Embed Size (px)

Citation preview

2017 WELLS FARGO INVESTMENT THOUGHT LEADERSHIP FORUM December 6, 2017

www.tpvg.com

FORWARDLOOKINGSTATEMENT

Some of the statements in this presentation constitute forward-looking statements, which relate to future events or our future performance or financial condition. The forward-lookingstatements contained in this presentation involve risks and uncertainties, including statements as to: our future operating results; our business prospects and the prospects of our portfoliocompanies ; our relationships with third-parties including venture capital investors; the impact and timing of our unfunded obligations; the expected market for venture capital investments;the performance of our portfolio and other investments that we may make in the future; the impact of investments that we expect to make; actual and potential conflicts of interest withTriplePoint Capital LLC (“TriplePoint Capital”) and TPVG Advisers LLC (our “Adviser”) and its senior investment team and Investment Committee; our contractual arrangements andrelationships with third-parties; the dependence of our future success on the general economy and its impact on the industries in which we invest; the ability of our portfolio companies toachieve their objectives; our expected financings and investments; the ability of our Adviser to attract, retain and have access to highly talented professionals, including our Adviser's seniorinvestment team; our ability to qualify and maintain our qualification as a regulated investment company, or “RIC, ” and as a business development company, or “BDC;” the adequacy of ourcash resources and working capital; and the timing of cash flows, if any, from the operations of our portfolio companies.

Such forward-looking statements may include statements preceded by, followed by or that otherwise include the words “may,” “might,” “will,” “intend,” “should,” “could,” “ca n,” “would,”“expect,” “believe,” “estimate,” “anticipate,” “predict,” “potential,” “plan” or similar words.

We have based the forward-looking statements included in this presentation on information available to us on the date of this presentation, and we assume no obligation to update any suchforward-looking statements. Actual results could differ materially from those anticipated in our forward-looking statements, and future results could differ materially from historicalperformance. Although we undertake no obligation to revise or update any forward-looking statements, whether as a result of new information, future events or otherwise, you are advised toconsult any additional disclosures that we may make directly to you or through reports that we in the future may file with the Securities and Exchange Commission (“SEC”), including annualreports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K. For a further discussion of factors that could cause our future results to differ materially from anyforward-looking statements, see the section entitled "Risk Factors" in the Company’s annual report on Form 10-K and other public filings.

Although we believe that the assumptions on whi ch these forward-looking statements are based are reasonable, any of those assumptions could prove to be inaccurate, and as a result, theforward-looking statements based on those assumptions also could be i naccurate. In light of these and other uncertainties, the inclusi on of a projection or forward-looking statement in thispresentation should not be regarded as a representation by us that our plans and objectives will be achieved. These risks and uncertainties include those described or identified in the “RiskFactors” section of the Company’s annual report on Form 10-K and elsewhere in our filings with the SEC. You should not place undue reliance on these forward-looking statements, whichapply only as of the date of this presentation.

This presentation contains statistics and other data that has been obtained from or compiled from information made available by third-party service providers. We have not independentlyverified such statistics or data.

These materials and any presentation of which they form a part are neither an offer to sell, nor a solicitation of an offer to purchase, an interest in the Company in any jurisdiction where theoffer or sale is not permitted or would be unlawful under the securities laws of such jurisdiction. The information presented i n this presentation is as of September 30, 2017 unless indi catedotherwise.

Page: 2

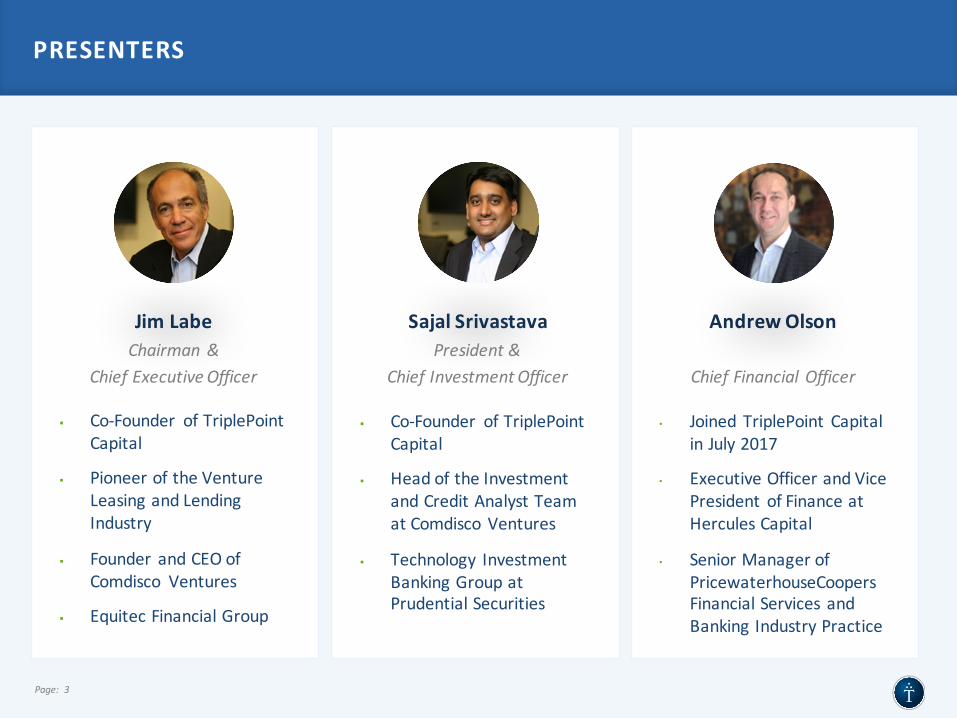

PRESENTERS

§ Co-Founder ofTriplePointCapital

§ PioneeroftheVentureLeasingandLendingIndustry

§ Founder andCEOofComdisco Ventures

§ EquitecFinancialGroup

Page: 3

§ Co-Founder ofTriplePointCapital

§ HeadoftheInvestmentandCreditAnalystTeamatComdiscoVentures

§ Technology InvestmentBankingGroupatPrudentialSecurities

JimLabeChairman&

ChiefExecutiveOfficer

SajalSrivastavaPresident&

ChiefInvestmentOfficer

• Joined TriplePoint CapitalinJuly2017

• ExecutiveOfficerandVicePresident ofFinanceatHerculesCapital

• SeniorManagerofPricewaterhouseCoopersFinancialServices andBankingIndustryPractice

AndrewOlson

ChiefFinancialOfficer

TPVGOVERVIEW

Page: 5

HIGHLYDIFFERENTIATED

BUILTFORSUCCESS

ALIGNEDWITHPUBLICSHAREHOLDERS

DELIVERINGRESULTS

- The 4 R’s -

Relationships

Reputation

References

Returns

TRIPLEPOINT VENTUREGROWTHBDCCORPOVERVIEW

HIGHLYDIFFERENTIATED

TRIPLEPOINT VENTUREGROWTHBDCCORPOVERVIEW

§ Provide highly-customized, senior secured “growth capital” loans § Targeted returns of 10% - 18% on debt investments from interest and fees§ Additional upside through equity “kickers” in the form of warrants

§ Ability to grow faster, finance business expansion & extend runway – enabling companies to achieve more milestones and command a higher future valuation

§ Longer exit timing for IPOs and M&A requires more capital§ Enables diversification of funding sources

§ Large & growing market opportunity for lending to venture growth stage companies § Highly fragmented, underserved market with high barriers to entry§ Complements equity investment from VC investors which helps to reduce downside

InvestmentObjective

UseCaseForVentureLending

MarketOpportunity

§ Lend to venture capital backed companies at the venture growth stage § Target companies backed by a select group of leading venture capital investors§ Focus on technology, life sciences, and other high growth industries§ Venture growth stage companies have distinct risk-mitigating characteristics

InvestmentStrategy

Page: 6

BUILTFORSUCCESS

TRIPLEPOINT VENTUREGROWTHBDCCORPOVERVIEW

§ Highly experienced executive and investment teams with co-founders that have worked together for more than 18 years

§ Proprietary processes benefiting from co-founders track record of lending to more than 2,000 companies and deploying more than $7 billion of capital (1)

§ TriplePoint Capital originates all deal flow – not a separate team for TPVG§ All deal flow is directly originated – do not utilize brokers/agents or syndications

§ 75% of leads and referrals are sourced from venture capital relationships

§ Managed by TriplePoint Capital, the leading global financing partner to venture capital backed companies across all stages of development

§ Exceptional brand name, reputation, track record, venture capital investor relationships and direct originations capabilities

IndustryLeadingExpertise

DirectOriginations

UniqueSponsorRelationship

§ Externally-managed business development company (BDC)§ Common stock trades on the New York Stock Exchange: “TPVG” § $75 million of notes trade on the New York Stock Exchange: “TPVY”

Structure

Page: 6 (1) Includes trackrecordpriortoTriplePoint Capital.

