Embed Size (px)

Citation preview

1

CHAPTER 1

INTRODUCTION

CHAPTER 1

2

INTRODUCTION

1.1. INTRODUCTION TO THE STUDY

A sale of credit is an evitable necessity in the business world of today. No

business can exist without selling the units in credit. The basic difference between

the credit sales and cash sales is the time gap in the receipt of cash.

Management of trade credit is commonly known as Management of

Receivables. Receivables are one of the three primary components of working

capital, the other being inventory and cash, the other being inventory and cash.

Receivables occupy second important place after inventories and thereby constitute

a substantial portion of current assets in several firms. The capital invested in

receivables is almost of the same amount as that invested in cash and inventories.

Receivables thus, form about one third of current assets in India. Trade credit is an

important market tool. As, it acts like a bridge for mobilization of goods from

production to distribution stages in the field of marketing. Receivables provide

protection to sales from competitions. It acts no less than a magnet in attracting

potential customers to buy the product at terms and conditions favorable to them

as well as to the firm. Receivables management demands due consideration not

financial executive not only because cost and risk are associated with this

investment but also for the reason that each rupee can contribute to firm's net

worth.

The book debts or receivable arising out of credit has three dimensions:-

It involves an element of risk, which should be carefully assessed. Unlike

cash sales credit sales are not risk less as the cash payment remains

undeceived.

It is based on economics value. The economic value in goods and

services passes to the buyer immediately when the sale is made in return for

an equivalent economic value expected by the seller from him to be

received later on.

3

It implies futurity, as the payment for the goods and services received by the

buyer is made by him to the firm on a future date.

The customer who represent the firm's claim or assets, from whom

receivables or book-debts are to be collected in the near future, are known as

debtors or trade debtors. A receivable originally comes into existence at the very

instance when the sale is affected.

Receivables may be represented by acceptance; bills or notes and the

like due from others at an assignable date in the due course of the business. As sale

of goods is a contract, receivables too get affected in accordance with the law of

contract e.g. Both the parties (buyer and seller) must have the capacity to contract,

proper consideration and mutual assent must be present to pass the title of goods

and above all contract of sale to be enforceable must be in writing. Receivables,

as are forms of investment in any enterprise manufacturing and selling goods on

credit basis, large sums of funds are tied up in trade debtors. Hence, a great deal of

careful analysis and proper management is exercised for effective and efficient

management of Receivables to ensure a positive contribution towards increase in

turnover and profits.

When goods and services are sold under an agreement permitting the

customer to pay for them at a later date, the amount due from the customer

is recorded as accounts receivables; so, receivables are assets accounts

representing amounts owed to the firm as a result of the credit sale of goods and

services in the ordinary course of business. The value of these claims is carried on

to the assets side of the balance sheet under titles such as accounts receivable, trade

receivables or customer receivables. This term can be defined as "debt owed to the

firm by customers arising from sale of goods or services in ordinary course

of business."

Instruments indicating receivables

Harry Gross has suggested three general instruments in a concern that

4

provide proof of receivables relationship. They are briefly discussed below: -

Open book account

This is an entry in the ledger of a creditor, which indicates a credit

transaction. It is no evidence of the existences of a debt under the Sales of Goods.

Negotiable Promissory Note

It is an unconditional written promise signed by the maker to pay a

definite sum of money to the bearer, or to order at a fixed or determinable time.

Promissory notes are used while granting an extension of time for collection of

receivables, and debtors are unlikely to dishonor its terms.

Increase in Profit

As receivables will increase the sales, the sales expansion would

favorably raise the marginal contribution proportionately more than the additional

costs associated with such an increase. This in turn would ultimately enhance the

level of profit of the concern.

Meeting Competition

A concern offering sale of goods on credit basis always falls in the top

priority list of people willing to buy those goods. Therefore, a firm may resort

granting of credit facility to its customers in order to protect sales from losing it

to competitors. Receivables acts as an attracting potential customers and retaining

the older ones at the same time by weaning them away firm the competitors.

Augment Customer's Resources

Receivables are valuable to the customers on the ground that it

augments their resources. It is favored particularly by those customers, who

find it expensive and cumbersome to borrow from other resources. Thus, not

only the present customers but also the Potential creditors are attracted to buy

the firm's product at terms and conditions favorable to them.

5

Speedy Distribution

Receivables play a very important role in accelerating the velocity of

distributions. As a middleman would act quickly enough in mobilizing his

quota of goods from the productions place for distribution without any hassle of

immediate cash payment. As, he can pay the full amount after affecting his sales.

Similarly, the customers would hurry for purchasing their needful even if they are

not in a position to pay cash instantly. It is for these receivables are regarded as

a bridge for the movement of goods form production to distributions among

the ultimate consumer.

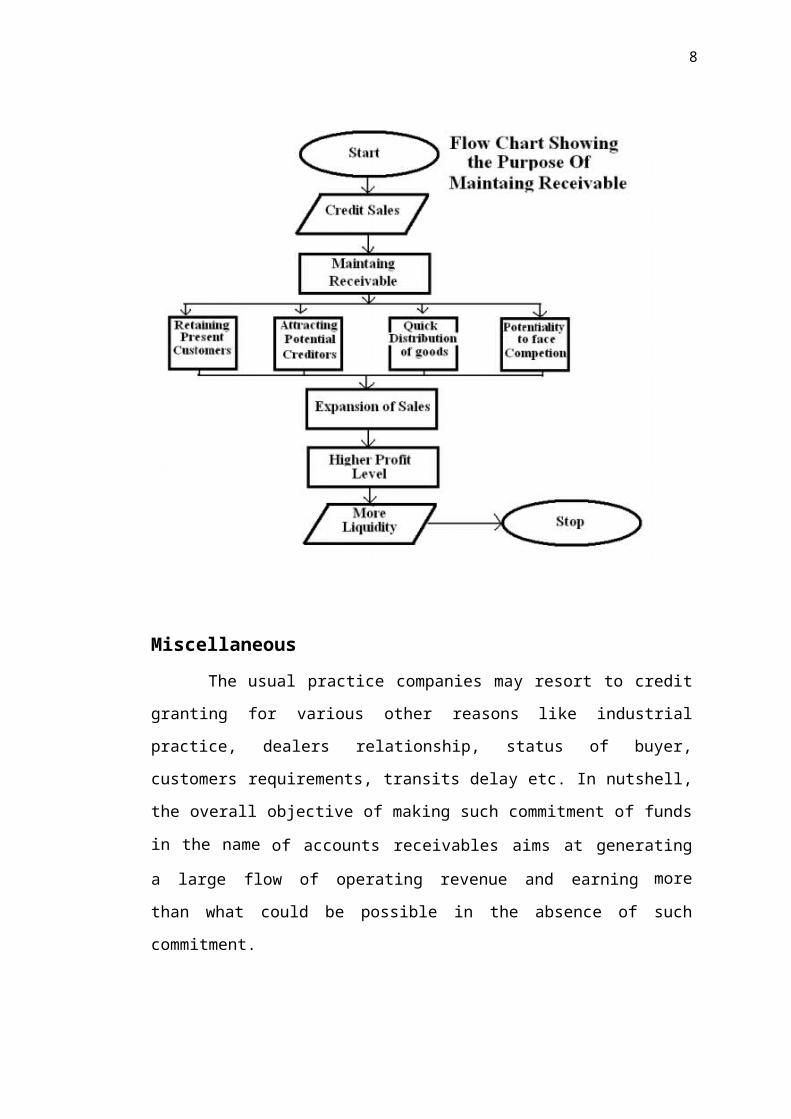

MiscellaneousThe usual practice companies may resort to credit granting for various

other reasons like industrial practice, dealers relationship, status of buyer,

6

customers requirements, transits delay etc. In nutshell, the overall objective of

making such commitment of funds in the name of accounts receivables aims at

generating a large flow of operating revenue and earning more than what could

be possible in the absence of such commitment.

Cost of Maintaining ReceivablesReceivables are a type of investment made by a firm. Like other

investments, receivables too feature a drawback, which are required to be

maintained for long that it known as credit sanction. Credit sanction means tie up

of funds with no purpose to solve yet costing certain amount to the firm. Such

costs associated with maintaining receivables are detailed below: -

Administrative CostIf a firm liberalizes its credit policy for the good reasons of either

maximizing sales or minimizing erosion of sales, it incurs two types of costs:

(A) Credit Investigation and Supervision Cost:

As a result of lenient credit policy, there happens to be a substantial

increase in the number of debtors. As a result the firm is required to analysis and

supervises a large volume of accounts at the cost of expenses related with

acquiring credit information either through outside specialist agencies or form its

own staff.

(B) Collection Cost:

A firm will have to intensify its collection efforts so as to collect the

outstanding bills especially in case of customers who are financially less sound. It

includes additional expenses of credit department incurred on the creation and

maintenance of staff, accounting records, stationary, postage and other related

items.

Capital Cost

7

There is no denying that maintenance of receivables by a firm leads to

blockage of its financial resources due to the tie log that exists between the date of

sale of goods to the customer and the date of payment made by the customer. But

the bitter fact remains that the firm has to make several payments to the

employees, suppliers of raw materials and the like even during the period of time

lag. Thus, a firm in the course of expanding sales through receivables makes way

for additional capital costs.

Production and Selling CostThese costs are directly proportionate to the increase in sales volume. In

other words, production and selling cost increase with the very expansion in the

quantum of sales. In this respect, a firm confronts two situations; firstly when the

sales expansion takes place within the range of existing production capacity, in

that case only variable costs relating to the production and sale would increase.

Secondly, when the production capacity is added due to expansion of sales in

excess of existing production capacity. In such a case incremental production and

selling costs would increase both variable and fixed costs.

Delinquency Cost

This type of cost arises on account of delay in payment on customer's

part or the failure of the customers to make payments of the receivables as and

when they fall due after the expiry of the credit period. Such debts are treated as

doubtful debts. They involve: -

(i) Blocking of firm's funds for an extended period of time,

(ii) Costs associated with the collection of overheads, remainders legal expenses

and on initiating other collection efforts.

Default CostDelinquency cost arises as a result of customers delay in payments of

cash or his inability to make the full payment from the firm of the receivables due

to him. Default cost emerges a result of complete failure of a defaulter (customer)

8

to pay anything to the firm in return of the goods purchased by him on credit.

When despite of all the efforts, the firm fails to realize the amount due to its debtors

because of him complete inability to pay for the same. The firm treats such debts as

bad debts, which are to be written off, as cannot be recovers in any case.

