Embed Size (px)

Citation preview

Video Surveillance: New Installed Base Methodology Yields Revealing Results

TECHNOLOGY.IHS.COM

The video surveillance and physical security industry has long divided public opinion. On one hand, supporters of the technology emphasize the need to protect people, assets, and critical infrastructure, drawing attention to how video surveillance helps solve crimes and provides important information in the aftermath of critical events such as natural disasters and terrorist attacks. On the other side of the debate, some groups have expressed concerns over what is perceived as government intrusion and the rise of a “Big Brother” state. Striking the appropriate balance between privacy and protection is not only challenging but is also often highly subjective.

A question often raised in this debate is: how many security cameras are, in fact, installed throughout the world?

For the first time, IHS is providing a measurable response to this delicate question, through a new methodology that takes into account the actual installed base of video surveillance cameras worldwide. IHS estimates the total number of security cameras installed globally in 2014 reached 245 million units, equivalent to one camera for every 29 people on the planet.

By 2016, the installed base is forecast to be closer to one camera for every 21 people, as the steep price declines expected to occur in the technology drive increased shipments of the analog, network, and high-definition close-circuit television (HD CCTV) cameras forming the total video surveillance market.

This new methodology sizing the installed base delivers some surprising insights. Whereas traditional models underscore shipment or revenue figures that provide a snapshot of the market’s performance in a particular year, the installed base provides a more nuanced look into the market—one that deals with the real-world presence of actively deployed cameras in the world today.

Location mattersYet the video surveillance installed base alone does not provide a complete picture of this fluid, shifting market. The number of installed security cameras at any particular area, location, or site varies dramatically across countries and regions.

Last year the United States was estimated to have the lowest number of people per security camera of any country or region globally. The country’s video surveillance market is driven by a number of factors, such as the perception of crime, the threat of terrorism, advances in technology, and the state of

Video Surveillance: New Installed Base Methodology Yields Revealing Results

TECHNOLOGY.IHS.COM

the economy. Fortunately, the country’s economic strength has enabled the United States to protect itself since the deadly terrorist attack of 11 September 2001, and video surveillance is now part of an overall plan to secure the nation’s borders. US companies have also been at the forefront of many technology advancements in the video surveillance field, especially in the area of video analytics. Furthermore, the immense size of the US market in terms of revenue has helped drive the adoption of video surveillance in many industries and sectors. Today most equipment vendors doing business in the US video surveillance market handle the shipping costs, essentially making it easier for distributors to sell a wide range of brands, a practice not common in other regions, such as Europe.

If the United States, with the third-largest population in the world at more than 320 million, had the least number of video surveillance cameras per person in installed base, China had the largest estimated installed base of security cameras. Nonetheless, because of its huge population—the world’s largest, at more than 1.3 billion—the East Asian country’s video surveillance installed base equated to just 13 people per installed camera. To be sure, the Chinese video surveillance market has been one of the fastest-growing during the last five years, with local vendors driving many of the

price declines across network and HD CCTV cameras. IHS forecasts that the installed base per population in China will be more in line by 2016 with that of the United States and Japan—another of the leading country markets for video surveillance by penetration rate.

In Western Europe, meanwhile, the penetration of security cameras is generally deep. For instance, the United Kingdom had an estimated 11 people per installed security camera in 2014, significantly higher than the next Western European region, the Nordics comprising Denmark, Norway, Sweden, Finland, and Iceland. The United Kingdom was an early adopter of analog CCTV systems, a legacy that can be seen in its large analog camera installed base even today. Interestingly, it is one of the few countries or regions where the number of people per camera is forecast to increase by 2016, counter to the trend of declining rates for many other areas. The projected growth in the United Kingdom is likely to be driven by the replacement of its older analog camera installed base, together with an expected increase in the country’s population that will drive an adjustment in the video surveillance installed base. The analog devices are expected to be replaced by newer network video surveillance equipment.

