Embed Size (px)

Citation preview

2016/17

Vietnam

PKF Worldwide Tax Guide 2016/17 1

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there double tax treaties in place? How will foreign source income be taxed? Since 1994, the PKF network of independent member firms, administered by PKF International Limited, has produced the PKF Worldwide Tax Guide (WWTG) to provide international businesses with the answers to these key tax questions. As you will appreciate, the production of the WWTG is a huge team effort and we would like to thank all tax experts within PKF member firms who gave up their time to contribute the vital information on their country's taxes that forms the heart of this publication. The PKF Worldwide Tax Guide 2016/17 (WWTG) is an annual publication that provides an overview of the taxation and business regulation regimes of the world's most significant trading countries. In compiling this publication, member firms of the PKF network have based their summaries on information current on 30 April 2016, while also noting imminent changes where necessary. On a country-by-country basis, each summary such as this one, addresses the major taxes applicable to business; how taxable income is determined; sundry other related taxation and business issues; and the country's personal tax regime. The final section of each country summary sets out the Double Tax Treaty and Non-Treaty rates of tax withholding relating to the payment of dividends, interest, royalties and other related payments. While the WWTG should not to be regarded as offering a complete explanation of the taxation issues in each country, we hope readers will use the publication as their first point of reference and then use the services of their local PKF member firm to provide specific information and advice. Services provided by member firms include: Assurance & Advisory;

Financial Planning / Wealth Management;

Corporate Finance;

Management Consultancy;

IT Consultancy;

Insolvency - Corporate and Personal;

Taxation;

Forensic Accounting; and,

Hotel Consultancy. In addition to the printed version of the WWTG, individual country taxation guides such as this are available in PDF format which can be downloaded from the PKF website at www.pkf.com

Vietnam

PKF Worldwide Tax Guide 2016/17 2

IMPORTANT DISCLAIMER This publication should not be regarded as offering a complete explanation of the taxation matters that are contained within this publication. This publication has been sold or distributed on the express terms and understanding that the publishers and the authors are not responsible for the results of any actions which are undertaken on the basis of the information which is contained within this publication, nor for any error in, or omission from, this publication. The publishers and the authors expressly disclaim all and any liability and responsibility to any person, entity or corporation who acts or fails to act as a consequence of any reliance upon the whole or any part of the contents of this publication. Accordingly no person, entity or corporation should act or rely upon any matter or information as contained or implied within this publication without first obtaining advice from an appropriately qualified professional person or firm of advisors, and ensuring that such advice specifically relates to their particular circumstances. PKF International Limited (PKFI) administers a family of legally independent firms. Neither PKFI nor the member firms of the network generally accept any responsibility or liability for the actions or inactions of any individual member or correspondent firm or firms. PKF INTERNATIONAL LIMITED JUNE 2016 © PKF INTERNATIONAL LIMITED All RIGHTS RESERVED USE APPROVED WITH ATTRIBUTION

Vietnam

PKF Worldwide Tax Guide 2016/17 3

STRUCTURE OF COUNTRY DESCRIPTIONS A. TAXES PAYABLE

COMPANY TAX - CORPORATE INCOME TAX (CIT) CAPITAL GAINS TAX BRANCH PROFITS TAX VALUE ADDED TAX (VAT) EXCISE TAX BUSINESS LICENCE TAX EXPORT – IMPORT TAX NATURAL RESOURCES TAX

B. DETERMINATION OF TAXABLE INCOME

DIVIDENDS LOSSES FOREIGN SOURCE INCOME TAX INCENTIVES

C. FOREIGN TAX RELIEF D. WITHHOLDING TAX E. EXCHANGE CONTROL F. PERSONAL TAX G. TREATY AND NON-TREATY WITHHOLDING TAX RATES

Vietnam

PKF Worldwide Tax Guide 2016/17 4

MEMBER FIRM City Name Contact Information Hanoi Nguyen Nhu Tien +849 12 005 808 [email protected] Ho Chi Minh City To Buu Toan +849 18 658 699 [email protected] BASIC FACTS Full name: Socialist Republic of Vietnam Capital: Hanoi Main languages: Vietnamese Population: 91,903,961 (2015 estimate) Major religion: Buddhism, Christianity and indigenous religions Monetary units: Vietnam Dong (VND) Internet domain: com.vn Int. dialling code: +84 KEY TAX POINTS • Corporate Income Tax is charged on any Enterprise carrying on a trade, business in Vietnam. All

Incomes (including incomes from overseas) of the Enterprises registered in accordance with the Law of Enterprises are subject to Corporate Income Tax (CIT).

