Embed Size (px)

Citation preview

Making sense of Vietnam market

1

WHAT WERE OUTSTANDING OVER THE WEEK?

Urea market remained quite bearish,

urea futures slumped

STC’s June 22 tender did not achieve

the expected results on low offers

Urea prices in the local market of

China continued to plunge

Urea prices in the Central Region

rebounded on tight supply

Urea prices at Bat Xat border gate fell

by about VND 200-300/kg

Fertilizer imports in June 2013 fell by

19.23% in volume and 23% in value

compared to the previous month

Weekly Report

Vietnam

Fertilizer

Market

(Week 24/06/2013 –27/06/2013)

ANALYSTS

Nguyen Trang Nhung

Dao Thi Dung

Tel: 84 4 7300 4550

Email:

Skype: nhung.agromonitor

daodungagm

_____________________________

Vietnam Market Analysis and Forecast

Joint Stock Company - Agromonitor

Room 1604, Building No. 101 Lang Ha

Street, Dong Da District, Hanoi

Tel: 84 4 6273 3596 /Mobile: 0943 411

411

Email: [email protected]

www.agromonitor.vn

Making sense of Vietnam market

2

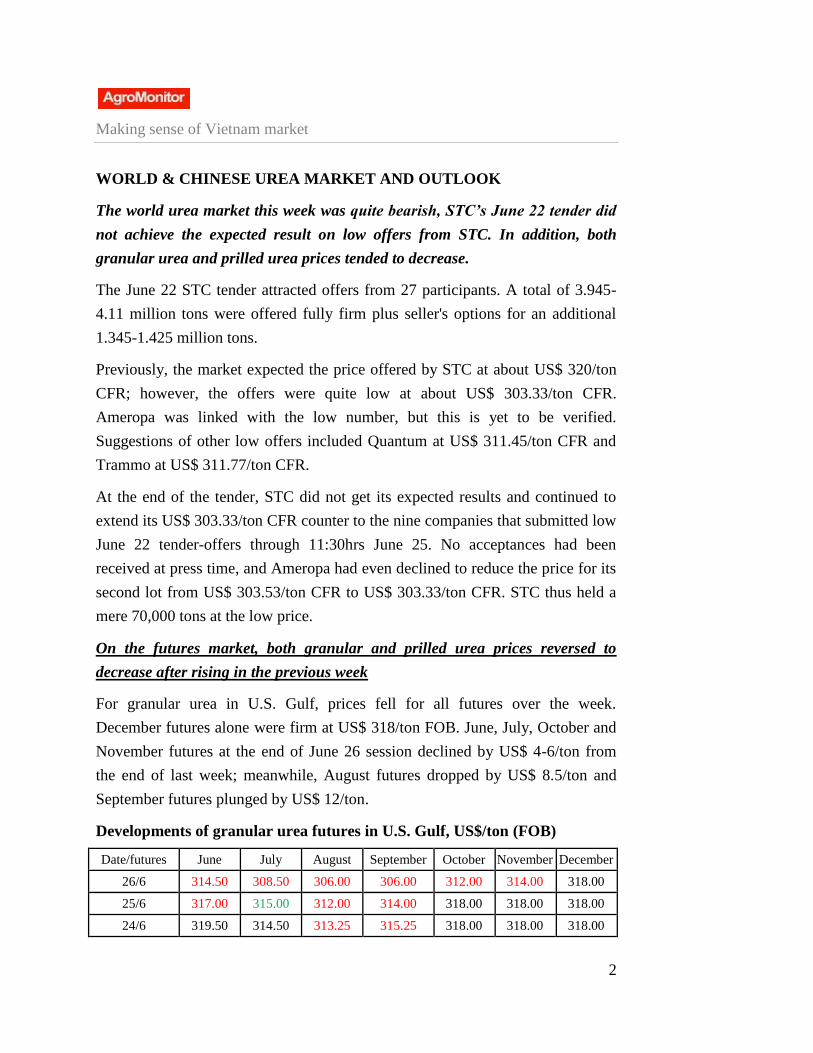

WORLD & CHINESE UREA MARKET AND OUTLOOK

The world urea market this week was quite bearish, STC’s June 22 tender did

not achieve the expected result on low offers from STC. In addition, both

granular urea and prilled urea prices tended to decrease.

The June 22 STC tender attracted offers from 27 participants. A total of 3.945-

4.11 million tons were offered fully firm plus seller's options for an additional

1.345-1.425 million tons.

Previously, the market expected the price offered by STC at about US$ 320/ton

CFR; however, the offers were quite low at about US$ 303.33/ton CFR.

Ameropa was linked with the low number, but this is yet to be verified.

Suggestions of other low offers included Quantum at US$ 311.45/ton CFR and

Trammo at US$ 311.77/ton CFR.

At the end of the tender, STC did not get its expected results and continued to

extend its US$ 303.33/ton CFR counter to the nine companies that submitted low

June 22 tender-offers through 11:30hrs June 25. No acceptances had been

received at press time, and Ameropa had even declined to reduce the price for its

second lot from US$ 303.53/ton CFR to US$ 303.33/ton CFR. STC thus held a

mere 70,000 tons at the low price.

On the futures market, both granular and prilled urea prices reversed to

decrease after rising in the previous week

For granular urea in U.S. Gulf, prices fell for all futures over the week.

December futures alone were firm at US$ 318/ton FOB. June, July, October and

November futures at the end of June 26 session declined by US$ 4-6/ton from

the end of last week; meanwhile, August futures dropped by US$ 8.5/ton and

September futures plunged by US$ 12/ton.

Developments of granular urea futures in U.S. Gulf, US$/ton (FOB)

Date/futures June July August September October November December

26/6 314.50 308.50 306.00 306.00 312.00 314.00 318.00

25/6 317.00 315.00 312.00 314.00 318.00 318.00 318.00

24/6 319.50 314.50 313.25 315.25 318.00 318.00 318.00

Making sense of Vietnam market

3

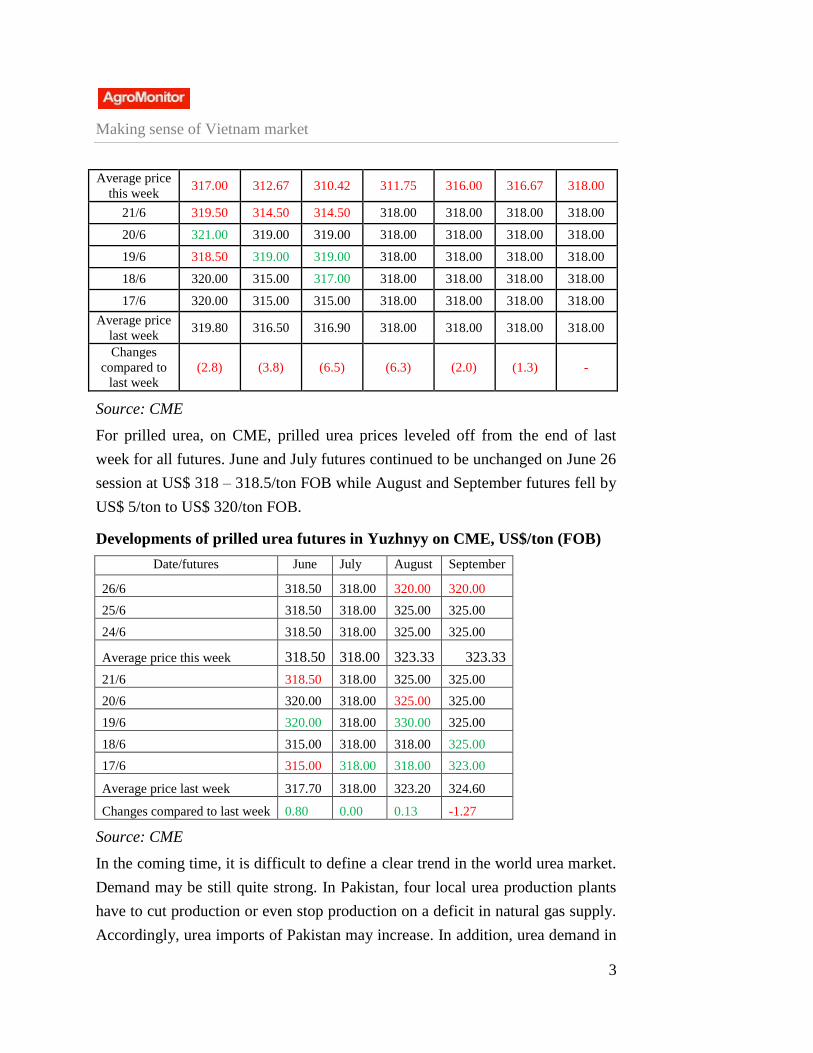

Average price

this week 317.00 312.67 310.42 311.75 316.00 316.67 318.00

21/6 319.50 314.50 314.50 318.00 318.00 318.00 318.00

20/6 321.00 319.00 319.00 318.00 318.00 318.00 318.00

19/6 318.50 319.00 319.00 318.00 318.00 318.00 318.00

18/6 320.00 315.00 317.00 318.00 318.00 318.00 318.00

17/6 320.00 315.00 315.00 318.00 318.00 318.00 318.00

Average price

last week 319.80 316.50 316.90 318.00 318.00 318.00 318.00

Changes

compared to

last week

(2.8) (3.8) (6.5) (6.3) (2.0) (1.3) -

Source: CME

For prilled urea, on CME, prilled urea prices leveled off from the end of last

week for all futures. June and July futures continued to be unchanged on June 26

session at US$ 318 – 318.5/ton FOB while August and September futures fell by

US$ 5/ton to US$ 320/ton FOB.

Developments of prilled urea futures in Yuzhnyy on CME, US$/ton (FOB)

Date/futures June July August September

26/6 318.50 318.00 320.00 320.00

25/6 318.50 318.00 325.00 325.00

24/6 318.50 318.00 325.00 325.00

Average price this week 318.50 318.00 323.33 323.33

21/6 318.50 318.00 325.00 325.00

20/6 320.00 318.00 325.00 325.00

19/6 320.00 318.00 330.00 325.00

18/6 315.00 318.00 318.00 325.00

17/6 315.00 318.00 318.00 323.00

Average price last week 317.70 318.00 323.20 324.60

Changes compared to last week 0.80 0.00 0.13 -1.27

Source: CME

In the coming time, it is difficult to define a clear trend in the world urea market.

Demand may be still quite strong. In Pakistan, four local urea production plants

have to cut production or even stop production on a deficit in natural gas supply.

Accordingly, urea imports of Pakistan may increase. In addition, urea demand in

Making sense of Vietnam market

4

India and other countries may also experience a soar. Meanwhile, supply remains

quite ample, especially when China starts to enter urea low-export tax window in

July. Some urea producers in China are currently shipping urea to the U.S., but

they have been unable to sell urea, which partly impacts urea supply in the U.S.