ALIGNEDWITHPUBLICSHAREHOLDERS

TRIPLEPOINT VENTUREGROWTHBDCCORPOVERVIEW

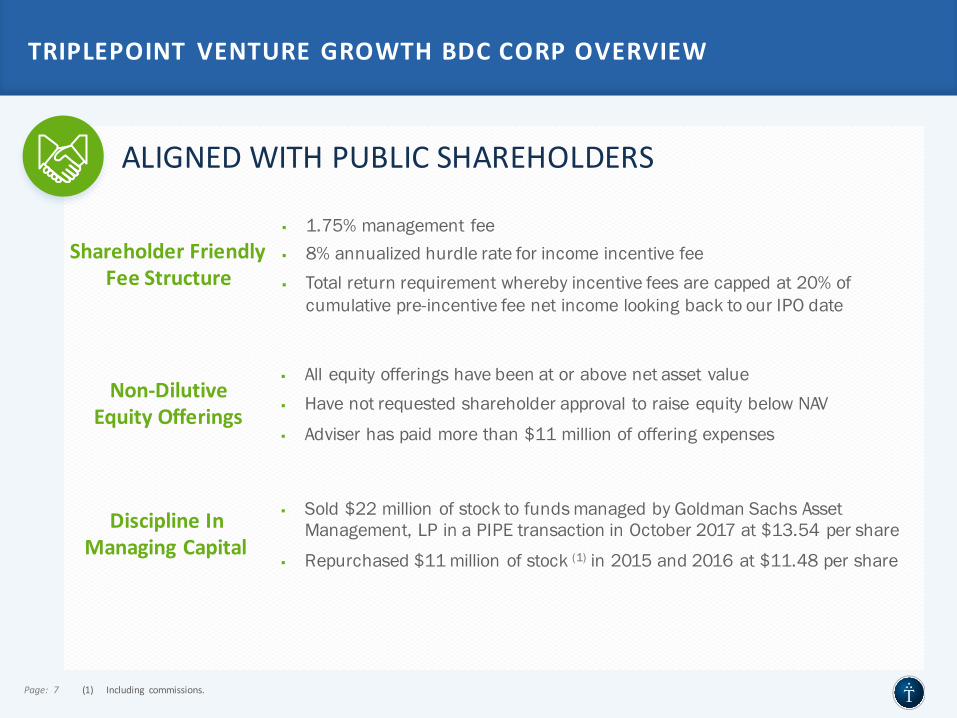

§ Sold $22 million of stock to funds managed by Goldman Sachs Asset Management, LP in a PIPE transaction in October 2017 at $13.54 per share

§ Repurchased $11 million of stock (1) in 2015 and 2016 at $11.48 per share

§ All equity offerings have been at or above net asset value§ Have not requested shareholder approval to raise equity below NAV

§ Adviser has paid more than $11 million of offering expenses

DisciplineInManagingCapital

Non-DilutiveEquityOfferings

§ 1.75% management fee§ 8% annualized hurdle rate for income incentive fee§ Total return requirement whereby incentive fees are capped at 20% of

cumulative pre-incentive fee net income looking back to our IPO date

ShareholderFriendlyFeeStructure

Page: 7 (1) Including commissions.

DELIVERINGRESULTS

Page: 8

TRIPLEPOINT VENTUREGROWTHBDCCORPOVERVIEW

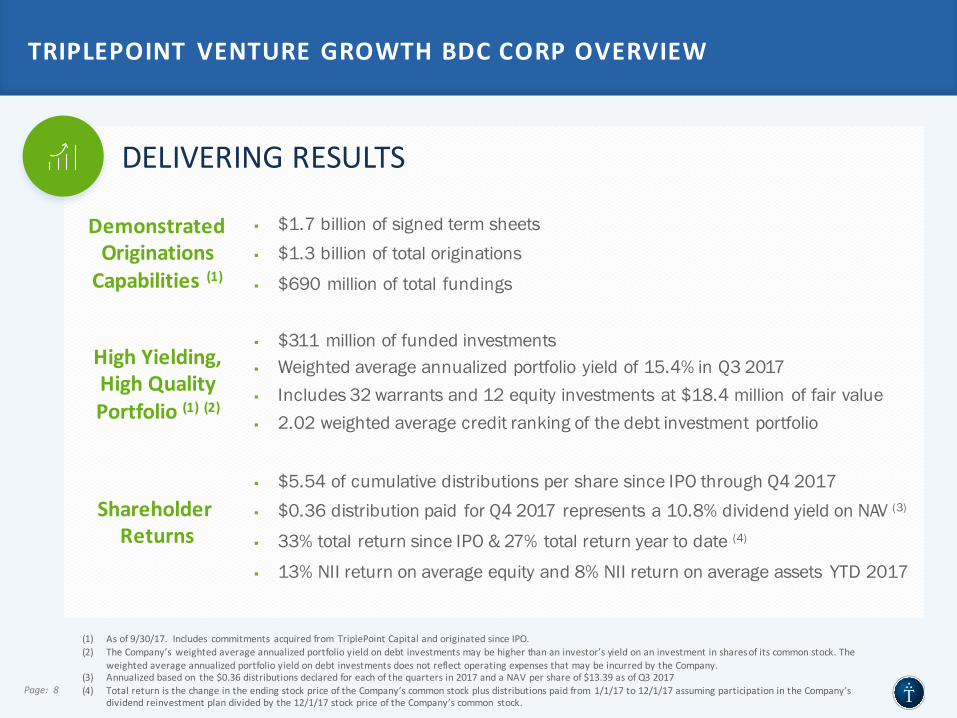

§ $5.54 of cumulative distributions per share since IPO through Q4 2017§ $0.36 distribution paid for Q4 2017 represents a 10.8% dividend yield on NAV (3)

§ 33% total return since IPO & 27% total return year to date (4)

§ 13% NII return on average equity and 8% NII return on average assets YTD 2017

§ $311 million of funded investments § Weighted average annualized portfolio yield of 15.4% in Q3 2017§ Includes 32 warrants and 12 equity investments at $18.4 million of fair value§ 2.02 weighted average credit ranking of the debt investment portfolio

ShareholderReturns

HighYielding,HighQualityPortfolio(1) (2)

§ $1.7 billion of signed term sheets§ $1.3 billion of total originations

§ $690 million of total fundings

DemonstratedOriginationsCapabilities(1)

(1) Asof9/30/17.Includes commitments acquiredfrom TriplePoint CapitalandoriginatedsinceIPO.(2) TheCompany’sweightedaverageannualizedportfolioyieldondebtinvestmentsmaybehigherthananinvestor’syieldonaninvestmentinsharesofitscommonstock.The

weightedaverageannualizedportfolioyieldondebtinvestmentsdoesnotreflectoperatingexpensesthatmaybeincurredbytheCompany.(3) Annualizedbasedon the$0.36distributionsdeclaredforeachofthequartersin2017andaNAVpershareof$13.39asofQ32017(4) TotalreturnisthechangeintheendingstockpriceoftheCompany’scommonstockplusdistributionspaidfrom 1/1/17to12/1/17assumingparticipationintheCompany’s

dividendreinvestmentplandividedbythe12/1/17stockpriceoftheCompany’scommon stock.