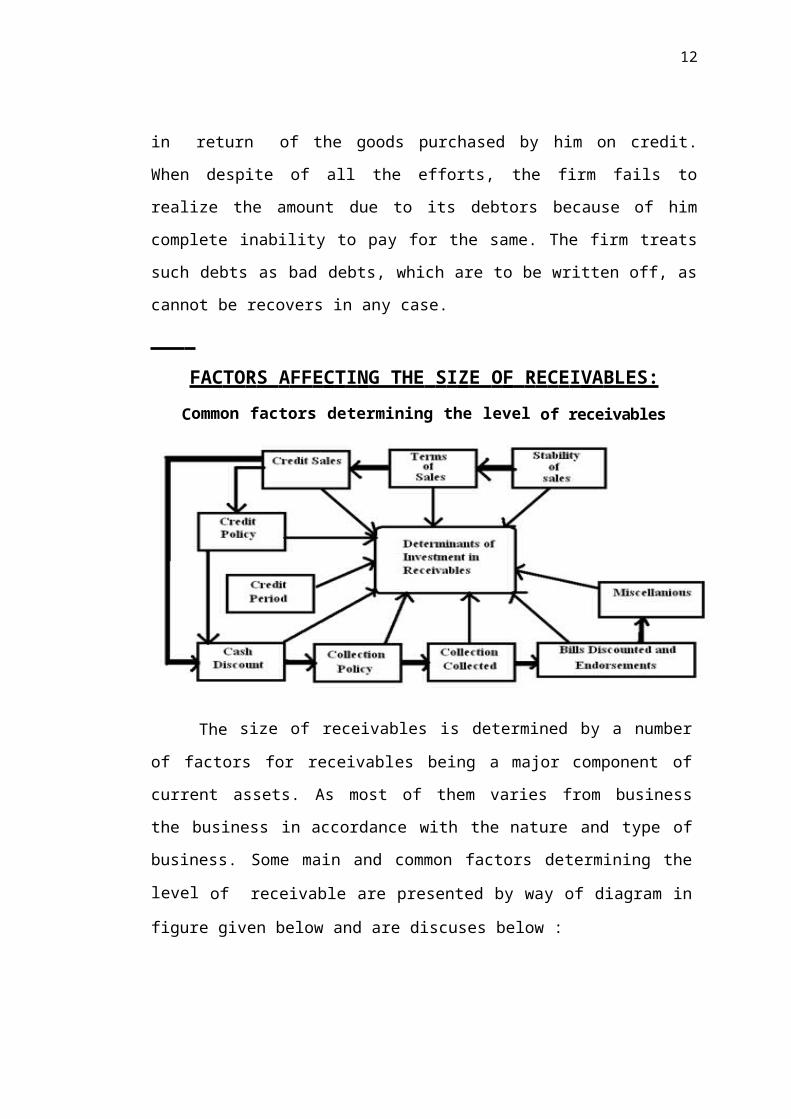

FAC TO R S A FF E C T I N G THE S I Z E O F R E C E I VA BLES: Common factors determining the level of receivables

The size of receivables is determined by a number of factors for

receivables being a major component of current assets. As most of them varies

from business the business in accordance with the nature and type of business.

Some main and common factors determining the level of receivable are presented

by way of diagram in figure given below and are discuses below :

Stability of Sales

Stability of sales refers to the elements of continuity and consistency in

the sales. In other words the seasonal nature of sales violates the continuity of

sales in between the year. So, the sale of such a business in a particular season

would be large needing a large a size of receivables. Similarly, if a firm supplies

goods on installment basis it will require a large investment in receivables.

9

Terms of Sale

A firm may affect its sales either on cash basis or on credit basis. As a

matter of fact credit is the soul of a business. It also leads to higher profit level

through expansion of sales. The higher the volume of sales made on credit, the

higher will be the volume of receivables and vice-versa.

The Volume of Credit SalesIt plays the most important role in determination of the level of

receivables. As the terms of trade remains more or less similar to most of the

industries. So, a firm dealing with a high level of sales will have large volume of

receivables.

Credit PolicyA firm practicing lenient or relatively liberal credit policy its size of

receivables will be comparatively large than the firm with more rigid or signet

credit policy. It is because of two prominent reasons: -

A lenient credit policy leads to greater defaults in payments by financially

weak customers resulting in bigger volume of receivables.

A lenient credit policy encourages the financially sound customers to delay

payments again resulting in the increase in the size of receivables.

Terms of saleThe period for which credit is granted to a customer duly brings about

increase or decrease in receivables. The shorter the credit period, the lesser is the

amount of receivables. As short term credit ties the funds for a short period only.

Therefore, a company does not require holding unnecessary investment by way of

receivables.

Cash Cash discount on one hand attracts the customers for payments before the

lapse of credit period. As a tempting offer of lesser payments is proposed to the

customer in this system, if a customer succeeds in paying within the stipulated

10

period. On the other hand reduces the working capital requirements of the

concern. Thus, decreasing the receivables management.

Collection policyThe policy, practice and procedure adopted by a business enterprise in

granting credit, deciding as to the amount of credit and the procedure selected for

the collection of the same also greatly influence the level of receivables of a

concern. The more lenient or liberal to credit and collection policies the more

receivables are required for the purpose of investment.

Collection collectedIf an enterprise is efficient enough in encasing the payment attached to the

receivables within the stipulated period granted to the customer. Then, it will opt for

keeping the level of receivables low. Whereas, enterprise experiencing undue delay

in collection of payments will always have to maintain large receivables.

Bills discounting and endorsementIf the firm opts for discounting its bills, with the bank or endorsing the

bills to the third party, for meeting its obligations. In such circumstances, it would

lower the level of receivables required in conducting business.

Quality of customerIf a company deals specifically with financially sound and credit worthy

customers then it would definitely receive all the payments in due time. As a

result the firm can comfortably do with a lesser amount of receivables than in case

where a company deals with customers having financially weaker position.

MiscellaneousThere are certain general factors such as price level variations,

attitude of management type and nature of business, availability of funds

and the lies that play considerably important role in determining the quantum of

11

receivables.

PRI NCI PLES OF CREDI T MANAGEMENT:

In order to add profitability, soundness and effectiveness to receivables

management, an enterprise must make it a point to follow certain well-established

and duly recognized principles of credit management.

The first of these principles relate to the allocation of authority

pertaining to credit and collections of some specific management.

The second principle puts stress on the selection of proper credit terms.

The third principles emphasizes a through credit investigation before a

decision on granting a credit is taken. And the last principle touches upon the

establishment of sound collection policies and procedures.

In the light of this quotation, the principles of receivables management can

be stated as:

1. Allocation or Authority

2. Selection of Proper Credit Terms

3. Credit Investigation

4. Sound Collection Policies and Procedures

OBJECTIVES OF CREDIT MANAGEMENT:

To attain not maximum possible but optimum volume of sales

To exercise control over the cost of credit and maintain it on a minimum

possible level.

To keep investment at an optimum level in form of the receivables

To plan and maintain a short average collection period.

The period goal of receivables management is to strike a golden mean

among risk, liquidity and profitability turns out to be effective marketing tool. As

12

it helps in capturing sales volume by winning new customers besides retaining to

old ones.

CREDIT POLICY:Credit policy of every company is at large influenced by two conflicting

objectives irrespective of the native and type of company. They are liquidity and

profitability. Liquidity can be directly linked to book debts. Liquidity position of

a firm can be easily improved without affecting profitability by reducing the

duration of the period for which the credit is granted and further by collecting the

realized value of receivables as soon as they fails due. To improve profitability

one can resort to lenient credit policy as a booster of sales, but the implications

are: -

1. Changes of extending credit to those with week credit rating.

2. Unduly long credit terms.

3. Tendency to expand credit to suit customer's needs; and

4. Lack of attention to over dues accounts.

The three important decisions variables of credit policy are:

1. Credit terms,

2. Credit standards, and

3. Collection policy.

1. Credit Terms

Credit terms refer to the stipulations recognized by the firms for making

credit sale of the goods to its buyers. In other words, credit terms literally mean

the terms of payments of the receivables

There are two important components of credit terms which are detailed below:-

(A) Credit period and

(B) Cash discount terms

13

A) Credit period

"Credit period is the duration of time for which trade credit is extended.

During this time the overdue amount must be paid by the customers."

While determining a credit period a company is bound to take into

consideration various factors like buyer's rate of stock turnover, competitors

approach, the nature of commodity, margin of profit and availability of funds etc.

The general way of expressing credit period of a firm is to coin it in

terms of net date that is, if a firm's credit terms are "Net 30", it means that the

customer is expected to repay his credit obligation within 30 days.

A firm may tighten its credit period if it confronts fault cases too

often and fears occurrence of bad debt losses. On the other side, it may

lengthen the credit period for enhancing operating profit through sales expansion.

Anyhow, the net operating profit would increase only if the cost of extending

credit period will be less than the incremental operating profit. But the increase

in sales alone with extended credit period would increase the investment in

receivables too because of the following two reasons: -

(i) Incremental sales result into incremental receivables,

(ii) The average collection period will get extended, as the customers will

be granted more time to repay credit obligation.

(B) Cash Discount Terms

The cash discount is granted by the firm to its debtors, in order to

induce them to make the payment earlier than the expiry of credit period allowed

to them. Granting discount means reduction in prices entitled to the debtors so as

to encourage them for early payment before the time stipulated to the i.e. the

credit period.

Cash discount is expressed is a percentage of sales. A cash discount term

is accompanied by (a) the rate of cash discount, (b) the cash discount period, and

(c) the net credit period. For instance, a credit term may be given as "1/10 Net 30"

that mean a debtor is granted 1 percent discount if settles his accounts with the

creditor before the tenth day starting from a day after the date of invoice. But in

14

case the debtor does not opt for discount he is bound to terminate his obligation

within the credit period of thirty days.

To make cash discount an effective tool of credit control, a business

enterprise should also see that is allowed to only those customers who make

payments at due date. And finally, the credit terms of an enterprise on the receipt

of securities while granting credit to its customers. Credit sales may be got secured

by being furnished with instruments such as trade acceptance, promissory notes or

bank guarantees

2. Credit Standards

Credit standards refers to the minimum criteria adopted by a firm for the

purpose of short listing its customers for extension of credit during a period of

time. Credit rating, credit reference, average payments periods a quantitative basis

for establishing and enforcing credit standards. Optimum credit standards can be

determined and maintained by inducing tradeoff between incremental returns and

incremental costs.

Analysis of Customers

The quality of firm's customers largely depends upon credit standards. The

quality of customers can be discussed under too main aspects; average collection

period and default rate.

(i) Average Collection Period

(ii) Default Rate

I.M. Pandey has cited three Cs of credit termed as character,

capacity and condition that estimate the likelihood of default and its effect

on the firms' management credit standards. Two more Cs has been added to the

three Cs of I.M. Pandey, namely; capital and collateral.

1.2. PROBLEM STATEMENT:

15

The main problem of the study is that the company faces the difficulties of

receiving payments from their customers. To determine the reason for the delay in

receiving payments from the debtors. To check whether their customers are paying

the amount correctly from the actual date of receipt within the payment due date. To

find out the number of days delay in receiving payment. Ratio is determined to

indicate payment period, collection period, return on owner equity. It throws light on

financial strength of the company and whether the trend over the years is favorable

or not. In this study, ratios are used for credit analysis. From the given secondary

data, trend analysis of sales and debtors for 3 years is to be determined for knowing

the impact of receivable in financial liquidity.

1.3. NEED & SCOPE OF THE STUDY

Measurement is another component within account receivable management.

Traditional ratios, such as turnover will measure how many times you were able to

convert receivables over into cash.

Measurements may need to be modified to account for wide fluctuations

within the sales cycle. The use of weights can help ensure comparable

measurements.

The following are the scope:

1. Fostering credit awareness

2. Understanding the need for a credit policy

3. Understanding financial statements

4. Applying financial analysis of financial statements

5. Allowing too much credit, or not managing the credit policy

carefully enough, could result in irrecoverable debts. This

represents a loss of income to the company, affecting both

profitability and cash flow. So credit management has to be done.

6. To reduce administrative cost and enhance office productivity

7. To manage your sales process more effectively by measuring

trends and analyzing performance.

16

8. How the managed calculations to fit your business needs

1.4. OBJECTIVE OF THE STUDY

Primary objective:

The objective of the receivables management is to promote sales and profits.

Also it focuses on how to augment money to meet the company’s working capital

requirements.

Secondary Objective:

i) To examine the receivables management practices followed by the

company

ii) To determine the relationship of receivables and sales

iii) To Compare Actual Date of Receipt from customers with the Payment

Due Date.

iv) To find out the reasons for the delay in getting the Payment

v) To find out the impact in the working capital of the company

vi) To offer suggestion to improve the receivables position.

1.5. RESEARCH METHODOLGY

The data that has been collected from various sources and presented in the

form of materialistic information is known as research methodology. Research

methodology is a systematic way to solve any research problem. It may be

understood as a science of studying how research is done scientifically.