• For resident individuals Personal, Income Tax is levied on their Incomes earned within and outside Vietnam’s territory, while non-residents are taxed only on their Incomes earned in Vietnam.

• Value Added Tax (VAT) is a tax levied on import goods and goods and service used in manufacturing, trading or consumption in Vietnam (except for exempted cases stipulated in law). There are two (2) methods to calculate VAT, which are credit-invoice method and direct method.

• Excise Tax is applied to specific luxury goods and services. A. TAXES PAYABLE COMPANY TAX - CORPORATE INCOME TAX (CIT) CIT rate generally applied is 22% and the rate from 32% to 50 % is applied to the business establishments involved in the prospecting, exploration and exploitation of petroleum and gas and other precious natural resources. From 1 January 2016, enterprises which apply the rate of 22% shall apply the rate of 20%. Enterprises established in accordance with the Vietnamese law (including cooperatives and non-business units) engaged in goods production or service provision activities and having an annual total turnover not exceeding VND 20 billion may be subject to the tax rate of 20%. However, CIT incentives and 20% tax do not apply to the following incomes: • Incomes from transfer of contributed capital or right to contribute capital; incomes from real estate

transfer; Incomes from transfer of project of investment or the right to participate in project of investment, transfer of the right to mineral exploration and extraction; incomes from overseas business operation.

• Incomes from exploration and extraction of petroleum, other rare and valuable resources, and income from mineral extraction.

• Income from provision of services subject to special excise tax prescribed by the Law on Special excise tax.”

Vietnam

PKF Worldwide Tax Guide 2016/17 5

The total income generated by Vietnamese enterprise shall be subjected to CIT regardless of whether the income is gathered in Vietnam or from overseas. Taxable income comprises income earned from manufacturing, trading and services, except for: • Income from cultivation, husbandry, aquaculture and salt production of cooperatives, from

cultivation, husbandry and aquaculture production of enterprises in geographical areas with particularly difficult socio-economic conditions; from fishing activities;

• Performance of technical service contracts directly serving agricultural production; • Performance of contracts for scientific research and development; • Income from goods manufacturing and trading or service provision activities of enterprises

employing disabled, drug-detoxified and HIV-infected labourers, who account for at least 30% of the average number of labourers of these enterprises in a year;

• Income from job training exclusively provided for ethnic minority people, the disabled, extremely disadvantaged children and people involved in social evils, people undergoing detoxification, detoxified people and HIV/AIDS-infected people-Aid received for educational, scientific research, cultural, artistic, charitable, humanitarian and other social activities in Vietnam;

• Income from the first-time transfer of certified emission reductions (CERs) of enterprises granted with emission reduction certificates. Subsequent transfers shall be liable to enterprise income tax under regulations.

Other Exemptions or reductions in CIT are stipulated in the relevant legal documents. Administration Enterprises shall make a self-declaration of CIT payable. The enterprise shall pay the amount of CIT provisionally payable determined each quarter during the year and shall finalize the whole CIT payable for the fiscal year within 90 days after the year end. Generally, the tax year for the purpose of tax finalisation shall be the calendar year, except for the enterprise who is permitted to apply a fiscal year other than the calendar year, tax year of this enterprise shall conform to its fiscal year. CAPITAL GAINS TAX There is no specific capital gains tax in Vietnam. Capital gains are treated as ordinary income for the purpose of calculating income tax. BRANCH PROFITS TAX There is no specific branch profits tax in Vietnam. Foreign Enterprises and Foreign Individuals are subject of Withholding Tax on Income that they earn in carrying business. VALUE ADDED TAX (VAT) VAT is a tax levied on imported goods and goods and services used for manufacturing, trading or consumption in Vietnam (except for the exempted cases stipulated in law). VAT Rate There are three levels of VAT rate. In general, goods or services are mostly subject to a rate of 10%, while some goods or services are subject to a rate of 5% or 0% depending on the type of goods or services. VAT payable = Output VAT – deductible VAT Output VAT is the total VAT on sold goods and services written on the VAT invoices. Deductible VAT comprise Input VAT which are total VAT on VAT invoice for purchase of goods and services (including fixed assets) serving the manufacture or sale of taxable goods and services, VAT on imported goods at Customs and VAT pay on behalf of foreign enterprises mentioned in the Withholding Tax. VAT shall be declare and pay monthly. For enterprises which have turnover of precedent year below VND fifty billion (VND 50,000,000,000) or newly establish, VAT can be declare and pay quarterly. If input VAT is not completely deducted in the period (month or quarter), the enterprise which uses credit-invoice method may deduct it from the tax incurred in the next period. If input VAT is not