RECENTDEVELOPMENTS

• Signedarecord$267millionoftermsheetsandclosed$122millionofnewdebtcommitments

• Fundedrecord$83million innewdebtandequityinvestments

• 15.4%weightedaverageannualizedportfolioyieldondebtinvestmentsforthe3nd quarter

• Realized$1millionofgainsfromthesaleofwarrantsandequityinvestment,or$0.07pershare

• Issued$75million of5.75%notesdue2022(TPVY),redeemed$55millionof6.75%notes(TPVZ)

• AppointedAndrewJ.OlsonasChiefFinancialOfficer

• Declared afourthquarterdistributionof$0.36pershare,payableonDecember 1,2017

• Totalinvestmentincomeof$40million,or$2.53pershare

• Netinvestmentincomeof$21million,or$1.32pershare

• Signed$460millionoftermsheetsandclosed$265millionofnewdebtcommitments

• Funded$155million innewdebtandequityinvestmentstoeighteenportfoliocompanies

• 17.4%weightedaverageannualizedportfolioyieldondebtinvestments

• Paid$17millionofdistributions,or$1.08pershare

Page: 9

THIRDQUARTER2017 HIGHLIGHTS

YEARTODATE2017 THROUGH THETHIRD QUARTERHIGHLIGHTS

RECENTDEVELOPMENTS

STODATE• Raisedapproximately $22million inaprivateplacement, frominvestmentfundsmanagedbythe

Alternative Investments&ManagerSelection GroupofGoldmanSachsAssetManagement,L.P.purchasing1.6million sharesat$13.54pershare

• Signed$55millionoftermsheets

• Closed$65millionofnewdebtcommitments to4venturegrowthstagecompanies

• Funded$76million innewdebtandequityinvestmentsto9portfoliocompanies

• Haveachieved thelowerendofourtargetleverage ratio(0.6x)

Page: 11

FOURTHQUARTER 2017HIGHLIGHTS TODATE(1)

(1) Asof12/5/17.Theselectinformationsetforthaboveispreliminary,issubjecttocompletionofourfinancialclosingprocedures andarenotacomprehensivestatementofourfinancial resultsasofDecember5,2017.Ouractualresultsasof12/31/17maydiffermateriallyasaresultofthecompletion oftheperiodandourfinancialclosingprocedures,finaladjustmentsandotherdevelopmentswhichmayarisebetweennowandthetimethatourfinancialresultsarefinalized.

TPVGBUSINESSHIGHLIGHTS

TRUSTEDPARTNERTOINDUSTRY LEADINGVENTUREBACKEDCOMPANIES

Page: 13(1) SelectedlistofcurrentandpastTPVGportfoliocompanies.

TRIPLEPOINT CAPITAL PLATFORM OVERVIEW

Page: 14

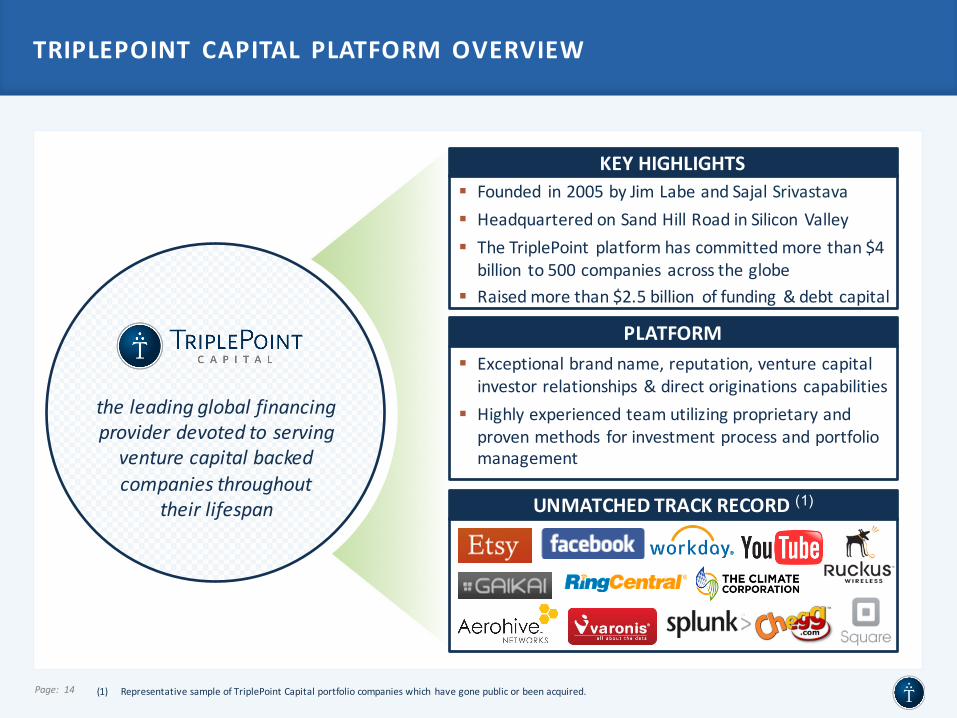

theleadingglobalfinancingproviderdevoted toservingventurecapitalbackedcompaniesthroughout

theirlifespan

(1) RepresentativesampleofTriplePoint Capitalportfoliocompanieswhich havegonepublicorbeenacquired.

KEYHIGHLIGHTS§ Founded in2005byJim LabeandSajalSrivastava§ HeadquarteredonSandHillRoadinSiliconValley§ TheTriplePoint platformhascommittedmorethan$4billion to500companies acrosstheglobe

§ Raisedmorethan$2.5billion offunding& debtcapital

PLATFORM§ Exceptionalbrandname,reputation,venturecapitalinvestorrelationships&directoriginations capabilities

§ Highlyexperiencedteamutilizingproprietaryandprovenmethods forinvestmentprocessandportfoliomanagement

UNMATCHEDTRACKRECORD(1)

TRIPLEPOINT CAPITAL’S UNIQUE LIFESPAN APPROACH

Page: 15

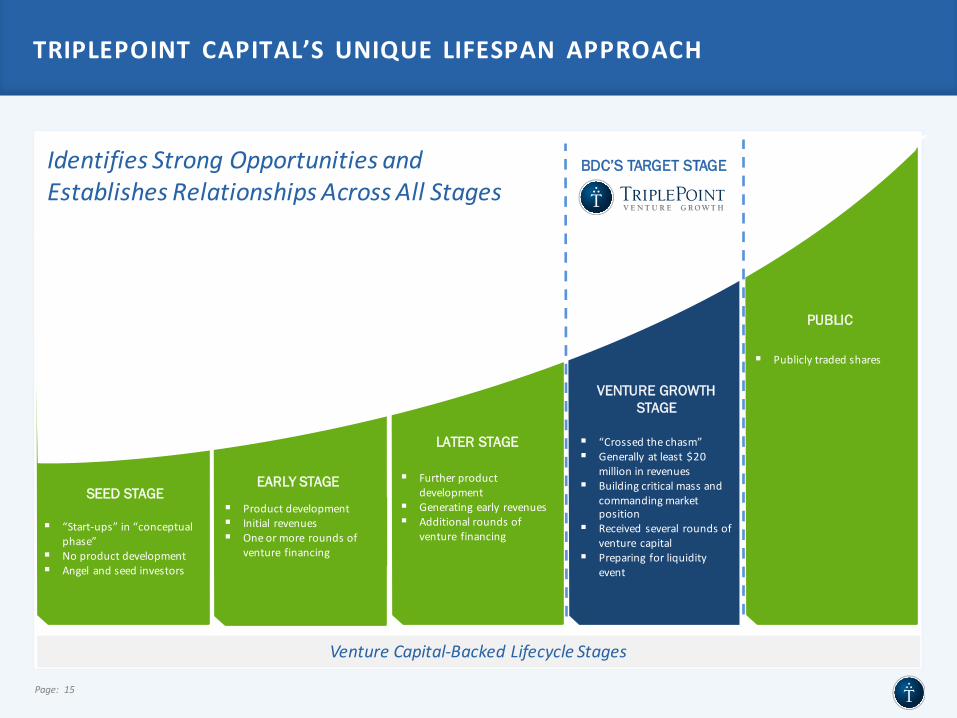

SEED STAGEEARLY STAGE

LATER STAGE

VENTURE GROWTHSTAGE

PUBLIC

§ “Start-ups”in“conceptualphase”