1.5.1. RESEARCH DESIGN

This research study adopts an Empirical research methodology. Such

research is often conducted to answer a specific question or to test a hypothesis. Any

conclusions drawn are based upon hard evidence gathered from information

17

collected from real life experiences or observations. This helps to understand and

respond to dynamics of situations. This research is widely used in stock market

research, analysis of financial statement, and other socio-science related researches.

1.5.2. DATA COLLECTION METHOD

Data collection methods are an integral part of research design. Problems

researched with the use of appropriate methods greatly enhance the value of the

research

In this study, the data are collected from the secondary sources. Secondary

data are indispensable for most organizational research. Such data can be internal or

external to the organization and accessed through the internet or perusal of recorded

or published information.

Secondary data can be used, among other things, for forecasting sales by

considering models based on past sales figures, and through extrapolation.

There are several sources of secondary data, including books and periodicals,

government publications of economic indicators, census data, statistical abstracts,

databases, the media, annual reports of companies, etc. Also included in secondary

sources are schedules maintained for or by key personnel in organizations, the desk

calendar of executives, and speeches delivered by them. Much of such internal data,

though, could be proprietary and not accessible to all.

The advantage of seeking secondary data sources is savings in time and costs

of acquiring information. Hence it is important to refer to sources that offer current

and up-to-date information.

For this research, the data is collected from the annual reports of the

company from the year 2008-09 to 2012-13. The annual report can be considered

as the most important and reliable source of financial data.

1.5.3. TOOLS USED

18

The following are the financial tools used for analysis and interpretation of

this study which is based on receivables management.

Ratio analysis tools used here are

1. Liquidity

a) Current ratio

b) Quick ratio

c) Net working capital to sales ratio

2. Profitability

d) Gross profit margin

e) Net profit margin

3. Activity

f) inventory turnover ratio

g) accounts receivable turnover ratio

h) average collection period

Trend Analysis of Debtors ( in months i.e. from Mar 2012- Apr 2013)

Trend of sales (from Mar 2012- Apr 2013)

1.6. CHAPTERISATION

The project consists of five chapters as described below:

Chapter 1: Chapter 1 deals with introduction to the study, problem

statement, need and scope of the study, Objectives of the study, Research

methodology and Limitations of the study.

Chapter 2: Chapter 2 deals with review of literature.

Chapter 3: Chapter 3 includes the industry profile and the company profile.

19

Chapter 4: Chapter 4 includes the data analysis and interpretation of the

study.

Chapter 5: Chapter 5 deals with the summary of findings, suggestions and

conclusion of the study.

1.7. LIMITATIONS OF THE STUDY

1. The study is based on the accounting information. Therefore it is

subject to change based on the market to demand conditions.

2. The study is basically based on the secondary information that is

annual reports of the company. Hence it is difficult to state that the

study is flawless when most of the study is based on the secondary

data.

3. The figures used in reports are taken from annual reports are taken

from the annual reports and has it does not have any impact on the

current transactions.

4. The whole study is based on observations in the past, which can only

be related to laws that operated in the past, as there is no evidence that

the laws will continue to operate in future also

20

CHAPTER 2

LITERATURE REVIEW

21

CHAPTER 2

LITERATURE REVIEW

Mamo, David, (1994), Receivables financing as a source of working capital,

Nursing Homes, 8, vol.43, 28

Financing through a securitization of receivables does not create a liability.

An asset—the receivables --is sold for cash; no loan has been granted.

Banks and finance companies are the most obvious source of receivables

financing. Their lending decision is generally driven by an analysis of a borrower's

financial statements. Consequently it is common for a company's line of credit to be

limited by how its debt compares to its equity base (the ratio of debt-to-worth) or for

the lender to set minimum levels of solvency for the company (the current ratio or

acid-test ratio).

Under these covenants, a lender limits his willingness to lend funds beyond a

predetermined point at which the company would be deemed either excessively

indebted or too short of cash for the payments it must meet. The receivables function

as part of the total collateral that the company pledges in order to strengthen its

corporate commitment to eventually repay the loan. In support of this, the company

usually must periodically produce a report (the borrowing base report) showing how

much in receivables it carries on its balance sheet.

Strischek, Dev, (2001), Looking for a vital sign in contractor accounts: The

receivables ratio, The RMA Journal, 10,vol. 83, 62-66

A contractor's receivables represent two significant elements of contractor

cash flow and working capital. Receivables constitute the major source of cash

inflow, and payables absorb a big share of cash outflow. A construction company's

ability to extend credit to its customers depends on its own trade creditors'

22

willingness to wait for their payments from the contractor's collection of its progress

billing receivables. The delicate balance of receivables and payables is key to the

financial success of the contractor. Contract receivables take longer to collect, and

the trade creditors expect prompt payment. The receivables ratio is a quick-and-easy

test of contractor viability.

Colabella, Patrick; Fitzsimons, Adrian P; Shoaf, Victoria,(2009), FASB Proposes

Disclosures About the Credit Quality of Financing Receivables and the

Allowance for Credit Losses, Commercial Lending Review, 5,vol. 24, 35-40

Specifically, the proposed FAS would require a creditor to disclose

information that would allow credit analysts and other financial statement users to

understand the following:

* The nature of credit risk inherent in the creditor's portfolio of financing receivables

* How that risk is analyzed and assessed in arriving at the allowance for credit losses

* The changes and reasons for those changes in both the receivables and the

allowance for credit losses

The proposed FAS would apply to all financing receivables held by creditors,

including all public and nonpublic entities that prepare financial statements.

The FASB states that the term "financing receivables" would include loans

defined as a contractual right to receive money on demand or on fixed or

determinable dates that are recognized as an asset in the creditor's statement of

financial position, whether originated or acquired.

Black, Tom, (1998), Using receivables purchasing to improve cash flow for small

businesses, Commercial Lending Review, 4, vol.13, 70-74

Within the last decade, a growing number of bankers have begun

supplementing their commercial product line with receivables purchasing programs,

boasting both exceptional yields and stable, satisfied customers.

23

By adhering to these 4 risk-management principles, bankers can significantly

mitigate risk in receivables purchasing: 1. Making a prudent initial credit decision, 2.

maintaining accurate and timely account information, 3. controlling the cash, 4.

Implementing effective monitoring procedures, and 5.providing protection against

changing credit circumstances.

Receivables purchasing has great potential for community banks. For bankers

willing to dig every day into invoices, payment terms, and billing statements,

receivables purchasing is a way to create profits.

Because receivables are the fastest-moving noncash asset a business has,

effective and consistent monitoring is the backbone of any credit facility based on

accounts receivable.

Paul, Salima Y, (2007), Organizing the credit management function, Credit

Management, 26-28, 30-31

If accounts receivable constitute one of the biggest but riskiest assets the

company is likely to have, one would expect special attention to be given to its

management. The way the credit function is organized has an effect on credit

management. So the management of this function should be part of the overall

objectives and should fit into the strategy of the business

It is widely accepted in credit management literature that factors such as the

nature of the product, the channels of distribution and whether companies can benefit

from economies of scale can affect the management of the credit function

Other factors affecting the credit management function is that it is widely

accepted that investment in the credit function and the time spent on each activity of

the credit management process have an impact on corporate performance.

The integration of the credit function within another department may be

desirable. Nevertheless, there may be a conflict of interest between credit objectives

and others. There may be incentives for the sales department, for instance, to

maximise the turnover and thus sales staff may offer more generous credit terms than

the industry norm or offer credit to risky customers. Consequently, more time and

24

resources are spent on back-end activities such as chasing unpaid bills, and the role

of credit mangers/controllers shifts to one of retrospective credit collection rather

than credit management and cannot be used proactively to contribute to the

enhancement of the company's performance.

Investing in the credit function is very important and may help trade credit

not just to remain a collectable asset but also to become one that is converted into

cash within the terms

Stevenson, Paul, (2005), Credit management policy, Credit Management, 8-18

The function of credit management is to maximize profitable sales, through

the prudent extension of credit, the balancing of financial risk and the efficient

collection of sales income within a framework of customer care. The primary

objectives of credit management include:

1. To ensure that all amounts due are collected according to the agreed payment

terms and that the most efficient methods of payment are used.

2. To identify high risk or marginal customers at an early stage, especially those

likely to get into financial difficulties and to take whatever action is thought

necessary to safeguard further sales to those customers.

3. Ensure that the cost of providing the goods/services on credit terms is at a level

that maximizes turnover with the minimum of risk.

4. Ensure that monthly cash collection targets are achieved.

5. Maintain a high quality of accounts receivable.

6. Develop a compatible working relationship with Sales, so that the needs of all

departments involved are satisfied to the benefit of the company as a whole.

Byl, Calvin D, (1994), Reporting accounts receivable to management, Business

Credit, 9, vol.96, 43

25

Managers need to have timely, accurate, and useful information to understand

and respond to the impact that the usually sizeable investment in accounts receivable

has on the cash flow and profitability of their operating units.

To determine what criteria for reporting on accounts receivable portfolios are

requested by management or used by credit departments in other companies in the

industry, a survey of credit managers from 34 agricultural companies was conducted

The survey participants were asked, "What do you consider to be the two

primary criteria for reporting the status of your accounts receivable to management?"

Their responses, though varied in detail, generally could be classified into five broad

categories:

1. Accounts Receivable Aging

2. Exception Reports

3. Days Sales Outstanding

4. Ratio Analysis

5. Trends Analysis Reports.

The responses from the seven survey participants using one criterion for their

reports fell into three different categories. Two used the Accounts Receivable Aging.

Two more used similar Ratio reports regarding the percentage of sales collected. The

other three used Exception Reports, but they were each a little different.

One of the participants reviewed only those accounts that were over their

credit lines as established by the credit department. Another participant reviewed all

accounts over 30 days past due. The other participant reviewed a watch list of

accounts that are of particular concern. The parameters for getting on this list were

not given.

Kerwin, Richard J, (1992), Field Examinations of Accounts Receivable, The

Secured Lender, 2, vol.48, 28

26

The best way to determine whether accounts receivables are fairly stated is

through a field examination. Risks involved in financing accounts receivable that

increase the lender's exposure for loss include: 1. the client may bill and hold. 2. The

client may pre-bill. 3. Returns, allowances, or other credits may dilute the value of

receivables. 4. The client may produce fictitious receivables. The auditor must ensure

that the receivables are valid and collectible.

Although each client employs different accounting methods and controls,

some general standards exist that can be adjusted as circumstances require.

The scope of the field examination includes:

* Reconciling the accounts receivable aging to the general ledger and the financial

statement.

* Reconciling the accounts receivable aging to reports produced by the client to the

lender.

* Verifying the aging.

* Verifying shipment of the goods.

* Reviewing the timeliness of the posting of payments and credit memos.

* Determining the concentration of customers.

* Determining if any pre billing or bill and holding exists.

* Reviewing credit approval procedures.

* Reviewing collection procedures.

Sims, C Paul, Jr; True, Patrick, (1997), Five keys to relying on accounts receivable

as a repayment source, The Journal of Lending & Credit Risk Management, 1,

vol.80, 40-44

27

Accounts receivable can represent a very sound repayment source because

they will typically convert to cash faster than any other asset on the balance sheet.

For the same reason, accounts receivable also can represent additional risks.

There are 5 keys to relying on accounts receivable as a repayment source: 1.

making a prudent initial credit decision, 2. maintaining accurate and timely

information, 3. ensuring control of the cash, 4. establishing effective monitoring

procedures, and 5. protecting against changing credit circumstances.

