Embed Size (px)

Citation preview

VIEWS FROM THE BENCH (PART 1): INSIGHTS FROM THREE

TRIAL JUDGES ON BEST PRACTICES FOR TRIAL LAWYERS IN INSURANCE CASES

Moderator STEPHEN A. MELENDI, Dallas

Tollefson Bradley Mitchell & Melendi

HON. NANCY K. JOHNSON, Houston U.S. Magistrate Judge

Southern District of Texas

HON. GRAY H. MILLER, Houston U.S. District Judge

Southern District of Texas

HON. JEFFREY A. SHADWICK, Houston Judge, 55th Civil District Court

State Bar of Texas 11TH ANNUAL

ADVANCED INSURANCE LAW COURSE April 24-25, 2014

Houston

CHAPTER 9

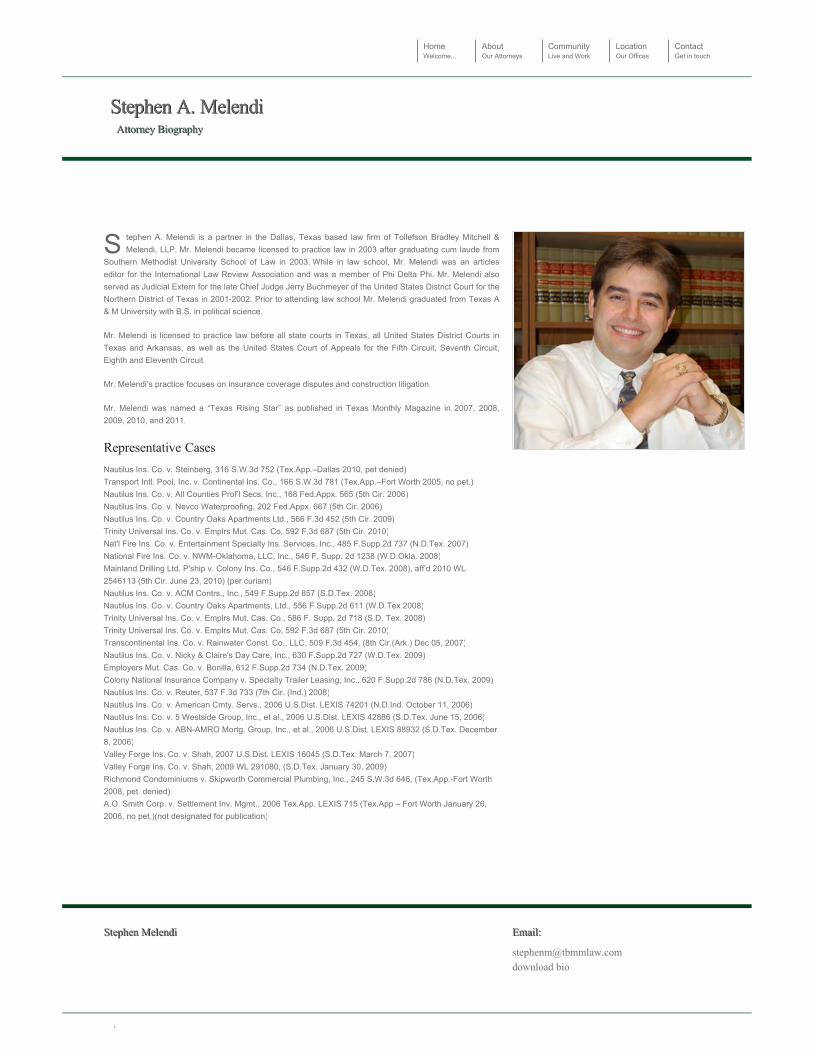

S tephen A. Melendi is a partner in the Dallas, Texas based law firm of Tollefson Bradley Mitchell & Melendi, LLP. Mr. Melendi became licensed to practice law in 2003 after graduating cum laude from

Southern Methodist University School of Law in 2003. While in law school, Mr. Melendi was an articles editor for the International Law Review Association and was a member of Phi Delta Phi. Mr. Melendi also served as Judicial Extern for the late Chief Judge Jerry Buchmeyer of the United States District Court for the Northern District of Texas in 2001-2002. Prior to attending law school Mr. Melendi graduated from Texas A & M University with B.S. in political science.

Mr. Melendi is licensed to practice law before all state courts in Texas, all United States District Courts in Texas and Arkansas, as well as the United States Court of Appeals for the Fifth Circuit, Seventh Circuit, Eighth and Eleventh Circuit.

Mr. Melendi’s practice focuses on insurance coverage disputes and construction litigation.

Mr. Melendi was named a “Texas Rising Star” as published in Texas Monthly Magazine in 2007, 2008, 2009, 2010, and 2011.

Representative CasesNautilus Ins. Co. v. Steinberg, 316 S.W.3d 752 (Tex.App.–Dallas 2010, pet denied)Transport Intl. Pool, Inc. v. Continental Ins. Co., 166 S.W.3d 781 (Tex.App.–Fort Worth 2005, no pet.)Nautilus Ins. Co. v. All Counties Prof’l Secs. Inc., 168 Fed.Appx. 565 (5th Cir. 2006)Nautilus Ins. Co. v. Nevco Waterproofing, 202 Fed.Appx. 667 (5th Cir. 2006)Nautilus Ins. Co. v. Country Oaks Apartments Ltd., 566 F.3d 452 (5th Cir. 2009)Trinity Universal Ins. Co. v. Emplrs Mut. Cas. Co, 592 F.3d 687 (5th Cir. 2010)Nat'l Fire Ins. Co. v. Entertainment Specialty Ins. Services, Inc., 485 F.Supp.2d 737 (N.D.Tex. 2007)National Fire Ins. Co. v. NWM-Oklahoma, LLC, Inc., 546 F. Supp. 2d 1238 (W.D.Okla. 2008)Mainland Drilling Ltd. P'ship v. Colony Ins. Co., 546 F.Supp.2d 432 (W.D.Tex. 2008), aff’d 2010 WL 2546113 (5th Cir. June 23, 2010) (per curiam)Nautilus Ins. Co. v. ACM Contrs., Inc., 549 F.Supp.2d 857 (S.D.Tex. 2008)Nautilus Ins. Co. v. Country Oaks Apartments, Ltd., 556 F.Supp.2d 611 (W.D.Tex.2008)Trinity Universal Ins. Co. v. Emplrs Mut. Cas. Co., 586 F. Supp. 2d 718 (S.D. Tex. 2008)Trinity Universal Ins. Co. v. Emplrs Mut. Cas. Co, 592 F.3d 687 (5th Cir. 2010)Transcontinental Ins. Co. v. Rainwater Const. Co., LLC, 509 F.3d 454, (8th Cir.(Ark.) Dec 05, 2007)Nautilus Ins. Co. v. Nicky & Claire's Day Care, Inc., 630 F.Supp.2d 727 (W.D.Tex. 2009)Employers Mut. Cas. Co. v. Bonilla, 612 F.Supp.2d 734 (N.D.Tex. 2009)Colony National Insurance Company v. Specialty Trailer Leasing, Inc., 620 F.Supp.2d 786 (N.D.Tex. 2009)Nautilus Ins. Co. v. Reuter, 537 F.3d 733 (7th Cir. (Ind.) 2008)Nautilus Ins. Co. v. American Cmty. Servs., 2006 U.S.Dist. LEXIS 74201 (N.D.Ind. October 11, 2006)Nautilus Ins. Co. v. 5 Westside Group, Inc., et al., 2006 U.S.Dist. LEXIS 42886 (S.D.Tex. June 15, 2006)Nautilus Ins. Co. v. ABN-AMRO Mortg. Group, Inc., et al., 2006 U.S.Dist. LEXIS 88932 (S.D.Tex. December 8, 2006)Valley Forge Ins. Co. v. Shah, 2007 U.S.Dist. LEXIS 16045 (S.D.Tex. March 7, 2007)Valley Forge Ins. Co. v. Shah, 2009 WL 291080, (S.D.Tex. January 30, 2009) Richmond Condominiums v. Skipworth Commercial Plumbing, Inc., 245 S.W.3d 646, (Tex.App.-Fort Worth 2008, pet. denied)A.O. Smith Corp. v. Settlement Inv. Mgmt., 2006 Tex.App. LEXIS 715 (Tex.App – Fort Worth January 26, 2006, no pet.)(not designated for publication)

Stephen MelendiStephen Melendi Email: Email:

Stephen A. MelendiStephen A. MelendiAttorney BiographyAttorney Biography

HomeWelcome...

AboutOur Attorneys

CommunityLive and Work

LocationOur Offices

ContactGet in touch

Copyright © 2007-2013 All rights reserved. Tollefson Bradley Mitchell & Melendi, LLP

Gray H. Miller, United States District Judge

Case Manager

Rhonda Moore-Konieczny Case Manager (713) 250-5129 (voice) (713) 250-5894 {fax) [email protected]

515 Rusk Avenue, Room 9010C Houston, Texas 77002-2605

Appearances Contact with Court Personnel Continuances Courtesy Copies of Documents Courtroom Procedures Depositions Discovery and Scheduling Disputes Emergencies Eouipment Exhibits Forms Initial Pretrial Conferences and Docket Control Orders Memoranda of Law Motion Practice Required Trial Materials Settlements and Orders of Dismissal Trial Settings Voir Dire

Career Law Clerk

Anna Archer Anna [email protected]

Education: University of Houston, B.S., Psychology University of Houston Law Center, J.D.

Term Law Clerk

David Schwan Dayjd [email protected]

Education: University of Dallas, B.A., History University of Houston Law Center, J.D.

Term Law Clerk

Heather Winter Heather [email protected]

Education: University of Texas, B.S., Government University of Houston Law Center, J.D.

Selected Decisions

Carico Inys, Inc. v. Tex. Ale. Bev. Comm'n Ass'n of Ale. Bev. Permit Holders v. City of Houston Serv. Emp'ees Int'l Union v. City of Houston United States ex re/lonqhi v. Lithium Power Tech. United States v. Yanez Aldridge v. Thaler Fisher v. Halliburton

Judge Gray H. Miller

:Biography

Education

Judge Gray H. Miller was appointed as a

United States District Judge by President George W. Bush

on April 25, 2006.

