Embed Size (px)

Citation preview

GROUP- BQ. 1 : What are the components of Business?Components of Business:The business is classified into following two components:

A. Industry

B. Commerce

A. Industry: Industry is the main component of business. The production aspect of business is known as industry. Industry is a place where production takes place. Industry creates form utility.

There are different types of industries classified on the basis of their activities performed.

1) Manufacturing Industry: Any industry that makes products from raw materials by the use of manual labour or machines and that is usually carried out systematically with a division of labour is known as manufacturing industry.

Manufactruing industry further devided into following categories:

A. Assembling Industry: B. Processing Industry: C. Analytical Industry:

2) Construction Industry: Construction is a process that consists of building or assembling of infrastructure. Construction Industry is one of the most booming industries.

3) Extractive Industry: Extractive industry deals with extraction of mineral oil from the crust of the earth. Example: fishing, mining etc. The industries which are involved in taking out the wealth from nature e.g. mining, fishing, hunting, agriculture etc. occupation involved on extractive industry are Fisherman, hunter, oil driller, lumberer, miner, farmer etc.

4) Genetic Industry: Genetic industry is concerned with re-production or multiplication of species and aims at producing genetically modified organisms. For example: poultry, planting nurseries, sericulture, cattle breeding, dairy farming, horticulture etc.

5. Service Industry:The industry, which earns profit by giving service, is known as service industry. Institutions like clinic, private hospital, banking, hotel, etc. are examples of service industry. B. Commerce:Another component of business is known as commerce. It is concerned with the distributional aspect. Commerce deals with transfer of ownership of goods and services. It facilitates movement of goods from the place of production to the place of consumption.

Commerce is further classified into two types: a. Trade

b. Aids to Trade

Buying and Selling of goods and services is called trade. Trade occurs when one thing occurs for another. Trade means exchange of goods, services, or both. A mechanism that allows trade is called a market.

The original form of trade was barter trade. Trade between two traders is called bilateral trade, while trade between more than two traders is called multilateral trade.

Trade exists between regions because different regions have a comparative advantage.

Trade is again sub-divided into two: I. Internal Trade

II. External Trade

I. Internal Trade: The trade conducted within the national boundaries of a country is known as internal trade. Internal trade can also be termed as Home trade or Domestic trade.

Example: Trade between Maharashtra and Gujarat. Internal trade can be further classified on the basis of their operation:

a. Wholesale trade

b. Retail trade

II. External trade: The trade, which is carried out beyond the national boundaries is called external trade. External trade is also known as international trade or foreign trade. External trade is exchange of capital, goods, and services across international borders.

External trade is sub-divided into three: a) Import trade

b) Export trade

c) Entrepot trade

b. Aids to Trade: There are various obstacles that can hinder the smooth running of trade. Aids to trade facilitates smooth conduct of trade. The activities that are involved in removing these obstacles are known as aids to trade.

An aid to trade involves the following functions:

i. Warehousing

ii. Transportation

iii. Insurance

iv. Banking

v. Advertising and sales promotion

Q. 2: Write short notes on MSME. Give the meaning and investment limit of MSME.

Definition of Micro, Small and Medium Enterprises:

The MSMED Act, 2006 defines the Micro, Small and Medium Enterprises based (i) on the investment in plant and machinery for those engaged in manufacturing or production, processing or preservation of goods and (ii) on the investment in equipment for enterprises engaged in providing or rendering of Services.

As per the ‘MSME at a Glance’ Report of the Ministry of MSMEs, the sector consists of 36 million units and provides employment to over 80 million persons. The Sector produces more than 6,000 products contributing to about 8% of GDP besides 45% to the total manufacturing output and 40% to the exports from the country.

In accordance with the provision of Micro, Small & Medium Enterprises Development (MSMED) Act, 2006 the Micro, Small and Medium Enterprises (MSME) are classified in two Classes:

1. Manufacturing Enterprises-he enterprises engaged in the manufacture or production of goods pertaining to any industry specified in the first schedule to the industries (Development and regulation) Act, 1951) or employing plant and machinery in the process of value addition to the final product having a distinct name or character or use. The Manufacturing Enterprise are defined in terms of investment in Plant & Machinery.

2. Service Enterprises:-The enterprises engaged in providing or rendering of services and are defined in terms of investment in equipment.

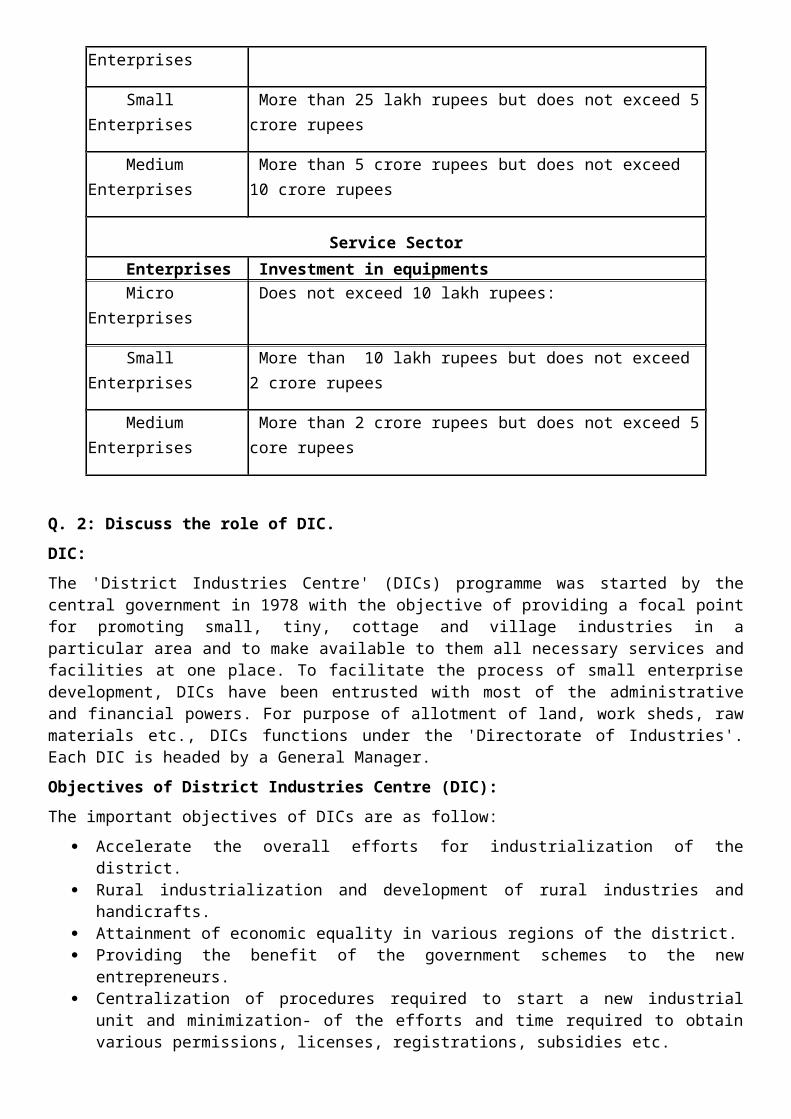

Manufacturing Sector Enterprises Investment in plant & machinery Micro Enterprises Does not exceed 25 lakh rupees

Small Enterprises More than 25 lakh rupees but does not exceed 5 crore rupees

Medium Enterprises

More than 5 crore rupees but does not exceed 10 crore rupees

Service Sector Enterprises Investment in equipments Micro Enterprises Does not exceed 10 lakh rupees:

Small Enterprises More than 10 lakh rupees but does not exceed 2 crore rupees

Medium Enterprises

More than 2 crore rupees but does not exceed 5 core rupees

Q. 2: Discuss the role of DIC.DIC:The 'District Industries Centre' (DICs) programme was started by the central government in 1978 with the objective of providing a focal point for promoting small, tiny, cottage and village industries in a particular area and to make available to them all necessary services and facilities at one place. To facilitate the process of small enterprise development, DICs have been entrusted with most of the administrative and financial powers. For purpose of allotment of land, work sheds, raw materials etc., DICs functions under the 'Directorate of Industries'. Each DIC is headed by a General Manager.

Objectives of District Industries Centre (DIC):The important objectives of DICs are as follow:

Accelerate the overall efforts for industrialization of the district. Rural industrialization and development of rural industries and handicrafts. Attainment of economic equality in various regions of the district. Providing the benefit of the government schemes to the new entrepreneurs. Centralization of procedures required to start a new industrial unit and minimization- of the

efforts and time required to obtain various permissions, licenses, registrations, subsidies etc.

Functions of District Industries Centre (DIC): Acts as the focal point of the industrialization of the district.

Prepares the industrial profile of the district with respect to : Statistics and information about existing industrial units in the district in the large, Medium,

small as well as co-operative sectors. Opportunity guidance to entrepreneurs. Provides information about local sources of raw materials and their availability. Provides Manpower assessment with respect to skilled, semi-skilled workers. Organizes entrepreneurship development training programs. Provides information about various government schemes, subsidies, grants and assistance

available from the other corporations set up for promotion of industries. Gives MSME registration. Advices the entrepreneurs on investments. Acts as a link between the entrepreneurs and the lead bank of the district. Implements government sponsored schemes for educated unemployed people like PMRY

scheme, Jawahar Rojgar Yojana, etc. Helps entrepreneurs in obtaining licenses from the Electricity Board, Water Supply Board,

No Objection Certificates etc. Assist the entrepreneur to procure imported machinery and raw materials. Organizes marketing outlets in liaison with other government agencies.

Q. 4: Differentiate between Journal and Ledger

Difference Between Journal and Ledger Journal1. Journal is a book of accounting where daily records of business transactions are first recorded in a chronological order i.e. in the order of dates.2. It is known as the primary book of accounting or the book of original/first entry.3. It is prepared out of transaction proofs such as vouchers, receipts, bills, etc.4. A journal is not balanced.5. Procedure of recording in a journal is known as journalizing, which performed in the form of a Journal Entry.6. It may be subdivided into a cash book, a sales day book, sales return day book, purchases day book, purchases return day book, B/R Book, B/P Book, Petty Cash Book. Ledger1. A ledger is an accounting book in which all similar transactions related to a particular person or thing are maintained in a summarized form.2. It is known as the principal book of accounting or the book of final entry.3. It is prepared with the help of a journal itself, therefore, it is the immediate step after recording a journal.4. Except nominal accounts all ledger accounts are balanced to find the net result.5. Procedure of recording in a ledger is known as posting.6. It may be sub-divided into General ledger, debtors/sales ledger, creditors/purchases ledger.

