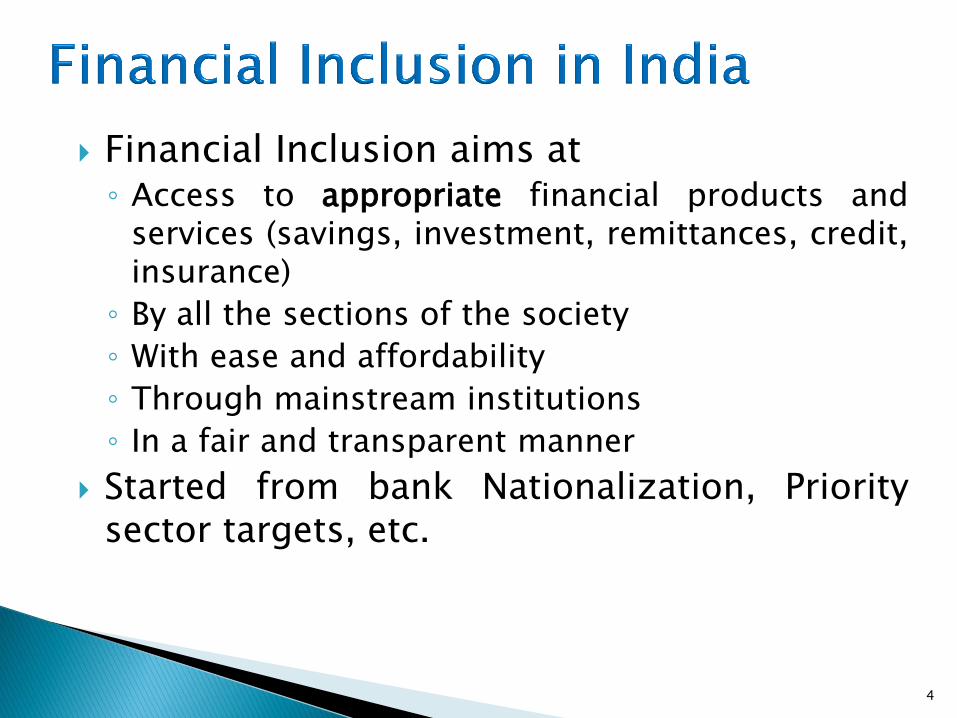

Financial Inclusion aims at ◦ Access to appropriate financial products and

services (savings, investment, remittances, credit, insurance)

◦ By all the sections of the society

◦ With ease and affordability

◦ Through mainstream institutions

◦ In a fair and transparent manner

Started from bank Nationalization, Priority sector targets, etc.

4

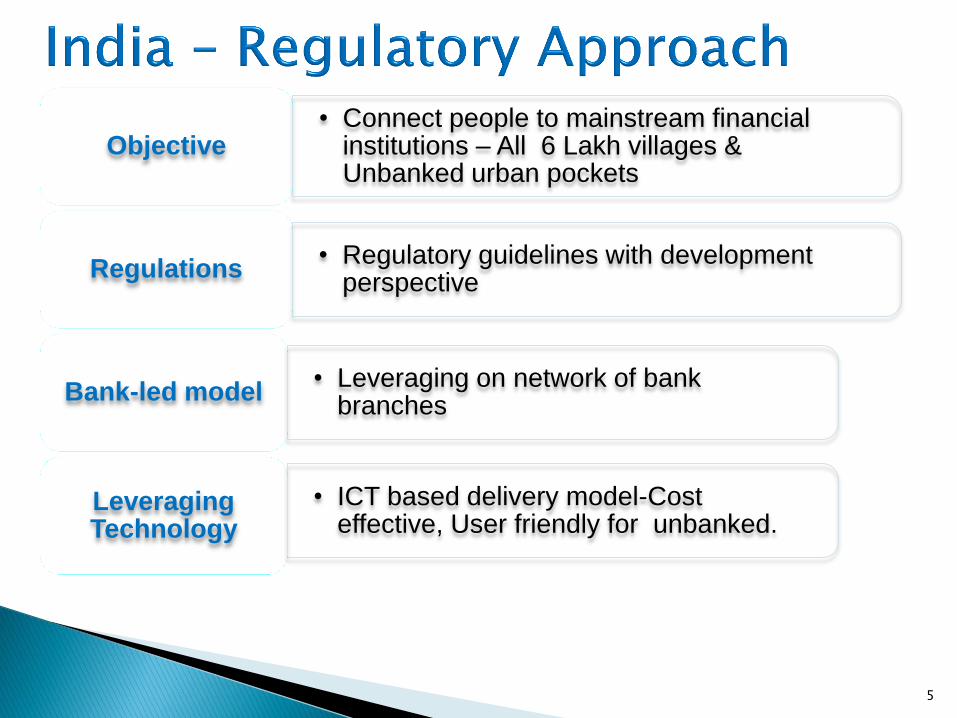

5

• Connect people to mainstream financial institutions – All 6 Lakh villages & Unbanked urban pockets

Objective

• Regulatory guidelines with development perspective

Regulations

• Leveraging on network of bank branches

Bank-led model

• ICT based delivery model-Cost effective, User friendly for unbanked.

