Embed Size (px)

Citation preview

Index

CONTENTS:

S.NO PARTICULARS PAGE NO1.

2.

3.

4.

5.

CHAPTER – IA. INTRODUCTIONB. NEED FOR STUDYC. OBJECTIVES OF THE STUDYD. SCOPE OF THE STUDYE. RESEARCH METHODOLOGYF. TOOLS USED IN PROJECTG. ADVANTAGES OF THE STUDYH. LIMITATIONS OF THE STUDY

CHAPTER – II

COMPANY PROFILE

CHAPTER – III

LITERATURE REVIEW

CHAPTER – IV

DATA ANALYSIS AND INTERPRETATION

CHAPTER – V

SUGGESTIONS AND CONCLUSION

BIBLOGRAPHY

3-6

8-15

17-46

48-64

66-6870

1

CHAPTER – 1A. IntroductionB. Need for studyC. Objectives of the studyD. Scope of the studyE. Research methodologyF. Tools used in projectG. Advantages of the studyH. Limitations of the study

2

INTRODUCTION

A mutual fund is just the connecting bridge or a financial intermediary that allows a

group of investors to pool their money together with a predetermined investment objective.

The mutual fund will have a fund manager who is responsible for investing the gathered

money into specific securities (stocks or bonds). When you invest in a mutual fund, you are

buying units or portions of the mutual fund and thus on investing becomes a shareholder or

unit holder of the fund.

Mutual funds are considered as one of the best available investments as

compare to others they are very cost efficient and also easy to invest in, thus by pooling

money together in a mutual fund, investors can purchase stocks or bonds with much lower

trading costs than if they tried to do it on their own. But the biggest advantage to mutual

funds is diversification, by minimizing risk & maximizing returns

3

NEED OF THE STUDY

1. Mutual funds are dynamic financial intuitions which play crucial role in an economy by

mobilizing savings and investing them in the capital market.

2. The activities of mutual funds have both short and long term impact on the savings in the

capital market and the national economy.

3. Mutual funds, trust, assist the process of financial deepening & intermediation.

4. To banking at the same time they also compete with banks and other financial intuitions.

5. India is one of the few countries to day maintain a study growth rate is domestic savings.

4

OBJECTIVES OF THE STUDY

1. To show the wide range of investment options available in MF’s by explaining various

schemes offered by different AMC’s.

2. To help an investor to make a right choice of investment, while considering the inherent

risk factors.

3. To understand the recent trends in the MF world.

4. To understand the risk and return of the various schemes.

5. To find out the various problems faced by Indian mutual funds and possible solutions.

5

LIMITATIONS OF THE STUDY:

1. The study is conducted in short period, due to which the study may not be detailed in all

aspects.2. The study is limited only to the analysis of different schemes and its suitability to different

investors according to their risk-taking ability.

3. The study is based on secondary data available from monthly fact sheets, web sites; offer

documents, magazines and newspapers etc., as primary data was not accessible.

4. The study is limited by the detailed study of various schemes.

5. The NAV’S are not uniform.

6

SCOPE THE STUDY

1. The study is limited to the analysis made for a Growth scheme offered by four

AMC’s.

2. Each scheme is calculated their risk and return using different performance

measurement theories.

3. Because of the reason for such performance is immediately analyzed in the issue.

4. Graphs are used to reflect the portfolio risk and return.

7

RESEARCH METHODOLOGY & TOOLS This study is basically depends on

1. Primary Data

2. Secondary Data

Primary data: The primary data collected from the different companies through enquiry.

Secondary data :

The secondary data collected from the different sites, broachers, news papers, company offer

documents, different books and through suggestions from the project guide and from the

faculty members of our college.

TOOLS USED IN THIS PROJECTThe following parameters were considered for analysis:

Beta

Alpha

Correlation coefficient

Treynor’s Ratio

Sharpe’s Ratio

ADVANTAGES OF THE MUTUAL FUNDS1. The investors risk is reduced to the minimum.

2. The funds managers maximize the income of the funds.

3. To achieve a similar degree of diversification, an individual investor as to spend

considerable and money.

4. In a mutual fund, it is possible to reinvest the dividend and capital gains.

5. Selection of shares debentures etc and timing is made available to investors. .

8

CHAPTER – 2COMPANYPROFILE

9

INTRODUCTION

The Housing Development Finance Corporation Limited (HDFC) was amongst the first to

receive an 'in principle' approval from the Reserve Bank of India (RBI) to set up a bank in the

private sector, as part of the RBI's liberalization of the Indian Banking Industry in 1994. The

bank was incorporated in August 1994 in the name of 'HDFC Bank Limited', with its

registered office in Mumbai, India. HDFC Bank commenced operations as a Scheduled

Commercial Bank in November 1995.

HDFC is India's premier housing finance company and enjoys an impeccable track record in

India as well as in international markets. Since its inception in 1977, the Corporation has

maintained a consistent and healthy growth in its operations to remain the market leader in

mortgages. Its outstanding loan portfolio covers well over a million dwelling units. HDFC

has developed significant expertise in retail mortgage loans to different market segments and

also has a large corporate client base for its housing related credit facilities. With its

experience in the financial markets, a strong market reputation, large shareholder base and

unique consumer franchise, HDFC was ideally positioned to promote a bank in the Indian

environment.

HDFC Bank's mission is to be a World-Class Indian Bank. The objective is to build sound

customer franchises across distinct businesses so as to be the preferred provider of banking

services for target retail and wholesale customer segments, and to achieve healthy growth in

profitability, consistent with the bank's risk appetite. The bank is committed to maintain the

highest level of ethical standards, professional integrity, corporate governance and regulatory

compliance. HDFC Bank's business philosophy is based on four core values - Operational

Excellence, Customer Focus, Product Leadership and People.

Capital Structure

As on 31st December, 2011 the authorized share capital of the Bank is Rs. 550 crore. The

paid-up capital as on said date is Rs. 455,23,65,640/- (45,52,36,564 equity shares of Rs. 10/-

each). The HDFC Group holds 23.87 % of the Bank's equity and about 16.94 % of the equity

is held by the ADS Depository (in respect of the bank's American Depository Shares (ADS)

10

Issue). 27.46 % of the equity is held by Foreign Institutional Investors (FIIs) and the Bank

has about 4,58,683 shareholders.

The shares are listed on the Bombay Stock Exchange Limited and The National Stock

Exchange of India Limited. The Bank's American Depository Shares (ADS) are listed on the

New York Stock Exchange (NYSE) under the symbol 'HDB' and the Bank's Global

Depository Receipts (GDRs) are listed on Luxembourg Stock Exchange under ISIN No

US40415F2002.

HDFC Bank is headquartered in Mumbai. The Bank at present has an enviable network of

1,725 branches spread in 771 cities across India. All branches are linked on an online real-

time basis. Customers in over 500 locations are also serviced through Telephone Banking.

The Bank's expansion plans take into account the need to have a presence in all major

industrial and commercial centres where its corporate customers are located as well as the

need to build a strong retail customer base for both deposits and loan products. HDFC is a

clearing/settlement bank to various leading stock exchanges.

The Bank also has 4,000 networked ATMs across these cities. Moreover, HDFC Bank's

ATM network can be accessed by all domestic and international Visa/MasterCard, Visa

Electron/Maestro, Plus/Cirrus and American Express Credit/Charge cardholders.

The Bank's Board of Directors is composed of eminent individuals with a wealth of

experience in public policy, administration, industry and commercial banking. Senior

executives representing HDFC are also on the Board.

Senior banking professionals with substantial experience in India and abroad head various

businesses and functions and report to the Managing Director. Given the professional

expertise of the management team and the overall focus on recruiting and retaining the best

talent in the industry, the bank believes that its people are a significant competitive strength.

HDFC Bank operates in a highly automated environment in terms of information technology

and communication systems. All the bank's branches have online connectivity, which enables

the bank to offer speedy funds transfer facilities to its customers. Multi-branch access is also

provided to retail customers through the branch network and Automated Teller Machines

(ATMs).

11

The Bank has made substantial efforts and investments in acquiring the best technology

available internationally, to build the infrastructure for a world class bank. The Bank's

business is supported by scalable and robust systems which ensure that our clients always get

the finest services we offer.