Judge Miller attended the United States Merchant Marine Academy from 1967 to 1969. He received a B.A. in 1974 and a J.D. in 1978 from the University of Houston, where he was a member of the Order of the Barons. He was admitted in 1978 to practice law in Texas. He is a member of the

• bar of the United States Supreme Court.

Work Experience

2006-present

1998-2006

1986-1998

1978-1986

1969-1978

United States District Judge, Southern District of Texas

Senior Partner, Fulbright & Jaworski L.L.P.

Partner, Fulbright & Jaworski L.L.P.

Associate, Fulbright & Jaworski L.L.P.

Police Officer, Houston Police Department

Professional Activities and Memberships

Judge Miller is a member of the Houston Bar Association, the State Bar of Texas, the Maritime Law Association of the United States, the Houston Maritime Arbitrators Association, and the Mariners' Club of Houston (Skipper 1994-1995). He has also served as a vice chair of the Admiralty and Maritime Law Committee of the Tort and Insurance Practice Section of the ABA. He is a life fellow of the Houston Bar Foundation and a fellow of the Texas Bar Foundation. f-Ie is a member of the Houston Marine Insurance Seminar Executive Committee and has served on the planning committees for seminars on Admiralty and Maritime Law sponsored by the State Bar of Texas, the University of Texas and South Texas College of Law. He is a frequent speaker at these seminars. Judge Miller is listed in the 2001-2006 editions of "The Best Lawyers in America" as one of the top admiralty lawyers In the country. He is also listed in the 2003 edition of "Euro Money's Guide to the World's Leading Maritime Lawyers" and was chosen as a "Texas Super Lawyer."

Judge Mlller is Vice President and Counselor to the Executive Committee of the Garland R. Walker American Inn of Court. He is also a judicial liaison to the Federal Bar Association, Southern District of Texas Chapter and an honorary member of the Phi Delta Phi International Legal Honor Society.

Member of Advisory Board, Cavalla Historical Foundation

Life Member, 100 Club of Houston

Life Fellow, Houston Bar Foundation

Fellow, Texas Bar Foundation

Associate Member, U.S. Merchant Marine Academy Alumni and Foundation

Board of Texas Department of Mental Health & Mental Retardation (2002-04)

Board of Trustees, Harris County Mental Health/Mental Retardation Authority (1991-99), Chairperson (1997-99)

Judge Shadwick graduated from the University of Kansas in 1978 and from Baylor University School of Law

School in 1981. Judge Shadwick became licensed to practice law in both Texas and Kansas in 1981. After

practicing in Kansas for five years, in 1986 Judge Shadwick moved to Houston where he became a shareholder

at Winstead, McGuire, Sechrest & Minick. He served two terms on the Houston ISD school board, including

one year at its president. Judge Shadwick is AV rated by Martindale-Hubbell.

Judge Shadwick was appointed Judge of the 55th Judicial District Court by Governor Perry in December 2007,

where he serves today.

Views From The Bench (Part 1): Insights From Three Trial Judges On Best Practices For Trial Lawyers In Insurance Cases Chapter 9

i

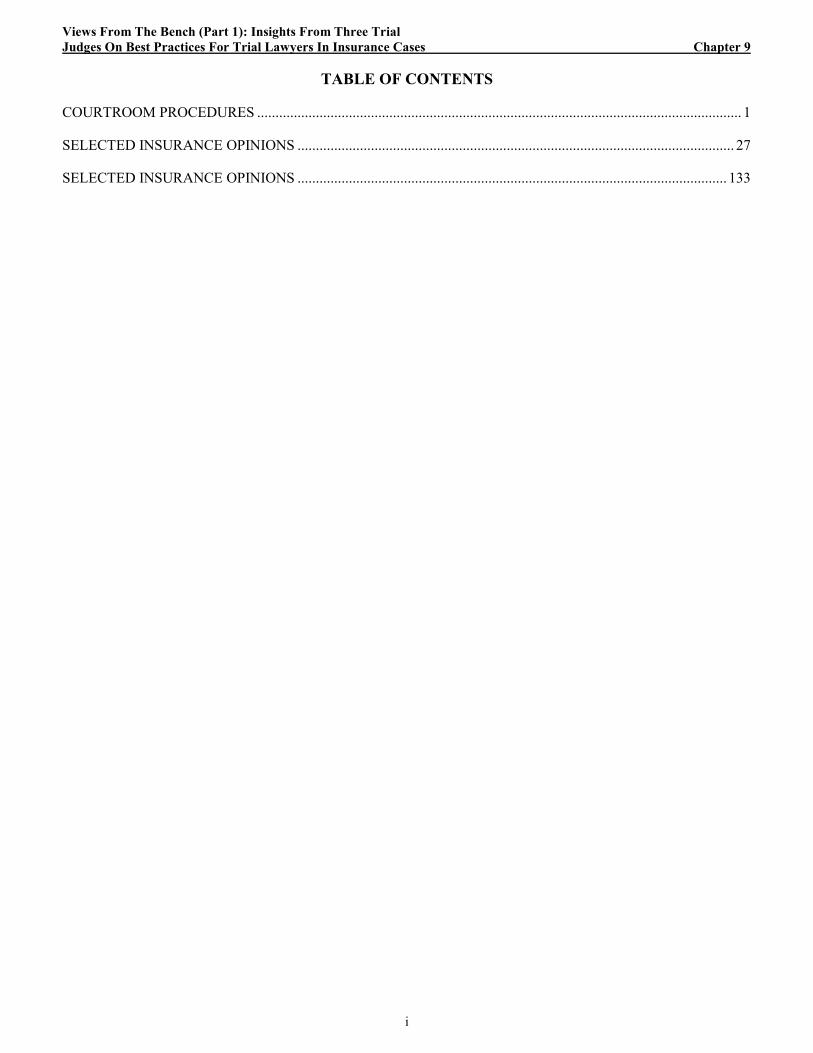

TABLE OF CONTENTS

COURTROOM PROCEDURES .................................................................................................................................... 1

SELECTED INSURANCE OPINIONS ....................................................................................................................... 27

SELECTED INSURANCE OPINIONS ..................................................................................................................... 133

HON. JEFF SHADWICK55th CIVIL DISTRICT COURT

HARRIS COUNTY, TEXAS

1

COURTROOM

PROCEDURES

3

Harris County District Courts Page 1 of!

Texas SupremeCourt RuleChanges

CaseInformation!nal!iLvCivilCourthouse Civil CourthouseTechnology

Pro hac viceCivilCourthouseDirections

ElectronicDocumentFiling Rules

Civil Ad LitemStandards andProcedures

General Civil CourtInformationClick on any of the links below toget more information about thegiven toplc...

Local Rulesfor the CivilCourts

Rules CivilElectronicMedia

Judge JeffShadwickHarrisCounty CivilCourthouse201 Caroline.9th FloorHouston.Texas 77002

Harris CountyDistrict Courts

Horne I Courts 1 Civil I Judge Jeff Shadwick

~Home 55th Civil CourtDistrict Clerk

Court InformationCourts -Local RulesGrand Jury InfoJury InfoProcess ServersJudicial AssignmentsBail Bond ScheduleDowntown LocationsCriminal Justice CenterCivil CourthouseDowntownDining

Other InformationFAQCourts & LawDC Web EmailVisiting the CourthouseApplicationsFOAMSCourt Reporters

Court Staff

Law Clerk

Daniel Flores

Jonathan Patton

George Cardenas

Rudy Guillen

Gina Wilburn

Court Phone: (713) 368-6055Fax Number:Law Clerk:

Clerk:

Assistant Clerk:

Coordinator:Bailiff:

Court Reporter:

713-368-6065

713-368-6055

713-368-6055

713-368-6050

713-368-6058

713-368-6056

55th Civil Court Information

Court Procedures

Court Staff

Standing Pre-Trial Order

A Few Words About Late Filings and Courtesy Copies

Harris County Administrative Offices of the District Courts 2006

Site best viewed in 1024X768 Resolution. For questions or comments Contact Us,

http://www.justex.net/Courts/Civil/CivilCourt.aspx?crt=2 4/4/20144

Harris County District Courts Page 1 of 1

Harris CountyDistrict Courts

Horne I Courts I Civil I Judge Jeff Shadwick I Court Details......

All motions and responses must have proposed orders.

The Court does not need a courtesy copy of any filed motion.

Docket Call for trials is held on Monday one week before the trial setting at 11 :00 a.m. The onlythings we will discuss at Docket Call is the length of trial and when your trial will likely start. We willmake every effort to give you a good idea when your case will start.

Pre-Trial Conferences are usually held on the morning of the trial. We will request a jury panel themorning trial starts. They usually arrive at 9:30 a.m. giving us little time to discuss pre-trial matters. Ifthe parties believe it will take more than 30 minutes to do those things listed below, let us know atDocket Call and other arrangments will be made for the week between Docket Call and the trial.

Court ProceduresAll oral motions are heard on Mondays at 9:00 and 10:00 a.m. Call the Clerk of the 55th for anassignment. The Clerk will also let counsel know whether motions will be by submission or oralhearing. Motions set for submission are also set at 9:00 a.m. on Mondays. The Court will, in almostall circumstances, rule on motions set for submission by Friday of the week the motion is submitted.If you have not recived a ruling by the second Friday after submission, please call the Clerk of the55th. WHETHER ORAL OR SUBMISSION, FILE AND SERVE THE APPROPRIATE NOTICE OFHEARING.

Back to judge PageJudge Jeff ShadwickHomeDistrict ClerkCourt InformationCourtsLocal RulesGrand Jury InfoJury InfoProcess ServersJudicial AssignmentsBail Bond ScheduleDowntown LocationsCriminal Justice CenterCivil CourthouseDowntownDining

Other InformationFAQCourts & LawDC Web EmailVisiting the CourthouseApplicationsFDAMSCourt Reporters

At the Pre-trial Conference be prepared to discuss the following items (please see the Standing PreTrial Order):

1. Trial Exhibits. Each party shall prepare and bring two extra copies of their exhibit list (one for thejudge and one for the Court Reporter). Be prepared to discuss which of your opponents' exhibits youdo and do not object to. I will rule on the objections before trial begins.