Q. 5: Differentiate between public limited and private limited company.

Differences between Public and Private Ltd. Company

The difference between public and private company can be drawn clearly on the following grounds:

1. The public company refers to a company that is listed on a recognised stock exchange and traded publicly. A Private Ltd. the company is one that is not listed on a stock exchange and is held privately by the members.

2. There must be at least seven members to start a public company. As against this, the private company can be started with minimum two members.

3. The is no ceiling on the maximum number of members in a public company. Conversely, a private company can have a maximum of 200 members, subject to certain conditions.

4. A public company should have at least three directors whereas the Private Ltd. company can have a minimum of 2 directors.

5. It is compulsory to call a statutory general meeting of members, in the case of a public company, whereas there is no such compulsion in the case of a private company.

6. In a Public Ltd. Company, there must be at least five members, personally present at the Annual General Meeting (AGM) for constituting the requisite quorum. On the other hand, in the case of a Private Ltd. Company, that number is 2.

7. The issue of prospectus/statement instead of the prospectus is mandatory in case of a public company, but this is not the case with the private company.

8. To start a business, the public company needs a certificate of commencement of business after it is incorporated. In contrast, a private company can start its business just after receiving a certificate of incorporation.

9. The transferability of shares of a Pvt. Ltd. company is completely restricted. On the contrary, the shareholders of a public company can freely transfer their shares.

10.A public company can invite the general public for subscribing shares of the company. As opposed, a private company has no right to invite public for subscription.

Q. 5: Describe the powers of Factory Inspector.

Powers of Inspectors.—Subject to any rules made in this behalf, an Inspector may, within the local limits for which he is appointed,—

(a) enter, with such assistants, being persons in the service of the Government, or any local or other public authority, 1[or with an expert] as he thinks fit, any place which is used, or which he has reason to believe is used, as a factory;

(b) make examination of the premises, plant, machinery, article or substance;(c) inquire into any accident or dangerous occurrence, whether resulting in bodily injury,

disability or not, and take on the spot or otherwise statements of any person which he may consider necessary for such inquiry;

(d) require the production of any prescribed register or any other document relating to the factory;

(e) seize, or take copies of, any register, record or other document or any portion thereof as he may consider necessary in respect of any offence under this Act, which he has reason to believe, has been committed;

(f) direct the occupier that any premises or any part thereof, or anything lying therein, shall be left undisturbed (whether generally or in particular respects) for so long as is necessary for the purpose of any examination under clause (b);

(g) take measurements and photographs and make such recordings as he considers necessary for the purpose of any examination under clause (b), taking with him any necessary instrument or equipment;

(h) in case of any article or substance found in any premises, being an article or substance which appears to him as having caused or is likely to cause danger to the health or safety of the workers, direct it to be dismantled or subject it to any process or test (but not so as to damage or destroy it unless the same is, in the circumstances necessary, for carrying out the purposes of this Act), and take possession of any such article or substance or a part thereof, and detain it for so long as is necessary for such examination;

(i) Exercise such other powers as may be prescribed: Provided that no person shall be compelled under this section to answer any question or give any evidence tending to incriminate himself.

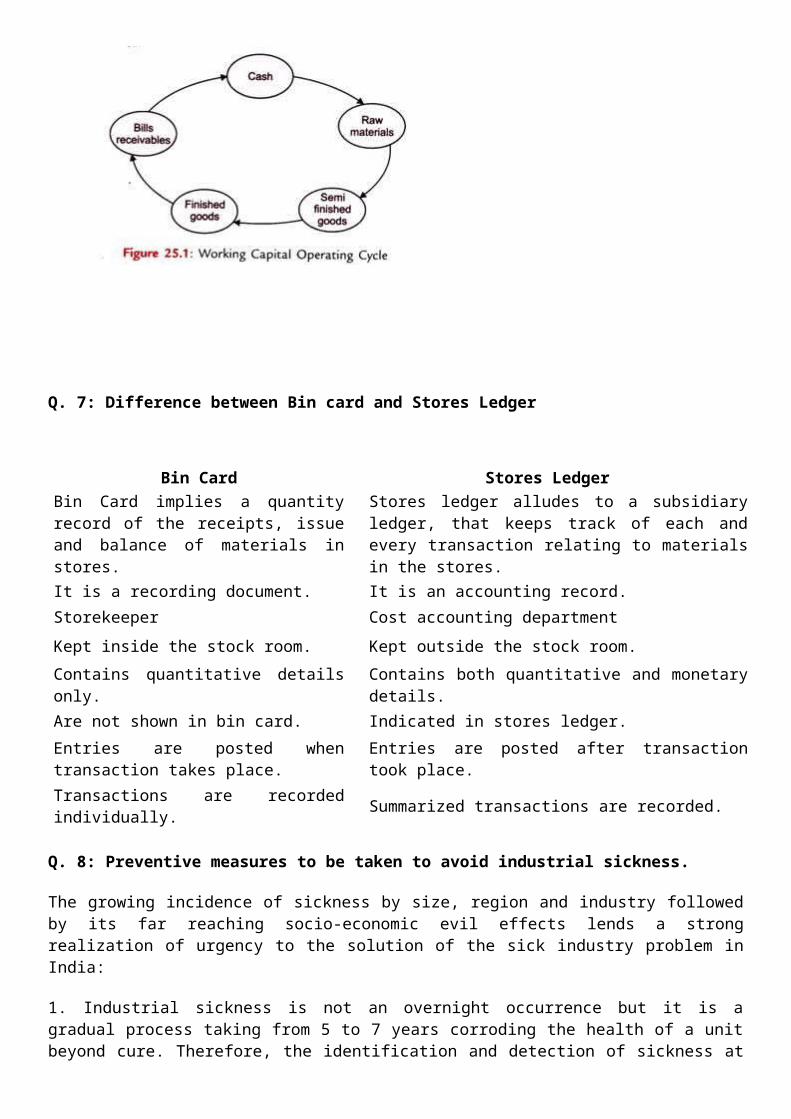

Q. 6: What is operating cycle?

The operating cycle is the average period of time required for a business to make an initial outlay of cash to produce goods, sell the goods, and receive cash from customers in exchange for the goods. This is useful for estimating the amount of working capital that a company will need in order to maintain or grow its business.

A company with an extremely short operating cycle requires less cash to maintain its operations, and so can still grow while selling at relatively small margins. Conversely, a business may have fat margins and yet still require additional financing to grow at even a modest pace, if its operating cycle is unusually long. If a company is a reseller, then the operating cycle does not include any time for production - it is simply the date from the initial cash outlay to the date of cash receipt from the customer.

The following are all factors that influence the duration of the operating cycle:

The payment terms extended to the company by its suppliers. Longer payment terms shorten the operating cycle, since the company can delay paying out cash.

The order fulfillment policy, since a higher assumed initial fulfillment rate increases the amount of inventory on hand, which increases the operating cycle.

The credit policy and related payment terms, since looser credit equates to a longer interval before customers pay, which extends the operating cycle.

Thus, several management decisions (or negotiated issues with business partners) can impact the operating cycle of a business. Ideally, the cycle should be kept as short as possible, so that the cash requirements of the business are reduced.

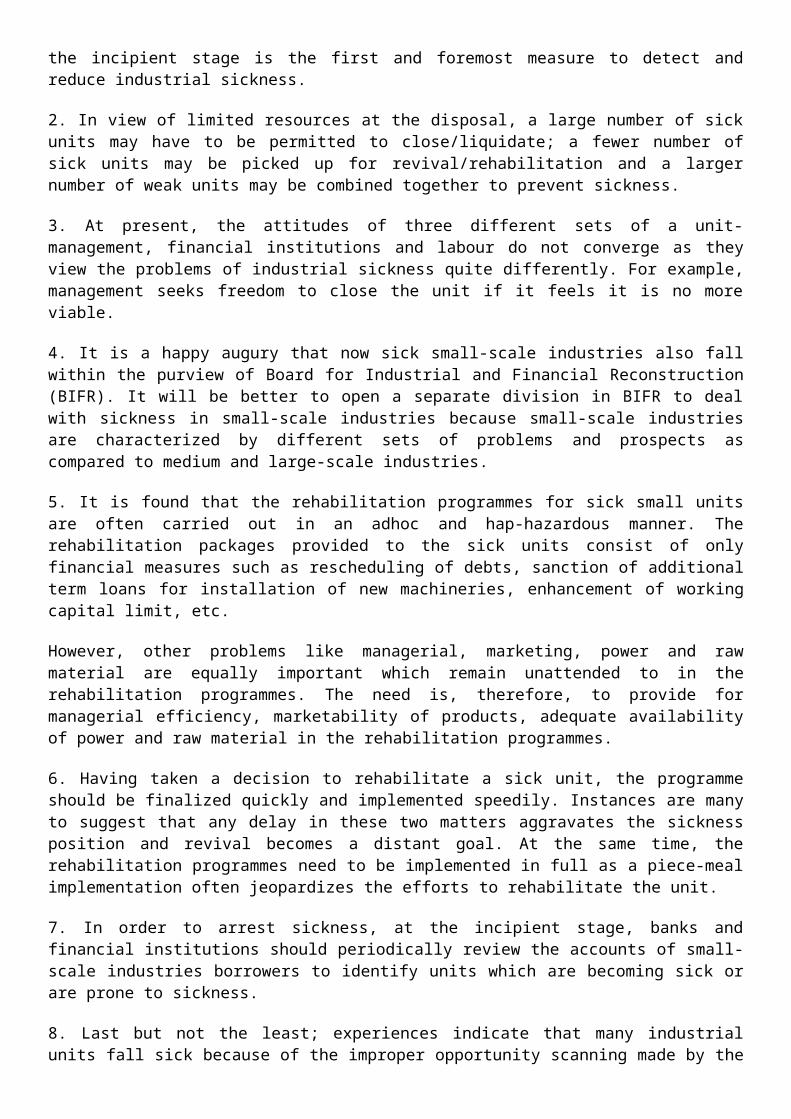

Q. 7: Difference between Bin card and Stores Ledger

Bin Card Stores LedgerBin Card implies a quantity record of the receipts, issue and balance of materials in stores.

Stores ledger alludes to a subsidiary ledger, that keeps track of each and every transaction relating to materials in the stores.

It is a recording document. It is an accounting record.

Bin Card Stores LedgerStorekeeper Cost accounting department

Kept inside the stock room. Kept outside the stock room.