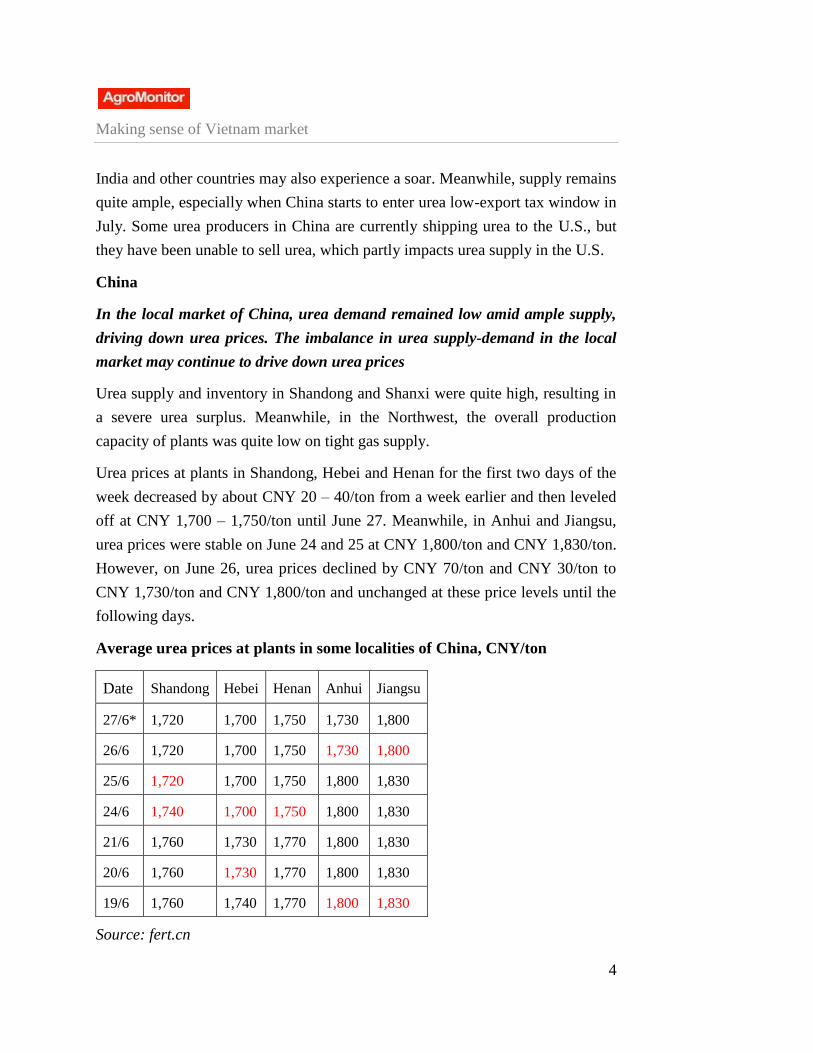

China

In the local market of China, urea demand remained low amid ample supply,

driving down urea prices. The imbalance in urea supply-demand in the local

market may continue to drive down urea prices

Urea supply and inventory in Shandong and Shanxi were quite high, resulting in

a severe urea surplus. Meanwhile, in the Northwest, the overall production

capacity of plants was quite low on tight gas supply.

Urea prices at plants in Shandong, Hebei and Henan for the first two days of the

week decreased by about CNY 20 – 40/ton from a week earlier and then leveled

off at CNY 1,700 – 1,750/ton until June 27. Meanwhile, in Anhui and Jiangsu,

urea prices were stable on June 24 and 25 at CNY 1,800/ton and CNY 1,830/ton.

However, on June 26, urea prices declined by CNY 70/ton and CNY 30/ton to

CNY 1,730/ton and CNY 1,800/ton and unchanged at these price levels until the

following days.

Average urea prices at plants in some localities of China, CNY/ton

Date Shandong Hebei Henan Anhui Jiangsu

27/6* 1,720 1,700 1,750 1,730 1,800

26/6 1,720 1,700 1,750 1,730 1,800

25/6 1,720 1,700 1,750 1,800 1,830

24/6 1,740 1,700 1,750 1,800 1,830

21/6 1,760 1,730 1,770 1,800 1,830

20/6 1,760 1,730 1,770 1,800 1,830

19/6 1,760 1,740 1,770 1,800 1,830

Source: fert.cn

Making sense of Vietnam market

5

Prices on June*: Projected

On export channel, many urea cargos shipped to the U.S. have not been able to

be sold. Export urea prices may continue to be revised down when STC’s tender

has a low offer of US$ 303.33/ton CFR. Accordingly, with a shipment cost of

about US$ 17 – 20/ton from China, the netback price in China will be about US$

283 – 286/ton FOB.

Last week, China rejected to supply urea at US$ 310/ton FOB and set a target to

sell urea at US$ 320/ton FOB; however, afterwards, China had to accept to sell

urea at US$ 300/ton FOB.

2. WORLD & CHINESE DAP MARKET AND OUTLOOK

DAP prices continued to be revised down in many regions and there were not

many transactions

Owing to the depreciation of Rupee, DAP importers of India were quite reserved.

Over the week, DAP prices of suppliers were about US$ 490 – 500/ton CIF.

However, there have not been any transactions at this price level.

DAP prices in the U.S. continued to be revised down to US$ 426/ton FOB.

According to a price quote from USDA, DAP prices in Illinois averaged US$

600/ton; and Southern Plains: down to US$ 550/ton.

China

The average DAP prices in the local market of China at the beginning of this

week were quite stable from the end of last week. However, on June 26

afternoon, urea prices reversed to drop by CNY 26/ton to CNY 2,880/ton.

Local DAP prices of China, CNY/ton

Date 26/6 25/6 24/6 23/6 21/6 20/6 19/6 18/6

Price 2880.00 2906.67 2906.67 2906.67 2906.67 2900 2906.67 2906.67

Source: sunsirs

Making sense of Vietnam market

6

3. POTASH MARKET

Potash prices continued to be low last week. According to a price quote from

USDA, retail potash prices in Illinois were US$ 520/ton.

Ural Kali and Belarus Potash signed a contract to supply over 1 million tons of

potash to India at US$ 427/ton. In January 2014, Urals Kali will sign a new

contract with India.

China

Chinese potash market remained quite bearish, some small import contracts were

defined in July. Especially, it is likely that contracts between China and suppliers

will be hard to be concluded in the coming month and will put pressure on the

spot market.

MOP prices in the local market of China this week inched lower by CNY 3/ton

from the end of last week to CNY 2,535.00/ton and were temporarily unchanged

until June 26.

Local MOP prices of China, CNY/ton

26/6 25/6 24/6 23/6 22/6 21/6

2535.00 2,535.00 2,535.00 2,538.33 2,538.33 2,538.33

Source: sunsirs

4. AMMONIA, UAN, SAN MAKRETS

Ammonia

Last week, ammonia prices in the world market dropped sharply in many

regions. In Yuzhnyy, ammonia prices fell by as much as US$ 35/ton to US$ 460

– 515/ton FOB; ammonia prices in Baltic also experienced an equivalent

decrease to US$ 470 – 525/ton FOB.

Making sense of Vietnam market

7

Ammonia prices in the world market, US$/ton

Baltic,

FOB

Yuzhnyy,

FOB

North

Africa,

FOB

Middle

East, FOB

India,

CIF

Southeast

Asia, CIF

Week (17-23/6)- 470 –

525

460-515 470-530 510 – 540 550-

580

467 – 635

Compared to

week (9-16/6)

-35 -35 -40 -15 -20 -58

Source: sunsirs

Fall prepay on the southwest Plains was as low as US$ 610/ton. Spot prices out

West aren’t that low, but some are at US$ 680/ton. Offers found by USDA last

week in Iowa and Illinois don’t yet show much of a reduction from spring highs.

Iowa was steady at US$ 882/ton, though the average in Illinois was down around

US$ 25/ton from its highs at US$ 866/ton, with some dealers there down to US$

750/ton.

UAN

Last week, UAN prices continued to be revised down. In U.S. Gulf, prices of

UAN 32% fell by US$ 4.5/st to US$ 240/st. Retailed UAN prices in the West

were US$ 350 – 380/ton for UAN 28%. As cited by USDA, prices of UAN 28%

in Iowa last week were around US$ 354 – 411/ton.

SA

Last week, the world SA prices rallied in Baltic while continuing to decrease in

other markets.

SA prices in some regions last week, US$/ton

Baltic,

FOB

Black

Sea

Southeast Asia,

CIF

Brazil,

CIF

Week (June 17-23) 145 145 160-165 180-185

Changes compared to week (June

10 - 16)

+5 -5 0 0

Source: fert.cn

Making sense of Vietnam market

8

DOMESTIC MARKET

Although domestic fertilizer demand tended to be weaker from several weeks

earlier, the demand was generally quite strong to serve summer-fall rice, fall-

winter rice, secondary crops and industrial crops. Volume of imported fertilizers

continued to be complemented in regions but with a small quantity. At Tran

Xuan Soan market, Southeastern region, Southwestern region, Central Region,

etc. there was still a tight supply of domestically-manufactured urea in some

localities over the week; urea prices rebounded after inching lower in the

previous week. Meanwhile, in the Central Region, although supply of Phu My

urea was also quite scarce, prices of Phu My urea generally remained quite stable

on weak demand. In Lam Dong, prices of urea were on the decrease. Prices of

other types such as NPK, SA and potash inched lower or temporarily leveled off.

Prices of urea reversed to go up on quite tight supply in the South

Urea supply is still being complemented in the South but with small quantity.

Volume of urea domestically manufactured is still quite tight while urea imports

have not been ample. Chinese urea was shipped to the South but the supply is

quite scarce. From early June to date, there has been no vessel carrying Chinese

urea arrived at Saigon ports but vessels carrying Indonesian urea and Philippine

urea constantly arrived at the ports. Specifically, at the end of a week earlier, one

vessel carrying 4,620 tons of Malaysian urea arrived at the port and it is

projected that this week, additional three vessels carrying 15,000 tons of urea

(including two vessels carrying 6,000 tons of Indonesian urea each and one

vessel carrying 3,000 tons of Malaysian urea) will arrive at Saigon ports.

Accordingly, prices of Phu My urea and Ca Mau urea rallied over the week

while there were very few transactions for Chinese urea.

It is projected that in the coming time, tight supply in some localities in the

region will likely be improved thanks to supply of domestically manufactured

urea when Phu My urea plant launches its products to the market as scheduled.

In addition, supply of imported urea will be also higher. Specifically, supply of

Chinese urea will be less tight because two vessels carrying about 9,500 tons of

Making sense of Vietnam market

9

Chinese urea are projected to arrive at Saigon port in the coming week.

However, demand for fertilizer to fertilize summer-fall rice will be on rise, so

fertilizer prices may be stable or even inch up in the coming time.