Leveraging Technology

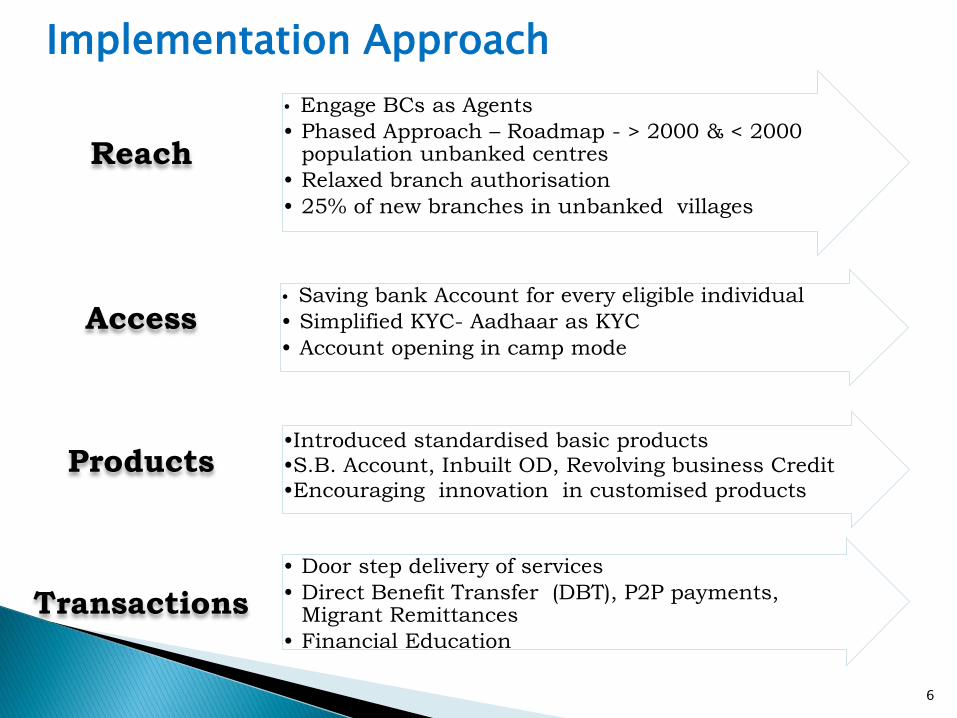

Implementation Approach

• Engage BCs as Agents

• Phased Approach – Roadmap - > 2000 & < 2000 population unbanked centres

• Relaxed branch authorisation

• 25% of new branches in unbanked villages

Reach

• Saving bank Account for every eligible individual

• Simplified KYC- Aadhaar as KYC

• Account opening in camp mode

Access

•Introduced standardised basic products •S.B. Account, Inbuilt OD, Revolving business Credit