Vietnam

PKF Worldwide Tax Guide 2016/17 6

completely deducted after 12 months or 4 quarters from the first month or quarter input VAT is incurred, the taxpayer shall receive a refund. Calculating VAT There two (2) methods to calculate VAT namely the Credit-invoice Method and the Direct Method. • For the Credit-invoice Method, VAT is calculated as:

Output VAT = Selling Price (excluding VAT) x VAT rate • For the Direct Method, VAT is calculated as:

VAT payables = selling price x rate of VAT (in direct method)

VAT payables includes the selling price. The VAT rates that apply to the Direct Method are: • 1% for distribution or supply goods, • 5% for services or construction (excluding building materials), • 3% for manufacturing, transport, services (associated with goods), construction (including

building materials), • 2% for other lines of business.

For the enterprises trading, fashioning of gold, silver and gemstones, VAT is calculate as follows: VAT payables = (selling price – cost price) x rate of 10% EXCISE TAX Excise Tax is applied to specific luxury goods, either imported or manufactured in Vietnam, and service. Excise Tax is calculated based on the quantity of taxable goods (service) sold, their taxable value, and their corresponding tax rate. Taxable value is sale price (excluding VAT) for manufactured goods and service or customs value for imported goods. Specific goods (service) and the tax rate are as follows:

Description Rate

A. Goods

1. Cigarettes, cigars and other tobacco products - before 1 January 2016 65% - from 1 January 2016 through 31 December 2018 70% - from 1 January 2019 75%

2. Liquor

a. from 20 degrees proof - before 01 January 2016 50% - from 01 January 2016 through 31 December 2016 55% - from 01 January 2017 through 31 December 2017 60% - from 01 January 2018 65% b. under 20 degrees proof - before 01 January 2016 25% - from 01 January 2016 through 31 December 2017 30% - from 01 January 2018 35%

3. Beer - before 01 January 2016 50% - from 01 January 2016 through 31 December 2016 55%

Vietnam

PKF Worldwide Tax Guide 2016/17 7

Description Rate

- from 01 January 2017 through 31 December 2017 60% - from 01 January 2018 65%

4. Automobiles under 24 seats

a. up to 9 seats 45% 60%

b. from 10 to 16 seats 30% c. from 15 to under 24 seats 15%

5. Two- and three-wheeled motorcycles of a cylinder capacity of over 125 cm3 20%

6. Aircraft 30% 7. Yachts 30%

8. Gasoline of various kinds, naphtha, reformed components and other compounds for mixing gasoline

7% 10%

9. Air-conditioners with capacity of 90,000 BTU or less 10% 10. Playing cards 40% 11. Votive paper and votive objects 70%

B Services

1. Discotheque, massage parlors and karaoke bars 30%

2. Casino and reward games, including jackpot, slot and other similar machines 25%

3. Betting business 25%

4. Golf business, including sale of membership cards and golf game tickets 10% 5. Lottery business 15%

BUSINESS LICENCE TAX Business License Tax is a tax on the business capital of business establishments. Annually, Business Licence Tax shall be paid within 31 January. For the new business establishment the deadline comes to the end of the first month of operation. Depend on the registration capital, Business Licence Tax is as follows:

Description Amount

1. Over VND 10 billion VND 3,000,000

2. From VND 5 billion to VND 10 billion VND 2,000,000

3 From VND 2 billion to VND 5 billion VND 1,500,000

3. Less than VND 2 billion VND 1,000,000 EXPORT – IMPORT TAX Export – Import Tax is levied on the goods exported or imported through Vietnamese border, on goods brought from the domestic market into non-tariff zones and vice versa and on other traded or exchanged goods that are considered imports or exports. Export – Import Tax rate for each exported or imported item is determined on the Export Tax and Import Tax tariff.

