Embed Size (px)

Citation preview

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

VC/M&A Tech MultiplesFrance 2021

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

Introduction

2

A “J” curb more than a “V” curb

After a bumpy but promising 2020, 2021 has been the true blossom of theEuropean Tech ecosystem. With more than €60bn in funding at the end ofQ3-21, it already represents almost a 2x growth from the 2020 full year figure(€32bn). On the current trend, Europe should reach €80bn in total funding, i.e.a 2.5x growth.Europe also became a substantial contributor to the worldwide herd ofunicorns with 115 members (incl. 39 newcomers in 2021) out of 850worldwide.

France has contributed to the European growth and one can clearly see thatthe French Tech ecosystem has matured with €8.2bn in total funding YTD and11 new unicorns. On the current trend, France would be around €11bn at theend of the year. Quite impressive! Yet, that’s only a 2x growth vs last year.Less that Europe’s 2.5x. Less than UK’s 2.4x (€28bn expected for 2021). Andless than the astonishing Germany’s 3x (€15bn expected for 2021).

In a broader perspective, we expect worldwide VC funding to rise up to€500bn in 2021, growing 2x from 2020 – just the same trend as France.

On the exit-side, we’ve seen some encouraging developments with theBelieve IPO on Euronext Paris for €2bn and the expected IPO of OVH in Q4-21 at €3.5bn. 2021 should reach €7.6bn in total exit, which would be the bestyear ever for the French ecosystem.

Arthur Porré, Co-Founder and Managing Partner, Oct. 11th, 2021

Tech exits transactions

Invested amount (€m) Deal count (#)

Deal Value (€m) Deal count (#)

VC fundraisings

Jan. Feb. Mar. Apr. May Jun. Jul. Aug. Sept.

Jan. Feb. Mar. Apr. May Jun. Jul. Aug. Sept.

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

VC trends

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

European startup fundraising is expected to growth 2x in 2021

Overview of European VC fundraising

4

VC trends

Invested amount (€bn)

Mega rounds are still mainly in the UK

Mega rounds > €100m (#)

€60bnInvested in Europe

(2021 YTD)

39New Unicorns

0 10 20 30 40 50

2017

2018

2019

2020

2021 YTD

UK Germany France

0

20

40

60

80

100

120

140

0

5

10

15

20

25

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 YTD

France Germany UK Rest of Europe Nb. of European unicorns

Nb. of European unicorns (#)

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

French VC fundraising has grown at a 47% CAGR since 2014 and is estimated to reach €10.5bn in 2021

Overview of French VC fundraising

5

VC trends

Invested amount (€bn) Deal count (#)

0.7

1.5

2.1 2.1

2.9

4.6

5.6

10.5

0

100

200

300

400

500

600

700

800

900

0

2

4

6

8

10

12

2014 2015 2016 2017 2018 2019 2020 2021e

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

Top 5 funding rounds of 2021

VC deals: 536 funding rounds in 2021 for €8.3bn in total deal value

6

VC trendsRecord year for French VC fundraisings

Invested amount (€m)

Fundraising amounts continue to increase

Median deal value (€m)

€574m

led by SoftBank

Deal count (#)

€472m

led by SoftBank

€408m

led by Eurazeo

€310m

led by Draper Esprit

€300m

led by General Atlantic

Top 3 Top 10 Others No. deals

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

Fewer seed deals in the ecosystem

VC investments by type of series (1/2)

7

VC trends

Proportion of deals (%)

Seed

Series A

Series B

Series C

Series D+

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

Median fundraisings keep rising especially for Series B+

VC investments by type of series (2/2)