The 5 C's of credit - character, capacity, conditions, capital, and collateral -

play a vital role in any prudent initial credit decision. The need for businesses to free

cash from their receivables is not going to disappear. The banks most successful at

capitalizing on this market opportunity will be those that recognize and control their

receivables risk.

Kontus, Eleonora, (2013), Management of Accounts Receivable in a Company,

Ekonomska Misao i Praksa, 1, vol. 22, 21-38

Accounts receivable is the money owed to a company as a result of having

sold its products to customers on credit. The primary determinants of the company's

investment in accounts receivable are the industry, the level of total sales along with

the company's credit and the collection policies.

The major decision regarding accounts receivable is the determination of the

amount and terms of credit to extend to customers. The total amount of accounts

receivable outstanding at any given time is determined by two factors: the volume of

credit sales and the average length of time between sales and collections.

The purpose of this study is to determine ways of finding an optimal accounts

receivable level along with making optimum use of different credit policies in order

to achieve a maximum return at an acceptable level of risk.

We hypothesize that by applying scientifically-based accounts receivable

management and by establishing a credit policy that results in the highest net

earnings, companies can earn a satisfactory profit as well as a return on investment.

28

CHAPTER 3

PROFILE

29

CHAPTER-3

PROFILE

INDUSTRY PROFILE

India has been known as the original home of sugar and sugarcane. Indian

mythology supports the above fact as it contains legends showing the origin of

sugarcane. India is the second largest producer of sugarcane next to Brazil. Presently,

about 4 million hectares of land is under sugarcane with an average yield of 70

tonnes per hectare.

India is the largest single producer of sugar including traditional cane sugar

sweeteners, khandsari and Gur equivalent to 26 million tonnes raw value followed by

Brazil in the second place at 18.5 million tones. Even in respect of white crystal

sugar. Indian has ranked No. 1 position in 7 out of last 10 years.

Traditional sweeteners Gur & Khandsari are consumed mostly by the rural

population in India. In the early 1930’s nearly 2/3rd of sugarcane production was

utilized for production of alternate sweeteners, Gur & Khandsari. With better

standard of living and higher incomes, the sweetener demand has shifted to white

sugar. Currently, about 1/3rd sugarcane production is utilized by the Gur &

Khandsari sectors. Being in the small scale sector, these two sectors are completely

free from controls and taxes which are applicable to the sugar sector.

The advent of modern sugar processing industry in India began in 1930 with

grant of tariff protection to the Indian sugar industry. The number of sugar mills

increased from 30 in the year 1930 - 31 to 135 in the year 1935-36 and the

production during the same period increased from 1.20 lakh tonnes to 9.34 lakh

tonnes under the dynamic leadership of the private sector.

The era of planning for industrial development began in 1950-51 and

Government laid down targets of sugar production and consumption, licensed and

installed capacity, sugarcane production during each of the Five Year Plan periods.

30

COMPANY PROFILE

EID Parry Limited is a public company headquartered in Chennai, South

India that has been in business for more than 225 years. It has many firsts to its

credit, including the manufacturing of fertilizers (1906) for the first time in

the Indian subcontinent. The company is currently engaged in the manufacture and

marketing of sugar and bio-products. Parry's is the oldest surviving mercantile name

in Chennai.

ORIGIN

EID Parry is one of the oldest business entities of the Indian subcontinent and

was originated by Thomas Parry, a Welshman who came to India in the late

1780s. On 17 July 1788, he started a business of banking and piece goods.

By 1819, a partnership firm named "Parry and Dare" Company was founded by

Thomas Parry and John William Dare. Parry's Corner, one of the most

prominent central business districts of Chennai, derives its name from Parry.

Over a period of time, the business established by Parry continued to grow, and

its flagship company EID Parry emerged.

In 1908 Parry & Company set-up ‘The Pottery’ unit in Ranipettai. Over the years

it was named as "Parryware".

Parry & Company Limited and East India Distileries & Sugars Limited were

merged to form EID Parry India Limited. In its more than 200 year existence,

this house remained active and operated many businesses.

The Murugappa Group took over EID Parry in 1981 from financial & public

institutions such as Life Insurance Corporation Of India, United Assurance Co,

and Unit Trust of India.

31

Sugar

E.I.D Parry along with its subsidiaries has nine sugar plants spread across South

India of which four are in Tamil Nadu, one in Puducherry, three in Karnataka and

one in Andhra pradhesh. The company has sugarcane crushing capacity of 34,750

TCD and cogeneration capacity of 146 MW across its sugar mills. The integrated

sugar units have been designed to optimize process efficiencies, increase sugarcane

recovery ratio and increase energy efficiency through reduced steam and power

consumption.

E.I.D Parry continues to be one of the low cost producers of international quality

sugar, through its innovative process and farmer centric practices.

South India and Tamil Nadu in particular has many advantages for sugar production

and E.I.D Parry is able to capitalize on these advantages:-

Cane productivity and sugar recovery per unit area is highest. The average

farm size is less than a hectare and is owned by farmers. Geographically,

Tamil Nadu has the advantage of good soil and abundant water and yield is

highest among the various states in India.

Farmers are willing to adopt new farming practices and cultivation

methodologies, including mechanization, to improve yield

Access to ports to reach export market and improved development of

infrastructure facilities.

Direct relationship with cane growers to ensure adequate cane availability

and supply

Sugarcane breeding remains the focus to ensure timely availability of never

varieties of cane.

Cane and manufacturing

New technologies are implemented in all the milling process, for efficient

process. Factories in Tamil Nadu are integrated with co-generation and distillery

operating at Nellikuppam & Sivaganga. In the sugar process, different types viz. raw

sugar, white sugar and value added products are produced.

32

To make the value chain sustainable, in-house Cane R&D and Cane

Extension are driving the technology to field for the better yield, recovery

improvement and cost reduction. Information technology developments are fully

utilized for efficient data system management and process monitoring.

Value added products

E.I.D Parry has been retailing its brand sugar in South India. Apart from

branded retail sugar, the company is moving up with the value chain to products like

pharma grade sugar which improve the margins. Investments are being made not

only in appropriate manufacturing facilities, but also in branding and offering

customized solutions for institutional customers.

Co-products

India’s demand for the power and the blending of ethanol with petrol opens

the opportunity for co products.

Co-generation of power (Cogen): The growing energy consumption in India

allows the sugar industry to play an increasingly important role in the energy

economy. Additionally, the power generated and exported by the cogen unit

is environment friendly and made available to rural areas where the mills are

located, by a de-centralized infrastructure. Thus, sugarcane is increasingly

becoming an energy crop. The former is in line with Clean Development

Mechanism (CDM) methodologies for cogen power and as a result carbon

credits have started flowing into the company.

Molasses and alcohol: Molasses, the by-product of sugarcane, can be

converted into various types of alcohols like Rectified Spirit, ENA and Fuel

Ethanol, providing another earning stream for the business.

Both these businesses are ‘green’ considering their renewable nature

and, more importantly, given the relatively steady demand; help reduce the

33

vulnerability of the company, which is exposed to the cyclicality of the sugar

business.

SUGAR

E.I.D Parry set up India’s first sugar plant at Nellikuppam in 1842. The

Pioneering spirit has seen E.I.D Parry setting up the first fully automated sugar plant

at Pudukottai in 2000, a distillery, and more recently, zero waste integrated sugar

complexes.

E.I.D Parry produces variety of sugars at its four fully automated plants in

Tamil Nadu and a fifth one at Puducherry. These cater to the food, bakery,

confectioneries and beverage manufacturing industries, and are also used in pharma

applications.

BIO-PRODUCTS

The Bio-products division of E.I.D Parry is committed to helping farmers

produce profitable agricultural produce through safe and sustainable agricultural

inputs.

The division has a state-of-the-art Azadirachitin manufacturing facility in

Tamil Nadu, to produce Neemazal, an Eco-friendly botanical Bio-pesticide. The

ISO-14001 certified manufacturing unit is the world’s largest Azadirachitin

extraction plant. Besides these, there’s also Neemazal and Abda a granular plant

vitaliser formulation for early establishment, crop vigour and higher yields.

Envisaging active participation in the global green drive, new non-azadirachitin,

organic/ green agri inputs are also being pursued for introduction in future.

NUTRACEUTICALS

34

A division of E.I.D Parry (India) Ltd, Parry Nutraceuticals is a world leader

in nutritional food supplements- the only producer of 100% Vegetarian Certified

Organic Spirulina. It is the only one in the world to commercially produce three

different species of micro algae at large scale. Parry Nutraceuticals exports to over

38 countries, the main markets being North America, the EU, Japan, Korea,

Malaysia, Russia, Australia and New Zealand.

With the global trend moving towards preventive healthcare, Parry

Nutraceuticals is at the threshold of a dynamic growth era.

Credit Control – Policy and Procedures OF E.I.D Parry Limited1.Introduction

As the organization grows, it will be difficult to address individual issues

in the absence of clear-cut policies and procedures on all major business activities

of the organization. Such policies, apart from serving as references to the functional

managers will also help new comers to understand the organization’s culture and

practices and integrate smoothly into the working of the organization.

Credit being one of the major tools of marketing and risk management a

major focus area for organization as a whole, it is very important to have a well-

defined policy on credit control and risk management.

2. Objectives

To determine the criteria for evaluating the creditworthiness of customers of

different categories

To develop guidelines for fixing credit limits for individual customers both in

35

terms of quantum and age.

3. Creditworthiness

Creditworthiness of a customer is determined based on the following

criteria. Customers are rated on each of these criteria and are awarded points based

on their standing. The sum total of the points obtained by a customer (Max 200)

will form the basis for awarding credit ratings to customers ranging from E

(Lowest) to AAA (Highest).

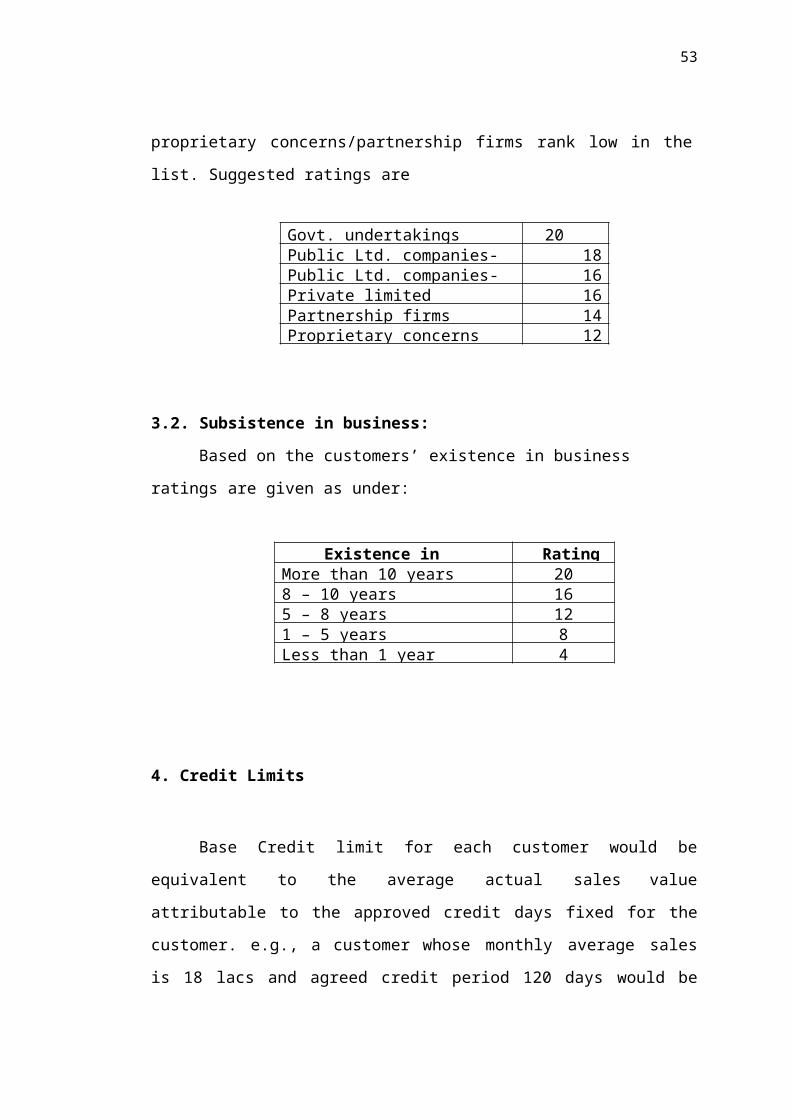

3.1. Constitution of the customer

While Govt. undertakings are most secure, proprietary concerns/partnership

firms rank low in the list. Suggested ratings are

Govt. undertakings 20 (max)Public Ltd. companies-Listed 18Public Ltd. companies-Unlisted 16Private limited companies 16Partnership firms 14Proprietary concerns 12