2. Video Depositions. Be prepared to discuss offers and objections.

3. Proposed Jury Charge. While we will have formal and informal jury charge hearings as the trialprogresses, please bring your proposed jury charge to the Pre-Trial Conference on a CD or jumpdrive so I can begin reviewing it during the trial.

4. Motions in Limine. The Court does not require a Motion which states that everyone will follow therules of evidence. Present only those items special to your case. Be prepared to discuss what youdo and do not agree upon.

5. law Briefs and Cases. Please brief and/or bring cases on unusual legal and evidentary issues.

Harris County Administrative Offices of the District Courts 2006

Site best viewed in "I024X768 Resolution. For questions or comments Conlact Us.

http://www.justex.netJCourts/Civil/CourtSection.aspx?crt=2&sid=158 4/4/20145

Harris County District Courts

Harris CountyDistrict Courts

Horne I Courts I eM! I Judge Jeff Shadwick I Court Details......

Page 1 of 1

There are new issues arising as we make this transition to electronic filing and this is one thatneedlessly consumes a great deal of our clerk's time.

A Few Words About Late Filings and Courtesy CopiesThere are few excuses for late filings. If you feel the need to file something within 24 business hoursof your hearing please file it with the District Clerk's office. If you provide a courtesy copy to the courtplease clearly mark it "Courtesy Copy" so we will know that it has already been filed and imaged sowe do not have to spend time trying to make that determination.

HomeDistrict ClerkCourt InformationCourtsLocal RulesGrand Jury InfoJury InfoProcess ServersJudicial AssignmentsBail Bond ScheduleDowntown LocationsCriminal Justice CenterCivil CourthouseDowntownDiningOther InformationFAQCourts & LawDC Web EmailVisiting the Courthouse

ApplicationsFDAMSCourt Reporters

JUdge Jeff Shadwick Back to judge Page

Harris County Administrative Offices of the District Courts 2006

Site best viewed in 1024X768 Resolution. For questions or comments Contact Us.

http://www.justex.netiCourts/Civil/CourtSection.aspx?crt=2&sid=302

jlllltex.rnet

4/4120146

Harris County District Courts Page 1 of2

At least three days before trial, or the Pre-Trial Conference, theparties must serve upon each other the following items (if any) for review:

CAUSE NO. _

Standing Pre-Trial Order

HomeDistrict ClerkCourt InformationCourtsLocal RulesGrand Jury InfoJury InfoProcess ServersJudicial AssignmentsBail Bond ScheduleDowntown Locations

. Criminal Justice CenterCivil CourthouseDowntownDiningOther InformationFAQCourts & LawDC Web EmailVisiting the CourthouseApplicationsFOAMS

Court Reporters

Judge Jeff Shadwick

Standing Pre-Trial Order

v.COUNTY, T E XA S

JUDICIAL DISTRICT

§

Back to judge Page

IN THE DISTRICT COURT OF§

§ HARRIS

§

§ 55th

1. Motion in Limine2. Video Deposition Offers and Objections3. Exhibit Lists (2 extra copies - one for the Court Reporter and one

for the Judge)4. Stipulations5. Briefs/Cases6. Proposed Jury Questions

Please file your Motion in Limine with the Clerk so that the Courtmay review it in preparation for trial

Prior to the day of trial or Pre-Trial Conference} the parties shallreview each others' items as set forth above and make their best efforts toagree upon as many exhibits, deposition offers, limine items and juryquestions as possible.

At the appearance for jury selection/triaIjPre-Trial Conference, bringthe originals of the items listed above directly to the Presiding Judge forfiling, review} discussion and rulings.

http://www.justex.netiCourts/CiviIlCourtSection.aspx?crt=2&sid=300 4/4120147

HARRIS COUNTY

LOCAL RULES OF THE DISTRICT COURTS

concerning the

ELECTRONIC FaINGOF COURTDOCUMENTS

PART 1. GENERAL PROVISIONS

Rule 1.1 PuI1lose

These rules govern the electronic f.tling and service of court documents, by any methodother than fax filing, in Harris County. These rules are adopted pursuant to Rule 3 a oftheTexas Rules ofCivil Procedure and may be known as the "Harris County Local Rules ofthe District Courts Concerning the Electronic Filing of Court Documents."

Rule 1.2 Effect on Existing Local Rules

These rules are adopted in addition to any other local rules ofthe district courts in HarrisCounty. These rules do not supersede or replace any previously adopted local rules.These rules are in addition to current local rules, Part 4 electronic court documents (faxfiling).

PART 2. DEFINITIONS

Rule 2.1 Specific Tenus

The following definitions apply to these rules:

(a) "Convenience fee" is a fee charged in connection with electronic filing that is in'addition to regular filing fees. A Convenience Fee charged by the District Clerk shall notbe considered as a court cost. '

(b) "District clerk" means the Harris County District Clerk.

(c) "Document" means a pleading, plea, motion, application, request, exhibit, brief,memorandum oflaw, paper, or other instrument in paper form or electronic form.

(d) "Electronic filing" is a process by which a filer files a court document with the districtclerk's office by means of an online computer transmission ofthe document in electronicform. For purposes ofthese rules, the process does not include the filing of

Approved - Board ofDistrict Judges 11/09/04

lof9

"

8

faxed documents which is described as the "electronic filing ofdocuments" in Section51.801, Government Code.

(e) "Electronic Filing Service Provider (EFSP)" is a business entity that provideselectronic filing services and support to its customers (filers). An attorney or law firmmay act as an EFSP. .

(f) "Electronic Service" is a method of serving a document upon a party in a case byelectronically transmitting the document to that party's e-mail address.

(g) ''Electronically File" means to file a document by means ofelectronic filing.

(h) "Electronically Serve" means to serve a document by means of electronic service.,

(i) "Filer" means a person who files a document, including an attorney.

(j) "Party" means a person appearing in any case or proceeding, whether represented orappearingyro se, or an attorney ofrecord for a party in any case or proceeding.

(k) "Regular Filing Fees" are those filing fees charged in connection with traditionalfiling.

(1) "Rules" are the Harris County Local Rules ofthe District Courts concerning theElectronic Filing of Documents.

(m) "Traditional Filing" is a process by which a filer files a paper document with a clerkor ajudge.

Rule 2.2 Application to Pro Se Litigants

The term "counsel" shall apply to an individual litigant in the event a party appears prosa,

PART 3. APPLICABILITY

Rule 3.1 Scope

(a) These rules apply to the filing ofdocuments in all non-juvenile civil cases, includingcases that are appeals from lower courts, before the various district courts withjurisdiction in Harris County.

(b) These rules apply to the filing ofdocuments in cases before the various district courtsreferred to in paragraph (a) above that are subsequently assigned to associate judges orany other similarjudicial authorities.

Approved - Board ofDistrict Judges 11109104

Z of9

9

!1I:,

Rule 3.2 Clerks

These rules apply only to the filing ofdocuments with the district clerk. These rules donot apply to the filing ofdocuments directly with ajudge as contemplated by TEX. R.CIV.P.74. '

Rule 3.3 Documents That May Be Electronically Filed

(a) A document that can be filed in a traditional manner with the district clerk may beelectronically filed with the exception ofthe following docUments: '

i) citations or writs bearing the seal ofthe court;

ii) returns ofcitation;

iii) bonds;

iv) subpoenas;

v) proof of service of subpoenas;

vi) documents to be presented to a court in camera, solely for the purpose of. obtaining a ruling on the discoverability ofsuch documents;

vii) documents sealed pursuant to TEX. R. CIV. P. 76a; and

viii) documents to which access is otherwise restricted by law or court order,including a document filed in a proceeding under Chapter 33, Family Code.

(b) A motion to have a document sealed, as well as any response to such a motion, maybe electronically filed.

Rule 34 Dgcuments Containing Signatures

(a) A document that is required to be verified, notarized, acknowledged, sworn to, ormade under oath may be electronically filed only as a scanned image.

(b) A document that requires the signatures ofopposing parties (such as a Rule 11agreement) may be electronically filed only as a scanned 'image.

(c) Any affidavit or other paper described in Rule 3.4(a) or (b) that is to be attached to anelectronically-filed document may be scanned and electronically filed along with theunderlying document.

Approved ~ Board ofDistrict Judges 11109104

30f9

10

(d) Where a filer has electronically filed a scanned image under this rule, a court mayrequire the filer to properly fIle the document in a traditional manner with the districtclerk. A third party may request the court in which the matter is pending to allowinspection ofa document maintained by the filer.

PART 4. FILING MECHANICS

Rule 4.1 TexasOnllne

(a) Texas Online is a project ofthe TexasOnline Authority, a state entity charged withestablishing a common electronic infrastructure thr<;mgh which state agencies and localgovernments may electronically send and receive documents and required payments.

(b) To become registered to electronically file documents, fIlers must follow registrationprocedures outlined by TexasOnline. The procedure can be accessed from TexasOu!ine'swebsite at ..www.texasonline.com...

(c) Filers do not electronically fIle documents directly with the district clerk. Rather,fIlers indirectly fIle a document with the district clerk by electronically transmitting thedocument to an electronic filing service provider (EFSP) which'then electronicallytransmits the document to TexasOuline which then electronically transmits the documentto the district clerk. A fIler fIling or serving a document must have a valid account withan EFSP and with TexasOnline.

(d) Consistent with standards promulgated by the Judicial Committee on InformationTechnology (JeTI'), TexasOnline will specifythe permissible formats for documents thatwill be electronically fIled and electronically served. . .

(e) Filers who electronically file documents will pay regular fIling fees to the districtclerk indirectly through TexasOuline by a method set forth by TexasOnline.

(f) An EFSP may charge filers a convenience fee to electronically file documents. Thisfee will be in addition to regular filing fees. .