•Encouraging innovation in customised products

Products

• Door step delivery of services

• Direct Benefit Transfer (DBT), P2P payments, Migrant Remittances

• Financial Education

Transactions

6

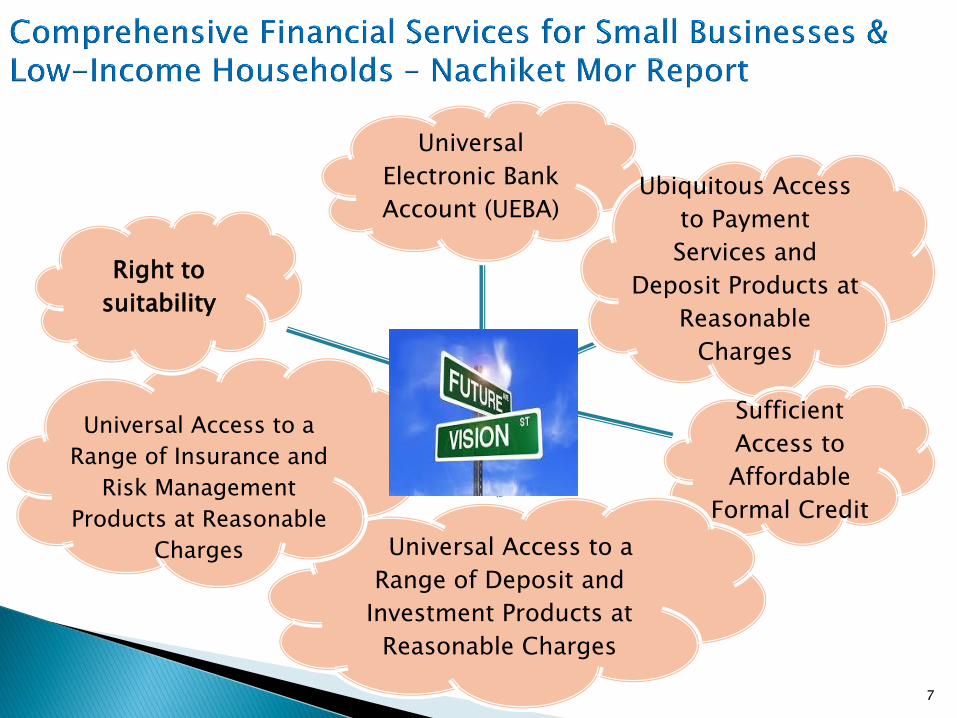

VISION

Universal

Electronic Bank

Account (UEBA) Ubiquitous Access

to Payment

Services and

Deposit Products at

Reasonable

Charges

Sufficient

Access to

Affordable

Formal Credit

Universal Access to a

Range of Deposit and

Investment Products at

Reasonable Charges

Universal Access to a

Range of Insurance and

Risk Management

Products at Reasonable

Charges

Right to

suitability

7

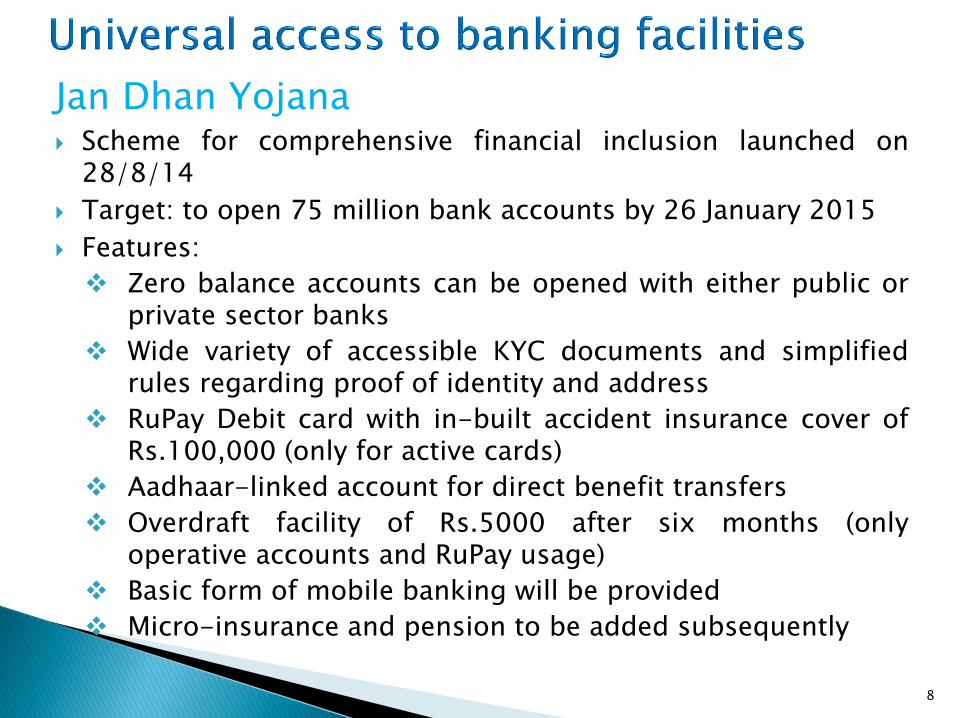

Jan Dhan Yojana Scheme for comprehensive financial inclusion launched on

28/8/14

Target: to open 75 million bank accounts by 26 January 2015

Features:

Zero balance accounts can be opened with either public or private sector banks

Wide variety of accessible KYC documents and simplified rules regarding proof of identity and address

RuPay Debit card with in-built accident insurance cover of Rs.100,000 (only for active cards)

Aadhaar-linked account for direct benefit transfers

Overdraft facility of Rs.5000 after six months (only operative accounts and RuPay usage)

Basic form of mobile banking will be provided

Micro-insurance and pension to be added subsequently

8

Agent Banking = Business correspondent

9

Who can be a BC ? Any one !

◦ from a village grocer, public phone booth operator to a large Telco / Non-banking Financial institution

◦ Attached to a branch – radius of 30 km (metro 5 km). Banks can relax the same to certain extent.