3.2. Subsistence in business:

Based on the customers’ existence in business ratings are given as under:

Existence in business RatingMore than 10 years 208 – 10 years 165 – 8 years 121 – 5 years 8Less than 1 year 4

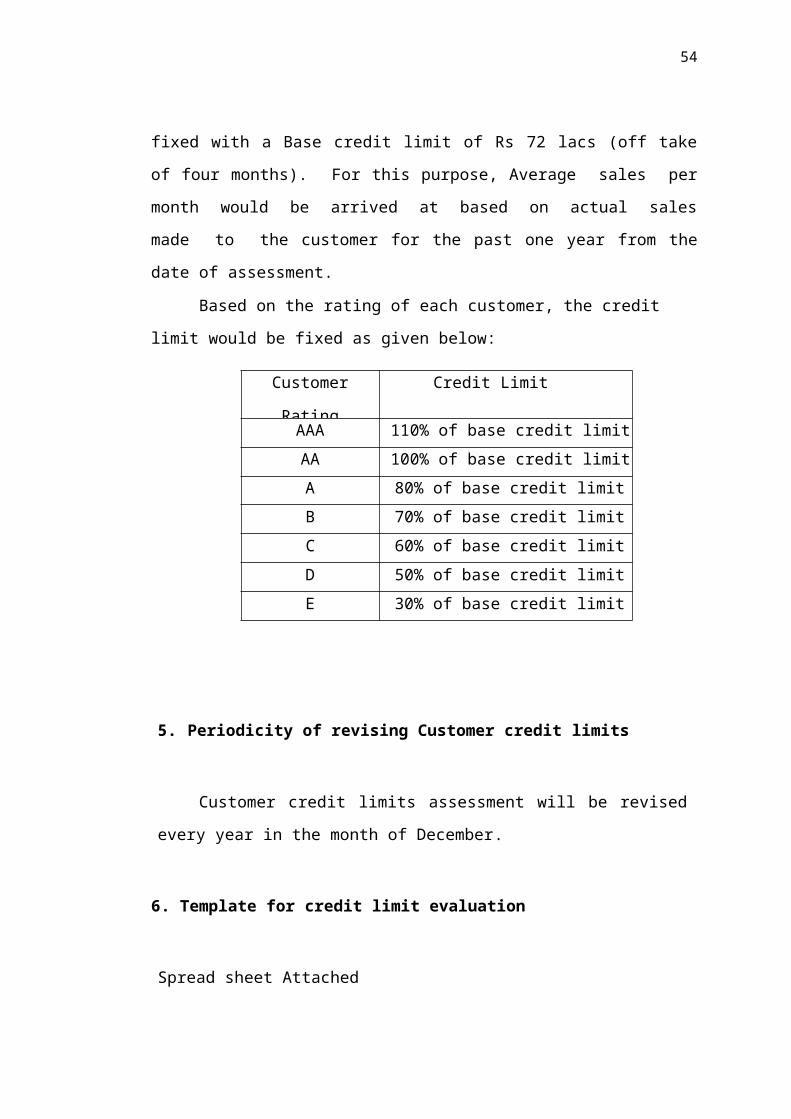

4. Credit Limits

36

Base Credit limit for each customer would be equivalent to the average

actual sales value attributable to the approved credit days fixed for the customer.

e.g., a customer whose monthly average sales is 18 lacs and agreed credit period

120 days would be fixed with a Base credit limit of Rs 72 lacs (off take of four

months). For this purpose, Average sales per month would be arrived at based

on actual sales made to the customer for the past one year from the date of

assessment.

Based on the rating of each customer, the credit limit would be fixed as given

below:

5. Periodicity of revising Customer credit limits

Customer credit limits assessment will be revised every year in the month

of December.

6. Template for credit limit evaluation

Spread sheet Attached

7. Responsibility of Credit Limit Fixation in SAP

Customer

Rating

Credit Limit

AAA 110% of base credit limit

AA 100% of base credit limit

A 80% of base credit limit

B 70% of base credit limit

C 60% of base credit limit

D 50% of base credit limit

E 30% of base credit limit

37

Finance team will send the customer wise base credit limits to marketing

team seeking their inputs on evaluation of other parameters like profits of

customers etc.,

Customer wise credit limit assessed for next year would be uploaded in

SAP by Business Finance head with the approval of Head of Sales and Marketing

and Business Head.

8. Approval authority for mid-term credit limit enhancement / reduction

Mid-term credit limit enhancement / reduction for any customer have to

be approved by Business head based on the recommendation of Head of Sales &

Marketing and Business Finance.

38

CHAPTER 4

DATA ANALYSIS AND INTERPRETATION

39

CHAPTER 4

DATA ANALYSIS AND INTERPRETATION

RATIO ANALYSIS

Ratio Analysis is the basic tool of financial analysis and financial analysis

itself is an important part of any business planning process as SWOT (Strengths,

Weaknesses, Opportunities and Threats), being the basic tool of the strategic analysis

plays a vital role in a business planning process and no SWOT analysis would be

complete without an analysis of company’s financial position. In this way Ratio

Analysis is very important part of whole business strategic planning.

A. LIQUIDITY

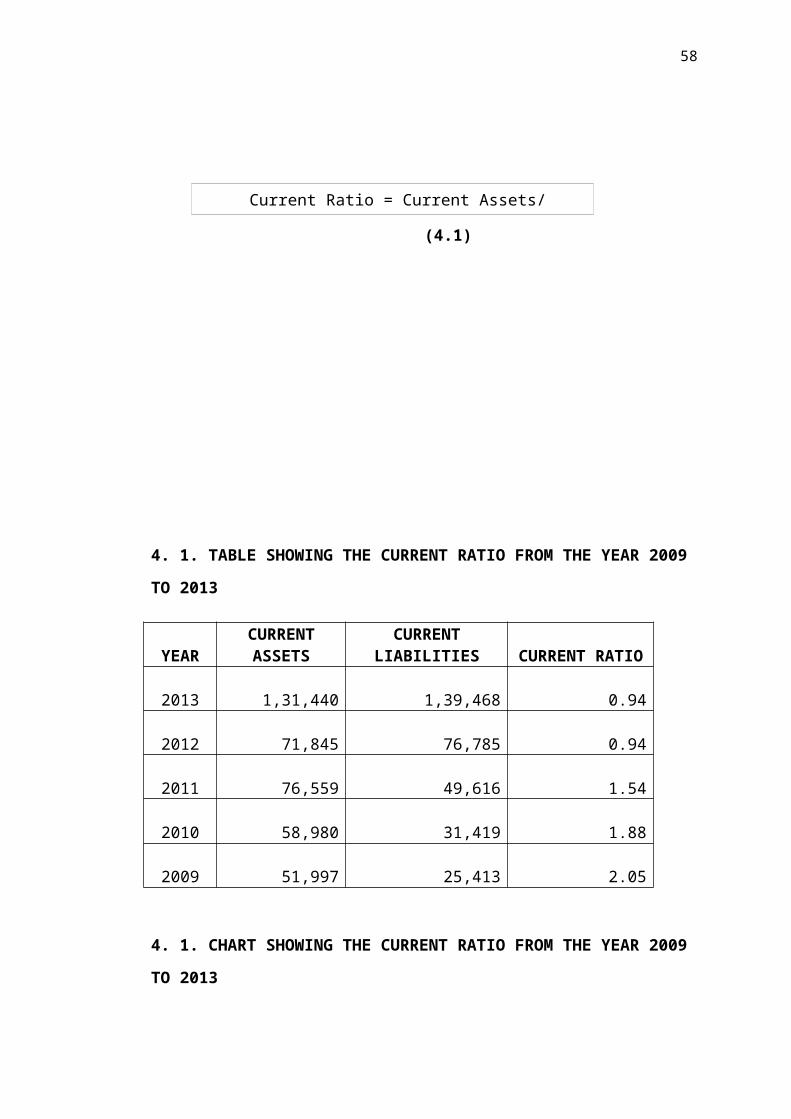

4.1. Current ratio:

Current ratio is the ratio of current assets of a business to its current

liabilities. It is the most widely used test of liquidity of a business and measures the

ability of a business to repay its debts over the period of next 12 months.

(4.1)Current Ratio = Current Assets/ Current liabilities

40

4. 1. TABLE SHOWING THE CURRENT RATIO FROM THE YEAR 2009

TO 2013

YEARCURRENT

ASSETSCURRENT

LIABILITIESCURRENT

RATIO

2013

1,31,440

1,39,468 0.94

2012

71,845

76,785 0.94

2011

76,559

49,616 1.54

2010

58,980

31,419 1.88

2009

51,997

25,413 2.05

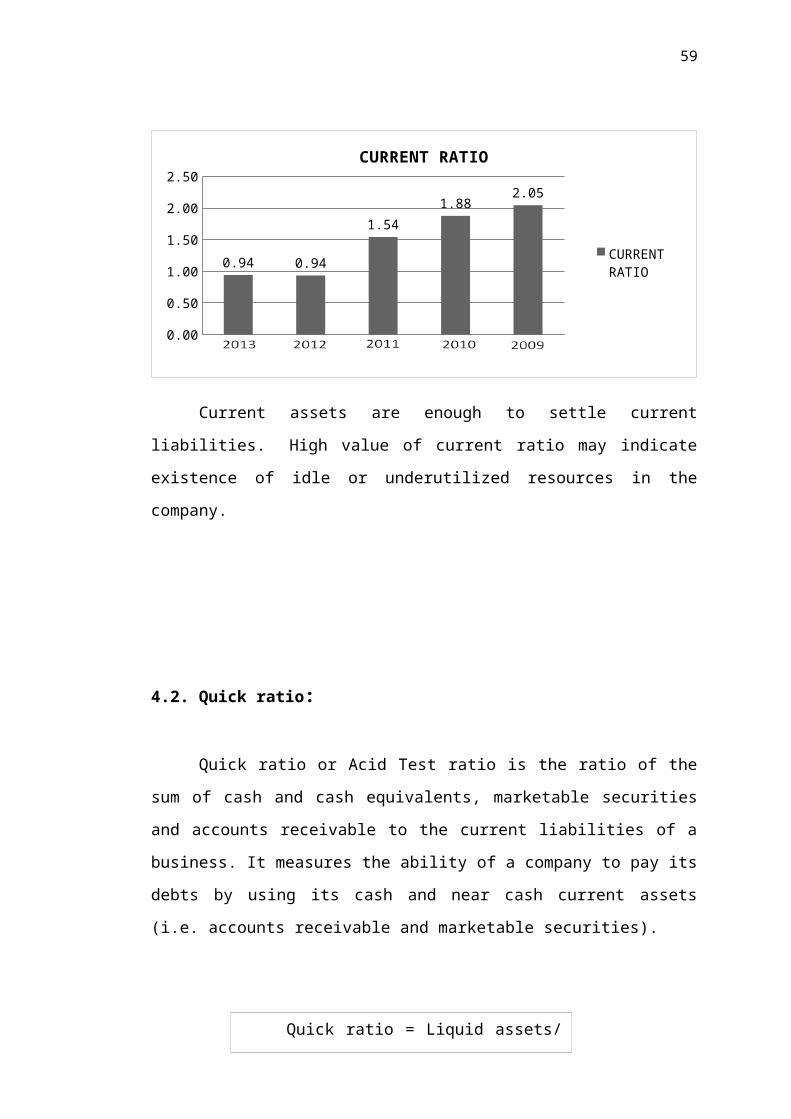

4. 1. CHART SHOWING THE CURRENT RATIO FROM THE YEAR 2009

TO 2013

0.00

0.50

1.00

1.50

2.00

2.50

0.94 0.94

1.54

1.882.05

CURRENT RATIO

CURRENT RATIO

Current assets are enough to settle current liabilities. High value of current

ratio may indicate existence of idle or underutilized resources in the company.