§ Noproductdevelopment§ Angelandseedinvestors

§ Productdevelopment§ Initial revenues§ Oneormore roundsof

venture financing

§ Furtherproductdevelopment

§ Generatingearly revenues§ Additionalroundsof

venture financing

§ “Crossedthechasm”§ Generallyatleast$20

millioninrevenues§ Buildingcriticalmassand

commandingmarketposition

§ Receivedseveral roundsofventurecapital

§ Preparing forliquidityevent

§ Publiclytradedshares

VentureCapital-BackedLifecycleStages

IdentifiesStrongOpportunitiesandEstablishesRelationshipsAcrossAllStages

BDC’S TARGET STAGE

WeTakeOurCustomersThroughtheRedZonetotheEndZone

TPVG’SAPPROACH/VENTUREGROWTHSTAGE

Page: 16

VentureGrowthStage

SeedStage

EarlyStage

LaterStage

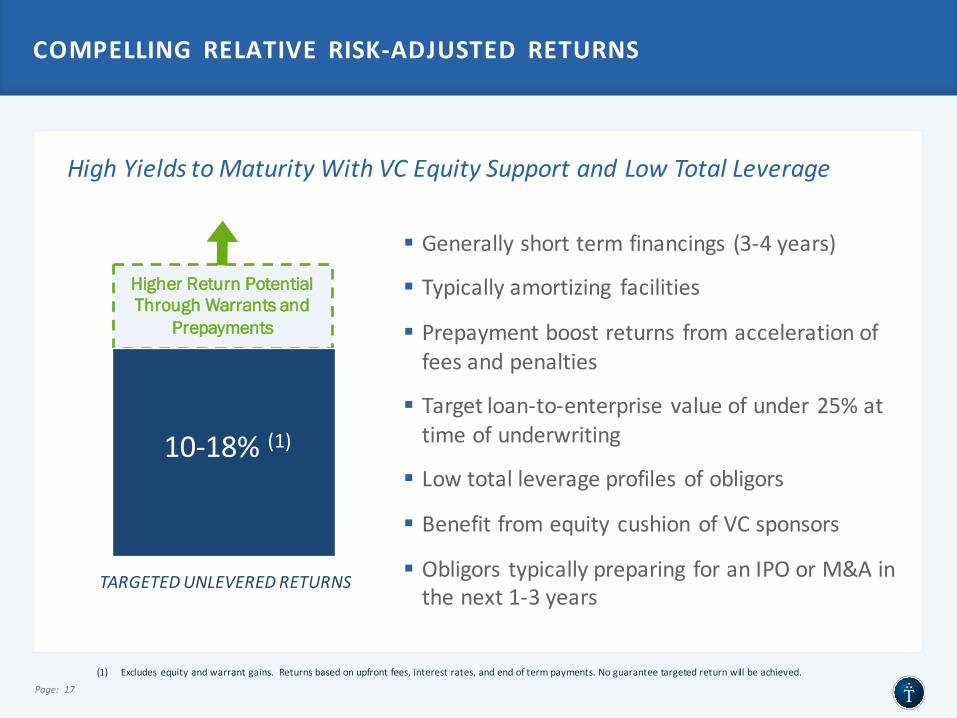

COMPELLING RELATIVE RISK-ADJUSTED RETURNS

Page: 17

(1) Excludes equityandwarrantgains.Returnsbasedonupfrontfees,interestrates,andendoftermpayments.Noguaranteetargetedreturnwillbeachieved.

§ Generallyshorttermfinancings (3-4years)

§ Typicallyamortizing facilities

§ Prepaymentboostreturns fromaccelerationoffeesandpenalties

§ Targetloan-to-enterprisevalueofunder25%attimeofunderwriting

§ Lowtotalleverageprofilesofobligors

§ BenefitfromequitycushionofVCsponsors

§ Obligors typicallypreparing foranIPOorM&Ainthenext1-3years

HighYieldstoMaturityWithVCEquitySupportandLowTotalLeverage

10-18%(1)

Higher Return Potential Through Warrants and

Prepayments

TARGETEDUNLEVEREDRETURNS

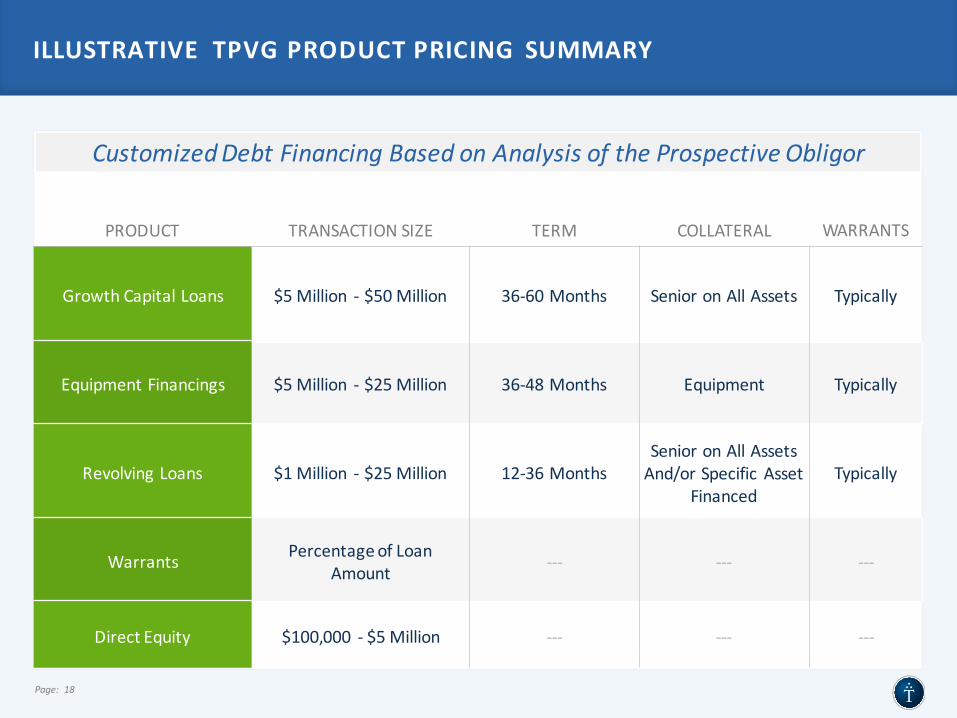

PRODUCT TRANSACTIONSIZE TERM COLLATERAL WARRANTS

GrowthCapitalLoans $5Million - $50Million 36-60Months SenioronAllAssets Typically

EquipmentFinancings $5Million - $25Million 36-48Months Equipment Typically

RevolvingLoans $1Million - $25Million 12-36MonthsSenioronAllAssetsAnd/orSpecific Asset

FinancedTypically

Warrants PercentageofLoanAmount --- --- ---

DirectEquity $100,000 - $5Million --- --- ---

CustomizedDebtFinancingBasedonAnalysisoftheProspectiveObligor

ILLUSTRATIVE TPVGPRODUCTPRICING SUMMARY

Page: 18

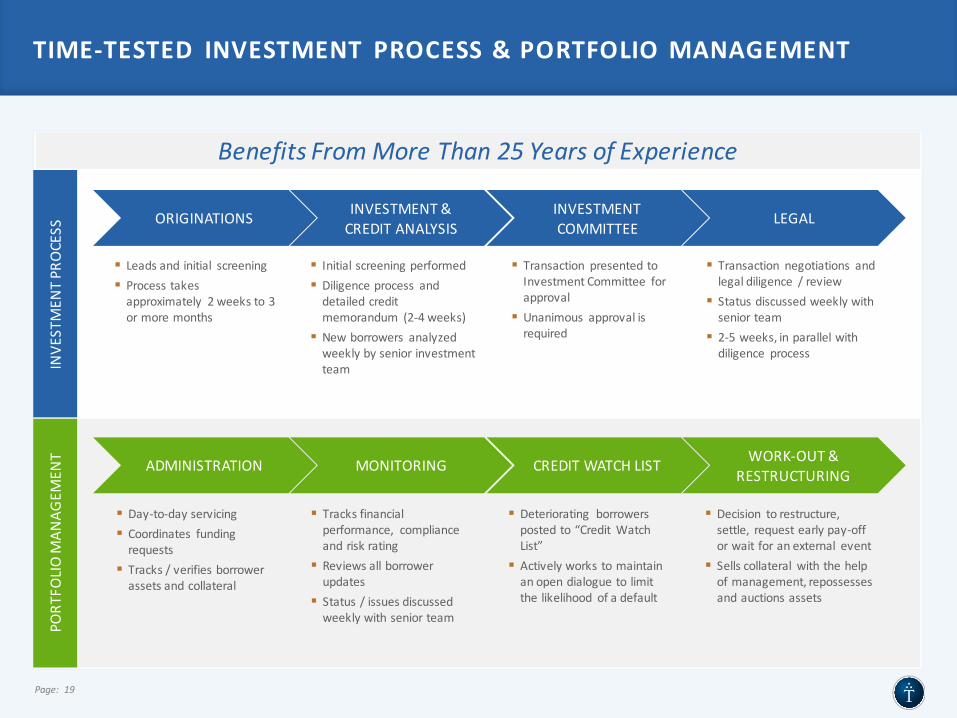

TIME-TESTED INVESTMENT PROCESS&PORTFOLIOMANAGEMENT

Page: 19

§ Leadsandinitial screening§ Processtakesapproximately 2weeksto3ormoremonths

§ Initialscreeningperformed§ Diligenceprocess anddetailedcreditmemorandum (2-4weeks)

