Embed Size (px)

Citation preview

Vietnam - Key real estate investment themes in 2017 and beyond Khanh Nguyen, Associate Director, Capital Markets, Vietnam, JLL5 October 2017

PositiveMomentum

Why Vietnam Now?

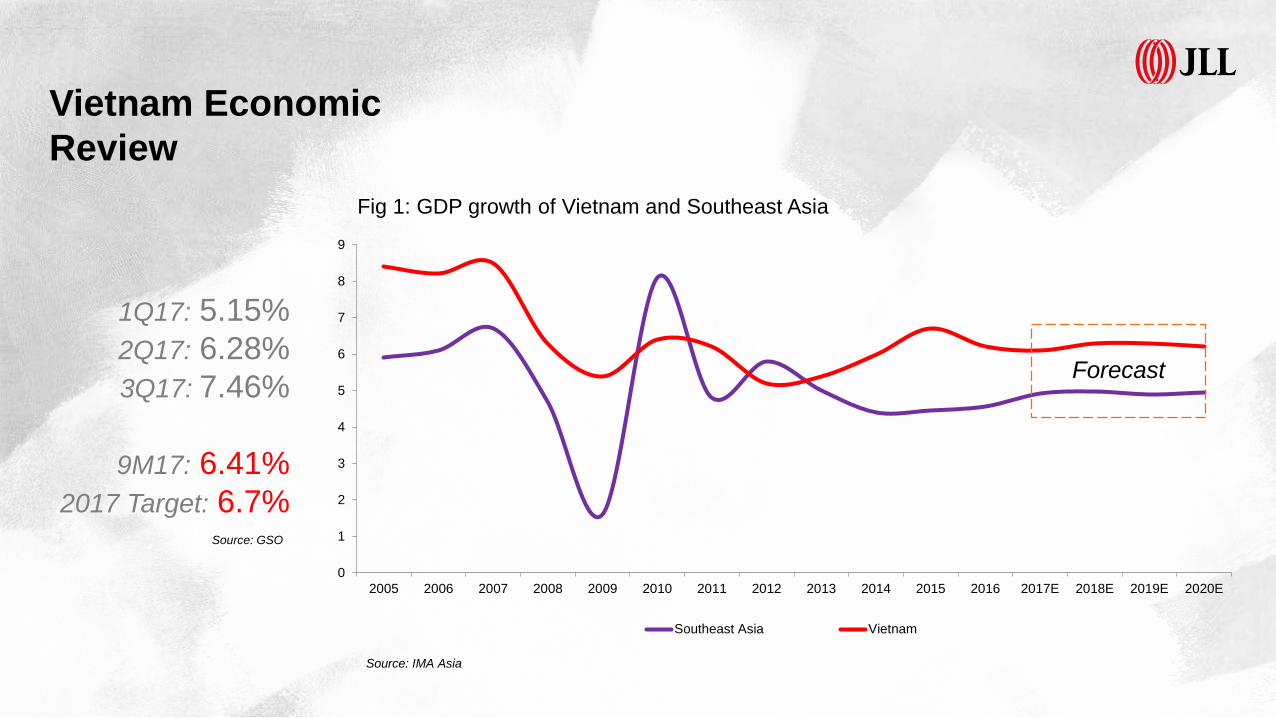

Vietnam Economic Review

0

1

2

3

4

5

6

7

8

9

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017E 2018E 2019E 2020E

Southeast Asia Vietnam

Fig 1: GDP growth of Vietnam and Southeast Asia

Forecast

Source: IMA Asia

1Q17: 5.15%2Q17: 6.28%3Q17: 7.46%

9M17: 6.41%2017 Target: 6.7%

Source: GSO

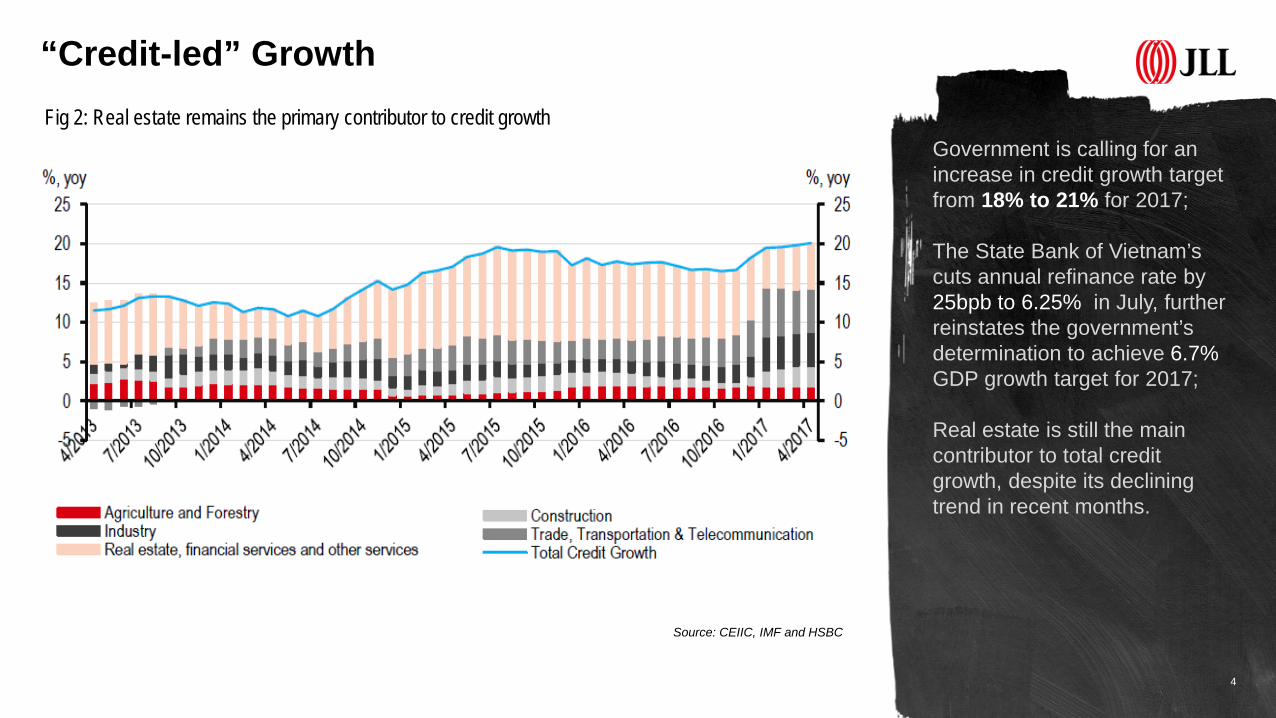

“Credit-led” Growth

4

Government is calling for an increase in credit growth target from 18% to 21% for 2017;

The State Bank of Vietnam’s cuts annual refinance rate by 25bpb to 6.25% in July, further reinstates the government’s determination to achieve 6.7%GDP growth target for 2017;

Real estate is still the main contributor to total credit growth, despite its declining trend in recent months.

Fig 2: Real estate remains the primary contributor to credit growth

Source: CEIIC, IMF and HSBC

5

Japan Singapore China TaiwanSouth Korea

Top 5 Countries Investing in Vietnam

Top 5 FDI Attracting Sectors

Vietnam FDI – 9M2017

$25.5bilManufacturing Real EstatePower Retail &

WholesaleReal EstateMiningRetail &

WholesaleNewly registered Capital $14.6bil

Total

Source: Ministry of Planning and Investment – Foreign Investment Agency (FIA Vietnam)