41

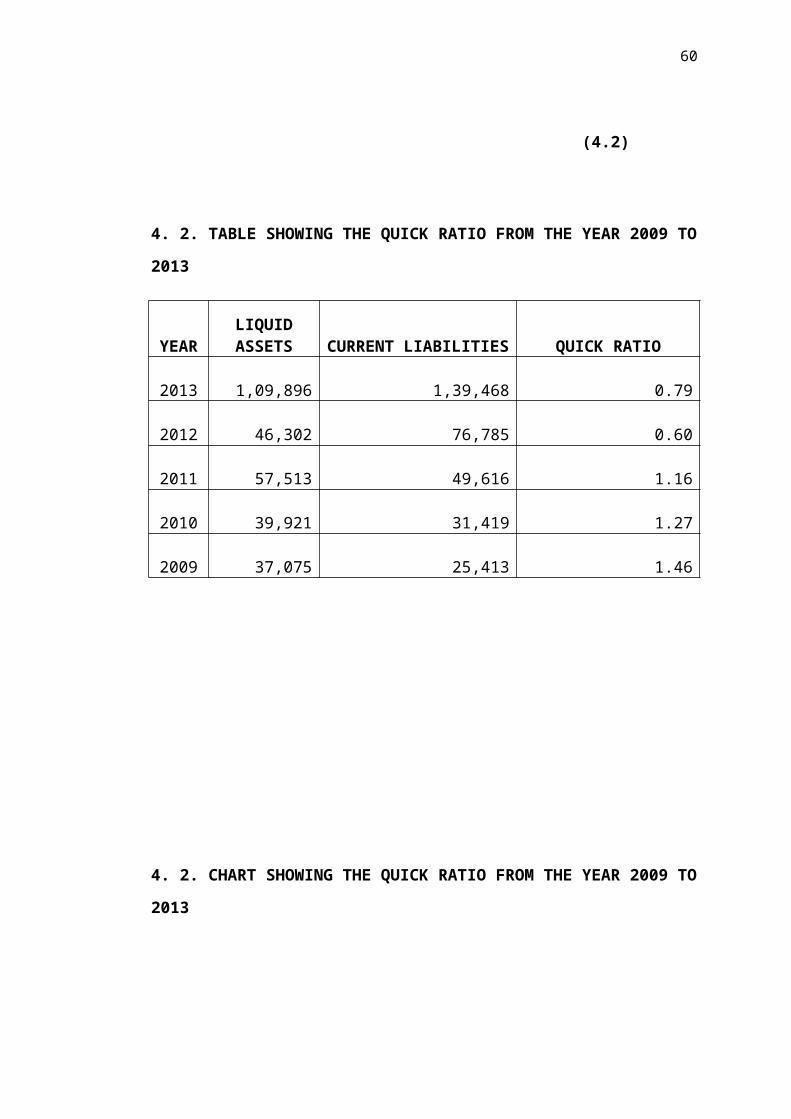

4.2. Quick ratio:

Quick ratio or Acid Test ratio is the ratio of the sum of cash and cash

equivalents, marketable securities and accounts receivable to the current liabilities of

a business. It measures the ability of a company to pay its debts by using its cash and

near cash current assets (i.e. accounts receivable and marketable securities).

(4.2)

4. 2. TABLE SHOWING THE QUICK RATIO FROM THE YEAR 2009 TO

2013

YEARLIQUID ASSETS CURRENT LIABILITIES QUICK RATIO

2013

1,09,896

1,39,468 0.79

2012

46,302

76,785 0.60

2011

57,513

49,616 1.16

2010

39,921

31,419 1.27

2009

37,075

25,413 1.46

Quick ratio = Liquid assets/ Current liabilities

42

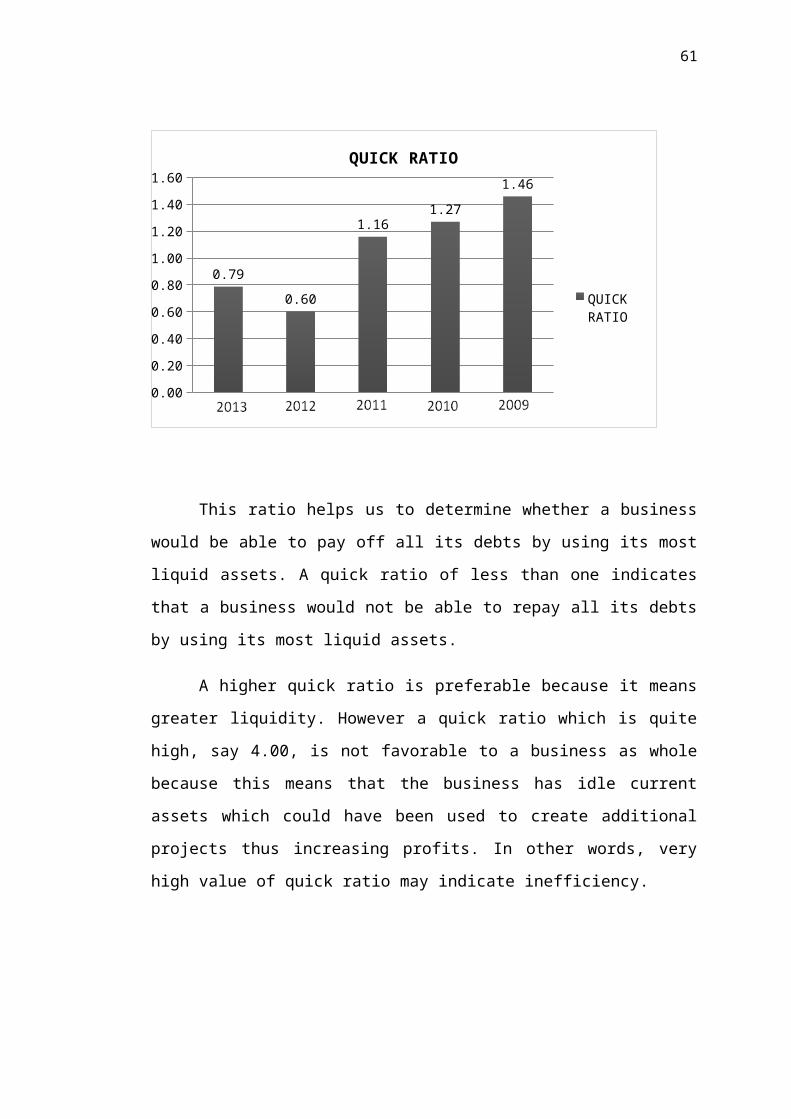

4. 2. CHART SHOWING THE QUICK RATIO FROM THE YEAR 2009 TO

2013

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

0.79

0.60

1.161.27

1.46

QUICK RATIO

QUICK RATIO

This ratio helps us to determine whether a business would be able to pay off

all its debts by using its most liquid assets. A quick ratio of less than one indicates

that a business would not be able to repay all its debts by using its most liquid assets.

A higher quick ratio is preferable because it means greater liquidity. However

a quick ratio which is quite high, say 4.00, is not favorable to a business as whole

because this means that the business has idle current assets which could have been

used to create additional projects thus increasing profits. In other words, very high

value of quick ratio may indicate inefficiency.

43

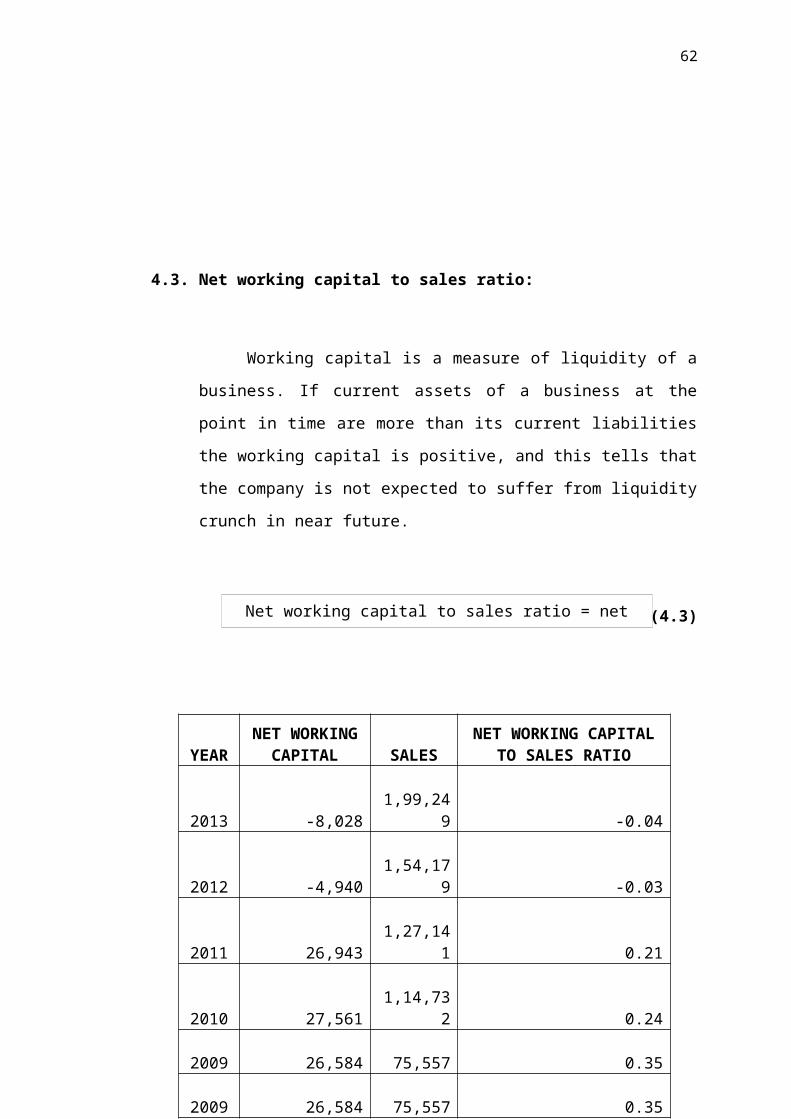

4.3. Net working capital to sales ratio:

Working capital is a measure of liquidity of a business. If current

assets of a business at the point in time are more than its current liabilities the

working capital is positive, and this tells that the company is not expected to

suffer from liquidity crunch in near future.