In the Central Region and Central Highlands, demand for fertilizers from

industrial crops was also weaker, so the demand did not put pressure on the

supply. In the Central Region, supply of Phu My urea over the week was quite

scarce; there was no supply of Chinese urea but vessels carrying Indonesian urea

constantly arrived at the ports. However, Indonesian urea was mainly shipped to

the Central Region on strong demand. Prices of urea in the regions temporarily

leveled off or even continued to inch lower over the week.

It is very likely that the above trend will be sustained in the short term when

demand does not rally robustly and a vessel carrying about 3,000-4,000 tons of

Phu My urea is projected to arrive at Da Nang port in the coming week. In

addition, another two vessels carrying about 4,000 tons of Indonesian urea is

also coming to the region in the coming time.

Prices of other types such as NPK, SA and potash in the South tended to go

down on quite ample supply amid weak demand. Prices of the items over the

week temporarily leveled off after dropping quite sharply in the previous week.

This week, two vessels carrying 12,000 tons of Philippine NPK bagged

are projected to arrive at Saigon ports. Accordingly, about 30,200 tons of

NPK will be imported through Saigon ports in June.

One vessel carrying 3,299 tons of Philippine SA bulk and one vessel

carrying 6,000 tons of Korean SA bulk arrived at Saigon ports. Therefore,

in June, SA imports through Saigon ports were 17,299 tons.

Universal Durban vessel carrying over 22,000 tons of Israeli potash

imported by Vinacam arrived at Khanh Hoi port on June 25, one day

earlier than expected. Of the figure, over 16,000 tons are projected to be

discharged to serve the demand in the South and over 7,000 tons are

projected to be shipped to the North.

Making sense of Vietnam market

10

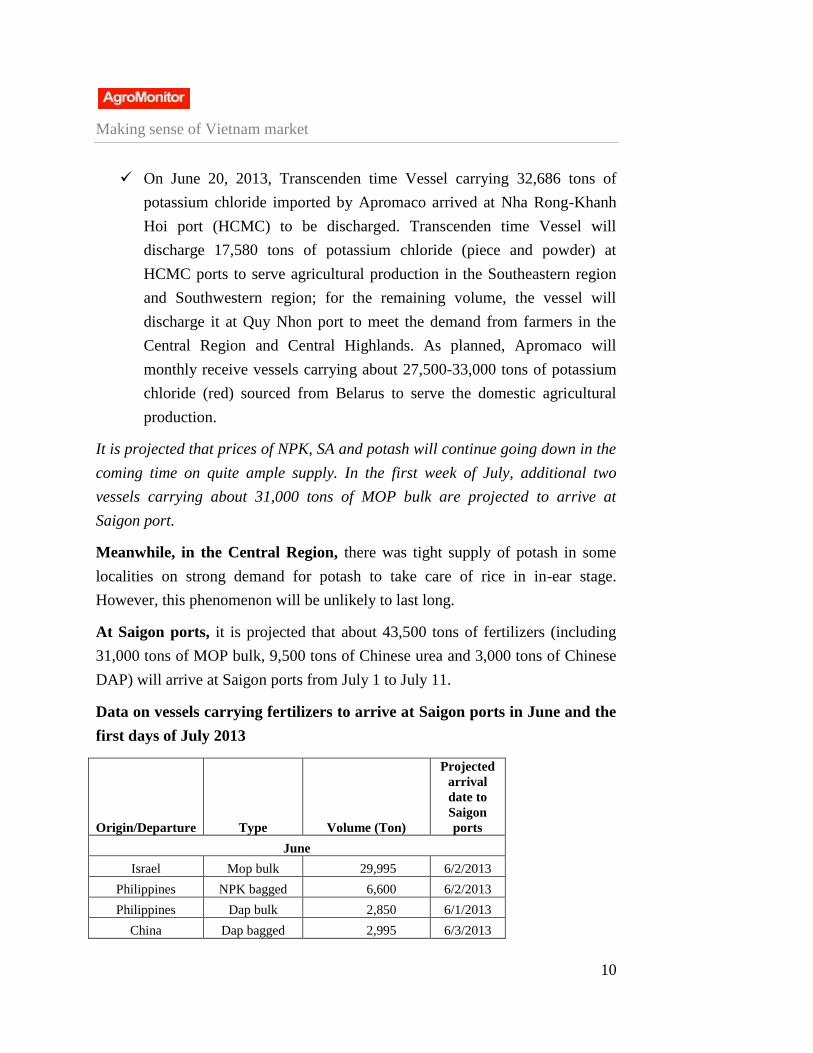

On June 20, 2013, Transcenden time Vessel carrying 32,686 tons of

potassium chloride imported by Apromaco arrived at Nha Rong-Khanh

Hoi port (HCMC) to be discharged. Transcenden time Vessel will

discharge 17,580 tons of potassium chloride (piece and powder) at

HCMC ports to serve agricultural production in the Southeastern region

and Southwestern region; for the remaining volume, the vessel will

discharge it at Quy Nhon port to meet the demand from farmers in the

Central Region and Central Highlands. As planned, Apromaco will

monthly receive vessels carrying about 27,500-33,000 tons of potassium

chloride (red) sourced from Belarus to serve the domestic agricultural

production.

It is projected that prices of NPK, SA and potash will continue going down in the

coming time on quite ample supply. In the first week of July, additional two

vessels carrying about 31,000 tons of MOP bulk are projected to arrive at

Saigon port.

Meanwhile, in the Central Region, there was tight supply of potash in some

localities on strong demand for potash to take care of rice in in-ear stage.

However, this phenomenon will be unlikely to last long.

At Saigon ports, it is projected that about 43,500 tons of fertilizers (including

31,000 tons of MOP bulk, 9,500 tons of Chinese urea and 3,000 tons of Chinese

DAP) will arrive at Saigon ports from July 1 to July 11.

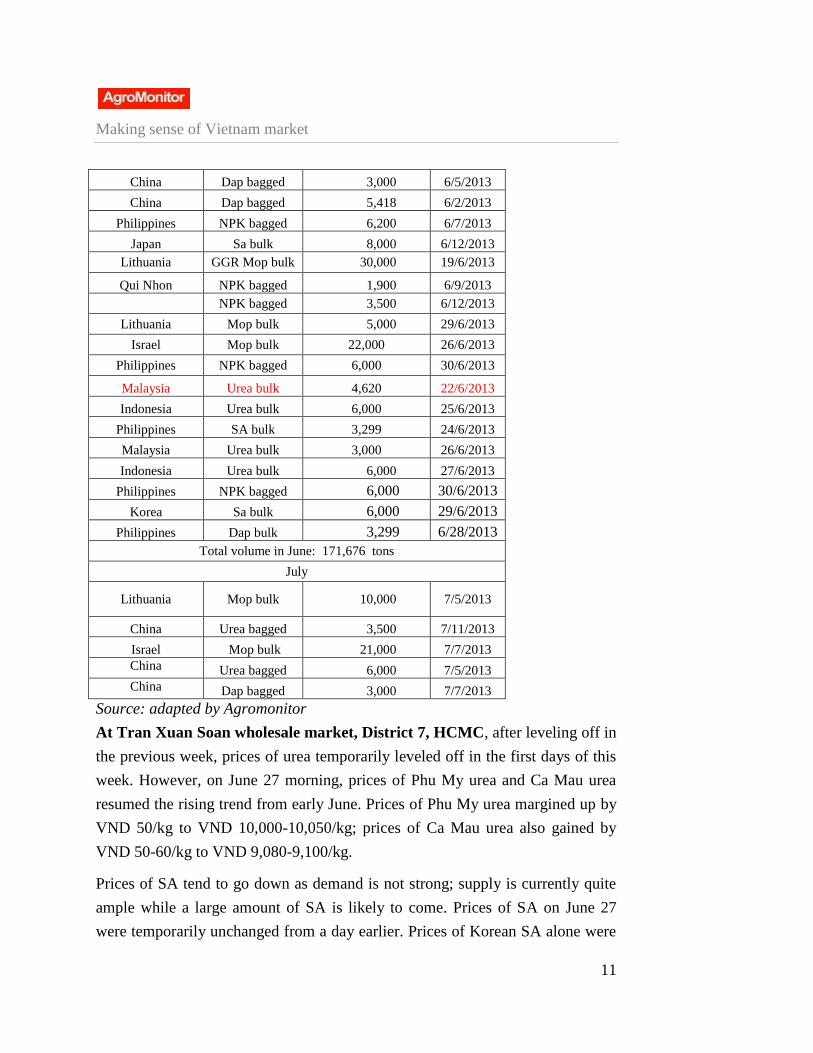

Data on vessels carrying fertilizers to arrive at Saigon ports in June and the

first days of July 2013

Origin/Departure Type Volume (Ton)

Projected

arrival

date to

Saigon

ports

June

Israel Mop bulk 29,995 6/2/2013

Philippines NPK bagged 6,600 6/2/2013

Philippines Dap bulk 2,850 6/1/2013

China Dap bagged 2,995 6/3/2013

Making sense of Vietnam market

11

China Dap bagged 3,000 6/5/2013

China Dap bagged 5,418 6/2/2013

Philippines NPK bagged 6,200 6/7/2013

Japan Sa bulk 8,000 6/12/2013

Lithuania GGR Mop bulk 30,000 19/6/2013

Qui Nhon NPK bagged 1,900 6/9/2013

NPK bagged 3,500 6/12/2013

Lithuania Mop bulk 5,000 29/6/2013

Israel Mop bulk 22,000 26/6/2013

Philippines NPK bagged 6,000 30/6/2013

Malaysia Urea bulk 4,620 22/6/2013

Indonesia Urea bulk 6,000 25/6/2013

Philippines SA bulk 3,299 24/6/2013

Malaysia Urea bulk 3,000 26/6/2013

Indonesia Urea bulk 6,000 27/6/2013

Philippines NPK bagged 6,000 30/6/2013

Korea Sa bulk 6,000 29/6/2013

Philippines Dap bulk 3,299 6/28/2013

Total volume in June: 171,676 tons

July

Lithuania Mop bulk 10,000 7/5/2013

China Urea bagged 3,500 7/11/2013

Israel Mop bulk 21,000 7/7/2013

China Urea bagged 6,000 7/5/2013

China Dap bagged 3,000 7/7/2013

Source: adapted by Agromonitor

At Tran Xuan Soan wholesale market, District 7, HCMC, after leveling off in

the previous week, prices of urea temporarily leveled off in the first days of this

week. However, on June 27 morning, prices of Phu My urea and Ca Mau urea

resumed the rising trend from early June. Prices of Phu My urea margined up by

VND 50/kg to VND 10,000-10,050/kg; prices of Ca Mau urea also gained by

VND 50-60/kg to VND 9,080-9,100/kg.

Prices of SA tend to go down as demand is not strong; supply is currently quite

ample while a large amount of SA is likely to come. Prices of SA on June 27

were temporarily unchanged from a day earlier. Prices of Korean SA alone were

Making sense of Vietnam market

12

VND 4,920-5,000/kg but some enterprises were preparing for offering Korean

SA at lower prices of VND 4,800-4,900/kg only.