Scope of activities:

◦ opening accounts

◦ Remittance – use NEFT / IMPS

◦ government benefit transfers

◦ cash withdrawal

◦ supply fresh notes

Corporate BCs; Many BCs are also authorised PPI issuers

10

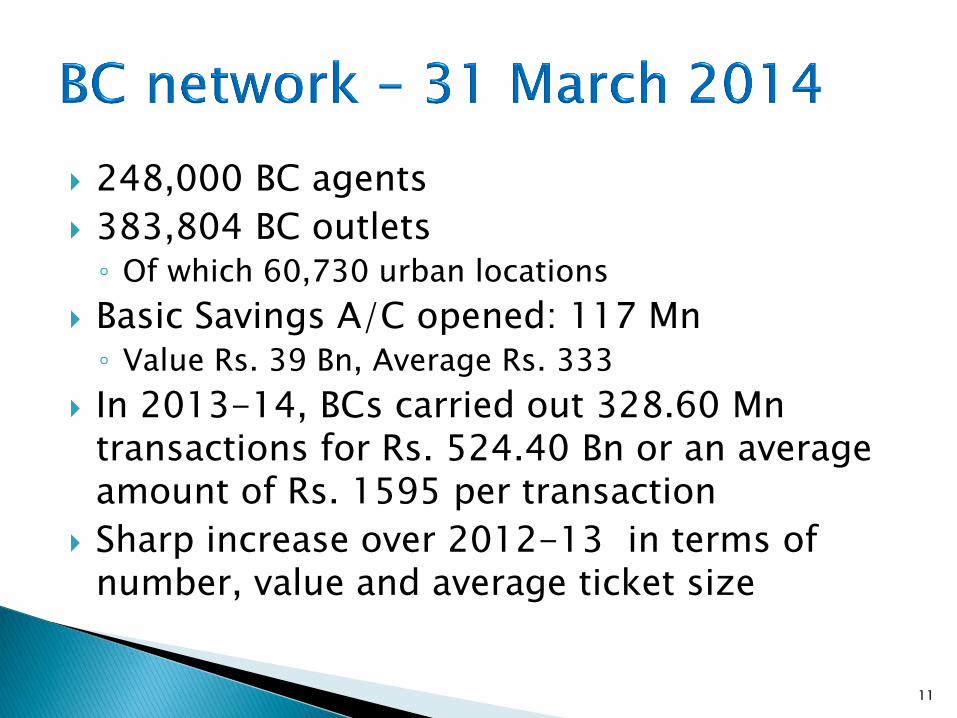

248,000 BC agents

383,804 BC outlets ◦ Of which 60,730 urban locations

Basic Savings A/C opened: 117 Mn ◦ Value Rs. 39 Bn, Average Rs. 333

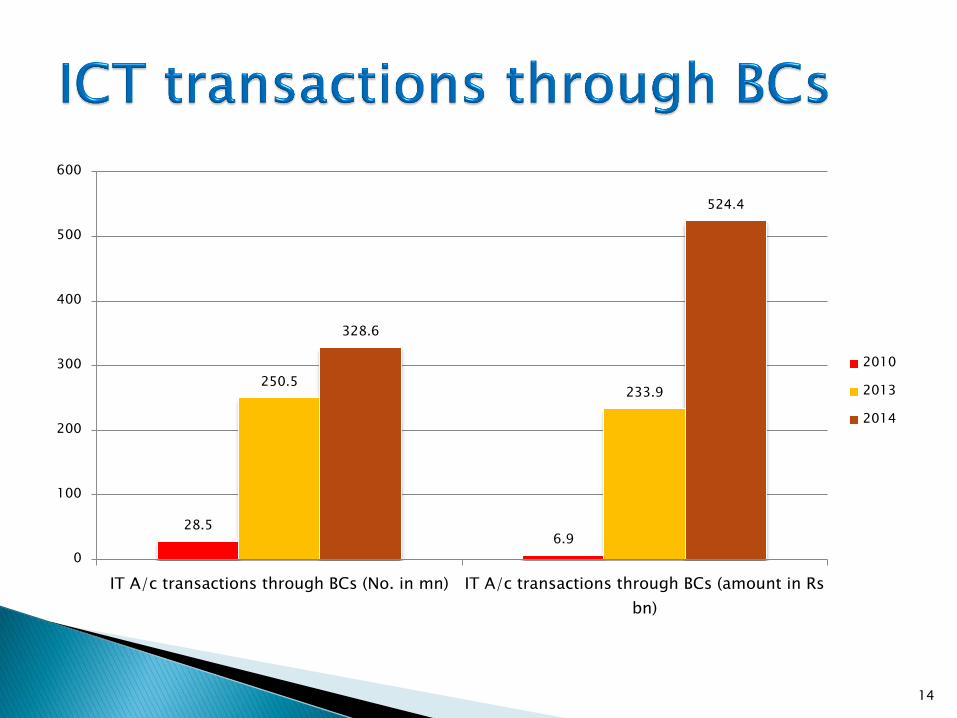

In 2013-14, BCs carried out 328.60 Mn transactions for Rs. 524.40 Bn or an average amount of Rs. 1595 per transaction