Contains quantitative details only. Contains both quantitative and monetary details.

Are not shown in bin card. Indicated in stores ledger.

Entries are posted when transaction takes place. Entries are posted after transaction took place.

Transactions are recorded individually. Summarized transactions are recorded.

Q. 8: Preventive measures to be taken to avoid industrial sickness.

The growing incidence of sickness by size, region and industry followed by its far reaching socio-economic evil effects lends a strong realization of urgency to the solution of the sick industry problem in India:

1. Industrial sickness is not an overnight occurrence but it is a gradual process taking from 5 to 7 years corroding the health of a unit beyond cure. Therefore, the identification and detection of sickness at the incipient stage is the first and foremost measure to detect and reduce industrial sickness.

2. In view of limited resources at the disposal, a large number of sick units may have to be permitted to close/liquidate; a fewer number of sick units may be picked up for revival/rehabilitation and a larger number of weak units may be combined together to prevent sickness.

3. At present, the attitudes of three different sets of a unit-management, financial institutions and labour do not converge as they view the problems of industrial sickness quite differently. For example, management seeks freedom to close the unit if it feels it is no more viable.

4. It is a happy augury that now sick small-scale industries also fall within the purview of Board for Industrial and Financial Reconstruction (BIFR). It will be better to open a separate division in BIFR to deal with sickness in small-scale industries because small-scale industries are characterized by different sets of problems and prospects as compared to medium and large-scale industries.

5. It is found that the rehabilitation programmes for sick small units are often carried out in an adhoc and hap-hazardous manner. The rehabilitation packages provided to the sick units consist of only financial measures such as rescheduling of debts, sanction of additional term loans for installation of new machineries, enhancement of working capital limit, etc.

However, other problems like managerial, marketing, power and raw material are equally important which remain unattended to in the rehabilitation programmes. The need is, therefore, to provide for managerial efficiency, marketability of products, adequate availability of power and raw material in the rehabilitation programmes.

6. Having taken a decision to rehabilitate a sick unit, the programme should be finalized quickly and implemented speedily. Instances are many to suggest that any delay in these two matters aggravates the sickness position and revival becomes a distant goal. At the same time, the rehabilitation programmes need to be implemented in full as a piece-meal implementation often jeopardizes the efforts to rehabilitate the unit.

7. In order to arrest sickness, at the incipient stage, banks and financial institutions should periodically review the accounts of small-scale industries borrowers to identify units which are becoming sick or are prone to sickness.

8. Last but not the least; experiences indicate that many industrial units fall sick because of the improper opportunity scanning made by the entrepreneurs themselves. They start an industrial unit mainly to avail of subsidies, concessions and incentives from the Government. We know that a small-scale industry entrepreneur is like a one-man band. He/she may possess one or two or three ingredients/requisites but not the all.

GROUP- C

Q. 1: What is the Role of an Entrepreneur in Economic Development?

Entrepreneur: The people who create these businesses are called entrepreneurs. A person who sets up a business or businesses, taking on financial risks in the hope of profit.

Entrepreneurship is the process of designing, launching and running a new business, which is more often than not, initially a small business, offering a product, process or service for sale or hire. Entrepreneurship has been described as the "capacity and willingness to develop, organize and manage a business venture along with any of its risks in order to make a profit".

The entrepreneur who is a business leader looks for ideas and puts them into effect in fostering economic growth and development. Entrepreneurship is one of the most important input in the economic development of a country. The entrepreneur acts as a trigger head to give spark to economic activities by his entrepreneurial decisions. He plays a pivotal role not only in the development of industrial sector of a country but also in the development of farm and service sector. The major roles played by an entrepreneur in the economic development of an economy are discussed in a systematic and orderly manner as follows.

1. Promotes Capital Formation: Entrepreneurs promote capital formation by mobilizing the idle savings of public. They employ their own as well as borrowed resources for setting up their enterprises. Such type of entrepreneurial activities leads to value addition and creation of wealth, which is very essential for the industrial and economic development of the country.

2. Creates Large-Scale Employment Opportunities: Entrepreneurs provide immediate large-scale employment to the unemployed to the nations. With the setting up of more and more units by entrepreneurs, both on small and large-scale numerous job opportunities are created for others. In this way, entrepreneurs play an effective role in reducing the problem of unemployment.

3. Promotes Balanced Regional Development: Entrepreneurs help to remove regional disparities through setting up of industries in less developed and backward areas. The growth of industries and business in these areas lead to a large number of public benefits like road transport, health, education, entertainment, etc. Setting up of more industries leads to more development of backward regions and thereby promotes balanced regional development.

4. Reduces Concentration of Economic Power: Industrial development normally leads to concentration of economic power in the hands of a few individuals which results in the growth of monopolies. In order to redress this problem a large number of entrepreneurs need to be developed, which will help reduce the concentration of economic power amongst the population.

5. Increasing Gross National Product and Per Capita Income: Entrepreneurs are always on the lookout for opportunities. They explore and exploit opportunities,, encourage effective resource mobilization of capital and skill, bring in new products and services and develops markets for growth of the economy. In this way, they help increasing gross national product as well as per capita income of the people in a country.

6. Improvement in the Standard of Living: Entrepreneurs play a key role in increasing the standard of living of the people by adopting latest innovations in the production of wide variety of goods and services in large scale that too at a lower cost. This enables the people to avail better quality goods at lower prices which results in the improvement of their standard of living.

7. Promotes Country's Export Trade: Entrepreneurs help in promoting a country's export-trade, which is an important ingredient of economic development. They produce goods and

services in large scale for the purpose earning huge amount of foreign exchange from export in order to combat the import dues requirement.

8. Mobilization of Local Resources: Entrepreneurs help to mobilize and utilize local resources like small savings and talents of relatives and friends, which might otherwise remain idle and unutilized. Thus they help in effective utilization of resources.

9. Growth of infrastructure: The infrastructure development of any country determines the economic development of a country, Entrepreneurs by establishing their enterprises in rural and backward areas influence the government to develop the infrastructure of those areas.10. Facilitates Overall Development: Once an enterprise is established, the process of

industrialization is set in motion. This unit will generate demand for various types of units required by it and there will be so many other units which require the output of this unit. This leads to overall development of an area due to increase in demand and setting up of more and more units.

Q. 2: What are the importance of management and differentiate between management and administration?Importance of ManagementThe importance of management in business is universally accepted. It acts as a driving force in business. Modern business is highly competitive and need efficient and capable management. It is through management that business activities are organized and conducted efficiently and objectives are achieved.

The following points will suggest the importance of management

1) Optimum use of resources: management facilities optimum utilization of available human and physical resources, which leads to progress and prosperity of a business enterprise. Even wastage of all types are eliminated or minimized.

2) Competitive strength: Management develops competitive strength in an enterprise. This enables an enterprise to develop and expand its assets and profits.

3) Cordial industrial relations: Management develops cordial industrial relation, ensures better life and welfare to employees and raises their morale through suitable incentives.

4) Motivates employees: It motivates employees to take more interest and initiative in the work assigned and contributes for raising productivity and profitability of the enterprise.

5) New techniques: Management facilities the introduction of new machines and new methods in the conduct of business activities. It also brings useful technologies developments and innovation in the management of business activities.

6) Effective management: Society gets the benefits of efficient management in terms of industrial development, justice to different social groups, consumer’s satisfaction and welfare and proper discharge of social responsibilities.

7) Expansion of business: Expansion growth and diversification of a business unit are possible through efficient management. It creates good corporate image to a business enterprise.

8) Team spirit: Management develops team spirit and raises overall efficiency of a business enterprise.

10) Effective use of managers: Management ensures effective use of managers so that the benefits of their experience, skills and maturity are available to enterprise.

11) Smooth functioning: Management ensures smooth, orderly and continuous functioning of an enterprise over a long period. It also raises the efficiency, productivity and profitability of an enterprise.

12) Reduces turnover and absenteeism: It reduces Labour turnover and absenteeism and ensures continuity in the business activities and operations.

Management is not only practiced in organization and business entities but management plays an important role in our daily lives and is practiced by every individual is some or the other way.

Differences between Management and Administration

The major differences between management and administration are given below:

1. Management is a systematic way of managing people and things within the organization. The administration is defined as an act of administering the whole organization by a group of people.

2. Management is an activity of business and functional level, whereas Administration is a high-level activity.

3. While management focuses on policy implementation, policy formulation is performed by the administration.

4. Functions of administration include legislation and determination. Conversely, functions of management are executive and governing.

5. Administration takes all the important decisions of the organization while management makes decisions under the boundaries set by the administration.

6. A group of persons, who are employees of the organization is collectively known as management. On the other hand, administration represents the owners of the organization.

7. Management can be seen in the profit making organization like business enterprises. Conversely, the Administration is found in government and military offices, clubs, hospitals, religious organizations and all the non-profit making enterprises.

8. Management is all about plans and actions, but the administration is concerned with framing policies and setting objectives.

9. Management plays an executive role in the organization. Unlike administration, whose role is decisive in nature.

10.The manager looks after the management of the organization, whereas administrator is responsible for the administration of the organization.

Management focuses on managing people and their work. On the other hand, administration focuses on making the best possible utilization of the organization’s

Q. 3: Define cost and elements of cost.

Cost - What is cost?In business and accounting, cost is the monetary value that a company has spent in order to produce something

Cost denotes the amount of money that a company spends on the creation or production of goods or services. It does not include the mark-up for profit.

From a seller’s point of view, cost is the amount of money that is spent to produce a good or product. If a producer were to sell his products at the production price, his costs and income would break even, meaning that he would not lose money on the sales. However, he would not make a profit.

From a buyer’s point of view the cost of a product is also known as the price. This is the amount that the seller charges for a product, and it includes both the production cost and the mark-up, which is added by the seller in order to make a profit.