8

VC trends

Median fundraising amount (€m) Seed Series A Series B Series C Series D+

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

1 out of 4 startups goes on to raise a 2nd round of financing

Startup cohorts and profiles by round

9

VC trends

Base 100

100

27

83 1 0.3

0

10

20

30

40

50

60

70

80

90

100

Round 1 Round 2 Round 3 Round 4 Round 5 Round 6

Seed Series A Series B Series C Series D

Median TTM revenue €0.7m €1.3m €2.4m €5.6m €12.5m

Median fundraising €1.0m €3.0m €7.0m €18.3m €40.5m

Median pre-money valuation €3.5m €9.0m €17.5m €52.0m €179.5m

Median dilution 29% 28% 27% 22% 21%

Median age (years) 3 4 5 7 8

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

Subscription and Commission models continue to attract the majority of investments

Distribution of deals by business model

10

VC trends

Proportion of deals by business model (%)

Subscription

Commission

Manufacturing

E-commerce

Service

Research

Others

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

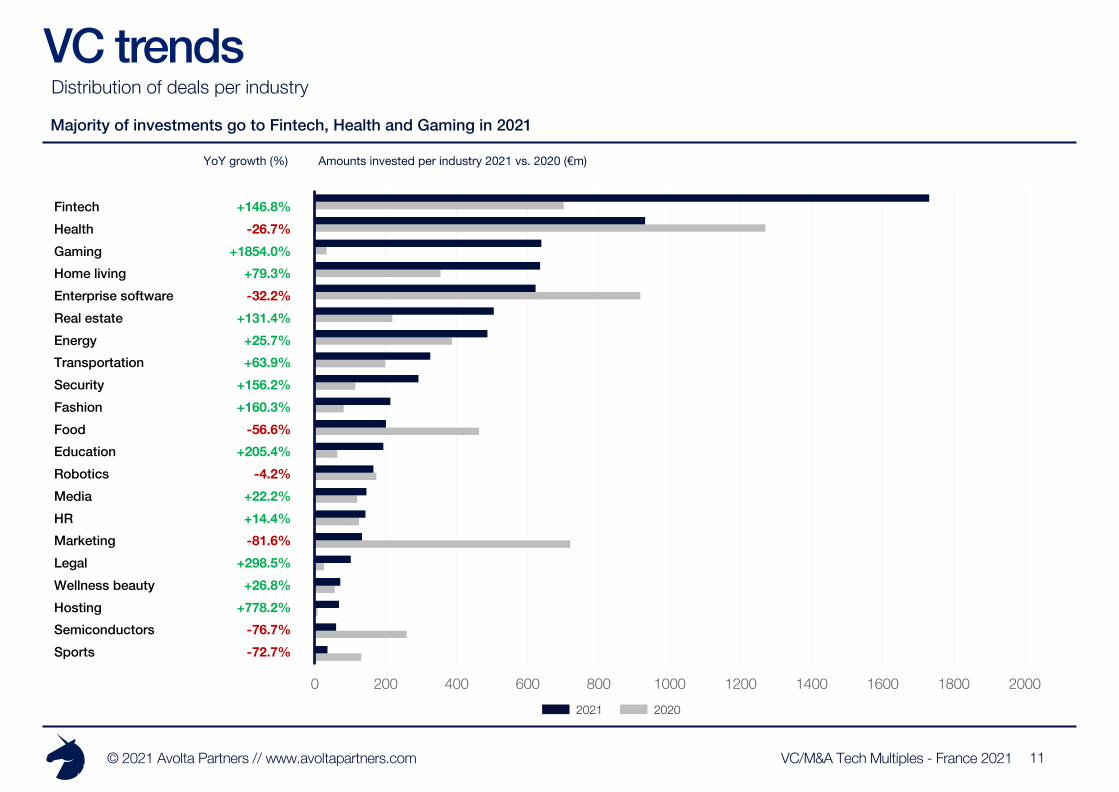

Majority of investments go to Fintech, Health and Gaming in 2021

Distribution of deals per industry

11

VC trends

Amounts invested per industry 2021 vs. 2020 (€m)

0 200 400 600 800 1000 1200 1400 1600 1800 2000

sportssemiconductors

hostingwellness beauty

Legalmarketing

jobs recruitmentmedia

roboticseducation

foodfashionsecurity

transportationenergy

real estateenterprise software

home livinggaming

healthfintech

YoY growth (%)