Sharp increase over 2012-13 in terms of number, value and average ticket size

11

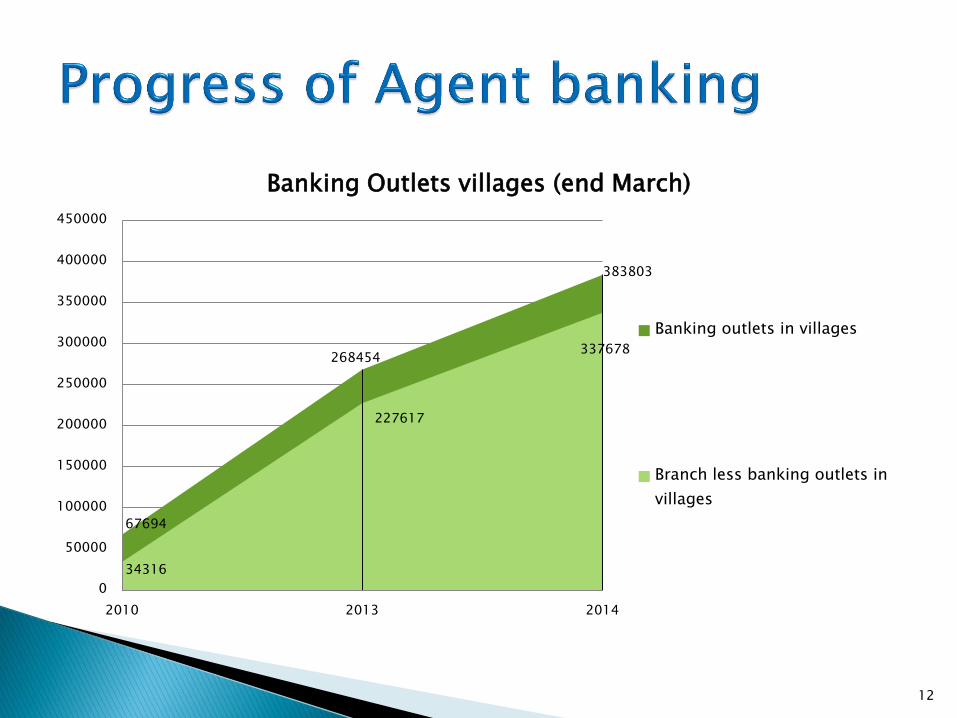

67694

268454

383803

34316

227617

337678

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

2010 2013 2014

Banking Outlets villages (end March)

Banking outlets in villages

Branch less banking outlets in

villages

12

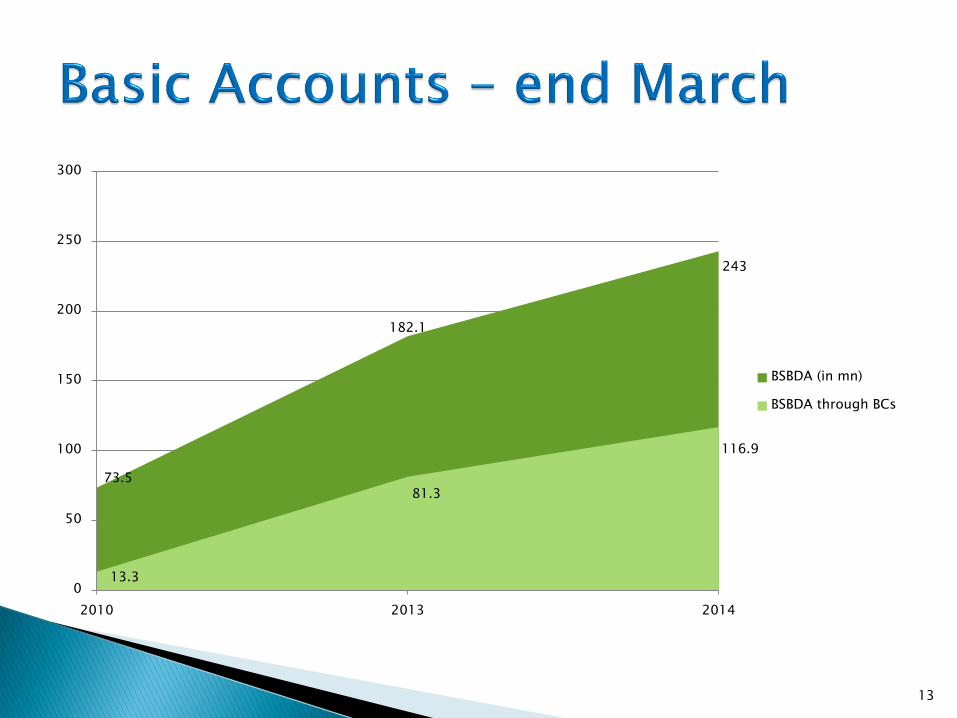

73.5

182.1

243

13.3

81.3

116.9

0

50

100

150

200

250

300

2010 2013 2014

BSBDA (in mn)