(g) TexasOnline will charge ftlers a convenience fee to electronically file documents.This fee will be in addition to regular filing fees and will be in an amount not to exceedthe amount approved by the TexasOnline Authority.

(h) The district clerk may charge filers a convenience fee to electronically file documents.This fee will be in addition to regular filing fees, credit card fees, or other fees.

Rule 4.2 Signatures

(a) Upon completion of the initial registration procedures, each fIler will be issued aconfidential and unique electronic identifier. Each fIler must use his or her identifier in

Approved - Board ofDistrict Judges 11109/04

4of9

11

order to electronically file documents. Use ofthe identifier to electronically filedocuments constitutes a "digital sigmiture" on the particular document

(b) The attachment of a digital signature on an electronically-filed document is deemed toconstitute a signature on the document for purposes ofsignature reqnirements imposed bythe Texas Rules ofCivil Procedure or any other law. The person whose name appearsfirst in the signature block ofan initial pleading is deemed to be the attorney in charge forthe purposes ofTexas Rules ofCivil Procedure 8, unless otherwise designated. Thedigital signature on any document filed is deemed to be the signature ofthe attorneywhose name appears first in the signature block ofthe document for the purpose ofTexasRules ofCivil Procedure 13 and 57.

(c) A digital signature on an electronically-filed document is deemed to constitute asignature by the filer for the purpose ofauthorizing the payment ofdocument filing fees.

Rule 4.3 Time Document is Filed

(a) A filer may electronically transmit a document through an EFSP to TexasOnline 24hours per day each and every day ofthe year, except during briefperiods ofstateapproved scheduled maintenance which will usually occur in the early hours ofSundaymoming.

(b) Upon sending an electronically-transmitted document to a filer's EFSP, the filer isdeemed to have delivered the document to the clerk and, subjectto Rule 4.3(h), thedocument is deemed to be filed. Ifa document is electronically transmitted to the filer'sEFSP and is electronically transmitted on or before the last day for filing the same, thedocument, ifreceived by the clerk not more than ten days tardily, shall be filed by theclerk and deemed filed in time. A transmission report by the filer to the filer's EFSP shallbe prima facia evidence ofdate and time oftransmission.

(c) On receipt ofa filer's document, the filer's EFSP must send the document to TexasOnline in the required electronic file format along with an indication ofthe time the filersent the document to the EFSP and the filer's payment information. TexasOnline willelectronically transmit to the fIler an "acknowledgment" that the document has beenreceived by TexasOnline. The acknowledgment will note the date and time that theelectronically-transmitted document was received by TexasOnline.

(d) Upon receiving a document from a filer's EFSP, TexasOnline shall electronicallytransmit the document to the district clerk. Ifthe document was not properly formatted,Texas Online will transmit a waming to the filer's EFSP.

(e) Not later than the first business day afterreceiving a document from TexasOnline, thedistrict clerk shall decide whether the document will be accepted for filing. The districtclerk shall accept the document for filing provided that the document is not misdirectedand complies with all filing requirements. The district clerk shall handle electronically-

Approved~BoardofDistrictJudges11109/04 .

Sof9

12

transmitted documents that are fJled in connection with an affidavit ofinability to affordcourt costs in the manner required by TEX. R. CN. P. 145. lfthe clerk fails to accept orreject a document within the time period, the document is deemed to have been acceptedand filed.

(f) lfthe document is accepted for filing, the district clerk shall note the date and time offiling which, with the exception of subsection (h) below, shall be the date and time thatthe filer transmitted the document to the filer's EFSP. The district clerk shall informTexasOnline ofits action the same day action is taken. TexasOnline shall, on that sameday, electronically transmit to the ftler's EFSP a "confirmation" that the document hasbeen accepted for filing by the district clerk. The EFSP will electronically transmit theconfirmation to the filer. This confirmation will include an electronically "fJle-marked"copy ofthe front page ofthe document showing the date and time the district clerkconsiders the document to have been filed.

(g) lfthe document is not accepted for ftling, the district clerk shall inform TexasOnlineofits action, and the reason for such action, the same day action is taken. TexasOnlineshall, on that same day, electronically transmit to the ftler's EFSP an "alert" that thedocument was not accepted along with the reason the document was not accepted. TheEFSP will electronically transmit the alert to the ftler.

(h) Except in cases of injunction, attachment, garnishment, sequestration, or distress .proceedings, documents that serve to commence a civil suit will not be deemed to havebeen filed on Sunday when the document is electronically transmitted to the filer's EFSP,TexasOnline, or the Clerk on Sunday. Such documents will be deemed to have been fJledon the succeeding Monday.

Rule 4.4 Filing Deadlines Not Altered

The electronic ftling of a document does not alter any ftling deadlines.

Rule 4.5 Multinle Documents

(a) Except as provided by subsection (b) below, a filer may include only one document inan electronic transmission to TexasOnline.

(b) A ftler may electronically transmit a document to TexasOnline that includes anotherdocument as an attachment (e.g., a motion to which is attached a briefin support ofthemotion).

Rule 4,6 Official DOGuwent

(a) The district clerk's ftle for a particular case may contain a combination ofelectronically-ftled documents and traditionally-ftled documents.

Approved - Board ofDistrict Judges 11/09104

60f9

13

(b) The district clerk may maintain and make available electronically-fIled documents inany manner allowed by law.

Rule 4.7 E-mail Address Required

In addition to the information required on a pleading by TEX. R. CN. P. 57, a fIler mustinclude an e-mail address on any electronically-filed document.

Rule 4.8 Document Format

(a) Electronically-filed documents must be computer-formatted as specified byTexasOnline. Electronically-fIled documents must also be formatted for printing on 8 Yz.inch by ll-inch paper.

(b) An electronically-filed pleading is deemed to comply with TEX. R. CN. P. 45.

fART 5. SERVICE OF DOO!MENTS OTHER THAN CITATION

Rule 5.1 Electronic Service ofDocuments Permissible

(a) In addition to the methods ofserving documents (other than the citation to be servedupon the filing ofa cause ofaction) set forth in lEX. R. CN. P. 21a, a fIler may servedocuments upon another party in the case by electronically transmitting the document tothat party at the party's email address. Service in such a manner is known as 'Electronicservice," and is permissible in the circumstances set out in paragraph (b) below.

(b) Documents may be electronically served upon a party only where that party has.agreed, in writing to receive electronic service in that case. The clerk shall adopt astandard form ofagreement which provides that the party has agreed to electronicallyaccept service, sets out the e-mail address where service should be sent, and informs theparty ofthe right to rescind the agreement by subsequent notice to the court. Theagreement must be fIled with the court and the form must be served on all other parties.

(c) By virtue ofelectronically fIling a document or serving a document or by agreeing toaccept service, a filer additionally agrees to provide information regarding any change inhis or her e-mail address to TexasOnline, the district clerk, and all parties in the case.

(d) A party who electronically fIles a document is not required to electronically servedocuments upon other parties. Electronic service ofdocuments is an optional method of

,service.

(e) A filer may electronically serve a document in instances where the document istraditionally fIled as well as in instances where the document is electronically fIled.

Approved - Board ofDistrict Judges 11/09104

70f9

14

Rule 52 Completion ofService and Date of Service

(a) Electronic service shall be complete upon transmission ofthe document by the f.tler tothe party at the party's e-mail address.

(b) Except as provided by subsection (c) below, the date ofservice shall be the date theelectronic service is complete.

(c) When electronic service is complete after 5:00 p.m. (recipient's time), then the date ofservice shall be deemed to be the next day that is not a Saturday, Sunday or legal holiday.

Rule 5.3 Time for Action After Service

Whenever a party has the right or is required to do some act within a prescribed period oftime after service of a document upon the party and that document is electronicallyserved, then three days shall be added to the prescribed period oftime.

Rule 5.4 Certification of Service

(a) Documents to be electronically served upon another party shall be sent before the timeor at the same time that the document is f.tled. .

(b) A filer who electronically serves a document upon another party shall make a writtencertification of such service that shall accompany the document when that document isf.tled. The written certification shall include, in addition to any other requirementsimposed by the Texas Rules ofCivil Procedure, the following:

(i) the f.tler's e-mail address or telecopier (facsimile machine) number;

(li) the recipient's e-mail address;

(iii) the date and time ofelectronic service; and

(iv) a statement that the document was electronically served and that theelectronic transmission was reported as complete.

PART 6. ELECTRONIC ORDERS AND yrnwING OF ELECTRONICALLYFILED DOCUMENTS

Rule 6.1 Courts Not Authorized to make Electronic Orders

(a) Judges shall continue to sign paper copies ofcourt orders, judgments, rulings, noticesand other court-produced documents ("court orders").

Approved - Board ofDistrict ludges 11109/04

80f9

15

(b) The district clerk may electronically scan a court order. The scanned court order maythen serve as the official copy ofthe court order. The district clerk is not required toelectronically scan court orders in order to create official electronic court orders.Electronic scanning ofcourt orders is at the option ofthe district clerk.

Rule 6.2 viewing ofElectronically.med DOCllmenp;

(a) The district clerk shall ensure that all the records ofthe court, except those madeconfidential or privileged by law or statute, may be viewed in some format by all persons .for free.

(b) Independent ofthe TexasOnline system and the requirement ofviewing accessdescribed in subsection (a), the district clerk may choose to provide for both filers and thegeneral public to electronically view documents or court orders that have beenelectronically filed or scanned. Where such provision has been made, persons mayelectronically view documents or court orders that have been electronically fIled orscanned. .

(c) Nothing in this rule allows for the viewing ofdocuments or court orders, in any form,that are legally confidential (e.g., papers in mental health proceedings).

PART 7. MTSCELLANEmJS PROVISIONS

Rule 7.1 Assigned Court to Resolve Disputes

..In the event a dispute should arise involving the application ofthese rules or variouselectronic filing issues, a district court assigned in accordance with local assignmentprocedures shall decide any dispute.

These rules shall become effective upon their approval by the Supreme Court ofTexas.