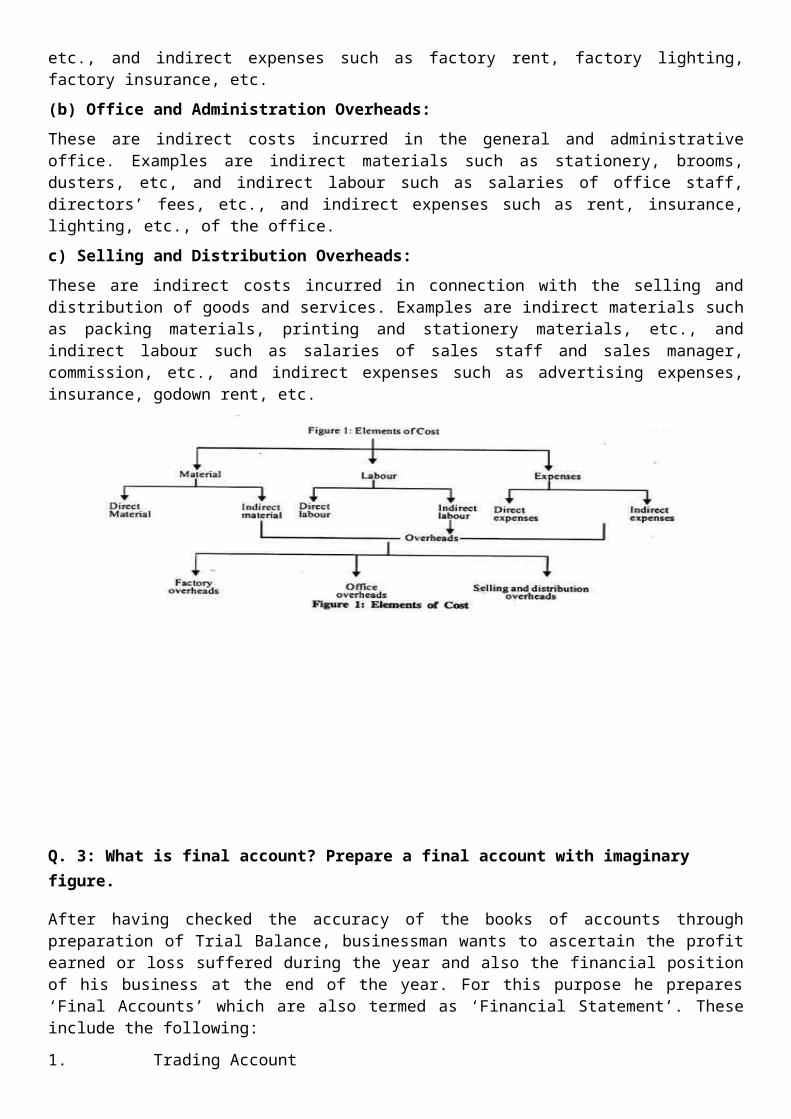

Elements of Cost

There are three important elements of cost, i.e., (1) Material, (2) Labour, and (3) Expenses.1. Material:Material may be classified into direct material and indirect material.

Direct Material: CIMA defines material cost as “the cost of commodities supplied to an undertaking.” All materials, which becomes an integral part of the finished product and which can be conveniently allocated to specific physical units is termed as direct material.

Some of the examples are all material components or spare parts specifically purchased, produced or supplied from stores, primary packing materials, and purchased or partly produced components. It is also called as process material or production material.

Indirect Material:All material, which is used for secondary purposes and cannot be allocated conveniently to specified physical units, is called as indirect material. A few examples are consumable stores, oil and waste, printing and stationery material, and etc. Indirect material may be used at the factory, office or selling and distribution divisions.

2. Labour:Human effort required to convert materials into finished products is termed as labour. It may be classified into direct labour and indirect labour.

Direct Labour:Labour, which plays an active and direct part in the production of a particular product, is termed as direct labour. CIMA defines labour cost as “the cost of remuneration (wages, salaries, commission, bonus, etc.) of the employees of an undertaking.” Direct labour cost can be conveniently and specifically charged to specific products.

Indirect labour: It is employed to carry out tasks incidental to goods produced or services rendered. Indirect labour cost cannot be practically traced to specific units of output. A few examples indirect labour costs are wages of storekeeper, salaries of office staff and salesmen, directors’ fees, etc. It may be incurred in the factory, office, and selling and distribution divisions.

3. Expenses: CIMA defines expenses as “the cost of services provided to an undertaking and the notional cost of the use of owned assets.” It may be classified into direct expenses and indirect expenses.

Direct Expenses: These are expenses, which can be directly allocated to a particular job, product or unit of service; They are also called as ‘chargeable expenses.’ Examples of such expenses are hire charges paid to some special machinery required for a particular contract, cost of designs or mould incurred in toy manufacturing, cost of blocks needed in book publishing, etc.

Indirect Expenses:These are expenses, which cannot be conveniently and directly allocated to a particular job, product or unit of service. They are incurred in common and can be apportioned to various cost centers or cost units proportionately on some basis. Examples of such expenses are factory rent, lighting, insurance, office and administration expenses, selling and distribution expenses, etc.

Overheads:The aggregate of indirect material cost, indirect labour cost, and indirect expenses is termed as overheads. Thus all indirect costs are overheads.

They may be classified broadly into types:

(a) Factory or Works Overheads: These are indirect costs incurred inside a factory or works. Examples are factory supplies such as oil, consumable stores, lubricants, indirect labour such as factory manager’s salary, timekeeper’s salary, etc., and indirect expenses such as factory rent, factory lighting, factory insurance, etc.

(b) Office and Administration Overheads: These are indirect costs incurred in the general and administrative office. Examples are indirect materials such as stationery, brooms, dusters, etc, and indirect labour such as salaries of office staff, directors’ fees, etc., and indirect expenses such as rent, insurance, lighting, etc., of the office.

c) Selling and Distribution Overheads: These are indirect costs incurred in connection with the selling and distribution of goods and services. Examples are indirect materials such as packing materials, printing and stationery materials, etc., and indirect labour such as salaries of sales staff and sales manager, commission, etc., and indirect expenses such as advertising expenses, insurance, godown rent, etc.

Q. 3: What is final account? Prepare a final account with imaginary figure.

After having checked the accuracy of the books of accounts through preparation of Trial Balance, businessman wants to ascertain the profit earned or loss suffered during the year and also the financial position of his business at the end of the year. For this purpose he prepares ‘Final Accounts’ which are also termed as ‘Financial Statement’. These include the following:

1. Trading Account

2. Profit and Loss Account

3. Balance Sheet

Trading Account

Trading account is prepared for calculating the gross profit or gross loss arising or incurred as a result of the trading activities of a business. In other worlds, it is prepared to show the result of manufacturing, buying and selling of goods. If the amount of sales exceeds the amount of

purchases and the expenses directly connected with such purchases, the difference is termed as gross profit. On the contrary, if the purchases, and direct expenses exceed the sales, the difference is called gross loss. A Trading Account records the amount of purchases of goods and also the expenses which are incurred in bringing that commodity to a saleable state. IN other words, all expenses which relate to either purchase of raw material for manufacturing of goods are recorded in the Trading Account. All such expenses are called ‘Direct Expenses’.

Form of Trading Account

TRADING A/C

(for the year ended……………..)

Dr. Cr.

Particular Amount Particulars Amount

Rs. Rs.

To Opening Stock

To Purchases

Less: Purchase Returns

or

Returns outward

To Wages

To Wages & Salaries

To Direct Expenses

To Carriage, or

To Carriage inwards, or

To Carriage on Purchase

To Gas, Fuel and Power

To Freight, octroi and cartage

To Manufacturing Expenses, or

Productive Expenses

To Factory Expenses, such as:

Factory Lighting

Factory Rent etc.

To Dock Charges and Clearing charges

To Import Duty or Custom duty

By Sales

Less: Sales Returns

or

Returns inwards

By Closing Stock

By Gross loss

(if any) transferred to Profit and Loss A/c

(Balancing Figure)