Fintech +146.8%Health -26.7%Gaming +1854.0%Home living +79.3%Enterprise software -32.2%Real estate +131.4%Energy +25.7%Transportation +63.9%Security +156.2%Fashion +160.3%Food -56.6%Education +205.4%Robotics -4.2%Media +22.2%HR +14.4%Marketing -81.6%Legal +298.5%Wellness beauty +26.8%Hosting +778.2%Semiconductors -76.7%Sports -72.7%

2021 2020

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

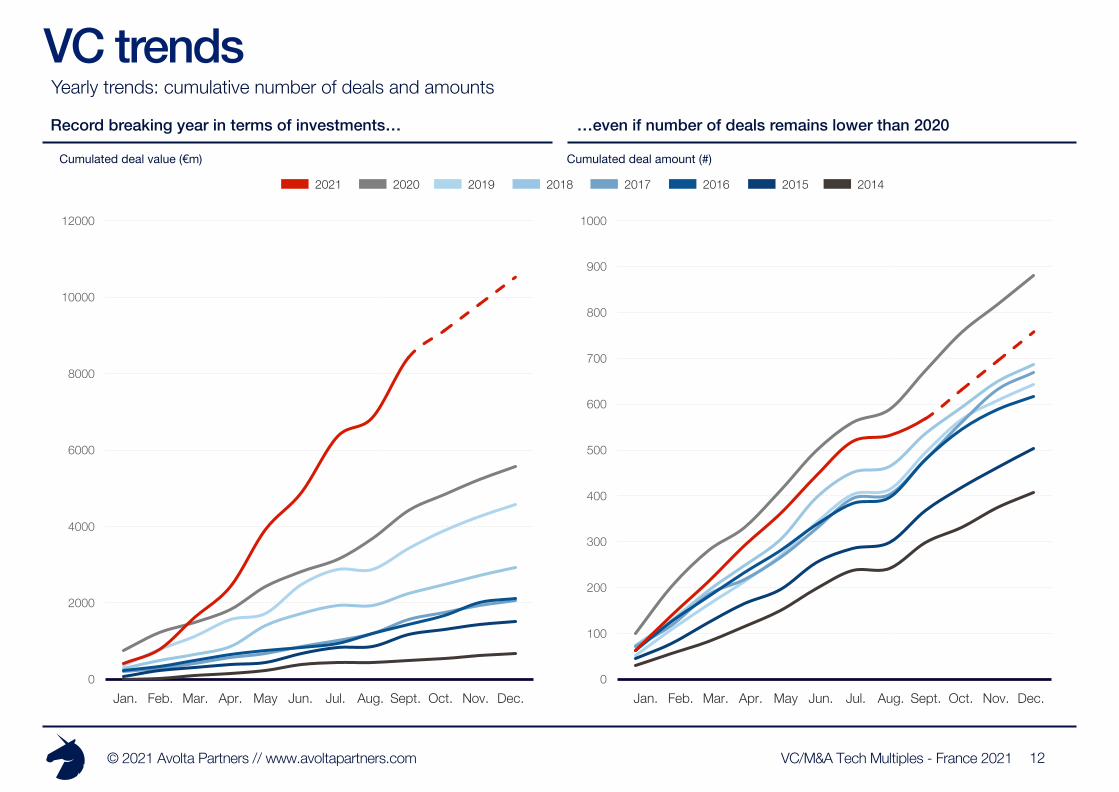

Record breaking year in terms of investments…

Yearly trends: cumulative number of deals and amounts

12

VC trends

Cumulated deal value (€m)

…even if number of deals remains lower than 2020

Cumulated deal amount (#)

2021 201620182020 2019 2017 2015 2014

0

100

200

300

400

500

600

700

800

900

1000

1 2 3 4 5 6 7 8 9 10 11 120

2000

4000

6000

8000

10000

12000

1 2 3 4 5 6 7 8 9 10 11 12Jan. Feb. Mar. Apr. May Jun. Jul. Aug. Sept. Oct. Nov. Dec. Jan. Feb. Mar. Apr. May Jun. Jul. Aug. Sept. Oct. Nov. Dec.