§ Newborrowers analyzedweeklybyseniorinvestmentteam

§ Transaction presentedtoInvestmentCommittee forapproval

§ Unanimous approvalisrequired

§ Transaction negotiations andlegaldiligence /review

§ Statusdiscussedweeklywithseniorteam

§ 2-5weeks,inparallelwithdiligence process

§ Day-to-dayservicing§ Coordinates fundingrequests

§ Tracks/verifiesborrowerassetsandcollateral

§ Tracksfinancialperformance, complianceandriskrating

§ Reviewsallborrowerupdates

§ Status/issuesdiscussedweeklywithseniorteam

§ Deteriorating borrowerspostedto“CreditWatchList”

§ Activelyworkstomaintainanopendialoguetolimitthelikelihood ofadefault

§ Decision torestructure,settle, requestearlypay-offorwaitforanexternal event

§ Sellscollateral withthehelpofmanagement,repossessesandauctionsassets

INVE

STMEN

TPR

OCESS

PORT

FOLIOMAN

AGEM

ENT

BenefitsFromMoreThan25YearsofExperience

ADMINISTRATION MONITORING CREDITWATCHLIST WORK-OUT&RESTRUCTURING

ORIGINATIONS INVESTMENT&CREDITANALYSIS

INVESTMENTCOMMITTEE

LEGAL

TPVGPORTFOLIOHIGHLIGHTS

HIGHYIELDING, HIGHQUALITY PORTFOLIO (1)(2 )

Page: 21

DEBTINVESTMENTFAIRVALUE$292.7Million

DEBTINVESTMENTCOSTBASIS$294.7 Million

NUMBEROFOBLIGORS19

NUMBEROFLOANS53

(1) FairvalueasofSeptember30,2017.(2)AlldataasofSeptember30,2017unlessindicated.

DEBTPORTFOLIO

$292.7MILLION(1)

WEIGHTEDAVERAGEYIELDONDEBTINVESTMENTS15.4%

COUPONINCOME10.4%

OID0.9%

ENDOFTERMPAYMENTS2.2%

PREPAYMENTS1.9%

YIELDPROFILE

15.4%YIELD

$158.2MILLION(2)

WARRANTPORTFOLIO

$10.7MILLION(1)

$158.2MILLION(2)

EQUITYPORTFOLIO

$7.7MILLION(1)

WARRANTFAIRVALUE$10.7Million

WARRANTCOSTBASIS$8.4Million

NUMBEROFWARRANTS32

NUMBEROFCOMPANIES32

DIRECTEQUITYFAIRVALUE$7.7Million

DIRECTEQUITYCOSTBASIS$6.1Million

NUMBEROFINVESTMENTS12

NUMBEROFCOMPANIES9

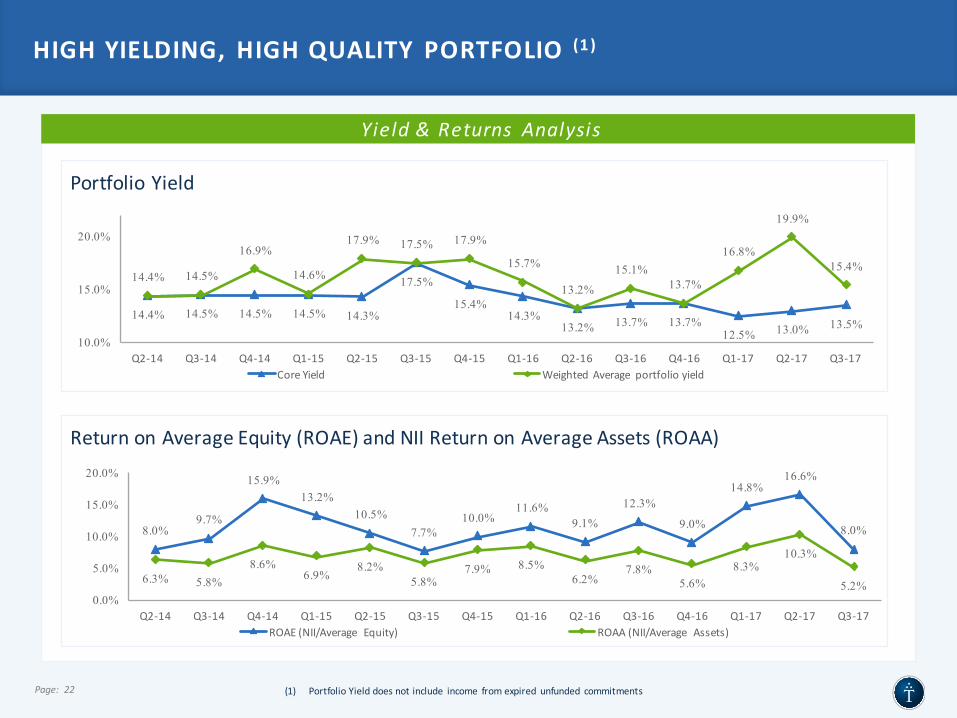

Yield&Returns Analysis

PortfolioYield

14.4% 14.5% 14.5% 14.5% 14.3%

17.5%

15.4%14.3%

13.2% 13.7% 13.7%12.5% 13.0% 13.5%

14.4% 14.5%

16.9%

14.6%

17.9% 17.5% 17.9%

15.7%

13.2%

15.1%13.7%

16.8%

19.9%

15.4%

10.0%

15.0%

20.0%

Q2-14 Q3-14 Q4-14 Q1-15 Q2-15 Q3-15 Q4-15 Q1-16 Q2-16 Q3-16 Q4-16 Q1-17 Q2-17 Q3-17CoreYield WeightedAverage portfolioyield

ReturnonAverageEquity(ROAE)andNIIReturnonAverageAssets(ROAA)

Page: 22

8.0%9.7%

15.9%13.2%

10.5%7.7%

10.0%11.6%

9.1%

12.3%

9.0%

14.8%16.6%

8.0%

6.3% 5.8%8.6%

6.9%8.2%

5.8%7.9% 8.5%

6.2%7.8%

5.6%8.3%

10.3%

5.2%0.0%

5.0%

10.0%

15.0%

20.0%

Q2-14 Q3-14 Q4-14 Q1-15 Q2-15 Q3-15 Q4-15 Q1-16 Q2-16 Q3-16 Q4-16 Q1-17 Q2-17 Q3-17ROAE(NII/Average Equity) ROAA(NII/Average Assets)

HIGHYIELDING, HIGHQUALITY PORTFOLIO (1)

(1) PortfolioYielddoesnotinclude income fromexpired unfunded commitments

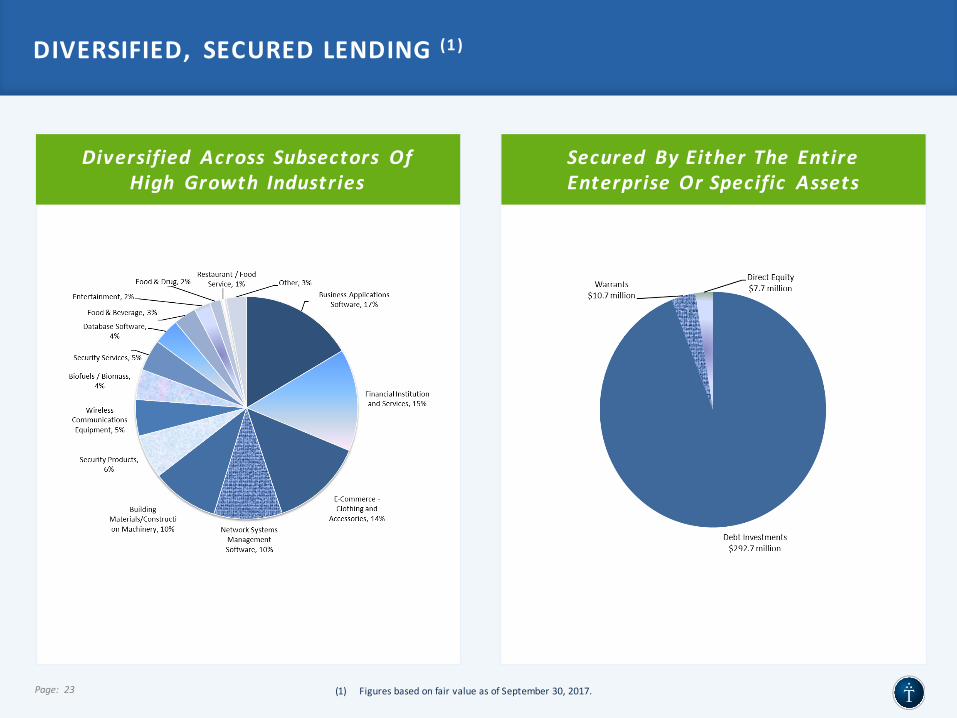

DIVERSIFIED, SECUREDLENDING (1)

Page: 23 (1) FiguresbasedonfairvalueasofSeptember30,2017.