To Royalty

To Gross Profit

Transferred to P & L A/c

(Balancing Figures

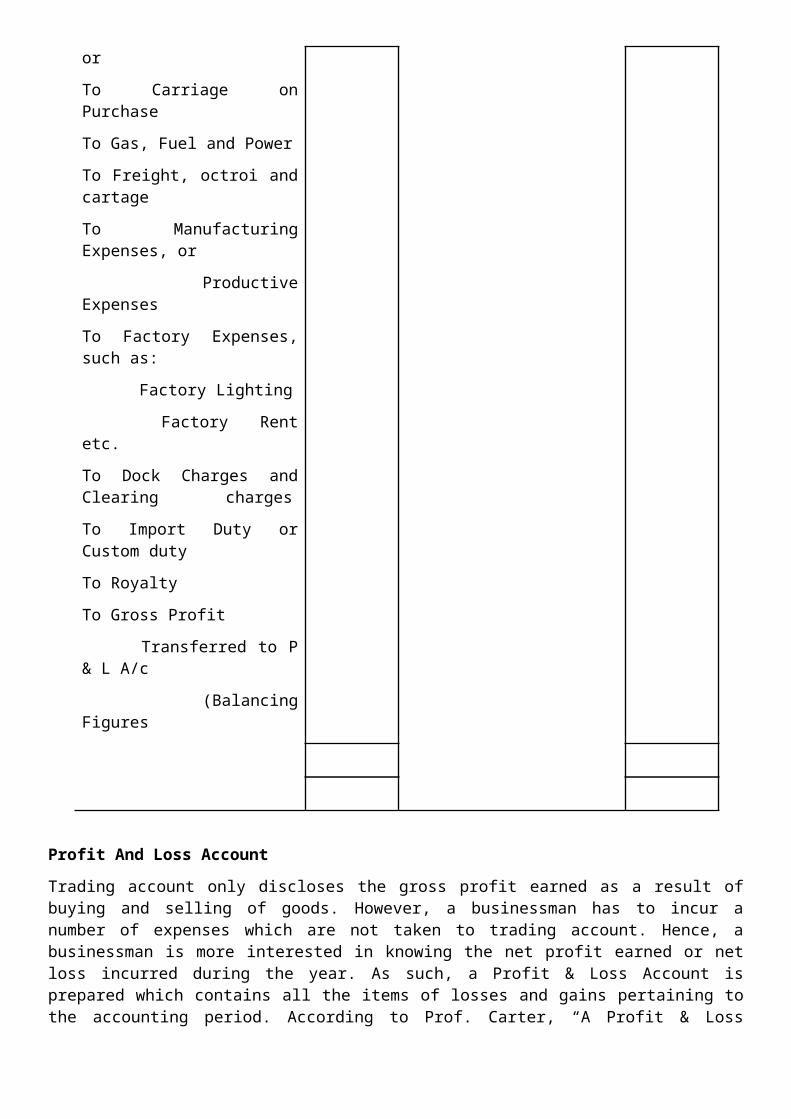

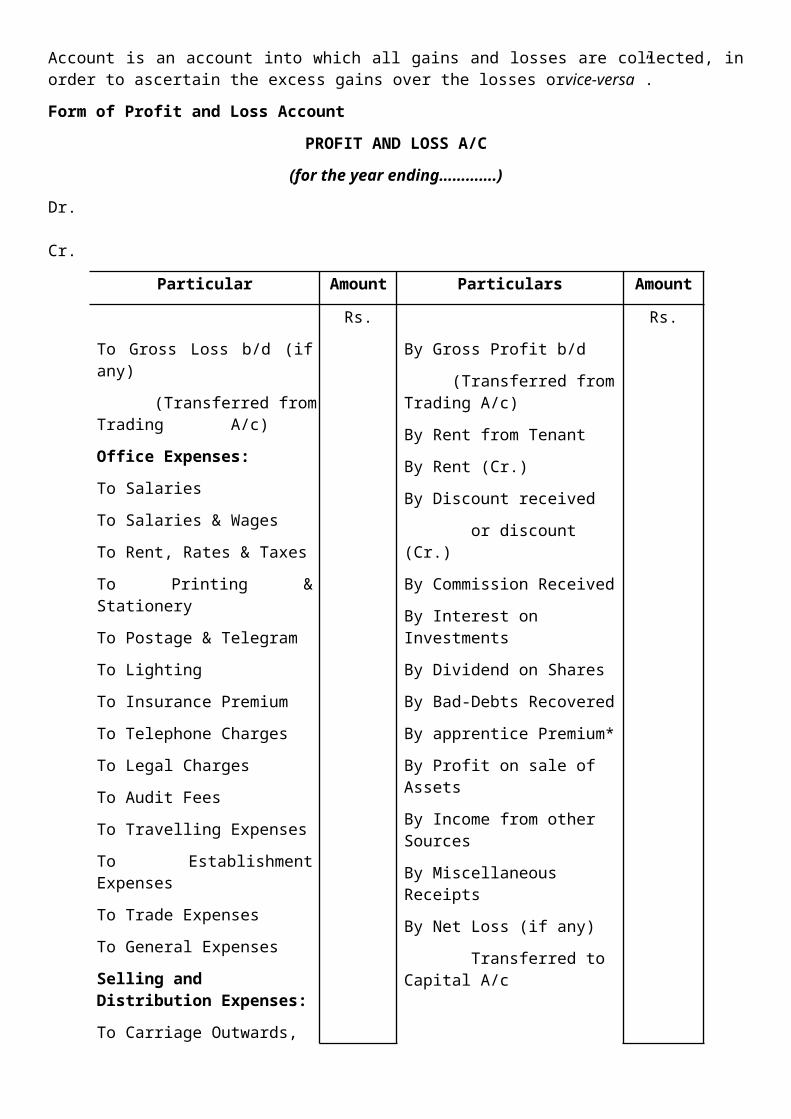

Profit And Loss Account

Trading account only discloses the gross profit earned as a result of buying and selling of goods. However, a businessman has to incur a number of expenses which are not taken to trading account. Hence, a businessman is more interested in knowing the net profit earned or net loss incurred during the year. As such, a Profit & Loss Account is prepared which contains all the items of losses and gains pertaining to the accounting period. According to Prof. Carter, “A Profit & Loss Account is an account into which all gains and losses are collected, in order to ascertain the excess gains over the losses orvice-versa”.

Form of Profit and Loss Account

PROFIT AND LOSS A/C

(for the year ending………….)

Dr. Cr.

Particular Amount Particulars Amount

Rs. Rs.

To Gross Loss b/d (if any)

(Transferred from Trading A/c)

Office Expenses:

To Salaries

To Salaries & Wages

To Rent, Rates & Taxes

To Printing & Stationery

To Postage & Telegram

To Lighting

To Insurance Premium

To Telephone Charges

To Legal Charges

To Audit Fees

By Gross Profit b/d

(Transferred from Trading A/c)

By Rent from Tenant

By Rent (Cr.)

By Discount received

or discount (Cr.)

By Commission Received

By Interest on Investments

By Dividend on Shares

By Bad-Debts Recovered

By apprentice Premium*

By Profit on sale of Assets

By Income from other

To Travelling Expenses

To Establishment Expenses

To Trade Expenses

To General Expenses

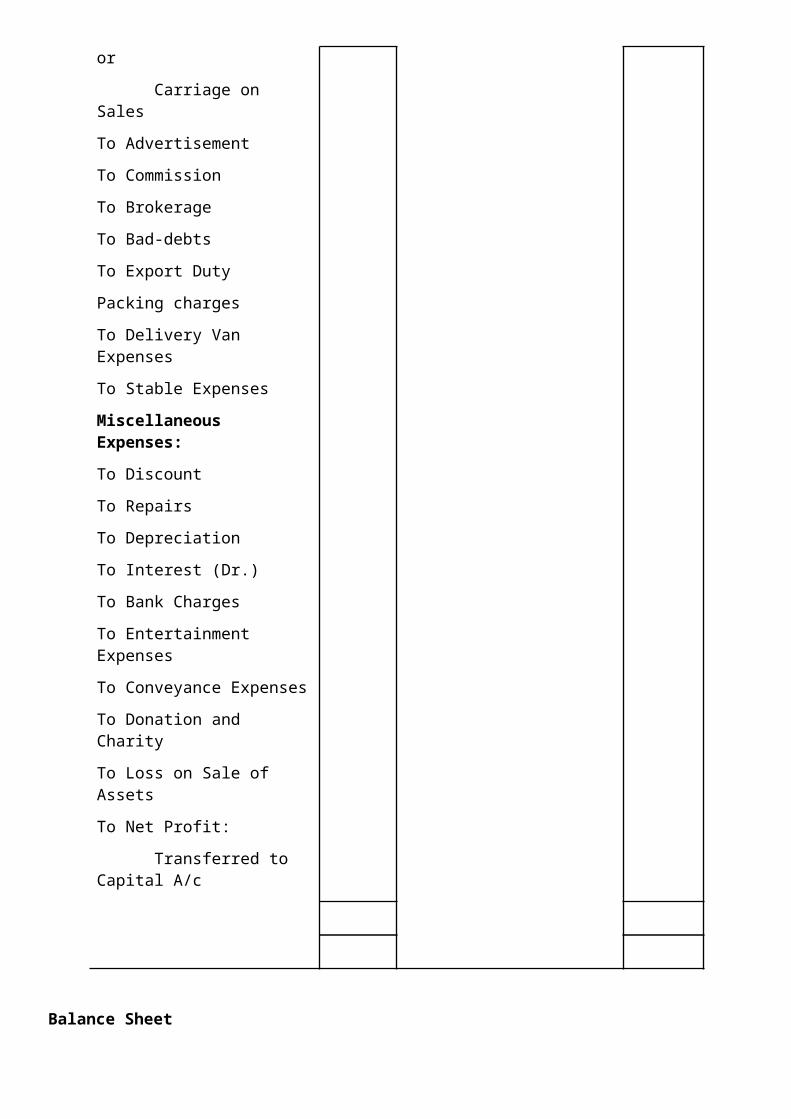

Selling and Distribution Expenses:

To Carriage Outwards, or

Carriage on Sales

To Advertisement

To Commission

To Brokerage

To Bad-debts

To Export Duty

Packing charges

To Delivery Van Expenses

To Stable Expenses

Miscellaneous Expenses:

To Discount

To Repairs

To Depreciation

To Interest (Dr.)

To Bank Charges

To Entertainment Expenses

To Conveyance Expenses

To Donation and Charity

To Loss on Sale of Assets

To Net Profit:

Transferred to Capital A/c

Sources

By Miscellaneous Receipts

By Net Loss (if any)

Transferred to Capital A/c

Balance Sheet

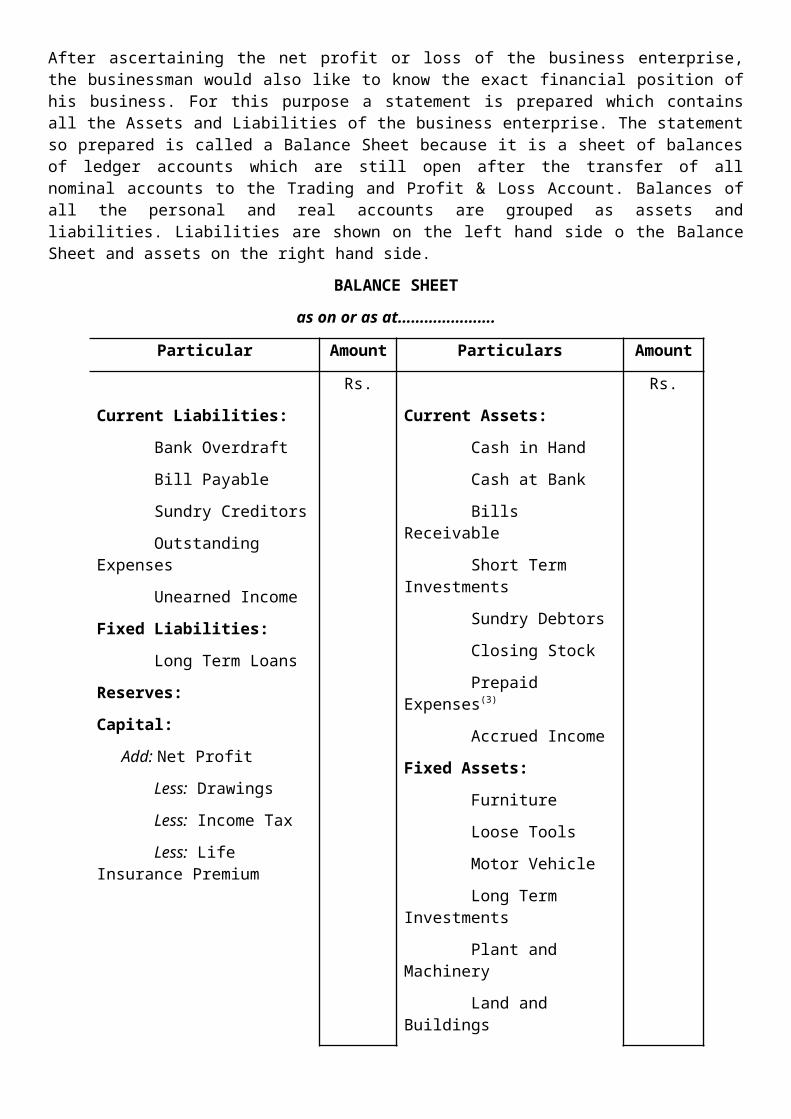

After ascertaining the net profit or loss of the business enterprise, the businessman would also like to know the exact financial position of his business. For this purpose a statement is prepared

which contains all the Assets and Liabilities of the business enterprise. The statement so prepared is called a Balance Sheet because it is a sheet of balances of ledger accounts which are still open after the transfer of all nominal accounts to the Trading and Profit & Loss Account. Balances of all the personal and real accounts are grouped as assets and liabilities. Liabilities are shown on the left hand side o the Balance Sheet and assets on the right hand side.