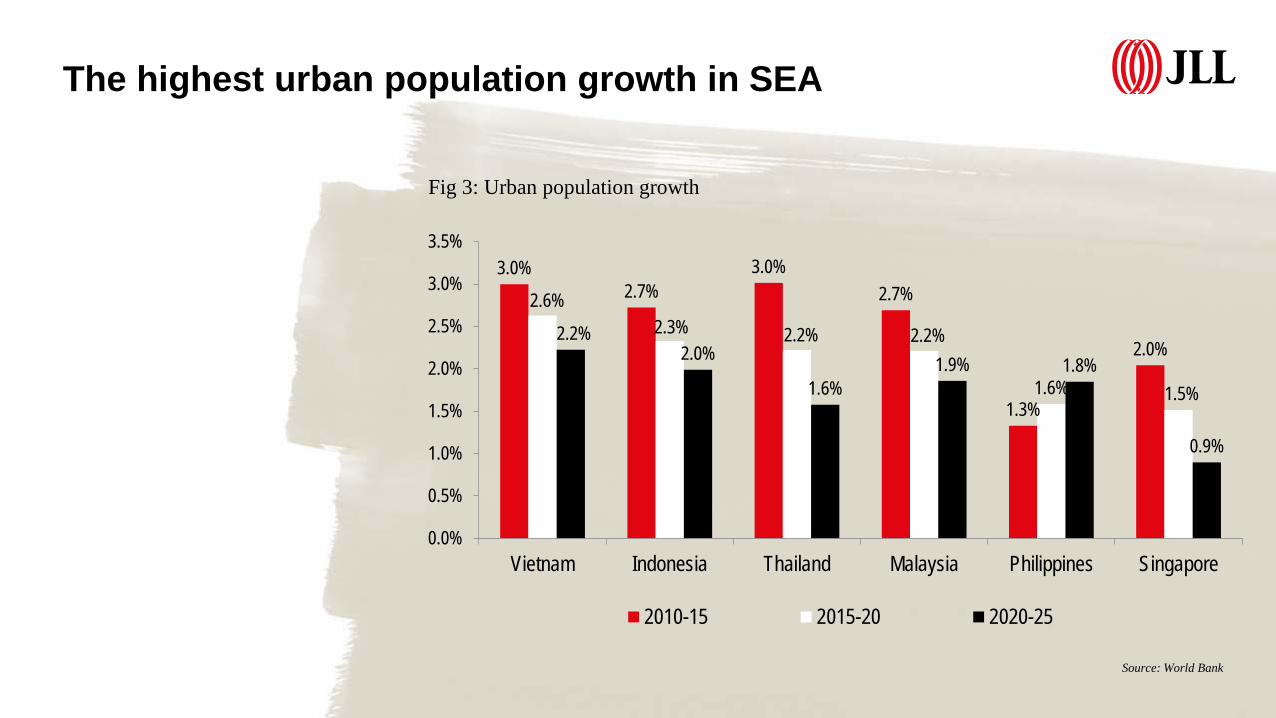

The highest urban population growth in SEA

3.0%2.7%

3.0%2.7%

1.3%

2.0%

2.6%2.3% 2.2% 2.2%

1.6% 1.5%

2.2%2.0%

1.6%1.9% 1.8%

0.9%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

Vietnam Indonesia Thailand Malaysia Philippines Singapore

2010-15 2015-20 2020-25

Fig 3: Urban population growth

Source: World Bank

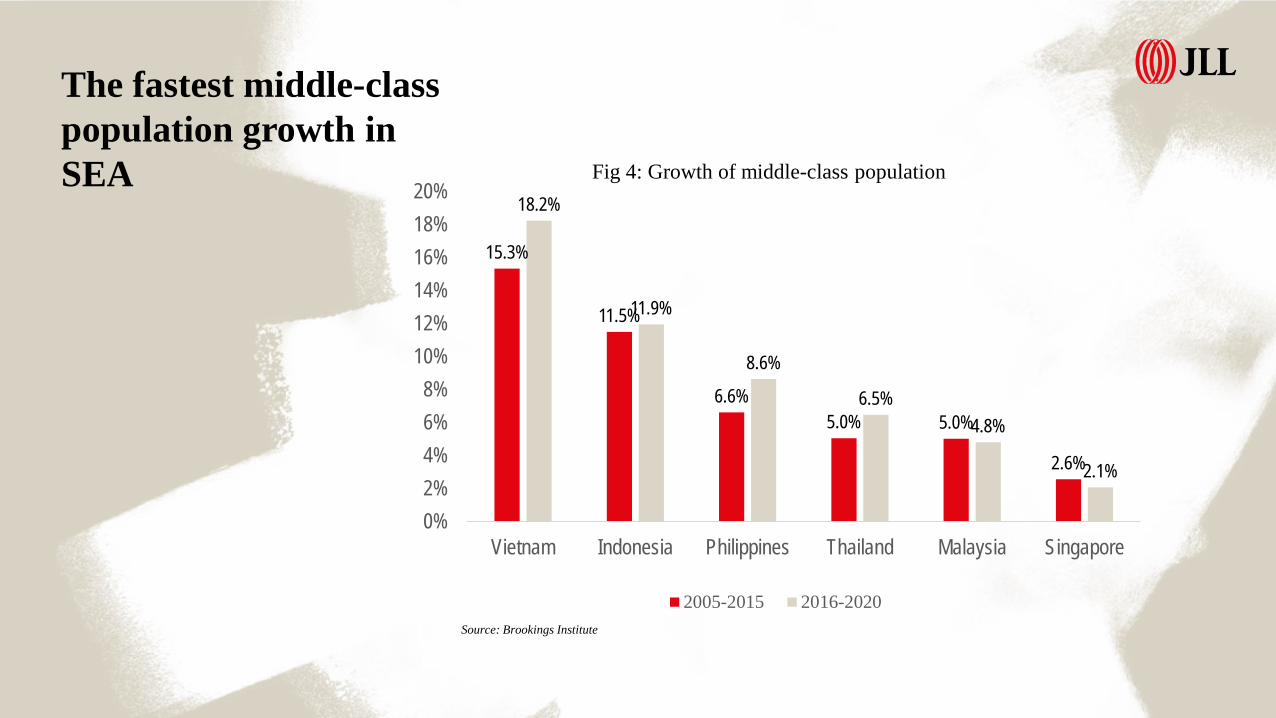

The fastest middle-class population growth in SEA

15.3%

11.5%

6.6%5.0% 5.0%

2.6%

18.2%

11.9%

8.6%

6.5%4.8%

2.1%

0%2%4%6%8%

10%12%14%16%18%20%

Vietnam Indonesia Philippines Thailand Malaysia Singapore

2005-2015 2016-2020

Fig 4: Growth of middle-class population

Source: Brookings Institute

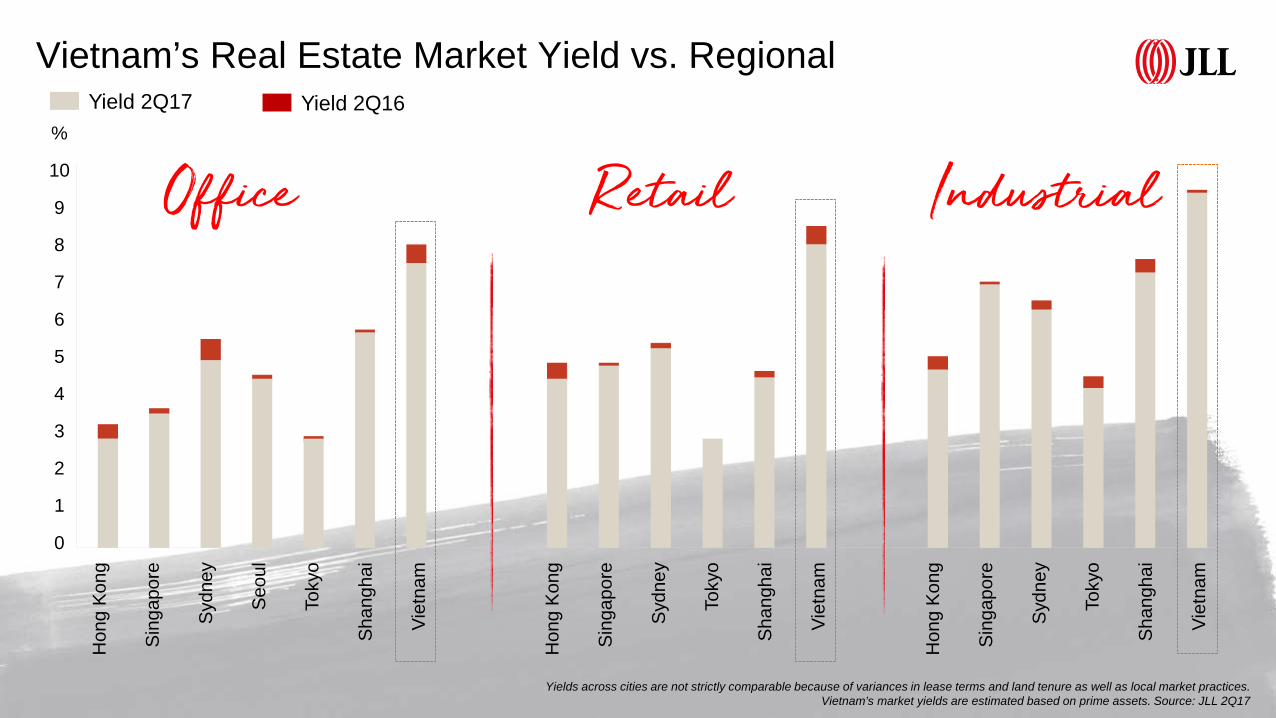

Vietnam’s Real Estate Market Yield vs. Regional

%

10

9

8

7

6

5

4

3

2

1

0

Hon

g K

ong

Sin

gapo

re

Syd

ney

Seo

ul

Toky

o

Sha

ngha

i

Viet

nam

Hon

g K

ong