BSBDA through BCs

13

28.5 6.9

250.5 233.9

328.6

524.4

0

100

200

300

400

500

600

IT A/c transactions through BCs (No. in mn) IT A/c transactions through BCs (amount in Rs

bn)

2010

2013

2014

14

15

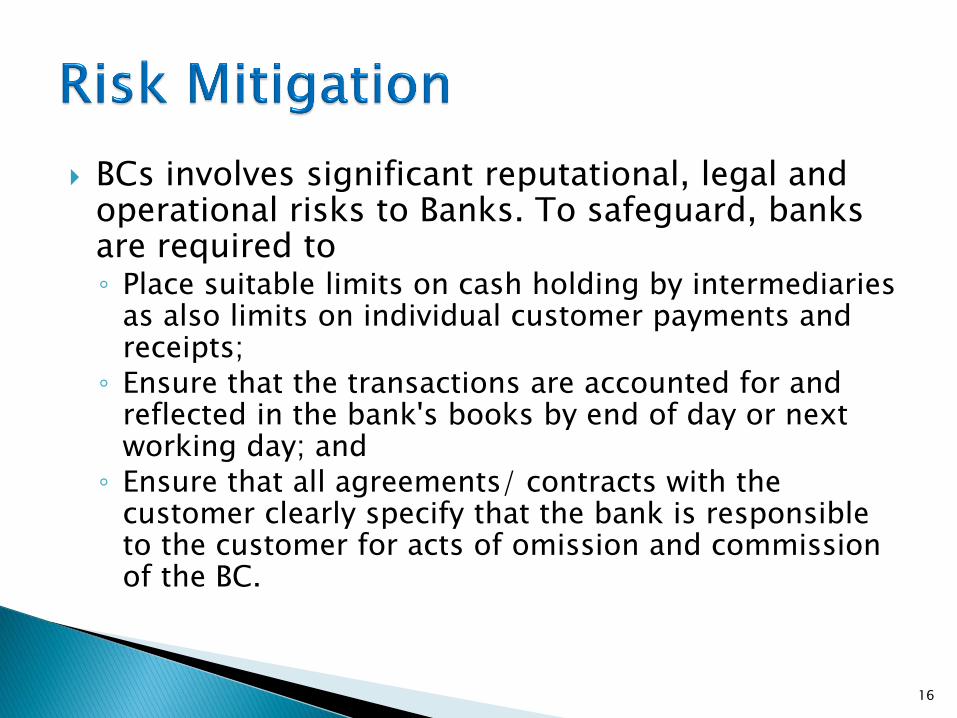

BCs involves significant reputational, legal and operational risks to Banks. To safeguard, banks are required to ◦ Place suitable limits on cash holding by intermediaries

as also limits on individual customer payments and receipts;

◦ Ensure that the transactions are accounted for and reflected in the bank's books by end of day or next working day; and

◦ Ensure that all agreements/ contracts with the customer clearly specify that the bank is responsible to the customer for acts of omission and commission of the BC.