The Bank has prioritized its engagement in technology and the internet as one of its key goals

and has already made significant progress in web-enabling its core businesses. In each of its

businesses, the Bank has succeeded in leveraging its market position, expertise and

technology to create a competitive advantage and build market share.

Wholesale Banking Services

The Bank's target market ranges from large, blue-chip manufacturing companies in the

Indian corporate to small & mid-sized corporate and agro-based businesses. For these

customers, the Bank provides a wide range of commercial and transactional banking

services, including working capital finance, trade services, transactional services, cash

management, etc. The bank is also a leading provider of structured solutions, which

combine cash management services with vendor and distributor finance for facilitating

superior supply chain management for its corporate customers. Based on its superior

product delivery / service levels and strong customer orientation, the Bank has made

significant inroads into the banking consortia of a number of leading Indian corporate

including multinationals, companies from the domestic business houses and prime public

sector companies. It is recognized as a leading provider of cash management and

transactional banking solutions to corporate customers, mutual funds, stock exchange

members and banks.

Retail Banking Services

The objective of the Retail Bank is to provide its target market customers a full range of

financial products and banking services, giving the customer a one-stop window for all

his/her banking requirements. The products are backed by world-class service and

delivered to customers through the growing branch network, as well as through alternative

delivery channels like ATMs, Phone Banking, Net Banking and Mobile Banking.

The HDFC Bank Preferred program for high net worth individuals, the HDFC Bank Plus

and the Investment Advisory Services programs have been designed keeping in mind

needs of customers who seek distinct financial solutions, information and advice on

12

various investment avenues. The Bank also has a wide array of retail loan products

including Auto Loans, Loans against marketable securities, Personal Loans and Loans for

Two-wheelers

Treasury

Within this business, the bank has three main product areas - Foreign Exchange and

Derivatives, Local Currency Money Market & Debt Securities, and Equities. With the

liberalization of the financial markets in India, corporate need more sophisticated risk

management information, advice and product structures. These and fine pricing on various

treasury products are provided through the bank's Treasury team. To comply with statutory

reserve requirements, the bank is required to hold 25% of its deposits in government

securities. The Treasury business is responsible for managing the returns and market risk

on this investment portfolio.

Credit Rating

the Bank has its deposit programs rated by two rating agencies - Credit Analysis & Research

Limited (CARE) and Fitch Ratings India Private Limited. The Bank's Fixed Deposit

programme has been rated 'CARE AAA (FD)' [Triple A] by CARE, which represents

instruments considered to be "of the best quality, carrying negligible investment risk". CARE

has also rated the bank's Certificate of Deposit (CD) programme "PR 1+" which represents

"superior capacity for repayment of short term promissory obligations". Corporate

Governance rating

The bank was one of the first four companies, which subjected itself to a Corporate

Governance and Value Creation (GVC) rating by the rating agency, The Credit Rating

Information Services of India Limited (CRISIL). The rating provides an independent

assessment of an entity's current performance and an expectation on its "balanced value

creation and corporate governance practices" in future. The bank has been assigned a

'CRISIL GVC Level 1' rating which indicates that the bank's capability with respect to wealth

creation for all its stakeholders while adopting sound corporate governance practices is the

highest.

13

On May 23, 2009, the amalgamation of Centurion Bank of Punjab with HDFC Bank

was formally approved by Reserve Bank of India to complete the statutory and

regulatory approval process. As per the scheme of amalgamation, shareholders of CBoP

received 1 share of HDFC Bank for every 29 shares of CBoP.

The merged entity will have a strong deposit base of around Rs. 1,22,000 crore and net

advances of around Rs. 89,000 crore. The balance sheet size of the combined entity

would be over Rs. 1,63,000 crore. The amalgamation added significant value to HDFC

Bank in terms of increased branch network, geographic reach, and customer base, and a

bigger pool of skilled manpower.

In a milestone transaction in the Indian banking industry, Times Bank Limited (another

new private sector bank promoted by Bennett, Coleman & Co. / Times Group) was

merged with HDFC Bank Ltd., effective February 26, 2000. This was the first merger

of two private banks in the New Generation Private Sector Banks. As per the scheme of

amalgamation approved by the shareholders of both banks and the Reserve Bank of

India, shareholders of Times Bank received 1 share of HDFC Bank for every 5.75

shares of Times Bank.

HDFC Bank Ltd. (BSE: 500180, NYSE: HDB) is a commercial bank of India,

incorporated in August 1994, after the Reserve Bank of India allowed establishing

private sector banks. The Bank was promoted by the Housing Development Finance

Corporation, a premier housing finance company (set up in 1977) of India. HDFC Bank

has 1,412 branches and over 3,295 ATMs, in 528 cities in India, and all branches of the

bank are linked on an online real-time basis. As of September 30, 2009 the bank had

total assets of INR 1006.82 billion. For the fiscal year 2009-09, the bank has reported

net profit of Rs.2,244.9 crore, up 41% from the previous fiscal. Total annual earnings of

the bank increased by 58% reaching at Rs.19,622.8 crore in 2009-09.

14

Business Focus

HDFC Bank deals with three key business segments - Wholesale Banking Services, Retail

Banking Services, and Treasury. It has entered the banking consortia of over 50 corporate for

providing working capital finance, trade services, corporate finance and merchant banking. It

is also providing sophisticated product structures in areas of foreign exchange and

derivatives, money markets and debt trading and equity research.

Wholesale Banking Services

The Bank's target m inroads into the banking consortia of a number of leading Indian

corporates including multinationals, companies from the domestic business houses and prime

public sector companies. It is recognised as a leading provider of cash management and

transactional banking solutions to corporate customers, mutual funds, stock exchange

members and banks.

Retail Banking Services

The objective of the Retail Bank is to provide its target market customers a full range of

financial products and banking services, giving the customer a one-stop window for all

his/her banking requirements. The products are backed by world-class service and delivered

to customers through the growing branch network, as well as through alternative delivery

channels like ATMs, Phone Banking, NetBanking and Mobile Banking.

HDFC Bank was the first bank in India to launch an International Debit Card in association

with VISA (VISA Electron) and issues the Mastercard Maestro debit card as well. The Bank

launched its credit card business in late 2001. By March 2011, the bank had a total card base

(debit and credit cards) of over 13 million. The Bank is also one of the leading players in the

“merchant acquiring” business with over 70,000 Point-of-sale (POS) terminals for debit /

credit cards acceptance at merchant establishments. The Bank is well positioned as a leader in

various net based B2C opportunities including a wide range of internet banking services for

Fixed Deposits, Loans, Bill Payments, etc.

15

Treasury

Within this business, the bank has three main product areas - Foreign Exchange and

Derivatives, Local Currency Money Market & Debt Securities, and Equities. These services

are provided through the bank's Treasury team. To comply with statutory reserve

requirements, the bank is required to hold 25% of its deposits in government securities. The

Treasury business is responsible for managing the returns and market risk on this investment

portfolio.

Distribution Network

HDFC Bank is headquartered in Mumbai. The Bank has an network of 1,725 branches spread

in 771 cities across India. All branches are linked on an online real-time basis. Customers in

over 500 locations are also serviced through Telephone Banking. The Bank has a presence in

all major industrial and commercial centres across the country. Being a clearing/settlement

bank to various leading stock exchanges, the Bank has branches in the centres where the

NSE/BSE have a strong and active member base.

The Bank also has 3,898 networked ATMs across these cities. Moreover, HDFC Bank's

ATM network can be accessed by all domestic and international Visa/MasterCard, Visa

Electron/Maestro, Plus/Cirrus and American Express Credit/Charge cardholders.

Housing Development Finance Corporation Limited or HDFC (BSE: 500010), founded 1977

by Ravi Maurya and Hasmukhbhai Parekh, is an Indian NBFC, focusing on home mortgages.

HDFC's distribution network spans 243 outlets that include 49 offices of HDFC's distribution

company, HDFC Sales Private Limited. In addition, HDFC covers over 90 locations through

its outreach programmes. HDFC's marketing efforts continue to be concentrated on

developing a stronger distribution network. Home loans are also Sharcket through HDFC

Sales, HDFC Bank Limited and other third party Direct Selling Agents (DSA).