Sin

gapo

re

Syd

ney

Toky

o

Sha

ngha

i

Viet

nam

Hon

g K

ong

Sin

gapo

re

Syd

ney

Toky

o

Sha

ngha

i

Viet

nam

Yield 2Q17 Yield 2Q16

Office Retail Industrial

Yields across cities are not strictly comparable because of variances in lease terms and land tenure as well as local market practices.Vietnam’s market yields are estimated based on prime assets. Source: JLL 2Q17

Moderate prime office rent growth is expected

Clock positions for the office sector relate to the main submarket in each city. Source:JLL 2Q 2017

“Capital value growth is expected

AP prime office rental clock, 2Q 2017

”

Who’s Looking AtVietnam Now?

Various international investors are very active

Source: JLL Research

Increasing recognition from global investors

establish $300 million hospitality

joint venture

acquires KumhoAsiana Plaza

Saigon in Ho Chi Minh City

in joint venture to develop prime

waterfront site in Ho Chi Minh City’s

Thu Thiem New Urban Area

hits first close of $46mfollow-up

round led by EXS Capital

Warburg Pincus and VinaCapital

Mapletree Keppel Land SonKim Land

signed a strategic

cooperation, Dated 22 sept

2017

Becamex IDC and Warburg Pincus (USA)

Source:

13

What Are They Looking For?

Investors’ Appetite

14

Income-generating assets

Development assets

• Prime location;• Grade A or B asset, international standard• Clear land title and ownership structure;• Long-term land tenure

• Clean & clear land title;• Fully compensated;• LUR Certificate, Master plan approval;• Strategic location and Good local partner

Source: JLL Research

Key Challenges in real estate investment in Vietnam

• Immature market and lack of transparency;

• Shortage of ‘clean’ and ‘clear’ land for residential and commercial projects;

• Infrastructure – Planning, implementation and extension or delay (Thu thiem bridge 2, metro line No. 1, etc.);