Approved ~ Board ofDistrict Judges 11109/04

90f9

16

SELECTED

INSURANCE OPINIONS

17

CAUSE NO. 2010-47654

IN THE DISTRICT COURT OF

FIREMEN'S FUND INSURANCECOMPANY

o-PM HOUSTON PROPERTIES,LTD., et al.

VS

§§§§§ HARRIS COUNTY*EXAS§ (&<s;;,§ ~)

§ 0§ 0 ~§ 55THJUD~DISTRICT

00ORDER AND FINDINGS ON DEFENDANT'S PLE~~HE J1JRISDICTION

~The Court conducted an evidentiary hearing o~~ndant's Plea to the Jurisdiction.

Pursuant to such hearing, the Court finds and rules as~s:

Defendant's Plea to the Jurisdiction is D~~D. The Plaintiffs have standing to make.,~

the claims in their Petition, as amended. . 0~.

Fireman's Fund Insurance comp;9<"Fireman's" or "Defendant") has filed a Plea to the

Jurisdiction questioning the stand.~f each Plaintiff to pursue a claim under the subject,"-~--

insurance policy. Fireman's .~Q~ that the Plaintiffs either had no ins\l~a1:Jle interest in the

prClperties which were da~~in Hurricane Ike, or are not named insureds under the policy. A

.plea to the jurisdictio~s the appropriate vehicle to challenge a party's lack of standing.o~([)r

Standing is a thr~ inquiry. MD. Anderson Cancer Center v. Novak, 52 S.W.3d 704, 710=~

(Tex. 2001~~ding is a component of subject matter jurisdiction. Waco ISDv. Gibson, 22

S.W.3d 849, 850 (Tex. 1998).

As set out in the Court's July 23,2013 Notice of Hearing, the hearing was pursuant to the

guidance found in Texas Department of Parks and Wildlife v. Miranda, 133 S.W.3d 217, 226-

228 (Tex. 2004). The Court is pursuing the "decision tree" described in that Notice. Plaintiff

18

has made objections to this process claiming that determining whether they have rights under the

subject insurance policy is nothing different than proving the first element ofa breach of contract

action. In taking evidence and ruling upon Fireman's plea, Plaintiffs assert that the Court is

improperly splitting its cause of action. Fireman's has not objected.

In previously denying Fireman's motion for summary judgment, th~urt found that~!@

there are issues of fact as to Plaintiffs' standing. Taking the next step i@ Miranda decision

~tree, having heard the evidence, the Court believes that ruling upo~standing issue does not

implicate the merits of the Hurricane Ike insurance claim raise~er the subject policy. Since

the existence, terms, and conditions of the 2008 insurancev~y are not contested, ruling upon

the standing question will not interfere with the j~~termination of an insurance claim.

Accordingly, the standing issue will not besubtni~O the jury in the insurance claim trial, and

the Court will resolve that issue here. ~

All insurance companies, includi~ireman's, require that every property insurance

policy has a named insured, and th~~amed insured be someone with an insurable interest in

the subject property. The 2006~~y which was the first between the parties for the period

relevant to this litigation re~~"Triyar Group" as named insured. The 2007 policy reflects

"Triyar Companies, LLCQ ~amed insured, as does the 2008 policy which was the policy under.~ ..

which Plaintiffs ~~eir claims.

At no~~as either Triyar Group or Triyar Companies, LLC ever an Owner, tenant, or

otherwise a~riy with an insurable interest in the real property which'suffered a casualty loss. In

addition, Triyar Group is not a legal entity at all, something which the Court found at a glance to

be perfectly obvious. There are no indicia of corporate status in its name. Triyar Companies,

LLC, was at one time a legal entity but not at the time it was listed as named insured on the

2

19

20008 policy. Despite these facts, Fireman's issued policies of insurance in their name.

Apparently, then, Fireman's did the very thing its witnesses earnestly assured this Court it would

never do: sell a policy to any entity which did not have an insurable interest, and perhaps was

not a real entity at all. This happened three times, in 2006 through 2008. The Court is left to

decide whether the parties had an agreement which violated Fireman's poli~r that they did. /f'~~

not have an agreement at all. The Court finds the former. y~

The evidence strongly supports the conclusion that "Triyar ~,,, which appears on the

2006 policy as named insured, was a mere placeholder name. df:!s placed there, interestingly,

by Fireman's. Defendant's Exhibits 156 and 25 tell the.t~ Triyar's insurance application,

Defendant's Exhibit 156, shows "Triyar companies~~l see attached" as proposed named

insured. Fireman's makes much ofa later "see att=.~ schedule" on the application as somehow!f!'-directing Fireman's to look at the apPlicatio~erently, but the Court sees no importance in

~~"see attached" versus "see attached scj@iile." There are, in fact, two schedules. The

@application includes a schedule at.~~s numbered pages 001048 and 001049, which has a

F'\)~'"column designated "Entity NameJ7 Defendant's witness testified unconvincingly that this

schedule gave them no cI~e~'1oever of those entities' interest in the listed properties. It was

perfectly obvious, to th~Mrt at least, that Defendant's Exhibit 156 reflects a list of single asseto{@

entities which O~~listed properties. A number of other conclusions may be possible, but

none which le~Q easily to mind. The cluelessness of Fireman's witnesses as to the contents of

this sChedu~uld only be explained as non-credible, post-casualty, revisionism. The Court did

not believe a word of it. The application then schedules the properties themselves at Bates

numbered pages 001053 and 001054, just as the cover page indicates. There is no confusion.

3

20

Fireman's.

The application also indicates "NAMED INSURED: Triyar Group" which is not an

entity at all. Fireman's indecision as to who to list as named insured was justified as was its

interest in specificity, but Fireman's claim not to know of the single assets entities was not. The

indecision lead to several inquiries to the broker. The parties disagreed about whether the

inquiries went unanswered. Apparently Fireman's simply elected to show "T~W Group" as the(~

m2~)nan1ed insured in the 2006 policy without other input. Paul Walker of ~nan's, not knowing

~what to do with "a1l the other entities," decided after the policy ~~und to "Please just go

with Triyar Companies LLC for now." Exhibit 25 (emphasis~~. That either Triyar Group

or Triyar Companies LLC was just a placeholder name is t~~ade very clear.~

Brian Klepchick's affidavit testimony supports t~ourt's view of what happened. The<t::)}'1"!Court believes his affidavit testimony that "In 200~~iyarCompanies, LLC applied for property

insurance from FFIC asking that SJM Realtx&~ ("SJM") and GPM Houston Properties, Ltd. S~~·

("GI'M") be included in the proposed 20~07 policy as additional insureds." His following

sentence in his Affidavit, "Such 200~~est was not accepted by FFIC," weighed very heavily\~

on the Court in its prior rulings\~ was noticed by the Court. Mr. Kelpchick recanted this

testimony in the hearing wit~""1roviding any reason behind the change other than to call it antFP

error. The Court belie.xWihe change simply met the current legal narrative being urged byi~

.~(Qr

~There~UCh testimony which centered around which party had a duty to get the name

right. cert~ both parties had their own reasoning for getting it right, and both were sloppy

not to do so. This case is not about legal duty; it is about whether the evidence reflects an

agreement. As set out herein, the parties chose to have the policies say what they say. When

Plaintiffs saw over the years that the named insureds were not listed individually, they were

4

21

simply seeing a policy which said what they thought the parties agreed it would say. There was

no reason for Plaintiffs to advise Fireman's of a problem. See Defendant's Exhibit 22, for

example.

When the 2007 and 2008 policies listed Triyar Companies, LLC as named insured, that

name was no less a placeholder than was Triyar Group in 2006. Exhibit~ states. Triyar®1

Companies, LLC also had no insurable interest in the various prope~ and, according to

~Defendant, should not have been the name on the policy. That Tri~~Ceompanies, LLC was or

~'d~~~?)was not a legal entity, or later changed its name, or transferr~~ assets, or not, is hardly the

point. The point is that the parties used the name as a Placeh~r for someone else.

~~Defendant's belief that any entity named Tri~~ed any portion of Greenspoint Mall

or San Jacinto Mall was not reasonable and hadollf1te to no basis in the evidence. Defendantf0er

knew or should have known that the owne~re GPM Houston Properties, Ltd. and SJM

Realty, Ltd., respectively. The 2006 ap~tion was clear enough on that point. Fireman'sr@

underwriters made minimal effort~~termine the aGtual owners of the malls despite their

sW~

, I

insistence that their-insured-mu. ve-an--insur~ble-cillterest-.P'ir~man'-s--wi.tnesses-advised-.fue------

Court of their due diligen:~ ~, but seemed to operate with a Gonfirmation bias whiGh Gaused

them to view informati~~n~GritkallY. All Fireman's had to do is look up title or ask for proof":@j

of title. The faG~~he names on the poliGies do not matGh the names on the appliGations,

m~ .whiGh do not ~"" the names on the proposals, undermine Fireman's reGent protestations. If

Fireman's ~undear they would not have issued the polky. That the issued the polky leads

the Court to believe either that they were dear, or dear enough.

The Court is therefore left to Gondude that the policies refleGt exaGtly what the parties

intended sinGe the parties dearly intended to enter into the insuranGe GontraGts at issue. Under a

5

22

time crunch to bind insurance by June 30, 2006, and having a good and long relationship with

the broker (Penn) with whom Fireman's could sort out the details later, Fireman's issued a policy

with Triyar Group as named insured in 2006 intending to later replace that with the names of the

actual owners. Having no duty to make a proposal or bind coverage, it was Fireman's who made

the decision. Calling the named insured "Triyar Companies LLC" in the 200'fui'n>! 2008 policies@}"'Jw

changes nothing. Fireman's underwriters appear to have simply carried~d prior work and,~

as in 2006, paid little attention to the named insured. Their testim;-.a:'Aelating to the absolute~r

importance of getting the named insured right made comO'@;;Jj;ense to the Court. Why

Fireman's ignored their standards made no sense, but appe~r-~ have happened.J?The Court finds the parties had an actual .~-~to contract between the insuranceQW!1

company and the actual owners of the propertie~hoever they were. The Court therefore~'"

reforms the 2008 policy to so reflect. This r~~tion does not impact a single provision of the

policy itself, which is highly regulated. It~ges only the entity that is "named insured" so that

the policy uses of"You" and other~terms now refer to GPM and 8JM.