(4.3)

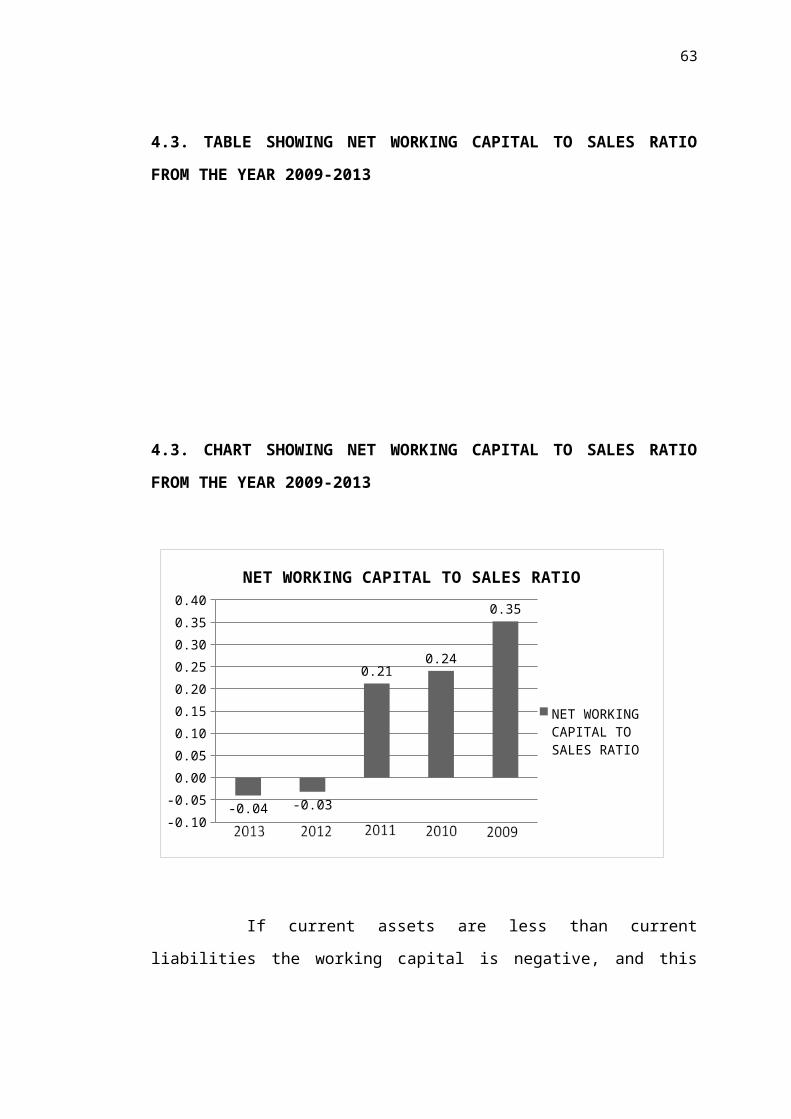

4.3. TABLE SHOWING NET WORKING CAPITAL TO SALES RATIO

FROM THE YEAR 2009-2013

4.3. CHART SHOWING NET WORKING CAPITAL TO SALES RATIO

FROM THE YEAR 2009-2013

Net working capital to sales ratio = net working capital/ sales

YEAR

NET WORKING CAPITAL SALES

NET WORKING CAPITAL TO SALES RATIO

2013

-8,028

1,99,249 -0.04

2012

-4,940

1,54,179 -0.03

2011

26,943

1,27,141 0.21

2010

27,561

1,14,732 0.24

2009

26,584

75,557 0.35

2009

26,584

75,557 0.35

44

-0.10

-0.05

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

-0.04 -0.03

0.210.24

0.35

NET WORKING CAPITAL TO SALES RATIO

NET WORKING CAP-ITAL TO SALES RA-TIO

If current assets are less than current liabilities the working capital is

negative, and this communicates that the business may not be able to pay off its

current liabilities when due.

B. PROFITABILITY

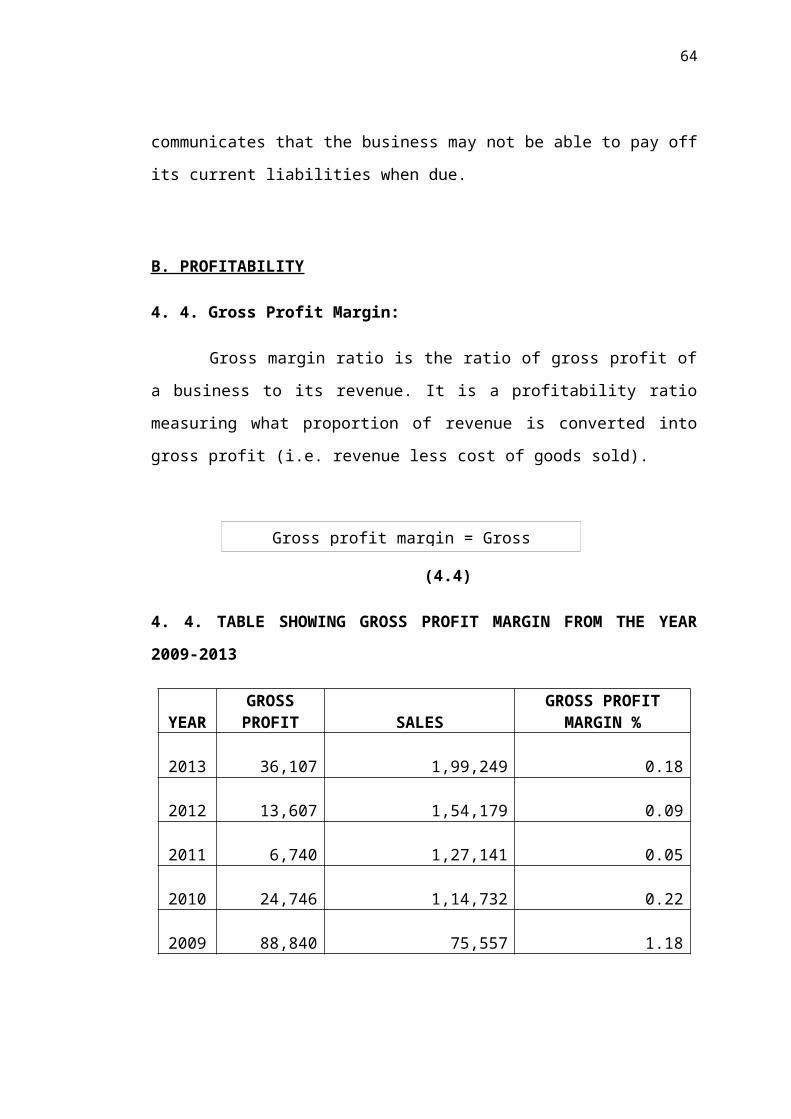

4. 4. Gross Profit Margin:

Gross margin ratio is the ratio of gross profit of a business to its revenue. It is

a profitability ratio measuring what proportion of revenue is converted into gross

profit (i.e. revenue less cost of goods sold).

(4.4)

4. 4. TABLE SHOWING GROSS PROFIT MARGIN FROM THE YEAR 2009-

2013

YEAR

GROSS PROFIT SALES

GROSS PROFIT MARGIN %

Gross profit margin = Gross profit / Sales * 100

45

2013

36,107

1,99,249 0.18

2012

13,607

1,54,179 0.09

2011

6,740

1,27,141 0.05

2010

24,746

1,14,732 0.22

2009

88,840

75,557 1.18

4. 4. CHART SHOWING GROSS PROFIT MARGIN FROM THE YEAR

2009-2013

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

0.180.09 0.05

0.22

1.18

GROSS PROFIT MARGIN

GROSS PROFIT MARGIN

Gross margin ratio measures profitability. Higher values indicate that more

cents are earned per dollar of revenue which is favorable because more profit will be

available to cover non-production costs. In this case higher gross margin ratio means

that the retailer charges higher markup on goods sold. But in the year 2013 it seems

to be very low.

4. 5. Net profit margin:

It is a popular profitability ratio that shows relationship between net profit after

tax and net sales. It is computed by dividing the net profit (after tax) by net sales.

46

(4.5)

4. 5. TABLE SHOWING THE NET PROFIT MARGIN FROM THE YEAR

2009-2013

4. 5.

CHART SHOWING THE NET PROFIT MARGIN FROM THE YEAR 2009-

2013

0.000.100.200.300.400.500.600.700.800.901.00

0.170.09 0.06

0.18

0.92

NET PROFIT MARGIN

NET PROFIT MARGIN

Net Profit Margin = Net Profit after Tax / Net Sales * 100

YEAR NET PROFIT SALESNET PROFIT

MARGIN%

2013 33,171 1,99,249 0.17

2012 13,732 1,54,179 0.09

2011 7,926 1,27,141 0.06

2010 20,528 1,14,732 0.18

2009 69,196 75,557 0.92

47

Comparing the ratio with the previous years’ ratio, the industry’s average and

the budgeted net profit ratio. A high ratio indicates the efficient management of the

affairs of business.

C. ACTIVITY

4. 6. Inventory Turnover Ratio:

Inventory turnover is the ratio of cost of goods sold by a business to its

average inventory during a given accounting period. It is an activity ratio measuring

the number of times per period; a business sells and replaces its entire batch of

inventory again.

(4.6)

4. 6. TABLE SHOWING THE INVENTORY TURNOVER RATIO FROM

THE YEAR 2009 TO 2013

YEAR SALESAVERAGE

INVENTORY

INVENTORY TURNOVER RATIO

(times)

2013

1,99,249

51,898 3.84

2012

1,54,179

22,295 6.92

2011

1,27,141

19,053 6.67

2010

1,14,732

16,991 6.75

2009

75,557

16,513 4.58

Inventory Turnover Ratio = Inventory / Net Sales

48

4. 6. CHART SHOWING THE INVENTORY FROM THE YEAR 2009 TO

2013

0.001.002.003.004.005.006.007.008.00

3.84

6.92 6.67 6.75

4.58

INVENTORY TURNOVER RATIO

INVENTORY TURNOVER RATIO

A higher value of inventory turnover indicates better performance and lower

value means inefficiency in controlling inventory levels. A lower inventory turnover

ratio may be an indication of over-stocking which may pose risk of obsolescence and

increased inventory holding costs. However, a very high value of this ratio may be

accompanied by loss of sales due to inventory shortage.

4. 7. Accounts Receivable Turnover Ratio:

Accounts receivable turnover is the ratio of net credit sales of a business to its

average accounts receivable during a given period, usually a year. It is an activity

ratio which estimates the number of times a business collects its average accounts

receivable balance during a period.

(4.7)

4. 7. TABLE SHOWING THE ACCOUNTS RECEIVABLE RATIO FROM

THE YEAR 2009 TO 2013

Accounts receivable turnover ratio = Net Credit Sales/ Average Accounts Receivable

49

YEARNET CREDIT

SALESAVERAGE ACCOUNTS

RECEIVABLE

ACCOUNTS RECEIVABLE TURNOVER

RATIO (times)

2013 1,99,249 21,790 9.14

2012 1,54,179 17,955 8.59

2011 1,27,141 12,310 10.33

2010 1,14,732 12,592 9.11

2009 75,557 11,957 6.32

4. 7. CHART SHOWING THE ACCOUNTS RECEIVABLE RATIO FROM

THE YEAR 2009 TO 2013

0.00

2.00

4.00

6.00

8.00

10.00

12.00

9.148.59

10.339.11

6.32

ACCOUNTS RECEIVABLE TURNOVER RATIO

ACCOUNTS RECEIVABLE TURNOVER RATIO

50

Generally a high value of accounts receivable turnover is favourable and

lower figure may indicate inefficiency in collecting outstanding sales. Increase in

accounts receivable turnover overtime generally indicates improvement in the

process of cash collection on credit sales. A very high value of this ratio may not be

favourable, if achieved by extremely strict credit terms since such policies may repel

potential buyers.