• Deal structuring to optimize the transaction value and tax purpose

Source: JLL Research

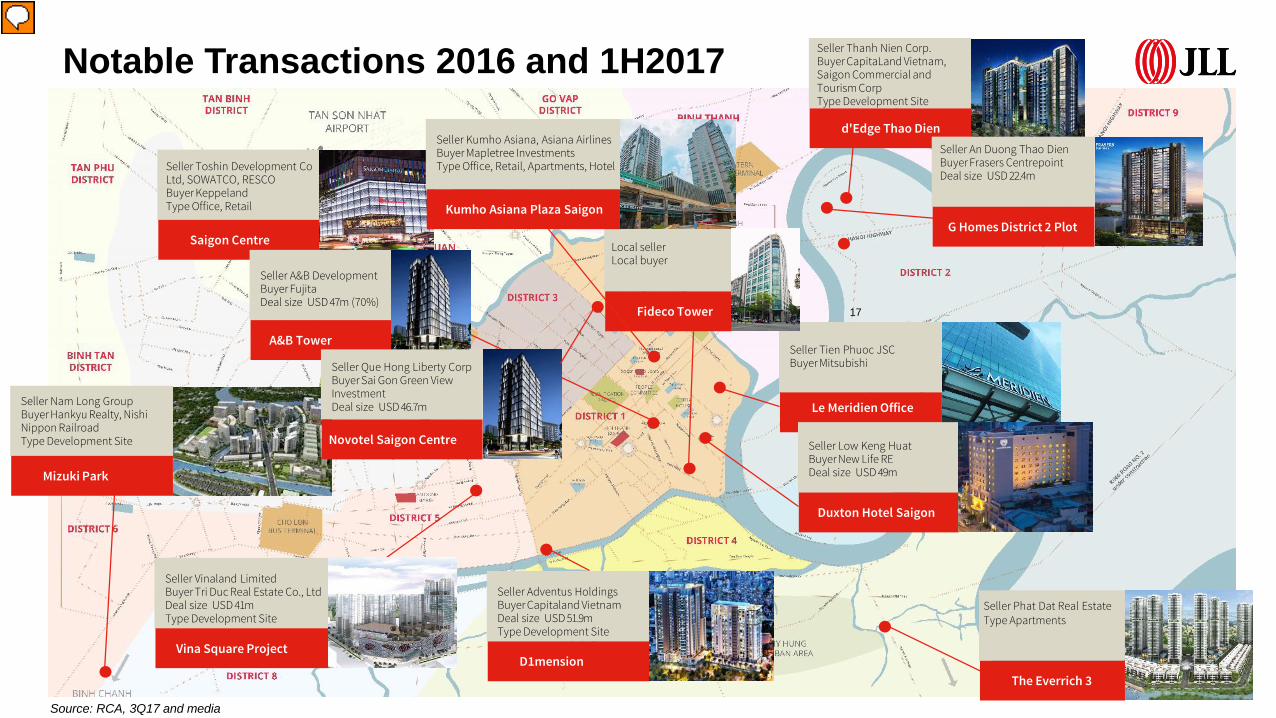

Major Transactions

17

Notable Transactions 2016 and 1H2017

Source: RCA, 3Q17 and media

Seller Phat Dat Real EstateType Apartments

The Everrich 3

17

Seller Thanh Nien Corp.Buyer CapitaLand Vietnam, Saigon Commercial and Tourism CorpType Development Site

d'Edge Thao Dien

17

Seller Adventus Holdings Buyer Capitaland VietnamDeal size USD 51.9mType Development Site

D1mension

17

Seller Tien Phuoc JSCBuyer Mitsubishi

Le Meridien Office

17

Local seller Local buyer

Fideco Tower

17

Seller Nam Long GroupBuyer Hankyu Realty, Nishi Nippon RailroadType Development Site

Mizuki Park

Seller Toshin Development Co Ltd, SOWATCO, RESCOBuyer KeppelandType Office, Retail

Saigon Centre

17

Seller Low Keng HuatBuyer New Life REDeal size USD 49m

Duxton Hotel Saigon

17

Seller An Duong Thao DienBuyer Frasers CentrepointDeal size USD 22.4m

G Homes District 2 Plot17

Seller Kumho Asiana, Asiana AirlinesBuyer Mapletree InvestmentsType Office, Retail, Apartments, Hotel

Kumho Asiana Plaza Saigon

Seller A&B DevelopmentBuyer Fujita Deal size USD 47m (70%)

A&B Tower

Seller Que Hong Liberty CorpBuyer Sai Gon Green View InvestmentDeal size USD 46.7m

Novotel Saigon Centre

17

Seller Vinaland Limited Buyer Tri Duc Real Estate Co., LtdDeal size USD 41mType Development Site