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

3.93.7

2.9

2.52.3 2.2

1.91.7 1.7

1.5 1.4 1.41.2 1.2 1.1 1.1 1.1 >1 >1 1.0 1.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

French unicorns by last round valuation

11 startups have reached unicorn status in 2021, France being the home of 21 unicorns

13

VC trends

Last round valuation (€bn)

Unicorn status reached in 2021 Unicorn status reached before 2021

1Headquarters in the U.S 2Exact amount not communicated by the company

1

1

1

2 2

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

Avolta Next 20: who will be France’s next unicorns?

14

VC trendsPossible French unicorns by last amount raised

Jul. 21 – Series C€142m

Sep. 20 – Series C€140m

Oct. 20 – Series C€315m

Nov. 16 – Series C€100m

Apr. 21 – Series C€100m

Jul. 21 – Series C€100m

Mar. 21 – Series D€90m

Jan. 20 – Series C€104m

May 21 – Series C€80m

Sep. 20 – Series C€77m

Dec. 20 – Series B€72m

May 21 – Series B€84m

Jun. 20 – Series C€70m

Jun. 21 – Series C€63m

Jan. 20 – Series C€63m

Dec. 20 – Series B€50m

Apr. 21 – Series C€70m

May 21 – Series B€82m

Jan. 19 – Series C€72m

Apr. 19 – Series B€36m

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

530 active investors on the market in France, with increasing amount of foreigners

Active investor trends and league tables

15

VC trends

# of active investors (excl. business angels)

Top 10 active VCs (last 12 months)

70 deals

20 deals

13 deals

13 deals

12 deals

11 deals

11 deals

11 deals

10 deals

9 deals

1.

2.

3.

3.

5.

6.

6.

6.

9.

10.

-

50

100

150

200

250

300

350

2014 2015 2016 2017 2018 2019 2020 2021e

French active investors Foreign active investors

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

1.9x

3.0x

9.2x

12.4x

-

5.0

10.0

15.0

20.0

25.0

-

5.0

10.0

15.0

20.0

25.0

French investorsonly

At least one foreigninvestor

The French ecosystem is attracting more foreign investors

Participation of foreign VCs in French rounds

16

VC trends

% of series with a foreign investor

EV/TTM revenue multiples

6.3x

4.2x

0%

5%

10%

15%

20%

25%

30%

35%

40%

Q114

Q214

Q314

Q414

Q115

Q215

Q315

Q415

Q116

Q216

Q316

Q416

Q117

Q217

Q317

Q417

Q118

Q218

Q318

Q418

Q119

Q219

Q319

Q419

Q120

Q220

Q320

Q420

Q121

Q221

Q321

North America United Kingdom Germany Asia Foreign1st Quartile 3rd Quartile

Med.

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

Top 5 new VC funds raised in 2021Record year for new VC funds raised

Overview of French VC funds

17

VC trends

Funds raised by French VCs (€bn)

€1.6bnRaised in Jul. 2021

€300m Raised in Feb. 2021

€250m Raised in Sep. 2021

€225m Raised in Mar. 2021

€660m Raised in Feb. 2021

0.3 0.2

0.40.3

1.10.9

2.1

1.7

1.0

1.3

3.6

0

1

2

3

4

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 YTD

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

0.9x

0.9x

1.5x

2.1x

2.7x

2.0x

4.5x

7.2x

7.8x

10.8x

- 2.0 4.0 6.0 8.0 10.0 12.0 14.0

- 2.0 4.0 6.0 8.0 10.0 12.0 14.0

VC multiples by business model and industry over the last 24 months

18

VC trendsEV/TTM revenue by business model EV/TTM revenue by industry

4.7x

Subscription

3.9x

Commission

2.6x

Manufacturing

2.2x

E-Commerce

1.5x

Service

Median Quartile 1 Quartile 3

Med.