Having found facts in sQort of reformation as outlined above, the Court need not

address waiver or estoppel..~ Court finds no fraud on the part of Fireman's which would!F~

justifY the result set out@'WJs Order and Findings. .¢Wl

IT IS SO~~ERED.

SIGN~ the 9 day of , 2013.

~

FILEDChris DanielDistrict Clerk

AUG 09 2013

6

23

0~/23/2a13 14:22 7133686820

CAUSE NO. 2010-47654

PAGE 02

FIREMEN'S FUND INSURANCECOMPANY

GPM HOUSTON PROPERTIES,LTD., et al.

vs

§ IN THE DISTRICT COURT OF§§§§ HARRIS COUNTY, TEXAS§§§§§ 55TH JUDICIAL DISTRICT

NOTICE OF HEARING

An evidentiary hearing on Defendant's Plea to the Jurisdiction will be held commencing

at 9:00 a.m. on July 26, 2013. The parties may submit exhibits, deposition excerpts and briefing,

as they choose, at any time prior to the commencement oflive testimony on the 26th•

In this hearing the Court will be guided by Texas Department 0/ Parks and Wildlife v.

Miranda, 133 S.W.3d 217, 226-228 (Tex. 2004). The Miranda caSe related to subject mlltter

jurisdiction rather than standing, but the Miranda Court's reasoning applies here. The Miranda

Court recognized that "in some cases, disputed evidence ofjurisdictional facts that also implicate

the merits of the case may require resolution by the finder of fact." [d. at 226. Citing other cases

with approval, the court recognh;ed that "predicate facts" can be so inextricably linked to the

merits that the court may defer resolution of the issue until trial. That inquiry is based upon

whether ''the jurisdictional issue is inextricably bound to the merits of the case."

This begs the question ofwbat are the merits of the Plaintiffs'case. Plaintiffs have argued

often to this Court that their case is about a casualty loss caused by Hurricane Ike, and not issues

relating to the insurance contract. "In this case," stated the Miranda court, "we address a plea to

the jurisdiction in which undisputed evidence implicates both the subject matter jurisdiction of

the court and the merits of the case." [d. at 226. Similarly, this Court is being asked to address a

JUL-23-2013 15:27 7133686820 P.002

24

07/23/2013 14:22•7133686820 PAGE 03

standing issue which may implicate the SUbject matter of Plaintiff's case. It is not clear that

Defendant's standing issue is inextricably linked to Plaintiffs' Ike case. That the insurance

policy is involved in both does not necessarily make the plea and the Ike claim inextricable.

According to Miranda, this Court exercises its discretion in deciding whether the

jurisdictional determination (or standing, in this case) should be made at a preliminary hearing or

await a lUller development of the case. Exercising this discretion, the Court is ordtlling the July

26 hearing. The evidence is "by affidavits or otherwise." Live testimony is included within

'·otherwise."

Plaintiff has offered case law which stands for the proposition that standing is not

jurisdictional; that is, Defendant's standing issue does not affect the court's power to make a

legal decision or enter a judgment. This concept is not in dispute. Defendant's iSSlile is whether

Plaintiffs may go forward, not whether the Court may. That Defendant's pleading is correctly

called a plea to the jurisdiction is merely semantically contusing. Plaintiffs' cases do not change

Miranda. This Court sees no controlling decisions from Houston's First or Fourteenth Court of

Appeals.

What Miranda addresses as none of Plaintiffs' cases do, is what procedure to follow

when a plea and the merits might overlap. It is a question of law whether the plea and the merits

overlap. Thus, giving Miranda a reasonable extension to a case where standing is at issue and

the standing issue relates to but may not be inextricably tied to the underlying claim, the three

tiered "decision tree" articulated by Defendants emerges: First, if there is no material issue of

fact or otherwise the issue can be decided as a matter of law, the inquiry ends and the Court rules

on the plea. Second, if there is a genuine issue of material fact the court must decide whether the

standing challenge inextricably implicates the merits of the Hurricane Ike case. If the merits of

2

JUL-23-2013 15:27 7133686820 99~ P.003

25

07/23/2013 14:22• 7133686820 PAGE 04

the two are not inextricably implicated, then the Court will determine the plea as a fact finder.

Third, ifthe merits of the Ike case are inextricably implicated then the standing issue will be tried

to the jury in the Ike claim case and the Court will have made no ruling other than to let the case

proceed.

IT IS SO ORDERED.

SIGNED on the 23 day of-J~

3

,2013,

71336e6e20 1'.004

26

HON. NANCY K. JOHNSON

UNITED STATES MAGISTRATE JUDGE

SOUTHERN DISTRICT OF TEXAS

SELECTED

INSURANCE OPINIONS

27

Continental Cas. Co. v. Consolidated Graphics, Inc., 656 F.Supp.2d 650 (2009)

West Headnotes (9)

111 Contracts~ Language of Instrument

Under Texas law, terms in contracts are giventheir plain, ordinary, and generally aceepted

meaning unless contract itself shows thatpal1icular definitions are used to replace thatmeaning.

656 F.Supp.2d 650United States District Court,

S.D. Texas,Houston Division.

CONflNENTAL CASUAI,TY COMPANY, Plaintiff,

v.CONSOLIDATED GRAPHICS, INC.; Thousand

Oaks Printing & Specialties, Inc. d/b/a T/O Printing,

and Daniel Chambers, an Individual, Defendants,

Sentry Insmance, a Mutnal Company, Intervenor,

v.Consolidated Graphics, Inc., Thousand Oaks

Plinting & Specialties Inc. d/b/a T/O Printing,

and Daniel Chambers, an Individual, Defendants.

Civil Action No. 4:08-CV

02383. I Aug. 28, 2009.

Synopsis

Background: Excess commercial gencral liability (CGL)

insurer sought declaratory judgment of no duty to defend

or indemnify insured printing company, pursuant to excessCOL policy's advertising injury coverage provision, againstcompetitor's action alleging misappropriation oftrade secrets,unfair business practices lind other torts. Primary CGL insurerintervened. Insurers moved for summary judgment, andinsured cross-moved for partial summary judgment againstprimary CGL insurer.

Holdings: The District Court, Nancy K. Johnson, UnitedStates Magistrate Judge, held that:

[1] competitor's pricing information, including infonnationabout past product promotions. potentially constituted"advertising idea," but

[2] competitor's claim of misappropriation of its pncmg

strategy in order "to solicit" was not within advcliising injuryprovision, given lack of implication of wide dissemination.

Insurerst.mptions bTfanted.

[2]

13]

[41

Cases that cite this headnote

Contracts4f-w Application to Contracts in General

Contracts

*"" Existence of ambiguity

Under Texas law, when contract, as written, canbe given definite or certain legal meaning, thenit is unambiguous as a matter of law, and courtenforces it as written.

Cases that cite this headnote

Insurance~ Exclusions, exceptions or limitations

Under Texas law, if insurance contractprovision, particularly an exclusionary clause,is susceptible to more than one reasonableinterpretation, court must resolve ambiguityin .favor of insured; insured's reasonableconstruction of exclusionary provision must beadopted even if insurerts construction is morereasonable.

Cases that cite this headnote

Insurance'iF' Pleadings

Under Texas law, court applying eight-comersrule in order to determine liability insurer'sduty to defend considers factual allegations ofunderlying complaint in light of insurance policywithout regard to allegations! truth or falsity.

1 Cases that cite this headnote

28

(5]

16]

Insurance"'" Pleadings

Under Texas law, court applying cight,cornersrule in order to determine liability insurer's dutyto defend interprets allegations of underlyingcomplaint liberally and resolves all doubt.

regarding duty to defend in fawr of insured.

I Cases that cite this headnote

Insurance<fi.j.'W Pleadings

Under Texas law, liability insurer is requiredto defend its insured against suit as long asallegation$ of underlying complaint potentiallygive rise to at least one claim covered byinsurance policy.

Cases that cite this headnote

191

2 Cases that cite this headnote

Insurtln£C~ Advertising Injury

InsuranceiP Misappropriation

Under Texas law, printing company's claimthat insured competitor had misappropriatedcompany's business history and pricing strategyin order "to solicit and misappropriate"company's customers was not within advertisinginjury coverage provisions of commercialgeneral liability (CGL) insurance policies, whichcovered use 01' misappropriation of another'sadvertising idea in insured's advertisement, andwhich defined advertisement as OInotice that isbroadcast or published to the general publicor specific m;lrket segments"; solicitation ofcustomers did not imply wide dissemination.

(7]

[S]

Jnsurancc~ Matters beyond ple'ldings

Under Texas law, court determining liabilityinsurer's duty to defend may not read facts intounderlying pleadings, look outside pleadings,or imagine factual scenarios that might triggercoverage.

I Cases that cite this headnote

Insurance""' Advertising Injwy

!Jnder Texas law as predicted by federal districtcourt, printing compl.lny's pricing information,including information about Hpromotionsgiven," potentially constituted "advertisingidea"under advertising injul'Y coverage provisionsof competitor's commercial general liability(CGL) insurance policies, which covered use ormisappropriation of another1s a.dvertising idea ininsured's advertising; promotions given, if notmere histoJical sales records, could constitutemethod of gaining customers or increasingsales, and in tunl confidential informationabout promotions given could be consideredadvertising idea.

2 Cases that ci tc this headnote

Attorneys and Law Firms

*652 John Charles Tollefson, Stephen A. Melendi,Tollefson Bmdley et aI., Dallas, TX, for Plaintiff.

Kathleen Hopkins Alsina, Phelps Dunbar LLP, Houston, TX,Usa Martin Lampkin. Selman Breitman, Los Angeles, CA,for Intervenor.

Richard Paul Colquitt, Fulhright & Jaworski, Houston, TX,

lor Defendants.

Opinion

MEMORANDUM OPINION

NANCY K. JOHNSON, United States Magistrate Judge.