Diversified Across Subsectors OfHigh Growth Industries

Secured ByEitherThe EntireEnterprise OrSpecific Assets

Strictly Confidential

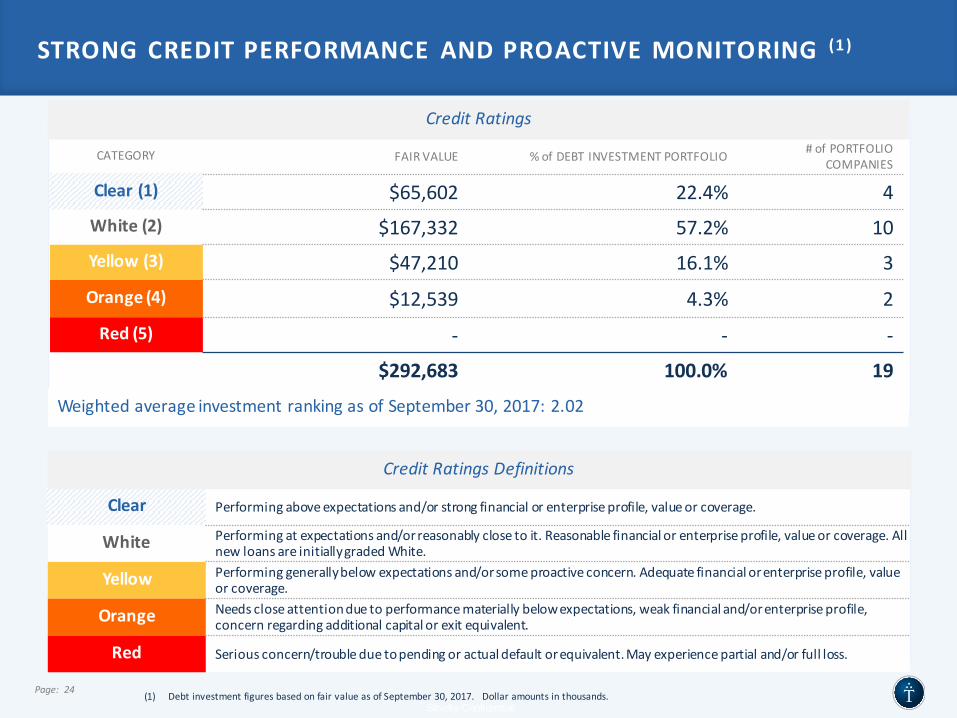

STRONGCREDITPERFORMANCE ANDPROACTIVEMONITORING (1)

Page: 24 (1) DebtinvestmentfiguresbasedonfairvalueasofSeptember30,2017.Dollaramountsinthousands.

Clear Performingaboveexpectationsand/orstrongfinancialorenterpriseprofile,valueorcoverage.

White Performingatexpectationsand/orreasonablyclosetoit.Reasonablefinancialorenterpriseprofile,valueorcoverage.AllnewloansareinitiallygradedWhite.

Yellow Performinggenerallybelowexpectationsand/orsomeproactiveconcern.Adequatefinancialorenterpriseprofile,valueorcoverage.

Orange Needscloseattentionduetoperformancemateriallybelowexpectations,weakfinancialand/orenterpriseprofile,concernregardingadditionalcapitalorexitequivalent.

Red Seriousconcern/troubleduetopendingoractualdefaultorequivalent.Mayexperiencepartialand/orfullloss.

CreditRatingsDefinitions

CATEGORY FAIRVALUE % ofDEBTINVESTMENTPORTFOLIO #ofPORTFOLIOCOMPANIES

Clear(1) $65,602 22.4% 4White(2) $167,332 57.2% 10Yellow(3) $47,210 16.1% 3Orange(4) $12,539 4.3% 2Red(5) - - -

$292,683 100.0% 19

WeightedaverageinvestmentrankingasofSeptember30,2017:2.02

CreditRatings

TPVGFINANCIALHIGHLIGHTS

Page: 26

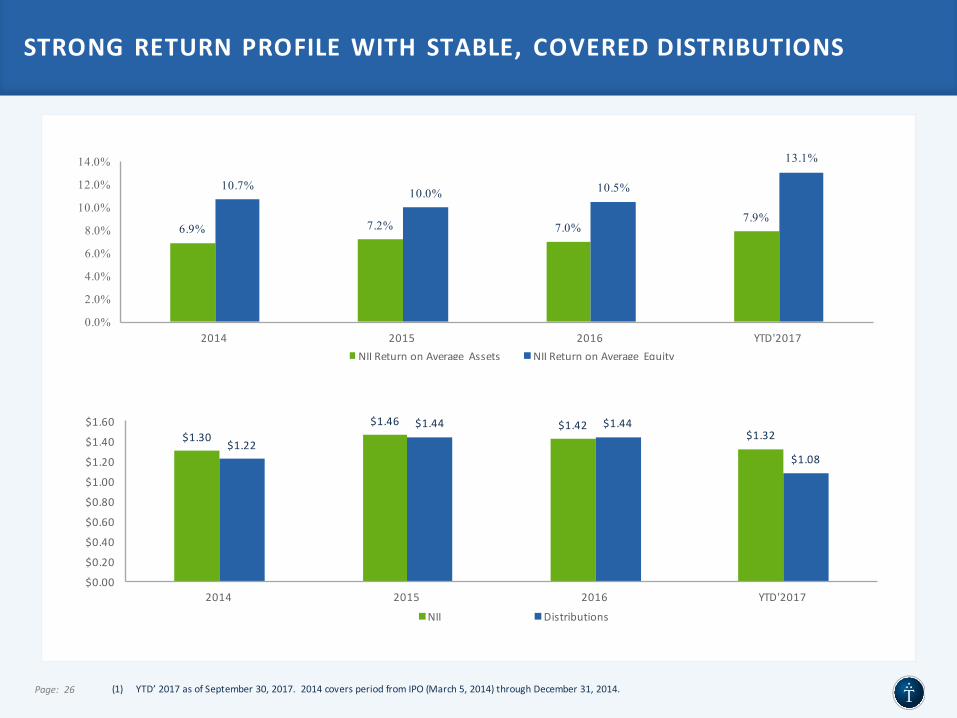

STRONGRETURNPROFILEWITHSTABLE, COVEREDDISTRIBUTIONS

(1) YTD’2017asofSeptember30,2017.2014coversperiodfromIPO(March5,2014)throughDecember31,2014.