Vietnam

PKF Worldwide Tax Guide 2016/17 8

NATURAL RESOURCES TAX Natural Resources Tax is levied on organizations and individuals conducting the exploitation of natural resources in Vietnam. Natural Resources Tax is determined by the actual natural resources exploited, the unit price and the tax rate stipulated for the specific resources. B. DETERMINATION OF TAXABLE INCOME Generally, deductible expenses which are deductible for the purpose of calculation of taxable income include expenses actually used for the production or trading in goods and services and expenses incurred with receipts or source documents issued in accordance with the law. • CIT payables = (Taxed income – Allocation to R&D fund) x CIT rate. • R&D fund is Science and Technology Development Fund. • Taxed income = Taxable Income – Exempt Income – Prior year loss carried forward. • Taxable income = Turnover – Deductible Expenses + Other Income. DIVIDENDS Income divided from capital contribution, share purchase, joint venture or economic association with domestic enterprises, after contributed capital recipients, share issuers or joint venture or association parties have paid Corporate Income Tax (CIT) under the Law on CIT shall be exempted from CIT. When the enterprises receive these income (dividends) before the tax calculation, the incomes shall not be exempted from CIT. In this case, the enterprise must pay CIT on this income at the common rate applied in this enterprise. For individuals, dividends are levied at a rate of 5%. LOSSES Enterprises which suffer losses shall be entitled to carry forward those losses to taxable income of the following years. Losses may be carried forward within five (5) years from the year following the year the loss arose. FOREIGN SOURCE INCOME Vietnamese enterprises which make an offshore investment and derive income from production and business activities overseas shall declare and pay CIT in accordance with the current Law on CIT of Vietnam. TAX INCENTIVES Specific incentives are provided for high technology fields, for new investment projects, and for expansion investment. Tax incentives (in CIT) comprise: • Preferential tax rates such as 10%, 15% or 20%; and, • Durations of Tax exemption at 2 or 4 years from the first profit-making year and a tax reduction of

50% for the following 4, 5 or 9 years. C. FOREIGN TAX RELIEF Vietnamese enterprises which make an offshore investment and derive income from production and business activities overseas shall declare and pay CIT in accordance with the current Law on CIT of Vietnam. In case these enterprises have paid income tax on incomes arising overseas, the paid tax amount (in Vietnam) may be subtracted but must not exceed the CIT amount payable under the Law on Corporate Income Tax.

Vietnam

PKF Worldwide Tax Guide 2016/17 9

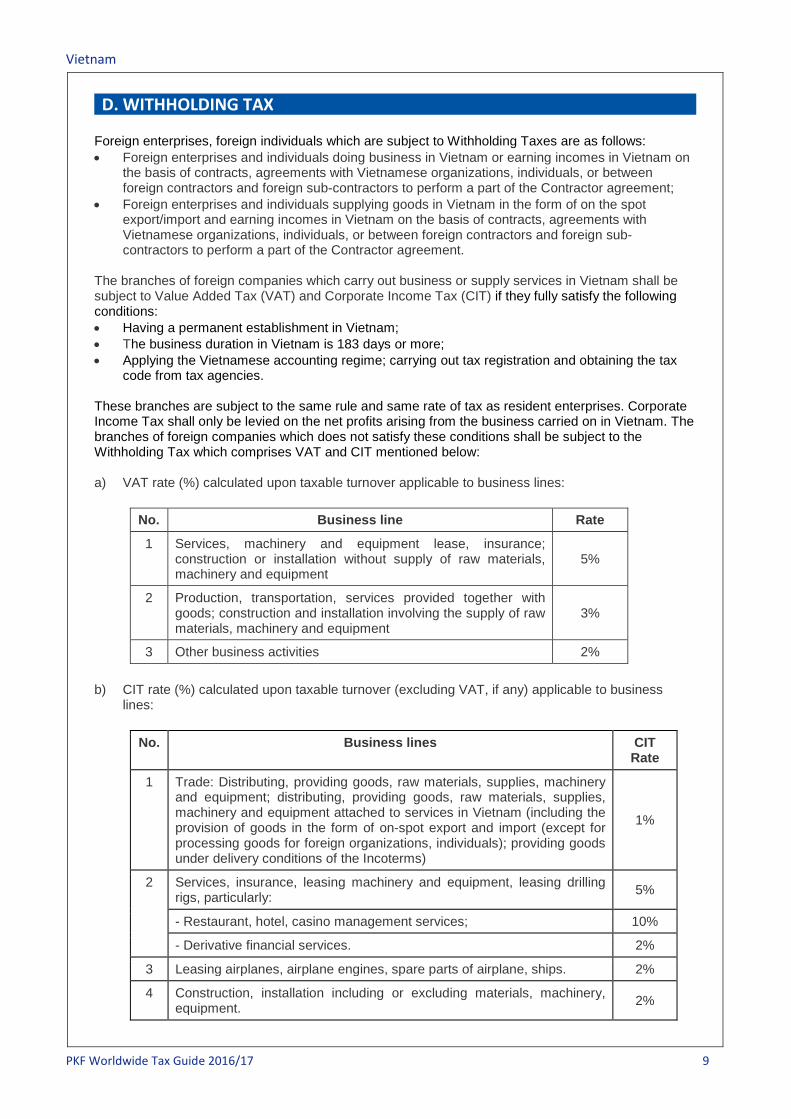

D. WITHHOLDING TAX Foreign enterprises, foreign individuals which are subject to Withholding Taxes are as follows: • Foreign enterprises and individuals doing business in Vietnam or earning incomes in Vietnam on

the basis of contracts, agreements with Vietnamese organizations, individuals, or between foreign contractors and foreign sub-contractors to perform a part of the Contractor agreement;