To cater to non-resident Indians, HDFC has an office in London and Dubai and service

associates in Kuwait, Oman, Qatar, Sharjah, Abu Dhabi, Al Khobar, Jeddah and Riyadh in

Saudi Arabia.

16

CHAPTER – 3

REVIEW

OF

LITERATURE

17

CONCEPT OF MUTUAL FUNDS

Like most developed and developing countries the mutual fund culture has been

catching on in India. There are various reasons for this. Mutual funds make it easy and less

costly for investors to satisfy their need for capital growth, income and/or income

preservation. And in addition to this a mutual fund brings the benefits of diversification and

money management to the individual investor, providing an opportunity for financial success

that was once available only to a select few.

A Mutual Fund is a trust that pools the savings of a number of investors who share a common

financial goal. The money thus collected is then invested in capital market instruments such

as shares, debentures and other securities. The income earned through these investments and

the capital appreciations realized are shared by its unit holders in proportion to the number of

units owned by them. Thus a Mutual Fund is the most suitable investment for the common

man as it offers an opportunity to invest in a diversified, -professionally managed basket of

securities at a relatively low cost. The flow chart below describes broadly the working of a

mutual fund:

Mutual Fund Operation Flow Chart

18

BENEFITS OF MUTUAL FUNDSInvesting in mutual has various benefits which makes it an ideal investment avenue.

Following are some of the primary benefits.

Professional investment managementOne of the primary benefits of mutual funds is that an investor has access to professional

management. A good investment manager is certainly worth the fees you will pay. Good

mutual fund managers with an excellent research team can do a better job of monitoring the

companies they have chosen to invest in than you can, unless you have time to spend on

researching the companies you select for your portfolio. That is because Mutual funds hire

full-time, high-level investment professionals. Funds can afford to do so as they manage large

pools of money. The managers have real-time access to crucial market information and are

able to execute trades on the largest and most cost-effective scale. When you buy a mutual

fund, the primary asset you are buying is the manager, who will be controlling which assets

are chosen to meet the funds' stated investment objectives.

DiversificationA crucial element in investing is asset allocation. It plays a very big part in the success of any

portfolio. However, small investors do not have enough money to properly allocate their

assets. By pooling your funds with others, you can quickly benefit from greater

diversification. Mutual funds invest in a broad range of securities. This limits investment risk

by reducing the effect of a possible decline in the value of any one security. Mutual fund unit-

holders can benefit from diversification techniques usually available only to investors

wealthy enough to buy significant positions in a wide variety of securities.

19

Low CostA mutual fund let's you participate in a diversified portfolio for as little as Rs.5, 000, and

sometimes less. And with a no-load fund, you pay little or no sales charges to own them.

Convenience and FlexibilityInvesting in mutual funds has its own convenience. While you own just one security rather

than many, you still enjoy the benefits of a diversified portfolio and a wide range of services.

Fund managers decide what securities to trade collect the interest payments and see that your

dividends on portfolio securities are received and your rights exercised. It also uses the

services of a high quality custodian and registrar. Another big advantage is that you can move

your funds easily from one fund to another within a mutual fund family. This allows you to

easily rebalance your portfolio to respond to significant fund management or economic

changes.

LiquidityIn open-ended schemes, you can get your money back promptly at net asset value related

prices from the mutual fund itself.

TransparencyRegulations for mutual funds have made the industry very transparent. You can track the

investments that have been made on you behalf and the specific investments made by the

mutual fund scheme to see where your money is going. In addition to this, you get regular

information on the value of your investment.

VarietyThere is no shortage of variety when investing in mutual funds. You can find a mutual fund

that matches just about any investing strategy you select. There are funds that focus on blue-

chip stocks, technology stocks, bonds or a mix of stocks and bonds. The greatest challenge

can be sorting through the variety and picking the best for you.

20

TYPES OF MUTUAL FUNDSGetting a handle on what's under the hood helps you become a better investor and put

together a more successful portfolio. To do this one must know the different types of funds

that cater to investor needs, whatever the age, financial position, risk tolerance and return

expectations. The mutual fund schemes can be classified according to both their investment

objective (like income, growth, tax saving) as well as the number of units (if these are

unlimited then the fund is an open-ended one while if there are limited units then the fund is

close-ended).

Open-Ended SchemesOpen-ended schemes do not have a fixed maturity period. Investors can buy or sell units at

NAV-related prices from and to the mutual fund on any business day. These schemes have

unlimited capitalization, open-ended schemes do not have a fixed maturity, there is no cap on

the amount you can buy from the fund and the unit capital can keep growing. These funds are

not generally listed on any exchange.

Open-ended schemes are preferred for their liquidity. Such funds can issue and redeem units

any time during the life of a scheme. Hence, unit capital of open-ended funds can fluctuate on

a daily basis. The advantages of open-ended funds over close-ended are as follows:

Close-Ended SchemesClose-ended schemes have fixed maturity periods. Investors can buy into these funds during

the period when these funds are open in the initial issue. After that such schemes can not

issue new units except in case of bonus or rights issue. However, after the initial issue, you

can buy or sell units of the scheme on the stock exchanges where they are listed. The market

price of the units could vary from the NAV of the scheme due to demand and supply factors,

investors’ expectations and other market factors

Classification According To Investment Objectives

21

Mutual funds can be further classified based on their specific investment objective such as

growth of capital, safety of principal, current income or tax-exempt income.

In general mutual funds fall into three general categories:

1] Equity Funds are those that invest in shares or equity of companies.

2] Fixed-Income Funds invest in government or corporate securities that offer fixed rates of

return are

3] While funds that invest in a combination of both stocks and bonds are called Balanced

Funds.

Growth Funds Growth funds primarily look for growth of capital with secondary emphasis on dividend.

Such funds invest in shares with a potential for growth and capital appreciation. They invest

in well-established companies where the company itself and the industry in which it operates

are thought to have good long-term growth potential, and hence growth funds provide low

current income. Growth funds generally incur higher risks than income funds in an effort to

secure more pronounced growth.

Growth and Income Funds Growth and income funds seek long-term growth of capital as well as current income. The

investment strategies used to reach these goals vary among funds. Some invest in a dual

portfolio consisting of growth stocks and income stocks, or a combination of growth stocks,

stocks paying high dividends, preferred stocks, convertible securities or fixed-income

securities such as corporate bonds and money market instruments. Others may invest in

growth stocks and earn current income by selling covered call options on their portfolio

stocks.

Fixed-Income Funds Fixed income funds primarily look to provide current income consistent with the preservation

of capital. These funds invest in corporate bonds or government-backed mortgage securities

that have a fixed rate of return. Within the fixed-income category, funds vary greatly in their

stability of principal and in their dividend yields. High-yield funds, which seek to maximize

yield by investing in lower-rated bonds of longer maturities, entail less stability of principal

than fixed-income funds that invest in higher-rated but lower-yielding securities.

22

Balanced fundsThe Balanced fund aims to provide both growth and income. These funds invest in both

shares and fixed income securities in the proportion indicated in their offer documents. Ideal

for investors who are looking for a combination of income and moderate growth.

Money Market Funds/Liquid Funds For the cautious investor, these funds provide a very high stability of principal while seeking

a moderate to high current income. They invest in highly liquid, virtually risk-free, short-term

debt securities of agencies of the Indian Government, banks and corporations and Treasury

Bills. Because of their short-term investments, money market mutual funds are able to keep a

virtually constant unit price; only the yield fluctuates.

Specialty/Sector FundsThese funds invest in securities of a specific industry or sector of the economy such as health

care, technology, leisure, utilities or precious metals. The funds enable investors to diversify

holdings among many companies within an industry, a more conservative approach than

investing directly in one particular company.

RISK Vs. REWARDHaving understood the basics of mutual funds the next step is to build a

successful investment portfolio. Before you can begin to build a portfolio, one should

understand some other elements of mutual fund investing and how they can affect the

potential value of your investments over the years. The first thing that has to be kept in mind

is that when you invest in mutual funds, there is no guarantee that you will end up with more

money when you withdraw your investment than what you started out with. That is the

potential of loss is always there. The loss of value in your investment is what is considered

risk in investing.