7.9x

Fintech

6.4x

Health

4.8x

Enterprise software

3.6x

Marketing

2.6x

Food

2.1x

Transportation

3.1x

Real Estate

3.5x

HR

2.0x

1.6x

1.5x

1.7x

2.6x

2.3x

2.4x

5.3x

6.7x

10.9x

3.1x

6.8x

8.1x

6.3x

11.2x

12.2x

- 2.0 4.0 6.0 8.0 10.0 12.0 14.0

- 2.0 4.0 6.0 8.0 10.0 12.0 14.0

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

Tech exit trends

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

French exits trends remain stable over the last 5 years

Overview of French exits

20

Tech exit trends

Deal value (€bn) Deal count (#)

5.8

4.5

4.9

5.5

7.6

0

50

100

150

200

250

300

350

400

0

1

2

3

4

5

6

7

8

9

2017 2018 2019 2020 2021e

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

Top 5 tech exits in 2021 YTD

Tech exit activity: 234 deals in 2021 for €3.5bn in deal value

21

Tech exit trendsIncreasing exits trends mostly driven by top deals

Deal value (€m) Deal count (#)

€1.9bnIPO Euronext Paris

by Cegid

by Marlin Equity Partners

IPO Euronext Paris

€450m

€200m

€119m

€106m

by Altus Group

Median EV remains stable

Median EV (€m)

Top 1 Top 3 Others Nb. deals

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

3.2x

1.0x

1.4x

13.1x

4.0x

5.1x

- 5.0 10.0 15.0

- 5.0 10.0 15.0

Still few IPOs

Distribution of deals by deal type

22

Tech exit trends

Percentage of deals (%)

Larger exits for IPOs and sponsor deals

EV/TTM revenue by deal type

Median EV at exit (€m)

2.5x

Corporate Dev

2.4x

Sponsor

6.1x

IPO

Median 1st Q. 1 3rd Q.Med.

IPO Sponsor Corporate Dev

17

62 59

CorporateDevelopment

Sponsor IPO

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

Tech exit deal value is comparable to previous years…

Yearly trends: cumulative number of deals and amounts

23

Tech exit trends

Cumulated deal value (€m)

…but greater number of deals

Cumulated deal count (#)

2021 2020Year of Date in Press 20182019 2017

Jan. Feb. Mar. Apr. May Jun. Jul. Aug. Sept. Oct. Nov. Dec. Jan. Feb. Mar. Apr. May Jun. Jul. Aug. Sept. Oct. Nov. Dec.

0

50

100

150

200

250

300

350

1 2 3 4 5 6 7 8 9 10 11 120

1000

2000

3000

4000

5000

6000

7000

1 2 3 4 5 6 7 8 9 10 11 12

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0% 2% 4% 6% 7% 9% 11%

13%

14%

16%

18%

20%

22%

23%

25%

27%

29%

30%

32%

34%

36%

37%

39%

41%

43%

45%

46%

48%

50%

52%

53%

55%

57%

59%

60%

62%

64%

66%

67%

69%

71%

73%

75%

76%

78%

80%

82%

83%

85%

87%

89%

90%

92%

94%

96%

98%

99%

13% of deals are over €150m EV

Distribution of deals by EV

24

Tech exit trends

% of deal value

3

2

1

<€50m

<€50m-€150m

>€150m

63%

25%

13%

% of deals

Exit value % of panel Var. YoY

3

2

1 The Happy Few

The Breakaways

The Peloton -14%

+56%

+18%

0% 25% 50% 75% 100%

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

Rank Investor # exits

#1 21

#2 11

#3 10

#4 8

#5 7

#5 7

#5 7

#6 6

#7 5

#7 5

The majority of exits are bootstrapped companies…

VC-backed vs. non-backed exits

25

Tech exit trends

…however, VC-backed exits show higher performance, size and time to exit

Top 10 VCs by no. of exits (last 12 months)