• Foreign enterprises and individuals supplying goods in Vietnam in the form of on the spot export/import and earning incomes in Vietnam on the basis of contracts, agreements with Vietnamese organizations, individuals, or between foreign contractors and foreign sub-contractors to perform a part of the Contractor agreement.

The branches of foreign companies which carry out business or supply services in Vietnam shall be subject to Value Added Tax (VAT) and Corporate Income Tax (CIT) if they fully satisfy the following conditions: • Having a permanent establishment in Vietnam; • The business duration in Vietnam is 183 days or more; • Applying the Vietnamese accounting regime; carrying out tax registration and obtaining the tax

code from tax agencies. These branches are subject to the same rule and same rate of tax as resident enterprises. Corporate Income Tax shall only be levied on the net profits arising from the business carried on in Vietnam. The branches of foreign companies which does not satisfy these conditions shall be subject to the Withholding Tax which comprises VAT and CIT mentioned below: a) VAT rate (%) calculated upon taxable turnover applicable to business lines:

No. Business line Rate

1 Services, machinery and equipment lease, insurance; construction or installation without supply of raw materials, machinery and equipment

5%

2 Production, transportation, services provided together with goods; construction and installation involving the supply of raw materials, machinery and equipment

3%

3 Other business activities 2% b) CIT rate (%) calculated upon taxable turnover (excluding VAT, if any) applicable to business

lines:

No. Business lines CIT Rate

1 Trade: Distributing, providing goods, raw materials, supplies, machinery and equipment; distributing, providing goods, raw materials, supplies, machinery and equipment attached to services in Vietnam (including the provision of goods in the form of on-spot export and import (except for processing goods for foreign organizations, individuals); providing goods under delivery conditions of the Incoterms)