Vina Square Project

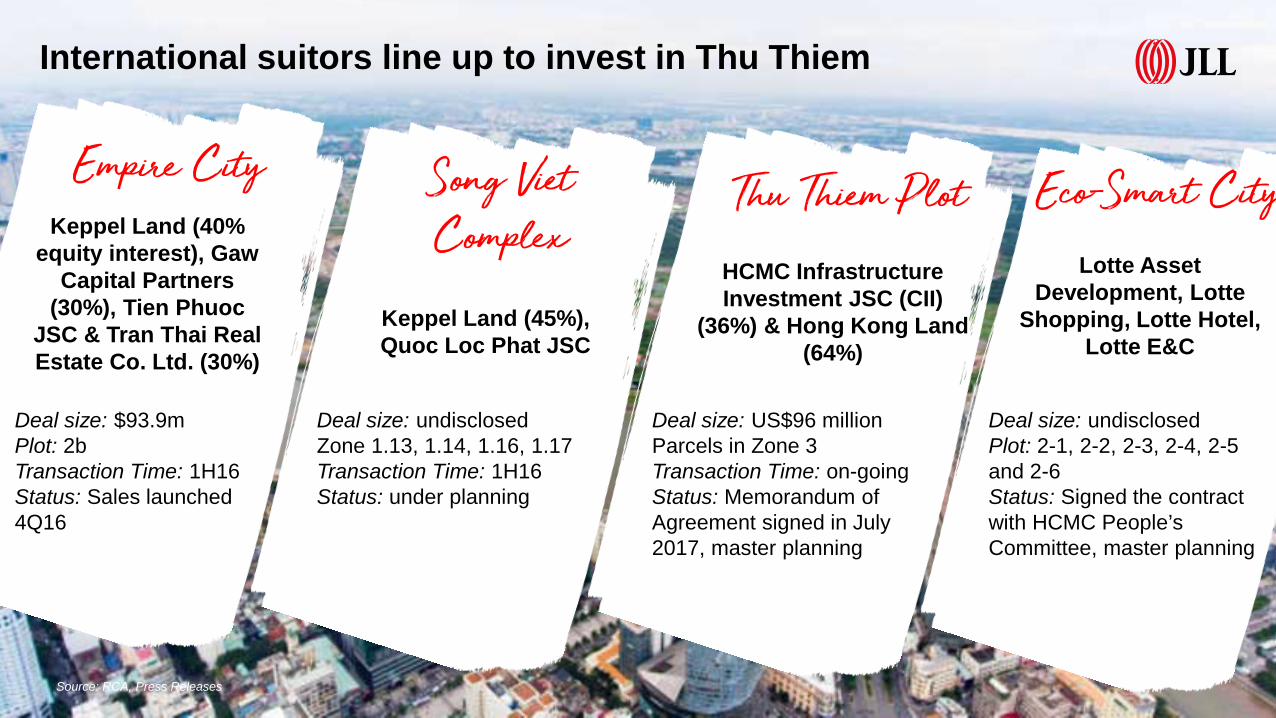

International suitors line up to invest in Thu Thiem

Keppel Land (40% equity interest), Gaw

Capital Partners (30%), Tien Phuoc

JSC & Tran Thai Real Estate Co. Ltd. (30%)

Deal size: $93.9mPlot: 2bTransaction Time: 1H16Status: Sales launched 4Q16

Empire City

Keppel Land (45%), Quoc Loc Phat JSC

Deal size: undisclosedZone 1.13, 1.14, 1.16, 1.17Transaction Time: 1H16Status: under planning

Song VietComplex

HCMC Infrastructure Investment JSC (CII)

(36%) & Hong Kong Land (64%)

Deal size: US$96 millionParcels in Zone 3Transaction Time: on-goingStatus: Memorandum of Agreement signed in July 2017, master planning

Thu Thiem PlotLotte Asset

Development, LotteShopping, Lotte Hotel,

Lotte E&C

Deal size: undisclosedPlot: 2-1, 2-2, 2-3, 2-4, 2-5 and 2-6Status: Signed the contract with HCMC People’s Committee, master planning

Eco–Smart City

Source: RCA, Press Releases

Market Outlook

20

Market Outlook – the key trends

• Continued strong interest from international investors, with buyers primarily from the Asia Pacific region, especially Japan, Singapore, and Korea;

• While it remains to be seen if the Chinese Government will introduce new rules around foreign investments, interest from Chinese companies into Vietnam still remains. We called a “pause-review-resume” process.

• Strong preference for income producing assets with expected rental and capital value growth;

• Due to the strong focus on Vietnam from regional investors, we expect M&A activities to reach record levels in 2017 and 2018.

© 2017 Jones Lang LaSalle IP, Inc. All rights reserved. 21

Khanh Nguyen, Associate Director, Vietnam, JLL