Pending before the court I is the Motion for SummaryJudgment (Docket Entry No. 27) tiled by PlaintiffContinentalCasualty Company ("Continental"), the Motion for SummaryJudgment (Doeket Entry No. 43) tiled hy Intervenor Sentrylnsurance, a Mutual Company ("Sentry"), and the Cross~

Motion for Partial Summary Judgment against Sentry(Docket Entry No. 47) tiled by Defendants Consolidated

29

Continental Ca•. Co. v. Consolidated Graphics. Inc.• 656 F.Supp.2d 650 (2009)

Graphics, Inc. ("CGX"), Thousand Oaks Printing Specialties,Inc. dlbla TID Printing ("TID Printing"), and DanielChambers ("Chambers"). The court has considered themotions, all relevant filings, and the applicable law. For thereasons set forth below, the court GRANTS Continental'sMotion for Summary Judgment, GRANTS Sentry's Motionfor Summary Judgment and DENIES Defendants' CrossMotiou for Summary Judgment.

The parties consented to proceed before the undersignedn1llgistrate judge for all proceedings, including trial andfinal judgment, pursuant to 28 U.s.C. § 636(c) andFederal Rule of Civil Procedure 73, Docket EntlY Nos,2,20.

implicates Continental's CQverag~, because the courtfinds that there is no lOadvcrtising injury" under thelanguage of either policy.

*653 A~ The b ..urollce Policies

1. Continental's PolicyContinental is a liability insurer that issued two conseeutivepolicies of excess umbrella liability insurance to CGX witheffective dates October 1. 2005, to April 1,2007, and April

1,2007, to April I. 2008. (th~ "Continental policy"). R For

the purposes of this action, the language of the policies iseffectively the same.

I. Case Background

This is a dispute over insurance coverage. Continental

issued two excess liability insurance policies to CGX. 2

Sentry issued two primary cQmmercial gell~ral liability

("CGL") policies to CGX. 3 CGX is a Texas eOl'poration, and

Defendant TID Printing is its subsidiaty based in California, 4

Chambers is an individual claiming coverage under the

policies. 5 This case involves a request for declaratoryjudgment whether Continental and Sentry (hereinafter "theInsure,,") have duties to defend and indemnitY CGX against alawsuit brought by a competitor for misappropriation oftrade

secrets. 6 Because the Insurers' policies have similar languagewith respect to the duties to defend and indemnitY, this court

will discuss both motions conCUlTently. 7

8

10 [d. at p. S.

Under the telms of the policy, Continental is requiredto pay on behalf of the insured sums in excess of thescheduled underlying insurance that the insured becomesiegally obligated to pay as a result of any "personal and

advertising injury" covered by the policy. 11 The policy

applies to "Personal and Advertising Injury" caused by oneor both of the following enumerated offCl1ses, among others:

9

Pl.'s Mot. Summ. J., Docket Entry No. 27, p. I.

Continental's policy provides excess umbrella liability

coverage over primary liability insurance issued by Sentry. 9It provides two types of coverage: I) "bodily injury"and "property damage" and 2) "personal and advertising

injury," 10 Here, COX claims coverage for "personal andadvertising" injury.

Pt.'s Mot. Summ. J.. Docket Entry No. 27. p. 1.2

3

4

Intervenor's Mot. Summ, 1, Docket Entry No. 43, p. 2.

Pl.'s Mot. Summ. 1, Docket Entry No. 27, p. I.

11 PL's Mot.Summ. l, Docket Entry No. 10, Ex. 3.Continental's Insurance Policy, p. CICOI27.

~~Advertisement" ... a notice that is broadcast or publishedto the general public 01' specific market segments about

g. The use of another's advertising idea in your~'adveltisement;"

12

h. Infringing upon another's copyright, trade dress or

slogan in your "advertisement;" 12

ld. at CIC013 J.

Additionally, the policy defines "advertisement" as follows:

[d.

[d.

CGX has raised the issue that Continental lacks summaryjudgment proof to detennine its duty la defend andindemnify because Continental, whose policy coveragerelates to Sentry's scheduled underlying insurance, hasnot presented evidence regardi!1g whether the Sentrycoverage is implicated by the Rudamac suit. Because thecourl is detennining Continental's and Senuy's coveragesimultaneously, this point is moot. This court does notneed to reach the issue of whether Sentry's coverage

7

6

5

30

Continental Cas. Co. v. Consolidated Graphics, Inc., 656 F.Supp.2d 650 (2009)

!d. atc;ICOJ29.

your goods, products or services for the purpose of

attracting customers or supporters .... 13

PL', Mot. Sunun. l, Docket No. 27, Ex. ), RudamacComplaint, p. CICOOOl.

Id,

The allegations that gave rise to the Rudamac suit are asfollows. Daniel Chambers ("Chambers"), the nephew of

Rudamac's owner and president, began his employment with

Rudamac nine years ago. 2\ \Vhen Chambers was refused anownership inte1'est in the company, he implemented a plan tomove a substantial. amount of Rudamac1s business to COX

and join the company as an employee. 22 Rudamac alleged in

its compiaint that Chambers "solicited customers" for CGX

during his employment and "in doing so, misappropriatedRudamac's trade secrets, customers and other valuable

proprietary information." 23 Specifically, Rudamac stated

that tbe misappropriated information included:

19

20

B. The Underlying Litigation (the "Rudamae suit")

On May 4, 2007, Rudamac, Inc. ("Rudamac"), a California

based printing company, med a complaint against CGX

in Califomia (hereinafter "the Rudamaccomplaint" or lithe

complaint"). 19 Tbe claims have been litigated in a lawsuit

styled Rudamac, Inc. v. Daniel Chambers, el ai" Cause No.

BC370594, Superior Court of the State of California, County

of Los Angeles ("the underlying case" or "the Rudamac

suit"). 20

Intervenor's Mot. Summ. 1., Docket Entry No, 43, Ex. 3,Sentry Policy p. 1 (unnumbered); Ex. 4, Sentry Policy,p. I (unnumbered).

16

Jd.. Ex:. 3, Sentry's Insurance Policy, pp. 001-007 of022;

Ex. 4. Sentry's Insurance Policy, pp. 001-007 of 022.

Coverage B of the Sentry policy provides that Sentry will

pay those sums that CGX becomes legally obligated to pay as

damages because of "advertising injuty" and has the duty to

defend any suit seeking those damages. 16

15

14

ld., Ex. 3, Sentry's Insurance Policy. pp. 006-007 of022;

Ex. 4. Sentry's Insurance Policy, pp. 00&.,007 of 022.

*654 Tbe Sentry policy's duty to defend/indemnify

speeifically applies to:

13

2, Sentry's Poliey

Sentry is a liability insurer that issued two primary CGL

policies to CGX effective frotn April 1, 2007, to April

1, 2008, (collectively, the "Sentry policy"). 14 11,e Sentry

poliey provides eoverage in two parts: 1) Coverage A for

"bodily injuty" or "property damage" and 2) Coverage B for

"adverti!:;ing injury." 15 Coverage A is not at issue here.

(2) "Advertising injury" caused by an

offense committed in the course ofadvertising your goods, .products, or

services; I?

21

22

23

Pl.'s Mol. Summ. J., Docket No. 27, p. 6.

Pl.'s Mot. Summ. J., Docket No, 27, Ex. 1. Rudamac

Complaint, p. CIC0002., to-17.

ld. at CIC0006,' to-l4.

17 ld.. Ex. 3, Sentry1s Insurance Policy, p. 007 of 022; Ex.4, Sentry's Insurance Policy, p. 007 of 022.

The Sentry policy sets out a list of enumerated offenses that

constitute advertising injuries. Relevant to this case is anadvertising injury arising out of ...

price information, including private data regardingthe competitive pricing of the products, protit margin,particularized pricing information such as mark \lPS,discounts, or other promotions given; terms of sale ...; and

cost information." 24

18

Rudamac alleged that this infonnation allowed CGX, among

other things, to HsoBcit customers and suppliers for neworders" and that its trade secrets were valuable to acompetitorbecause they could H use this information to ... leam how

to contact suppliers and customers:,25 All of Rudamac'strade secrets. the complaint alleged, were kept on a secured

c. Misappropriation of advertising

ideas or style of doing business; 18

Id., Ex. 3, Sentry's Insurance Policy, p. 016 of 022; Ex.4. Sentry's Insurance Policy. p. 016 of 022.

The Seiltry policy does not define the tern> "advertising."

24 ld. at CIC00007.' 15-21.

31

Continental Cas. Co. v. Consolidated Graphics, Inc., 656 F.Supp.2d 650 (2009)_._'~_~'__""_'~""~__,,_~,,~~~_<__",,,w~~._~__.__._~_"•.-__.w.,_·,_·."~. ,,_~~_~__,_,"."__.~,_ ", _, _"~"~"_·.W'~'"_'.W~'''_" '_''''' '_""" __'_""_',,,W ,",.'"_

and password-protected computer network, and, throughout

Chambers' employment, COX was aware of and understood

the confidential and proprietary nature of the infoonation. 26

III. Applicable Law

Brown v. City .of Houslon. Tex., 337 F.3d 539, 540-41

(5th Cir.2003). The movant must infoon the court of the

basis for the summary judgment motion and must point to

relevat'lt excerpts from pleadings. depositions. answers to

interrogatories, admissions, Of affidavits that demonstrate theabsence of genuine factual issues. Celolex Corp., 477 U.S.

at 323, 106 S.Ct. 2548; Topalian v. Ehrman. 954 F.2d 1125,

1131 (5tll Cil'.1992). If the moving plll1y meets its burdeu,

the nonmoving party must then go beyond the pleadings

and produce competent evidence that establishes each of the

challenged elements of the case, and which demonstratesthat genuine issues of material fact do exist which must beresolved at trial. Celotex, 477 U.S. at 324, 106 S.Ct. 2548.