6.9% 7.2% 7.0%7.9%

10.7%10.0% 10.5%

13.1%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

2014 2015 2016 YTD'2017NIIReturnonAverage Assets NIIReturnonAverage Equity

(1)

$1.30$1.46 $1.42

$1.32$1.22

$1.44 $1.44

$1.08

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

2014 2015 2016 YTD'2017

NII Distributions

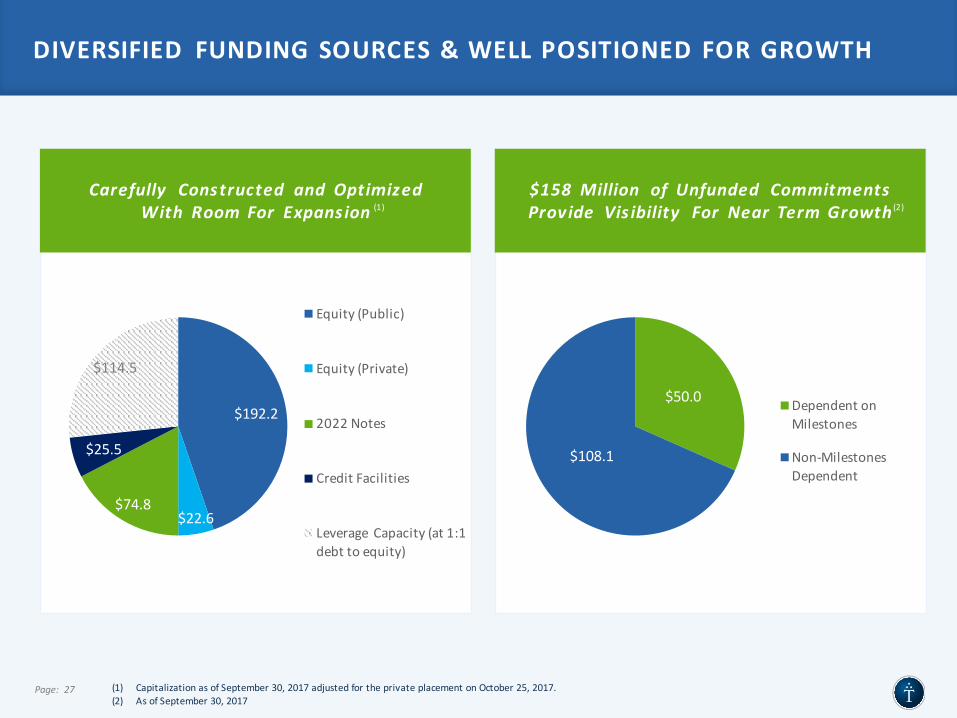

DIVERSIFIED FUNDINGSOURCES&WELLPOSITIONEDFORGROWTH

Page: 27 (1) CapitalizationasofSeptember30,2017adjustedfortheprivateplacementonOctober25,2017.(2) AsofSeptember30,2017

$192.2

$22.6$74.8

$25.5

$114.5

Equity(Public)

Equity(Private)

2022Notes

CreditFacilities

Leverage Capacity(at1:1debttoequity)

$158 Million of Unfunded Commitments Provide Vis ibility For Near TermGrowth

Carefully Constructed and OptimizedWith RoomFor Expans ion (1)

$50.0

$108.1

DependentonMilestones

Non-MilestonesDependent

(2)

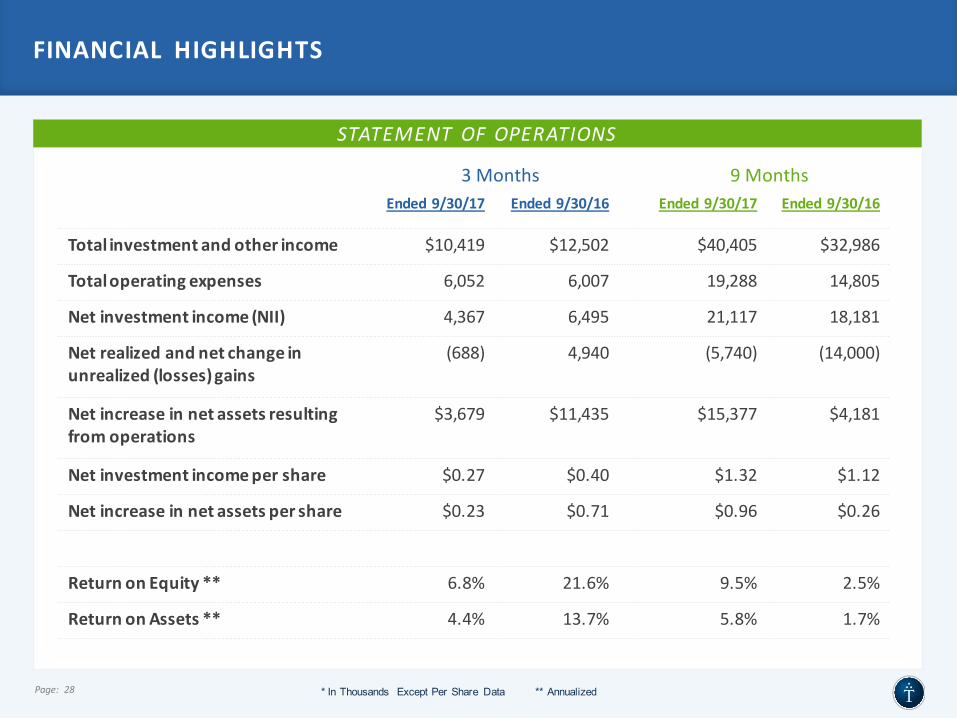

FINANCIAL HIGHLIGHTS

Page: 28

Ended9/30/17 Ended 9/30/16 Ended 9/30/17 Ended 9/30/16

Totalinvestmentand otherincome $10,419 $12,502 $40,405 $32,986

Totaloperatingexpenses 6,052 6,007 19,288 14,805

Netinvestmentincome(NII) 4,367 6,495 21,117 18,181

Netrealizedandnetchange inunrealized(losses)gains

(688) 4,940 (5,740) (14,000)

Netincreaseinnetassetsresultingfromoperations

$3,679 $11,435 $15,377 $4,181

Netinvestmentincomepershare $0.27 $0.40 $1.32 $1.12

Netincreaseinnetassetspershare $0.23 $0.71 $0.96 $0.26

ReturnonEquity** 6.8% 21.6% 9.5% 2.5%

ReturnonAssets** 4.4% 13.7% 5.8% 1.7%

* In Thousands Except Per Share Data ** Annualized

STATEMENTOFOPERATIONS

3Months 9Months

FINANCIAL HIGHLIGHTS

Page: 29 * In Thousands Except Per Share Data ** Includes Restricted Cash

9/30/17 6/30/17 12/31/16 9/30/16

Investmentsatfairvalue $311,136 $253,804 $374,311 $308,857

Short-terminvestments $94,962 $89,943 $39,990 $79,829

Cash** $8,472 $83,471 $15,478 $20,762

Totalassets $417,605 $430,595 $434,222 $414,346

Borrowings $97,802 $113,477 $168,288 $110,194

Totalliabilities $202,846 $214,062 $218,359 $199,954

Totalnetassets $214,759 $216,533 $215,863 $214,392

Netassetvaluepershare $13.39 $13.52 $13.51 $13.44

STATEMENTOF ASSETS&LIABILITIES

Page: 30

HIGHLYDIFFERENTIATED

BUILTFORSUCCESS

ALIGNEDWITHPUBLICSHAREHOLDERS

DELIVERINGRESULTS

- The 4 R’s -

Relationships

Reputation

References

Returns

TRIPLEPOINT VENTUREGROWTHBDCCORP

Strictly Confidential

RESEARCHCOVERAGE

Page: 31

MitchelPenn(410)583-5976

JonathanBock(704)410-1874

CaseyAlexander(646)452-7083

APPENDIX

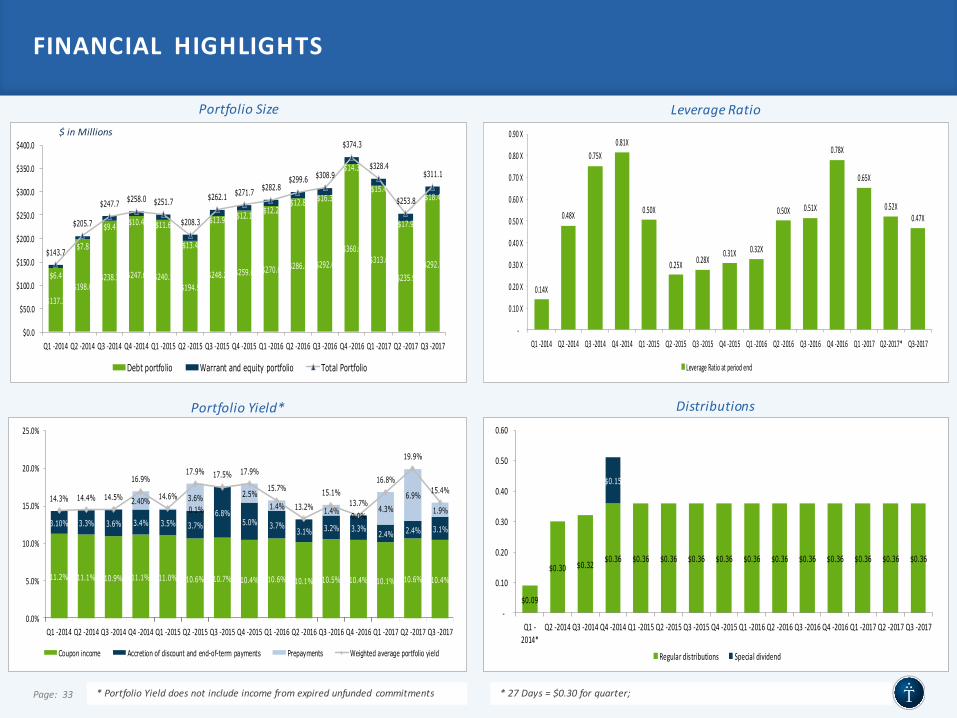

FINANCIAL HIGHLIGHTS

PortfolioSize LeverageRatio

PortfolioYield* Distributions

*27Days=$0.30forquarter;*PortfolioYielddoesnotincludeincomefromexpiredunfunded commitments