TECHNOLOGY.IHS.COM

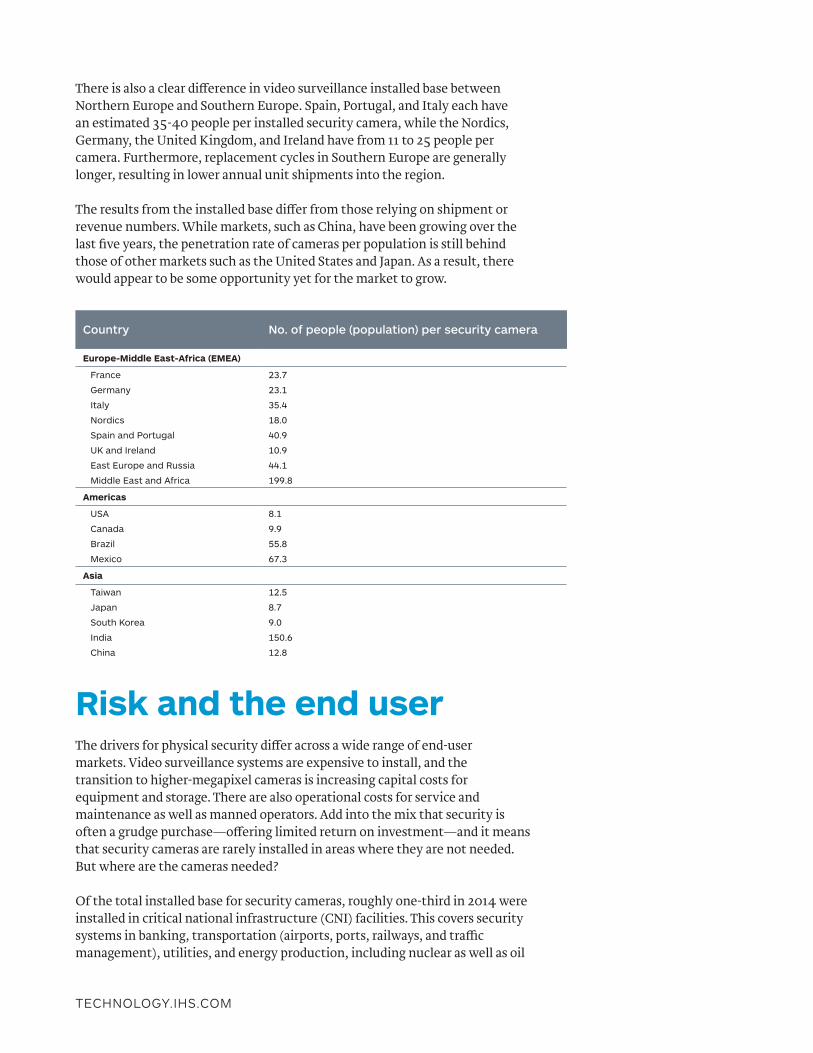

There is also a clear difference in video surveillance installed base between Northern Europe and Southern Europe. Spain, Portugal, and Italy each have an estimated 35-40 people per installed security camera, while the Nordics, Germany, the United Kingdom, and Ireland have from 11 to 25 people per camera. Furthermore, replacement cycles in Southern Europe are generally longer, resulting in lower annual unit shipments into the region.

The results from the installed base differ from those relying on shipment or revenue numbers. While markets, such as China, have been growing over the last five years, the penetration rate of cameras per population is still behind those of other markets such as the United States and Japan. As a result, there would appear to be some opportunity yet for the market to grow.

Risk and the end user The drivers for physical security differ across a wide range of end-user markets. Video surveillance systems are expensive to install, and the transition to higher-megapixel cameras is increasing capital costs for equipment and storage. There are also operational costs for service and maintenance as well as manned operators. Add into the mix that security is often a grudge purchase—offering limited return on investment—and it means that security cameras are rarely installed in areas where they are not needed. But where are the cameras needed?

Of the total installed base for security cameras, roughly one-third in 2014 were installed in critical national infrastructure (CNI) facilities. This covers security systems in banking, transportation (airports, ports, railways, and traffic management), utilities, and energy production, including nuclear as well as oil

Country No. of people (population) per security camera

Europe-Middle East-Africa (EMEA)

France 23.7

Germany 23.1

Italy 35.4

Nordics 18.0

Spain and Portugal 40.9

UK and Ireland 10.9

East Europe and Russia 44.1

Middle East and Africa 199.8

Americas

USA 8.1

Canada 9.9

Brazil 55.8

Mexico 67.3

Asia

Taiwan 12.5

Japan 8.7

South Korea 9.0

India 150.6

China 12.8

TECHNOLOGY.IHS.COM

and gas. The threats against which CNI security systems need to protect range from terrorism and “lone-wolf” attacks, to the protection of employees and guarding against theft.

Furthermore, each sector has unique risks that must be mitigated. Airports have large perimeters that need protection, as well as landside-airside boundaries that must be secured. For their part, ports have large expanses of water that can create additional challenges when using video-content-analysis software to identify threats. Meanwhile, nuclear facilities need to guard against the danger of a reactor leak.

Key risks driving video surveillance use in CNI:• Terrorism/lone-wolf attacks• Staff protection• Theft of assets• Perimeter protection

Another one-third of security cameras were installed last year in what can broadly be termed as commercial applications. This includes retail, hotels, manufacturing facilities, and sporting stadiums. Typically these security cameras are privately owned and designed to protect guests and staff members, as well as to secure assets such as machinery, merchandise, and infrastructure.

Unlike many applications in CNI, security cameras in the commercial market are not normally monitored at the control room. Instead, the video surveillance is often used as evidence following a criminal activity.

Key risks driving video surveillance use in commercial:• Internal and external theft• Staff protection• Fraud• Theft of assets

For the final one-third of the installed base for security cameras, residential accounted for approximately 5%, and could be found across healthcare, government, and education security systems. City surveillance, a subset of the government vertical market, accounted for about 7% of the total global installed base of cameras, although there is significant regional bias with three-quarters of these cameras estimated to be installed as part of China’s vast Safe City programs. The two markets for Europe-Middle East-Africa (EMEA) and the Americas accounted for 8% and 7%, respectively.