Risk then, refers to the volatility -- the up and down activity in the markets and individual

issues that occurs constantly over time. This volatility can be caused by a number of factors --

23

interest rate changes, inflation or general economic conditions. It is this variability,

uncertainty and potential for loss, that causes investors to worry.

Different types of mutual funds have different levels of volatility or potential price change,

and those with the greater chance of losing value are also the funds that can produce the

greater returns for you over time. So risk has two sides: it causes the value of your

investments to fluctuate, but it is precisely the reason you can expect to earn higher returns.

You might find it helpful to remember that all financial investments will fluctuate. There are

very few perfectly safe havens and those simply don't pay enough to beat inflation over the

long run.

TYPES OF RISKS

All investments involve some form of risk. Consider these common types of risk and evaluate

them against potential rewards when you select an investment.

Market RiskAt times the prices or yields of all the securities in a particular market rise or fall due to broad

outside influences. When this happens, the stock prices of both an outstanding, highly

profitable company and a fledgling corporation may be affected. This change in price is due

to "market risk". Also known as systematic risk.

24

Inflation RiskSometimes referred to as "loss of purchasing power." Whenever inflation rises forward faster

than the earnings on your investment, you run the risk that you'll actually be able to buy less,

not more. Inflation risk also occurs when prices rise faster than your returns.

Credit RiskIn short, how stable is the company or entity to which you lend your money when you invest?

How certain are you that it will be able to pay the interest you are promised, or repay your

principal when the investment matures?

Interest Rate RiskChanging interest rates affect both equities and bonds in many ways. Investors are reminded

that "predicting" which way rates will go is rarely successful. A diversified portfolio can help

in offsetting these changes.

Exchange riskA number of companies generate revenues in foreign currencies and may have investments or

expenses also denominated in foreign currencies. Changes in exchange rates may, therefore,

have a positive or negative impact on companies which in turn would have an effect on the

investment of the fund.

Investment Risks The sectored fund schemes, investments will be predominantly in equities of select

companies in the particular sectors. Accordingly, the NAV of the schemes are linked to the

equity performance of such companies and may be more volatile than a more diversified

portfolio of equities.

Call RisksCall risk is associated with bonds have and embedded call option in them. This option gives

the issuer the right to call back the bonds prior to maturity. Then investor how ever is

exposed to some risks here. The price of the callable bond many not rise much above the

price at which the issuer may call the bond.

25

Changes in the Government PolicyChanges in Government policy especially in regard to the tax benefits may impact the

business prospects of the companies leading to an impact on the investments made by the

fund. Effect of loss of key professionals and inability to adapt business to the rapid

technological change.

An industries' key asset is often the personnel who run the business i.e. intellectual

properties of the key employees of the respective companies. Given the ever-changing

complexion of few industries and the high obsolescence levels, availability of qualified,

trained and motivated personnel is very critical for the success of industries in few sectors. It

is, therefore, necessary to attract key personnel and also to retain them to meet the changing

environment and challenges the sector offers. Failure or inability to attract/retain such

qualified key personnel may impact the prospects of the companies in the particular sec

Investment cycle in Mutual Funds

26

Types of mutual funds

27

History of the Indian Mutual Fund Industry:

The mutual fund industry in India started in 1963 with the formation of Unit Trust of India, at

the initiative of the Government of India and Reserve Bank the. The history of mutual funds

in India can be broadly divided into four distinct phases

First Phase – 1964-87(UTI MONOPOLY)

An Act of Parliament established Unit Trust of India (UTI) on 1963. It was set up by the

Reserve Bank of India and functioned under the Regulatory and administrative control of the

Reserve Bank of India. In 1978 UTI was de-linked from the RBI and the Industrial

Development Bank of India (IDBI) took over the regulatory and administrative control in

place of RBI. The first scheme launched by UTI was Unit Scheme 1964. At the end of 1988

UTI had Rs.6, 700 crores of assets under management.

Second Phase – 1987-1993 (Entry of Public Sector Funds)

1987 marked the entry of non- UTI, public sector mutual funds set up by public sector banks

and Life Insurance Corporation of India (LIC) and General Insurance Corporation of India

(GIC). SBI Mutual Fund was the first non- UTI Mutual Fund established in June 1987

followed by Can bank Mutual Fund (Dec 87), Punjab National Bank Mutual Fund (Aug 89),

Indian Bank Mutual Fund (Nov 89), Bank of India (Jun 90), Bank of Baroda Mutual Fund

(Oct 92). LIC established its mutual fund in June 1989 while GIC had set up its mutual fund

in December 1990.

28

At the end of 1993, the mutual fund industry had assets under management of Rs.47, 004

cores.

Third Phase – 1993-2003 (Entry of Private Sector Funds)

With the entry of private sector funds in 1993, a new era started in the Indian mutual fund

industry, giving the Indian investors a wider choice of fund families. Also, 1993 was the year

in which the first Mutual Fund Regulations came into being, under which all mutual funds,

except UTI were to be registered and governed. The erstwhile Kothari Pioneer (now merged

with Franklin Templeton) was the first private sector mutual fund registered in July 1993.

Fourth Phase – since February 2003

In February 2003, following the repeal of the Unit Trust of India Act 1963 UTI was

bifurcated into two separate entities. One is the Specified Undertaking of the Unit Trust of

India with assets under management of Rs.29, 835 crores as at the end of November 2003,

representing broadly, the assets of US 64 scheme, assured return and certain other schemes.

The Specified Undertaking of Unit Trust of India, functioning under an administrator and

under the rules framed by Government of India and does not come under the purview of the

Mutual Fund Regulations.

The second is the UTI Mutual Fund Ltd, sponsored by SBI, PNB, BOB and LIC.

GROWTH IN ASSETS UNDER MANAGEMENT

29

India is at the first stage of a revolution that has already peaked in the U.S. The U.S. boasts of

an Asset base that is much higher than its bank deposits. In India, mutual fund assets are not

even 10% of the bank deposits, but this trend is beginning to change. Recent figures indicate

that in the first quarter of the current fiscal year.

The formation and operations of mutual funds in India is solely guided by SEBI (Mutual

Fund) Regulations, 1993, which came into force on 20 November 1993. The regulations have

since been replaced by the Securities and Exchange Board of India (Mutual Funds)

Regulations, 1996, through a notification on 9 December 1996.

A mutual fund comprises four separate entities, namely sponsor, mutual fund trust, AMC and

custodian. They are of course assisted by other independent administrative entities like

30

banks, registrars and transfer agents. We may discuss in brief the formation of different

entities, their functions and obligations.

The sponsor for a mutual fund can by any person who, acting alone or in combination with

another body corporate establishes the mutual fund and gets it registered with SEBI. The

sponsor is required to contribute at least 40 per cent of the minimum net worth (Rs 10 crore)

of the asset management company. The sponsor must have a sound track record and general

reputation of fairness and integrity in all his business transactions.

As per SEBI Regulation, 1996, a mutual fund is to be formed by the sponsor and registered

with SEBI. A mutual fund shall be constituted in the form of a trust and the instrument of

trust shall be in the form of a deed, duly registered under the provisions of the Indian

Registration Act, 1908, executed by the sponsor in favor of trustees named in such an

instrument.

The trustees have the right to obtain relevant information from the AMC, as well as a

quarterly report on its activities. They can also dismiss the AMC under specific condition as

per SEBI regulations.

At least half the trustees should be independent persons. The AMC or its employees

cannot act as a trustee. No person who is appointed as a trustee of a mutual fund can be

appointed as a trustee of any other mutual fund unless he is an independent trustee and prior

permission is obtained from the mutual fund in which he is a trustee.

As per SEBI guidelines, an asset management company is appointed by the

trustees to float the schemes for the mutual fund and manage the funds raised by selling units

under a scheme. The AMC must act as per SEBI guidelines, trust deeds and management

agreement between trustee & the AMC.