BALANCE SHEET

as on or as at………………….

Particular Amount Particulars Amount

Rs. Rs.

Current Liabilities:

Bank Overdraft

Bill Payable

Sundry Creditors

Outstanding Expenses

Unearned Income

Fixed Liabilities:

Long Term Loans

Reserves:

Capital:

Add: Net Profit

Less: Drawings

Less: Income Tax

Less: Life Insurance Premium

Current Assets:

Cash in Hand

Cash at Bank

Bills Receivable

Short Term Investments

Sundry Debtors

Closing Stock

Prepaid Expenses(3)

Accrued Income

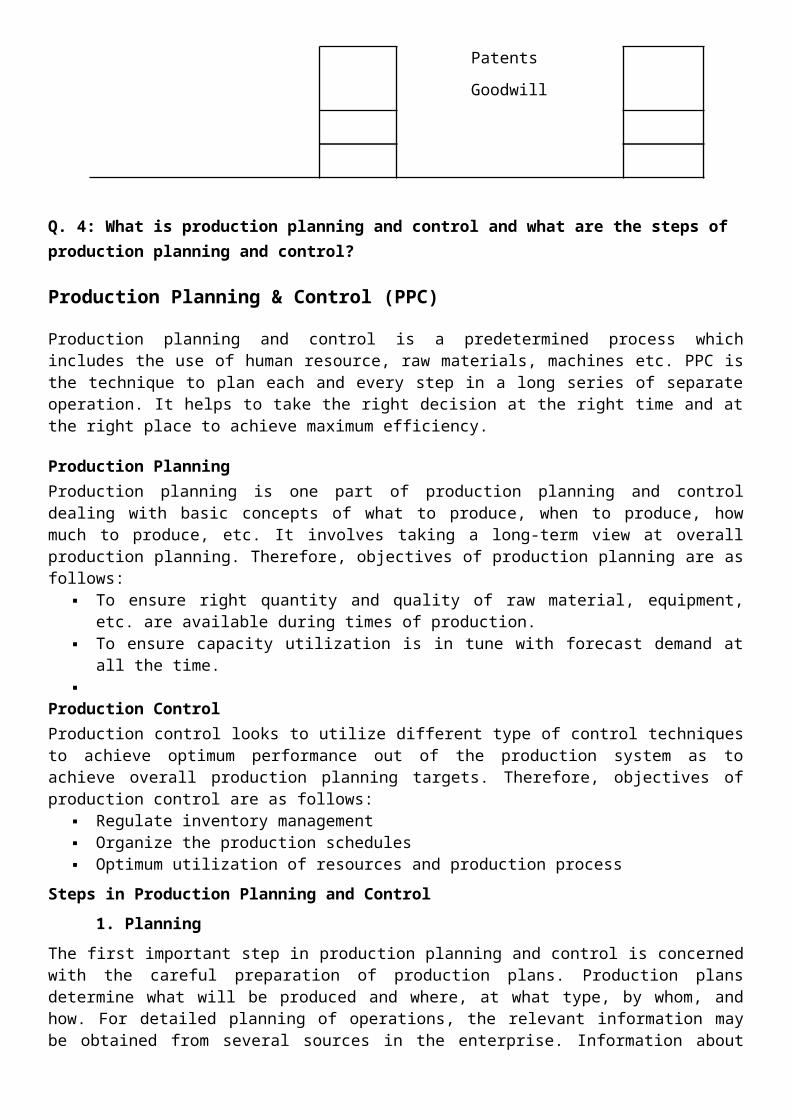

Fixed Assets:

Furniture

Loose Tools

Motor Vehicle

Long Term Investments

Plant and Machinery

Land and Buildings

Patents

Goodwill

Q. 4: What is production planning and control and what are the steps of production planning and control?

Production Planning & Control (PPC)

Production planning and control is a predetermined process which includes the use of human resource, raw materials, machines etc. PPC is the technique to plan each and every step in a long

series of separate operation. It helps to take the right decision at the right time and at the right place to achieve maximum efficiency.

Production PlanningProduction planning is one part of production planning and control dealing with basic concepts of what to produce, when to produce, how much to produce, etc. It involves taking a long-term view at overall production planning. Therefore, objectives of production planning are as follows:

To ensure right quantity and quality of raw material, equipment, etc. are available during times of production.

To ensure capacity utilization is in tune with forecast demand at all the time.

Production ControlProduction control looks to utilize different type of control techniques to achieve optimum performance out of the production system as to achieve overall production planning targets. Therefore, objectives of production control are as follows:

Regulate inventory management Organize the production schedules Optimum utilization of resources and production process

Steps in Production Planning and Control1. Planning

The first important step in production planning and control is concerned with the careful preparation of production plans. Production plans determine what will be produced and where, at what type, by whom, and how. For detailed planning of operations, the relevant information may be obtained from several sources in the enterprise. Information about quantity and quality of products to be manufactured may be obtained from customers’ orders and the sales budget, and information about production facilities may be obtained from the management and the engineering department. Thus, the planning function formulates production plans, and translates them into requirements for men, machinery and materials.

Whatever be the planning period, production planning helps in avoiding randomness in production, providing regular and steady flow of production activities, utilizing production facilities to its maximum for minimizing operating costs and meeting delivery schedules; coordinating various departments of the enterprise for maintaining proper balance of activities, and above all, providing the basis for control in the enterprise.

2. Routing The next important function of production planning and control is routing which involves the determination of the path (i.e. route) of movement of raw materials through various machines and operations in the factory. “Routing includes the planning of where and by whom work shall be done, the determination of the path that work shall follow, and the necessary sequence of operations”. To find this path, emphasis is placed on determining operating data, which usually includes planning of ‘where’ and ‘by whom’ work should be done, the determinations of the path that work shall follow, and the necessary sequence of operations. These operating data are contained in the standard process sheet which helps in making out a routing in the standard process sheet which helps in making out a routing chart showing the sequence of operations and the machines to be used. If the machine loan chart indicates the non-availability of certain machines, alternate routing may also be included on the routing chart. The most efficient routing may have to be compromised with the availability of the machines at a particular time. In other words, “routing establishes the operations, their path and sequence, and the proper class of machines and personnel required for these operations.”

From the above, it can be inferred that routing is one of the highly essential elements and prime considerations of production control because many production control functions are closely related processes and are dependent on routing functions. Thus, it is essential to solve the different

problems concerning: appropriate personnel; full utilization of machines; and determining with precise degree the time required in the production process.

4. SchedulingScheduling is planning the time element of production – i.e. prior determination of “when work is to be done”. It consists of the starting and completion times for the various operations to be performed. In other words, scheduling function determines when an operation is to be performed, or when work is to be completed, the difference lies in the details of the scheduling procedure. To work out effectively, the scheduling, as a part of production control function, determines the time when each operation called for on the route sheet is to be done on the specified machine in order to meet the desired delivery dates. Good control function directs not only the time that each particular operation should start but also indicates the progress of each manufacturing part, the amount of work ahead of each machine, and the availability of each machine for the assignment of new work.

Schedules are of two types: Master schedule and Detailed schedule. Activities, if recorded on plant-wise basis, would be preparing master schedule, while mere detailed schedules are employed to plan the manufacturing and assembly operations required for each product.

5. DispatchingDispatching is the part of production control that translates the paper – work into actual production. It is the group that coordinates and translates planning into actual production. Dispatching function proceeds in accordance with the details worked out under routing and scheduling functions. As such, dispatching sees to it that the material is moved to the correct work place, that tools are ready at the correct place for the particular operations, that the work is moving according to routing instructions. Dispatching carries out the physical work as suggested by scheduling. Thus, dispatching implies the issuance or work orders. These work orders represent authority to produce. These orders contain the following information:

The name of the product;

The name of the part to be produced, sub-assembly or final assembly;

The order number;

The quantity to be produced;

Descriptions and numbers of the operations required and their sequence,

The departments involved in each operation

The tools required for particular operation; and

Machines involved in each operation and starting dates for the operations.

6. ExpeditingExpedition or follow-up is the last stage in the process of production control. This function is designed to keep track of the work effort. The aim is to ensure that what is intended and planned is being implemented. “Expediting consists in reporting production data and investigating variances from predetermined time schedules. The main idea behind expedition is to see that promise is backed up by performance”.

Q. 5: What is advertising and what are the media of advertising?

AdvertisingAdvertising is nothing but a paid form of non-personal presentation or promotion of ideas, goods or services by an identified sponsor with a view to disseminate information concerning an idea, product or service. The message which is presented or disseminated is called advertisement. In

the present day marketing activities hardly is there any business in the modern world which does not advertise. However, the form of advertisement differs from business to business.

According to Wheeler, “Advertising is any form of paid non-personal presentation of ideas, goods or services for the purpose of inducting people to buy.”

Various media for AdvertisingAdvertising media are the means to transmit the message of the advertiser to the desired class of people. Channels or vehicle by which an advertising message is brought to the notice of the prospective buyer. There is no dearth of media today. It may be direct or indirect. Direct method of advertising refers to such methods used by the advertiser with which he could establish a direct contact with the prospective hand involve the use of a hired agency for spreading the information. Most of the media are indirect in nature, e.g., press publicity, cinema, etc. The various media that are commonly used are being explained here.

Indoor Advertising:When advertising is made through newspapers, magazines, radio, T.V. programmes or cinema programme in Video etc., so that people can get the message at home, it is known as Indoor advertisement. People read or listen to the advertisement when they are indoor. People can be benefited by indoor advertising as they can read the newspapers or see television programme when they are having leisure time.

Press Media:- Advertisement in newspapers, magazines, journals etc., can be called as press advertising. It is the most popular and widely used means of advertising. It is the most economical media of advertisement. Growth of literacy and development of press also pave the way for these press media.

Radio: Radio is the quickest medium of advertising when compared to newspapers or magazines. Sound moves faster than other media. It is a popular medium of advertising for a commercial firm. Radio makes its appeal to the car. Commercial radio broadcasting has become popular and is widely used in all countries.