1%

2 Services, insurance, leasing machinery and equipment, leasing drilling rigs, particularly: 5%

- Restaurant, hotel, casino management services; 10%

- Derivative financial services. 2%

3 Leasing airplanes, airplane engines, spare parts of airplane, ships. 2%

4 Construction, installation including or excluding materials, machinery, equipment. 2%

Vietnam

PKF Worldwide Tax Guide 2016/17 10

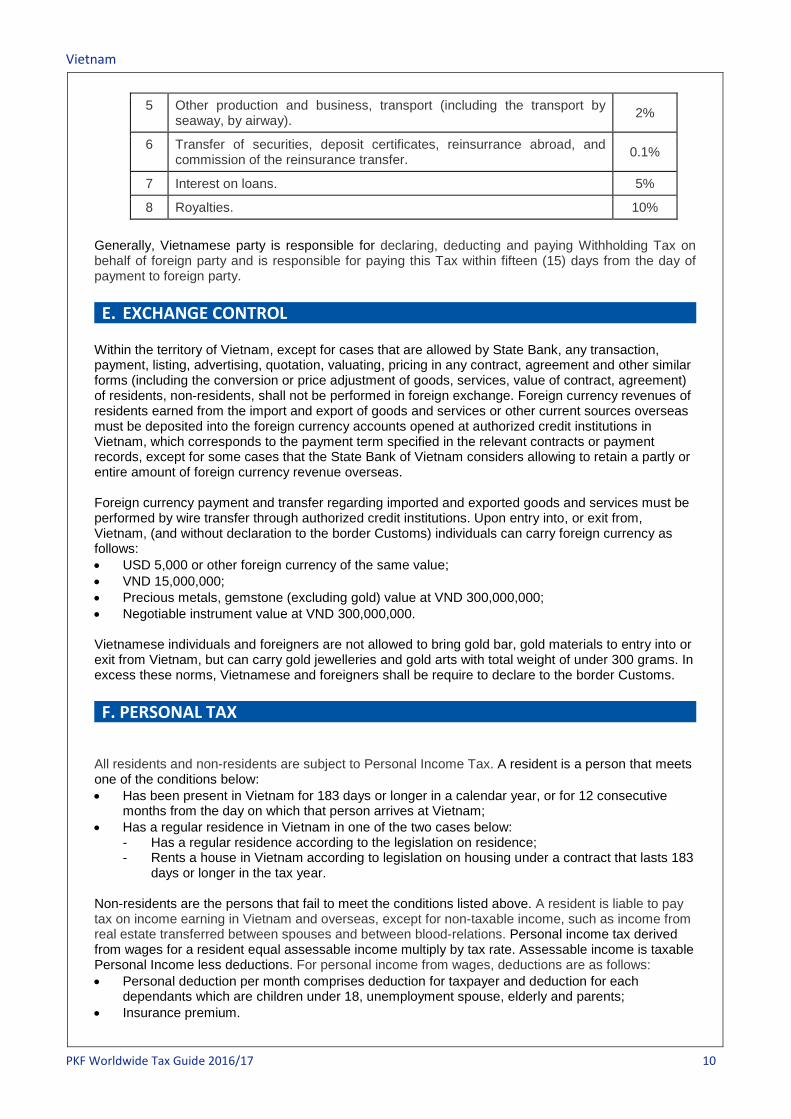

5 Other production and business, transport (including the transport by seaway, by airway). 2%

6 Transfer of securities, deposit certificates, reinsurrance abroad, and commission of the reinsurance transfer. 0.1%

7 Interest on loans. 5%

8 Royalties. 10% Generally, Vietnamese party is responsible for declaring, deducting and paying Withholding Tax on behalf of foreign party and is responsible for paying this Tax within fifteen (15) days from the day of payment to foreign party. E. EXCHANGE CONTROL Within the territory of Vietnam, except for cases that are allowed by State Bank, any transaction, payment, listing, advertising, quotation, valuating, pricing in any contract, agreement and other similar forms (including the conversion or price adjustment of goods, services, value of contract, agreement) of residents, non-residents, shall not be performed in foreign exchange. Foreign currency revenues of residents earned from the import and export of goods and services or other current sources overseas must be deposited into the foreign currency accounts opened at authorized credit institutions in Vietnam, which corresponds to the payment term specified in the relevant contracts or payment records, except for some cases that the State Bank of Vietnam considers allowing to retain a partly or entire amount of foreign currency revenue overseas. Foreign currency payment and transfer regarding imported and exported goods and services must be performed by wire transfer through authorized credit institutions. Upon entry into, or exit from, Vietnam, (and without declaration to the border Customs) individuals can carry foreign currency as follows: • USD 5,000 or other foreign currency of the same value; • VND 15,000,000; • Precious metals, gemstone (excluding gold) value at VND 300,000,000; • Negotiable instrument value at VND 300,000,000. Vietnamese individuals and foreigners are not allowed to bring gold bar, gold materials to entry into or exit from Vietnam, but can carry gold jewelleries and gold arts with total weight of under 300 grams. In excess these norms, Vietnamese and foreigners shall be require to declare to the border Customs. F. PERSONAL TAX All residents and non-residents are subject to Personal Income Tax. A resident is a person that meets one of the conditions below: • Has been present in Vietnam for 183 days or longer in a calendar year, or for 12 consecutive

months from the day on which that person arrives at Vietnam; • Has a regular residence in Vietnam in one of the two cases below:

- Has a regular residence according to the legislation on residence; - Rents a house in Vietnam according to legislation on housing under a contract that lasts 183

days or longer in the tax year. Non-residents are the persons that fail to meet the conditions listed above. A resident is liable to pay tax on income earning in Vietnam and overseas, except for non-taxable income, such as income from real estate transferred between spouses and between blood-relations. Personal income tax derived from wages for a resident equal assessable income multiply by tax rate. Assessable income is taxable Personal Income less deductions. For personal income from wages, deductions are as follows: • Personal deduction per month comprises deduction for taxpayer and deduction for each

dependants which are children under 18, unemployment spouse, elderly and parents; • Insurance premium.