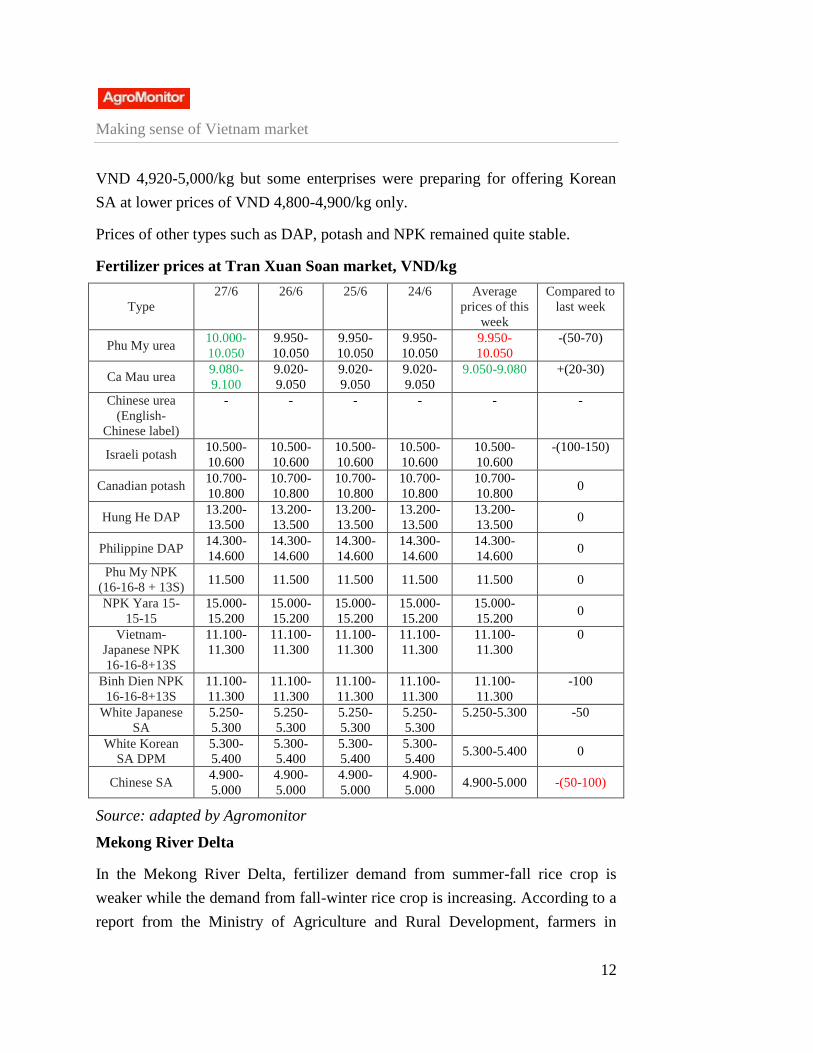

Prices of other types such as DAP, potash and NPK remained quite stable.

Fertilizer prices at Tran Xuan Soan market, VND/kg

Type

27/6 26/6 25/6 24/6 Average

prices of this

week

Compared to

last week

Phu My urea 10.000-

10.050

9.950-

10.050

9.950-

10.050

9.950-

10.050

9.950-

10.050

-(50-70)

Ca Mau urea 9.080-

9.100

9.020-

9.050

9.020-

9.050

9.020-

9.050

9.050-9.080 +(20-30)

Chinese urea

(English-

Chinese label)

- - - - - -

Israeli potash 10.500-

10.600

10.500-

10.600

10.500-

10.600

10.500-

10.600

10.500-

10.600

-(100-150)

Canadian potash 10.700-

10.800

10.700-

10.800

10.700-

10.800

10.700-

10.800

10.700-

10.800 0

Hung He DAP 13.200-

13.500

13.200-

13.500

13.200-

13.500

13.200-

13.500

13.200-

13.500 0

Philippine DAP 14.300-

14.600

14.300-

14.600

14.300-

14.600

14.300-

14.600

14.300-

14.600 0

Phu My NPK

(16-16-8 + 13S) 11.500 11.500 11.500 11.500 11.500 0

NPK Yara 15-

15-15

15.000-

15.200

15.000-

15.200

15.000-

15.200

15.000-

15.200

15.000-

15.200 0

Vietnam-

Japanese NPK

16-16-8+13S

11.100-

11.300

11.100-

11.300

11.100-

11.300

11.100-

11.300

11.100-

11.300

0

Binh Dien NPK

16-16-8+13S

11.100-

11.300

11.100-

11.300

11.100-

11.300

11.100-

11.300

11.100-

11.300

-100

White Japanese

SA

5.250-

5.300

5.250-

5.300

5.250-

5.300

5.250-

5.300

5.250-5.300 -50

White Korean

SA DPM

5.300-

5.400

5.300-

5.400

5.300-

5.400

5.300-

5.400 5.300-5.400 0

Chinese SA 4.900-

5.000

4.900-

5.000

4.900-

5.000

4.900-

5.000 4.900-5.000 -(50-100)

Source: adapted by Agromonitor

Mekong River Delta

In the Mekong River Delta, fertilizer demand from summer-fall rice crop is

weaker while the demand from fall-winter rice crop is increasing. According to a

report from the Ministry of Agriculture and Rural Development, farmers in

Making sense of Vietnam market

13

Mekong River Delta are deploying a production plan for fall-winter rice crop and

tenth-month rice crop with the planned rice sowed area of 897,630 ha (including

700,000 ha of fall-winter rice). According to the schedule, in June, about

200,000 ha of rice is projected to be sowed; July: 400,000 ha and August:

200,000 ha.

Sowing pace of fall-winter rice crop (the third crop) this year soared. As of June

15, farmers in the whole Mekong River Delta sowed 157 thousand ha, up sharply

from over 40 thousand ha of the same period last year. Some provinces with fast

sowing pace included Dong Thap (89.2 thousand ha, up by 4 times year on year),

Can Tho city (28.5 thousand ha, up by 3 times), etc. However, in some remote

areas of Kien Giang, Hau Giang, Vinh Long, rice sowed area was lower

compared to the same period last year or farmers in some areas even have not

sowed rice because of unfavorable weather and water shortage.

Fertilizer demand was generally quite strong; prices of urea continued to go up

while prices of other types temporarily leveled off.

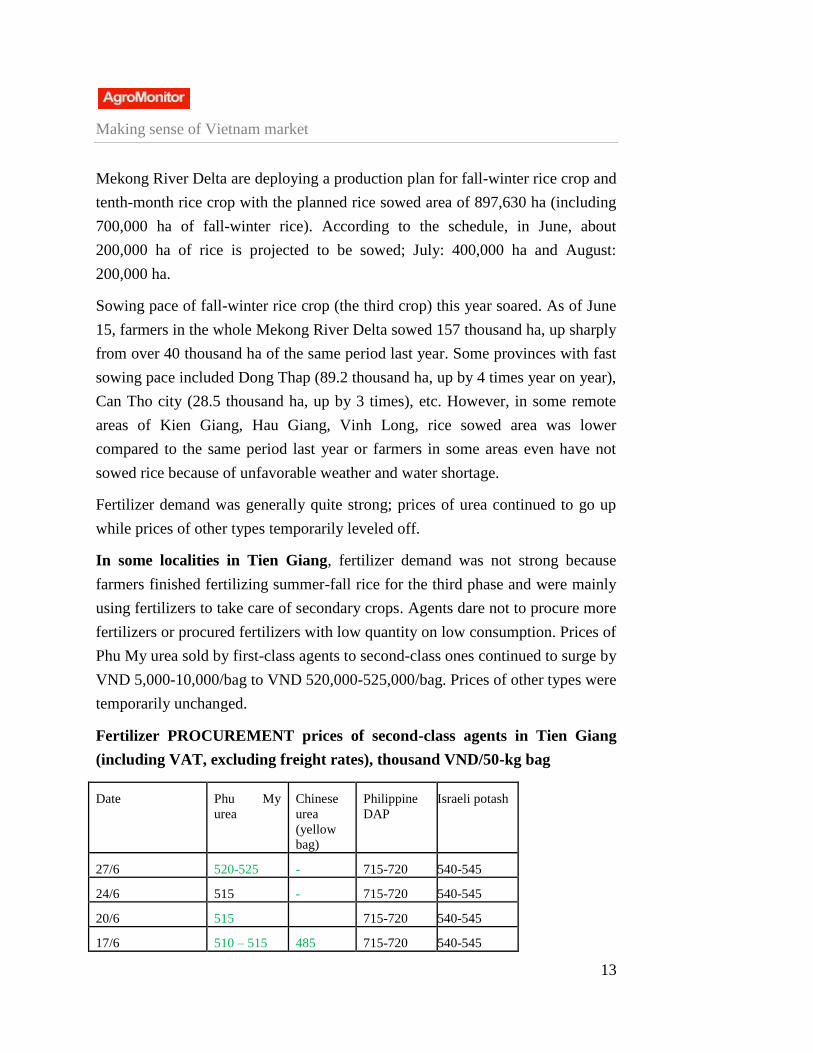

In some localities in Tien Giang, fertilizer demand was not strong because

farmers finished fertilizing summer-fall rice for the third phase and were mainly

using fertilizers to take care of secondary crops. Agents dare not to procure more

fertilizers or procured fertilizers with low quantity on low consumption. Prices of

Phu My urea sold by first-class agents to second-class ones continued to surge by

VND 5,000-10,000/bag to VND 520,000-525,000/bag. Prices of other types were

temporarily unchanged.