Median EV/TTM Revenue Median EV Median time to exit

4.2x

1.8x

-

1.00

2.00

3.00

4.00

5.00

1 2

€48.1m

€23.8m

-

10.00

20.00

30.00

40.00

50.00

60.00

1 2

8 years

11 years

-

2.00

4.00

6.00

8.00

10.00

12.00

1 2VC backed Bootstrapped VC backed Bootstrapped VC backed Bootstrapped

VC-backedBootstrapped

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2017 2018 2019 2020 2021 YTD

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

Targets’ characteristics

Tech exits characteristics

26

Tech exit trendsExits are gaining maturity

TTM revenue at exit (€m)

Median EV has increased over the last 5 years

Median EV (€m)

10 yearsmedian years to exit

€3mmedian funds1 raised at

exit

1Sample is based on companies who have raised funds

59%of companies are

profitable

€3.0m

€5.3m €4.8m

€9.2m

0

1

2

3

4

5

6

7

8

9

10

2017 2018 2019 2020

€18m €25m €18m

€61m

€31m

0

20

40

60

80

100

2017 2018 2019 2020 2021 YTD

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

Around 70% of acquirers are French…

Distribution of acquirers by geography

27

Tech exit trends

Deal count

…but foreign countries acquire the most value

Deal value

France AsiaEurope North America

Top acquirers since 2017 (#) Top acquirers since 2017 (€m)

4

4

4

4

5

5

5

5

7

7

YTD YTD

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

Public tech companies show high performance

Avolta Partners’ Public French Tech Index1

28

Tech exit trends

Index value

1Index represents returns of an equally-weighted portfolio of all tech IPOs since Jan. 2017

0

20

40

60

80

100

120

140

160

180

Jan-17 Jul-17 Jan-18 Jul-18 Jan-19 Jul-19 Jan-20 Jul-20 Jan-21 Jul-21

IPO characteristics & breakdown

+55.0%

+30.4%

€55mmedian EV at IPO

34%of companies show positive

returns since IPO

Tech index CAC Small

14%

8%

6%

6%

3%2%

2%9%

HealthEnergyRoboticsTelecomTransportationGamingMarketingOther

+570.2% for the B.V.P. Nasdaq Emerging Cloud Index (U.S) over the same period

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

0.9x

1.1x

1.3x

1.7x

2.0x

2.7x

1.5x

4.8x

8.4x

10.5x

- 2.0 4.0 6.0 8.0 10.0 12.0 14.0

- 2.0 4.0 6.0 8.0 10.0 12.0 14.0 0.8x

2.7x

1.4x

1.6x

1.6x

2.1x

2.5x

2.9x

1.6x

5.2x

5.1x

5.7x

3.4x

13.4x

8.4x

15.0x

- 2.0 4.0 6.0 8.0 10.0 12.0 14.0

- 2.0 4.0 6.0 8.0 10.0 12.0 14.0

EV/TTM revenue by business model

Exit multiples by business model and industry

29

Tech exit trendsEV/TTM revenue by industry

Median 1st Quartile 3rd Quartile

Med.

3.2x

Subscription

3.8x

Commission

2.1x

Manufacturing

1.3x

E-Commerce

1.1x

Service

4.6x

Fintech

3.5x

Health

4.2x

Enterprise software

2.3x

Marketing

3.6x

Food

2.8x

Transportation

3.2x

Real Estate

1.5x

HR

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

Contact us

30

Research team

Arthur PorréFounding Partner

Pascal FarrugiaDirector

Alexandre MeiersSenior Analyst

Victor EbersoldSenior Analyst

Julien GakpeAnalyst

David KaddouchAnalyst

Jacques-Henri ChecriAnalyst

Matthieu SionAnalyst

Déborah BourgeotSenior Analyst

Naomi DarkoSenior Analyst

Pierre PinsaultAnalyst

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com 31

Building a platform for Tech corporate finance

With 80 deals closed in 6 years, we chose from the beginning to be pan-Europeanand data-driven. So we built Avolta.io, a unique platform to automate processesand scale our ability to help fast-growing tech companies in Europe.