A material fact is a fact that is identified by applicablesubstantive law ~s critical to the outcome ofthe suit. Anderson

v. Uberty Lobby, Inc.. 477 U.S. 242, 248, J06 S.C!. 2505,

91 L.Ed.2d 202 (1986). To he genuine, the dispute regarding

a material ract must be supported by evidence such that a

reasonable jury could resolve the issue in favor ofeither party.Id. at 250, 106 S.Ct. 2505. When considering the evidence,

"[d]oubts are to be resolved in favor of the nonmoving party,

and any reasonable inferences are to be drawn in favor ofthat party." Evans v. City (ifHouston, 246 F.3d 344, 348 (5th

Clf.2001).

Id. at C1C00009, ~ 3-4.

Id. at C1COOOI.

26

27

28

25

/d. atCJCOOOI2,~ 1-4.

Rudamac pled the following counts against COX: I)l'l'lisappropriation oftrade secrets; 2) unfair business practices;3) intentional interference with prospective economicadvantage; 4) breach of fiduciary duty; 5) constructive tmst;

6) unjust enrichment; 7) a demand for accounting; and 8)

intentional interference with at will employment relations. 28

Trial was held in this matter on December 9, 2008, and verdict

was entered on February 2, 2009. 29 The judgment found,

based on the jury's verdict, that CGX committed three torts:

interference with economic relations, breach of fiduciary

duty. and misappropriation of trade secrets. 30

Id. at C1C00007, ~ 28.

Based upon the facts of the case, Rudamac alleged that COX

"utilized [Rudamac's] *655 successful business history and

pricing strategy to solicit and misappropriate customers and

trade secrets." 27

As this declaratory action is in federal court under diversityjurisdiction. state law governs substantive matters. Erie R.R.v. Tompkins. 304 U.S. 64, 78, 58 S.Ct. 817, 82 L.Ed. 1188

(1938). Because Texas is the forum state in this matter, the

court applies Texas' choice of law rules. Gual'. NatlfIns. Co.v. Azrock Indus., 21 J F.3d 239, 243 (5th Cir.2000) (citing

Klaxon Co. v. Stelltof' Elee. Mfg. Co.. 313 U.S. 487, 496, 61

S.Ct. 1020,85 L.Ed. 1477 (1941) *656 and stating that a

federal district court sitting in diversity must apply the forum

state's conflict of laws rules).

PI,'sSecQnd SuppJ~m~nt to Mot. Summ. J., Docket EntryNo. 37, p. I.

30

29

ld., Ex. 1, Judgment, Rudamac suit.

As a result, Rudamac was awarded $5,698,000 in damages

and, due to ti,e findings of willful, malicious, oppressive,

and fraudulent conduct, the jury awarded punitive damages

against Thousand Oaks Printing for $1,500,000 and against

CGX for $6,647, 000. 31

Summmy judgment is warranted when the evidence revealsthat no genuine dispute exists regarding any material factand the moving party is entitled to judgment as a matter

of law. Fed.R.Civ.P. 56(e); CelOlex Corp. v. Calrell, 477U.S. 317, 322, 106 S.C!. 2548, 91 L.Ed.2d 265 (1986);

31 Id. at p. 8.

II. Snmmary Judgment Standard

Any insurance policy payable to a "citizen or inhabitant" ofTexas by an insurance company doing business in Texas isheld to be governed by Texas law regardless of where the

contract was executed or where the premiums arc paid. Tex.Ins.Code art. 21.42. Continental does business in Texas, andthe named Insured 011 the policy, CGX, is a Texas corporation.

Thus, Texas substantive law applies. The parties agree that

Texas law applies to the interpretation ofthe policies. 32

"_~'._.__"W""'''"''~~ .~_' ~'_'M.•._"~._,~_.~_"_~M_.~" ~." ~"...~._ ".".~_._~_~_.~_ ~_~_~"_~.~'_.'_'."._. __

\\I:estld\vNexr [L:!- 11";oi\,:;(;'(; F;8ut~~fS ;~G C:D!(i'

32

Continenlal Cas. Co. v. Consolidated Graphics, Inc., 656 F.Supp.2d 650 (200~)

A. Burden of Proof and Contract Interpretation

In gelleral. the insured bears the initial burden of e,tabli,hing

that there is coverage under an applicable insurance policy,while it is the insurer's burden to prove the applicability ofan

exclusion pennitting it to deny coverage. Lincoln Gen. Ins.Co. v. Reyna, 401 F.3d 347, 350 (5th Cir.2005) (applying

Texas law and pladng burden on insurer to demonstratethat the only reasonable interpretation supports exclusion);

Venture EllcodillgServ., Illc. v. At!. Mut. Ills. Co.. 107 S.W.3d

729, 733 (Tex.App.-Fort Worth 2003, pet, denied) (stating

that the Texas Insurance Codc places the burden on the insurer

to prove any exception to coverage); see also Tex. Ins.CodeAnn. § 554.002 (placing the burden on the insurer to prove

the applicability of a coverage exclusion). If the insurer issuccessful, the burden shifts back to the insured to prove thatan exception to the exclusion applies. Guar. Nat 'I Ins. Co.v. Vic Mfg. Co., 143 F.3d 192, 193 (5th eir. 1998) (applying

Texas law).

(11 Under Texas law, insurance policies are subject to the

rules of contract interpretation. AZl'oek Indus., 211 F.3d at

243; Progressive COUllty Mut. IllS. Co. l'. Sink, 107 S.W.3d

547, 551 (Tex.2003). In construing the terms of a contract,

the court's primary purpose is always to ascertain the trueintent of the parties as expressed in the written instrument.Mid-Century Tlls. Co. of Tex. v. Lindsey, 997 S.W.2d 153,

158 (Tex.1999); Nat'l Union Fire Ins. Co. of Pittsburgh,Pa. v. CHI Indus.. 907 S.W.2d 517, 520 (Tex.1995). To this

end, the court reads all provisions within the contract as awhole and gives effect to each tenn so that no part of the

agreement is left without meaning. MCI Telecomms. Cmp.

v. Te"" Utils. Elee. Co" 995 S.W.2d 647, 652 (Tex.1999);

see also Provident Life & Accident Ins. Co. v. Knott. 128S.W.3d 21 I, 216 (Tcx.2003) (warning the court to "exercise

caution not to isolate particular sections or provisions fromthe contract as a whole"). Tenns in contracts are given theirplain, Ol;dinary, and generally accepted meaning unless thecontract itself shows that particular definitions· are used toreplace that meaning. Bituminous Cas. Corp, v. Maxey, 110S.W.3d 203,208-09 (Tcx.App.-Houston [1st Dist,) 2003, pet.

denied) (citing W Reserve Life Ins. v. Meadows, 152 Tex.559,261 S,W.2d 554, 557 (1953)).

32 PI.', Mot. Summ. J., Docket Entl)' No. 27, p. 3;Intervenor's Mot. Summ. J.,·Oocket Entry No; 43. p. 8;See Def.'s Response, Docket Entry No. 28, (citing Texaslaw).

(21 131 When a contract, as written, can be given "a

definite or certain legal meaning," then it is unambi&,'Uousas a matter of law and the court enforces it as written.CBI IlIdu"., 907 S.W.2d at 520. If, however, a contract

provision. particularly an exclusionary clause, is susceptibleto morc than one reasonable interpretation, the court mustresolve the ambiguity in favor of the insurcd. Sillk, 107S.W.3d at 551; see also Mid-Continent Cas. Co. v. Swift

'657 Energy Co., 206 F.3d 487, 491 (5th Cir.2000)

(HIn Texas, when an insurance policy is ambiguous orinconsistent, the. const11lction that would afford coverageto the insured must govern."). In fact, if the insured'sconstruction of an exclusionctry provision is reasonable,it must be adopted, even if the insurer's constnlc\ion ismore reasonable, BolandrolJ v. Sq(eeo IllS. Co. ofAlii., 972S.W.2d 738, 741 (Tex. 1998). The court will not find a

contract ambiguous, however, merely because the partiesadvance conflicting interpretations. Kelley-Coppedge, lnc. v.Highlallds Tlls. Co., 980 S.W.2d 462, 465 (Tex, 1998).

B. Duty to Defend

In Texas, an insurer1s duty to defend and duty to indemnifyare two distinct and separate duties. Trinity Universal/ns. Co.

v. Cowall. 945 S.W,2d 819, 821-22 (Tex. 1997). Under the

Ueight·comers" or ucomplaint allegation" rule, an insurer'sduty to defend its insured arises if the complaint in thesuit against the insured alleges facts that potentially support

claims for which there is coverage. Nat'[ Union Fire Ins. Co.q( Pittsburgh, Pa, v, Merchs. Fost Motor Lilies, Ille" 939S.W.2d 139, 141 (Tex. 1997). In detennining whether this

duty exists, the court1s only job is to compare the four cornersof the pleading with the four corners ofthe insurance policy.

Reyna, 401 F.3d at 350; see alsa Merehs. Fast Mator Lines,Tile., 939 S.W.2d at 141.

(41 [51 [61 (7] When applying Ihe eight-corners rule, the

court considcl'S the factual al1egatJons in light ofthe insurancepolicy without regard to their tl11th or falsity. See ArgonautSw. Tlls. Ca. v. Maupill, 500 S.W.2d 633.635 (Tex.1973).

The eourt interprets the allegations liberally and resolves all

doubts regarding the duty to defend in favor of the insured.Merchs. Fast Motor Lines, Ille.. 939 S,W.2d at 141, Aninsurer is required to defend its insured against suit as longas the allegations potentially give rise to at least one claimcovered by the insurance policy. Utica Nat'l IllS. Co. ofTe",.v. Am. Illdem. Co.. 141 S.W.3d 198,201 (Tex.2004) ("A

liability insurer is obligated to defend a suit ifthe facts alleged

in the pleadings would give rise to any claim within thecoverage of the policy."); see also Lafarge CO/po v. HaNford

33

Conllnenlal Ca•. Co. v. Consolldalad Graphics, Inc., 656 F.Supp,2d 650 (2009)

COX asserts that the Rudaraac suit alleges a cognizableadvertising injury beeause it contains allegations that fitone of the enumerated offenses in each policy: "g. the useof' ano'ther's advertising idea in your 'adv~rtisen'lcnt' .. (theContinental policy); and "c. Misappropriation of advertising

ideas or style of doing business" (the Sentry policy). 35