Television: It is of recent origin. It is more popular in advanced countries especially in the U.S.A. In Delhi the first television centre was set up in 1962, followed by Bombay, Calcutta, Lucknow, Madras etc. Television advertising is the latest medium of mass communication and is widely used for advertisement. It is an audio-visual medium, because one can see and hear. The maximum number of television sets are in Maharashtra followed by Delhi.

Film: The effects of television medium and film medium are the same. Film advertising is also advantageously used by advertiser. Cinema is an audio-visual medium of communication and offers opportunities to advertisers for screening commercial films and slides. In India, there are about 7000 cinema houses and 3,500 touring cinemas (approximate). The maximum number of cinema houses is in Andhra Pradesh, followed by Tamil Nadu, Maharashtra, Uttar Pradesh and Kerala. The maximum number of touring cinemas is in Tamil Nadu, followed by Andhra Pradesh and Kerala. For almost all consumer goods manufacturers are advantageously using this medium.

Outdoor Advertising: Outdoor advertising passes the message to those people who are moving audience. Generally, almost all the people go out on some purpose or other-office, walk, sightseeing, journey, park visit etc. This outdoor advertising has the best effects of advertising. Before discussing the types of outdoor advertising, let us discuss the merits and demerits of this advertising

Types of Outdoor Advertising: 1. Mural Advertising (Posters): At present this is a common form of advertising. The posters are made in attractive colours in brief and printed. The poster is a sheet of paper. The matter is depicted on it. Then the prepared posters are pasted on walls or boards. Film showers use this

medium for advertising and the posters are pasted in such a manner that they are projected to the people at bus stand, railway station, marketplace, parks, libraries, and crowded areas.

The cost is less. It is flexible. It has a short life, because in cities, posters pasted in the morning, may disappear in the evening by pasting new papers on them. In certain places like cities, the space has to be hired for pasting posters.

2. Advertising Boards: These are also posters, but have better status than ordinary posters. The boards are fixed at the areas where people frequently assemble. Such boards are fixed at decent and neat places. They appear more attractive than posters.

3. Vehicular Advertising: This moving advertisement finds place on vehicles-buses, trains etc. The vehicle passes through many places and many people happen to see it.

4. Painted Display: It is an artist’s work. This display is large in size. It is visible from a distance. It finds place at crossings, compound walls or erected structures built of poles or pillars.

5. Travelling Display: These are the advertisements as posters, small in size, written beautifully and placed inside trains, buses, tramcars, vans etc. The travelling people, in these vehicles, repeatedly notice it and keep it in their memory.

6. Electric Display: Electric display is more attractive. It is popular now-a-days. The beauty and attractiveness depend upon the skill of electrical engineers. Another method is that of running bulbs strap and it looks like moving. Such arrangements are common in big cities. During night time or in dark background, it is more bright and alluring. It is costly.

7. Sky Advertising: Sky advertising and sky writing have become popular. Big balloons with message written on them or attached to them are allowed to float in the air. Big kites containing advertisement may be floated in the open air. Sky writing is a kind of advertising played by the pilot, through aero plane, either by forming smoke or by illumination.

Karnataka State Lottery Agencies have adopted big balloons for the sake of publicity. The inscription or writing on the balloon will speak about the products. Almost all the circus companies use the high powered revolving search lights to attract the attention of the public. All these types of advertisements can be seen from a long distance.

8. Sandwich-men: Sandwich-men are hired by the advertisers. They move or walk down through busy roads and streets. They dress in a peculiar way with fancy clothes. They carry posters of the product of the advertisers. They utter slogans. They create certain type of musical sounds. This sort of advertisement has short life, but is effective. Cinema theatres usually adopt this method of publicity.

9. Handbills (Leaflets): Handbills are common and too cheap. Handbills, which are in the form of leaflets are distributed among the people through hired men. Sometimes, music bands are also played along with distribution of leaflets. Only interested persons may go through the handbills. The handbill distributor distributes copies of the handbill to all, who pass nearby. An uninterested person receives it by one hand and throws it away by the other hand. This type of advertising is suitable for small business people.

Direct Advertising: The object of direct advertising is to create a direct contact with the customers. The advertiser can keep a close touch with the customers or the public, who are supposed to have interest in his product. He contacts them and keeps a close touch with them through mail advertising. It is a common method. It is also known as direct mail advertising.

1. Sales Letters: Sales letters are persuasive in nature. Many firms think every letter that goes out from the firm is a sales letter, because every business letter aims at an opportunity to sell the firm’s product or earn a goodwill for the firm. To a certain extent, the salesman is substituted by the sales letters because the purpose of salesman and sales letters is the same, i.e., push up the sales. Drafting a sales letter is in the form of advertising, to create an interest in the mind of the reader. Sales letters are cheaper and convenient.

2. Circulars: It carries communication to a number of addresses. The circular letter contains information about the products. It is generally cyclostyled or is in the printed form. It carries less attention than the sales letter. The merits and demerits are similar to sales letters.

3. Booklets and Catalogues: These contain more particulars of the product and the firm. Booklets are in the form of a small book. Catalogue contains more information than a booklet. Fundamentally both are similar. Catalogue will be more attractive and it contains illustration of products with details and price lists.

4. Folders: These are letters or cards containing details of the products. They contain illustration. Folders can be sent without an envelop. The folders can be folded conveniently, as they are made of thick paper. These are generally adopted by publishers, medical firms, industrialists etc. The folders must be attractive.

5. Package Inserts: This is a system through which leaflets about the products are inserted in the packets of products. The package insert may contain details of the same product or other products of the same firm. Thus, it is an advertisement.

6. Store Publication: This is also known as ‘house organs’. Certain firms may publish periodicals or magazines which contain information about the development of the firm. These will be distributed to wholesalers, retailers etc., free of cost. This will also explain the product in detail.

Promotional Advertising: The object of promotional advertising is to increase the sales. These are also known as ‘display advertising’. By this, we mean that the products are systematically kept in a place so as to attract the attention and notice of the lookers. It demonstrates the products.

The following are the important types: 1. Window Display (outside display): Window display is the medium used to attract the public by creating an interest in them. The products dealt in by the firm are placed at the front of the firm, trying to create an arousing interest in the minds of them. A good arranged system of window display naturally increases the sales. It gives a memorizing attitude to the public, even if one is not entering the shop at the sight of the display.

2. Interior Display: In large-scale organisations, they use this type of display. Glass-doored cupboards, sunglass show-cases are used for internal display. Window display is arranged outside, but interior display is inside the shop. The related articles are displayed within easy reach. It is easy for the buyers to get the products needed by them.

3. Show-room: Consumers always insist on prior inspection of the products, which they aim to purchase. Therefore sellers must provide facility for their inspection. Buyers are not satisfied with mere publicity. They want to have a close look at the product. In a show-room, not only the needed products are kept, but different products also.

And this creates an inward interest on other products, when one makes a purchase of the needed item. In the show-room, salesmen are there to explain about the prospects. It must be highly decorated and must have good lighting arrangement with good atmosphere. For instance, textile mills, and firms producing furniture, refrigerators, television sets, radio sets and other luxurious items must have generally show-rooms.

4. Exhibition: It is known to everyone. This is also known as trade shows. The idea behind the exhibition is to promote sales of the goods exhibited. All, big or small, manufacturers reserve stalls in the exhibition area to exhibit their products. Exhibitions are popular and it is the place where competitors meet. They are held on local, national or international level.

Q. 6: What are the Reasons and Causes of Industrial Sickness in India

The various external and internal causes of Internal Sickness in India have been discussed below:

1. External causes

Recession in the Market: Sometimes recession hits the whole industry as a result of which individual units are unable to sell their products. The availability of credit is also restricted during such times which jeopardize the production activities of such units. Hence, the work of these units comes to a standstill.

Decline in Market Demand for the product: A product may reach a stage of maturity and ultimately a stage of decline. This happens when new better products invade the market and make the old product redundant.

Excessive competition in the Market: Excessive competition in the market will justify the survival of only the fittest firm. The high cost units over time will become weak and fall sick.

Erratic supply of Inputs: Erratic and insufficient supply of inputs like raw-materials, power, skilled manpower, finance, credit and transport at reasonable prices could cause disturbance in the production schedule and ultimately result in sickness of the firm.

Government Policy: Excessive govt., control and restrictions on capacity utilisation, location, product mix, product quality, prices, distribution etc. come in the way of smooth functioning of the firms and often result in sickness of the firm. Further, frequent changes in government policy relating to industrial licensing, import, exports, taxation, credit can make healthy units sick overnight.

Unforeseen circumstances: Natural calamities such as droughts, floods earthquakes, accidents and wars etc. may turn some units sick and enviable.

2. Internal Causes

Faulty planning: At the planning stage itself, weak foundations may be laid, which may ultimately result in downfall of the unit.

Incompetent Entrepreneurs: Many persons starting new business lack technical knowledge of the product they want to manufacture. It is the normal case with small scale entrepreneurs. They sometimes plough into production activity, without bothering to find out the marketing potential of their product or sometimes they start production without properly calculating the ultimate cost. Poor maintenance of plant and machinery, constant technical problems with maintenance of production volume, quality, time schedule and cost limits may ultimately spell doom for the firm.

Problems relating to Management: Since Production, marketing, finance, etc. are in the hands of management, any wrong decision by them in regard to these fields may ultimately ruin a firm. The management may lack business acumen to make demand projections, to push the product in the market, to build up market image and customer loyalty, to face competition and so on.

Improper level and use of working capital can also ruin the firm. Similarly, poor industrial relations, lack of human resources planning, faulty wage and promotional policies can cause problems for the existence of the firm. So, incompetent management is the most important reason behind industrial sickness.

Financial problems: These problems are generally faced by small units. Often the financial base of the small units is very weak. They generally borrow from their own known sources or banks, rather than approaching market. Generally, they are unable to meet their debt obligations in time

and these debts accumulate. Banks normally do not help at this stage when symptoms begin to show the problem and sickness becomes chronic.

Labor unrest: Labor unrest for a long period may ultimately spell doom for the firm.

The above causes are general causes of sickness. A firm could get sick because of one or more of the above causes. However, it has been found that industrial sickness results more due to faulty, careless behaviour and attitude of management, than due to any other reason. In many cases, irresponsible and callous behaviour of the managers has been found to be the most important cause of sickness for the firm.