Fertilizer PROCUREMENT prices of second-class agents in Tien Giang

(including VAT, excluding freight rates), thousand VND/50-kg bag

Date Phu My

urea

Chinese

urea

(yellow

bag)

Philippine

DAP

Israeli potash

27/6 520-525 - 715-720 540-545

24/6 515 - 715-720 540-545

20/6 515 715-720 540-545

17/6 510 – 515 485 715-720 540-545

Making sense of Vietnam market

14

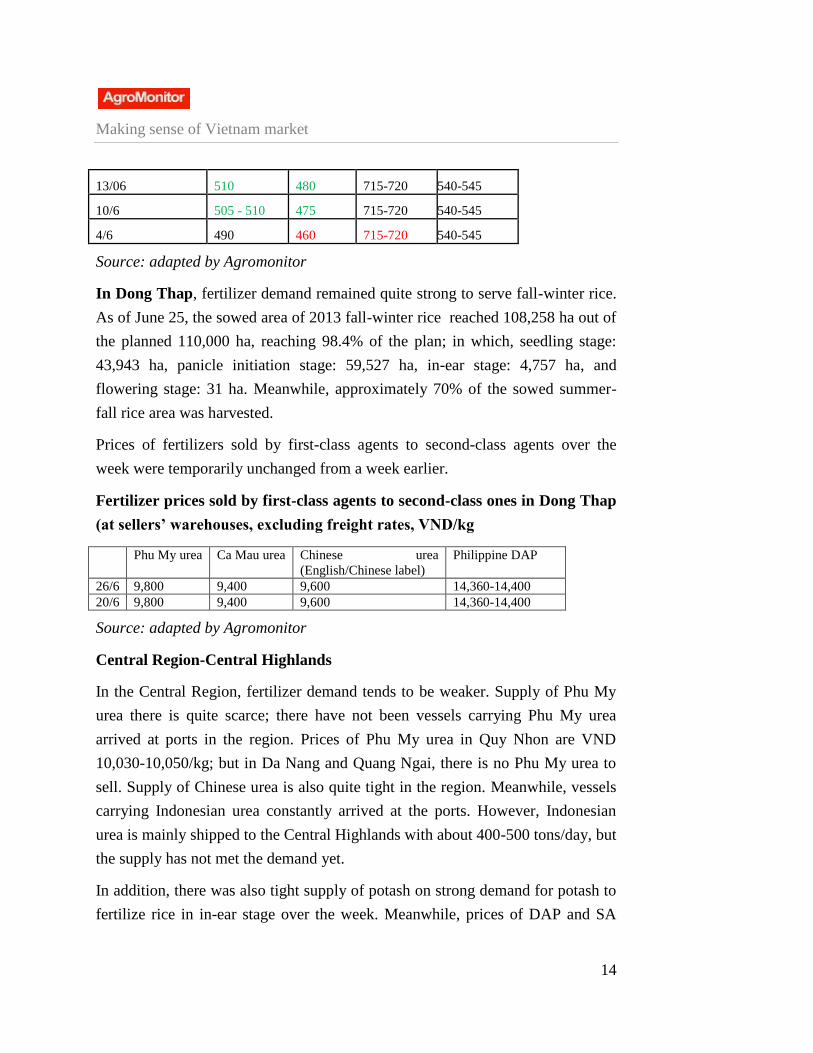

13/06 510 480 715-720 540-545

10/6 505 - 510 475 715-720 540-545

4/6 490 460 715-720 540-545

Source: adapted by Agromonitor

In Dong Thap, fertilizer demand remained quite strong to serve fall-winter rice.

As of June 25, the sowed area of 2013 fall-winter rice reached 108,258 ha out of

the planned 110,000 ha, reaching 98.4% of the plan; in which, seedling stage:

43,943 ha, panicle initiation stage: 59,527 ha, in-ear stage: 4,757 ha, and

flowering stage: 31 ha. Meanwhile, approximately 70% of the sowed summer-

fall rice area was harvested.

Prices of fertilizers sold by first-class agents to second-class agents over the

week were temporarily unchanged from a week earlier.

Fertilizer prices sold by first-class agents to second-class ones in Dong Thap

(at sellers’ warehouses, excluding freight rates, VND/kg

Phu My urea Ca Mau urea Chinese urea

(English/Chinese label)

Philippine DAP

26/6 9,800 9,400 9,600 14,360-14,400

20/6 9,800 9,400 9,600 14,360-14,400

Source: adapted by Agromonitor

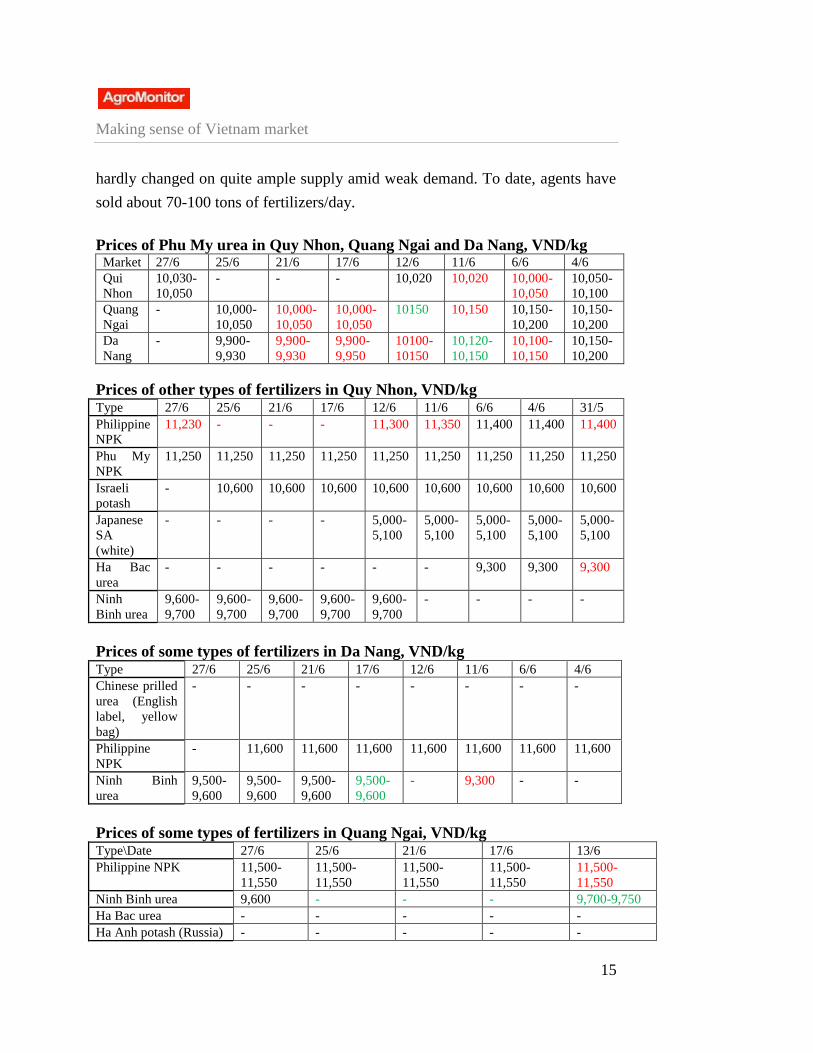

Central Region-Central Highlands

In the Central Region, fertilizer demand tends to be weaker. Supply of Phu My

urea there is quite scarce; there have not been vessels carrying Phu My urea

arrived at ports in the region. Prices of Phu My urea in Quy Nhon are VND

10,030-10,050/kg; but in Da Nang and Quang Ngai, there is no Phu My urea to

sell. Supply of Chinese urea is also quite tight in the region. Meanwhile, vessels

carrying Indonesian urea constantly arrived at the ports. However, Indonesian

urea is mainly shipped to the Central Highlands with about 400-500 tons/day, but

the supply has not met the demand yet.

In addition, there was also tight supply of potash on strong demand for potash to

fertilize rice in in-ear stage over the week. Meanwhile, prices of DAP and SA

Making sense of Vietnam market

15

hardly changed on quite ample supply amid weak demand. To date, agents have

sold about 70-100 tons of fertilizers/day.

Prices of Phu My urea in Quy Nhon, Quang Ngai and Da Nang, VND/kg Market 27/6 25/6 21/6 17/6 12/6 11/6 6/6 4/6

Qui

Nhon

10,030-

10,050

- - - 10,020 10,020 10,000-

10,050

10,050-

10,100

Quang

Ngai

- 10,000-

10,050

10,000-

10,050

10,000-

10,050

10150 10,150 10,150-

10,200

10,150-

10,200

Da

Nang

- 9,900-

9,930

9,900-

9,930

9,900-

9,950

10100-

10150

10,120-

10,150

10,100-

10,150

10,150-

10,200

Prices of other types of fertilizers in Quy Nhon, VND/kg Type 27/6 25/6 21/6 17/6 12/6 11/6 6/6 4/6 31/5

Philippine

NPK

11,230 - - - 11,300 11,350 11,400 11,400 11,400

Phu My

NPK

11,250 11,250 11,250 11,250 11,250 11,250 11,250 11,250 11,250

Israeli

potash

- 10,600 10,600 10,600 10,600 10,600 10,600 10,600 10,600

Japanese

SA

(white)

- - - - 5,000-

5,100

5,000-

5,100

5,000-

5,100

5,000-

5,100

5,000-

5,100

Ha Bac

urea

- - - - - - 9,300 9,300 9,300

Ninh

Binh urea

9,600-

9,700

9,600-

9,700

9,600-

9,700

9,600-

9,700

9,600-

9,700

- - - -

Prices of some types of fertilizers in Da Nang, VND/kg Type 27/6 25/6 21/6 17/6 12/6 11/6 6/6 4/6

Chinese prilled

urea (English

label, yellow

bag)

- - - - - - - -

Philippine

NPK

- 11,600 11,600 11,600 11,600 11,600 11,600 11,600

Ninh Binh

urea

9,500-

9,600

9,500-

9,600

9,500-

9,600

9,500-

9,600

- 9,300 - -

Prices of some types of fertilizers in Quang Ngai, VND/kg Type\Date 27/6 25/6 21/6 17/6 13/6