Our platform concatenates European deals in the Tech Industry with information onvaluation, revenues and structuration. We source this private data from our networkof providers, business partners and investors, combining it with unique insights fromour team of analysts.

We extracted from our 10,000+ deals private database all Tech companiesmonitored from Q1-14 to Q3-21 for companies headquartered in France.

Enterprise Value (EV)Calculated as Equity Value + Net Debt when legal information is found. Otherwiseestimated EV from several sources: dealroom.co, Mergermarket, Crunchbase,CFNews, Avolta’s private networks and public media.

Exit types

• Corporate dev: the acquirer is a corporate• PE fund: the acquirer is a private equity fund (non-leveraged, LBO,

MBO, OBO)• IPO: Initial Public Offering though financial markets

Business Models

• Subscription: SaaS or more traditional licensing revenue• Commission: platform debiting a defined take rate from its flows• Manufacturing: production and resale of goods• Performance: built around usage from a recurring user community• eCommerce: buy and online resale of goods• Audience: traffic-based revenue• Service: margin between labor cost and service invoice price• Research: strong R&D focus to keep high barriers to entry

Data. Data. Data.Methodology

Leveraging quality data providers

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com 32

§ 80 deals / €1bn completed in 6 years- Incl. 15 deals / €300m in the last 12 months- 20 deals for €600m in our current portfolio

(€30m avg. transaction)

§ All types of transactions (€10-€300m EV)- M&A & LBO: 50% of our deals- Fundraising (Series A/B/C+) : 50% of our deals

§ 70% cross-border deals

§ 100% Tech companies, with major focus on:- Fintech / Insurtech- Mobility- B2B SaaS- Marketplace/eCommerce- Deeptech (AI, Blockchain, Space, etc.)- FoodTech/Agtech- Consumer brand- HR/EdTech- Health- Proptech

Leading M&A Advisor in Tech in Europe on €10-300m DealsAbout Avolta Partners

VC/M&A Tech Multiples - France 2021© 2021 Avolta Partners // www.avoltapartners.com

Alexandre MeiersSenior [email protected]

Disclaimer

The information contained in this report has been produced by Avolta Partners based on third-party information. While Avolta Partners has made every effort to ensure the reliability of thedata included in this report, Avolta Partners cannot guarantee the accuracy of the informationcollected and presented. Therefore, the Avolta Partners cannot accept responsibility for anydecision made or action taken based upon this report or the information provided herein.This presentation is for the exclusive use of the people to whom it is addressed and isintended for general information purposes only. It is not intended to constitute legal or otherprofessional advice and should not be treated as such.Appropriate legal advice must be sought before making any decision, taking any action orrefraining from taking any action in reliance on the information contained in this presentation.Avolta Partners does not assume any responsibility for any person’s reliance upon theinformation contained herein.

© Copyright Avolta Partners 2021

Avolta Partners

With more than 80 deals closed in 6 years, Avolta Partners has proven to be one of the most active M&Aboutique in Europe in the Tech Industry. As a result, our team of 20 people has learned how to maximise thevalue of a deal – both valuation and legal conditions – thanks to a proven methodology and hard-nosednegotiations.

Dedicated team

Arthur PorréManaging [email protected]

Pascal [email protected]

Victor EbersoldSenior [email protected]

![[vc 1037 - listing.archiviolocation.com · [vc 1037] ARCHIVIOLOCATION.COM [vc 1037] ARCHIVIOLOCATION.COM [vc 1037] ARCHIVIOLOCATION.COM [vc 1037] ARCHIVIOLOCATION.COM. archivio location](https://img.pdfslide.us/doc/110x75/5fcd99d1df347e1ae154645c/vc-1037-vc-1037-archiviolocationcom-vc-1037-archiviolocationcom-vc-1037.jpg)