The Importance of Accounting KnowledgeMutual funds in India are required to follow the accounting policies laid down in SEBI

(Mutual Fund) Regulations, 1996 and the amendments in 1998. This section of the workbook

summarizes the important Regulations, and periodical budgets.

31

Net Asset Value (NAV)A mutual fund is a common investment vehicle where the assets of the fund belong directly to

the investors. The fund does not account for investors' subscriptions as liabilities or deposits

but as Unit Capital. On the other hand, the investments made on behalf of the investors are

reflected on the assets side and are the main constituents of the balance sheet. There are,

however, liabilities of a strictly short-term nature that may be part of the balance sheet. The

fund's Net Assets are therefore defined as the assets minus the liabilities. As there are many

investors in a fund, it is common practice for mutual funds to compute the share of each

investor on the basis of the value of Net Assets Per Share/Unit, commonly known as the Net

Asset Value (NAV).

The following are the regulatory requirements and accounting definitions lay down by SEBI.

NAV = Net Assets of the scheme / Number of Units Outstanding, i.e. Market value of

investments + Receivables + Other Accrued Income + Other Assets

Accrued Expenses-Other Payables-Other Liabilities

No. Of Units Outstanding as at the NAV date

A fund's NAV is affected by four sets of factors:

-- Purchase and sale of investment securities

-- Valuation of all investment securities held

-- Other assets and liabilities, and

-- Units sold or redeemed

Pricing of Units:

Although NAV per share defines the value of the investor's holding in the fund, the

fund may not repurchase the investor's units at the same price as NAV. However, SEBI

requires that the fund must ensure that repurchase price is not lower than 93% of NAV (95%

in the case of a closed end fund). On the other side, a fund may sell new units at a price that is

different from the NAV, but the sale price cannot be higher than 107% of NAV. Also, the

difference the repurchase price and the sale price of the unit is not permitted to exceed 7% of

the sale price.

32

=

Fees and Expenses:

An AMC may incur many expenses specifically for given schemes, and other

common expenses. In any case, all expenses should be clearly Unidentified and allocated to

the individual schemes. The AMC may charge the scheme with investment management and

advisory fees that are fully disclosed in the offer document subject to the following limits:

@ 1.25% of the first Rs. 100 crore of weekly average net assets outstanding in the

accounting year, and @ 1% of weekly average net assets in excess of Rs. 100 crore.

For no load schemes, the AMC may charge an additional management fee up to 1% of

weekly average net assets outstanding in the accounting year.

Initial Issue Expenses:

When a scheme is first launched, the AMC will incur significant expenses, whose

benefit will accrue over many years. All expenses cannot, therefore, be charged to a scheme

in the first year itself. SEBI permits "amortization" of initial expenses as follows:

For a closed-end scheme floated on a 'load' basis, the initial issue expenses shall be

amortized on a weekly basis over the period of scheme. For example, a 5-year (i.e. 260 week)

closed-end scheme with initial issue expenses of Rs. 5 lakhs must charge Rs.1923 (5 lakhs /

260 weeks) every week to the fund. It cannot charge the entire amount of Rs. 5 lakhs at the

time of issue.

For an open-end scheme floated on a 'load' basis, initial issue expenses may be amortized

over a period not exceeding five years. For example, if an open-end scheme has initial issue

expenses of Rs. 10 lakhs, it need not charge this entire amount to the fund in the year of issue.

Instead, it may charge Rs. 2 lakhs (10 lakhs / 5 years) per year to the fund, thereby spreading

the charge of initial issue expenses over a maximum of 5 years. Issue expenses incurred

during the life of an open-end scheme cannot be amortized.

33

Un amortized portion of initial issue expenses shall be included for NAV calculation,

considered as "other asset". The investment advisory fee cannot be claimed on this asset.

Hence, they have to be excluded while determining the chargeable investment management /

advisory fees. While calculating the maximum amount of chargeable expenses, the un

amortized portion of the initial issue expenses will not be included as part of the average

weekly net assets figure.

Accounting Policies: Investments are required to be marked to market using market prices. Any unrealized

appreciation cannot be distributed, and provision must be made for the same.

Dividend received by the fund on a share should be recognized, not on the date of

declaration, but on the date the share is quoted on ex-dividend basis. For example, if a fund

owns shares on which dividend is declared on April 5, and the shares are quoted on ex-

dividend basis on April 20, the dividend income will be included by the fund for

distribution/NAV computation only April 20.

In determining gain or loss on sale of investments, the average cost method must be

followed to determine the cost of purchase. This will be applied by security.

Purchase / sale of investments should be recognized on the trade date and not settlement

date

Bonus / rights shares should be recognized only when the original shares are traded on the

stock exchange on an ex-bonus /ex-rights basis

Income receivable on investments, which is accrued, but not received for 12 months beyond

due date, should be provided for, and no further accrual should be made for such investment

An investment shall be regarded as non-performing if it has provided no returns through

dividend/interest for more than 2years at the end of the accounting year

VALUATION Mutual funds value their investments on a 'mark-to-market' basis with reference to the date

on which they are valued i.e., the valuation date.

Valuation of Traded Securities:

34

Where a security is traded on a stock exchange, it is valued at the last quoted closing price

on the stock exchange where it is "principally traded".

If a security is not traded on any stock exchange on a particular valuation day, the value at

which it was traded on the selected/other stock exchange on the

Earliest previous day may be used, provided such date is not more than 60 days prior to the

valuation date.

Valuation of traded securities, once the market price is obtained as above, is quite simple.

The fund will multiply its current holding in number of shares or bonds by the applicable

market price to get the "mark to market" value.

valuation of Non-traded Securities: When a security is not traded on any stock exchange for 60 days prior to the valuation date,

it must be treated as non-traded' scrip.

Non-traded securities shall be valued 'in good faith' by the AMC on the basis of appropriate

valuation methods, which shall be periodically reviewed by the trustees and reported by the

auditors as fair and reasonable. The following principles are to be applied for the valuation of

non-traded securities:

Equity instruments: are to be valued on the basis of capitalization of earnings solely or in

combination with its balance sheet Net Asset Value. For this purpose, capitalization rate will

be determined by reference to the price or earning rations of comparable traded securities

with an appropriate discount for lower liquidity to be used.

Debit instruments: are to be valued on a yield to maturity basis, the capitalization factor

being determined for comparable traded securities with an appropriate discount for lower

liquidity.

Call money, bills purchased: under rediscounting and short term deposits with banks are

to be valued at cost + accrual: other money market instruments at yield at which they are

currently traded; non-traded instruments (not traded for 7 days) will be valued at cost plus

interest accrued till the beginning of the valuation day plus the difference between

redemption value and cost, spread uniformly over the remaining maturity of the instruments

35

Government Securities: are to be valued at yield to maturity based on prevailing

market rate

Convertible debentures and bonds: non-convertible component is to be valued as a

debt instrument, and convertible as any equity instrument. If after Conversion, the resultant

equity instrument would be traded pari passu with an existing instrument, which is traded, the

value of the latter instrument can be adopted after an appropriate discount for the non-

tradability of the instrument.

RISK INVOLVED IN MUTUAL FUNDS INDUSTRY:

Mutual funds are not free from risk. It is so because basically the mutual funds also invest

their funds in stock markets on shares, which are volatile in nature and are not risk free, the

following risk are inherent in their dealing.

INHERENT RISK FACTORS:

1) Market Risks:In general there are certain risks associated with the every kind of investment on shares. They

are called market risks. These market risks can be reduced, but cannot be completely

eliminated even by a good investment.

2) Scheme RisksThere are certain risks inherent in the scheme itself. It all depends upon the nature of the

scheme. For instance, in a pure growth scheme, risks are greater.

3) Investment Risks Whether the mutual fund makes money in shares or loses depends upon the investment

expertise of the Asset Management Company. If the investment advice goes wrong, the fund

has to suffer a lot.

4) Business RisksThe corpus of a mutual fund might have been invested in a company’s shares. If the business

of that company suffers any set back, it cannot declare any dividend. It may even go to the

extent of winding up its business.

5) Political RisksSuccessive Governments bring with them fancy new economic ideologies and policies. It is

often said that many economic decisions are politically motivated.