Philippine NPK 11,500-

11,550

11,500-

11,550

11,500-

11,550

11,500-

11,550

11,500-

11,550

Ninh Binh urea 9,600 - - - 9,700-9,750

Ha Bac urea - - - - -

Ha Anh potash (Russia) - - - - -

Making sense of Vietnam market

16

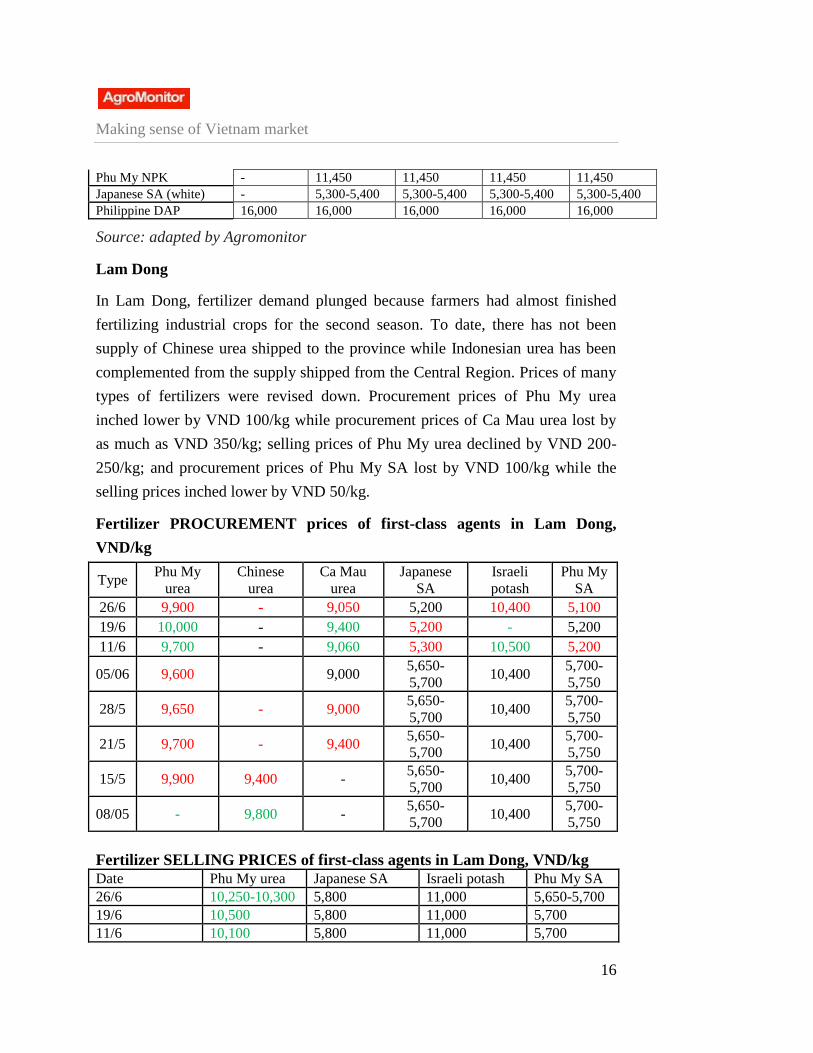

Phu My NPK - 11,450 11,450 11,450 11,450

Japanese SA (white) - 5,300-5,400 5,300-5,400 5,300-5,400 5,300-5,400

Philippine DAP 16,000 16,000 16,000 16,000 16,000

Source: adapted by Agromonitor

Lam Dong

In Lam Dong, fertilizer demand plunged because farmers had almost finished

fertilizing industrial crops for the second season. To date, there has not been

supply of Chinese urea shipped to the province while Indonesian urea has been

complemented from the supply shipped from the Central Region. Prices of many

types of fertilizers were revised down. Procurement prices of Phu My urea

inched lower by VND 100/kg while procurement prices of Ca Mau urea lost by

as much as VND 350/kg; selling prices of Phu My urea declined by VND 200-

250/kg; and procurement prices of Phu My SA lost by VND 100/kg while the

selling prices inched lower by VND 50/kg.

Fertilizer PROCUREMENT prices of first-class agents in Lam Dong,

VND/kg

Type Phu My

urea Chinese

urea Ca Mau

urea Japanese

SA Israeli

potash Phu My

SA

26/6 9,900 - 9,050 5,200 10,400 5,100

19/6 10,000 - 9,400 5,200 - 5,200

11/6 9,700 - 9,060 5,300 10,500 5,200

05/06 9,600

9,000 5,650-

5,700 10,400

5,700-

5,750

28/5 9,650 - 9,000 5,650-

5,700 10,400

5,700-

5,750

21/5 9,700 - 9,400 5,650-

5,700 10,400

5,700-

5,750

15/5 9,900 9,400 - 5,650-

5,700 10,400

5,700-

5,750

08/05 - 9,800 - 5,650-

5,700 10,400

5,700-

5,750

Fertilizer SELLING PRICES of first-class agents in Lam Dong, VND/kg

Date Phu My urea Japanese SA Israeli potash Phu My SA

26/6 10,250-10,300 5,800 11,000 5,650-5,700

19/6 10,500 5,800 11,000 5,700

11/6 10,100 5,800 11,000 5,700

Making sense of Vietnam market

17

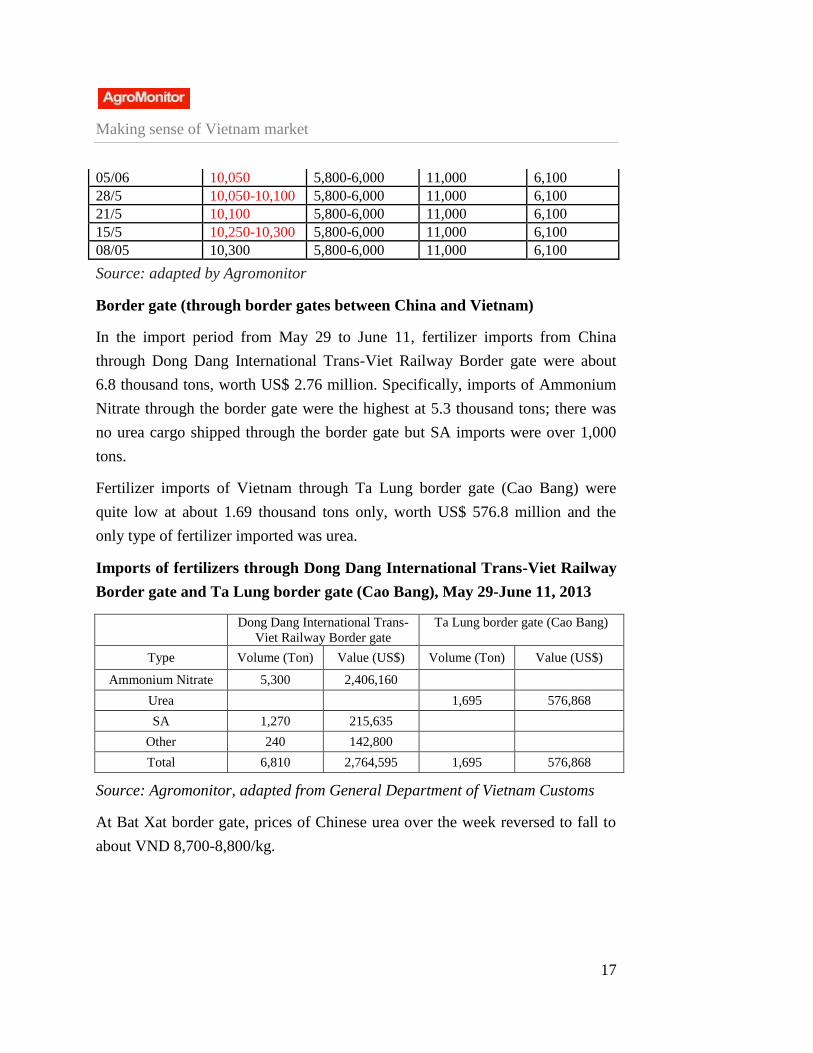

05/06 10,050 5,800-6,000 11,000 6,100

28/5 10,050-10,100 5,800-6,000 11,000 6,100 21/5 10,100 5,800-6,000 11,000 6,100

15/5 10,250-10,300 5,800-6,000 11,000 6,100

08/05 10,300 5,800-6,000 11,000 6,100

Source: adapted by Agromonitor

Border gate (through border gates between China and Vietnam)

In the import period from May 29 to June 11, fertilizer imports from China

through Dong Dang International Trans-Viet Railway Border gate were about

6.8 thousand tons, worth US$ 2.76 million. Specifically, imports of Ammonium

Nitrate through the border gate were the highest at 5.3 thousand tons; there was

no urea cargo shipped through the border gate but SA imports were over 1,000

tons.

Fertilizer imports of Vietnam through Ta Lung border gate (Cao Bang) were

quite low at about 1.69 thousand tons only, worth US$ 576.8 million and the

only type of fertilizer imported was urea.

Imports of fertilizers through Dong Dang International Trans-Viet Railway

Border gate and Ta Lung border gate (Cao Bang), May 29-June 11, 2013

Dong Dang International Trans-

Viet Railway Border gate

Ta Lung border gate (Cao Bang)

Type Volume (Ton) Value (US$) Volume (Ton) Value (US$)

Ammonium Nitrate 5,300 2,406,160

Urea

1,695 576,868

SA 1,270 215,635

Other 240 142,800

Total 6,810 2,764,595 1,695 576,868

Source: Agromonitor, adapted from General Department of Vietnam Customs

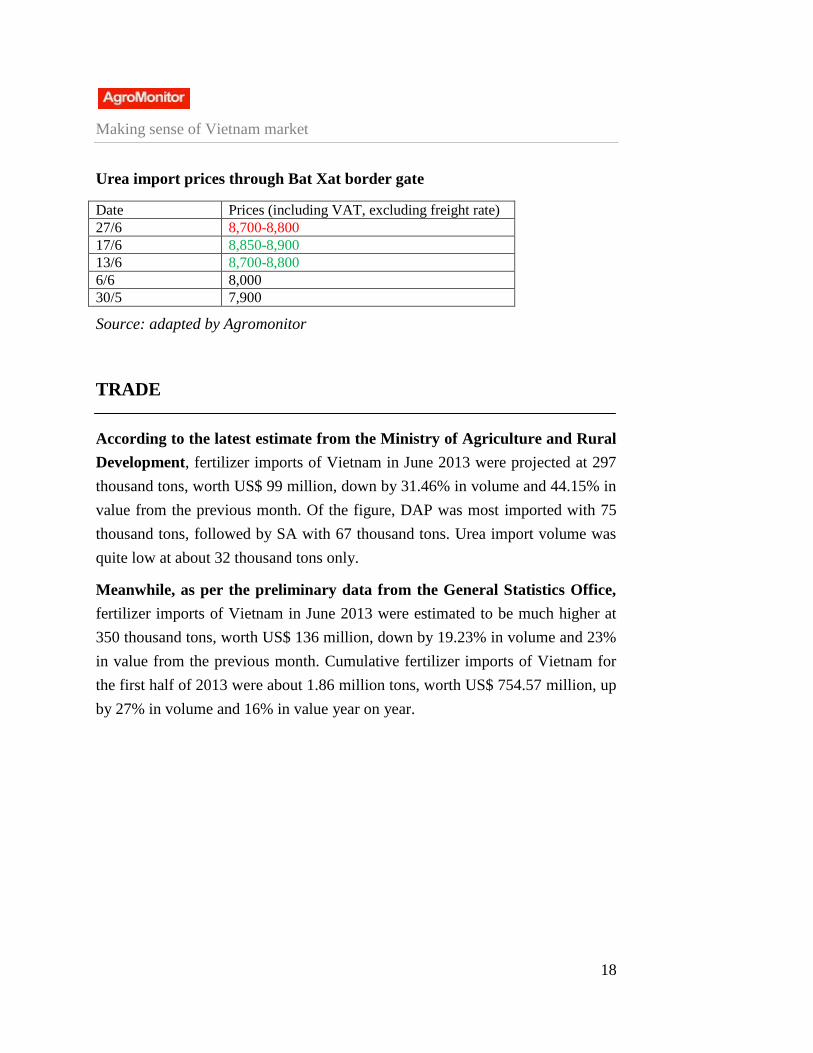

At Bat Xat border gate, prices of Chinese urea over the week reversed to fall to

about VND 8,700-8,800/kg.

Making sense of Vietnam market

18

Urea import prices through Bat Xat border gate

Date Prices (including VAT, excluding freight rate)

27/6 8,700-8,800

17/6 8,850-8,900

13/6 8,700-8,800

6/6 8,000

30/5 7,900

Source: adapted by Agromonitor

TRADE

According to the latest estimate from the Ministry of Agriculture and Rural

Development, fertilizer imports of Vietnam in June 2013 were projected at 297

thousand tons, worth US$ 99 million, down by 31.46% in volume and 44.15% in

value from the previous month. Of the figure, DAP was most imported with 75

thousand tons, followed by SA with 67 thousand tons. Urea import volume was

quite low at about 32 thousand tons only.