How to size an installed baseMeasuring the installed base of security cameras is not an easy task. The video surveillance market has a highly fragmented supply chain. Globally there are hundreds of equipment vendors, thousands of distributors, and tens of thousands of systems integrators and installers—with each group selling, distributing, fitting, and replacing analog, network, and HD CCTV cameras.

A number of approaches can be taken when estimating the installed base. However, these can be broadly grouped into two methods: those that extrapolate a localized estimate; and those that model the installed base using another data source.

Extrapolating from a sample size works best when looking at a smaller geographic area. For example, the number of security cameras can be counted in one city center and extrapolated to similar cities. The difficulty with this method comes when extrapolating across vertical markets and geographic regions, as very different market drivers and inhibitors can characterize the markets and regions.

TECHNOLOGY.IHS.COM

The second method is to model the installed base using a reported data source. For estimates on the global installed base of video surveillance cameras, IHS constructed its database based on information collected during video surveillance research for reports published between 2004 and 2014. This decade of video surveillance data was analyzed as follows:• Annual unit shipments of security cameras were

taken from the base-year data of historic IHS video surveillance reports.

• These unit shipments were split into key geographic subregions.

• For each region, unit shipment data was further segmented into 11 end-user industries.

• An estimate was made for the average replacement cycle of a network and analog security camera for each vertical market.

• Interviews and completed questionnaires from video surveillance equipment vendors and security systems integrators were used to make these estimates.

Modeling the installed base from reported base-year data takes into account the regional differences present in the video surveillance market. It considers different

product and country market growth rates, takes into account the impact of regional pricing, and recognizes the effect of new technology trends on the installed base.

Worth noting is that estimates for the installed base refer to only security cameras that remain active. Cameras that have been installed and are no longer being recorded, monitored, or actively used for surveillance are not considered in the installed base number. Old cameras that are not removed from a building but have been replaced as part of the building’s security system are not included as part of the installed base estimate.

Estimates for the average lifespan of a security camera were made for each region, end-user industry, and equipment vendor. These were based on primary interviews with equipment vendors and systems integrators. The estimates represents an average, and have taken into account cameras that fail quickly and those that are not replaced for a much longer period of time.

9003-TB-0415

TECHNOLOGY.IHS.COM

Follow the conversation @IHS4Tech

9003-TB-0415

Video surveillance: the new normal2014 was pivotal for the video surveillance industry. For many years the general trend has been one of network cameras replacing analog types. Network equipment vendors, for the most part, have benefited from this rising tide lifting all boats. Improvements in technologies—such as video analytics, image quality, and higher-megapixel cameras—also served to drive end users to transition to the network.

However, something changed in 2014.

This was the first year that real price pressure was seen in the network video surveillance market. A year earlier, HD CCTV cameras had exploded onto the market, shipping just below 1.2 million cameras worldwide in 2013. HD CCTV equipment offers high-fidelity, low-latency video that can be transmitted over existing coaxial cable. Selling at a much lower price point than previously had been seen for high-definition products, HD CCTV camera shipments continued to increase in demand in 2014.

Second, the semiconductor market, driven by Chinese suppliers, made significant breakthroughs in the manufacturing process for chips used in network cameras. This led to increased price pressure from a number of Chinese equipment vendors, increasing the shipments of cameras sold into the market but impacting total market revenue and the margins available. The new normal is now a far more competitive network video surveillance market.

Competing in 2015With the commoditization of many features of the network camera and the increased pressure on margins, new competitive challenges are being placed on video surveillance equipment vendors. One solution is to differentiate through technology, such as video analytics.

Video-content-analysis software examines live or recorded video streams to detect, classify, and track predefined objects or behavior patterns. It is used as a means to automate the monitoring process, and can

be particularly effective in proactively identifying events as they happen or in extracting information from recorded video. Algorithms—such as those to detect perimeter intrusions, objects moving the wrong way, dwell time, and people-counting—can all help differentiate a particular brand of security camera from its competition. That being said, challenges remain in convincing the market that video surveillance is truly ready for mass adoption. Heavily hyped but then burned by poor technology in the past, video analytics has suffered a blow to its credibility, which will take time to fix.

Another strategy that equipment vendors may take is to focus on key vertical or niche markets. The video surveillance market is extremely fragmented, and even end users in the same vertical market often have different requirements and product needs. This means that opportunities exist to build products targeted at such niche applications as well as building relationships with the distribution, integrator, and consultant community in order to take advantage of projects. This approach is also likely to help maintain profit margins.

Again, there are challenges with this strategy. It is time- and resource-intensive to build—as well as to maintain—relationships with both key participants in the channel and the size of the projects, and the quantity of products sold will not necessarily justify the costs involved. It is also a difficult business model to scale.

Finally, the industry is likely to see further merger-and-acquisition activity as vendors combine resources, consolidate costs, and look to provide a more complete offering of cameras, recorders, and software to drive revenue growth. Partnering—or acquiring—the right company could be, in reality, the best strategy to compete in 2015 and beyond.

Niall Jenkins is associate director for video surveillance at IHS.

For more information on this white paper or on IHS research relevant to this topic, refer to the Video Surveillance research area from the Industrial, Security and Medical research service of IHS Technology.