36

PARAMETERS DESCRIPTION

The following parameters were considered for analysis:

Beta

Alpha

Correlation coefficient

Treynor’s Ratio

Sharpe’s Ratio

Jensen’s Ratio

37

BetaBeta is a measure of volatility, or systematic risk, of a security or portfolio in comparison to

the market as a whole. Beta measures a stock's volatility, the degree to which a stock price

fluctuates in relation to the overall market. Investment analysts use the Greek letter beta, ß. It

is calculated using regression analysis. A beta of 1 indicates that the security's price will

move with the market. A beta greater than 1 indicates that the security's price will be more

volatile than the market, and a beta less than 1 means that it will be less volatile than the

market.

Here is a basic guide to various betas:

Negative beta - A beta less than 0 is possible but highly unlikely. People used to

think that gold and gold stocks should have negative betas because they tended to do

better when the stock market declined, but this hasn't been true overall.

Beta = 0 - Basically this is cash (assuming no inflation).

Beta between 0 and 1 - Low-volatility investments, such as utilities, are usually in

this range

Beta = 1 - This is the same as an index, such as the S&P 500 or some other index

fund.

Beta greater than 1 - This denotes anything more volatile than the broad-based

index, like a sector fund.

Beta greater than 100 - This is impossible because the stock would be expected go

to zero on any decline in the stock market. The beta never gets higher than two to

three.

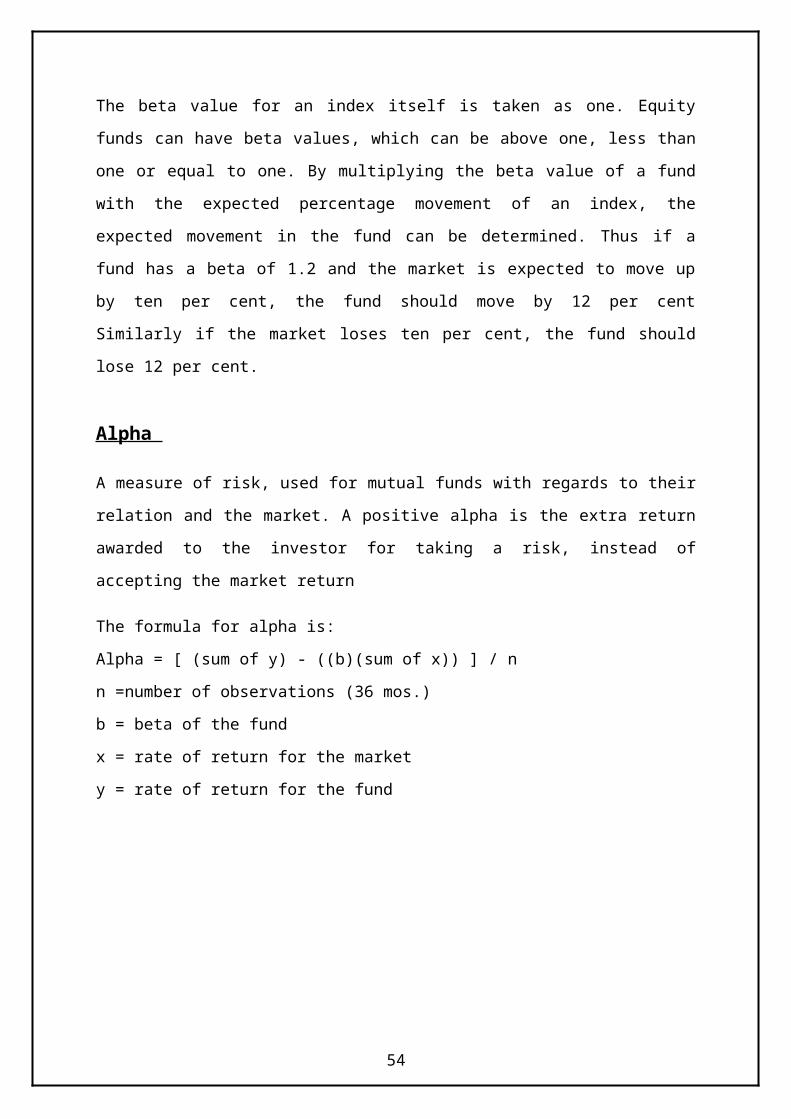

The beta value for an index itself is taken as one. Equity funds can have beta values, which

can be above one, less than one or equal to one. By multiplying the beta value of a fund with

the expected percentage movement of an index, the expected movement in the fund can be

determined. Thus if a fund has a beta of 1.2 and the market is expected to move up by ten per

38

cent, the fund should move by 12 per cent Similarly if the market loses ten per cent, the fund

should lose 12 per cent.

Alpha

A measure of risk, used for mutual funds with regards to their relation and the market. A

positive alpha is the extra return awarded to the investor for taking a risk, instead of accepting

the market return

The formula for alpha is:

Alpha = [ (sum of y) - ((b)(sum of x)) ] / n

n =number of observations (36 mos.)

b = beta of the fund

x = rate of return for the market

y = rate of return for the fund

39

Standard Deviation

Standard deviation is probably used more than any other

Measure to describe the risk of a security (or portfolio of securities). If you read an academic

study on investment performance, chances are that standard deviation will be used to gauge

risk. It's not just a financial tool, though. Standard deviation is one of the most commonly

used statistical tools in the sciences and social sciences. It provides a precise measure of the

amount of variation in any group of numbers--the returns of a mutual fund.

Measure of the dispersion of a set of data from its mean. The more spread apart the data is,

the higher the deviation. Standard deviation is applied to the annual rate of return of an

investment to measure the investment's volatility (risk).

Correlation

Correlation is a useful tool for determining if relationships exist between securities. A

correlation coefficient is the result of a mathematical comparison of how closely related two

variables are.

The relationship between two variables is said to be highly correlated if a movement in one

variable results or takes place at the same time as a similar movement in another variable.

Correlation analysis is a measure of the degree to which a change in the independent variable

will result in a change in the dependent variable. A low correlation coefficient (e.g., ±0.1)

suggests that the relationship between the two variables is weak or non-existent. A high

correlation coefficient (e.g., ±0.80) indicates that the dependent variable will most likely

change when the Independent variable changes. Correlation can also be used for a study

between an indicator and a stock or index to help determine the predictive abilities of changes

in the indicator.

40

PORTFOLIO MEASUREMENT METHODS:

We are interested in discovering if the management of a mutual fund is performing well; that

is, has management done better through its selective buying and selling of securities than

would have been achieved through merely “buying the market” ––picking a large number of

securities randomly and holding them throughout the period?

The most popular ways of measuring management’s performance are

1. Sharpe’s Performance Measure

2. Treynor’s Performance Measure

3. Jensen’s Performance Measure

SHARPE’S RATIOSharpe’s is the summary measure of portfolio performance which properly adjusts

performance for risk. It measures the risk premiums of the portfolio relative to the total

amount of risk in the portfolio.

The Sharpe’s index is given by:

Sharpe’s Index = (Average return on portfolio – Risk less rate of interest)

(Deviation of returns on portfolio)

Graphifically the index measures the slope of the line emanating from the risk less rate

outward to the portfolio in question. Thus, the Sharpe Index summarizes the risk and return

of a portfolio in a single measure that categorizes the performance of the fund on a risk-

adjusted basis. The larger the value of Sharpe Index the better the portfolio has performed.

TREYNOR’S RATIOTreynor’s ratio measures the risk premium of the portfolio, where risk premium equals the

difference between the return of the portfolio and the risk less rate. The risk premium is

related to the amount of systematic risk assumed in the portfolio. Graphically; the index

measures the slope of the line emanating outward from risk less rate to the portfolio under

consideration.

Treynors ratio is given as (Average return of portfolio –Risk less rate of interest)

Treynor Index = ------------------------------------------------------- Beta coefficient of portfolio

41

Jensen’s Performance Measure (Michael)

It refers the actual return earned in portfolio and return expected out of portfolio given its

level of risk.

CAPM – is used to calculate the expected return. The difference between the expected return

and act retain can be said the return earned out of the mandatory of systematic risk.