Meanwhile, as per the preliminary data from the General Statistics Office,

fertilizer imports of Vietnam in June 2013 were estimated to be much higher at

350 thousand tons, worth US$ 136 million, down by 19.23% in volume and 23%

in value from the previous month. Cumulative fertilizer imports of Vietnam for

the first half of 2013 were about 1.86 million tons, worth US$ 754.57 million, up

by 27% in volume and 16% in value year on year.

Making sense of Vietnam market

19

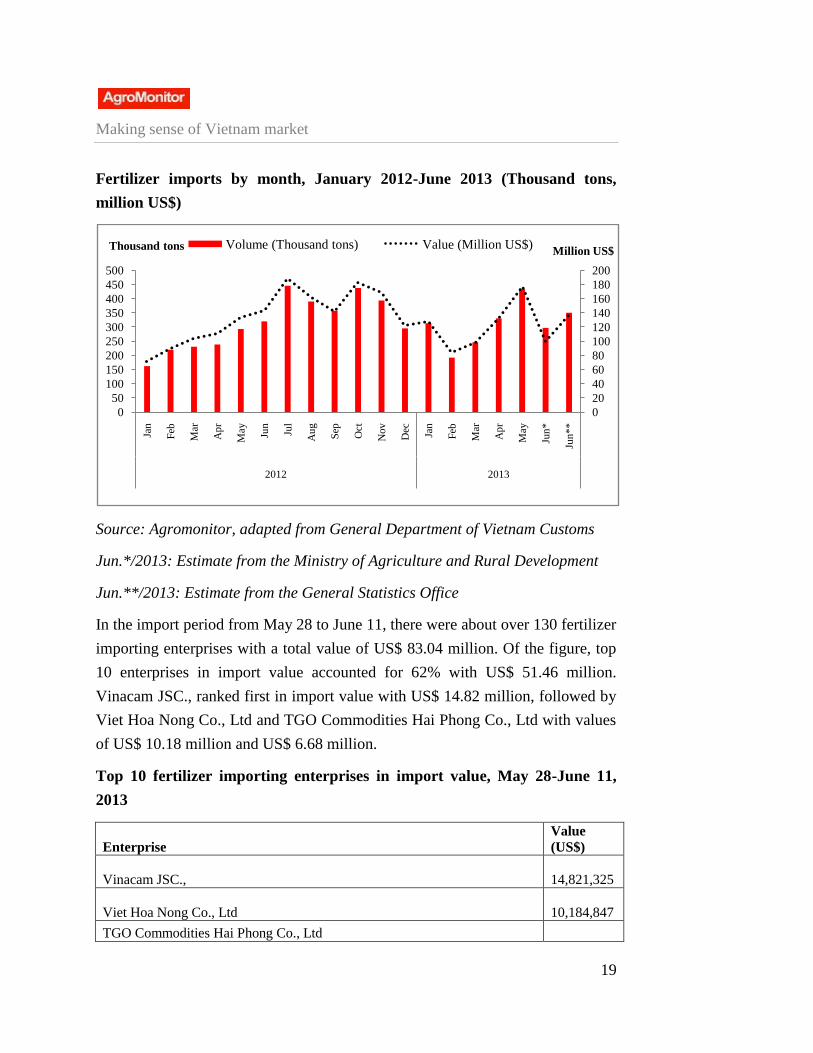

Fertilizer imports by month, January 2012-June 2013 (Thousand tons,

million US$)

Source: Agromonitor, adapted from General Department of Vietnam Customs

Jun.*/2013: Estimate from the Ministry of Agriculture and Rural Development

Jun.**/2013: Estimate from the General Statistics Office

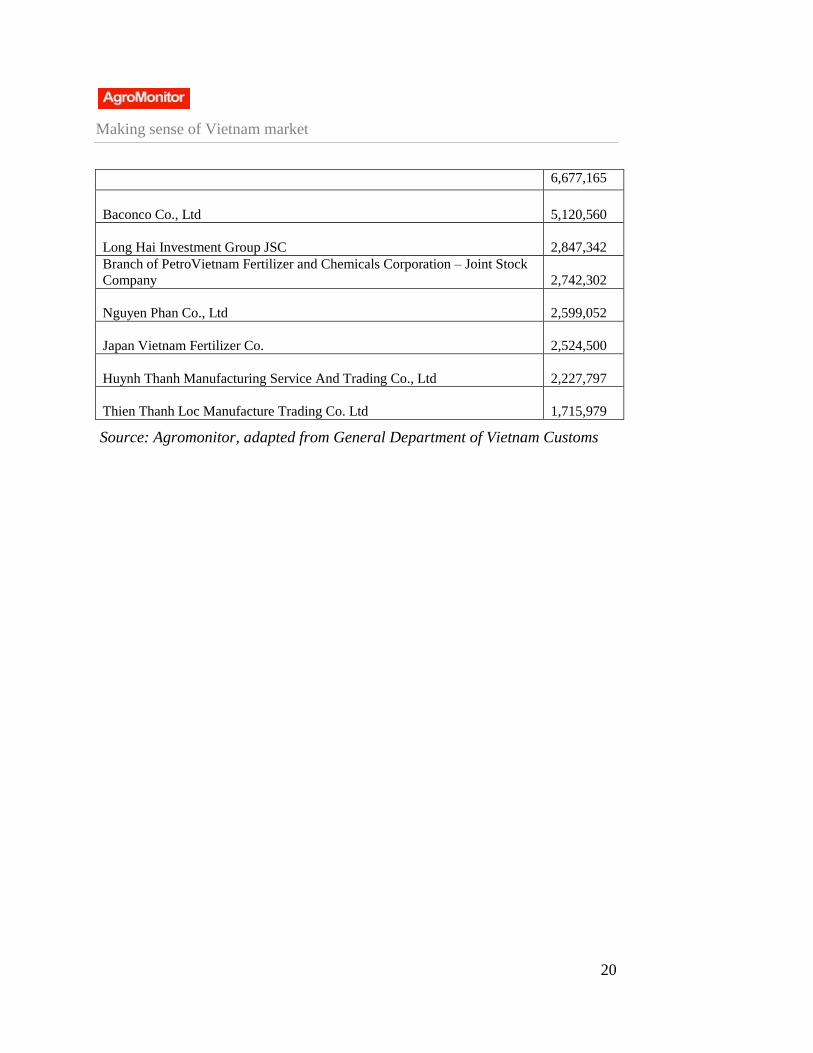

In the import period from May 28 to June 11, there were about over 130 fertilizer

importing enterprises with a total value of US$ 83.04 million. Of the figure, top

10 enterprises in import value accounted for 62% with US$ 51.46 million.

Vinacam JSC., ranked first in import value with US$ 14.82 million, followed by

Viet Hoa Nong Co., Ltd and TGO Commodities Hai Phong Co., Ltd with values

of US$ 10.18 million and US$ 6.68 million.

Top 10 fertilizer importing enterprises in import value, May 28-June 11,

2013

Enterprise

Value

(US$)

Vinacam JSC.,

14,821,325

Viet Hoa Nong Co., Ltd

10,184,847

TGO Commodities Hai Phong Co., Ltd

0

20

40

60

80

100

120

140

160

180

200

0

50

100

150

200

250

300

350

400

450

500

Jan

Feb

Mar

Ap

r

May

Jun

Jul

Au

g

Sep

Oct

Nov

Dec Jan

Feb

Mar

Ap

r

May

Jun

*

Jun

**

2012 2013

Thousand tons Million US$Volume (Thousand tons) Value (Million US$)

Making sense of Vietnam market

20

6,677,165

Baconco Co., Ltd

5,120,560

Long Hai Investment Group JSC

2,847,342

Branch of PetroVietnam Fertilizer and Chemicals Corporation – Joint Stock

Company

2,742,302

Nguyen Phan Co., Ltd

2,599,052

Japan Vietnam Fertilizer Co.