Vietnam

PKF Worldwide Tax Guide 2016/17 11

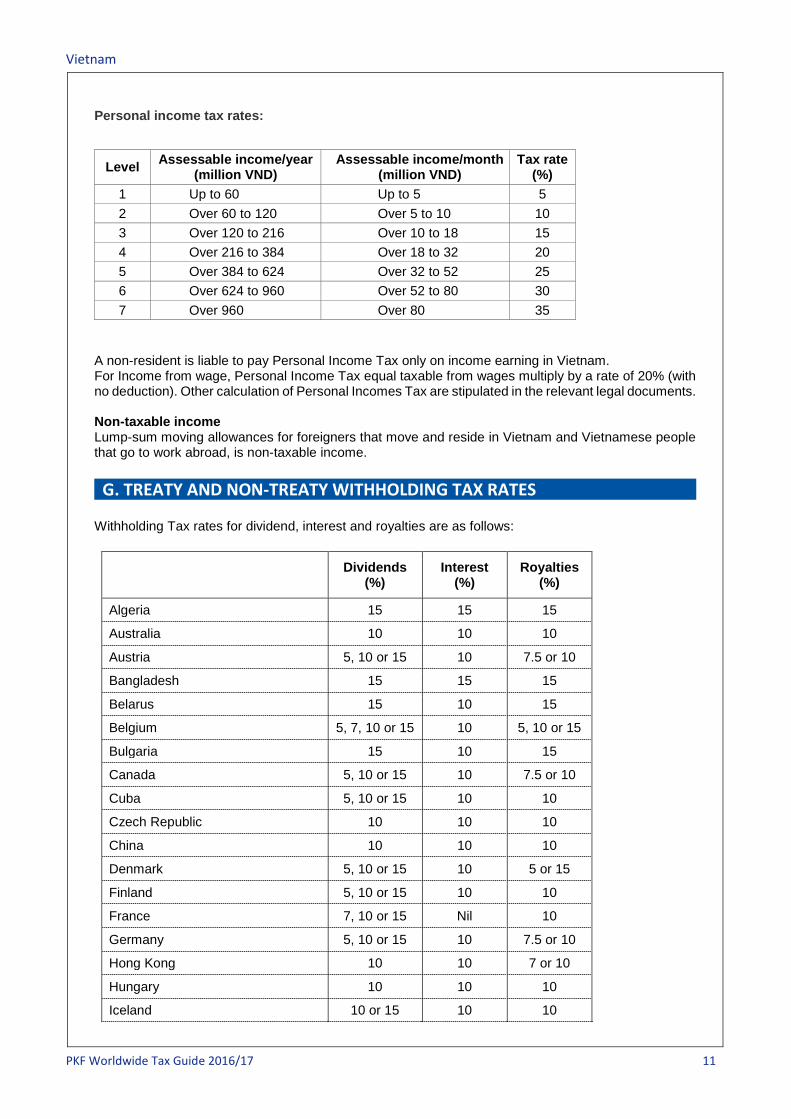

Personal income tax rates:

A non-resident is liable to pay Personal Income Tax only on income earning in Vietnam. For Income from wage, Personal Income Tax equal taxable from wages multiply by a rate of 20% (with no deduction). Other calculation of Personal Incomes Tax are stipulated in the relevant legal documents. Non-taxable income Lump-sum moving allowances for foreigners that move and reside in Vietnam and Vietnamese people that go to work abroad, is non-taxable income. G. TREATY AND NON-TREATY WITHHOLDING TAX RATES

Withholding Tax rates for dividend, interest and royalties are as follows:

Dividends (%)

Interest (%)

Royalties (%)

Algeria 15 15 15

Australia 10 10 10

Austria 5, 10 or 15 10 7.5 or 10

Bangladesh 15 15 15

Belarus 15 10 15

Belgium 5, 7, 10 or 15 10 5, 10 or 15

Bulgaria 15 10 15

Canada 5, 10 or 15 10 7.5 or 10

Cuba 5, 10 or 15 10 10

Czech Republic 10 10 10

China 10 10 10

Denmark 5, 10 or 15 10 5 or 15

Finland 5, 10 or 15 10 10

France 7, 10 or 15 Nil 10

Germany 5, 10 or 15 10 7.5 or 10

Hong Kong 10 10 7 or 10

Hungary 10 10 10

Iceland 10 or 15 10 10

Level Assessable income/year (million VND)

Assessable income/month (million VND)

Tax rate (%)

1 Up to 60 Up to 5 5 2 Over 60 to 120 Over 5 to 10 10 3 Over 120 to 216 Over 10 to 18 15 4 Over 216 to 384 Over 18 to 32 20 5 Over 384 to 624 Over 32 to 52 25 6 Over 624 to 960 Over 52 to 80 30 7 Over 960 Over 80 35

Vietnam

PKF Worldwide Tax Guide 2016/17 12

Dividends (%)

Interest (%)

Royalties (%)