This excess return refers the manager’s predictive ability and managerial skills.

CAPM

rp = rf + (rm – rf)

Differential return is calculated as follows:

p = rp - rp

p =positive ––> Superior returns

p = Negative ––> Unskilled management (worse portfolio)

p = 0 ––> Neutral performance

Higher alpha represents superior performance of a fund and vice versa.

42

INDUSTRY PROFILE ( Industry profile then company profile)

Banking in India originated in the last decades of the 18th century. The oldest bank in

existence in India is the State Bank of India, a government-owned bank that traces its origins

back to June 1806 and that is the largest commercial bank in the country. Central banking is

the responsibility of the Reserve Bank of India, which in 1935 formally took over these

responsibilities from the then Imperial Bank of India, relegating it to commercial banking

functions. After India's independence in 1947, the Reserve Bank was nationalized and given

broader powers. In 1969 the government nationalized the 14 largest commercial banks; the

government nationalized the six next largest in 1980.

Currently, India has 96 scheduled commercial banks (SCBs) - 27 public sector banks (that is

with the Government of India holding a stake), 31 private banks (these do not have

government stake; they may be publicly listed and traded on stock exchanges) and 38 foreign

banks. They have a combined network of over 53,000 branches and 17,000 ATMs.

According to a report by ICRA Limited, a rating agency, the public sector banks hold over 75

percent of total assets of the banking industry, with the private and foreign banks holding

18.2% and 6.5% respectively

Early history

Banking in India originated in the last decades of the 18th century. The first banks were The

General Bank of India which started in 1786, and the Bank of Hindustan, both of which are

now defunct. The oldest bank in existence in India is the State Bank of India, which

originated in the Bank of Calcutta in June 1806, which almost immediately became the Bank

of Bengal. This was one of the three presidency banks, the other two being the Bank of

Bombay and the Bank of Madras, all three of which were established under charters from the

British East India Company. For many years the Presidency banks acted as quasi-central

banks, as did their successors. The three banks merged in 1921 to form the Imperial Bank of

India, which, upon India's independence, became the State Bank of India.

Indian merchants in Calcutta established the Union Bank in 1839, but it failed in 1848 as a

consequence of the economic crisis of 1848-49. The Allahabad Bank, established in 1865 and

still functioning today, is the oldest Joint Stock bank in India. It was not the first though. That

honor belongs to the Bank of Upper India, which was established in 1863, and which

43

survived until 1913, when it failed, with some of its assets and liabilities being transferred to

the Alliance Bank of Simla.

When the American Civil War stopped the supply of cotton to Lancashire from the

Confederate States, promoters opened banks to finance trading in Indian cotton. With large

exposure to speculative ventures, most of the banks opened in India during that period failed.

The depositors lost money and lost interest in keeping deposits with banks. Subsequently,

banking in India remained the exclusive domain of Europeans for next several decades until

the beginning of the 20th century.

Foreign banks too started to arrive, particularly in Calcutta, in the 1860s. The Comptoire

d'Escompte de Paris opened a branch in Calcutta in 1860, and another in Bombay in 1862;

branches in Madras and Pondichery, then a French colony, followed. HSBC established itself

in Bengal in 1869. Calcutta was the most active trading port in India, mainly due to the trade

of the British Empire, and so became a banking center.

The Bank of Bengal, which later became the State Bank of India.

The first entirely Indian joint stock bank was the Oudh Commercial Bank, established in

1881 in Faizabad. It failed in 1958. The next was the Punjab National Bank, established in

Lahore in 1895, which has survived to the present and is now one of the largest banks in

India.

Around the turn of the 20th Century, the Indian economy was passing through a relative

period of stability. Around five decades had elapsed since the Indian Mutiny, and the social,

industrial and other infrastructure had improved. Indians had established small banks, most of

which served particular ethnic and religious communities.

44

CHAPTER-4

Data analysis and

interpretation

46

DATA ANALYSIS AND INTERPRETATION:-

For the purpose of data analysis and interpretation the following mutual funds have been

chosen;

a) SBI Magnum Equity Fund Growth

b) Birla Sun life 95 Growth

c) Kotak 30 Growth

d) TATA Equity Management Fund Growth

Each product has been analyzed using the following tools and the results tabulated, presented

graphically and the evaluation of the same has been given under the caption 'Interpretation'

below the graph.

Calculations of Risk of SBI Magnum Equity fund Growth for the

period of 1st November to 31st November 2012

DateMarket Level

( NIFTY)

Market

Return

SBI Mag-

num Equity

fund Growth

Return

11/1/12 3033.45 21.08

11/2/12 3046.75 0.44 21.22 0.66

11/5/12 3121.45 2.45 21.69 2.21

11/6/12 3112.8 -0.28 21.86 0.78

11/7/12 2920.4 -6.18 20.7 -5.31

11/9/12 2873 -1.62 20.18 -2.51

47

11/12/12 2773.1 -3.48 19.75 -2.13

11/13/12 2744.95 -1.02 19.64 -0.56

11/14/12 2835.3 3.29 20 1.83

11/15/12 2736.7 -3.48 19.56 -2.20

11/16/12 2828.45 3.35 19.87 1.58

11/19/12 2846.2 0.63 19.98 0.55

11/20/12 2796.6 -1.74 19.63 -1.75

11/21/12 2706.15 -3.23 19.18 -2.29

11/22/12 2713.8 0.28 19.11 -0.36

11/23/12 2678.55 -1.30 18.71 -2.09

11/27/12 2771.35 3.46 19.24 2.83

11/28/12 2849.5 2.82 19.62 1.98

11/29/12 2823.95 -0.90 19.47 -0.76

11/30/12 2874.8 1.80 19.71 1.23

Average Return -0.36 -0.42

Standard deviation (Risk) 2.75 2.15

Beta 0.75

48

Graphical Presentation of SBI Magnum Equity Fund-Growth For the

month of November 12

INTERPRETATION:

SBI Magnum Equity Fund-Growth has been analyzed and it is found that there is a negative

growth. How ever on the basis of the avg returns of SBI there is a negative growth 0.42 as

against the index avg of negative 0.36 the beta being less than 1 the stock is not highly

volatile.

49

Calculations of Risk of Birla Sun life 95 Growth

for the period of 1st November to 31st November 2012

DateMarket Level

( NIFTY)

Market Re-

turn

Birla Sun life

95 GrowthReturn

11/1/12 3033.45 159.95

11/2/12 3046.75 0.44 162.21 1.41

11/5/12 3121.45 2.45 163.7 0.92

11/6/12 3112.8 -0.28 163.84 0.09

11/7/12 2920.4 -6.18 154.38 -5.77

11/9/12 2873 -1.62 154.48 0.06

11/12/12 2773.1 -3.48 152.69 -1.16

11/13/12 2744.95 -1.02 152.59 -0.07

11/14/12 2835.3 3.29 155.28 1.76

11/15/12 2736.7 -3.48 152.9 -1.53

11/16/12 2828.45 3.35 154.27 0.90

11/19/12 2846.2 0.63 156.12 1.20

11/20/12 2796.6 -1.74 155.72 -0.26

11/21/12 2706.15 -3.23 153.08 -1.70

11/22/12 2713.8 0.28 151.88 -0.78

11/23/12 2678.55 -1.30 150.67 -0.80

11/27/12 2771.35 3.46 151.51 0.56

11/28/12 2849.5 2.82 152.33 0.54

11/29/12 2823.95 -0.90 151.76 -0.37

11/30/12 2874.8 1.80 152.91 0.76

Average Return -0.36 -0.28

Standard deviation 2.75 1.69

50

Graphical Presentation of Birla Sun life 95 Growth

For the month of November 12

INTERPRETATION:

Birla Sun life 95 Growth have been analyzed and it is found that there is a negative growth.

How ever on the basis of the avg returns of Birla Sun life there is a negative growth 0.28as

against the index avg of negative 0.36 the beta being less than 1 the stock is not highly

volatile.