16

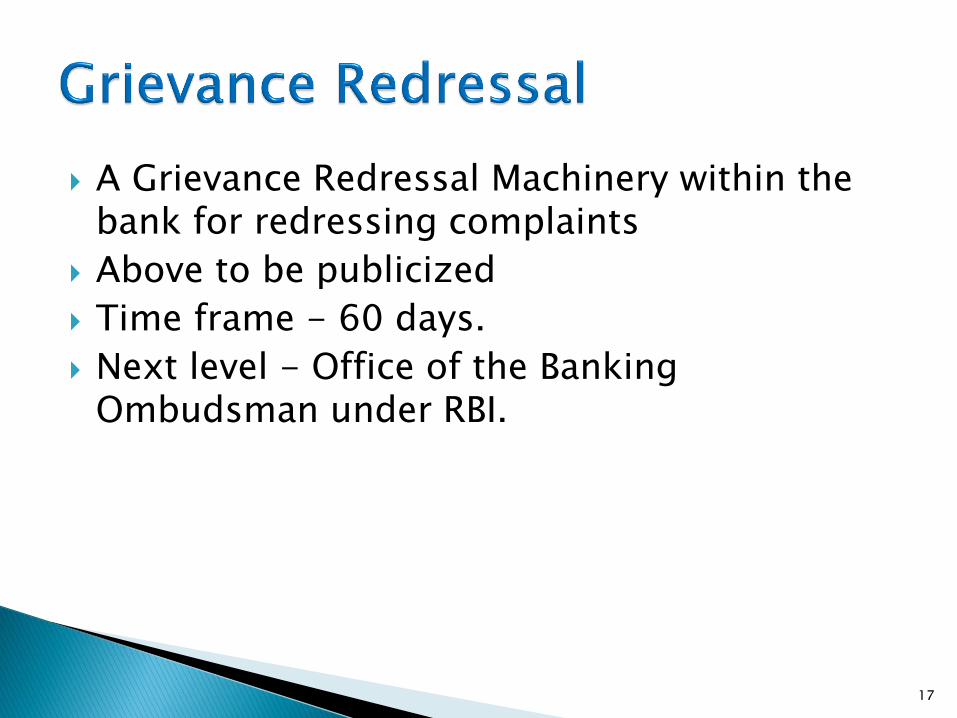

A Grievance Redressal Machinery within the bank for redressing complaints

Above to be publicized

Time frame - 60 days.

Next level - Office of the Banking Ombudsman under RBI.