2,524,500

Huynh Thanh Manufacturing Service And Trading Co., Ltd

2,227,797

Thien Thanh Loc Manufacture Trading Co. Ltd

1,715,979

Source: Agromonitor, adapted from General Department of Vietnam Customs

Making sense of Vietnam market

21

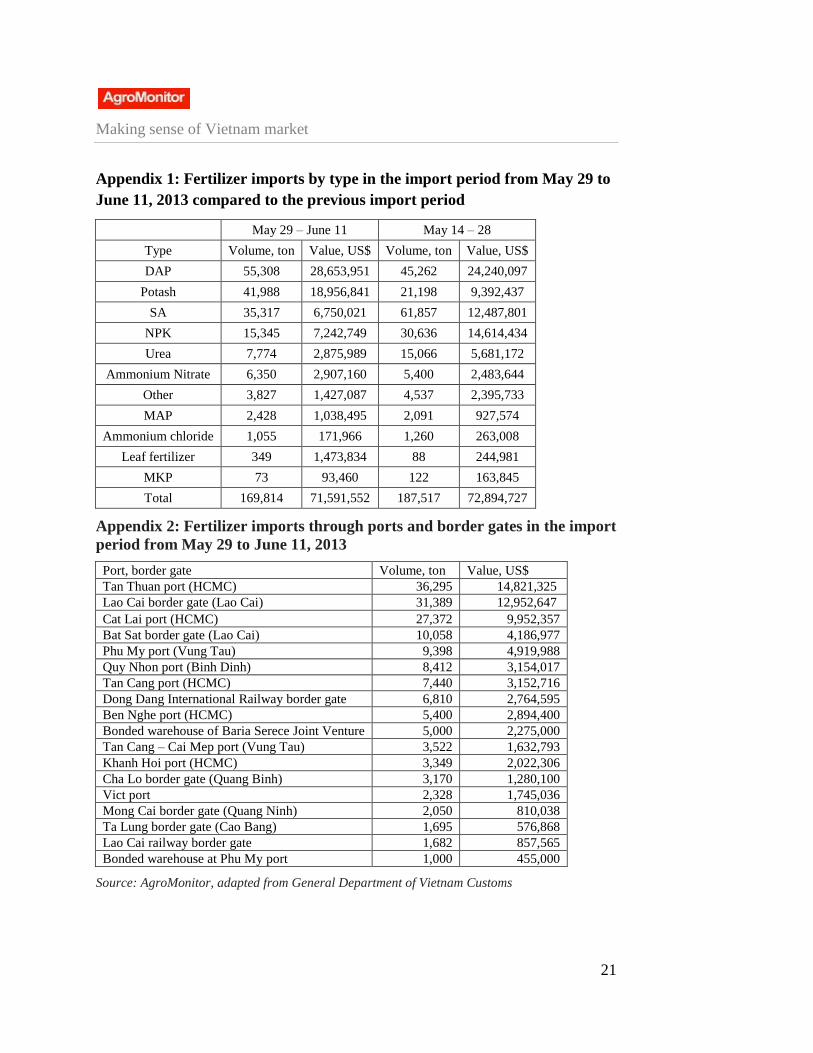

Appendix 1: Fertilizer imports by type in the import period from May 29 to

June 11, 2013 compared to the previous import period

May 29 – June 11 May 14 – 28

Type Volume, ton Value, US$ Volume, ton Value, US$

DAP 55,308 28,653,951 45,262 24,240,097

Potash 41,988 18,956,841 21,198 9,392,437

SA 35,317 6,750,021 61,857 12,487,801

NPK 15,345 7,242,749 30,636 14,614,434

Urea 7,774 2,875,989 15,066 5,681,172

Ammonium Nitrate 6,350 2,907,160 5,400 2,483,644

Other 3,827 1,427,087 4,537 2,395,733

MAP 2,428 1,038,495 2,091 927,574

Ammonium chloride 1,055 171,966 1,260 263,008

Leaf fertilizer 349 1,473,834 88 244,981

MKP 73 93,460 122 163,845

Total 169,814 71,591,552 187,517 72,894,727

Appendix 2: Fertilizer imports through ports and border gates in the import

period from May 29 to June 11, 2013

Port, border gate Volume, ton Value, US$

Tan Thuan port (HCMC) 36,295 14,821,325

Lao Cai border gate (Lao Cai) 31,389 12,952,647

Cat Lai port (HCMC) 27,372 9,952,357

Bat Sat border gate (Lao Cai) 10,058 4,186,977

Phu My port (Vung Tau) 9,398 4,919,988

Quy Nhon port (Binh Dinh) 8,412 3,154,017

Tan Cang port (HCMC) 7,440 3,152,716

Dong Dang International Railway border gate 6,810 2,764,595

Ben Nghe port (HCMC) 5,400 2,894,400

Bonded warehouse of Baria Serece Joint Venture 5,000 2,275,000

Tan Cang – Cai Mep port (Vung Tau) 3,522 1,632,793

Khanh Hoi port (HCMC) 3,349 2,022,306

Cha Lo border gate (Quang Binh) 3,170 1,280,100

Vict port 2,328 1,745,036

Mong Cai border gate (Quang Ninh) 2,050 810,038

Ta Lung border gate (Cao Bang) 1,695 576,868

Lao Cai railway border gate 1,682 857,565

Bonded warehouse at Phu My port 1,000 455,000

Source: AgroMonitor, adapted from General Department of Vietnam Customs

Making sense of Vietnam market

22

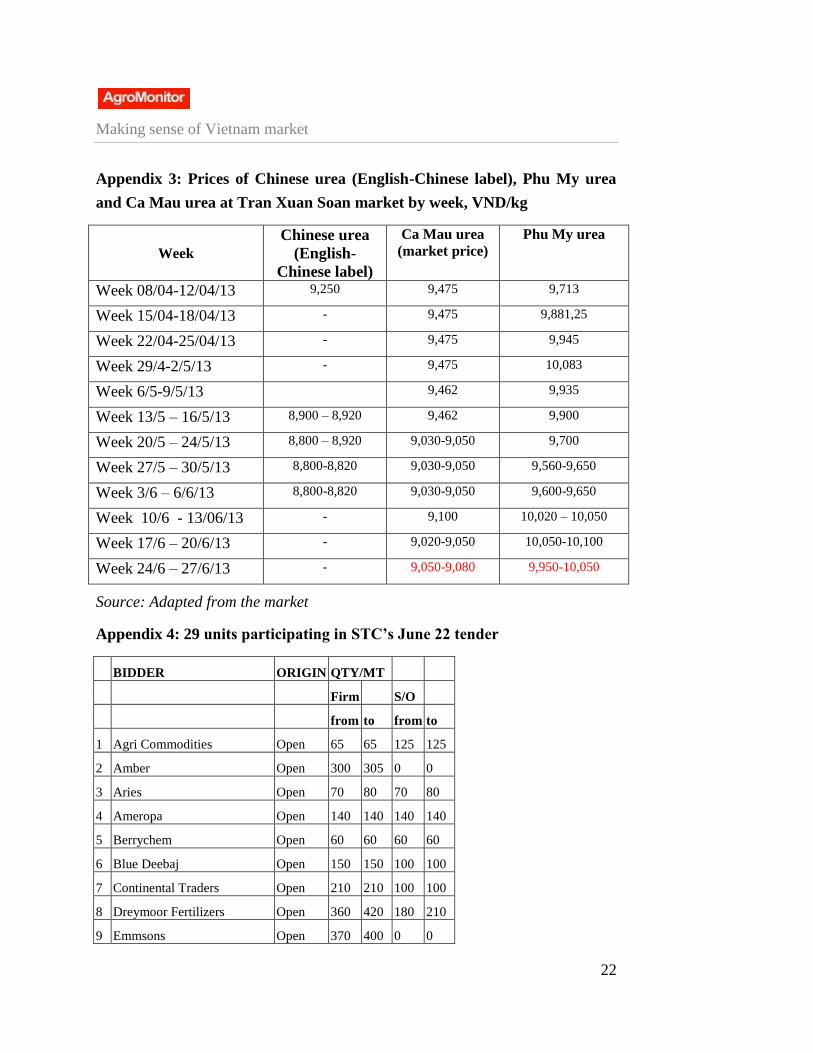

Appendix 3: Prices of Chinese urea (English-Chinese label), Phu My urea

and Ca Mau urea at Tran Xuan Soan market by week, VND/kg

Week

Chinese urea

(English-

Chinese label)

Ca Mau urea

(market price) Phu My urea

Week 08/04-12/04/13 9,250 9,475 9,713

Week 15/04-18/04/13 - 9,475 9,881,25

Week 22/04-25/04/13 - 9,475 9,945

Week 29/4-2/5/13 - 9,475 10,083

Week 6/5-9/5/13 9,462 9,935

Week 13/5 – 16/5/13 8,900 – 8,920 9,462 9,900

Week 20/5 – 24/5/13 8,800 – 8,920 9,030-9,050 9,700

Week 27/5 – 30/5/13 8,800-8,820 9,030-9,050 9,560-9,650

Week 3/6 – 6/6/13 8,800-8,820 9,030-9,050 9,600-9,650

Week 10/6 - 13/06/13 - 9,100 10,020 – 10,050

Week 17/6 – 20/6/13 - 9,020-9,050 10,050-10,100

Week 24/6 – 27/6/13 - 9,050-9,080 9,950-10,050

Source: Adapted from the market

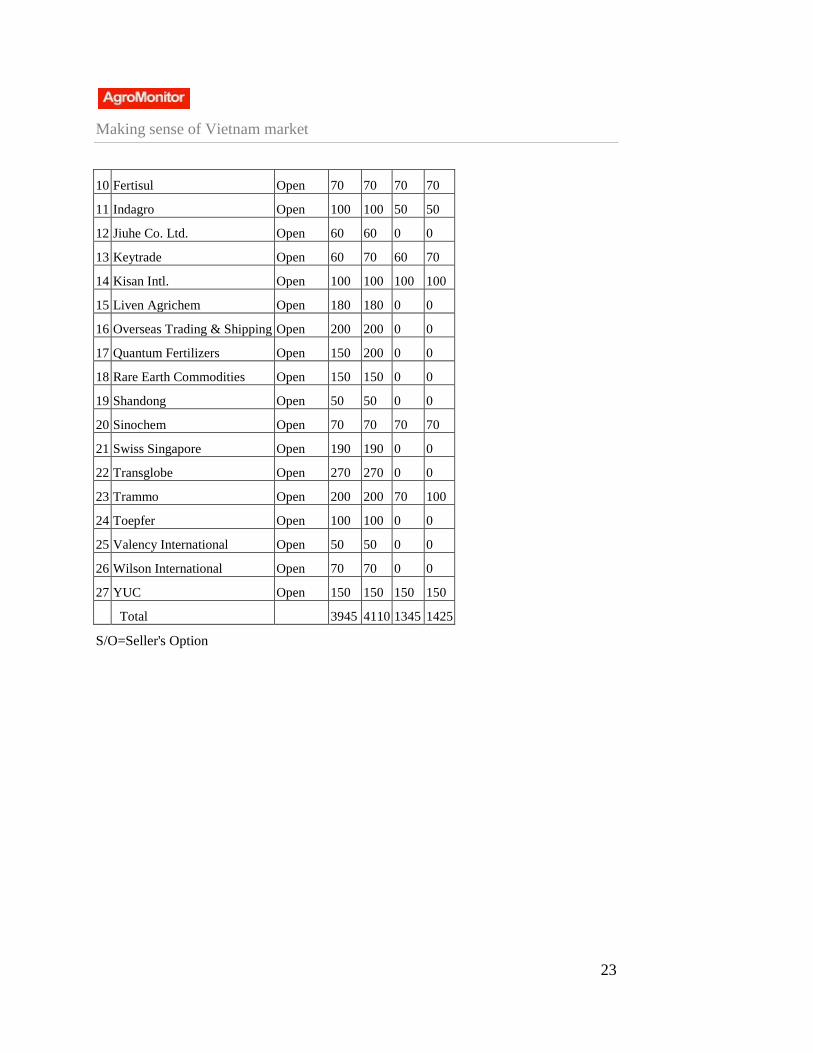

Appendix 4: 29 units participating in STC’s June 22 tender

BIDDER ORIGIN QTY/MT

Firm S/O

from to from to

1 Agri Commodities Open 65 65 125 125

2 Amber Open 300 305 0 0

3 Aries Open 70 80 70 80

4 Ameropa Open 140 140 140 140

5 Berrychem Open 60 60 60 60

6 Blue Deebaj Open 150 150 100 100

7 Continental Traders Open 210 210 100 100

8 Dreymoor Fertilizers Open 360 420 180 210

9 Emmsons Open 370 400 0 0

Making sense of Vietnam market

23

10 Fertisul Open 70 70 70 70

11 Indagro Open 100 100 50 50

12 Jiuhe Co. Ltd. Open 60 60 0 0

13 Keytrade Open 60 70 60 70

14 Kisan Intl. Open 100 100 100 100

15 Liven Agrichem Open 180 180 0 0

16 Overseas Trading & Shipping Open 200 200 0 0

17 Quantum Fertilizers Open 150 200 0 0

18 Rare Earth Commodities Open 150 150 0 0

19 Shandong Open 50 50 0 0

20 Sinochem Open 70 70 70 70

21 Swiss Singapore Open 190 190 0 0

22 Transglobe Open 270 270 0 0

23 Trammo Open 200 200 70 100

24 Toepfer Open 100 100 0 0

25 Valency International Open 50 50 0 0

26 Wilson International Open 70 70 0 0

27 YUC Open 150 150 150 150

Total 3945 4110 1345 1425

S/O=Seller's Option