4. 8. Average collection period:

It is also called Days' sales outstanding ratio which is used to measure the

average number of days a business takes to collect its trade receivables after they

have been created. It is an activity ratio and gives information about the efficiency of

sales collection activities.

(4.8)

YEAR

NO. OF

WORKING

DAYS

ACCOUNTS

RECEIVABLE

TURNOVER RATIO

AVERAGE

COLLECTION

PERIOD (days)

2013 365 9.14 40

2012 365 8.59 42

2011 365 10.33 35

2010 365 9.11 40

2009 365 6.32 58

4. 8. TABLE SHOWING THE AVERAGE COLLECTION PERIOD FROM

THE YEAR 2009 TO 2013

4. 8. CHART SHOWING THE AVERAGE COLLECTION PERIOD FROM

THE YEAR 2012 TO 2013

Average Collection Period = Accounts Receivable/ Credit Sales * Number of Days

51

0

10

20

30

40

50

60

70

40 4235

40

58

AVERAGE COLLECTION PERIOD

AVERAGE COLLECTION PERIOD

Since it is profitable to convert sales into cash quickly, this means that a

lower value of Days Sales Outstanding is favorable whereas a higher value is

unfavorable. However it is more meaningful to create monthly or weekly trend of

DSO. Any significant increase in the trend is unfavorable and indicates inefficiency

in credit sales collection.

4. 9. TABLE SHOWING TURNOVER OF VARIOUS BUSINESS SEGMENTS

OF E.I.D PARRY LTD

52

4. 9. CHART SHOWING TURNOVER OF VARIOUS BUSINESS

SEGMENTS OF E.I.D PARRY LTD

Bus. Segments 2012-13 2011-12

Sugar 1,53,293 1,19,210

Cogeneration 14,409 13,064

Distillery 20,186 11,508

Sugar total 1,87,888 1,43,782

Bio-pesticides 7,321 7,628

Nutraceuticals 5,731 4,359

Others 408 369

Bio & Nutra Total 13,460 12,356

Total 2,01,348 1,56,138

53

bio-pesticidesnutraceuticals others sugar 0

20000

40000

60000

80000

100000

120000

140000

160000

180000

200000

TURNOVER OF VARIOUS BUSINESS SEGMENTS

Sum of 2012-13Sum of 2011-12

The total turnover of the Company grew by 29% from 1,56,138 Lakh in the year 2011-12 to

2,01,348 Lakh in the year 2012-13. The increment was the result of the following:

Growth in Sugar division‘s sales from 1,43,782 lakh to 1,87,888 Lakh in 2012-13 mainly

driven by increased power export, alcohol sales and merger of Haliyal & Sankili units with

EID’s sugar business.

Growth in Nutraceuticals division’s sales from ` 4,359 lakh to ` 5,731 lakh in 2012-13.

4. 10. TABLE SHOWING THE MONTHLY TOTAL SALES DURING THE

FINANCIAL YEAR 2012-2013

54

4. 10. CHART SHOWING TREND OF SALES FOR THE FINANCIAL YEAR

2012-2013

Sum of

Apr-12

Total

Sum of

May-12

Total

Sum of

Jun-12

Total

Sum of

Jul-12

Total

Sum of

Aug-12

Total

Sum of

Sep-12

Total

Sum of

Oct-12

Total

Sum of

Nov-12

Total

Sum of

Dec-12

Total

Sum of

Jan-13

Total

Sum of

Feb-13

Total

Sum of

Mar-13

Total

0100000000200000000300000000400000000500000000600000000700000000800000000

TREND OF SALES

trend of sales

From the above chart it indicates that in the month of March-2013the sales is

very high and in the beginning of the year it seems to be lowest and later in the

month of October-2012 again there is a fall in sales value.

4. 11. CHART SHOWING THE TREND OF DEBTORS FOR THE

FINANCIAL YEAR 2012-2013

SUMMARY OF MONTHSTOTAL SALES AMOUNT (RS)

Sum of Apr-12 Total 7575149.36Sum of May-12 Total 42780178Sum of Jun-12 Total 98964913Sum of Jul-12 Total 81667999Sum of Aug-12 Total 43150863Sum of Sep-12 Total 81994402Sum of Oct-12 Total 25991279.94Sum of Nov-12 Total 43703675.58Sum of Dec-12 Total 82407937.47Sum of Jan-13 Total 50662451.95Sum of Feb-13 Total 121895947Sum of Mar-13 Total 730894185

55

Total0

100

200

300

400

500

600

700

800TREND OF DEBTORS

Sum of MAR 2013Sum of Feb-13Sum of Jan-13Sum of Dec-12Sum of Nov-12Sum of Oct-12Sum of Sep-12Sum of Aug-12Sum of Jul-12Sum of Jun-12Sum of May-12Sum of Apr-12

This chart indicates that amount due seems too low in the beginning of the

year and subsequently it has increased at the end of the year. In the middle of the

year the debtor value seems to remain constant i.e. in the month of August,

September and October.

4. 12. CHART SHOWING MONTHWISE SUMMARY OF DEBTORS

56

east HO south west0

100

200

300

400

500

600

MONTHWISE SUMMARY OF DEBTORSSum of MAR 2013Sum of Feb-13Sum of Jan-13Sum of Dec-12Sum of Nov-12Sum of Oct-12Sum of Sep-12Sum of Aug-12Sum of Jul-12Sum of Jun-12Sum of May-12Sum of Apr-12REGION

VALUES

The above chart gives a detailed report of the debtors showing their status in

regional level where the highest amount due is indicated in the south region. And the

head office which is in Chennai indicated the lowest.

57

CHAPTER 5

RESULTS AND DISCUSSION

CHAPTER 5

58

RESULTS AND DISCUSSION

5.1. SUMMARY OF FINDINGS

1. High value of current ratio may indicate existence of idle or underutilized

resources in the company.(from table 4.1 and chart 4.1)

2. Quick ratio of less than one indicates that the current assets comprises of too

much non-liquid assets. (from table 4.2 and chart 4.2)

3. Current assets are less than current liabilities the working capital is negative,

and this communicates that the business may not be able to pay off its current

liabilities when due. (from table 4.3 and chart 4.3)

4. Lower value of gross profit margin indicates that fewer cents are earned per

dollar of revenue which is unfavorable because less profit will be available to

cover non-production costs. (from table 4.4 and chart 4.4)

5. Comparing the net profit ratio with the previous years’ ratio, the industry’s

average and the budgeted net profit ratio. A lower ratio indicates the

inefficient management of the affairs of business. (from table 4.5 and chart

4.5)

6. It is observed that in the year 2013 it indicates a lower inventory turnover

ratio, an indication of over-stocking which may pose risk of obsolescence

and increased inventory holding costs. In the year 2012, it indicates a very

high value of this ratio which may be accompanied by loss of sales due to

inventory shortage. (from table 4.6 and chart 4.6)

7. In the year 2011 it is observed that there is a high value of accounts

receivable turnover which is favourable and lower figure may indicate

inefficiency in collecting outstanding sales. (from table 4.7 and chart 4.7)

8. Since it is profitable to augment working capital, this means that a lower

value of Days Sales Outstanding is favorable whereas a higher value is

unfavorable. Here in the year 2013 it is low which favorable. (from table 4.8

and chart 4.8)

59

9. The total turnover of the Company grew by 29% from 1,56,138 Lakh in the

year 2011-12 to 2,01,348 Lakh in the year 2012-13. (from table 4.9 and chart

4.9)

5.2. SUGGESTIONS

From the study made on the receivables position of the Company it is

observed that they are in very have to:-

1. Strengthen their management of receivables.

2. State explicit and articulate credit policies.

3. An efficient collection program.

4. Better co ordination between production, sales, and finance

departments.

5. A higher value of inventory turnover indicates better performance

efficiency in controlling inventory levels.

6. A very high value of accounts receivable turnover ratio may not be

favorable, if achieved by extremely strict credit terms since such policies may

repel potential buyers.

5.3. CONCLUSION

This project focuses on the receivables management which plays a crucial

role in the working capital of the company. The analysis of the project reveals that

there is high volatility in extending credit period to customers.

The analysis further reveals that there is great scope in increasing the sales

volume, in managing better collection.

The suggestions offered clearly indicated the efforts to be undertaken in

better receivables management and increasing the turnover.

60

If these suggestions are taken note of by company, then define rely the

company can very well manage the working capital position with better collection

through increased sales.

61

APPENDIX

Particulars As atMarch 31,

2013

As atMarch 31,

2012

As atMarch 31,

2011

As atMarch 31,

2010

As atMarch 31,

2009

A. EQUITY AND

LIABILITIES

1. Shareholders' funds

(a) Share Capital 1,758 1,737 1,732 1,727 1,722

(b) Reserves and Surplus 1,32,930 120,026 1,13,296 1,07,907 95,210

1,34,688 121,763 1,15,028 1,09,634 96,932

2. Non-Current Liabilities

(a) Long Term Borrowings 75,916 33,327 30,888 57,552 53,853

(b) Deferred Tax Liabilities

(Net)

13,380 12,564 12,689 13,875 10,888

89,296 45,891 43,577 71,427 64,741

3. Current Liabilities

(a) Short Term Borrowings 96,393 45,644 27,921 26,309 18,362

(b) Trade Payables 21,547 12,513 9,511 - -

(c) Other Current Liabilities 20,497 17,801 11,156 - -

(d) Short Term Provisions 1,031 827 1,028 5,110 7,051

1,39,468 76,785 49,616 31,419 25,413

TOTAL 3,63,452 2,44,439 2,08,221 2,12,480 1,87,086

62

B. ASSETS

1. Non-Current Assets

(a) Fixed Assets

(i) Tangible Assets 1,22,870 76,494 78,272 81,640 79,515

(ii) Intangible Assets 107 5 18 - -

(iii) Capital Work in

Progress

6,201 4,917 3,250 3,578 7,009

(b) Non Current Investments

87,110 67,978 42,714 68,282 48,561

(c) Long Term Loans &

Advances

15,724 23,200 7,408 - -

2,32,012 172,594 131,662 1,53,500 1,35,085

2. Current Assets

(a) Current Investments - 300 700 - -

(b) Inventories 78,253 25,543 19,046 19,059 14,922

(c) Trade Receivables 21,544 22,036 12,910 11,710 13,474

(d) Cash and Cash

Equivalents

1,692 3,457 4,940 7,403 8,591

(e) Short Term Loans &

Advances

23,854 17,543 38,866 20,612 14,942

(f) Other Current Assets 6,097 2,966 97 196 68

1,31,440 71,845 76,559 58,980 51,997

Miscellaneous expenditure 4

TOTAL 3,63,452 244,439 2,08,221 2,12,480 1,87,086

63

FINANCIAL HIGHLIGHTS TAKEN FROM ANNUAL REPORT OF

2012-2013 OF E.I.D. PARRY (INDIA) LIMITED

64

REFERENCES

1. Joy, O.M.: Introduction to Financial Management (Madras: Institute for Financial Management and Research, 1978), P.210.

2. Robert N. Anthony: Management Accounting, Op. Cit., P.291

3. Prasanna Chandra: Financial Management, Op. Cit., P.291

4. R.K. Mishra: Problems of Working Capital Op. Cit, P.94

5. R.J. Chambers: Financing Management (Sydney: The Law Book Co., Ltd., 1967), PP.273-274

6. Agarwal, N.K.: Management of Working Capital, Op. Cit., P.54

7. I.M. Pandey : Op. Cit., P.381

E- REFERENCES

http://www.currentratioformula.com/

http://accountingexplained.com/financial/ratios/receivables-turnover

http://www.eidparry.com/investors/annual-reports.aspx

http://www.eidparry.com/

http://www.scribd.com/doc/28065175/Receivables-Management

http://www.investopedia.com/terms/c/credit-control.asp