India 10 10 10

Indonesia 15 15 15

Italy 5, 10 or 15 10 7.5 or 10

Japan 10 10 10

Kazakhstan 5 or 15 10 10

Korea 5 10 5 or 15

Kuwait 10 or 15 15 20

Laos 10 10 10

Luxembourg 5, 10 or 15 10 10

Malaysia 10 10 10

Mongolia 10 10 10

Morocco 10 10 10

Mozambique 10 10 10

Myanmar 10 10 10

Netherlands 5, 7, 10 or 15 7 or 10 5, 10 or 15

New Zealand 5 or 15 10 10

North Korea 10 10 10

Norway 5, 10 or 15 10 10

Pakistan 15 15 15

Palestine 10 10 10

Poland 10 or 15 10 1, 10 or 15

Philippines 10 or 15 15 15

Qatar 5 or 12.5 10 5 or 10

Romania 15 10 15

Russia 10 or 15 10 15

Saudi Arabia 5 or 12.5 10 7.5 or 10

Serbia 10 or 15 10 10

Seychelles 10 10 10

Singapore 5, 7 or 12.5 10 5 or 15

Sri Lanka 10 10 15

Sweden 5, 10 or 15 10 5 or 15

Switzerland 7, 10 or 15 10 10

Taiwan 15 10 15

Spain 7, 10 or 15 10 10

Tunisia 10 10 10

Thailand 15 10 or 15 15

Ukraine 10 10 10

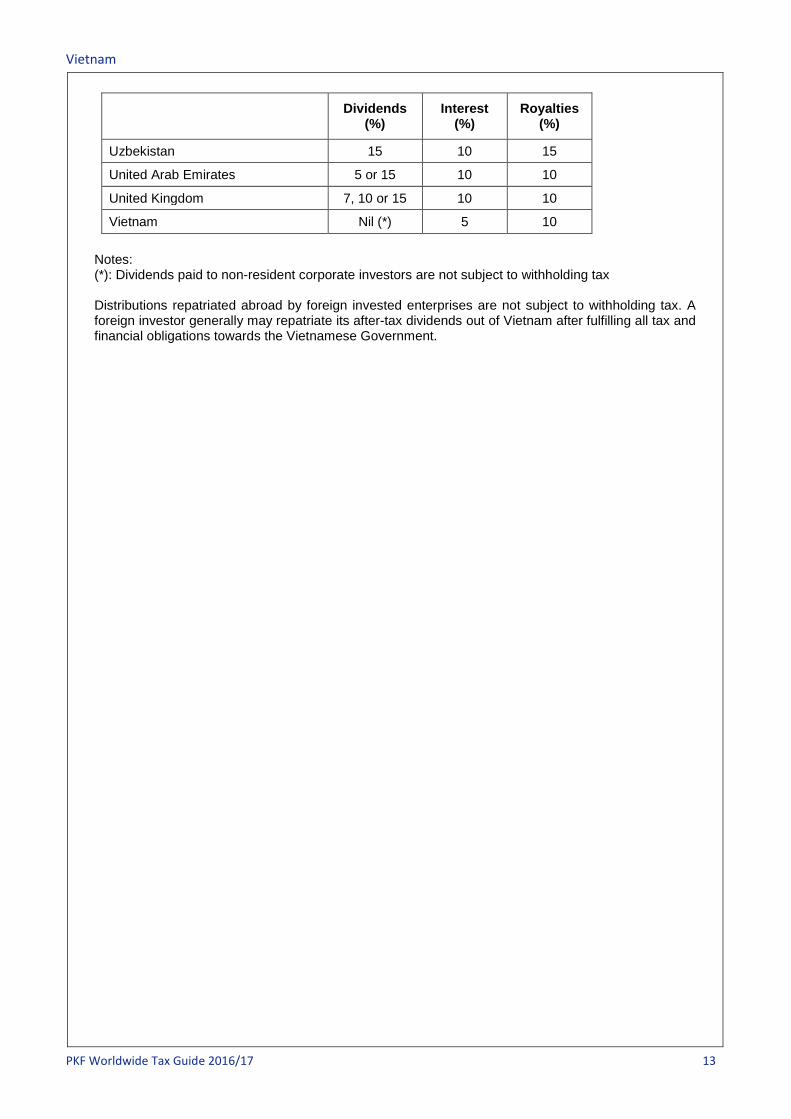

Vietnam

PKF Worldwide Tax Guide 2016/17 13

Dividends (%)

Interest (%)

Royalties (%)

Uzbekistan 15 10 15

United Arab Emirates 5 or 15 10 10

United Kingdom 7, 10 or 15 10 10

Vietnam Nil (*) 5 10 Notes: (*): Dividends paid to non-resident corporate investors are not subject to withholding tax Distributions repatriated abroad by foreign invested enterprises are not subject to withholding tax. A foreign investor generally may repatriate its after-tax dividends out of Vietnam after fulfilling all tax and financial obligations towards the Vietnamese Government.