Calculations of Risk of Kotak 30 Growth

for the period of 1st November to 31st November 2012

Date Market

Level

Market Re-

turn (x)

Kotak 30

GrowthReturn(y)

51

( NIFTY)

11/1/12 3033.45 57.62

11/2/12 3046.75 0.44 57.94 0.56

11/5/12 3121.45 2.45 59.18 2.14

11/6/12 3112.8 -0.28 59.22 0.07

11/7/12 2920.4 -6.18 56.44 -4.69

11/9/12 2873 -1.62 55.55 -1.58

11/12/12 2773.1 -3.48 53.99 -2.81

11/13/12 2744.95 -1.02 53.55 -0.81

11/14/12 2835.3 3.29 54.64 2.04

11/15/12 2736.7 -3.48 53.31 -2.43

11/16/12 2828.45 3.35 54.56 2.34

11/19/12 2846.2 0.63 54.73 0.31

11/20/12 2796.6 -1.74 53.92 -1.48

11/21/12 2706.15 -3.23 52.47 -2.69

11/22/12 2713.8 0.28 52.5 0.06

11/23/12 2678.55 -1.30 51.76 -1.41

11/27/12 2771.35 3.46 53.03 2.45

11/28/12 2849.5 2.82 54.04 1.90

11/29/12 2823.95 -0.90 53.86 -0.33

11/30/12 2874.8 1.80 54.54 1.26

x y

52

Average Return -0.36 -0.35

Standard deviation 2.75 2.07

Beta 0.75

Graphical Presentation of KOTAK 30 Growth Fund

For the month of November 12

53

INTERPRETATION:

KOTAK 30 Growth Fund has been analyzed and it is found that there is a negative growth.

How ever on the basis of the avg returns of KOTAK there is a negative growth 0.35 as

against the index avg of negative 0.36 the beta being less than 1 the stock is not highly

volatile.

Calculations of Risk of TATA Equity Management Fund Growth

for the period of 1st November to 31st November 2012

54

DateMarket Level

( NIFTY)

Market Re-

turn (x)

TATA Equity Man-

agement Fund

Growth

Return(y)

1/11/12 3033.45 7.94

2/11/12 3046.75 0.44 7.98 0.50

5/11/12 3121.45 2.45 8.1 1.50

6/11/12 3112.8 -0.28 8.12 0.25

7/11/12 2920.4 -6.18 7.7 -5.17

9/11/12 2873 -1.62 7.57 -1.69

12/11/12 2773.1 -3.48 7.42 -1.98

13/11/12 2744.95 -1.02 7.39 -0.40

14/11/12 2835.3 3.29 7.53 1.89

15/11/12 2736.7 -3.48 7.33 -2.66

16/11/12 2828.45 3.35 7.46 1.77

19/11/12 2846.2 0.63 7.49 0.40

20/11/12 2796.6 -1.74 7.38 -1.47

21/11/12 2706.15 -3.23 7.25 -1.76

22/11/12 2713.8 0.28 7.24 -0.14

23/11/12 2678.55 -1.30 7.14 -1.38

27/11/12 2771.35 3.46 7.24 1.40

55

28/11/12 2849.5 2.82 7.35 1.52

29/11/12 2823.95 -0.90 7.34 -0.14

30/11/12 2874.8 1.80 7.42 1.09

x y

Average Return -0.36 -0.42

Standard deviation 2.75 1.86

Beta 0.65

56

Graphical presentation of TATA Equity Management Fund Growth For

the month of November 12

INTERPRETATION:

TATA Equity Management Fund Growth has been analyzed and it is found that there is a

negative growth. How ever on the basis of the avg returns of TATA Equity there is a negative

growth 0.42 as against the index avg of negative 0.36 the beta being less than 1 the stock is

not highly volatile.

57

Sharp index and Treynor index are calculated

For the month of November 12

Name of the Fund Return

(Rm)

Risk(std

dev)

Beta

(β)Rf

Sharp's Treynor

(Rm-

Rf)/σ

(Rm-

Rf)/β

SBI Magnum Equity Fund

Growth -0.42 2.15 0.75 0.06 -0.22 -0.64

Birla Sun life 95 Growth -0.28 1.69 0.51 0.06 -0.20 -0.67

Kotak 30 Growth -0.35 2.07 0.75 0.06 -0.20 -0.55

TATA Equity Management

Fund Growth-0.42 1.86 0.65 0.06 -0.26 -0.73

58

The graphical representation of Sharp Index:

INTERPRETATION:

From the above table and graph we can know that Birla sunlife and kotak are giving

good returns and they are in first position,

And the second position is SBI

59

The graphical representation of TREYNOR Index:

INTERPRETATION:

From the above table and graph we can know Kotak is performing well and it

is in first position

And the second position is SBI

The general trend in the reduction of the market price for various mutual funds

studied is not encouraging the stock market index has also been falling

continuously because of general economic slow down how ever the funds are

ranked considering sharp and trenyors in the order of performances

FINDINGS

60

SHARPE’S : As per Sharpe performance measure, a high Sharpe ratio is preferable as it

indicates a superior risk adjusted performance of a fund. From the above table Birla sun life

and kotak show a better risk-adjusted performance out of top4 AMC’S.

TREYNOR’s: As per TREYNOR’S ratio the Treynor’s reward to volatility - having high

positive index is favorable. Therefore, as per this ratio also Kotak PORTFOLIO

MANAGEMENT is preferable.

61

CHAPTER-5

SUGGESTIONS

AND

CONCLUSION

62

SUGGESTIONS

Suggestions should be in paragraph format

Investing Checklist

Financial goals & Time frame

(Are you investing for retirement? A child’s education? Or for current income? )

Risk Taking Capacity

Identify funds that fall into your Buy List

Obtain and read the offer

Documents match your objectives

In terms of equity share and bond weightings, downside risk

protection, tax benefits offered, dividend payout policy, sector focus

Performance of various funds with similar objectives for at least 3-5 years

Think hard about investing in sector funds For relatively aggressive investors

Close touch with developments in sector, review portfolio regularly – Look for `load'

costs

Management fees, annual expenses of the fund and sales loads

Look for size and credentials

Asset size less than Rs. 25 Crores

Diversify, but not too much

Invest regularly, choose the S-I-P

MF- an integral part of your savings and wealth building plans.

63

RECOMMENDATIONS AND SUGGESTIONS

1) Brand building:

Brand building is an exercise, which every business enterprise will have. Brand is the

soul of an institution; it survives on it, lives with it and cherishes it. Example: BIRLA

SUNLIFE MUTUAL FUND has a brand, every bank, insurance companies; mutual fund

companies have got their own brands.

2) Strength full Strategies:

Every AMC should try to turn into a more modern, a more vibrant, a more transparent

and regulatory compliance institution. It is with this in mind, every institution should try to

come up with verity of different type of products to fill different investment objectives

3) Marketing tools for total quality achievement:

1. Large Network.

2. Effective Man power

3. Distribution across the Market

4. Customer relations(Building better relationships)

5. Value added service

4) Innovation :

MF industry can be classified morely into three categories like equity, debt and balanced.

And there is also complexive in nature. Fund managers are not able to reach niche market.

The products are should be innovative that can meet niche market. Here MF should follow

the FMCG industry innovative strategy.

64

CONCLUSION:

From the study analysis conducted it is clear that in EQUITY FUNDS-BIRLA

SUNLIFE MUTUAL FUND is performing very well.

Investing in the KOTAK MUTUAL FUND (GROWTH) will leads to profits.

By seeing the overall performance KOTAK MUTUAL FUND is performing very

well.

The prospective investors are needed to be made aware of the investment in mutual

funds.

The Industry should keep consistency and transparency in its management and

investors objectives.

There is 100% growth of mutual fund as foreign AMCS are in queue to enter the

Indian markets.

Mutual funds can also perctrate in to rural areas.

65

BIBLIOGRAPHY

66

BIBILIOGRAPHY:

I. TEXT BOOKS

Prasanna Chandra, Financial Management: Theory and Practice, 7/e,

2008, Tata McGraw-Hill Education

Add more text books

Donald E Fischer & Ronald J Jordan,

H.Sadhak Mutual Fund in India

II. WEB SITES

www.amfiindia.com

www.religare.com

www.bseindia.com

67

Security Analysis Portfolio Management