17

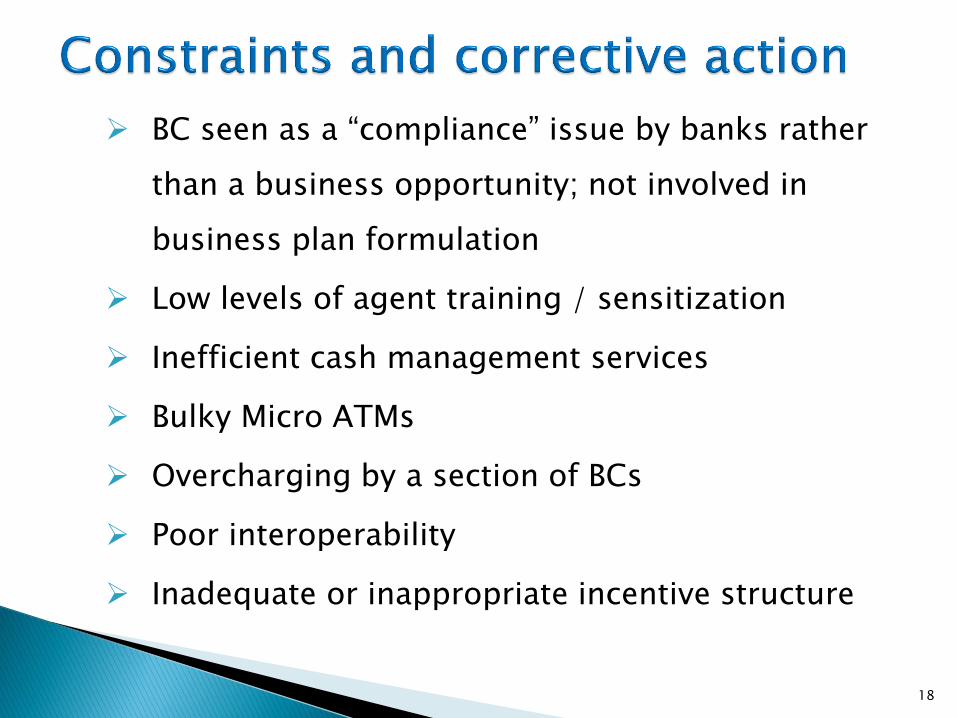

BC seen as a “compliance” issue by banks rather

than a business opportunity; not involved in

business plan formulation

Low levels of agent training / sensitization

Inefficient cash management services

Bulky Micro ATMs

Overcharging by a section of BCs

Poor interoperability

Inadequate or inappropriate incentive structure

18

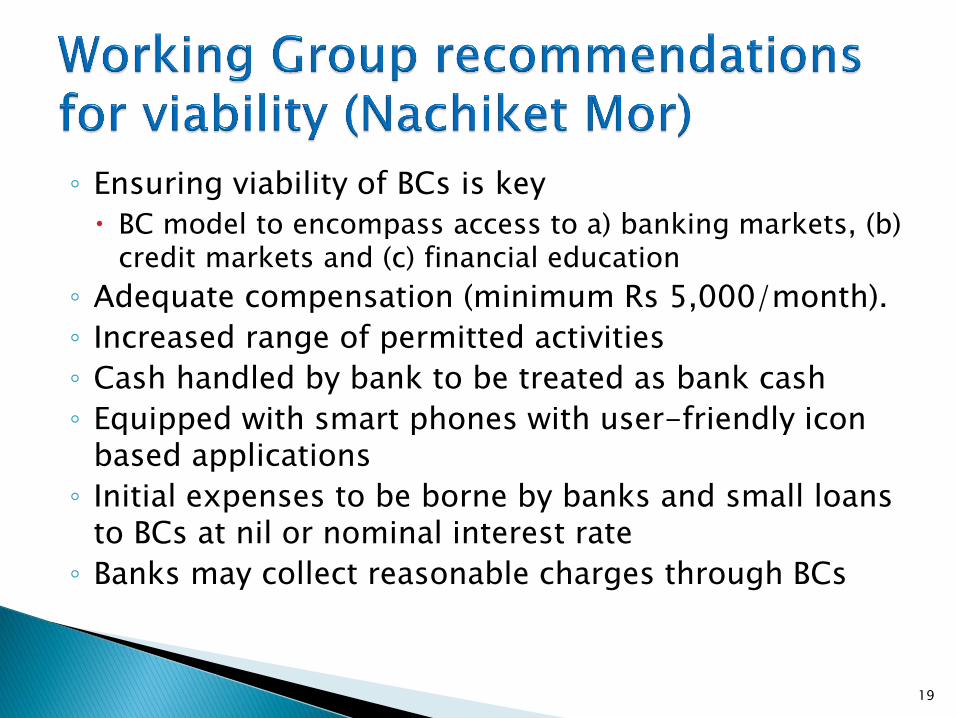

◦ Ensuring viability of BCs is key

BC model to encompass access to a) banking markets, (b) credit markets and (c) financial education

◦ Adequate compensation (minimum Rs 5,000/month).

◦ Increased range of permitted activities

◦ Cash handled by bank to be treated as bank cash

◦ Equipped with smart phones with user-friendly icon based applications

◦ Initial expenses to be borne by banks and small loans to BCs at nil or nominal interest rate

◦ Banks may collect reasonable charges through BCs

19

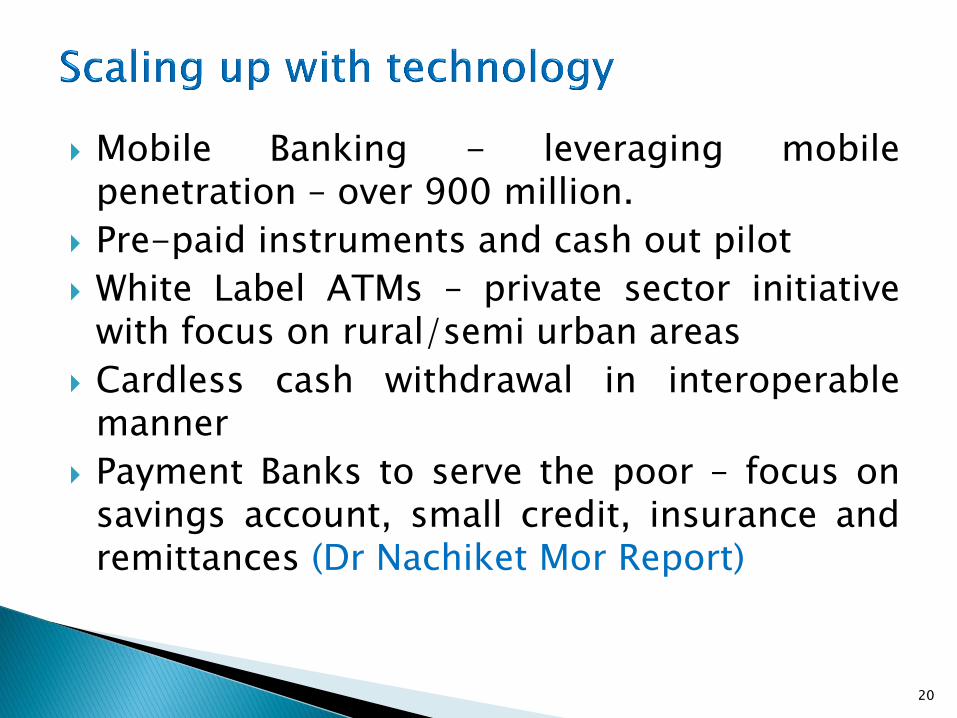

Mobile Banking - leveraging mobile penetration – over 900 million.

Pre-paid instruments and cash out pilot

White Label ATMs – private sector initiative with focus on rural/semi urban areas

Cardless cash withdrawal in interoperable manner

Payment Banks to serve the poor – focus on savings account, small credit, insurance and remittances (Dr Nachiket Mor Report)

20

Thank you

21