Q. 7: What are the Provisions for Labour Welfare in India under Factories Act. 1948?

Some of the provisions relating to the Labour Welfare as mentioned in the Factories Act, 1948 are: (1) Washing Facilities (2) Facilities for storing and drying clothing (3) Facilities for sitting (4) First aid appliances (5) Canteens (6) Shelters, rest rooms and lunch rooms (7) Creches and (8) Welfare officers

The Factories Act, 1948 contains the following provisions relating to Labour Welfare:

(1) Washing Facilities:

In every factory (a) adequate and suitable facilities shall be provided and maintained for the use of workers; (b) separate and adequately screened facilities shall be provided for the use of male and female workers; (c) such facilities shall be easily accessible and shall be kept clean.

(2) Facilities for storing and drying clothing:

In every factory provision for suitable place should exist for keeping clothing not worn during working hours and for the drying of wet clothing.

(3) Facilities for sitting:

In every factory, suitable arrangements for sitting shall be provided and maintained for all workers who are obliged to work in a standing position so that the workers may take advantage of any opportunity for rest which may occur in the course of work. If in any factory workers can efficiently do their work in a sitting position, the Chief inspector may require the occupier of the factory to provide such seating arrangements as may be practicable.

(4) First aid appliances:

Under the Act, the provisions for first-aid appliances are obligatory. At least one first-aid box or cupboard with the prescribed contents should be maintained for every 150 workers. It should be readily accessible during all working hours.

Each first-aid box or cupboard shall be kept in the charge of a separate responsible person who holds a certificate in the first-aid treatment recognised by the State Government and who shall always be readily available during the working hours of the factory.

In every factory wherein more than 500 workers are ordinarily employed there shall be provided and maintained an ambulance room of the prescribed size containing the prescribed equipment. The ambulance room shall be in the charge of properly qualified medical and nursing staff. These facilities shall always be made readily available during the working hours of the factory.

(5) Canteens:

In every factory employing more than 250 workers, the State government may make rules requiring that a canteen or canteens shall be provided for the use of workers. Such rules may provide for (a) the date by which the canteen shall be provided, (b) the standards in respect of constitution, accommodation, furniture and other equipment of the canteen; (c) the foodstuffs to be served therein and charges which may be paid thereof; (d) the constitution of a managing committee for the canteens and representation of the workers in the management of the canteen; (e) the items of expenditure in the running of the canteen which are not to be taken into account in fixing the cost of foodstuffs and which shall be borne by the employer; (f) the delegation to the Chief inspector, of the power to make rules under clause (c).

(6) Shelters, rest rooms and lunch rooms:

In every factory wherein more than 150 workers are ordinarily employed, there shall be a provision for shelters, rest room and a suitable lunch room where workers can eat meals brought by them with provision for drinking water.

Where a lunch room exists, no worker shall eat any food in the work room. Such shelters or rest rooms or lunch rooms shall be sufficiently lighted and ventilated and shall be maintained in a cool and clean condition.

(7) Creches:

In every factory wherein more than 30 women workers are ordinarily employed there shall be provided and maintained a suitable room or rooms for the use of children under the age of six years of such women.

Such rooms shall provide adequate accommodation, shall be adequately lighted and ventilated, shall be maintained in clean and proper sanitary conditions and shall be under the charge of women trained in the care of children and infants.

The State government may make rules for the provision of additional facilities for the care of children belonging to women workers including suitable provision of facilities:—

(a) For washing and changing their clothing

(b) of free milk or refreshment or both for the children, and

(c) for the mothers of children to feed them at the necessary intervals.

(8) Welfare officers:

In every factory wherein 500 or more workers are ordinarily employed, the occupier shall employ in the factory such number of welfare officers as may be prescribed under Sec. 49(1). The State government may prescribe the duties, qualifications and conditions of service of such officers.

Q. 8: What are the various forms of business organization?

FORMSOF BUSINESS ORGANISATIONHave you ever thought who brings the required capital, takes the responsibility of arranging other resources, puts them into action, and coordinates and controls the activities to earn the desired profits? If you look around, you will find that a small grocery shop is owned and run by a single individual who performs all these activities. But, in big businesses, it may not be possible for a single person to perform all these activities. So in such cases two or more persons join hands to

finance and manage the business properly and share its profit as per their agreement. Thus, business organizations may be owned and managed by a single individual or group of individuals who may form a partnership firm or a joint stock company. Such arrangement of ownership and management is termed as a form of business organization.

A business organization usually takes the following forms in India:

(1) Sole proprietorship

(2) Partnership

(3) Joint Hindu Family

(4) Cooperative Society

(5) Joint Stock Company

SOLE PROPRIETORSHIP

The term ‘sole’ means single and ‘proprietorship’ means ‘ownership’. So, only one person is the owner of the business organisation. This means, that a form of business organization in which a single individual owns and manages the business, takes the profits and bears the losses, is known as sole proprietorship form of business organization. He is therefore, entitled to the profits and has to bear the loss of business, however, he can take the help of his family members and also make use of the services of others such as a manager and other employees.

MERITS OF SOLE PROPRIETORSHIP FORM OF BUSINESS ORGANISATION

(a)Easy to Form and Wind Up: It is very easy and simple to form a sole proprietorship form of business organisation. No legal formalities are required to be observed. Similarly, the business can be wind up any time if the proprietor so decides.

(b)Quick Decision and Prompt Action: As stated earlier, nobody interferes in the affairs of the sole proprietary organisation. So he/she can take quick decisions on thevarious issues relating to business and accordingly prompt action can be taken.

(c)Direct Motivation: In sole proprietorship form of business organisations. the entire profit of the business goes to the owner. This motivates the proprietor to work hard and run the business efficiently.

(d)Flexibility in Operation: It is very easy to effect changes as per the requirements ofthe business. The expansion or curtailment of business activities does not require manyformalities as in the case of other forms of business organisation.

(e)Maintenance of Business Secrets: The business secrets are known only to the proprietor. He is not required to disclose any information to others unless and until hehimself so decides. He is also not bound to publish his business accounts.

(f)Personal Touch: Since the proprietor himself handles everything relating to business, it is easy to maintain a good personal contact with the customers and employees. By knowing the likes, dislikes and tastes of the customers, the proprietor can adjust his operations accordingly. Similarly, as the employees are few and work directly under the proprietor, it helps in maintaining a harmonious relationship with them, and run the business smoothly.

LIMITATIONSOFSOLEPROPRIETORSHIPFORMOFBUSINESSORGANISATION(a)Limited Resources: The resources of a sole proprietor are always limited. Being the single owner it is not always possible to arrange sufficient funds from his own sources. Again borrowing funds from friends and relatives or from banks has its own implications. So, the proprietor has a limited capacity to raise funds for his business.

(b)Lack of Continuity: The continuity of the business is linked with the life of the proprietor. Illness, death or insolvency of the proprietor can lead to closure of the business. Thus, the continuity of business is uncertain.

(c)Unlimited Liability: You have already learnt that there is no separate entity of the business from its owner. In the eyes of law the proprietor and the business are one and the same. So personal properties of the owner can also be used to meet the business obligations and debts.

(d)Not Suitable for Large Scale Operations: Since the resources and the managerial ability is limited, sole proprietorship form of business organisation is not suitable forlarge-scale business.

(e)Limited Managerial Expertise: A sole proprietorship from of business organization always suffers from lack of managerial expertise. A single person may not be an expert in all fields like, purchasing, selling, financing etc. Again, because of limited financial resources, and the size of the business it is also not possible to engage the professional managers in sole proprietorship form of business organisations.

PARTNERSHIP

Partnership’ is an association of two or more persons who pool their financial and managerial resources and agree to carry on a business, and share its profit. The persons who form a partnership are individually known as partners and collectively a firm or partnership firm. Partnership form of business organisation in India is governed by the Indian Partnership Act, 1932 which defines partnership as “the relation between persons who have agreed to share the profits of the business carried on by all or any of them acting for all”.MERITSOFPARTNERSHIPFORMOFBUSINESSORGANISATION(a)Easy to Form: A partnership can be formed easily without many legal formalities. Since it is not compulsory to get the firm registered, a simple agreement, either in oral,writing or implied is sufficient to create a partnership firm.

(b)Availability of Larger Resources: Since two or more partners join hands to start partnership firm it may be possible to pool more resources as compared to sole proprietorship form of business organisation.

(c)Better Decisions: In partnership firm each partner has a right to take part in the management of the business. All major decisions are taken in consultation with and with the consent of all partners. Thus, collective wisdom prevails and there is less scope for reckless and hasty decisions.

(d)Flexibility: The partnership firm is a flexible organisation. At any time the partnerscan decide to change the size or nature of business or area of its operation after takingthe necessary consent of all the partners.

(e)Sharing of Risks: The losses of the firm are shared by all the partners equally or asper the agreed ratio.

(f)Keen Interest: Since partners share the profit and bear the losses, they take keen interest in the affairs of the business.

(g)Benefits of Specialisation: All partners actively participate in the business as per their specialisation and knowledge. In a partnership firm providing legal consultancy to people, one partner may deal with civil cases, one in criminal cases, and other in labour cases and so on as per their area of specialisation. Similarly two or more doctors of different specialisation may start a clinic in partnership.

(h)Protection of Interest: In partnership form of business organisation, the rights of each partner and his/her interests are fully protected. If a partner is dissatisfied with any decision, he can ask for dissolution of the firm or can withdraw from the partnership.

(i)Secrecy: Business secrets of the firm are only known to the partners. It is not required to disclose any information to the outsiders. It is also not mandatory to publish the annual accounts of the firm.

LIMITATIONSOFPARTNERSHIPFORMOFBUSINESSORGANISATIONA partnership firm also suffers from certain limitations. These are as follows:

(a)Unlimited Liability: The most important drawback of partnership firm is that the liability of the partners is unlimited i.e., the partners are personally liable for the debt and obligations of the firm. In other words, their personal property can also be utilized for payment of firm’s liabilities.

(b)Instability: Every partnership firm has uncertain life. The death, insolvency, incapacity or the retirement of any partner brings the firm to an end. Not only that any dissenting partner can give notice at any time for dissolution of partnership.

(c)Limited Capital: Since the total number of partners cannot exceed 20, the capacity to raise funds remains limited as compared to a joint stock company where there is no limit on the number of share holders.

(d)Non-transferability of share: The share of interest of any partner cannot be transferred to other partners or to the outsiders. So it creates inconvenience for the partner who wants to transfer his share to others fully and partly. The only alternative is dissolution of the firm.

(e)Possibility of Conflicts: You know that in partnership firm every partner has an equal right to participate in the management. Also every partner can place his or her opinion or viewpoint before the management regarding any matter at any time. Because of this, sometimes there is friction and quarrel among the partners. Difference of opinion may give rise to quarrels and lead to dissolution of the firm.