$137.3$198.0

$238.3 $247.6 $240.1 $194.9

$248.2 $259.6 $270.6 $286.8 $292.6

$360.0 $313.0

$235.9 $292.7

$6.4

$7.8

$9.4 $10.4 $11.6

$13.4

$13.9 $12.1 $12.2 $12.8 $16.3

$14.3

$15.4

$17.9

$18.4

$143.7

$205.7

$247.7 $258.0 $251.7

$208.3

$262.1 $271.7 $282.8 $299.6 $308.9

$374.3

$328.4

$253.8

$311.1

$0.0

$50.0

$100.0

$150.0

$200.0

$250.0

$300.0

$350.0

$400.0

Q1-2014 Q2-2014 Q3-2014 Q4-2014 Q1-2015 Q2-2015 Q3-2015 Q4-2015 Q1-2016 Q2-2016 Q3-2016 Q4-2016 Q1-2017 Q2-2017 Q3-2017

Debt portfolio Warrant and equity portfolio Total Portfolio

0.14X

0.48X

0.75X0.81X

0.50X

0.25X 0.28X0.31X 0.32X

0.50X 0.51X

0.78X

0.65X

0.52X0.47X

-

0.10X

0.20X

0.30X

0.40X

0.50X

0.60X

0.70X

0.80X

0.90X

Q1-2014 Q2-2014 Q3-2014 Q4-2014 Q1-2015 Q2-2015 Q3-2015 Q4-2015 Q1-2016 Q2-2016 Q3-2016 Q4-2016 Q1-2017 Q2-2017* Q3-2017

LeverageRatioatperiodend

$0.09

$0.30 $0.32$0.36 $0.36 $0.36 $0.36 $0.36 $0.36 $0.36 $0.36 $0.36 $0.36 $0.36 $0.36

$0.15

-

0.10

0.20

0.30

0.40

0.50

0.60

Q1-2014*

Q2-2014 Q3-2014 Q4-2014 Q1-2015 Q2-2015 Q3-2015 Q4-2015 Q1-2016 Q2-2016 Q3-2016 Q4-2016 Q1-2017 Q2-2017 Q3-2017

Regulardistributions Specialdividend

11.2% 11.1% 10.9% 11.1% 11.0% 10.6% 10.7% 10.4% 10.6% 10.1% 10.5% 10.4% 10.1% 10.6% 10.4%

3.10% 3.3% 3.6% 3.4% 3.5% 3.7%6.8%

5.0% 3.7%3.1% 3.2% 3.3% 2.4% 2.4% 3.1%

2.40%0.1%3.6% 2.5%

1.4% 1.4% 0.0%4.3%

6.9%

1.9%14.3% 14.4% 14.5%

16.9%

14.6%

17.9% 17.5% 17.9%

15.7%

13.2%

15.1%13.7%

16.8%

19.9%

15.4%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Q1-2014 Q2-2014 Q3-2014 Q4-2014 Q1-2015 Q2-2015 Q3-2015 Q4-2015 Q1-2016 Q2-2016 Q3-2016 Q4-2016 Q1-2017 Q2-2017 Q3-2017

Coupon income Accretion of discount and end-of-term payments Prepayments Weighted average portfolio yield

$inMillions

Page: 33

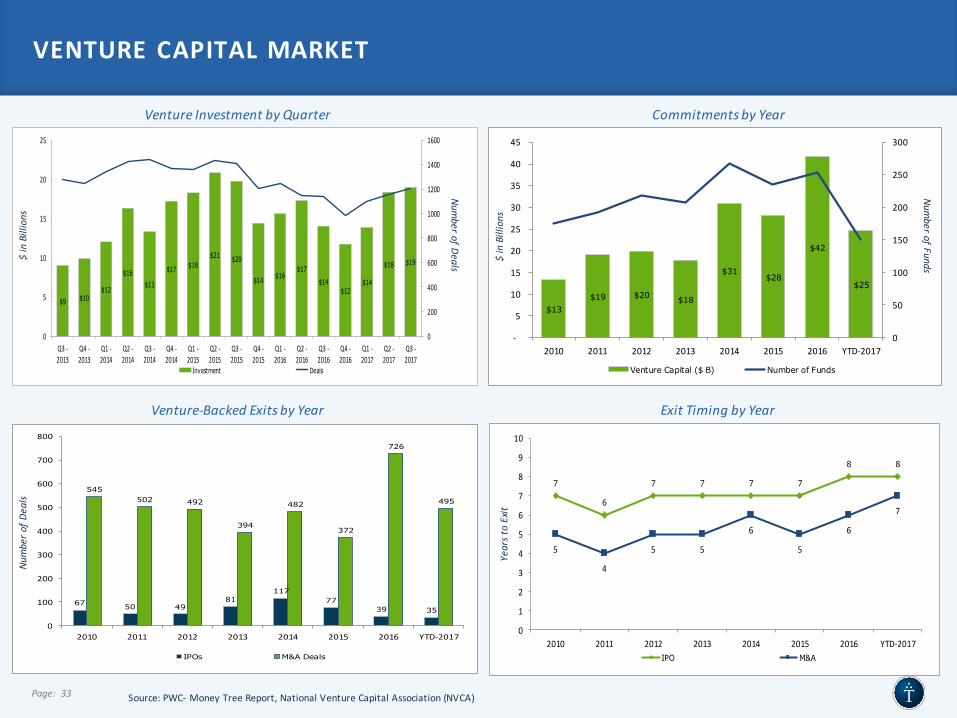

VENTURECAPITALMARKET

Page: 33

VentureInvestmentbyQuarter CommitmentsbyYear

Venture-BackedExitsbyYear ExitTimingbyYear

Source:PWC- MoneyTreeReport,NationalVentureCapitalAssociation(NVCA)

$9 $10$12

$16$13

$17 $18$21 $20

$14 $16$17

$14$12

$14

$18 $19

0

200

400

600

800

1000

1200

1400

1600

0

5

10

15

20

25

Q3-2013

Q4-2013

Q1-2014

Q2-2014

Q3-2014

Q4-2014

Q1-2015

Q2-2015

Q3-2015

Q4-2015

Q1-2016

Q2-2016

Q3-2016

Q4-2016

Q1-2017

Q2-2017

Q3-2017

Investment Deals

$inBillions

NumberofDeals

$13$19 $20 $18

$31$28

$42

$25

0

50

100

150

200

250

300

-

5

10

15

20

25

30

35

40

45

2010 2011 2012 2013 2014 2015 2016 YTD-2017

Venture Capital ($ B) Number of Funds

$inBillions

NumberofFunds

67 50 4981

11777

39 35

545502 492

394

482

372

726

495

0

100

200

300

400

500

600

700

800

2010 2011 2012 2013 2014 2015 2016 YTD-2017

IPOs M&A Deals

Numbero

fDeals

7

6

7 7 7 7

8 8

5

4

5 5

6

5

6

7

0

1

2

3

4

5

6

7

8

9

10

2010 2011 2012 2013 2014 2015 2016 YTD-2017IPO M&A

YearstoExit

COMPETITIVE LANDSCAPE

FragmentedMarketwithLimitedCompetitionGivenHighBarrierstoEntry

Page: 35

EARLYSTAGEVENTURE

DEBTFUNDS

OTHERVENTUREBDCsVENTURE

BANKS

LATERSTAGEVENTURE

DEBTFUNDS

OPPORTUNISTICDEBTFUNDS

EarlyStage

LaterStage

Public

SeedStage

VentureGrowthStage